Abstract

Why are government jobs so attractive to talented individuals in many non-democratic countries? We identify state power as a key factor. We analyze the impact of China’s recent value-added tax reform, an expansion of taxation power, on citizens’ preferences for tax administration positions, as revealed by participation in the National Civil Service Exam. Using a difference-in-differences approach that leverages pre-reform subnational variation in tax composition and a dataset of 166,012 government job openings from 2010 to 2021, we find that the reform attracted more and higher-ability individuals to tax-related state positions. The effect is particularly strong for positions involving greater regulatory power or those located in prefectures with higher graft opportunities. An original survey reveals that exam takers perceive increased power and benefits in tax agencies after the reform. Evidence from Chinese General Social Surveys suggests the talent drawn to the state likely comes from the private sector.

Introduction

In Democracy in America, Alexis de Tocqueville observed, “it is a constant fact that in our day, in the United States, the most remarkable men are rarely called to public offices” (Tocqueville, [1835] 2000). Tocqueville believed that in democracies, civil servant jobs are not particularly enticing to society’s brightest minds. This is because democratic institutions channel the public’s aversion to elitism, particularly in government offices. The instability of government careers due to elections and term limits further dissuades accomplished individuals from pursuing them. In stark contrast, citizens in less democratic or non-democratic countries often exhibit a strong preference for government jobs. In Bangladesh, such jobs are considered privileges and significant opportunities. The introduction of a quota system limiting students’ access to civil servant jobs in 2024 sparked nationwide protests and violent crackdowns, resulting in 200 deaths and thousands of injuries and arrests. 1 Similarly, in China, millions of individuals take the Civil Service Exam annually in hopes of securing a government position. For instance, in 2021, the most sought-after jobs attracted a staggering 20,602 applicants competing for a single position. 2 At top Chinese universities such as Tsinghua and Fudan, 50%–70% of graduates land positions within the state sector every year. 3 China and Bangladesh are not isolated cases. Similar preferences for government jobs are evident in Singapore, Iran, Vietnam, Russia, Egypt, and many other non-democratic countries. What explains non-democratic governments’ ability to attract talented individuals to the state?

In this paper, we identify state power as a key factor attracting talent to the state apparatus in non-democratic regimes. Following Way (2005), we conceptualize state power along three dimensions: control, scope, and size. Control refers to top officials’ ability to enforce obedience from subordinates to suppress opposition and maintain stability, enabled by centralized fiscal and administrative power. Scope encompasses the range of issues under state influence, with such regimes expanding control over the economy and society to stifle opposition and limit private sector autonomy. Size involves the nationalization of key sectors to expand state reach and secure internal resource control. Together, non-democratic regimes often expand state power by enhancing central fiscal capacity and broadening the scope and size of control for political survival. Although the broader literature often discusses these processes under the heading of state building, our argument focuses more specifically on state power expansion, by which we mean the expansion of the state’s fiscal, coercive, and regulatory reach in non-democratic regimes.

Unlike state building in liberal democracies, which often emphasizes representative institutions, the rule of law, and accountability mechanisms that limit the opportunities for public officials to benefit from state power, state power expansion in non-democratic regimes invariably yields tangible rewards for those within the system. For example, enhanced central fiscal capacity enables the regime to allocate more resources, offering state employees better material benefits. The expansion of state control over the economy and society, often at the expense of the private sector, not only makes careers in the state sector more secure and promising but also grants state employees opportunities to secure privileges and extract graft from society, especially given that checks on the authority of government officials are limited in these regimes (Frye & Shleifer, 1997). Perceiving the benefits of government jobs in a powerful state, talented citizens are thus attracted to the state apparatus. This logic may also extend to weak or illiberal democracies, where limited institutional constraints allow state power expansion to yield comparable private returns for public officials.

The ability of a powerful state to attract talent is especially strong when combined with merit-based recruitment. Leaders in non-democracies have long utilized the state sector to co-opt societal actors (Ang, 2016; de Mesquita et al., 2005; Liu, 2023; Magaloni, 2006; Rosenfeld, 2017; Svolik, 2012). However, if the hiring of state employees relies on connections, clientelism, or nepotism (Calvo & Murillo, 2004; Fukuyama, 2014; Hassan et al., 2023; Jiang, 2018), a powerful state may draw more individuals to the state sector but not necessarily those of high ability. Faction-based political selection and the tendency to prioritize loyalty over competence can also impede these regimes’ capacity to attract high-ability talent from society (Shih et al., 2012; Zakharov, 2016). Nevertheless, if a regime can implement merit-based recruitment, even partially, in its political selections—as has been observed in many countries such as China (Landry et al., 2018; Liu, 2023) and Ghana (Brierley, 2021)—then a powerful state is likely to attract a significant amount of talent to the regime. 4

To provide empirical evidence, we examine the impacts of China’s value-added tax (VAT) reform—a recent expansion of state taxation power—on citizens’ preferences for tax administration positions revealed through participation in the National Civil Service Exam (NCSE). Between 2012 and 2016, China implemented the most significant tax reform in the past two decades by effectively replacing the business tax (BT) with the VAT. The stated purpose of the VAT reform was to ease the tax burden on service industries, but it also significantly increased central tax bureaus’ tax-extraction capacity (Zhang, 2021, p. 53). This enhanced central fiscal capacity is a critical feature of state power expansion. Moreover, VAT has a self-enforcing nature because it incentivizes downstream client firms to request invoices from suppliers to reclaim the VAT they have paid. This chain of tax enforcement makes tax evasion more challenging for private enterprises (Pomeranz, 2015), especially when compared to the BT system, where high nominal tax rates in China made evasion extremely prevalent (Zhang, 2021, p. 77). By enhancing tax enforcement through the VAT system over a much larger number of enterprises that previously paid the BT, the VAT reform also expanded the scope of state control—another critical feature of state power expansion.

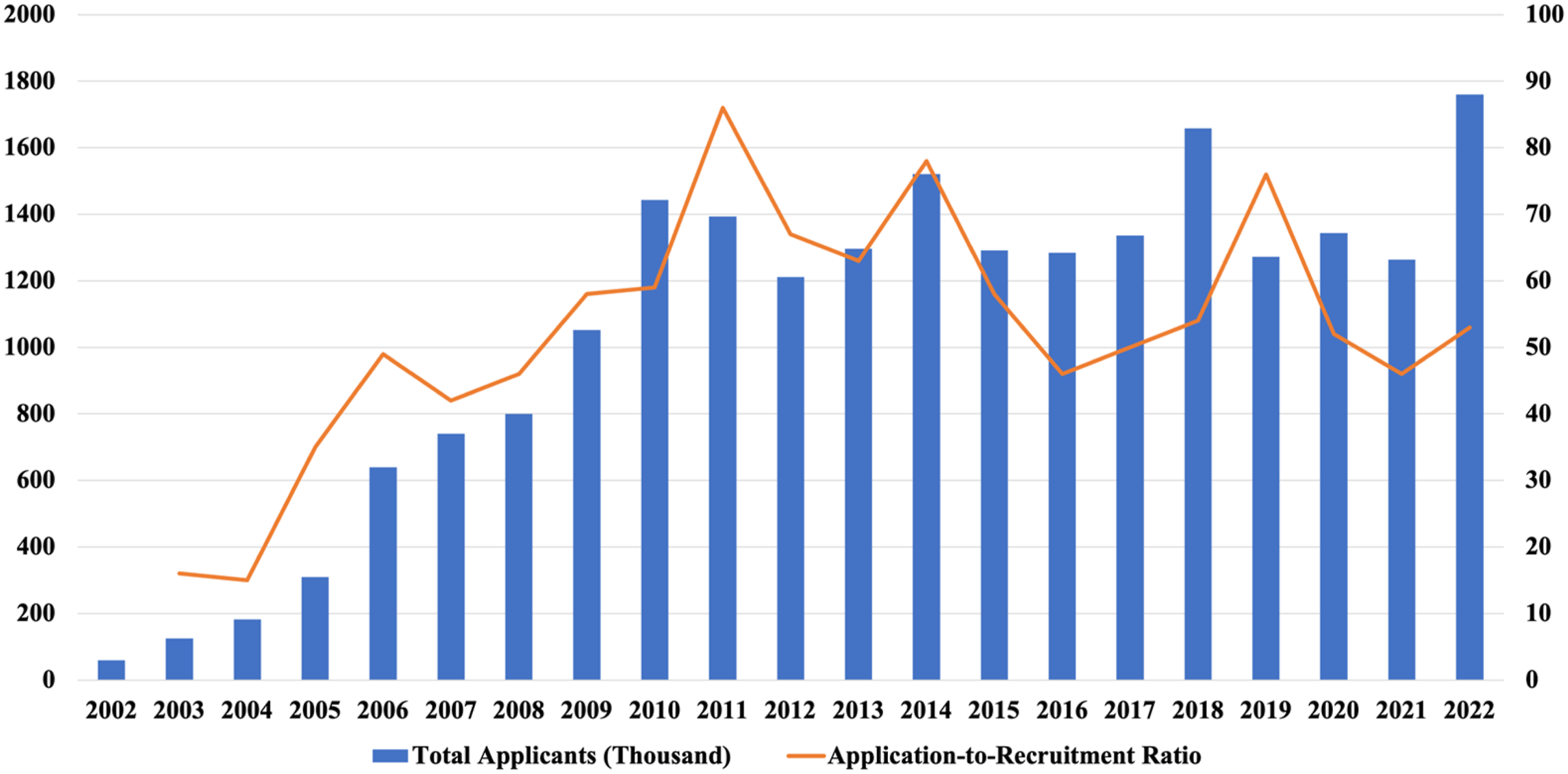

China’s NCSE has been a merit-based system for recruiting government officials through standardized exams open to all Chinese citizens since 1994 (Liu, 2023). In 2003, the number of applicants doubled from the 2002 figure to 125,000 and has kept rising ever since. In 2021, over 2.12 million participated in the exam, each with only a one-in-68 chance of securing a government job. The sheer number of applicants and the exam’s intense competition underscore the growing allure of government jobs in recent years. This phenomenon is known in China as the “civil servant fever”, or “gong wu yuan re (公务员热).” Because different positions attract varying numbers of exam takers, the level of competition for each position reflects citizens’ preferences for specific government jobs. We expect the VAT reform to increase the attractiveness of tax administration positions, as the reform signals an expansion of state taxation power.

