Abstract

A growing set of epidemiological data links personal financial debt to negative mental and physical health outcomes. These findings point to debt as a potentially significant socioeconomic determinant of population health, especially given rising rates of household and consumer debt in industrialized nations. However, the political and economic contexts in which rising consumer debt is embedded and the ways in which it is experienced in everyday life are underexplored in this epidemiological literature. This gap leaves open questions about how best to situate and understand debt as a health determinant with both psychosocial and neo-material attributes. In this article, we discuss findings from a qualitative study of personal debt experience in Boston, Massachusetts. Participants’ debt narratives highlight the powerful feelings of shame, guilt, and personal responsibility that debt engenders. The findings point to the influence of neoliberal ideology in shaping emotional responses to debt and suggest that these responses may be important pathways through which debt affects health. We discuss our findings within the broader landscape of American neoliberal economic policy and its role in shaping trends of consumer debt burden.

Keywords

Across the industrialized world, adults are experiencing rising consumer financial debt, and in the United States that increase is particularly dramatic. In 1980 an American household’s debt was equivalent to about 65% of its annual disposable income; today that figure is 105%, 1 and 80% of all American households report being in debt. Home mortgage loans are responsible for much of this increase,2,3 as was highly publicized during the housing bubble rupture in 2007 and subsequent 2008 financial crisis. However, other forms of consumer debt, such as auto loans, credit cards, and most strikingly, student debt, have since taken over, reaching an all-time high of $3.2 trillion in 2014.3,4 A growing body of epidemiological research suggests this ballooning consumer debt has important implications for health. Several studies have now found that individuals who are in financial debt or have experienced a home foreclosure have higher risk of negative mental health outcomes, including depression, anxiety, and psychological distress, and are at increased risk for committing self-harm or attempting suicide.4–16 Other studies have linked financial debt to measures of physical health, including lower self-reported general health, higher obesity, higher blood pressure, poorer sleep quality, and lower aggregate life expectancy.17–22

This growing literature suggests that consumer debt is an important socioeconomic determinant of health, and research continues to investigate the nature of its impact across a range of outcomes and settings. However, like much other research on socioeconomic status (SES) and health, studies thus far have paid relatively little attention to the political economic contexts that underlie consumer debt or the consequences of these conditions for the lived experience of being indebted. Several authors have noted, with respect to social inequality more broadly, 23–25 that research focusing on conventional SES measures (i.e., income and education) “without understanding the process of power, context and meaning through which socioeconomic resources are obtained and experienced” 23 nurtures an incomplete view of socioeconomic effects on health that may ignore other critical pathways. Similarly, without explicating the political economic underpinnings of consumer debt, current epidemiological studies risk reifying debt as an attribute of individuals that is immune to external forces and is decontextualized from its actual embedding in culture and policy.

Further contributing to the lack of contextualization, the felt experience of consumer debt in the everyday lives of individuals and families is largely absent from epidemiological research. This absence is particularly problematic given that the mechanisms through which debt impacts mental and physical health are still unclear. A psychosocial stress pathway seems likely,13,19 and better understanding the psychosocial and emotional experience of debt and the meaning that it holds for individuals in their daily lives would greatly facilitate efforts to trace this pathway. As Kaplan and Lynch 24 have argued, taking the time to elaborate such experiential and contextual factors, especially with interdisciplinary approaches that can overcome the “crude”-ness of some quantitative measures, is essential to social epidemiological work: “what is needed is an ‘epidemiology of everyday life’ that would describe, with nuance and depth, the links between neomaterial conditions and the forces that generate them, psychosocial states, the social milieu, and health outcomes.” 24

In this article, we seek to contribute to such an epidemiology of everyday life, as it pertains to consumer debt in the United States. We draw on anthropological theory and method, such as Dressler’s “third moment” notion in medical anthropology, 26 emphasizing a synthetic approach to social determinants of health such that cultural and structural forces, emic and etic perspectives, are seen in interplay rather than opposition. Similarly, in biocultural anthropology, Hicks and Leonard 27 build on Goodman and Leatherman’s 28 seminal work to encourage greater attention to the ways in which social and cultural experiences that impinge on health are both constructed and constrained by historical political economic process. In these synthetic approaches, qualitative methods that prioritize local knowledge and expertise and situate informant statements within broader life narratives and circumstances 29 are essential for unveiling the rich experiential realities through which social forces “get under the skin.”

With that in mind, we report findings in this paper from a qualitative study of adult experiences with debt in the Dorchester neighborhood of Boston, Massachusetts. As part of a broader project exploring the biological and physical health impacts of debt and credit disparities, this study offers an informative lens onto the lived experience of indebtedness. Residents of this large and diverse neighborhood represent a wide variety of ways in which people can have debt – from young students struggling with education loans and first credit cards, to single mothers utilizing multiple credit options to make ends meet, and middle-aged professionals balancing mortgages on income-generating properties. Their stories of living with debt reveal important insights about the processes through which debt is both experienced and embodied, including as a source of emotional and physical suffering as well as a constraint on bodily needs and actions.

We analyze these processes of suffering within the context of neoliberal ideology and the political trends that have helped to funnel Americans into debt while simultaneously making them bear the weight of shame, guilt, and responsibility. We pay particular attention to the bodily metaphors and idioms people use to describe their debt as revealing windows into the power of debt ideology as a source of embodied suffering. We believe that attending further to these issues in the epidemiological literature enhances our understanding of the mechanisms through which debt operates as a health determinant as well as the structural considerations that will need to be weighed in any potential future intervention efforts.

Methods and Sample

Methods

Data for this paper come from the Price of Debt Study, a 5-year, mixed-methods exploration of debt and its association with multiple health outcomes and disease biomarkers. The study is divided into 2 phases: a qualitative study of debt experience (phase 1), providing contextual ethnography to situate epidemiological findings as well as inform instrument development for the measurement of debt in subsequent research; and a quantitative phase (phase 2) assessing multiple aspects of individual debt exposure alongside questionnaire measures of mental and physical health and biomarkers of cardiovascular and metabolic disease risk. The National Institute on Minority Health and Health Disparities funded the study. All study activities were reviewed for the ethical treatment of human subjects, and the study was granted approval by the institutional review board of the lead author’s university.

During phase 1, we conducted semi-structured, in-person interviews with 31 people living with debt in the Boston, Massachusetts, neighborhood of Dorchester. The Boston area is ripe for exploration of American financial strain. As a major metropolitan city well known for having one of the highest concentrations of higher education institutions in the country, Boston also has the fourth highest cost of living of major U.S. cities and the seventh most expensive real estate market in the country.30,31 While Boston overall reflects these trends, the Dorchester neighborhood remains relatively accessible and is thus both racially and economically diverse: according to census data, Dorchester is 37% black, 28% white, 14% Latino, and 12% Asian, and it has a median household income of just under $50,000. With more than 92,000 residents, it is also Boston’s largest neighborhood, with residents dispersed among several distinct residential and commercial areas. 32 Educational opportunities also draw students to Dorchester, because it is also home to the only major public university in the city, the University of Massachusetts Boston. This diversity and large student population make Dorchester a particularly interesting site in which to explore the lived experience of debt.

Participants were recruited to the study through advertisements posted in public areas as well as through word of mouth and snowball sampling. Two of the authors (ZD and FS) conducted and digitally recorded our interviews with Dorchester residents in a private room in a university setting. Interviews lasted between 30 min and 2.5 h, with most interviews lasting around 1 h. Participants also completed a brief demographic questionnaire and were compensated $50 for their time, plus reimbursed for travel expenses.

In addition to capturing narratives of residents’ life histories of debt, our interviews narrowed in on key topics to help us to understand the range of different forms of debt that people had incurred, their personal experiences and difficulties with debt, the impact of debt on their everyday lives, and strategies they had for preventing or coping with those impacts. We also asked residents to share with us their broader views on debt, beyond their personal experience, so that we might better understand their philosophical attitudes towards debt. This section of the interview included asking participants to share with us words or phrases they most readily associate with terms like “debt” and “indebted.” The full set of interview questions is available upon request from the lead author. The full research team (2 interviewers and lead investigator) had weekly meetings to discuss the progress of interviews and review interview notes. When the team agreed that data saturation had been reached and no substantially new information was being gathered, 33 recruitment and interviewing were stopped.

All 3 authors participated in the analysis of transcribed interviews. We coded a priori themes determined by the semi-structured interview guide accordingly. Over a series of in-person meetings, the research team discussed emergent themes in the data, including recurrent phrases, concepts, experiences, and behaviors not already captured by the interview guide coding structure. Through a process of iterative discussion, we reached consensus regarding the theme and subtheme structure of the data, and we created a comprehensive codebook. Using this codebook, we tagged and analyzed interview text data using NVivo qualitative software, including tabulating theme and code frequency when appropriate. We analyzed questionnaire data using SPSS software. Means and sample frequencies were calculated as appropriate.

Sample

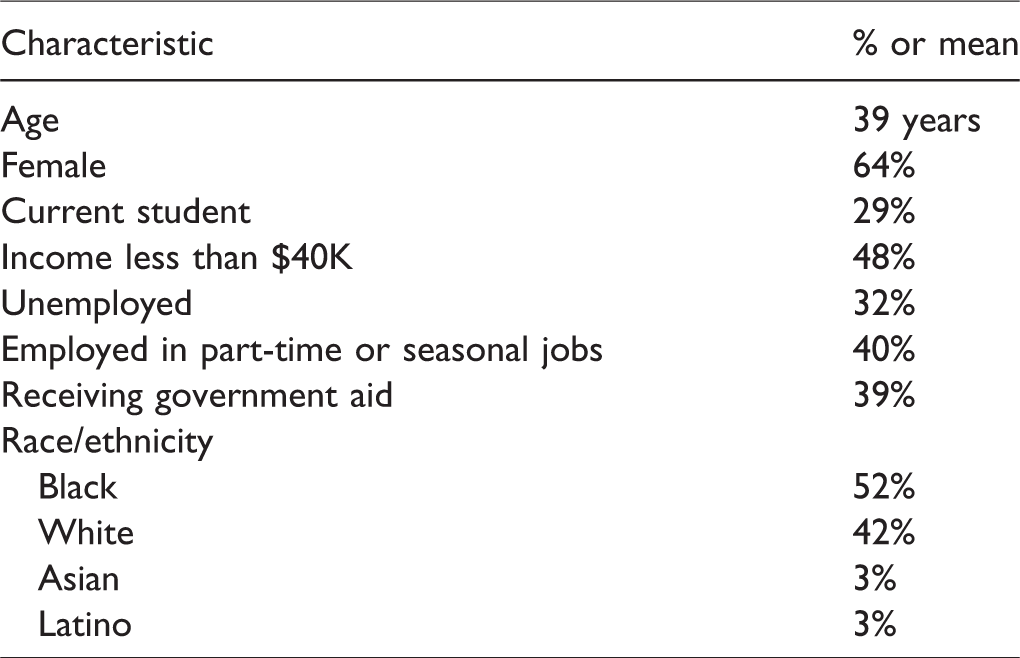

The Dorchester residents we interviewed were quite diverse across a range of characteristics (see Table 1 for summary). Our sample of participants reflects a breadth of ages ranging from 26 to 65 years, with an average age of 39. The diversity in our sample roughly reflects that of the neighborhood; participants were 64% female, 52% black, 42% white, and 3% each Asian and Latino. We aimed to have our sample reflect the experiences of students as well as non-students; 9 of our participants (29%) were current students. As employment status has a most certain impact on debt experience, we also aimed for our study to reflect this variation. Many of the people we interviewed reported struggling to maintain secure employment: 32% were unemployed, and of those with jobs, 40% worked part-time or seasonally. Roughly half of the sample (52%) reported an annual income over $40,000, but incomes varied dramatically, ranging from less than $5,000 to over $150,000.

Sample Characteristics.

The debt profiles of the Dorchester residents we spoke with mirrored national trends in some ways but diverged in others. Not surprisingly, given the expense of the Boston housing market, only 5 of our participants (16%) had ever had a home mortgage. Other forms of debt, especially noncollateralized debt, were much more common. Of these, credit cards were the most common, with 87% of participants having active credit cards and 62% carrying balances. Student loans were the next most common source of debt among our participants: 74% of our participants had student loans, on which they owed $33,000 on average. Beyond these most common forms of debt, participants also reported a number of other sources of debt. Roughly half of the sample (55%) had car loans, and 32% had taken a payday or other short-term loan at some point in their life. Half of the sample (52%) reported having had medical debt, either in the form of unpaid bills or copays, and other expenses charged to credit cards. To contend with their debt burden, a large majority of the sample – 81% – had borrowed money from family or friends.

Qualitative Results and Themes

Embodied Suffering

One of the more robust themes in our interviews was participants’ recurrent mention of the profound impact of debt on their emotional and physical selves. Regardless of the type or source of debt that people carried, participants described their experience of being in debt as encompassing a sense of suffering. More than just feeling stress, participants described emotional and psychological pain that at times extended to their physical bodies and their senses of self. For Lisa, a 29-year-old black woman, her debt deeply altered her sense of possibility in her own future. While in her 20s, Lisa had taken on almost every form of debt possible, with the exception of a home mortgage, but it was her $73,000 in student debt that weighed the heaviest on her and loomed the largest in her life. Lisa described her experience with debt as one of profound grief for the life she felt was lost as a result of it: I was grieving what my life would be like if I didn’t have debt . . . I’ll have the breakdown, I’ll have the tears, I’ll grieve the life I’m hoping I’ll one day have, and I’ll grieve it because I think it’s not going to be possible with all this debt.

This importance of the body as a site of debt experience was further reinforced by the common use of somatic expressions – “locked in, stifled, like I can’t get out”; “like I’m on a treadmill”; “[like being in] a sinkhole, quicksand”; “drowning in debt”; [trying to] “keep your head above water.” Many of these expressions are quite common idiomatic phrases; commonplace enough that at first their appearance in our participants’ debt narratives may seem unremarkable. But idioms reveal important information about shared meaning and experience; they convey cultural understandings and express collectively recognizable experiences of distress, hardship, and suffering. In our conversations, the idioms used to describe indebtedness reinforce that, for many, the burden of debt is experienced as a bodily sensation, not only a socioeconomic position or emotional stressor.

Denying and Using the Body to Manage Debt

In addition to somatic expressions and emotional and physical suffering, Dorchester residents described other ways in which debt intersected with their bodies, including using, denying, and punishing the body in their struggle to deal with or manage their debt. Lisa, who earlier described grieving a life she would never have because of her debt, sought ways to earn extra income to pay her student loans that included the use of her body. Lisa initially took out federal loans to pay tuition for her public college education, but when faced with an unplanned pregnancy she took out additional loans, including private ones, to help pay for living expenses and her new baby while completing her degree. Private student loan companies are notoriously unforgiving and unforthcoming when it comes to negotiating payment plans, 38 and indeed Lisa struggled to pay back the $73,000 in student loan debt she accrued while completing her bachelor’s degree. Even with that degree, at the time of our interview Lisa was unemployed and had decided to sell her body as a pregnancy surrogate to earn money to pay her debts.

While Lisa did not express distress about being a surrogate, her decision to earn extra income through the use of her body highlights one of the many ways in which the burden of debt can have a direct impact on the physical self and the choices people make about their bodies. For others we spoke with, these choices often were a source of distress. Several people described the financial strain of their debt causing them to skip meals, eating only once or twice a day, going without new shoes and clothes when they needed them, or wearing dirty clothes instead of paying for laundry. Others described denying themselves perceived luxuries or nonessential activities because of their debt, and the inner struggle or conflict that this sometimes caused. Pam, a 26-year-old white woman, described her efforts to stay focused on paying her debt at the expense of living a full young life: I get paid every week, and now that I’m getting my bills synchronized and I already have this routine, I feel like I’m getting outside my comfort zone to start paying off my debt. Because I feel like – what am I going to have left over for my recreational use? Which, honestly, I shouldn’t necessarily be thinking that way. But if I just focus on my debt I’m afraid that I’m not really going to have a life. Sometimes I have these moments or stretches of time where I am very disciplined and focused . . . marking every little thing down, to how far I’m going to stretch my food budget so I can set aside an extra $10 to $15 this week, and watch how much electricity I use so the bill isn’t as high. . . . But then I hit a wall and it’s so tiring, and I can’t do this anymore. And then I’ll just say forget it, I’m going to do something nice for myself and spend money I don’t really have or should probably be putting towards paying off a debt or a bill, but I’m just going to do something nice for myself because I feel like I really need to, but then I feel really bad about it . . .

Shame, Guilt, and Personal Responsibility

Feelings of shame, failure, guilt, and irresponsibility were expressed frequently by several of the Dorchester residents we spoke with. We heard sentiments such as “it’s my fault, I should have tried to save” and “I used to feel like I was a bad person because I didn’t pay my debt.” For some, like Tom and Penny, both white and around 30 years old, it was their experiences with persistent debt collection that prompted these feelings. Tom described his experience with debt collectors as making him feel “horrible, like a loser, just like crap. [Like] man I'm such a loser . . . I messed up somewhere in my life.” Penny expressed a similar sense of anguished personal failure: “[You feel] like you failed at life . . . I just want to cry. I feel suffocated. I feel like I can’t breathe. You feel like less of a person . . . ”

Lisa, before accruing the student loans that eventually led her to earn money as a surrogate, also struggled with debt collection early in life. After having surgery to remove a painful ovarian cyst at the age of 19, collections agencies began harassing her for the $9,000 medical bill. Lisa described one particularly traumatic phone call she received while sitting on campus during her first year of college: this is what really made me cry, [when the debt collector asked] ‘why did you have it done when you didn’t have the money or the insurance?’ I remember her telling me that, and I think she was just doing her job. . . . Looking back I should have said ‘who are you to question me about my own health decisions about my reproductive system?’ . . . I just felt terrible. That was the first time I felt that heaviness, like I felt like I did something bad, and I feel like I’m a bad person because I can’t pay this off.

Neoliberal Ideology and Policy

The feelings of shame and failure that our participants brought up also point to the internalization of personal responsibility narratives, which are deeply embedded in neoliberal ideology, as an important component of the impact of debt on well-being and health. The neoliberal agenda, which focuses on freeing property, markets, and individual entrepreneurial actors from regulatory constraints, has at its core the ideals of personal freedom and its corollary – personal responsibility.42,43 As David Harvey 42 describes, these ideals, while “compelling and seductive,” become twisted within the enactment of the neoliberal state apparatus: “The social safety net is reduced to a bare minimum in favor of a system that emphasizes personal responsibility. Personal failure is generally attributed to personal failings, and the victim is all too often blamed.” 42

In the case of consumer debt, the process of neoliberalization and shifting financial responsibility is quite clear. Since the early 1980s, the neoliberal economic agenda has steadily eviscerated the financial security of poor and working Americans. Real wages for all but the top income earners have declined since 1979, while during the same period housing prices have soared and the cost of undergraduate education has risen 1200%. 44 While income inequality has skyrocketed to pre-Great Depression era levels, 45 income insecurity has risen even more dramatically. Data from the Panel Study of Income Dynamics shows that the percentage of American families experiencing a drop in income of 50% or more over a 2-year period has risen sharply – from 7% to 16% since 1970. 46 With the prices of basic needs like housing and education rising and the level, security, and predictability of families’ economic means falling, Americans are increasingly forced to rely on credit as their only available means to make ends meet or provide any financial cushion.

Further conspiring to funnel Americans into indebtedness are neoliberal policies gutting regulatory control of the credit and lending industries. 47 In addition to allowing interest and penalties to be charged with little oversight, this deregulation has also “democratized” credit, 48 extending the reach of certain loan mechanisms to underserved markets. But greater access to credit does not translate into credit equality and instead often functions to expand the divide between rich and poor and between minority and white borrowers. Despite wider availability of mortgage loans, for instance, black homeowners are charged almost half a percentage point higher interest on average for mortgages than whites, even with equivalent credit and debt histories.\cenveospan{48–50} Furthermore, black young adults are more likely to have student debt than whites yet are less likely to complete the degree for which they are paying. 51 In other evidence of credit disparities, low-income families are more likely to have debt from paying for basic living expenses like food and utilities, 52 and poor and minority neighborhoods are more likely to be “unbanked” and served exclusively by predatory, high-interest, payday lenders. 47

These disparities in quality credit and financial options fundamentally reduce opportunities for upward mobility and financial security for many Americans while disproportionally affecting poor and minority households. They also highlight the uncomfortable and often contradictory positions in which individuals often find themselves when making financial decisions, especially when faced with limited resources. As our participants’ narratives illustrate, individuals who are trapped into needing loans to afford basic necessities, including costly medical procedures or education to ensure their economic future, are then susceptible to feeling a sense of personal failure for having made a bad “choice.” Anthropologist Brett Williams 47 has described this twisted and painful irony as the “credit trap.” She aptly observes that “the illusion of choice and our own feelings of complicity hide the fact that debt is embodied domination, that the purpose of consumer credit is to keep you in debt in perpetuity.” 47

Some of the Dorchester residents we spoke with were keenly aware of this credit trap and the unfairness of its accompanying portrayal of indebtedness as a personal or moral failure. As one resident observed: I think when you hear what media say about people and their debt or people not paying their bills or whatever, you always hear the worst stories about people being negligent. And someone not paying their bills is not always them choosing not to pay their bills; a lot of times it’s people making hard choices all the time. And I think that’s important.

Conclusions: Debt and Epidemiology Revisited

Our findings clearly indicate that, in the current neoliberal climate, financial debt is a source of bodily suffering. The general association of debt with suffering, however, has a deeper history. In his opus Debt: The First 5000 Years, David Graeber 54 describes the use of early Vedic religious texts by contemporary theorists seeking to demonstrate the primacy of debt in human social and economic history. As he describes, the 1500–1200 BC Sanskrit texts comprise the earliest writing on debt and lend support to the idea that, preceding money and economy, debt can best be understood through the lens of religion: the nature of life itself is a debt, one we are born into, and payable ultimately to death. Illustrating this point, Graeber states that in the texts, “debt seems to stand in for a broader sense of inner suffering from which one begs the gods . . . for release.” 54 Our findings in Dorchester are quite resonant with this early observation and suggest that in the contemporary neoliberal economy of the United States, debt continues to be a form of profound suffering.

While burgeoning epidemiological studies provide quantitative support for the notion of debt as suffering – through documenting debt as a source of stress and a risk factor for negative emotional and physical health outcomes – they neglect the lived reality of that suffering and the pathways through which it manifests. The stories of the Dorchester residents we spoke with offer a deeper look into the human experience – the “epidemiology of everyday life” – of having debt. Our participants described feelings of deep loss and injury to their senses of self and self-worth. They expressed profound feelings of shame and failure that at times crippled their ability to move forward with their lives. And they pointed to the variety of ways that debt can become written in and on the body as it alters the way they feed, clothe, treat, and perceive their physical selves. Future epidemiological research would be well served by incorporating measures, such as of shame, guilt, and behaviors of bodily denial, that capture this embodied experience. It may well be that these are key pathways through which debt functions as a determinant of health, and data that explicitly speaks to their association with health will do much to further our understanding of debt as a socioeconomic risk factor.

Furthermore, the deep embedding of this debt experience, including its emotional toll and embodied reality, in both ideologies and policies of individual responsibility suggest that neoliberalism plays a key role in the impact of debt on health and well-being. By enforcing socially normative values of personal responsibility, neoliberal doctrine helps to obscure and de-historicize the real political underpinnings of rising inequality and consumer debt, making it appear as though inequitable economic conditions are naturally occurring rather than orchestrated and that individual financial decisions are purely personal and unconstrained.42,43 This kind of historical erasure and naturalization of systems of oppression and inequality has been a consistent strategy in the enactment of the neoliberal agenda, 42 and we suggest that greater attention should be paid to this issue in epidemiological research on debt.

The ways in which researchers employ and describe debt as a variable in their studies can have implications for broader discourses and public understandings of debt. In the same way that uncritical usage of the race concept in biomedicine has contributed to naturalizing that problematic concept,55,56 operationalizing debt as a personal risk factor without acknowledging its political and economic context could encourage popular associations of debt with unfettered personal irresponsibility and failure. This is particularly salient within the context of health, as the body is a powerful site in which discourses of moral authority and behavioral policing are both written and received. In his analysis of the neoliberal context of “lifestyle epidemiology,” Chris Mayes 57 makes a similar point regarding the surveillance of individual behavior in obesity research and public health messaging, in which “the everyday choice of individuals indicates the success or failure of the subject to form a healthy lifestyle.” 58 In the case of debt, if research continues to point to its associated health consequences without critically assessing the origins of indebtedness, it risks a narrative that not only individuals’ life chances but also their bodies and health are at risk from their poor financial decisions.

By further attending to the neoliberal and political economic context of debt, epidemiological research can therefore help to inform public discourses around debt as well as policy. The psychological and bodily suffering of people living in debt offers powerful evidence for needed policy reform. By specifying aspects of credit deregulation, loan forgiveness, mortgage lending, or finance and banking policy that apply to measures of debt being investigated, epidemiological studies linking debt and health could speak more directly to the ways in which their scientific evidence informs relevant debates. We hope to see more researchers engage with this broader and more critical exploration of debt as the burgeoning epidemiology on this topic moves forward.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the National Institutes of Health/National Institute on Minority Health and Health Disparities (Grant #R01-MD00723)