Abstract

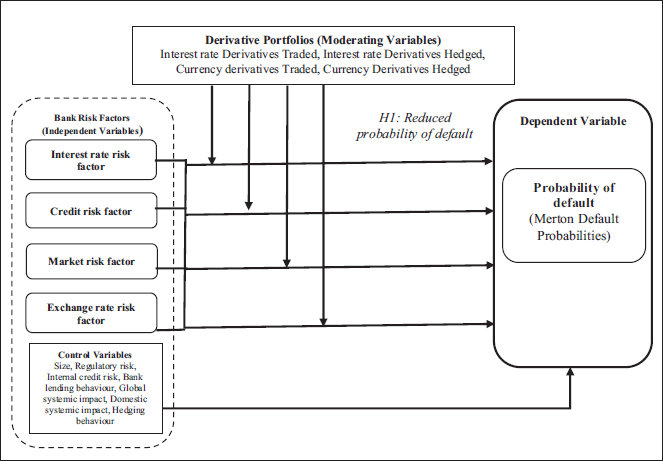

Banks’ role as financial intermediaries necessitates the use of financial derivatives for trading and hedging, and exposes banks to the probability of default. This unattended default probability, along with the external risk exposure of banks, translates into contagious risk. This three-dimensional effect between derivative usage, external risk and default probability leads to economic failure. Studies rarely address the fact that derivatives are an intermediary (moderator), used to either transfer or diversify the risk absorbed through financial intermediation. This article aims to identify the moderating impact of derivatives on the relationship between banks’ probability of default and banks’ risk exposures. The study involves data from 110 commercial banks between 2005 and 2019 to perform a moderation effect on pooled panel data. Results show that the hedged derivatives, along with the market risk factor and the exchange rate risk factor, have a significant moderating effect on the default probability of banks. It is further identified that the default probability of a systemically important bank is linked to the default of its financial system of home or parent country (D-SIB) rather than global economic system.

Keywords

Introduction

Commercial banks, as intermediaries, take the upper hand in the function of financial intermediation. The transaction cost and information asymmetry of the intermediation process navigate the banks towards a risk transformation process for survival (Diamond, 1984), which otherwise increases the bank defaults internally and externally. Banks diversify risk through changes in investment avenues, entering into financial innovation, monitoring borrowers and maintaining capital reserves quoted by regulators to absorb unexpected losses that may impact the depositors. Hence, maturity transformation and risk transformation are inevitable to maintain market discipline in the intermediation process.

Most often, derivatives serve as risk management instruments, but they often uncover their default side. This three-dimensional cum moderating relationship between derivative usage, external risk and default probability has led to the failure of economic systems around the world. Hence, the article aims to identify the moderating impact of derivatives on the relationship between banks’ probability of default and banks’ risk exposures. The study involves data from 110 commercial banks in India, both Indian and foreign, actively operating between 2005 and 2019. Section II of the article deals with theoretical linkage, novelty of research and the development of the research question. Section III describes the sample, data and variables of the study, and Section IV covers methodology, derivatives as moderators of risk, testing of the hypothesis, results, implications and conclusion.

Theoretical Linkage

The failure in the risk–return trade-off in the financial structure of a ‘too big to fail’ (TBTF) organisation leads to a capital shortfall. Not all capital shortfalls translate into systemic risk that leads to default. It begins with systematic risk for the organisation and then contributes to the probability of default. In the case of banks, the unattended default probability of ‘TBTF banks’ (BCBS, 2021) becomes contagious risk through the interconnected nature of the banking system and eventually the country faces an economic crisis (Fiordelisi & Marques-Ibanez, 2013). To counteract such events, the Bank for International Settlements (BIS) enforced adequate capital ratios. Hence, managing default probabilities and maintaining capital adequacy norms are considered primary macroprudential factors in asset quality management. Even though the three pillars of the Basel Committee focus on the regulation of all categories of banking risks, primary focus has always been given to credit risk, along with stress testing, for it is the core risk of the banking business.

The seminal work of Robert C. Merton in 1973 on option pricing, extended into Black–Scholes formula of option pricing in the same year, furthered the application of the model in all suitable research areas. Many studies have been attempted using the model to measure the credit risk of financial institutions (Fiordelisi & Marques-Ibanez, 2013; Hilscher & Raviv, 2014; Parrado-Martínez et al., 2019; Peresetsky et al., 2011) and non-financial institutions (Lozinskaia et al., 2017; Singh & Mishra, 2016) or of a particular financial instrument (Jouault et al., 2011), often extending to the banking industry since banks are linked to the economic health of the nation.

These models are targeted in two directions, namely the accounting approach and the structural approach, which includes market factors. The work of Altman (1968) and Ohlson (1980) enhanced further exploration of default or stability literature in the accounting method. The structural models of Scholes and Black (1973) option pricing theory and Merton (1973) prompted empirical studies on probability of default models at the market level. Studies with the Merton Model (MM) do not include financial innovation, whereas studies on VaR models give more importance to financially innovative instruments (Acharya, 2009; Berkowitz & O’Brien, 2002; Duffie & Pan, 1997; Jorion, 1996). The work of Fahlenbrach et al. (2012) is the only work which links the probability of default with financial derivatives.