We use a difference-in-differences (DiD) strategy to causally identify the effect of the VAT reform on the popularity of tax administration jobs and applicants’ ability level. We exploit variations in pre-reform BT to VAT ratios across 289 Chinese prefectures and sort them into a high BT-VAT group and a low BT-VAT group based on the pre-reform mean BT-VAT ratio. Our DiD strategy compares these two groups before and after 2016, the year when the VAT reform was fully rolled out. The rationale is that the VAT reform would have increased the power of tax agencies in prefectures with high BT-VAT ratios more than that of those with lower ratios.

We collect a novel dataset that combines all NCSE job postings from 2011 to 2021, a total of 166,012 job posts. The key outcome measures are the number of applicants and the applicant-to-recruitment (App-to-Recruit) ratio, which reflect the popularity and competitiveness of a position, respectively. We also use the interview cutoff score to measure the ability level of applicants, as a higher cutoff score indicates a better candidate pool. We divide the data into two subsamples: (1) job openings affiliated with the State Administration of Taxation (the SAT sample), and (2) job openings outside the State Administration of Taxation (the Non-SAT sample). We primarily focus on the SAT sample, while the non-SAT sample serves as a placebo test and enables us to examine the spillover effects of power expansion in tax administration.

We find that, among the SAT sample, the VAT reform increased the number of applicants, the App-to-Recruit ratio, and the interview cutoff score by 20.7%, 18.4%, and 1.1% of their respective means in the high BT-VAT group relative to the low BT-VAT group. Since a one-point change in test scores can eliminate a substantial number of candidates, the ability level of the finalists increased significantly. These effects remain robust when using a continuous treatment measure of BT-VAT ratio, controlling for time-varying prefecture-level covariates, and applying different methods to assign high-low BT-VAT groups. Conversely, no significant effects of the VAT reform were observed among the Non-SAT sample, suggesting that the talent attracted to SAT positions is unlikely to come from the pool of applicants for other government jobs. As a central agency, the SAT may draw talent from the pool of applicants for Local Administrations of Taxation (LATs) if the reform shifted talent allocation through power centralization. To address this concern, we first use data on the Zhejiang Provincial Civil Service Exams and show that the VAT reform also increased applications to the LATs. 5 We further analyze self-reported employment data from six waves of the Chinese General Social Survey and show that the VAT reform reduces the likelihood of an individual working in the private sector compared to the public sector, suggesting that the reform drew talent from the private sector into the broader state sector, beyond tax agencies. These results together suggest that state power expansion through the VAT reform likely attracts talent to the SAT from broader society rather than from other state agencies.

State building helps attract talent to the state sector in the short run because citizens can easily perceive the increased power and benefits associated with government jobs following the expansion of state power. However, the long-term impact of state building on talent allocation may be ambiguous and contingent on specific contexts. If a non-democratic regime expands state power at society’s cost, this can enhance the allure of government jobs even in the long run. On the other hand, state building may facilitate economic growth in countries where the state was previously too weak to offer basic public goods, infrastructure, and social order. If, in the long run, state building proves more beneficial to the private sector than to the public sector, it could redirect talent away from the state sector. Our evidence appears to support the former scenario in China, as five years following the VAT reform, there is a sustained influx of talent into state tax agencies.

One key mechanism by which state power expansion attracts talent is the lack of constraints on state power and associated graft opportunities. To explore this mechanism, we first categorize jobs into those with greater power, such as tax inspection jobs, and those with less power, such as office and front desk positions. We find that the VAT reform led to significantly larger increases in the attractiveness of jobs with more power. We further construct a prefectural-level measure of corruption opportunities using the number of investigated officials prior to the 2012 anti-corruption campaign. We find that the VAT reform attracts more and better talent in prefectures with greater corruption opportunities.

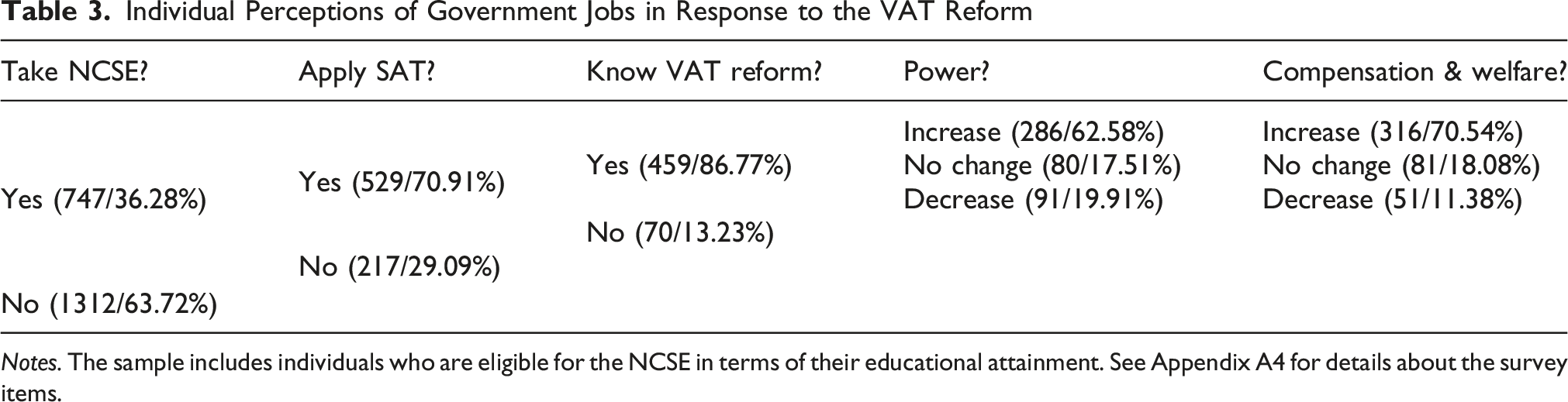

We further conducted an online survey of 3,700 citizens and identified 788 eligible respondents who have either taken or plan to take the NCSE. We find that most individuals aiming for SAT jobs are aware of the VAT reform, and the vast majority perceive an increase in the power and benefits of SAT jobs following the reform. Regression analyses find that respondents with higher social status and greater educational attainment are more likely to associate the reform with increased power for SAT agencies. These findings align with our argument that state power expansion attracts societal elites into the state in pursuit of power and privileges—contrasting with De Tocqueville’s observations in America.

State Power Expansion and Talent Attraction

State building is one of the most widely discussed but contested concepts in political science (Centeno et al., 2017). The literature often uses state capacity interchangeably with power, strength, and institutions, with definitions emphasizing implementation, policy scope, coercive ability, or bureaucratic competence (e.g., Dahl, 1957; Evans & Rauch, 1999; Fukuyama, 2004; Lowi, 1964; Mann, 1984; Migdal, 1988; Weber, 1946). In this paper, we define state building as the centralization of coercive power and resource extraction, which can then be used to maintain political order and/or provide public goods (Centeno et al., 2017).

The literature on state building largely emphasizes the European experience characterized by the development of representative institutions, the rule of law, constraints on executive power, and a professional, merit-based bureaucracy (Besley & Persson, 2009; Fearon & Laitin, 2003; Herbst, 2000; Jackson & Rosberg, 1982; Migdal, 1988; Slater, 2010; Tilly, 1985; Weber, 1946). Scholars attribute the association between state building and democratic institutions to factors such as political fragmentation following the fall of the Roman Empire (Stasavage, 2020), the weak bargaining power of rulers relative to elites (North & Weingast, 1989), the influence of Christianity (Fukuyama, 2014, pp. 229–261), and sovereign borrowing practices (Cox, 2016; Saiegh, 2005). Even theories emphasizing interstate conflict and resource extraction note that European states’ selective extension of protection to different social classes “constrained the rulers themselves, making them vulnerable to courts, to assemblies, to withdrawals of credit, services, and expertise” (Tilly, 1985, p. 186).

Democratic state building does not necessarily make government jobs attractive to society’s most talented individuals. As Tocqueville noted, the equalization of conditions in democratic societies could lead to “tyranny of the majority” and mediocrity in governance (Tocqueville, [1835] 2000). Specifically, citizens’ disdain for elites and elitism could be channeled by electoral systems and potentially affect the attractiveness of government positions for highly talented individuals. Moreover, factors such as the electoral process, transparency, and checks and balances often limit officials’ opportunities to benefit from public offices (Eggers & Hainmueller, 2013). 6 This aligns with the concept of the Weberian bureaucratic state, which emphasizes a professional, neutral, and competent bureaucracy governed by codified rules (Evans & Rauch, 1999; Weber, 1946). In other words, democratic state building can result in diminished incentives for talented individuals to pursue careers in the public sector. This view is consistent with recent empirical evidence on a relatively lower degree of meritocracy among U.S. federal employees compared with Chinese civil servants (Boittin et al., 2016) and public skepticism of science in democracies (Jiang & Wan, 2023).

While much of the existing literature focuses on democratic state building, strong states also emerge within non-democratic regimes without leading to democratic development (Huang, 2023; Y. Wang, 2022a, 2022b). Examples of powerful states can be found in the Soviet Union/Russia, China, Saudi Arabia, the United Arab Emirates, Singapore, and others. In these contexts, state building is aimed at increasing the power and resources of incumbent governments to ensure their survival (Way, 2005). As Way argues, state power in non-democracies often expands through three dimensions: control, scope, and size. Control refers to the degree to which top officials can depend on subordinates to suppress opposition and manipulate elections. This is influenced by fiscal health and patronage, both of which typically require the centralization of fiscal and administrative power. Scope pertains to the range of issues leaders exert control over. Greater state control over the economy can stifle opposition, while a strong private sector often supports independent media and opposition movements. To expand their scope, non-democratic regimes often implement policies that limit private sector autonomy and increase state intervention in economic and social spheres. Size impacts fiscal stability and the regime’s exposure to Western democratization pressures, especially in the post–Cold War period. This often involves nationalizing economic sectors to expand state reach and secure internal resource control. In short, the core logic of state building in such regimes is to expand state power for political survival.

These key features of state power expansion in non-democracies, particularly its expansion in scope, sharply contrast with democratic state building, which is characterized by limited government rather than pervasive control. As Fukuyama (2004) observes, the United States operates under a system of limited government that carefully restricts the scope of state activity. Within that restricted scope, however, the state wields substantial power—not merely on paper but in its capacity to enact and enforce laws and policies effectively. This effectiveness is achieved largely through citizens’ voluntary compliance with laws due to the regime’s legal-rational legitimacy and adherence to the rule of law (Weber, 1946).

