Abstract

Once scaled, online platforms reconfigure value to remain competitive. Reconfiguration in online platforms may take a different form than in pipelines, as online platforms are intermediaries that generate network effects among the sides they connect. They also face stiff competition from other spheres due to lower barriers to entry. Why and how do online platforms reconfigure value? By examining 13 Indian online platforms that have achieved a certain level of success (such as tipped markets, investor confidence, or profitability), this article offers four strategies for reconfiguring online platforms: enhance interactions, enhance capabilities, offer new services, and nurture new transactions.

Value reconfiguration is not a new phenomenon. Businesses regularly reconfigure value for further growth. Ansoff’s pioneering work categorized growth alternatives for a business into market development, market penetration, product development, and diversification. 1 His examination of several American firms revealed that companies that stuck to their traditional products or methods could not grow. Among the recent works, Westerman and Bonnet identify five ways businesses can innovate: reinventing industries, substituting products/services, creating new digital businesses, reconfiguring value delivery models, and rethinking value propositions. 2 Value reconfiguration is also quite common in the online space. Most online platforms have emerged out of reinventing value in existing industries. And those that have grown exponentially following a unique value proposition accepted by the market also had reconfigured for further growth, lest they lose out to the competition. 3 We use the term “value reconfiguration” to describe this phenomenon and use it in a broader sense of change (augmentation, diminution, or replacement) to an existing value proposition. Based on the research on value creation in platforms, we present a framework for understanding value reconfiguration in online platforms.

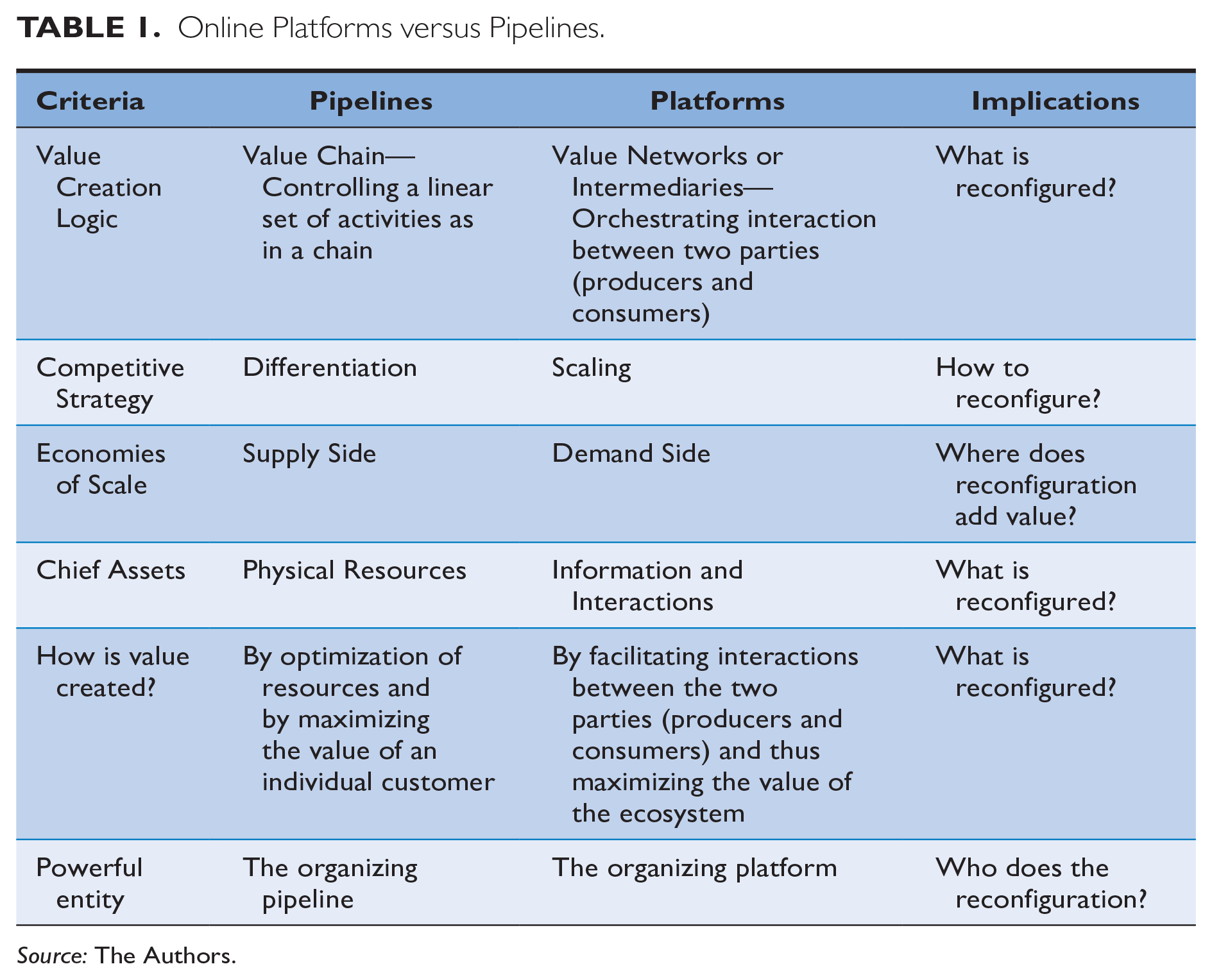

Why is this examination any different for online platforms? Multi-sided platforms have been in existence for a long time. This examination is necessary as the value creation logic is quite different for online platforms (see Table 1). Online platforms scale quickly, as it is evident that out of the top ten firms by valuation, the top five are online platforms. 4 While the principles of scale and scope economies still apply, their form differs as the costs and risks of digitally mediated platform competition are essentially different. 5

Online Platforms versus Pipelines.

Source: The Authors.

First, while most businesses operate as value chains or pipelines (where the value is created by controlling a linear set of activities), online platforms operate as intermediaries (where the value is created by orchestrating interactions between two parties, namely, producers and consumers). 6 They engage two or more sides of the market and enhance interactions among them. Second, the economies of scale are on the demand side in online platforms as against the supply side in pipelines. Therefore, while pipelines create value for their customers, online platforms create value for the entire ecosystem. 7 Hence, online platforms should reconfigure value for the entire ecosystem. Third, while the pipelines configure assets to produce customer value, online platforms configure the information and orchestrate interactions to create and reconfigure value for the ecosystem. 8 Fourth, the online platforms (or intermediaries/value networks) are usually more powerful than the two sides they connect. Particularly, if the market gets tipped, they erect deadly barriers to entry. 9 Contrast it with traditional value chains, such as General Electric or Ford Motors, which have long held powerful positions in their supply chain. Finally, the primary competitive strategy in the case of pipelines is differentiation, whereas online platforms compete by scaling, usually by subsidizing one side of the platform. 10 Therefore, the reconfiguration strategy must be more toward scaling the platform than creating differentiation. Considering these differences, examining reconfiguration strategies in online platforms is necessary to understand their growth strategies.

