Abstract

The objective of this study was to elucidate the medical causes and consequences of foreclosure. We surveyed 90 households undergoing foreclosure in 2013–2014 in Maricopa County, Arizona on two occasions approximately five months apart. At baseline, median monthly household income was $3,000, and median mortgage payment $1,350. Only 10% of respondents lacked health insurance when surveyed, although 28% had experienced a gap in coverage within the past two years. Fifty-seven percent identified a medical debt or another medical cause of their foreclosure, and 54% had taken on new debt to pay medical bills; 10% had mortgaged their home for this reason. Although 57% of respondents had a chronic condition requiring ongoing care, more than half reported delaying or skipping a needed medical visit. At follow-up, one-third of respondents had been unable to afford food, and 3 respondents reported becoming homeless; 46% said foreclosure had worsened their health; and 63% had already incurred new medical debts. Medical debt and medical problems frequently contribute to foreclosure, even among insured families. Foreclosure compromises access to care and basic necessities like food and shelter, and worsens self-reported health.

Foreclosure is a legal procedure for the seizure of real property due to non-payment of a secured loan (e.g., mortgage or home equity loan). During and after the recent Great Recession (approximately December 2007–June 2009), millions of families lost their homes to foreclosure. In 2010, the peak year, banks and other lenders initiated more than 2.8 million foreclosures, affecting 2.23% of all homes in the U.S. 1 Although foreclosures have subsequently fallen by half, their incidence remained higher in 2013 than in 2007, the year prior to the economic downturn. 2 In May 2015, there were 41,000 completed foreclosures, nearly double the monthly average of 21,000 between 2000 and 2006. 3

Illness and medical bills contribute to about 62% of bankruptcies.4,5 Yet despite the ubiquity of foreclosures, and growing recognition that housing is an important social determinant of health, few recent studies have examined the medical causes and consequences of foreclosure that homeowners identify. Even fewer have used a longitudinal design or detailed questioning to explore the foreclosure experience, or assessed areas particularly hard hit by foreclosure. We sought to address these issues by surveying households in foreclosure in Arizona, which has experienced some of the steepest home value declines and highest foreclosure rates in the U.S.

Methods

Using the Westlaw© online database service, we identified all foreclosure filings in Maricopa County Arizona during three periods: December 18–24, 2013 (Round 1), December 26, 2013–January 4, 2014 (Round 2) and June 10–26, 2014 (Round 3), and gathered information on property type, and owner name and address. We removed commercial properties and properties likely to be vacant (i.e., the property address and current owner address did not match), leaving 1,486 properties for further review. We used the People Finder database function of the LexisNexis© online database service to obtain telephone numbers associated with the property address and owner. We excluded the 663 properties without a phone number listed for the owner at the foreclosed property address or with a phone number that the database indicated was very likely disconnected. An additional 33 properties were excluded for other reasons (e.g., duplicate entries, deceased owner, or trust-owned), leaving a total of 790 homeowners eligible for inclusion in the study.

We contacted homeowners to recruit them into our study using techniques from Dillman’s Total Design Method. 6 These techniques included: the use of university letterhead; hand-signatures; hand-stamped mailings; a mailed survey booklet with colorful front and back pages; and multiple modes of respondent contact (i.e., letter, post-card, email, phone call). We initially sent each foreclosed homeowner a letter that briefly explained the study, provided a web-address for homeowners who wished to complete the survey on-line, notified the homeowner that they would receive a mail packet soon, and described the study eligibility criteria: U.S. citizenship or permanent resident status; residence in the foreclosed property for at least 6 of the last 12 months; ownership of the home in foreclosure; and age 18 years old or older. The mail packet that followed contained: (1) a disclosure letter describing the study and human-subjects protections, (2) a survey booklet and instructions how to complete the survey online or by phone, (3) a stamped-self-addressed envelope for the mail booklet return and (4) a one dollar cash incentive. All materials were in English and Spanish.

