Abstract

Financial inclusion is an important aspect of achieving economic growth in South Asia. The present study is offered to examine the key factors of financial inclusion in South Asian countries. The study considered the 2017 World Bank Global Findex database for the analysis. The probit regression model is used to find the relationship between financial inclusion and its determinants for individual country level as well as for the group of South Asian countries. The results have shown that socio-economic variables like age, gender, education, income and workforce are important factors of financial inclusion. The higher income quintiles, upper education classes and workforce participation have a higher probability of owning bank accounts and greater chances of accessing formal savings and borrowings. Female households are still vulnerable in the process of financial inclusion in South Asian countries. The study suggested that financial inclusion can be enhanced with higher education, higher income and more workforce participation.

Introduction

Financial inclusion has always been one of the main agendas for both developing and developed countries. Goal 10 of the 17 Sustainable Development Goals is listed as a facilitator in reducing inequalities within the nation. According to the World Bank Group, one of the ways of reducing inequality and extreme poverty, which could foster the well-being of society, is through financial inclusion. It has become a topic of interest for researchers, decision-makers and other stakeholders in the financial sector. The actual meaning of financial inclusion is when an individual or any entity has easy and safe access to useful and good-value financial products and services. Simultaneously, an individual can conveniently do easy and safe transactions, payments, credit, savings and insurance. Access to a transaction account, which enables people to store money, send money and receive payments, is the first step towards broad financial inclusion. It serves as a gateway to further financial services (World Bank, 2020). Financial inclusion is also one of the key focuses of the Reserve Bank of India and the Indian government in developing policies and programmes. It provides vulnerable groups, such as weaker and low-income groups, with timely access to financial services and adequate and cheap credit (Rangarajan, 2008). According to the Reserve Bank of India, financial inclusion means easy access to financial goods and services for all sections of society, including weaker portions and low-income groups. This can only be achieved by proper regulation of the mainstream institutional players (Joshi, 2014).

The article attempts to study the financial inclusion of South Asian nations in particular because this region occupies a vital place on the world economy map. The region is the most densely inhabited in the world and is home to one-fifth of the world’s population. The South Asian region is estimated to grow at a 6.9 per cent annual rate in 2018 and is expected to grow collectively strongly by 7.0 per cent in 2022 and 7.4 per cent in 2023 (Asian Development Outlook, 2022). According to the World Economic Outlook, 2024, this region’s actual growth rate in 2022 is 6.5 per cent and is expected to be robust, around 6.0 per cent in 2024.

There is much potential for economic growth and development in these regions, which motivates us to study the South Asian region. According to the World Bank Group Report, 2018, robust growth might resume in countries like India, Bangladesh, Pakistan and Sri Lanka, although Afghanistan, Bhutan and the Maldives might only have moderate growth (World Bank, 2018). Financial inclusion is essential in South Asia to promote inclusive growth, reduce poverty and inequality, enhance resilience and empower individuals and communities to achieve their full economic potential (Omar & Inaba, 2020).

Undoubtedly, financial inclusion has always played a pivotal role in the growth of South Asian nations. It has contributed to the growth of South Asian countries with efficient resource allocation, reduced financial and informational costs and enhanced institution’s efficiency in managing funds (Sarma & Pais, 2011). It has also contributed to economic growth by building financial infrastructure, boosting economic activities and creating employment opportunities in South Asian regions. Various literature unveils a positive linkage between economic growth and financial inclusion in South Asian countries. The increased usage of mobile and internet services has expanded the dimension of financial inclusion and further contributes to the economic growth of SAARC countries (Lenka & Barik, 2018). Financial accessibility also leads to higher income, significantly impacting the economic growth in SAARC countries (Thomas et al., 2017). Other studies (Biswas, 2023; Mehrotra et al., 2009; Sharma, 2016) have confirmed the positive linkage between financial inclusion and economic growth.

However, although there is a positive linkage between financial inclusion and economic growth, financial inclusion is still at its worst in South Asia. The region has faced many hurdles in the path of financial inclusion. Bank borrowing, using debit and credit cards, saving deposits and usage of other factors are all at low levels in South Asian nations (Mani, 2016). The gender gap in access to financial services continues to be an issue in these regions, making it difficult for women to manage their finances appropriately. The issue of gender bias still exists, with more male users in South Asia than female users. The World Bank (2016) identifies some of the major issues that could hinder achieving financial inclusion in South Asian nations. First, the regions are still affected by desperate poverty, social exclusion, inadequate infrastructure and substantial social inequality (Hasina, 2003). Second, the regions are also vulnerable to climate change and natural disasters. Due to the impact of climate change, there is continued mass suffering, such as increased poverty, a rise in agricultural prices, the spread of disease and child mortality. Third, the region also faced higher social exclusion due to gender, age and economic and educational status. In line with the preceding discussions of all major issues discussed above, there is a need for the study to understand the hindrance to the demand side of financial inclusion of South Asian nations. Our study specifically tries to determine if there are any socio-economic characteristics like income, education or having a job, as well as individual-level characteristics such as age and sex that could impact financial inclusion in South Asian nations.