By contrast, non-democratic states seek to expand both the scope and size of the state to control society and the private sector, prioritizing regime stability and survival. Moreover, without the rule of law, citizens often lack voluntary compliance, prompting rulers to further expand the scope of state activities to compensate for the lack of effectiveness and to rely on coercive measures for enforcement. These differences imply that state power expansion in non-democratic regimes is not accompanied by limited government or executive constraints; instead, it often involves the concentration of resources to the state sector while systematically weakening the private sector and societal forces to consolidate state control. In this sense, state power expansion in such settings entails not only absolute state power expansion but also changes in relative state power—how strong the state is compared to the private sector. In a weak society with an underdeveloped private sector, a relatively stronger state, even if weak in absolute terms, can still maintain regime stability. But when the private sector grows rapidly, as in China during the reform era, the regime faces strong incentives to expand state power—both in scope and size—to contain the rising influence of the market. Consequently, state power expansion in non-democratic regimes often involves not just building capacity but also deliberately constraining private-sector development to maintain the state’s relative dominance. This is a crucial reason why state power expansion draws talent to the state sector from society in non-democratic regimes.

State power expansion makes government jobs particularly attractive, in part because power in these regimes is often unconstrained. Rulers use the state sector to co-opt both the masses and elites (de Mesquita et al., 2005; Magaloni, 2006; Svolik, 2012), deter opposition and rebellion by keeping potential rivals close (Gandhi & Przeworski, 2007), and establish patron-client networks to secure loyalty and maintain power (Blaydes et al., 2010). A state with significant power and resources can create entry barriers and grant officials substantial authority, privileges, and opportunities for personal enrichment, often through corrupt and opaque practices (Haber, 2006). The lack of power constraints in these systems often leads to economies marked by corruption, informal practices, and high barriers to entry for those without political connections (Chen et al., 2021; Fisman, 2001; Manion, 2004; Shih, 2008; Wang, 2022). Scholars have long linked corruption to non-democratic rule (e.g., Ang, 2020; Gerring & Thacker, 2004; Treisman, 2007). But precisely for this reason, government jobs can be more lucrative than those in mature democracies, which can further draw in talented individuals to the state sector.

For citizens in non-democratic regimes, an expansion of state power relative to the private sector provides government jobs with many advantages. First, a stronger state is more effective at extracting taxes and resources for the regime, allowing it to offer better material benefits to state employees. Second, the increased regulatory power affords state employees more privileges in society and potentially more opportunities to engage in graft. Third, the hierarchical structures and relative stability of these governments, characterized by the absence of regular power alternations, provide talented individuals with longer career paths and brighter career prospects. Fourth, when the power and regulatory capacity of the state grow, state employees enjoy higher social status, as the state sector possesses more discretionary power over society and the private economy. Finally, expanding state power also increases job security in the public sector as it signals that the government is too big to fail. While some of these factors might be applicable in democracies during phases of state power expansion, they are certainly more salient in non-democratic systems. Importantly, these advantages constitute immediate benefits of government employment that citizens can easily perceive from observing state power expansion. Thus, state power expansion should increase talent attraction, at least in the short run.

State power expansion increases the number of applicants to government jobs.

State power expansion increases the competitiveness of applications for government jobs.

Of course, if the job recruitment system of the state sector is biased toward loyalty and patron-client connections rather than pure talent or ability, the expansion of state power would not attract higher-ability individuals to the state sector. However, if the expansion of state power is paired with a merit-based recruitment system, we would expect it to increase the ability level of applicants for government jobs. Here, ability refers to performance or cognitive skills, including test-taking capacity, and does not imply moral virtue. In other words, high-ability individuals may be intelligent yet also greedy, corrupt, or power-seeking.

State power expansion combined with a merit-based recruitment system increases the ability level of applicants to government jobs.

An important mechanism through which state building in non-democratic countries makes government jobs more attractive to citizens is the often-unconstrained power and regulatory prowess associated with those jobs. Since some jobs involve greater regulatory authority than others, state power expansion will have varying effects on jobs with different levels of power and regulatory prowess.

State power expansion increases the attractiveness of government jobs offering greater regulatory power compared to those offering less power.

State power expansion can attract talent to the state sector in the short run by offering immediate and visible benefits of government employment, but its long-run effects are context-dependent. In some settings, stronger state capacity may promote private-sector development by securing property rights, improving infrastructure, and reducing crime (Dincecco & Katz, 2016; Fukuyama, 2014), making private-sector jobs more attractive over time. In others, a growing private sector may become politically threatening, prompting non-democratic regimes to reassert control through regulatory tightening and expanded state intervention. China illustrates this dynamic trajectory: state capacity initially enabled private-sector growth, but the regime later expanded state power to maintain its relative dominance. When state power increases relative to the private sector, sustained talent flows toward the state sector are more likely to occur. Thus, we propose the following research question (RQ): RQ: What is the long-run effect of state power expansion on the popularity of government jobs in a particular country?

Two scope conditions are crucial for observing state power expansion and talent attraction in non-democratic regimes. First, the regime must have both the incentives and capabilities to expand the power of the state. Thus, our argument may not apply to rentier states where rulers can attract talent through resource rents without the need to expand state power. Similarly, it may not apply to failed or failing states where rulers lack the ability to increase state power or exert control over society. Second, the regime must implement at least partially merit-based recruitment for political positions. Without this, the expansion of state power is unlikely to attract high-ability individuals to the state sector, particularly in countries where cronyism, nepotism, and connections predominate in official recruitment. Of course, in weak democracies where constraints on opportunistic behavior by public officials are limited, state power expansion may have similar talent-attraction effects.

The theory suggests that unconstrained state power creates opportunities for graft that can attract talent to the state sector, making corruption deeply entrenched in such systems. Because rampant corruption undermines regime legitimacy, central authorities often launch anti-corruption campaigns to contain it, which can temporarily reduce the attractiveness of government jobs (Lai & Li, 2024). However, because these regimes depend on expanding state power for political survival and lack incentives to constrain that power through effective checks and balances, corruption tends to resume once anti-corruption efforts subside, alone with the inflow of talent into the state sector. In this sense, the logic closely resembles what Manion (2004) describes as “corruption by design.”

Institutional Background

This section first explains why the VAT reform is a suitable case for this study. It then offers a brief overview of the expansion of state power in China over the past two decades, focusing particularly on the VAT reform and the phenomenon of “Civil Servant Fever.”

Value-Added Tax

In this paper, we focus on value-added tax (VAT) reforms as a form of state power expansion. A VAT is a broad-based consumption tax levied at each stage of production, with firms able to credit taxes paid on intermediate inputs. Because downstream firms must obtain invoices from upstream suppliers to claim input tax credits, VAT creates supply-chain transparency and mutual monitoring that constrains tax evasion. It is therefore attractive to governments seeking stable and enforceable revenue, particularly where income or sales taxation is difficult (Keen & Lockwood, 2010). VAT reforms therefore reflect a significant expansion of state power over the private sector, a feature that closely matches the concept of state power expansion discussed above.

Although all regimes may adopt VAT, often in response to fiscal pressures, economic crises, or the need to combat tax evasion (Keen & Lockwood, 2010; Mahon, 2004), their subsequent uses of VAT revenue differ markedly across regime types. In Western democracies, VAT revenues constitute a major source of funding for expansive welfare states (Kato, 2003; Wilensky, 2002). Democratic accountability facilitates redistribution through social transfers, while constitutional liberalism constrains public officials from privately benefiting from tax revenues. By contrast, non-democratic regimes typically lack strong mechanisms of accountability for redistribution, and VAT revenues are more often used to strengthen the state apparatus, control society, and reward state employees. The absence of effective constraints on tax and regulatory officials allows expanded fiscal capacity to translate into greater material benefits for these officials, regulatory privileges, and opportunities for rent extraction. Thus, a VAT reform is more likely to increase the attractiveness of taxation jobs in these regimes.

State Power Expansion and the VAT Reform in China

In the early reform era, China deliberately reduced direct state control over the economy in order to promote growth. The state liberalized markets, privatized many state-owned enterprises (SOEs), opened space for private and foreign investment, and decentralized fiscal authority to subnational governments (e.g., Qian, 2017). For example, in 1991, SOEs held a 68% share of industrial output, but this figure fell to 35% in 2003 (Naughton, 2018). This process of marketization and deliberate reduction of state power allowed the rise of the private sector and was one of the main drivers of China’s spectacular economic growth (Naughton, 2018).

Yet this liberalization also created new political risks. A growing private sector and a more active civil society increased the possibility that economic actors outside the state could demand greater autonomy, rights, and accountability (Dickson, 2016; Gold, 1990; O’Brien & Li, 2006; Perry, 2008; Teets, 2009). In response to these consequences of economic liberalization, the Chinese Communist Party (CCP) gradually reasserted control over both the economy and society, especially from the mid-2000s onward, in a pattern consistent with state power expansion described by Way (2005). It re-centralized authority over SOEs, strengthened their dominance in strategic sectors, relied on state-controlled financial institutions to channel resources toward state firms, and, under Xi Jinping, expanded regulatory oversight and Party presence within private firms (Hsueh, 2011; Shih, 2008; Song et al., 2011). 7 In short, market liberalization was first tolerated to generate growth, but once the private sector became economically and politically consequential, the regime moved to bring it back under tighter state control.

As a critical aspect of state power expansion, the Chinese state’s capacity to extract tax revenues has also significantly increased over the past two decades, particularly in the collection of VAT. Like many other countries, China adopted and expanded the VAT during periods of fiscal stress faced by the central government. In 1994, the CCP Central Committee introduced a tax-sharing system (“fen shui zhi”) to strengthen the central government’s fiscal capacity. The most important new tax was the value-added tax (VAT) levied on most manufactured goods at a uniform rate of 17%, while other industries still paid the Business Tax (BT). The VAT was collected by a new central tax agency, the State Administration of Taxation (SAT). The SAT is a ministerial-level department under the direction of the State Council and is responsible for collecting taxes and enforcing state revenue laws. It has branch offices in most counties in China. The VAT revenues were shared between the central and local governments at a 75:25 ratio in the 1990s.

