Abstract

Why do countries diverge significantly in the levels of income inequality across the Global North? Most scholars believe that the answer lies in the ways that economic resources are organized through institutions. Drawing on a country-level, longitudinal dataset from 1985 to 2016 matched with three other data sources, the author explains how and to what extent institutions matter for income inequality across the “varieties of capitalism.” To sort countries based on their institutional similarities, the author conducts cluster analysis and examines the extent to which institutions predict variation in the levels of income inequality, both cross-nationally and within each cluster of countries. In cross-national, panel data regressions, strong evidence is presented that labor market interventions such as vocational rehabilitation programs as well as characteristics of corporate governance are important determinants of income inequality.

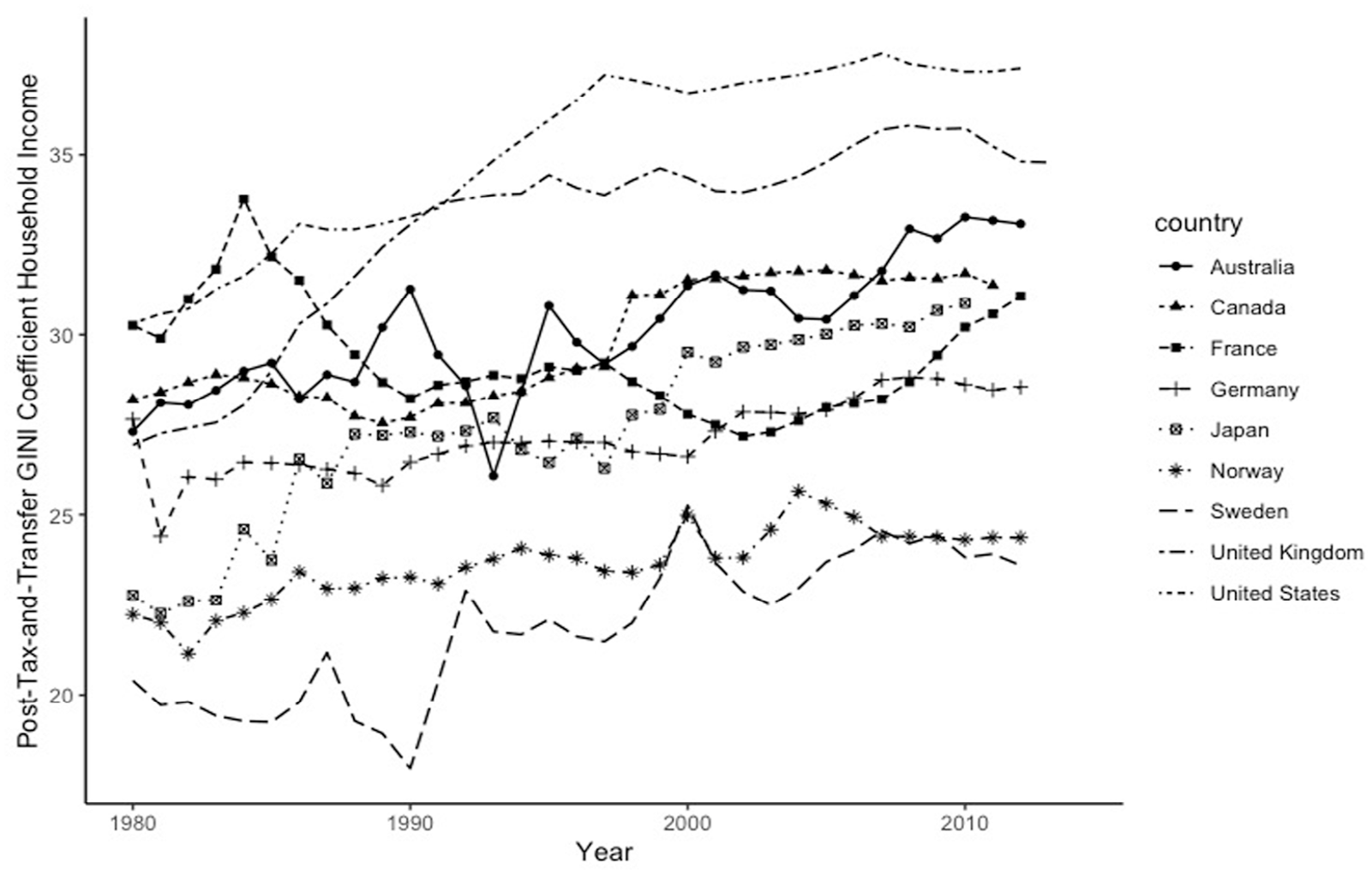

Since the 1980s, most countries in the Global North have experienced a significant rise in the levels of income inequality. Numerous comparative studies on income inequality have consistently shown that within-country inequality often measured by the Gini index has risen (Brandolini and Smeeding, 2011; Clark, 2020; Nolan et al., 2014; Salverda et al., 2014). As plotted in Figure 1, income inequality—the gap between the rich and the poor—has widened in most countries in the Global North over the past four decades. While the magnitude of change varies substantially across countries, the broad trend is unmistakable: rising income inequality has been the defining challenge of societies in late capitalism. 1 Research on income inequality from across three disciplines, namely, economics, political science, and sociology has put forward four main explanations: (1) skill-biased technical change: a shift in the production of technology that favors skilled over unskilled labor by increasing its relative productivity and, therefore, its relative demand (Acemoglu, 1998, 2002; Autor et al., 1998, 2003; Bluestone and Harrison, 1988; Katz and Murphy, 1992); (2) decline of organized labor, stagnation of welfare state generosity, and the ever-weakening standards of employment protection as a result of the new dominant neoliberal regime (Brandolini and Smeeding, 2011; Kenworthy and Pontusson, 2005; Lemieux, 2008; Pontusson et al., 2002; Rueda and Pontusson, 2000; Western and Rosenfeld, 2011); (3) tax policies, changes in compensation practices, and the rise of the “top-earners” epitomized by the premiums associated with high salaries of top management, particularly in the United States (Beckfield, 2006; Cernat, 2004; Leigh and Posso, 2009; Piketty, 2014; Piketty and Saez, 2006); and (4) changes in family formation and practices such as assortative mating and a significant increase in the number of single-mother families (Goldstein and Kenney, 2001; Schwartz, 2010).

Net (post-tax-and-transfer) Gini coefficient household income.

In the sociological tradition, social stratification research often relies on human capital dimensions (i.e. educational attainment, parental resources, network of social capital) in order to predict social and economic inequalities among individuals (McCall and Percheski, 2010; Western et al., 2008). While the human capital approach in the social stratification research is informative, there is a wide consensus among scholars from across social science disciplines that much of social and economic inequalities observed both within and between countries are directly resulted from the ways in which economic resources are organized through institutions (Kenworthy and Pontusson, 2005; Lemieux, 2008; Pontusson et al., 2002; Rueda and Pontusson, 2000). This behooves us to pay close attention to the role that institutions—and not just individual attributes—play in generating distributive outcomes (Beramendi and Rueda, 2014). Hence, an important body of scholarship has developed in political science and economic sociology known as the “varieties of capitalism” (henceforth, VoC) that underscores the important role of institutional configurations across different countries in producing socioeconomic outcomes (Hall and Soskice, 2001; Witt and Jackson, 2016).

The VoC approach was first articulated by Peter Hall and David Soskice (2001) in their seminal introductory book Varieties of Capitalism where they set out, in the Weberian sense, two ideal-types of capitalist economies, namely, liberal market economies (i.e. the United States, United Kingdom, Canada, Australia, New Zealand, Ireland) and coordinated market economies (i.e. Germany, Austria, Switzerland, Belgium, Sweden, Japan). Institutions lie at the heart of the VoC approach to the study of economy and society, and the differences in their designs implicate economic and social outcomes including macroeconomic growth, living standards, employment relations, patterns of technical change, as well as social and economic inequalities, among others (Amable, 2003; Baccaro and Pontusson, 2016; Hall and Soskice, 2001; Hope and Soskice, 2016; Schmidt, 2002; Streeck and Yamamura, 2001; Witt and Jackson, 2016). The VoC approach understands capitalism not as a unified or static economic system, but one that varies significantly across time and space, and that the sources of these variations are identifiable: they lie in “system coordination” and “institutional complementarities” (Amable, 2016; Deeg, 2005; Hall and Soskice, 2001: 17). Here, institutional complementarities refer to a set of subsystems that not only yield better—or worse—macroeconomic outcomes (Amable, 2016), but also govern the capital and labor relations. When such institutional complementarities are presented in the “right” form, they increase aggregate welfare and reduce income and social inequalities. Institutional complementarities thus create a significant degree of coordination capacity, one that is independent of the market’s coordination capacity. In this sense, the famous German vocational training system and the extensive Norwegian social security network are conspicuous examples of such institutional complementarities. Essentially, the VoC literature seeks to underscore the importance of non-market coordinating forces, emphasizing both the interventions of the state to “de-commodify” social services (Esping-Andersen, 1990) and to coordinate economic actions such that standards of living are raised and social disparities are reduced. Using this framework, variation in the levels of income inequality observed within different countries can be re-examined in a way that complements and extends the existing literature on institutions and income inequality.