The study is relevant to South Asian nations, as it must pave the path to success if extreme poverty is to be defeated. Adopting a robust policy for financial inclusion is one method that can achieve higher economic growth and reduce poverty. As against this backdrop, there is a critical need to find out the determinants of financial inclusion in South Asian countries.

The article aims to measure and comparatively analyse the level of financial inclusion across South Asian countries. Here, we have used financial inclusion to mean ‘access to’ and ‘the use’ of formal financial services. Following Fungáčová and Weill (2015), we have taken three dimensions of financial inclusion: owing formal bank accounts, formal savings and formal borrowings. Individual level characteristics such as age, sex and socio-economic characteristics of the people, such as education, income and employment, are considered as independent variables for this study (Demirgüç-Kunt & Klapper, 2013).

This study examines the determinants of financial inclusion and attempts to analyse disparities in the level of financial inclusion across nations regarding gender, age, education, employment and income.

Literature Review

This section elucidates the review of literature related to various determinants of financial inclusion at individual country levels as well as groups of country levels and the use of Findex data in various studies to see the impact of financial inclusion in the growth of the nation and also tries to find gaps in the previous studies.

Access to bank accounts, including their usage, is the initial step towards achieving broad financial inclusion. There are a lot of beneficial effects of financial inclusion. Research studies from the past have shown how access to financial tools affects people’s savings rates (Aportela, 1999). Not only does it boost domestic savings, but it also gives women more say in household-level decision-making (Ashraf et al., 2010). Roy and Chaterjee (2016) also identified a lack of savings as a main hurdle to financial inclusion. Hannig and Jansen (2010) have shown how potential financial inclusion costs would compensate for its great benefits in the future. It would bring financial stability to an economy through an inclusive and more diversified financial system.

Nevertheless, women are continuously in a disadvantageous position. Over the period, men have been more exposed to financial inclusion than women (Asare & Wright, 2012). There is a significant gender gap in account ownership and usage of credit and savings products (Ahmed et al., 2023; Ohiomu & Ogbeide-Osaretin, 2019).

Various studies have tried to study the determinants of financial inclusion for South Asian nations in particular. Kumar (2013) examined the determinants of financial inclusion in India, such as branch network expansion and the region’s socio-economic and environmental setup. Evans (2016) noted significant determinants for Africa, such as per capita income, broad money (per cent of GDP) and literacy. Singh and Stakic (2021) looked at the geographical factors of SAARC nations, such as ATMs, and a demographic factor, such as commercial bank branches. Jana et al. (2024) identified demographic and socio-economic variables for India, such as gender, educational qualification, domicile or place of residence, age, occupation, income and financial literacy, as essential determinants that influence the usage of financial services (Giday, 2023).

Afterwards, the studies have tried to look at the demand side determinants of financial inclusion such as usage and accessibility of financial services—availability, penetration and usage dimension (Biswas, 2023; Thomas et al., 2017). Mani (2016) tried to look at the determinants such as bank services, debit and credit card use, bank borrowing and savings deposits for South Asian nations.

Few studies have also explored the World Bank’s Global Financial Inclusion Index Database (Findex data) to focus on the usage side of financial products to measure various determinants of financial inclusion. Demirgüç-Kunt & Klapper (2013) introduced the concept of using formal financial services using Findex data to look at the pattern of formal financial product usage (Allen et al., 2016). Demirgüç-Kunt et al. (2013) used the data to evaluate gender inequalities in financial services. Fungáčová and Weill (2015) used it to analyse financial inclusion in China and compared it to the other BRICS countries. Zins and Weill (2016) used it to examine the factors of financial inclusion in African nations. Dar and Ahmed (2021) used the database to examine the determinants of financial inclusion in India using financial inclusion measures such as formal account ownership, use of accounts for saving and borrowing, and ownership and use of a debit card.

Most studies found that socio-economic and geographical factors are important determinants of financial inclusion. Significantly, few studies are related to the demand-side determinants of financial inclusion in South Asian countries. This study is different from other studies by considering both the demand-side determinants, especially usage and accessibility, and adopting different methodological approaches, such as pooled probit methodology, for both individual countries and groups of countries to study the financial inclusions in South Asian nations.

Data and Methodology

To examine the determinants and to make a country-level comparison in financial inclusion in South Asian countries, we have used the 2017 Global Findex database. We have relied on the Findex database 2017 because it provides reliable information on inclusive financial systems, focusing solely on accessing and using financial services and products. The database contains individual-level data collected in 2017 from a poll of over 150,000 adults across 140 economies. Each year, Gallup, Inc. questioned around 1,000 people in each nation as part of its Gallup World Poll. The collected database is unique, containing the World Bank Group’s user-side data set of indicators of 148 nations. The user-side data set gives a clear insight into the subjective and objective barriers to access, such as no access to a formal account due to its high costs, physical distance and lack of proper documentation.

