Abstract

Criminologists have long been interested in understanding why people commit crime. Perhaps an even more interesting question is what accounts for the offending of individuals who occupy white-collar positions. Most explanations of white-collar offending have relied on extant criminological theories that have been developed to account for street or juvenile offending. One theoretical explanation that was specifically developed to explain white-collar crime is the fear of falling hypothesis or the notion that the motivation for crime is the fear of losing what one has worked so hard to obtain. This study presents the results of an original data-collection effort designed to test this hypothesis. Data collected among business-experienced adults indicate that the fear of falling is inversely related to intentions to price-fix but positively related to internal and legal constraints against price-fixing. Taken together, these results suggest that the fear of falling may serve as a reminder of the attainments that could be lost, should the illegality be committed.

Introduction

When Sutherland (1940) introduced the term “white-collar crime,” he set out not only to challenge the existing perceptions of criminals—that of men from disadvantaged neighborhoods and broken homes—but he also set out to challenge the extant theories of his time that focused primarily on poverty and social disorganization as the root causes of crime (Weisburd, Waring, & Piquero, 2008). Despite Sutherland’s attempt at developing a general theory of crime (i.e., differential association) to be applied to all types of offenders, including the group of offenders he identified as “white-collar” (Sutherland, 1983), empirical investigations of white-collar offending have been few and far in between.

The general lack of such empirical research can be attributed to a myriad of reasons, including the lack of attention paid toward this type of crime among theorists and researchers generally (Hirschi & Gottfredson, 1987) as well as to the added difficulty associated with collecting the necessary data to conduct empirical investigations (Simpson, 2003). This is not to suggest that there have not been any empirical studies examining white-collar crime. More recently, there has been a significant increase of empirical research on offender decision making in a corporate crime context (Benson & Moore, 1992; Paternoster & Simpson, 1996; Piquero, Exum, & Simpson, 2005; Piquero, Tibbetts, & Blankenship, 2005; Simpson, 2002). Despite these strides, a great many theoretical hypotheses have yet to be empirically examined.

This article presents the results of an original data-collection effort designed to provide an exploration on an as of yet untested hypothesis, Wheeler’s (1992) fear of falling, or the notion that motivation for crime is fear of losing what one has worked so hard to attain. Before this hypothesis is reviewed, a brief summary of key theoretical approaches used to understand white-collar offending, with particular attention paid to the rational-choice framework, is provided.

Extant Research on White-Collar Offending

Several different criminological theories have been empirically applied to explain white-collar offending. Theoretical investigations began with Sutherland’s application of differential association theory to explain white-collar crime and have been extended to various neutralization theories’ applications (Benson, 1985; Cressey, 1953; Piquero, Tibbetts, et al., 2005) as well as incorporated control theory perspectives (Lasley, 1988; Piquero & Piquero, 2006) including Gottfredson and Hirschi’s (1990) general theory of crime (Benson & Moore, 1992; Langton, Piquero, & Hollinger, 2006; Simpson & Piquero, 2002), and more recent research has focused on the rational-choice framework.

With its reliance on classical school assumptions of human nature (i.e., free will, hedonism, and rationality) and its focus on the risks and rewards associated with criminal behavior (Cornish & Clarke, 1986), the rational-choice framework has been a natural fit for some scholars trying to understand the decision-making process of white-collar offenders (Paternoster & Simpson, 1993; Shover & Hochstetler, 2006; though see Ermann & Rabe, 1997; Vaughan, 1996). At its core, rational choice assumes that crime is committed after reasoned actors weigh the costs associated with the potential act against the potential benefits or gains that will be derived from the act. Researchers examining the potential benefits of selected criminal acts have found support for their addition into the expected utility model of offending (Nagin & Paternoster, 1993; Piliavin, Thornton, Gartner, & Matsueda, 1986; Simpson, Paternoster, & Piquero, 1998). Other rational-choice theorists have added additional individual and contextual factors into the model to help explain the decision-making process. For example, gender (Tibbetts & Herz, 1996), morality (Bachman, Paternoster, & Ward, 1992; Grasmick & Bursik, 1990; Paternoster & Simpson, 1996) and enduring individual differences such as low self-control or impulsivity (Nagin & Paternoster, 1993; Piquero & Tibbetts, 1996; Simpson & Piquero, 2002), self-serving bias (Nagin & Pogarsky, 2003), and the desire for control (Piquero, Exum, et al., 2005; Piquero, Schoepfer, & Langton, 2010) have all been examined within the rational-choice framework and applied to a variety of crimes.

