Abstract

Do employees fare better in firms they partly own? Examining workers’ reviews of their employers on Glassdoor, the authors compare employee satisfaction between firms in which workers own company shares through an employee stock ownership plan (ESOP) and conventional firms in which they do not. Focusing on establishments in US manufacturing, the authors find employees report greater satisfaction in firms with ESOPs overall and with specific job attributes such as culture and work–life balance. The satisfaction premium associated with an ESOP is greater when the ESOP is collectively bargained or employees own a larger stake of firm equity. Employee satisfaction thus differs by ownership arrangement.

Keywords

The idea of employees having ownership in their firms has been of great interest to policymakers across the political spectrum. From Margaret Thatcher 1 and Ronald Reagan 2 to Bernie Sanders, 3 both right-leaning and left-leaning policymakers have advocated for employee ownership. Academic researchers as well have expressed support for the idea that offering employees a stake in their firms can lead to a more engaged workforce, more productive firms, and a more equitable society. In his 19th-century writings on political economy, morals, and utilitarianism, John Stuart Mill argued that employee ownership would provide such benefits, and in addition, contribute to workers receiving greater happiness from their employment. 4 We empirically test Mill’s hypothesis, asking whether workers experience improved satisfaction in firms with ESOPs.

Though employee ownership can be implemented in diverse ways and degrees, employee stock ownership plans, or ESOPs, are the most common vehicle in the United States for implementing broad-based employee ownership. Other ownership structures include, for instance, broad-based equity compensation plans, employee ownership trusts, cooperatives, and professional partnerships. 5 According to data from the National Center for Employee Ownership (NCEO), approximately 6,300 firms in the United States have an ESOP, representing about 14.7 million workers. 6 ESOPs are not just a US phenomenon; they are also prevalent in other large economies. In Europe, as of 2022, there were approximately 6.8 million employee shareholders who collectively held €447 billion in capitalization. 7 In China, by the end of 2019, at least 430,000 employees were participating in a company ESOP. 8 Employee ownership is thus a global phenomenon that impacts millions of workers.

Various potential benefits of employee ownership involving, for instance, pay, fringe benefits, job security, or job satisfaction, have been evaluated empirically in other contexts. In this article, we focus on employee satisfaction between firms that are partly or fully employee-owned through an ESOP and conventional firms in US manufacturing. The presence of an ESOP may alter employee satisfaction since, for instance, ESOPs operate within a legal framework specifying arrangements for direct and indirect influence from employees in firm decision-making. Additionally, since workers directly profit when the firm profits, interpersonal relationships between coworkers and supervisors may differ in the presence of an ESOP, for better (e.g., collaborative teamwork) or for worse (e.g., peer pressure).

Compared with past work, we leverage a large data set that spans many firms with many establishments in many labor markets. We distinguish between ESOP firms and conventional firms. Further, we distinguish between ESOPs that were introduced by management and ESOPs that were introduced through collective bargaining between unions and management. We differentiate between these two types of ESOPs because collectively bargained ESOPs may be established such that workers have more influence on workplace decisions, which in turn can enhance the provision of workplace amenities that are associated with improved job satisfaction. We also identify whether an establishment is unionized. Within a firm, some establishments may be unionized while others are not—meaning a firm with a collectively bargained ESOP may have both, unionized and non-unionized establishments.

Theoretically, we analyze the implications of employee ownership for employee satisfaction. First, firms with ESOPs are likely to provide bundles of compensation, workplace culture, workplace safety, and other amenities that, for a given expense, more closely align with workers’ preferences because of a greater willingness to share information by both management and workers. Second, with greater cooperation among employees in different roles and ranks as well as between workers and management, productivity is likely to be greater in ESOP firms than in conventional firms, generating a larger surplus that can be in part allocated to workers in the form of better pay and working conditions. Additionally, we posit that ESOPs introduced through collective bargaining agreements will exhibit stronger effects on employee satisfaction than ESOPs that are introduced by management alone.

Empirically, we use employer reviews from Glassdoor to compare employee satisfaction between firms with ESOPs and conventional firms. Because substantial heterogeneity occurs across sectors of the economy by, for instance, job design, compensation, and organizational culture, to reduce the effect of any such unobservables we narrow in on a large cross-section of workers in the US manufacturing sector over the past decade. To identify the relation between employee ownership and employee satisfaction, the ideal experiment would be to randomly assign workers to firms and randomly assign firms to having an ESOP. This approach is, of course, not feasible. While we do test how employee satisfaction evolves after a firm adopts an ESOP compared with conventional firms that do not, using a difference-in-differences framework, it is not our benchmark specification because there are few ESOP adoptions and few employee surveys before and after adoption to argue a definitively causal relation. We instead employ as our benchmark a fixed effects research design. We identify establishments operating in the same industry and geographic area that belong to either an ESOP firm or a conventional firm and compare employee satisfaction between them.

Previous Literature

Most of the literature on employee satisfaction and employee ownership focuses on just one or a few determinants of satisfaction and on a single aspect of ownership. Any trade-off that exists between the various components of a work arrangement are not captured in most studies, and ownership is often defined only in terms of rights to profit. The literature provides limited inference about the association between ownership type and employee satisfaction, especially in the overlapping presence of a union—though there are exceptions, such as Kruse, Freeman, and Blasi (2010) and McCarthy et al. (2011), which we outline below.

Several studies compare worker outcomes between firms with employee ownership and conventional firms. The most comprehensive study is that of Kruse et al. (2010), who concluded “prior research on employee outcomes under shared capitalism has yielded generally positive results,” but note the results may be context specific. Kruse et al. (2010) considered two samples: the nationally representative General Social Survey (GSS) and a National Bureau of Economic Research (NBER) sample, which is a survey of employees in 14 US firms, nine of which have an ESOP and only one of which is publicly traded and employees control a minority ownership stake. In firms with greater employee involvement in shared capitalism (e.g., profit sharing, gain sharing, stock options, or employee ownership), Kruse et al. (2010) documented tendencies for greater participation in decisions, higher quality supervision and treatment of employees, greater concern for workplace safety, greater pay and benefits, improved job security, and higher job satisfaction. That said, there are limitations. For one, the two samples produced mixed findings. While job satisfaction is statistically greater under shared capitalism in the NBER sample—and only when other human resource policies are not accounted for—it is not statistically significant for the GSS sample. Additionally, the waves of the GSS considered in Kruse et al. (2010) do not record whether the firm has an ESOP, 9 and the NBER sample comprises a few firms that were each intentionally selected because of their use of shared capitalism—limiting the generalizability of these results to ESOPs more broadly or ESOPs of varying types, e.g., those for publicly traded firms or established through collective bargaining.

Specific job attributes that may affect employee satisfaction have been studied in the context of ESOPs. For job security, Kurtulus and Kruse (2018) observed, among publicly traded firms, greater employment stability in ESOP firms. Garcia-Louzao (2021) found that ESOP firms in Spain offer greater employment stability than conventional firms, while wages and hours worked fluctuate similarly across both firm types. For labor turnover, Whitfield, Pendleton, Sengupta, and Huxley (2017) found no association with employee share ownership schemes in the United Kingdom. For wages, Kim and Ouimet (2014) concluded that introducing an ESOP in public firms does not reduce wages. Using data from the Survey of Consumer Finances, Kruse et al. (2022) found that employee share owners are not overexposed to financial risk. For workplace safety, the emerging evidence suggests positive effects from an ESOP, such as a reduction in injury rates (Palis and Kruse 2024), though Grunberg, Moore, and Greenberg (1996) found workplace safety was no better, and perhaps worse, in firms with employee ownership in the plywood industry. 10

Our focal measure of interest is employee satisfaction. While previous work has considered job satisfaction and employee ownership, such analyses have largely been limited to single firms or occupations and found mixed conclusions. 11 Long (1978) found job satisfaction increased after employees purchased a trucking company; Tucker, Nock, and Toscano (1989) showed employee satisfaction rose after an ESOP was introduced at a small company; and Gamble, Culpepper, and Blubaugh (2002) showed, in a comparison of 321 airline pilots across three firms, that employees in a firm with an ESOP experience greater job satisfaction as their perceptions of management’s commitment to the ESOP strengthen. Further, using survey data from 37 firms with ESOPs, Klein (1987) observed greater employee satisfaction when the company makes larger contributions to the ESOP, management is strongly committed to employee ownership, and the firm maintains an extensive ESOP communication program—a finding echoed by Buchko (1992). Arando, Gago, Jones, and Kato (2015), however, examined retail cooperatives that belong to the same firm but differ in their degree of employee ownership and concluded workers with fuller ownership and voice report lower satisfaction than those with more limited participation.

A key innovation in using the Glassdoor data is the possibility to examine employee satisfaction not just overall but with regards to workplace attributes, such as firm culture and work–life balance. Workers place high monetary value on having improved non-wage attributes (Maestas et al. 2023), and intangible aspects, such as culture and respect, factor into the satisfaction workers experience from their working arrangements (Dube, Naidu, and Reich 2022; Sockin 2022). Considering only differences in pay or fringe benefits would overlook additional benefits or compensating differentials workers may face working for a firm with an ESOP.

The literature suggests mixed effects of ownership type on the elements of working arrangements that determine employee satisfaction. Past work has generally analyzed small samples and few firms, focused on variation within ESOP firms rather than against conventional firms, and not considered the interplay between an ESOP and a union. A rare exception is McCarthy et al. (2011), who investigated if an interaction effect occurs between shared capitalism and unionization on job satisfaction. But unionization in this context refers to union presence at the establishment level, not whether the firm has a collectively bargained ESOP. We analyze both. Further, the takeaways of McCarthy et al. (2011) were mixed, since the interaction effect is sensitive to accounting for other working conditions, such as job security and close supervision. The literature has also often made comparisons between firms with multiple establishments, which may differ not only by ownership type but along other dimensions, such as location, industry, unionization, and size. Thus, it remains inconclusive which ownership arrangement provides greater satisfaction to employees.