How do institutional complementarities—differences in institutional designs and blueprints of national economies across the Global North—explain the divergent levels of income inequality that we observe? The institutional approach to the study of income inequality posits that much of economic and social inequalities are directly resulted from the ways in which economic resources are organized through institutions (Acemoglu and Robinson, 2015; Krueger, 2012; Piketty, 2014; Piketty and Saez, 2003; Piketty et al., 2018). In this context, institutions signify both codified rules or formal arrangements as well as various domains of policymaking (Hall and Soskice, 2001). Given that the levels of income inequality have risen dramatically in the Global North over the past four decades (see Figure 1), it would be instructive to further investigate the extent to which differences in the institutional designs of national economies explain variation in the levels of income inequality cross-nationally. Drawing on the VoC perspective, I examine how and to what extent institutional complementarities—differences in the institutional designs of national economies—within different regimes 2 of market economies produce such divergent levels of income inequality. It is crucial to note that what predicts variation in the levels of income inequality in liberal market economies may be different than that of social democratic market economies. Hence, the analysis of within-regime determinants of income inequality is particularly significant.

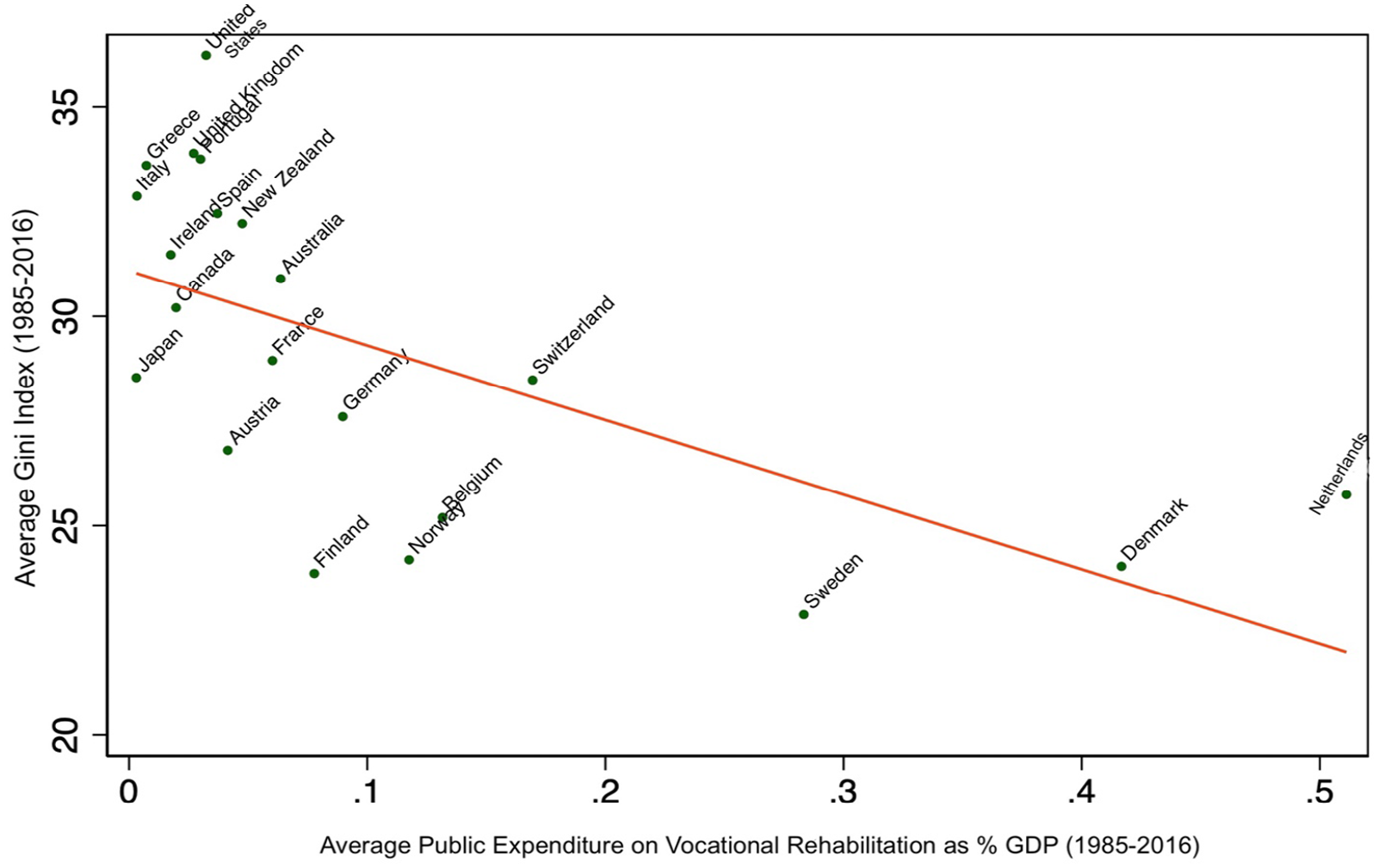

This article makes three contributions to the comparative institutions research more broadly (Brady et al., 2009; Korpi, 1983) and the VoC literature more specifically (Pontusson et al., 2002; Roberts and Kwon, 2017; Rueda and Pontusson, 2000). First, this study demonstrates that public expenditure on vocational rehabilitation programs, an important form of labor market intervention, inhibits income inequality cross-nationally. In a recent and important report by the UK Parliament, 8.4 million working-age (16–64) individuals reported disability in 2020 (Powell, 2021). This constitutes 20 percent of the entire workforce in the United Kingdom (Powell, 2021). In addition, in 2020, the Labor Force Survey in Norway reported that 17 percent of the entire working-age population reported disability (Statistics Norway, 2020). Similar percentages of the workforce with disability can be found elsewhere. Hence, the percentage of the workforce with disability across the Global North is not negligible. Vocational rehabilitation programs provide stable employment opportunities with benefits to individuals with disabilities, facilitating their labor market participation despite physical limitations (OECD, 2019). Therefore, this is an important mechanism by which income inequality is inhibited. To the best of my knowledge, this study is the first that examines the effect of vocational rehabilitation programs as an important dimension of institutional complementarities on the levels of income inequality cross-nationally. The strong, negative association between average levels of public expenditure on vocational rehabilitation programs and income inequality can be clearly seen in the bivariate scatterplot in Figure 2 (r = −0.62).

Bivariate scatterplot of Gini index and vocational rehabilitation programs.