The proliferation and expansion of the rational-choice framework has also been carried over into the study of white-collar crime (Paternoster & Simpson, 1993; Shover & Hochstetler, 2006). For example, Paternoster and Simpson (1993) present a subjective utility theory of corporate offending that not only adheres to the elements of the rational-choice framework—their model includes costs and benefits of an act, is crime specific, and decision making is affected by contextual characteristics of the crime—but also adds to it. Like other rational-choice explanations, Paternoster and Simpson focus on the individual actor as the decision maker who assesses the perceived costs and benefits associated with a specific act. Due to the very nature of corporate offending—the notion that the acts further organizational goals or benefit the organization rather than the individual directly—they also specify their model to take into account the costs and benefits of the organization and not just solely those of the individual. In this regard, they presented a rational-choice framework that is sensitive to the uniqueness of corporate offending and allowed for the influence of not only individual preferences but also those preferences or preferred ways of the organization itself.

Paternoster and Simpson’s (1993) rational-choice model delineates that the decision-making process incorporates an array of factors—some of which are common in tests of rational-choice theories (such as the certainty and severity of formal and informal sanctions as well as moral inhibitions), others that are corporate crime specific (such as characteristics of the criminal event), and those that are drawn from other theoretical explanations (such as sense of legitimacy/fairness from the procedural justice literature). In total, their factors include the following: (a) certainty/severity of formal sanctions, (b) certainty/severity of informal sanctions, (c) certainty/severity of loss of respect, (d) cost of rule compliance, (e) benefits of noncompliance, (f) moral inhibitions, (g) sense of legitimacy/fairness, (h) characteristics of the criminal event, and (i) prior offending history.

Collectively, these insights have been important for developing a line of theoretical and empirical research that has led to important insight into understanding the decision-making factors associated with white-collar offending, some of which are similar to those for more traditional street offenses and some of which are unique to white-collar crimes. At the same time, much is left to be explored and a great number of theoretical expositions and hypotheses put forward to help understand white-collar crime have yet to be investigated. One such hypothesis, which forms the basis of the current investigation, is Wheeler’s (1992) fear of falling explanation.

Fear of Falling

Most theoretical accounts of white-collar offending have been adapted from extant criminological theories (as reviewed above) that were designed to explain street crimes or juvenile delinquency. As such, very few explanations have been proffered to account specifically or uniquely for white-collar offending. 1 One such example is Wheeler’s (1992) fear of falling.

Drawing from the qualitative offender accounts (as presented in presentence investigation reports) from the Yale Study data, Wheeler (1992) set out to understand the motivations and decisions associated with white-collar offending. Noting that many explanations toward white-collar crime were often grounded in the assumption of greedy offenders or “the-more-you-have-the-more-you-want-account,” he offered another causal explanation of white-collar offending, that is, the fear of falling (Wheeler, 1992, p. 115). 2

By integrating concepts from microeconomics (specifically from Kahneman & Tversky’s [1979] prospect theory) with offender accounts of their behavior, Wheeler (1992) notes that losses will perceptually matter more than gains to one’s relative standing, location, or position in society. In other words, it is not the motivation of getting more or getting ahead as suggested by greed accounts that incite white-collar offenders to commit crime but it is the trepidation of losses that looms large in the minds of these would-be criminals. He notes that “it was the fear of serious financial loss, and what it would mean to him and his family that led him to do something he knew was wrong” (Wheeler, 1992, p. 116). Wheeler also adds that the fear of falling can be equally applied to the loss of status and prestige as well as to the loss of money.

Current Focus

Evidence to date on the fear of falling is largely anecdotal and tends to be gleaned from offenders’ accounts as reported in presentence investigation reports (Weisburd, Wheeler, Waring, & Bode, 1991). As such, few studies have yet to test the specific fear of falling hypothesis that the motivation for white-collar crime “is not selfish ego gratification, but rather the fear of falling—of losing what they have worked so hard to gain” (Weisburd et al., 1991, p. 189). The current study sets out to test the fear of falling hypothesis within a rational-choice framework. Wheeler’s (1992) hypothesis may act as an important ingredient in the rational-choice, decision-making calculus by forcing individuals to consider an additional set of costs and benefits. As such, the study incorporates the avoidance of a loss (the fear of falling) as an input to be taken into consideration during the decision-making process.