As part of the revision to the 1994 tax arrangement, the central government implemented the “VAT for business tax” reform (“ying gai zeng”, or VAT reform for short) to replace business taxes with the VAT from 2012 to 2016. While this reform reflected fiscal power centralization and weakened local governments’ fiscal autonomy, it also substantially expanded state power over society. The VAT is an important tax in China because it can reduce tax evasion. Like many developing countries, China relies heavily on indirect taxes on goods and services rather than individual taxpayers, as they are easier to collect. But this led to a narrower tax base and a high nominal tax rate. In China, most taxes are levied directly on enterprises, while the nominal tax rates are too high for firms to afford. Consequently, local officials give firms huge amounts of tax breaks to foster economic growth, especially before officials’ performance evaluations (Chen & Zhang, 2021), and tax evasion was rampant in the post-reform era (Zhang, 2021). Since the business tax is levied on firms’ total sales revenue without subtracting firms’ intermediate input costs, tax evasion is easy as long as firms do not issue invoices for their sales (and they have no incentives to do so). In contrast, the VAT relies on invoice-based input tax credits, creating a chain of tax enforcement that makes evasion much more difficult. Thus, the shift from the BT to the VAT can significantly expand the strength and scope of state power in tax extraction.

The VAT reform marked an important milestone in the expansion of taxation capacity in China. Figure A2 shows VAT revenues and total tax revenues relative to the total budgetary fiscal revenues at the national level over time. Following the reform in 2016, the share of VAT in government fiscal revenues has significantly increased. With greater reliance on VAT as a tax source since 2016, the government has seen an increase in the share of total tax revenue within the overall fiscal revenue, reversing the previous downward trend. Both revenue trends suggest an increase in the government’s tax extraction capacity following the reform. The reform directly reflects state power expansion by enhancing central fiscal capacity and expanding the scope of state power. Specifically, it strengthened the centralized State Administration of Taxation (SAT) and its local branches, the agency responsible for collecting VAT.

China’s Civil Servant Fever

Alongside the power expansion of the Chinese state, the number of NCSE applicants increased sharply in the 2000s. In 2003, the number doubled to 125,000 from that of the previous year. In 2005, China enacted the Civil Servant Law, which took effect in 2006 and codified civil service recruitment based on open examinations, rigorous evaluation, and equal competition, marking the institutionalization of merit-based recruitment in the civil service (Huang, 2026; Liu, 2023). Since then, there has been a steady increase in the number of applicants and the applicant-to-recruitment ratio (Figure 1). The number of applicants reached 1.4 million in 2010 and became relatively stable afterward. In 2022, more than 2.12 million participated in the NCSE, while the total number of college graduates in that year was 9.1 million. There are also huge variations in the applicant-to-recruitment ratio. In 2022, the average number of applicants per job opening is 68. Some jobs received zero applicants, whereas the most popular job attracted 20,602 applicants. With a waning job market due to the COVID-19 pandemic, more and more individuals, including many fresh college graduates, prioritize seeking stable civil service jobs by taking the NCSE. Total Number of Applicants and Application-to-Recruitment ratio by Year. Source: Data for 2002–2009 come from the Beijing news at https://bit.ly/4bKJCg3. Data for 2010–2022 are authors’ calculations

The NCSE is administered by the State Administration of Civil Service (SACS). It fills positions for three types of government organizations: central party organs, central state administrations (including their local branches), and public administrations governed by the Civil Servant Law. The NCSE fills positions in central departments as well as their branch offices at all levels of government, including the provincial, prefecture, county, and township levels. Parallel to the NCSE is the Provincial Civil Service Exam (PCSE), which fills positions only at local levels. Our empirical study focuses on the NCSE because it includes positions at both central and local levels, especially considering that the VAT reform directly influences the power of the State Administration of Taxation, a central tax agency with local branches all over China.

Data and Empirical Strategy

This section first introduces the comprehensive database of NCSE job openings we compiled. It then outlines a difference-in-differences design that uses the VAT reform as a policy shock to causally estimate the effect of state power expansion on citizens’ preferences for civil servant jobs.

Data and Measures

Our NCSE database contains demand-and supply-side information on China’s civil service job market from 2011 to 2022. Each October, the central government releases vacancy postings for the next year’s NCSE. Applicants then select one position before taking the written exam, after which the government announces the minimum score required for each position’s interview stage.

The demand-side information in our NCSE data comes directly from the full list of job postings, which detail the central government’s needs and requirements for potential civil servant candidates. The supply side information is reflected by the number of applicants for each NCSE position every year. We also collected information about the interview cutoff score for each position as a proxy for the ability level of the candidate pool. The 2011-2014 NCSE data were collected from the government website. The 2014-2021 NCSE data were scraped from the websites of two major companies that provide training materials to NCSE takers, Huatu Education and Zhonggong Education.

The prefecture-level business tax (BT) and value-added tax (VAT) data for 2007 to 2011 are from the Regional Statistical Yearbooks 2008 to 2012 as in Zhang et al. (2022). We merge the prefecture-level tax data with the NCSE dataset based on the job location at the prefecture level and calculate the BT-to-VAT ratio in 2011. Excluding prefectures with missing in-formation and extreme values for BT-VAT ratios, we end up with 288 prefectures. 8 In addition, we collected a set of prefecture-level economic variables from the China City Statistical Yearbook 2011 to 2021 as our covariates.

From the NCSE database, we mainly focus on three outcome variables. The first outcome variable is the total number of applicants for an NCSE position i in year t, denoted as Applicants

i,t

.

9

To measure the competitiveness of a position, we construct the Applicant-to-Recruitment (App-to-Recruit) ratio of position i in year t as the ratio of the total number of applicants and the total number of recruitment slots, i.e.,

Empirical Strategy

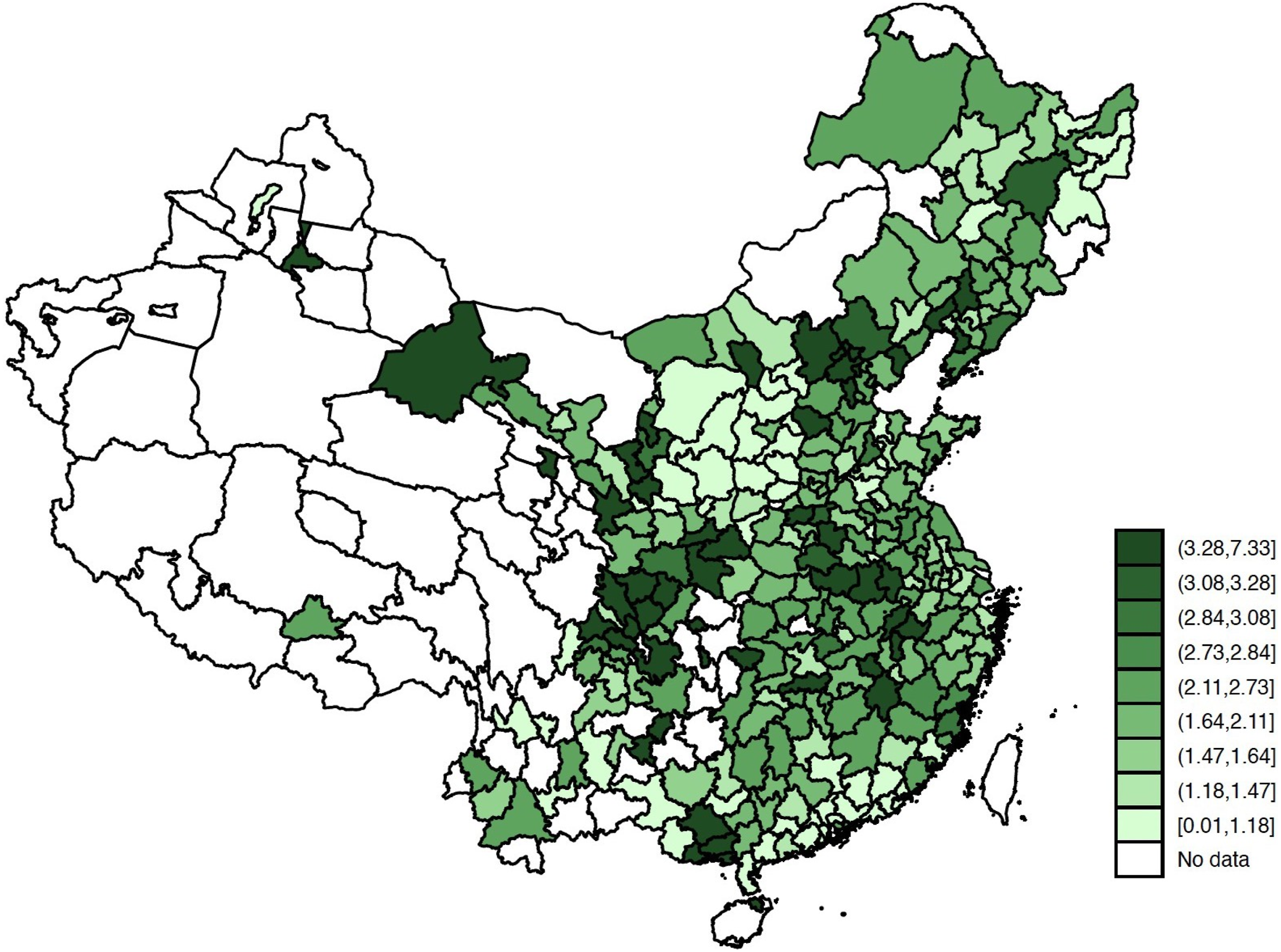

To causally identify the effect of state power expansion on citizens’ preferences for civil servant jobs in China, we take advantage of the VAT reform and exploit subnational variations in prereform tax compositions–the ratios of business taxes to value-added taxes (BT-VAT ratios). Figure 2 presents the geographic distribution of BT-VAT ratios across prefectures in China in 2011, the year before the pilot reform. Intuitively, the VAT reform should have a larger impact on localities where the government levied more business taxes than value-added taxes before the reform. In particular, because the VAT makes tax evasion more difficult, tax agencies in localities with higher BT-VAT ratios have larger increases in regulatory power and can potentially collect more tax after the reform. In addition, since the SAT collected the VAT whereas the Local Administration of Taxation levied the BT before the reform, replacing the BT with the VAT enlarges the tax base for the SAT. This gives the SAT more power and revenue in localities with higher BT-VAT ratios than the SAT in localities with lower BT-VAT ratios. Given these perceived increases in power and revenue in SAT agencies, we expect the VAT reform to have a larger effect on individuals’ preferences for SAT jobs in localities with higher BT-VAT ratios. BT-to-VAT ratio by prefectures, 2011

Based on this logic, we construct a dummy variable that equals 1 if a prefecture has a pre-reform BT-VAT ratio greater than the national average and 0 otherwise. 11 We end up with 113 prefectures with pre-reform BT-VAT ratios above the national average and 175 prefectures with pre-reform BT-VAT ratios below the national average. Note that, following Cao et al. (2022), we did not use the BT-VAT ratio as a continuous treatment measure for two reasons. First, prefectures’ BT-VAT ratios are likely left-skewed because few prefectures have a well-developed tertiary industry–the sector previously subject to the BT levy. Second, individuals’ responses to the VAT reform are unlikely to be linear with respect to the reform’s intensity in different localities: they tend to remain insensitive to small to moderate changes in tax composition until a certain threshold is reached. That said, robustness checks using the continuous measure in Appendix Table A3 yield results consistent with the dichotomous specification.