We sent non-respondents a post-card reminder, a duplicate mail packet (Round 1 only), and a final letter requesting their participation. We then attempted to reach non-respondents by phone, calling up to 12 times per household. The duplicate mail packet was not used in Rounds 2 or 3 due to negligible response in Round 1, high numbers of returned unopened mail materials, and limited resources which we thought would be better used for phone follow-up.

Homeowners who completed a baseline survey were contacted approximately 5 months (range 2–7 months) later and asked to complete a follow-up telephone survey. Participants received $50 for each completed interview (or $25 if they did not want to provide a SSN which was required for incentives totaling $50 or more).

The baseline questionnaire asked about demographic characteristics, insurance status, health and health services use of the respondent and their spouse or partner, debts, and information about the home in foreclosure. Respondents were asked about 25 specific causes of the foreclosure, and could add “some other cause.” For analysis, we classified these causes as being housing market-related or family-related. A cause was considered housing market-related if, in a more favorable housing market, sale of the home could have prevented the problem leading to foreclosure (e.g., by providing sufficient funds to repay all outstanding home-related debt). For simplicity, we named the remaining factors (which were unrelated to the housing market) “family” factors, and we further classified these as either “medical-related” or “non-medical related” (e.g., job-loss).

We also defined a broader category of medical foreclosures that included respondents who indicated they had taken on new debts to pay medical bills, in addition to those citing a specific medical-related cause of foreclosure.

The follow-up survey collected data on changes in selected demographic, health, debt, housing and foreclosure characteristics.

Differences in continuous variables were assessed with t-tests, while categorical variables were assessed using chi square tests.

Results

Of the 790 households whom we attempted to reach, the post office returned mail for 170 respondents and another 183 respondents had disconnected or non-functioning phones; thus we failed to make contact with 44.7% of intended respondents. Respondents from 90 of the remaining 437 foreclosed households completed baseline surveys, a cooperation rate of 20.6% and an overall response rate of 11.4%. We obtained follow-up surveys from 76 respondents.

To assess response bias we examined publicly available housing records. Median square footage of home, number of bedrooms or bathrooms, last price when sold or tax valuation did not differ significantly between responders and non-participants (non-response, not eligible, refused and withdrew).