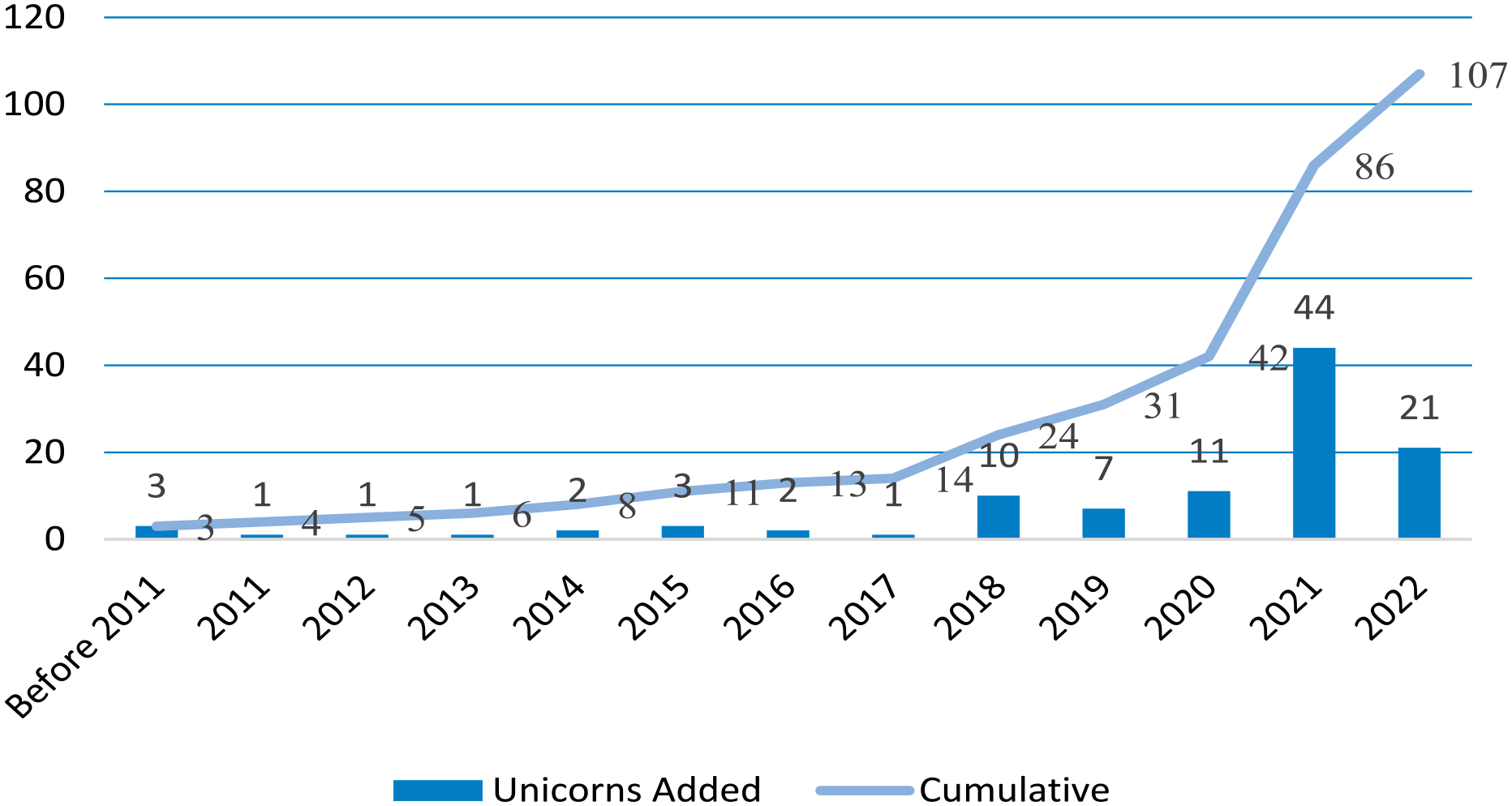

To this effect, we examine why, when, and how online platforms reconfigure. We draw inspiration for our work by examining 13 successful Indian online platforms. India is now the third largest ecosystem after the United States and China in terms of the number of startups. As of August 2022, there are more than 77,000 recognized startups in 56 diverse industrial sectors (IT Services 13%, healthcare 9%, education 7%, professional and commercial services 5%, agriculture 5%, and food and beverages 5%). 11 As of September 2022, around 107 startups have acquired unicorn status—a privately held startup valued at over US$1 billion (see Figure 1). It is difficult to say whether an online platform is successful, given the history of quick failures of even big online platforms (such as Orkut) or the downscaling of Didi in China. 12 We consider online platforms as achieving a certain level of success if they have achieved profitability, gained a substantial userbase and amount of transactions, or have strong investors’ confidence (allowing them a unicorn status). Some of these platforms also operate in markets that have tipped and do not allow the entry of other players. 13 We have considered online platforms from different sectors to render a certain level of generalizability to our findings.

Startups acquiring unicorn status in India (year-wise and cumulative).

Value Reconfiguration in Online Platforms

Why Do Online Platforms Reconfigure Value?

Reconfiguration is a common phenomenon that we witness in the online space. Some prominent examples include the following:

Amazon invested in streaming content. It already had access to a vast customer base, but bundling Amazon Prime with streaming content blocked customers from switching to competitors. 14

Xiaomi invested in the entire Internet of Things (IoT) ecosystem to make its smartphone a controller device for smart homes. 15

Zomato used customer data to provide consultancy to restaurants. 16

Alibaba used customer data to offer preferential advertisement services to sellers on its platform. 17

Reconfiguration is necessary to survive and thrive in digitally mediated competition. Scholarly research has identified the strength of network effects as the core characteristic behind the success of a digital platform. 18 Zhu and Iansiti present five basic network properties that determine the scalability, profitability, and, ultimately, sustainability of online platforms: strength of network effects, network clustering, risk of disintermediation, vulnerability to multihoming, and network bridging. 19 Out of these five, the latter four determine the first, that is, the strength of network effects. Network clustering refers to a network fragmented into local clusters, allowing competitors to enter one’s space. Uber experiences clustered networks as it needs to build a similar network in each city, as against Airbnb, which experiences a single global network. A clustered network weakens the network effects. The risk of disintermediation implies that users on a platform can bypass it to transact with each other. It weakens the network effects and hence potential monetization. Similarly, vulnerability to multihoming (users or service providers present on multiple platforms simultaneously) weakens network effects. Platforms in multiple lines of business can strengthen their network effects by bridging them. For example, Amazon bridges its network effects derived from its web services with the network effects derived from its marketplace. Doing so increases the strength of its network effects. Hence, successful platforms should look for ways to reconfigure value that helps them strengthen their network effects. Based on the recent scholarly work, we generalize four reasons online platforms reconfigure value.

