Abstract

The COVID pandemic has ravaged the economic health of all countries round the world. This work is a commentary on the scale of the impact the disease has created on the economy and how the country has responded to the challenge. It looks into the interventions of the government as well as their possible implications on the macroeconomic health of the country. We have also suggested measures that could assist in redeeming the economic health and bringing out the vulnerable businesses from existential crisis.

Introduction

They say it’s a once-in-a-century event (Tedros Adhanom Ghebreyesus, WHO Director-General on 3 August 2020) and the modern-day healthcare and economic systems across the world are being tested each day for their resilience in fighting the war with COVID-19. While the health tragedy was responded with travel and meeting restrictions from governments across the world, the resultant economic shocks are likely to surpass any other crisis experienced since decades. As scientists and drug companies scamper to produce the treatment every country is desperate to lay its hands on, the World Bank envisages a bleak outlook for the global economy. In its June 2020 edition of Global Economic prospects, it had envisaged an over 5% contraction in global GDP in 2020, which is a staggering erosion in spite of a spate of fiscal and monetary support measures announced by the governments all over the world. The fallout has primarily been attributed to the huge job losses, insolvent businesses and disintegration of global trade linkages. The virus has shown no signs of receding, and vulnerable economies in the developing economies are finding it difficult to ramp up the healthcare system with falling revenues and increasing incentives. The journey to sustained economic growth seems distant as the threat of millions of people plunging back into poverty seems to undo the progress achieved in decades of implementing systemic reforms.

While the oil prices shocked the world, supply chain disruptions in agriculture and allied food sectors have dented the food sector’s growth. The tourism, hospitality and entertainment sectors have borne the major brunt, and they are likely to see the slowest recovery. Investments in these sectors by micro units are majorly financed by banks who would be staring at huge NPAs in this otherwise robust performing sector. The analysts cannot figure out the implications till there is a clear indication of how long the pandemic would continue and there are evidences of periodic disruptions. While these informal sector units may not contribute very heavily to the overall GDP, they contribute hugely to employment and their distress would have a cascading effect on the demand patterns. While the banks introduced short moratoriums based upon their short-term assessment of the situation way back when in the initial stages of the crisis, the way it has panned out so far, comprehensive restructuring exercises will be required with specific interventions for each sector to prevent collapses of very high order. The research and data tools which were used in pre-COVID area have become irrelevant creating further complications for designing policy deliverables for coming out of this economic havoc.

The UNCTAD report (September 2020) states that the impact of COVID on world economy is equivalent of complete destruction of Indian, Brazilian and Mexican economies. In fact, the April–June 2020 data by the Ministry of Statistics and Programme Implementation (Government of India) reveals that the Indian economy shrank the most among all big economies of the world. The USA and Italy economies were hit by 9% and 18%, respectively, while India has taken a plunge of over 20% which does not include the large informal sector. One solace was that the agriculture and food sector didn’t collapse as it engages a vast segment of workers on a daily basis. The Utility services and construction sector has witnessed a downward spiral by over 13% while hospitality plummeted by over 10% during the first quarter (statista.com) which had the country into lockdown and the recovery would be painstakingly slow.

India’s Response

The estimates of fall in India’s GDP during FY20–21 range up to 25% and beyond. The substantial job losses due to contraction of small and medium-sized enterprises (SMEs) are likely to plunge significant numbers of population below the poverty line. The migrant crisis witnessed during the lockdown period is evident of the employment crisis expected to unfold by next year. Various state governments have initiated steps to create job opportunities in native areas for these displaced workers, but it cannot be expected to provide a turnaround early and easily. A large section of the workforce in western and southern states in India comprises of migrants from North and Eastern parts of the country. They work in labour-intensive sectors such as construction, hospitality and textiles and survive on daily wages basis. The reverse migration started when their earnings dried up and majority of these workers who used to remit earnings back home are now in dire straits. Centre for Monitoring Indian Economy (CMIE) estimated for an urban unemployment rate over 30% in April 2020. While many economists and social welfare activists have recommended doling out financial aids through monthly credits into the bank accounts of these jobless beneficiaries, it is extremely difficult for the government to sustain such move given the longevity and scale of the crisis. Given the scale of fiscal deficit likely to occur due to falling tax revenue, it will further impede the government’s ability to provide financial relief for a longer duration.