Here, we use the data to examine the proportions of individuals who use formal financial systems in terms of access, formal savings and borrowings in South Asian countries across gender, occupation and age.

Methodology

We run a pooled probit regression model for each South Asian country because the dependent variables, such as account ownership, formal savings and formal borrowings, are binary outcome variables with two possibilities—Yes or No. In this way, we will see the impact of individual and socio-economic characteristics on an individual’s accessibility, borrowing and saving patterns, especially in formal financial institutes. We only focus on the formal financial sources in line with the study by Demirgüç-Kunt & Klapper (2013).

Econometrics Model

The empirical model mainly focuses on three dimensions of the use of bank accounts (a) owing formal bank accounts, (b) formal savings and (c) formal borrowings.

The dependent variable y1

ij

is a binary variable. The probit model is justified when the dependent variable is binary, errors are normally distributed, and predictors suit the normal CDF. Therefore, we use the probit model using the maximum likelihood estimation (MLE) method to estimate its determinants. The pooled probit model is specified following the approach of Allen et al. (2016).

where countries and individuals are noted by i and j simultaneously, y*1 ij is a latent variable, x1 i is a vector of the country’s characteristics, Z1 ij is a vector of individual-level characteristics like age, sex, income, education and employment, β and γ are the vectors of parameter and ɛ1 ij is a normally distributed error term.

The coefficients of a probit model give the direction of the effects and are not interpreted like linear regression models. Therefore, we used the marginal effect in the probit regression model to interpret the coefficients. Marginal effects for continuous variables represent the instantaneous rate of change. The equation for marginal effects for continuous independent variables is given below:

In the case of binary independent variables, the marginal effect shows the change in predicted probabilities as the binary independent variable changes by 1 unit. For example, the discrete change in a regressor that takes the values {0, 1}. The model for the marginal effects of binary independent variables is given below:

Variables

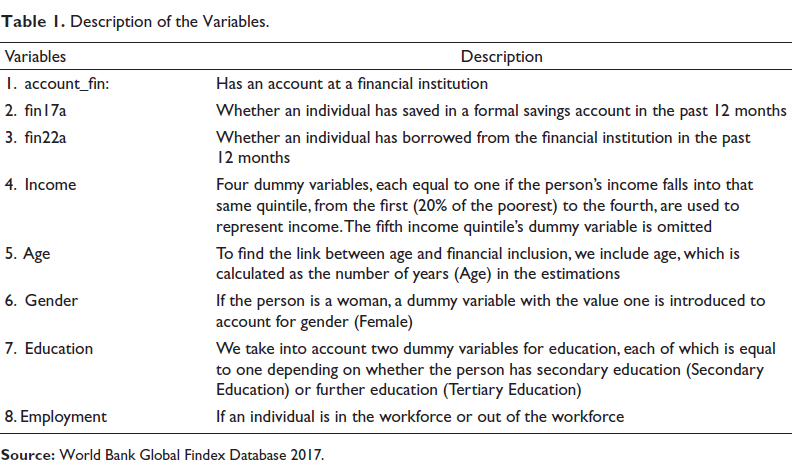

The dependent variables are (‘account_fin’) account ownership in formal institutes, (‘fin 17a’) formal savings, and (‘fin 22a’) formal borrowings (Demirgüç-Kunt & Klapper, 2013). Here ‘account_fin’ is defined as a measure of financial inclusion accounts ownership in the formal financial institution, ‘fin 17a’ is defined as saving in the formal institutions in the past 12 months, and ‘fin 22a’ is defined as borrowing from the formal institutions in the past 12 months. Account Access is one of the characteristics of financial inclusion in having a bank account. Formal savings means whether or not a person saves money at formal financial institutions, another indicator of financial inclusion. Formal credit means access to credit from credible financial institutions and is the third indicator of financial inclusion. The study’s independent variables are individual characteristics like age, sex and other socio-economic characteristics such as education, income and employment (Fungáčová & Weill, 2015; Giday, 2023). The description of the variables is presented in Table 1.

Description of the Variables.

The study initially presents the percentage distribution of account ownerships, savings and borrowings in financial institutions of South Asian countries. Further, the distribution of financial services is explained by gender, education classes, employment categories and income quintiles. Finally, the precisions of these distributions are evaluated by probit regression models. The results of the probit regression model find the important determinants of financial inclusion in South Asian countries.

