Abstract

Young adults aged 19 to 29 are significantly less likely than those in other age groups to have health insurance since most family insurance policies cut off dependents when they turn 19 or finish college. Between 2003 and 2009, several U.S. states relaxed their eligibility requirements to allow young adults to remain covered under their parents’ employer-provided health insurance policies. For those who qualify for these benefits, the expansion of dependent coverage partially reduces the value of being employed by a firm that provides health insurance or of working full-time, as adult children can now obtain health insurance through an alternate channel. The authors employ quasi-experimental variation in the timing and generosity of states’ eligibility rules to identify the effect of the policy changes on young adults’ labor market choices. Their results suggest that the expansion increases the group dependent coverage rate and reduces labor supply among young adults, particularly in full-time employment.

A strong linkage between health insurance and labor supply is often observed in the United States, as two-thirds of the working-age population have private insurance coverage that comes through employment. 1 Given the high costs of obtaining coverage for young adults entering the labor market, health insurance could be a critical factor in labor supply decisions, and changes in health insurance policies could affect young adults’ labor market choices. In this article, we study how state-level expansions of dependent coverage affect young adults’ work decisions using quasi-experimental variation in the implementation years and generosity of states’ eligibility rules for identification. Young adults are less likely to have health insurance than those in other age cohorts; for example, only 66% of 22-year-olds in the United States have health insurance, which is the lowest rate of coverage among the entire U.S. population. 2 As a result, several states, mostly between 2003 and 2009, have expanded the rules for eligibility to allow young adults to be covered under their parents’ employer-provided health insurance. These states have taken measures to expand dependent coverage to young adults with qualifications based on their age, marital status, student status, or whether the dependents have children; the requirements vary from state to state.

The state dependent coverage expansion would affect health insurance coverage among young adults, but there might be unintended effects on young adults’ labor supply as a consequence as well. In the absence of the states’ policy changes, it would have been difficult for young adults to obtain coverage unless they had jobs offering group private insurance. Thus, those who value health insurance but who do not have access to it other than through their employment might have a greater incentive to work—that is, employment that provides health insurance has an implicit value. The expansion laws provide an insurance option that is not tied to young adults’ own jobs. As this implicit value decreases with the relaxation of coverage rules, those who become eligible for extended dependent coverage would be more inclined to withdraw from the workforce or be less likely to work full-time. That is, the strong linkage between health insurance and labor supply might weaken with the expansion of access to dependent coverage.

We investigate whether the various states’ interventions in the private health insurance market have discouraged young adults from participating in the labor market. Examining the labor market choices of young adults is important as young adults are experiencing a period of employment in which the most important on-the-job training and human capital investment are occurring and because their early career choices have long-term consequences. Provision of health insurance is an important consideration when people make job choices (Currie and Madrian 1999), and accordingly, analysis of policy interventions that grant greater coverage to young adults can aid in understanding how the provision of additional sources of health insurance may affect that group’s labor supply. We find that expanding the provision of dependent coverage increases the dependent coverage rate and reduces labor supply among young adults, particularly in full-time employment. Job-lock theory predicts that when an insurance option not linked to employment becomes available, individuals will be less likely to take up or keep jobs that provide health insurance and will be more likely to change employers, switch to part-time jobs, or quit working altogether (Madrian 1994). Our results show that in most cases, a decline in young adults’ own private insurance is accompanied by a decrease in full-time employment without a reduction in the uninsured rate; rather, young adults appear to have shifted from employer-sponsored plans to group dependent coverage. The results imply that the expansion of dependent coverage may play a role in reducing job-lock among some young adults.

Analyzing the effects of state laws on young adults’ labor market behavior may address important questions of job-lock and offer a better understanding of the overall effects of dependent coverage expansion. To date, there has been little research into how access to health insurance that is not tied to employment affects young adults’ labor market choices. Although numerous empirical studies on health insurance provision and labor market outcomes have been conducted in the job-lock literature, previous studies have focused on outcomes among other cohorts such as the elderly or lower-income, single mothers (see Gruber and Madrian 2002 for a more complete review of this broader literature), and few studies have employed natural experiments. 3 One exception is Antwi, Moriya, and Simon (2013), which documented the early effects of expansion of dependent coverage in the 2010 Affordable Care Act (ACA) on health insurance outcomes and labor supply. The authors found that young adults worked fewer hours and were less likely to work full-time as a result of the expansion. In this article, we focus on pre-ACA periods. 4 One important advantage associated with analyzing the changes in the states’ insurance policies (which took place before the federal ACA reform) is that the availability of pre-state-reform and post-state-reform data allows us to perform an event study that maps out trends observed before and after the policy changes. It is difficult to conduct such an analysis of the expansion of dependent coverage in the ACA because many states had already adopted dependent coverage prior to the introduction of the law and because post-ACA data are still limited.

Background

Expansion of Dependent Coverage

Young adults between the ages of 19 and 29 constitute the largest segment of the uninsured population in the United States; they represented nearly one in three uninsured people in 2008, totaling approximately 13.7 million people (Collins and Nicholson 2010). There are several reasons why young adults may not obtain health insurance coverage. First, until recently, they lost dependent coverage status under their parents’ private plans upon turning 19 or finishing college (up to age 24). Also, most young adults aged 19 or above have limited access to public health insurance, with eligibility for insurance such as Medicaid generally being restricted to very low-income families or to disabled adults. 5 In addition, since they have limited work experience, young adults often do not have access to affordable employer-sponsored insurance. Because of their youth they may also feel invincible and thus are even less likely to obtain health insurance. These factors, in combination with high premiums for individual health insurance plans, have caused young people to be unable to access coverage or have made them uninterested in taking up other types of coverage; accordingly, they are more likely to be uninsured than people in any other age group.

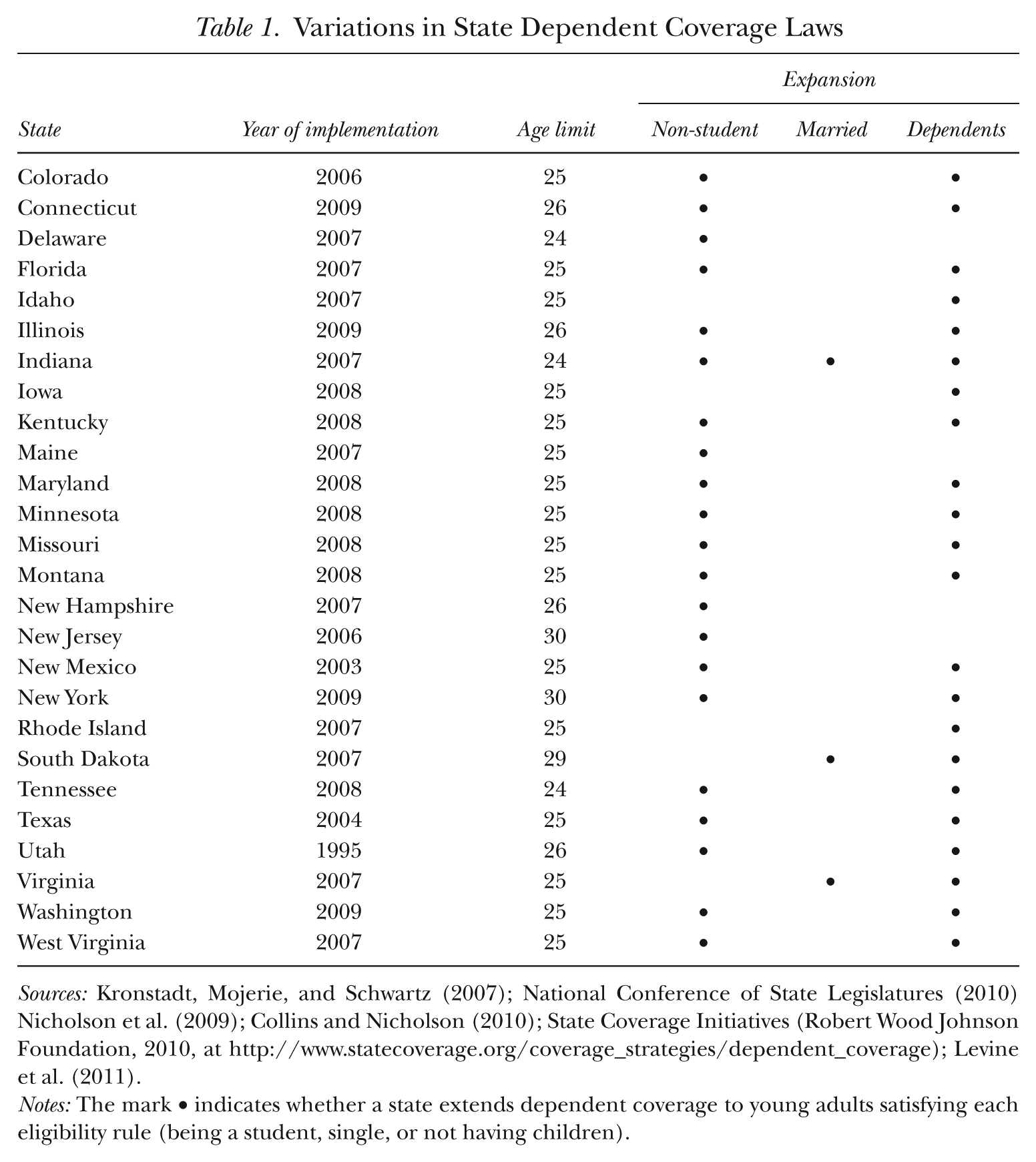

To help them stay insured, several states have expanded eligibility rules and have allowed young adults to remain covered under their parents’ employer-provided health insurance policies. As of 2010, 27 states had passed laws that increased the age of dependency for insurance purposes. Table 1 shows how the laws’ requirements for coverage vary across states. The upper age limit varies considerably, ranging from 24 in Delaware, Indiana, and Tennessee to 30 in New Jersey and New York. The definitions of dependent young adults also vary across states. In some states, eligibility is restricted to full-time students, unmarried young adults, or young adults without their own dependents. For example, Idaho, Iowa, Rhode Island, South Dakota, and Virginia require young adults to be full-time students, while states except for Indiana, South Dakota, and Virginia require that they be unmarried if they are to be covered under their parents’ plans. In addition, Delaware, New Hampshire, and New Jersey have requirements that the young adults must have no children of their own.

Variations in State Dependent Coverage Laws

Sources: Kronstadt, Mojerie, and Schwartz (2007); National Conference of State Legislatures (2010) Nicholson et al. (2009); Collins and Nicholson (2010); State Coverage Initiatives (Robert Wood Johnson Foundation, 2010, at http://www.statecoverage.org/coverage_strategies/dependent_coverage); Levine et al. (2011).

Notes: The mark • indicates whether a state extends dependent coverage to young adults satisfying each eligibility rule (being a student, single, or not having children).

The states’ expansion of coverage rules does not, however, apply to employers that provide health benefits directly to their employees (i.e., self-insured firms) (Pierron and Fronstin 2008). Under the Employee Retirement Income Security Act of 1974 (ERISA), the state-level regulations apply only to employers that purchase insurance through a carrier (i.e., fully insured firms), and these employers are likely to be small firms. 6 The implication for our study is that we expect the effect of the expansion of dependent coverage to be larger for young adults when their parents work in small firms and have private group health insurance, as we show below.

The expansion creates a safety net for young adults who might not otherwise find affordable coverage in the individual insurance market and also reduces risks that are commonly experienced at key life transitions such as graduation. Before the expansion of dependent coverage provisions, the insurance protection that a young person enjoyed by virtue of his or her parents’ employer’s policy or through his or her student health plan was lost upon graduation. Thus young adults who were not full-time students were more likely to be uninsured after graduation from high school or college. Even though young adults enter the labor market after school, they may experience difficulties in finding jobs with health benefits. As they are at the beginning of their careers, the jobs available to them—typically jobs at small firms, with low wages, or part-time or temporary jobs—often do not offer health benefits. 7 Therefore, the state reforms provided an attractive alternative to purchasing insurance through their own employers or through student plans or to remaining uninsured.

