Abstract

This paper has studied electricity pricing under a regulated structure during post power sector reform in Odisha, India. It is found that Odisha has adopted the average cost pricing principle for determining electricity price with the rate of return regulation. This process of tariff determination not only takes a long time but also involves huge cost. Further, actual tariffs levied by the Odisha Electricity Regulatory Commission (OERC) are at variance with the broad principles of rational pricing policy. This uneconomic pricing policy has adverse impact on the financial health of the distribution companies. However, the Electricity Act of 2003 has brought about a radical change in the power scenario across the country, including the state of Odisha, by introducing open access and trading of power.

Keywords

Introduction

The electricity supply industry (ESI) has been a subject of reform and change all over the world for more than two decades. Traditional electricity utility was regarded as a natural monopoly and was considered to be a unique public good that deserves special treatment and protection to ensure efficient supply. Accordingly, vertically integrated generation, transmission and distribution (T&D) systems as state-owned undertakings were established in most countries. However, the technical and financial performance of the state-owned electricity utilities was unsatisfactory and the utilities were starved of investment resources. Therefore, in order to reap the advantage of a more efficient and competitive market, a number of countries have been reforming and restructuring their ESIs. There has been a paradigm shift in the power sector from natural monopolies to a competitive model by encouraging unbundling and privatization of generation, T&D functions with a hope that restructuring will reduce various components of costs of supply and lowering tariff rates, benefiting the consumers (Singh and Kumar, 2006).

The pricing policy of electricity has an important bearing not only on the growth of the ESI, but also on overall economic efficiency, growth and equity in the economy. The pricing of electricity gives appropriate signals for investment, production and consumption. However, charging prices below the cost of production to meet social objectives can lead to over-consumption, waste of national resources and damage to the environment. On the contrary, charging unduly high prices can be inimical to industrial competitiveness. Similarly, in pursuit of social objectives, when utilities charge discriminating prices for different categories of consumers, the changes in relative prices can alter resource allocation in unintended ways, with adverse consequences for both allocative efficiency and equity (Rao et al., 1998). Again, when a transition is attempted from statutory public monopoly to a competitive environment, reforms in pricing policy become essential.

Although the case of setting electricity prices on an economic basis is compelling, there are considerable difficulties in evolving such a rational policy. As the ESI sector is characterized by a considerable degree of monopoly, setting regulated prices in a rational manner has been a challenging task for most utilities. Even when unbundling of various components and creation of a more competitive environment has progressed in recent years, regulation of pricing has become necessary to ensure a proper market. Since Odisha, a poor state in India, was the first to initiate and adopt reform process in the entire country, a study of the pricing policy of electricity adopted by the state is pertinent and would serve as an indicator of the direction in which the reform process is moving.

Scholars in electricity pricing, such as Chamberlin (1985), LittleChild and Vaidya (1992), Munasinghe (1992) and Reddy (1995), have worked on the determination of an optimal price for electricity. They have studied the significance of the marginal cost principle in electricity price determination and do not find any reason to follow average cost pricing, since it used historic data, which proved inadequate for price fixation. They preferred to apply long-run and short-run marginal cost principles for determining unit cost. For long-term planning applications, long-run marginal cost is found to be more appropriate than the short-run marginal cost.

The work of Wee and Li (1995) on the pricing aspect of electricity supply in China made it clear that in the wake of globalization, tariff restructuring becomes inevitable. They suggest that a power sector reform in the economy would be highly useful to introduce an optimal pricing policy in this sector.

The Korean Electric Power Corporation (KEPCO), which is responsible for generation, T&D of electricity in Korea, has implemented sophisticated tariff structures incorporating long-run marginal cost and the time of the day tariff. The tariff levels are fixed on the basis of the anticipated rate of return (RoR) on investment. KEPCO’s experience in tariff policy led State Electricity Boards (SEBs) of developing countries to follow the Korean example.

Rao et al. (1998) examined at length the nature, characteristics and issues found in the tariff in India. They observed that actual tariffs levied by SEBs are at variance with the broad principles of rational pricing policy, which is incentive compatible and is required to generate resources for reinvestment. They have pointed out that economic considerations do not seem to have dictated the determination of tariff. The tariff on different categories of consumers bears no relationship to the marginal cost of supplying electricity to them. In fact, in some cases the tariff is inversely related to the average costs, underlining the importance of political factors.

Natural monopolies have little chance of being driven out of a market by more efficient new entrants, which puts customers at risk. Consequently, some form of regulation is necessary to protect the customers’ rights in monopoly industries such as electricity T&D. In addition, electricity networks are crucial elements in creating an efficient market place for electricity selling, and regulatory intervention is necessary to guarantee that the terms defined for using T&D facilities do not prevent competition (Beesley, 1992). In other words, regulation is essential to maintain the freedom of entry (Vickers and Yarrow, 1988).

The original objectives of regulation are to avoid monopoly inefficiency and protect customers from monopoly exploitation. In a market economy, competition takes care of price regulation and provides companies with incentives for efficient operation. Broadly defined, economical efficiency requires that tariffs are designed to: (1) achieve efficient use of energy; (2) minimize production costs; (3) provide clear investment incentives; and (4) result in efficient organization of the electric services industry (Olson and Richards, 2003). According to Vickers and Yarrow (1988), competition provides an incentive system that impels privately owned firms to behave in ways that are broadly consistent with efficient resource allocation. However, in some industries, these forces of competition are weak or non-existent and these industries are often considered to possess the characteristics of natural monopolies. The electricity distribution business tends to fall into the category of non-existent forces of competition and, consequently, electricity distribution companies typically have franchised monopoly positions in specifically defined areas. In such a business environment, customers are at risk and, hence, some form of regulation is necessary. In general, regulation is expected to give the distribution companies incentives to act in the public interest. In other words, the value of the regulatory commitment depends on the power of the regulatory incentive schemes (Newbery, 1997).