Considering the vast literature, a morphological analysis was conducted on the derivatives literature between 1995 and 2019. Eight research gaps were systematically brought out, and one among them was the ‘Moderating role of currency derivatives on the relationship between bank risk exposure and probability of default’ (Nisha A & Madhumathi, 2022b). The existing studies that use VaR models focus only on market variables, whereas Merton’s default model includes both internal and external default risks of a financial entity and has been underutilised in derivatives literature.

Research Question and Hypothesis

Constant occurrence of financial crises with derivative downfalls indicates the need for exploration on the role of derivatives over banks’ risk exposure. Being precautious before the risk occurs is the only resort for banks to manage uncertain failures. Therefore, identifying whether derivatives used by banks for hedging and trading have any moderating impact on their default probability is a gap in the literature and is converted into the following researchable question and hypothesis.

‘Do derivatives moderate bank risk exposure and its impact on default probability of banks?’

H1: Derivative portfolios moderate the relationship between bank risk and its impact on the default probability of banks.

Novelty of the Research

The current research gap is the outcome of a systematic analysis of the derivatives and risk management literature. Although studies like Venkatachalam (1996) exhaustively analysed the hedging and trading impact of derivatives, they fail to study the linkage between hedge and trade behaviour with respect to default probabilities. When compared to the VaR model, the MM is a holistic approach that combines both internal and external default.

Most of the emerging nation studies use balance sheet liabilities as a proxy for market debt while calculating the MM, but this study attempts to adjust the book value of liabilities to the unknown market value of debts using Löffler and Posh’s (2007) methodology to calculate default probability. When NPAs are the major source of credit risk, the present study incorporates changes in bond rates as an external credit risk of banks. Inclusion of foreign banks brings out challenging results and adds contribution to the existing literature as the number of foreign banks operating in India is 49% of the total banks selected for the study.

The categorisation of banks as TBTF by the BCBS has been a less tapped phenomenon in published banking literature in terms of derivatives. These banks are too large and deeply interconnected to other banks in the domestic and global financial system that their default would corrupt the soundness of the corresponding economic system. Hence, the framework of calculating systemically important banks (SIBs) includes factors related to the size, interconnectedness and complexity of the bank (BCBS, 2021). The G-SIB banks are identified by the BCBS, whereas D-SIB banks are identified by the central bank of every country using a similar framework. Thus, considering the relatedness of TBTF to the default probability, the variable has been added to the study as one of the controls. Therefore, the present study’s methods and results might be relevant to an emerging country’s banking system.

Data and Variables

Sample Selection and Data

The study covers all commercial banks in India in the past 15 years, between 2005 and 2019, including the foreign banks, small finance banks, along with the public and private banks operating in India. There were a total of 119 scheduled commercial banks listed on the RBI website by the end of March 2020. Only 110 banks made it to the selection list for the study, and nine were dropped either for discontinued operation or non-availability of data for a minimum of 3 years. The data required for measuring various risk factors, bank-related variables, global indices or lists, and international and Indian level notional prices of financial derivatives have been collected from the databases of Bloomberg, BIS, NSE, BSE, RBI and Centre for Monitoring Indian Economy (PROWESS). Table 1 provides a detailed description of all the variables of the study.