Strengthen turf

Early success with generating network effects does not necessarily indicate continued success, as network effects are fragile barriers to entry. 20 Knee argues that the strength of network effects in online platforms depends on their ability to gain market share at which they can financially break even, the durability of their customer relationships, and their ability to optimize product and price based on the transaction data. 21 Thus, although network effects make online platforms practically invincible, they may still be vulnerable. 22 A few online platforms experience diminishing network effects with time. Uber’s network, for example, is subjected to congestion when many drivers join the platform. An increase in the number of drivers beyond saturation creates negative value for them as they now compete for the same set of riders. Similarly, a competitor may enter with a superior value proposition that may induce negative network effects even in a platform experiencing strong network effects. Consider how Orkut was driven out by Facebook or the threat posed by ChatGPT to Google’s search (an otherwise invincible search platform). Recent scholars have also questioned the assumed unbounded growth in digital platforms arising out of network effects and show that growth becomes limited over a period of time. 23 Therefore, online platforms regularly reconfigure value to strengthen their network effects. 24 They create new growth platforms to build families of products and services and extend their capabilities into multiple new domains to avert existential disaster. 25 They thus establish complementary barriers lest they get displaced by competing platforms. 26 Xiaomi, which started as a provider of Android-based operating systems for mobile devices, became an IoT powerhouse within seven years. 27 It connected with demand- and supply-side stakeholders, and by bolstering tangible benefits for all, it built a solid customer base of tech-savvy and value-conscious customers. After that, it began its IoT journey by using its smartphone as a controller for various smart home products (such as TVs, air conditioners, air purifiers, and smart lamps). It also sought partners who could help it quickly expand the range of its IoT offerings. Although Xiaomi was already an established platform, it reconfigured and made its turf invincible.

Stifle competition

Another reason why platforms reconfigure is to stifle competition. It is similar to strengthening turf (offensive strategy) but attacks the problem from the opposite side (defensive strategy). Teece’s profiting from innovation (PFI) model proposes blocking as a strategy to stifle competition. 28 Once the business is at scale and the market has tipped, online platforms block further competition and build barriers to entry. 29 One of the ways they block the competition is by adding value to their core offering. With access to greater consumer data, online platforms are better positioned to predict what customers want and, thus, provide better value to them. In a head-on competition with Netflix, Amazon India invested in streaming content and bundled it with free delivery through Amazon Prime. The prime subscription coerced customers to repeatedly purchase from Amazon (to recover at least their subscription amount) even if the savings in delivery cost itself was not of much value. By bundling it with streaming content, Amazon could attract several users and intensify competition with Netflix.

Look for new avenues of monetizing the platform

Smart platforms do not just remain matchmakers but invest in capabilities that make network effects fast, simple, and easy. 30 An online platform can look for several growth alternatives in existing or new markets. They can complement their product portfolio with services and access new modes of innovation. 31 Zomato is an excellent example of reconfiguring value for further monetizing its platform. It took various steps to monetize its platform once the Indian food delivery market tipped to Zomato and Swiggy. It started providing consulting services to restaurant owners about customer behavior (including their likes and dislikes). It also invited restaurants to advertise and build apps on its platform (through Zomato Whitelabel). Similarly, Alibaba allowed sellers to join its platform for free while earning revenue through preferential listing and advertising. It provided them with various other services, such as microloans at low interest rates.

Re-invigorate the waning network effects

Hot products often lose steam, so it becomes necessary to evolve to build platforms or service offerings rather than products to avert the existential crisis. 32 Existing platforms witness waning network effects as competitors with superior value propositions enter the competitive space. With the widespread acceptance of WhatsApp and Instagram, Facebook saw decreasing usage of its platform and, hence, waning network effects. Similarly, the search engine market tipped toward Google, although many other search engines (such as Bing) were in the market. Google remained the winner-take-all for many years and had almost 97% market share in most countries. From 2000 to 2010, other e-commerce giants started building their turf in the search business. Amazon became the search engine for products, as LinkedIn and Facebook were for people. With the mobile platform becoming prominent, Google could have lost even mobile searches had it not launched Android, 33 an operating system for mobile devices for free where third parties also complement through building their mobile apps. As the searches begin to move to voice (such as Siri and Alexa), Google is in tough competition with Amazon and Apple to retain its hegemony in the search business. And hence, there is a need for value reconfiguration to prevent network effects from waning.

When Should Online Platforms Consider Reconfiguring Value?

Online platforms usually experiment with their value proposition to identify how to target their users. We do not consider such experiments as value reconfiguration. We consider value reconfiguration as any reconfiguration after a platform has gained sufficient scale. Therefore, sufficient scale is necessary for an online platform before it starts reconfiguring value. What is sufficient is subjective and varies from platform to platform. There could be various inflection points when a platform may consider reconfiguring value. First, an online platform has reached the scale where network effects have kicked in. It is now growing due to its network effects and considers value reconfiguration for the various reasons mentioned earlier. Second, the market has tipped to a few players, and entry of competitors is next to impossible. The platform now considers avenues for monetizing its platform. Third, the platform has achieved profitability and wishes to remain sustainable. Fourth, investors are willing to invest heavily in the platform for a small percentage of equity. The platform is now trying to reconfigure using such investment for further growth in the market.