Theoretical aspects of electricity pricing policies

The necessity of studying pricing policy has been widely accepted in all utility systems and the case of electricity is no exception. The economic principles of determining prices of electricity are not unique; the special characteristics of the ESI call for the consideration of additional factors. Three alternative pricing policies can be adopted for pricing electricity utilities. These are:

monopoly pricing;

full-cost/average cost pricing;

marginal cost pricing.

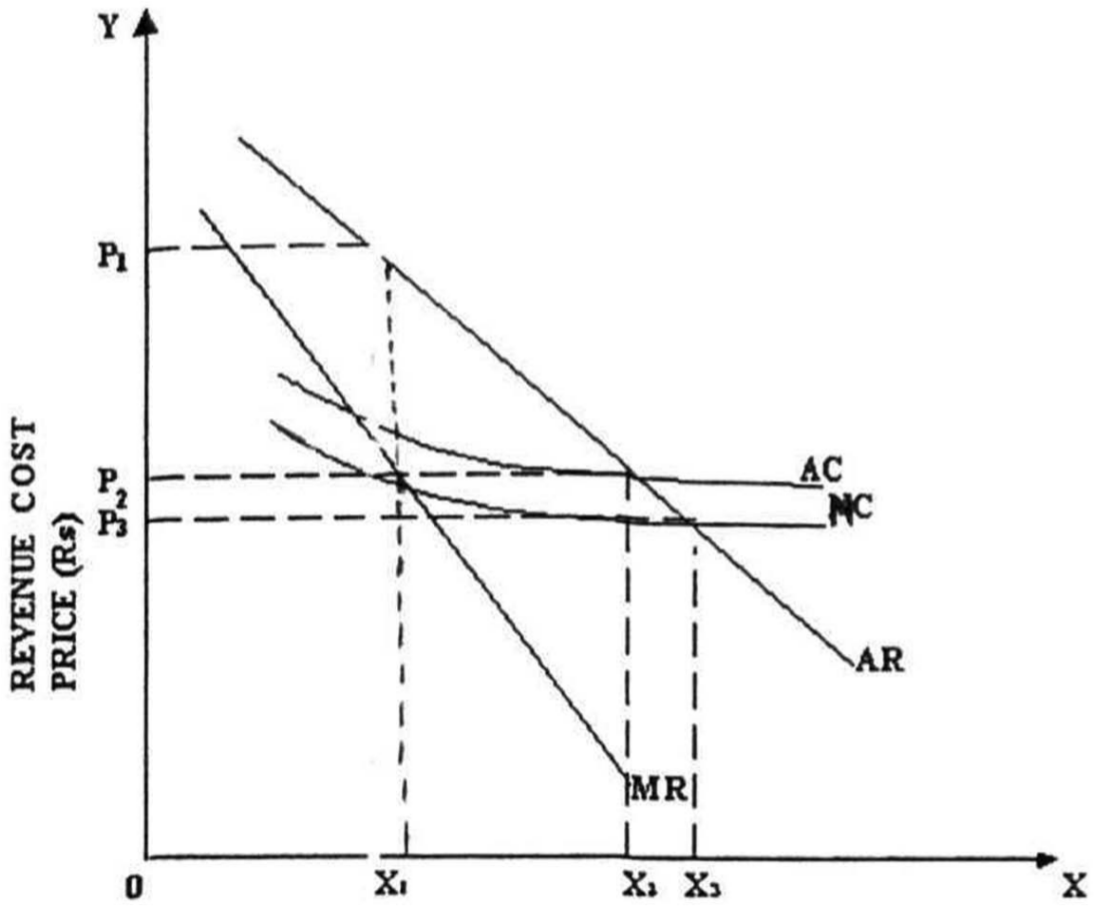

These three pricing policies are illustrated with the help of Figure 1, which depicts a decreasing cost industry. When monopoly pricing policy is adopted, the equilibrium price and output are determined with the intersection of MC and MR curves. The equilibrium price would be OP1 and output would be OX1. This would provide monopoly profit to the firm and would be intolerable to the public. On the other hand, if the utility is following full-cost pricing (in this method the price is determined by adding a fixed mark-up to the cost of acquiring or producing the product), it would produce OX2 output with a price of OP2. This is said to provide a fair return on the investment in the utility. This pricing method is the most popular method. However, the welfare of the society cannot be maximized by using full-cost pricing, as the value of the added services exceeds the marginal cost of the added output of these services. The welfare-maximizing approach indicates that the prices of electricity should equal the marginal costs. If the utility is priced on the basis of MC, the recommended price would be OP3 and the output would be OX3. The welfare of the society is maximum, because at OP3 the value of the product to the marginal user equals the value of the resources used up in the production of the last unit (measured by MC). It may be noted that in the case of a decreasing cost industry, the fixation of prices to equal the marginal costs would not enable the utility to cover the total costs, which makes the departure from the marginal cost pricing rule necessary.

Electric utility pricing.

The second-best solution considers the electric utility as a multi-product firm (product differentiation, for example, may be in terms of the time of use or consumer category) and, according to this, optimal prices are given where the difference between the price and marginal cost is proportional to every product (category of consumer). This implies that prices ought to vary inversely with own price elasticity of the product (Rao et al., 1998). Thus, computation of second-best prices necessitates information on marginal costs and own price elasticity of demand at the optimum output configuration.

The literature on the two-part tariff and multi-part tariff has shown that it is possible to evolve prices varying with the amount of electricity consumption (Rao et al., 1998), which would also fulfil the desired conditions: (i) price for marginal unit equals the marginal cost, and (ii) total revenue equals total cost.