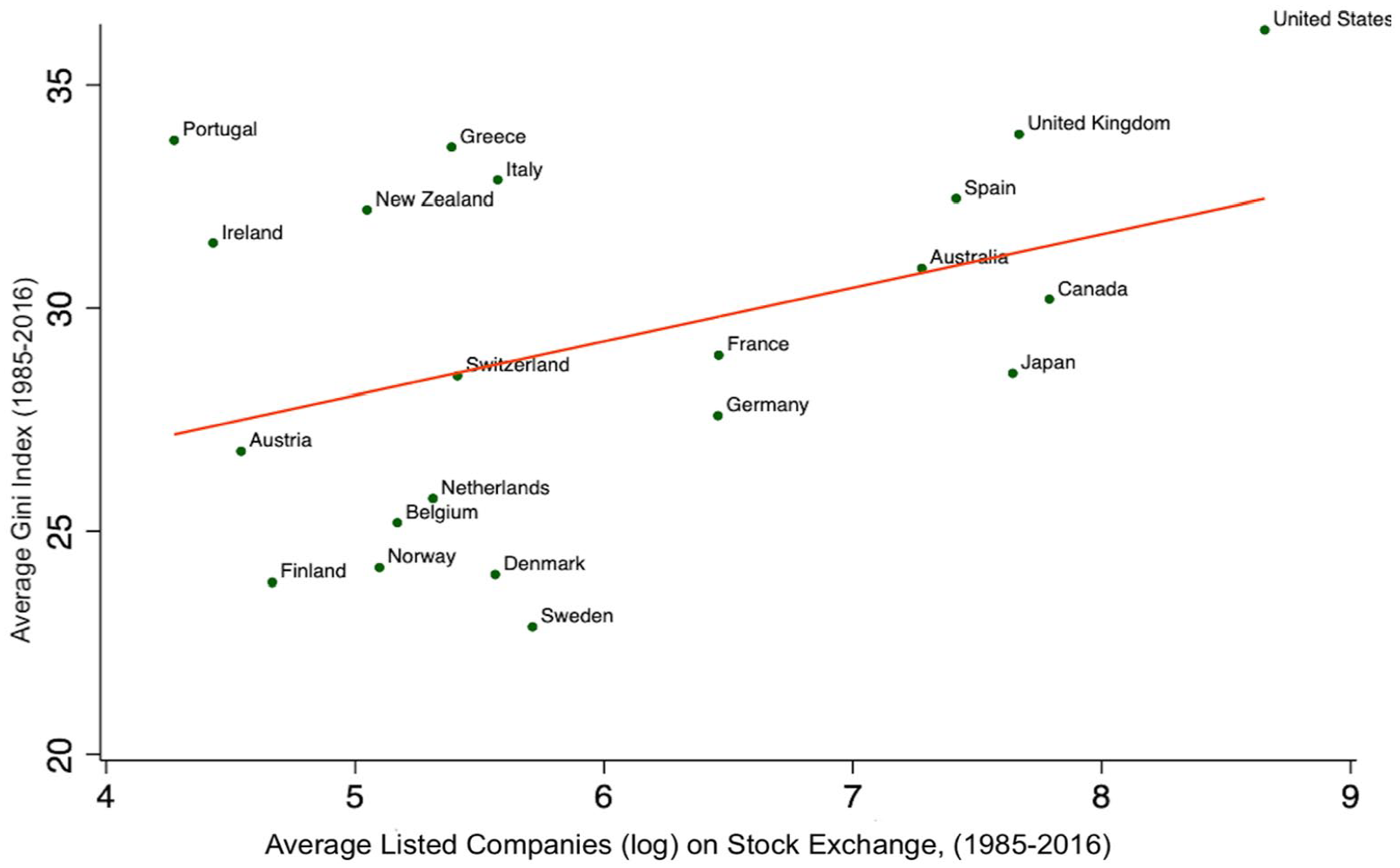

Second, I test the relationship between the volume of companies listed on stock exchange on the levels of income inequality, highlighting an important institutional dimension of corporate governance. Previous research has demonstrated that financialized, 3 corporate governance is associated with higher levels of income inequality cross-nationally (Flaherty, 2015; Godechot, 2016; Huber et al., 2022). These studies have predominately relied on stock market capitalization or the volume of stocks traded as a percentage of gross domestic product (GDP), which are measures of the degree of financialization of the corporate governance. However, the relationship between the mode of capital allocation to firms and the levels of income inequality within countries has not been explored. This is another critical void that this research fills. Capital is allocated to firms predominantly through two major channels under different regimes of capitalism: stock exchange in a liberal market economy such as the United States versus relational banking (i.e. long-term lending) in a coordinated market economy such as Germany (Aoki, 1994; Hall and Soskice, 2001; Witt and Jackson, 2016). While previous research has demonstrated that financialized corporate governance is associated with higher levels of income inequality cross-nationally (Flaherty, 2015; Godechot, 2016; Huber et al., 2022), the relationship between the mode of capital allocation to firms and the levels of income inequality within countries has not yet been explored. I find that capital allocation through stock exchange leads to higher levels of income inequality within countries, and that the mode of capital allocation to firms bears on distributive outcomes. Indeed, as shown in the scatterplot in Figure 3, there is a clear, positive correlation between the number (log) of firms and income inequality (r = 0.4).

Bivariate scatterplot of Gini index and listed companies on stock exchange.

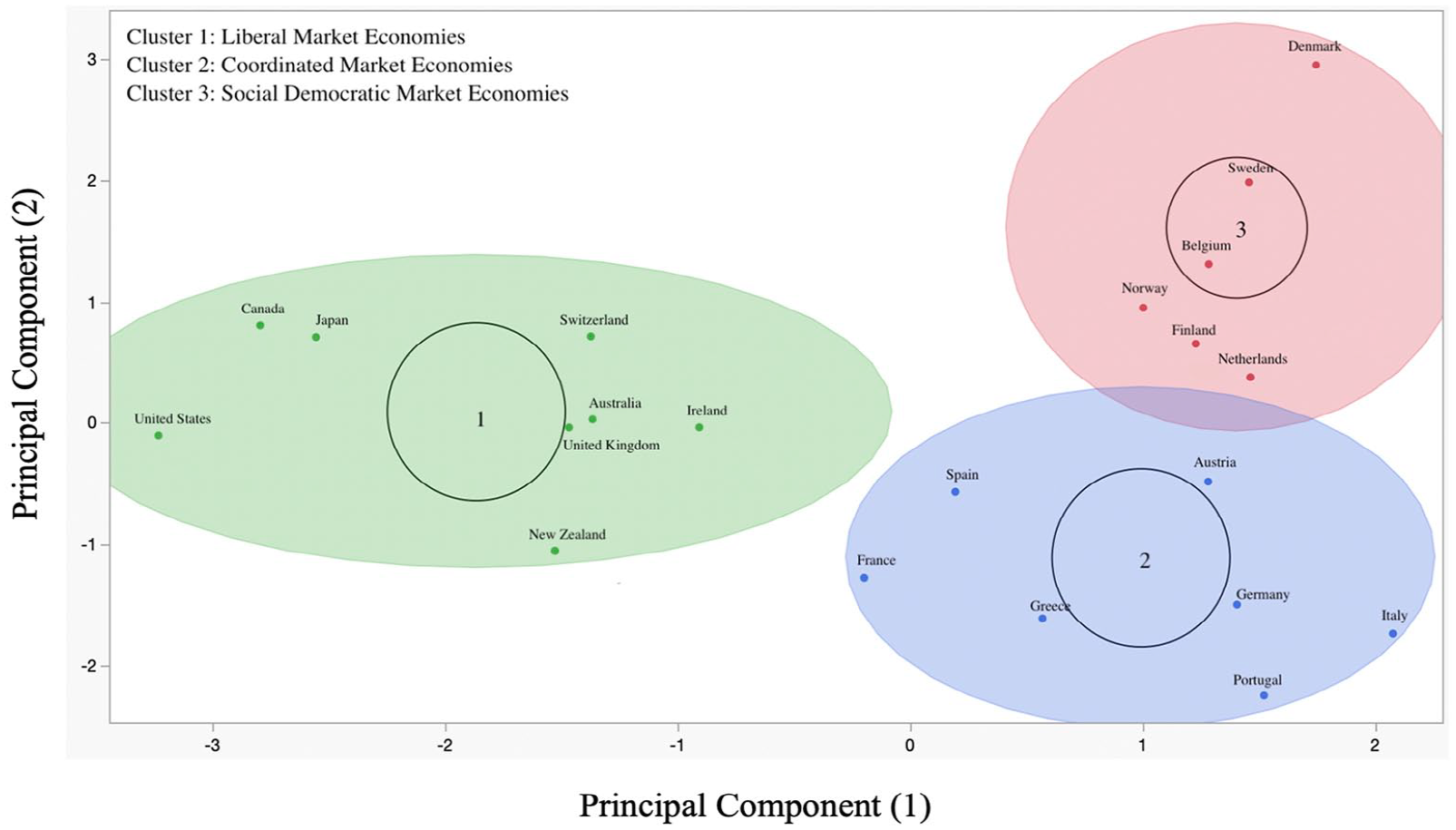

Third, I draw on a popular unsupervised machine learning algorithm known as k-means cluster analysis to explore how countries can be sorted and grouped based on their institutional similarities. Cluster analysis is construed as an inductive and morphological approach (Hastie et al., 2009), because it allows the data to “speak for themselves” (Ermakoff, 2019). While this study is not the first attempt at conducting cluster analysis of national economies (Schneider and Paunescu, 2012), it certainly presents a more up-to-date taxonomy of the VoC. Institutions are dynamic in spite of their resilience (Streeck, 2011; Thelen, 2014). The dynamic character of institutions thus behooves us to take the crucial effect of time into account. In order to present a more up-to-date typology of the VoC, I take the average values of the institutional variables for each country over the past 5 years (2011–2016) of the panel data. The cluster analysis presented here also incorporates an understudied dimension of institutional complementarities namely, vocational rehabilitation programs.

In what follows, I will first identify the institutional spheres by which we can distinguish VoC. Second, I will conduct cluster analysis in order to sort and group countries based on their institutional similarities. The VoC scholars have put forward numerous typologies in order to categorize national economies (Amable, 2003; Hall and Soskice, 2001; Whitley, 1999). By conducting cluster analysis, I avoid taking for granted the existing typologies that we have been bequeathed from previous research, but present a more up-to-date version. Third, I will use the clusters generated to examine the determinants of income inequality within each regime of capitalism. Drawing on a uniquely constructed cross-national, panel data entitled “Comparative Welfare States in the 21st Century” (Brady et al., 2020) matched with two other data sources, namely, the Global Economy Dataset (2018) and World Intellectual Property Organization (WIPO, 2020) Statistics Data, I explore the determinants of income inequality across various regimes of advanced capitalist economies. In so doing, I explore the extent to which institutional complementarities within VoC matter for explaining divergent distributive outcomes such as income inequality.

Varieties of Capitalism

The VoC literature identifies five spheres within which firms coordinate their activities with other actors (Amable, 2003; Hall and Gingerich, 2009; Hall and Soskice, 2001; Deeg, 2005; Schmidt, 2002; Streeck and Yamamura, 2001). The first sphere is industrial relations. Coordination of collective action, strikes, bargaining over wages, and working conditions are usually undertaken through workers’ associations and labor unions, which fall in the sphere of industrial relations. The labor force in liberal market economies (LMEs) is often less organized and unions tend to be both weaker and fewer in number than that of coordinated market economies (CMEs) (Hall and Soskice, 2001; Kenworthy, 2005). CMEs set wages through industry-level bargaining between trade unions and employer associations, and by equalizing wages at equivalent skill levels across an industry, this version of capitalism makes it difficult for firms to poach workers. The upshot is that workers tend to be more loyal to their employers in CMEs than LMEs (Hall and Soskice, 2001; Thelen, 2007).

The second sphere is a set of labor market interventions through educational systems, vocational training, and rehabilitation programs. While LMEs tend to invest in general—“portable”—skills transferrable across firms rather than company and asset-specific skills, the CMEs have a labor force with a high degree of industry and asset-specific skills, usually trained through various apprenticeship programs. In this vein, Germany is a canonical example of such labor market interventions in the form of vocational training and rehabilitation programs (Amable, 2003; Thelen, 2007). Career trajectories in CMEs therefore tend to be stable while fluid labor markets in LMEs incentivize poaching and employees’ movement between firms (Hall and Soskice, 2001). In addition, the CMEs exhibit significantly larger expenditure on vocational rehabilitation programs compared with LMEs (see Figure 5 in Appendix 1).