The other aspect of dealing with the wounds of the battered economy is providing a suitable stimulus to uplift the demand and investment deficit. The European Union and the USA have gone ahead with unprecedented levels of bailout packages knowing well that there is no alternative. The funding of such a stimulus is an issue of concern for all the governments across the world. Although the USA and Japan have announced stimuli packages to the size of 11% and 21% of their GDP respectively (Source: Statista.com), it is difficult for countries like India to go for a splurge. The prospective inflation and devaluation of rupee may be a trade-off in deciding how much stimulus can be injected into the economy. There is a silver lining though under the present circumstances. The sharp fall in crude oil prices followed by weakening demand of imports turned India into a net exporter or with a current account surplus for the quarter ended June 2020. This had not happened since March 2007. The downward spiral in the import demands due to halt in production activities as well as lower sentiment has helped in easing the pressure on rupee. This, combined with modest external debt and strong foreign exchange reserves, may help the public exchequer to withstand the burden of required stimulus to a limited extent. The measures announced in India are a mix of fiscal, monetary and regulatory level initiatives. From providing food and direct money transfers to financial sector reforms for farmers and micro, small and medium enterprises (MSME) units, India is looking at both short-term and long-term reforms required for the economy to heal faster once the contagion is kept in check.

The Collapse Indicators

Looking at the population density and crippled health infrastructure, especially in semi-urban and rural areas, the death toll due to COVID-19 spread was projected to be at alarming levels by naysayers with some estimates running into millions of deaths. However, those predictions by some elite institutions have proved to be way off the mark. After more than six months of the encroachment of the virus into the country and recovery rate of over 75%, the casualties are far below these forecasts. The fatality rate at below 2% of those infected has been one of the lowest in the world, and the patient recovery rate has ensured that the infrastructure created so far is more than adequate to handle future requirements. The stock market crashed in panic due to uncertainty and fear of long recession but has since been steadily recovering from the historic lows in March 2020. Many sectors including automobile are now struggling to reach pre-COVID levels even though recurring lockdowns are threatening to derail the progress again. However, sectors like aviation, cinemas, restaurants, hotels, entertainment and fitness centres, live events including sports, training institutions and public transport are all badly affected and still waiting for the light to emerge in the dark tunnel they have been relegated to.

During the budget presentation for FY20–21, the nominal GDP forecast was pegged at a modest 10%, which now appears to be surreal. Global investment banks and rating agencies are now discounting that expectation by more than 80%. The key impact of the crisis is densely concentrated around the following factors.

Weak Demand

A steep fall in non-essential consumption owing to falling incomes, uncertainty about longevity of the crisis, disruptions in supply chain and poor sentiment has led to the contraction in demand. The top lines for both domestic as well as international markets are severely impacted. Since the consumption demand has dwindled, the economists have suggested the government to aid in creating demand by way of investment in infrastructure, introducing tax incentives, and direct fund transfer in beneficiary accounts. This would bring fiscal imbalance, but that has to be taken out of consideration for these extraordinary times and even reaching up to 10% of GDP would not be unreasonable. Demand and investment by the private sector are independent and although severe contraction is still being considered as a short-term phenomenon, but the longer it takes for health situation to normalise, the longer will be the impact of recession.