Several studies have examined the effects of the state-level mandates on health insurance outcomes, but they present mixed evidence. For instance, Levine, McKnight, and Heep (2011) found that the extended dependent coverage laws increased private health insurance coverage among young adults, resulting in a reduction in the overall uninsured rate. Monheit, Cantor, DeLia, and Belloff (2011) also showed that the states’ policies have increased young adults’ dependent coverage rates, but they found no significant effect on the uninsured rate among young adults. 8 While these previous studies on the state-level expansion of dependent coverage have tended to focus on health insurance outcomes, evidence of the effect on young adults’ labor market choices arising from the states’ expansion is sparse. More recently, several articles have investigated the early effects of the ACA’s dependent coverage provisions on health insurance outcomes (Sommers and Kronick 2012; Antwi et al. 2013) and have suggested that the federal mandate is effective in increasing the numbers of young adults with insurance. Only one article (Antwi et al. 2013) analyzed the labor market outcomes arising from the introduction of the ACA. Our article fills the gap in the existing literature as no published study to date has examined labor market outcomes of changed insurance provisions using data pertaining to state-level interventions. In addition, unlike earlier studies, ours also provides extensive robustness checks, a falsification test, and an event study. The rich variation in the timing and generosity of changed eligibility rules among states allows us to examine more than the average effect of policy changes.

Conceptual Framework of Health Insurance and Labor Supply

Individuals who value health insurance but have access to it only through their own employment may work longer hours than they otherwise would, even though their marginal value of leisure exceeds their marginal product of labor. It is also possible that some young adults starting their careers would accept a full-time job even though they would prefer not to because health insurance premiums for individual plans are very high compared with those for group plans and group coverage is typically offered with full-time employment. The fact that employers tend to restrict health insurance benefits to full-time workers results in a non-convex budget constraint in a choice set between leisure and consumption (or income); once workers work enough hours to be classified as full-time employees, they receive health insurance, and the portion of their budget constraint jumps up vertically by the consumption value of the insurance (Buchmueller and Valletta 1999).

For young adults who work full-time even though they would prefer to work fewer hours in the absence of the kink in the budget constraint, the expansion in dependent coverage would effectively smooth out this kink in the budget set. In fact, the availability of parental health insurance acts like an increase in unearned income, with the pure income effect predicting that young adults would decrease total work hours. Thus, as full-time work will no longer carry the advantage of access to health insurance, the extended coverage laws might encourage more people to seek part-time jobs.

Figure 1 illustrates the labor-leisure tradeoff with and without parental dependent coverage. The horizontal axis measures the amount of leisure consumed, and the vertical axis measures total income, including health insurance benefits. Prior to the expansion of dependent coverage, an individual faced a kinked budget constraint of MQPH, so that health insurance is offered if he or she works at least T–N0 hours. The slope of the constraint reflects the individual’s wage, and the right vertical portion HT is non-labor income. The height of the vertical portion QP represents the consumption value of health insurance benefits associated with working full-time. If dependent coverage is not available, the individual might maximize utility at N0, qualifying for her own health insurance and working T–N0 hours.

A Young Adult’s Budget Constraint with and without Parental Dependent Coverage

The expansion of the availability of dependent coverage alters the budget constraint to MQD, smoothing out the kink and increasing the affordable set by QDHP for eligible individuals. The upper right vertical portion DH reflects the value of health insurance benefits from parental coverage, assuming the value of parental coverage and that of employer-sponsored insurance (ESI) are similar. Now the individual can obtain health insurance even though he or she does not work full-time. The new utility-maximizing choice might be N1. In the situation depicted in Figure 1, the expansion of dependent coverage reduces labor supply by N0–N1. From our budget constraint analysis, we see that young adults are expected to reduce their labor supply in market production if they are likely to be covered by their parents’ health insurance policies. This prediction also means that this decrease in labor supply would be accompanied by a decline in ESI.

This framework may have other empirical predictions. Some young adults are likely to work fewer hours even before the expansion if they greatly value leisure or non-labor-market activities due to other competing demands such as taking care of children. This means that they have steeper indifference curves and optimize their work decision somewhere on PH rather than on Q. Since they work less than full-time, they do not have ESI. After the policy change, the expanded budget set could further reduce young adults’ work hours. 9 The decrease in labor supply among these young adults would not be accompanied by a decline in ESI but by a reduction in other types of insurance or in the uninsured rate. In addition, young adults are likely to differ in their perceived value of health insurance. The vertical distance (PQ) would be greater for those who put higher value on health insurance than for those who do not. Before the expansion, higher perceived value would attract some young adults to work full-time at the margin to obtain private insurance from employment. It is these young adults whose decrease in labor supply is accompanied by a decline in their own private insurance.

Previous studies examined the effects of spousal health insurance on own labor supply (Currie and Madrian 1999; Gruber and Madrian 2002). Such studies indicated a strong negative effect of the existence of spousal health insurance on own probability of working full-time; this is true both when it is assumed that the availability of spousal health insurance is exogenous to own labor supply and when instrumental variable approaches are used. 10 Our estimation strategy uses variation from a clear policy intervention. Thus it is less subject to the problem of assuming exogeneity of an alternative source of health insurance.

Empirical Strategy

We are interested in identifying the causal effects on labor market outcomes of state laws allowing young adults to remain covered under their parents’ health insurance. We use a difference-in-differences approach in which we compare the pre- and post-law changes in insurance coverage and labor market outcomes of those who are and are not affected by the policy intervention. We model the relationship as follows:

where Y refers to an outcome variable for individual i in state s in year t. We examine outcomes among young adults in states that expanded dependent coverage (expansion states), where outcomes of interest are health insurance coverage as well as labor market choices such as overall labor supply and full-time work. Treated is an imputed measure that defines who will be newly eligible after the policy change is implemented based on the state laws described in the previous section. Even before the coverage extensions, dependent status (and therefore eligibility) was not lost until age 24 as long as the young adults continued with their schooling. In our analysis, we focus on newly eligible young adults (= Treated) rather than those who have always been eligible (students who are aged 24 or younger) because the former group is most likely to benefit from the expansion. That is, students up to 24 years old are not newly eligible, and Treated is imputed to be zero. Post is a binary variable indicating whether the state and year are affected by the policy changes. The interaction term, Treated × Post, is an indicator that the observation comes from the treated group after the expansion had occurred. We call this interaction term the newly affected group, who will be most likely to respond to the policy changes. As discussed in the previous section, if the expansion allowed young adults to be covered by parental health insurance and lowered the incentive to work among the newly eligible, we would expect β1 to have a negative sign, especially when the dependent variable is working full-time.

X is a vector of demographic characteristics that include age, student and marital status, gender, having any children, whether the young person resides with parents or not, race dummies, and family income expressed as a percentage of the federal poverty line and its squared term. We also control for state and year fixed effects. To the extent that Post is determined by some time-invariant state-specific conditions (i.e., states that have typically had high uninsured rates among young adults might adopt the new laws earlier), state fixed effects will absorb such state differences. Year fixed effects will capture any factors that are common to all states within a given year. We also control for Unemp, the unemployment rate at the state and year level, in order to capture overall time-varying economic conditions for each state. If the state unemployment rate influences outcome variables and the policy itself, omitting it from incidence studies would bias the estimated effect of the policy. 11 Standard errors are clustered by state.

We use only the expansion states in our main analysis rather than setting up eligibility measures in non-expansion states. By 2010, 27 states had passed the expansion laws, and the eligibility requirements were different across these states. As previously discussed, in some states eligibility is restricted to full-time students, whereas other states require that young adults should not have dependents of their own. Most states require young adults to be unmarried in order to be covered by their parents’ health insurance plans. On the other hand, states that did not pass laws expanding coverage do not have any eligibility measures, and for this reason we exclude non-expansion states in our main analysis. In the robustness check, however, we extend our analysis by including these non-expansion states in two ways: 1) using common eligibility rules imposed by the expansion states; and 2) imputing Treated to be zero for individuals in non-expansion states. It is important to note that the results are robust to the inclusion of non-expansion states.

We also look at differential effects across gender on both health insurance coverage and labor supply using Equation (1). The effects of extended dependent coverage on insurance status and labor market outcomes are expected to be stronger among those who value insurance highly. Loosely speaking, health insurance coverage is likely to be more valuable for females than for males. Gruber (1994) found that women of childbearing age tended to receive lower wages when several state and federal mandates made insurance cover childbirth costs. This finding implies that such women could face higher premiums for health insurance and be forced into lower-wage jobs if they were to acquire their own health insurance. Therefore, we expect to see greater effects of the policy change on women than on men. We further examine the differential effects between women who have and do not have children, as women with children might respond differently to the expansion if they have greater preference toward non-labor-market activities.

In addition, we test for differential effects depending on the size of the firm at which the young adults’ parents are employed. As discussed earlier, the expansion applies to only a subset of parents. ERISA provides that self-insured firms (which are likely to be large firms) cannot be regulated by state-level laws, and for this reason we expect that young adults whose parents are covered by fully insured plans (which are likely to be provided by small firms) are affected more by the policy change than are others.

Our estimation strategy employs variation where the availability of alternative insurance is driven by a policy intervention. One concern with this strategy is that Treated may be endogenously determined if a behavioral response is at the eligibility margin; that is, some young adults may find it advantageous to become eligible as the intervention phases in. Table 1 shows that eligibility is different across states in terms of whether those states allow young adults to be non-students, to be married, and to have dependents. We test for the possibility of a behavioral response to the policy change by estimating the following regression equation:

Equation (2) tests whether the young adults in the expansion states changed their behavior to become eligible in response to the states’ changed eligibility rules. We are interested in the behavioral outcome Z that might be affected by the eligibility rules. The dependent variable Z is a binary variable indicating whether a young adult is a student, is single, or has children. In addition, we test whether the policy change affects the likelihood that young adults live with their parents because we later use restricted samples based on parental information, which is available only when young adults reside with their parents. We also run a regression in which the dependent variable Z is an indicator of having a parent who has private coverage and works at a small firm (so that the young adults are affected even under ERISA). Finally, we run regressions in which the dependent variable Z is Treated to test whether the policy reforms have affected young adults’ propensity to be eligible for dependent coverage in the expansion states. In all cases, the estimated

In addition to Equation (2), we introduce binary variables indicating whether each state requires young adults to be students, to be unmarried, and not to have their own dependent(s), based on the information in Table 1. Instead of using Post only, we interact Post with these binary variables to accommodate the fact that eligibility measures vary across states. In all variants of Equation (2), the coefficients on the interactions of each eligibility measure and Post are close to zero and are not statistically significant, indicating that there is less of a concern about endogenous behavioral change at the eligibility margin. 12

