Abstract

This article discusses India’s trade in medical devices from 2003 to 2021. Given the product heterogeneity of medical devices, this article follows a technological ranking of medical devices based on a risk-based product classification. Using international trade data at the harmonised system six-digit level, it develops a regional intensity index to understand the direction of India’s exports and imports. It uses the revealed comparative advantage index to understand the competitiveness of exports from India and segregates total trade into one-way and two-way trade. Using the product quality vertical index, the article separates two-way trade in products of similar quality from two-way trade in products of differentiated goods, that is, horizontal and vertical intra-industry trade, respectively (HIIT and VIIT). It finds that, between 2003 and 2021, India’s imports became more biased towards medium-to-high technology products, while, in exports, low-technology products became more prominent. Quality analysis suggests that India traded in products of similar quality for medium-to-high technology products, while it was a net quality exporter for low-technology items. Furthermore, between 2003 and 2021, India could not retain competitiveness in exports of products for which it had HIIT or VIITH, suggesting that Indian exports did not catch up in terms of quality.

Keywords

Introduction

Recently, the government has introduced a plethora of policy initiatives, including the production linked incentive (PLI) scheme, to reduce India’s import dependence and increase India’s competitiveness in medical device exports. Medical devices have been recognised as a sunrise sector. Devices are heterogeneous in their uses and differ widely in their technological embodiment. To promote the industry under the Make in India programme and PLI scheme, it is essential to understand the state of development and technological composition of the domestic industry. Since trade signals underlying domestic production, the technological capability of the local industry can be understood by analysing the type of trade, the type of devices India exports, and the products in which India is globally competitive. A limited number of studies have been done on the Indian medical device industry (Datta et al., 2013; Datta & Selvaraj, 2019; Ghosh, 2022; James & Jaiswal, 2020; Jha et al., 2024). While these studies indicate that India is highly import-dependent for medical devices, none analyse the type and composition of India’s trade in medical devices in the context of technological ranking. The objective of this article, thus, is to study India’s trade in medical devices during the period 2003–2021 in order to understand the type and pattern of trade, global competitiveness in different products, and to analyse changes in the technological composition of the exports and imports. International trade can be taken as a proxy for domestic manufacture—countries export products in which they specialise and import products in which their local manufacturing capabilities are low. Hence, by exploring the technological composition of trade, this article contributes to the understanding of industrial upgrading in the Indian medical devices industry.

Data and Methodology

The technological classifications given by the UNCTAD (United Nations Conference on Trade and Development) or OECD (Organisation for Economic Co-operation and Development) have limited applicability in understanding the intra-industry technological composition of the devices industry. Under the OECD classification, most of the products that constitute the device industry are listed as high technology. Moreover, it only lists high-technology products and does not help in separating medium-technology products from low-technology products. The UNCTAD classification is based on three-digit standard international trade classification (SITC) codes. The medical device industry can only be defined at the most disaggregated level of harmonised system (HS) codes (six-digit) (Table 1). 1 Concordance between HS six-digit and SITC three-digit creates problems. To circumvent this, we use the risk-based classification of the USFDA (United States Food and Drug Administration), combined with the use-based classification given by Torsekar (2018). However, a word of caution worth mentioning here is that since the inferences drawn from this analysis are based on this specific system of technological classification, any analysis following other systems of technological classification can lead to different inferences about the technological composition of India’s trade.

The USFDA classifies Class 1 devices as those that present the least health risks to patients. These face the lowest barriers to regulatory approval. Class 2 devices are those that pose a slightly greater health risk and are generally seen as similar to an existing product in the market. Class 3 devices are subject to the most rigorous regulatory procedures. More technologically sophisticated devices belong to higher risk classes. Torsekar (2018) classifies devices into six groups—disposables, surgicals, therapeutics, implants, diagnostics, and furniture and in vitro diagnostics (IVD). Disposables and surgicals consist of Class 1 devices and are considered the low-technology group, while implants, therapeutics and diagnostics consist mainly of Classes 2 and 3 products and, hence, constitute the medium-to-high-technology group. ‘Furniture & IVD’ embodies wide product heterogeneity and is kept outside this technological classification.