Theoretical Framework

Properties of Employee Ownership in ESOPs

An ESOP is a broad-based ownership plan in which employees across organizational hierarchy levels participate. The firm contributes stock or money to purchase stock for an ESOP trust, using loans, union-negotiated wage concessions, or firm profits. The trust allocates shares proportionally to employees’ compensation (below a ceiling to prevent top-heavy ownership) and tenure, though some firms distribute shares equally. Employees collectively may own any percentage of firm equity, from minority stakes to complete ownership. 12 ESOPs are introduced for several reasons, including a desire to motivate workers for better performance; management in public firms seeking to ally with employees to control a larger share of shareholder votes to ward off a hostile takeover attempt; an owner’s desire to share company wealth with workers; a mechanism for retiring owners to sell a company; tax benefits; and workers foregoing wage increases in exchange for ownership, often to preserve jobs. 13

ESOPs can be established in two ways. The first is unilaterally by management, referred to herein as management-introduced ESOPs. The second is through collective bargaining with labor unions, referred to herein as collectively bargained ESOP (Hoffman and Brown 2017; Foley et al. 2025). In management-introduced ESOPs, all employees are eligible to participate, regardless of union affiliation, though unions may choose to decline participation (Yates 2006). In collectively bargained ESOPs, management and unions negotiate the terms of the ESOP, which may include employee involvement in decision-making, union- or worker-elected trustees, expanded roles for ESOP committees, and a continued role for unions in administering the ESOP. While collectively bargained ESOPs represent a minority of ESOP firms, they often include large companies with substantial union presence, for example, Ford, Cummins, and Caterpillar (Foley et al. 2025).

US federal regulations specify aspects of ownership rights allocation, supplemented by firm-specific details in the “ESOP document,” which is drafted by management with union input in collectively bargained ESOPs. Ownership rights span three key dimensions:

ESOP committees, which are present for most ESOPs, provide another channel for employee influence. Committee members may be appointed by the board, elected by employees, or staffed by volunteers, and they facilitate communication between employees and management while encouraging participation in establishment-level decision-making (Clifford, Rodgers, and Mackin 2003). 14 ESOP trustees and committees act on behalf of all ESOP participants, including employees across skill levels and managerial employees.

In contrast to the broad representation of ESOP structures, unions typically represent only segments of non-managerial employees and generally lack corporate voting rights or board representation. As noted above, firms with collectively bargained ESOPs often introduce additional forms of employee participation, elevating employee influence at both establishment and corporate levels (Yates 2006).

Union involvement may further enhance information access. Establishments in ESOP firms with union presence employ more communication and participatory techniques than those without unions (Yates 2006). The extent of ownership in unionized establishments correlates positively with enhanced information access, training, and participation opportunities (Logue and Yates 2001)—effects particularly pronounced for firms with collectively bargained ESOPs in which unions directly assist in establishing ESOP structure.

Employee Satisfaction

Employee satisfaction represents the utility an employee derives from various job elements, including compensation, benefits, safety, job stability, autonomy, advancement opportunities, interpersonal relations, work–life balance, and recognition. Researchers often use employee satisfaction as a proxy for employee well-being, as it constitutes a “viable index of the work-related component of utility” (Bryson et al. 2016) and may be the only measure capturing “the entire panoply of job characteristics” (Hamermesh 2001). Employee satisfaction though is not necessarily personal well-being; whereas the former is specific to one’s job—meaning it excludes aspects of one’s life outside of their job—the latter can be seen as reflecting aspects of life both on and off the job (Wright and Bonett 2007).

Different elements contribute to overall satisfaction, and similar satisfaction levels can result from various combinations of these elements. Given that individuals vary in their preferences, employees will value job attributes in dissimilar ways, with some, for instance, preferring autonomy at the expense of safety, and others perhaps preferring the opposite.

Mechanisms Linking Ownership to Employee Satisfaction

We theorize that employee ownership may enhance employee satisfaction relative to conventional firms through three distinct yet interrelated mechanisms: 1) increased productivity generating a larger economic pie, 2) preferential distribution of resources to employee-owners, and 3) better alignment between workplace elements and employee preferences. The strength and effectiveness of these mechanisms in particular organizations depend on, for instance, how well employee ownership is implemented (e.g., the reliance on complementary practices), the intensity of employees’ ownership stake, and the presence of a union and its functions. We comment on some of these factors below.

Mechanism 1: Enhanced Productivity Through Ownership Rights

In ESOP firms, incentives are more closely aligned across all stakeholders. Broad-based ownership connects employees at all organizational levels, fostering cohesion throughout the hierarchy of the firm. Employee-owners have stronger incentives to work efficiently and monitor the performance of their peers, though free-rider tendencies may moderate this effect. Access to operational information enables employee-owners to identify improvement opportunities, while decision-making rights empower them to act on such insights.

This alignment of incentives and responsibilities reduces agency problems and promotes collaboration, motivation, and productivity (Kim and Han 2019). The dual stake of employment and wealth gives employee-owners longer time horizons than external shareholders, encouraging decisions that generate long-term productivity. 16 Bryson and Freeman (2010), for instance, showed a positive association between shared capitalism and labor productivity among UK firms.

Research has identified complementarity among these practices as crucial for productivity. Such combination of practices, often termed high-performance work systems (HPWS), contribute to productivity and positive employee outcomes (Ben-Ner and Jones 1995; Ichniowski and Shaw 1997; Cappelli and Neumark 2001; Bloom and van Reenen 2011). ESOP firms inherently align incentives, decision-making, and information sharing into a cohesive system. While some conventional firms adopt similar practices through profit-sharing and information sharing, these can be altered or terminated at management’s discretion (often appearing as “flavor of the month” initiatives), whereas ESOPs are more difficult to terminate, especially those that have been established through collective bargaining.

On balance, theoretical arguments suggest ESOPs achieve greater productivity than comparable conventional firms, generating larger resource pools that can support higher satisfaction for all stakeholders, including employees. This productivity advantage likely increases with the proportion of employee ownership. However, as noted in the literature (Faleye, Mehrotra, and Morck 2006; Guedri and Hollandts 2008), strong employee decision-making power at the company level, when used to prioritize employee benefits over external shareholders’ interests, may offset potential productivity gains.

Empirically, whether an ESOP increases the size of the surplus to be shared with employees remains inconclusive. A meta-analysis on a diverse set of firms with employee ownership and conventional firms in many countries by O’Boyle, Patel, and Gonzalez-Mulé (2016) suggested a small productivity advantage for employee-owned firms. A study of Japanese firms found that the introduction of an ESOP increased productivity 4–5%, with these gains taking years to materialize (Jones and Kato 1995). A study of UK firms found mixed evidence for labor productivity and financial performance in the presence of an ESOP, suggesting the relation may be context-specific and vary with economic conditions (Whitfield et al. 2017). For ESOPs in publicly traded firms, Kim and Ouimet (2014) documented productivity gains, especially among smaller firms. Faleye et al. (2006) argued increased labor power in firm governance—through employee block ownership of more than 5% of shares acquired via ESOPs, other stock-based benefit plans, or a combination of both—impedes risk-taking, mergers, and long-term investments because employees are more risk-averse than traditional shareholders, resulting in slower growth and lower productivity. Using French data, Guedri and Hollandts (2008) identified an inverted U-shaped relation between employee ownership and performance: While moderate levels of ownership enhance motivation and satisfaction, beyond a threshold, the negative effects described by Faleye et al. (2006) outweighed the benefits. A summary of the literature is cautiously presented by Kruse et al. (2022): “The accumulated evidence on the economic performance of firms that have employee ownership gives no reason to think that performance would be hurt, and in fact suggests that performance may be enhanced.”

Mechanism 2: Preferential Distribution of Firm Resources

Through decision-making rights and information access, employee-owners can influence resource allocation to favor their interests. This provision includes enhancing wages, benefits, and workplace amenities, potentially at the expense of external shareholders.

Low- and mid-level managers in firms with employee ownership may be sympathetic to their subordinates’ needs, having observed the positive effects of ownership on motivation and productivity. These managers also benefit from many of the same non-excludable amenities as their subordinates, including organizational culture and work–life balance, motivating them to support improvements to employee well-being.

This redistribution effect strengthens as employees gain larger ownership stakes and in firms with collectively bargained ESOPs where unions formalize employee input into governance structures. Corradini, Lagos, and Sharma (2025), for instance, showed that when unions make women central to their agenda, collective-bargaining agreements include more female-friendly amenities; and as a result, turnover and absenteeism fall, suggesting improved job satisfaction.

Mechanism 3: Alignment of Resource Allocation and Employee Preferences

Many aspects of the workplace function as public goods, provided at similar levels to employees in the same unit or job category. With heterogeneous preferences, satisfaction levels vary for identical combinations of job attributes. Average satisfaction increases when resources align with average employee preferences rather than those of “marginal” employees (i.e., those who are indifferent between staying with the firm or exiting).

Employee ownership facilitates the expression of workers’ preferences through improved communication channels, decision-making participation, and reduced concerns that management will misuse information about workers’ desires (Drèze 1976; Jirjahn and Smith 2018). Consequently, even if total resources allocated to employee well-being were identical between employee-owned and conventional firms, employees in the former would likely derive greater satisfaction because resources would better match their true preferences.

Unions enhance this mechanism through systematic preference aggregation, but typically represent only part of the workforce, and union–management relations in conventional firms often suffer from mistrust. This mistrust may also affect firms with management-introduced ESOPs, especially when unions decline ESOP participation—potentially diminishing the differences between, in the presence of a union, firms with management-introduced ESOPs and conventional firms.

Collectively Bargained vs. Management-Introduced ESOPs

These three mechanisms should operate more strongly in firms with collectively bargained ESOPs than in firms with management-directed ESOPs given differences in implementing fundamental ownership rights.

For productivity enhancement, collectively bargained ESOP firms benefit from established union–management communication channels that facilitate information sharing and provide additional employee voice. While management-introduced ESOPs also provide information rights and decision-making influence, they may less effectively aggregate employee knowledge without formalized collective representation. The joint commitment to the ESOP by management and unions in collectively bargained ESOPs fosters trust and cooperation, reducing adversarial relationships that could undermine productivity.

Regarding resource distribution, union involvement in collectively bargained ESOPs provides an institutional framework for advocating employee interests in corporate decisions. Unions’ expertise in negotiating compensation, benefits, and employment terms, combined with ownership rights, likely secures more favorable resource distribution than in management-directed ESOPs, where employee advocacy lacks comparable institutional support.

For preference alignment, firms with collectively bargained ESOPs likely achieve improved matching between workplace attributes and employee preferences through unions’ systematic information gathering via surveys, meetings, and elected representatives. This structured preference aggregation complements ESOP participation, producing more accurate knowledge about employee priorities. Firms with management-introduced ESOPs may attempt similar information gathering, but without independent institutional structures, these efforts may be less comprehensive and credible.