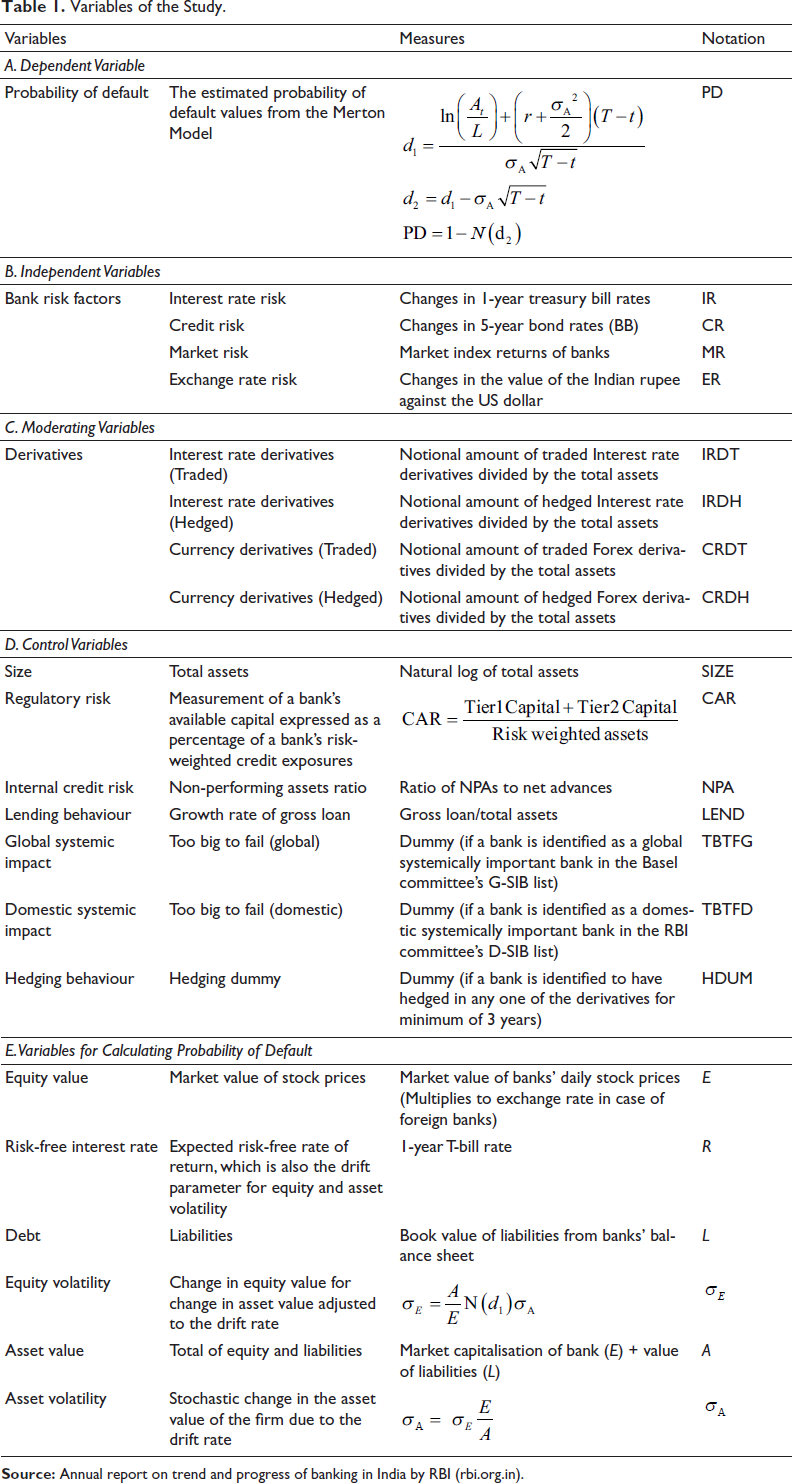

Variables of the Study.

Variables of the Study.

Hypothesised Independent Variables

The current study adopts market-based risks. The firm-level risks in macroeconomic perspectives are considered and brought under the title bank of risk factors, namely interest rate risk, credit risk, foreign exchange risk and equity risk. Based on the capital market perspective, the risk factors are derived from the publicly available market domain. The proxies for bank risk factors have been defined and collected following the methodologies of Begenau et al. (2015) and Nisha A and Madhumathi (2022a), for measurement (Table 1).

Methodology to Derive Risk Exposures (Independent Variables)

Using a market-based model, the returns of 1-year T-bills, 5-year BB bonds, the market index and foreign exchange rate, along with the conditional variance of stock returns, are regressed against the market value of the banks. Using the following regression model, the annual estimates of bank-wise beta coefficients are derived, and these coefficients are used as the proxy for the independent variables of the study, namely market risk, interest rate risk, credit risk and exchange rate risk (Agrawal & Sehgal, 2018; Nisha A & Madhumathi, 2022a; Sehgal & Agrawal, 2017).

Mean equation:

where Rj,

t

is the annualised stock return of bank j at time t; Rm,t is the annual rate of return on the market index (Nifty 500) at time t; Rr,t is the annual rate of change in the 1-year treasury bills at time t; Rc,t is the annual change in the 5-year corporate bond at time t; Rf,t is the annual rate of change of the Indian rupee against the US dollar at time t; hj,t is the conditional variance of bank stock returns; and εj,t is a serially uncorrelated normally distributed random error term. Coefficients βm,βr, βc and βf represent market, interest rate, credit and exchange rate risks, respectively, and β0 is a constant term. The

Variance equation:

Conditional variance, hj,t−1, is determined by the past behaviour of the lagged squared error terms obtained from the mean equation, ε2 j,t −1, is the previous period’s conditional variance, hj,t–1, and the preceding period’s conditional interest rate volatility, CIV t −1. α1 and α2 are the ARCH and GARCH terms, respectively, α3 is the coefficient of lagged interest rate volatility and α0 is the constant. This process results in annual estimates of beta coefficients, which are used as measures of risk.

Hypothesised Dependent Variable: Default Probability of Banks

In the balancing equation (Assets (A) = Liabilities (L) + Owners’ Equity (E)), the typical condition of default happens when the equity owners exercise their option to walk away from the bank by selling off their ownership. The default probability of a bank is a function of its credit risk with respect to the walk-away option held by equity owners during times of economic distress. Since the equity value is considered as an option (European call option) contract, this is where, in the empirical research, the famous MM of probability of default is a suitable model to estimate the probability of bank default.