Trade data have been accessed from the UN Comtrade and the International Trade Centre (ITC) Trademap databases. We use the trade similarity and trade overlap approaches developed by Fontagné and Freudenberg (1997) to separate one-way trade (OWT) from two-way trade (TWT) and then the product quality space approach of Azhar and Elliott (2006) to understand vertically and horizontally differentiated TWT. The revealed comparative advantage (RCA) index is used to understand India’s competitiveness in the global market. Following Balassa, the RCA index for country i in commodity j is defined as the ratio of country i’s share in world exports of commodity j to that of country i’s share in total world exports. The index is calculated as follows

2

:

Where

to either a designated market, a region, or the whole world.

Country i is said to have an RCA in a commodity j if RCAij exceeds one.

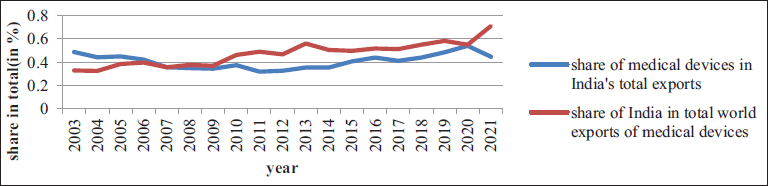

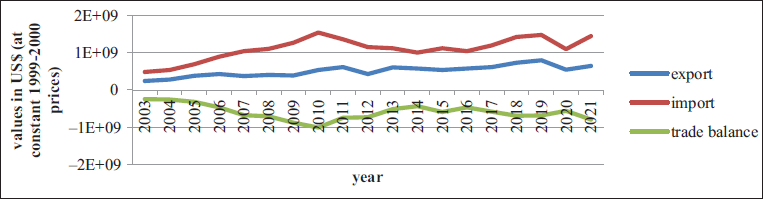

In 2003, devices had a marginal share of 0.49% by value in India’s total export basket. This increased to 0.6% in 2020 before falling to 0.44% in 2021 (Figure 1). Device exports from India made up 0.3% of total world exports of medical devices in 2003, which increased to 0.71% in 2021. Exports grew at a trend rate of 5% and increased from $245 million in 2003 to $654 million in 2021 (at 1999–2000 prices), while imports grew at a trend rate of 4% and increased from $488 million in 2003 to $1,454 million in 2021 (at 1999–2000 prices) 3 (Figure 2). At current prices, exports increased from $295.5 million in 2003 to $1,760 million in 2021, while imports increased from $503 million to $4,475 million, respectively. Imports have always exceeded exports, resulting in a negative trade balance for India in medical devices.

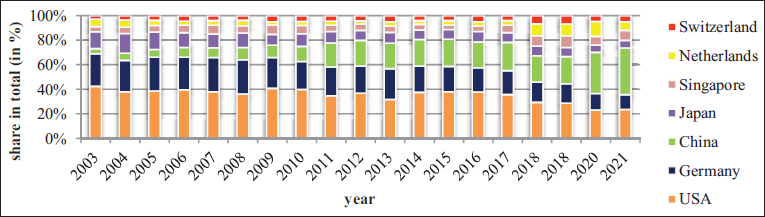

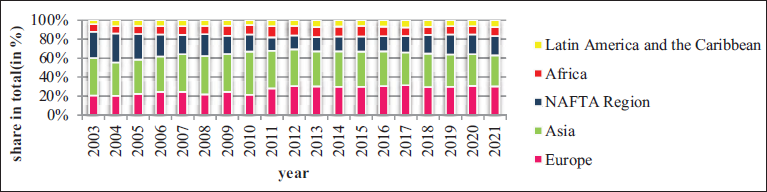

The USA, Germany, China and Japan were the top four countries from where India imported medical devices (Figure 3). Cumulatively, 67% of India’s imports came from these four countries in 2003, which reduced to 56% in 2021. If Singapore, the Netherlands and Switzerland are included (which have also been significant contributors to India’s imports) alongside these four countries, India is seen to have cumulatively imported more than 75% of her devices from these seven countries in 2003 and 69% in 2021, suggesting that imports to India have been regionally concentrated. India’s exports of devices have had Asia, Europe and the NAFTA (North American Free Trade Agreement) region as their main destinations (Figure 4). The share of exports to Asia reduced from 39.7% in 2003 to 32.7% in 2021, while the share of the NAFTA region declined from 27.7% in 2003 to 20.7% in 2021. This gap was filled by Europe, whose share in Indian medical devices exports increased from 20.8% in 2003 to 30.2% in 2021.