Economists have considered marginal cost pricing principles as the most efficient pricing theory so far as theoretical economic analysis is concerned. The literature emphasizes the importance of marginal costs in designing a rational pricing policy in contrast to the concept of average costs evaluated historically, usually used in accounting and literature.

Significant differences in determining the structure of prices for different consumer categories exist among countries, depending upon the extent of regulation, policy constraints and social objectives. The traditional approach has been to average the cost elements across different classes of consumers, which result in cross-subsidization among different categories of consumers. Although cost-based discrimination cannot in principle be objected to, discrimination based on social objectives can have a serious adverse effect on incentives.

The objectives would be to approximate the prices that theoretically would be achieved in a competitive situation and this generally involves setting prices equal to the marginal cost for a particular level of output. The objective would also be to ensure that the pricing signals provide correct incentives to expand the contracted capacity to match supply and demand.

In order to understand the pricing of electricity as a product, we need to consider the economic characteristics of electricity supply that impinge upon the determination of the ultimate price to the consumer. The electricity supply has typically large economies of scale in generation and transmission and the production of electricity requires a capital-intensive infrastructure. The electricity involves simultaneity of production and consumption, there is non-differentiation of the product, electricity is locational and time dependent, there is no storage mechanism and hence electricity is dedicated to the delivery mechanism. Electricity thus offers these peculiarities and hence the pricing is to be uniform, locational and related to time of use.

Regulation of electricity prices

While reforms in utility industries, such as those facilitated by national competition policy, have encouraged competition, the continued existence of monopoly power in parts of those industries has left a residual need for some form of price regulation. Infrastructure industries such as electricity are an example where there can be such a residual need for regulation. With regulation now very much focused on pricing of key bottleneck facilities, the success of price regulation will be an important determinant of investment in infrastructure sectors, with implications for economic growth more generally.

In traditional economic theory, the market for electricity is not competitive. Hence, regulation is required to set tariffs as close as possible to the competitive idle. Traditionally, an electricity utility has the natural monopoly; it can use its market power and set prices artificially high. The regulators prevent this abuse of monopoly by setting prices exogenously. The regulation of the tariff is therefore an evolutionary process that changes according to the requirement of the industry. However, the question arises as to which form of utility regulation to choose. There are broadly three important forms of regulation, viz. cost of service regulation (including direct price setting and Rate of Return), price cap regulation and performance-based regulation (PBR).

Cost of service regulation

Cost of service regulation (also known as cost-plus regulation) can be either direct price setting or Rate of Return regulation. While cost of service regulation has tended to become less favoured in recent years, it still continues to play an important role in Odisha electricity regulation.

The most intrusive form of regulation occurs when the government takes an active role in setting the prices that can be charged. Prior to reforms, governments played a key role in price setting for publicly owned electricity authorities. In recent times, the price-setting model of regulation has come under strong criticism in the literature. A major focus of this criticism has been the lack of clear objectives (or the presence of competitive objectives) established for the rate-setting body. While the role of the government department or utility commission is to act as a market surrogate and set the price, that task is performed in a political and social context. While the economic criterion of efficiency is an input to the rate-making process, there may be significant pressure for the regulator to suppress economically efficient pricing structures.

In the RoR regulation, the firm’s costs are reviewed, and costs deemed to be unnecessary are eliminated. Here prices and their structure are set to generate enough revenue to cover costs and provide a fair RoR. The key property of RoR regulation is that it permits the regulator to limit the profit level that can be achieved. Restraining profits by fixing the maximum return on investment provides the enterprise with a degree of autonomy in conducting its affairs while limiting monopoly behaviour.

However, the directing effects of RoR regulation are imperfect in the sense that they give incentives for over-capitalization but not for efficiency improvements. Indeed, RoR regulation has rather commonly been criticized because it lacks incentives for efficiency improvements and encourages firms to engage in strategic behaviour (Jamasb and Pollit, 2003). Irastorza (2003), on the other hand, sees traditional regulation as problematic because it does not encourage cost reductions and efficiency improvements, and may reward over-investments. The incentives for cost reductions are largely absent, because the authorized prices are consistently linked to realized costs (Bernstein and Sappington, 1999). Roach (2003) argues that cost-plus regulation puts the distribution business into a stagnant course, as it focuses on constraining profits rather than on constraining costs and encouraging innovation.

Price cap regulation

Price cap regulation, as an alternative to traditional RoR regulation, developed as a practical regulatory tool in the early 1980s in Britain. Price cap regulation provides desirable incentives to achieve and improve productive efficiency, while reducing the information burden of regulation. Unlike RoR regulation, price caps do not require imprecise and often arbitrary measures of a rate base or return on capital and eliminate the need to allocate costs when only some parts of a firm are regulated. Price cap regulation is sometimes called ‘CPI - X’, (in the United Kingdom ‘RPI-X’) after the basic formula employed to set price caps. This takes the rate of inflation, measured by the Consumer Price Index (UK Retail Prices Index, RPI) and subtracts expected efficiency savings, called the ‘X factor’ (Sappington and Weisman, 2010).

In its simplest form a price cap simply sets a maximum allowed inter-temporal path for the price of a specific product. The price in any given year may be capped at a level that alters over time in response to a price index that is exogenous to the regulated firm and a factor (X) set in advance by the relevant regulator. The maximum price then rises in line with the main index of retail prices (CPI in Australia) but falls at a rate X set in advance. The value of X is meant to reflect potential cost savings by the firm due to either increased efficiency or technological progress. The X factor is set to reflect expected firm productivity improvements.

It is found from the literature that the experience with price cap regulation has generally been a success. Price cap offers a better alternative than the more traditional forms of regulation, and owing to the incentives they foster, price caps have the potential to yield better outcomes in terms of economic efficiency, while requiring relatively minimal regulatory effort. The disadvantage of price cap regulation, however, is that the desirable properties of price caps can be eroded due to poor implementation.