Choked MSMEs

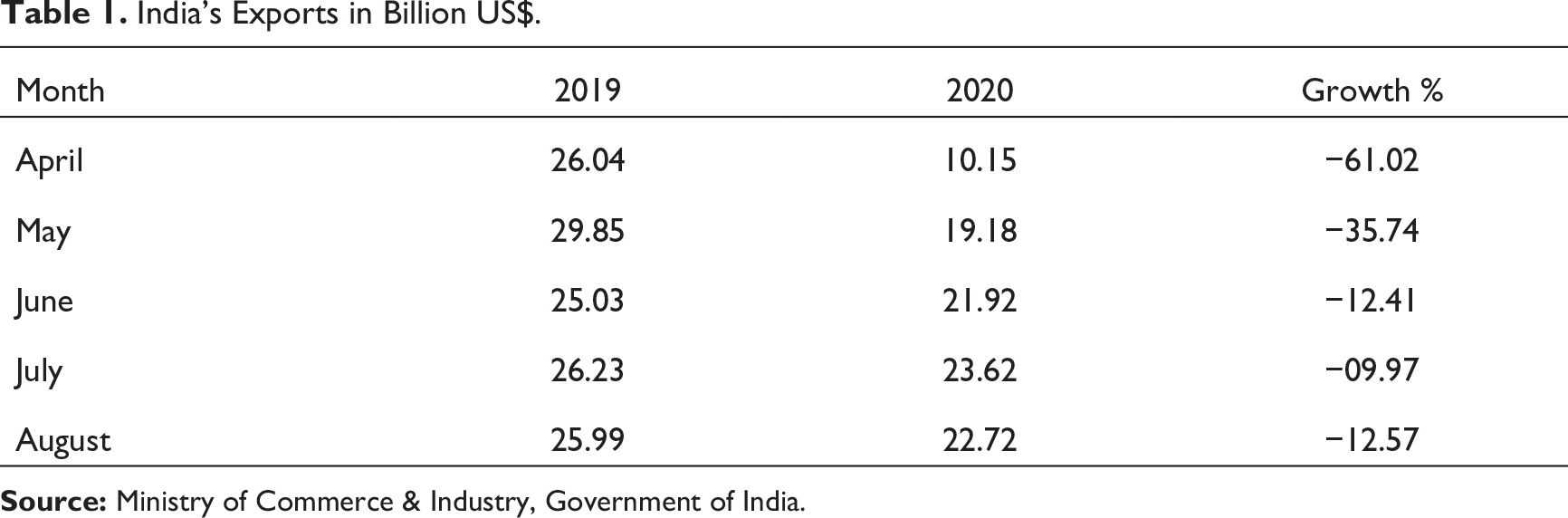

India’s Exports in Billion US$.

India’s Exports in Billion US$.

The revenue generation has been at a standstill and since the whole sector mainly runs on debt-based capital, the ever-accumulating bank dues, especially on the term loan instalments, might threaten the existence of many of these. RBI has already formed a committee and asked banks to liberally go for loan restructuring options, but traditional interventions will not help the sector, and there needs to be at least two to three years of handholding support. The restructuring terms have to be liberal and banks should be allowed to exercise their credit monitoring and NPA recovery activities with prudence so that they do not stifle the business operations and in turn reduce their own asset quality.

Subdued Foreign Trade

The June 2020 quarter which saw many countries across Europe as well as USA and China battling with infections and strict lockdowns resulting in around 27% decrease in international trade in goods(UNCTAD Global Trade Update on June 10, 2020) with the figure for South Asia as high as 40%. The reduction in supply of intermediate goods from China is also likely to impact global output. The WTO has further projected up to 30% decrease in overall merchandise trade for 2020. Various countries had imposed restrictions on trade movements in the June 2020 quarter post which there has been some easing but economic ravages have resulted in drying up of demand. To top that, international cargo has become expensive as passenger flights are disrupted which has limited transport capacities. Other supply chain disruptions include strict protocols, increased documentation and quarantine measures at various ports leading to unwanted delays and increase in costs. Labour availability has also been an issue due to lockdowns as public transport was shut in cities. Overall, the slump in exports hampered operations and financial stability severely in the second quarter of 2020, and difficult working conditions at present may render these firms uncompetitive in challenging international market.