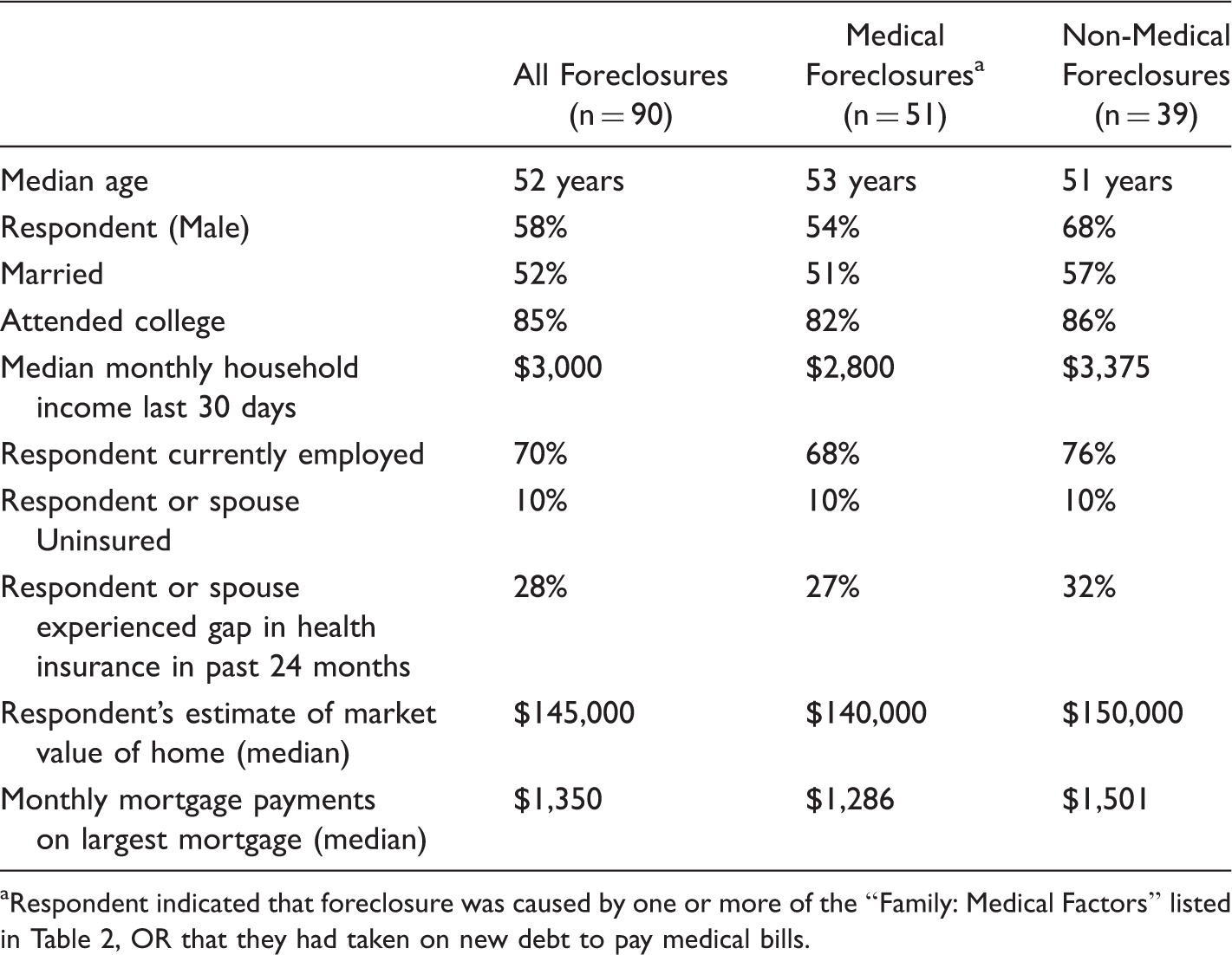

Demographic Characteristics of Persons Experiencing Foreclosure, With and Without a Medical Contributor a to Foreclosure, 2012/2013.

Respondent indicated that foreclosure was caused by one or more of the “Family: Medical Factors” listed in Table 2, OR that they had taken on new debt to pay medical bills.

Ninety percent of respondents reported that they and their spouse/partner had health insurance at the time of the survey. However, more than one-quarter had experienced a gap in coverage within the past two years.

