Abstract

Administrative burden has emerged as a critical lens for understanding the unintended consequences of public service delivery and regulatory practices. While the concept has been extensively applied to analyze citizen–state interactions, less attention has been paid to how administrative burden affects private actors. This study addresses this gap by extending administrative burden theory to the domain of public–private partnerships, with a focus on how “one matter initiatives” in developing countries can alleviate regulatory barriers. Drawing on firm-level data from the World Bank Enterprise Survey, we examine whether and how streamlining governance reduces administrative burden and improves the regulatory climate. The empirical results show that streamlining governance significantly reduces administrative burden and enhances the regulatory climate. These effects are more pronounced for small and medium-sized enterprises, underscoring the reform's distributional impact. Mediation analysis shows that administrative burden serves as a key mechanism through which reform initiatives influence business perceptions of government performance. The findings highlight the relevance of administrative burden theory in non-Western governance contexts and demonstrate the value of incorporating business perspectives into public administration research. By offering empirical evidence from China’s “One Matter Initiative”, this study contributes to a more global and nuanced understanding of how streamlining governance can foster a more enabling environment for enterprise development.

This study highlights that streamlining administrative procedures through initiatives like China’s “One Matter Initiative” significantly reduces administrative burden. For practitioners, the findings suggest that procedural simplification can effectively improve public–private partnerships, particularly in non-Western governance systems. Focusing on service coordination and reducing transaction friction is key to responsive and business-oriented public administration.

Megacity Governance in China shows how reform-driven streamlining governance can reshape regulatory practices. The “One Matter Initiative” demonstrates that reducing administrative burden is not only a technical efficiency but also a strategic step toward building good city governance. For practitioners, the key lesson is that coordinated service delivery and burden reduction carry broader significance: they reinforce city governance capacity and offer a replicable model for reform in other contexts.

Keywords

Introduction

Governments around the world are under growing pressure to simplify regulation and reduce procedural complexity. As public administration research increasingly recognizes, governance is not experienced solely through laws or institutional forms, but through everyday interactions with administrative systems (Secchi et al., 2024). The design and delivery of procedures for how policies are implemented has emerged as a central dimension of compliance and performance (Baekgaard, Halling and Moynihan, 2025b; Ferraioli, 2025; Martin, Delaney and Doyle, 2024).

This paper engages with a growing body of scholarship that frames bureaucratic procedures as central mechanisms of governance, focusing specifically on the context of China. Recent reform efforts, especially the “One Matter Initiative” (gaoxiao ban cheng yi jian shi), have aimed to streamline interdepartmental processes and deliver unified, time-bound services for enterprise users. This initiative represents a proceduralist approach to governance transformation (Liu and Wei, 2024), which reengineers service chains without altering formal legal authority. China's reform efforts provide a distinct model of institutional innovation in a non-Western (Chen et al., 2023; Li and Chen, 2024), high-capacity state. A salient example is China's “One Matter Initiative”, which restructured business start-up procedures. Prior to the reform, new firms had to approach multiple bureaus separately for licensing, tax registration, social insurance, and utility connections (Li and Wang, 2023; Liu et al., 2022), each with distinct documentation and timelines. The reform integrated these requirements into a single digital portal with unified documentation, standardized checklists, and a joint time limit. This illustrates a broader shift from reducing the number of regulations (formal deregulation) to redesigning procedural architectures so that regulatory requirements are coordinated and delivered as one matter (Chun et al., 2023; Ma and Christensen, 2020).

Although administrative burden theory has traditionally focused on citizen-facing welfare programs, recent research suggests that corporations too encounter significant procedural frictions that affect their perceptions of state competence and fairness (Giannella et al., 2024). This study builds on this insight by examining how procedural streamlining initiatives affect corporations’ perceptions of the regulatory environment in China. More specifically, we address a second, underexplored gap in the literature: the causal mechanisms linking administrative reforms to institutional perceptions. Few have modeled how burden mediates the relationship between procedural reforms and perceived regulatory quality.

To fill these gaps, this study develops and tests a three-path conceptual model using corporation-level data from the World Bank China Enterprise Survey. The empirical strategy applies multi-equation regression and mediation models to examine how streamlining governance affects perceived administrative burden and institutional trust among corporations operating across different sectors and regions.

In response to ongoing debates about administrative burden and public–private partnerships (PPP), this study sets out to examine how the Chinese “One Matter Initiative” reduces administrative burden and enhances corporations’ perceptions of the regulatory climate. It seeks to: (1) to develop a conceptual framework that links governance streamlining to the experience of regulatory interactions at the corporation level; (2) assess the mediating role of administrative burden in explaining how procedural reforms influence corporations’ regulatory evaluations; and (3) explore whether these effects vary by corporation characteristics, particularly size and age. These objectives aim to fill important gaps in the literature on administrative burden and public sector reform, particularly in non-Western and transitional contexts.

This study offers three contributions. First, it theoretically extends the administrative burden into the domain of public–private interactions, addressing calls to conceptualize corporations as key actors in governance systems. Second, it operationalizes the “One Matter Initiative” using real-world procedural indicators, capturing granular variation in public–private partnerships. Third, by grounding the analysis in a non-Western, developing-state context, it contributes to the diversification of administrative burden research, which remains heavily Western-centric in both geography and service orientation.

Literature review and hypotheses

Public–private partnerships and administrative burden

Public–private partnerships have emerged as a widely adopted governance model in both advanced and developing economies (Witt et al., 2023). Rooted in the logic of new public management, PPP frameworks are premised on the assumption that public goals can be more efficiently achieved through the integration of private sector innovation (Fleta-Asín et al., 2020; Koppenjan et al., 2022; Liu et al., 2020). This collaborative model has expanded beyond infrastructure delivery to encompass a range of regulatory and service-oriented domains (Casady et al., 2020). While public–private partnerships are designed to leverage private sector capabilities in achieving public objectives (Rosell and Saz-Carranza, 2020), their effectiveness often hinges on the procedural interfaces that govern corporation–state interactions (Pimenova, 2025). Understanding how administrative burden operates within PPP arrangements is essential to evaluating their institutional performance (Koppenjan et al., 2022; Schomaker, 2020). This paper adopts such a perspective, positioning administrative burden not as a peripheral cost but as a central dimension of public–private governance quality.