We divide our sample into two subsamples: the SAT sample, which includes jobs affiliated with the State Administration of Taxation, and the non-SAT sample, which comprises jobs affiliated with all other state agencies. We expect that the VAT reform affects people’s preferences for SAT jobs rather than non-SAT jobs. Table A1 presents the summary statistics of the treatment and outcome variables by the two subsamples.

We designate post-2016 as the treatment period because the VAT reform was not fully implemented until mid-2016. See Table A2 for the timeline of the roll-out of the reform. The pre-2016 pilot reform in transportation and related sectors only affected a small fraction of the economy. As shown in Figure A3, the share of industrial output from the transportation, storage, and postal-service sectors accounted for roughly 4% of the total GDP. Given the very small share of these sectors in the economy, the pilot reform should have a negligible impact on individuals’ job preferences.

12

Therefore, we define our post-treatment year starting from 2017 and estimate the following model:

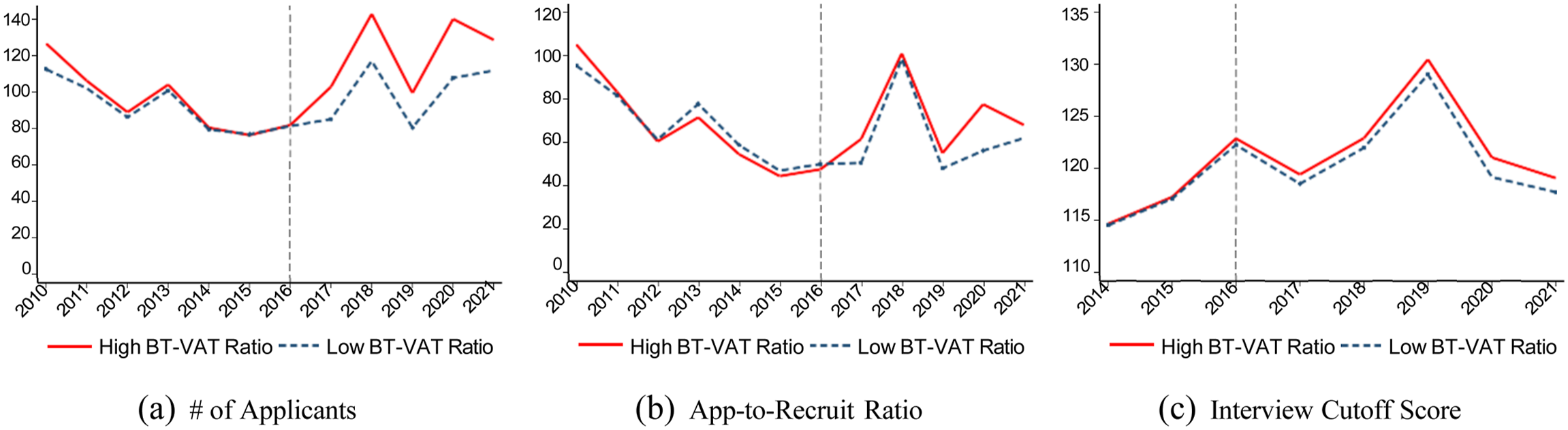

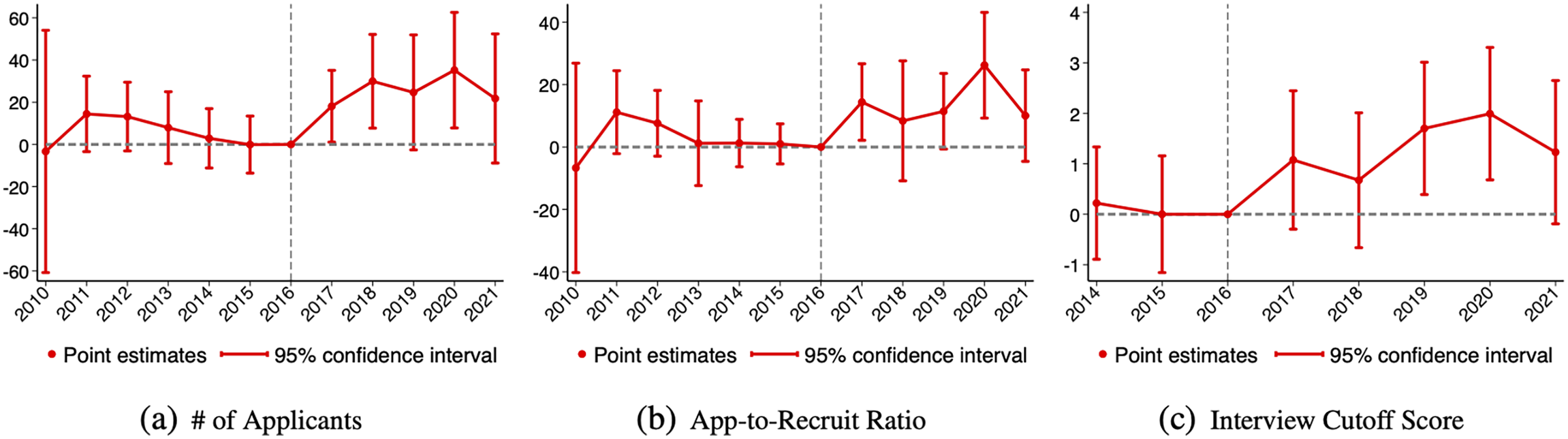

We are interested in β, which captures the change in individuals’ preferences for civil servant jobs located in the high BT-VAT regions versus low BT-VAT regions following the VAT reform. The parallel pre-trends observed between the two groups prior to 2016 (Figure 3) support the validity of the DiD estimation. A placebo test using a dynamic DiD model further shows the lack of pretreatment effects (see Figure 4). Average NCSE outcomes by high and low BT-VAT prefectures. Notes. Annual averages by high versus low BT-VAT groups are plotted using the SAT sample Dynamic effects on NCSE outcomes. Note. Point estimates and 95% confidence intervals are estimated based on the SAT sample

Empirical Findings

This section presents the main results on the effects of the VAT reform on talent attraction, conducts a series of robustness checks, and examines the underlying mechanisms. It also explores the sources from which the central state attracts talent.

Main Results

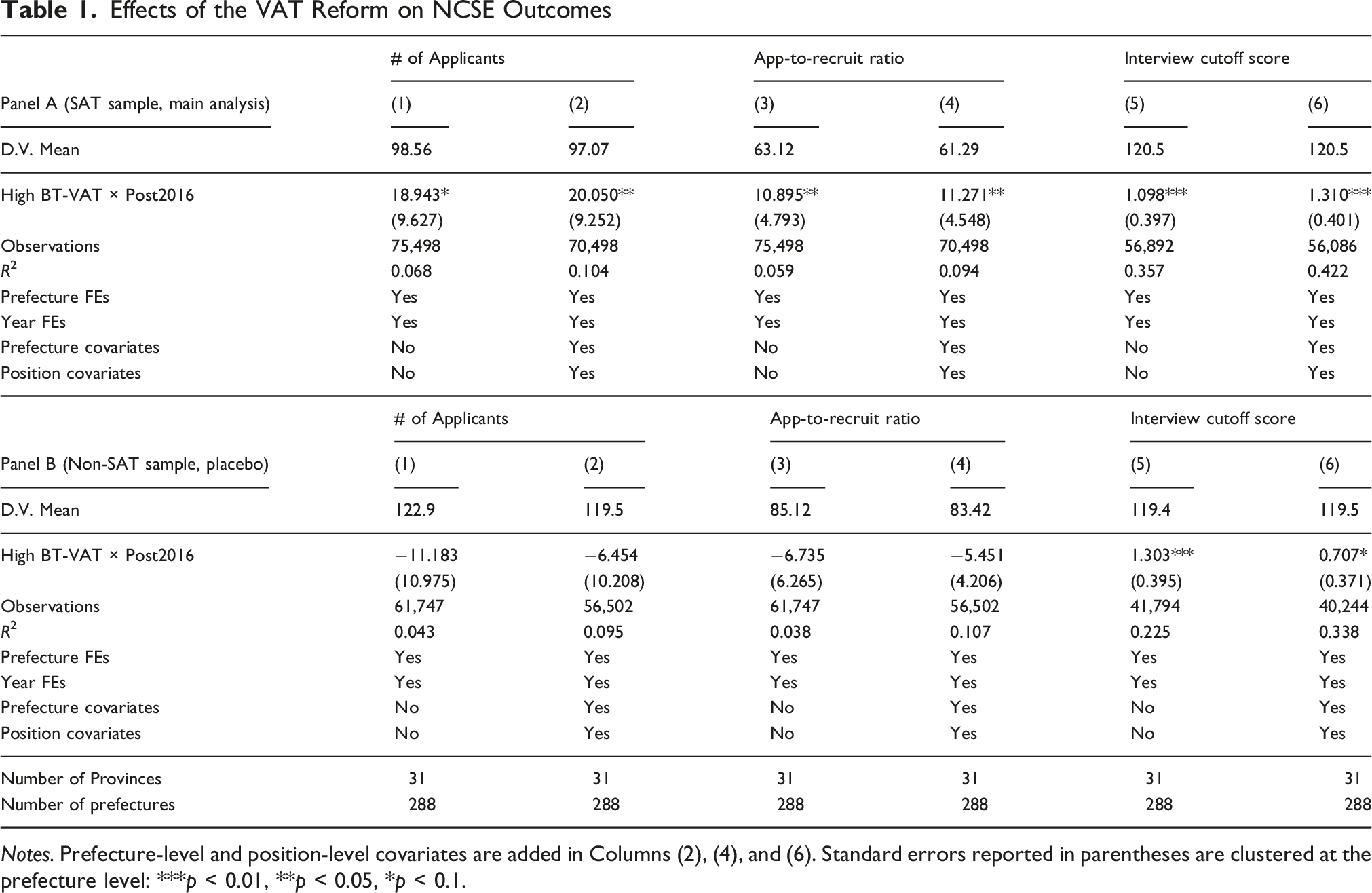

Table 1 Panel A reports the main effects of the VAT reform on talent recruitment for civil servant jobs affiliated with the State Administration of Taxation (the SAT sample). Columns (1), (3), (5) include prefecture and year fixed effects. In Columns (2), (4), and (6), we add prefecturelevel and position-level covariates. Consistent with our expectations, job openings in prefectures with high pre-reform BT-VAT ratios after the VAT reform see increases in the number of applicants (H1), the App-to-Recruit ratio (H2), and the minimum scores required for interviews (H3) compared with job openings in prefectures with low pre-reform BT-VAT ratios. The magnitudes are large. We observe an increase of 20 additional applicants (Column [2]) and an 11-percentage-point rise in the Applicant-to-Recruit ratio (Column [4]) for each job opening in high BT-VAT ratio prefectures compared to those in low BT-VAT ratio prefectures after the reform. Both represent increases of more than 20% relative to their pre-reform means. Column (6) further indicates that the minimum score for interviews increased by 1.3 points for each job opening in high BT-VAT ratio prefectures compared with those in low BT-VAT ratio prefectures (the mean is 120 points). This is a significant increase because, in a standard exam, a one-point difference can eliminate a large number of contestants. The findings suggest that the VAT reform increased the number of applicants, made jobs more competitive, and improved the ability level of the recruited talent for jobs affiliated with the State Administration of Taxation and its local branches.