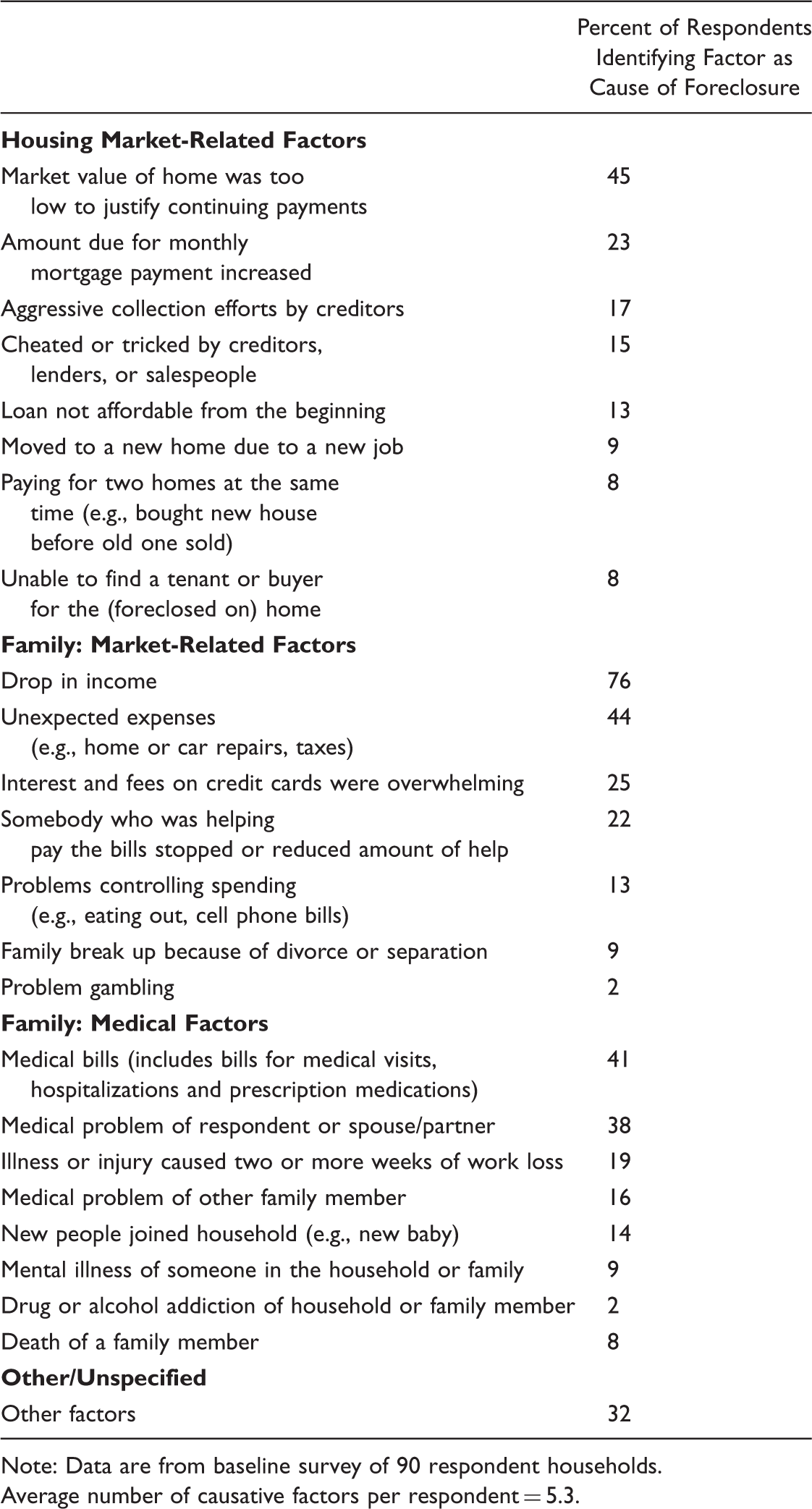

Causes of Foreclosure Identified by Persons Experiencing Foreclosure.

Note: Data are from baseline survey of 90 respondent households.

Average number of causative factors per respondent = 5.3.

Medical issues were prominent among these family factors. Two-fifths of all respondents cited medical bills as a cause of foreclosure, while one-fifth stated that income loss due to illness was a cause of foreclosure. Overall, 56.7% of respondents identified medical debts or a medical cause of their foreclosure. An additional 3.3% reported losing at least 2 weeks of work-related income (approximately equivalent to one month’s mortgage payment) due to an illness of themselves or a family member, but did not cite this as a cause of foreclosure.