A regional intensity index can be defined as

Where

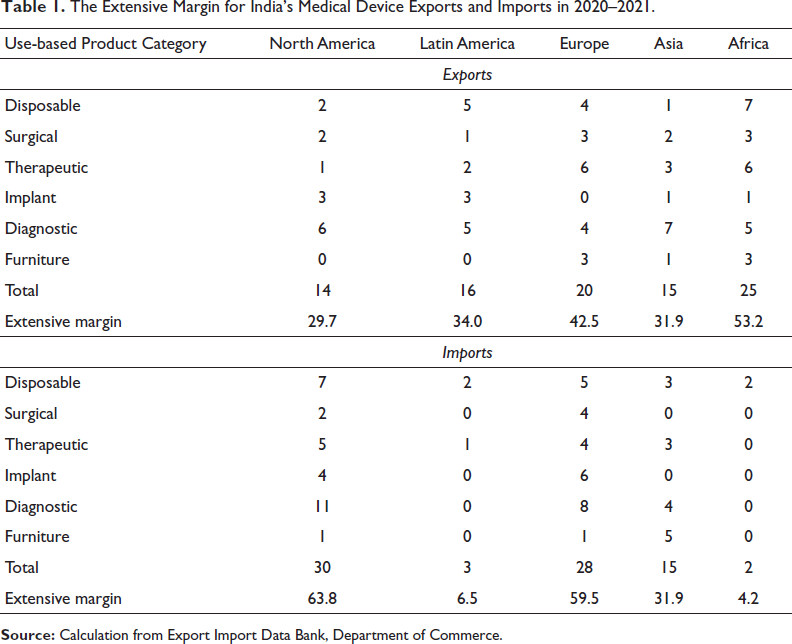

The Extensive Margin for India’s Medical Device Exports and Imports in 2020–2021.

In 2020–2021, the extensive margin for exports was highest for Africa, followed by Europe, while for imports, it was highest for North America and Europe. Africa was the most over-represented region in India’s exports of medical devices, followed by Europe, while India’s imports of medical devices primarily came from North America and Europe.