If the firm pays no dividends, the equity value can be determined with the standard Black–

Scholes call option formula:

where,

r denotes the logarithmic risk-free rate of return, N( ) is the cumulative normal density function, A is the value of assets, L is the face value of debts proxied by total liabilities,

The final estimate of PD is arrived at using the d2 (Distance to Default) values as below:

PD = N(−d2)

The MM of PD requires knowledge of the market value of debt each year. Unlike developed economies, developing economies rarely publish the market value of debt, especially for banks. Hence, the entire estimation of PD is performed using a two-fold method of Löffler and Posh (2007) method of PD calculation, wherein the market value of equity is used to scale the reported debt value of banks, and adjusted asset values and asset volatilities are calculated accordingly. Using Merton’s credit risk model, the yearly probability of default for 110 Indian commercial banks was estimated for 2005 to 2019. The estimated default probabilities are regressed in a hierarchical equation with the independent variables and the interaction variables of derivative portfolios to check for the moderation effect. The variables used for estimating default probabilities of banks are described in Table 1.

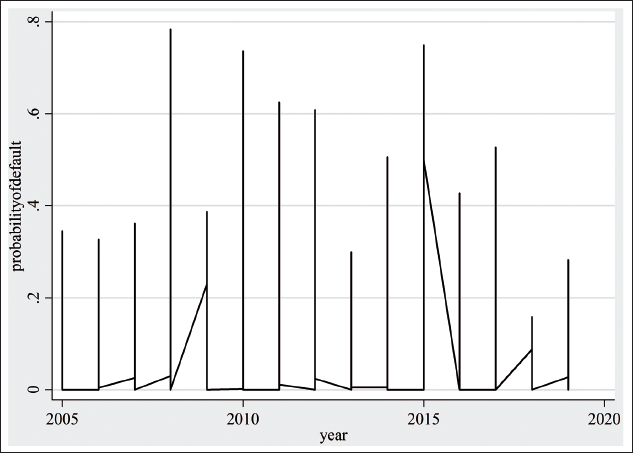

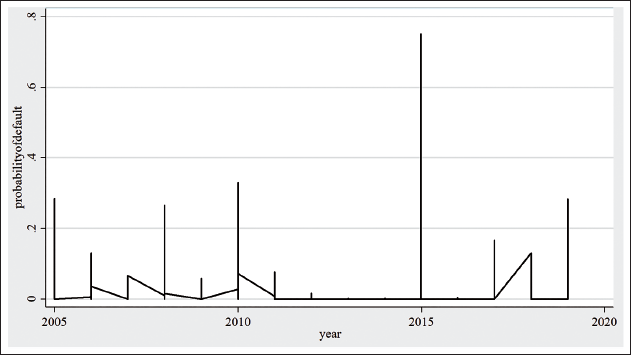

Figure 1 shows the distribution of default probabilities estimated. Every time the probability values went above 0.6, the economy was exposed to events of economic crisis. The subgroup graphs show the time-varying changes in the probability of default values for public sector, private sector and foreign banks. Small finance banks that are added to the study do not have default probabilities due to their short-term existence, lack of trading in their stocks and non-availability of the value of liabilities for more than 3 years. Hence, any available details are added to the category of private sector banks.

From the trend lines, it is evident that during the global financial crisis of 2008, the resilience in the capital markets was brought about through the stable stock movements of public sector banks, but they show rising default probabilities above the threshold of 0.6 during the European crisis (Figure 2). The period of merger of Indian banks (2015–2017) shows rising probabilities due to the consolidated leverage on the State Bank of India (Appendix 2), signalling the need for hedging.

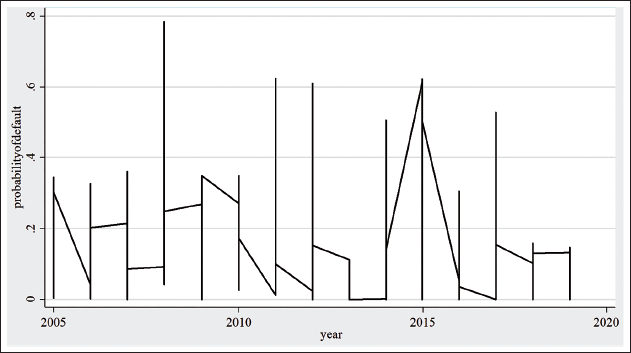

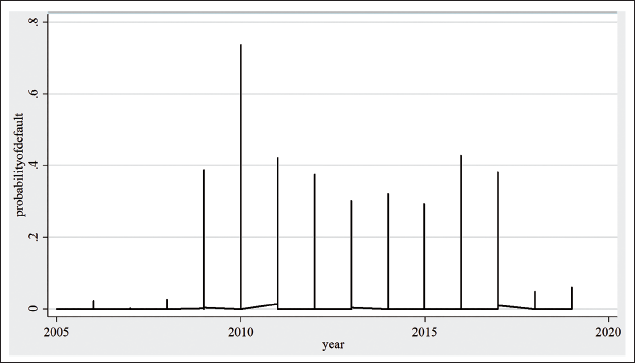

The private sector banks’ graph shows that their default probabilities have touched 0.8, which is close to one, meaning the exact default condition (Figure 3). Foreign banks have remained stable throughout the second decade of the study period, but in the first decade, the year 2010 shows the spillover effects of the European debt crisis on the market values of foreign banks (Figure 4). Hence, a probability of 0.6 can be considered as a threshold value for Indian banks.