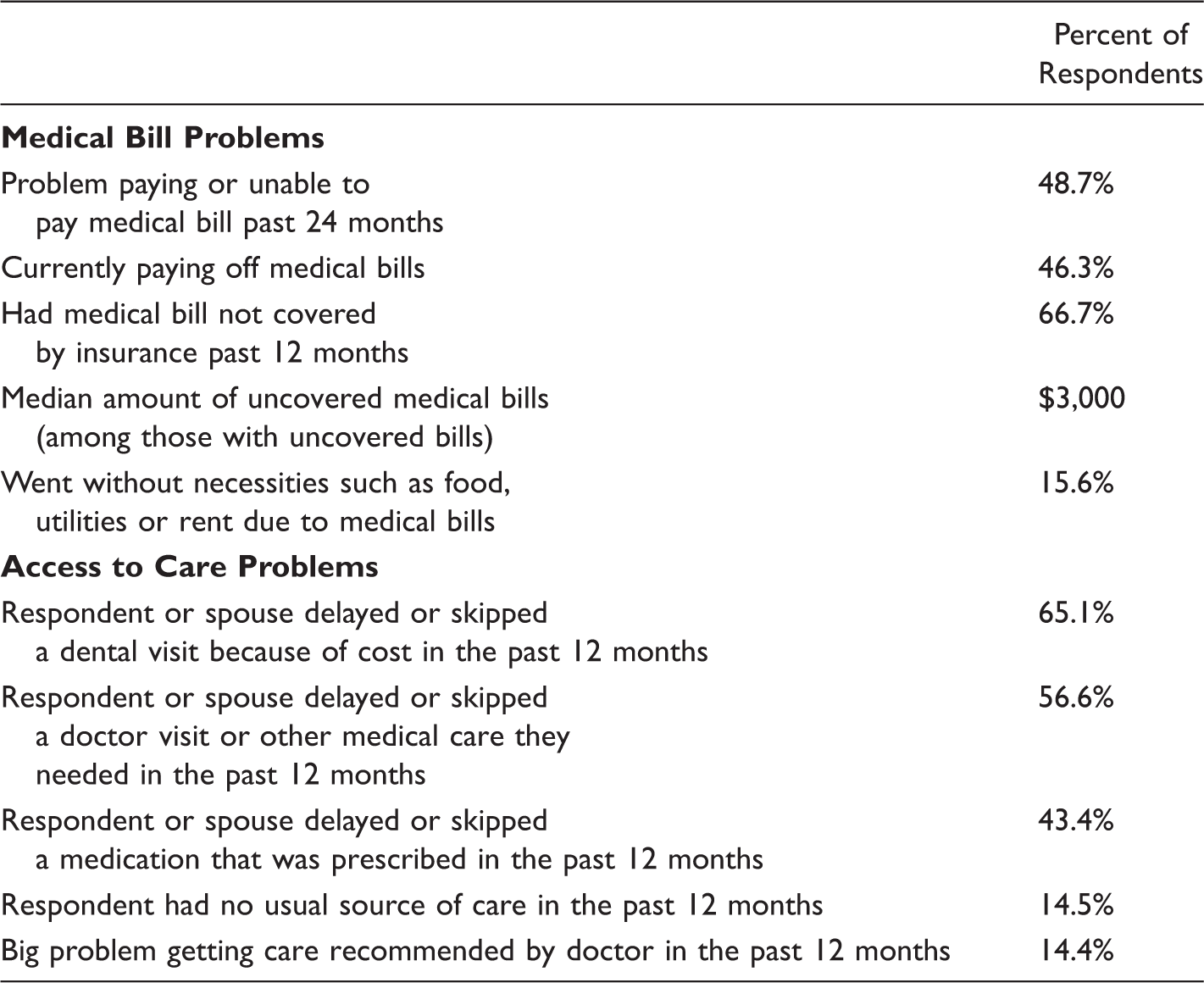

Financial Problems Due to Medical Bills and Problems in Access to Medical Care Reported at Baseline (n = 90) or Follow-Up (n = 76) Surveys of Families Experiencing Foreclosure.

