Abstract

This article incorporates international transfer of financial capital, a process that is essential to the offshoring of labour services across time zones but has been ignored. Considering two identical countries, we check the effect of utilisation of time-zone difference, which involves virtual transfer of financial capital along with labour services. Time-zone difference reduces the production time, enabling producers to repay the borrowed financial capital earlier and incur a lower interest rate compared to autarky. Consequently, both countries experience an increase in productivity. Further, because of the inclusion of financial capital transfer, both countries experience different changes in their factor prices. This implies that it becomes necessary for policy makers to decide whether to promote their country as a source or a host.

Introduction

Offshoring service tasks to professionals residing in different time zones (TZs) helps producers dedicate full 24 hours to work without burdening the professionals for overtime or night shifts. When virtual tasks are divided between different TZs, or more specifically, non-overlapping TZs, a particular task is undertaken by affiliates of one location in their regular working time and at the end of the day, they hand over the task digitally to the next location where the working hours have just started. This process of virtually trading labour services helps countries to develop a comparative advantage in service production (Kikuchi, 2009; Marjit, 2007). Marjit and Mandal (2017), Kikuchi and Marjit (2011) and Mandal (2015) show that virtual trade of labour services across TZs contributes to a country’s growth. Further contributions, such as Nakanishi and Long (2015) and Kikuchi and Long (2011), show the effects of trading labour services across TZs on different sectors of the economy. Other important contributions in this area are Kikuchi and Iwasa (2010), Matsuoka and Fukushima (2010), Tomasik (2013), Dettmer (2014), Nakanishi and Long (2020), Prasad et al. (2017), Nakanishi (2019), etc. Beyond these, some recent studies have highlighted the significance of trading labour services across different TZs through multiple aspects. Nakanishi and Long (2020) check the effect of offshoring Research and Development services across different TZs on growth rates of wages, product quality, etc. Mandal and Das (2023), incorporating the time-saving role of TZ difference, compare the effect of distance on goods and services trade. Prasad and Mandal (2024) prove that offshoring labour services, between non-overlapping TZs, benefits service production despite inter-country skill differences.

Even though there are many significant contributions showing the role of TZ difference for service provision, most focus only on the trade of labour services. However, while trading labour services across TZs, it is likely that there is a transfer of financial capital in the form of payment to the affiliates. Therefore, along with labour services, movement of financial capital also takes place, which has hardly been considered in the existing research based on utilisation of TZ difference. In this article, we incorporate this point and consider that along with labour services, the required financial capital is also transferred to perform the task. While doing so, we follow Marjit et al. (2020), which is the only work that incorporates the movement of financial capital across TZs. Marjit et al. (2020) focus on conditions for profitable transfer of financial capital across TZs. Further, it expresses the possibility of utilising TZ differences for using borrowed financial capital economically. Taking cue from this work, our objective is to check the effect of utilisation of TZ difference—which takes place to economise on financial capital cost—on factor prices and output of both the source and host countries. For this purpose, we frame a model following Ethier (1982), Chakraborty (2003) and Kikuchi (2011). Our model depicts the preparation of a final good in three stages. In the first stage, a sector produces differentiated services; second, the differentiated services are assembled by another sector to produce a composite good. In the third stage, the composite good is used to prepare the final good. In our model, following Marjit et al. (2020), financial capital is borrowed for a certain period that includes both day and night, but production occurs only during the daytime. Therefore, with idle nights, the interest on the borrowed financial capital increases. 1 In this case, if parts of the production process are shifted to another TZ, production will be accomplished earlier, saving both time and cost of financial capital. We incorporate this time- and cost-saving effect of utilising the TZ difference to check the effects on different sectors and factors of both the partner countries.