The asymmetric information theory of strikes (Tracy 1986; Card 1990) helps rationalize why collectively bargained ESOPs might generate greater satisfaction. By reducing information asymmetries, these arrangements lower the risk of disputes and improve bargaining efficiency. Cramton, Mehran, and Tracy (2008) found that strike incidence declines after ESOP adoption in unionized firms, and Cramton, Tracy, and Mehran (2015) showed that the announcement of a collectively bargained ESOP yields significantly larger stock market gains compared with the announcement of a management-introduced ESOP.

It remains an open question whether the mechanisms for collectively bargained ESOPs described above are enhanced or muted when the establishment locally has union coverage. We do not conjecture here about the effects of local union presence on job satisfaction between collectively bargained and management-introduced ESOPs; we instead consider it an empirical question—one that given our data we can examine.

Hypotheses and Selection Issues

Based on our theoretical framework, we propose:

This follows from our three mechanisms: ESOP firms generate larger economic rents that can support improved working conditions, allocate a greater share of resources to employee well-being, and distribute resources to better match employee preferences. While effects might vary across workers, we expect positive overall effects across the workforce.

As employees’ financial stakes increase, all three mechanisms strengthen—as long as employee representatives use their governance power responsibly. Larger ownership stakes enhance productivity incentives, increase influence over resource distribution, and improve preference alignment. Greater ownership brings increased decision-making power and information access, both foundational to our identified mechanisms.

This hypothesis is based on the prediction that collectively bargained ESOPs provide greater worker influence on decision-making at all levels of a firm that may lead to a more favorable set of job attributes. The union is also a long-term legal guarantor to the implementation of the negotiated ESOP terms and the continuity of the ESOP. The formalized union role in establishing and administering the collectively bargained ESOP strengthens all three mechanisms: enhancing productivity through better information flows and cooperation, securing more favorable resource distribution through institutional advocacy, and achieving better preference alignment through systematic aggregation of employee priorities.

Before proceeding to the data and empirical analysis, we acknowledge potential selection biases. Workers who prefer participatory, long-term employment may seek jobs in firms with ESOPs, potentially inflating average employee satisfaction. Higher-quality firms might be more likely to adopt an ESOP, or conversely, firms might adopt ESOPs in response to poor performance. Our empirical design, along with our difference-in-differences analysis and numerous robustness tests, seeks to limit these concerns. Nevertheless, we interpret our results as revealing associations rather than strictly causal effects.

Data and Measures

Our analysis focuses on employee ownership in the US manufacturing sector, an industry that accounts for one-fifth of US ESOPs. 17 Our analytical sample combines a database of ESOP firms from the National Center for Employee Ownership (NCEO) and employer reviews from Glassdoor. We make use of online job ads from Burning Glass Technologies (BGT) to analyze firms’ labor demand and allocate establishments to local labor markets. We restrict the analysis to full-time employees.

Since these data sources exist separately, no single identification number is used for each firm. However, since we observe firms’ names in each data set, we can harmonize and match on names, keeping matches made with a sufficiently high degree of confidence. The details of this process are described in Online Appendix A. (Hereafter, “Appendix” will be referring to our online file.) We identify establishments as the pairing of a firm and a US city, the most granular geography observed in Glassdoor reviews.

We incorporate a number of supplementary data sources. These sources include Compustat (to identify whether a firm is publicly traded), the Office of Labor Management Standards and the National Labor Relations Board (to identify whether an establishment is unionized), pay reports from Glassdoor (to consider an employee’s wage), and the Occupational Safety and Health Administration (to consider an establishment’s injury rates). For purposes of exposition, we relegate their descriptions to Appendix B.

National Center for Employee Ownership

The National Center for Employee Ownership (NCEO) collects data from IRS Form 5500 concerning a firm’s employee stock ownership plan (ESOP). We obtain a list of ESOPs from the NCEO as of 2020 using files made available by the U.S. Department of Labor. Each observation corresponds to an active ESOP—meaning terminated plans are excluded—with more than one participant. For each ESOP, in addition to the firm name and address, we observe the plan’s start date, the number of participants in the plan, and whether the plan is pursuant to a collective bargaining agreement. In 2020, contributions made by participants in these firms and total benefits paid to participants were $93 billion and $144 billion, respectively.

The number of manufacturing firms with ESOPs in the NCEO database is 1,298. While we are able to match approximately 20% of these firms to Glassdoor, since Glassdoor coverage skews toward larger firms, the firms that we match represent 72% of all ESOP participants in US manufacturing. Most ESOPs are in privately held firms (92%) and in most ESOPs employees own a minority stake (70%). Since our sample almost entirely comprises ESOP firms in which employees hold a minority stake (see Appendix Table A1), we abstain from making separate inferences for firms in which employees hold a majority stake. Our focal variable of interest is whether an establishment has an ESOP, which we capture through an indicator equal to 1 if the firm is in the NCEO data set, and 0 otherwise. We also calculate two measures of ownership intensity to consider possible heterogeneity between ESOPs. The first is the ratio of total plan assets to total firm equity, for which firm equity is available for public firms through Compustat, and the second is the ratio of total plan assets to the number of participating employees. 18 Although a single firm may sponsor multiple ESOPs, because our empirical analysis focuses on differences between workers by whether their firm is employee-owned, distinguishing between ESOPs in the case of multiples is not of meaningful concern.

Glassdoor Reviews

Our measures of employee satisfaction come from Glassdoor, an online platform for workers to search for jobs, compare their pay with that of others, and learn about a firm’s workplace attributes through reviews written by current and former employees. Visitors to Glassdoor are incentivized to contribute through a “give-to-get” mechanism, whereby users gain access to the content provided by others once they contribute themselves. 19 To satisfy the give-to-get mechanism, a visitor typically provides an employer review or a pay report, though they could alternatively rate a firm’s benefits or disclose an interview experience.

Our analysis focuses on employer reviews, for which a sample submission form is presented in Appendix Figure A1. We also make use of workers’ pay reports but only insofar as they offer two additional observables not available in an employer review: a worker’s pay and years of work experience. We are able to merge a worker’s employer review with their pay report (if they provide both) because we observe a unique identifier for each worker. We consider reviews submitted by current or former employees from 2012 through 2024. To reduce the computational burden of matching firm names, we restrict—based on data from Burning Glass Technologies (described in more detail below)—our attention to establishments that advertise on average at least one production worker vacancy per year over a six-year period. 20

Each employer review constitutes an employee-employer match in which we observe the worker’s job title, location, firm tenure (i.e., years employed with the firm), and whether the match is still an ongoing employment relationship or has ended. For a subset of workers who have completed a profile on the platform, we observe their gender and age. Our final sample consists of 233,000 reviews spanning 18,000 establishments representing 5,500 firms. Sample sizes for ESOP and conventional firms, on average per establishment or labor market, are presented in Appendix Table A2. For an employer review, workers provide a 1–5 stars Likert scale rating for their job satisfaction overall. They similarly rate their satisfaction with five subcategories: career opportunities, compensation and benefits, culture and values, senior leadership, and work–life balance. These six ratings are our principal outcomes of interest. Beyond these ratings, each respondent provides a free-text description of the positive (“pros”) and negative (“cons”) aspects of their job. Further, workers report whether they would recommend their employer to a friend, approve of the CEO’s performance, and have a positive outlook of the firm’s prospects over the next six months.

Glassdoor reviews offer a unique look into the hard-to-observe aspects of satisfaction that may differ between employee-owned and conventional firms, yet are unavailable in nearly all other data sets with individual employers. 21 A growing body of literature has studied Glassdoor reviews to speak to employee satisfaction directly (e.g., Liu, Makridis, Ouimet, and Simintzi 2022; Sockin 2022; Gornall et al. 2025) or employer reputation with regard to employee satisfaction (e.g., Sockin and Sojourner 2023). As to whether reviews on Glassdoor have external validity for labor markets more broadly, Sockin (2022) showed that, between industries and occupations, job satisfaction ratings on Glassdoor have a robust correlation of about one-half with overall satisfaction ratings in the National Longitudinal Survey of Youth 1997 (NLSY97), a nationally representative survey. However, Sockin (2022) found the average job satisfaction level in Glassdoor was below that of the NLSY97, suggesting respondents on Glassdoor may be less satisfied than the average employee within each firm. Firms that experience improved job satisfaction ratings on Glassdoor outperform firms in the stock market that experience declines (Green, Huang, Wen, and Zhou 2019), suggesting Glassdoor ratings reveal fundamental information about firms that traditional observables cannot fully capture.

As ratings of satisfaction are intrinsically subjective, it is possible respondents differently interpret the survey or differently value an additional star. The survey does not include a description of each item, and respondents may exhibit different reporting functions (Oswald 2008) such that a three-stars rating may be considered positive for some but neutral or negative for others. As Bond and Lang (2019) noted, this latter property is problematic for comparing the mean level across subgroups—as our analysis does between workers at ESOP firms and workers at conventional firms. The comparison we are making is not across workers of different observable characteristics but rather a characteristic of the employers for whom they work, so for the psychometric properties of Glassdoor ratings to bias our results, any such differences would have to correlate with employee ownership. Further, given that we account for observable differences across workers (e.g., age and job title) and firms (e.g., Tobin’s Q and size), such differences would have to correlate with employee ownership on unobservables. We see no clear reason why they should.

Burning Glass Technologies Job Advertisements

Differences in employee satisfaction between employee-owned and conventional firms could reflect differences in hiring practices, for example, the offering of greater wages or the targeting of different skills. With this in mind, we examine online job postings from Burning Glass Technologies (BGT), which scrapes more than 40,000 online job boards and company websites. A growing literature has used BGT data to study firms’ demand for skills (e.g., Deming and Kahn 2018; Ben-Ner, Urtasun, and Taska 2023). We consider the demand for general human capital, that is, required years of education or work experience, and specific human capital, such as engineering, operations, and people skills. 22 We also consider whether advertised pay differs between employee-owned and conventional firms by considering the logarithm of the posted wage.

We focus on job postings for US manufacturing firms from 2017 to 2022. We use the BGT data to partition establishments into local labor markets, that is, industry cross commuting zone pairs. For industry, each job posting includes a 3-digit North American Industry Classification System (NAICS) code. We assign establishments to their most frequent industry. For commuting zone, we match county Federal Information Processing System (FIPS) codes in BGT to US commuting zones using the crosswalk of Autor and Dorn (2013). We incorporate two BGT measures into our benchmark specification as controls. The first, to proxy for establishment size, is the logarithm of firms’ job postings at a given latitude and longitude. The second, to proxy for firm size, is the logarithm of establishments observed for each firm. 23 The resulting sample, for which summary statistics are available in Appendix Table A4, includes 6.26 million job ads.