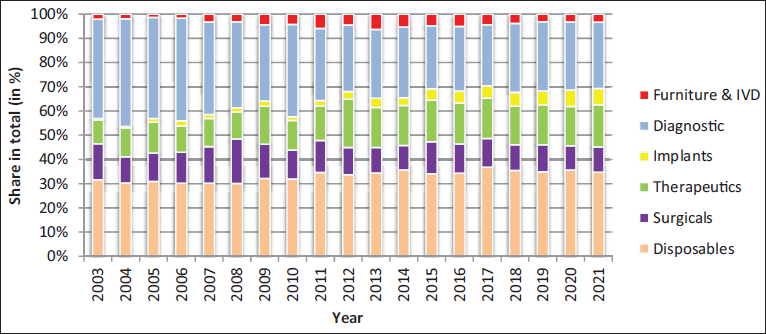

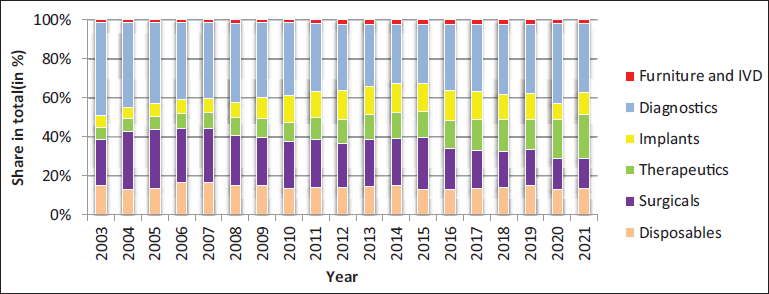

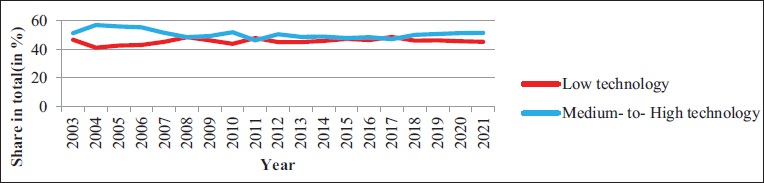

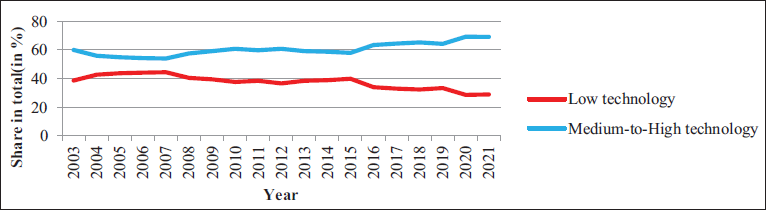

Between 2003 and 2021, the share of medium-to-high technology products declined in India’s medical device exports, while the share of low-technology products increased (Figures 5 and 6). In 2003, around 57% of exports were of medium-to-high technology, while low-technology products contributed 41%. In 2021, the shares of the medium-to-high technology group and the low-technology group were 51.5% and 45.5%, respectively. Indian imports between 2003 and 2021 may be divided into two phases. In the first phase, between 2003 and 2015, India’s imports of medium-to-high technology devices decreased. In the second phase, between 2015 and 2021, India’s imports of medium-to-high technology products increased. These changes led to the widening of the gap between the shares of medium-to-high technology and low technology products in India’s imports and a narrowing of the gap between the two groups in India’s exports of medical devices (Figures 7 and 8).

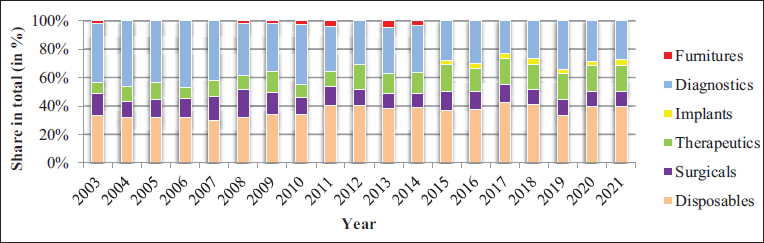

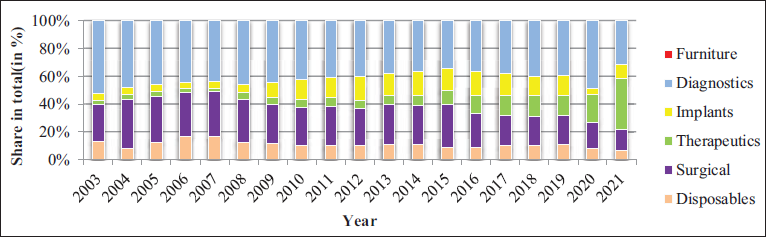

India’s exports of medical devices have been highly concentrated, with the cumulative share of the top 15 products being 87% in 2003 and 75% in 2021 (Figure 9). Likewise, imports of medical devices to India have also been highly concentrated, with the top 15 products having a cumulative share of 87% in 2003 and 80.5% in 2021 (Figure 10). There has been a high overlap between the top 15 products in exports and imports. There was an overlap of seven products in 2003, eight products in 2010, and nine products in 2015. Such overlaps between the top items of imports and exports are suggestive of a high presence of intra-industry trade (IIT) in medical devices.

The RCA index is calculated for India’s device exports (using the trade data at the six-digit HS level) for 2 years, 2003 and 2021. Depending on the RCA values in the 2 years, the products are assigned to any of the three following groups:

Classic—products in which the country had an RCA in both 2003 and 2021. Disappearing—products in which the country had an RCA in 2003 but lost the RCA in 2021. Emerging—products in which the country had no RCA in 2003 but gained RCA in 2021.