Administrative burden consists of three core dimensions: learning costs, compliance costs and psychological costs (Tiggelaar and George, 2025), originally conceptualized in citizen-facing welfare settings (Baekgaard et al., 2025a). In this study, administrative burden is treated as a relational and perceptual outcome shaped by the design of governance procedures. Empirical evidence shows that the procedural design of the state can impose significant burdens on businesses (Gilad and Assouline, 2024; Stanica et al., 2022). Studies have demonstrated that procedural complexity erodes corporations’ confidence in the regulatory climate (Chudnovsky and Peeters, 2022). In contrast, corporations operating in jurisdictions with more streamlined governance report higher satisfaction with regulatory enforcement (Giannella et al., 2024). When applied to the domain of public–private collaboration, administrative burden appears as a central determinant of procedural legitimacy (Baekgaard and Madsen, 2024). By analyzing how corporations interpret and respond to regulatory processes, especially in high-intervention contexts like China's “One Matter Initiative,” this study conceptualizes administrative burden as a relational outcome produced by the design and delivery of governance itself. This integrative perspective links the promise of PPP efficiency with the realities of procedural navigation, offering a framework for understanding how streamlined governance conditions institutional outcomes in collaborative public administration.

To enhance analytical clarity and align each hypothesis with its specific theoretical context, this study distributes the four hypotheses across subsections of the theoretical framework. Each hypothesis corresponds to a distinct causal pathway, reflecting different dimensions of how the Chinese “One Matter Initiative” influences administrative burden and regulatory climate. This structure allows for more targeted explanations and facilitates clearer empirical testing in subsequent sections.

Streamlining governance and China’s “One Matter Initiative”

Streamlining governance refers to the simplification, integration, and rationalization of administrative procedures to reduce administrative burden. It seeks to minimize transactional frictions and improve regulatory responsiveness. Within the context of PPP, streamlining governance is particularly vital, as the effectiveness of these collaborative arrangements hinges on predictable and efficient interfaces between corporations and state agencies.

The “One Matter Initiative” exemplifies an ambitious effort to streamline governance at scale. Launched as a central component of the digital government agenda (Chun et al., 2023), the initiative seeks to consolidate fragmented approval processes into unified with a single application (Tsai-Lin et al., 2021). Rather than altering formal legal mandates or agency jurisdictions, the reform operates through procedural innovation such as redesigning cross-departmental sequences and standardizing documentation. The relevance of the “One Matter Initiative” to PPP frameworks lies in its direct impact on administrative burden (Wang and Ma, 2022). By streamlining interactions across tax, permit, and infrastructure domains, the reform aims to alleviate learning costs, compliance costs and psychological costs that typically hinder productive engagement in public–private ventures. Furthermore, it redefines the procedural boundaries through which corporations interpret the state's regulatory climate, moving beyond symbolic performance indicators to measurable gains in procedural efficiency.

Hypothesis 1 centers on the foundational relationship between streamlining governance and perceived administrative burden. Drawing on the core logic of the Chinese “One Matter Initiative,” this hypothesis posits that simplifying procedures, integrating service windows, and clarifying regulatory responsibilities will significantly reduce the subjective burden experienced by enterprises when interacting with government authorities. Prior studies suggest that the perceived costs of compliance are shaped not only by regulatory intensity but also by administrative complexity and fragmentation. In line with this perspective, H1 aims to test whether institutional efforts to streamline governance structures are effectively lowering the time, effort, and uncertainty involved in navigating government services.

Hypothesis 2 builds on the conceptual assumption that administrative burden operates as a significant determinant of how corporations perceive the overall regulatory climate. When corporations encounter excessive paperwork, opaque procedures, or redundant approval processes, they are more likely to form negative assessments of the government's responsiveness and regulatory competence (Xian et al., 2021; Yee and Liu, 2021). Prior research has emphasized that administrative burdens not only hinder compliance but also erode trust in regulatory institutions and diminish corporations’ perceptions of procedural justice (Herd and Moynihan, 2025). Hypothesis 2 therefore posits that lower levels of perceived burden should be associated with more favorable assessments of the regulatory climate, particularly in environments undergoing institutional reforms.

Hypothesis 3 advances the argument by positioning administrative burden as a mediating mechanism between streamlining governance and corporations’ regulatory perception. While institutional reforms such as the Chinese “One Matter Initiative” are designed to improve the business environment, their effects on corporations’ perceptions may not be direct. Instead, these reforms may first reduce the procedural and cognitive costs that corporations face, which in turn shapes their evaluation of the regulatory environment. This hypothesis aligns with the broader literature on policy implementation and street-level bureaucracy, suggesting that structural reforms must be experienced at the operational level to produce meaningful perceptual change (Ferraioli, 2025). Hypothesis 3 thus tests a core causal pathway through which governance reforms translate into corporation-level outcomes.

These hypotheses capture the idea that governance reforms aimed at simplifying procedures are not automatically translated into improved regulatory environments. Rather, the pathway runs through the experience of burden: only when corporations perceive a reduction in their cognitive, procedural, and emotional costs does the institutional climate appear more transparent, predictable, and supportive.

Heterogeneity of administrative burden

While administrative burden is a pervasive feature of governance, its impact is not uniform across all corporations. Organizational characteristics significantly shape how burden is experienced and ultimately translated into perceptions of the regulatory climate (Baekgaard, Halling and Moynihan, 2025b). This heterogeneity is especially salient in transitional and decentralized regulatory contexts, where formal procedures are often implemented unevenly across regions and sectors (Mikkelsen, Madsen and Baekgaard, 2024). Larger and more mature corporations typically possess greater administrative capital and established networks for resolving disputes. Smaller and younger corporations are disproportionately affected by procedural burdens owing to limited internal resources and weaker bargaining power (Martin, Delaney and Doyle, 2024).

While the “One Matter Initiative” campaign aims to provide equal access to streamlined procedures, in practice, larger corporations often benefit first owing to their proximity to government service hubs or their political-economic embeddedness. Smaller corporations, especially those in peripheral regions or informal sectors, continue to face higher transaction costs in dealing with public authorities. Given these patterns, we hypothesize a conditional relationship between administrative burden and regulatory climate:

Methodology

Mediation model specification

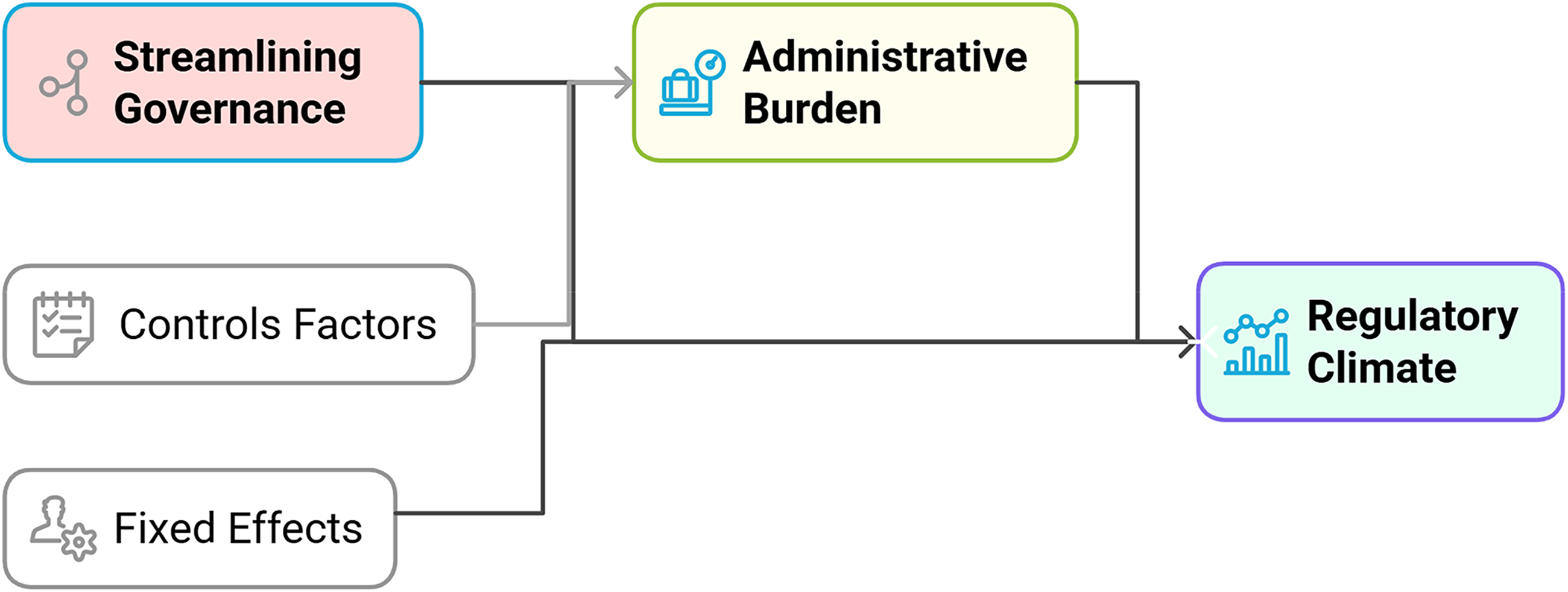

To empirically test the proposed hypotheses, we employ a two-step regression strategy to examine both the direct effects of the “One Matter Initiative” and the mediating role of administrative burden. The analysis begins by estimating the effect of streamlining governance on two outcome variables: perceived administrative burden and the regulatory climate. Subsequently, we assess whether administrative burden serves as a mediating mechanism linking reform efforts to regulatory perception. This study applies a multi-equation linear modeling strategy to empirically examine how streamlining governance shapes firm perceptions of the regulatory climate. Figure 1 is the mediation empirical model that guides this study.

Empirical analysis model.

The central proposition is that streamlining governance alters the way administrative procedures are organized and delivered. By consolidating multiple approvals into an integrated workflow, streamlining reforms are expected to reduce administrative burden. Lower administrative burden, in turn, contributes to improvements in the regulatory climate, since firms perceive fewer obstacles, lower transaction costs, and more predictable interactions with government. The framework also allows for a direct effect of streamlining governance on regulatory climate, beyond the mediating channel of administrative burden. This acknowledges that procedural integration may shape firms’ perceptions not only by reducing burdens but also by signaling government capacity, policy stability, and institutional reliability. In addition, a set of firm-level control variables and industry and region fixed effects are incorporated to account for heterogeneity. These controls ensure that the observed relationships capture the impact of streamlining reforms rather than background structural factors.

Firm-level dataset and variables

This study draws on firm-level data from the World Bank Survey (https://www.worldbank.org/businessready/data). The China round covers 2189 private sector establishments, including both fresh interviews (n = 1972) and panel follow-ups (n = 217), making it the largest enterprise-level institutional diagnostic dataset currently available for China.

The survey employs a stratified random sampling design with three stratification criteria: industry sector (manufacturing and services, following ISIC Rev.4 codes), corporation size (small, 5–19 employees; medium, 20–99; large, 100–269; very large, 270+), and geographic region (six macro-regions: North, Northeast, East, Central, Southwest, and Northwest). The sample frame was constructed using data from the National Bureau of Statistics of China as of November 2023, and stratification ensured representativeness across all major sectors and corporation types.

Variable measurement

To empirically examine the impact of streamlining governance on corporations’ perceptions of the regulatory environment, mediated by administrative burden, we constructed a set of theoretically grounded variables based on the China Enterprise Survey administered by the World Bank. Table 1 summarizes the key variables used in this study, including the main explanatory, mediating, and outcome measures, as well as a set of corporation-level controls.

Variables and measures.

Source: Prepared by the authors.

This study conceptualizes streamlining governance as the simplification and integration of government procedures that firms must navigate when seeking public services such as permits, licenses, and utility access. In line with the logic of China's “One Matter Initiative,” the focus is reducing regulatory stringency per se and minimizing redundant steps and procedural opacity that impose costs on users. Drawing from administrative burden theory, we view streamlining as a procedural reform aimed at alleviating learning, compliance, and psychological burdens by reengineering how firms experience and interact with government systems. The explanatory Streamlining Governance is operationalized through four perceptual indicators: (1) permit process intensity; (2) tax contact frequency; (3) trade procedure exposure; and (4) infrastructure coordination. Each item captures a specific dimension of public–private partnerships that reflects procedural clarity. Respondents were asked to rate the extent to which each domain constituted an obstacle to their corporation's operations, using an ordinal scale ranging from “No obstacle” to “Very severe obstacle.” To ensure conceptual clarity and internal consistency, all component indicators are coded such that higher values consistently reflect a greater degree of streamlining governance. These indicators are then standardized and aggregated into a composite index using principal component analysis. While the items are statistically distinct, they share a unifying conceptual logic: each captures a dimension of how much effort firms must expend to complete a typical regulatory task. This proceduralist lens aligns with the broader administrative burden literature, which highlights the cumulative effects of seemingly small frictions on perceived institutional fairness and efficiency.

The mediating variable, administrative burden, is measured along three dimensions as well: (1) perceived permit burden; (2) perceived tax administrative procedure; and (3) perceived tax burden. These measures are designed to capture the perceived difficulty or friction corporations experience when engaging with government procedures, particularly in licensing and taxation. The outcome regulatory climate is proxied through corporation-reported perceptions of three critical governance challenges: (1) perceived corruption barrier; (2) perceived policy instability; and (3) perceived judicial inefficiency. These items reflect how institutional weaknesses shape the overall regulatory environment in which corporations operate. All three are measured as perceived obstacles to doing business and interpreted as indicators of broader regulatory predictability and trust in formal institutions.