Restrictions in Service Sector

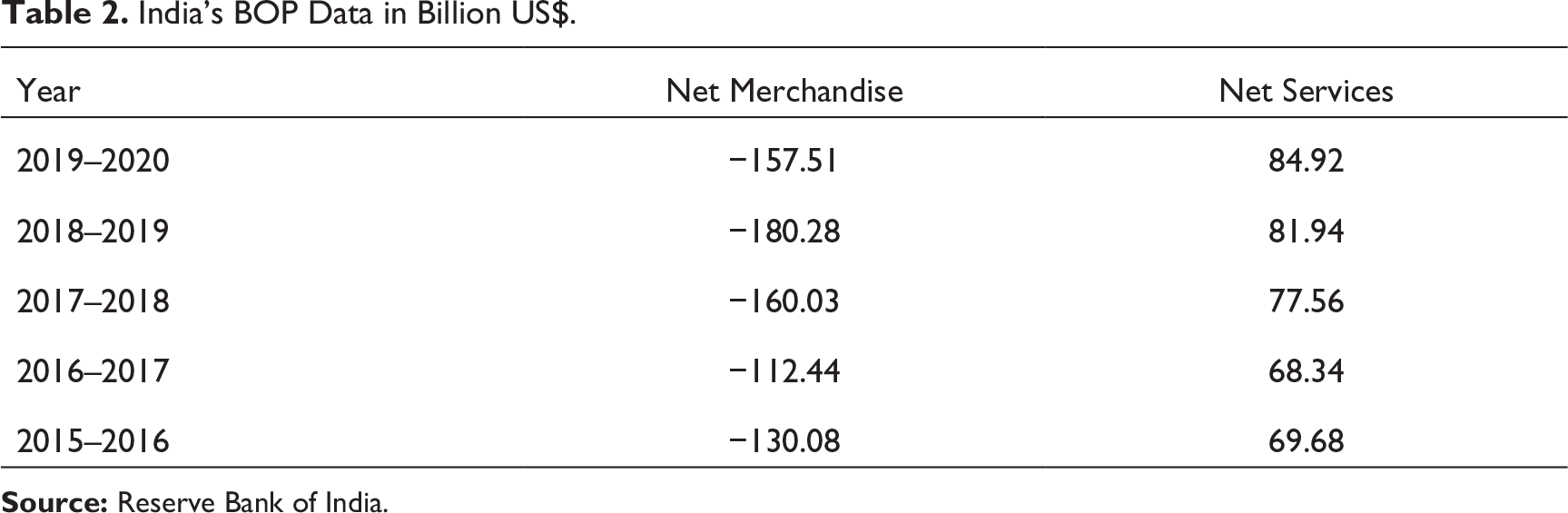

India’s BOP Data in Billion US$.

Many businesses in the service sector were one of the first to be forced to shut down early March and will be the last to open doors to customers. While the opening is uncertain, the bigger worry is the time the customers will take in gaining confidence in paying for these services. Restaurants have slightly recovered with takeaway services as major food delivery operators have reported sales to be slowly inching towards pre-crisis levels. However, dine-in customers, who are the mainstay for majority of the outlets, are almost negligent. Hospitality and Tourist travel firms in the north and eastern part of the country lost the lucrative summer while the west and south locations are looking at a dull winter season. The vehicle loans for the travel companies as well as those providing transport to schools, colleges and offices are in substandard category. Cinemas are waiting to open the door for patrons as a slew of films take the alternate route of releasing over the OTT platform creating a content crisis for the theatre distribution circuit. It will be a long time indeed when crowds will throng the cinemas and the government is not likely to permit them to operate with existing seating arrangements and some structural changes may be required. Also, the income from refreshments is also likely to drop with apprehension towards unpacked food items. Other recreational activities such as live concert performances, fairs and sports with packed audiences also seem to be a distant reality.

The Oxford Coronavirus Government Response Tracker (OxCGRT) at the University of Oxford has been tracking the government responses the world over on various parameters hinging around three broad areas: restrictions for containment, health investment and economic revival. Although it does not have data on India but the broad interventions across the globe show the uniformity in approach by various governments with Europe, China and Australia taking the strictest measures. While India chose to go for tough lockdown during the primary stage to build capacity for health infrastructure, the migrant travel issue grabbed headlines. The reverse migration turned out to be a humanitarian and economic crisis following which various state governments across the country. In line with other countries, the government went ahead with an announcement of a large relief package, which focused on direct transfers to farmers, increase in MNREGA wage rates and support to MSMEs. The major interventions included provision of ₹300,000 crores to fund collateral free loans for around 4 million units as well as subordinate debt for handholding distressed SMEs having the potential to expand. The micro unit investment limit has been revised substantially upwards and no differentiation made between service and manufacturing sectors. Another promotional move has been to reserve tenders up to ₹200 crores exclusively for domestic players so that they do not have to worry about foreign competition. Statutory EPF deduction by employers has been brought down to 10% from existing 12% to curtail expenses. Since MSMEs thrive on fairs and exhibitions for networking, promotion and sales, it is vital to create alternate channels in view of present circumstances. The government is promising them e-linkage and an early payment of dues by the PSUs for tiding over cash crisis. Large amount of funds have been earmarked for creating infrastructure towards enhancing food processing and horticulture value chain.

A key element of intervention from the government has to be towards strengthening financial institutions lending to small businesses and retail borrowers so that they are not wary of making fresh inroads into the market. A scheme to provide additional liquidity to the tune of ₹30,000 crores to non banking finance companies (NBFCs) and housing finance companies (HFCs) through an special purpose vehicle (SPV) is therefore in the pipeline. The RBI would buy debt instruments from the SPV who in turn would use the funds to buy stressed assets from the NBFCs and infuse liquidity into the sector for acquiring new business. In addition to this, a partial credit guarantee scheme has also been worked out for the finance companies. Similar liquidity injunction to the size of ₹90,000 crores is being worked out for power distribution companies so that they can make onwards payment to power producing companies. This will be done by providing them funds against their receivables from state corporations. All the public sector contractors would be given extensions on completing projects without imposing any penalty while real-estate developers be given extensions on due dates for all projects. The small loans under ‘Shishu’ category of Mudra financing scheme will get interest subvention to lower the hardships for the most vulnerable category of borrowers.

