Abstract

With the recent COVID-19 pandemic, among other crises (e.g., Russia–Ukraine conflicts and recession projections) threatening organizations’ financial conditions across the globe, supervisors may not only encounter challenges such as job cuts that test their ethical leadership, but also experience financial insecurity themselves. However, our knowledge of why and when supervisors’ ethical leadership behaviors may be affected in such a situation remains quite limited. In this research, we draw on uncertainty management theory (UMT) to examine the potential influence of financial insecurity on ethical leadership. Specifically, we suggest that financial insecurity triggers anxiety in supervisors, which inhibits their demonstration of ethical leadership. We also propose organizational pay fairness as a boundary condition for this process, such that supervisors who perceive their pay as fair are less susceptible to the anxiety resulting from financial insecurity than those who perceive their pay as unfair. Results from two multi-source, multi-wave studies supported our hypothesized model. We conclude by discussing the theoretical and practical implications of our findings.

Keywords

Leaders have never led through a pandemic before, and the sense of anxiety and hopelessness we’re all feeling is also being felt by our business leaders. (Dr Nora Koslowski, Financial Times)

The COVID-19 pandemic among other crises has tested ethical leadership in many ways. In leading through times of crisis, organizational leaders encounter a broad range of challenges that require them to signal their ethical standards—for example, when managing trade-offs between job cuts and the broader rights of society, or in needing to be mindful of the effects of their choices on the lives and futures of their subordinates (Allal-Chérif et al., 2021; Beasley and Adkins, 2020). Defined as the demonstration and promotion of normatively appropriate conduct through personal and interpersonal relationships (Brown et al., 2005: 120), ethical leadership has been associated with subordinate well-being and performance-related outcomes (Bedi et al., 2016; Ng et al., 2021), which are essential in times of crisis and structural changes (Collings et al., 2021). Thus, it is crucial to better understand the factors that promote or impede ethical leadership practices in organizations.

To date, research on the antecedents of ethical leadership has explored both personal (e.g., moral identity) and contextual (e.g., ethical culture) facets of morality to predict its occurrence (Den Hartog, 2015). These studies provide insights into the influence of stable individual differences (e.g., moral identity) and organizational contexts (e.g., ethical cultures) on ethical leadership. However, they have not addressed how changing dynamics, such as the COVID-19 pandemic response, create uncertainty surrounding some of the most basic attributes of a leader’s job—financial security and the subsequent impact on ethical leadership. Indeed, the pursuit of sufficient financial resources to cover current and future expenses has been a key motivation for people to seek managerial roles (Deci and Ryan, 2008; Gupta and Shaw, 2014). For instance, an industry survey in the United Kingdom shows that senior managers earn 3.3 times more than employees (Hay Group, 2021). However, the COVID-19 pandemic’s disruptions to the global economy, coupled with the most recent Russia–Ukraine conflicts, have introduced new dimensions of uncertainty into business outlooks and financial conditions, threatening the security of managers’ financial resources (McKinsey, 2021; Wilson et al., 2020). A recent report (Bhutta et al., 2020) reveals that nearly 50% of working adults, including those in managerial roles, perceive themselves to be financially insecure, which is to say that they perceive themselves to have insufficient financial resources to achieve their financial goals (Howell et al., 2013). Managers, especially those at the lower level of the organizational hierarchy, are more prone to experience financial insecurity (Wilson et al., 2020), and as such, the demand for managers to engage in ethical leadership is contextualized in an unprecedented yet under-studied situation in which the managers themselves are experiencing financial insecurity and struggling to meet their own basic needs.

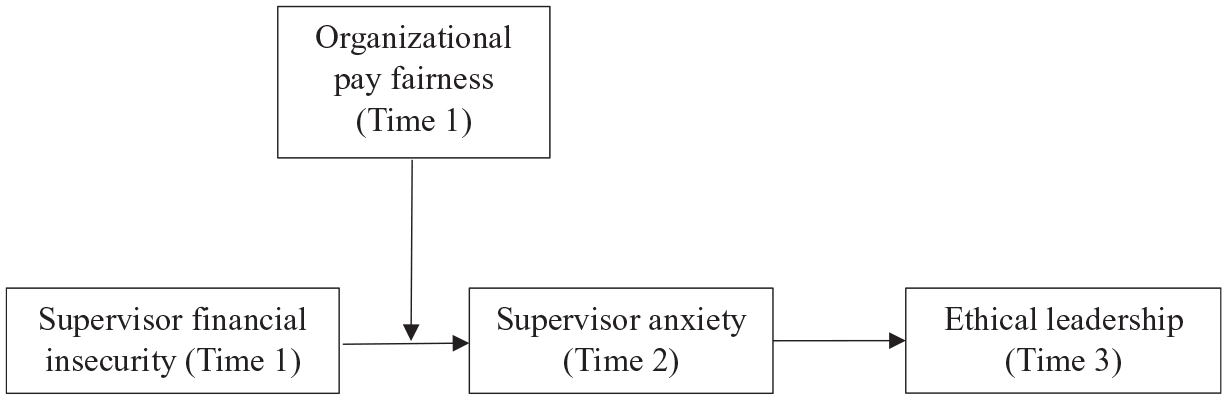

The aim of this research is therefore to investigate the potential influence of financial insecurity on ethical leadership among supervisors. This endeavor offers both theoretical and practical value by enriching our understanding of how leaders navigate and respond to uncertainty. To achieve our objective, we draw on uncertainty management theory (UMT; van den Bos and Lind, 2002) to explain the underlying mechanism and boundary condition of the association between financial insecurity and ethical leadership. UMT concerns people’s anxiety and subsequent behaviors in the face of various sources of uncertainty. According to van den Bos (2001), when individuals perceive that they are not in control, they experience uncertainty; as a situation in which supervisors are not in control of their financial situations, financial insecurity—the belief that one cannot or will not be able to meet one’s financial needs—represents a source of uncertainty (van den Bos and Lind, 2002). Drawing on UMT, we propose that financial insecurity, as an uncertain situation, elicits feelings of anxiety, which may provoke self-protection and draw attention away from other desires or standards, and thus inhibit ethical leadership behavior. Further, UMT proposes that fairness-related information can help individuals cope with anxiety, and that perceived fairness regarding the outcomes is a more significant mitigator than other types of justice in the face of uncertainty (Lind and van den Bos, 2002). We thus propose that perception of pay fairness, defined as the perceived fairness of the financial resources received from the organization (Gupta and Shaw, 2014), acts as a key boundary condition of the relationship between supervisor financial insecurity and ethical leadership via supervisor anxiety, and theorize that supervisors’ perception of pay fairness weakens the extent to which their financial insecurity heightens the anxiety that inhibits ethical leadership behaviors (see Figure 1).

Theoretical model.

Our research makes several contributions to the literature. First, we enrich the literature on the antecedents of ethical leadership by identifying supervisors’ management of their own financial insecurity as a prerequisite for their ethical leader behaviors. In doing so, we depart from past research that has tended to rely on personality and social learning perspectives in promoting ethical leadership (e.g., Babalola et al., 2019; Mayer et al., 2009; Walumbwa and Schaubroeck, 2009). In contrast, we suggest that otherwise ethical leaders may compromise their ethical behaviors in order to fulfill their basic financial security needs, thus adding a broader social context to the study of behavioral ethics. Second, we clarify the underlying mechanism through which financial insecurity translates into reduced ethical leadership behaviors. By returning to the root of UMT, we examine the foundation of uncertainty management—with supervisors’ state anxiety as a mechanism—and explore possible reasons for reduced ethical behaviors from an emotional perspective. Third, we add nuance to our understanding of how and when supervisor financial insecurity impedes ethical leadership practices by highlighting pay fairness as a crucial element that may mitigate the negative effects of supervisor financial insecurity on ethical leadership. Finally, we enrich the financial insecurity literature, which has thus far only explored financial insecurity’s effects on a limited range of employee health, financial, and work–family outcomes (e.g., Lawrence et al., 2013; Odle-Dusseau et al., 2018; Sharma et al., 2014). We respond to repeated calls for a broader understanding of financial insecurity (e.g., Odle-Dusseau et al., 2018) by considering the important yet often neglected factor of supervisors’ perceived financial insecurity. Though supervisors are generally paid more because of their leadership responsibilities, their financial insecurity is an increasing reality. We contribute to this line of research by showing that supervisors’ financial insecurity impacts not only their own behaviors, but also their employees’ outcomes via ethical leadership.

Theory and hypothesis development

Uncertainty management theory

UMT (Lind and van den Bos, 2002; van den Bos and Lind, 2002) explains how people deal with and respond to uncertainty, defined as a situation in which the likelihood of occurrence of a particular outcome is unknown (Alvarez et al., 2018; Milliken, 1987), or more broadly as a situation that is not predictive or difficult to understand (van den Bos and Lind, 2002). According to UMT, one of the most significant challenges in life is coping with the uncertainty of making decisions before their consequences are revealed, as the desire for predictability and certainty is deeply instinctive (van den Bos, 2001). From this perspective, uncertainty is undesirable, unpleasant, and challenging (van den Bos et al., 2008).

Emerging research is rapidly expanding the types and sources of uncertainty to include the self (De Cremer and Sedikides, 2005), relationships (Knobloch and Solomon, 2002), and organizations. Indeed, organizations are rich in uncertainty because they experience constant changes arising from technology, competition, climate change, and crises such as natural disasters or pandemics. For instance, Thau et al. (2009) showed that authoritarian management style yielded a type of uncertainty that interacted with abusive supervision to increase employees’ deviant behaviors. Takeuchi et al. (2012) showed that short job tenure induced uncertainty and reduced employees’ voice behavior, and both Loi et al. (2012) and Wang et al. (2015) identified job insecurity as another source of uncertainty in the organizational setting. In these organizational circumstances, the fact that employees lose their jobs or do not receive direction from their leaders does not represent uncertainty per se; rather, it is the concern about these issues, the sense of insecurity about their future employment and financial circumstances, that constitutes the uncertainty (Lind et al., 2000). These studies have expounded the types and sources of uncertainty but have not explained the mechanism of uncertainty-induced effects (Loi et al., 2012; Thau et al., 2007). Though Wang et al. (2015) were the first to examine work enagement as the pathway for employees’ uncertainty management responses, they did not tap directly into the root of UMT—that is, the emotional process that drives uncertainty management behaviors.