Conceptualizing Value Reconfiguration in Online Platforms

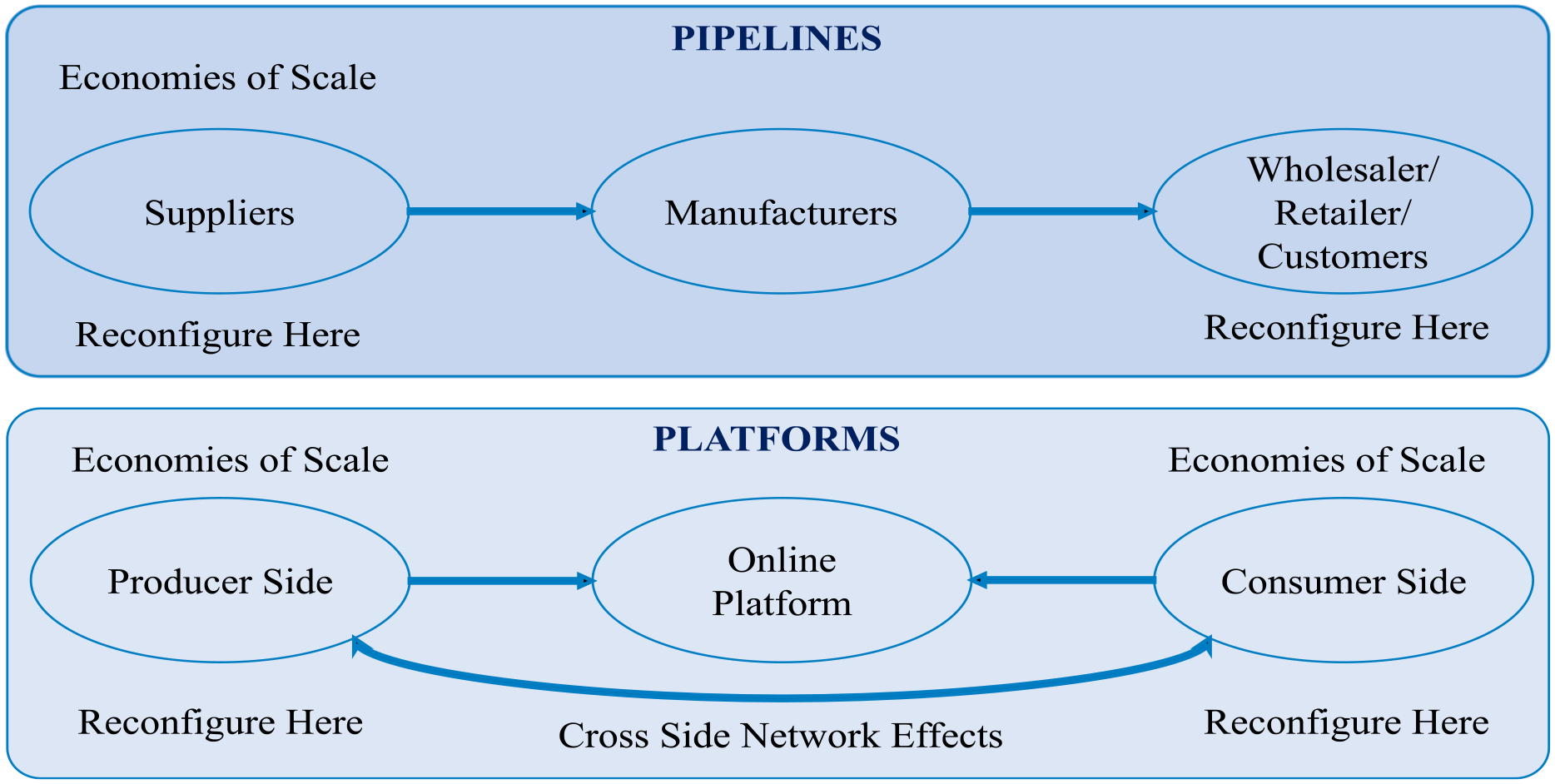

As discussed earlier, online platforms differ from pipelines (see Figure 2). In pipeline businesses, economies of scale are on the supply side. That is, the greater a firm produces, the better its marginal profitability. Thus, a firm may achieve scale through market penetration and market development. Further growth happens when it launches new products or diversifies. 34 Again, if it launches new products, it needs to achieve sufficient market to achieve economies of scale. In an online platform, economies of scale are on the demand side. Therefore, online platforms attempt to achieve scale by quickly building their userbase. Cross-side network effects between its two sides help it achieve such a scale quickly. Thus, reconfiguration should happen on both sides of the platform (the producer and consumer side). Moreover, reconfiguration should enhance value for the entire ecosystem, as against pipelines, where value is enhanced primarily for customers. In other words, online platforms can enhance value by reconfiguring the provider, consumer, or both sides.

Conceptualizing value reconfiguration in pipelines and platforms.

Value can be reconfigured in various ways, such as substituting products/services, creating new models of value delivery, and providing more value for the same product. 35 Online platforms also reconfigure value for exerting greater control over the ecosystem or for improved governance. 36 We focus on value reconfiguration from the perspective of strengthening network effects, considering that online platforms create value by enhancing their network effects. 37 Therefore, we conceptualize strategies for value reconfiguration in online platforms depending on which side benefits from such reconfiguration by experiencing enhanced network effects.

Method

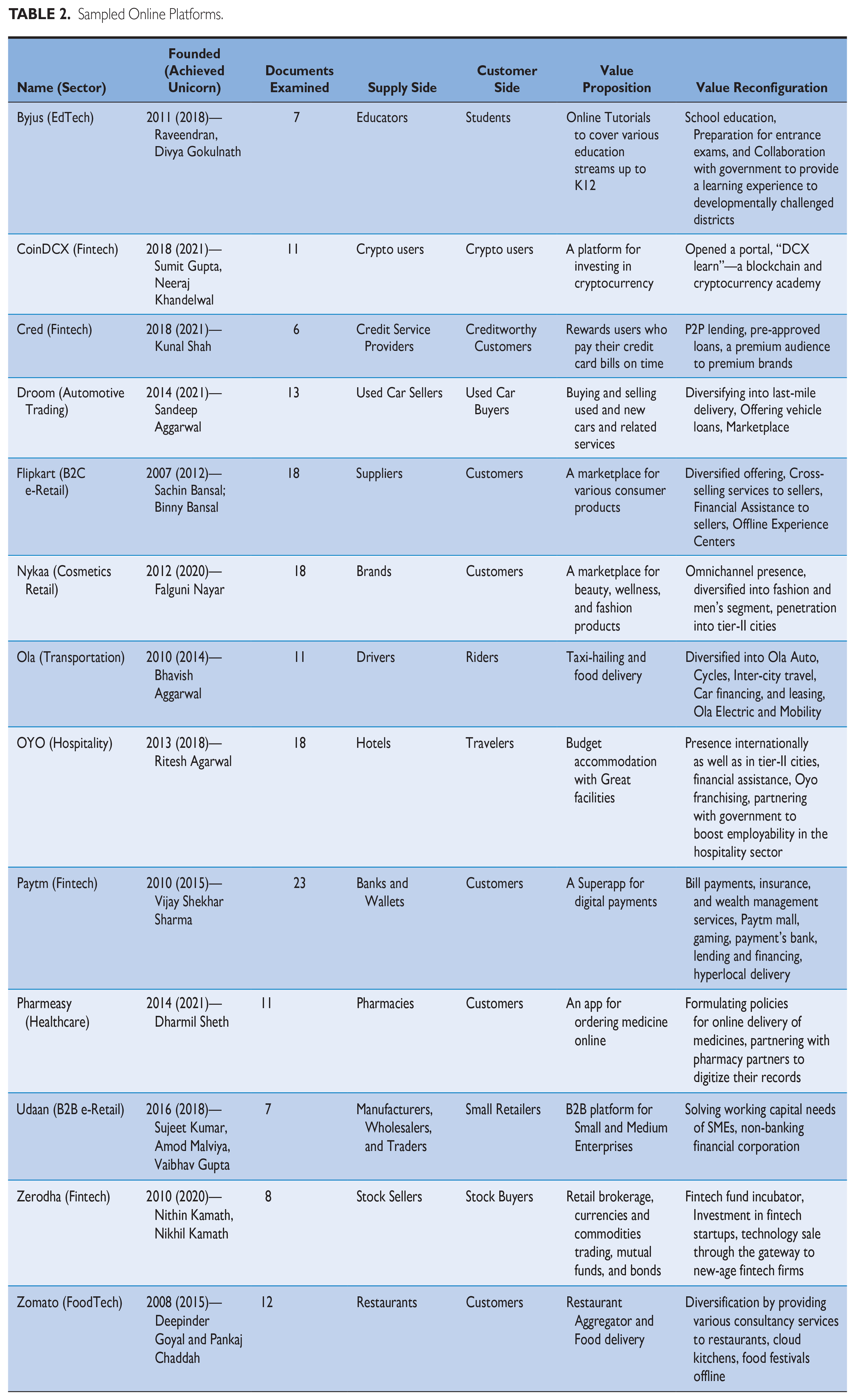

We conducted an exploratory examination of the 13 Indian online platforms that have been unicorns for at least a year. Examining cases is appropriate for investigating new and developing phenomena to create new theories. 38 We relied on theoretical sampling for our case selection. 39 Being a unicorn is not necessarily an indication of success. It simply reflects an investor’s confidence in an online platform. These platforms fulfill one or more of the criteria mentioned earlier (i.e., profitability, substantial userbase, or strong investors’ confidence). The selected online platforms represent various sectors, such as EdTech, Online retail, Fintech, Hospitality, Fashion, Taxi, Food, Pharma, and Used cars (see Table 2). Out of 42 platforms that became unicorns by 2020, we selected nine prominent ones representing diverse sectors. We added four more well-known unicorns of 2021 to represent healthcare, automotive retail, and a different kind of Fintech. These cases have different founding dates spread across a decade, which helps mitigate any bias due to macroeconomic conditions prevalent at a point in time and hence leads to better generalizability.