Statistical findings

Descriptive statistics and correlation analysis

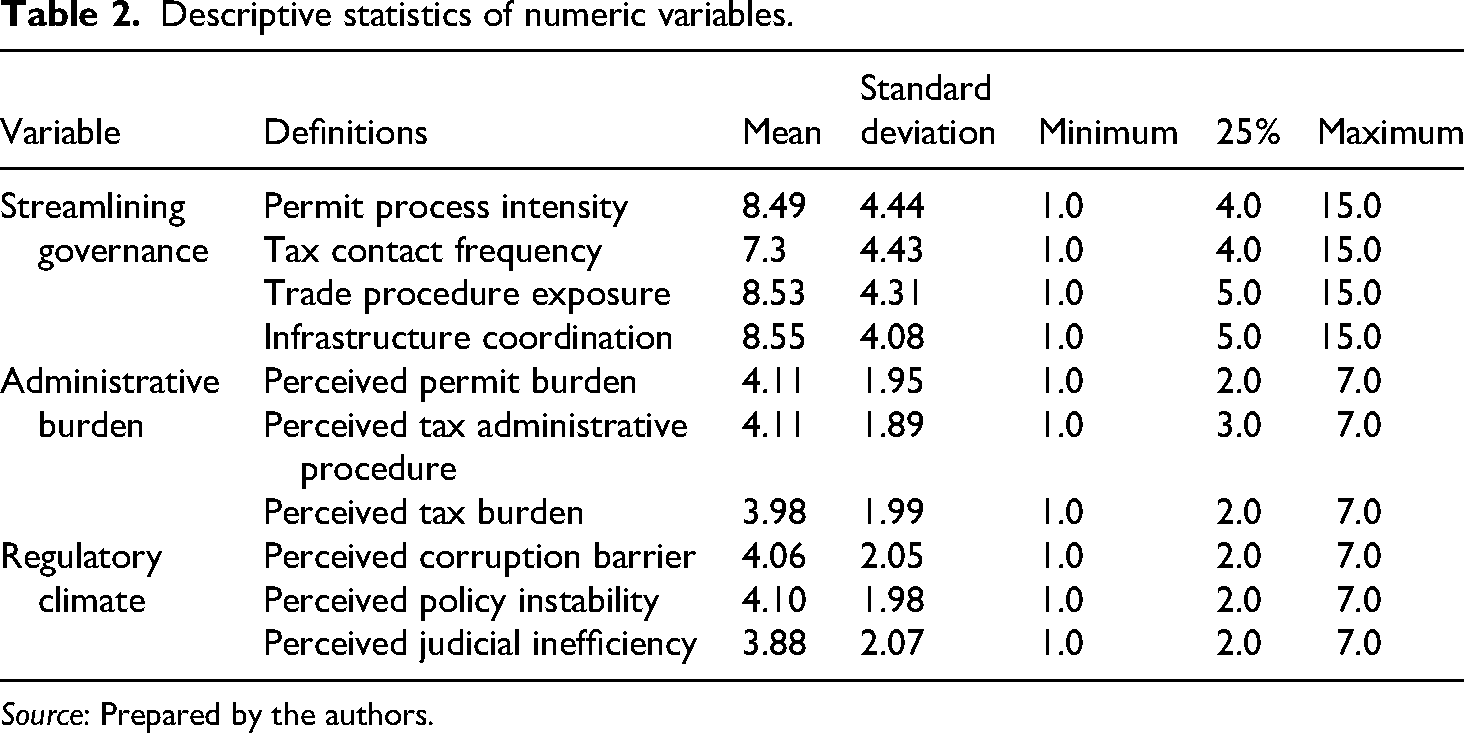

To provide an overview of the sample characteristics and to establish a foundation for subsequent analysis, we begin by presenting the descriptive statistics of the key numeric variables used in the regression models. Table 2 summarizes the central tendencies and distributional properties of these variables.

Descriptive statistics of numeric variables.

Source: Prepared by the authors.

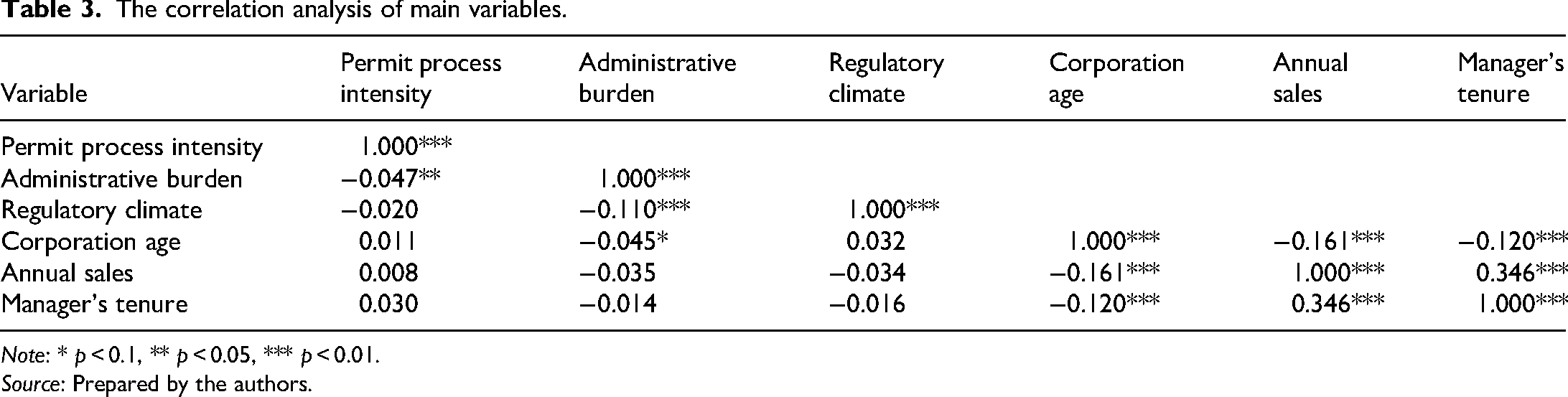

The variable Permit Process Intensity, our main explanatory measure of streamlining governance, has a mean of 8.49, with a standard deviation of 4.44, and ranges from a minimum of 1 to a maximum of 15. The mediating variable administrative burden captured through corporations’ perceived tax administrative procedure has a mean of 4.11 (SD = 1.89), with values ranging from 1 to 7. Notably, the distribution is slightly more right-skewed, as the 75th percentile reaches 3. Table 3 reports the Pearson correlation coefficients among the principal variables used in the empirical analysis.

The correlation analysis of main variables.

Note: * p < 0.1, ** p < 0.05, *** p < 0.01.

Source: Prepared by the authors.