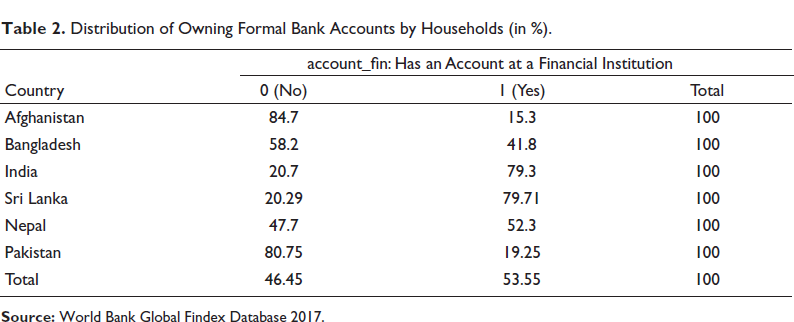

Table 2 reports the descriptive statistics of the percentage of the population with a bank account in a financial institution. Overall, nearly more than half of the population of the South Asian region has an account. Afghanistan, Pakistan and Bangladesh have over half of the individuals with bank accounts. In contrast, Nepal, India and Sri Lanka have more than 50 per cent of the population with access to an account.

Distribution of Owning Formal Bank Accounts by Households (in %).

Distribution of Owning Formal Bank Accounts by Households (in %).

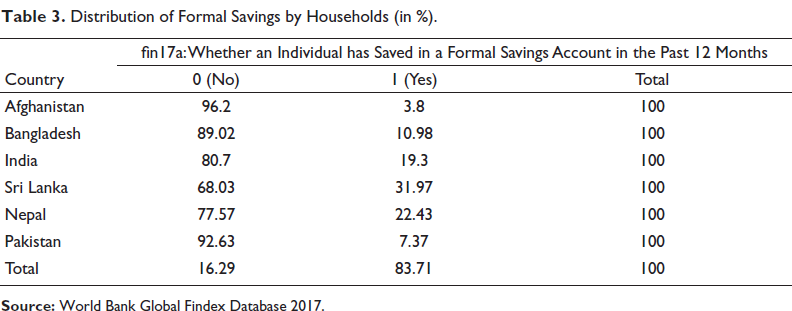

Table 3 shows Afghanistan, Bangladesh, Pakistan and India have a significantly lower proportion of the population (less than 20 per cent) who saved in formal savings accounts in the past 12 months. Sri Lanka and Nepal have moderate population levels with formal savings behaviour. Overall, in South Asian countries, there is a huge disparity in the population who still do formal savings. Nearly 16 per cent of the population does formal savings, while a large chunk still uses informal sources for saving purposes.

Distribution of Formal Savings by Households (in %).

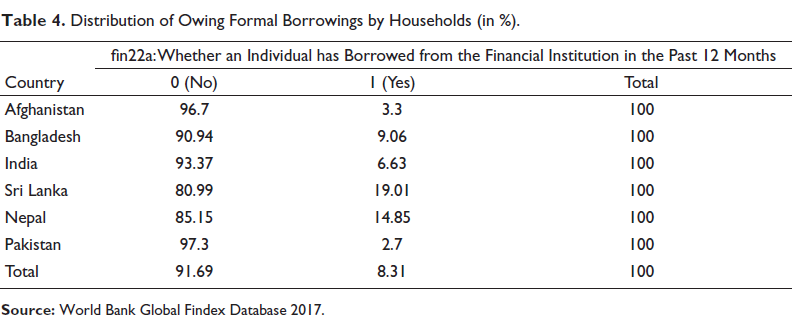

Table 4 shows that South Asian countries are far behind in formal borrowings. Only around 8 per cent of the population relies on a formal source of borrowing. Countries like Afghanistan, Pakistan, India and Bangladesh, where less than 10 per cent of the population relies on the formal source of borrowing. Nepal and Sri Lanka are still ahead regarding borrowings from formal sectors among the six South Asian nations.

Distribution of Owing Formal Borrowings by Households (in %).

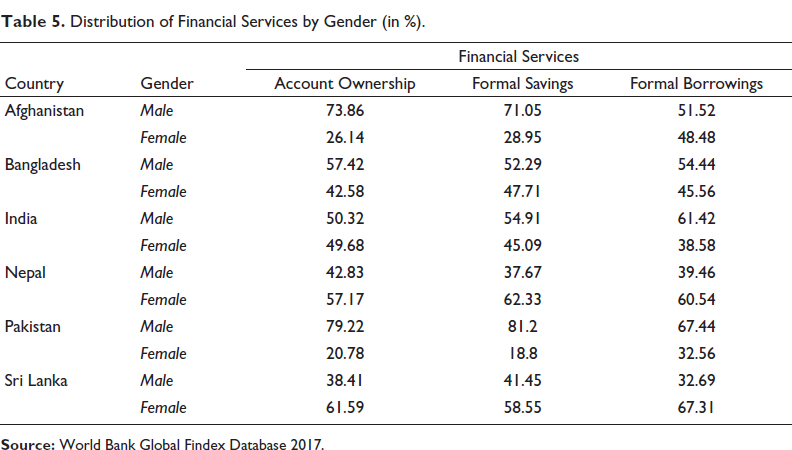

Table 5 represents variation in three indicators—formal account ownership, formal savings and formal borrowings across gender. Afghanistan and Pakistan have a large gap in the percentage of individuals in account ownership and formal savings. Females are a higher proportion of the population, having account ownership, formal savings and formal borrowings in Nepal and Sri Lanka. In nations like India and Pakistan, there is a considerable gender gap in formal borrowings. This result aligns with the previous study (Fungáčová & Weill, 2015; Zins & Weil, 2016). This result suggests that women are more empowered using financial services in Nepal and Sri Lanka than in other South Asian countries.