The third sphere is corporate governance, which concerns the question of how capital is allocated to firms in either of the two VoC. While LMEs encourage firms to be attentive to the prices of shares in the equity market and secure funds through the stock market, firms in CMEs usually secure funds through “patient capital” and relational banking (Vitols et al., 1997; Vitols, 2005). Capital is allocated to firms (large and small) through stock and equity markets in LMEs, whereas firms in CMEs depend on bank-coordinated capital allocation (Witt and Jackson, 2016). It is important to note that the difference in access to the sources of finance between LMEs and CMEs is not arbitrary nor contingent. If the financial markets in CMEs are deregulated in the way they are in LMEs, facilitating long-term employment will face serious challenges. As a result, it becomes harder for firms to recruit skilled labor or sustain worker loyalty (Aoki, 1994; Jackson and Miyajima, 2007). It is thus with reason that countries across the VoC exhibit different degrees of “financialization” of national economies which then implicates both capital allocation to firms and the levels of income inequality.

The fourth sphere is the internal management of the firms and the degree of employment protection across various sectors of the economy. It is often the case that in CMEs, company-level workers councils—composed of elected employee representatives—are usually endowed with considerable authority over layoffs, which stands in glaring contrast with LMEs “employment at will” tradition. In LMEs, the upper echelon of the firms has almost unilateral control over the decision-making processes, including substantial autonomy to hire or fire for a good reason, bad reason, and no reason at all without incurring legal liability. In CMEs, however, top managers of the firm must secure agreement for major decisions from supervisory boards, which include employee representatives as well as major shareholders (Aoki, 1994; Jackson and Miyajima, 2007). The German “co-determination” councils in firms involve workers to participate in the internal management of the firms, which increases the participatory dimension of workers in the managerial domain (Turner et al., 2001). Hence, the lack of employer coordination in LMEs is indicative of a less regulated and more flexible labor markets. The direct result of this is that LMEs feature considerably less employment protection compared with CMEs.

The fifth sphere is innovation and technological change. Hall and Soskice proposed that LMEs and CMEs show distinct patterns of institutional comparative advantage for radical or incremental innovations. Radical innovation “entails substantial shifts in product lines, the development of entirely new goods, or major changes to the production process,” whereas incremental innovation is “marked by continuous but small-scale improvements to existing product lines and production processes” (Hall and Soskice, 2001: 381). Hall and Soskice conclude that the combination of factors such as patient capital, long-term employment, and firm-specific skills in the CMEs enable more efficient production in industries with incremental patterns of innovation, because the relative immobility of labor and capital restrained firms to focus their efforts on improving existing lines of production. Conversely, fluid capital markets with short-term employment and general skills in LMEs facilitate efficient production in industries with radical patterns of innovation, as these conditions support firms using external markets to mobilize risky equity finance and workers with different skill sets, and thereby take advantage of new technological breakthroughs.

These are the five spheres by which the institutional diversity across national contexts presents itself in a more pronounced way. Indeed, there is a general consensus among scholars that significant variation exists across these core institutional domains, including industrial relations, employment relationship, financial systems, interfirm networks, corporate governance, and of course, the characteristics of the state itself (Hall and Gingerich, 2009; Hall and Soskice, 2001; Whitley, 1999; Witt and Redding, 2013). A number of studies have attempted to explore how such differences allow categorization of distinct types of institutional configurations that go beyond Hall and Soskice’s (2001) original binary categorization of LMEs and CMEs. For example, Amable (2003) identifies five versions of capitalism, namely, market-based, Asian, Continental European, social-democratic, and Mediterranean. Looking beyond the Global North and the “developed” countries, the typologies of the VoC have also been extended to the Global South (Witt and Jackson, 2016). In addition, Schneider and Paunescu (2012) use cluster analysis incorporating data in different points in time to investigate how countries can be grouped together based on their institutional configurations.

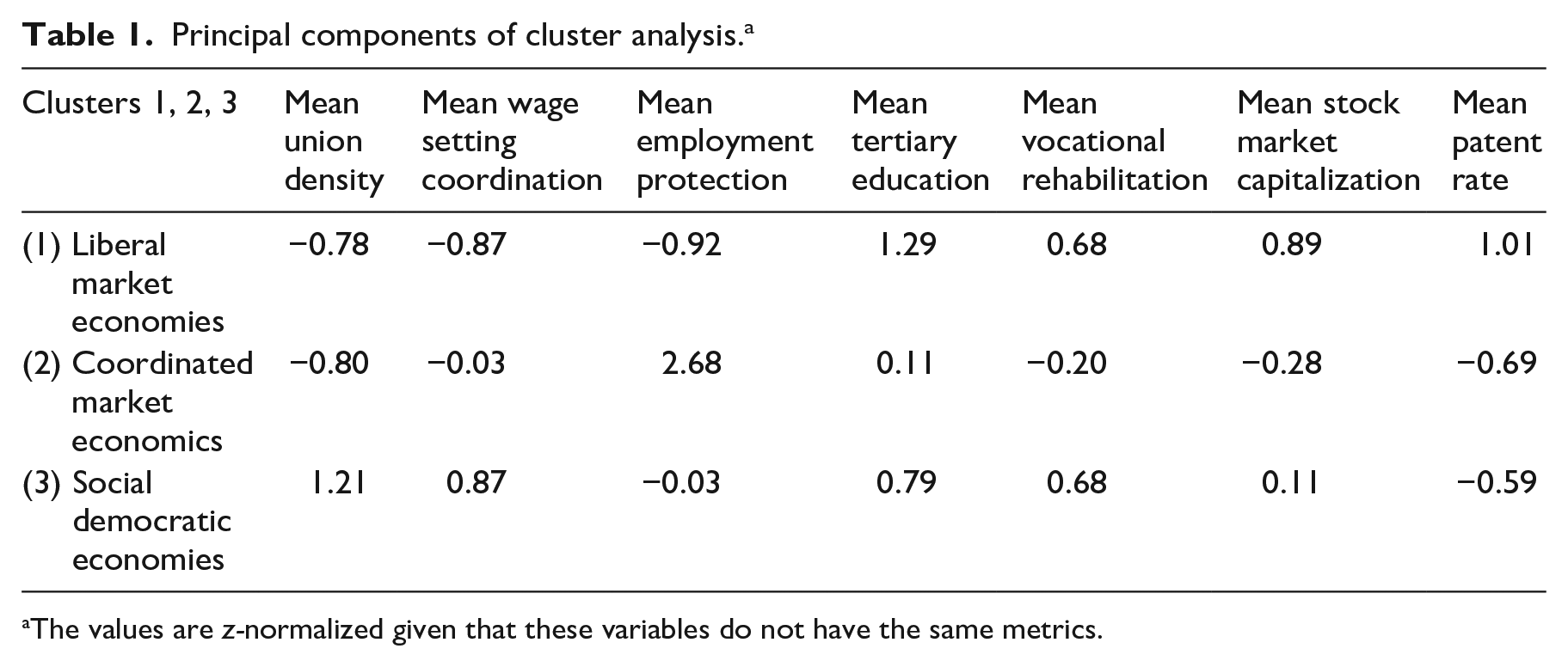

Drawing on the latest data available, I conduct cluster analysis to generate a more up-to-date typology of the VoC based on the institutional characteristics. 4 I incorporate a number of variables connected to the five spheres of institutional configurations across the VoC. The five spheres that I enumerated are universally accepted to be different from each variety of capitalism to another (Amable, 2003; Hall and Gingerich, 2009; Hall and Soskice, 2001; Schneider and Paunescu, 2012; Whitley, 1999; Witt and Redding, 2013). A cluster, in this sense, refers to a collection of data points aggregated together because of certain similarities (Everitt et al., 2011). The cluster analysis here is based on the following variables. Union density (i.e. defined as net union membership as a percentage of employed wage and salary earners), wage setting coordination (i.e. degree of coordination in setting wages by firms, industries, and the state) are both included in order to capture the two important dimensions of industrial relations, namely, collective bargaining and wage setting coordination. An index of employment protection is included to capture the degree of employment security. Public expenditure in vocational rehabilitation programs is incorporated in order to capture the volume of expenditure in workers’ training and rehabilitation. In addition, the percentage of the 25 to 64-year-old adult population with tertiary degrees is included because in the VoC literature, a high share of university graduates is a characteristic of LMEs, whereas a high share of graduates from occupational training and apprenticeship programs is a characteristic of CMEs (Schneider and Paunescu, 2012). Stock market capitalization as a percentage of GDP measures the degree and intensity of financialization of the corporate governance, and patent rate captures the effect of technical change. Hence, the variables incorporated in this cluster analysis capture various dimensions of the five spheres by which VoC can be distinguished. It is worth emphasizing that the selection of these variables is not arbitrary, they are based on the differences in the institutional spheres of national economies that I delineated above. Indeed, in all attempts at generating taxonomies of the VoC, a combination of the variables that I underscored above have been considered (Amable, 2003; Hall and Gingerich, 2009; Hall and Soskice, 2001; Schneider and Paunescu, 2012; Whitley, 1999; Witt and Redding, 2013). 5

As noted, cluster analysis in this article is conducted using the k-means method, which is an unsupervised technique to group data objects given their similarities (Everitt et al., 2011). That is to say, a data point is considered to be in a particular cluster if it is closer to that cluster’s centroid than any other centroid. In effect, k-means clustering aims to partition n observations into k clusters in which each observation belongs to the cluster with the nearest mean, which serves as a prototype of the cluster. The clusters generated can also be statistically tested in order to obtain the optimal number of clusters. The cubic clustering criterion (CCC) test is conducted to investigate the optimal number of clusters using Ward’s minimum variance, and the performance of the CCC is evaluated by Monte Carlo methods. I explored a wide range of clusters (between 2 and 8) in order to discern which number of clusters is optimal. After conducting cluster analysis, the CCC score indicated that 3 is the optimal number of clusters. Hence, given the institutional variables I incorporated, 3 is the optimal number of clusters whereby within cluster/group differences are minimized and the between cluster/group differences are maximized. Indeed, this is the whole objective behind conducting the k-means algorithm. Appendix 1 at the end of this article includes a discussion of the k-means cluster analysis algorithm as well as its technical dimensions. As emphasized, cluster analysis using the k-means technique is inductive because it falls under the unsupervised learning algorithms (Everitt et al., 2011; Hastie et al., 2009).