Sampled Online Platforms.

We studied the website of each unicorn to understand its present offerings to all sides of its network. We then collected data for each of these unicorns on the Internet. The study of the website provided us with the key directions around which the search had to be targeted, along with a general search around the strategies adopted by the case. The data included online news and magazine articles. Since the Internet offers a vast spectrum to search, all cases were searched for a particularly new theme when encountered to ensure proper coverage. For example, on discovering a new theme private label for the online platform “Nykaa” in the general search, we made a directed search for this phenomenon for all the other online platforms. Thus, we conducted multiple iterations till no new themes emerged. We also searched for the interviews of the founding members published online, interviews with founders, and expert analyses from various websites. Since the founding dates of the unicorns varied, the data available for each online platform varied from 30 to 150 months. We examined a total of 163 documents.

We first examined the business model of the unicorn and made notes about its various sides and value propositions. We then identified specific themes within the content collected from news and magazine articles (such as private labels). We then searched for such themes for each unicorn. One of the authors then thoroughly searched and read the case-related information to identify the steps taken by the case. The other author was initially kept out of the coding activity to act as the “Devil’s advocate” in evaluating the assigned codes. 40 Thus, we conducted multiple iterations till no new themes emerged. We then manually coded these themes to identify the best practices. Then, we collected interviews conducted by leading media houses for each of these unicorns to examine their perspective. Table 2 presents a snapshot view of the sampled online platforms.

Findings

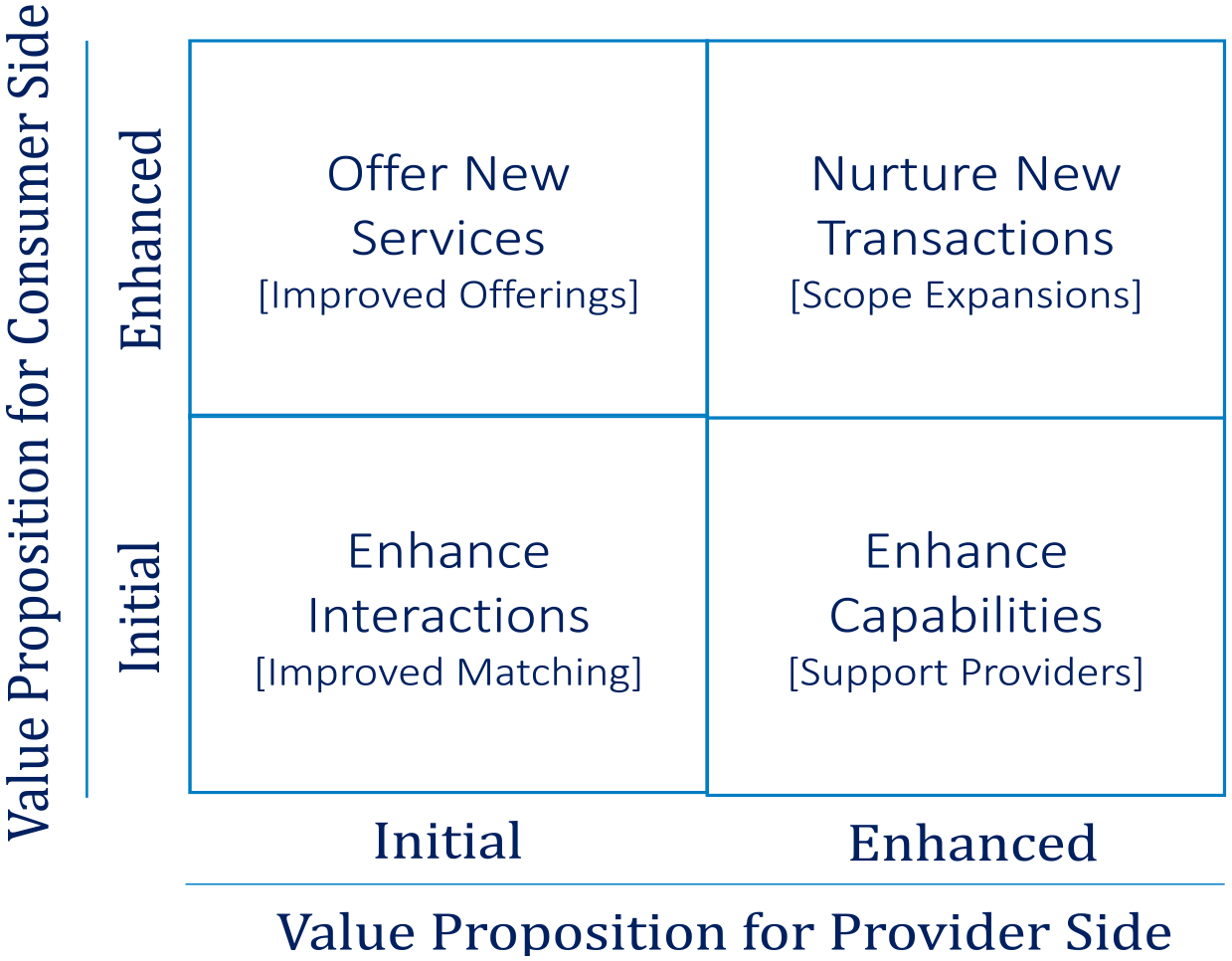

By examining where the value was created by the online platforms (producer side, consumer side, or both), we could identify four strategies (see Figure 3) that platforms apply to reconfigure their value: enhance interactions, enhance capabilities, offer new services, and nurture new transactions.

Reconfiguration strategies for online platforms.

Enhance Interactions

With time, the existing userbase (both producer and consumer side) starts dwindling. 41 It is natural as they become aware of the flaws/limitations in the initial value proposition and expect improvement. They may begin multi-homing or switch platforms for a better value proposition. To prevent such situations, online platforms improve matchmaking between providers and consumers. They do so primarily by leveraging transaction data. By analyzing transaction data, online platforms provide a better customer experience. Here, the value reconfiguration happens by enhancing the match on the initial value proposition for both the provider and consumer side. For example, Google Search provides recommendations as one inputs words in its search bar, thus providing better matching. Doing so prevents searchers from switching to other search engines. Improving matchmaking strengthens turf and reinvigorates the waning network effects.