As mentioned before, significant studies check the effect of time-zone-difference-induced trade of labour services on factor prices and output, considering different situations. However, papers such as Kikuchi and Marjit (2011), and Marjit and Mandal (2017) consider the case where both countries outsource night-shift production to each other; therefore, both economies experience the same effects. Again, studies considering one-way outsourcing, such as Mandal et al. (2018), and Matsuoka and Fukushima (2010), focus only on how the outsourcing country is affected, ignoring the outsourcee. In contrast, we check the effect of utilising TZ difference on both the countries where one offshores, while the other works on the offshored task. A recent contribution, Nakanishi and Long (2020), also takes the case of one-way outsourcing. However, they consider non-identical trade partners and focus primarily on the growth rates. Our study considers identical countries and explores the effects on factor prices and output resulting from the transfer of labour services and financial capital. Considering identical countries highlights the sole impact of financial capital movement. Further, it helps determine whether a country benefits more as a host or a source—which again is an unexplored question in this specific field of time-zone-difference-induced trade.

The second section elaborates the basic model under autarky. The third section deals with the situation when one of the sectors offshore to a country located in a different TZ using the communication network. The fourth section considers the model without financial capital to demonstrate the difference in results when financial-capital transfer is ignored. The fifth section concludes the article. Details of mathematical analyses are supplied in Appendices A–C. Appendix D considers the case of mutual offshoring. 2

The Basic Model

We consider two identical countries, H and S, located in non-overlapping TZs. There are three sectors, X, Y and Z. Sector Z consists of n number of differentiated service-producing firms facing a monopolistically competitive market. The outputs of sector Z firms are assembled to form a composite service (X) by sector X. X is used in sector Y to produce a final good (Y). 3 Each country has four factors of production: skilled labour (L), unskilled labour (U), financial capital (K) and physical capital (T). To pay the variable inputs (L and U), financial capital is borrowed at a per-day interest rate of r. Details of each sector are as follows:

Y, the numeraire good, is produced using X and U in one workday (12 hours). Y has a Cobb–Douglas production function exhibiting constant returns to scale:

Y producers equate the marginal revenue product (MRP) of inputs with the marginal cost (MC) to maximise profit subject to production function (1). The MRP of X is

with PX being the MC of X, at equilibrium

Similarly, equating MRP of U and its MC, we have

where wU is the wage of U. Since K is borrowed to pay the unskilled labours, the actual cost of one unit of U becomes wU (1 + r).

X is prepared within 12 hours by assembling the available differentiated services (zi). The production function of X is

The service varieties (zi) are imperfectly substitutable with each other. Therefore, v in Equation 4 is the elasticity of substitution between each pair of zi.

X producers minimise their cost subject to the production function (Equation 4). The first-order conditions of the minimisation problem are as follows:

or

and

In Equations 5 and 6, PX is the price of X. Equation 5 gives the demand function for zi. Note that the number of z firms is large enough such that individual strategic behaviour is negligible and each z firm charges the same price. Further, we assume that each z firm faces the same cost conditions. Therefore, the profit-maximising output and price of all the z firms will be the same. Thus, with n number of firms, Equations 4 and 6 can be written, respectively, as

and

Sector Z consists of n firms that produce differentiated services using skilled labour (L) as a variable input and physical capital (T) as a fixed input. The production is divided into two stages; each stage requires 12 hours of work. We assume that only 12 hours of daytime are utilised for work and nighttime is the leisure time. One unit of z is produced using T and aLZ units of L. Each stage is assumed to use one unit of L; thus, aLZ = 2.

4

If w is the per-day wage of L, then the total amount L receives for one unit of z is aLZw. Therefore, aLZw amount of K is borrowed from a financial institution at a per-day interest rate r. Since it takes 2 days to produce z, the cost of aLZw amount of K is aLZw(1 + r)2. If the ith firm produces zi(i = 1, 2, … n) units of differentiated service, the total cost (TC) of production is

where t is the rent of T and x is the fixed amount of T required to produce any number of outputs. This fixed input can be interpreted as the Information and Communication Technology (ICT) infrastructure. Under equilibrium, each firm equates marginal revenue (MR) with MC. The MC is aLZw(1 + r)2.