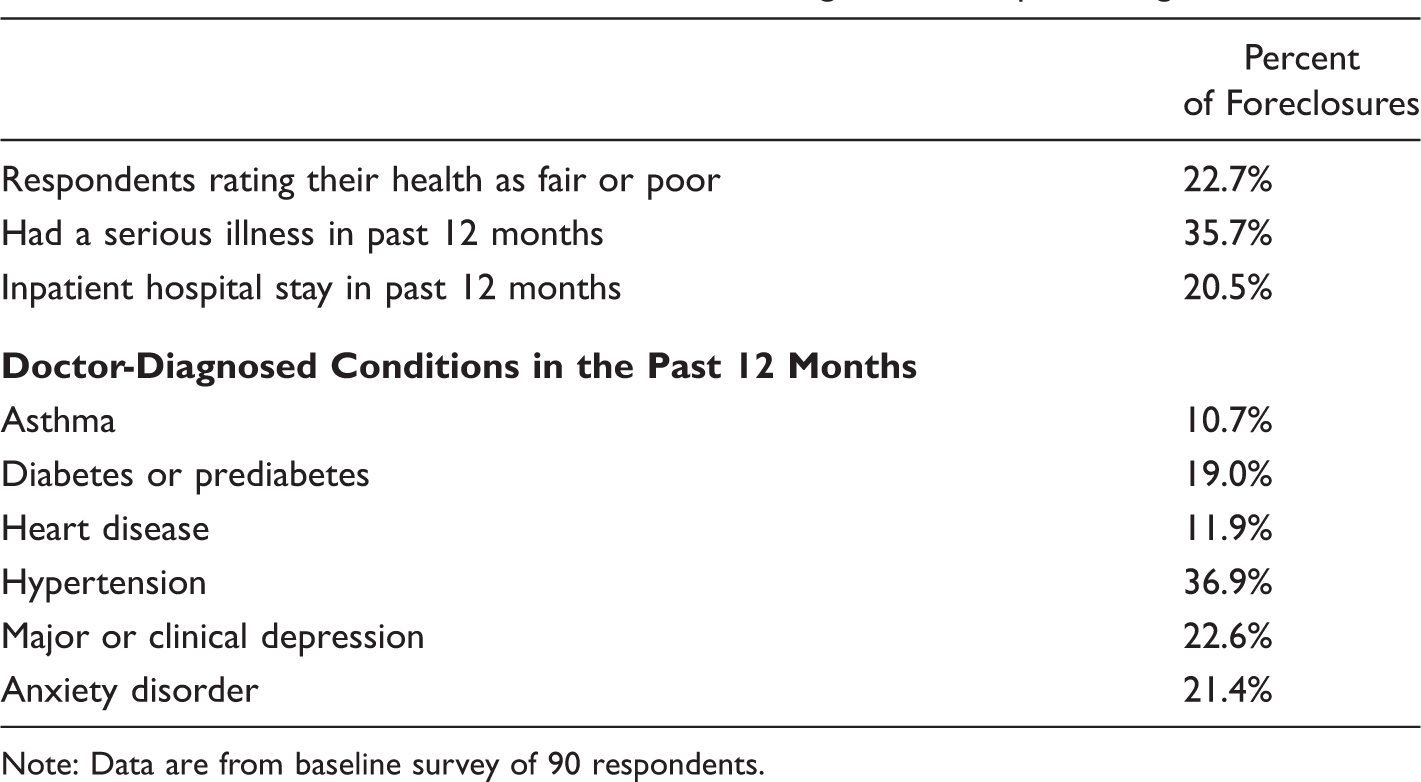

Health Status and Medical Problems Among Persons Experiencing Foreclosure.

Note: Data are from baseline survey of 90 respondents.

Discussion

Our data suggest that health and medical issues often contributed to foreclosure, and that the experience of foreclosure compromised access to medical care. Moreover, many families in foreclosure were unable to afford medications, and some even food and shelter. A disturbing number suffered additional financial setbacks caused by illness and new medical bills during the foreclosure process.