Control Variables

The control variables of the study, such as size, regulatory risk, internal credit risk, bank lending behaviour, global systemic impact, domestic systemic impact and hedging behaviour, are chosen from the existing literature with maximum citation for their relevance in risk management, and they are provided in Table 1 with descriptions. The variables global systemic impact and domestic systemic impact are the dummy variables signifying the banks which are recognised as the globally SIBs and domestically SIBs RBI (2022) form the reports of 2021 by the BIS and RBI, respectively. Since the study aims to address the moderating impact of derivatives, further importance is given to the purpose of derivatives, namely hedging and trading. The dummy variables ‘hedging behaviour’ and ‘trading behaviour’ (1 if a bank is identified to have hedged or traded in any one of the derivatives for a minimum of 3 years, otherwise 0) were created to control for the hedging and trading instinct of banks, but ‘trading behaviour’ was dropped due to high multicollinearity.

Derivatives as Moderators and Methodology for Moderation

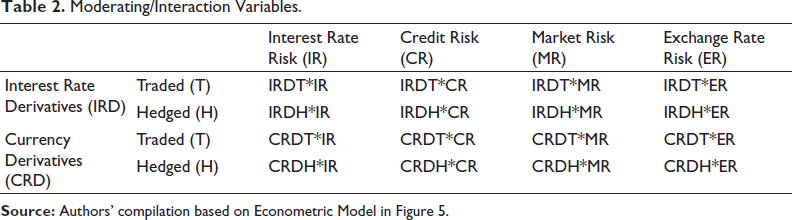

Derivatives, being an intermediary (moderator), are used to either transfer or diversify the risk absorbed through financial intermediation. Tests of moderation are conducted in many forms using a variety of statistical packages. Quantitative research works are often two-tailed due to the continuous nature of the data and its distribution. To run a perfect trivariate model of structural equation in moderation analysis, the dependent variable must be a latent variable, whereas this is not the case in quantitative analyses. Hence, the moderation function is termed the statistical interaction function in quantitative analysis (Hall & Sammons, 2013). Instead of path and structured analysis, interaction variables are generated by multiplying variables of interest with moderating variables and added to the regression model chosen for the study, and to illustrate the same, the following econometric model (Figure 5) is used.

Moderating/Interaction Variables.

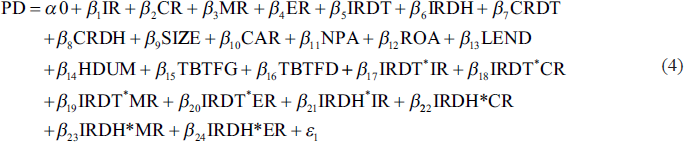

The empirical analysis of moderation begins with a base model using multiple regression to validate the impact of derivatives on banks. There are five stages in this hierarchical regression model. The base equation comprises the dependent variable PD, the independent variables IR, CR, MR and ER, IRDT, IRDH, CRDT and CRDH, and the control variables SIZE, CAR, NPA, ROA, LEND, HDUM, TBTFG and TBTFD. The base model is run with independent variables including derivative portfolios without interaction, control variables and the dependent variable. Once the impact of derivatives on the default probability of banks has been established through the base model, the estimated moderating role of derivatives is checked using a hierarchical regression method with the addition of interaction variables one by one.

Inference and Moderation Method

The independent and interacted moderating variables are by nature continuous variables. Hence, to interpret the results of the moderation effect, the inference methods suggested by Cohen et al. (2003) and Aguinis et al. (2017) for continuous interaction variables are followed. Since the data are set into a panel, a unit root test was performed, and it confirmed that the data are stationary. The correlation between the variables has also been analysed, and it shows significant results (Appendix 1). For performing statistical interaction among continuous variables, the pooled panel regression method is used in a hierarchical fashion, and the derived results are systematically inferred to provide evidence on the moderating role of derivatives on bank risk and its impact on the default probability of banks.

Hypothesis Testing

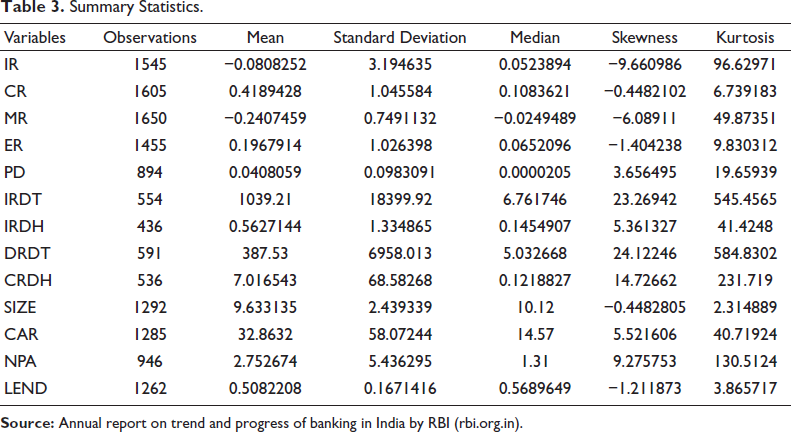

Summary Statistics.

