Abstract

The bulk of the world trade in commodities now a days consist of intermediate goods, which play an essential role in production and creation of value-added. As a consequence, the global production process is getting much more integrated today than ever before. To understand and examine this internationalisation in Indian manufacturing industries, using World Input–Output Database (WIOD), we have estimated the foreign and domestic value-added contents in export and output of Indian manufacturing for the period 2000 to 2014. Further, to complement this analysis, we have also performed regression estimations to identify the relationship between export, imported inputs use, and output growth of Indian manufacturing industries. Our study reveals low usage of domestic inputs use and more usage of imported inputs. These indicate stronger backward linkages in production and weak forward linkages in global consumption and production networks. Regression analysis also strengthens the finding of higher backward participation of the manufacturing sector. We have employed panel vector error correction model, fully modified ordinary least square and dynamic OLS models. Our results reveal a robust long-run causality between imported inputs usage and export-growth of the sector.

Introduction

The proliferation of international and regional integration related to the global decentralisation of production is mainly reflected by the increase in the trade flow of intermediate products and final products across countries. As a result, the increasing standardisation of manufacturing production processes has shifted to developing and emerging economies, while advanced economies have shifted to operating bases (Baldwin, 2012). Therefore, all countries are linked together through global product sharing. As a result of participating in global value chains, the focus of countries has shifted to tasks related to their comparative and competitive advantages (Jangam & Akram, 2019), which has also actively extended the duration of exports (Türkcan & Saygili, 2018; Zhu et al., 2019).

Emerging market economies (EMEs) have become major exporters of primary, intermediate and final manufactured goods (Gereffi & Sturgeon, 2013). They also play an important role in changing the end markets of global value chains (GVC) (Staritz et al., 2011). The study by Grossman and Rossi-Hansberg (2008) identified several channels through which trade increases domestic value-added, including the division of labour. Learn by doing, competition, and technology spillover, are important means of global value chains (Kee, 2015; OECD et al., 2019). Halpern et al. (2015) have mentioned the availability of cheaper, more efficient, and diversified intermediate inputs.

Since the 1990s, countries like South Korea, China, Turkey, Indonesia, Thailand and India have increased their shares of total value-added in global manufacturing (Baldwin & Lopez-Gonzales, 2015; Hanson, 2012; Kwon & Ryou, 2015; Nathan, 2018) and helped in building conducive GVC-oriented industrial policy (Chang & Andreoni, 2020; Hauge, 2020). Various theoretical approaches like traditional Ricardian and Heckscher-Ohlin type trade models have been used to explain the GVCs (Gereffi et al., 2001, 2005) and global production network (GPN) (Coe et al., 2008a, 2008b; Henderson et al., 2002; Yeung & Coe, 2015).

Baldwin and Venables (2015) have modelled how product-specific value chains influence the competitiveness of the concerned industries through their forward and backward linkages. In a recent paper, Pahl and Timmer (2020) studied the impact of participation in global value chains on economic improvement. They found strong evidence that further integration of global value chains has a positive impact on productivity. Jangam and Rath (2021) have studied the economic upgrading process of 24 EMEs during 1995–2011. They find that domestic value-added in export has significantly improved through the forward and backward linkages of GVCs.

Over the past 25 years, the share of trade in parts and components between developing countries has more than quadrupled. Between 1995 and 2009, global value chain trade revenue increased sixfold in China and fivefold in India (OECD et al., 2014). In the past decade, policymakers in India have predicted significant increases in exports and, although not always achieved, clearly articulating ambitious goals in various strategic documents.

To achieve the targeted export growth, India needs to strengthen its participation in the global integration process for several reasons. Currently, global exports consist primarily of intermediate products, accounting for approximately 70% of the world’s exports of goods and services (Asian Development Bank, 2018). Given these advantages, countries cannot sustain high-speed export growth without improving GVC and GPN participation. Also, in the case of emerging economies like India, GVC offers new opportunities to participate in world trade by developing and strengthening niche markets for specific products. It also helps build local business capabilities through cross-border transfer of knowledge, investment opportunities, efficient management, and other global best practices. Access to these international best practices provides emerging economies with significant development opportunities and increased export potential. Increasing GVC and GPN participation could contribute to achieving India’s other development goals, including creating productive jobs and achieving high growth in manufacturing’s share of GDP (Mitra et al., 2020).