Effects of the VAT Reform on NCSE Outcomes

Notes. Prefecture-level and position-level covariates are added in Columns (2), (4), and (6). Standard errors reported in parentheses are clustered at the prefecture level: ***p < 0.01, **p < 0.05, *p < 0.1.

Long-Term Effects

We use a dynamic DiD model to allow for treatment effects to change over time. Figure 4 shows that the treatment effects on the number of applicants, the App-to-Recruit ratio, and the minimum scores required for interview eligibility in the SAT sample remain substantial and statistically significant even five years after the VAT reform. This suggests that the reform increased the popularity of SAT jobs in the long term.

Robustness Checks and Alternative Explanations

In the main analysis, we divide the sample into two groups by the mean value of the pre-reform BT-VAT ratio at the prefecture level. This approach is used because individuals’ perceptions of the VAT reform are unlikely to be linear; they may remain insensitive to small or moderate changes in tax composition. Nevertheless, we replicate the analysis using the continuous measure of the pre-reform BT-VAT ratio (Appendix Table A3). The results are consistent with those from Table 1. We also use the 2007–2011 (pre-reform period) average BT-VAT ratio instead of the 2011 value to divide the sample, and the results remain robust (Appendix Table A4).

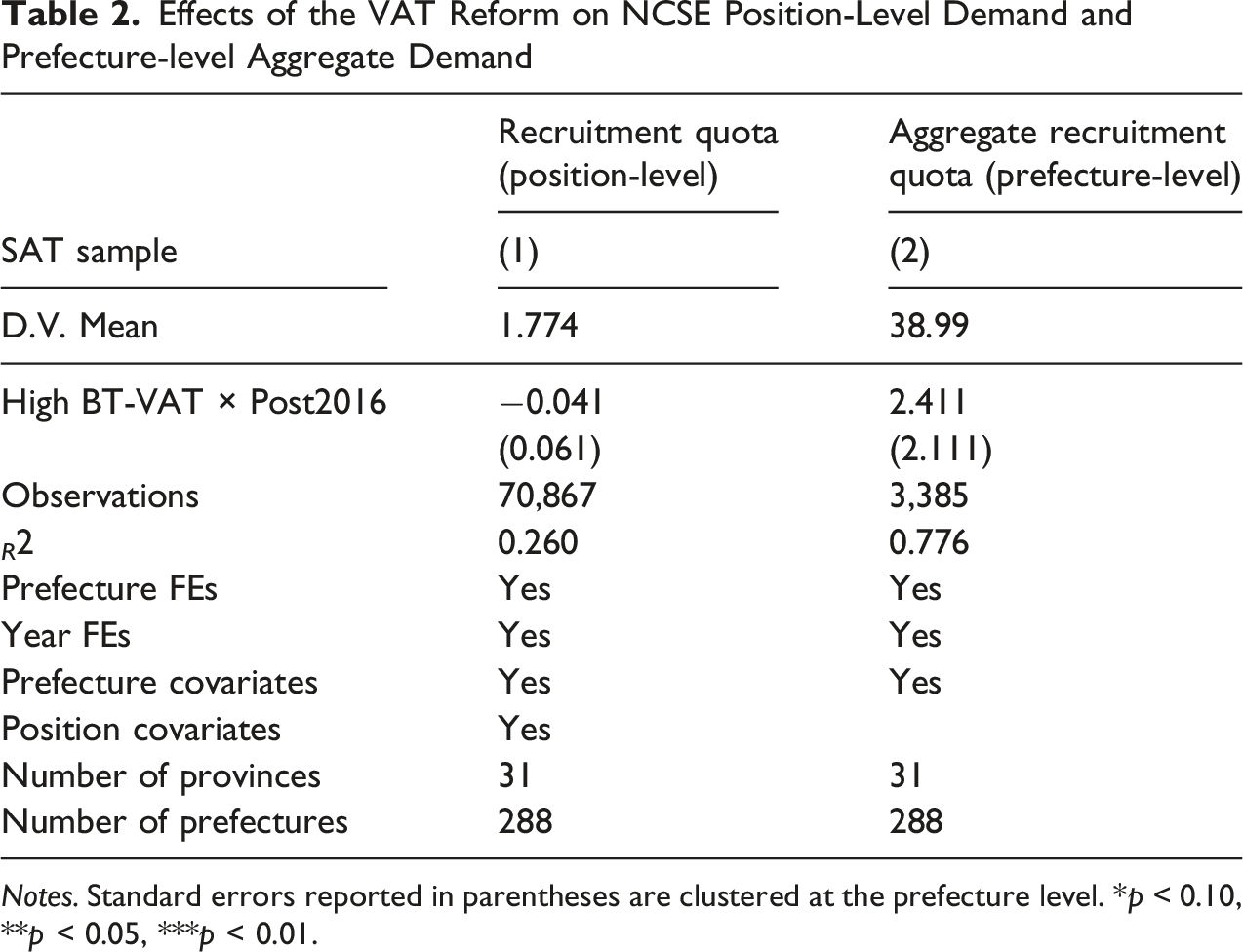

One may also be concerned that our results could be driven by an increase in government job openings in prefectures with high BT-VAT ratios after the reform rather than reflecting changes in applicants’ preferences. For example, many local-tax bureau cadres would probably be transferred to the SAT following the reform. Thus, fewer positions would be available for new recruitment, resulting in more intense competition.

Effects of the VAT Reform on NCSE Position-Level Demand and Prefecture-level Aggregate Demand

Notes. Standard errors reported in parentheses are clustered at the prefecture level. *p < 0.10, **p < 0.05, ***p < 0.01.

We further conduct a series of robustness checks to rule out alternative explanations for our findings. First, our results are robust even after controlling for province-specific heterogeneous trends and time-varying effects of pre-pilot economic conditions in 2011 (Table A6). Second, we show that the results are unlikely to be driven by the 2019 integration of Local Tax Administrations into the SAT, as the integration was proposed only in late 2018, took effect in 2019, and would be expected to reduce—rather than increase—the attractiveness of SAT positions due to the crowded agency after the integration. Against this explanation, our dynamic estimates reveal significant increases in applications and competition as early as 2017 (Figure 4), and the results remain robust when restricting the sample to pre-2019 years (Table A7), thereby also alleviating concerns about confounding shocks from both the integration and the COVID-19 pandemic. Third, we demonstrate that exam takers’ anticipatory behavior around the reform does not bias our estimates by excluding the 2016–2017 transition period (Table A8). Finally, we implement a triple-difference design that exploits agency-by-prefecture-by-year variations to show that the post-2016 increase in applications and competition is specific to SAT agencies in high BT-VAT prefectures (Table A9), confirming that the VAT reform—rather than broader labor-market or institutional trends—drove the surge in talent attraction.

Mechanisms: Power, Benefits, and Graft Opportunities

Individual Perceptions of Government Jobs in Response to the VAT Reform

Notes. The sample includes individuals who are eligible for the NCSE in terms of their educational attainment. See Appendix A4 for details about the survey items.

Moreover, Table A10 presents a regression analysis based on the survey data. Results show that elites–individuals in higher social classes or with higher educational attainment–are more likely to perceive increases in power and benefits associated with SAT agencies after the VAT reform. In particular, elites are significantly more likely to expect an increase in power following the VAT reform. Together, the two pieces of evidence from this survey support our argument that job applicants, especially those in higher social classes or with higher education levels, applying for positions affiliated with the SAT in the NCSE perceive that the reform has made those positions more powerful and lucrative. 13