Distribution of Financial Services by Gender (in %).

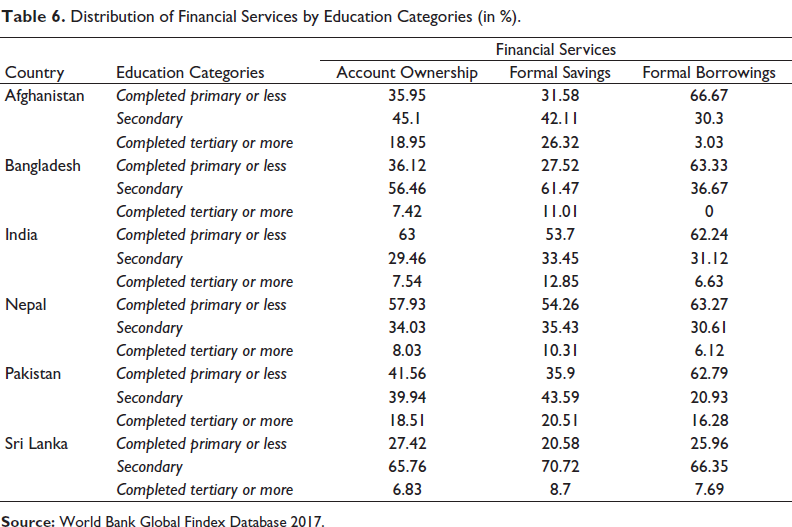

Table 6 reports the distribution of financial services of households by education categories. The results have shown that, except for India, the secondary educated households in other South Asian regions use more financial services. In India, those who have completed primary or less education use more financial services than other education categories. The results also found that households in higher education categories use fewer financial services than other education categories in South Asian regions. This may be due to fewer households in higher education classes in South Asia.

Distribution of Financial Services by Education Categories (in %).

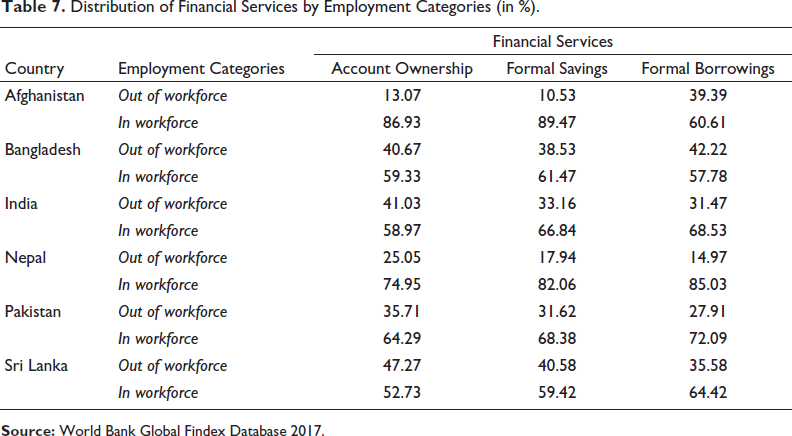

The tabulation of access to financial services by employment categories is presented in Table 7. The results have shown that those in the workforce use more for financial services. In Afghanistan and Pakistan, the workforce has more bank account ownership and uses more formal savings than in other South Asian countries. The workforce households in Pakistan and Nepal use further formal borrowings more than in other South Asian countries. The results found that those out of the workforce have less access to financial services.

Distribution of Financial Services by Employment Categories (in %).