In the case of India, very limited attempts have been made so far to study the linkage effects of the manufacturing sector using IO framework, and to study the causality relationship between imported inputs usage and export of the sector. To fill this literature gap, we have attempted to study the same. Our study adds value to the current literature by contributing a structural scenario of the overall internationalisation of Indian manufacturing. The disaggregated level analysis also gives us a picture of the relative position of their participation in GPN and GVC.

The trade disintegration is primarily analysed through vertical specialisation (VS) of the production processes. VS captures the sequential production stages that involve multiple countries who carry out some stages of the production sequence (Hummels et al., 2001). It can be measured by calculating foreign value-added content in exports (FVA), which also captures the backward integration of the country in GVC. Further, domestic value-added content (DVA) in export captures the forward integration of a country. We have primarily followed Hummels et al.’s (2001) methodology in this study. Our estimates indicate low usage of domestic inputs and higher use of imported inputs by Indian manufacturing at an aggregate level. We have also observed larger backward links and lower forward participation in GPN and GVC. At the industry level, we find that the faster-growing sectors in terms of trade intensity are having more forward and backward participation in production and consumption networks. The identified sectors are coke and petroleum, pharmaceuticals, basic metals, other transport equipment, and chemicals. Regression analysis complements the finding of higher backward participation of the manufacturing sector. A robust long-run causality exists among export growth, imported inputs, and output growth. Also, unidirectional causality from imported inputs used to export growth is viewed in the short run.

The rest of the article is organised as follows: in Section II, we have described the data and the computational framework of domestic and foreign contents in export and output. Results and analysis are given in Section III. In Section IV, we have enumerated the empirical model to study the causality between export, imported inputs, and output of industries. Section V explains the econometric methodology, baseline results and robustness check. Finally, Section VI provides concluding remarks along with some policy prescriptions.

Data and Computational Framework

For our analytical purpose, we have used the World Input–Output Database (WIOD), release 2016, covering the data for 2000 to 2014 (latest available). In WIOD, the industry classification is made as per ISIC rev. 4, adhering to the System of National Accounts (SNA) of 2008 version. The input–output table is created with 54 manufacturing and service sectors. In our industry-level analysis, we have taken the 18 manufacturing sectors (see Appendix I). To compute the domestic and foreign value-added of these individual sectors, we have taken the inputs of service sectors, that is, all 54 sectors have been considered. Following Hummels et al. (2001), we consider the following three identities:

The use of domestic production for each product gives us the total domestic supply as (in matrix notation):

Or,

Where, Similarly, total import is the total utilisation of sectoral imported products, that is,

Or,

Where, Finally, the supply side gives,

Or,

Or,

Where,

Where,

Where,

Similarly, the domestic and foreign input-contents in gross output can be calculated as

Where,

Foreign and Domestic Value-Added Contents in Export

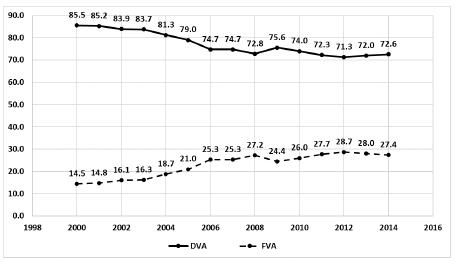

We have used equations (4) and (5) to compute the DVA and FVA contents in each unit of final demand of gross domestic output. These values are then used to calculate the value-added contents in total exports (Figure 1). Our estimation reveals weakening forward participation of the Indian manufacturing sector in GPN and consumption network (–1.61% per annum) from 2000 to 2014. The FVA in export (Figure 1) indicates that backward linkages in GVC of Indian manufacturing have increased (12.4% per annum) with a decreasing rate (–0.4%).