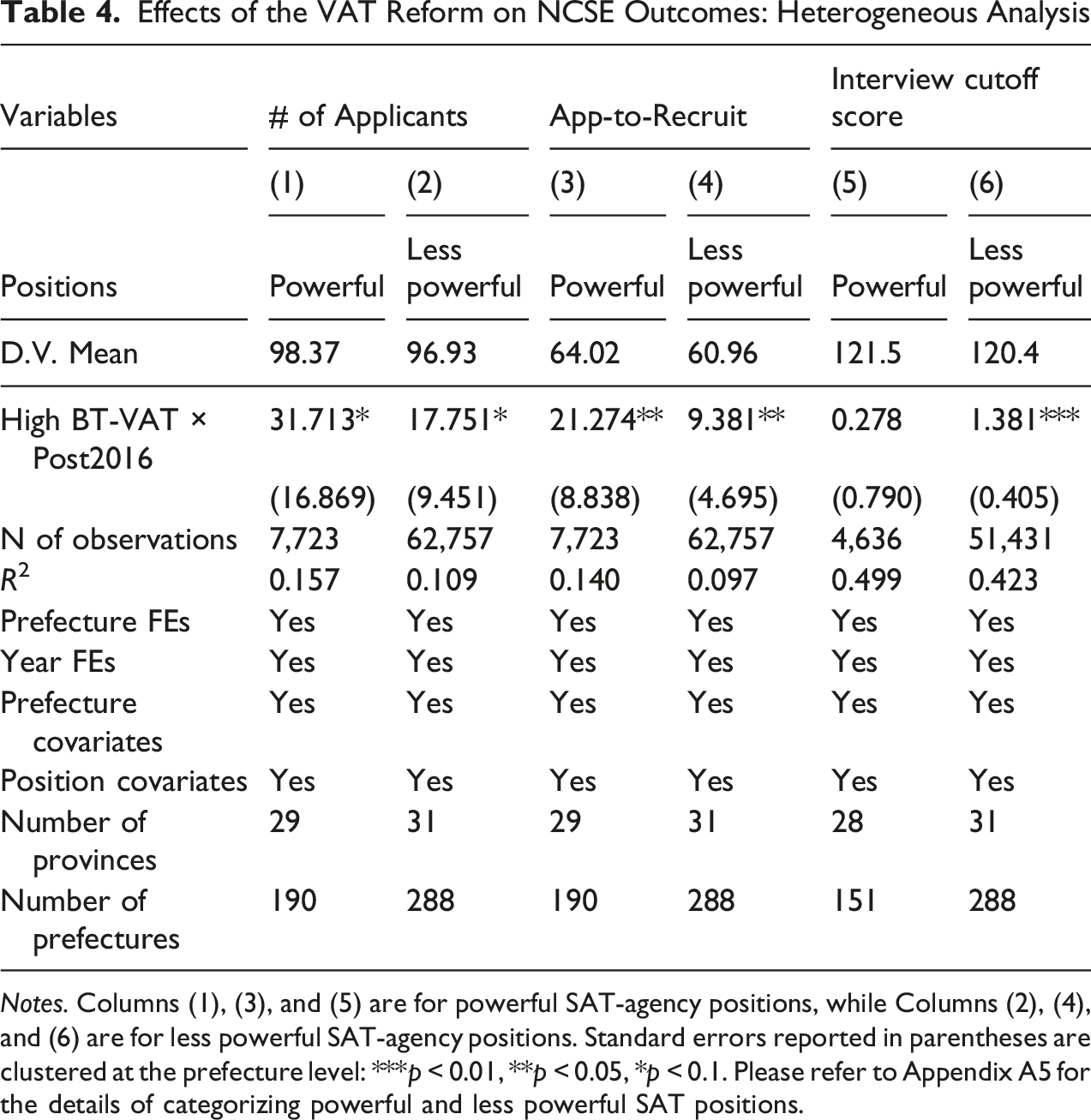

As discussed in the theory section, state power expansion in non-democratic regimes makes government jobs particularly attractive because the lack of power constraints on government officials allows them to benefit from the amplified power and regulatory prowess. This logic implies that powerful positions in the state sector should attract more applicants than positions with less power. To test this hypothesis (H4), we examine the heterogeneous effects of the VAT reform on the popularity of different job openings within the SAT agencies. Certain roles in the SAT agencies entail greater discretionary power over taxation issues of the private sector, endowing SAT employees with more authority, privileges, and graft opportunities. Our interviews with SAT employees indicate that roles in tax-base management, auditing, and enforcement possess greater authority than other jobs, such as front desk and office jobs. If the VAT reform amplified the power and benefits linked to certain SAT roles, job posts involving such roles would be perceived by applicants as particularly empowering and therefore attract more applicants.

We utilize the description and title of job posts in the NCSE dataset to identify powerful positions. Following the suggestions of our interviewees working in tax agencies, we consider a position “powerful” if the textual information contains keywords such as “tax base,” “tax inspection,” “tax audit,” and “tax law enforcement.” In total, we identified around 12% of all SAT positions as “powerful.” Note that “powerful” and “less powerful” positions are in relative terms. Appendix A5 provides detailed information about the categorization.

Effects of the VAT Reform on NCSE Outcomes: Heterogeneous Analysis

Notes. Columns (1), (3), and (5) are for powerful SAT-agency positions, while Columns (2), (4), and (6) are for less powerful SAT-agency positions. Standard errors reported in parentheses are clustered at the prefecture level: ***p < 0.01, **p < 0.05, *p < 0.1. Please refer to Appendix A5 for the details of categorizing powerful and less powerful SAT positions.

We also provide suggestive evidence that candidates may prefer positions with greater graft opportunities by examining how the effect of the VAT reform varies with regional differences in historical corruption levels. Using the anti-corruption campaign database from Y. Wang and Dickson (2022), we construct a prefecture-level measure of corruption based on the number of past cases. We find that, following the reform, SAT positions in regions with higher perceived graft opportunities attracted significantly more and higher-ability applicants (Table A13).

State-Society Talent Allocation

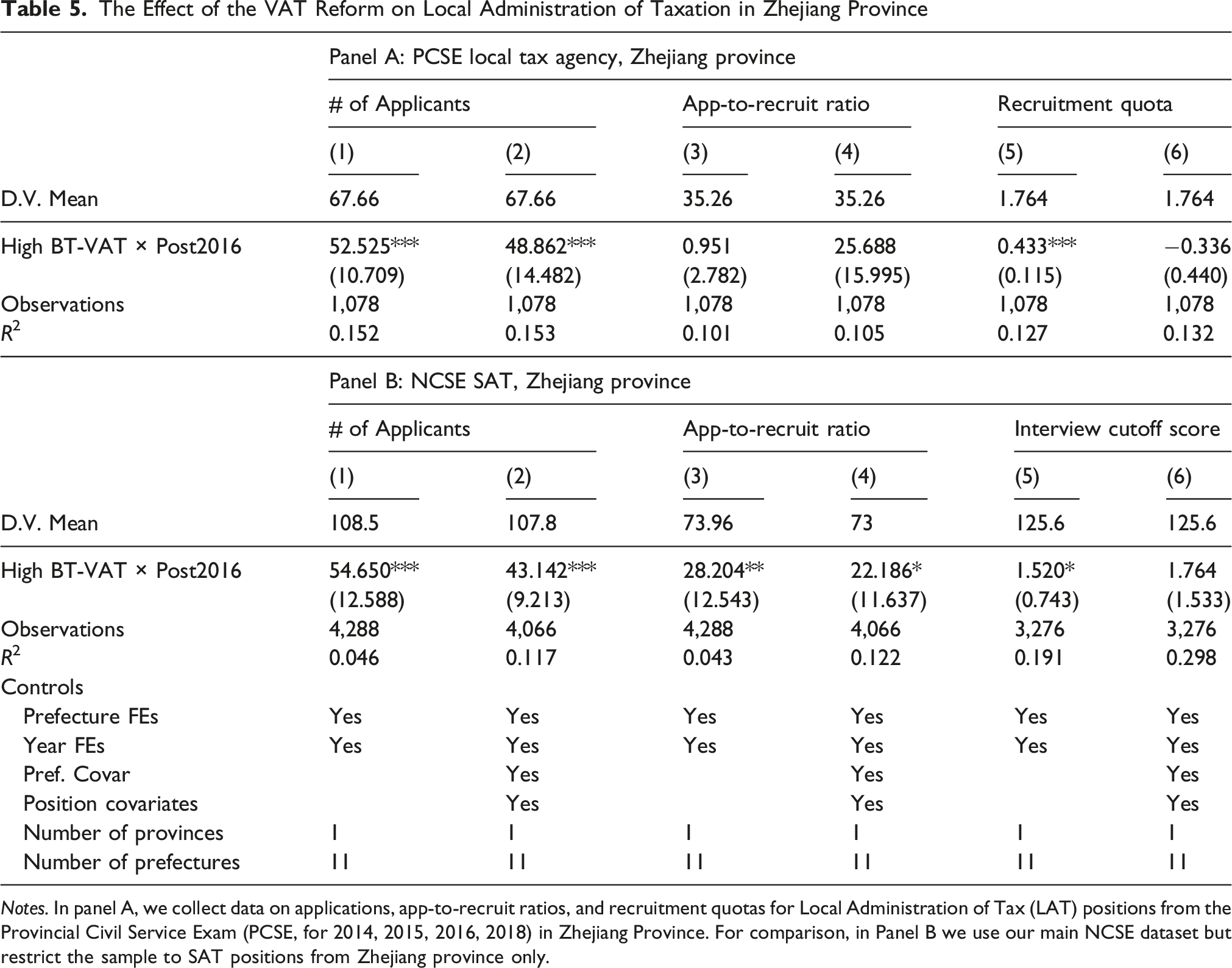

Our main results show that the VAT reform attracted more talent to positions in the State Administration of Taxation (SAT), and that this talent did not come from the pool of applicants for non-SAT jobs within the national civil service system. However, it remains possible that these applicants were not drawn from broader society but instead consisted of individuals who would otherwise have applied for positions in the Local Administrations of Taxation (LATs), especially given that the VAT reform also entailed fiscal power centralization.

The Effect of the VAT Reform on Local Administration of Taxation in Zhejiang Province

Notes. In panel A, we collect data on applications, app-to-recruit ratios, and recruitment quotas for Local Administration of Tax (LAT) positions from the Provincial Civil Service Exam (PCSE, for 2014, 2015, 2016, 2018) in Zhejiang Province. For comparison, in Panel B we use our main NCSE dataset but restrict the sample to SAT positions from Zhejiang province only.

We find that following the VAT reform, both the number of applicants (Columns [1] and [2]) and the application-to-recruitment ratio (Columns [3] and [4]) increased for local and national tax agencies in Zhejiang. 16 Panel A, Columns (5) and (6), further show that the VAT reform did not reduce recruitment quotas for local taxation positions. Although this analysis is limited to Zhejiang Province due to data availability constraints, the positive effects observed for both PCSE and NCSE in the same province suggest that the VAT reform is unlikely to reflect a reallocation of government talent from local tax agencies to the central tax authority.