Sample Summary

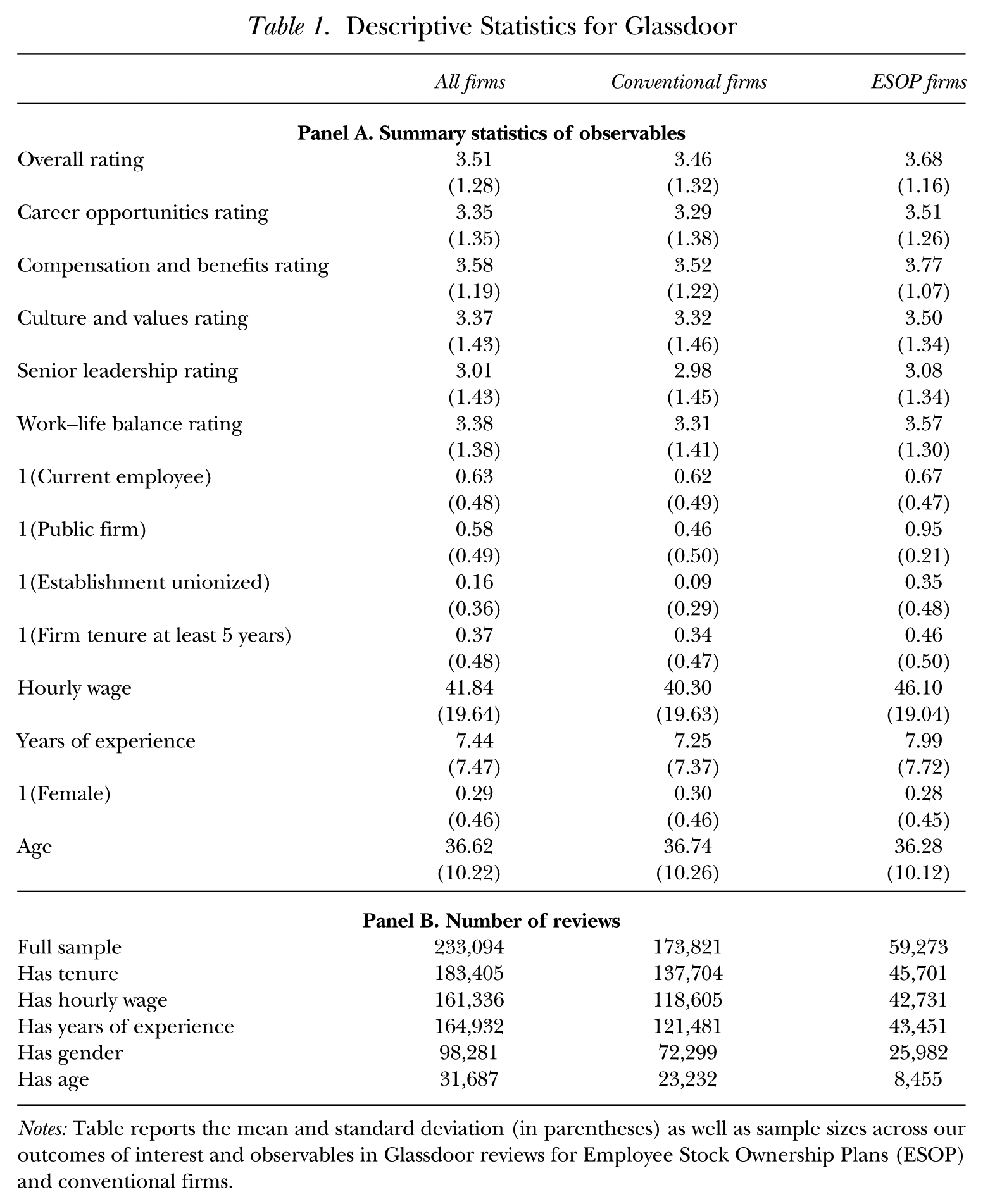

Table 1 presents summary statistics for the sample of Glassdoor reviews for ESOP and conventional firms. There are 233,094 employee reviews. The majority (63%) are submitted by current employees, 58% are from public firms, and 16% are from establishments we have identified as being unionized. Employees in firms with ESOPs exhibit longer firm tenure on average than those in conventional firms: Of workers in firms with ESOP, 46% have tenure of five years or longer compared with 34% in conventional firms. Looking at the full distribution, workers in firms with ESOPs within our sample are nearly twice as likely as workers in conventional firms to have firm tenure of more than 10 years (see Appendix Figure A2). To account for such differences in firm tenure, we include a fixed effect for each category of firm tenure in our regression analyses. Moreover, workers in firms with ESOPs report receiving greater hourly wages and have on average more years of experience. Employees in ESOP firms also report greater job satisfaction. Compared with conventional firms, workers report 6.4% greater overall job satisfaction in firms with ESOPs. They also report greater satisfaction on average with career opportunities, compensation, culture, leadership, and work–life balance.

Descriptive Statistics for Glassdoor

Notes: Table reports the mean and standard deviation (in parentheses) as well as sample sizes across our outcomes of interest and observables in Glassdoor reviews for Employee Stock Ownership Plans (ESOP) and conventional firms.

Identification Strategy

We aim to identify whether differences are apparent in latent dimensions of employee satisfaction between firms with ESOPs and conventional firms. Our identification strategy compares the Glassdoor ratings of workers in ESOP firms and conventional firms operating in the same local labor markets, accounting for observable characteristics of workers, establishments, and firms. Our benchmark empirical specification follows

where Yi,j,k,l,t reflects a Glassdoor rating submitted in year-quarter t by employee i with job title j working at firm k’s establishment in location l. The 1{ESOP}k is an indicator equal to 1 if firm k is employee-owned with an ESOP, and 0 otherwise. The vector of worker-level observables Xi,t includes an indicator for whether the worker is still employed with the firm when their review is submitted and fixed effects for the worker’s tenure with the firm. The vector of establishment-level observables Xk,l includes the logarithm of firm k’s total establishments, the logarithm of firm k’s total vacancies in location l, an indicator the establishment for firm k in location l is unionized, and an indicator firm k is public. 24 We include fixed effects λn(k),c(l) for each NAICS industry n(k) within manufacturing, of which there are 19; cross commuting zone c(l), of which there are 459; each two-digit SOC occupation λo(j); and each calendar year-quarter λt. The coefficient β captures, among workers with the same occupation in the same local labor market, the mean difference in job satisfaction between workers in an employee-owned firm and workers in a conventional firm.

Since this analysis is cross-sectional, we cannot claim a short-run causal relationship. It is possible that unobservable worker or firm factors, such as task complexity, capital intensity, or selection into employee ownership, confound our results. Nonetheless, given the richness of our fixed effects model, such factors, in order to bias our estimates, would have to be correlated with both job satisfaction and employee ownership; and at the same time, be orthogonal to our covariates, for example, the industry and size of the firm, the commuting zone, unionization of the establishment, and the worker’s occupation. It is also possible causality runs in the reverse direction. For one, it could be that workers with certain preferences select into ESOP firms—though this seems unlikely given the particularly low incidence with which ESOP firms advertise employee ownership in their job postings. 25 It could also be that more satisfied workplaces select into employee ownership. Given the infrequency with which firms adopt employee ownership during our sample period, speaking to establishment-level selection, while interesting, is not feasible. 26

To allay this concern, we consider two additional analyses. The first narrows in on workers who review both an employee-owned firm and a conventional firm, allowing for within-worker identification through the inclusion of worker fixed effects. This is discussed in the Sensitivity Analysis section below. The second narrows in on firms that adopted employee ownership. Given the dearth of manufacturing employers that convert to employee ownership after 2012 and have coverage in the Glassdoor sample, we cannot implement an event-study research design around the timing of ESOP adoption. 27 However, for a limited sample of employers that do adopt an ESOP, we can estimate a difference-in-differences design as in Kim and Ouimet (2014). 28 As this analysis is still largely suggestive, we relegate the results to the Plausibly Causal Research Design section rather than making it our benchmark. Together, the two suggest our results are less the product of selection into employee ownership and more likely the presence of an ESOP.