Several online platforms leverage customer data to provide an enhanced experience. Byjus—the leader in the Indian Edtech space—has grown fast with the help of its analytics engine. It provides a personalized learning experience to its students using artificial intelligence and machine learning:

“The backbone of BYJU’S personalization engine is its rich learning profile. It is powered by deep Knowledge graphs of over one lakh concepts and relationships that have been created to design personal learning journeys—videos, questions, adaptive flows, quizzes, flashcards, correctional learning videos, and so on. Additionally, the learning content is also tagged to multiple other properties and parameters. For example, when a student starts their learning journey, a rich learning profile is built for each student to personalize the experience. This enables us to customize and personalize the learning experience based on their strengths and weaknesses, and their specific learning gaps, pace, and needs.” (Byju Raveendran, CEO, Byju’s)

42

Similarly, Droom—an online platform that facilitates the buying and selling of used cars—has leveraged the capabilities of artificial intelligence and machine learning to create algorithms for inspecting and evaluating vehicles, leveraging images and historical data. It offers a marketplace where most players are focused on product discovery only:

“We have been creating India’s most delightful experience in buying and selling automobiles online. Lately, we have been investing in making loans and insurance easier after you buy an automobile at Droom. We are also investing heavily in our last-mile delivery solution for the automobile, including a test drive or delivery of a car at your doorstep in a flatbed truck.” (Sandeep Agrawal, CEO, Droom)

43

Enhance Capabilities

Online platforms need to reconfigure the value proposition for the provider side. Generally, they generate growth by incentivizing the provider side to join the platform. Usually, online platforms provide additional monetary incentives if the provider side is able to achieve its targets. Such incentives may also take the form of financial assistance for enhancing the capabilities of the provider side. Several online platforms (such as Flipkart, OYO, Ola, and Droom) provide financial assistance to suppliers. Financial assistance, however, locks the provider side to the online platform till they clear their debts. As growth kicks in, such incentives dwindle, provoking the provider side to look for a better value proposition. Multi-homing weakens network effects, so online platforms need to enhance the value proposition for their suppliers. They do so by enhancing the capabilities of their suppliers by providing consultancy, financial assistance, and a bouquet of services. Enhancing capabilities also offers online platforms new avenues of monetization and stifles competition to a certain extent.

Zomato—an online player in the food delivery space—has invested heavily in educating its partners (restaurant owners). In its Zomato Kitchen offering, it works with certain restaurant owners who wish to expand their business to more locations with minimum cost. Leveraging the transactions’ data on its platform, it offers consultative services to new restaurants to expand in new geocodes. Zomato is now offering Zomato Pure—supply chain management of the raw material for the restaurants by working directly with the farmers, mills, and producers to provide the raw material. It also collects used cooking oil from them and delivers it to bio-diesel plants. By providing more services, Zomato adds more revenues from the same userbase.

Paytm Mall, which started as a marketplace for various product categories covering daily essentials, grocers, and electronics, has adopted the o2o (Offline to Online) model, bringing the existing offline stores online. After customers order products online, it transfers them to the brand/offline stores for installation and delivery, thus eliminating warehouse and logistic infrastructure. It thus brings greater revenue for offline merchants because of its hyperlocal nature. Paytm also offers onboarding support to its sellers for digitalization and taxation rules and hence tries to cover more related needs of its stakeholders. Doing so also allows it to earn more revenues from the existing userbase.

Similarly, Udaan—an online platform in the B2B retailing space—that connects suppliers to retailers has also done good work in developing the capabilities of small retailers. It leverages the power of artificial intelligence and machine learning to calculate creditworthiness, provides voice assistants on its app, route optimization, and other data-driven value-added services to sellers. It has identified the root cause of retailers’ problems in sourcing. Retailers lack a credit system for working capital, due to which they source from suppliers at dictated costs. These suppliers, in effect, provide for their working capital. Udaan offers products on credit by considering the transaction history of the retailer. Thus, it has become an NBFC (Non-Banking Financial Corporation) by solving the credit problem of retailers:

“It is difficult for them to get a loan or a working capital line from a financial institution like a bank. Hence, suppliers, wholesalers, family, and friends become the people who finance these merchants. Now, Udaan is trying to address these problems by coming onto the platform to make credit transparent. We create credit lines for our buyers based on their transactions and user behavior on the platform. This enables us to create a credit product, which is based on economic data, and is transparent to both buyers and sellers.” (Sujeet Kumar, Co-founder, Udaan)

44

Offer New Services

Online platforms also reconfigure value propositions for their consumer side. Once a platform has garnered a substantial userbase, it can leverage it by providing new services. By providing related services that enhance the initial value proposition, online platforms strengthen their turf, reinvigorate waning network effects, and build new avenues for monetization.

Cred—an online platform that rewards users for paying their credit card bills on time and assigns them a credit score—amassed a substantial 1 million creditworthy users in just two years. It then pitched its creditworthy userbase several related services that can be obtained when a user has a credit score of 750 (scores range from 300 to 900). 45 An increased credit score helped users apply for a higher loan amount from any bank and access pre-approved loans from the Credit store. Another program, “CRED cash,” allowed users to access a pre-approved credit line of INR 500,000 simply on the app, without any documents, calls, or physical visits. 46 CRED members could receive this amount instantly in their bank accounts. Since the creditworthy user side could act as both lenders and receivers, Cred launched Cred Mint in association with Liquiloans (a P2P non-banking finance company registered with the Reserve Bank of India), a peer-to-peer lending platform whereby its eligible users can lend money (0.1-1.0 million INR) at up to 9% per year interest rate. 47 Cred spreads such loan amounts on around 200 plus eligible borrowers.

Another player in the Indian Fintech space—Paytm—started with digital payments. It gained prominence during demonetization when the government of India encouraged people to use digital payments.

48

Paytm is now a super app facilitating peer-to-peer transactions through its digital wallets. Users can now use it to pay bills, recharges (such as MobileSim and FASTag), and insurance and wealth management.

49

Paytm has partnered with other financial institutes to provide lending options to its users. It has also entered into gaming and content to keep its users engaged:

“We are clear that content is an obligation of a customer’s daily life. When consumers open Paytm for a transaction, we don’t want to restrict it to just that. We want to make something available so they can keep coming back. That [is] making us go into gaming and content.” (Vijay Shekhar Sharma, Founder, Paytm)

50

Similarly, OYO—an online platform for booking varieties of low-cost accommodation—has expanded its offerings in related spheres such as corporate stays, wedding destinations, and leisure stays. To start the franchise model, it has partnered with the hotel owners and converted their property into OYO property. Anybody can walk in and book accommodation as in any other hotel. Now, it offers a variety of accommodations in several markets:

“We started our foray into real estate with the launch of OYO LIFE, our long-term rental offerings, followed by the Weddingz acquisition. More recently, with the acquisition of the @Leisure Group, rechristened as OYO Vacation Homes, we became one of the largest vacation rental companies in the world. In all these cases, we are offering something new while remaining true to our core mission of creating quality spaces.” (Ritesh Agarwal, Founder and CEO, OYO)

51

Online platforms also enhance their existing offerings through related acquisitions. Pharmeasy—an online platform in the heavily regulated pharmacy space—provides several offerings over its basic service of delivering prescription and over-the-counter pharmaceutical drugs to the home. It serves a wide range of healthcare needs of its users and provides teleconsultation services. It has also acquired Thyrocare—an established firm in diagnostic tests. Now, users can call its agents at home for sample collection and receive their diagnostic reports online. Most sample collections (such as blood, urine, or stool) require patients to fast (even from water). Collecting these at home makes life easier for patients as they do not have to go to the diagnostic centers and wait in line for their turn.