Data and Method

Because the fear of falling hypothesis has received little research attention, an original data-collection effort was necessary to help fill this void. In winter 2005, a vignette survey was distributed to 87 adults participating in several returning higher education business courses in the mid-Atlantic region of the United States. The voluntary nature of the survey was announced prior to survey distribution and no respondent refused participation. The survey instrument contained several questions regarding factors that affect or influence the decision-making process of individuals, including rational choice and deterrence variables, demographic characteristics, and a hypothetical vignette designed specifically to assess the fear of falling.

Surveys utilizing vignettes is a common methodology in the social sciences (Rossi & Anderson, 1982) and has been used in criminology generally (Nagin & Paternoster, 1993; Piquero & Tibbetts, 1996) and in studying corporate crime in particular (Paternoster & Simpson, 1996; Piquero, Exum, et al., 2005; Piquero & Piquero, 2006; Piquero, Tibbetts, et al., 2005; Simpson, 2002; Simpson & Piquero, 2002). The use of hypothetical intentions to offend based on the scenario method raises the question about how well such intentions-measures relate to actual offending in the future. 3 There is a lengthy set of studies documenting a strong link between reported intentions and actual behavior (Fishbein & Ajzen, 1975; Kim & Hunter, 1993). For example, Green (1989) found a strong, positive correlation (r = .85) between intentions to offend at Wave 1 and actual offending at Wave 2 in his longitudinal study. Pogarsky (2004) further demonstrated the validity of intentions-based offending measures when he linked these responses to actual deviance in the same study. Finally, additional research by Tittle, Ward, and Grasmick, (2003) found that many criminological constructs relate to offending using prior and projected criminal activity. In sum, this extant knowledge base provides confidence that the scenario methodology is appropriate for the task at hand—especially given the lack of any prior study assessing the fear of falling hypothesis.

There may be some initial unease with the use of a convenience sample especially in light of representativeness. Although this may not be an ideal sample, it is important to remember that almost no data exists on the fear of falling. As is often the case with preliminary investigations of untested theories, initial investigations are less than perfect but still provide a useful first step. With this in mind, the current sample is sufficient to study the fear of falling because as this motivational factor was derived from the white-collar crime literature it is important that it be tested with individuals who have business experience. The current sample contains respondents who indicated on average 10 years of business experience (ranging from 0-30 years) with almost 70% of the sample indicating managerial experience at either “low management” (21%), “middle management” (38%), or “upper management” (9%) levels.

Each respondent was presented with a hypothetical vignette describing in detail the conditions in which a corporate manager engages in price-fixing and was then asked to indicate the likelihood that he or she would do what the manager in the scenario did. As there are no available existing measures of the fear of falling in the literature, an original approach to assess this key independent variable was developed to fall in line with Wheeler’s (1992) expectation that the fear of falling would serve as a provocation to engage in white-collar crime. The fear of falling condition used in the scenario was based on Wheeler’s speculation that “the loss from a mortgage foreclosure or having to shift the kids from a private to a public school” would apply to white-collar offenders in the private sector (p. 117).

Two versions of the scenario were randomly administered to survey participants. One version of the scenario contained a passage depicting the fear of falling condition (underlined below but not during survey administration), whereas the other version omitted the specific passage. The scenario (with the fear of falling passage) was as follows:

Databurn, a company specializing in recordable cds, is a medium-sized company that in recent years has experienced both declines and gains in revenue as competition in its industry continues to strengthen. J. Jones was promoted to manager after 6 years of service with Databurn and has recently been contacted to meet with competitors to discuss next year’s product pricing. As the school year is almost complete at his kids’ private school, J. Jones needs to immediately schedule the meeting with competitors so as not to interfere with the annual family European vacation. J. Jones is worried that if the company does not engage in price-fixing, the company’s sales will decline and if that happens the annual family vacations will have to stop and the kids’ private-school education will be put into jeopardy. At the meeting, J. Jones decides to participate in product pricing for next year.

Dependent Variable

After reading the scenario, respondents were asked, “What is the chance that you would act as the manager did under these circumstances?” That is, they were asked to estimate the likelihood that they would engage in product pricing (i.e., price-fixing). Response options ranged from 1 (no chance at all) to 5 (50% chance) to 10 (100% chance). As such, the dependent variable (M = 3.18, SD = 2.77) represents respondents’ self-reported intentions to offend.