As Table 1 demonstrates, countries are clustered around seven main “components” (i.e. institutional variables) that are universally taken to address institutional designs and complementarities in the VoC literature (Hall and Gingerich, 2009; Hall and Soskice, 2001; Iversen and Soskice, 2009; Schneider and Paunescu, 2012; Whitley, 1999). Given the varying scales of the variables incorporated in the cluster analysis, I z-normalized to avoid any “artificial effects of the different size” or metric of the variables (Schneider and Paunescu, 2012: 738). Countries that have lower levels of union density, wage setting coordination, and employment protection but the highest levels of stock market capitalization and patent rate are the liberal market economies (see Table 1). Conversely, countries that exhibit the highest levels of union density, wage setting coordination, employment protection, and expenditure on vocational rehabilitation are the social democratic market economies. Those countries that fall in between this continuum are the coordinated market economies. In Figure 4, liberal market economies are located around the centroid of the first cluster, while social democratic market economies are located around the centroid of the third cluster. One can easily note the enormous difference in the average of union density, wage bargaining coordination as well as stock market capitalization between clusters in Table 1.

Principal components of cluster analysis. a

The values are z-normalized given that these variables do not have the same metrics.

K-means cluster analysis.

As alluded earlier, cluster analysis in this research takes the temporal effect into account given that institutions are not static. Indeed, as the “liberalization thesis” suggests, some of the institutional characteristics of national economies (i.e. employment protection and union density) have considerably declined since the 1990s (Bacarro and Howell, 2017; Hall and Thelen, 2009; Schneider and Paunescu, 2012; Streeck, 2011; Thelen, 2011). By incorporating the average values of the time-varying institutional variables for the past 5 years (2011–2016) of the panel data, I have considered a sufficient “time-lapse” to capture the temporal effect on the changing characteristics of institutions with the most recent data available in the cluster analysis. The most conspicuous advantage of this approach as opposed to just using data from one point in time lies in some of the noticeable changes we observe in the typology presented here compared with others (Hall and Gingerich, 2009; Hall and Soskice, 2001; Hicks and Kenworthy, 2003; Iversen and Soskice, 2009; Schneider and Paunescu, 2012). For example, Japan had always been construed as a CME, but as exhibited in the cluster analysis in this article, it has now completely moved in the opposite direction: Japan is now in the proximity of Canada in the LMEs’ cluster (See Figure 4). 6 Moreover, the Netherlands has been consistently considered to be a coordinated market economy (Hall and Soskice, 2001) but is now part of the social democratic market economies variety.

While I rely on the most updated cluster analysis in this article by averaging the values of the variables I incorporate over the last 5 years of the panel data, I have also demonstrated how countries cluster together based on different time periods in Appendix 1. By taking the average values of the variables over 5-year time intervals (i.e. 1985–1990; 1991–1995; 1996–2000; 2001–2005; 2006–2010), I have also conducted cluster analysis temporally (see Tables 9 to 14 and Figures 6 to 11 in Appendix 1). 7 As shown in Figures 6 to 10, with the exception of a few cases such as Japan, Ireland, and Austria that have drifted toward different regimes of capitalism over time, most countries have remained in their respective regime over the past three decades. As a result, drawing on the averaged values of variables over the past 5 years of the panel data for the purpose of cluster analysis allows us to present the most up-to-date typology of the VoC.

Data and variables

I explicated the theoretical foundation on which the institutional differences within VoC rest. This section details the data, method, and variables that are used in the empirical analysis. To empirically test how those differences in the institutional designs of advanced capitalist economies affect the levels of income inequality, I use fixed-effect regression models. The time span of the panel data for this study is from 1985 to 2016. Drawing on multiple panel datasets, namely, Comparative Welfare Dataset (Brady et al., 2020), 8 the Global Economy (2019), and the World Intellectual Property Organization (WIPO, 2020), I examine the extent to which institutional complementarities matter for determining the levels of income inequality across various regimes of capitalism. Detailed statistical description of the variables for each country is presented in Table 4, Appendix 1 at the end of the article.

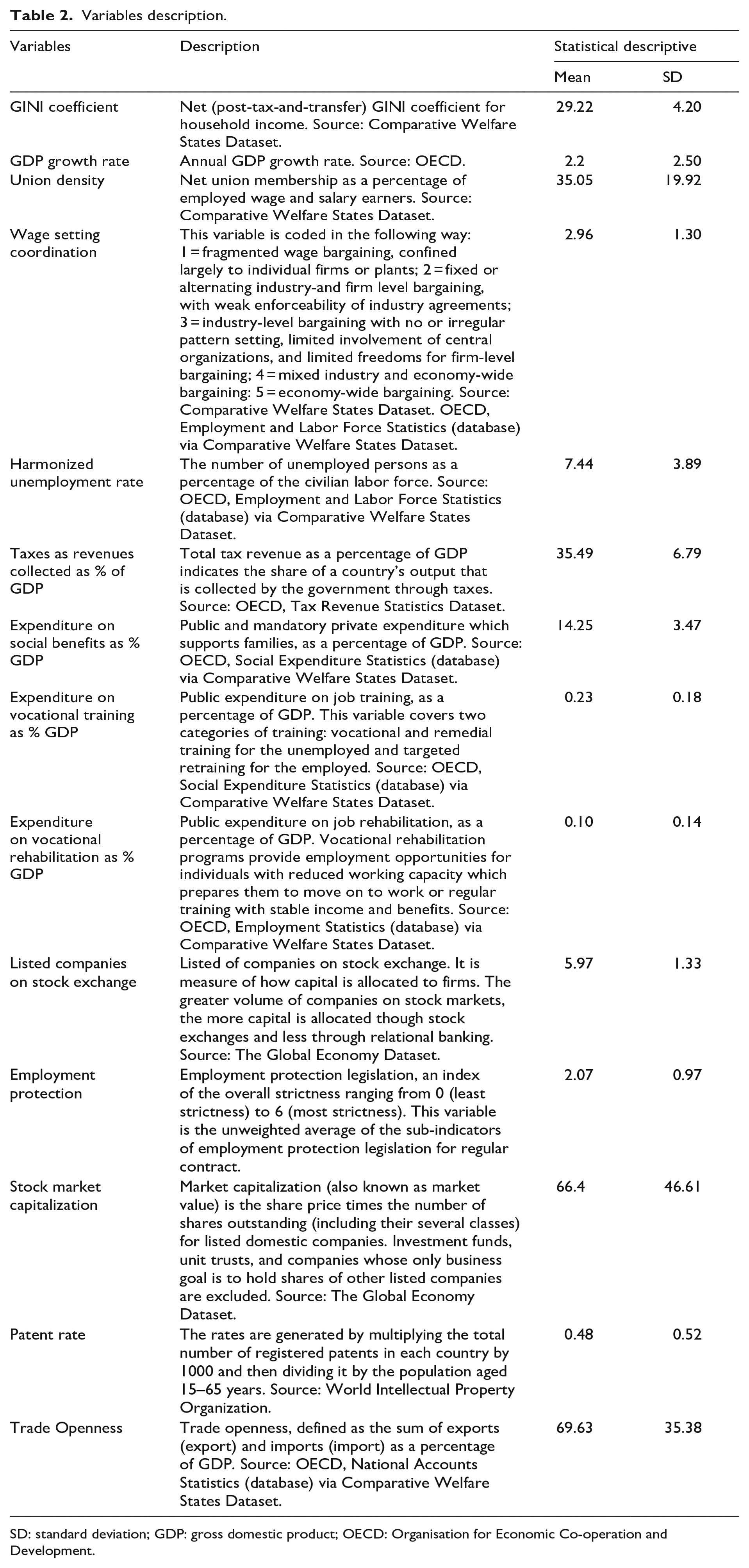

I incorporate a host of variables that directly pertain to the institutional complementarities across VoC. Table 2 presents the definition and sources of the variables included in this study. The variables that have already been examined in other cross-national studies on income inequality include (1) union density; (2) wage setting coordination; (3) unemployment rate; (4) employment protection in legislation; (5) stock market capitalization as a measure of financialization; (6) total public expenditure on social benefits and welfare as a percentage of GDP 9 (Alderson and Nielsen, 2002; Godechot, 2016; Huber et al., 2022; Mahutga et al., 2017; Roberts and Kwon, 2017; Rueda and Pontusson, 2000); (7) tax revenues as a percentage of GDP, which is a measure of the degree of the government’s extractive capacity and its fiscal resources since it includes all forms of taxes levied (i.e. income, profits, payroll, ownership and transfer of property, goods and services, etc.) (OECD, 2019). The variables that have not yet been examined in previous research on income inequality from the VoC perspective that I test in this study include: (8) public expenditure on vocational training programs as a percentage of GDP; (9) public expenditure on vocational rehabilitation programs as a percentage of GDP; (10) listed companies on stock exchange as a dimension of corporate governance as to how capital is allocated to firms; and (11) patent rate as a measure of technical change. I include two controls in the model specification: globalization and population. Given the salience of the globalization thesis in the study of income inequality (Alderson and Nielsen, 2002; Hager, 2018; Kollmeyer, 2015; Roberts and Kwon, 2017), I control for trade openness defined as the sum of exports and imports as a percentage of GDP at current prices, which is often used as a measure of globalization (Kollmeyer, 2015; Rueda and Pontusson, 2000). In auxiliary analysis, I also controlled for the volume of imports from the Global South as a measure of deindustrialization and the proportion of single mother families to account for demographically oriented explanation of income inequality. 10 Both of these measures, however, suffer from a significant number of missing data, which would severely reduce my sample size and the time span of the panel study. But even when I include these controls for a much smaller sample, the results are consistent.