All coefficients are calculated using a balanced sample of observations enterprise survey, with significance levels denoted at the 10, 5, and 1% thresholds. The matrix provides an initial overview of the direction and strength of associations between the explanatory, mediating, and outcome variables, as well as key controls. Permit process intensity is negatively correlated with administrative burden (r = –0.047, p < 0.05), suggesting that streamlining efforts in permit-related procedures are modestly associated with lower perceived burdens. Although the magnitude of the correlation is small, its significance supports the notion that procedural improvements may have broader administrative spillovers. The relationship between administrative burden and regulatory climate is also negative and statistically significant (r = –0.110, p < 0.01), indicating that corporations facing greater administrative complexity are more likely to report institutional unpredictability. This correlation aligns with the theoretical expectation that burdensome administrative systems can erode trust in the formal institutional environment. Permit process intensity itself is only weakly and insignificantly associated with regulatory climate (r = –0.020, not significant), suggesting that the relationship may be indirect.

Regression and robustness

To examine the relationship between streamlining governance and corporations’ perceptions of the regulatory climate, we estimate a series of ordinary least squares regression models. Table 4 presents the baseline results as well as a set of robustness checks.

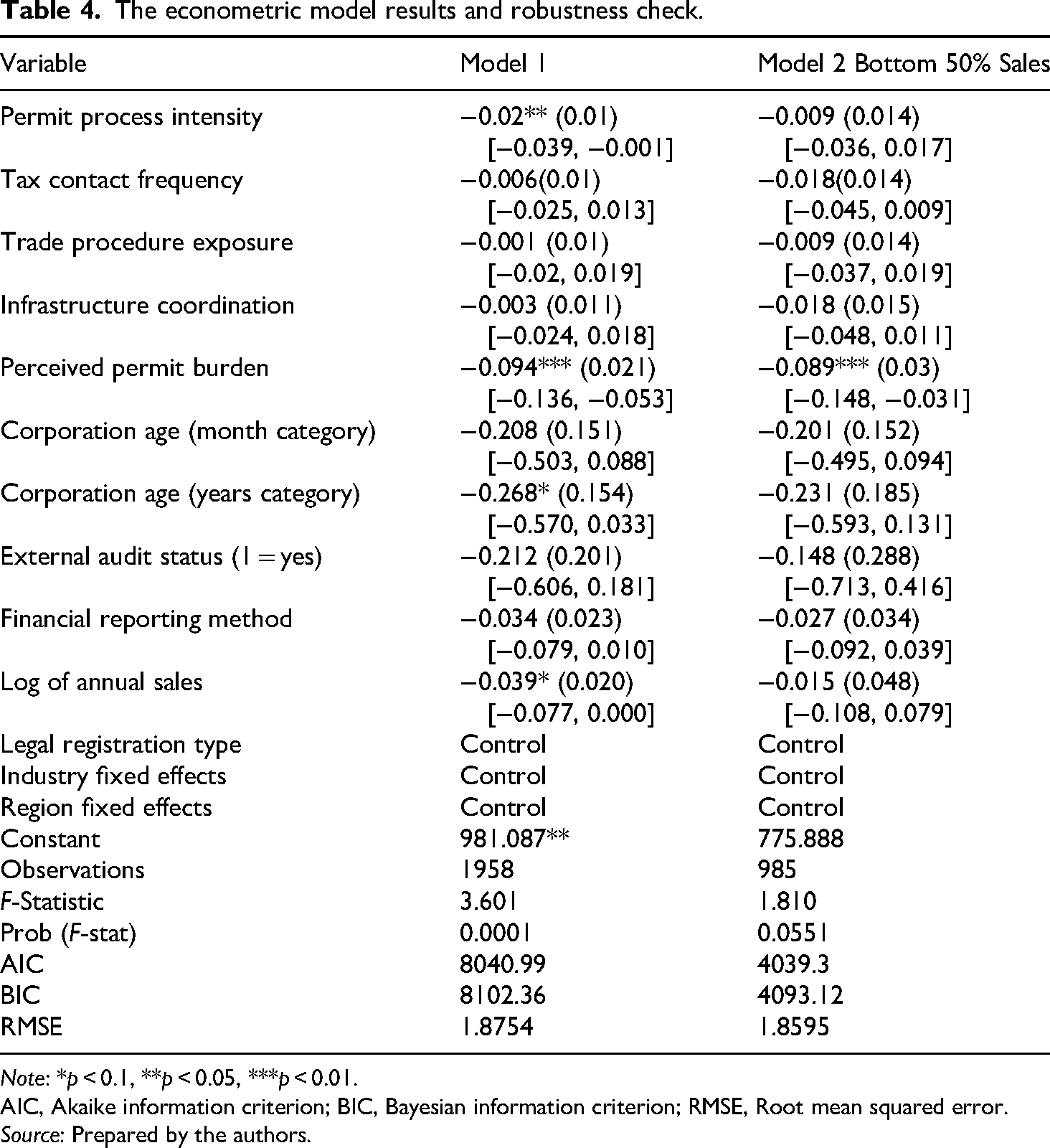

The econometric model results and robustness check.

Note: *p < 0.1, **p < 0.05, ***p < 0.01.

AIC, Akaike information criterion; BIC, Bayesian information criterion; RMSE, Root mean squared error.

Source: Prepared by the authors.

Table 4 reports the results from regression models investigating the relationship between streamlining governance and administrative burden. The dependent variable is corporations’ self-reported perception administrative burden. In Model 1, the coefficient for permit process intensity is −0.020 (p < 0.05), with a standard error of 0.010 and a 95% confidence interval ranging from −0.039 to −0.001. Other streamlining variables, such as tax contact frequency and infrastructure coordination, exhibit negative but mostly insignificant coefficients across Models 1 and 2. Perceived permit burden as an obstacle is the most consistently significant. Its coefficient is −0.094 (p < 0.01), with a standard error of 0.021 and a confidence interval of [−0.136, −0.053], suggesting that corporations facing greater security concerns are more likely to experience heavier administrative burdens. Corporation age (years category) also shows an insignificant negative association (β = −0.208). In contrast, financial reporting method (β = −0.034) and external audit status (β = 0.212) do not display statistically significant effects.

Robustness check Model 2 restricts the sample to corporations in the bottom 50% of the log sales distribution. The estimated coefficient for permit process intensity remains negative (β = −0.009) but becomes statistically insignificant (CI = [−0.036, 0.017]), indicating that streamlining effects may be less pronounced among smaller corporations. Other governance variables remain statistically insignificant in this subgroup. Model 2 fit statistics include an R2 of 0.0497, an adjusted R2 of 0.0391, and a root mean squared error (RMSE) of 1.8595, which are relatively higher than the values for Model 1, suggesting that the determinants of burden may be more observable among small-scale enterprises.