Independent Variables

Fear of falling

As noted earlier, fear of falling was a varied condition in the scenario with half of the sample randomly receiving the scenario with the fear-oriented condition, whereas the other half did not receive it. The analysis includes a dichotomous variable indicating whether the individual received the fear-oriented scenario (coded 1) or did not (coded 0).

Perceived risk

Following the extant literature that investigates rational-choice explanations of corporate offending, perceived risk was measured at both the individual as well as the firm level (Paternoster & Simpson, 1996; Piquero, Exum, et al., 2005; Simpson, 2002; Simpson & Piquero, 2002). On reading the scenario, respondents were presented with the following three individual-based deterrence questions: (a) “What is the chance you would be arrested for a criminal offense if you did what the manager did under these circumstances?” (b) “What is the chance you personally would be sued if you did what the manager did under these circumstances?” and (c) “What is the chance you personally would be investigated by a regulatory agency if you did what the manager did under these circumstances?” Response options ranged from 1 (no chance at all) to 5 (50% chance) to 10 (100% chance). Items were summed to form the deterrence-self scale. Factor analysis indicated the presence of a single underlying factor and the scale exhibited good internal consistency (α = .93). The respondents also provided answers to three organization-based deterrence questions: (a) “What is the chance the firm would be criminally prosecuted if you did what the manager did under these circumstances?” (b) “What is the chance that the firm would be sued if you did what the manager did under these circumstances?” and (c) “What is the chance that the firm would be investigated by a regulatory agency if you did what the manager did under these circumstances?” Response options ranged from 1 (no chance at all) to 5 (50% chance) to 10 (100% chance). Items were summed to form the deterrence-organization scale. Factor analysis indicated the presence of a single underlying factor and the scale exhibited good internal consistency (α = .91). Because the two scales were highly correlated, they could not be employed individually in the analysis; thus, they were combined into a general risk scale (α = .96). Higher values indicate a higher likelihood of perceived sanction risk (M = 30.247, SD = 14.792, range = 6-60).

Perceived morality

With regard to the perceived seriousness of the act, after reading each scenario, respondents were asked to indicate how morally wrong the act portrayed in the scenario was: “How morally wrong is the act portrayed in the scenario?” Response options ranged from 1 (not wrong at all) to 5 (somewhat wrong) to 10 (very wrong). Higher values connote a higher perception that the act is morally wrong (M = 6.872, SD = 2.738).

Perceived benefit

Two items corresponding to intrinsic and extrinsic rewards are used (Katz, 1988; Nagin & Paternoster, 1993; Simpson & Piquero, 2002): (a) “How exciting or thrilling would it be to engage in the act portrayed in the scenario?” and (2) “How much would it advance your career if you did what the manager did under these conditions?” Response options for each question ranged from 1 (not at all) to 10 (very exciting for the first item and a great deal for the second item). Because the two items were positively correlated (r = .43), they were combined into a perceived benefits scale (M = 7.416, SD = 4.125, range = 2-19). Factor analysis indicated strong support for a single factor and scale reliability was acceptable (α = .60) especially given the small sample size and limited number of items. 4