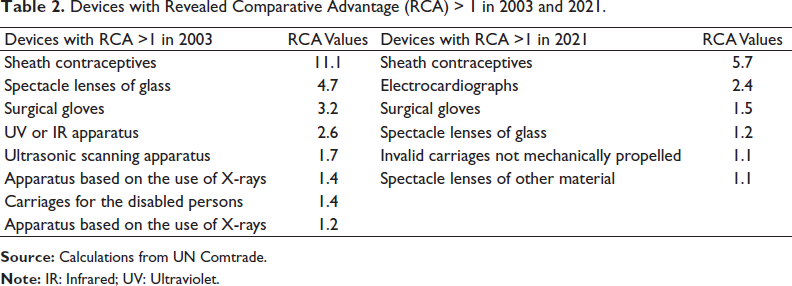

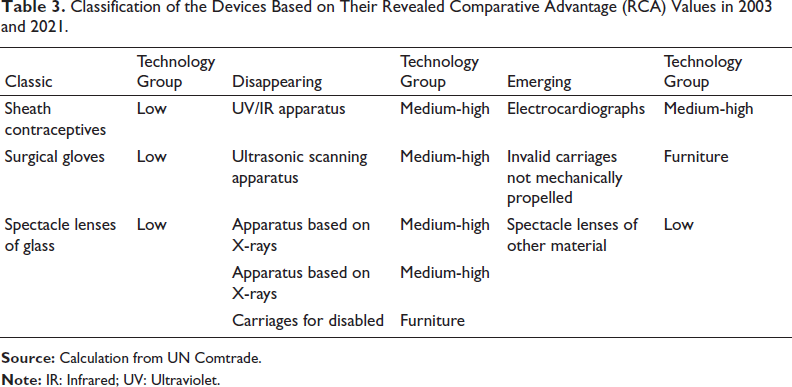

Both in 2003 and 2021, India had the greatest RCA in ‘sheath contraceptives’, a low-tech disposable item (Table 2). In 2003, eight products had RCA > 1, which reduced to six in 2021. In 2021, disappearing products contributed more to exports (11.5%) than emerging products (10.6%) and classic products (7.7%). The number of products in which India lost advantage exceeded the number of products in which it gained advantage, leading to an overall reduction in the country’s competitiveness in the world market. Disappearing products included medium-to-high technology diagnostic products, like ‘ultrasonic scanning apparatus’ and ‘apparatus based on X-rays’, while classic products comprised of low technology items, like ‘sheath contraceptives’, ‘spectacle lenses, glass’ and ‘surgical gloves’ (Table 3).

Devices with Revealed Comparative Advantage (RCA) > 1 in 2003 and 2021.

Devices with Revealed Comparative Advantage (RCA) > 1 in 2003 and 2021.

Classification of the Devices Based on Their Revealed Comparative Advantage (RCA) Values in 2003 and 2021.

The Grubel–Lloyd (GL) index is the most commonly used measure for measuring two-way IIT. The index is given as:

where

According to Fontagné and Freudenberg (1997), trade is considered to be TWT or IIT for any product when the value of the minority flow is at least 10% of the value of the majority flow, that is, they fulfil the following condition:

and

If the minority flow is less than 10% of the majority flow, it is considered to be OWT. Once OWT has been defined and removed from total trade, TWT remains. The next step is to separate these TWT flows into those that are similar in quality (horizontal IIT or

where

The PQV index provides a measure of vertically differentiated quality dispersion in total TWT flows. The index is one when the unit value of exports equals the unit value of imports, that is, all TWT flows are equal in quality, and there is no vertical IIT; it is less than one when the unit value of exports is less than the unit value of imports; and it is more than one when the unit value of exports is more than the unit value of imports. Vertically differentiated trade in high-quality products

Azhar and Elliott (2006) suggest that if imports and exports of any product share at least 85% of their costs (costs here are reflected in the value or price per unit of output), it can be taken as TWT in horizontally differentiated products. This suggests a value of 0.15 for