There exist few studies, which also reveal these estimates closer to us. In a very recent study, Goldar et al. (2017) have shown a steady increase in import content in merchandise export of India from 1995 to 2011 using IO tables of the Annual Survey of Industries (Central Statistics Office) database. They have accounted for 26% of foreign content in merchandise export during 2011, which was raised from 11% in 1995. Veeramani and Dhir (2019) have also shown a steady decline in domestic value-added in gross export from 86% to 65% during 1999–2000 to 2012–2013.

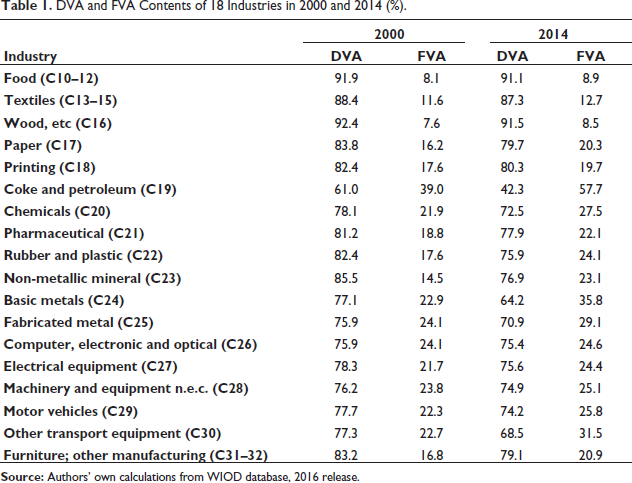

DVA and FVA Contents of 18 Industries in 2000 and 2014 (%).

The estimates reveal that FVA contents in each unit of final demand have increased for most of the manufacturing industries from 2000 to 2014. The DVA contents in per unit final demand of almost all industries (except food, textile, and wood products) have decreased over time. Notably, the FVA content in each unit of final demand of coke and petroleum product was higher (58%) than its domestic content among all manufacturing industries. Few sectors like rubber and plastic (8.6%), fabricated metal (7.6%), pharmaceuticals (6.6%), in chemicals (5.7%) show substantial growth in their FVA content relative to others. For the other industries, namely coke and petroleum, basic metal, paper, non-metallic, and other transport equipment, the FVA contents have increased by 2% to 5%.

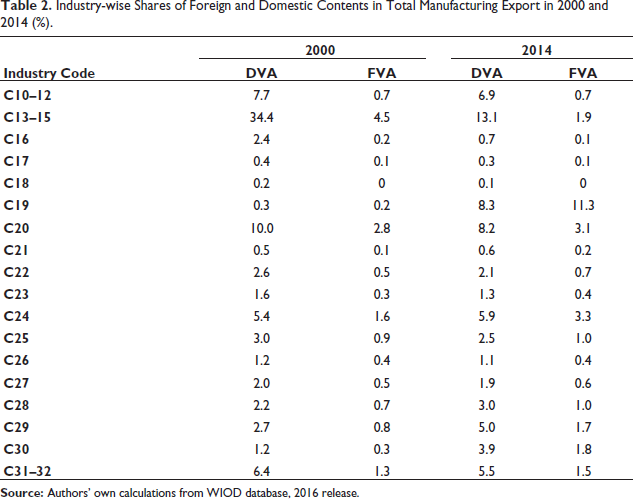

Industry-wise Shares of Foreign and Domestic Contents in Total Manufacturing Export in 2000 and 2014 (%).

The industries that show substantial growth in foreign and domestic value-added contents in total exports are coke and petroleum, motor vehicles, basic metals, and other transport equipment. Coke and petroleum has reported the highest growth in domestic value addition (18.9% per annum) and FVA content (28.2% per annum) in total manufacturing export of the country during 2000–2014. The DVA share in total export of basic metal was increased by 12.7% with a decreasing rate of 0.8% per annum. The other transport equipment, and motor vehicles grew at a rate of 3.6%, and 9% per annum respectively. The FVA shares in export have increased significantly by 11.55% per annum in other transport equipment industry and by 6.06% per annum in the motor vehicles.