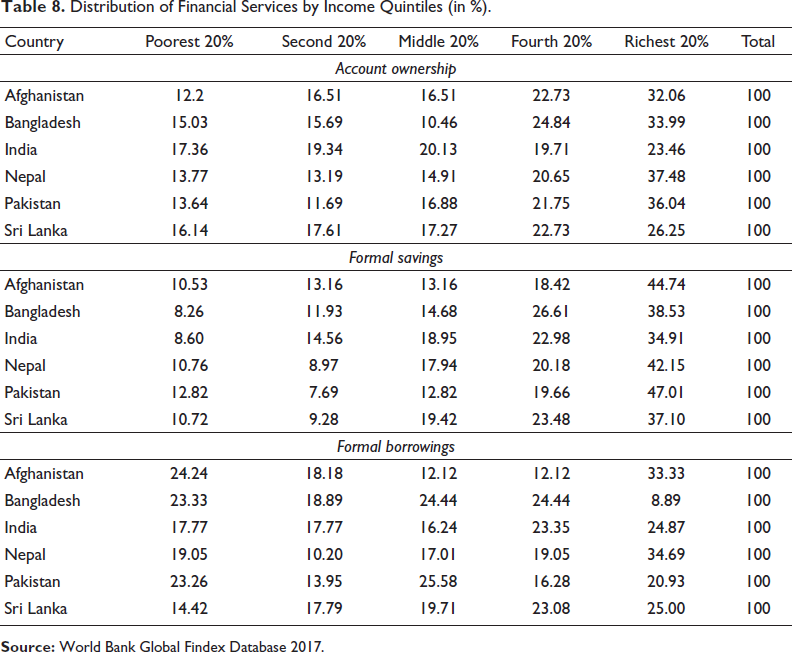

The results of financial services distribution by income quintile households are presented in Table 8. The results found that more than 50 per cent of the fourth and richest income quintiles of households use bank accounts and formal savings in South Asian countries. Apart from Nepal, more than 50 per cent of first-, second- and third-income quintiles income households of South Asian countries use formal borrowings. The results found that the highest quintile households have more bank accounts and save more in formal sources, and the lowest quintiles use more formal borrowings.

Distribution of Financial Services by Income Quintiles (in %).

Results of the Probit Regression Model

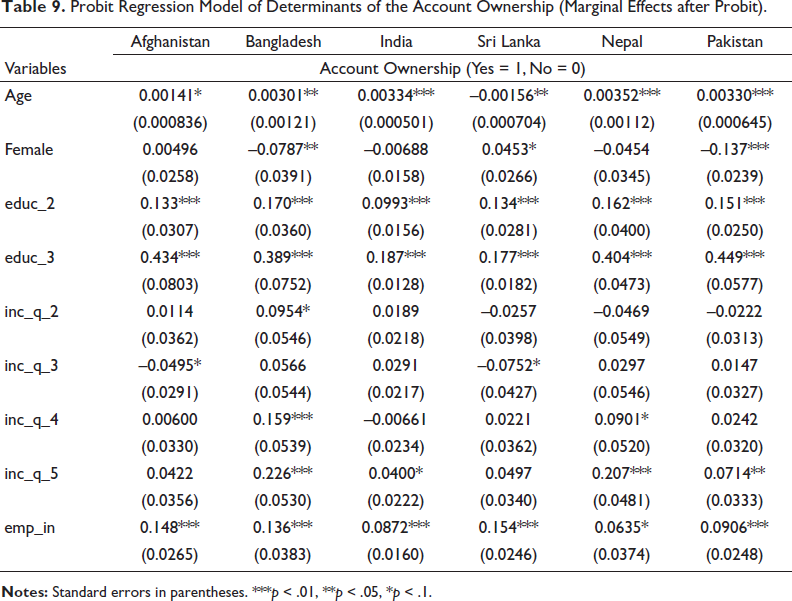

Table 9 displays the outcomes of the probit regression model conducted at the country level to analyse bank account ownership in South Asian nations. The findings indicate that individuals with higher education or income tend to possess more formal bank accounts. This trend aligns with theoretical expectations and economic reasoning, as elevated education and income often correlate with increased financial literacy, stability and accessibility to banking services.

Probit Regression Model of Determinants of the Account Ownership (Marginal Effects after Probit).

Likewise, employed or engaged in work individuals are more likely to own bank accounts across all South Asian countries. This association can be attributed to the regular income streams typically associated with employment, rendering employed individuals attractive customers for formal financial institutions.

Furthermore, certain individual characteristics, such as age, affect formal account ownership differently. In Sri Lanka, being older is negatively associated with formal account ownership, whereas this coefficient appears positive and significant in other South Asian countries.

Female households generally negatively and significantly impact bank account ownership in most South Asian countries. However, in the case of Sri Lanka, female-headed households demonstrate increased access to formal banking services. This deviation implies the presence of distinct socio-economic dynamics or policy interventions in Sri Lanka that have promoted greater financial inclusion for women.