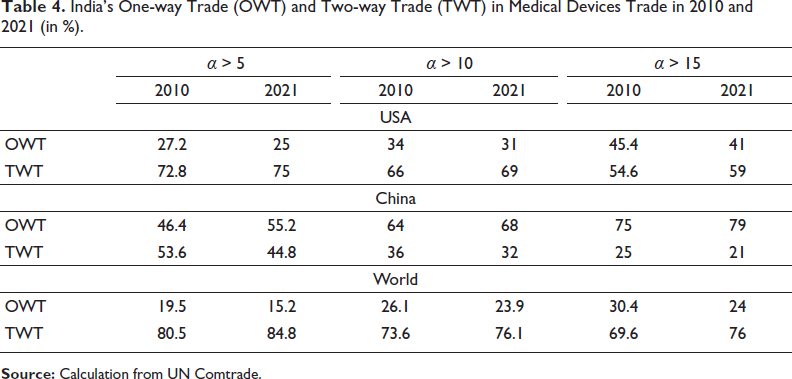

Table 4 gives the classification of trade in 2010 and 2021 into OWT and TWT based on different cutoff values for α. For α at 10%, in 2010, 73.6% of India’s global trade in medical devices was TWT. OWT made up only 26.1% of the total trade. In 2021, 76.1% of India’s total trade comprised TWT, reducing the contribution of OWT to 23.9%. 6 While India’s bilateral trade with China in medical devices is dominated by OWT, that with the USA is dominated by TWT. Between 2010 and 2021, India’s bilateral trade with China became more of the OWT type, while that with the USA became more of the TWT type—in 2010, 36% of India’s bilateral trade with China and 66% of India’s bilateral trade with the USA were TWT trade, which, in 2021, reduced to 32% for China and increased to 69% for the USA. Since αat 5% and 15% also yield similar patterns, the following analysis is done only for α at 10%.

India’s One-way Trade (OWT) and Two-way Trade (TWT) in Medical Devices Trade in 2010 and 2021 (in %).

India’s One-way Trade (OWT) and Two-way Trade (TWT) in Medical Devices Trade in 2010 and 2021 (in %).

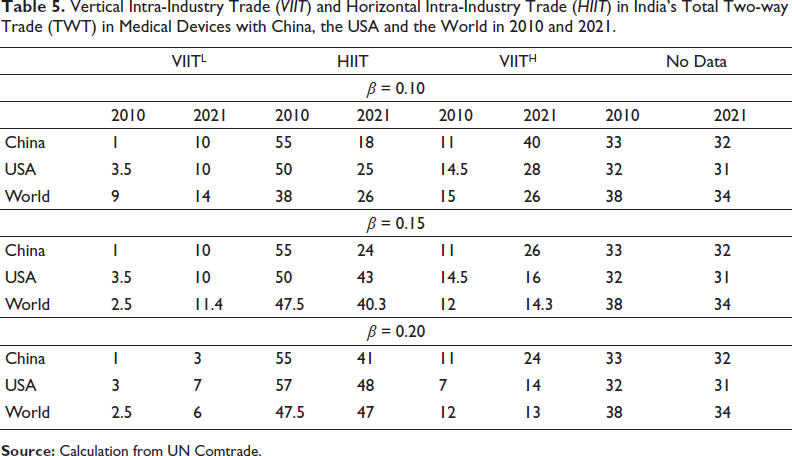

Table 5 differentiates between qualitatively different TWT flows across the various use-based medical device categories.

7

At the threshold level of β = 0.15, between 2010 and 2021, India’s TWT trade with the world became more of the VIIT type—

Vertical Intra-Industry Trade (VIIT) and Horizontal Intra-Industry Trade (HIIT) in India’s Total Two-way Trade (TWT) in Medical Devices with China, the USA and the World in 2010 and 2021.