The electrical equipment, other non-metallic mineral, and rubber and plastic have shown a negative growth in DVA contents of export and positive growth in their FVA contents of export. The shares of DVA and FVA contents of pharmaceutical, non-metallic, fabricated metal industries are stagnant over the period. Among the indigenous industries, textile has shown a declining trend in both the shares, which indicates its lower participation in the value chain over time.

Foreign and Domestic Value-Added Contents of Gross Output

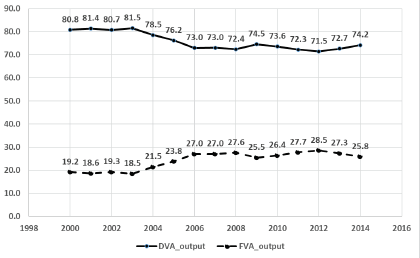

Domestic and foreign value-added contents in gross manufacturing output (

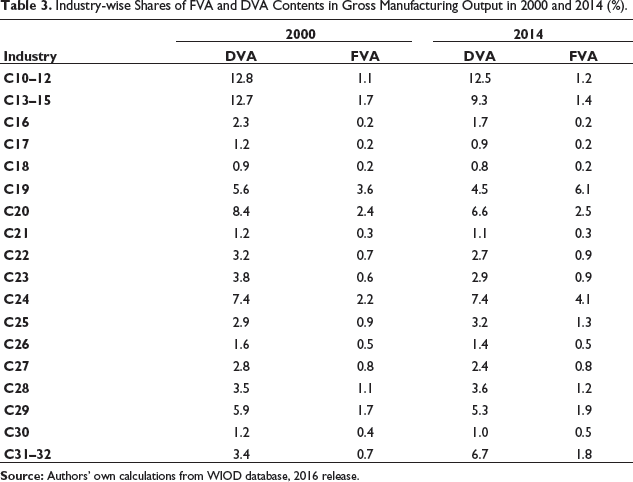

Our estimation shows a marginal decrease of 0.94% in the domestic value-added share in gross manufacturing output during the period. The share of foreign value-added content has increased by 3.12%, growth significant at 1% level (Figure 2). These findings are quite close to Banga (2014) and Joseph (2016). Banga (2014) indicated a falling trend in DVA ratio to gross output for all manufacturing industries during 1995–2009. Her study concluded that Indian manufacturing is not beneficially linked with GVCs. Joseph (2016) reported that in Indian manufacturing, the import intensity 1 is steep during 2009–2012 in 12 product-specific manufacturing sectors.

Our disaggregated level calculations of these ratios (Table 3) indicate that only in fabricated metal and machinery and equipment n.e.c., the domestic value-added contents to total output have increased marginally by 0.97% and 0.78% per annum respectively. Rest all 16 industries either have shown negative or stagnant growth rates in case of their domestic value addition to total manufacturing production. These signify that most industries are using foreign inputs (both direct and indirect) over domestic inputs in their production.

Industry-wise Shares of FVA and DVA Contents in Gross Manufacturing Output in 2000 and 2014 (%).

In basic metal and fabricated metal industries, the growth rates of DVA contents in output are 7.1% and 6.3%, respectively, but they fall by 0.3% per annum. The FVA content in output has increased at 16% per annum, with a declining trend of 0.5% annually in basic metal. In fabricated metal, the growth rate increases (17%) at a decreasing rate of 0.8% per annum.

Textile, chemicals, motor vehicles, coke and petroleum, paper, other non-metallic mineral, pharmaceutical, printing media have reduced their domestic inputs usage over time, and shown a negative growth rate in the shares of

Further, our

The above analysis gives us an understanding of the forward and backward integration of manufacturing sectors along with their effectiveness in international outsourcing. Further, this analysis provoked us to explore the causality nexus between export, imported inputs, and output of industries. The theoretical argument behind this causal nexus is based on the models developed by Grossman and Helpman (1991), Rivera-Batiz and Romer (1991), and others, who expounded that international trade increases specialised inputs, and lead to a production growth. The primary argument is based on the Export-led-growth hypothesis whose theoretical foundation is stemmed from neoclassical endogenous growth models. For the analytical purpose, we consider the following simple model to strengthen our econometric method. Considering Keynesian open economy model where the equilibrium can be written as:

Where, Y, C, I, X and M are sectoral output, domestic consumption, investment, sectoral export, and import. Considering the real parts of the economy, the more general implicit functional form of the above equation can be written as

We have investigated the causality relationship of the variables at the sectoral level based on this model. Hence, we have calculated the export, imported inputs, and output shares of the manufacturing industries from WIOD database. The balanced panel has been constructed by taking 18 manufacturing industries for 15 years (2000 to 2014). Considering the possible non-linearity of the above variables, we can expand them using Taylor expansion logarithmically around the origin, given their regularity condition. Thus, we have taken appropriate lags of each variable.

This section is divided into two subsections. In the first subsection, we have described and implemented the baseline econometrics methodology to study the causal relationship between the variables. In the second subsection, we have performed the robustness check of the analysis.

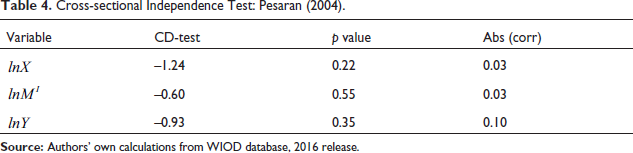

Cross-sectional Dependency Test

Cross-sectional Independence Test: Pesaran (2004).

Cross-sectional Independence Test: Pesaran (2004).

Following the literature and considering the possible endogeneity, we have performed the following steps to study the cointegration and causality between the variables.

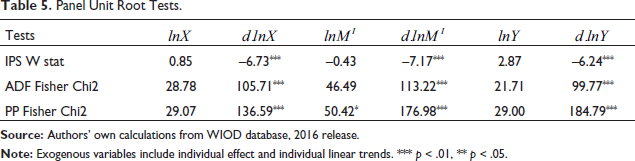

Panel Unit Root Test

To examine the long-run relationships between the chosen variables (

Panel Unit Root Tests.

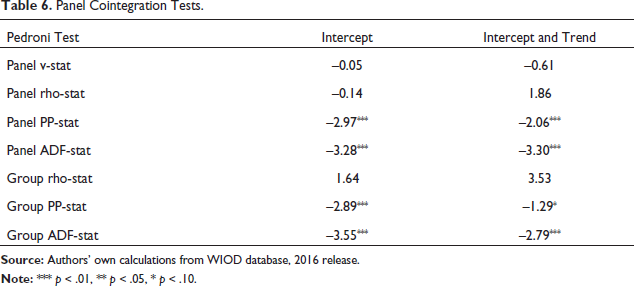

Panel Cointegration

Panel Cointegration Tests.

Pedroni took seven residual-based panel cointegration statistics. First four panel cointegration statistics include panel rho, panel-v, panel non-parametric (PP), and panel parametric (ADF) statistics, based on pooling along the within-dimension. Panel PP and are parallel to the Phillips and Perron (1988) test. The last three tests are group-PP, group-ADF, and group-rho statistics based on pooling along the between-dimension. For our variables, from the first group (within dimension), Panel PP-stat and Panel ADF-stat reject the null of ‘no cointegration in heterogeneous panels’ at 1% level. From the second group (between dimension), group PP-stat and group ADF-stat are found significant to reject the null (Table 5). We have taken both with and without a trend. We have used AIC for optimal lag selection. Hence, most of the test statistics are indicating the prevalence of cointegration among the variables.

Panel Causality

The cointegrating relationship of the variables prompts us to undertake causality analysis by employing the Panel Vector Error Correction Model (PVECM) to study the long-run relationship among the variables. We use the two-step procedure of Engle and Granger (1987). In the first step, we hypothesise that export shares of industries depend on imported input shares of the industries and the output shares. Hence, we run the following long-run log-linear model, based on Cobb-Douglas formulation:

Estimating (10) gives us the estimated residual

Where,

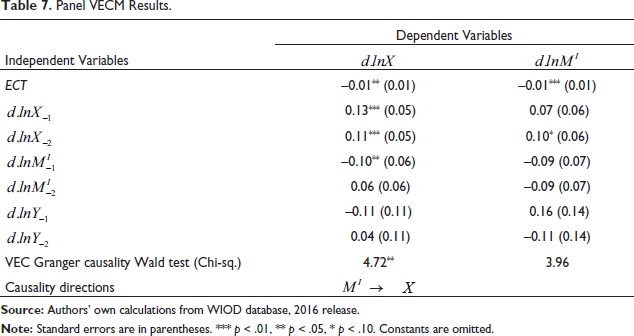

Panel VECM Results.