Control variables

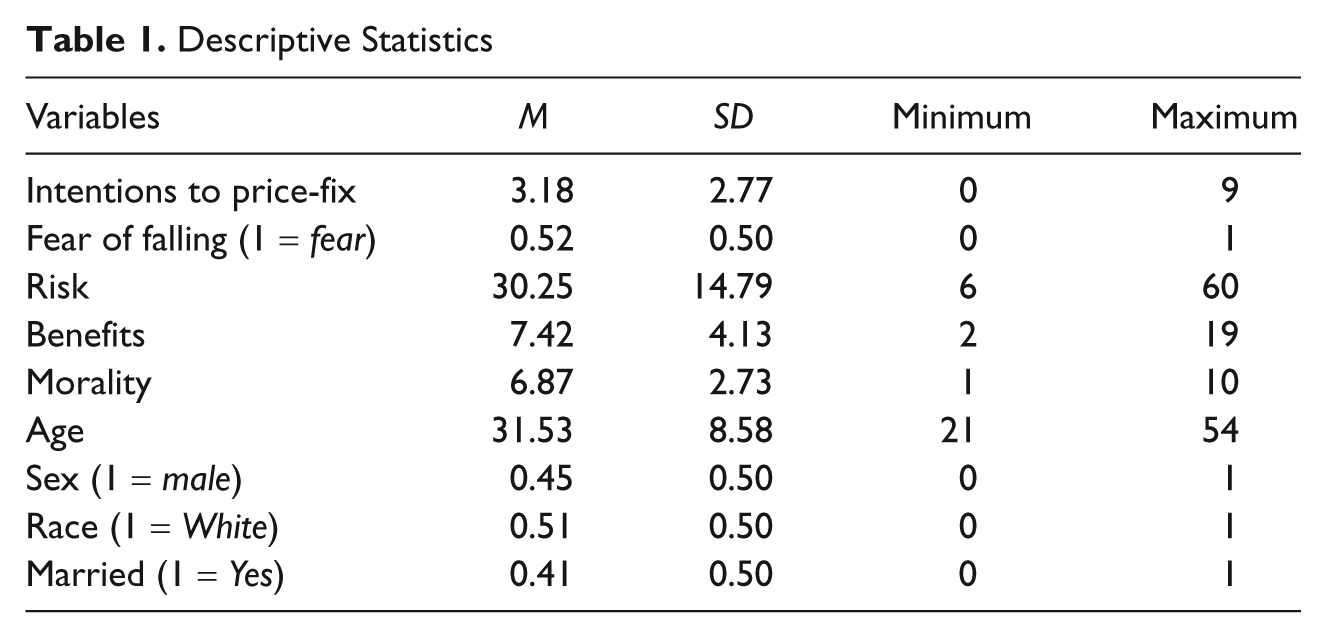

Four variables were used to control for the demographic characteristics of respondents. Age of the respondent ranged from 21 to 54 years, with a mean of 32 years. Sex was coded dichotomously with “0” indicating a female respondent and “1” indicating a male respondent. Almost half of the sample (45%) consisted of male respondents. Race was coded as “0” (non-White) or “1” (White) with 51% of the sample being White. Married was a dichotomous variable indicating whether the respondent was married (1 = yes), with 41% of the sample reporting being married. Table 1 provides descriptive information for all variables.