Job Satisfaction and ESOP Presence

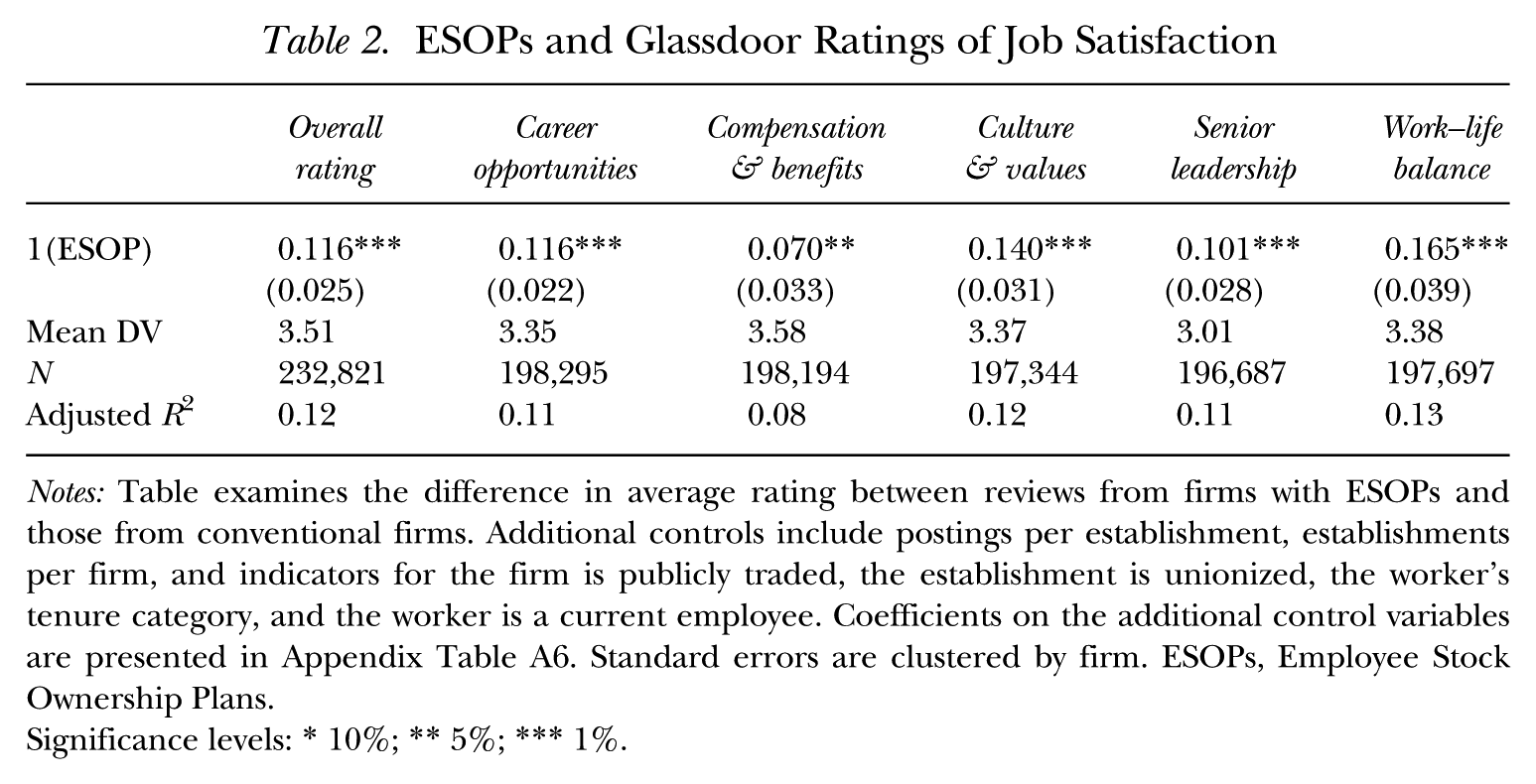

We begin by estimating Equation (1) on workers’ overall ratings of job satisfaction. The result, recorded in the first column of Table 2, is a statistically and economically significant premium of 0.12 stars in job satisfaction at ESOP firms, supporting Hypothesis 1. Given a sample average of 3.51 stars, this difference translates to a premium of approximately 3%. Put another way, given a standard deviation in overall ratings of 1.28 stars (see Table 1), employees at firms with ESOPs enjoy on average 0.09 standard deviation greater job satisfaction. To put this 0.116-star premium into perspective, it is larger in magnitude than the declines observed following news that a firm engaged in tax avoidance (Lee, Ng, Shevlin, and Venkat 2021) or corporate misconduct (Gadgil and Sockin 2025), though shallower in magnitude than the declines observed after a firm receives an Accounting and Auditing Enforcement Release (AAER) from the U.S. Securities and Exchange Commission (Zhou and Makridis 2021). 29

ESOPs and Glassdoor Ratings of Job Satisfaction

Notes: Table examines the difference in average rating between reviews from firms with ESOPs and those from conventional firms. Additional controls include postings per establishment, establishments per firm, and indicators for the firm is publicly traded, the establishment is unionized, the worker’s tenure category, and the worker is a current employee. Coefficients on the additional control variables are presented in Appendix Table A6. Standard errors are clustered by firm. ESOPs, Employee Stock Ownership Plans.

Significance levels: * 10%; ** 5%; *** 1%.

These estimates may seem economically small, and one might have anticipated larger differences given that we study structural differences in firm ownership compared with singular instances of corporate behavior. Nevertheless, it is worth noting that Gornall et al. (2025) considered the effects of private equity leveraged buyouts (LBOs), which similarly involved a change in employee ownership, on Glassdoor ratings and documented effects that are about one-half the magnitude of the premia associated with employee ownership. In turn, our estimates appear reasonably non-trivial.

Importantly, workers value being in a workplace that provides them with greater job satisfaction. Workers will forego a higher wage to enjoy amenities that provide them with greater satisfaction, for example, research (Stern 2004) or corporate social responsibility (Burbano 2016), and workers who are dissatisfied with their jobs are more likely to voluntarily quit (Freeman 1978; Akerlof et al. 1988; Card et al. 2012). One additional star in Glassdoor overall rating is valued on average by workers as the equivalent of about $10,000 in annual income (Sockin 2022). According to this estimate, employees at firms with ESOPs experience $1,160 in additional amenity value, or 1.4% of the average wage in our sample, each year from their jobs.

To better understand what aspects of work fuel this satisfaction premium, we re-estimate Equation (1) using workers’ ratings for each of the five subcategories. The coefficients are presented in the remaining columns of Table 2. Across all five dimensions, we observe greater satisfaction at ESOP firms. While the differences are broad-based, the largest gap is for work–life balance, equivalent to 0.12 standard deviations. The smallest gap is for compensation and benefits—suggesting that pecuniary differences are not the driving force behind the premium, a concern we return to in our sensitivity checks.

Heterogeneity between Firms with ESOPs

While workers in ESOP firms exhibit greater job satisfaction, not all ESOP firms are alike. For instance, some have collectively bargained ESOPs while others do not; some have ownership plans that account for a greater stake in firm equity than others.

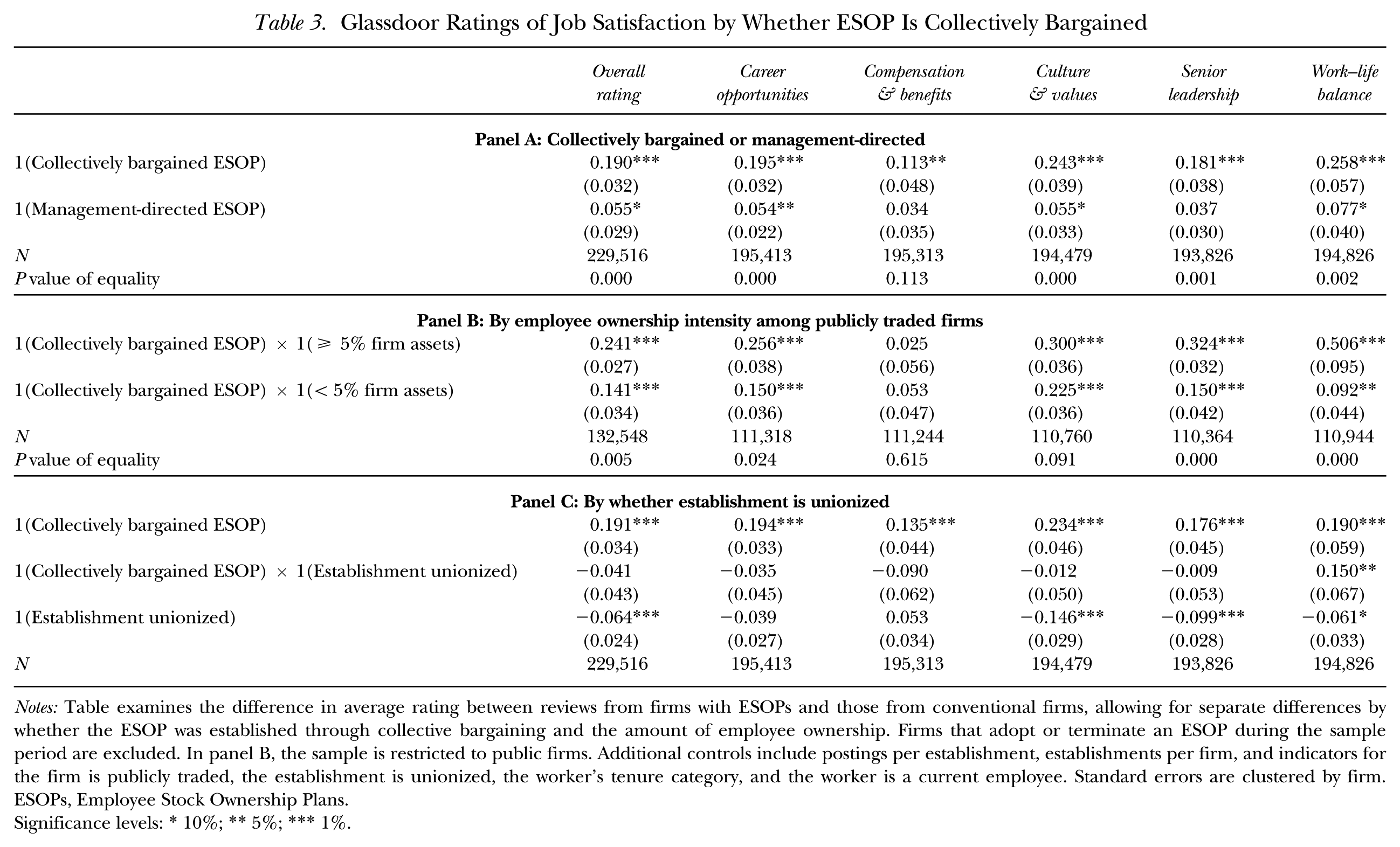

Glassdoor Ratings of Job Satisfaction by Whether ESOP Is Collectively Bargained

Notes: Table examines the difference in average rating between reviews from firms with ESOPs and those from conventional firms, allowing for separate differences by whether the ESOP was established through collective bargaining and the amount of employee ownership. Firms that adopt or terminate an ESOP during the sample period are excluded. In panel B, the sample is restricted to public firms. Additional controls include postings per establishment, establishments per firm, and indicators for the firm is publicly traded, the establishment is unionized, the worker’s tenure category, and the worker is a current employee. Standard errors are clustered by firm. ESOPs, Employee Stock Ownership Plans.

Significance levels: * 10%; ** 5%; *** 1%.

Two key takeaways emerge. First, we observe positive coefficients for job satisfaction overall for both, collectively bargained ESOPs and management-introduced ESOPs. With regard to the five subcategories, we observe, compared with conventional firms, statistically significant differences for both with respect to career opportunities, culture, and work–life balance. Second, supporting Hypothesis 2, collectively bargained ESOPs experience more than triple the gains in job satisfaction. For overall job satisfaction, as well as for satisfaction with each subcategory except compensation, the premium among firms with collectively bargained ESOPs is significantly larger than that observed among firms with management-introduced ESOPs. For firms with collectively bargained ESOPs, the additional satisfaction workers enjoy compared with conventional firms is large. Even conditional on the observables and fixed effects included in Equation (1), we observe statistically significant improvements of 0.11–0.17 standard deviations in satisfaction across the five subcategories.