In Table 7, columns 1 and 2 represent the estimation results of equations (11a) and (11b), respectively. The coefficients of ECTs (

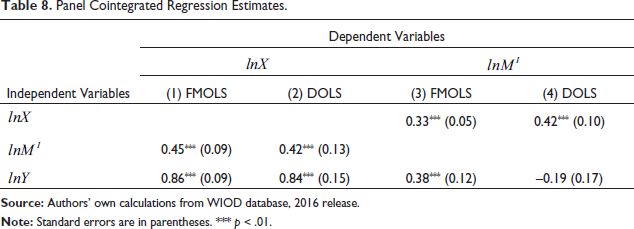

Panel Cointegrated Regression Estimates.

Columns 1 and 2 results reveal that the long-term elasticity of export with respect to imported-inputs use is 0.4, which signifies 1% increase in imported-inputs usage increased the export of the industries by 0.4%, significant at 1% level. Similarly, output elasticities estimated from both models are 0.8. Thus, both FMOLS and DOLS models signify that the exportability of Indian manufacturing is inelastic with respect to both imported inputs and output of the sectors. On the contrary, columns 3 and 4 results indicate the inelasticity of imported inputs use with respect to the export of industries.

Few earlier studies are worth mentioning here, which calculated the import intensities of Indian manufacturing sectors (see Bhat et al., 2007; Bhat & Paul 2009; Bhattacharya, 1989; Pitre, 1992). These studies did not employ any econometric methodology to determine the long-term relation between imported inputs usage and export growth. Still, their import intensity calculations and their trend for Indian manufacturing for various periods (starting from 1970–1971 to 2003–2004) support our findings. Bhattacharya (1989) used the IO matrix and found that during 1970–1980, the import intensity of Indian manufacturing had been a little over 10% in 1973–1974, which decreased to 8.26% in 1979–1980. He, thus, argued that the sectoral increase in the import content in the manufacturing sector might have been due to export-linked import liberalisation policy. Pitre (1992) observed that it is much less than the aggregate manufacturing production of the economy. Bhat et al. (2007) have also found significant progress in import intensities of Indian manufacturing at the aggregate level. Bhat and Paul (2009) have expanded the analysis for the decade of the 2000s. They found a 24% increase in import intensity in 2003–2004 from 12.9% in 1993–1994.

Robustness Check

To check the robustness of our baseline results, we have employed the Autoregressive distributed lag model (ARDL) model developed by Pesaran et al. (1999) by taking

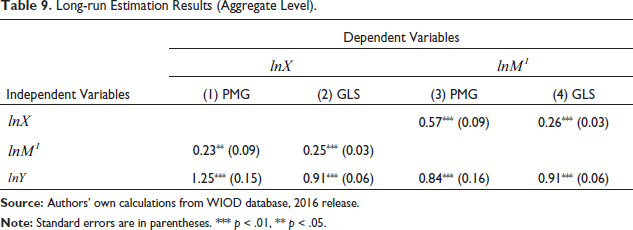

Long-run Estimation Results (Aggregate Level).

Further, we have conducted Wooldridge (2002) test for autocorrelation in panel data and found AR(1). We employ seemingly unrelated regression estimation (SURE) after finding autocorrelation of order 1 and considering cross-sectional dependence. In Table 9, column 2 represents the estimated Generalised Least Square (EGLS) results with

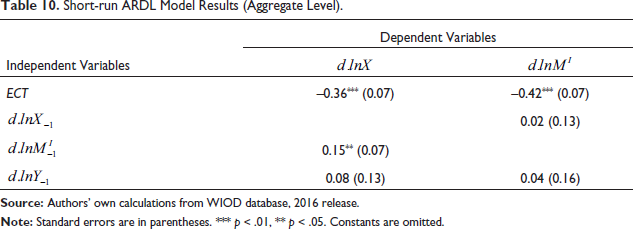

Short-run ARDL Model Results (Aggregate Level).