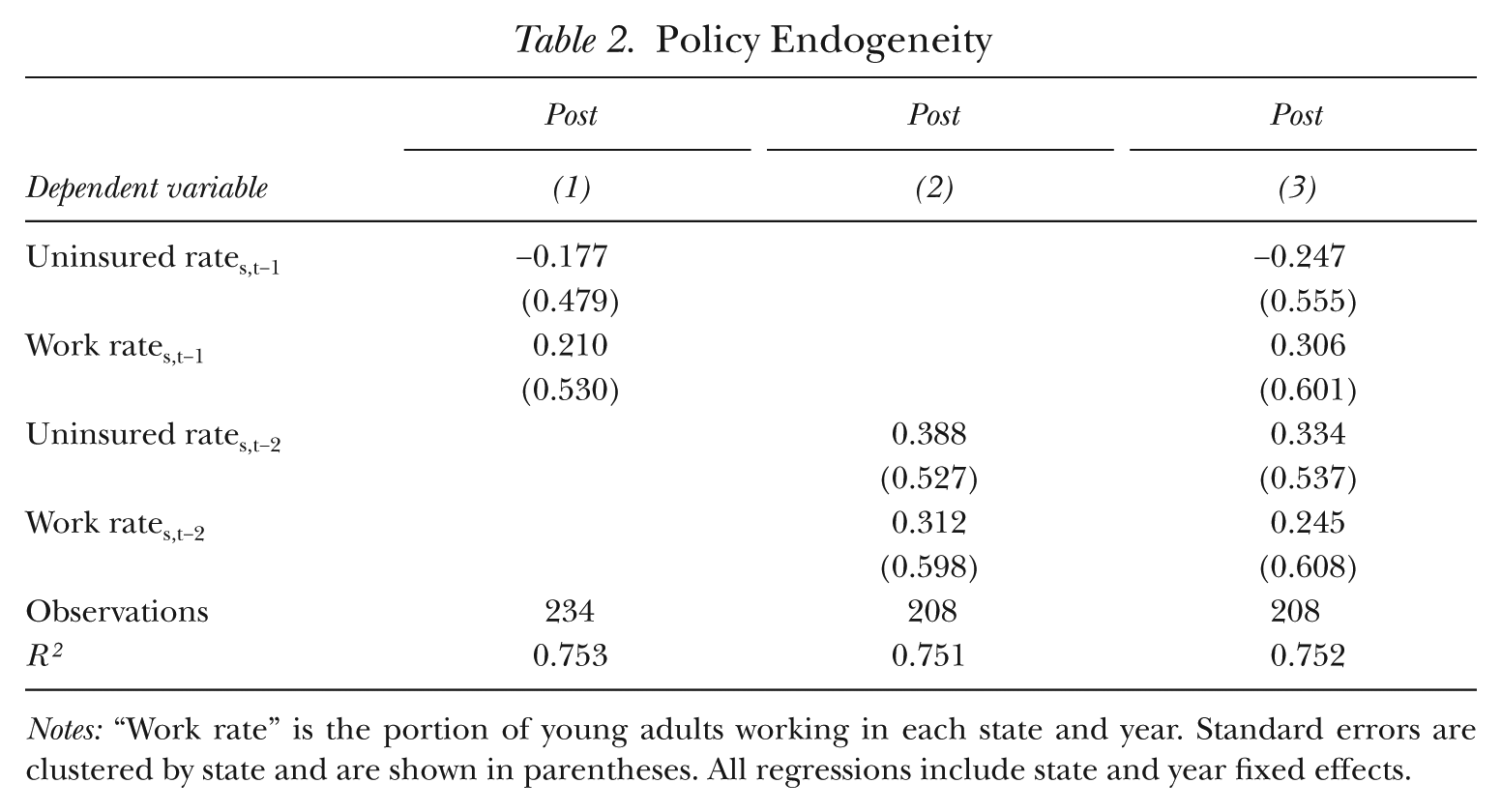

Another concern is policy endogeneity. In order to insulate the analysis from potential bias caused by policy endogeneity, we have to ensure that either time-varying state-level variables did not change between the pre- and post-law periods or that they changed in an identical manner in the expansion states and in states yet to enact new policies (Besley and Case 2000). The problem that is not resolved by controlling for state fixed effects is that the timing of the implementation of the new policy may depend on pre-law changes in uninsured rate among young adults. That is, if there were specific trends in the uninsured rate and employment that were correlated with the timing of adoption of expanded dependent coverage across states, a difference-in-differences approach could be problematic. To confirm whether this is the case, we test whether the timing of the policy change is endogenously determined by young adults’ uninsured rate and labor supply. The reported coefficients in Table 2 are from the model in which we regress Post (compressed to one observation per state and year) on the average of young adults’ lagged and two-year lagged uninsured rate and work rate (i.e., the proportion of young adults working in each state and year). We find no significant effect of the previous uninsured rate and labor supply on the state’s policy change. This result implies that policy endogeneity is not a huge concern.

Policy Endogeneity

Notes: “Work rate” is the portion of young adults working in each state and year. Standard errors are clustered by state and are shown in parentheses. All regressions include state and year fixed effects.

Data

We use the 2001–2010 March Current Population Survey (CPS) data. 13 The March CPS contains a wealth of information on individual circumstances, including health insurance status and labor market choices. In addition, it has a large sample size and allows for nationally representative estimates when we use sampling weights. 14 Most states that extended dependent insurance coverage adopted the laws between 2003 and 2009. In order to focus on a period when the majority of state actions occurred, our analysis covers the period from 2000 to 2009, which is presented in the 2001–2010 CPS because insurance and employment information is backdated one year. We exclude Massachusetts in our analysis since broader health insurance reform was implemented in this state at the same time as the extended dependent coverage law was introduced (Long, Yemane, and Stockley 2010).

Our sample comprises young adults aged 19 to 24 in the expansion states. In some states the age limit increased to 25 or higher, but the March CPS does not have information on student status when a respondent is older than 24. In the robustness check, we also extend the age of the sample, assuming that young adults more than 25 years old are not students. Several other sample restrictions are made in the analysis. For example, we exclude disabled individuals and those in the armed forces because they are eligible for other sources of health insurance, and their work patterns are likely to be different from those of others.

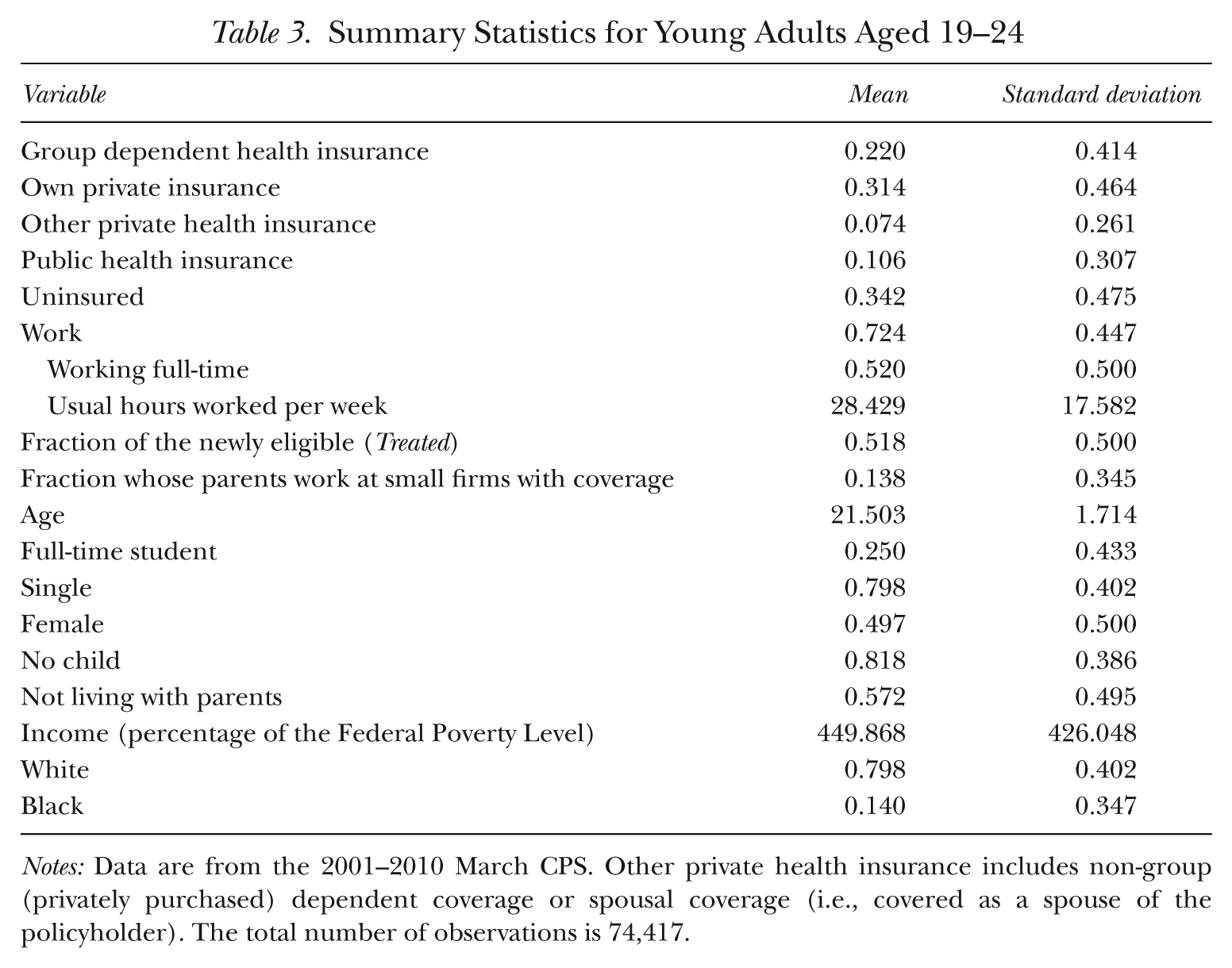

Table 3 reports summary statistics for our sample of young adults. The first five outcomes relate to health insurance coverage. 15 The first three rows are the mean values for three types of private insurance. Private insurance can be categorized into six types in total, and we collapse them into the three most relevant categories: group dependent insurance, own private insurance, and other private health insurance. 16 Group dependent coverage means a respondent is covered as a dependent on an employment-based (group) health insurance policy. Own private insurance indicates that a young adult is covered by any private insurance policy (either a group or non-group insurance policy) as a policyholder. Other private health insurance pools the remaining types of private insurance—non-group dependent insurance and spousal coverage insurance. Most young adults with private health insurance are covered by either group dependent coverage or their own private plan; 22% are covered by group dependent coverage, 31.4% have their own private insurance plans, and only 7.4% are covered by other private insurance. A total of 10.6% of young adults aged 19 to 24 are covered by public health insurance. About a third of young adults in the sample are uninsured, which is very high compared with the overall uninsured rate of 15% among the U.S. population.

Summary Statistics for Young Adults Aged 19–24

Notes: Data are from the 2001–2010 March CPS. Other private health insurance includes non-group (privately purchased) dependent coverage or spousal coverage (i.e., covered as a spouse of the policyholder). The total number of observations is 74,417.

What follows next are the mean values for work-related variables. A total of 72.4% of young adults in the sample are employed, with a large portion of them working full-time (72% of those employed). Young adults in the sample on average worked 28.4 hours per week. The remaining variables are the control variables in the main regressions. Those who are newly eligible for insurance constitute 51.8% of the sample (those newly affected, Treated × Post, are about 17.4% of the sample). On average, 25% are enrolled as full-time students; the majority of these young adults are single and do not have children (79.8% and 81.8%, respectively). A total of 42.8% are living with their parents, and only in this case do we have information about their parents such as whether they work at small-sized firms or whether they have employer-provided health insurance. If it were the case that living arrangements were affected by the policy change, using only this sample would be potentially problematic. As discussed above, however, the likelihood that young adults live with their parents is not affected by the laws, suggesting a lack of concern for selection bias.