This may, for instance, reflect the presence of workers’ rights being written into collectively bargained agreements, which Arold, Ash, MacLeod, and Naidu (2024) showed is positively correlated with workers’ perceptions of management being pro-worker. Note that this differential does not reflect the fact that firms with collectively bargained ESOPs tend to be publicly traded; when we re-estimate this specification restricting the sample to only publicly traded firms, the satisfaction premia are still positive and significantly larger among collectively bargained ESOPs (see Appendix Table A7).

We also consider whether there is an interaction between employee-ownership stake and whether the ESOP is collectively bargained. In panel B of Table 3, restricting the sample to public firms, we separate collectively bargained ESOPs into those representing at least 5% of firm assets and those representing less. While we document positive, statistically significant satisfaction premia for both, the premia are significantly larger for the former compared with the latter. For overall job satisfaction, whereas the premium is 0.241 stars among firms where the ESOP represents at least 5% of firm assets, it is 0.141 stars among firms where the ESOP represents less. While this suggests an additional satisfaction boon when the ownership stake is above 5%, we caution there are few firms with a collectively bargained ESOP that represents at least 5% of firm assets.

Last, we recognize between-establishment variation in unionization status within firms with collectively bargained ESOPs. So far, we have documented complementarity between unions and ESOPs by showing that the agreement between management and unions to create and maintain a collectively bargained ESOP produces greater job satisfaction than when an ESOP is introduced and directed unilaterally by management. Here we focus on the unionization status of individual establishments, which does not necessarily require the same degree of collaboration between management and unions as does the creation of an ESOP. (Some unions may even elect not to be covered by the ESOP.) In our sample, 48% of reviews for collectively bargained ESOPs are from workers in unionized establishments. To formally test whether the satisfaction premium among firms with collectively bargained ESOPs reflects the local presence of a union, we interact an indicator for the establishment that is unionized with an indicator for the firm that has a collectively bargained ESOP. The results are recorded in Table 3, panel C.

In conventional firms, workers in unionized establishments report lower satisfaction compared with non-unionized establishments overall and for each subcategory except compensation. 31 Interacting our indicator for the presence of a collectively bargained ESOP with the indicator for an establishment that is unionized produces coefficients that are not statistically different from zero, with the exception of work–life balance. 32 This finding suggests that workers throughout the firm benefit, through elevated job satisfaction, from a collectively bargained ESOP, not just those who are represented by a union—suggesting a complementarity when unions are involved in the construction of the ESOP.

Taken together, the results of Table 3 suggest a synergistic relationship between unions and employee ownership, which accords with the findings of McCarthy et al. (2011) who argued unions and financial participation are complementary.

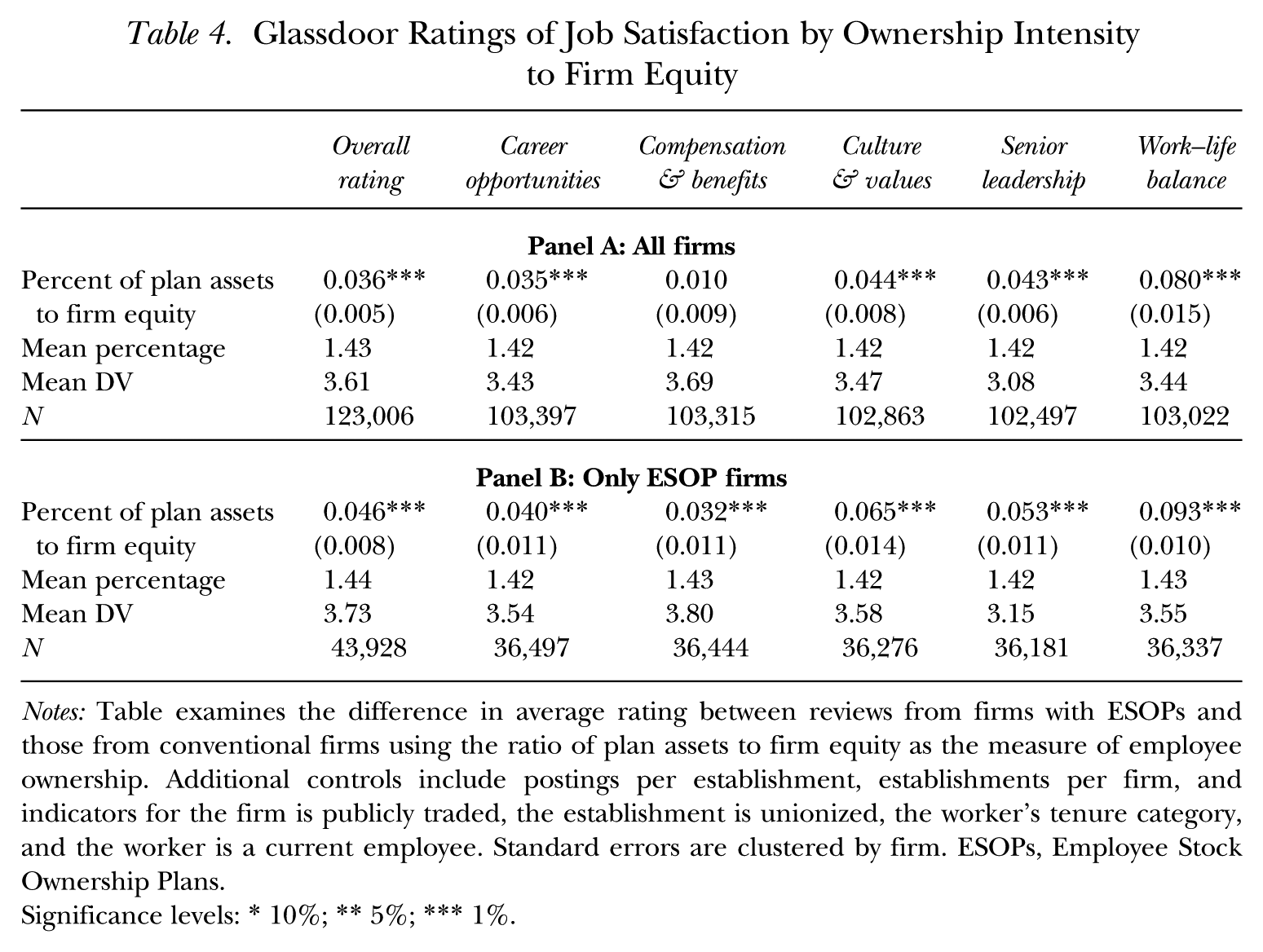

In lieu of our binary indicator, we consider the ratio of plan assets to firm equity—an alternative, continuous measure that preserves differences in ownership intensity between ESOP firms. Within our sample of publicly traded, ESOP firms, ESOPs comprise on average 1.43% of firm equity. For all conventional firms in our sample, the ratio of plan assets to firm equity is zero. Re-estimating Equation (1) with the ratio of plan assets to firm equity as our independent variable of interest are presented in Table 4. Consistent with Hypothesis 1a, we find employees experience greater job satisfaction when there is employee ownership (panel A) and that, among ESOP firms, there is a positive relation between the intensity of ownership and job satisfaction (panel B). Among publicly traded, ESOP firms, we estimate that a one standard deviation increase in the fraction of firm assets under management by the ESOP is associated with 0.09 standard deviation greater job satisfaction overall.

Glassdoor Ratings of Job Satisfaction by Ownership Intensity to Firm Equity

Notes: Table examines the difference in average rating between reviews from firms with ESOPs and those from conventional firms using the ratio of plan assets to firm equity as the measure of employee ownership. Additional controls include postings per establishment, establishments per firm, and indicators for the firm is publicly traded, the establishment is unionized, the worker’s tenure category, and the worker is a current employee. Standard errors are clustered by firm. ESOPs, Employee Stock Ownership Plans.

Significance levels: * 10%; ** 5%; *** 1%.

These results are consistent with findings that show employees in more intensive shared ownership programs are more cooperative than employees in firms with less intensive programs (Freeman, Blasi, and Kruse 2010). Workers who cooperate often rely on peer monitoring that is based on trust and a stronger organizational culture that complements formal control and supervision methods (Tsui and Vance 2023). If such cooperation and trust induce improved interpersonal relationships among co-workers and with management, we anticipate workers would feel more satisfied with their jobs (Sockin 2022).

Heterogeneity between Employees

While these results reveal that job satisfaction is greater on average in ESOP firms, they do not speak to whether that premium is enjoyed by all workers within the firm. To examine whether this satisfaction boon is enjoyed universally, we re-estimate Equation (1) but partition the sample into six observable categories according to whether the employee is a manager or not, a current or former employee at the time of the review, and employed with the firm for less than or at least five years. The estimates within each of these six subsamples are recorded in Appendix Table A9.

Considering first heterogeneity by occupation, both non-managers and managers experience greater job satisfaction in ESOP firms. Looking within the same establishment, the differences are not statistically significant (see Appendix Table A10). Next, we investigate employees still with the firm and employees who have since left. Both the former and the latter report significantly higher satisfaction in ESOP firms, though within the same establishment, the premium is significantly larger for former employees. This could reflect less frequent involuntary separations (e.g., Kruse et al. 2010; Whitfield et al. 2017), which would imply former employees at ESOP firms are more likely to have left on their own volition, or regret having left for a conventional firm. It could also simply reflect how employees receive ESOP benefits upon separating, which may produce a satisfaction boon from receiving a windfall in income that former employees of conventional firms, absent severance pay (which is not required under the Fair Labor Standards Act), would not receive. 34

Finally, we consider how long workers have been with the firm. If the satisfaction premium widens with firm tenure, then that would suggest there is a learning process by which workers become more satisfied as they adapt to a workplace with employee ownership. If it does not, that would indicate the boon to job satisfaction is present from the onset of employment—suggesting possible selection into employee ownership, either on the side of the worker or the firm, or the constant presence of favorable workplace characteristics. Separating workers into those with fewer than five years of firm tenure and those with more, we observe greater satisfaction in ESOP firms for both groups. Looking within the same establishment though, the premia are significantly smaller for workers with more than five years of firm tenure, suggesting perhaps workers sour somewhat about their jobs after they are fully vested in the ESOP. While we find positive effects uniformly by firm tenure (see Appendix Table A11), suggesting there could be selection into employee ownership, evidence presented in the Plausibly Causal Research Design section suggests our results are not the product of selection.

Sensitivity Analysis

We next test the robustness of our Glassdoor results to a number of modeling and sampling decisions. The results, unless otherwise stated, are presented in Appendix Table A12.