The key tenet of UMT is that anxiety is a mechanism that explains how the experience of uncertainty drives dysfunctional behaviors (Lind and van den Bos, 2002). This is because uncertainty encodes a perceived inability to understand the means and outcomes of the situation—for instance, the direction in which the situation is changing, the impact on those involved, and the responses that could be successful (Milliken, 1987). People facing uncertain situations thus tend to feel anxious about their ability to avoid or mitigate possible negative consequences. They are also anxious because uncertainty implies risk, as erroneous decisions could result in severe make-or-break consequences (Waldman et al., 2001). According to UMT, people in uncertain situations seek buffers to render the uncertainty more manageable (Lind and van den Bos, 2002). Accordingly, we argue that supervisor financial insecurity represents an uncertain circumstance that triggers supervisor anxiety—the feelings of tension, worry, and apprehension experienced by those in leadership positions (Spielberger, 1972)—which then reduces supervisors’ ethical leadership at work.

Financial insecurity, supervisor anxiety, and supervisor ethical leadership

Ethical leadership involves emphasizing and reinforcing appropriate behaviors in the workplace with the goal of encouraging subordinates to adhere to ethical standards (Brown et al., 2005). Enacting such leadership behaviors not only requires supervisors to actively promote ethical behaviors, but also demands that they demonstrate consistency in their own behaviors by remaining fair and honest (Brown et al., 2005; Den Hartog, 2015). However, drawing from UMT, we predict that ethical leadership will be hindered by the anxiety that arises from supervisor financial insecurity.

Financial insecurity is a subjective assessment of one’s inability to meet financial responsibilities to fulfill needs that are reliant on material resources such as income, savings, and credit (Howell et al., 2013). The subjective nature of this assessment makes it independent of objective financial status (e.g., the actual amount of income) (Sinclair and Cheung, 2016). Research indicates that people are more likely to be influenced by their perceptions of a situation than by its objective nature (Lewin, 1951); from the UMT perspective, this is because the uncertainty associated with the perceived lack of control is undesirable and frustrating even when the objective risks are relatively low (van den Bos and Lind, 2002).

We expect financial insecurity to induce supervisor anxiety for two reasons. First, the safety and stability offered by financial security is a fundamental human desire (Deci and Ryan, 2008). Regardless of its form, money is used to satisfy basic physiological needs and is an important precondition of overall life satisfaction (Howell et al., 2013). When people fear that they do not have enough financial resources to meet their needs, they experience stress, frustration, and reductions in health, well-being, and overall mental functioning—experiences that may trigger their anxiety (e.g., Corman et al., 2012; Frijters et al., 2004; Howell et al., 2013; Johnson and Krueger, 2006). Second, financial insecurity represents an uncertain situation that brings disruptions to familiar routines and suggests the lack of choice or effectiveness in achieving desired ends (Ploetner et al., 2020; Romo et al., 2022). Predictability and reduced uncertainty are among the most common human desires (van den Bos, 2001). In this respect, supervisors who are financially insecure are likely to experience feelings of pressure, worry, and unease over their futures (Lind and van den Bos, 2002). These unpleasant feelings constitute anxiety (Mathews, 1990), which reflects “a state of distress and/or physiological arousal in reaction to stimuli including novel situations and the potential for undesirable outcomes” (Brooks and Schweitzer, 2011: 44). In contrast to other negative emotions—for example, fear, which is short-lived and indicates an intense emotional reaction to an immediate threat—anxiety is more diffuse, distal, and likely to persist until the uncertainty is resolved (Grupe and Nitschke, 2013). Accordingly, supervisors who perceive financial insecurity may be preoccupied with their financial circumstances until the insecurity is successfully resolved or brought under control.

In turn, we expect anxiety derived from supervisors’ financial insecurity to hinder their ethical leadership behaviors. UMT suggests that when dealing with anxiety, people devote a great deal of attention to the uncertainty of their situation, and that this focus on stress motivates self-protection behaviors (Lind and van den Bos, 2002). Self-protection involves prioritizing one’s own interests above all others (Kish-Gephart et al., 2010), and research has shown that anxiety can induce self-protective reactions that cause individuals to be less mindful of ethical principles (e.g., Zhang et al., 2020). Specifically related to ethical leadership, some work suggests that ethical and unethical leadership directly contrast with one another because of the tension between altruistic and self-interested motives (Den Hartog, 2015). Therefore, it is likely that when in an anxious emotional state, supervisors compromise the values and norms required for ethical leadership.

In addition, anxiety often acts as a self-sustaining cycle. A common response to anxiety is an increase of focus on the source of the anxiety in an attempt to find solutions or escapes (Eysenck et al., 2007; Pacheco-Unguetti et al., 2010); yet the longer a person dwells on the causes of their anxiety, the more intensely they perceive the associated threat (Mathews, 1990). This then triggers the rapid engagement of mechanisms to defend, escape, or avoid danger to the self. Anxiety induced by perceived financial insecurity is no different (Hermans et al., 2011), and the inclination to rapid defense is to the detriment of ethical decision making (Kouchaki and Desai, 2015). Indeed, research has shown that the anxiety induced by economic difficulties leads to emotional responses that erode moral reasoning (e.g., Lu et al., 2020). In particular, individuals feeling anxious tend to focus narrowly on coping with the threat and, in so doing, pay less attention to ethical principles (Lu et al., 2020). Thus, when faced with a threatening situation such as financial insecurity, anxious supervisors will be more likely to compromise their ethical standards by prioritizing their search for means to reduce their anxiety and avoid further uncertainty over their commitment to integrity and rationality (Brown et al., 2005). In sum, we argue that the anxiety resulting from supervisor financial insecurity will likely inhibit ethical leadership behaviors:

Hypothesis 1: Supervisor financial insecurity is negatively and indirectly related to ethical leadership via supervisor anxiety.

Organizational pay fairness as a moderator

UMT further posits that as people respond to uncertainty, they seek information in the broader work context to help them cope with it (van den Bos and Lind, 2002). In UMT terms, fairness-related information is an essential means through which people mitigate the deleterious effects of uncertainty (Lind and van den Bos, 2002). Along this line, we propose that in the context of financial insecurity, organizational pay fairness will serve as an essential boundary condition that moderates the indirect relationship between supervisor financial insecurity and ethical leadership via supervisor anxiety. Organizational pay fairness describes the assessment that outputs (e.g., rewards, punishments, and salary) relative to inputs (e.g., working hours, educational background, work experience, and job responsibilities) are adequately balanced among organizational members (Adams, 1965; Kim et al., 2015). We focus on perceived pay fairness in the organization rather than the actual level of pay because research has shown that it is the former that most strongly drives decision making and behavior in the workplace (Fong, 2010; Wade et al., 2006).

Perceived pay fairness signals a generic sense of fair treatment regarding pay and the allocation of financial resources in the organizational context (Lind and Tyler, 1988; Tangirala and Alge, 2006). It not only conveys to supervisors that they are valued (Lind and Tyler, 1988; Shin, 2016; van den Bos and Lind, 2002), but also indicates a clear and fair standard that they can use when mobilizing resources and inputs to improve their financial situations. This social information helps supervisors maintain a sense of control over their circumstances (van den Bos and Lind, 2002). According to UMT, people are less likely to experience anxiety when insecurity about the future is mitigated by the perception of fairness, because organizational pay fairness enables them to more accurately predict and exercise control over their financial future.

In contrast, when organizational pay fairness is perceived as low, supervisors’ rates of inputs and outputs may be perceived as unfavorable compared with others (Kim et al., 2015). Research shows that unfair payment exacerbates the uncertainty of financial conditions because organizations do not provide a stable rule for supervisors to rely on in predicting and accounting for their future financial capabilities (Shin, 2016). In this regard, organizational pay fairness acts as a yardstick for estimating both current and future paychecks, as well as financial circumstances in general (Fong, 2010). Thus, financially insecure supervisors are more likely to experience anxiety when they perceive pay unfairness because they are less able to predict their future income even should they change their inputs by working harder or for longer hours (Kim et al., 2010). Such unpredictability and lack of control embedded in perceptions of low pay fairness can exacerbate the feelings of anxiety that result from supervisor financial insecurity, leading to the following hypothesis:

Hypothesis 2: Organizational pay fairness moderates the positive relationship between supervisor financial insecurity and supervisor anxiety, such that this relationship is weaker when organizational pay fairness is high rather than low.

Given that we predicted that supervisor anxiety will mediate the negative relationship between supervisor financial insecurity and ethical leadership (Hypothesis 1) and that the relationship between supervisor financial insecurity and supervisor anxiety will be moderated by organizational pay fairness (Hypothesis 2), we also expect that organizational pay fairness moderates the indirect relationship between supervisor financial insecurity and supervisor ethical leadership. This suggests a moderated mediation pattern as hypothesized below:

Hypothesis 3: Organizational pay fairness moderates the indirect relationship between financial insecurity and ethical leadership via supervisor anxiety, such that this indirect relationship is weaker when organizational pay fairness is high rather than low.

Overview of study methods

We tested our hypotheses in two studies with heterogeneous samples. This multi-study design renders our results and conclusions more reliable, confirmatory, and illustrative of the conceptual model (Tsang and Kwan, 1999). Study 1 tests the main hypotheses using time-lagged data from working professionals (supervisor–subordinate dyads) in China, and Study 2 replicates the findings by accounting for additional sources of uncertainty (e.g., perceived workplace and life uncertainty). This approach is consistent with UMT’s assumption that uncertainty exists in everyday life and manifests in a variety of ways (Alvarez et al., 2018; Milliken, 1987). Our goal was to establish whether financial insecurity is a more powerful indirect predictor of ethical leadership (via supervisor anxiety) than other types of uncertainty.