Using the demand function of zi obtained in Equation 5, we get

5

Now, equating MR with MC, we have

Free entry and exit in sector Z drives down the profit to zero. Therefore,

As mentioned earlier, the price and output of z firms will be the same; thus, the equilibrium condition of a representative z firm is

and

We assume full employment of factors of production. Therefore, the full employment conditions are as follows:

and

L¯, T¯, U¯ and K¯ are the fixed supplies of skilled labour, physical capital, unskilled labour and financial capital, respectively. In Equation 11, the total skilled labour employed in sector z (aLZzn) equals L¯. Similarly, in Equation 12 the total physical capital used by sector z, that is, xn, equals T¯, and in Equation 13 the total unskilled labour employed in sector Y equals U¯. In Equation 14, K¯ is divided into the amount borrowed by sector z (L¯w) to pay L and the amount borrowed by sector Y (U¯wU) for paying U.

Now, we move towards solving the model and obtaining equilibrium values. Detailed calculations are provided in Appendix A. From Equation 12, the number of z firms within the economy is

Putting the value of n in Equation 11, the per-firm service output is obtained:

Using Equations 7, 8, 13 and 16 in Equation 2, we get the price of intermediate service:

where

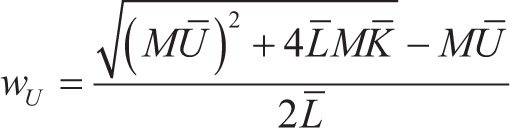

Now, substituting Equation 18 in Equation 14, we have the equilibrium value of wU:

Therefore, from Equation 18 the value of w is

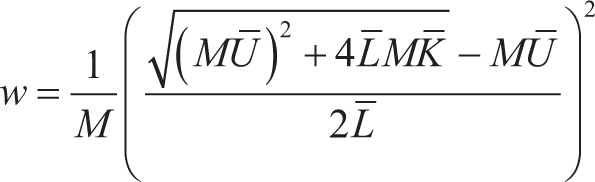

Putting the value of wU in Equation 3, we get the per-day cost of one unit of K:

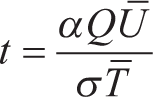

Next, t is obtained by substituting the value of Pz and z in Equation 10,

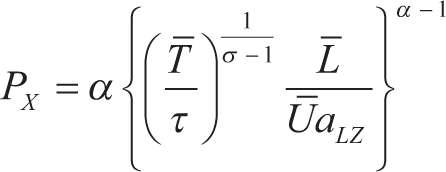

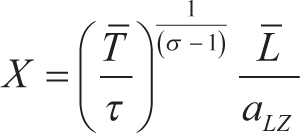

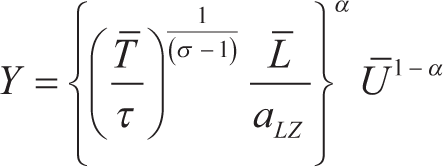

Similarly, with the values of Pz, z and n, we obtain PX:

and the output of X is

This implies that the amount of final good produced is

Therefore, the model is solvable, and now we have the equilibrium values of all the endogenous variables.

Effect of Utilising the Time-zone Difference

If z production is divided between non-overlapping TZs, one stage of z can be produced in H in its regular working hours and the other stage in S, during H’s nighttime. Therefore, the entire production can be accomplished in 24 hours of one calendar date and interest on borrowed K will have to be paid only for 1 day. Thus, to save the cost, suppose z producers of country S offshore one of the stages 6 to country H along with the required amount of financial capital. 7 Hence, we take S as the source country and H as the host country. Here, only z firms can utilise the TZ difference as X and Y are produced within one dayshift eliminating the need for fragmentation and time-zone utilisation. We further assume that X and Y are sold within domestic boundaries. 8

Now, for the after-offshoring values of the variables, we use superscript ‘S’ and ‘H’ for the source and host countries, respectively. However, for the variables whose post-offshoring values are the same for both countries, the superscript ‘I’ is used. The changes experienced by both countries are as follows. First is the change in the cost of z production. After fragmentation, H produces only one stage of z using one unit of domestic L and x amount of T; L is paid using the transferred financial capital. They sell the first stage to the z producer of S who has supplied the required financial capital.