Variables description.

SD: standard deviation; GDP: gross domestic product; OECD: Organisation for Economic Co-operation and Development.

The outcome variable incorporated in this study is Gini coefficient (post-tax-and-transfer) for household income. The choice to use this outcome variable was not arbitrary. First, there was no missing data for this variable and OECD’s series of Gini coefficients are of the highest quality data on income inequality that we have available cross-nationally. Second, income generated from employment accounts for the lion’s share of earnings in countries of the Global North and the distribution of income from employment by other measures (i.e. 90/10 ratio) correlate quite closely with cross-national measures of income distribution such as the Gini coefficient. Third, the post-tax-and-transfer Gini coefficient is a better measure of income inequality compared to pre- tax-and-transfer Gini coefficient because the former takes into account the households’ disposable rather than gross income (Mahutga et al., 2017; Piketty, 2014; Pontusson et al., 2002; Rueda and Pontusson, 2000). Fourth, and as a robustness check, I also test the analysis with Solt’s (2020) standardized inequality database, but the results are similar.

Method

Since the dataset analyzed here is structured as a multilevel panel dataset where repeated measures of income inequality and other variables are nested within time and countries, I use a fixed-effects model to account for the heterogeneity of unobserved variables. It should be noted that I initially modeled the data as a random-effects specification, but after running the Hausman test, the random-effects specification was resoundingly rejected at α < 0.001.

Fixed-effects regression models are widely used in longitudinal and panel data in the social sciences (Angrist and Pischke, 2008), and their virtue lies in their ability to adjust for unobserved, unit-specific and time-invariant confounders when estimating effects from observational data (Halaby, 2004; Imai and Kim, 2019). But while fixed-effects models adjust for unobserved and time-invariant confounders, time-varying omitted variables may still confound the estimates. Finding a way to adjust for time-varying confounders in a fixed-effect model has recently been an important area of discussion in the use of panel data in social science research (Halaby, 2004; Imai and Kim, 2019). Recent methodological literature on panel data analysis underscores the strategy to adjust for time-varying confounders by including lagged independent variables (Halaby, 2004; Imai and Kim, 2019). 11 Therefore, in order to account for the time-varying confounders (in addition to the time-invariant ones), I lag all of the time-varying covariates in the model demonstrated below

Equation (1) is a fixed-effects regression model with country-specific intercept

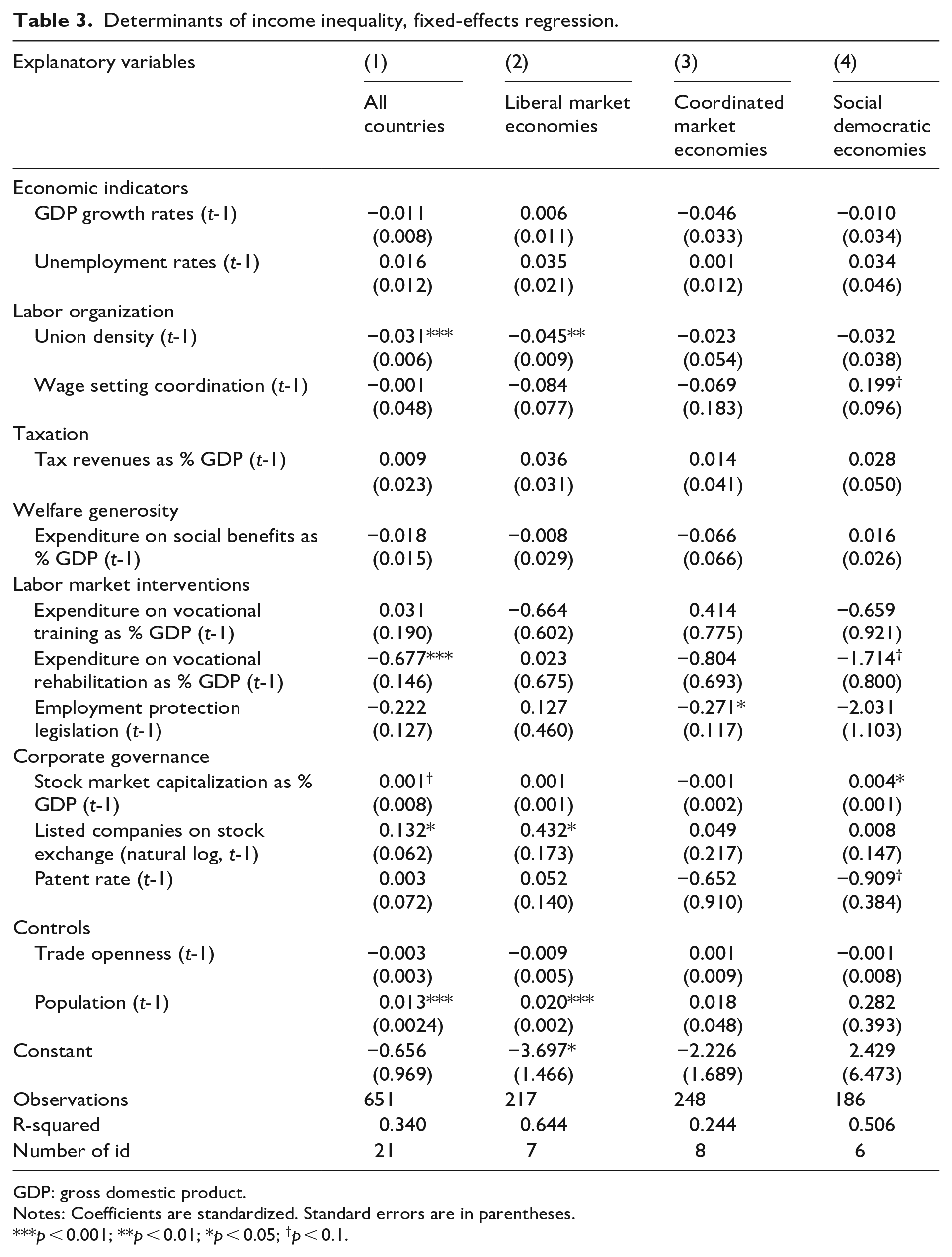

I examine multiple models of the determinants of income inequality across 21 countries in the Global North. Four models are presented in Table 3: Model (1) incorporates a whole array of variables that are directly connected to the institutional complementarities of national economies but does not restrict the sample to any variety of capitalism. It is crucial to note that what matters for the levels of income inequality in liberal market economies may well be different than that of social democratic market economies. In order to investigate how and to what extent the effects of institutions vary across VoC, I restrict the sample to those countries that fall under each regime of capitalism, namely, liberal market economies (LMEs), coordinated market economies (CMEs), and social democratic market economies (SDMEs). I then run the fixed-effects model with lagged independent variables separately for each variety of capitalism in order to demonstrate the within-regime determinants of the levels of income inequality. The models (2, 3, and 4) in Table 3 demonstrate the determinants of the levels of income inequality within each regime of capitalism. 12

Determinants of income inequality, fixed-effects regression.

GDP: gross domestic product.

Notes: Coefficients are standardized. Standard errors are in parentheses.

p < 0.001; **p < 0.01; *p < 0.05; †p < 0.1.

Results

The results of fixed-effects models with lagged independent variables are demonstrated in Table 3. The coefficients signify the effect of temporal change in independent variables on change in the dependent variable (Halaby, 2004; Imai and Kim, 2019). To ease interpretation, I standardize the coefficients, so that the effect size of each independent variable can also be compared easily with others. Table 3 demonstrates the results for the determinants of the levels of income inequality across the VoC. Model 1 in Table 3 demonstrates the results cross-nationally, with no sample restriction. The associational power of the working class measured by union density as well as public expenditure on vocational rehabilitation programs inhibit income inequality, whereas capital allocation to firms through stock markets (i.e. listed companies on stock exchange) and financialized corporate governance (i.e. stock market capitalization) incubate it. More precisely, a standard deviation increase in union density leads 0.03 standard deviation decrease in the level of income inequality within countries. Whereas a standard deviation increase in the expenditure on vocational rehabilitation programs leads to 0.67 standard deviation decrease in the level of income inequality, a standard deviation increase in the natural log of the listed companies on stock exchanges leads to 0.13 increase in the level of income inequality within countries. I also find greater degree of employment protection to have an inhibiting effect on the levels of income inequality, though its statistical significance is marginal. 13

The results of my analysis exhibit two novel findings. First, the persistent negative effect of changes in public expenditure on vocational rehabilitation programs—a vastly underexplored area in cross-national research on inequalities—on the levels of income inequality. Public expenditure on vocational rehabilitation programs is aimed at facilitating labor market participation for individuals with disability, enabling them to generate stable income and benefits for themselves (OECD, 2019). This result is particularly new. Indeed, across model specifications, I find a negative association between public expenditure on vocational rehabilitation programs (i.e. as a crucial labor market intervention) and the levels of income inequality (α < 0.05), and with a relatively large effect size. As noted, workers with disability sometimes constitute up to 20 percent of the workforce across countries in the Global North (Powell, 2021), and the extent to which employees with disability participate in ordinary paid work that generates stable income and benefits is a major contributing factor to reducing the levels of income inequality. Importantly, an OECD (2019) report indicates that only 35 percent of individuals with disability are able to find employment in Spain, whereas 55 percent of individuals with disability are likely to find employment opportunities in Finland, which is a much higher percentage. 14 We can also observe the average Gini coefficient for household income for the time period that is examined in this study (1985–2016) in Spain is significantly higher than Finland (see Figure 5, Appendix 1). Equal treatment of individuals with disability in the hiring processes enables them to generate fiscal resources and benefits, which then allow them to achieve better labor market outcomes. Investment in vocational rehabilitation programs thus inhibits income inequality within countries.

