Abstract

In this article, we examine the Indian garment industry to examine the effect of clusters on the sales of this industry. The data has been collected through a primary survey in five garments clusters in India. The variable that is significant in explaining sales in most equations is technology proxied by imported machinery. It has been argued that inter-firm linkages and linkages between firms, service providers and institutions are crucial for competitiveness and this is best achieved through a cluster. Studies on clusters have shown that some clusters have been able to deepen their inter-firm division of labour, raise their competitiveness and break into international markets. The development of the cluster in India has followed the ‘top-down’ approach and the natural process through which linkages are developed are yet to occur in most clusters.

Introduction

The apparel industry was central to the industrialisation process of many developed countries (like Japan) and the newly industrialising countries (Dickerson, 1999). The short-term effects of engaging in this sector come from employment, income and foreign exchange while long term effects include export diversification. The apparel industry is organised through buyer driven chains (Gereffi & Memedovic, 2003). In these chains, large retailers, marketers and branded manufacturers play the key roles in setting up decentralised production networks in a variety of exporting countries, which are usually located in developing countries. Exports in this sector are dominated by developing countries. In 2015, the top 10 exporters of clothing included eight developing countries (China, Bangladesh, Vietnam, Hong Kong, India, Turkey, Indonesia and Cambodia). However, India has been losing its share of the world apparel trade; in 2016 it was 3.5%, compared to 6% in 2013.

The literature on global value chains and clusters has led to the discussion on co-evolution, the nature of internationalisation of activities and the role of lead firms (De Marchi et al., 2018). At the heart of the discussion is the issue of competitiveness. Firms are continually under pressure to improve competitiveness in the present world (Humphrey & Schmitz, 2000). The interaction between local and global clusters in developing countries assumes importance as well as the role of industrial policy in achieving this objective.

In this article we study the reasons for India’s declining garment exports through the lens of global value chains. We examine the effect of South Asian competition on Indian garment industries and conclude that it is negligible. In this context, we examine the Indian garments industry to examine the effect of clusters on the sales of this industry. We also argue that the main reason for India’s poor performance in garments exports is the lack of proper clusters. The natural process through which linkages are developed are yet to occur in most clusters studied in this article.

The structure of the article is as follows: in the next section we discuss the literature with respect to clustering and why it assumes importance in the context of certain industries. The third section discusses the Indian garments 1 industry. The fourth section sets out the empirical exercise used in this article. The fifth section presents the results of the empirical exercise. The sixth section concludes with policy implications.

Literature Survey

The importance of local sources of competitiveness has been emphasised in four strands of literature (Humphrey & Schmitz, 2000): (a) Business studies; (b) New economic geography; (c) Innovation studies; and (d) Regional science. The business studies literature emphasised the factors that lead to competitiveness. Competitiveness in exports can be achieved by an increase in productivity. According to Porter (1990), competitiveness can be achieved through a mix of endowments, factors price and policies. While it may be possible to increase competitiveness in the short run through low costs, in the long run increase in productivity is necessary to sustain competitiveness. This literature highlights the importance of local rivalry and supplier networks in achieving competitiveness.

The new economic geography literature emphasised the importance of increasing returns from clustering (Krugman, 1991, 1995). Agglomeration of related economic activity is a central feature of economic geography (Ciccone & Hall, 1996; Krugman 1991; Marshall, 1920; Porter 1990). In his work, Principles of Economics, Marshall (1920) showed why clustering would especially help small enterprises compete. He noted that agglomeration of firms engaged in similar or related activities generated a range of localised external economies that lowered costs for clustered producers. Economists have tended to highlight at least three drivers of agglomeration—input–output linkages, labour market pooling and knowledge spillover. Each of these mechanisms is associated with cost or productivity advantages to firms that result in increasing returns to geography. Another agglomeration driver that has emerged in the literature is the role of local demand, structure of regional business and social networks (Markusen, 1996; Porter, 1990, 1998; Saxenian 1994).

The literature has tended to contrast two potential types of agglomerating forces: localisation (increasing returns to activities within a single industry) and urbanisation (increasing returns to diversity at the overall regional level). Delgado et al. (2010) move beyond the issues of localisation and urbanisation and examine the agglomeration forces arising among closely related and complementary industries. Industries within a cluster benefit by sharing common technologies, knowledge, inputs and cluster specific institutions. They evaluate the impact of clusters on regional economic performance, which includes growth in employment, wages, business creation and innovation.

The nexus between innovation and learning has also sprung from the regional science literature. Pietrobelli (2007) argues that inter-firm linkages and linkages between firms, service providers and institutions are crucial for competitiveness and this is best achieved through a cluster. Upgrading of local firms is often enhanced through horizontal linkages and collective efficiency in local clusters (Pietrobelli & Rabellotti, 2007). 2

The regional science literature contributed immensely to the study of clusters through the study of industrial districts. Clusters are defined as sectoral and spatial concentration of firms. Development of clusters can take either of two routes: spontaneous and policy driven. Policy driven clusters are set up by the actions of the government, and particularly followed the success of well-known industrial clusters such as Silicon Valley (Richardson, 2010). Wallsten (2004) observes that very little is known about the effectiveness of policy interventions on industrial clusters. Richardson (2010) studies the ways in which policy driven clusters affect internationalisation in the context of Malaysia. His findings point out (in the context of the clusters he studied) that exchange of knowledge between firms (which is regarded as key to the success of a cluster) may be limited in a policy driven cluster, at least in the short run.

Clusters are common in a wide range of countries and sectors (Nadvi & Schmitz, 1994). However, the growth experiences of clusters widely vary. Studies on clusters have shown that some clusters have been able to deepen their inter-firm division of labour, raise their competitiveness and break into international markets (Nadvi, 1999; Schmitz, 1995). Clustering is particularly relevant in the early stages by helping small enterprises grow. Although there have been many studies on clusters in the context of developed countries, the studies in the context of developing countries are more recent and have grown out of the role of small-scale industry to industrialisation (Schmitz, 1989). Summarising the literature on clusters in the context of developing countries, Schmitz and Nadvi (1999) point out that industrial clustering is significant in developing countries.

Subsequent work on has focused on deliberate effects of collective action (Brusco, 1990; Tendler & Amorin, 1996, etc.). While the literature on clusters is for promoting collective efficiency, the value chain literature is about gaining access to chains. Humphrey and Schmitz (2000) contend that there is scope local for industrial policy by looking at the two literature together. 3 Cluster analysis does not theorise links of regional cooperation to the world. On the other hand, value chain literature, tends to overlook the decisions outside the chains, at the local level, which matters since it influences integration (Riedel et al., 2009). Our article contributes to the literature by integrating these two strands and hence fills an important gap. This article examines this issue in the context of the Indian garment industry. This is the main objective of this article.

The Indian Garment Industry

The structure of the garment industry in India is rather complex with the bulk of units being small and medium firms (Roy, 2009). The garment industry in India caters to both, the domestic market and exports. The readymade garment segment contributes to 43% of the Indian textile exports, which includes cotton garments and accessories, manmade fibre garments and other textile clothing (Ministry of Textiles, 2016). The contribution of the textiles and garments sector to employment is significant, providing 19% of the industrial workforce in 2013 (Technopak, 2012). The garments industry provides a quarter of the jobs in this sector. 4

The AEPC (2009) study estimated that 95% of the production is in the top 19 clusters, whose annual production is 8,900 million pieces and produced in 33,371 garment units. Nearly 80% of the national production of garments is concentrated in ten clusters: Kolkata, Mumbai, Tirupur, Ludhiana, Indore, Bellary, Jaipur, Bangalore, Chennai and Okhla. 5 The clusters are specialised in terms of type of garments (either woven or knitted) and the variety of the products (men’s, women’s or children’s). The domestic market is a category with products of a lower quality than those exported, and mass-produced items. The segment can be subdivided into items that are branded and sold through organised retail and those that are not branded. The prices of the unbranded segment are significantly lower than those in the branded segment (for a comparable product). The branded segment faces competition from imports while in the latter there is competition from Bangladesh. Of the cost of production of a garment, 55% to 60% is incurred in the raw materials which include fabric, accessories, sewing thread, and so on.

The process of manufacturing a garment comprises of several steps: cutting, stitching, embroidery, fixing of accessories, dyeing, and so on. The maximum value addition to textiles is done by the apparel sector, which is the last stage of the textile value chain (Ray & Miglani, 2018). Ramaswamy and Gereffi (2000) state that apparel products were India’s leading export product and achieved rapid growth in the late 1980s and in the early 1990s. However, the country’s share of world apparel exports has not risen since 1994 due partly to slowdown in the United States and the EU. 6 Moreover, the apparel industry has remained outside the industrial reforms of the 1990s.

Empirical Exercise

Data Collection and Sample

We examine the Indian garments industry to examine the effect of clusters on the sales of this industry. In order to examine the extent of competition to India from products manufactured in the other South Asian countries, we conducted a survey of apparel manufacturers in India. Tirupur, Kolkata, Ludhiana, and Bangalore emerge as the leading centres while the combined sales of the Delhi NCR region make it one of the top business centres for apparel products. While Kolkata specialises in kid’s garments and men’s innerwear and shirts, the Delhi cluster manufactures products mainly for women. Both Bangalore and Tirupur are largely export oriented while the Kolkata cluster caters largely to the domestic market. Ludhiana specialises in winter wear. The face-to-face survey of these clusters of the apparel industry of India was conducted over a span of 30 days in September to October 2010 using a semi-structured questionnaire. The clusters are categorised in terms of two aspects: (a) type of garments (i.e., knitting or woven); and (b) variety of products (men, women, kids wear).

Data Analysis

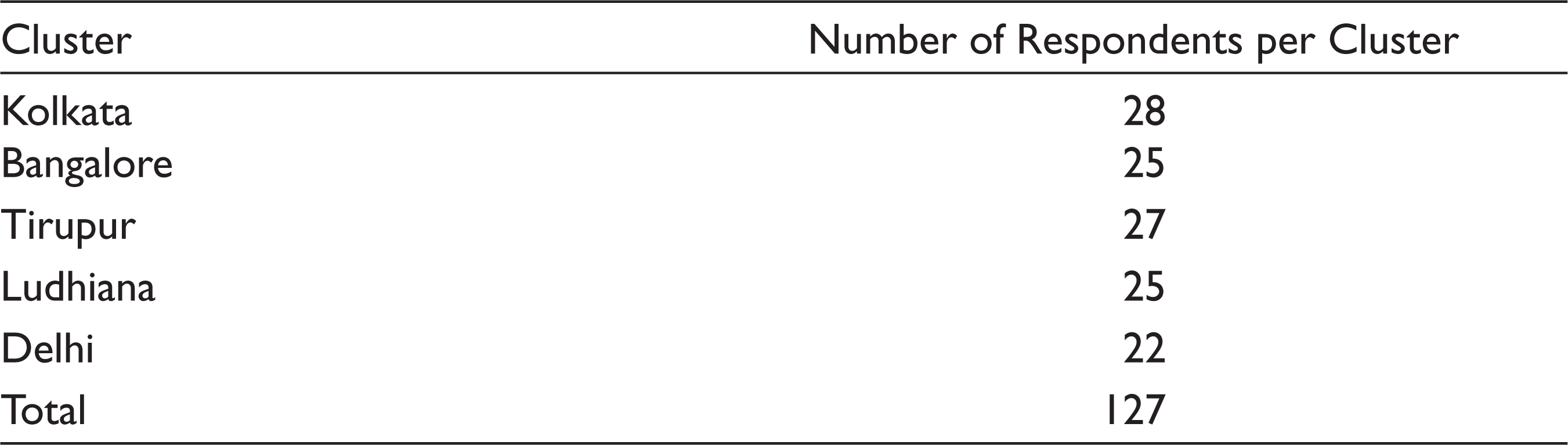

127 firms were interviewed with approximately 25 respondents in each cluster. Table 1 shows the number of firms surveyed per cluster.

Cluster Coverage.

In terms of the product categories surveyed, Table 2 shows the share of firms producing men’s, women’s and kids wear in the surveyed firms. Some firms manufacture all three types of garments.

Category Coverage.

Table 3 shows the kind of firms interviewed in terms of their turnover, whether they were producing for the domestic market or were exporting, how many of them were using imported machinery and whether there was a size correlation with this technology usage, and the age of the firms in terms of the number of years in operation. We have categorised the sample in terms of size which has been captured through sales turnover.

Key Characteristics of the Sample.

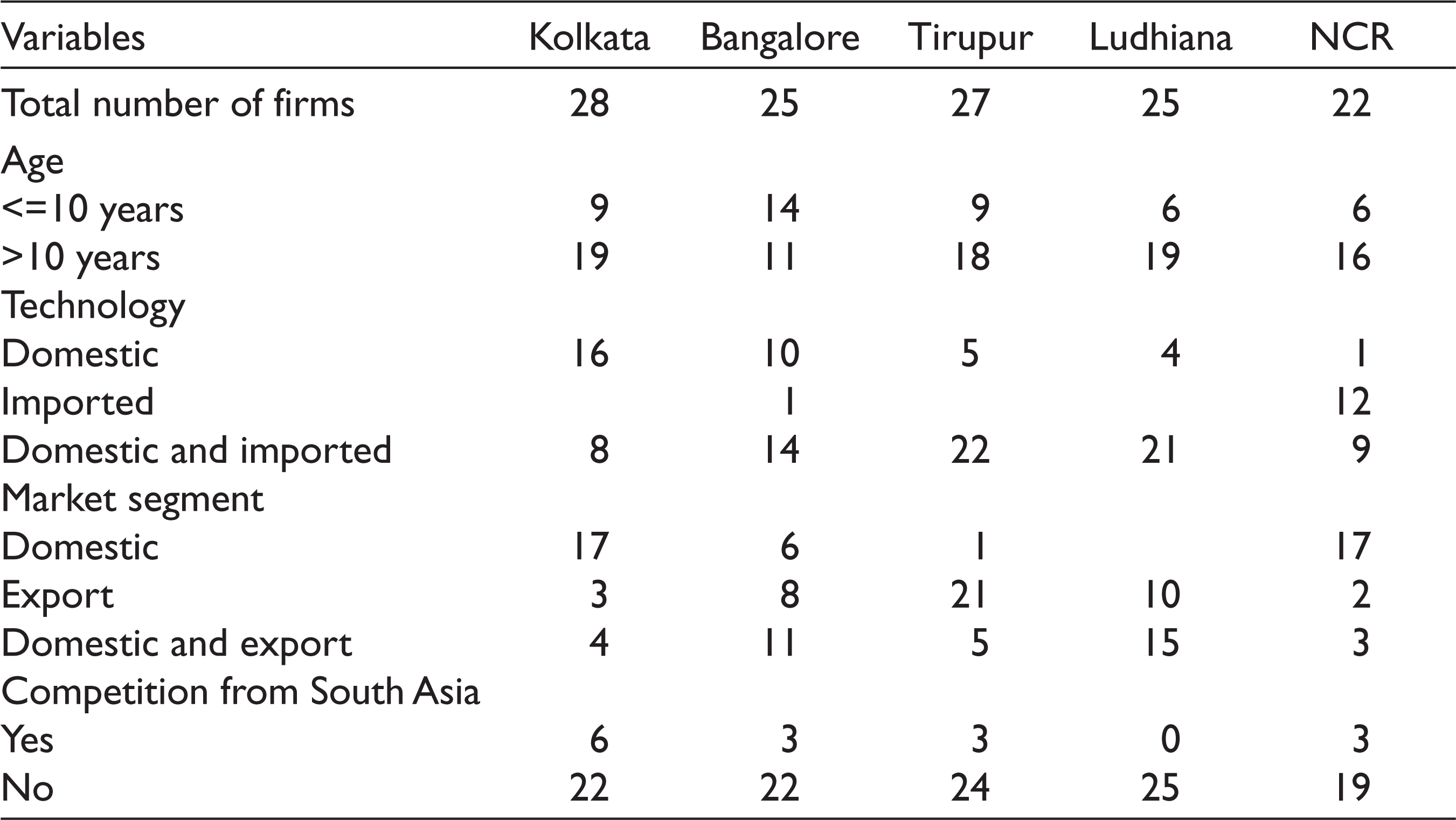

The categorisation of the firms (shown in Table 3) in terms of large and small has been done in the following manner: a firm with sales turnover of more than ₹300 million has been categorised as large, while a firm with sales turnover of less than ₹300 million has been defined as small. This definition should then be interpreted with the caveat that this is strictly not the definition used by the Annual Survey of Industries and we will us the terms ‘larger’ and ‘smaller’ to highlight this aspect. We notice from the table that larger firms are not catering to the domestic market exclusively—all of them are also exporting. A significant proportion of the smaller firms are producing only for the domestic market and a large number of these firms belong to the Kolkata cluster. A very significant number of firms are using imported machinery, though the proportion is higher for the large firms. We examine this issue in greater detail in the regression exercise below. Looking at the age of the firms in terms of the number of years in operation, we see that most of the firms are more than ten years old.

The small-scale sector is defined in India either in terms of the number of employees or in terms of investment in plant and machinery. There are problems categorising size in terms of both of the above criteria. While we have information on the number of employees in our sample, firms use contractual labour as well and such employees are not usually counted as the formal employees of the firm. On the other hand, most firms typically outsource a large part of their production to ‘job workers’ and the only employees they report are administrative personnel who are not production workers. 7 This presents a problem in enumerating the firm size based on the number of employees. The second relates to the use of plant and machinery in defining the size of the firm. Again, due the practice of outsourcing by firms, investment in plant and machinery is low for typically small firms. Some of the respondents have said that only stitching is done in house while the rest of the activities are outsourced. Hence, we have used the sales turnover as a measure of the size of the firm.

Turning to the nature of competition faced by the Indian firms, we find most firms said that they face no competition from the South Asian countries. This is important since India is losing ground in the garments exports and if not to the South Asian countries, who is it losing ground to? As shown in Table 4, we have categorised firms by the market segment, to which they are catering, as domestic, export and both. None of the larger firms are catering to the domestic segment only—they are either exporting or serving both the domestic and export market as already mentioned above. Firms that are exporting only, face very little competition from the South Asian countries. We discuss this in details later.

As far as the domestic market is concerned, the competition is not coming from South Asia but mainly from other countries such as China, Cambodia, Vietnam, and so on. This is evident from Table 4: the number of firms reporting facing any competition from South Asia (comprising of Bangladesh, Sri Lanka and Pakistan) is 23 against 40 from other countries. Moreover, most of the competition faced by the firms in the domestic segment is coming from other firms in the domestic segment. This implies that the domestic market in itself is highly competitive and does not face any significant competition from South Asian products.

Firm Size and Competition.

There is a distinction that has to be made, however, in the nature of the competition faced by the firms from South Asia. This is shown in Table 5. The smaller firms have reported that some of them do face competition from the South Asian countries, especially in some products like swimwear from Sri Lanka. From the Table 5 we see that of the firms catering to the domestic sector and as well as exporting, 64 of them are smaller while 11 of them are larger. A smaller number of firms in the ‘smaller’ category report competition from abroad and mainly from China: 26 out of 64 while for the ‘larger’ group it is 7 out of 11. Competition from South Asia was similar: 7 out of 64 for the smaller group against 4 out of 11 for the larger group.

Competitiveness of Firms Catering to Domestic and Domestic-Export Market.

Effect of Technology.

In the case of increased competition, how should the firms cope with the increased imports? Technology is the key to facing the challenge of greater imports and competition. Turning to the role of imported machinery we note that, 8 of the 38 domestic segment firms use imported machinery, while the corresponding figure for the export segment is 42 out of 50. About 37 of the 39 firms belonging to the both domestic and export segment use imported machinery. This is not surprising since export product are of better quality than domestic products and the values addition using imported machinery can be far greater. About 67 of the 105 smaller firms use imported machinery while 20 of the 21 larger firms use imported machinery. This is due to the fact that imported machines are far costlier than the corresponding domestic machines, and hence, are unaffordable by the smaller firms. Most of the imported machines were imported from Japan, Taiwan, China, Singapore and EU for the processes of dyeing, knitting, cutting and stitching.

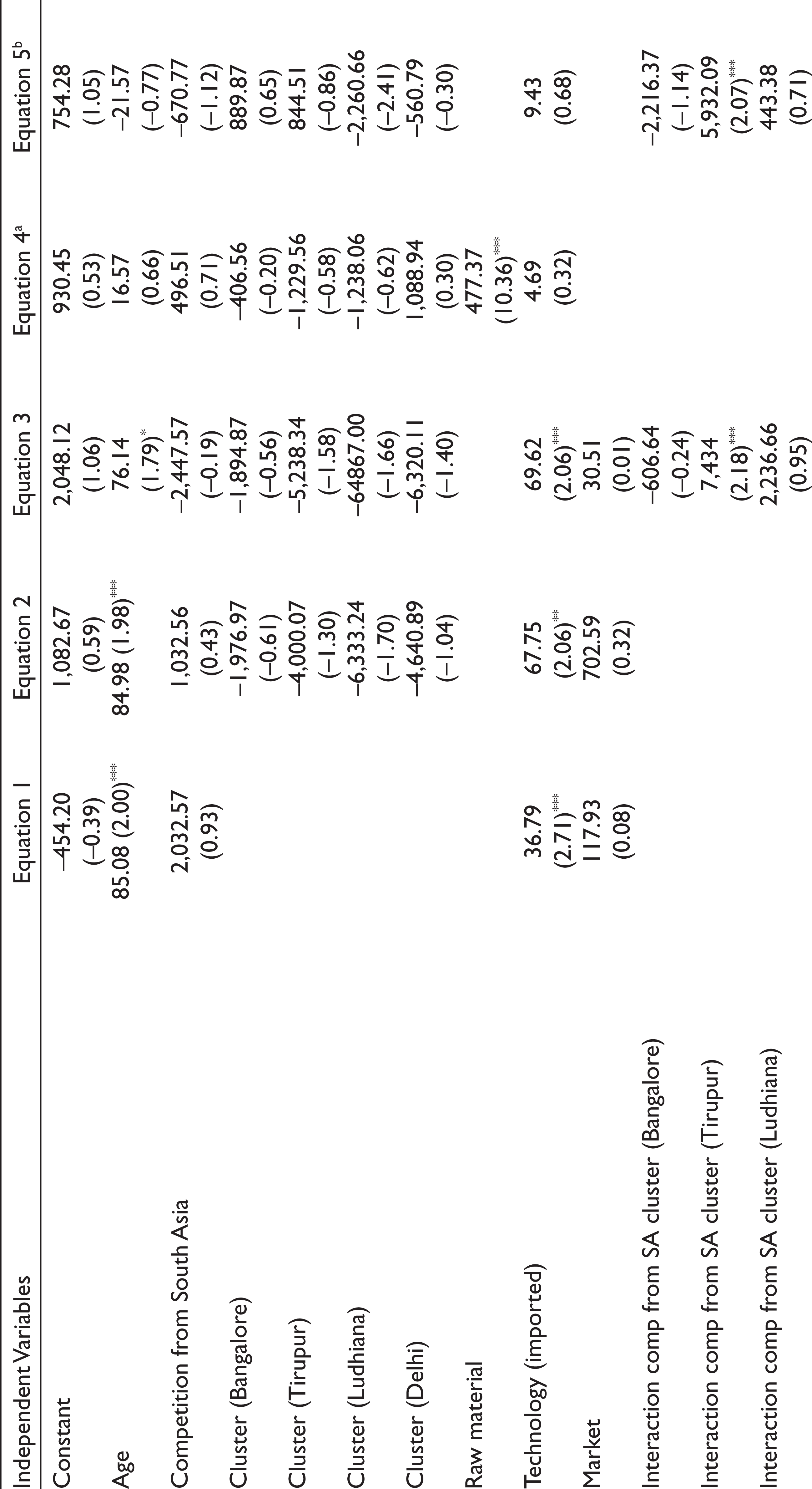

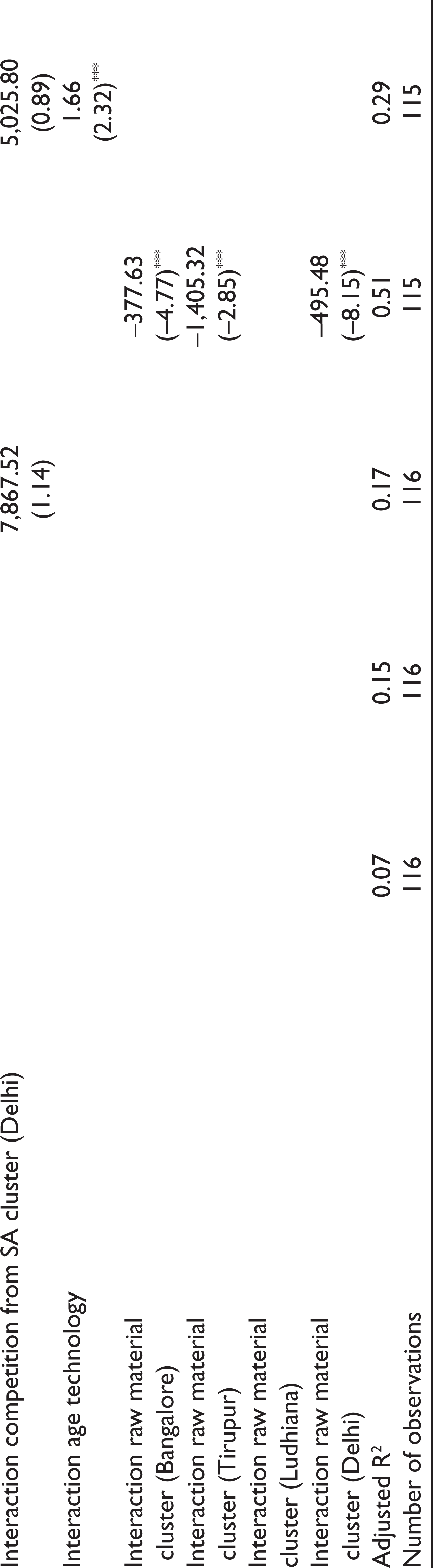

The dependent equation in the regression is sales of the firm. The independent variables are the age of the firm (Age), the cluster to which the firm belongs (Cluster), whether the firm is selling exclusively to the domestic market (Market), foreign market or the both, the effect of competition from South Asia (Competition from South Asia), and the technology used by the firm (Technology (imported)). Complete information on all the variables was available for 126 firms. Table 7 presents the descriptive statistics of the data used for the survey in terms of each cluster. The data point is available only for one year: 2009. Hence the OLS regression has been run for the cross section of firms on which the survey was conducted.

Descriptive Characteristics.

We note several points from the table: the number of older firms is greater in Kolkata and Ludhiana. The number of firms using domestic technology only is largest in Kolkata. As also noted earlier, the garments manufactured by the Kolkata cluster are mainly for the domestic market and require very little value addition. From the Table 7 we see, the number of firms catering only to the domestic segment is highest in Kolkata. None of the firms surveyed in the Ludhiana cluster were exporting and also none of them are facing any competition from South Asia. Using the data obtained from the primary survey, we have tried to capture whether the South Asian countries are exerting any influence on the Indian firms. One problem encountered in understanding clusters is that statistical significance in industrial production is hard to determine as economic regions do not respect administrative boundaries and industrial classifications often fail to capture the existing specialisation (Krugman, 1991). Thus, the design of the empirical exercise has to be done with caution, keeping the nature of data in mind.

Garments have played a critical role in the industrial development of a country. Staritz (2012) observes that the increasing importance of developing countries’ buyers can lead to new opportunities for LIC apparel exporters. The article states that the sector still provides opportunities for industrial development and this requires proactive industrial policies in LICs to further upgrading and local value capture and a focus away from solely exporting to the USA and Europe to regional and domestic markets. As noted by Gereffi (1995), in the export oriented garment sectors of South Korea, Taiwan and Hong Kong, new synthetic materials and computer aided designs aided the process. This brings to the for the role of upgrading as emphasised by the GVC literature. The process of industrialisation has to take into account the challenges of capital accumulation, financing, accumulation of knowledge, employment and demand growth (Ray, 2020). How has this manifested in the context of the Indian garment industry?

Empirical Specification

Rodriguez-Clare (2007) argues that if a developing country has a comparative advantage in a sector with Marshallian externalities (due to which firms benefit from the production and innovation activities of neighbouring firms in the same or related industries) temporary import substitution can work. However, Marhsallian externalities are not intrinsic to any sector but depend on the way production is organised. The externalities are related to the technology and so how the goods are produced matter (Porter, 1998). Lopez-Acevedo et al. (2017) have observed that agglomeration economies matter in South Asia. Agglomeration may arise from the specialisation of a region in a particular industry where firms share common inputs or knowledge (localisation economies). On the other hand, agglomeration may be the result of exploiting the overall diversity of industries in a regional economy (urbanisation economies). The magnitude of estimated impact of agglomeration on firm productivity is similar to that found in developed countries. However, data limitations prevent them from testing the impact of agglomeration on productivity and hence confirming which of the channels are more dominant in the apparel industry.

In line with the discussion above, the regression equation can be written as:

Variables

Results of the Regression.

We do not have information on the value of the raw materials used by the firms. However, as noted before raw materials constitute a significant cost. 13 In recent times, there has been a huge increase in the raw material costs especially due to the increase in the price of cotton. This variable is significant and has been reported in Table 8, in equation 4 where the dependent variable is export sales. It is also significant in other variants of the dependent variable.

Results

The results of the regression exercise are presented in Table 8. Equation 1 uses the age of the firm, competition from South Asia, use of imported raw material and source of technology employed (whether imported, domestic or both) as independent variables. From the table, we note that age, use of imported raw material and imported technology are significant.

The market variable is insignificant in most versions of the equation and implies that sales are not affected by the market to which the firm caters. The Indian domestic market is increasing at a phenomenal rate which has made it as attractive as the export market. We have run the regressions separately for the domestic or both, and export market and is reported in equation 5 and 4 in Table 8. Model 5 in Table 8, contains in addition to the variable in Model 4, interaction terms.

The variable Imported Technology is significant, and has revealed the role of the cluster in the context of technology. We have also tried an interaction term with the age of the firm and the imported technology—this is also significant with a positive sign. The variable Age also has the right sign and is statistically significant in most versions of the equation.

The cluster (location of firm with each cluster represented as a dummy), has been used as an independent variable in equation 2. None of the cluster variables in equation 2 are significant. The variable cluster should reflect the fact that the linkages in the cluster are aiding or hampering sales in line with the arguments by Schmitz (1989), Richardson (2010). We should thus expect a positive sign if the cluster linkages are aiding the sales. The variable cluster, however, is very interesting. The coefficient of the variable is negative but insignificant for all clusters (except Ludhiana) suggesting that there is no effect of clusters on sales of a firm. The variable ‘cluster’ must be interpreted with a caveat that the results depend on how the variable is modelled in the equation. The negative sign does not conform to the literature which states that agglomeration results in better firm performance. The cluster dummies are not statistically significant by themselves but as interaction terms with competition from Bangladesh (South Asia) or with import of raw materials, reinforcing the point on externalities. 14 The firms interviewed pointed out that the proximity of their production unit with other processing units leads to cost efficiency and hence, allows them to sell their product at a competitive price (as argued by Porter, 1998).

We have also run the above equations with employees as the dependent variable. We have information on full time workers, and contractual workers. We have run the regressions separately on the full time, contractual and total workers. However, from our data, we do not have information on the number of production workers. The results from this exercise broadly confirm the results obtained in the exercise with sales as the dependent variable, though most of the variables except technology are statistically insignificant. This confirms the importance of productivity in improving competitiveness (Sala-i-Martin et al., 2007). We have also used sales as another explanatory variable in the employees’ regression. Sales also captures the size of the firm and in the version of the regression with employees as the dependent variable, the effect of size on the performance of firms is being controlled. However, with the inclusion of the sales in the equation, technology becomes insignificant.

Competition from South Asia

The variable competition from South Asia is not statistically significant by itself, but as an interaction term with the cluster dummy. The coefficient of this variable is positive and significant for Tirupur but insignificant for Ludhiana and Delhi, and negative and insignificant for Bangalore. The interaction term of cluster with competition from South Asia is significant for Tirupur. This indicates that (compared to the benchmark cluster Kolkata), the effect of competition from South Asia, increases as the cluster is considered. Thus, at least in the case of Tirupur, belonging to the cluster is adding sales.

From Table 8, we observe that the variable competition from South Asia is insignificant in all versions of the regression. This corroborates with our findings of the survey that each of the South Asian country specialises in different categories of apparel products and hence, do not pose a threat to each other. Indian products involve a higher value addition, such as embroidery vis-à-vis products of other South Asian countries and lie somewhere in between the products manufactured by Turkey and other South Asian countries in terms of quality. They are thus, catering to different segments of the export market. Tewari (2008) observes that there is a clear division of labour in South Asia’s sectoral composition and specialisation in the textiles and clothing sector. South Asian countries have strong comparative advantage in clothing (though not in the same items) and are net exporters of clothing. While Bangladesh manufactures simple apparel such as t-shirts, shirts and alike in bulk, Sri Lanka is engaged in production of swimwear and women’s undergarments. Pakistan is primarily a supplier of fabrics especially denims and manufactures bed linen and other household apparels. India, on the other hand, manufactures superior quality woven and knitted products. Bangladesh’s exports is dominated by clothing while Pakistan’s exports by textiles. The import intensity of T&C in the region is low, especially imports of clothing (Tewari, 2008).

India is in the middle with share of clothing in exports at 43% while share of textiles is 57% in 2013 (Ray et al., 2016). In case of India, firms usually take up small orders and deliver products with value additions such as embroidery, sequencing, printing, and so on. One of the interviewees pointed out that to meet the changing demands of the Indian buyer, large retail stores like Shoppers Stop and Pantaloon replace their old stock every 15–20 days with new designs and cuts. This given an edge to the domestic manufacturers who can meet this requirement of value-added apparel more easily as compared to South Asian manufacturer. Lopez-Acevedo and Robertson (2016) observe that India will need to expand into man-made fibres (MMF) to gain global market share. Quality, lead time, compliance and reliability are issues that India faces and its advantage in design is not critical for export-oriented apparel industry.

The main reason for India’s poor performance (compared to Bangladesh) is the lack of proper clusters. 15 This is in line with Roy (2009), who discusses the Delhi NCR and the Tirupur cluster and argues that while the Delhi NCR agglomeration appears like a cluster, it is not what an industrial cluster should be: it is more of an estate than a cluster. The development of the cluster in India has followed the ‘top down’ approach and the natural process through which linkages are developed are yet to occur (at least in Delhi NCR).

Yet another reason comes from the discussion of the institutional framework of policy making in India. 16 Kennedy (2014) has argued that in India, the emergence of sub national state spaces, which is a historical process, has changed the institutional framework of the country. 17 These state spaces provide examples of governance mechanisms such as rules and policies for industrial development, and regulatory tools for promoting new clusters. She argues that economic policy making has to be viewed from this perspective, since the ‘reworked institutional context and sub national scales are crucial for understanding emerging patterns of economic governance’. Shirley (2005) says that informal institutions influence the ways of functioning of a democracy that are not often examined. 18

Martin et al. (2008) point out that policies promoting agglomeration are unnecessary. Using data from French firms, they show that while clusters do bring economic benefits, such as productivity gain, there is a bell-shaped curve between productivity gains and agglomeration. They argue that policies that attempt to foster more dispersion of economic activities to reduce regional inequalities also have efficiency costs. Lall et al. (2004) find that market access and proximity to transport hubs provide net benefits to firms in four sectors of India. This means that locating in urban areas with its associated costs is preferred due to the unequal distribution of transport infrastructure. De Marchi et al. (2018) have argued that there is need to rethink the balance between manufacturing, services and innovation.

Conclusion and Policy Implications

In this article, we examine the Indian apparel industry to examine the effect of clusters on the sales of this industry. We argue that the main reason for India’s poor performance (compared to Bangladesh) is the lack of proper clusters. The natural process through which linkages are developed are yet to occur in most clusters studied in this article. This naturally leads to the question that what policies should be followed to encourage cluster formation or should that be left to firms too? While there is a lot of extant literature on this issue, the linkage between trade and industrial policies along with land acquisition, access to other inputs, and so on, has been emphasised often. What has not been discussed is that sometimes the ‘top-down’ approach of policy driven clusters will not work and other alternatives need to be explored. Notably, the discussion on how sub national state spaces in India, has changed the institutional framework of the country is also missing. Through this article, we show why it is important to discuss these issues further in order to improve our competitiveness and exports.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.