A country having VIITL can be said to be a net quality importer of that product, while, if it has VIITH, it is a net quality exporter of that product. If trade is of the HIIT type, the country exports and imports goods of similar quality. In 2010, in her trade with the world, India was a net quality exporter of three products, which increased to five in 2021 (Table 6). In both 2010 and 2021, in bilateral trade with the USA, India was a net quality exporter of four products, while in bilateral trade with China, in 2010, India was a net quality exporter of two products, which increased to three in 2021. 8

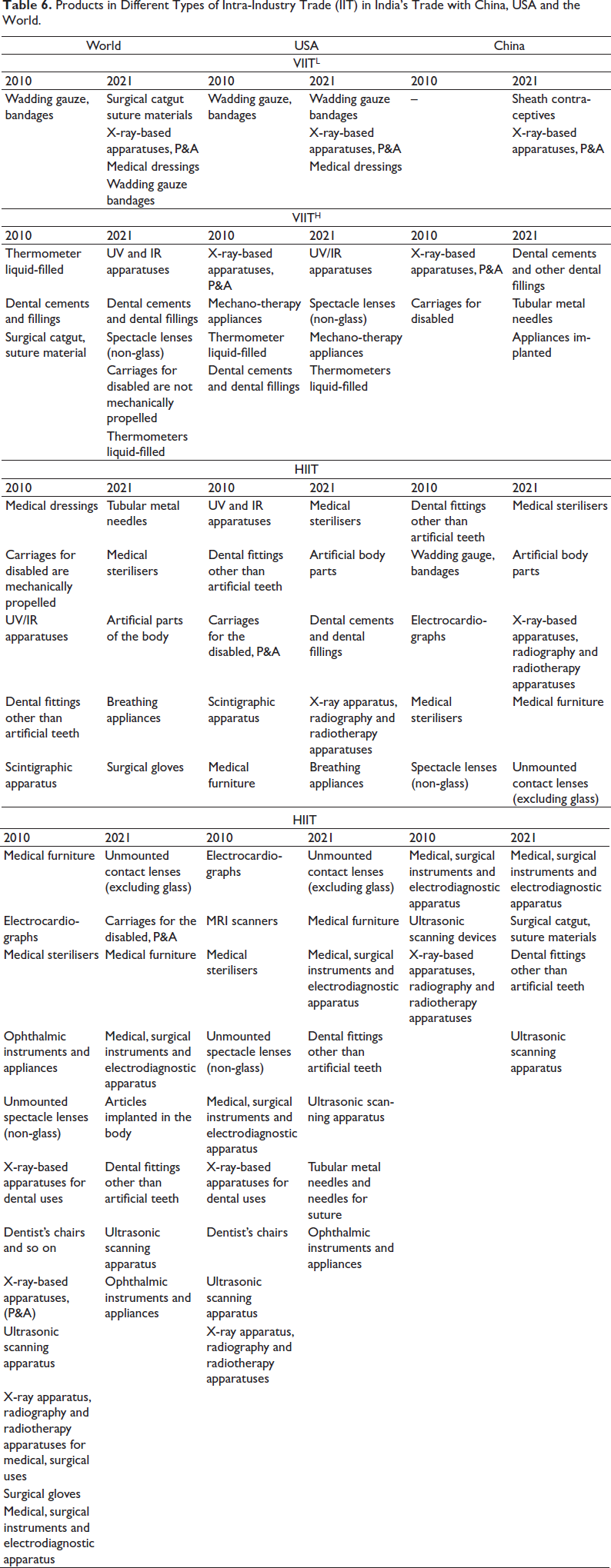

Products in Different Types of Intra-Industry Trade (IIT) in India’s Trade with China, USA and the World.