We also alter the baseline model to allow for the possibility that workers in ESOP firms have different tasks, requirements, or seniority than those in conventional firms. We do so in two ways. First, we consider a more granular characterization of each worker’s role in the firm, their job title. 36 The results are similar if were to include a fixed effect for each job title in lieu of a fixed effect for each occupation. Second, we recognize that ESOP firms might utilize differently shaped job ladders than conventional firms, such that job titles may not be comparable between them. To this end, we categorize the seniority of each worker by the mean years of experience among all workers with the same firm and job title. The idea is that as job titles become more senior, they require more years of experience to be accessed (Sockin and Sockin 2019), a minimum which may differ by firm. Again, we observe greater satisfaction in ESOP firms (see Appendix Table A14).

Next, we recognize that, even within the same industry, workers may differentially sort into employee ownership. In turn, the demographic composition of the workforce may differ between ESOP and conventional firms. When we account for differences by gender and human capital accumulation with the inclusion of gender cross years of experience fixed effects, the takeaways are similar. 37 The same is true, despite the even smaller sample, if we were to instead include gender cross age fixed effects (see Appendix Table A15). Thus, our results do not reflect differences in firm composition by age, experience, or gender.

The differences in job satisfaction we document could reflect differences in wages rather than non-wage aspects beyond pay as higher-paid workers do exhibit greater job satisfaction (Sockin 2022). To rule out this possibility, we consider workers who, for the same job, contribute both a Glassdoor review and Glassdoor pay report. We then re-estimate Equation (1), including as an additional observable the logarithm of hourly wage. Still, we observe a satisfaction premium within ESOP firms. This is perhaps not too surprising though given that wages exhibit little predictive power for overall satisfaction beyond the five subcategory ratings (see Appendix Table A16).

Although we include a comprehensive set of firm- and establishment-level controls, they are not exhaustive. For instance, not accounted for are firm size (not just new vacancies), age, and profitability. 38 Including these additional controls does not change the results. We also ensure that no single firm or establishment drives our results since under the baseline, the unit of analysis is each review, meaning one firm with many reviews may have outsize influence. If we were to apply sample weights such that each firm (see Appendix Table A17) or establishment (see Appendix Table A18) is given equal weight, the premium in job satisfaction among ESOP firms persists. Finally, we show our results do not reflect differential responses to the COVID-19 pandemic by considering only reviews from before March 2020.

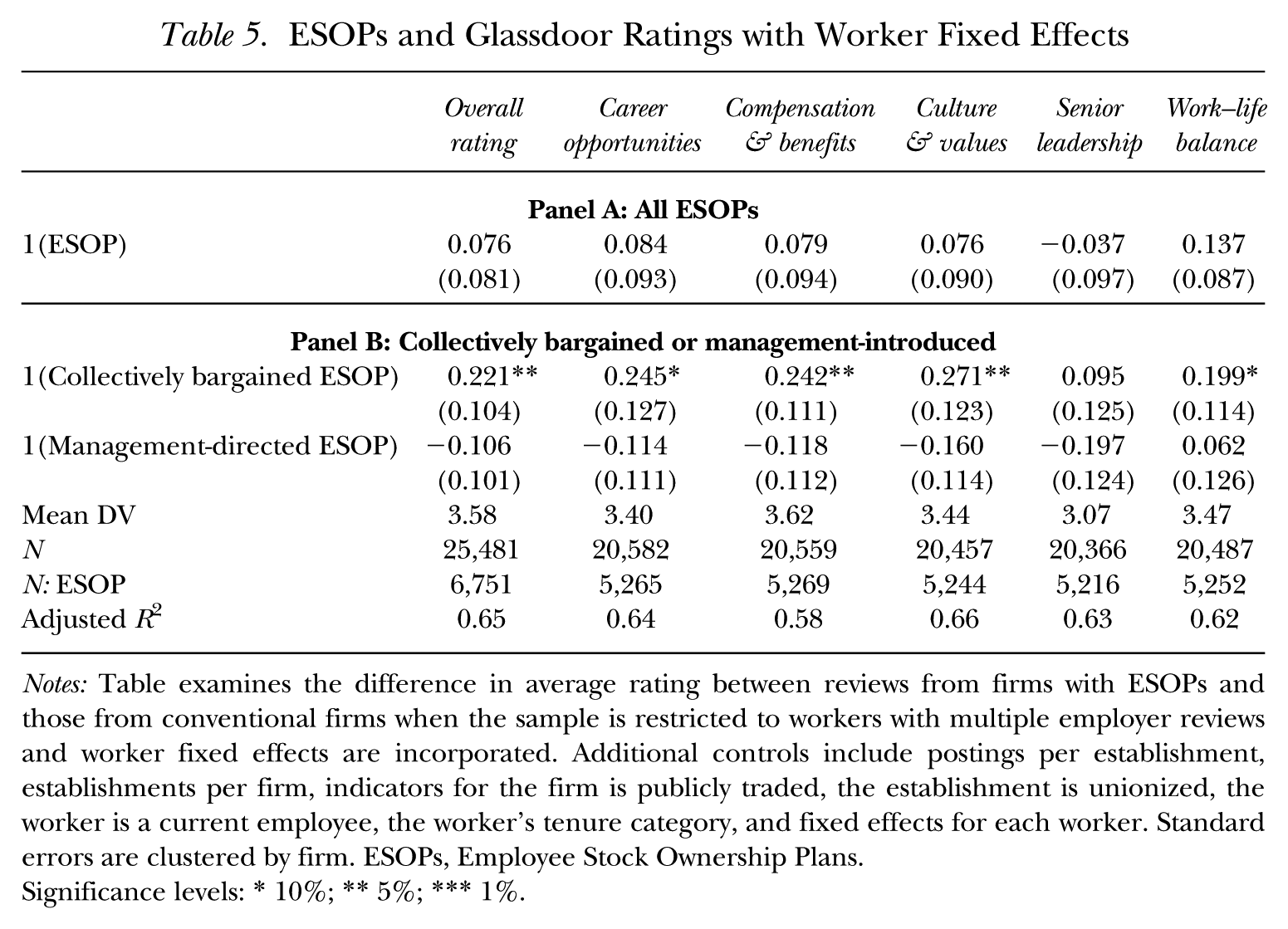

ESOPs and Glassdoor Ratings with Worker Fixed Effects

Notes: Table examines the difference in average rating between reviews from firms with ESOPs and those from conventional firms when the sample is restricted to workers with multiple employer reviews and worker fixed effects are incorporated. Additional controls include postings per establishment, establishments per firm, indicators for the firm is publicly traded, the establishment is unionized, the worker is a current employee, the worker’s tenure category, and fixed effects for each worker. Standard errors are clustered by firm. ESOPs, Employee Stock Ownership Plans.

Significance levels: * 10%; ** 5%; *** 1%.

Under this within-worker specification, we observe broadly positive coefficients, though we cannot reject that they are statistically different from zero at conventional levels. When we separate ESOP firms into those with and without a collectively bargained ESOP, we observe significantly higher satisfaction, even for the same worker, overall and for four of the five subcategories if the firm has a collectively bargained ESOP. That we observe such satisfaction premia even for the same worker suggests the robustly positive estimates we document for employee satisfaction within firms with collectively bargained ESOPs are not the product of workers differentially selecting into employee ownership.

Additional Mechanisms

Why might workers within an ESOP firm report greater job satisfaction, especially with regards to culture, career opportunities, leadership, and work–life balance? Below, we test four possible explanations beyond collective bargaining agreements and ownership stake.

One possibility is that employees in firms with ESOPs are more optimistic about the future prospects for their firms. In this case, satisfaction today may reflect perceived job stability or future earnings growth. Indeed, job seekers will actively avoid firms with worse financial prospects (e.g., Brown and Matsa 2016). In a Glassdoor review, workers can report whether they approve of the performance of the CEO and whether they have a positive business outlook for the firm over the next six months. Creating an indicator variable for each of these two outcomes and re-estimating Equation (1) reveals that workers in ESOP firms have similar rates of CEO approval and business outlooks (see Appendix Table A19). This suggests rosier outlooks do not drive our results.

Since these are manufacturing firms, where workplace accidents can be especially harmful or even fatal, a second explanation may relate to differences in safety on the job. Indeed, workers have been found to be more satisfied when they feel their work environment is safer (Gyekye 2005), and they are willing to forego higher wages to work in jobs not characterized by poor working conditions (Gronberg and Reed 1994) and that have lower fatality risks (Lavetti and Schmutte 2025). We investigate workplace hazards using data from the Occupational Safety and Health Administration (OSHA). Although ESOP firms experience fewer cumulative injuries, cases in which workers need to leave work due to an injury or illness, and deaths per 100,000 hours worked (see Appendix Table A20), the satisfaction premium we observe among ESOP firms does not appear to reflect ESOP firms’ improved safety outcomes (see Appendix Table A21). Greater safety may well affect employee satisfaction but not the individual components we study here.

A third possibility is that ESOP firms require different skills and workers than non-ESOP firms. While workers in firms with employee ownership report greater satisfaction even within the same job titles, the same position may require different tasks or responsibilities across employers. For instance, Deming and Kahn (2018) concluded that firms explain 30% of the total variation in (posted) skill requirements. To test whether differences exist in skill requirements between ESOP and conventional firms, we compare the content of their job postings. We consider not only the years of education and experience required, but the listing of engineering and operations skills, as these cover the spectrum of skills required in manufacturing (Ben-Ner et al. 2023), as well as people skills, which have grown in prevalence over time (Deming 2017). We also compare posted wages, as some firms may advertise higher pay to attract workers. Using our sample of job ads, we re-estimate Equation (1) and record the coefficients for each measure in Appendix Table A22.

For years of education and minimum years of experience, we observe no significant differences between ESOP and conventional firms. For the listing of engineering, operations, or people skills, despite these skills being common in job ads (see Appendix Table A3), we again observe no significant differences between ESOP and conventional firms. Last, we find little difference in the wages ESOP and conventional firms advertised. Together with the low incidence with which employee ownership is mentioned in job postings (see Appendix Table A5), we interpret these results as evidence against workers differentially sorting on observables into ESOP firms.

Last, we consider whether the satisfaction premium reflects differential personnel practices. Kruse et al. (2010) documented a complementarity between employee ownership and high-performance work systems (HPWS), such as job training and supervision. Similarly, Bloom and van Reenen (2011) argued there are complements among human resource management practices, such as individual bonuses, group bonuses, and team work. To the extent that an ESOP constitutes a group incentive for workers, greater satisfaction within ESOP firms may reflect other HPWS.