Results

Main Results

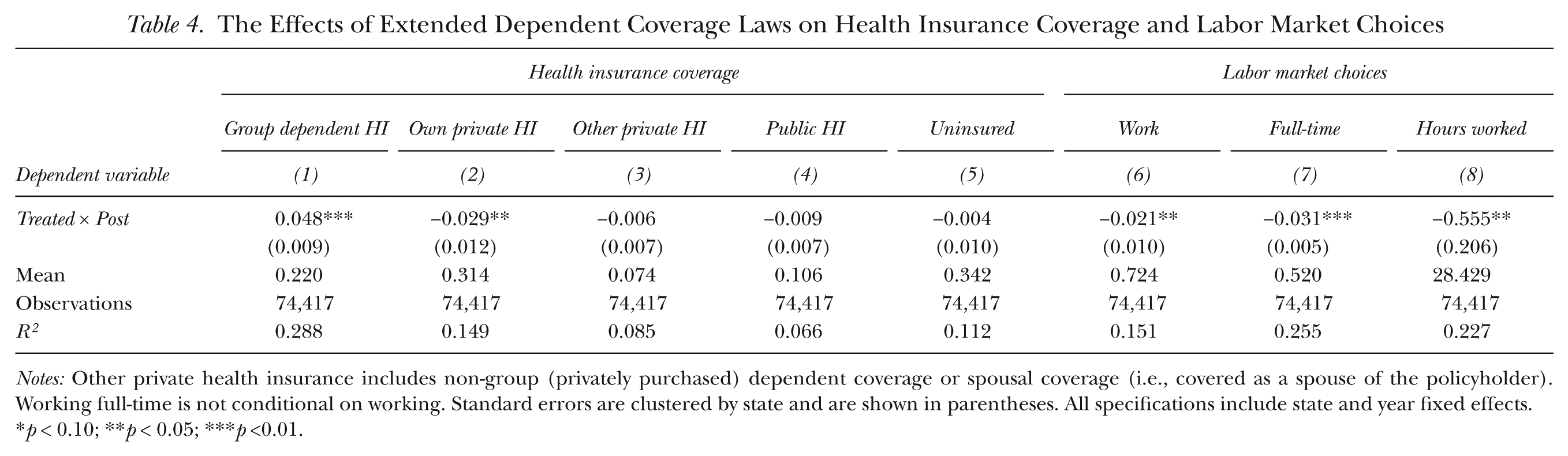

Table 4 presents the results from the difference-in-differences approach in regression Equation (1). All models are estimated using OLS. As health insurance is a channel through which labor market outcomes are affected, we begin by discussing the effect of extended dependent coverage laws on health insurance coverage. Column (1) shows that those who are newly affected by the law (Treated × Post) are 4.8 percentage points more likely to be covered by group dependent health insurance than the control group. More than 50% of the effect appears to come from a decrease in the likelihood that a young adult has his or her own private health insurance, as shown in column (2). The probability of being covered by public insurance is not affected by the law; we find little evidence of “reverse crowding out,” which could happen if the availability of group private insurance results in a switch from public to private insurance for the overall sample. Last, we find no evidence that those newly affected by the law are less likely to be uninsured (column 5). This finding is similar to that of Monheit et al. (2011), who found no significant decrease in the uninsured rate among young adults as a result of the change in the law. 17

The Effects of Extended Dependent Coverage Laws on Health Insurance Coverage and Labor Market Choices

Notes: Other private health insurance includes non-group (privately purchased) dependent coverage or spousal coverage (i.e., covered as a spouse of the policyholder). Working full-time is not conditional on working. Standard errors are clustered by state and are shown in parentheses. All specifications include state and year fixed effects.

p < 0.10; **p < 0.05; ***p <0.01.

Our findings suggest that there is no improvement on the extensive margin of increasing coverage for targeted young adults (i.e., the newly eligible); rather, we see evidence of shifting between the types of insurance young adults obtain. One possible reason for such switching behavior is that the marginal cost to parents of adding another dependent to their insurance policy could be lower than the young adult’s own coverage premium, and young adults may accordingly have incentives to receive coverage as dependents rather than be covered through their own employer-sponsored insurance plans. In average terms, the cost of covering an additional dependent through family coverage is 11% less than the cost of single coverage. 18 Parental dependent coverage also allows young adults to exercise greater flexibility in changing jobs and to delay working until they find jobs with better match quality. By remaining covered by their parents’ insurance plans, young adults additionally enjoy access to a wider variety of jobs, including those that do not necessarily provide health insurance.

The next columns of Table 4 present the results in terms of labor market choices. The dependent variable in column (6) is an indicator variable of whether a young adult works. The introduction of the law expanding coverage, on average, reduces young adults’ labor supply by 2.1 percentage points, which is a modest distortion given that the average labor market participation rate is 72%. 19 To understand the sources of this change, we examine in columns (7) and (8) whether the new law affects the likelihood of a young adult’s working full-time and the usual hours worked per week. The results show that the probability of working full-time declines by 3.1 percentage points with usual hours worked decreasing by 0.555 hours. 20 The extended dependent coverage laws provide an insurance option that is not tied to employment, and as a result, young adults are more likely to switch to part-time jobs or to quit working altogether. The changes in labor market outcomes are accompanied by a decrease in health insurance under own name, as shown in column (2). From the welfare perspective, the switch from own private to dependent coverage may increase young adults’ welfare to the extent that parental coverage is cheaper and of higher quality than their own coverage from employment. If own health insurance that is replaced by dependent coverage is purchased through a private plan that has higher premiums than employer-sponsored insurance, then the potential benefit from changing plans may be even larger. In addition, the expansion is beneficial for some young adults who had to keep full-time jobs for fear of losing coverage (but who would otherwise prefer to work part-time or not to work), allowing them to choose a more flexible work arrangement.

In results obtained but not reported here, we also explore other work-related outcomes such as 1) young adults’ propensity to work at a large-sized firm with more than 100 employees; 2) young adults’ likelihood of being self-employed; and 3) the number of employers that the young adult has had in the preceding year. These outcomes appear to be unaffected by the expansion of dependent coverage. 21

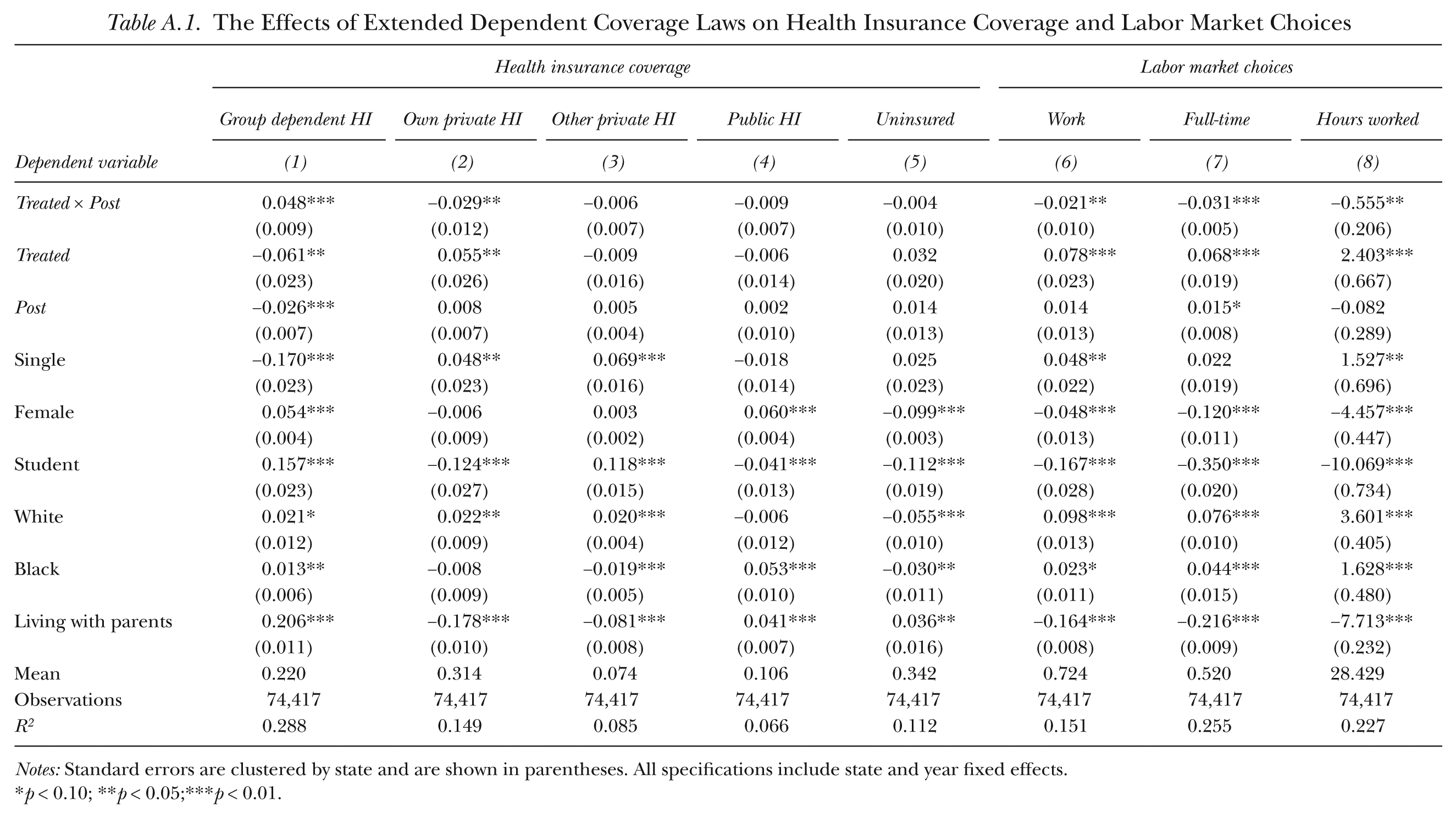

Appendix Table A.1 shows the estimated coefficients for selected control variables included in the regression analysis. For instance, single individuals are more likely to work and are less likely to be covered by dependent coverage. The opposite is true for students and those living with their parents; they are more likely to be on dependent coverage and are less likely to work. There are some racial differences in both health insurance and labor supply decisions. In particular, young white adults are both more likely to work and more likely to be covered by dependent health insurance than are young black adults. Overall, the coefficients show sensible signs; however, a causal interpretation is unwarranted as most variables, such as being single and being a student, are likely to be correlated with unobserved variables that determine insurance coverage and work decisions.

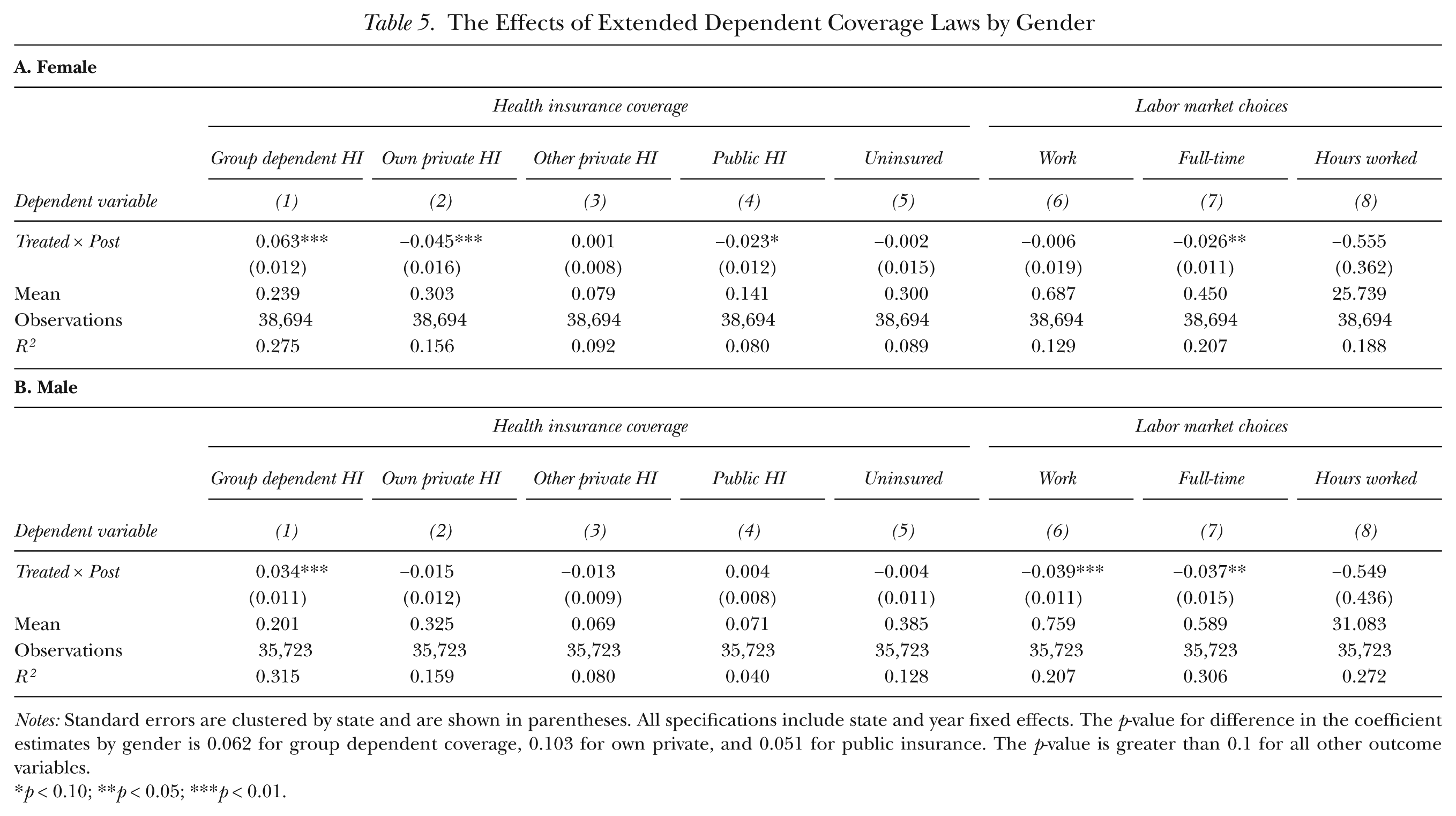

Table 5 examines how young female and male adults differentially respond to the extension of dependent coverage. Generally, women are charged higher premiums because as a group they tend to consume more medical services than men. In particular, women of childbearing age tend to need more health care than men because of the combined demands of pregnancy and family planning. 22 Partly as a result of this fact, young women typically pay more than young men for individual health insurance (National Women’s Law Center 2008), unless they live in one of the 10 states in which gender rating is illegal. 23 Therefore, women may have greater incentives than men to be covered by parental insurance plans than to seek coverage under their own plans.