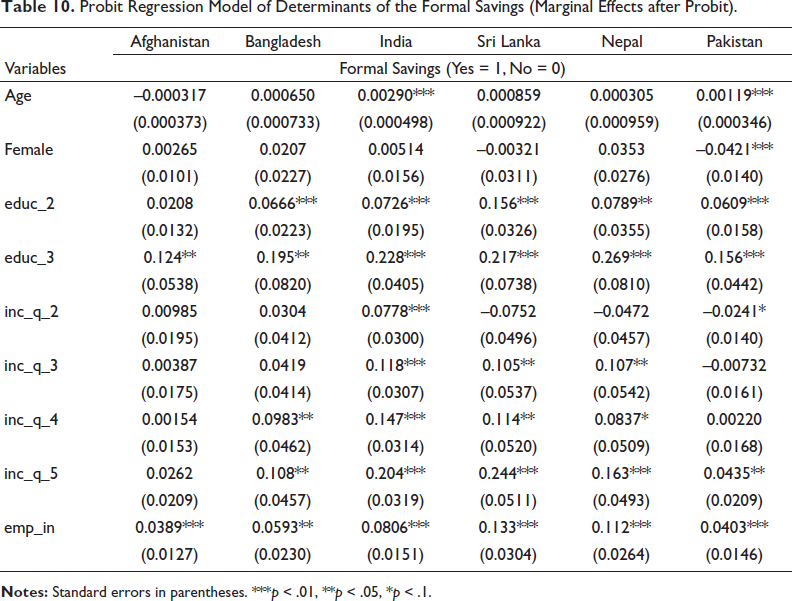

Table 10 presents the findings regarding the determinants of formal savings behaviour among households. Across most South Asian countries, individual-level characteristics such as age, education and employment positively influence households’ inclination towards formal savings.

Probit Regression Model of Determinants of the Formal Savings (Marginal Effects after Probit).

Moreover, households in higher income quintiles and those with higher levels of education demonstrate a more pronounced and statistically significant inclination towards formal savings. This suggests that higher income and education levels positively foster a culture of formal savings among households. Notably, in countries like India and Sri Lanka, the impact of education and income on household savings appears to be more substantial compared to other South Asian nations, indicating the significant role of these factors in shaping saving behaviour in these countries.

The results also shed light on gender disparities in formal savings behaviour. In Pakistan, females tend to save less in formal financial institutions, while this gender difference is not statistically significant in other South Asian countries. This result emphasises the significance of addressing gender-specific obstacles to financial inclusion and advocating for equal access to formal savings opportunities across the region.

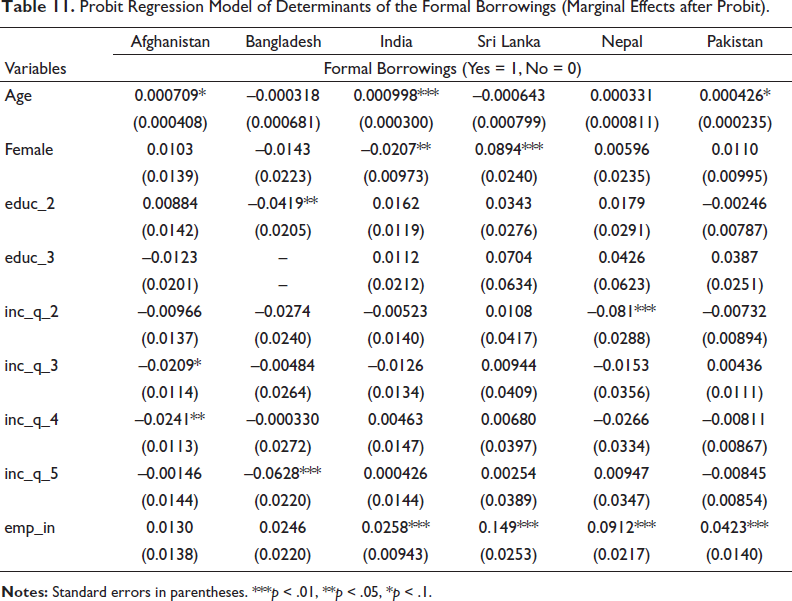

Table 11 presents the findings regarding significant factors influencing formal borrowings behaviours among households in South Asian regions. In the context of formal borrowings, age and employment demonstrate a positive impact on formal borrowings across most South Asian countries. These results suggest that individuals with stable employment and maturity are often perceived as having lower credit risks by formal financial institutions. Interestingly, in Sri Lanka, the impact of employment on formal borrowings appears to be more pronounced compared to other South Asian countries.

Probit Regression Model of Determinants of the Formal Borrowings (Marginal Effects after Probit).

Furthermore, the results indicate divergent effects of gender on formal borrowings behaviour. In Sri Lanka, the female dummy variable positively impacts formal borrowings, whereas it shows a negative impact in India. In most South Asian countries, the coefficients of education and income are found to be insignificant in determining formal borrowings behaviour. However, in Nepal, the coefficient of the second income quintile displays a negative and significant relationship with household borrowing attitudes.