The basic idea of price cap regulation is to set limits to the prices of monopoly services. The strength of price cap regulation is that it gives incentives for cost-efficiency and allows companies some flexibility to adjust the structure of prices within the basket (Beesley, 1992).

Performance-based regulation

Under PBR, performance measures are used to motivate the firm. This involves linking the profits of the firm (or employee remuneration) to performance measures in such a way that the firm’s profits are permitted to increase if it achieves certain performance standards. In this manner, the firm has an incentive to seek out cost-efficiencies and to improve customer services so that it will be permitted to achieve higher returns. However, difficulties can arise in implementing such schemes. It may be difficult to find easily defined objective performance measures that can be controlled by the firm. Also the firm may have an incentive to achieve a target at very high costs, which can then be passed on to consumers.

Power sector reform in India and Odisha

Reform in India

During the 1980s, due to deteriorating financial performance and poor operating performance of SEBs in India, the onus of setting up new generation capacities fell increasingly on central sector utilities. However, in order to control the fiscal deficit of the government of India, the reform in the electricity sector was initiated in the early 1990s with the opening of the sector for private Independent Power Producers (IPPs). Against the backdrop of the balance-of-payment crisis in 1991, the Indian government decided to liberalize its economic policies. Many structural changes took place, including delicensing, greatly reduced trade barriers, and opening the door to foreign capital – both direct and portfolio. Recognizing that electricity and other infrastructure sectors required substantial investments in the face of resource constraints because of fiscal tightening, the IPP policy was announced to allow investment by the private sector (including foreign capital) in electricity generation. Prior to this, although some private sector licensees operating in a few urban areas, the electricity sector was mostly in the hands of SEBs or central government owned utilities created to supplement the efforts of SEBs in generation and transmission sub-sectors (Pandey and Morris, 2009).

Even as the IPP policy was being operationalized, the idea was that the inefficiencies of the SEBs could be overcome by pursuing unbundling and privatization. The initiative in this direction came largely from multilateral agencies, including the World Bank and the Asian Development Bank. These agencies, besides providing for the services associated with unbundling – consultancy services for laying out the framework, process consultancy for privatization, studies to develop financial plans for restructuring, etc. – also laid out significant amounts by way of low cost loans to the SEBs. There was also much that was wanting in the understanding of the consultancy firms that developed the framework for unbundling during this period. Since this happened at a time when the budgetary provisions of the centre were under stress, many state governments picked up ‘reform’ as conceived by these multilateral agencies, as an agenda with the principal element being the unbundling. Unbundling was seen as a necessary prior condition for privatization (Pandey and Morris, 2009). The early studies showed the need for significant upping of the tariffs, since the leakages and technical losses were projected to continue. Odisha was one of the earliest states to pursue unbundling and, unlike many others, followed it up with privatization of the distribution companies with the transmission company being still in state hands.

Reform to the sector was brought about by legislation by the Government of India in the shape of the Electricity Act, 2003, which came into effect from 10 June 2003. The Electricity Act, 2003, envisaged objectives that had provisions for sweeping changes to the sector. The Government of India also issued the National Electricity Policy (NEP) and National Tariff Policy (NTP) guidelines, charting a path for the stakeholders to move forward. The Electricity Act has provisions that are path breaking in nature, intended to make the sector fair for all the stakeholders and, most importantly, easing barriers of entry for private players. The objectives envisaged in the Electricity Act, 2003, are as follows: consolidating the laws relating to generation, transmission, distribution, trading and supply; promoting competition; protecting the interests of consumers and supply of electricity to all areas; rationalization of the electricity tariff; transparent policies on subsidies; promotion of efficient and environmentally benign policies; non-discriminatory open access; constitution of Central Electricity Regulatory Commission (CERC) and State Electricity Regulatory Commissions (SERCs). The Electricity Act has provided necessary thrust to the Indian Electricity sector and many states have moved forward to initiate the process of reform by unbundling their monolithic boards through corporatization.

By May 2012, SERCs had been constituted in all the states and two Joint Electricity Regulatory Commissions had been created, one for the states of Mizoram and Manipur and another for Goa and the Union Territories of Andaman and Nicobar, Lakshadweep, Chandigarh, Daman & Diu, Dadra and Nagar Haveli and Puducherry; 19 states have unbundled their utilities, including Tripura, which has been corporatized; the State Governments of Bihar, Kerala, Jharkhand and Sikkim have initiated steps towards corporatization/unbundling (Power Finance Corporation, 2012).

The Electricity Act, 2003, also provides for newer concepts such as Open Access and Power Trading. Open Access on the T&D network is allowed on payment of charges to the utility, which enables a number of players to utilize these capacities and transmit power from generation to the load centre. Trading, now a licensed activity, helps provide an innovative pricing mechanism, leading to competition.

With the new Act, a liberalized market structure is provided. A customer has a number of choices to get his power. The generators can also compete among themselves to supply power to distribution companies/individual customers. There is a provision for surcharges to meet the current level of cross-subsidy, if a consumer opts to get electricity directly from a generator or any source other than his own distribution licence and has been allowed open access by the regulator. However, there is no surcharge when the distribution company buys power from a generator directly.

The Electricity Act, 2003, has also made provision for trading of electricity and the distribution companies are now free to trade the power without obtaining any licence. To promote power trading in a free power market, two power exchanges are currently operating in India, viz., the Indian Energy Exchange (IEX) and Power Exchange India Limited (PXIL). IEX has been modelled based on the experience of one of the most successful international power exchanges, Nordpool. These power exchanges have been developed as market-based institutions for providing price discovery and price risk management to the electricity generators, distribution licensees, electricity traders, consumers and other stakeholders. Participation in the exchange operations is voluntary. At present, exchanges offer day-ahead operations whose time line is set in accordance with the operations of Regional Load Dispatch Centres (RLDCs). Power exchanges coordinate with the National Load Dispatch Centres (NLDCs), RLDCs and State Load Dispatch Centres (SLDCs) for scheduling of traded contracts to get up-to-date network conditions. Currently, about 96% of the market transactions in India are in the form of bilateral (long- and short-term) contracts. The rest is dealt with by two power exchanges (Balijepalli et al., 2010).