The Effects of Extended Dependent Coverage Laws by Gender

Notes: Standard errors are clustered by state and are shown in parentheses. All specifications include state and year fixed effects. The p-value for difference in the coefficient estimates by gender is 0.062 for group dependent coverage, 0.103 for own private, and 0.051 for public insurance. The p-value is greater than 0.1 for all other outcome variables.

p < 0.10; **p < 0.05; ***p < 0.01.

The results in Table 5 indicate that women are indeed more likely to take advantage of the increased access to parents’ health insurance. As shown in column (1), the likelihood of having dependent coverage increases by 6.3 percentage points for women, compared with 3.4 percentage points for men. The increase in dependent coverage for women appears to largely arise from a decrease in own private health insurance (4.5 percentage points).

The results in columns (6) to (8) in Table 5 show corresponding labor market choices by gender. A decline in the likelihood of working at all is more prominent for affected young male adults than for young female adults. The effect on the likelihood of working full-time is salient for both women and men. The affected young women are 2.6 percentage points less likely to work full-time, while affected young men are 3.7 percentage points less likely to do so. The fact that full-time work among women has decreased without any corresponding effect on overall labor supply suggests that women are likely to make a substitution away from full-time to part-time jobs. This is perhaps why we observe a corresponding decrease (although not one-to-one) in the probability of holding private insurance under one’s own name, with full-time workers more likely to be offered private insurance than part-time workers. The results show that women decrease own private insurance more than they decrease employment or full-time employment. This is expected if some of the young adults switch from own private coverage to their parents’ dependent coverage but do not change their labor market behavior, perhaps because dependent coverage is cheaper than their own private insurance or it offers better access to health care. Young male adults are more likely to withdraw their labor altogether than they are to replace full-time with part-time work. A decline in both labor supply and full-time work does not translate into a decrease in own health insurance for young male adults. One possible interpretation is that affected young male adults have worked at firms that did not provide health coverage or they have not obtained own private insurance because they worked fewer hours before the expansion. In this case, the changes in labor supply decisions are not accompanied by a decrease in own private coverage. 24

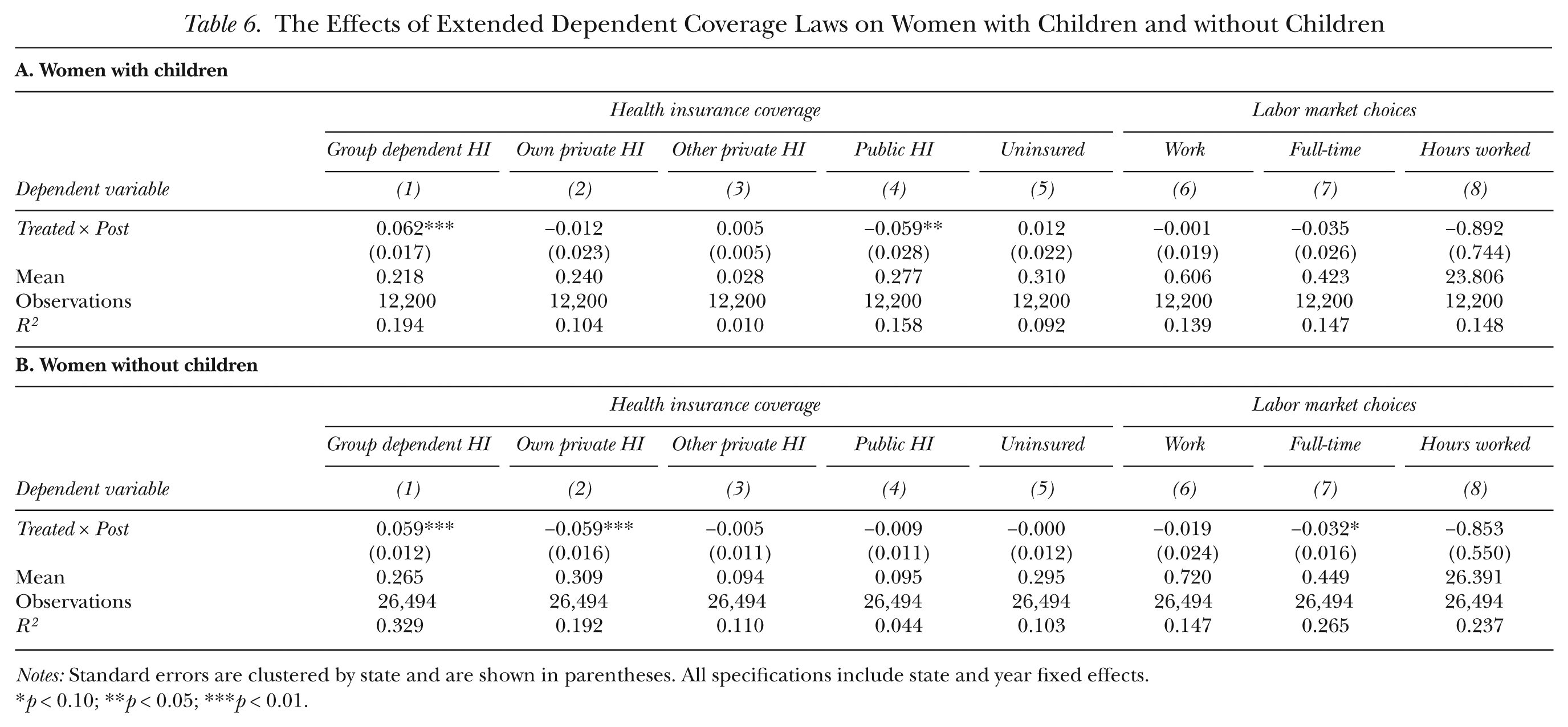

Table 6 further examines the effect of extended dependent coverage laws on women categorized by whether they have children. Women, both with and without children, show a similar likelihood of being covered by group dependent coverage upon being eligible (the difference is not statistically significant). The increase in dependent coverage among women with children is mostly driven by reduction of public health insurance. In contrast, childless women replace own private insurance with dependent coverage. Women with children might have a higher chance of reverse crowding out as they are about three times more likely to be covered by public insurance than are childless women (27.7% vs. 9.5%). 25 Some eligible young adults previously covered by public insurance might find it advantageous to switch to dependent coverage because of the differences in perceived quality offered by public and private insurance. Dependent coverage is extended from parents’ private health insurance, and private insurance is likely to provide better access to care than is public insurance, with potentially less stigma attached (Remler and Glied 2003; Hahn 2013). The reduction in labor supply is less salient among women with children since fewer such women were working compared with women without children (60.6% vs. 72%). The likelihood of decreasing full-time work is similar in magnitude (column 7), but it is imprecisely estimated with a larger standard error for women with children. Switching to dependent coverage from public insurance without much change in labor supply among women with children would be welfare-enhancing as this switch is most likely initiated by those who put stronger emphasis on quality of health insurance (or those who are concerned with stigma).

The Effects of Extended Dependent Coverage Laws on Women with Children and without Children

Notes: Standard errors are clustered by state and are shown in parentheses. All specifications include state and year fixed effects.

p < 0.10; **p < 0.05; ***p < 0.01.

The Effects of the Extended Dependent Coverage Laws with Restricted Sample

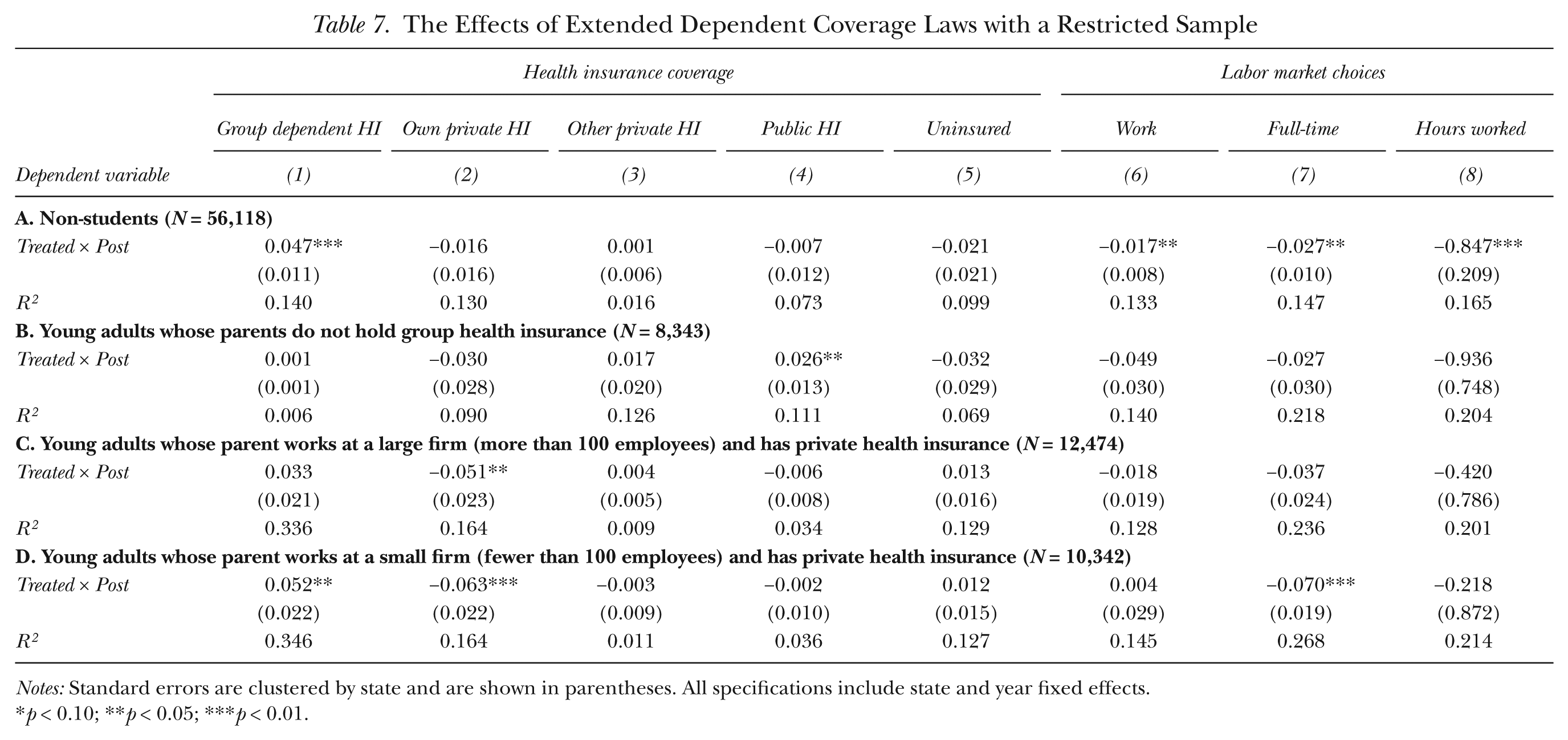

Table 7 shows the effects of dependent coverage laws using several sample restrictions based on student status and parents’ characteristics. The results shown in panel A are estimated using only non-students since the newly affected group is composed of non-students and they are the more relevant population for examining labor market outcomes. The restriction allows the comparison group to be more similar to the treated group. As discussed, we do not find any behavioral change in the likelihood of being a student in response to the law changes, and hence, sample selection bias is less of a concern. The results show that the newly eligible young adults, upon changes in the law, are more likely to be covered by group dependent health insurance relative to their counterparts who are non-students and are unaffected by the law. When this different comparison group is used in the analysis, we do not observe any significant decline in the probability of having own coverage, although the sign is the same as in the main results. The next columns show the labor market outcomes for non-students. We find a pattern similar to that in the full sample: labor supply and full-time work decrease by 1.7 and 2.7 percentage points, respectively. That is, those non-students newly affected by the change in the law are less likely to work full-time than are the non-students unaffected by the law, decreasing overall labor supply among this group.