Study 1

Data were collected from two sources: full-time employees who took a part-time management course through a training organization in China, and their supervisors (front-line managers). These employees came from a variety of industries, including finance, E-commerce, information technology, construction, manufacturing, and petrochemicals. With the assistance of the training organization’s managers, one author introduced the objectives and procedures of this study to the employees enrolled in the course (n = 630). We emphasized that their participation was voluntary and ensured that their responses would be kept anonymous and used for research purposes only. To participate in this study, each employee needed to provide their supervisor’s email address and ask their supervisor to complete our surveys. After one week, 429 employees and their supervisors agreed to participate. Upon receiving their consent, we sent out surveys directly to ensure they completed their respective surveys. After completion, each participant was given ¥30 (about USD 4.3) to demonstrate our gratitude for their cooperation.

The surveys of the subordinates and their supervisors were matched via the supervisors’ email addresses. At Time 1, 362 supervisors (84.38% response rate) provided demographic information and data on financial insecurity, organizational pay fairness, and control variables (i.e., moral identity, perceived top management bottom-line mentality (BLM), perceived organizational ethical culture, and overall organizational justice). We also received responses from 310 subordinates (72.26% response rate) who rated their supervisors’ ethical leadership at Time 1. Three weeks later, at Time 2, 310 supervisors from Time 1 (14.36% attrition rate) provided data on anxiety, while at Time 3 (after another three weeks), 310 subordinates from Time 1 rated their supervisors’ ethical leadership.

After combining the surveys and eliminating data with incomplete responses, we retained surveys from 305 dyads (71.10% response rate). We then screened the data further and identified eight supervisors who had failed our attention check. Therefore, our final sample comprised 297 dyads (69.23% response rate). The supervisors and subordinates were, on average, 40.74 years old (SD = 7.38) and 32.90 years old (SD = 5.54), respectively, and 69% of the supervisors and 54% of the subordinates were women. On average, the supervisors had worked in their organizations for 11.14 years (SD = 7.43), whereas the subordinates had worked with their current leaders for 3.79 years (SD = 2.96). All supervisors held college degrees (12.80% supervisors had associate degrees, and 87.20% had bachelor’s degrees or higher).

Measures

We used a six-point Likert scale (1 = strongly disagree, 6 = strongly agree) for all measures except supervisor anxiety to reduce potential central tendency. All items were written in Chinese. To ensure the accuracy of our written items, we followed the translation and back-translation procedures recommended by Brislin (1980).

Financial insecurity

We used the three items developed by McCubbin and Comeau (1991) and adopted by other scholars, such as Odle-Dusseau et al. (2018), to assess financial insecurity at Time 1. A sample item read as follows: “I seem to have little or no trouble paying my bills on time.” Similar to previous studies, such as Lawrence et al. (2013), we then reverse coded all items to reflect financial insecurity (α = 0.74).

Organizational pay fairness

Organizational pay fairness was assessed at Time 1 using the three items developed by Kim et al. (2015). Each supervisor was asked to think of a colleague with an educational background, work experience, and job obligations comparable to their own. Supervisors were then asked, “Compared with this colleague, to what extent do you perceive the following items are fair to you (1 = extremely unfair to 6 = extremely fair): salary level, the amount of pay, and the opportunity to become financially wealthy?” (α = 0.87).

Supervisor anxiety

We measured supervisor anxiety at Time 2 following Brooks and Schweitzer (2011) and using a five-point Likert-type scale ranging from 1 (not at all) to 5 (extremely). Supervisors recalled the extent to which they felt nervous, anxious, worried, or apprehensive regarding their financial situation over the previous three weeks (α = 0.93).

Ethical leadership

At Time 3, subordinates were asked to rate their supervisors’ ethical leadership for the three-week period following the last survey using Brown et al.’s (2005) 10-item scale. Sample items included the following: “My supervisor sets an example of how to do things the right way in terms of ethics” and “My supervisor discusses business ethics or values with employees” (α = 0.91).

Control variables

Previous studies have demonstrated that supervisors’ gender, age (Brown and Treviño, 2014), moral identity (Mayer et al., 2012), and perceived top management BLM (e.g., Babalola et al., 2020) play critical roles in shaping supervisors’ ethical leadership behaviors. Thus, we controlled for these variables in our analysis. We measured moral identity at Time 1 using Aquino and Reed’s (2002) five-item scale. Supervisors were asked to respond to statements about whether the listed characteristics (e.g., “caring,” “compassionate,” and “kind”) described themselves (α = 0.86). In addition, we measured perceived top management BLM using the four-item scale developed by Greenbaum et al. (2012) at Time 1 (α = 0.82). Additionally, whether a leader demonstrates ethical leadership is likely to be impacted by organizational context, such as the perceived organizational ethical culture (Schaubroeck et al., 2012). Thus, we also controlled for perceived organizational ethical culture at Time 1 using Shin et al. (2015)’s three-item scale (e.g., “Employees in our company are expected to adhere to ethical rules and procedures prescribed by the company”) (α = 0.83). To exclude the potential impact of overall organizational justice on the emergence of ethical leadership, we also controlled for this construct using Ambrose and Schminke (2009)’s six-item scale at Time 1 (α = 0.89). Finally, to further enhance the robustness of our model, we controlled for subordinates’ baseline ratings of their supervisors’ ethical leadership at Time 1 (α = 0.89). Our results were substantively the same with and without all of the control variables.

Analysis and results

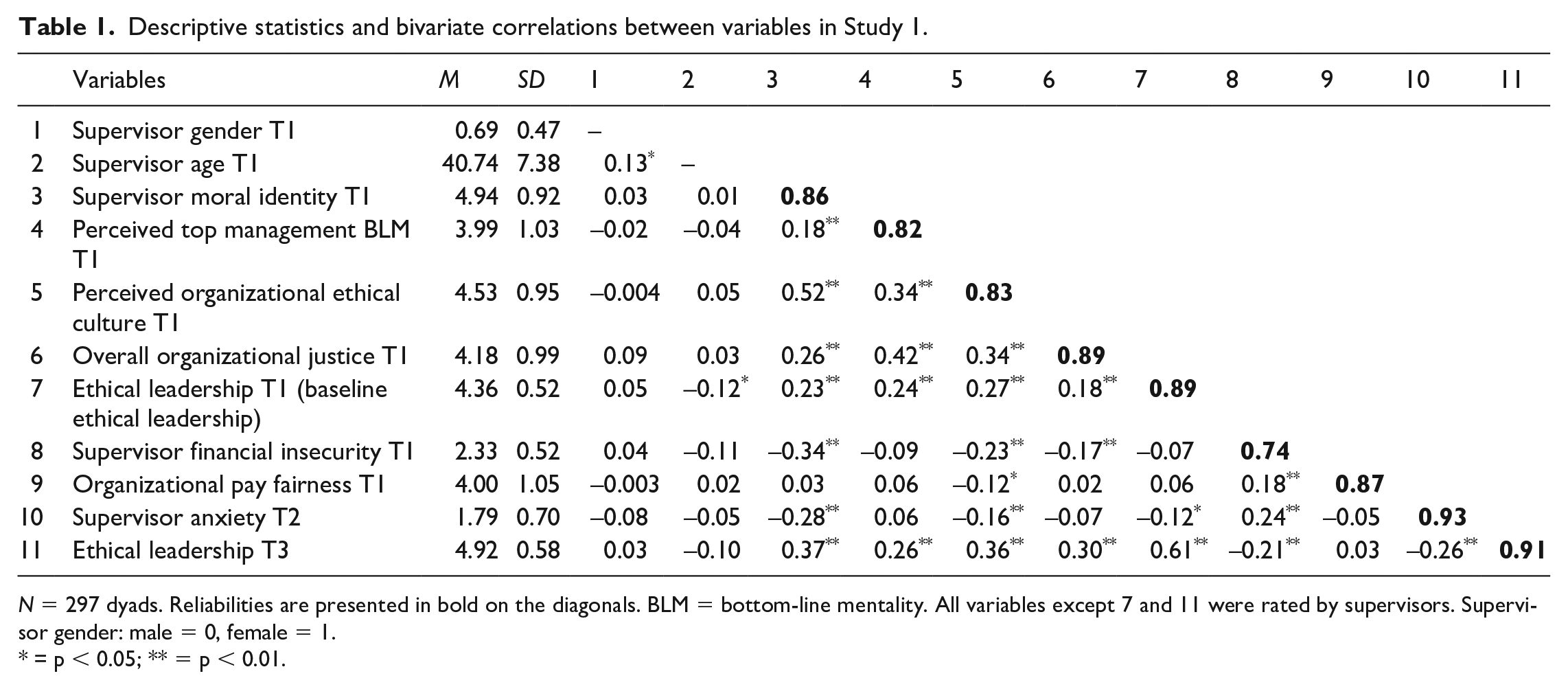

The descriptive statistics, reliabilities, and correlations are displayed in Table 1. All alpha reliabilities were acceptable (0.74 or above; Nunnally and Bernstein, 1994), and all correlations were in the expected directions. For example, supervisor anxiety was negatively associated with ethical leadership (γ = −0.26, p < 0.01).