Reform in Odisha

Odisha initiated the process of reforms way back in 1993 on the advice of the World Bank, and the reforms finally began with the legislation of the Orissa Electricity Reform Act in 1995. The Orissa State Electricity Board (OSEB), like other SEBs, was a vertically integrated monolithic organization that essentially performed all the three vital functions, viz. generation, T&D of electricity. However, over the years it could not live up to the expectations of consumers on growing needs of electricity, maintaining minimum service requirements and a competitive tariff to sustain itself. The OSEB dismally failed in both operational and financial performance, and thus was always dependent upon state government subvention to compensate for the mounting losses. Since the state was directly regulating OSEB activities, it was prone to political interference of varying degrees as suited populist objectives. From day-to-day operational matters to tariff setting, all were susceptible to such interventions. It was plagued with the problems of high T&D losses, large outstanding dues of central sector generating companies, inadequate investment and irrational tariff structure. The state was compensating the electricity board through subvention, which in turn caused a huge dent in its own fiscal balance. The Board was not able to generate a minimum return of 3% as required under the Electricity Supply Act, 1948, on its net fixed assets after meeting fixed and operating costs, interests and tax liabilities. Up until the late 1970s, Odisha was a power surplus state. However, with the growth of heavy industries and rural electrification during the sixth and seventh five-year plans, the power shortage began to mount. During the period from 1980 to 1994, the state saw chronic power cuts, which became statutory. There was an urgent need to step up power generation to meet growing demand. However, the financially sick OSEB was unable to mobilize the massive fund requirement to bring about capacity addition and upgrade a matching T&D network. The non-remunerative tariff and heavy dependence on government subsidy were the primary causes of the Board’s dismal financial status. The state government could no longer take on the burden in its budget for increasing allocation on power generation in the face of compelling social expenditure on health, education, etc.

Odisha, therefore, embarked upon the process of reforms in 1995 with the enactment of the Orissa Electricity Reform Act and a radical programme of reform to address the fundamental issues underlying the poor performance of the OSEB and to revive its moribund electricity industry. The legislation of the Orissa Electricity Reform Act, 1995, paved the way for the creation of functional entities, such as the Odisha Hydro Power Corporation (OHPC) for hydro generation, and the GRID Corporation of Odisha (GRIDCO) responsible for both T&D of electricity. The independent three-member Regulatory Commission was set up by the Government of Odisha. The distribution business was subsequently hived off from GRIDCO from 1 April 1999 by creation of four distribution companies on a zonal basis: the Southern, Western, Northern and Central distribution companies. The companies were later offered for sale at 51% shareholding for the management contract. The management contracts of three companies, the Southern, Western, and Northern distribution companies, were awarded to the private company BSES (now R-Infra) and the central contract was bagged by another private company, AES. The management contract of AES was later cancelled by the regulator in 2005 for violation of licence conditions. It is relevant to mention that under the privatization model, no sale of assets had actually taken place and the assets have only been assigned to the respective privatized companies. Fifty-one per cent of the share capital of the distribution business has been sold at a premium to the private investors. Trading and transmission functions of GRIDCO have been separated with effect from 1 April 2005, with GRIDCO looking after trading and Odisha Power Transmission Corporation Limited (OPTCL) looking after the transmission functions.

The whole privatization exercise was undertaken on the advice of the World Bank, who also prepared a road map of turn-around for the sector. The reform was intended to bring in private players to the sector, thereby importing better technology and management practices, equity infusion from the shareholders so required for the cash strapped sector, better consumer services and ultimately lower electricity prices to consumers. The key features of the reform programme were restructuring and unbundling of OSEB; private sector participation in generation, transmission, distribution and supply; establishment of an independent regulatory body; competitive bidding for procurement of power in new generation; a licensing system in respect of the T&D activities; and tariff setting to attract investment from private investors.