Mediation and mechanism analysis

To further explore the mechanism through which streamlining governance influences corporations’ perceptions of the regulatory climate, we conduct a mediation analysis. Table 5 reports the results of this analysis, including the direct, indirect, and total effects across sequential regression models.

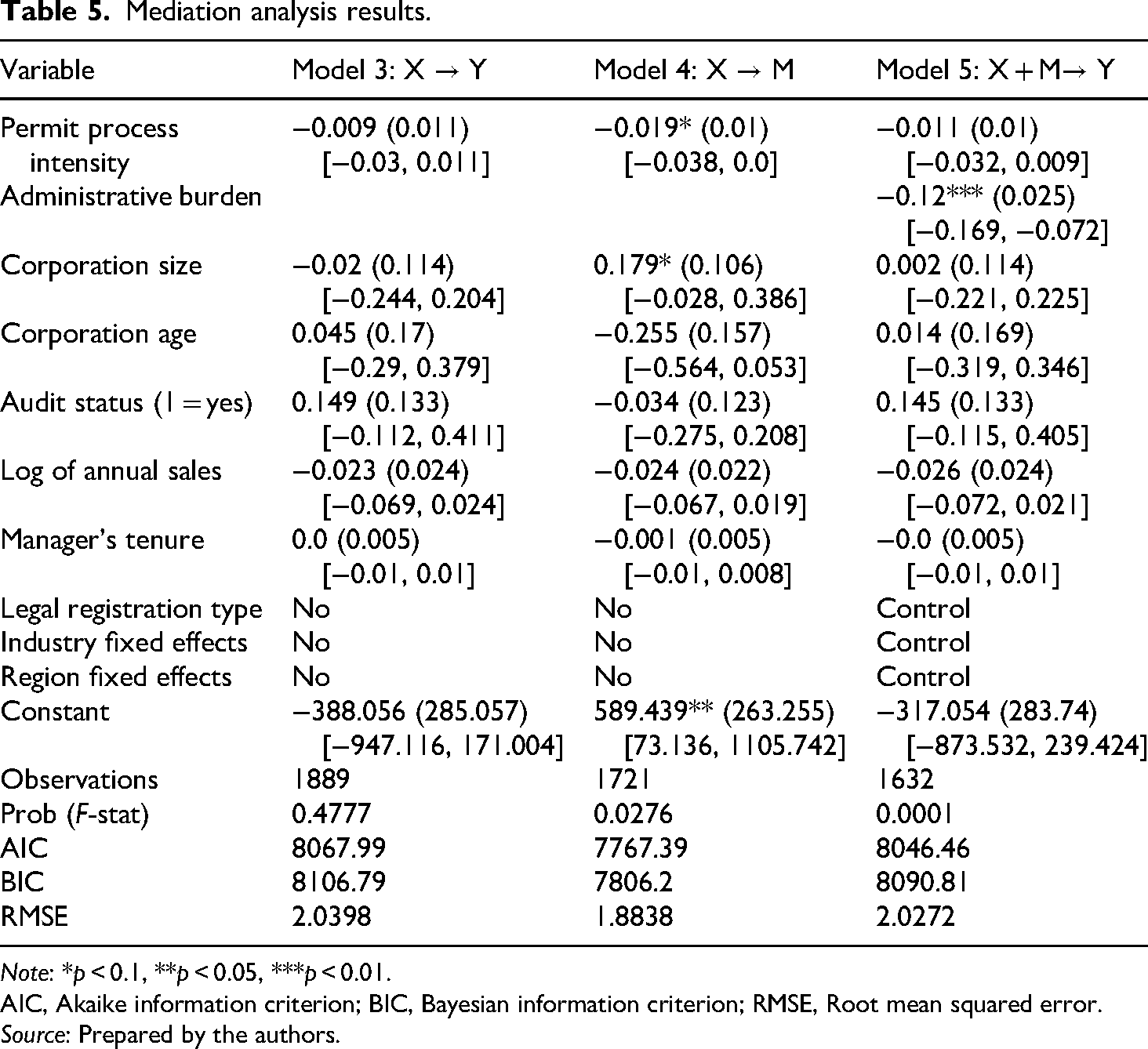

Mediation analysis results.

Note: *p < 0.1, **p < 0.05, ***p < 0.01.

AIC, Akaike information criterion; BIC, Bayesian information criterion; RMSE, Root mean squared error.

Source: Prepared by the authors.

Table 5 displays the findings from a regression-based mediation analysis aimed at assessing whether the impact of permit process intensity on corporations’ perceptions of the regulatory climate is transmitted indirectly through changes in administrative burden. In Model 3, which regresses regulatory climate on permit process intensity and controls, the coefficient on permit process intensity is −0.009, with a standard error of 0.011 and a 95% confidence interval ranging from −0.030 to 0.011, suggesting a negative but statistically insignificant relationship. The model explains a modest portion of variance, with an R2 of 0.0529 and an adjusted R2 of 0.0374, based on 1889 observations. In Model 4, which estimates the effect of permit process intensity on administrative burden, the independent variable emerges as statistically significant at the 10% level. The estimated coefficient is – 0.019 (SE = 0.010; 95% CI: −0.038–0.000), implying that greater streamlining in permit procedures corresponds to lower tax-related administrative burden as perceived by corporations. Control variables show the expected directional signs. For instance, corporations that underwent external audits report lower burden (β=–0.034), although the result is not statistically significant. Corporation age is also negatively related to burden (β = –0.255), suggesting that younger corporations tend to feel more encumbered.

Model 5 includes both permit process intensity and administrative burden as predictors of regulatory climate. The coefficient for administrative burden is –0.12, with a standard error of 0.088 and a confidence interval from −0.169 to −0.072. The direct effect of permit process intensity also remains insignificant (β = –0.007, SE = 0.011). The model yields an R2 of 0.0562, an adjusted R2 of 0.0389, and an RMSE of 2.0272, offering a slight improvement over Model 3. Notably, in this model, the log of annual sales continues to be positively associated with regulatory perceptions (β = 0.055, SE = 0.029; 95% CI: −0.002–0.112), reinforcing the notion that larger or more complex corporations perceive greater constraints in institutional environments. To formally test whether administrative burden acts as a significant mediator between permit process intensity and regulatory climate, we conducted a Sobel test. This statistical procedure computes the significance of the indirect effect based on the product of the coefficient from the X→M path (a = –0.019) and the M→Y path (b = –0.12). Using the Sobel formula for the standard error:

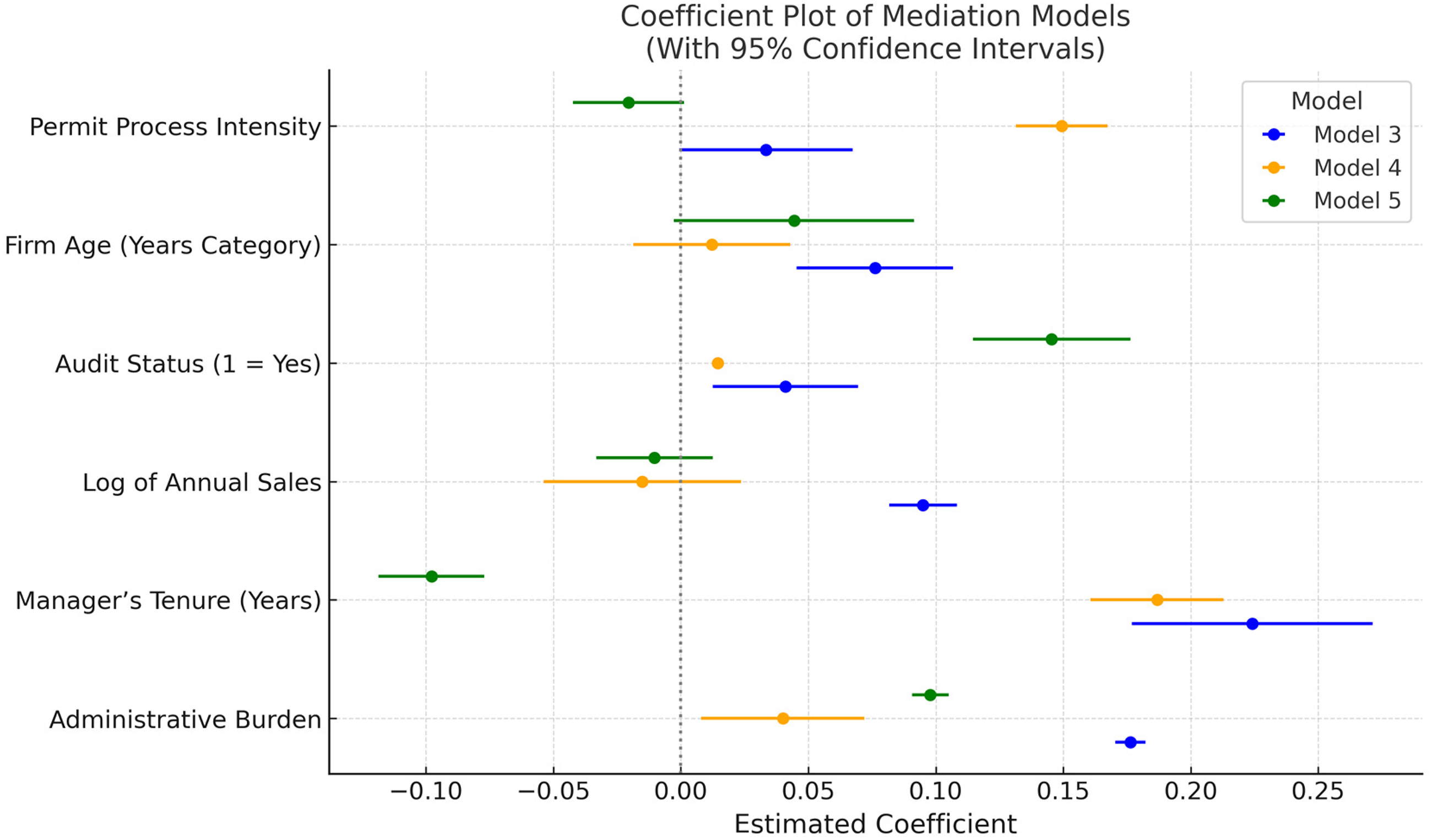

The resulting indirect effect is 0.0022. The Sobel standard error, derived from the combined variances of both path coefficients, is calculated as 0.0013. This yields a Z-score of 1.7811 and a corresponding two-tailed p-value of 0.0749. Although the p-value does not meet the conventional 0.05 threshold, the result is marginally significant at the 10% level, indicating tentative evidence for partial mediation. That is, corporations operating under streamlined permitting regimes may experience a reduction in administrative burden, which in turn may shape how they assess broader regulatory constraints. While the overall effect size remains modest, the directionality and structure of the relationships align with theoretical expectations from administrative burden and institutional constraint literature. Figure 2 presents the estimated coefficients from three ordinary least squares regression models used in the mediation analysis results in Table 5.

Visualizing coefficients and confidence intervals from mediation analysis.