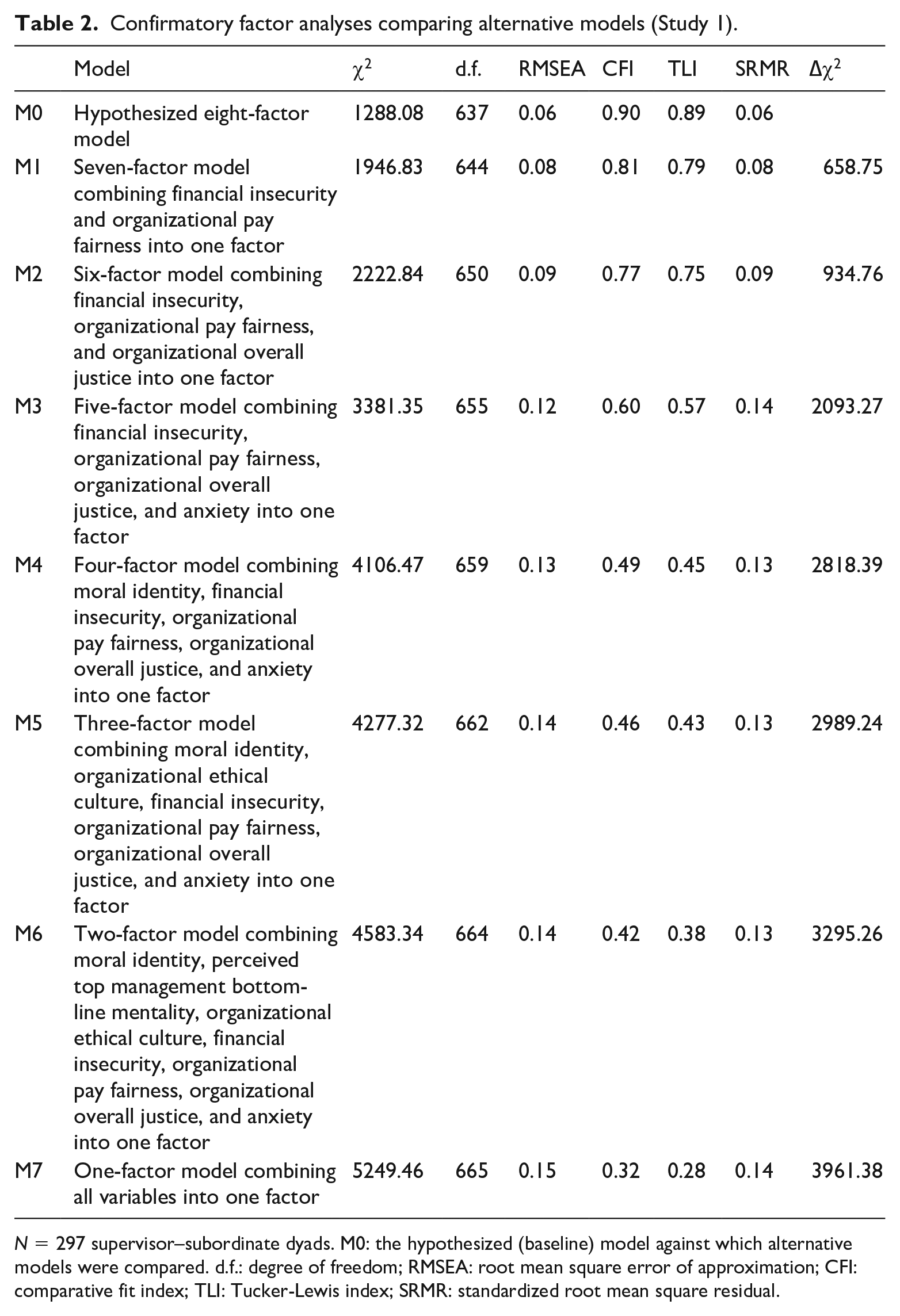

We performed a confirmatory factor analysis (CFA) with maximum likelihood estimation (MPlus 8.0) to assess the discriminant validity of the study variables, including moral identity, perceived top management BLM, perceived organizational ethical culture, financial insecurity, pay fairness, perceived overall justice, state anxiety, and ethical leadership. Our results showed that the hypothesized eight-factor model fit the data well (χ2(637) = 1288.08, p < 0.01; CFI = 0.90, RMSEA = 0.06, SRMR = 0.06) and yielded a better model fit than did alternative models (see Table 2). These results supported the discriminative validity of our constructs. Using measurement invariance testing (Vandenberg and Lance, 2000), we confirmed that subordinates’ ratings of their supervisors’ ethical leadership were measured meaningfully and consistently between T1 and T3 (configural invariance: χ2 = 180.48, d.f. = 73, CFI = 0.95, RMSEA = 0.07, SRMR = 0.09; metric invariance: χ2 = 201.57, d.f. = 82, CFI = 0.94, RMSEA = 0.07, SRMR = 0.10; strong invariance: χ2 = 239.08, d.f. = 102, CFI = 0.93, RMSEA = 0.07, SRMR = 0.11).

Descriptive statistics and bivariate correlations between variables in Study 1.

N = 297 dyads. Reliabilities are presented in bold on the diagonals. BLM = bottom-line mentality. All variables except 7 and 11 were rated by supervisors. Supervisor gender: male = 0, female = 1.

= p < 0.05; ** = p < 0.01.

Confirmatory factor analyses comparing alternative models (Study 1).

N = 297 supervisor–subordinate dyads. M0: the hypothesized (baseline) model against which alternative models were compared. d.f.: degree of freedom; RMSEA: root mean square error of approximation; CFI: comparative fit index; TLI: Tucker-Lewis index; SRMR: standardized root mean square residual.

Hypothesis testing

We tested our hypotheses using Mplus 8.0. Bootstrapping was performed on 5000 samples to yield 95% bias-corrected confidence intervals. We adopted this bootstrapping approach because it provides more accurate estimates of standard errors and confidence intervals compared with traditional methods, such as the Sobel (1982) test (Edwards and Lambert, 2007).

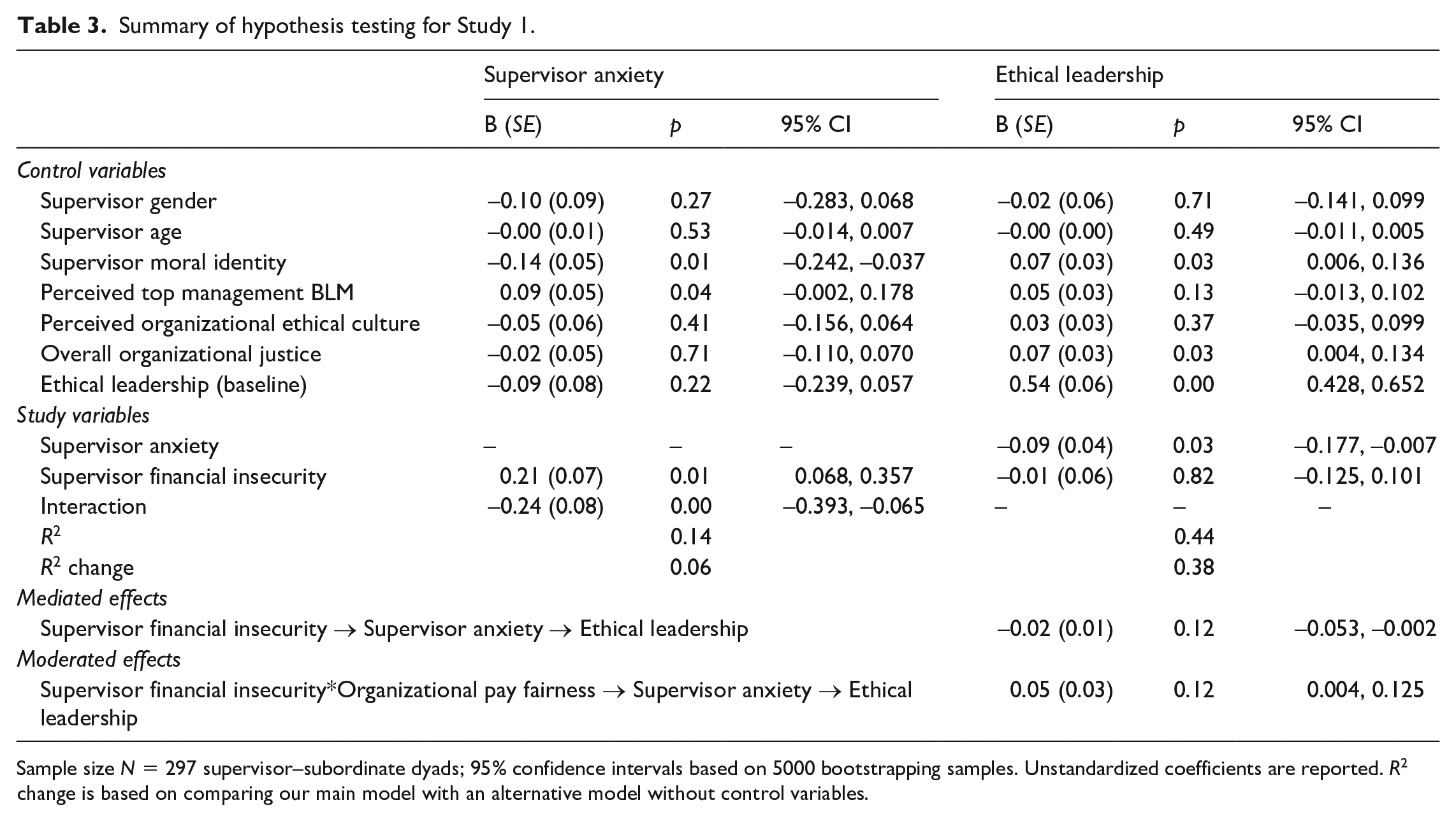

Hypothesis 1 proposed that supervisor anxiety mediates the relationship between financial insecurity and ethical leadership. As shown in Table 3, we found that the relationship between financial insecurity and supervisors’ anxiety was significantly positive (B = 0.21, SE = 0.07, p < 0.01, 95% CI [0.068, 0.357]). Meanwhile, anxiety was negatively associated with ethical leadership (B = −0.09, SE = 0.04, p < 0.05, 95% CI [–0.177, –0.007]). Overall, the indirect effect of financial insecurity on ethical leadership via supervisors’ anxiety was significant (indirect effect = −0.02, SE = 0.01, 95% CI [–0.053, –0.002]). Hence, Hypothesis 1 was supported.

Summary of hypothesis testing for Study 1.