9

In addition to supplying K, the source country also compensates the host-country z-producers, and thus the total amount the source country z producer pays is PHZ. Therefore, PHZ is the value of the first stage of z production received by a host-country producer. With zI being the post-offshoring quantity of z produced by each firm, the total cost of producing the first stage of zI units by a representative host-country producer is

At equilibrium,

The zero-profit condition is

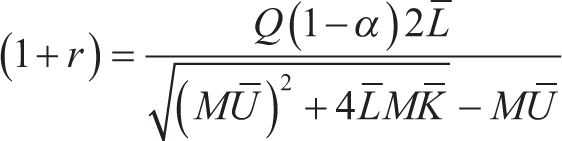

On the other hand, z producers of S produce only one stage employing L and T for only 12 hours. Now, the source-country z producer borrows an amount equal to the sum of what must be paid to domestic L and PHZ. However, because of TZ difference, the rate of interest on K is paid for only 1 day. Thus, the cost of K for producing one unit of z is

Putting the value of PHZ from Equation 26

where wI is the wage of L after offshoring. Since S is the sole owner of services (z), wage of L is determined by S. Further, as both countries’ skilled labours are identical, they must be paid the same wage. Therefore, we take wS = wH = wI.

Equating MR and MC, we get

and the zero-profit condition is

Another change that the countries experience is in their skilled-labour constraint. Since each country produces only one stage of z using only one L per unit, the skilled-labour endowment equation in both countries becomes:

Equation 30 denotes each z-firm’s post-offshoring output. This implies that the world supply of z is nzI.

Third, with K being supplied from S, z firms in H will not use domestic K. Hence, the full-employment equation of K in H, post-offshoring, becomes

Conversely, z producers in S now must borrow the amount

Putting the value of PHZ,

Using Equation 30,

The endowment equations of T and U, Equations 12 and 13, however, remain unchanged.

Now, with S being the sole provider of z, host-country X producers need to obtain z from S. The total supply of z is thus divided between H and S. Since both countries are identical, they demand equal amounts of z. The demand-supply equality implies,

Subsequently, the production function of X in both countries, post-offshoring, becomes

However, PX given by Equation 8, and the equilibrium conditions of Y production (Equations 2 and 3) remain the same as before. Using the values of n and zX, the post-offshoring outputs of X and Y in each country are

The above quantities of X and Y when compared with autarky are found to be unchanged as the world supply of z remains the same after offshoring. However, in the offshoring situation, the same amount of z is produced 24 hours earlier than in the autarkic situation. Subsequently, as z is produced 24 hours earlier, X and Y production are also accomplished earlier. Thus, there is an increase in output per unit of time implying an increase in productivity. 10 This gives us the following proposition:

Proposition 1: Utilisation of TZ difference to reduce financial capital cost increases the productivity of all the sectors of both the source and host countries.

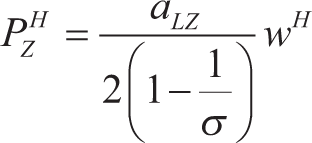

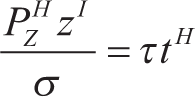

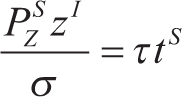

Now, we observe the changes in factor prices. Let us start with the effect on rent of physical capital. Equation 30 shows that the post-offshoring amount of intermediate and final z is twice the amount produced in autarky by a single country. Moreover, from the zero-profit condition of z, the rent of T depends on the number of z stages produced, which positively affects the T owners. The rent of T in S is 11

where

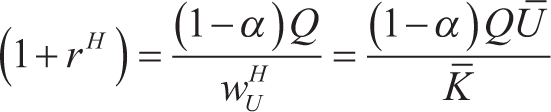

Comparing tH with the autarkic rent t (check Appendix C), we get tH < t, which implies that physical capital owners of H lose when z producers opt to work on the offshored task. This is because, even though there is a rise in units of z stages produced, the price that H receives for z (PHZ) is the price of only one stage, less than what they received in autarky. This suggests that the loss from producing only one stage outweighs the gain of producing larger number of one stage. Further, it is evident that tS > tH as ts depends on the price of final z (refer to Equation 29), which is certainly more than the price of just the first stage. Therefore, we have the following proposition:

Proposition 2: With the movement of labour services and financial capital to a different TZ, the physical capital owners of the source country gain through a rise in rent, whereas the physical capital owners of the host country lose. The rent in the source country becomes greater than that in the host country.

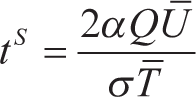

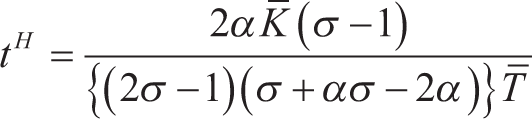

Next, we observe the impact of offshoring on the unskilled wages of both countries. After offshoring, the wages received by U in H and S are,

12

respectively,

and

Since

Thus, the proposition from the above discussion is as follows:

Proposition 3: Due to movement of labour services and financial capital across TZs, the source-country unskilled labours receive a lower wage than that of the host country. Nevertheless, compared to autarky, the unskilled labours of both countries gain if

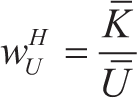

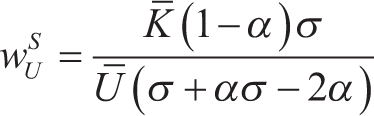

Now, moving towards examining the effect on the cost of K we observe that the per-day cost depends on the unskilled wage. This may be understood from the following equilibrium values:

and

Comparison of the above two expressions reveals that the per-unit cost of financial capital in S, post-offshoring, becomes higher than in H. The likely reason for

Proposition 4: The cost-saving approach of z firms makes the host country’s financial capital owners earn less than the source country, irrespective of whether the financial capital owners gain or lose by offshoring.

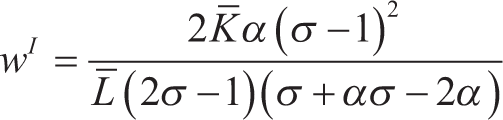

Next, the equilibrium value of skilled wage in the offshoring situation (wI) is

15

Though the demand of L remains unchanged, the skilled wage changes as we have considered the transfer of K along with labour services, and if

Proposition 5: Even when productivity increases in the skilled-labour-specific sector, skilled labours benefit only under certain conditions where endowment levels, elasticity of substitution between z-varieties and unskilled labour’s share in the final output become important factors.

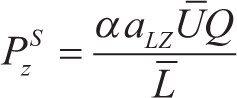

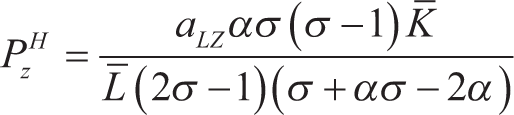

Now, we seek the equilibrium price of z. Using the value of wI and

and the price for producing one stage of z is

Thus, price of z remains unchanged. Therefore, the effect of reduction in the financial capital cost because of utilisation of TZ is absorbed by the factor prices. From the above exercise, we get the following proposition.

Proposition 6: Transfer of financial capital and labour services between non-overlapping TZs does not alter the price of differentiated services but affects the factor prices of both the countries. The ultimate effect on factor prices and their relative global position in terms of earnings depends on the characteristics of the country and whether the country is a host or a source.

Model Without Financial Capital

In this section, we adopt a simplified version of our model where the presence of financial capital is ignored and only three factors of production are considered—skilled labour, unskilled labour and physical capital.