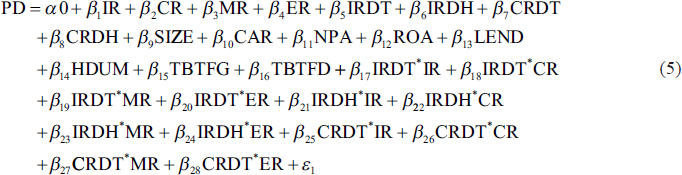

The hierarchical equations with moderated variables (in bold) are added at each stage to the base equation, and the econometric models are given below:

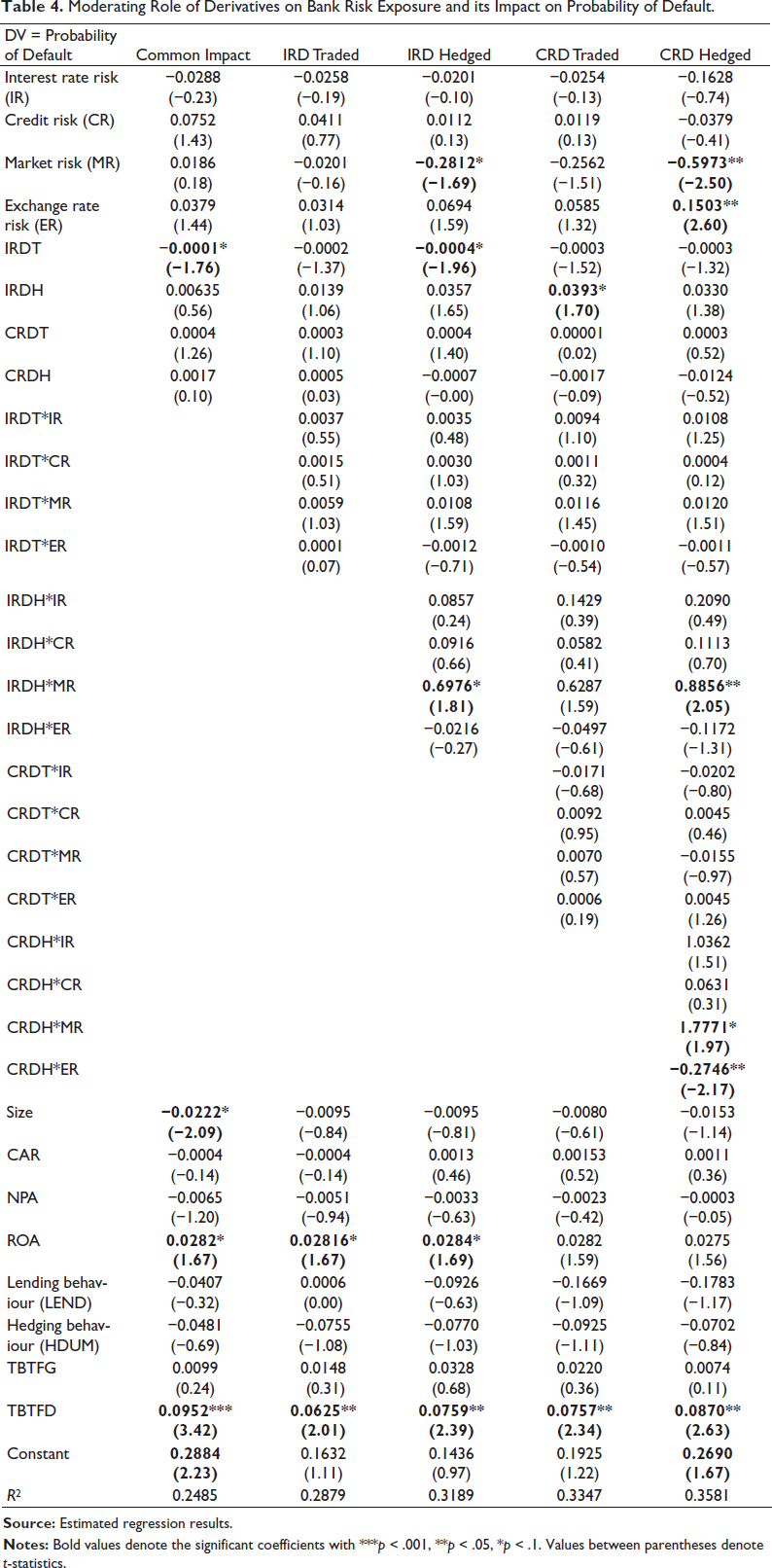

Results of the Moderating Effect of Derivatives on Bank Risk Exposure and Its Impact on the Default Probability of Banks

