Abstract

Indian direct tax collections have remained sluggish over the period coupled with the lesser tax buoyancy have compelled the government to collect revenues from the untapped or under-tapped sources to finance the galloping expenditure such as the health and defence. To achieve the fixed money value targets the taxmen have been putting excessive pressures on the taxpayers who have created a panic, likely to tantamount to infamous tax terrorism and tax disputes have arisen blocking substantial tax revenues in litigations. Taking this in to cognisance the government has attempted to rationalise the tax system by introducing tax amnesty scheme such as the Vivad-se-Viswas and by launching a Faceless Assessment Scheme (FAS) and tax charter, which is likely to address the tax disputes significantly. To increase the revenue, the best approach for the government is to broadening the tax base, reducing the tax rates, rationalising the tax system, formalising the unorganised sectors and by enhancing the lower household incomes substantially in lieu of serving notices to the non-filers is the need of the hour.

The Context

Kautilya had written in the Arthashastra (150 AD) that revenues should be collected to increase the incomes as well as to reduce the expenditure, which has its relevance and reflections in the Indian fiscal policy. Interestingly, Indian fiscal reform has not yielded any such impressive outcomes inasmuch it has insignificantly contributed in the revenue generation process through taxation rather has prioritised the fiscal consolidation process through reigning expenditures. Literature has pointed that tax collections have been influenced by multiple factors—tax policy, assessment effect, rate effect and structural changes in the economy. Again, tax rate changes likely to have significant impacts depending on any country’s position in the rate revenue curve; and even moderate increase could enhance the revenue collection in the short run coupled with challenges. India having a quasi-federal structure with 28 states and 7 union territories, where the Constitution has empowered the central and state governments to impose certain kind of taxes along with their expenditure responsibilities under the Article 265, whereas under the Article 269 taxes have been levied and collected by the central government and assigned to the states. The provisions of intergovernmental transfers to mitigate the states’ vertical and horizontal fiscal imbalances likely have adversely impacted the tax efforts. To curb the fiscal deficit of the states within a threshold limit of 3 per cent of their gross state domestic product (GSDP) and to eliminate the primary deficit, the central government has enacted the Fiscal Responsibility and Budget Management Act (FRBMA), 2003. Surprisingly, the boom witnessed in the Indian economy in 2005–06 has been primary contributed by the private consumption coupled with investments especially debt finance due to credit boom in the economy rather than any tax buoyancy.

Data and Methodology

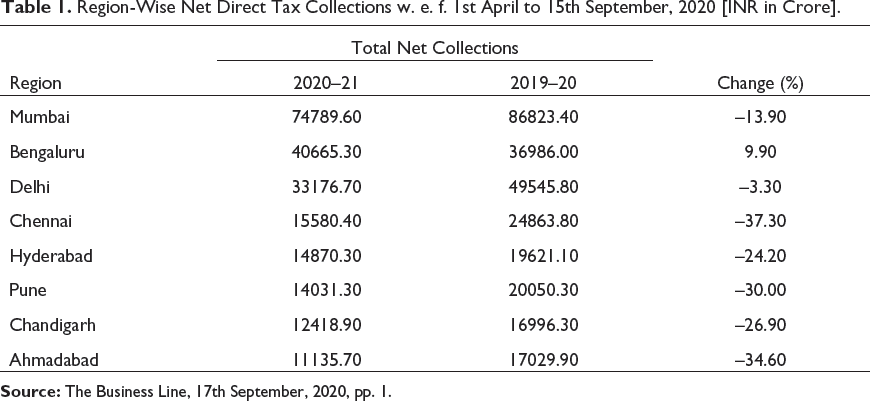

Region-Wise Net Direct Tax Collections w. e. f. 1st April to 15th September, 2020 [INR in Crore].

From Table 1 it has been evident that, barring Bengaluru all other regions have reported de-growth in net direct tax collections where in the Ahmadabad region the collections has significantly dropped by 34.60 per cent on y-o-y basis. The impact of the pandemic, introduction of the FAS and timely payment of interest on advance tax would likely to improve the collections but it has been estimated that the shortfall would be in the range of 20 per cent–22 per cent, a consequence of the contraction in the GDP. Accordingly, the fiscal deficit could be expanded and likely to accelerate the quantum of government borrowings substantially.