Second, I find that a crucial dimension of corporate governance, namely, the mode of capital allocation to firms (i.e. listed companies on stock exchanges) also affects the levels of income inequality. This suggests that as capital is allocated more through stock exchange, the levels of income inequality increased within countries. The effect of financialization on income inequality often measured by “stock market capitalization” in cross-national studies is well known (Dore, 2000; Huber et al., 2022; Flaherty, 2015; Godechot, 2016; Roberts and Kwon, 2017; Sjöberg, 2009), but less known is the relationship between the mode of capital allocation to firms and income inequality. Listed companies on stock exchange allows us to test the relationship between the mode of capital allocation to firms and the levels of income inequality. While previous studies have found financialization of corporate governance to be positively associated with income inequality, my results demonstrate that the mode of capital allocation to firms is also positively associated with an increase in the levels of income inequality. That is to say, as capital has been allocated more through stock markets as opposed to relational banking, the levels of income inequality have increased within countries and over time (Aoki, 1994; Aoki and Dore, 2001; Jackson, 2003).

Are the determinants of income inequality the same across VoC? For example, does union density matter for income inequality in CMEs as much as it matters in LMEs? How may the results change if I restrict the sample to each regime of capitalism that are identified by the cluster analysis? It is plausible to suggest that what determines the levels of income inequality in Germany as the exemplar of the coordinated market economies may well be different than those of Sweden as a conspicuous example of the social democratic market economies. To explore the predictors of regime-specific estimates of income inequality across the VoC, I restrict the sample to those countries that constitute each regime. It must be noted that the models with the restricted samples are similar to fully interacted ones whereby each independent variable is interacted with dummy variables indicating a variety of capitalism.

When restricting the sample to only LMEs as presented in Model (2), union density inhibits inequality while more capital allocation to firms though stock exchange incubates it. Hence, my results demonstrate that declining unionization as well as the increasing number of listed companies on the stock exchange have led to increased levels of income inequality in LMEs. Model (3) demonstrates the results for CMEs. Crucially, for CMEs, employment protection inhibits income inequality. That is to say, as the degree of employment protection waned or stagnated over time, the levels of income inequality increased in CMEs. In SDMEs, as shown in Model (4), the financialization of corporate governance through greater stock market capitalization is positively associated with the levels of income inequality. Conversely, public expenditure on vocational rehabilitation programs is negatively associated with the levels of income inequality across SDMEs, though its statistical significance is only marginal. I find no support for patent rate as a measure of technical change to facilitate or impede income inequality cross-nationally in the pooled fixed-effects Model (1), but technical change measured by patent rate has marginal inhibiting effect on the levels of income inequality across SDMEs (Model 4). To further investigate the impact of technical change on income inequality, I used two alternative measures. First, total expenditure by both the public and private sectors on research and development (R&D) in each country over time, and second, proportion of the working population in each country who completed a college degree. Neither of these variables are statistically significant.

These are my key results, and the ones related to vocational rehabilitation programs and mode of capital allocation to firms are particularly new. However, one may wonder if the results are robust to alternative estimation choices, so I conducted a number of robustness checks. I find these results to be statistically significant at conventional level (α < 0.05) when I add a linear measure of time, when I omit one country at a time to test whether the results were driven by the outlying country, and when I employ random (rather than fixed) effects model whose results are exhibited in Table 7, Appendix 1. In fact, I find particularly consistent results when I run random effects model in order to explore between-country—as opposed to within-country—effects of the independent variables on the outcome variable.

In auxiliary analysis, I also explored a number of interaction effects. For example, I explored whether the interaction between employment protection expenditure on social benefits and tax revenues, employment protection and vocational training expenditure, employment protection and vocational rehabilitation expenditure, and listed companies on stock exchange and stock market capitalization explain variation in the levels of income inequality cross-nationally. However, none of these interactions are statistically significant. The interaction effect between public expenditure on vocational rehabilitation and public expenditure vocational training is the only instance that is statistically significant, though only at the non-conventional level (p < 0.1). It must be noted that I also pursued the “interaction approach” by interacting the fixed-effects model with a categorical variable indicating each regime of capitalism. The results are particularly consistent, and they are exhibited in Table 8 of Appendix 1.

Discussion and conclusion

Scholars from across social science disciplines agree that much of income and social inequalities are the direct result of the ways in which economic resources are organized through institutions and their interaction with each other (Acemoglu and Robinson, 2015; Hall and Soskice, 2001; Huber and Stephens, 2014; Rueda and Pontusson, 2000; Thelen, 2007). The VoC perspective endows us with the analytical tool to differentiate which institutions are—and which are not—conducive toward building a more socially and economically equitable society. One of the central goals of this study was to deepen the engagement with the VoC perspective and the broader research on income inequality. By identifying a number of variables that capture the effects of differential institutional blueprints of national economies, this study explored what institutional factors matter for the levels of income inequality, both cross-nationally and within each regime of capitalism. There is a wide consensus among scholars that the endogenous evolution of institutions and their interaction influence how gains of economic actions are distributed among individuals (Acemoglu and Robinson, 2015; Hall and Soskice, 2001). Building on previous research that takes an institutional approach to the study of income inequality (Kenworthy and Pontusson, 2005; Roberts and Kwon, 2017; Rueda and Pontusson, 2000), this article made three contributions.

First, it demonstrates that within-country temporal change in the levels of public expenditure on vocational rehabilitation programs negatively impacts the levels of income inequality. That is to say, as public expenditure in vocational rehabilitation programs declined (or in some cases stagnated) over time, the levels of income inequality increased within countries over the time span of the panel data. The relationship between this important labor market intervention, namely, vocational rehabilitation programs and income inequality has not been tested in previous research. This is a crucial dimension of institutional complementarities that has been ignored and this study is the first to present this novel finding. To be sure, there has been a body of scholarship known as “active labor market policies” (ALMP) mostly in the economics tradition, but the ALMP literature has been mostly concerned with the extent to which such policies and interventions can help reduce unemployment (Crépon and Van Den Berg, 2016; Laun and Thoursie, 2014; Lechner et al., 2011), and not so much income inequality. In addition, the literature on the ALMP often uses the sum volume of expenditure on labor market policies when it examines its relationship with a socioeconomic outcome. It does not “parse out” the effect of specific policies such as vocational rehabilitation programs that specially targets individuals with work limitation and disability (Rueda, 2015). After all, public expenditures on “vocational rehabilitation programs and training,” “direct job creation,” and “start-up incentives” all fall under the broad category of active labor market policies, but each may—or may not—have an effect on a particular socioeconomic outcome (OECD, 2019). In this article, I specially demonstrate the effect of one policy within the broad category of active labor market policies, namely, public expenditure on vocational rehabilitation programs. I find that the expenditure on vocational rehabilitation programs is negatively associated with the levels of income inequality within countries. However, when I examine its effect on income inequality within regimes, it is only marginally significant in SDMEs.

Second, I find evidence that the mode of capital allocation to firms—an important dimension of corporate governance (Aoki, 1994; Aoki and Jackson, 2008)—bears on the levels of income inequality within countries. The greater the volume of companies listed on the stock exchange suggests that capital is allocated to firms more through the stock market, and less through relational banking (i.e. long-term lending). 15 As companies rely more on the stock market to secure funds (as opposed to relational banking), the levels of income inequality increase over time. This finding suggests that a particular dimension of corporate governance, namely, capital allocation to firms through the stock exchange bears on income inequality. As noted, the previous research has found a positive association between a measure of financialization, namely, stock market capitalization and income inequality (Mahutga et al., 2017; Huber et al., 2022; Roberts and Kwon, 2017). For example, Huber et al. (2022: 444) in their most recent study use stock market capitalization as an indicator of financialized corporate governance and find that it is positively associated with income inequality. However, stock market capitalization and listed companies on the stock exchange are not the same. If stock market capitalization is a measure of financialized corporate governance, the volume of listed companies on the stock exchange measures the mode of capital allocation to firms. That is to say, the greater volume of companies listed on the stock exchange signifies more capital allocation through the stocks market as opposed to relational banking. I find that the greater allocation of capital to firms through the stock exchange incubates income inequality within countries.