The Effects of Extended Dependent Coverage Laws with a Restricted Sample

Notes: Standard errors are clustered by state and are shown in parentheses. All specifications include state and year fixed effects.

p < 0.10; **p < 0.05; ***p < 0.01.

In the remaining panels in Table 7, we restrict the sample to young adults by various parental characteristics. As previously discussed, there is lack of concern for the selection bias based on parents’ eligibility. The main results presented so far were based on a sample comprising all young adults without considering the implications of ERISA, which exempts self-insured firms (which are likely to be large firms) from state-level regulations. Thus, only those parents who work in fully insured firms and who hold group health insurance can extend their group coverage to their adult children. We do not exploit this narrower definition of eligibility (i.e., both young adults and their parents satisfy the requirements) as the main benchmark, as we have only a crude proxy for fully insured firms, which is firm size, and parental information is available only for those young adults who live with their parents. What is presented here, therefore, is meant to provide suggestive evidence showing whether the general predictions implied by the presence of ERISA hold.

Following from ERISA, we posit that parents are more likely to be able to extend their coverage if they hold group health insurance and work at small firms with fewer than 100 employees. In panel B, we show the results for the sample comprising young adults whose parents do not hold any group health insurance and are thus least likely to extend group coverage. The coefficient estimate on Treated × Post is generally close to zero and insignificant. One exception is in column (4) when the outcome variable is public health insurance, where the coefficient estimate is positive and significant. One possible reason is that some arbitrary correlation between public health insurance and the policy for this particular subgroup occurs, suggesting a type I error. Another possible reason is that some young adults in this particular subgroup might have been eligible for public health insurance even before the expansion but did not take up such insurance because they were not aware that they were eligible. As state governments started introducing the new laws with potentially great outreach efforts such as information campaigns, however, this state-level intervention could have served to lower the information costs of eligibility rules for not only dependent coverage but also public insurance. Thus it is possible that this subgroup might become more likely to take up public coverage than before.

In panel C, we restrict the sample to young adults whose mother or father holds group private health insurance and works at a firm with more than 100 employees. Thus this subgroup is still less likely to be affected by the policy change. Again, we find that the effects are not statistically significant in most cases. One exception in panel C is column (2), in which the probability of holding own private insurance is significantly affected by the expansion. One possible reason is that our proxy for self-insured firms based on firm size is imperfect. Nonetheless, none of the labor market outcomes of main interest are significantly affected by the policy reform.

Last, in panel D, we restrict the sample to those young adults whose parents hold group private health insurance and work at small firms with fewer than 100 employees and are thus the most likely to be affected by the policy. As expected, we generally find that the law has a larger effect than the benchmark case in Table 4. This cohort is 5.2 percentage points more likely to have group dependent health insurance, and this change comes mostly from a decrease in own private coverage. Further, full-time work decreases by 7 percentage points among this group, while overall labor supply seems to be unaffected by the policy change.

Robustness Checks

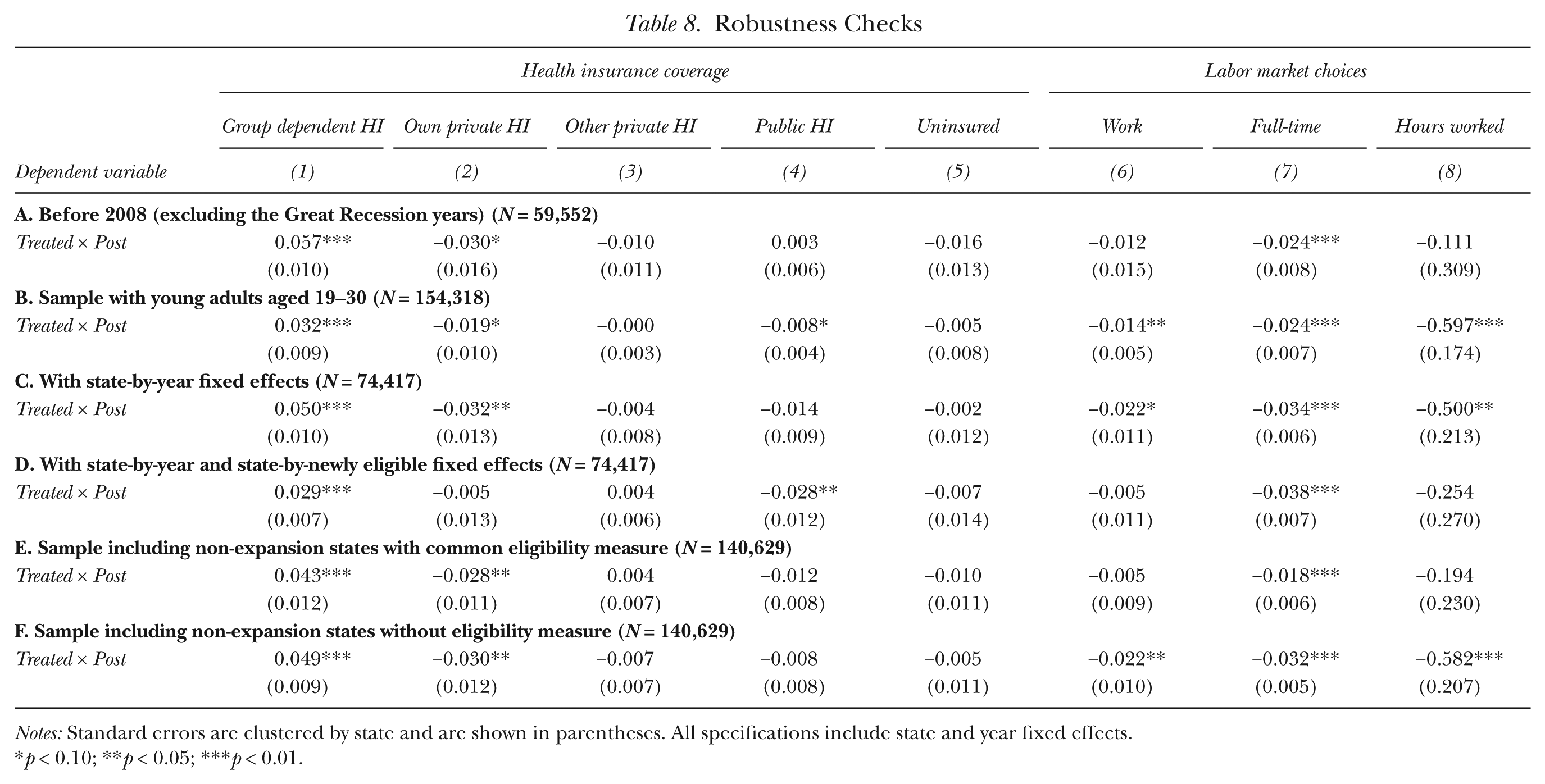

We experiment with a few restrictions on the nature of samples and specifications that may lead to a more convincing case for identification and show our results in Table 8. First, we consider that the Great Recession in 2008 might have differentially affected states’ capacity to expand private insurance, resulting in a nonrandom timing of policy implementation. We therefore use the years before the Great Recession in panel A and establish results that are similar to the baseline specifications in Table 4. We also include mortgage foreclosure rates (for both overall and subprime mortgages) as additional time-varying state control variables (the results are not shown). Different years and the additional variables do not, however, affect the results.

Robustness Checks

Notes: Standard errors are clustered by state and are shown in parentheses. All specifications include state and year fixed effects.

p < 0.10; **p < 0.05; ***p < 0.01.

So far we have focused on young adults aged 19–24 as information on student status is not available for comparatively older young adults. In panel B, we include young adults up to 30 years of age and assume that those above the age of 24 are not students. The magnitude of the effects decreases somewhat compared with the main estimates in Table 4, although the effects of the law on the probability of holding group dependent coverage, own private insurance, probability of working, working full-time, and hours worked remain statistically significant.

Next, in panel C, we show the estimates obtained after controlling for pairwise interactions of state and year fixed effects, which subsume time-varying state-specific conditions such as the unemployment rate and other welfare benefits that could have independent effects on young adults’ health insurance and labor market outcomes. The results are virtually unaffected. As a further check, we include a state-specific linear time trend. In general, this specification provides a more convincing estimate by identifying the effect independently from any existing trends in the outcome variable. It is possible, however, that including state-specific trends may actually exacerbate the bias depending on the dynamic response. Wolfers (2006) argued that the resulting counterfactuals from including state-specific trends would be misleading if the effects differ drastically across time, as the trends in this case will absorb the actual effects of the policy, not just capture the existing trends. Our coefficient estimates are not sensitive to the inclusion of these trends (the results are not reported), indicating less concern for confounded counterfactuals that consist of not only the existing trends but also the response to the policy shock itself.

In panel D, we further include pairwise interactions of the newly eligible dummy and state fixed effects to control for time-invariant differences across eligible and ineligible young adults within each state, in addition to pairwise interactions of state and year fixed effects. We do not include interactions of newly eligible and year fixed effects because if every pairwise combination were included, there would be no separate identifying variation left over in Treated × Post. Thus, if both state and year fixed effects interact with newly eligible, then no real gain occurs from pooling with the ineligible group. The most affected outcomes are the likelihood of holding private insurance under one’s own name (column 2) and working at all (column 6), and the coefficients for these outcomes are no longer statistically significant. Under this specification, however, newly eligible young adults are still more likely to obtain dependent coverage and withdraw their labor supply from full-time employment.

Although we use only the states that passed the expansion law, so as to provide cleaner estimates, alternative strategies can be used by pooling the states that did not pass the law. Since non-expansion states have not established eligibility rules, we impose the most common eligibility criterion observed in Table 1—being unmarried—to the young adults in the non-expansion states, which is similar to the strategy used by Levine et al. (2011). Alternatively, one can include non-expansion states and presume that no young adult in these states is eligible, as was done in Monheit et al. (2011). The results of including non-expansion states are shown in panels E and F. When a common eligibility measure is used in the non-expansion states, the effects on group dependent coverage and probability of working full-time remain statistically significant at the 1% level. When we assume no one is eligible in non-expansion states, the estimates are very similar to the main results, which is not surprising as much of the variation provided by the non-expansion states is subsumed by state fixed effects.

One can also include full pairwise interactions of state and year fixed effects along with interactions of the newly eligible dummy and state fixed effects like panel D in the samples used in panels E and F, in which we include non-expansion states as additional controls. Including these pairwise interactions will, however, explicitly remove the role of non-expansion states, and thus the results controlling for these pairwise fixed effects would be the same as the results using only the expansion states. We confirmed that the results using the non-expansion states with full pairwise interactions are identical to those in panel D and omit the results.

To summarize, the sensitivity tests offered in this section suggest that the results on group dependent coverage and the probability of working full-time are robust throughout, whereas the results on own private insurance, working at all, and usual hours worked are sensitive in some specifications.