The association between housing instability or foreclosure and mental health problems is well established.7–15 Foreclosure is such a well-known stressor that it is included in a commonly-used stress assessment tool, the Social Readjustment Rating Scale; in large population surveys asking people to rank the stressfulness of 51 life events, foreclosure ranks sixth. 16

Several studies have also linked housing instability to poor physical health. A study of 4,200 borrowers who received credit counseling in Minneapolis-Saint Paul between 1991 and 2003 found that health problems contributed to 20–25% of foreclosures. 17 In a 2005 survey of 299 predominantly minority, low income households in Chicago, 33% of respondents listed medical problems as a cause of their foreclosure. 18 Among 1,692 individuals seeking free assistance with tax return preparation, one-eighth reported that medical debt had resulted in adverse housing outcomes such as inability to obtain or pay a mortgage. 19 A Freddie Mac survey of chief causes of mortgage delinquencies (which often presages foreclosure) found that loss of income was the most frequent cause – 36% in 2006 – and illness ranked second at 21%. 20 In a 2006 survey of 128 households in four states on the brink of foreclosure, about half of respondents listed at least one medical cause of their foreclosure. 21

A 2009 study in Philadelphia found high uninsurance and skipped-prescription rates among people in foreclosure; 9% reported that a medical condition was the primary reason for foreclosure, and 22.7% owed money to medical creditors. 7 In a nationwide cohort of older adults, 68 people behind on mortgage payments reported poorer baseline health and access to care than their peers, and suffered more food insecurity and medication non-adherence. 13 Living in proximity to foreclosed homes has been associated with increased obesity. 22 High rates of ill health have been found in zipcodes with high foreclosure rates. 23 In a 2014 study using recent data from the National Longitudinal Study of Youth 1979, the acquisition of a work-limiting health problem or serious chronic condition was associated with mortgage default and home foreclosure. This association was partially mediated by loss of health insurance as well as income. 24

Our results are consistent with this previous research, and our repeated survey design helps establish that foreclosure may be both a cause and consequence of medical problems.

Our study has important strengths and limitations. Strengths include that the survey was carried out in a region that was hard hit by the foreclosure crisis, but has not been the focus of previous studies. Moreover, we collected much more detailed information about the causes and consequences of foreclosure than has been available from previous research.

The major limitation of our study is the low contact and response rates, a problem that has also been encountered in previous survey-based studies. Families in foreclosure are particularly difficult to contact because many relocate. Moreover people in foreclosure are often exposed to unpleasant and distressing debt-collection calls, and hence may be reluctant to answer calls from unfamiliar numbers or to open unsolicited mail. In addition, foreclosure is highly stigmatizing. While we offered participants who completed surveys a $50 honorarium, the institutional review board forbade us from mentioning the amount of compensation in our pre-survey letter to participants due to concern that stating the amount would be “coercive”. This restriction likely lowered our response rate. However, the similarity of the housing characteristics of responders and non-responders gives reassurance regarding the representativeness of our sample.

The conditions in which people are born, grow, live, work, and age – so-called “social determinants” – have a decisive impact on health. Adequate, secure, safe and stable housing – and the policies that facilitate it – are key components of a healthy social environment. Housing determines exposure to toxins such as lead and asthma triggers; access to adequate heating and cooling; and proximity to critical neighborhood resources such as parks, fresh fruits and vegetables, safe streets, and good schools. Medical and housing problems often interact to initiate a downward spiral; sudden and unforeseen financial shocks due to illness can aggravate housing insecurity, which in turn, further compromises health.

Regulation and enforcement to shield consumers from financial institutions’ deceptive and unfair lending practices are key to helping many families avoid losing their homes. But health-related policy initiatives could also help homeowners avoid the harms attendant on foreclosure. Improving disability insurance, mandating paid sick leave, and assuring first-dollar coverage of medical bills – a reversal of the recent trend toward rising health insurance co-payments and deductibles – would stabilize family finances in the face of health problems and, in some cases, prevent foreclosure. The misfortune of illness should not be compounded by the trauma of losing a home.

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Support for this publication was provided by the Robert Wood Johnson Foundation’s Public Health Law Research program.