Sample size N = 297 supervisor–subordinate dyads; 95% confidence intervals based on 5000 bootstrapping samples. Unstandardized coefficients are reported. R2 change is based on comparing our main model with an alternative model without control variables.

According to Hypothesis 2, the effect of financial insecurity on supervisor anxiety is moderated by supervisors’ perception of organizational pay fairness, such that the relationship is weaker when supervisors’ perception of organizational pay fairness is higher. As demonstrated in Table 3, the moderating effect was significant (B = −0.24, SE = 0.08, p < 0.01, 95% CI [–0.393, –0.065]). Following the advice of Aiken and West (1991), we illustrated the interaction effect in Figure 2. More specifically, the interaction plot and simple slopes in Figure 2 (+/−1 standard deviation from the mean) suggest that the relationship between financial insecurity and supervisors’ anxiety was weaker at higher (B = −0.04, SE = 0.11, p = 0.72, 95% CI [–0.249, 0.192]) rather than lower (B = −0.46, SE = 0.12, p = 0.00, 95% CI [0.221, 0.685]) levels of organizational pay fairness. These results supported Hypothesis 2.

Interactive effect of supervisor financial insecurity and organizational pay fairness on supervisor anxiety (Study 1).

We proceeded to test Hypothesis 3, which proposed supervisors’ perception of organizational pay fairness as a first-stage moderator in our mediation model. As demonstrated in the testing of Hypothesis 2, the interaction of financial insecurity and organizational pay fairness was negatively associated with supervisor anxiety. In addition, we found that for supervisors who perceived high organizational pay fairness, the link between financial insecurity and ethical leadership via supervisor anxiety was insignificant (B = 0.004, SE = 0.01, p = 0.74, 95% CI [–0.016, 0.031]). In contrast, the relationship was negative and significant for supervisors who perceived low organizational pay fairness (B = −0.04, SE = 0.03, p = 0.09, 95% CI [–0.104, –0.005]). Additionally, the index of moderated mediation was significant (index = 0.05, SE = 0.03, p = 0.12, 95% CI [0.004, 0.125]). Taken together, these results provided clear support for Hypothesis 3.

Study 2

Data were collected from two sources: full-time employees working in China, and their supervisors. These employees worked in industries such as logistics, medicine, investment, retail, advertising, air transportation, and media. With the assistance of a market research firm in China, participants were contacted, and the purpose of the research project was explained to them. We obtained rosters of supervisors and employees interested in participating. These rosters included their positions, supervisor–subordinate dyadic relations, mobile phone numbers, email addresses, and other information. Next, we used Questionnaire Star software to create unique links for each questionnaire and sent them to each participant by email. On the front page of each questionnaire, we explained the anonymity of the survey and promised that the data would only be used for academic research. After completing the survey, each participant submitted it to the online platform directly and received a reward of ¥ 20 (about 3 US$) each time. We obtained data at three time points with an interval of one week. The last four numbers of each participant’s mobile phone were used to match the data across different time points.

At Time 1, we distributed questionnaires to 407 supervisors and 407 subordinates. We received responses from 377 supervisors (92.63% response rate) and 357 subordinates (87.71% response rate). Supervisors provided data on financial insecurity, organizational pay fairness, two measures of perceived uncertainty (workplace uncertainty and life uncertainty), demographic information, and other control variables (moral identity, perceived top management BLM, organizational ethical culture, and overall organizational justice). Subordinates also rated their supervisors’ ethical leadership at Time 1, which served as a baseline control variable. At Time 2, 336 supervisors (10.88% attrition rate) provided data on anxiety, and at Time 3, a total of 286 subordinates (19.89% attrition rate) rated their supervisors’ ethical leadership. After removing all unusable surveys and matching data from the three waves, our final sample included 278 supervisor–subordinate dyads. The average age of the supervisors and subordinates was 39.39 years (SD = 6.37) and 32.92 years (SD = 5.65), respectively. Approximately 45% of the supervisors and 54% of the subordinates were women. Supervisors had been with their organizations for an average of 7.75 years (SD = 5.54), and subordinates had been with their leaders for 3.86 years (SD = 3.28). All supervisors held college degrees (76.60% supervisors had bachelor’s degrees or higher).

Measures

We used the same scale as in Study 1 to measure financial insecurity (α = 0.93), organizational pay fairness (α = 0.96), supervisor anxiety (α = 0.85), and ethical leadership (α = 0.96), and the same set of control variables for consistency. In addition, we measured perceived workplace uncertainty at Time 1 by adapting four items from Colquitt et al. (2012) to the work context. Example items included the following: “Many things seem unsettled at work,” “If I think about work, I feel a lot of uncertainty,” and “I cannot predict how things will go at work” (α = 0.89). Perceived life uncertainty was assessed at Time 1 by adapting four items from Colquitt et al.’s (2012) scale to the life context. Example items included the following: “Many things seem unsettled in my life,” “If I think about my life, I feel a lot of uncertainty,” and “I cannot predict how things will go in my life” (α = 0.92).

Analysis and results

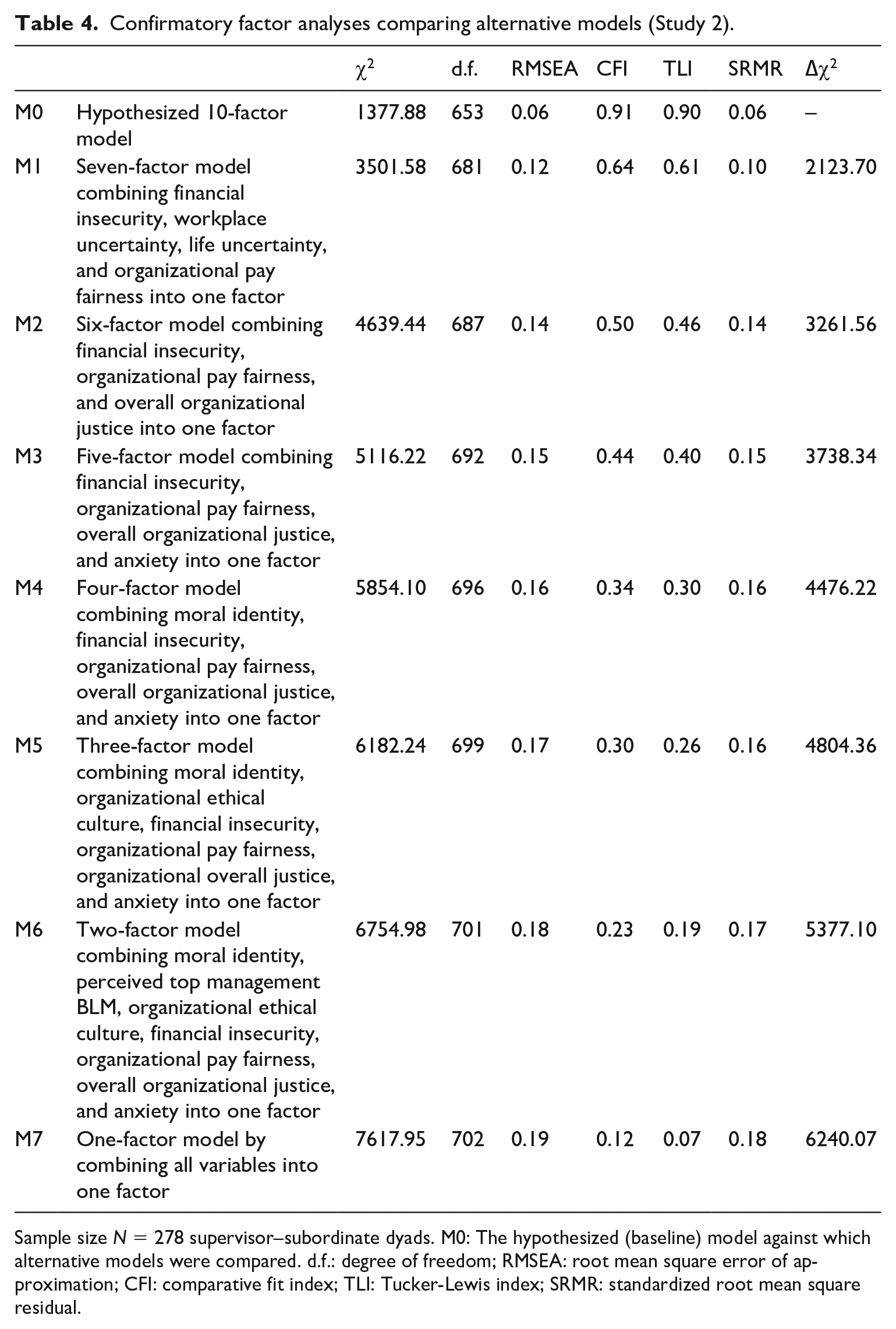

Prior to testing our hypotheses, we estimated a series of CFAs to ensure the discriminant validity of the measurement items. We created three parcels for our measure of ethical leadership to ensure an adequate indicator-to-sample ratio (i.e., to reduce the number of parameter estimates relative to the sample size). Following Little et al. (2013), the first parcel was randomly assigned two high- and two low-loading items, whereas the second and third parcels were randomly assigned two high- and one low-loading items, respectively. Our hypothesized 10-factor model involving financial insecurity, workplace and life uncertainty, moral identity, perceived top management BLM, organizational ethical culture, organizational pay fairness, overall organizational justice, supervisor anxiety, and ethical leadership showed an adequate goodness of fit: χ2(653) = 1377.88, p < 0.001; CFI = 0.91, RMSEA = 0.06, SRMR = 0.06. This model performed better than did all alternative models (see Table 4). Measurement invariance testing confirmed that the subordinates’ ratings of their supervisors’ ethical leadership were measured meaningfully and consistently between T1 and T3 (configural invariance: χ2 = 172.73, d.f. = 78, CFI = 0.97, RMSEA = 0.07, SRMR = 0.04; metric invariance: χ2 = 189.66, d.f. = 88, CFI = 0.97, RMSEA = 0.06, SRMR = 0.04; strong invariance: χ2 = 192.57, d.f. = 108, CFI = 0.97, RMSEA = 0.05, SRMR = 0.08).