Descriptive Statistics

Results

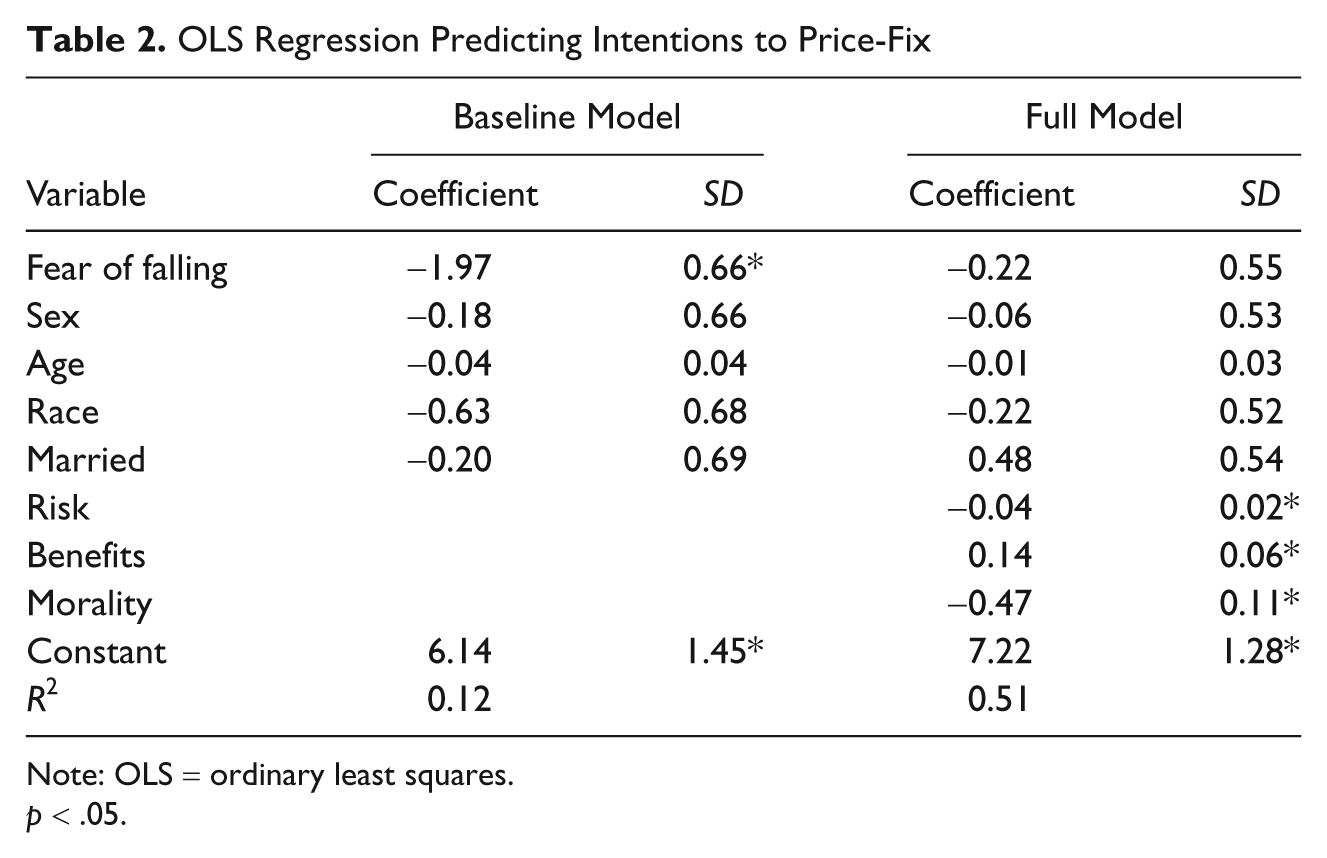

The analysis begins with a baseline model containing the fear of falling indicator and the four control variables (sex, age, race, and married). As can be seen in Table 2, the fear of falling coefficient is significant and exhibits a negative effect indicating that individuals receiving the fear of falling version of the vignette were less—and not more—likely to indicate affirmative intentions to engage in price-fixing. This result runs counter to Wheeler’s (1992) fear of falling hypothesis. None of the demographic variables were significantly associated with intentions to offend.

OLS Regression Predicting Intentions to Price-Fix

Note: OLS = ordinary least squares.

p < .05.

To better understand the motivations of white-collar offending, rational-choice variables (risk, benefit, and morality) were added into a full model predicting the intentions to engage in price-fixing. Results indicate that controlling for these perceptual measures eliminates the previously significant effect for fear of falling, perhaps pointing to an indirect effect of fear of falling. With respect to the three perceptual measures, both risks and morality are significantly and negatively associated with intentions to price-fix, indicating that respondents who associate more risk with price-fixing as well as respondents who hold higher moral beliefs are less likely to do what the manager in the vignette did ( i.e., engage in price-fixing). However, respondents who perceived benefits associated with the act were more likely to report intentions to engage in price-fixing. As before, none of the four control variables were significantly related to intentions to price-fix.