We take two complimentary approaches. One approach involves considering three HPWS, specifically autonomy, bonuses, and job training, and identifying differences in their quality between firms through Glassdoor reviews. We measure these HPWS by marking whether a worker discusses them positively (in the pros) or negatively (in the cons). For each HPWS, we assign a score of +1 to a review if the HPWS is discussed in the “pros,”−1 if in the “cons,” and 0 otherwise. We then take the firm-level average across reviews to proxy for differences in the quality of each HPWS across firms. Adding these firm-level measures of HPWS to Equation (1) does little to alter the satisfaction premium observed among ESOP firms (see Appendix Table A23).

The other approach involves investigating what aspects of a firm are associated with having an ESOP. In addition to the firm-level observables from Glassdoor reviews, we incorporate additional HPWS from other data sets. Using Glassdoor pay reports, we calculate, for each firm, average pay, the standard deviation of pay, and the fraction of workers that receive a cash bonus. From Refinitiv (see Appendix B), we obtain firms’ environmental, social, and governance (ESG) scores. We then estimate a logit model predicting whether a firm has an ESOP with these measures, the results for which are available in Appendix Table A24. While firms that are publicly traded, larger, older, and have more unionized establishments are more likely to have an ESOP, none of these additional HPWS predict employee ownership. Greater job satisfaction though is positively associated with having an ESOP, even conditional on these HPWS. Taken together, the evidence suggests additional HPWS cannot rationalize our results.

Plausibly Causal Research Design

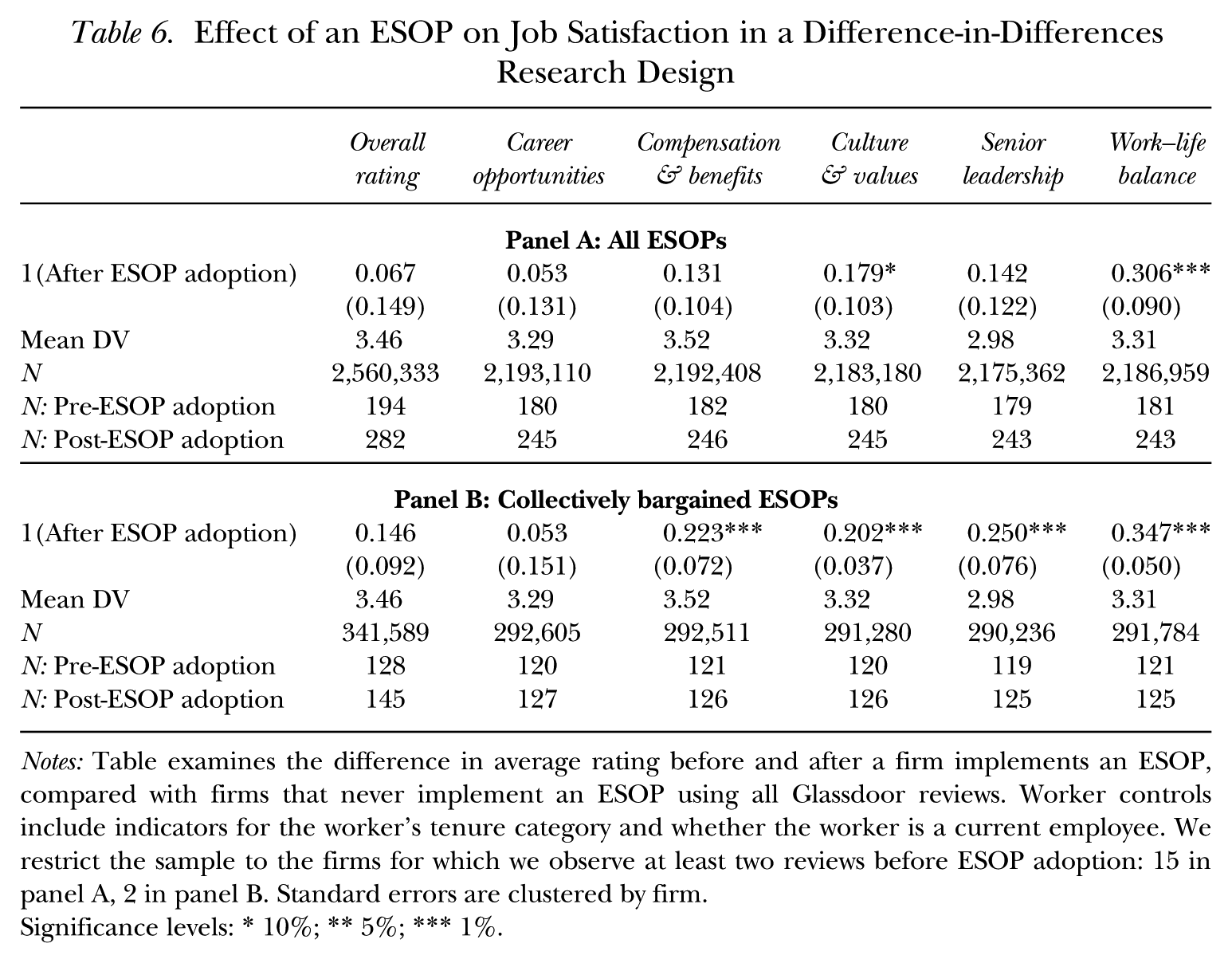

Since we observe Glassdoor reviews for some firms before and after they adopt an ESOP, in the spirit of Kim and Ouimet (2014), we can estimate a difference-in-differences research design in which we compare the change in job satisfaction after a firm adopts an ESOP with the differences in job satisfaction over time for firms that never adopt an ESOP. This exercise is plausibly causal, however given the sparseness of the sample for firms that adopt an ESOP during our time period, we are unable to test for parallel trends in our outcomes of interest before ESOP adoption. 39 Moreover, given that we observe reviews before and after ESOP adoption for only 15 firms, our estimates may well lack external validity. As such, we interpret these results as further suggestive evidence. To address the staggered timing of ESOP adoption over the sample period, we follow Cengiz, Dube, Linder, and Zipperer (2019) and create a stacked data set. More specifically, for each ESOP adopter r, we replicate the reviews for conventional firms and create a stacked data set of r-many subsamples. The difference-in-differences specification then follows:

It includes the same fixed effects and covariates as the benchmark specification of Equation (1), with the addition of firm fixed effects λk, as well as the interaction with a subsample fixed effect λr. Under Equation (2), the coefficient of interest β captures the average change in Glassdoor ratings within a firm after the firm adopts an ESOP, compared with the average change in Glassdoor ratings among firms that do not. The variable 1{After ESOP adoption}k,t is an indicator equal to 1 if firm k has adopted an ESOP as of period t, and 0 otherwise. The results are presented in Table 6.

Effect of an ESOP on Job Satisfaction in a Difference-in-Differences Research Design

Notes: Table examines the difference in average rating before and after a firm implements an ESOP, compared with firms that never implement an ESOP using all Glassdoor reviews. Worker controls include indicators for the worker’s tenure category and whether the worker is a current employee. We restrict the sample to the firms for which we observe at least two reviews before ESOP adoption: 15 in panel A, 2 in panel B. Standard errors are clustered by firm.

Significance levels: * 10%; ** 5%; *** 1%.

When we look at all 15 ESOP adopters in panel A, we observe positive coefficients for culture and values and work–life balance that are statistically distinguishable from zero at conventional levels. While the estimates for other categories are also positive, they are not statistically distinguishable from zero. When we consider in panel B only the firms that adopted collectively bargained ESOPs, of which there are two, we observe broadly positive effects on employee satisfaction that are statistically significant and of a similar magnitude to the estimates observed in Tables 3 and 5. After the collectively bargained ESOP is introduced, satisfaction with four of the five subcategories for these two firms jump an additional 0.20–0.35 stars compared with ratings for firms that never adopt an ESOP. This evidence suggests that our results at least in part reflect changes that materialize once an ESOP is introduced. It is worth noting that changes in ownership do not guarantee improved employee satisfaction, as Gornall et al. (2025) showed job satisfaction declines following a private equity leveraged buyout.

Discussion and Concluding Remarks

This study advances our understanding of firm ownership structure and employee satisfaction. We first introduce a framework that links employee ownership to employee satisfaction through the mechanisms of enhanced productivity, resource distribution, and alignment with employee preferences. We then empirically show that workers in firms with ESOPs report greater satisfaction with their jobs overall and with workplace attributes, such as firm culture and work–life balance, compared with their counterparts in firms without ESOPs.

Our theory underscores the importance of psychological ownership and reduced agency costs in driving these mechanisms. Regardless of an employee’s role or rank, an ESOP, as a broad-based employee stock ownership plan, provides a mechanism for employee voice and shared ownership. Although ownership stakes are not equal, shared ownership marries the long-term financial interests of all employee-owners, for example, production workers, engineers, and managers, as well as non-employee-owners. Through voice and shared ownership, employees can mold the nature of work toward their preferences more than they could in conventional firms. If a union agrees to the ownership sharing, it can act as a complementary voice and guarantor of the interests of its members who participate in ownership, enhancing the effects of an ESOP.

Although our empirical analysis is largely cross-sectional and neither people nor establishments are assigned randomly to ownership type, our estimates and accompanying heterogeneity and sensitivity tests, as well as our difference-in-differences analysis among a small set of firms that introduced an ESOP after 2012, strongly suggest employees experience improved satisfaction in the presence of an ESOP. This premium in job satisfaction, while statistically significant, is modest though at no more than one-tenth of a standard deviation. Employee ownership through an ESOP is thus not necessarily transformative for employee satisfaction but incremental. The premium in satisfaction is larger when the ESOP is established through collective bargaining between management and unions and when employees hold a greater stake of firm equity—suggesting a complementarity between unions and employee ownership as well as a role for ownership intensity.

Our study does have limitations. First, we lack data to directly test the mechanisms we hypothesize as linking ownership and satisfaction, as such data are not available in establishment, firm, or private and government databases. Future research may shed light on these mechanisms through case studies of firms with employee ownership and conventional firms that operate in similar environments. Second, our analysis focuses on a single economic sector in a single country. While we believe these findings have broader applicability, future research may investigate the relationship between employee ownership and job satisfaction in various cultural settings and markets. And third, our findings are based on a particular form of employee ownership. It would be interesting to investigate the effects of employee ownership on job satisfaction in cooperatives and partnerships where the exercise of employee rights affects the mechanisms that lead to job satisfaction in different ways than in ESOPs.