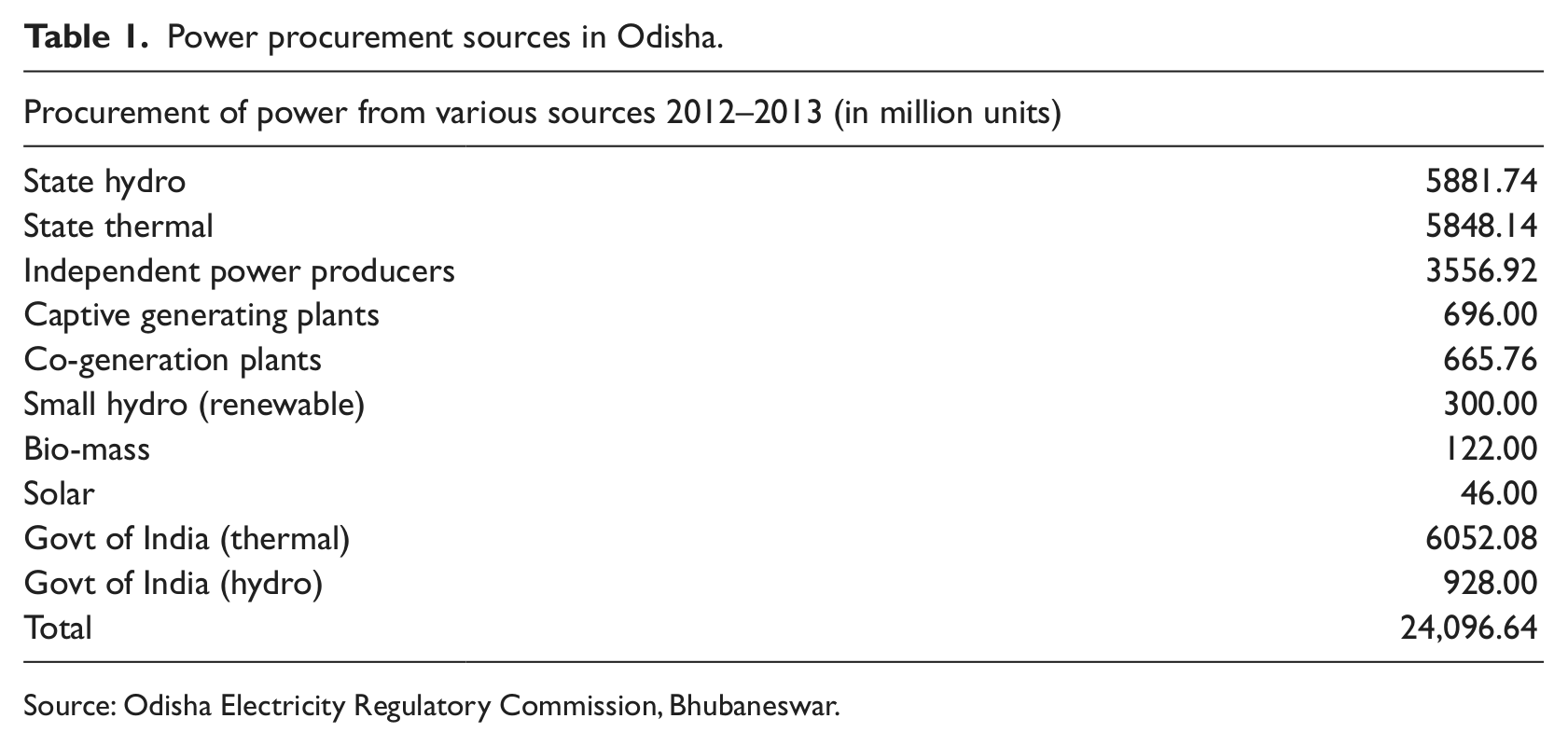

Odisha at present procures power of about 24,000 million units in total as of the year 2012–2013. The 70% demand of the state is met from their own sources, including hydro, thermal, co-generation and a few renewable sources, such as small hydro, bio-mass and solar. The balance demand of 30% for the state is provided by the central generating stations (both thermal and hydro) of the Government of India through the allocated share of those plants (Table 1).

Power procurement sources in Odisha.

Source: Odisha Electricity Regulatory Commission, Bhubaneswar.

The reform process in Odisha is now more than one and half decades old. The Odisha reform has seen the rapid changes that the electricity sector has undergone, both in the state and in the entire country. Various legislations have impacted the reform process and it has weathered the storm appropriately to show direction for others to follow with all its trials and tribulations. Since Odisha was the first state to initiate and adopt a reform process in India, a study of the performance is pertinent and would serve as an indicator of direction in which the reform process is moving. The present paper makes an attempt to study the structure of electricity pricing after the reform initiated during 1995.

Pricing of electricity in Odisha

Odisha has adopted the average cost pricing principle for determination of the electricity price. The regulation adopted by the Odisha Electricity Regulatory Commission (OERC) is the RoR regulation, which is also known as cost-plus regulation. The RoR regulation was as envisaged in the earlier Electricity Supply Act, 1948 (Sixth Schedule). This is a traditional form of regulation wherein a company’s historic costs are reviewed and prices are set to allow profits that deliver the required RoR. The RoR is relatively risk free and allows the company to be financed at a lower required RoR than under other approaches.

The retail tariff in Odisha applicable to the consumers of electricity is a combination of cost of generation and T&D, and is determined in the following stages.

In the first stage, the distribution companies submit the annual revenue requirement (ARR) or costs of meeting a given demand to the OERC along with their proposal for tariff revision. This cost constitutes power purchase cost, operating costs and capital costs. The power purchase cost includes the cost of power purchase, including transmission and SLDC charges. The operating costs include costs of repair and maintenance, establishment and administration and miscellaneous expenditures. On the other hand, capital costs include depreciation, interest on debt and return on equity, if the distribution companies have equity capital. Depreciation is based on the straight-line method and is applied to the net capital stock (at book value) at the beginning of the year.

In the second stage, the OERC invites objections and perusal of the tariff proposal from the general public.

In the third stage, the OERC conducts a public hearing and undergoes consultation with the state advisory committee.