Having access to customer transaction data, platforms can generate insights about the unfulfilled needs of the market. They try to address those needs if economically viable. For example, Flipkart—an online retailer now owned by Walmart—has penetrated different aspects of customers’ needs and product categories, like the sale of refurbished products through 2gud.com (starting with the phone segment). It has expanded its offering through various acquisitions, such as Cleartrip for online ticketing and Myntra for fashion products:

“In 2013, we were doing similar things—both Myntra and Flipkart were selling fashion in a similar way. At that time, deciding took a while, but within a year, we saw Myntra doing a lot of things that were really different from Flipkart. So, the front end became very different. They were investing a lot into private brands, so they were building their own brands as well, which customers liked. They were really doing a lot of fashion-only things, which Flipkart would never do on its platform. Flipkart was always known to be a horizontal platform. At the end of that second year, we were kind of neck and neck in sales. So, we thought it made a lot of sense having Myntra in the fold as well because that would help us when our customers were really fashion-first and fashion-forward. Flipkart worked to cater to customers who would prefer the right apparel or the right shoes and were seeking more value. So that way, we could attack both segments, and it has played out really well. Since we acquired Myntra, it has grown almost 15 to 20 times within four or five years.” (Binny Bansal, Co-Founder, Flipkart)

52

Nurture New Transactions

Online platforms reconfigure value by nurturing new transactions. Nurturing new transactions takes the form of scope expansions, such as creating new channels to provide a seamless experience to their customers (omnichannel strategy) or reaching more customers (alternate channels/franchises). Doing so allows them to access new markets and thus strengthen their turf, stifle competition, and generate new avenues for monetization.

An excellent example of the omnichannel strategy is Nykaa—an online retailer in the women’s fashion space—which has leveraged the power of its data. It started with catering to cosmetics and personal care for women and later diversified into fashion and offers for the men’s segment. It also built on its strong offline presence for better conversion rates online and by entering smaller cities in India. It has expanded and opened offline stores and kiosks in offline shopping malls, where users can purchase and get suggestions on beauty and fashion from the store staff.

“Today’s customer is a 100 percent omnichannel customer. They want the convenience of being able to shop in whichever way is most convenient, whether on mobile, social media, or at a store. We talked to our customers a lot, and they were asking for it. They wanted to interact with the brand. Women are demanding these products.” 53

Online platforms also empower different categories of suppliers by entering into private labels. Such suppliers do not carry any brand name, though they supply the same product quality to various brands. Having access to customer transaction data, online platforms are aware of the price point at which customers purchase various products. They then launch products with a private label near this price point. Private labels have huge margins (almost double that of brands) in specific product categories

54

:

“If you look at any successful retailer globally, they have a pretty large and sustainable business of private brands across categories. Somewhere in the middle of 2016, as a leadership team, we sat down and looked at our business over the next 3-5 years. One of the many things that came out as an area of opportunity was the lack of a private brand business.” (Adarsh K. Menon, Vice-President and Head of Private Brands, Flipkart)

55

Nykaa has leveraged the power of its data to launch new products under its private label:

“A lot more Millennials have been coming to our website, and they have been telling us about trends, and what we are doing is that we are listening to them and launching products that they have been telling us to launch. . . . We believe private labels in fashion will have a far higher percentage share than beauty and could contribute up to 40% as the business grows. We don’t want to be a discount-led fashion website; we would rather be a curated, style-led one.” (Falguni Nayar, Founder and CEO, Nykaa)

56

Other platforms are also foraying into omnichannel strategy. Flipkart is opening offline experience centers—buy zones, where customers can walk in to get the touch and feel of the product before ordering online. Byjus has acquired the Indian offline coaching institute “Akash”—a leader in providing offline coaching for prestigious entrance exams to engineering and medical graduate courses to put a strong foothold in its omnichannel presence. Zomato organizes food festivals to assert its offline presence. Paytm has ventured into an online-to-offline model for hyperlocal delivery.

Online platforms also create alternate channels to reach more customers. Byjus facilitates live interactions to reach more customers. According to a fixed schedule, it provides richer connection-offering products, such as live tutoring and doubt resolution sessions. This is in addition to leveraging self-paced learning through pre-created content and technology-assisted adaptive learning. Byjus has partnered with the tech giant Google to offer its pedagogy for free to participate in the pilot project at schools in India for the digital transformation of educators (Project Vidyartha). It has also partnered with the Indian government policy think tank Niti Aayog to offer a quality learning experience to a few developmentally challenged districts. Thus, it is a step toward making its curriculum penetrate schooling systems and impact the entire education ecosystem.

Zerodha—an online discount stockbroker—has launched a partner or remisier program, a stockbroking franchise model based on revenue sharing. The partners act as mini hubs to get trading clients for Zerodha. They could open their offices or operate in any other flexible manner. It has also opened Rainmatter. Rainmatter is its fintech fund and incubator for investing in several fintech startups to grow the Indian capital markets. It offers its ingenious technical infrastructure through an accessible gateway (Kite connect) to new-age fintech firms to build their platforms. Hence, it infuses standards in this domain based on its Application Programming Interface (API)-based technical platform developed ingeniously by its Full Stack Developers:

“We believe that just great charting and trading tools or zero brokerage won’t be enough. Using Kite Connect, we are providing an easily accessible gateway to new-age fintech firms to build their platforms using Zerodha infrastructure.” (Nitin Kamath, CEO, Zerodha)

57

Similarly, CoinDCX—a cryptocurrency exchange—has opened an investment wing that provides for incubating new startups in this field, partnering with premium engineering colleges in India and research labs globally to foster research and train the talent for this new emerging blockchain and related domains like preventing money laundering:

“The funds raised will be allocated to expand (bring more Indians to crypto and make crypto a popular investment asset class in India). Apart from this, we will be joining hands or entering into partnerships with key fintech players to expand the crypto investor base, set up a Research and Development (R&D) facility, strengthen policy conversations through public discourse, work with the government to introduce favorable regulations, education and amping up the hiring initiatives.” (Sumit Gupta, Co-founder and CEO, CoinDCX)

58

Reconfiguration Strategies and Network Effects

We found that online platforms regularly reconfigure to enhance their network effects. The four reconfiguration strategies—enhance interactions, enhance capabilities, offer new services, and nurture new transactions—address the four reasons for reconfiguration (strengthening turf, stifling competition, looking for new monetization avenues, and re-invigorating the waning network effects). Although online platforms figure out several avenues of monetization through reconfiguration, actual monetization depends on their pricing strategy.