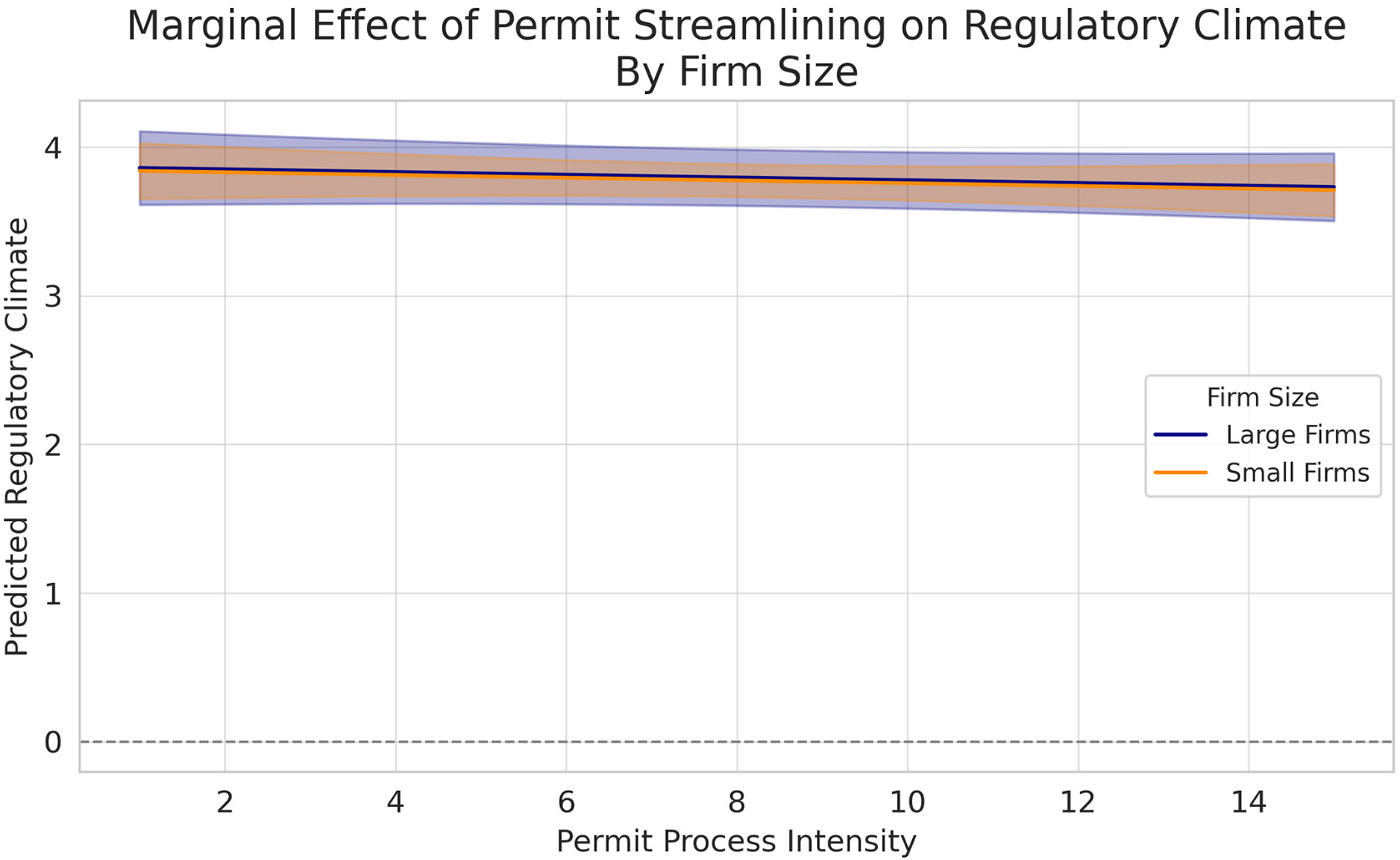

Model 3 (permit process intensity → regulatory climate)is baseline estimation, Model 4 (permit process intensity → administrative burden), and Model 5 (permit process intensity + administrative burden → regulatory climate). Each point represents the coefficient estimate for a given variable, and horizontal lines indicate 95% confidence intervals. The vertical dashed line at zero marks the threshold of statistical neutrality. To enhance visual clarity, each model is represented using a distinct line style, solid for Model 3, dashed for Model 4, and dashed–dotted for Model 5, while maintaining consistent color coding across models. Figure 3 illustrates the marginal effects of permit process streamlining on corporations’ perceptions of the regulatory climate, differentiated by corporation size.

Marginal effect of permit streamlining on regulatory climate.

Based on Model 3 of the mediation framework, the plot presents predicted values of regulatory climate (y-axis) across a continuum of permit process intensity (x-axis), holding all other control variables constant at their mean values. The solid blue line represents large corporations, while the solid orange line corresponds to small corporations. Shaded bands indicate 95% confidence intervals around the estimated marginal effects. The results reveal that small corporations exhibit a consistently more negative perception of the regulatory climate.

Discussion

The empirical findings of this study underscore the central role of procedural design in shaping corporations’ perceptions of institutional legitimacy. As hypothesized, streamlining governance, operationalized through the frequency of permit processes and administrative interactions, was associated with a measurable reduction in perceived administrative burden. This, in turn, partially mediated corporations’ evaluations of the regulatory climate. These results lend robust support to the argument that the experiential dimension of governance matters deeply, not only for citizens but also for private organizations navigating the state.

In contrast to reform narratives that focus on legal codification or structural change, our findings demonstrate that procedural architecture itself can generate or alleviate institutional trust. This insight aligns with recent studies emphasizing the importance of policy delivery over policy design (Chudnovsky and Peeters, 2022; Martin et al., 2024), particularly in regulatory environments where formal rules may be uniform. In the Chinese case, the “One Matter Initiative” reform offers a compelling illustration: despite a top-down bureaucratic structure, procedural variation across corporations remains salient, and its consequences are empirically observable in corporation-level perceptions.

Our mediation analysis shows that administrative burden is not simply a by-product of regulatory complexity, it is the mechanism through which corporations internalize and interpret governance quality. When corporations are streamlined, they report fewer procedural costs and express greater confidence in the broader institutional environment. This finding reinforces the behavioral logic of administrative burden theory (Baekgaard et al., 2025a) and extends it into a less-studied organizational context. The observed heterogeneity across corporation types suggests that procedural reform is not experienced uniformly. These findings echo prior work on “burden tolerance” and the unequal capacity of organizations to navigate state systems. This complements previous work suggesting that the cost of compliance is as much cognitive and emotional as it is financial or legal (Giannella et al., 2024; Holler and Tarshish, 2024).

This study contributes to international administrative scholarship by demonstrating how non-Western procedural reform can yield measurable behavioral outcomes, enriching the geographic and institutional diversity of administrative burden theory. While previous empirical evidence has largely come from welfare-state contexts, our study situates China's procedural innovation within a global discourse of governance quality and regulatory trust.

Conclusion and remarks

This study focuses how streamlining governance reforms affect corporations’ perceptions of the regulatory climate, and whether this relationship is mediated by administrative burden. Governments should recognize that regulatory effectiveness is a function not only of legal form, but also of how rules are enacted and delivered in practice. Investing in workflow integration and reducing unnecessary interactions can yield measurable improvements in business sentiment. Reform strategies must also be attentive to the diversity of administrative subjects. China's case offers broader lessons for the international community. Future studies may build on these insights to explore similar procedural experiments in other high-capacity but institutionally distinct regimes.

At the same time, this study is not without limitations. The cross-sectional nature of the data constrains causal inference, and the operationalization of streamlining governance relies on corporation perceptions of administrative frequency, which may be affected by unobserved expectations or prior institutional exposure. Future research may benefit from panel data or experimental designs, as well as from qualitative inquiry into the organizational behavior of street-level bureaucrats in delivering procedural reform.

Supplemental Material

sj-docx-1-ras-10.1177_00208523251381187 - Supplemental material for Streamlining governance: How the “One Matter Initiative” reduces administrative burden and optimizes the regulatory climate in cities

Supplemental material, sj-docx-1-ras-10.1177_00208523251381187 for Streamlining governance: How the “One Matter Initiative” reduces administrative burden and optimizes the regulatory climate in cities by Liao Fuchong and Zhang Chun in International Review of Administrative Sciences

Footnotes

Acknowledgments

This work was funded by the Chey Institute for Advanced Studies International Scholar Exchange Fellowship (ISEF2024-2025). Zhang Chun, the corresponding author, thanks the Toshiba International Foundation: Bridging Cultures through Academic Research (FY2025). Korea–China Public Policy Experts Research Network (KF Ref. 2221100-1630) and Kurita Water and Environment Foundation (25P001) are also acknowledged.

Funding

This work was funded by the Humanities and Social Sciences Research Project—The China Ministry of Education (23YJC630105); and the National Social Science Fund (24ZDA051; 22AZD141), Shenzhen University (868-000001033315).

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

Authors biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.