The hierarchical regression provides the marginal significance of the moderating variables and the incremental impact on the variance brought into the model by the addition of a moderator variable at each level to the existing regression model. Table 4 shows the impact of bank risk factors on the default probabilities of banks and the enhanced, buffering or antagonistic interaction effect (Cohen et al., 2003) in the same relationship given a unit change in the traded or hedged position of financial derivatives. Independently, MR has a negative significance, and ER has a positive significance on the default probabilities of banks at the overall level. This shows that exposure of banks to higher market risk decreases default probabilities, and increased exposure to exchange rate risk increases the default probabilities of banks. Though traded and hedged interest rate derivatives (IRDT and IRDH) have a significant impact in the first four models, in the final model comprising all derivatives, only hedging on derivatives (IRD and CRD) becomes a significant activity by banks.

Moderating Role of Derivatives on Bank Risk Exposure and its Impact on Probability of Default.

Common Impact: No Moderation

This model considers derivatives only as independent variables, not as moderators. Only the IRDT is negatively significant, meaning that banks can reduce their default probabilities by increasing their position in traded interest rate derivatives. Among the control variables, SIZE is negatively significant at 10%. This explains that the greater the total assets, and lesser would be the probability for banks to default. The control variables ROA and TBTFD are positively significant at 10% and 1%, respectively. Hence, when banks try to increase their return on assets, they tend to increase their probability of default, and when a bank is categorised as a domestic systemically important bank (TBTF at the domestic market), then they are also highly significant to the probability of default.

Moderation: Interest Rate Derivatives Traded

When the traded interest rate derivatives are interacted with the bank risk factors and added to the model as moderators, except for the control variables ROA and TBTFD, none of the independent and moderating variables shows any significance to the default probability of banks. The notable change in the moderation is the negative sign of IR and MR without moderation, and it becomes positive after moderation. This change in the direction of the slope of interest rate risk exposure and market risk exposure at a given change in the traded interest rate derivatives, though not significant, does increase the probability of banks’ default. Hence, IRDT as a moderator does not show a significant moderation effect on the impact of bank risk on the banks’ probability of default, but it surely contributes to the probability of default.

Moderation: Interest Rate Derivatives Hedged

In this model, the hedged interest rate derivatives are included as moderators after interacting them with the bank risk factors. The moderator IRDH*MR is positively significant at 10%. The market risk, which is negatively significant at 10% without moderation, has a significant change in the direction of the slope conditional on the given change in hedged interest rate derivatives. This indicates that a change in the hedging position of interest rate derivatives potentially increases the market risk exposure of banks on the probability of default and eventually increases the default probability itself. This is called buffering interaction, wherein the MR variable, which reduced the default probability of banks at an individual level, tends to show increased exposure at the moderated level. Just as in the previous model, the control variables ROA and TBTFD show positive significance on default probabilities.

Moderation: Currency Derivatives Traded

The addition of traded currency derivatives as moderators does not show any significant moderation effect on the probability of default values of banks. The only change in the model is the change of sign for market risk at a moderate level with CRDT on the probability of default.

Moderation: Currency Derivatives Hedged

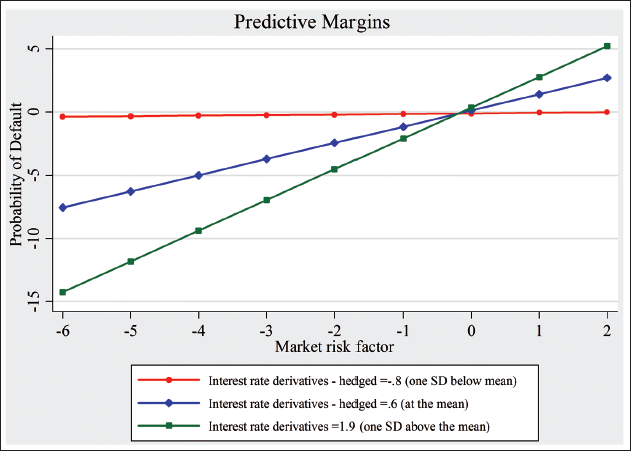

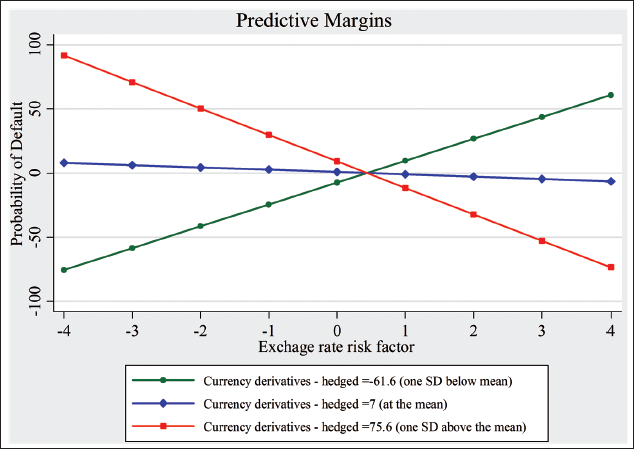

The inclusion of hedged portfolios of currency derivatives along with other derivative portfolios of the study illustrates a significant role of hedging on the probability of default of banks. The hedged derivatives, along with the market risk factor and exchange rate risk factor, have a significant moderating effect on the default probability of banks. The given change in the hedged-interest rate derivatives once again creates buffering interaction by increasing the impact of market risk exposure on the default probability of banks (van Ofwegen et al., 2012) whereas the impact reduces the default probability of banks if market risk is regressed independently without moderation (Figure 6).