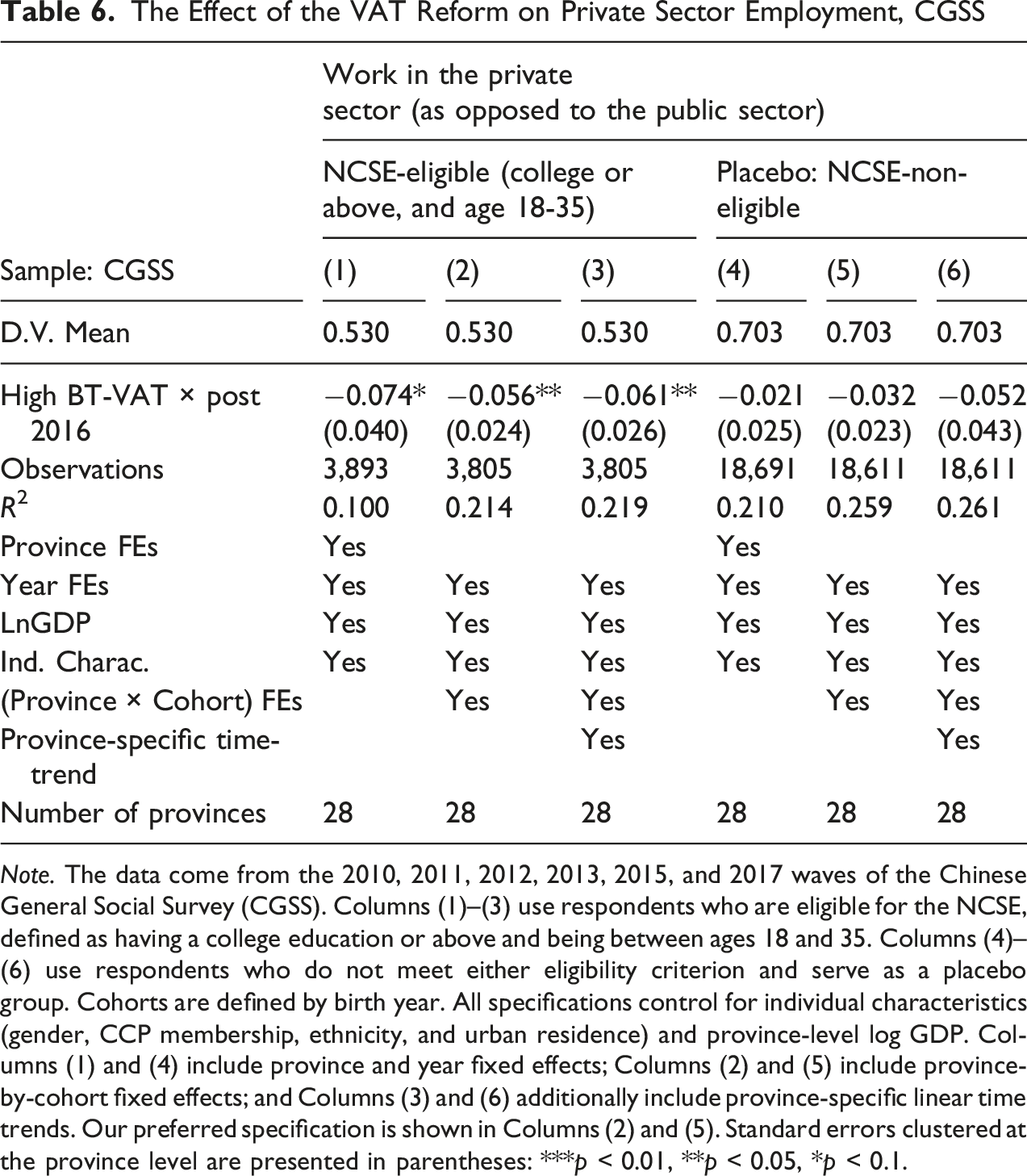

To explore the impact of the VAT reform on the general labor market, we use six waves of the Chinese General Social Survey (CGSS) from 2010 to 2017. 17 The CGSS is a nationally representative survey project run by Chinese academic institutions since 2003. It contains a wide range of employment information, including the ownership type of an individual’s employer. We aggregate our prefecture-level BT-VAT measure to the provincial level and merge it with the CGSS data, as the province is the finest geographic unit in the CGSS. 18 The average BT-VAT ratio at the provincial level is about 2.4, which is comparable to the prefecture-level average. Following our main analysis, we construct a dummy variable, “High BT-VAT”, which equals 1 if a province’s 2011 BT-VAT ratio is above the national mean, and 0 otherwise.

We use a DiD specification to estimate the effect of the VAT reform on the general labor-market outcome. The outcome variable is a dummy variable that equals 1 if an individual works in the private sector and 0 if the individual works in the public sector. 19 Within survey respondents who have active employment status, age, birth-year, and education-attainment information in non-agricultural sectors (23,137 observations in 28 provinces), we focus on individuals eligible for the NCSE, i.e., with college education and aged between 18 and 35, according to the NCSE’s requirements for education and age. Consequently, the subgroup with a high school education or below, or age beyond the above range serves as a placebo group. The VAT reform should have no effect on the placebo group.

The Effect of the VAT Reform on Private Sector Employment, CGSS

Note. The data come from the 2010, 2011, 2012, 2013, 2015, and 2017 waves of the Chinese General Social Survey (CGSS). Columns (1)–(3) use respondents who are eligible for the NCSE, defined as having a college education or above and being between ages 18 and 35. Columns (4)–(6) use respondents who do not meet either eligibility criterion and serve as a placebo group. Cohorts are defined by birth year. All specifications control for individual characteristics (gender, CCP membership, ethnicity, and urban residence) and province-level log GDP. Columns (1) and (4) include province and year fixed effects; Columns (2) and (5) include province-by-cohort fixed effects; and Columns (3) and (6) additionally include province-specific linear time trends. Our preferred specification is shown in Columns (2) and (5). Standard errors clustered at the province level are presented in parentheses: ***p < 0.01, **p < 0.05, *p < 0.1.

Taken together with our earlier findings that the additional talent did not come from applicant pools for either local tax agencies or non-tax central agencies, these results suggest that the expansion of the Chinese state’s tax extraction capacity redirected talent away from the private sector and toward the state sector. This shift could be attributed to both the increased power and benefits within the state sector and a decline in the private sector due to state power expansion, although it is challenging to separate these effects.

Conclusion

This paper distinguishes state power expansion in non-democracies from democratic state building and examines its impact on state-society talent allocation. It highlights a crucial mechanism by which state building attracts talent to government positions: state employees can benefit from the amplified regulatory power due to the lack of constraints on government officials in such settings. Our finding that state power expansion through the VAT reform attracted more and higher-ability talent to take the NCSE in China is particularly notable against the backdrop of an ongoing corruption crackdown that deters applications for government positions (Lai & Li, 2024). Theoretically, this attraction to power and graft opportunities is more pronounced in non-democratic regimes than in democracies, which potentially explains the high appeal of civil servant jobs in China compared to the U.S. This may also help explain Boittin et al. (2016)’s empirical finding that Chinese civil servants exhibit a higher degree of meritocracy than U.S. federal employees. Future research could explore whether state power expansion has similar effects on talent allocation in more democratic contexts.

Our theory and findings have important implications for corruption and economic performance. We argue that talent is attracted to powerful state positions because unconstrained state power creates material benefits and graft opportunities. When combined with merit-based recruitment, this dynamic implies that smart but potentially dishonest individuals are more likely to self-select into public-sector jobs. This logic helps explain the findings of a recent working paper by Liu et al. (2026), which shows that dishonest individuals, measured by graduate dissertation plagiarism, are more likely to enter and advance within China’s public sector. When such individuals fill and rise within government positions, it is unsurprising that corruption becomes deeply entrenched in the bureaucracy. Unconstrained regulatory authority along with dishonest officials could lead a country’s economy to operate through informal practices, cronyism, and political connections (Chen et al., 2021; Wang, 2022). Although economic growth remains possible because petty corruption is constrained by the party-state while “access money” shapes business–government relations to facilitate growth (Ang, 2020), this model falls short of a first-best institutional arrangement.

Although talent attraction is likely an unintended consequence of state power expansion, it has important implications for political stability under unconstrained state power. It highlights a fundamental tension between political stability and economic development. In resource-poor countries such as China, economic liberalization and private-sector growth are important because sustained growth provides performance legitimacy for the regime (Dickson, 2016; Magaloni, 2006). Indeed, the state’s retreat from direct control over the private economy was a major driver of China’s growth during the reform era (Naughton, 2018). Yet a thriving private sector may also generate demands for greater political autonomy and freedom, thereby threatening regime survival. In response, the regime may seek to reassert control by expanding state power and constraining the private sector. This process can also redirect talent from the private sector into the state, further weakening private-sector growth (Bai et al., 2025). As a result, even if expansive state power can help a country achieve rapid growth in the short run, the long-term economic prospects may be more uncertain, forcing the state to rely on other sources of legitimacy over time.

In light of the above discussion, although this paper does not examine the relationship between talent attraction and regime stability, it implies a potential mechanism of regime survival: rulers may enhance state power to attract talent to the regime, instead of leaving them in society as sources of instability (Rosenfeld, 2017). Furthermore, our argument also suggests the possibility of a feedback loop between talent allocation and state capacity. If state building along with merit-based recruitment attracts talent to the state sector, those individuals may in turn further strengthen the state’s capacity and reach. This may help explain why strong states emerged in other non-democratic regimes, such as Vietnam, Singapore, pre-war Japan, and South Korea before 1988. Future research in these directions is worth exploring.

Supplemental Material

Supplemental Material - State Power Expansion and Talent Attraction: Evidence From China’s Civil Servant Fever

Supplemental Material for State Power Expansion and Talent Attraction: Evidence From China’s Civil Servant Fever by Bo Feng, Qiwei He, Xin Jin, Xu Xu in Comparative Political Studies

Footnotes

Acknowledgments

We thank Jiewei Li for providing the 2010–2014 NCSE raw data; Li Zhang, Ming Lu, and Yali Liu for the prefecture-level tax data; Chao Liang for the prefecture-level resident population data; Xun Cao and Mingqin Wu for the prefecture statistical yearbooks; and Xueyue Liu and Haolong Xu for the list of China’s administrative district codes. Jax Peng, Kevin Ma, Kelvin Wang, Yui Wang, and Johnson Zheng provided excellent research assistance. We also thank Loren Brandt, Raymond Fisman, Lei Guang, Justin Jihao Hong, Matías Iaryczower, Ruixue Jia, Guoer Liu, Dan Mattingly, Barry Naughton, Jennifer Pan, Susan Shirk, Guo Xu, Yiqing Xu, Deborah Yashar, Changdong Zhang, Shuang Zhang, Congyi Zhou, and participants at the 2022 American Political Science Association Annual Meeting, the Cambridge Chinese Politics Research Workshop, the Comparative Politics Research Seminar at Princeton University in 2023, the 2023 Labor Work in Progress Seminar at Cornell University, the seventh Seminar at Zhejiang University of Finance and Economics, the sixth International Conference of China and Development Studies in 2023, the Research Seminar at Fudan University in 2025, the Research Seminar at the National University of Singapore Business School in 2025, and the China Research Workshop at the 21st Century China Center at UC San Diego in 2026 for helpful comments. We thank the editor and anonymous reviewers for their constructive comments and suggestions. All remaining errors are our own.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Xu Xu received funding from the University Committee on Research in the Humanities and Social Sciences at Princeton University.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.