Confirmatory factor analyses comparing alternative models (Study 2).

Sample size N = 278 supervisor–subordinate dyads. M0: The hypothesized (baseline) model against which alternative models were compared. d.f.: degree of freedom; RMSEA: root mean square error of approximation; CFI: comparative fit index; TLI: Tucker-Lewis index; SRMR: standardized root mean square residual.

Hypothesis testing

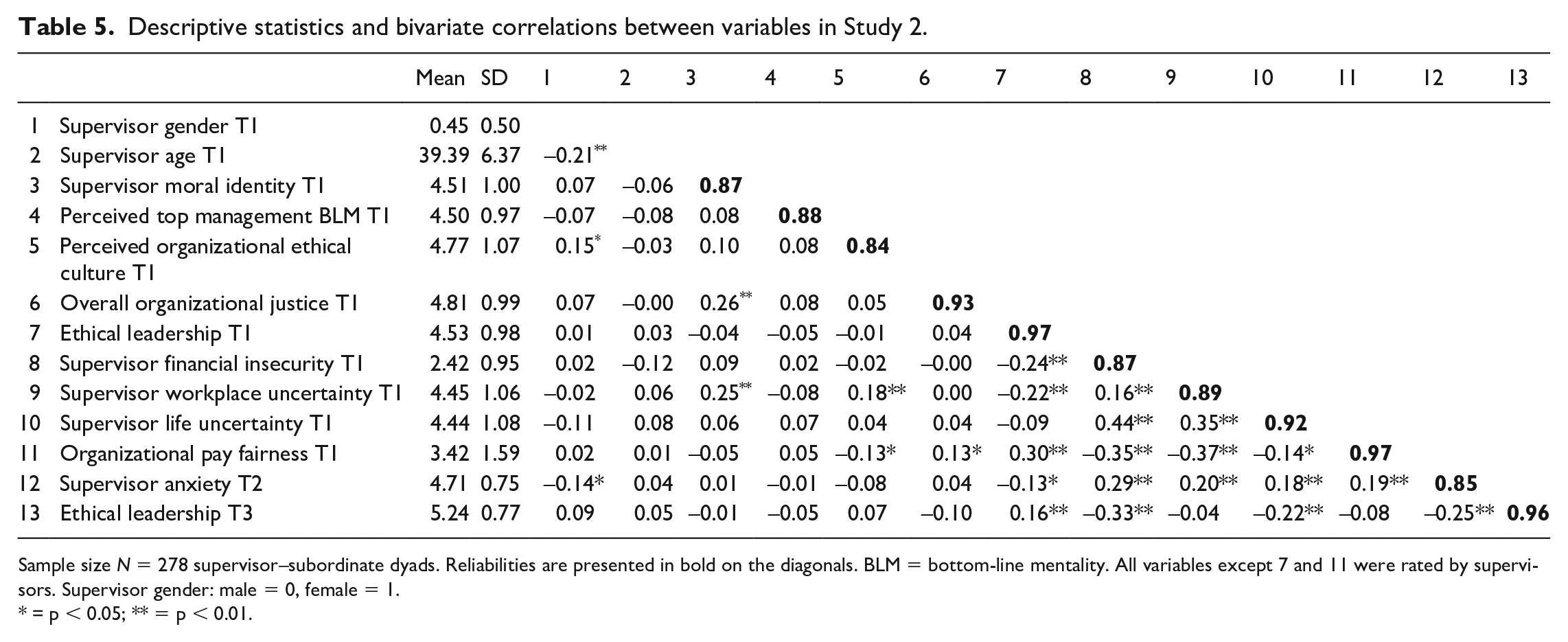

We tested out hypotheses in Mplus using the same analytical approach (path analysis with 95% bias-corrected bootstrapped confidence intervals) as in Study 1, with the exception that perceived workplace and life uncertainty were now included as additional control variables. Table 5 shows the descriptive statistics, reliabilities, and correlations between the study variables, and Table 6 shows the results of the direct, mediated, and moderated paths in our model.

Descriptive statistics and bivariate correlations between variables in Study 2.

Sample size N = 278 supervisor–subordinate dyads. Reliabilities are presented in bold on the diagonals. BLM = bottom-line mentality. All variables except 7 and 11 were rated by supervisors. Supervisor gender: male = 0, female = 1.

= p < 0.05; ** = p < 0.01.

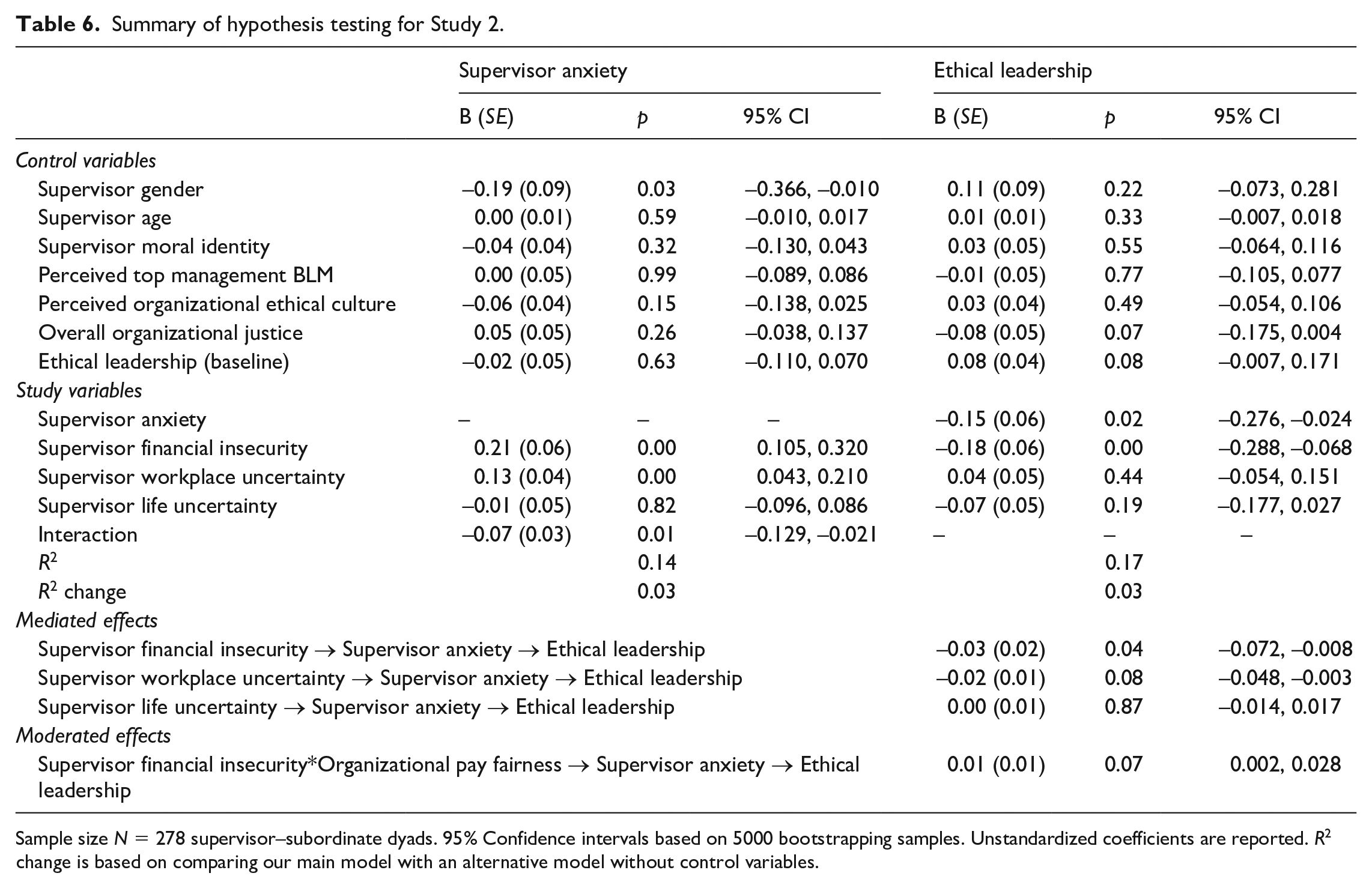

Summary of hypothesis testing for Study 2.

Sample size N = 278 supervisor–subordinate dyads. 95% Confidence intervals based on 5000 bootstrapping samples. Unstandardized coefficients are reported. R2 change is based on comparing our main model with an alternative model without control variables.

As shown in Table 6, the relationship between supervisor financial insecurity and supervisor anxiety was significant and positive (B = 0.21, SE = 0.06, p < 0.001, 95% CI [0.105, 0.320]). Supervisor workplace uncertainty also showed a significant and positive relationship with supervisor anxiety (B = 0.13, SE = 0.04, p < 0.001, 95% CI [0.043, 0.210]); however, the relationship between supervisor life uncertainty and supervisor anxiety was not significant (B = −0.01, SE = 0.05, p > 0.05, 95% CI [–0.096, 0.086]). With regards to ethical leadership, supervisor financial insecurity (B = −0.18, SE = 0.06, p < 0.001, 95% CI [–0.288, –0.068]) and supervisor anxiety (B = −0.15, SE = 0.06, p < 0.01, 95% CI [–0.276, –0.024]) showed significant and negative direct relationships, whereas the relationships involving supervisor workplace uncertainty (B = 0.04, SE = 0.05, p > 0.05, 95% CI [–0.054, 0.151]) and supervisor life uncertainty (B = −0.07, SE = 0.05, p > 0.05, 95% CI [–0.177, 0.027]) were not significant.

The indirect path from supervisor financial insecurity to ethical leadership via supervisor anxiety was significant and negative (indirect effect = −0.03, SE = 0.02, p < 0.05, 95% CI [–0.072, –0.008]), thus providing full support for Hypothesis 1. In contrast, supervisor workplace uncertainty (indirect effect = −0.02, SE = 0.01, p = 0.08, 95% CI [–0.048, –0.003]) had a significant and marginal indirect relationship with ethical leadership via supervisor anxiety, whereas supervisor life uncertainty (indirect effect = 0.00, SE = 0.01, p = 0.87, 95% CI [–0.014, 0.017]) had no significant indirect relationship with ethical leadership via supervisor anxiety. Comparing the magnitudes and statistical significance of these indirect effects, we can deduce that supervisor financial insecurity is a stronger indirect predictor of ethical leadership (via supervisor anxiety) than the other two forms of perceived uncertainty. 1

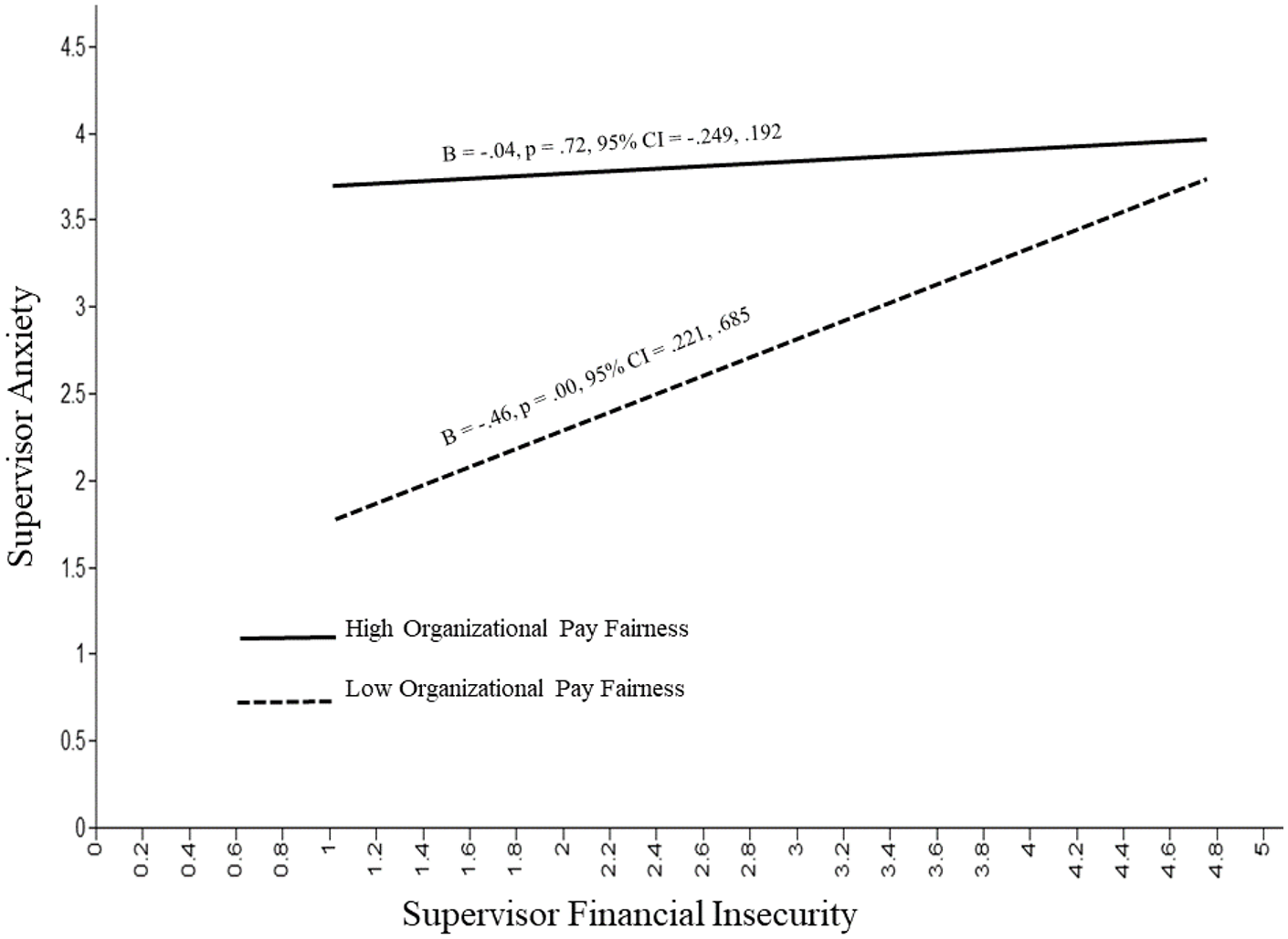

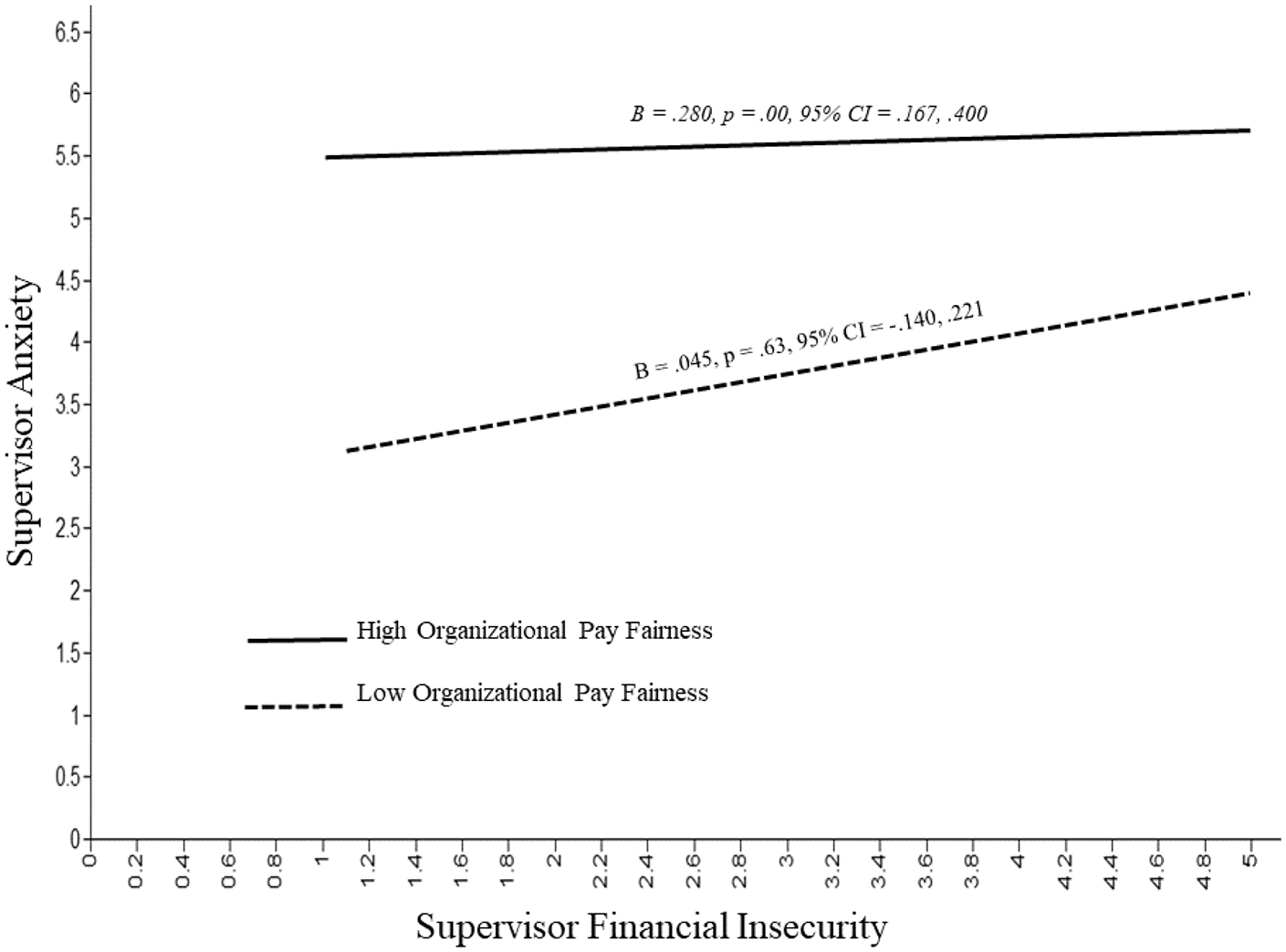

Hypotheses 2 and 3 were examined by adding the interaction term between supervisor financial security and organizational pay fairness to the above path analysis. This was a first-stage moderated mediation model (Edwards and Lambert, 2007), where the magnitudes of the respective indirect paths were estimated to be conditional upon organizational pay fairness. As shown in Table 6, the interaction between supervisor financial insecurity and organizational pay fairness had a significant and negative influence on supervisor anxiety (B = −0.07, SE = 0.03, p = 0.01, 95% CI [–0.129, –0.021]). The interaction plot and simple slopes in Figure 3 (+/− 1 standard deviation from mean) suggest that the relationship between financial insecurity and supervisors’ anxiety was weaker at higher (B = 0.05, SE = 0.09, p = 0.63, 95% CI [–0.140, 0.221]) rather than lower (B = 0.28, SE = 0.06, p = 0.00, 95% CI [0.167, 0.400]) levels of organizational pay fairness. The analysis further revealed that the negative indirect relationship between supervisor financial insecurity and ethical leadership via supervisor anxiety was weaker at higher levels of organizational pay fairness (Index = 0.01, SE = 0.01, p = 0.07, 95% CI [0.002, 0.028]).

Interactive effect of supervisor financial insecurity and organizational pay fairness on supervisor anxiety (Study 2).

Discussion

The assumption that managerial roles inherently impart financial security is increasingly challenged by an evolving organizational reality in which the global economy is undergoing unprecedented disruptions, such as the COVID-19 pandemic and the recent Russia/Ukraine conflicts. As a consequence of these changes, supervisors’ abilities to meet their financial needs now and in the future are becoming unpredictable. This context legitimates the importance of our investigation of supervisor financial insecurity. Across two studies, we drew from UMT to show that supervisors’ financial insecurity is positively related to their state anxiety, which results in a reduction of ethical leadership behaviors. We also found that this mediated relationship is mitigated by supervisors’ perception of organizational pay fairness. These findings make timely and important contributions to both management literature and managerial practice.

Theoretical implications

First, we contribute to the ethical leadership literature by introducing a novel antecedent that hinders its occurrence. Since Brown et al.’s (2005) development of the ethical leadership construct, scholars have predominantly focused on its positive impacts (Bedi et al., 2016; Den Hartog, 2015). However, if ethical leaders produce numerous favorable outcomes for organizations and employees, why wouldn’t all leaders embrace such leadership practices? To this end, we adopt a novel view by proposing that leaders may face impediments that hinder their ethical leadership. Specifically, we add to the limited but growing literature on challenges to maintaining ethical leadership and introduce financial insecurity as a novel factor inhibiting supervisors from embracing the practice of ethical leadership. This stream of research has suggested that contextual factors, such as status threat (Zhang et al., 2020), amoral management (Greenbaum et al., 2015), and top management’s attitudes (Greenbaum et al., 2021), may function as impediments. Though these insights are valuable, they do not speak to the more fundamental needs of supervisors—that is, the security need of fulfilling financial resources (see Deci and Ryan, 2008). Under-specifying the role of financial insecurity risks producing an incomplete picture that constrains the further theorization of ethical leadership.

Consistent with UMT, we introduce financial insecurity as a type of uncertainty and demonstrate the challenges to maintaining ethical leadership from an uncertainty management perspective. This novel lens reveals an alternative explanation to the available ethical leadership literature by showing that supervisors’ financial security can hinder ethical leadership practices. Bringing supervisor financial insecurity to the forefront of ethical leadership research extends the scope of available investigation of ethical leadership (e.g., Greenbaum et al., 2021). Without such a discussion, scholars may be overly optimistic about promoting ethical leadership while lacking awareness of its challenges. Thus, a more comprehensive view of ethical leadership is required not only to recognize its potential impediments theoretically, but also to remind organizations of possible hindrances that may make ethical leadership less likely.

Second, we contribute to the ethical leadership literature by clarifying an underlying mechanism through which financial insecurity relates to reduced ethical leadership. Although UMT is founded on state anxiety as a mechanism for the impact of uncertainty on individual behaviors (Lind and van den Bos, 2002), to the best of our knowledge, no established management studies have fully examined this theoretical foundation. For instance, Thau et al. (2009) described how supervisor authoritarian management style as a type of uncertainty interacted with abusive supervision to exaggerate employees’ deviant behaviors, but they did not tap into the mechanism of such effects. Takeuchi et al. (2012) explored how employees experiencing uncertainty owing to shorter job tenures are less likely to engage in voice behavior, but they did not explore the potential underlying pathways. Similarly, Thau et al. (2007) and Loi et al. (2012) applied UMT without delving into the underlying processes. Building on these endeavors, Wang et al. (2015) first examined work engagement as the pathway for employees’ uncertainty management. However, they did not investigate the root of UMT—that is, the emotional process that drives uncertainty management behaviors. We return to the root of UMT, introduce state anxiety to the occurrence of ethical leadership in our research, and demonstrate its critical and unique influence beyond alternative mechanisms such as intrinsic motivation. In doing so, we not only support the foundation and extend the application of UMT to the ethical leadership literature, but also deepen our understanding of the difficulties some supervisors encounter in embracing ethical leadership from an emotional perspective.

Third, we contribute to the ethical leadership literature by identifying organizational pay fairness as a more robust contextual factor for understanding ethical leadership, especially after controlling for several notable alternative explanations (e.g., moral identity) that may influence ethical leadership (Mayer et al., 2012). Our results reveal that, as a crucial organizationally embedded factor that attenuates the indirect effect of financial insecurity on ethical leadership, pay fairness is especially desirable in financially troubled times. Its impact goes beyond overall organizational justice, as it is not the actual payment that mitigates financial insecurity, but rather the perception that organizational policies on payment are fair. 2 We thus introduce a novel contingency—pay fairness—to the literature on ethical leadership. Although studies on pay fairness have been prevalent in the justice and human resource management literature (Kim et al., 2019; Marescaux et al., 2019; McFarlin and Sweeney, 1992; Soltis et al., 2013), our study demonstrates that its impact goes beyond these fields and affects how leaders respond to uncertainty, therefore ultimately shaping ethical leadership behaviors. This further emphasizes that in trying times when organizations tend to reduce expenses to survive crises or structural changes, it becomes even more important to prioritize pay fairness in order to maintain ethical leadership. In so doing, our research addresses the call to incorporate financial situations into organizational behavior research (Leana and Meuris, 2015), and suggest there may be profound benefits in incorporating issues of pay fairness into leadership research more broadly.

Finally, our work also contributes to the emerging literature that seeks to understand the implications of financial insecurity in the workplace. To date, researchers have predominantly investigated the consequences of employee financial insecurity (e.g., Lawrence et al., 2013; Odle-Dusseau et al., 2018; Sharma et al., 2014), with almost no studies examining the effects of supervisor financial insecurity. Supervisors are an important part of organizational leadership in that they interpret top management expectations and provide day-to-day directions to front-line employees (Yukl, 2006). As our findings demonstrate, supervisor financial insecurity can inhibit ethical leadership behaviors, which will eventually impact employees via leader influence and daily leader directions. Therefore, compared with employee financial insecurity, which solely impacts employee behaviors, supervisor financial insecurity entails double costs that impact both supervisors and employees in the workplace.

Practical implications

Our study has important implications for managerial practice. First, we highlight the far-reaching consequences of financial insecurity for supervisors. Specifically, we demonstrate the effect of financial insecurity via anxiety on supervisors’ ethical leadership. The implications of ethical leadership can be quite rewarding for organizations (Bedi et al., 2016; Den Hartog, 2015). Our work suggests that supervisors may behave less ethically in the workplace as a result of their own financial insecurity. Our findings thus suggest the need for organizations to offer adequate financial packages to supervisors to the extent that the organization’s financial situation allows. Alternatively, organizations can offer financial management training such as retirement fund management, and financial services such as tax consulting, from which supervisors can learn how to effectively manage their savings and wisely plan their expenditures and retirement funds (Anderson et al., 2004).

Second, our study highlights the critical role of organizational pay fairness beyond other factors such as overall organizational justice in helping supervisors mitigate their negative reactions to financial insecurity. Because pay fairness relies on effective human resource management systems (Barber and Simmering, 2002), it is important for organizations to ensure that supervisors are remunerated fairly. These efforts can relieve anxiety and ultimately cultivate leader ethical behaviors. Thus, our work suggests that financial insecurity is not a mere private/individual issue but an issue that organizations can address by building and improving fair pay systems (Barber and Simmering, 2002). One means to this end is transparent policies on pay fairness. Organizations can inform their employees about how their pay compares with relevant others both within and outside of the organization. Clear policy statements are required not only to avoid misunderstanding or confusion by supervisors over their current and future financial packages, but also to ensure that supervisors have financial predictability and thus better control over their financial state. To this end, organizations can also create hassle-free, confidential, and anonymous feedback channels through which supervisors can safely express their feelings and concerns about the fairness of the organizational pay system. The feedback received can provide organizations with suggestions to improve their pay systems (Dulebohn and Martocchio, 1998).

Finally, our findings regarding the role of anxiety in transmitting the effect of financial insecurity on ethical leadership suggest that organizations must better assist supervisors in attending to and regulating their negative feelings. Specifically, training programs such as meditation and counseling can help supervisors practice emotional regulation to better manage their anxiety (Hülsheger et al., 2013; Kumar et al., 2008). Developing such remedies may promote supervisors’ ethical influence on subordinates (i.e., ethical leadership), which is important for organizations given the benefits of ethical leadership (Bedi et al., 2016).

Strengths, limitations, and future research directions

The present study has several strengths. For example, we tested our theoretical model using data collected from two sources and separated our measurements in time. We also examined the effects of supervisor financial insecurity on ethical leadership while controlling for previously established antecedents (e.g., moral identity and top management BLM) and ruling out the possible influence of organizational ethical culture or other types of uncertainty. These enhance the robustness of our findings and our contributions to the literature.

Despite these strengths, we acknowledge several limitations that also point to avenues for future research. For instance, our field study design cannot provide causal inferences. To reduce this weakness, our theoretical model was guided by UMT’s suggestion that perceived uncertainty along with fairness information provoke anxiety and influence subsequent behaviors. Consistent with our theoretical model, we collected data at three points in time. Additionally, our measures were rated by both supervisors and subordinates to reduce common-method variance concerns (Podsakoff et al., 2003). We also instructed supervisors to report their state anxiety at Time 2 with regard to their perceived financial insecurity at Time 1 and controlled for ethical leadership at Time 1. Despite these efforts, we are cautious about making causal claims. Thus, we encourage future studies to conduct experimental designs to better establish the causal direction of our proposed relationships.

Conclusion

Despite scholars’ growing interest in the antecedents of ethical leadership, little attention has been paid to impediments, such as financial insecurity, that supervisors may face in maintaining ethical leadership. In this regard, our study investigates whether supervisor financial insecurity hinders ethical leadership behaviors. Drawing on UMT, our work highlights supervisor anxiety as a key mechanism for the association between financial insecurity and reduced ethical leadership. We further demonstrate that organizational pay fairness effectively mitigates the indirect association between supervisor financial insecurity and ethical leadership. We hope our research opens additional avenues for future studies to explore the effects and boundary conditions of financial insecurity on supervisor behaviors in the workplace.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: National Natural Science Foundation of China (grant nos 72072019, 72102220, 72174096, and 72132009), the Fundamental Research Funds for the Central Universities of China (grant no. ZYGX2020FRJH012), and the Research Innovation Fund Project of CWAS of UESTC accredited by Ministry of Education, China (grant no. CXJJ2022072702).