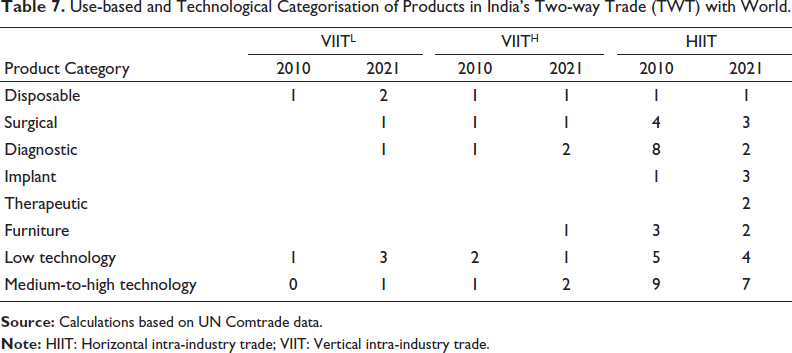

In products that belong to the medium-to-high technology group, India’s trade with the world has been mainly of the HIIT type (Table 7). In 2021, India had HIIT in 13 products, of which seven belonged to the medium-to-high technology group. In 2021, India had VIITL in three low-technology products, while it had VIITH in two medium-to-high technology products and a single low-technology product. At the product level, (either in 2010 or in 2021), we find that India had HIIT in diagnostic products like ‘electrocardiographs’, ‘magnetic resonance imaging (MRI) scanners’, ‘ultrasonic apparatuses’, ‘electrodiagnostic apparatuses’ and ‘X-ray-based apparatuses’, VIITH in diagnostic products like ‘thermometers’, ‘ultraviolet (UV) & infrared (IR) apparatuses’, ‘X-ray-based apparatus (parts and accessories)’ and VIITL only in ‘X-ray-based apparatus (parts and accessories)’. Products like ‘electrocardiographs’, ‘MRI scanners’ and ‘ultrasonic apparatuses’ are more value- and technology-intensive than, for example, ‘thermometers’, 9 indicating that even within the medium-to-high technology group, India exhibited HIIT in more value- and technology-intensive products, while it exhibited VIITH in simpler products like thermometers.

Use-based and Technological Categorisation of Products in India’s Two-way Trade (TWT) with World.

We can also develop a connection between the type of TWT in a particular product and India’s changing competitiveness in it, as seen from the RCA index. For example, out of the three emerging products, India had VIITH in one, ‘carriages for the disabled not mechanically propelled’, in 2021, while in ‘unmounted spectacle lenses excluding glass’ it had HIIT. Among the disappearing products, in 2021, India had HIIT in two products—‘ultrasonic scanning apparatuses’ and ‘carriages for disabled parts and accessories’. It had VIITH in one product, ‘UV and IR apparatuses’, and it had VIITL in one product, ‘apparatuses based on X-ray, parts and accessories’. This indicates that, between 2003 and 2021, India could not retain competitiveness in products in which it had VIITH or HIIT. 10

This article finds that the medical device trade has had a marginal contribution to India’s total exports from 2003 to 2021, and India’s contribution to world exports of medical devices was minuscule during this period. Indian imports of medical devices always exceeded their exports, leading to a negative trade balance across all years. Both exports and imports were highly regionally concentrated, with more than 55% of imports coming from the USA, Germany, China and Japan and more than 80% of exports going to Asia, NAFTA and Europe.

During the last decade, India’s trade with the world became more of the TWT type, and within TWT, trade in differentiated products increased, while that is similar products declined (VIIT increased and HIIT declined). India’s imports became more biased toward medium-to-high technology products, while in exports, low-technology products become more prominent. 11 Within TWT, quality analysis using the PQV index suggests that India traded in products of similar quality (HIIT) for medium-to-high technology, while it was a net quality exporter (VIITH) of simpler products. Furthermore, between 2003 and 2021, India could not retain competitiveness in exports of products for which it was either a net quality exporter or traded in goods of the same quality.

Exports, taken as a proxy for domestic manufacture, imply that the local industry in India has not seen much technological upgrading, is more focused on manufacturing low-technology items, and is falling behind in manufacturing technology-intensive devices. In this regard, the recently introduced PLI scheme for technology-intensive products is a welcome step. Under this scheme, the government provides financial incentives to selected companies based on their threshold investment and incremental sales, for manufacturing technology-intensive devices like MRI and computed tomography (CT) scanners, linear accelerators, cath labs and so on. Thirty-two applicants have been approved under this scheme. 12 Aided by the scheme, increased local manufacture of such products will lead to industrial upgrading. Further, over time, higher local production of technology-intensive products can reduce dependence on imports, increase India’s RCA, and make India a net quality exporter of such products.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest regarding the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.