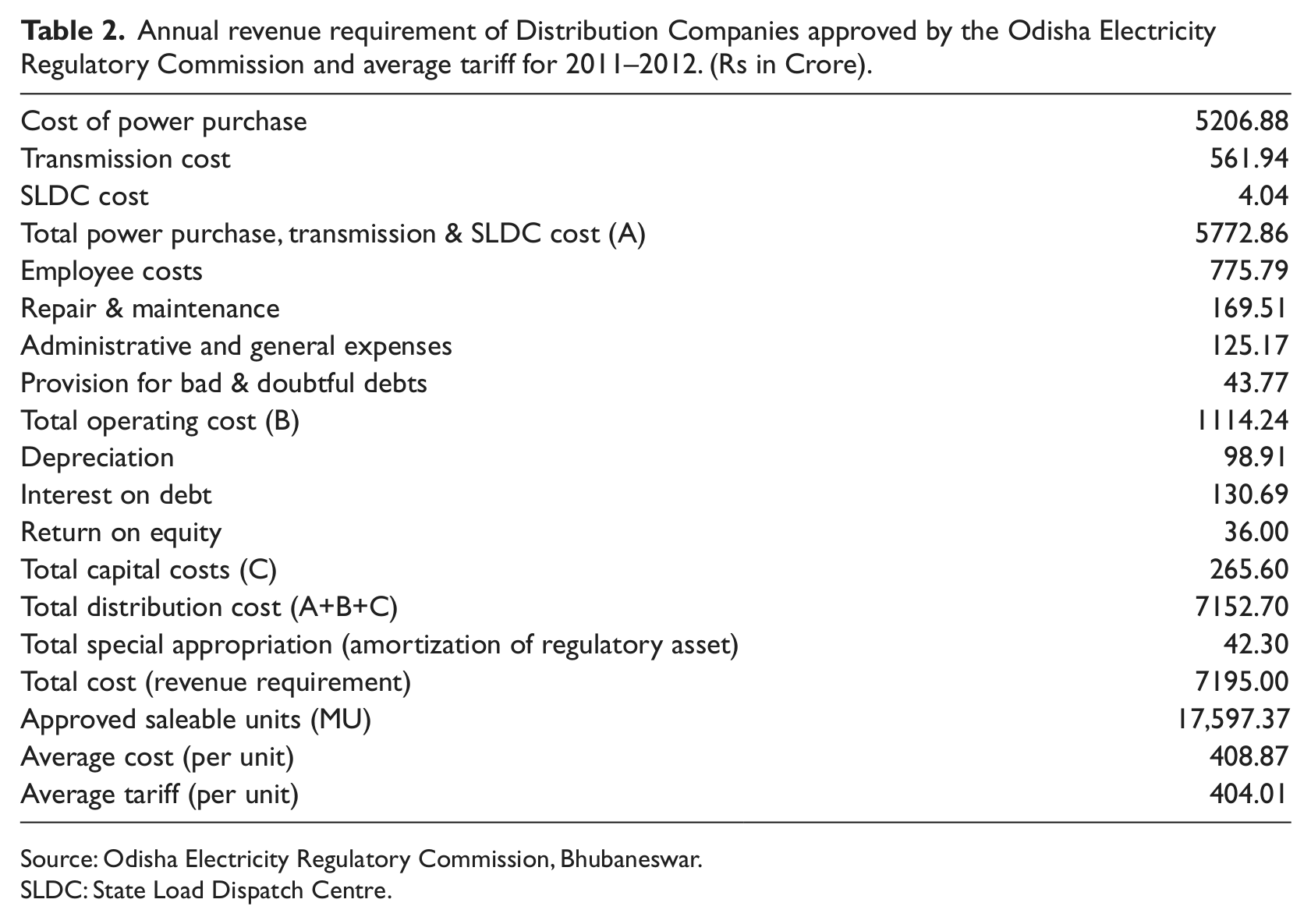

The last stage is the fixation of the tariff. The OERC examines the ARR proposals of the distribution companies and, based on normative principles, estimates the total costs and approves the units for sale. Thus, the average cost per unit sale of electricity is calculated and accordingly prices are set. An illustration of detailed costs and average tariff approved by the OERC for 2011–2012 is presented in Table 2.

Annual revenue requirement of Distribution Companies approved by the Odisha Electricity Regulatory Commission and average tariff for 2011–2012. (Rs in Crore).

Source: Odisha Electricity Regulatory Commission, Bhubaneswar.

SLDC: State Load Dispatch Centre.

The OERC also conducts an annual truing-up exercise after DISCOMs Distribution Companies (DISCOMs) submit audited accounts and allows additional expenses in the case of variance with approval. The negative variance is generally recognized as the regulatory asset, which is amortized over a period of few years. Positive true up is also recognized but has not been adjusted with the ARR so far. The principle of truing up is laid down in the tariff orders. Amortization of regulatory assets also affects the pricing of electricity, as these past liabilities are included in the current price.