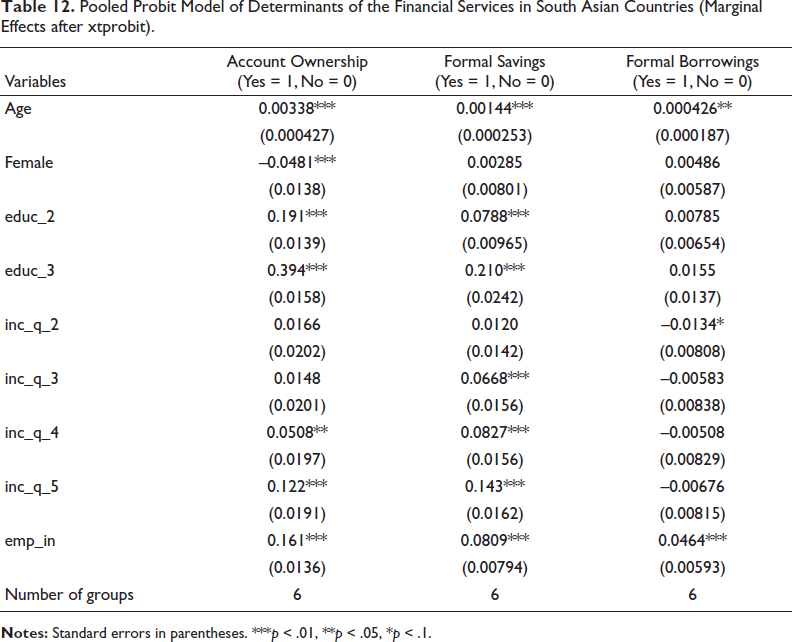

Finally, the study used the pooled regression model because it provides more accurate estimations due to more observations. Also, the estimation procedure allows the estimations of a group of countries in South Asian regions. The study presents pooled probit regression models to find the important determinants of financial services in South Asian countries as a group in Table 12. The results are stable with the country-level analysis. The results have shown that higher education categories and higher income quintiles have a higher chance of having formal account ownership and using formal savings. The households in the workforce have a higher chance of using financial services. Female households have less access to formal bank accounts. The results also revealed that the aged population has a higher chance of using formal accounts, formal savings and borrowings.

Pooled Probit Model of Determinants of the Financial Services in South Asian Countries (Marginal Effects after xtprobit).

The study employed a pooled regression model for its higher accuracy in estimations, attributed to a larger number of observations. This approach also enables estimations across a group of countries in the in the South Asian region. The findings, as presented in Table 12 using pooled Probit regression models, are consistent with the results obtained from country-level analysis. The results indicate that individuals in higher education categories and higher income quintiles are more likely to have formal account ownership and engage in formal savings. Moreover, households with active participation in the workforce are also more inclined to utilize financial services. However, the findings suggest that female-headed households exhibit less access to formal bank accounts, indicating potential gender disparities in financial inclusion. Additionally, the aged population demonstrates a higher likelihood of using formal accounts, formal saving, and borrowing, implying the importance of catering financial services to the needs of older individuals.

The results from cross-tabulation methods and probit regression analysis found that higher income quintiles, higher education classes and those in the workforce have higher chances of availing of financial services in South Asian countries. The findings of this study supported the existing studies by Fungáčová and Weill (2015), Zins and Weill (2016) and Dar and Ahmed (2021).

The analysis reveals several key insights into financial behaviours and determinants within South Asian countries. Firstly, higher education and income levels positively correlate with formal bank account ownership and savings behaviour. Employment status also plays a significant role, with employed individuals more likely to own bank accounts and engage in formal savings. However, the impact of age varies, with older individuals more likely to use formal financial services in some countries.

Gender disparities are evident, with female-headed households having less access to formal bank accounts. This underscores the need to address gender-specific obstacles to financial inclusion. Furthermore, the results reveal divergent effects of gender on formal borrowings behaviour in South Asian countries.

Female households are still vulnerable to accessing financial services. As people experience various types of restraints, the following explanation helps to justify the result. Formal financial institutions occasionally require documentation to take credit, such as confirmation of identification and address (The World Bank, 2016). The cost of formal financial services is too high, making them unaffordable. Many services need a financial investment or payment of a charge. For instance, the borrowers are responsible for paying the processing cost for loans and the annual price for using a locker. A minimum balance must be maintained in the savings bank accounts. Both credit and debit cards have an annual fee. People with low income frequently are not given access to financial services like loans because they cannot offer enough security or guarantee, which makes them too dangerous for lenders to lend to (Kempson et al., 2004).

The study’s findings highlight critical implications for policymakers in South Asian countries. Higher income and education levels and workforce participation are associated with increased access to financial services. Addressing gender disparities is paramount, as female-headed households encounter obstacles to formal banking. To foster financial inclusion, policymakers must prioritise gender-specific barriers and ensure accessibility for marginalised communities. This entails reducing the cost of financial services, expanding infrastructure and tailoring products to meet the needs of underserved populations. Promoting education, employment and women’s empowerment can drive economic growth through enhanced financial inclusion, but government-concerted efforts are crucial to bridge existing gaps. This study overlooks the supply side of financial inclusion, such as physical and digital infrastructure availability. The results of the analysis may not trigger financial inclusion unless the government provides access to financial services.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.