16

Comparison of the results obtained in this analysis with those obtained in the previous sections will highlight the importance of incorporation of financial-capital movements. In the main model, offshoring is not possible without financial capital transfer, as producers of H need funds to undertake production. However, for the sake of comparison, this section ignores the source of funds and considers that only two factors (L and T) are required for service production. Therefore, now the total cost of a representative z firm is

Equating MR and MC gives

The zero-profit condition is

The production function of X and Y, and full employment conditions for L, T and U remain unchanged. Following a similar analysis as in the previous model, we get the equilibrium values as follows:

and

Now, when z producers of S offshore half of the production to H, each country uses only one unit of L for producing one unit of z. Therefore, the full employment equation of L of both countries becomes

As

Note that, since the number of intermediate and final products must be same, zI is the post-offshoring value of z in both countries. As the financial capital movement is ignored, offshoring only affects the skilled-labour endowment equation while other endowment equations remain unchanged. Moreover, the variables of both countries undergo the same change. Therefore, post-offshoring values are denoted by the superscript I for both countries.

Now, comparing the before and after-offshoring values of z, we have

Similar to the previous model, since S is the owner of z, it produces double amount of z, which is divided between both countries to produce X. This implies that X producers of both countries get the same amount of z for production as in autarky, but one day earlier. Consequently, the production of X and subsequently Y is accomplished earlier, indicating an increase in output per unit of time. Turns out, in the case of output, ignoring financial capital does not affect the outcome of utilising the TZ difference.

Now, coming to the effect on output prices and factor prices, we encounter that as the world supply of z does not change, there are no changes in the price of z, X and

and

Comparing the before and after-offshoring values, we have

and

Therefore, offshoring to a non-overlapping TZ doubles the remuneration of factors involved in service production. The current picture differs considerably from the case where we have incorporated the role of financial capital. In the current case, only the factors involved in service production are affected, and the effect on both countries is the same. On the other hand, in the previous case both the source and host countries experienced different changes, and all the factor prices were affected. Thus, it is evident how much difference the consideration of financial capital entails, which was ignored in the analyses of utilisation of TZ difference so far.

Conclusion

The study considers the role of TZ difference in making borrowed financial capital economical by enabling nighttime production, which allows firms to repay earlier and save costs. Given this cost-reducing role of TZ difference, we point out that the literature analysing the effects of virtual trade across TZs has ignored the movement of financial capital and focused only on the transfer of labour services. Therefore, the article checks the effect of virtual transfer of financial capital along with labour services in a monopolistically competitive framework. Specifically, we investigate how factor prices and output are affected by transferring financial capital, while offshoring labour service, to an identical country located in a non-overlapping TZ. Further, we observe which country, source or host, is benefitted more by the utilisation of TZ difference. Results show that both countries gain from increased productivity across all sectors. However, understanding whether being a source country is beneficial or a host country is not straightforward when it comes to the effect on factor prices. The source and the host country’s factor prices are affected differently because of the incorporation of financial capital transfer. Physical capital owners of the source country gain, while those of the host country lose. The unskilled wage of the host country becomes higher than that of the source country. Consequently, financial capital owners of the source country earn more than those of the host country. Therefore, our analysis gives the policy makers an idea about whether to promote service firms for being an outsourcer or outsourcee, for the decision affects the returns to factors differently. Depending on which factor of production needs to be favoured in the economy, the policy makers can encourage the service firms to make their country a host or source.

In the penultimate section, we have considered the model without financial capital to highlight its role in shaping the outcome of offshoring across different TZs. The section reveals that it was only after incorporating financial-capital transfer did it become evident that the two countries experience different changes in factor prices; otherwise, the impact was identical.

Footnotes

Acknowledgements

This article is based on a part of the PhD thesis of the first author. We are thankful to the two anonymous referees for their helpful and constructive comments which helped us to improve the exposition of the article. However, the usual disclaimer applies.

Authors’ Contribution

All authors have made substantial contributions in preparing the manuscript, approved its submission and have accepted responsibility for the entire content of this manuscript.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.