In terms of strengthening network properties as promulgated by Zhu and Iansiti, these reconfiguration strategies strengthen network effects, reduce multihoming, and possibly bridge networks. 59 Their effect on network bridging depends on how well an online platform bridges network effects in its platform. Similarly, their effect on reducing the risk of disintermediation depends on a platform’s monetization strategy. Alibaba could allow sellers and buyers to bargain on its platform as it did not charge them, leaving them with little incentive to disintermediate. Thus, a platform does run the risk of disintermediation if it does not have a proper monetization strategy.

Reflections on Global Online Platforms

Indian space is a nascent space for online platforms. Most of the online platforms we examined were either one-sided or two-sided platforms. All the 13 sampled Indian online platforms have scaled and are now reconfiguring their value in some form. Given the realities and frailties of the Indian ecosystem and the lack of infrastructure, they scaled quite fast. They may not all be profitable yet, but given the emphasis on the core, they might turn profits quickly. Surprisingly, none of these online platforms had advertisement as their primary revenue model. They may invite advertisements from within their supplier base, but advertisers do not form any side in these platforms. Contrast this with the platform giants originating from the United States. Facebook, Google, and Amazon, for example, are all multi-sided platforms. Facebook and Google are primarily driven by advertisements. Bringing in advertisers has a waning effect on the network effects as users who do not wish to be interrupted by advertisements may start leaving the platform. Apart from these structural differences, the value reconfiguration strategies, as promulgated in this article, apply to global online platforms.

Enhance Interactions

Once a platform scales, the userbase must remain engaged. If the interactions on a platform are reduced, it is a sign of waning network effects. Platforms keep their users engaged by enhancing their offerings. They also leverage transactional data and acquire firms to enhance their offerings, thus enhancing interactions between the two sides. Enhancing interactions helps strengthen the cross-side network effects for the firm. Unlike offline firms, online platforms benefit from having access to the transaction data, which they can slice and dice to generate meaningful insights and enhance interactions between the two sides of the platform. Global online platforms also enhance interactions between their sides and reconfigure services to keep the users engaged. For example, Amazon regularly analyzes transaction data to reconfigure its offerings.

However, online platforms must be careful in deriving conclusions from data. In a recent move, Zomato launched ten-minute delivery, copying Blinkit’s ten-minute delivery strategy. 60 It noticed that customers were looking for restaurants with shorter delivery times. Zomato felt that the future is for faster delivery times. However, the model received severe criticism from the public, as it endangered the delivery crew and traffic management. Changing to a ten-minute delivery also required Zomato to move away from its focus on meals to snacks, as most meals cannot be prepared and delivered in ten minutes. Facing mounting losses, Zomato had to shut down its ten-minute delivery. 61 Leveraging customer data to stifle competition also invites the attention of anti-competitive regulatory bodies. If convicted, the penalties could be very severe. Zomato also came under the scanner of the Competition Commission of India, which highlighted the possibility of its using consumer data to stifle competition. By analyzing transaction data, online platforms launch private labels/cloud kitchens at the desired price points. Such stifling of one’s complementors using the transaction data is prohibited by regulations.

Enhance Capabilities

Online platforms empower their provider side by providing them with a slew of services, thus enhancing their businesses. While this is not a very common practice among offline firms, several global online platforms do practice this as a strategy. For example, they offer microloans at reduced interest rates. Alibaba provides financial support to several suppliers and, in turn, has gained a loyal userbase. This is because online platforms know more about their users than most loan-providing institutions. Amazon empowers its providers with various services, such as packaging and logistics. They also provide insights to the provider side, helping them to improve businesses.

However, such enhancement of capabilities could also be seen as an encroachment into the profits of sellers or an attempt to lock them in with the online platform. Consider the case of Ola/Uber services in the Indian city of Bangalore. There has been strong unrest from the drivers on account of Ola/Uber charging high commissions (to the tune of 20%-30%) from the drivers. Particularly those who are now locked in because of availing loans from Ola/Uber are unable to leave the platform. 62 Such an attempt to lock in the userbase may invite anti-competitive inquiries and/or legislative policies that may go against the platform. Similarly, several Amazon/Flipkart sellers (particularly small ones) are opposing their opaque/one-sided governance policies and have taken legal recourse by forming an association. They find their profits dwindling and losing connections with their customers (as their customers are now customers of Amazon/Flipkart). 63

Offer New Services

Online platforms offer new and related services and thus reconfigure value propositions for their consumer side. The common thread in the successful Indian online platforms was that they all provided related services. Related services enhance existing network effects. Global platforms also offer new services to their existing userbase. For example, Facebook offered several new services to its userbase, including newsfeed and e-commerce, advertising, and third-party apps.

However, new services should be related to the platforms’ initial value proposition, or else it may deter the userbase. For example, Askme started as an infomediary and provided information about local businesses to consumers. It later attempted to leverage the userbase by becoming an online retailer, but failed miserably. 64

Nurture New Transactions

After a few years of operations, a few online platforms entered into offline space through an omnichannel strategy. They open their offline presence either directly or through franchises. Quite common is the opening of experience centers, where people experience their products offline and order online, or vice versa, where people experience their products online and order offline. Most global online platforms have also entered into omnichannel retailing. Threadless—a global community-driven online platform for t-shirts and similar merchandise—opened its experience centers for people to experience the story behind its unique designs. Apple has also opened a few offline stores across the world.

Again, such moves, particularly launching private labels, invite anti-competitive inquiries. The government of India has proposed disallowing private labels by brands associated with e-commerce platforms for promotion or sale. 65

Conclusion

By examining 13 Indian online platforms, we identify four prominent strategies that online platforms use to reconfigure their value after gaining scale. These include enhancing interactions, enhancing capabilities, offering new services, and nurturing new transactions. While several scholars present these strategies well, we add value by categorizing them as a 2 × 2 framework. The context of India also plays an important role in how online platforms configure value. The value reconfiguration must strengthen an online platform’s existing network effects for a firm to become stronger. 66 However, platforms must be careful as value reconfiguration moves may come under the scanner of anti-competitive agencies if they allow undue leverage of the provider side. Practitioners can use this framework to judge the potential success of an online platform in terms of its ability to strengthen network effects.

Footnotes

Acknowledgement

We would like to acknowledge the editor and anonymous reviewers for their excellent and insightful review comments that helped shape this paper. This paper has benefited enormously from the review process of CMR.

Notes

Author Biographies

Kuchi Sanchita is the Director (Data Science) of AI Labs at American Express and is pursuing doctoral studies at the Indian Institute of Management Raipur in the area of Information Systems (email:

Sumeet Gupta is a Professor of Information Systems at the Indian Institute of Management Raipur and pursues teaching and research in electronic commerce (email: