Abstract

Numerous scholars have noted social issues such as inequality and insufficient social capital as limitations of efficiency-oriented neoliberal development strategies. In this context, the Moon Jae-in administration in South Korea declared social value as the core value of the state. Therefore, public institutions are required to prioritize social value. Beyond ideological discussions, these social and policy changes suggest the need for concrete discussions on how to practically realize social value. Public institutions have strengthened their social responsibility, contributing to local communities and low-income groups. However, companies often consider social responsibility a cost, which impedes growth. As public enterprises, a type of public institution, have the characteristics of a company, their inherent goals of profitability or entrepreneurship may be limited by enhancing publicness to realize social value. Therefore, public enterprises face the challenge of realizing social value in a way that benefits both society and business. To devise measures to realize social value by strengthening publicness while ensuring profitability, this study focuses on Creating Shared Value (CSV), which benefits both companies and society. Publicness and profitability, two values that public enterprises pursue, are discussed, and Corporate Social Responsiblilty (CSR) is compared with the CSV perspective, which aims to benefit both. This study devises measures from the CSV perspective for realizing social value in the Korea Expressway Corporation, a public enterprise. Implications for other public enterprises are highlighted.

Points for practitioners

As the need for public institutions to solve social issues has increased, public enterprises face the challenge of realizing social value while ensuring profitability. In this context, this study took the CSV approach and conducted a case study on the Korea Expressway Corporation to present plans for public enterprises to create social value by fulfilling their purpose. By suggesting a process and detailed projects from the CSV perspective, this study will help practitioners to create social value tailored to the characteristics of each public enterprise.

Introduction

Facing social issues such as the extreme imbalance of wealth and a deteriorating sense of community, the Moon Jae-in administration, which began in 2017, declared improving social value to be the core of their national agenda. Accordingly, the administration began to emphasize the realization of social value as the ultimate goal of public institutions with publicness. Emphasis on strengthening public institutions' publicness increased based on the criticism that New Public Management (NPM), a public management ideology rooted in neoliberalism, overemphasizes efficiency. Over the past few decades, NPM, which originated from Western countries, has spread globally as one of the most popular and dominant models of administrative reform. The NPM reform movement effected a paradigmatic change in the conceptualization of the government's role and how it should be performed (Kim and Han, 2015).

As NPM theory is based on two theoretical foundations of managerialism and new institutional economics (Hood, 1991; Rhodes, 1997), the key to NPM-inspired reform is to establish an incentive system that applies the principle of competition and liberates bureaucrats from bureaucratic control under the system, thereby enabling them to work freely as public entrepreneurs. However, even the Organisation for Economic Co-operation and Development (OECD), a long-time defender of NPM, argued that it is a “reform that generated unexpected negative consequences,” and that it is “an outcome from failing to understand that management in the public sector not only delivers and provides public services but also possesses and realizes the value of governance.” Another criticism of the NPM paradigm is the continuous “privatization failure” (Dannin, 2005). In this context, the pursuit of social value has emerged as a new objective for public institutions.

However, among various types of public institutions, public enterprises must work toward entrepreneurship as well as publicness. Therefore, it is necessary to discuss whether social value can be realized while pursuing both values together. In particular, the present study focuses on the Korea Expressway Corporation (KEC), a public enterprise in charge of constructing and maintaining expressways, which is an infrastructure used by all citizens and thus more relevant to people's lives than some other public goods. Moreover, there are few public goods other than expressways for which the two values of entrepreneurship and publicness conflict. For example, although the government had been exclusively responsible for constructing expressways since the 1970s, in the 1990s, public–private partnership was actively adopted with the goal of improving the efficient use of finances. However, differences in tolls depending on whether the operating body was a public or private organization raised questions about fairness. Thus, a policy to reduce tolls on expressways operated by private companies has been adopted to promote publicness. As there is an urgent need to create ways to provide social value without sacrificing economic value, the KEC was chosen as the subject of this study.

Even before social value was actively discussed, many studies were conducted on corporate social responsibility (CSR) among both private and public organizations. Even though CSR investment has sometimes been interpreted as social value realization (e.g. Kim and Kim, 2020), they differ in that social value should be used as a core strategy throughout the policy process (Yoon et al., 2017), but CSR programs have only limited relevance to the business (Porter and Karmer, 2011). However, the concept of social value has not been established academically. Thus, this study examines the concept of social value to achieve the policy goal of social value realization by public institutions. Since understanding social value as CSR may weaken the corporate character of a public enterprise, we adopted the concept of CSV to overcome this limitation. Finally, as public enterprises face the demand to actually realize social value, we developed specific tasks to help other public enterprises facing the same challenges understand and realize social value.

In summary, this study aimed to provide realistic measures based on Porter and Kramer’s (2011) Creating Shared Value (CSV) perspective to realize social value through corporate activities using the KEC as a case study. As CSV is a relatively new concept, it is necessary to increase our understanding of its underlying mechanisms and the ways in which it can be realized (Ilmarinen and Akpinar, 2018). This study not only used CSV as a theoretical framework to achieve the policy goal of helping public enterprises realize the social value that is demanded of them alongside economic value but also identified specific projects for the KEC which provide both types of value. Furthermore, this study analyzed both value types quantitatively, thereby contributing to the realization of CSV in real-world settings. This study's most significant contribution will be the use of the CSV perspective and identification of specific projects to realize actual social value, which could otherwise remain an ambiguous policy goal. Based on the results, we highlight implications for other public enterprises.

Theoretical background

Social value of public enterprises

Emergence and significance of social value

Every era is defined by a particular value type. Whereas “economic value” was the dominant ideology in the era of high economic growth, “political value” defined the era of democratization (Lee, 2019). In the 30 years since democratization, South Korea has achieved a national average income of USD 30,000. However, there has been growing public opinion that a development model focused on economic growth raises issues such as income polarization, unfair competition, major disasters and hinderance of social integration. Thus, there are increasing calls to pursue “social value” to develop communities and promote public interest.

Social value realization was originally required by social enterprises. In public organizations, an emphasis on social value developed owing to the limitations of NPM, which was the mainstream theory of the public sector in the late twentieth century. In this context, the Public Services (Social Value) Act was introduced in 2012 for public organizations in the UK. Accordingly, all local authorities, including the Government of the UK, gained the right and responsibility to consider social, environmental and economic value when selecting a business for the commission of a public service contract of £170,000 or more. After the bill was passed, the role of service providers in procuring public services in the UK was defined as not only creating economic benefits but also enabling service beneficiaries to experience positive results in employment, collaboration and equal opportunities among sectors.

The emergence of the concept of social value in Korean public institutions can be traced to the “Basic Act on Social Value Realization of Public Institutions” proposed by then Representative Moon Jae-in in 2014. The proposed Act contains basic matters necessary to realize social value, including the definition thereof, the responsibilities and roles of public institutions, basic and regional promotion plans, annual implementation plans, a social value committee and social value performance evaluations. Article 3 of the Act defines social value as “values that can contribute to public interest and community development in all areas including society, economy, environment, and culture.” Although this bill did not pass at the time, it was submitted again at the 21st National Assembly in 2020. This proposed Act seeks to enhance publicness in society by considering social values in the process of policy establishment, implementation, and evaluation in public institutions (Lee et al., 2017).

Public enterprises: concepts and approaches

Government corporations, a concept similar to public enterprises, are institutions owned and controlled by the government, and are a legally distinct entities from the rest of the government (Stanton and Moe, 2002). State-owned enterprises are hybrid organization that operate in the market environment but embrace public policy goals in their strategic direction (Johanson and Vakkuri, 2017). 2 Korean scholars have offered various definitions of public enterprises. They have been defined as organizations run by the government in a corporate manner with the aim of promoting public welfare (Won, 2018) and companies in which the government has ownership or the right of control through direct or indirect investments to achieve public goals (Lee, 2009). Kim (2014) emphasizes public ownership in defining public enterprises, which is similar to OECD concepts. Thus, public enterprises can be defined as companies in which the government has ownership or the right of control through direct or indirect investments to achieve public goals, that are also profit-seeking administrative organizations (Yoo, 2012).

Countries use different terms to refer to quasi-governmental organizations or public institutions, and operate separate laws. According to Article 6 of “The Law on the Operation of Public Institutions,” organizations designated as such in South Korea are subject to the management and application of this law. Public institutions are divided into public enterprises, quasi-governmental institutions, and non-classified public institutions. Public enterprises are delineated as market-based and quasi-market-based, and quasi-governmental institutions as fund management-based and commissioned service-based. 3 As of 2020, 340 institutions are identified for management under this law: 36 public enterprises, 95 quasi-governmental institutions, and 209 non-classified public institutions. With the enforcement of the Law on the Operation of Public Institutions in 2007, the Ministry of Economy and Finance currently conducts integrated management evaluations. Indicators provide criteria for evaluating and implicitly guiding the direction of public enterprise management for the evaluated organization. The evaluation categories for public institutions are divided into business management and main businesses (Lee, 2016).

Public enterprises are also classified as a type of policy tool. Public enterprises are used as tools to plan for economic development when the necessary industry is not cultivated because of risk or insufficient capital, are used as tools for income redistribution and welfare policy by supplying essential goods or services at low prices, and may degrade economic efficiency when used as tools for employment policy and job creation to reduce unemployment (Yoon, 1995).

Social value as a policy goal of public enterprises in Korea

By definition, public enterprises possess the characteristics of a “hybrid organization” that pursues both publicness and entrepreneurship/profitability, as Dimock (1961) and Robson (1960) confirm. Mazzolini (1979) proposed a “profit goal” and a “tool goal” as inherent goals of public enterprises, where the profit goal is the expectation of maximum economic performance, and thus profitability, as in normal companies. Moreover, public enterprises function as tools of the government's socioeconomic policies when the government places special demands on them. This makes public enterprises pursue publicness, thereby enabling them to conduct government projects. The share of publicness and profitability pursued by public enterprises is not fixed, but varies with the situation and the institution's characteristics (Mazzolini, 1979). Thus, the value goals of public enterprises may vary according to national characteristics and circumstances.

The main policy at the start of every administration in South Korea has included public institution reform, although policy directions have varied (Lee, 2018). In the late 1990s, the Kim Dae-jung administration (1998–2003) agreed on the need for small government after restructuring consequent to the financial crisis. In the subsequent Roh Moo-hyun administration (2003–2008), the demand for decentralization increased, social conflict intensified, and demand grew for transparency and improved public services. The Lee Myung-bak administration (2008–2013) followed, which aimed to advance public institutions by promoting institutional integrations, privatizations, functional adjustments, and management efficiency. The Park Geun-hye administration (2013–2016) aimed to normalize the role of public institutions. To reduce debt and strengthen the competition system, it introduced debt reduction policies, a performance-based salary system, and a wage peak system. Thus, public institution policies vary over time owing to changes in the policy environment and transitions between conservative and progressive administrations.

In May 2017, among the 100 Policy Tasks, the Moon Jae-in administration selected “To restructure public entities to take the lead in realizing social values,” and included social value as a management evaluation item for these institutions. In addition, there are many policies including the social value realization of public institutions: three proposed laws on realizing social value, management evaluation reform, the job policy roadmap, a comprehensive government innovation plan, public institution innovation guidelines, and a public institution innovation growth plan. Among these, management evaluation is a powerful tool that impacts the operation of public institutions. Evaluation indicators need to be redesigned to place greater weight on social value realization while conducting the companies’ unique business. As shown in Table S1, 4 the item “Social Value Realization” was created through the 2018 Management Evaluation Handbook restructuring plan. In response to the 2018 Management Evaluation, reform and implementation considering social value were required across main businesses and in the operation of entire institutions.

Specifically, strategic planning in the Business Management category requires a balance between social values and efficiency, and a reflection of policy tasks in the planning and implementation of main businesses, thereby leading to the consideration of social value in organization-wide strategic planning.

Realization of social value in public enterprises: tension between publicness and profitability

As mentioned above, the current administration is demanding that public institutions realize social value by strengthening publicness, which is a shift from the promotion of NPM policies, such as corporate management techniques to increase efficiency in the public sector. Therefore, to promote the realization of social value in public enterprises, the publicness of public enterprises must be discussed. From the perspective of the organizational publicness theory, publicness began to be discussed when determining criteria to distinguish between public and private organizations. In this context, public and private organizations are distinguished based on ownership, whereas publicness is understood as government ownership (Dahl and Lindblom, 1953). In contrast, the dimensional approach distinguishes public and private organizations according to the degree of control based on the organization's open system, and interprets publicness as control in this process (Bozeman, 1987; Emmert and Crow, 1988; Perry and Rainey, 1988).

From the core or dimensional approach that understands publicness in terms of government ownership or degree of influence from political authority, the publicness of public enterprises can be judged based on government investment in or influence on them. However, regarding outcomes, from an integrated perspective or normative approach, which understands publicness as the extent to which the public value of goods or services is achieved, the publicness of public enterprises can be measured by the extent to which public value is achieved in the services that an enterprise provides. This can be connected to public value theory, a counter-ideology to NPM theory. Public value theorists Bozeman (2007) and Moulton (2009) contend that the core of publicness comprises values and norms, not the attributes of providers of services. When a public enterprise seeks to achieve social value by understanding its publicness from a public value perspective, the nature of a public enterprise becomes closer to that of a social enterprise, which is at the crossroads of the market, public policies and civil society (Nyssens, 2007). A social enterprise, the primary purpose of which is to pursue social goals and to generate benefits for the society, interprets social value as public value (Bandini et al., 2020). Bandini et al. (2020) also point out that a social enterprise is required to combine two very different objectives of social and financial objectives in fundamental ways. Likewise, a public enterprise is required to realize social value while both publicness and profitability are balanced.

Aligned with an emphasis on the publicness of public enterprises, management evaluation has been implemented to try to strengthen public institutions' social responsibility. Nevertheless, when defining social value realization as CSR only, there is a limitation of increased costs of implementing social responsibility tasks that are not closely related to corporate missions. In this context, this study is interested in deriving strategies and projects that can contribute to both profitability and social value, particularly when conducting the organization’s own business. In their study on the public enterprise K-water, Jung and Park (2020) classified the realization of social value into three categories, with the need to actively perform tasks corresponding to overlapping areas in the society and business categories from the CSV perspective. From this perspective, this study attempts to use Porter and Kramer’s (2011) CSV to derive tasks for public enterprises to realize social value.

Creating Shared Value

Concept: Corporate Social Responsibility vs. Creating Shared Value

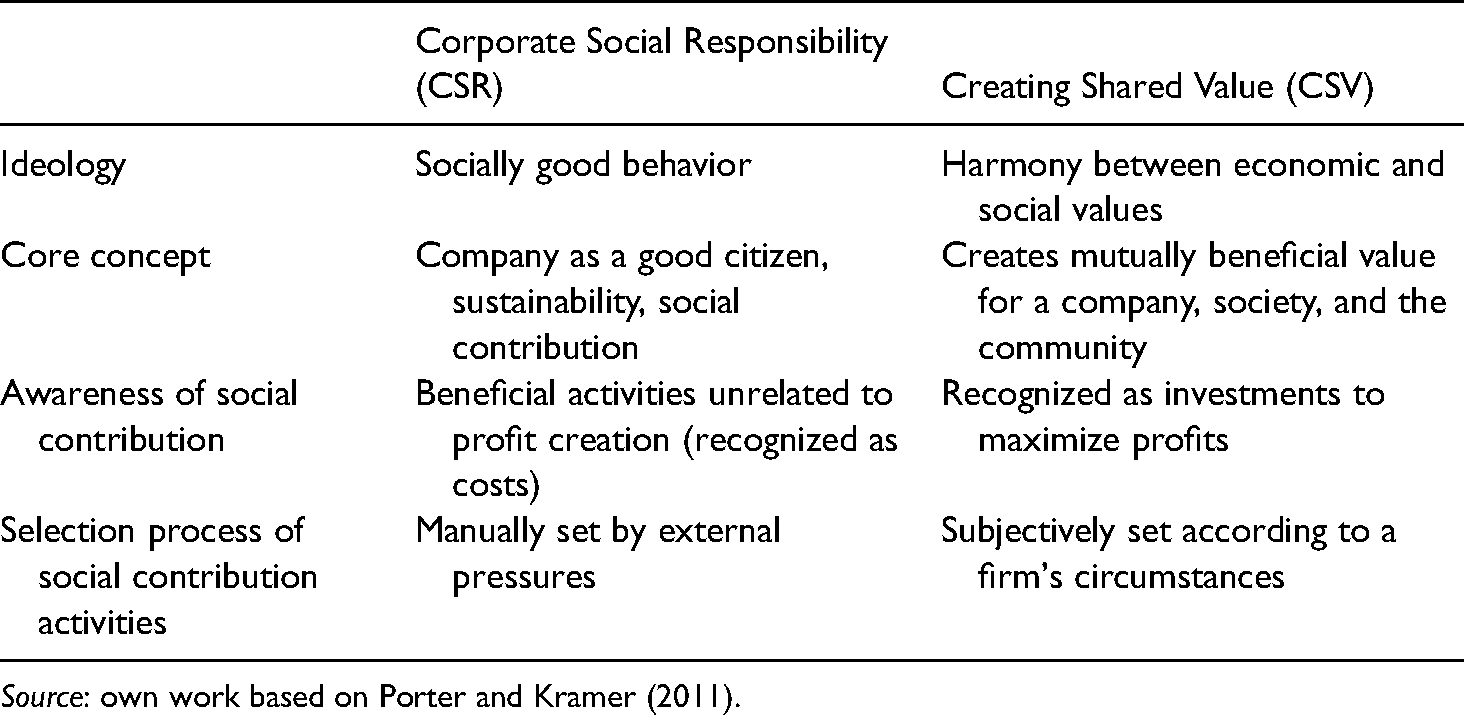

Introduced in 2011 in the Harvard Business Review, CSV developed from a concept of shared value proposed by Porter and Kramer (2006). Comparing CSV and CSR, Porter and Kramer (2011) described the concept of shared value as policies and operating practices that improve a community's economic and social conditions while simultaneously enhancing organizational competitiveness. Unlike CSR, a type of philanthropic action in which existing social contributions are unrelated to the corporate logic of profit maximization, CSV is a new management method that promotes corporate profit while creating shared value through activities that benefit the firm (Porter and Kramer, 2011).

Numerous scholars have defined CSR (e.g. Bowen, 1953; Carroll, 1979; Jones, 1980), and these definitions have been expanded to include perspectives on firms' roles and positions in the social environment, and to consider firms' long-term roles in a dynamic social system, from purely economic to CSR activities and proactive social responsibility (McGee, 1998). Various firms—from small and medium-sized and public to large enterprises—are already actively performing such CSR activities; however, this has been limited by the recent global economic crisis. Since these activities are performed by reinvesting some corporate profits into society, firms perceive CSR as a cost. In response, new management strategies are required. One solution is CSV, which can create economic and social value through profit-seeking activities (Jung and Park, 2020).

Creating Shared Value is based on a firm's participation in solving social problems, and is thus often criticized in terms of its originality and regarded as a part of strategic CSR. However, CSV is a different concept, in that it aims to enhance social contributions as part of a firm's key strategies (Porter and Kramer, 2011; Scagnelli and Cisi, 2014). It is not enough for a firm to become socially responsible by participating in philanthropic activities, as implied by CSR, or take responsibility for environmental and social contribution, as implied by the concept of TBL (Triple Bottom Line). Creating Shared Value is also different from stakeholder management in that it focuses more on creating social and economic value than how such value is distributed among all stakeholders (Ilmarinen and Akpinar, 2018). Furthermore, CSV differs from CSR in that pursuing social value is considered an investment to maximize profits. Whereas a firm's CSR activities are not directly related to its economic activities, CSV activities simultaneously promote corporate profits and address social problems, benefiting both the firm and society. Furthermore, unlike CSR—in which a firm identifies social needs, constructs a new value chain suitable for those needs, and conducts social activities—CSV opens new markets, generates profits, reduces costs, and provides social benefits (Jung and Park, 2020). Table 1 compares CSR and CSV.

Comparison between Corporate Social Responsibility and Creating Shared Value.

Source: own work based on Porter and Kramer (2011).

Activity process (strategy and measurement)

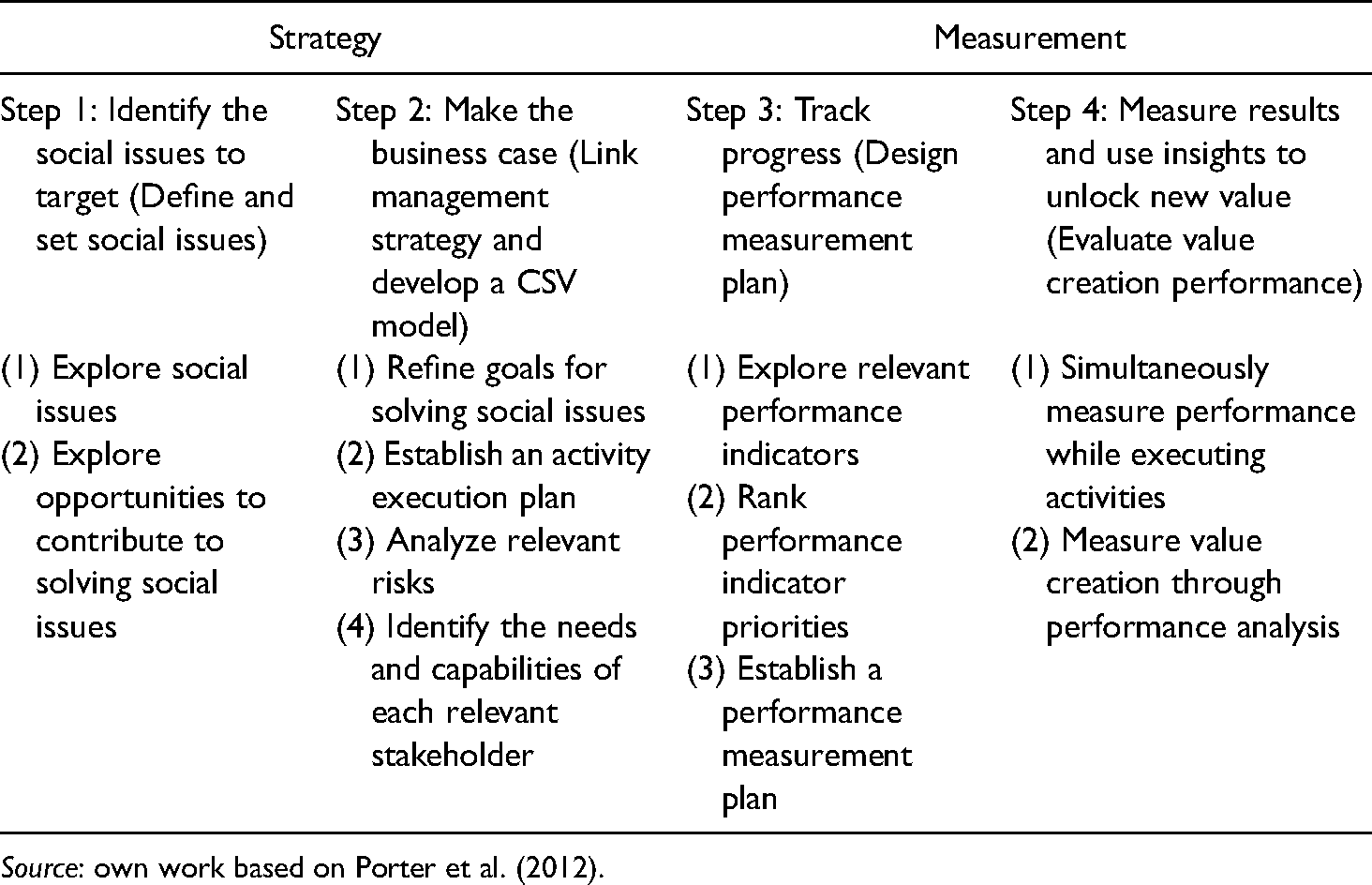

Creating Shared Value activities involve investing in social value that can create and improve economic value. Furthermore, they often increase business performance (e.g. improved sales, productivity, and profitability) through sufficient investment in social value to achieve social performance. Porter and Kramer's CSV strategies include solving social problems by reconceiving products and markets, strengthening social and environmental responsibility by redefining productivity in the value chain, and creating a regional development and cooperation plan through enabling local cluster development.

Creating Shared Value is a cyclical process that involves identification by defining and setting social problems and developing a shared value model, measurement through a performance measurement plan and evaluating the performance of value creation, and discovery of new value from the results. Thus, it must be structured and systemized to enable continuous improvement through a repeated process. Shared value is measured to assess the creation of social and business value. These measurements are used to communicate with management and external stakeholders to create shared value and increase positive influence (Porter et al., 2012). Table 2 outlines the measurement process for an integrated CSV strategy.

Measurement process for an integrated CSV strategy.

Source: own work based on Porter et al. (2012).

Case study: Korea Expressway Corporation

There are previous case studies that show how CSV can be applied to a specific industry or company. For example, Ilmarinen and Akpinar (2018) conducted a case study on relatively small national banks in Finland and examined how and to what extent shared value or social value can be created. The results showed that expanding customer prosperity is the most suitable approach for small banks to take. Additionally, Lee et al. (2014) analyzed the transformation process of the SPC Group, a Korean bakery franchise, from CSR to CSV, with a focus on supplier relationship management.

In Korea, CSV studies have been conducted for public enterprises; however, these previous studies showed some limitations. Kim and Pyo (2018) examined the model and assessment index for social value realization of port authorities (i.e. the main agents managing and operating ports), and presented a quantitatively measurable Key Performance Index focusing on five social value indicators of the management assessment system. Further, they analyzed strategies for implementing the vision, mission, and social value of each port authority as well as stakeholders, through which they presented a social value model for the delivery and purchase of port services based on the business territories unique to port authorities. However, this study merely developed projects that meet the assessment index, without providing a theoretical framework. Lee and Kim (2018) introduced the Korea Electric Power Corporation's CSR activities and presented social participation activities that considered the corporation's characteristics and could be helpful as CSV activities, thereby providing concrete potential projects. Despite the contribution of this previous study, they only conceptually approached CSV and failed to quantitatively measure economic or social value. Jung and Park (2020) conducted a case study on K-water regarding how to turn existing CSR activities into CSV activities as part of the efforts of public enterprises to adapt to the Fourth Industrial Revolution. Their study was significant in that it examined the conceptual difference between CSR and CSV, interpreted the shared value of CSV in the age of the Fourth Industrial Revolution, and set a specific direction for projects. However, they failed to closely examine the economic or social value of these projects. In the present study, to develop practical and feasible ideas from the ideological discussion on realizing social value in public enterprises, we identified social value tasks based on CSV in the KEC. To identify these tasks, we conducted a “social value matching–social value verification–business value verification–CSV analysis of tasks,” as presented in this section.

Essence and business of the Korea Expressway Corporation

Modern Korea's economic growth has been led by the government, and Korea is a typical example of the East Asian developmental state within the theory of developmental states. Public enterprises were widely used as construction agents, especially for infrastructure projects, in the initial development period. The KEC was founded in 1969 by the Korea Expressway Corporation Act, because, as a condition for a loan, the Asian Development Bank demanded the establishment of a public enterprise to construct and maintain the expressways. The KEC performs the duties of a public institution defined by Article 12 of the Korea Expressway Corporation Act. 5

In essence, the KEC's business activities outlined in the Act are to contribute to transportation development through the construction, installation, and management of roads and road-related facilities, to enhance transportation convenience and to contribute to the national economy's balanced development. In addition, the KEC's essential business activities as defined in the Management Policy of their CEO are to contribute to economic development and balanced local development through road construction, to improve competitiveness in the road transportation industry, and to create a safe road environment. Thus, according to the aforementioned Law and policy, KEC's business activities are to create a safe and pleasant road environment through the construction, improvement, and maintenance of expressways, and to drive industrial and economic development and promote the country's balanced development.

Analyzing the KEC value chain confirms its social value and profit creation structure through its support and main activities of planning, designing, constructing, operating, and maintaining expressways, facilities and structures, and auxiliary facilities as shown in Figure S1. 6 Expressway-related activities are primarily conducted through outsourcing and construction contracts, while the planning and construction of “facilities and structures” are basically included in road construction and expansion plans. The “planning–maintenance” processes and the actors and methods of auxiliary facilities vary according to the type of facility and its operation management. Figure S2 shows the process of determining value activities for expressways in detail.

Exploring how to realize social value from the CSV approach

From the CSV perspective, corporate activities should create social value while simultaneously seeking profits. To investigate how to realize social value from the CSV approach, among various methodologies and indicators (Figure S3), this study basically employed 12 value types of the bill for the realization of social value of public institutions (Social Value Act) and mainly used social performance incentives to analyze the social value of tasks.

Social value matching

There are various criteria for defining social value. This study presented those required for public institutions in the proposed Social Value Act and reflected them in the management evaluation to match the social value of the KEC. To identify tasks to realize social value, this study confirmed the promotion background, goals, implementers, specified tasks, implementation methods, period, region, beneficiaries, and expected effects of each of the KEC's existing 70 implementation tasks, and then determined whether they were conceptually related to the 12 social value items defined in the proposed Social Value Act (Figure S4).

Social value verification

The creation of social value was verified by measuring or estimating the performance of social value items identified through social value matching in monetary units. However, if measurement is unsuitable or difficult, it can be verified by applying qualitative judgment criteria.

As illustrated in Figure S5, this study established measurement indicators to assess and manage the KEC's social value performance. These include social performance incentive (SK social performance evaluation) indicators, 7 deduction and input indicators, and the transportation facility investment evaluation guidelines. To verify social value, this study mainly used social performance incentive indicators, which are measured according to four monetary value criteria: social service performance, employment performance, social ecosystem performance, and environmental performance. When measurement was inappropriate or difficult, qualitative criteria or transportation facility investment evaluation guidelines were applied.

Business value verification

To verify the creation of business value, improved business performance based on increased sales, income, and size, and improved operation, procurement, efficiency, and profitability can be measured using direct and proxy indicators (Figure S6). Of the indicators that measure improved profitability (e.g. return on equity, accounting profit, operational efficiency, and business feasibility evaluation), this study used the present value of free cash flow. Free cash flow enables a monetary value measurement, reflects capital value and fluctuations in profitability, and allows for easy measurement and comparison of each period's generated profits. Thus, it was deemed to be an appropriate business value creation indicator in the present study.

Identification and analysis of CSV tasks

As the final step, this study assessed the tasks' suitability, expansion, reproduction, growth, and sustainability to determine whether they were aligned with the essence and purpose of the business and had scale and sustainability. The CSV tasks were thus identified and selected.

As shown in Figure S7, Step 1 was confirming whether the CSV task satisfies the KEC's essence and purpose. To be a representative task, in the shared value suitability metric verified through four items, at least one item must be aligned with the company's essence and purpose. In Step 2, it was confirmed whether the CSV task's value creation mechanism would sufficiently grow through expansion and reproduction, and determined if its scale or potential to grow to such a scale would be suitable for the KEC. It was then confirmed whether the task's potential scale of CSV satisfied the condition of at least KRW 1 billion (USD 0.8 million) per year, based on which it could become a representative task. Finally, Step 3 evaluated the sustainability of the shared value created through the task. For the KEC to invest in and manage it as a representative task, its value creation must last for at least three years.

Through the abovementioned process, a group of representative tasks for CSV in the KEC were selected, as shown in Figure S8. For example, as shown in Figure S9, the KEC could generate profits through its rental business by renting spaces in rest areas, which could be used as a platform to create social value by supporting the growth of social enterprises and creating jobs for disadvantaged groups. The KEC's revenue would then increase alongside sales in line with the growth of these social enterprises, and consequently, rent reduction would not become a cost for the organization.

Figure S10 provides a more detailed explanation of the process by which social and economic value are derived by focusing on the task of “the autonomous cooperative driving test-bed and technology venture center project” for social value realization.

Discussion

Corporations worldwide are currently facing strong public demands to take on social roles. However, according to Utting and Margues (2013), little research has been conducted on the social responsibility of public organizations, and there has been a lack of theoretical and practical basis in the studies that have been conducted. In light of this situation, this study, which focused on how public enterprises could achieve social value by applying the CSV framework, has significant academic and practical implications. For example, this study presented “profit generation through rent” as a business project that the KEC could implement to create economic value as well as encourage growth and job creation in social enterprises. This task could be classified as a case of Porter and Kramer's concept of “reconceiving products and markets,” and followed their measurement process for an integrated CSV strategy. First, job creation would be defined as a social issue to which the KEC could contribute by launching a new project to lease empty spaces at rest stops. Then, the KEC would measure and compare the two value types with regard to the benefits and costs. The research findings of CSV case studies could be benchmarked by public enterprises that need to secure economic feasibility.

Conclusions and implications

To address imbalances and create an inclusive society, social value is emphasized in Korean society, and public institutions are required to strengthen their publicness. However, when public enterprises focus on publicness, a conflict may arise between social and economic goals. Consequently, public enterprises must realize social value while maintaining entrepreneurship and managing corporate sustainability. Accordingly, this study employed the concept of CSV, in which a firm pursues economic and social values simultaneously, to identify measures by which public enterprises could strengthen publicness in a practical manner.

From the CSV perspective, this study identified tasks for the KEC that would satisfy social and business values. The findings show that CSV related to the KEC's mission, vision, and strategic goals can maximize shared value in terms of publicness/public interest and efficiency/profitability through the synergy of creating social and economic value. First, the value chain based on the KEC's business can simultaneously generate economic and social value for the public, small and medium-sized enterprises, the socially underprivileged, and local residents, while also promoting business expansion. Businesses that create economic and social value can interact to expand CSV through these sustained efforts. While social value creation may temporarily reduce the KEC's profits, it would enhance publicness and profitability over the long term. The KEC could achieve sustainable CSV by building a foundation for it, institutionalizing and commercializing CSV tasks, and devoting efforts to sustainable growth. Representative CSV tasks were selected if the following three criteria were satisfied: relevance to the essence and purpose of the KEC, suitability of scale, and value sustainability.

This study is significant as it defined the realization of social value by public enterprises, an under-researched topic, as “based on the institution's business.” Furthermore, it investigated how to accomplish CSV based on the KEC's core assets and platforms of the KEC. Finally, it proposed a plan to maximize utilization value by developing a CSV task selection process based on available platforms, such as rest areas, which are rare, non-imitable, and non-movable assets possessed by the KEC. The results of this study are expected to help public enterprises design and execute individual businesses that create social value and fulfill their purpose while pursuing entrepreneurship and publicness in harmony.

Although demands have been placed on firms to realize social value, this has often been understood as CSR. However, as CSR is perceived as a kind of cost, CSV is presented as a new method for social value realization. This can be seen in the case presented for in the KEC. In 2012, the KEC held a ceremony proclaiming their intention to become a CSR leader, and donated bloodmobiles to the Korean Red Cross. To ensure green management, KEC also decided to produce wood pellets by planting 240 thousand Italian poplars along 15 closed expressways. However, these were not exactly CSV projects. The CSV projects introduced in this study demonstrate the ability to create economic value in addition to social value. This specifically has managerial implications for social value realization from a CSV perspective. Furthermore, this extends previous CSR-based public institution policies, such as strengthening social responsibility and emphasizing ethical management.

This was a single case study and thus had limitations in generalizing the results to other public institutions or countries. However, it can lead to more research on public enterprises with both publicness and profitability that utilize CSV, which will help to discover the limitations of CSV theory and establish more practical and realistic methods to apply it to on-site operations. Further research can be conducted to assess the economic and social value creation effects of the CSV projects presented in this study, thereby identifying and potentially overcoming the academic and practical limitations of CSV theory.

Supplemental Material

sj-docx-1-ras-10.1177_00208523211029765 - Supplemental material for Social value in public enterprises from the perspective of Creating Shared Value (CSV): The case of the Korea Expressway Corporation

Supplemental material, sj-docx-1-ras-10.1177_00208523211029765 for Social value in public enterprises from the perspective of Creating Shared Value (CSV): The case of the Korea Expressway Corporation by Yongwon Kim and Hyeon-joung Kim in International Review of Administrative Sciences

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This work was supported by the Korea Expressway Corporation Research Institute.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.