Abstract

The author uses German linked employer-employee data to estimate the impact of intra-firm wage dispersion on the probability that establishments pay for further training. About half of all establishments in the estimation sample cover all direct and indirect training costs, which contradicts the standard human capital approach with perfect labor markets. The main finding of cross-section, panel, and instrumental variable probit estimations is that establishments with larger intra-firm wage compression are more likely to cover all direct and indirect training costs, which is consistent with theoretical considerations of the “new training literature” about imperfect labor markets.

Employer-provided further training has received increasing attention in economics during the past decades. One reason is its importance for productivity and economic growth. Another reason is the stimulating theoretical work of the “new training literature” that has further developed the standard human capital framework by Becker (1962). Becker modeled decisions to invest in on-the-job training in an economy with perfect labor markets (e.g., wages equal productivity in all firms, no mobility costs, complete information, no union-bargained collective contracts). His main finding was that firms do not cover the costs for general training and that firms and workers share the costs for firm-specific training. Workers can keep all returns to training in the former case, whereas workers and firms share the returns in the latter case. Since empirical observations suggest, however, that firms are highly involved in training and even pay for general training—for example, the German apprenticeship system (Acemoglu and Pischke 1998; Mohrenweiser and Zwick 2009)—the new training literature has challenged the assumption of perfect labor markets and Becker’s results for training cost coverage (for extensive reviews of the theoretical and empirical training literature see, for example, Asplund 2005 and Leuven 2005).

Eckaus (1963) stated that firms in imperfect labor markets are likely to pay for more training than Becker’s model would predict. For example, firms cannot so easily let workers pay for their training if training and regular output are jointly produced and training costs cannot be perfectly identified. More influential is Eckaus’s notion that firms would have incentives to pay for training if they could capture rents from it, which would be the case for not perfectly mobile workers. Katz and Ziderman (1990) and Chang and Wang (1996) emphasized information asymmetries from which imperfect labor mobility arises. They assumed that current firms have private information about the productivity of a worker after training. Because other firms do not have this information, they cannot pay the same wages as the current firm. Consequently, the current firm has at least to some degree the opportunity to pay wages below the trained worker’s marginal product and to capture rents from training.

A series of prominent articles by Acemoglu and Pischke (1998, 1999a, 1999b) also analyzed the cost coverage of training in imperfect labor markets. The basic rationale is that firms bear training costs if they have monopsony power and can capture rents from training as a result of wage compression (wages relatively more compressed than productivity, wage increases smaller than productivity increases after training [Acemoglu and Pischke 1999a]). Examples are information asymmetries with respect to a worker’s training, ability, and motivation (Acemoglu and Pischke 1998) as well as labor market institutions that affect firms’ wage structures such as employment protection, minimum wages, collective contracts, and codetermination (Acemoglu and Pischke 1999b). Dustmann and Schönberg (2009) focused in their model on unions that increase wage compression when they bargain minimum wages in collective contracts, which in turn increases firm-financed training. They presented empirical support for apprenticeship training in German firms.

To sum up, one core element in theoretical models of the new training literature is that firms with more compressed wage structures (lower intra-firm wage dispersion) should have larger incentives to pay for training because they are better able to capture rents from training. Pischke (2005: 51) concludes: “Strictly speaking, labor market institutions are not really necessary for this argument, although the example of a minimum wage highlights the workings of the model nicely. However, what is necessary for firms to invest is simply that the wage structure w(t) is compressed, i.e. that w(t) is flatter than f(t) [wages w and productivity f are functions of the level of training t]. If this is the case, then the rents the firm can earn from more skilled workers will be greater than the rents earned from less skilled workers. Hence, it may invest in training.” Consequently, firms with more compressed wage structures should also be more likely to cover all training costs. I test this hypothesis below by using linked employer-employee data for large profit-maximizing establishments in Germany, which allows me to generate conditional intra-firm wage-dispersion measures. In doing this, I partly follow the suggestion by Acemoglu and Pischke (1999b: 567) that “[f]uture empirical work should test the more micro-level implications that follow from our analysis and contrast them with those of the standard theory.”

Although a large number of empirical studies on firms’ determinants of training already exist for Germany (e.g., Düll and Bellmann 1998, 1999; Gerlach and Jirjahn 2001; Gerlach, Hübler, and Meyer 2002; Allaart, Bellman, and Leber 2009; Bellmann, Hohendanner, and Hujer 2010; Goerlitz 2010; Stegmaier 2010; Goerlitz and Stiebale 2011) and other countries (for literature reviews see, for example, Asplund 2005 and Leuven 2005), only a few studies have explicitly examined firms’ determinants of training cost coverage (Leber 2000; Bellmann and Düll 2001). From several empirical studies, we know, however, that firms bear most of the direct training costs and that much of the training is general (e.g., Loewenstein and Spletzer 1998, 1999 and Barron, Berger, and Black 1999 for the United States; Pischke 2001 for Germany; Booth and Bryan 2005 for the United Kingdom). In my estimation sample, about half of all training establishments cover even all indirect and direct training costs—that is, the training takes place during paid working time and the establishment pays for all outlays such as course fees and travel costs. Such a complete training cost coverage is of course largely inconsistent with Becker’s model, because in that model establishments would not pay at all for general training and only partly for firm-specific training.

As far as I know, no econometric study has yet explicitly tested whether a positive correlation between intra-firm wage compression and cost coverage of employer-provided further training exists. Two studies by Almeida-Santos and Mumford (2005) and Ericson (2008), however, looked at the relationship between wage compression within occupations and individual worker’s training participation. Almeida-Santos and Mumford (2005) found with British linked employer-employee data a negative correlation between wage dispersion and training incidence and duration—that is, more compressed wages lead to more training. Ericson (2008) found with data from the Swedish Labour Force Survey that general training duration is positively correlated with wage dispersion, whereas the duration of firm-specific and mixed training is not significantly affected by the wage dispersion measures. In both studies, however, the wage compression proxies measured not the intra-firm wage dispersion but the wage dispersion within occupations and across firms. For Germany, Beckmann (2002a, 2002b) analyzed indirectly the effect of wage compression on apprenticeship training by using proxies such as collective contract coverage, which positively affects the probability and intensity of apprenticeship training.

Data and Estimation Strategy

Estimation Sample

The data I use are the cross-sectional models of the German linked employer-employee data set of the Institute for Employment Research (LIAB) (Alda, Bender, and Gartner 2005). 1 The LIAB links employer-side information from the IAB Establishment Panel with employee information from administrative data. The administrative employee data stem basically from the notification procedure for unemployment, pension, and health insurances. Employers must notify the social security agencies about all employees who are covered by social security at the start and at the end of an employment relationship as well as on the last day of each year. These administrative employee data include socio-demographic characteristics and individual daily gross wages of workers (in euros), which are used to generate variables for the conditional intra-firm wage dispersion as an inverse measure for wage compression. Disadvantages of the data are that no information about working hours is available and that wages are censored at the upper earnings limit for social security contributions. 2 Because of the absence of working hours in the data, meaningful aggregate wage variables at the establishment level can be computed only for full-time workers (with the exclusion of apprentices, trainees, etc.). The wage censoring leads to a downward bias when proxies for intra-firm wage dispersion are generated because we observe too low wages (wages equal the social security contribution limit) for high-wage workers (wages above the social security contribution limit). This bias should, however, be much smaller for conditional than for unconditional wage-dispersion measures (e.g., standard deviation of workers’ wages in an establishment) because the conditional wage dispersion takes into account differences in worker characteristics (e.g., qualifications) and explicitly right-censored wages by applying censored regression techniques such as Tobit regressions.

As the focus is on establishments’ determinants of complete cost coverage of further training, the IAB Establishment Panel is the main data source for the subsequent analysis. The panel contains data on establishments from all sixteen German federal states (Bundesländer) and all industries. Every year more than 15,000 establishments with at least one employee covered by social security are interviewed in an unbalanced panel design survey. The sample is stratified according to 10 establishment sizes and 16 industries in each federal state, with oversampling of larger establishments. The observational unit is the establishment—that is, the local unit in which major activities of an enterprise are carried out. The main goal of the survey is to gain insights into the establishment’s most important parts of operation, decision making, and more specifically employment.

For the purpose of this study, I use the waves 2005 and 2007 because they contain information about coverage of direct and indirect training costs. 3 Because of the interest in establishments’ profit-maximizing rationales for training cost coverage, the sample is restricted to profit-maximizing establishments from the private sector that have trained at least one worker in the first half of a survey year. As training is likely to occur not continuously (i.e., most workers are likely to receive their training once in a while and not the same amount of training in every time period or always in the first half of a survey year), the sample is further restricted to establishments with at least 100 workers to mitigate this problem. The sample restriction to larger establishments is also preferable in order to make the wage-dispersion measures at the establishment level meaningful. Because only full-time workers are considered for the generation of wage variables at the establishment level, I impose the additional restriction that there be at least 10 such workers in the establishment from whom the wage information is generated. Finally, I considered only those establishments without missing values in the variables I used. In total, 2,118 establishments for the year 2005 and 2,011 establishments for the year 2007 remain in the sample for the subsequent empirical analysis. Of these, 1,136 are represented in both years—that is, in 2005 as well as 2007 (balanced panel).

Estimation Strategy and Variables

To analyze establishments’ determinants of complete training cost coverage, I generate a binary variable (COSTCOV), which takes the value 1 if an establishment states that it usually pays for all direct costs (e.g., course fees, travel costs) and also bears the indirect costs (i.e., the training takes place during paid working time). 4 About half of the establishments in the sample completely cover all training costs. Because of the binary dependent variable, I estimate binary probit models. The explanatory variable of main interest is the intra-firm wage compression, for which a proxy can be generated from the administrative employee data. The simplest approach would be to use the standard deviation of full-time workers’ daily wages in a given establishment, which would measure the unconditional wage dispersion. This dispersion has, however, the disadvantage that it does not account for differences in worker characteristics such as qualifications, which affect productivity and wage classifications. Therefore, a conditional wage-dispersion measure is a much better proxy for wage compression.

I follow the approach of Winter-Ebmer and Zweimüller (1999), who analyzed the effect of intra-firm wage dispersion on establishment performance. 5 Exploiting the nature of the linked employer-employee data set, I estimate log-linear Mincer earnings functions for full-time workers separately for every establishment in a given year. The dependent variable is the log of workers’ individual daily wages. The explanatory variables include the usual productivity-related individual worker characteristics such as age, squared age, tenure, squared tenure, highest qualification categories (no job qualification as reference group, apprenticeship degree, university degree), and a female dummy. To account for censored wages in the data, I estimate Tobit regressions with different upper earnings limits for East and West Germany as well as for the year 2005 and the year 2007. 6 On the basis of the results for an establishment’s earnings function, I then generate the standard error of the Tobit regression as a proxy for the intra-firm wage compression (logWSERT). The standard error of the regression in an establishment can be interpreted as the standard deviation of workers’ individual error terms in an estimated earnings function for this establishment in a given year. A larger standard error of the regression indicates a larger conditional intra-firm wage dispersion and consequently lower intra-firm wage compression.

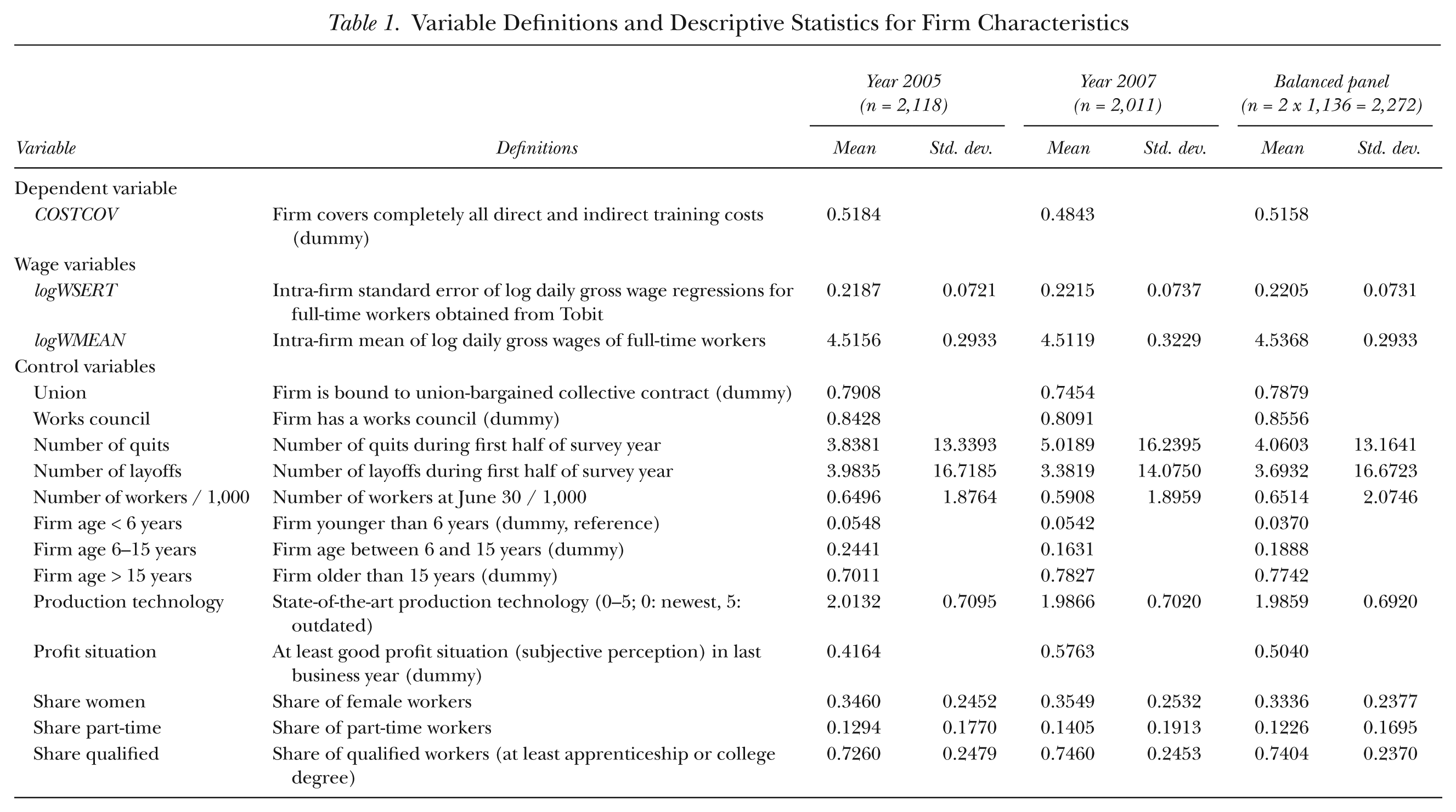

Descriptive statistics for the intra-firm wage compression proxy (logWSERT) are displayed in Table 1. Mean standard errors of the regressions are on average approximately 0.22 with a standard deviation of 0.07. 7 When comparing the means and standard deviations of my estimated standard errors of the regressions with the results of Winter-Ebmer and Zweimüller (1999), I find only small differences. Winter-Ebmer and Zweimüller (1999) used data of workers in 130 firms, which were obtained from Austrian social security records for the years 1975 to 1991. Their estimated standard errors of Tobit regressions for the log of monthly income have a mean of 0.205 with a standard deviation of 0.074.

Variable Definitions and Descriptive Statistics for Firm Characteristics

Because a larger standard error of the wage regression (logWSERT) might be the result of larger wage levels in an establishment, the probit regressions for COSTCOV also include the mean of log daily wages of full-time workers in an establishment in a given year (logWMEAN) as a control variable. The probit regressions further control for important differences between establishments that might affect training as well as wage structures. Industrial relations are important in this context because unions and works councils are often associated with more compressed wage structures and more training for workers (e.g., Acemoglu and Pischke 1999b; Dustmann and Schönberg 2009). Moreover, the regressions include variables for the number of layoffs and quits, the number of workers, three establishment age categories, state-of-the-art production technology, profit situation, share of women, share of part-time workers, share of qualified workers, 16 federal state dummies, and 15 industry dummies, which should control for a large set of potential differences between establishments with different degrees of wage compression. Table 1 presents complete variable definitions and descriptive statistics.

I estimate the determinants of cost coverage (COSTCOV) using binary probit models for the separate cross-sections 2005 and 2007 as well as a random-effects probit model for a balanced panel. The random-effects model serves mainly as a robustness check to account for within-establishment variance, because a likelihood-ratio test rejects the hypothesis that the within-establishment variance does not significantly contribute to the total variance. I choose the random-effects model over a fixed-effects model for several reasons. At first, no consistent fixed-effects estimators exist for probit or logit models in short panels because of the incidental parameter problem. Fixed-effects linear probability models are also not a feasible estimation strategy because training cost coverage, wage structures, and industrial relations are structural establishment characteristics based on strategic decisions; thus changes are not common and are unlikely to be in effect rapidly. Accordingly, within-establishment variance is very low for most variables of interest in my data. Nevertheless, in the robustness check section, I estimate an establishment fixed-effects linear probability model and a correlated random-effects probit model, which explicitly take unobserved establishment heterogeneity into account. Though not statistically significant because of the low within-establishment variance, these estimates support the main findings from the cross-section and random-effects probit models. In an attempt to further check the sensitivity of the main findings, I apply an IV probit approach in the robustness checks, which again supports the main findings that are presented in the next section.

Estimation Results

Main Findings

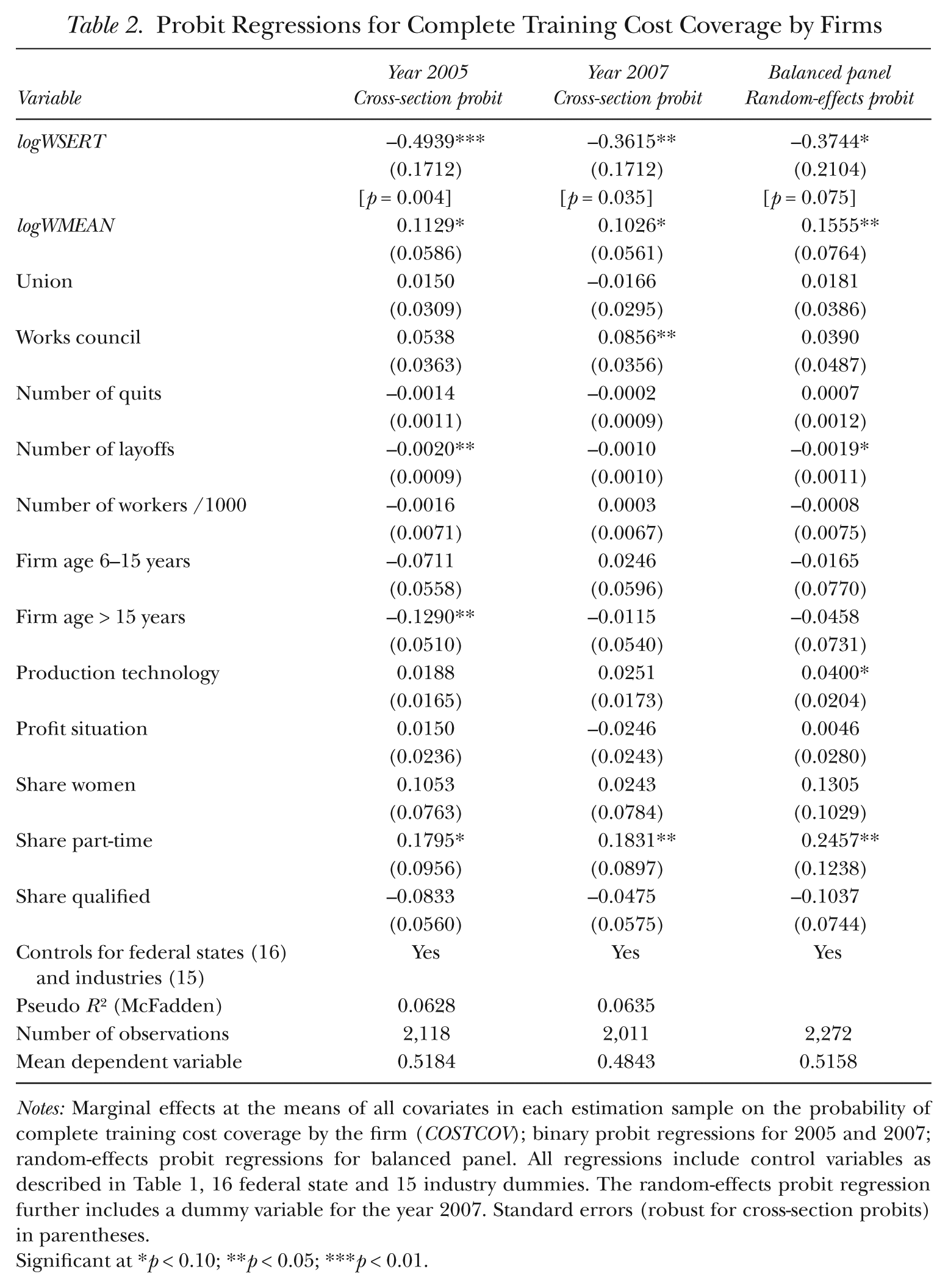

Table 2 presents the results of the binary probit regressions for the probability that an establishment covers completely all direct and indirect training costs (COSTCOV). The first column contains the results of the cross-section probit for the year 2005 and the second column the results for the year 2007. The third column presents the results of the random-effects probit model for the balanced panel. To facilitate the quantitative interpretation, I compute marginal effects at the means of all covariates in each estimation sample.

Probit Regressions for Complete Training Cost Coverage by Firms

Notes: Marginal effects at the means of all covariates in each estimation sample on the probability of complete training cost coverage by the firm (COSTCOV); binary probit regressions for 2005 and 2007; random-effects probit regressions for balanced panel. All regressions include control variables as described in Table 1, 16 federal state and 15 industry dummies. The random-effects probit regression further includes a dummy variable for the year 2007. Standard errors (robust for cross-section probits) in parentheses.

Significant at *p < 0.10; **p < 0.05; ***p < 0.01.

The main finding can be seen from the first row of marginal effects in Table 2. A larger standard error of an establishment’s workforce wage regression (logWSERT) is significantly negatively correlated with the probability that an establishment pays all direct and indirect training costs throughout all three regressions—that is, establishments with lower intra-firm conditional wage dispersion (more compressed wage structures) are on average more likely to cover all training costs. A 0.1 log point higher standard error of the wage regression decreases the cost coverage probability in the year 2005 on average by 4.9 percentage points (p = 0.004) and in the year 2007 by 3.6 percentage points (p = 0.035). 8 The random-effects probit regression yields a comparable marginal effect of minus 3.7 percentage points (p = 0.075) per 0.1 log point higher standard error of the regression. The findings are consistent with the theoretical consideration that establishments can capture rents from training because of intra-firm wage compression, which provides incentives for establishments to pay for further training.

Moreover, the results in Table 2 indicate that unions have no significant effects throughout all regressions, whereas works councils are positively correlated with the probability that an establishment completely covers training costs. Hence, it seems as if establishment-level codetermination is more influential in this context than union bargaining. Only a few control variables significantly affect the cost coverage probability in a consistent pattern across the regressions. Establishments with more layoffs have a lower probability of completely covering all training costs, which might be explained by amortization aspects and a loss in employment flexibility if adjustment costs increase after the establishment has paid for training. Furthermore, the share of part-time workers indicates a positive correlation with the training cost coverage probability. This finding might be surprising at first glance if amortization aspects are taken into account. Because part-time workers are often associated with the flexible part of an establishment’s workforce (periphery), one would expect establishments to invest less in their human capital. There may be several explanations for these findings. First, since I use aggregate establishment-level data, the share of part-time workers, as part of the peripheral workforce, might be an indicator for the existence of dual internal labor markets, in which establishments rely on stable employment relationships with, and provide training for, their core workforce. Second, workers of the peripheral workforce are by definition more often newly employed by an establishment and might need work instructions that are paid for by the establishment. Third, part-time workers have on average lower income, which might lead to credit constraints so that the establishment might have to pay for the training. These interpretations are, however, only speculations that cannot be tested with the data I use.

Robustness Checks

I have performed several robustness checks on the sensitivity of the main findings, summarized below. 9 I have used alternative proxies for the intra-firm wage compression (dispersion) variable. First, I have used the standard deviation of full-time workers’ daily wages in an establishment (unconditional wage dispersion). Second, I have used simple linear regressions instead of Tobit regressions to generate the standard errors of the wage regressions for each establishment. Both alternative variables are negatively correlated with the probability that an establishment pays all training costs at even higher significance levels than the standard errors of Tobit regressions (logWSERT).

The next robustness checks deal explicitly with unobserved establishment heterogeneity. I have applied two panel estimation techniques that are both problematic for my data because of very low within-establishment variance for most variables of interest. Nevertheless, they should be mentioned. First, I have estimated an establishment fixed-effects linear probability model. The estimated marginal effects for the intra-firm wage-dispersion variable have the negative sign known from the previous probit models. Because of the low within-establishment variance, however, the effects are not statistically significant. Still, the results indicate a negative rather than a positive correlation between intra-firm wage dispersion and training cost coverage if time-invariant unobserved establishment heterogeneity is taken into account in a fixed-effects linear probability model. Moreover, I have reestimated the random-effects probit model with additional variables that contain the means of each observed establishment characteristic over time, which is known as Mundlak’s approach (Mundlak 1978). The inclusion of group means in random-effects models controls intuitively for unobserved heterogeneity and allows dependence between the random effects and the regressors. This approach is a widespread method in econometrics and can also be applied for probit models (Chamberlain 1980), which are sometimes called correlated random-effects probit models (for a detailed textbook discussion see, for example, Wooldridge 2010: 610–19). The results of the correlated random-effects models indicate again a negative rather than a positive correlation between intra-firm wage dispersion and training cost coverage, even though the effects are not statistically significant because of the low within-establishment variance.

Another source of endogeneity might be reverse causality—that is, the causal link might not go from wage compression to training cost coverage but the other way around. If establishments pay for training, workers might receive lower returns to training, which decreases wage differentials between trained and untrained workers and consequently increases wage compression. To deal with this endogeneity problem, I have estimated instrumental variable (IV) probit regressions (for detailed discussions see Rivers and Vuong 1988 and Wooldridge 2010: 585–94). Note that IV estimation strategies are also suitable to deal with potential omitted variable biases.

As instruments, which affect the intra-firm wage compression, I use the lowest observed wage of a worker in an establishment and the mean of the intra-firm standard errors of log daily wage regressions within industry and federal state cells. Previous studies about training have often emphasized institutional minimum wages, which are, however, not that common in Germany and not observed in the data. Whereas institutional minimum wages can be seen as exogenous to establishments, the lowest observed wage in an establishment is a rather technical instrument that has the advantage of exploiting large between-establishment variance. The rationales for using the mean of the intra-firm standard errors of log daily wage regressions within industry and federal state cells as a second instrument are norms and spillover effects in regional labor markets (e.g., an establishment’s wage structure is affected by institutional developments in the past and by wage structures of other establishments in the same industry and region). From a theoretical point of view, both instruments should be significantly correlated with the intra-firm wage compression in the first-stage regression. But to be valid instruments, they should have no further direct impact on the probability of training cost coverage in the second-stage regression. The lowest observed wage in an establishment might fulfill this critical condition because it seems unlikely that larger establishments adjust their general employment policies such as training cost coverage explicitly to the lowest-paid worker. For the mean of the intra-firm wage dispersion within industry and federal state cells, it is, however, not so easy to justify this condition because norms and spillover effects in regional labor markets that affect establishments’ wage structures might also affect their decisions about training cost coverage. Besides these potential problems, I start with IV probit estimates that use both instruments before using the lowest observed log daily wage in an establishment as a single instrument.

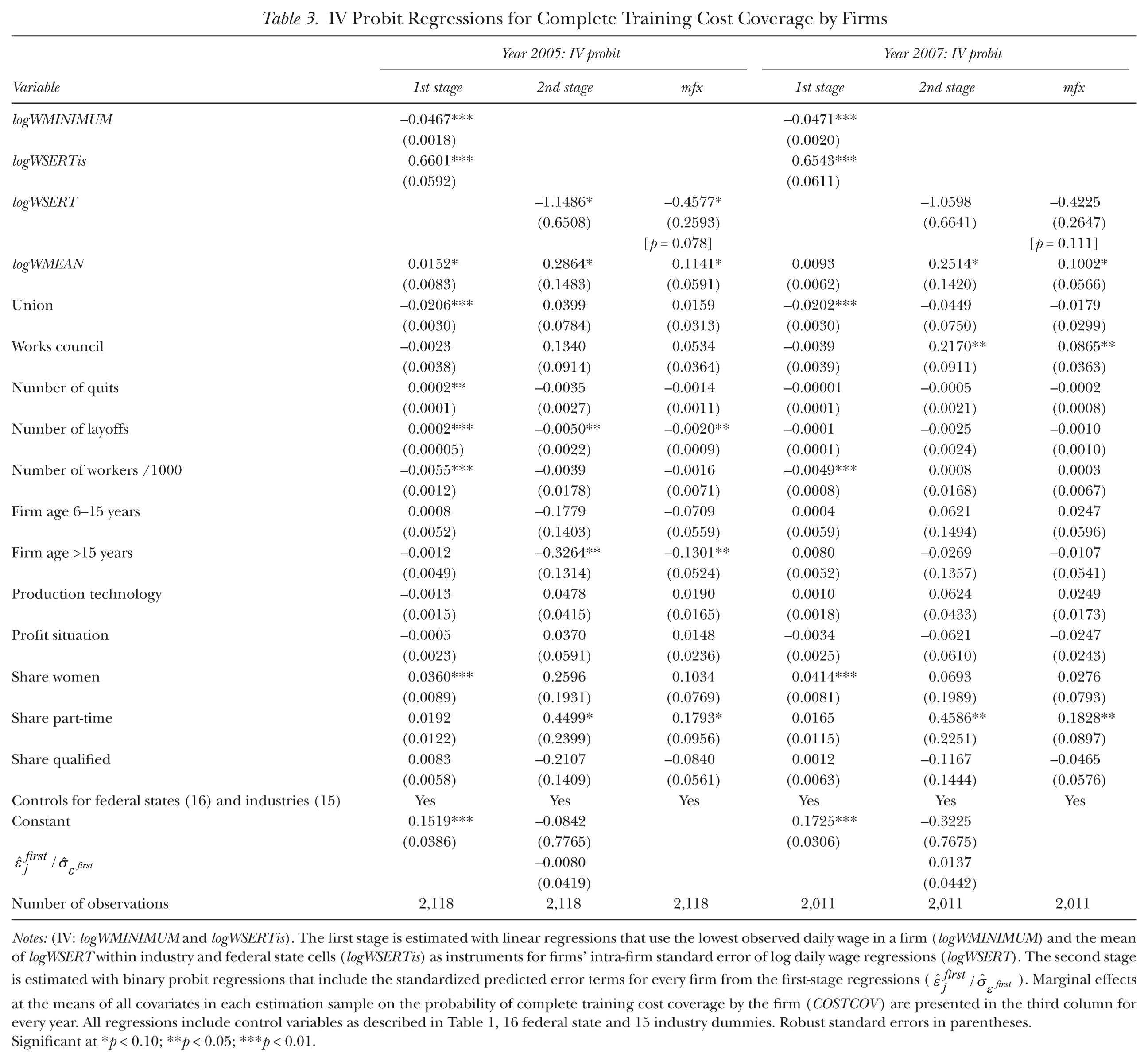

I estimate the first stage in the IV probit framework with linear regressions that use the lowest observed log daily wage in an establishment (logWMINIMUM) and the mean of the intra-firm standard errors of log daily wage regressions within 15 industry and 16 federal state cells (logWSERTis) as instruments for an establishment’s intra-firm standard error of log daily wage regressions (logWSERT). Table 3 shows that logWMINIMUM is indeed negatively correlated and logWSERTis is positively correlated with logWSERT at high statistical significance levels in the first-stage regressions. I then estimate the second stage with binary probit regressions that include the standardized predicted error terms for every establishment from the first-stage regressions (

IV Probit Regressions for Complete Training Cost Coverage by Firms

Notes: (IV: logWMINIMUM and logWSERTis). The first stage is estimated with linear regressions that use the lowest observed daily wage in a firm (logWMINIMUM) and the mean of logWSERT within industry and federal state cells (logWSERTis) as instruments for firms’ intra-firm standard error of log daily wage regressions (logWSERT). The second stage is estimated with binary probit regressions that include the standardized predicted error terms for every firm from the first-stage regressions (

Significant at *p < 0.10; **p < 0.05; ***p < 0.01.

The coefficients for the standardized predicted error terms are not significantly different from zero in either 2005 or 2007, and the Wald test of exogeneity cannot be rejected. Therefore, endogeneity seems not to be an important issue in my application. Marginal effects on the probability of complete training cost coverage by the establishment (COSTCOV) are presented in the third column for every year. As I have used the same estimation samples and compute comparable marginal effects at the means of all covariates in each estimation sample, the IV probit results can be compared in size with the probit results in Table 2. The results in Table 3 reveal marginal effects of minus 4.6 percentage points in the year 2005 and minus 4.2 percentage points in the year 2007 per 0.1 log point higher standard error of the wage regression. These marginal effects are comparable in size to the results in Table 2. The statistical significance levels, however, are lower in the IV probit regressions because of larger standard errors (p = 0.078 in the year 2005, p = 0.111 in the year 2007).

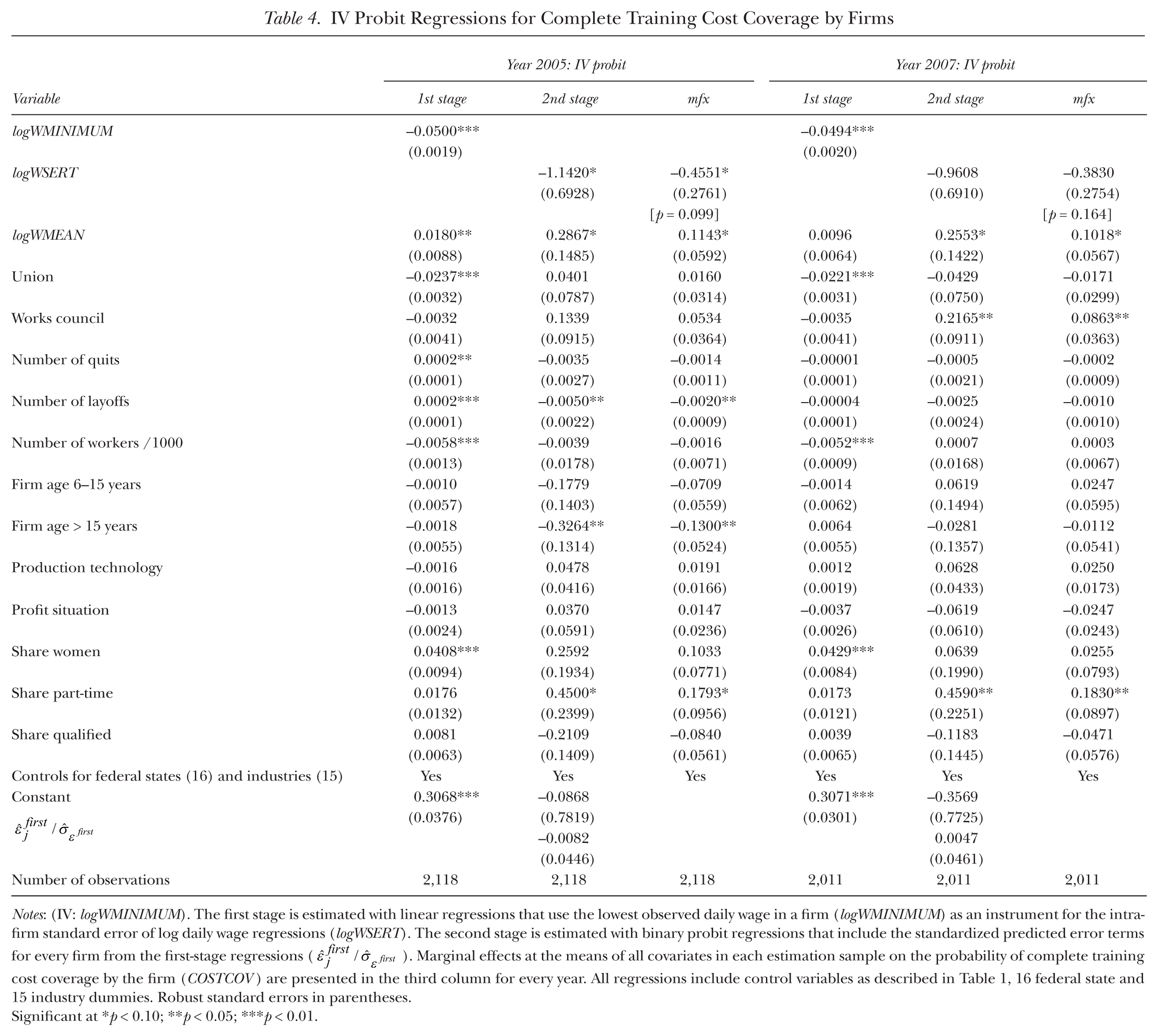

Table 4 presents IV probit results for the use of the lowest observed log daily wage in an establishment (logWMINIMUM) as a single instrument in order to check the sensitivity of the above IV probit regressions with two instruments. The results do not change notably. Again, the coefficients for the standardized predicted error terms are not significantly different from zero in either 2005 or 2007, and the Wald test of exogeneity cannot be rejected. A 0.1 log point increase of the standard error of the wage regression decreases the probability of complete cost coverage by 4.6 percentage points (p = 0.099) in the year 2005 and by 3.8 percentage points (p = 0.164) in the year 2007, which is comparable in size with the previous results.

IV Probit Regressions for Complete Training Cost Coverage by Firms

Notes: (IV: logWMINIMUM). The first stage is estimated with linear regressions that use the lowest observed daily wage in a firm (logWMINIMUM) as an instrument for the intra-firm standard error of log daily wage regressions (logWSERT). The second stage is estimated with binary probit regressions that include the standardized predicted error terms for every firm from the first-stage regressions (

Significant at *p < 0.10; **p < 0.05; ***p < 0.01.

The last robustness check is concerned with the establishment sample, which is very conservative with respect to establishment size because only establishments with at least 100 workers have been included. The preference for this conservative sample restriction was driven by potential sample selectivity and measurement errors with respect to training and the intra-firm wage-dispersion variables in smaller establishments. Despite these potential problems, I have relaxed the sample restriction and reestimated all regressions for a sample of establishments with at least 10 workers. The overall results do not change notably. The estimated marginal effects for the wage compression (dispersion) variable are statistically significant at even higher levels than in the sample of larger establishments, which can be at least partly attributed to the larger sample size, which has increased to more than 4,000 establishments in each year and to more than 2,000 establishments in the balanced panel.

Conclusion

In this empirical article, I have used German linked employer-employee data, which contain information about establishments’ cost coverage of training and allow me to generate the conditional intra-firm wage dispersion as proxy for an establishment’s wage compression. The main finding of my econometric analysis is that establishments with more compressed wage structures are more likely to cover all direct and indirect training costs. This finding is inconsistent with Becker’s model of on-the-job training in perfect labor markets, but it is consistent with theoretical considerations of the new training literature that firms can capture rents from training because of wage compression in imperfect labor markets, which provides incentives for them to pay for training. Moreover, it seems as if union-bargained collective contracts have no significant direct effects on training cost coverage that go beyond the effects of unions on general wage compression, whereas the existence of a works council is rather positively correlated with complete cost coverage, even after controlling for differences in establishments’ wage structures. Thus, codetermination at the establishment level seems to be more important than union bargaining when it comes to strategic training decisions in establishments, which accords with the explicit role of works councils in establishments’ training practices stated in the German Works Constitution Act (Betriebsverfassungsgesetz).

Three caveats are in order with respect to my empirical analysis, which leave room for future research. First, the presented results might still suffer from omitted-variable bias and reverse-causality issues. To deal with those endogeneity problems and to establish a causal effect, it would be helpful to have longer panel data sets and better instrumental variables. The applied IV approach in this article did not indicate problems of endogeneity, however. Second, although I use a linked employer-employee data set to compute variables for the intra-firm wage compression, the data comprise training information only at the aggregated establishment level and not for individual workers. Therefore, my analysis could not account for worker heterogeneity with respect to differences in training cost coverage. Third, the focus of my analysis is on testing one core element of the new training literature, namely, the positive effect of wage compression on training cost coverage by firms. To provide concrete policy recommendations for stimulating human capital investments, “in future work, the link between these stories and training can be more carefully derived, yielding empirical predictions to determine which sources of wage compression, if any, are important in encouraging firm-sponsored training” (Acemoglu and Pischke 1999b: 567). My finding that establishments with union-bargained collective contracts have significantly lower wage dispersion (see first-stage regressions in Table 3 and Table 4) shows that unions influence establishments’ wage structures. This finding and those of Beckmann (2002a, 2002b) and Dustmann and Schönberg (2009) suggest that unions are likely to be one important factor in the context of stimulating human capital investments, even if their effect might run through the indirect channel of compressed wage structures.

Footnotes

Acknowledgements

I thank Michael Beckmann, Lutz Bellmann, Knut Gerlach, Christian Grund, Olaf Hübler, Matthias Kräkel, Markus Leibrecht, Jens Mohrenweiser, and participants at the Institute for Employment Research (IAB) Colloquium in Nürnberg 2011, at the 15th Colloquium on Personnel Economics in Paderborn 2012, at the 26th Annual Congress of the European Society for Population Economics (ESPE) in Bern 2012, at the IAB Establishment Panel User Conference in Nürnberg 2012, and at seminars in Lüneburg for helpful comments.

This study uses the cross-sectional model of the Linked Employer-Employee Data (LIAB) (Years 2005 and 2007) from the IAB. Data access was provided on site at the Research Data Centre (FDZ) of the German Federal Employment Agency (BA) at the IAB and by remote access. Upon request, I can provide my program codes; direct inquiries to

2

Approximately 10% of full-time workers have such right-censored wages.

3

Questions about training cost coverage have been asked by an interviewer in the IAB Establishment Panel also in the years 1999 and 2009. I have decided against the use of the year 1999 because this wave has a significantly lower sample size and does not contain establishments from all federal states. Since 2000 the IAB Establishment Panel is conducted in all German federal states. A minor reason for the restriction is also that major labor market reforms in Germany were implemented after 1999. The year 2009 is not included in the analysis in order to exclude the effects from the economic crisis, during which many establishments in Germany used short-time work (Kurzarbeit). As one element of short-time work programs is financing training of employed workers, the question about training cost coverage by establishments is obviously affected and not comparable with the previous years. In fact, the establishments in the IAB Establishment Panel have explicitly been asked about training cost coverage by the Federal Employment Agency under short-term work programs in the year 2009, which is an interesting topic but beyond the scope of this article.

4

The binary variable COSTCOV is a combination of answers to two questions in the IAB Establishment Panel: (1) “Does the training usually take place during paid working time or during workers’ leisure time?” (COSTCOV = 1 if training during paid working time). (2) “Do workers usually have to cover all, part, or none of the direct training costs?” (COSTCOV = 1 if workers cover none of the direct costs).

5

This approach has been widely used with linked employer-employee data in order to study the effects of wage inequality on firm performance measures such as productivity and profits. For a literature review see Mahy, Rycx, and Volral (2011: Appendix Table A1).

6

7

In the robustness check section (see Table 3 and ![]() ), I estimate IV probit models, in which the first-stage regressions give some insights into the determinants of the intra-firm wage compression proxy (logWSERT). For example, establishments bound to a union-bargained collective contract have significantly lower intra-firm wage dispersion, whereas works councils are not significantly correlated with the wage-dispersion variable. Moreover, larger establishments have significantly lower wage dispersion, and establishments with a larger share of women have larger wage dispersion.

), I estimate IV probit models, in which the first-stage regressions give some insights into the determinants of the intra-firm wage compression proxy (logWSERT). For example, establishments bound to a union-bargained collective contract have significantly lower intra-firm wage dispersion, whereas works councils are not significantly correlated with the wage-dispersion variable. Moreover, larger establishments have significantly lower wage dispersion, and establishments with a larger share of women have larger wage dispersion.

8

For the interpretation of the economic significance of the effect size recall that logWSERT has a mean of 0.22 with a standard deviation of 0.07 (see descriptive statistics in ![]() ). Thus, an increase by one standard deviation of logWSERT decreases the cost coverage probability by approximately three percentage points.

). Thus, an increase by one standard deviation of logWSERT decreases the cost coverage probability by approximately three percentage points.

9

The complete results of the robustness checks can be requested from the author.