III. Findings and Conclusion

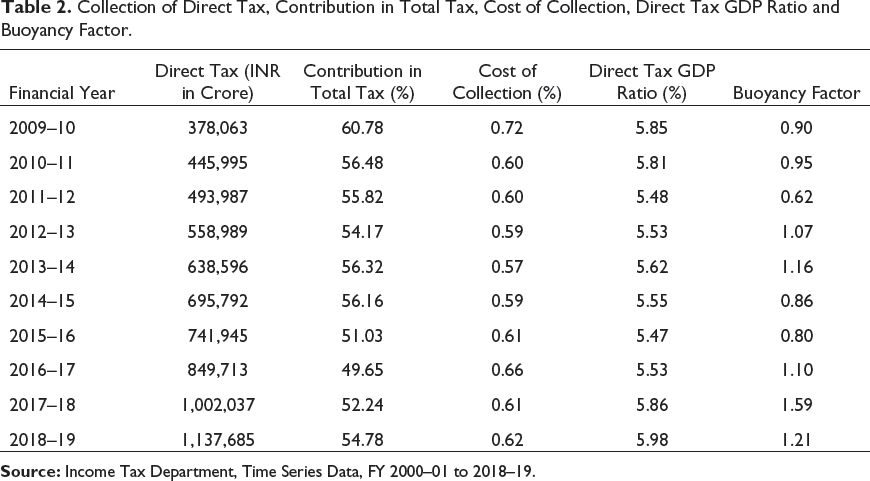

Collection of Direct Tax, Contribution in Total Tax, Cost of Collection, Direct Tax GDP Ratio and Buoyancy Factor.

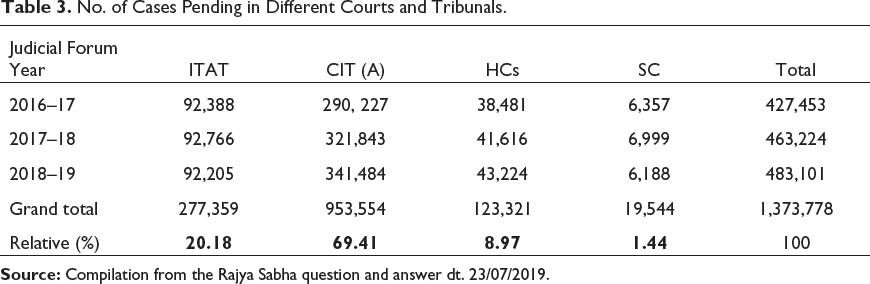

No. of Cases Pending in Different Courts and Tribunals.

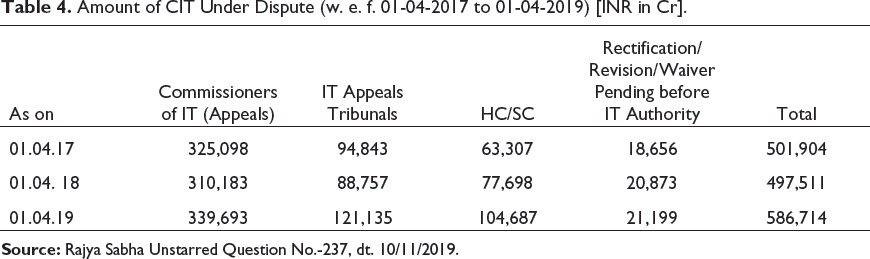

Amount of CIT Under Dispute (w. e. f. 01-04-2017 to 01-04-2019) [INR in Cr].

From Table 4 it has been evident that CIT under litigation before the IT Commissioners (Appeals) have reported an increase around 9.51 per cent during 2018–19 vis-a-vis 2017–18, whereas the pending amount lying with the ITAT have also registered an increasing trend on the y-o-y and during 2018–19 it has increased by whopping 36.47 per cent. Similarly, the CIT revenue blocked with the different Hon’ble HCs and in the Hon’ble SC has reported growth by 34.73 per cent in 2018–19, whereas Rectification/Revision/Waiver Pending with the tax administration has reported an increase marginally by 1.56 per cent during the same period.

Three fundamental components viz. determination, computation and payment should be reflected in a good tax administration (Shome, 2019). Again, the father of the Indian taxation reforms Raja Chelliah led Committee way back had recommended to broaden the tax base, lowering the marginal tax rates, minimising the tax rate differentiation and to undertake measures for making the tax administration and enforcement more effective. Accordingly, instead of meeting the fixed money value geographical area-based target, the tax administration should focus on minimising the tax gap. For increasing the tax revenues in line with the Kelker Committee recommendations the tax administrations should target the ‘missing middle’ instead harassing the honest taxpayers. The best approach should be comprehended by broadening the tax base, reducing the personal income tax rates in the competitive level with the global peers, further rationalising the tax system, formalising the unorganised sectors and by enhancing the lower household incomes substantially in lieu of serving notices to the non-filers and by evading the tax evasions (Deb & Chakraborty, 2016). The FAS along with the Vivad-se-Viswas scheme introduced in 2020 could increase the tax collections from the untapped or under-tapped sources substantially against the stigma of infamous tax terrorism.