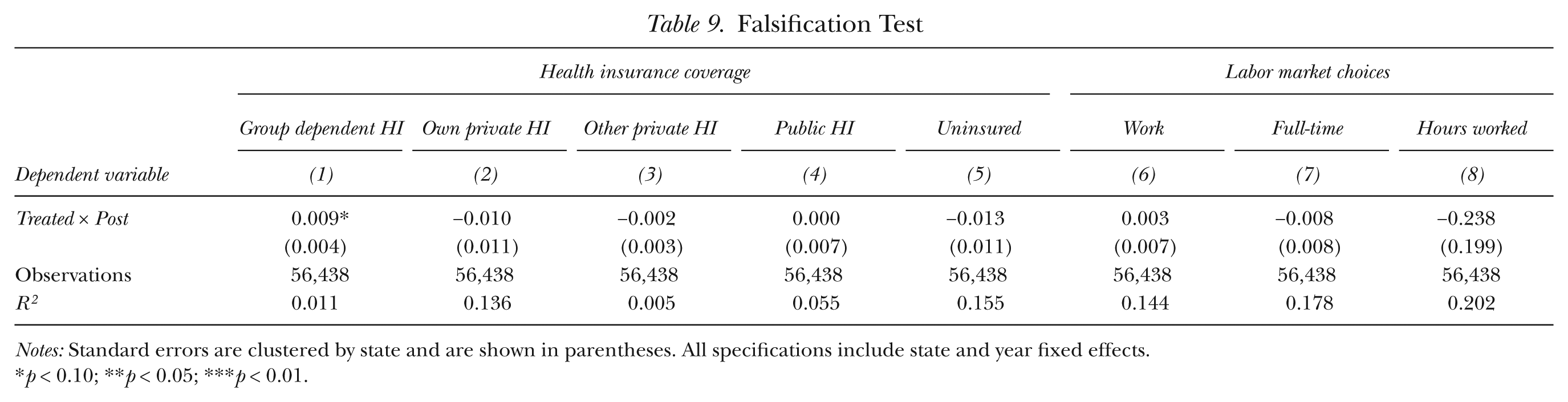

Falsification Test

As discussed, states have expanded dependent coverage but have imposed varying eligibility requirements such as age, student status, marital status, and whether young adults have children. In this section, we offer a simple falsification test using slightly older young adults whose age is high enough to prevent them from being eligible but who otherwise would satisfy the requirements of each state. The idea behind the test is that these ineligible young adults would exhibit trends similar to those for eligible young adults as they satisfy all the requirements except for the age limit requirement. Thus, if the expansion of dependent coverage truly affects the targeted group, we should observe no effect or substantially smaller effects when an ineligible sample is used than when an eligible sample is used. Table 9 shows the results using the sample of young adults up to age 30 who do not satisfy the age requirements of each state. We define Treated as meeting all the states’ criteria other than the age limit. The estimated coefficient for group dependent coverage is 0.009 and is marginally significant at the 10% level. 26 Considering that the coefficient for dependent coverage in Table 4 is 0.048, the effect is considerably smaller. Other results are close to zero and are not statistically significant, confirming that it is not trends in health insurance and labor market specific to otherwise eligible (mainly single) young adults that drive the effect. 27

Falsification Test

Notes: Standard errors are clustered by state and are shown in parentheses. All specifications include state and year fixed effects.

p < 0.10; **p < 0.05; ***p < 0.01.

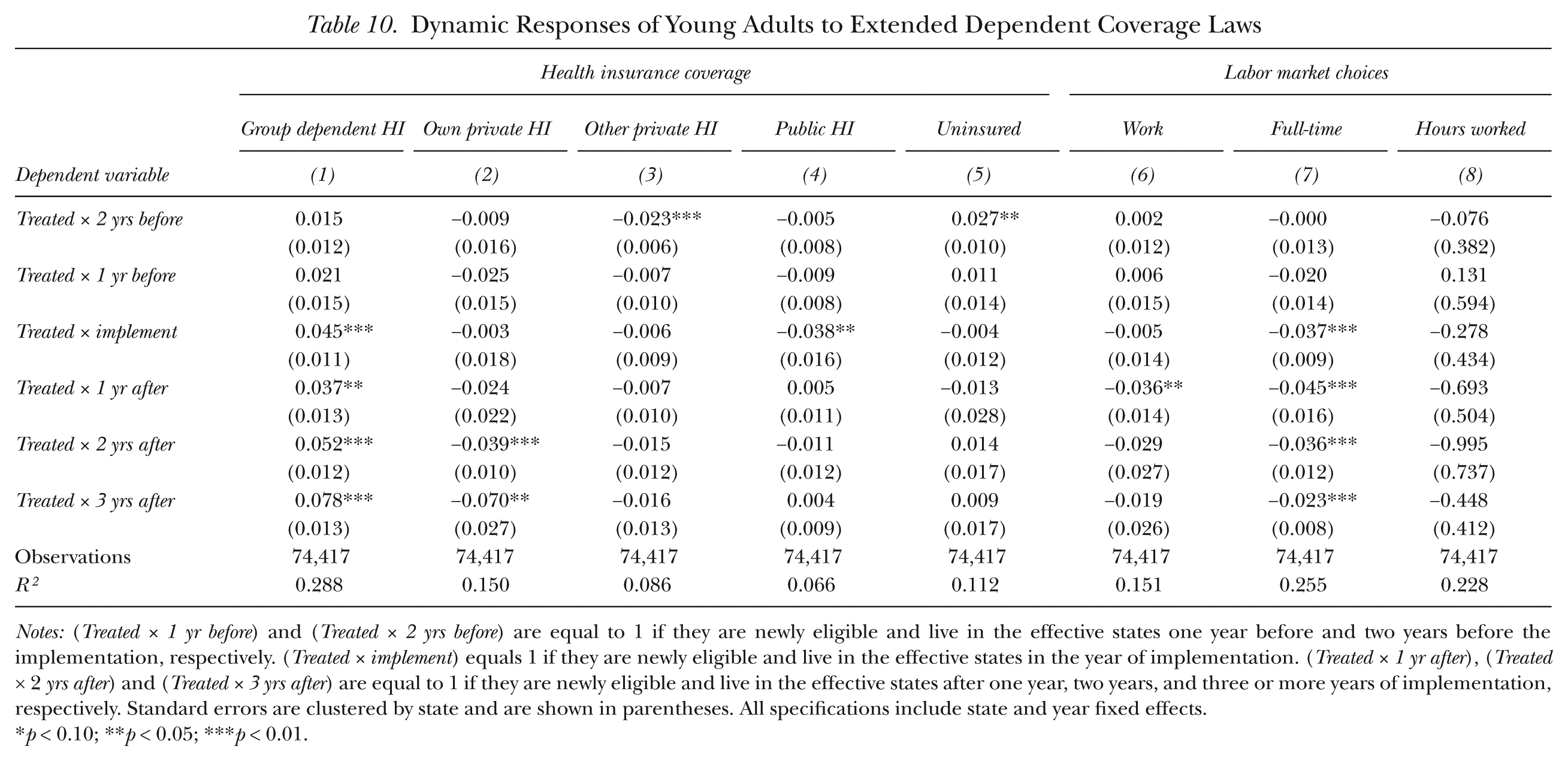

Dynamic Response of the Extended Dependent Coverage

In this section, we perform an event study analysis to investigate whether state laws have differential effects on health insurance and labor market choices across years. This analysis allows us to map out the trend in these outcomes for the periods before and after the policy changes. That is, from the event study, we can look at young adults’ dynamic responses to expanded dependent coverage provisions.

To see this, we introduce five binary variables that indicate one year, two years, and three years after the implementation of the new laws, as well as one year and two years before the implementation (so earlier lags are omitted), and interact those variables with the newly eligible variable, Treated. In particular, we estimate the following equation:

where

Table 10 reports the coefficients of the differential timing effects from the event study. In general, there is no pre-trend except for the probability of having other insurance and being uninsured. In all cases, however, the coefficients right before the policy intervention (

Dynamic Responses of Young Adults to Extended Dependent Coverage Laws

Notes: (Treated × 1 yr before) and (Treated × 2 yrs before) are equal to 1 if they are newly eligible and live in the effective states one year before and two years before the implementation, respectively. (Treated × implement) equals 1 if they are newly eligible and live in the effective states in the year of implementation. (Treated × 1 yr after), (Treated × 2 yrs after) and (Treated × 3 yrs after) are equal to 1 if they are newly eligible and live in the effective states after one year, two years, and three or more years of implementation, respectively. Standard errors are clustered by state and are shown in parentheses. All specifications include state and year fixed effects.

p < 0.10; **p < 0.05; ***p < 0.01.

As shown in column (1), there are no significant effects on the likelihood of obtaining group dependent coverage before the implementation. On the other hand, compared with the period before the implementation, those targeted by the law had a greater probability of obtaining dependent coverage in the year of implementation by 4.5 percentage points. The law gains momentum and the increase in dependent coverage is 3.7 percentage points in the second year (one year after the implementation) and 5.2 percentage points in the third year. In the later years, compared with the omitted pre-reform period, young adults are 7.8 percentage points more likely to obtain dependent coverage. Own private insurance in column (2) starts to decline two years after the intervention.

Columns (6) to (8) in Table 10 show that the pre-policy change trend is not a significant concern for labor market outcomes, as the pre-law change coefficients of work-related outcome variables are close to zero, and none are statistically significant. The effect on labor supply shows a large decline in the second year and not much effect in later years. The effect on full-time work starts to decline immediately after the implementation and peaks in the second year. The likelihood of working full-time continues to decrease in the third and later years but at a smaller magnitude.

As an increase in job mobility can be accompanied by an expansion of dependent coverage, young adults may delay providing their labor or may voluntarily withdraw from the labor market until they find a job with high match quality, particularly during the earlier period of the policy expansion. The results suggest that this tendency disappears over time. The increasing pattern shown in dependent coverage implies that the new job chosen after the period of job search tends not to offer private health insurance or that young adults prefer to remain covered by dependent coverage even when they have the option of employer-provided health insurance. The apparent increase in the rate of switching over time from own private to dependent coverage also presents a consistent story. 28

Policy Implications and Conclusion

In this article, we investigate the effects of state-level dependent coverage expansion on various health insurance and labor market choices. Young adults aged 19 to 29 are significantly less likely to have health insurance since most family insurance policies cut off dependents from coverage when they turn 19 or when they finish college. In order to improve continuity of coverage for young adults, more than half of the U.S. states have intervened in the private insurance market, mostly between 2003 and 2009, by expanding dependent eligibility to young adults aged 24 to 30.

The expected outcome of this intervention is different from that for earlier governmental efforts to reduce the uninsured rate, which mainly involved targeting poor households by expanding public insurance programs such as Medicaid and the State Children’s Health Insurance Program (SCHIP). As the eligible income threshold increased, the earlier reforms resulted in crowding out of private insurance by public insurance (Cutler and Gruber 1996). The intervention in the private insurance market, however, affects families who are not necessarily poor and who are presumably more active in the labor market. Therefore, states are faced with a potential crowding out of other types of private insurance by dependent private insurance. In addition, the tight linkage between private health insurance and employment observed in the United States can be expected to lead to unintended behavioral responses, not just in the health insurance market but also in the labor market.

Before the expansion of parental health insurance, young adults had difficulty obtaining coverage unless they had a full-time job with employer-provided health insurance. For those who qualify for expanded dependent coverage, having continued access to health insurance through their parents’ plans partially reduces the value of being employed full-time. By employing the quasi-experimental variation in the implementation years and eligibility rules of state laws that were introduced mostly between 2003 and 2009, we identify the effects of the policy changes on young adults’ health insurance status and labor market outcomes. Our baseline results suggest that the state-level expansions of dependent coverage have increased group dependent coverage among young adults by 4.8 percentage points. We find, however, no evidence that the expansions have increased overall coverage. One possible explanation for this is that newly eligible young adults endogenously respond to the changes in the law by reducing their labor supply, decreasing the likelihood of obtaining private health insurance through their own employment. This behavioral change partially undermines the states’ efforts to increase health insurance coverage, as those who were previously covered in any event initiated much of the increase in dependent private coverage. Thus the laws have been largely ineffective in attracting those who were previously uninsured, at least among the targeted group in our study. Our results are robust to a variety of empirical specifications and sample selection.