Challenges to Recovery

Looking at the approach towards lowering the catastrophic damages of the ongoing economic crisis, it appears clear that systemic interventions have been introduced which can bring long term benefits to businesses which survive and continue to thrive. However, there are many businesses which have acquired structural weaknesses due to the prevailing situations in the last six months due to which they will not be able to avail the benefits of these interventions. This is especially applicable to units operating in the service sector as detailed earlier in this discussion. Their operations have been disrupted to a limit beyond normal redemption and are bound to collapse if they have debt burden. They will also impact the banks having exposure on them. Giving them fresh lending opportunities is not likely to help much. Office retail spaces are shrinking owing to vast majority of companies opting for work from home options, hotels and vacation spaces are looking at long road to revival of customer confidence. Similarly travel, cinema, etc. are sectors bleeding with mounting losses and a long period of depressed top line. They will need large scale restructuring with impactful tax reliefs for a substantial time period.

Much of the shock in the services sector is due to its informal nature that operates with daily demand from people at work. Their customers are relegated to staying at home or preferring to minimise spending leading to drying up of revenues. Many of these were served by the microfinance companies which are now likely to come under stress. Government interventions flowing through banking channels are not likely to give them much relief. The bigger firms however are likely to benefit from the package and tide over only if they are not highly leveraged. The steady fall in revenue due to consumer’s demand shift along with fixed costs liability is likely to further stress them. In similar situations, the western world has seen corporate bailouts by the government like the financial crisis in 2008.

The banking sector in the pre-COVID era was already reeling from stressed assets and RBI was pushing banks for the cleaning up act. The mergers of PSUs were also aimed at driving synergies and cutting flab but the longevity of the present crisis is threatening to undo all the progress made. Alarming levels of NPAs had already forced the banks to be extremely cautious in granting credit but post-COVID period, the credit monitoring for existing accounts as well as processing fresh proposals will be very challenging. Many vulnerable firms would have to pay the price for it. Since much of the government support package is likely to be routed through the banking channel, it is all the more important to ensure that the banks are in good shape. It was already becoming difficult for the government to provide additional capital for implementation of Basel 3 norms across the banks. Now the fresh provisioning requirements for substandard assets will be a big headache. The RBI has to relook into its options for capital adequacy. The present crisis is a double whammy for banking as neither are they well capitalised nor the government is in a strong position to support them owing to its own fiscal limitations.

The Road Ahead

With no parallels in the distant memory, the system does not have the experience to glide over the economic trauma inflicted by the COVID calamity. The reactions may be piece-meal, staggered, impulsive or well-planned but the outcomes may be far from intended. The economy does need a push up from the government, but it should be targeted towards strengthening the system and making way for bold moves. Some of the possible measures that can be put into consideration are the following: The historic lows in oil pricing couldn’t have come at a better time, and the government has not passed the benefit to the users. Instead of using it as a compensation for improving fiscal imbalance, the surplus should be directed towards funding the host of relief packages aimed at unemployed small workers and distressed micro finance units. The budget deficit may not be put as a cause of concern and countries around the world are doing it, and hence, there will be no serious relative impact in the long run if the fundamentals of the economy are kept intact. Putting great weight behind the banks and microfinance institutions to enable them to roll out vanilla products in collaboration with social development agencies. Bankers alone might not be able to lend confidently during the present stressful circumstances but there are a range of activities that are now finding market stability which can be ideal for small ticket advances. State- or district-level bankers committees can identify partners who can help them scout and develop bankable projects and send standardised proposals to branches with a post sanction monitoring support of three years. Low inflation is usually predicted in such times which can help RBI to introduce further rate cuts to bring down cost of capital for small businesses. Income tax rates may be relooked as a tool to revive consumption demand at least for the present financial year. Interest waivers and credit guarantee scheme for expansion of MSME units which have continued operations with at least 50% activity post lockdown. This is essentially required to lower cost of credit and infuse capital into well-performing units. Using a product on lines of MNREGA for urban centres to bring in as many workers as possible from the informal sector that lost jobs during the pandemic. It can be directed at taking on projects not conflicting with social distancing and other measures required during the health crisis. Standard layout of broad activities in sanitation, waste disposal and infrastructure creation may be designed so that they are in full swing as soon as the situation improves. The silver lining during the whole crisis has been rejuvenation of physical environment, and it has shown how climate sustainability can still be restored. The government and the institutions should bring in environmental stability back into business as statistics have shown more people in India die of poor quality of air and water than possibly any virus.