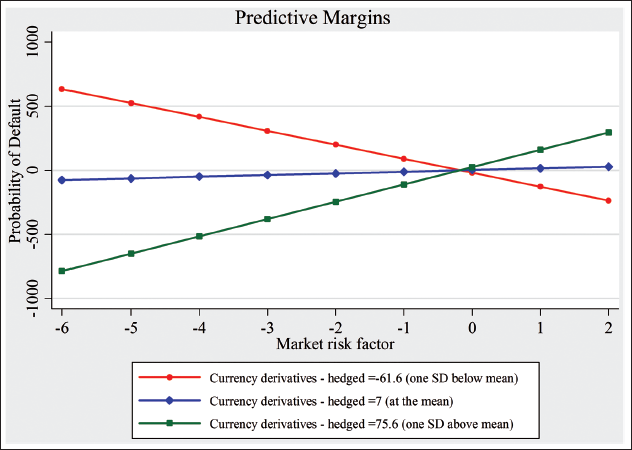

A similar moderation effect is shown by market risk on default probability of banks when interacting with the hedged currency derivatives (Figure 7). In contrast, the similar change in the position of hedged currency derivatives give negative sign to the exchange rate exposure on the probability of banks’ default (Figure 8). Therefore, exchange rate risk tends to diminish the default probabilities of banks, conditional on a given change in the hedging position of currency derivatives. Though derivatives as a hedge are expected to reduce the default probability of a bank, hedging beyond the need to offset liquidity risk may lead to credit and interest rate risk since the excess liquidity will force the banks to increase their credit portfolios.

The negative moderation impact (Figures 6 and 7) supports the proposition of Wagner (2007) that banks reduce their balance sheet risks by facilitating the liquidation of assets through credit derivative instruments. Credit derivatives increase liquidity by shifting the bank risk to the derivative market and increase bank profits initially, but in the long run, with increased liquidity, banks tend to absorb more credit or interest rate risk, and that affects the probability of default condition when economic externalities become unfavourable. Indian banks also exhibit this tendency with increased default probability when interest rate and currency derivative hedge positions increase above average. Whereas, if hedged derivatives are maintained below the average, they tend to reduce the default probability of Indian banks. In the final model, TBTFD is the only control variable that remained significant, indicating the impact of domestic-level systemic bank characteristics on the default probability of banks.

Model Fitness

Comparing the other four models with the fifth model, the R2 value is high for the final model with all moderator variables, which signifies the goodness of fit of the variables used. The probability of default of banks being a highly correlated factor, many bank-level variables and trading behaviour proxy have been dropped due to the problem of high variance inflation factor. With the limited significant variables, the model still explains 36% of the variance in the probability of default through the chosen variables of the study.

Implications

It is verified from the models that only hedging of derivatives shows a moderation effect on the default probability of banks. The significance of the variable TBTFD indicates that the default probability of a systemically important bank is linked to the default of its financial system of the home or parent country, rather than the global economic system. Also, irrespective of the moderating effect of derivatives, the bank characteristics for systemic importance significantly increase the default probability of banks. Market risk exposure generally reduces the probability of banks’ default, but when it becomes conditional to the change in hedged financial derivatives becomes the driving force for bank default. For a bank to remain safe from defaulting when market risk exposure is high, it is better for banks to avoid hedging on financial derivatives. Banks that have the potential to default during the presence of exposure to foreign exchange risk can consider changing their hedging positions on currency derivatives.

Bank’s default happens through many factors. One among them is derivatives. Derivatives gain limelight for their impact on the probability of default, due to their intensity of usage post the financial crisis and because of their wide usage in hedging intermediation risk. The study has taken all the possible variables, avoiding variables causing multicollinearity, to test the moderating effect of derivatives, especially with respect to the purpose for which they are used. The hierarchical model gradually shows the evident moderation effect hedging produces on the default probability of banks. Not through trading but only through hedging, derivatives moderate the probability of default of commercial banks.

In the case of a commercial bank, the test results support that any default probability arising through exchange rate risk can be moderated by increasing hedged portfolios on currency derivatives. It is apparent that hedged-derivative portfolios can be used to moderate the risk arising from default probabilities by merely altering the hedged ratio on derivatives. Hence, it is recommended that banks need to make the right choice to trade or hedge a particular derivative instrument based on the particular risk factor they are exposed to at that very moment when they reach the threshold level of default.

Footnotes

Declaration of Conflict of Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.