ARDL model indicates short-run unidirectional causality from imported inputs uses to export share; that is, imported inputs usage significantly increase the export of Indian manufacturing industries. This result is also conferring the robustness of our PVECM results.

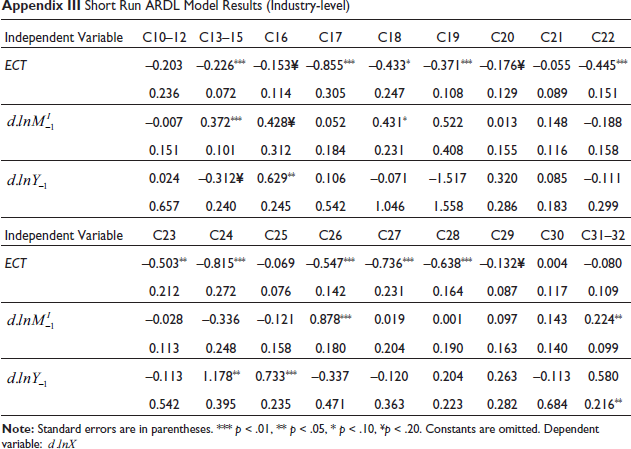

Besides, the ARDL model also gives us the long-run and short-run results at the industry level.

Taking

In this article, we have tried to perceive the nature of trade intensities of the Indian manufacturing sector by computing the domestic and foreign contents in manufacturing export and output. For our analytical purpose, we have used WIOD database to calculate these measures or indices. We have studied the trends of these indices to identify the position of Indian manufacturing in the global product sharing network. Further, we have calculated the export shares, imported inputs share, and output shares of individual industries using the database to understand the relationship among the variables. The primary purpose of the regression analysis is to see whether the usage of the imported input is affecting the export of the sector or not.

This study reveals a larger involvement of Indian manufacturing in the GVC and GPN over time through its backward linkages. At the industry level, manufacturing goods’ trade can be classified into two categories as ‘processed intermediate goods’ and ‘primary products used as intermediaries’ (Kowalski et al., 2015; Paul & Barua, 2021). Our results indicate that India’s trade intensities have increased in processed intermediate products like coke and petroleum, motor vehicles, basic metals, and other transport equipment industries.

Internationalisation is predominant in the processed intermediate goods’ industries like coke and petroleum, other non-metallic minerals, motor vehicles, machinery and equipment n.e.c., trailers and semi-trailers, rubber and plastic industries; and high-tech processed intermediate manufacturing like pharmaceuticals, chemicals, computer, electronic and optical, electrical equipment. Long-run causality between imported inputs and export growth is quite prevalent in these faster-growing sectors.

This study will help us to design appropriate industrial and trade policy for the manufacturing sector of India. Given the ambit of ‘Make in India’ initiatives taken by the Government, industries with the higher potential to add value to their export should be encouraged. Therefore, a further liberalised trade policy is conducive to expand the export of the manufacturing sector. Sector-specific policies are needed to be designed so that the fast-growing manufacturing sectors can create larger forward and backward linkages in GVCs. In addition, existing tariff and non-tariff measures related policies are needed to review to enhance international integration.

Summary Statistics

Short Run ARDL Model Results (Industry-level)

Footnotes

Acknowledgements

I am deeply grieved by the sudden demise of my co-author, Professor Alokesh Barua, due to COVID-19. I dedicate this article as a tribute to Professor Alokesh Barua. We sincerely thank Professor Abhijit Das, Head, Centre for WTO Studies and Professor Manoj Pant, Director, Indian Institute of Foreign Trade for their insightful comments, which have immensely helped us in framing the study. We also wish to acknowledge their grant of support to undertake this study.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Raw data were generated at World Input–Output Database (

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.