Third, I conducted cluster analysis with the most recent data available on the institutional characteristics of national economies in most countries of the Global North. To investigate how countries can be grouped together based on their institutional arrangements, I used an unsupervised machine learning algorithm known as k-means clustering. Instead of taking for granted the existing (mostly deductive) typologies of VoC, I conducted cluster analysis to inductively demonstrate how countries can be distinctly grouped together (Ermakoff, 2019; Hastie et al., 2009). The motivation to conduct cluster analysis stems from the fact that institutions are not static, as the “liberalization thesis” suggests (Streeck, 2011; Thelen, 2007, 2014), and the clustering here takes into account the important effect of time on the changing and dynamic characteristics of institutions. By conducting cluster analysis, this article not only takes an inductive approach similar to that of Schneider and Paunescu (2012), but also presents a more up-to-date picture of how countries can be grouped together based on their institutional similarities. For example, it shows how Japan, a country that has consistently been labeled as a coordinated market economy has moved toward a socioeconomic system characteristic and reminiscent of liberal market economies. This is largely due to the fact that institutions evolve and change over time (i.e. unions decline, employment protection weakens, expenditure in vocational rehabilitation programs dwindles, etc.), and that the institutional arrangements, which once allowed Japan to be categorized as a coordinated market economy 20 years ago (Hall and Soskice, 2001) is no longer the case. By drawing on the latest data available, I account for the endogenous evolution and changes in institutions when we attempt to cluster countries, as Acemoglu and Robinson (2015) emphasize.

Cross-nationally, I find evidence for crucial institutional blueprints such as labor unions, public expenditure on vocational rehabilitation programs, and the mode of capital allocation to firms as important determinants of income inequality. While more capital allocation to firms through stock markets incubates income inequality, the organizational power of the working class (i.e. measured by union density) and labor market interventions in the form of public expenditure on vocational rehabilitation programs inhibit it. It is worth emphasizing that the negative effect of expenditure on vocational rehabilitation programs on the levels of income inequality has not been previously explored in cross-national research on institutions and income inequality, and this is particularly a novel finding of this study. Vocational rehabilitation programs facilitate more labor market participation for individuals with work limitation and disability, enabling them to generate stable income and benefits for themselves and ultimately improve their labor market outcomes (OECD, 2019). My results exhibit strong evidence that more investment in vocational rehabilitation has important implications for reducing the levels of income inequality.

As alluded earlier, to explore regime-specific determinants of income inequality, I restricted the sample to countries that fall under each variety of capitalism informed by the cluster analysis. There are no particular reasons to believe that what explains variation in the levels of income inequality in LMEs is the same in SDMEs. Indeed, restricting the sample to each regime of capitalism and then running the fixed-effects model allow us to explore the heterogeneity of determinants across VoC. Within clusters, and specifically for LMEs, union density is a negative determinant of the levels of income inequality. This suggests that as union density—the associational power of the working class that enables them to win concessions from the employers for better material conditions—declined, the levels of income inequality increased within countries (Mahutga et al., 2017; Freeman and Katz, 1995; Gottschalk and Smeeding, 1997; Kenworthy and Pontusson, 2005; Kollmeyer and Peters, 2019; Rueda and Pontusson, 2000). In CMEs, employment protection inhibits income inequality. More substantively, as employment protection weakened, income inequality increased in CMEs. For SDMEs, the financialization of corporate governance measured by stock market capitalization positively predicts variation in the levels of income inequality, suggesting that as corporate governance became more financialized, the levels of income inequality increased within countries in SDMEs. In addition, public expenditure on vocational rehabilitation programs negatively predicts the outcome variable in SDMEs, though its statistical significance is marginal (α < 0.1).

In short, building on previous cross-national studies, the primary purpose of this article was to bring the VoC perspective to bear on income inequality research by identifying variables that directly correspond to the institutional complementarities of national economies. The necessity to look at the role of institutional designs of national economies and their differences stems from the fact that much of social and income inequalities are a direct result of the ways in which economic resources are organized through institutions. The VoC perspective presents a useful analytical lens by which we can differentiate what institutional designs are most conducive toward building a more socially and economically equitable society. If anything, the recent COVID-19 pandemic crisis has shown that the way in which institutions are set up and the way they interact with each other shape the strategies that the state adopts to respond to shocks and disasters, both in terms of containing its dissemination and providing relief to those most affected by it. Institutions thus heavily influence how economic resources are distributed, and this study identified the institutional variables across different regimes of capitalism that are most conducive to egalitarian outcomes from the VoC perspective.

Footnotes

Appendix 1

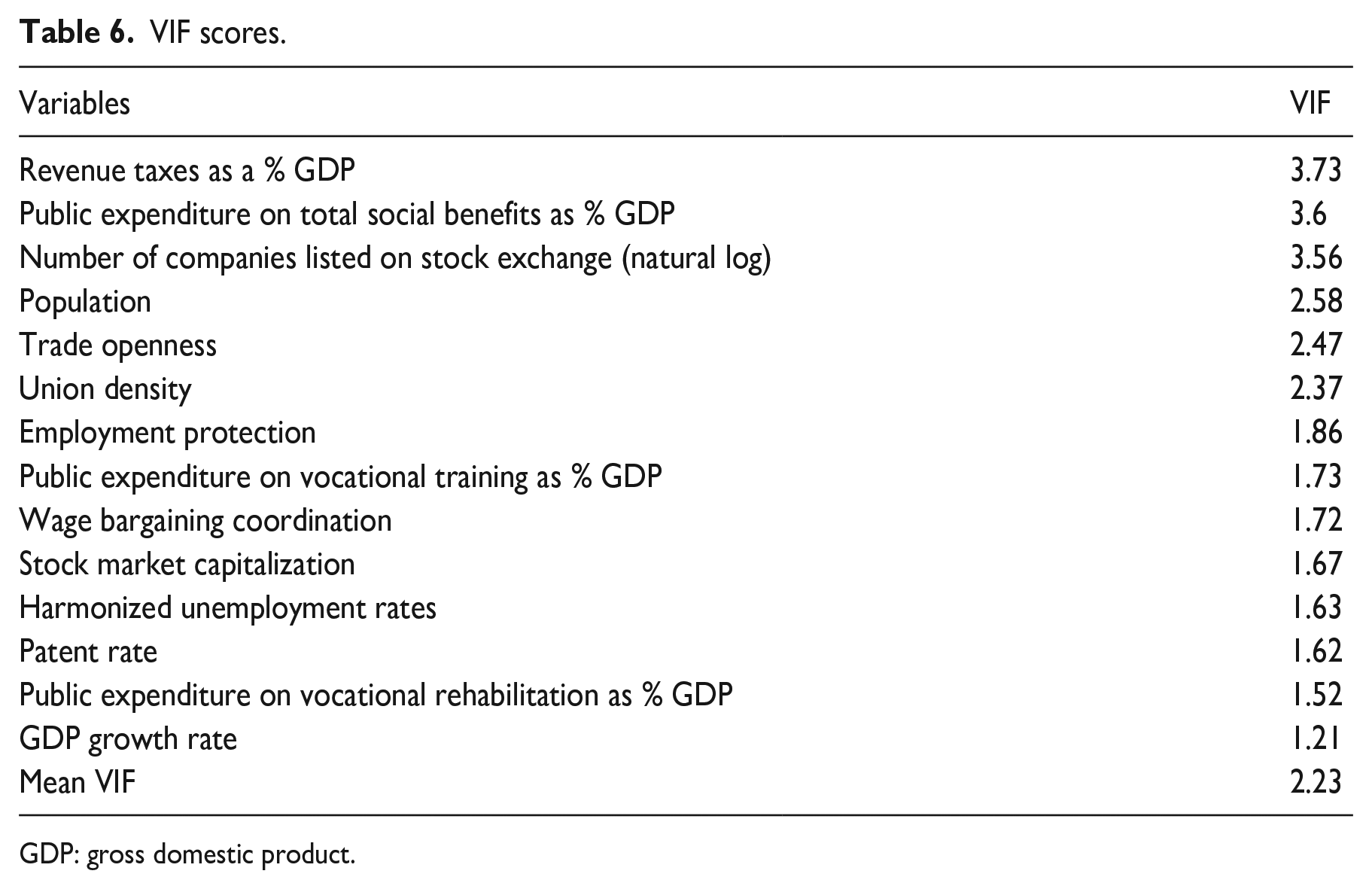

VIF scores.

| Variables | VIF |

|---|---|

| Revenue taxes as a % GDP | 3.73 |

| Public expenditure on total social benefits as % GDP | 3.6 |

| Number of companies listed on stock exchange (natural log) | 3.56 |

| Population | 2.58 |

| Trade openness | 2.47 |

| Union density | 2.37 |

| Employment protection | 1.86 |

| Public expenditure on vocational training as % GDP | 1.73 |

| Wage bargaining coordination | 1.72 |

| Stock market capitalization | 1.67 |

| Harmonized unemployment rates | 1.63 |

| Patent rate | 1.62 |

| Public expenditure on vocational rehabilitation as % GDP | 1.52 |

| GDP growth rate | 1.21 |

| Mean VIF | 2.23 |

GDP: gross domestic product.

Acknowledgements

I dedicate this article to the memory of Erik Olin Wright, who provided unstinting moral and intellectual support for this research project since its inception. Especial thanks to Ivan Ermakoff, Jane Collins, Joel Rogers, Tim Smeeding, Christine Schwartz, Gøsta Esping-Andersen, Thomas Piketty, Elizabeth Hirsh, Arne Kalleberg, Peter Hall, Lane Kenworthy, Myra Marx Ferree, John Levi Martin, Robert Freeland, Pam Oliver, Douglas Hemken, Jingying He, and Alexis Econie for their helpful comments on the earlier iterations of this paper. I have also benefited from the comments provided by the participants of ‘Politics, Culture and Society’ and ‘Sociology of Economic Change and Development’ workshops at the University of Wisconsin–Madison’s Sociology Department as well as ‘Cross-National and Comparative Studies of Inequality’ session at the Population Association of America conference.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.