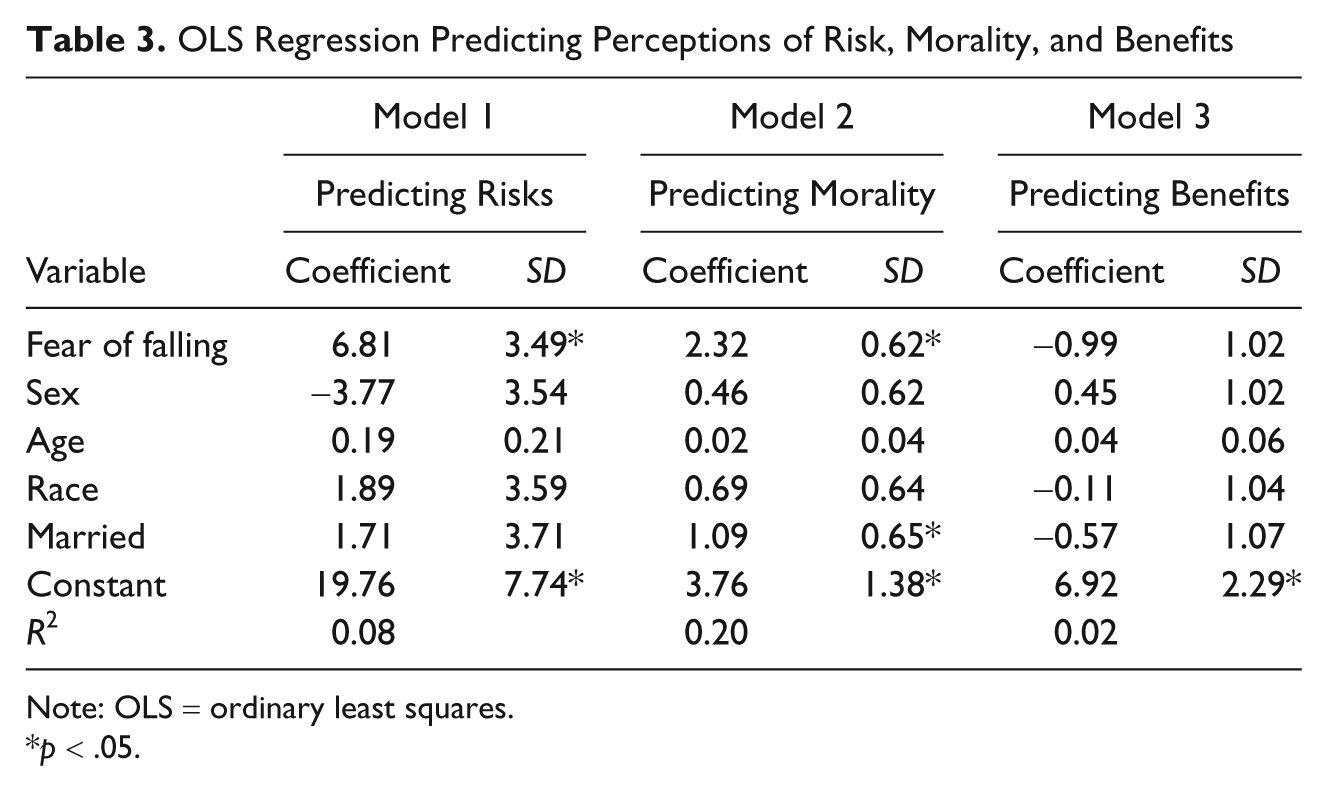

The results from the full model raise the possibility that the fear of falling may be operating through the rational-choice considerations. As such, fear of falling may not serve as a provoker of price-fixing but instead may serve as a reminder to the respondents of what they have to lose should they engage in price-fixing. To examine this possibility, three alternative models (shown as Models 1-3 in Table 3) were estimated where each of the perceptual measures serve as the dependent variable.

OLS Regression Predicting Perceptions of Risk, Morality, and Benefits

Note: OLS = ordinary least squares.

p < .05.

Beginning with the perceived risks of sanctions (Model 1), results reveal that none of the demographic variables emerge as significant predictors but that fear of falling does exhibit a significant and positive effect. This suggests that individuals who received the fear of falling condition in their scenario were significantly more likely to report higher perceived sanction threats than those who did not received the condition. Thus, it appears that fear served to heighten respondents’ awareness of the risks of detection. Model 2 displays the results for predicting morality, and once again fear of falling is significantly and positively related to perceived moral beliefs suggesting that the respondents in the fear condition reported higher moral beliefs associated with price-fixing intentions. It again appears that the fear of falling served to remind respondents about their moral stance against the commission of a crime. One of the demographic variables, married, was marginally significant in this model, with married respondents reporting higher moral beliefs. Finally, the results predicting perceived benefits, shown in Model 3, indicate that neither the demographic variables nor the fear of falling is significant predictors of perceived benefits. This is not an unexpected finding given that the average perceived benefit for those receiving (M = 7.00) and not receiving (M = 7.89) the fear condition were not significantly different (t = 0.99, p > .05).

Discussion

This article sought to investigate an as-of-yet unexamined hypothesis in the white-collar crime literature concerning the fear of falling or the notion that the motivation for white-collar offending stems not from greed but rather from individuals’ perceptions of economic security (Hochstetler, Kerley, & Mason, 2002) or more precisely the potential loss of economic security, status, or prestige. With so little research attention since this hypothesis was first advanced, both an original data collection and the creation of an approach to empirically measure the fear of falling were necessary. Following previous tests of white-collar crime (Simpson, 2002), data were collected from a sample of respondents who reported having prior business experience and who were returning to school for additional education. An original measure of the fear of falling was constructed via of a hypothetical vignette that used price-fixing as crime exemplar and presented half of the respondents with the condition that the manager would no longer be able to take the family on (presumably expensive) European vacations and jeopardize the ability to continue to send the kids to a private school. Two key findings emerged from this initial investigation into the fear of falling hypothesis.

First, the effect of the fear of falling was significant, but it exerted a negative—and not the expected positive—effect on intentions to engage in white-collar crime. Recall that Wheeler (1992) argued that “it should be among those in fear of falling rather than those holding steady or on the rise, where a higher proportion of the white-collar offenders may be found” (p. 117). It seems as though the fear of falling condition presented in half of the scenarios served as a reminder to the respondents who received it of what they had to lose instead of provoking them to engage in the crime to protect their status and associated benefits. When rational-choice perceptual measures (e.g., sanction risks, morality, and potential benefits) were controlled, the previously observed significant direct effect of the fear of falling vanished. This hinted at the possibility that the fear of falling effect was operating indirectly through the perceptual rational-choice-oriented measures.

Second, the examination of the indirect effects of fear of falling revealed that, indeed, fear of falling heightened respondents’ perceptions associated with sanctions and moral beliefs (but not perceived benefits). Specifically, respondents receiving the fear of falling condition reported significantly higher perceived sanction threats and moral beliefs against the commission of price-fixing. Thus, although fear of falling appears to inhibit rather than increase the likelihood of price-fixing, this effect is mediated through situational variables such as perceived sanctions and perceived moral beliefs.

Taken together, these results are important not only because they provide the first attempt to create a measure of the fear of falling but more generally also because they add to the small knowledge base concerning individual-based predictors of white-collar offender decision making. With respect to the theoretical base, although it may be premature to suggest a complete revision of Wheeler’s (1992) hypothesis, the findings do underscore that individuals are sensitive to what they have to lose as well as to the situational factors that may emerge during the course of their decision-making process. Thus, results offer support for theories of white-collar offending, which highlight the importance of individual decision-making styles and relevant situational influences.

Although the findings are intriguing and are an important continued step in the testing of white-collar offending motivations, they are not without limitations. First, this was the first attempt to measure the fear of falling. Although the fear of falling condition closely followed Wheeler’s (1992) depiction of what it would look like for the more common white-collar offender, this is the first time the concept has been operationalized and measured in empirical research. As such, there exists no reference point with which to compare this measure and to derive its effects. This initial attempt to measure and test Wheeler’s fear of falling hypothesis employed only one scenario that was based on a specific set of criteria and potential losses (private schooling and family vacationing). Perhaps other worded scenarios may provide a stronger assessment of the hypothesis and/or generate different results. 5 Future research should not only replicate this measure but also develop other measurement strategies to capture the fear of falling.

Second, the present study only focused on one type of white-collar crime, price-fixing, which is commonly referred to as a corporate crime because of the direct benefits to the organization rather than to the individual. Therefore, it is unknown whether the fear of falling findings would vary for other white-collar crimes or shed light on motivations for street crimes. For example, would the fear of falling effect be more salient for crimes in which the individual gains direct personal rewards such as the white-collar crimes of fraud or embezzlement or more general street crimes? Third, given its focus on providing an initial assessment of the fear of falling hypothesis, the current study did not examine any potential influence of macro-level contextual factors, such as firm culture or structure, on the individual’s decision-making process (Simpson et al., 1998; Vaughan, 1996). Future studies need to not only include such factors but also consider manipulating them, because prior studies testing organizational theories have suggested that these contextual factors may influence decision-making processes. Finally, the sample size in this study was modest and comprised of people who were returning to (business) school. Although the sample focused on individuals with business experience, future assessments of fear of falling should be attempted with larger and more diverse samples that include individuals throughout an entire corporate structure (from entry-level employees to top-level executives) as well as from a range of different types of businesses (from small and local businesses to national and international business ventures). In addition, fear of falling, although derived from accounts of white-collar offenders, could be extended and applied to understanding the motivations of street offenders.

In sum, the current study’s results show that the fear of falling is an important topic that has been underresearch in the white-collar crime area, and although the study is limited in several respects, the present data and analysis are a necessary step to begin addressing this issue. Researchers should continue to collect data on white-collar crime and remain persistent in developing theoretical accounts of white-collar offending whether the offense occurs for the individual’s own benefit or for the benefit of their organization.

Footnotes

The author(s) declared no potential conflicts of interests with respect to the research, authorship, and/or publication of this article.

The author(s) received no financial support for the research, authorship, and/or publication of this article.