Recently passed federal health-care reforms allow young adults to stay on their parents’ plans longer by expanding dependent eligibility until age 26. The analysis of state experiences with extended dependent coverage can inform the effectiveness of these reforms. Our results show that the intervention in the health insurance market may have important implications for labor supply decisions. We find that disincentives to work full-time may have lasting effects (as long as three years after the policy implementation) and that work disincentives peak in the second year after the policy comes into effect but are mitigated thereafter. This effect on the labor market is an unintended consequence of the intervention.

Footnotes

Appendix

The Effects of Extended Dependent Coverage Laws on Health Insurance Coverage and Labor Market Choices

| Health insurance coverage |

Labor market choices |

|||||||

|---|---|---|---|---|---|---|---|---|

| Group dependent HI |

Own private HI |

Other private HI |

Public HI |

Uninsured |

Work |

Full-time |

Hours worked |

|

| Dependent variable | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

| Treated × Post | 0.048*** | −0.029** | −0.006 | −0.009 | −0.004 | −0.021** | −0.031*** | −0.555** |

| (0.009) | (0.012) | (0.007) | (0.007) | (0.010) | (0.010) | (0.005) | (0.206) | |

| Treated | −0.061** | 0.055** | −0.009 | −0.006 | 0.032 | 0.078*** | 0.068*** | 2.403*** |

| (0.023) | (0.026) | (0.016) | (0.014) | (0.020) | (0.023) | (0.019) | (0.667) | |

| Post | −0.026*** | 0.008 | 0.005 | 0.002 | 0.014 | 0.014 | 0.015* | −0.082 |

| (0.007) | (0.007) | (0.004) | (0.010) | (0.013) | (0.013) | (0.008) | (0.289) | |

| Single | −0.170*** | 0.048** | 0.069*** | −0.018 | 0.025 | 0.048** | 0.022 | 1.527** |

| (0.023) | (0.023) | (0.016) | (0.014) | (0.023) | (0.022) | (0.019) | (0.696) | |

| Female | 0.054*** | −0.006 | 0.003 | 0.060*** | −0.099*** | −0.048*** | −0.120*** | −4.457*** |

| (0.004) | (0.009) | (0.002) | (0.004) | (0.003) | (0.013) | (0.011) | (0.447) | |

| Student | 0.157*** | −0.124*** | 0.118*** | −0.041*** | −0.112*** | −0.167*** | −0.350*** | −10.069*** |

| (0.023) | (0.027) | (0.015) | (0.013) | (0.019) | (0.028) | (0.020) | (0.734) | |

| White | 0.021* | 0.022** | 0.020*** | −0.006 | −0.055*** | 0.098*** | 0.076*** | 3.601*** |

| (0.012) | (0.009) | (0.004) | (0.012) | (0.010) | (0.013) | (0.010) | (0.405) | |

| Black | 0.013** | −0.008 | −0.019*** | 0.053*** | −0.030** | 0.023* | 0.044*** | 1.628*** |

| (0.006) | (0.009) | (0.005) | (0.010) | (0.011) | (0.011) | (0.015) | (0.480) | |

| Living with parents | 0.206*** | −0.178*** | −0.081*** | 0.041*** | 0.036** | −0.164*** | −0.216*** | −7.713*** |

| (0.011) | (0.010) | (0.008) | (0.007) | (0.016) | (0.008) | (0.009) | (0.232) | |

| Mean | 0.220 | 0.314 | 0.074 | 0.106 | 0.342 | 0.724 | 0.520 | 28.429 |

| Observations | 74,417 | 74,417 | 74,417 | 74,417 | 74,417 | 74,417 | 74,417 | 74,417 |

| R2 | 0.288 | 0.149 | 0.085 | 0.066 | 0.112 | 0.151 | 0.255 | 0.227 |

Notes: Standard errors are clustered by state and are shown in parentheses. All specifications include state and year fixed effects.

p < 0.10; **p < 0.05;***p < 0.01.

Acknowledgements

We are grateful to Julie Cullen, Roger Gordon, Eli Berman, and Gordon Dahl for their insightful comments. We also thank Prashant Bharadwaj, Rachana Bhatt, Tiffany Chou, Oana Tocoian, Myoung-Jae Lee, Stephen Miller, Philip Neary, Sarada, Choon Wang, Barbara Wolfe, and seminar participants at UC San Diego, Monash University, Australian National University, University of Sydney, Yonsei University, and the 2012 Econometric Society Australasian Meeting for helpful discussions. We gratefully acknowledge financial support from Monash University.

Additional results and copies of computer programs used to generate the results presented in the article are available from the authors at

1

This calculation is from the March Current Population Survey for 2001–2010. The working-age population is defined as those aged 16 to 64.

3

In investigating the effects of the expanded health insurance on job-lock, Bansak and Raphael (2008) found that expanding public health insurance to near-poor households helps the benefited parents switch jobs without losing their health insurance. Similarly, Hamersma and Kim (2009) found that parental Medicaid expansions increase the likelihood of quitting a job voluntarily, particularly among single mothers. ![]() , using a natural experiment, found an increase in job mobility of prime age male workers as a result of the continuation of coverage mandates adopted by a number of states and the federal government.

, using a natural experiment, found an increase in job mobility of prime age male workers as a result of the continuation of coverage mandates adopted by a number of states and the federal government.

4

Most ACA proposals are applicable as of 2014, but the dependent coverage mandate was implemented as an early provision of the ACA in September 2010. This mandate allows young adults to remain covered by a parent’s health plan until they are 26 years of age. In this article, we use data up to 2010 to focus on state-level interventions.

5

The State Children’s Health Insurance (SCHIP), which has an eligibility income limit that is higher than Medicaid, is available to people up to the age of 19.

6

7

The likelihood of offering health insurance coverage among small firms (those with fewer than 10 employees) is low and has decreased substantially from 57% in 2000 to 49% in 2008 (Kaiser Family Foundation and Health Research and Educational Trust 2009).

8

For states that have not passed extended dependent coverage laws, unmarried young adults are considered eligible (the most common eligibility criterion for those states that expanded the laws is that young adults should be unmarried) in Levine et al. (2011), whereas young adults in non-expansion states are considered ineligible in ![]() . Further, five states (Illinois, Maryland, Minnesota, Missouri, and Montana) are used as reform states in Monheit et al. (2011) but not in Levine et al. (2011), while Washington State is used as a reform state in Levine et al. (2011) but not in Monheit et al. (2011). Our investigation suggests that the different assumptions about eligibility partly explain the differences between their findings.

. Further, five states (Illinois, Maryland, Minnesota, Missouri, and Montana) are used as reform states in Monheit et al. (2011) but not in Levine et al. (2011), while Washington State is used as a reform state in Levine et al. (2011) but not in Monheit et al. (2011). Our investigation suggests that the different assumptions about eligibility partly explain the differences between their findings.

9

If young adults did not work at all before the expansion, their labor supply would not change.

10

![]() argued that even those studies that use instrumental variables (which typically predict the likelihood of a spouse’s having health insurance using observable characteristics of the spouse such as human capital) are potentially biased if there is positive assortative mating on the observables. They addressed this concern by using the degree of association between spouse’s health insurance and own sick leave, which should not have any causal relationship, as a proxy for the extent of bias resulting from the assortative mating. After differencing out this bias, they found that spouse’s health insurance still has negative effects on the probability of an individual’s working full-time at a firm that provides health insurance.

argued that even those studies that use instrumental variables (which typically predict the likelihood of a spouse’s having health insurance using observable characteristics of the spouse such as human capital) are potentially biased if there is positive assortative mating on the observables. They addressed this concern by using the degree of association between spouse’s health insurance and own sick leave, which should not have any causal relationship, as a proxy for the extent of bias resulting from the assortative mating. After differencing out this bias, they found that spouse’s health insurance still has negative effects on the probability of an individual’s working full-time at a firm that provides health insurance.

11

We also used a one-year lag of the unemployment rate to avoid the concern that young adults’ labor supply may be determined simultaneously with the unemployment rate when the dependent variable concerns labor market outcomes. We found very little change in the coefficient estimates. Also, the estimates are virtually unaffected when we include pairwise interactions of state and year fixed effects, as shown below in the section on robustness.

12

The results are available upon request.

13

Data were extracted from the Integrated Public Use Microdata Series (IPUMS) website http://cps.ipums.org/cps (![]() ).

).

14

Other data commonly used to analyze health insurance come from the Survey of Income and Program Participation (SIPP). 2004 SIPP panel data, however, do not separately identify two reform states (Maine and South Dakota); the same state identifiers are assigned for Maine and Vermont, and for North Dakota, South Dakota, and Wyoming.

15

The insurance coverage variables are not mutually exclusive since young adults can report being covered under, for example, group dependent and own private insurance (less than 2% in the sample). When we estimate the baseline specification by allocating only one type of health insurance, the results do not change much across the chosen types of insurance.

16

The six types are derived by dividing each of the two main categories—group (employment-based) and non-group (individually purchased) insurance—into three possible subcategories—coverage under one’s own name, as a child dependent, or as a spouse dependent of the insurance holder.

17

![]() found that extended dependent coverage was effective in increasing health insurance coverage in some subgroups of young adults. Several aspects of their methodology are different from ours. For instance, they assumed the most common eligibility criterion that the young adults must be unmarried in states that have not passed extended dependent coverage laws, whereas we use only expansion states. We also use more updated laws and include more recent samples in our analysis. When using the assumption about eligibility as Levine et al. (2011) do, we find that the coefficient estimate of the reform on the uninsured rate is not statistically significant. The estimate, however, increases 2.5 times in magnitude, from −0.004 to −0.010, which is somewhat consistent with Levine et al. (2011).

found that extended dependent coverage was effective in increasing health insurance coverage in some subgroups of young adults. Several aspects of their methodology are different from ours. For instance, they assumed the most common eligibility criterion that the young adults must be unmarried in states that have not passed extended dependent coverage laws, whereas we use only expansion states. We also use more updated laws and include more recent samples in our analysis. When using the assumption about eligibility as Levine et al. (2011) do, we find that the coefficient estimate of the reform on the uninsured rate is not statistically significant. The estimate, however, increases 2.5 times in magnitude, from −0.004 to −0.010, which is somewhat consistent with Levine et al. (2011).

18

In 2010, annual premiums for family coverage were $13,871 and the employee share was $3,721 (26.8% of the premiums) on average, whereas the premium for single coverage was $4,940 and the employee share was $1,021 (20.7%) on average (![]() ). According to the Health and Human Services Department, the additional cost for each dependent was $3,380 per annum. If we apply the same employee share of family coverage, the employee’s marginal cost per dependent is $906. Thus, in average terms, the cost of covering an additional dependent through family coverage is 11% less than the cost of single coverage. In addition, some family coverage policies do not require holders to incur an additional cost in adding a dependent, and thus, the potential beneficiary would have a greater monetary incentive to take up dependent coverage.

). According to the Health and Human Services Department, the additional cost for each dependent was $3,380 per annum. If we apply the same employee share of family coverage, the employee’s marginal cost per dependent is $906. Thus, in average terms, the cost of covering an additional dependent through family coverage is 11% less than the cost of single coverage. In addition, some family coverage policies do not require holders to incur an additional cost in adding a dependent, and thus, the potential beneficiary would have a greater monetary incentive to take up dependent coverage.

19

Census data suggest that the young adult population (18–24) in the United States was 30,672,088 in 2010 (2010 Census brief: Age and sex composition). Summary statistics show that roughly 51.8% of the young adults would be newly eligible under the policy extension. Our back-of-the-envelope calculation shows that 333,650 young adults would reduce their labor supply as a result of the policy change using the estimate for the average marginal effect of the policy among those newly eligible.

20

Using the SIPP data, ![]() found that the federal dependent coverage expansion reduced the likelihood of working full-time by 2.2 percentage points after implementation, which is a 5.8% decrease (our estimate for full-time working is a 6% decrease); however, they did not find a significant reduction in probability of being employed. The difference between their estimates and ours could reflect that some of the young adults in control groups in their study were already affected by the state-level reform before the ACA. In addition, the two sets of results are not directly comparable because of the differences in data sets, empirical strategy, and period of study. The overall labor displacement effect of the ACA, however, could be larger than the state-level intervention because the federal reform affects a broader population.