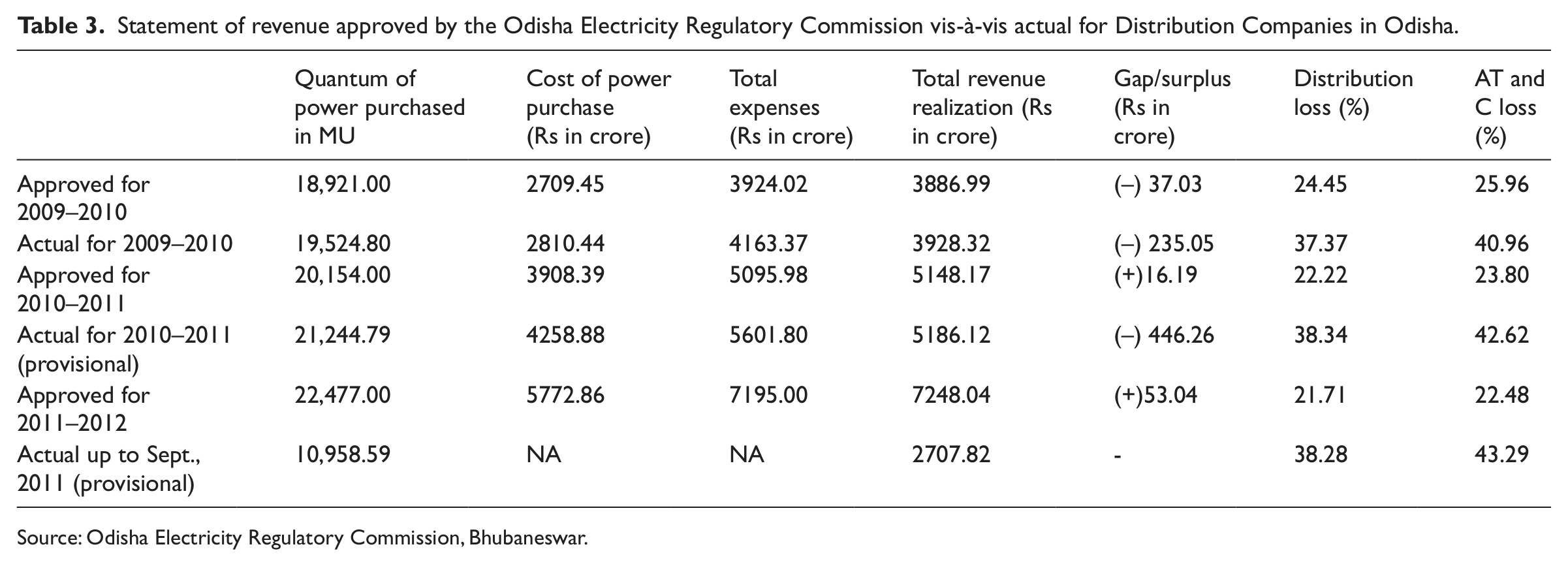

The OERC approves the power purchase cost, transmission charges, SLDC charges and other expenditure for GRIDCO, SLDC etc., after prudent checks and to meet the total expenditure of the concerned distribution licensee, revenue realization is estimated on a normative basis and adopting distribution loss as per the business plan is approved by the OERC. However, the actual gap/surplus at the end of the financial year is very often more than the amount assessed by the OERC, which is due to an increase in the quantum of power purchase, an increase in the average rate of power purchase cost and non-achievement of the loss level fixed by the OERC for the distribution companies. This can be seen in Table 3. This affects the tariffs in subsequent years due to the provision of truing up.

Statement of revenue approved by the Odisha Electricity Regulatory Commission vis-à-vis actual for Distribution Companies in Odisha.

Source: Odisha Electricity Regulatory Commission, Bhubaneswar.

At the stage of tariff determination, socio-economic and political considerations also play an important role. Although the cost of electricity supply in rural and remote areas is higher than in urban areas, electricity is supplied to the former at prices below costs, ostensibly for achieving balanced development and to remove rural–urban disparity, but actually due to political compulsions. Similarly, although the costs at low tension (LT) ends are higher than at high tension (HT) ends, a lower rate is charged for domestic and agricultural users who are supplied power at the LT end.

This process of tariff determination takes not only a long time of about three and half months, but also involves huge cost. Further, actual tariffs levied by the OERC are at variance with the broad principles of rational pricing policy, which is incentive compatible and is required to generate resources for reinvestment. There are also historical reasons that impinge upon the present cost of electricity. As a first step towards initiation of reform, the Government of Odisha notified the transfer scheme in April 1996 and took over the T&D assets of the erstwhile OSEB. The value of the assets were ascertained at Rs 1200 crore, which included Book value plus capitalized expenses and interest. The Government then reinvested them in GRIDCO after up-valuing the assets by an additional Rs 1194 crore and adjusted the subsidies and electricity charges payable to GRIDCO, totalling Rs 340 crore. In addition, GRIDCO issued Rs 253 crore worth of shares and Rs 400 crore worth of zero coupon bonds to the state government; Rs 1146 crore of loans and liabilities were also assigned to it. The impact of revaluation of assets on four DISCOMs was of Rs 630 crore, which were only project-specific liabilities. While the assets were up-valued there was no such up-valuation of the liabilities. The only component of the asset up-valuation that had bearing on the price of electricity was depreciation, which jumped to Rs 128.02 crore for 1998–1999 from Rs 81.69 crore in 1996–1997. Thus, the up-valuation of assets by over Rs 2000 crore (128%) resulted in increase in the Bulk Supply Tariff by 24 paisa per unit, the cumulative financial impact of Rs 590 crore. The state government also withdrew subsidy support to the DISCOMs, which was to the tune of Rs 250 crore per annum. There were also huge unclear dues of the government departments to the tune of Rs 170 crore. All these factors contributed to the rise in price of electricity on the very inception of the reforms, which impacted cost of electricity in future years.

Besides the above factors that led to the increase in price of electricity, we have also observed the following demerits in the present electricity pricing policy in Odisha.

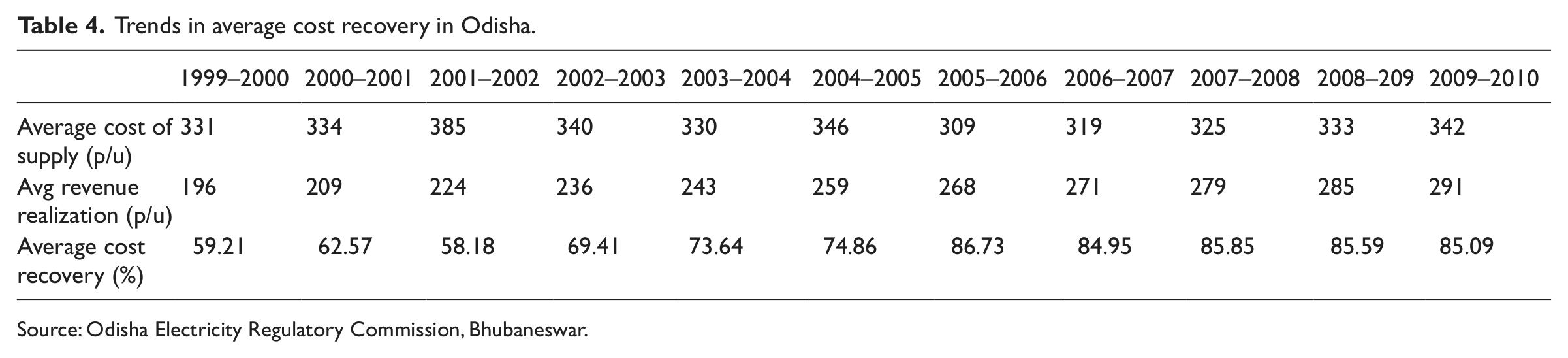

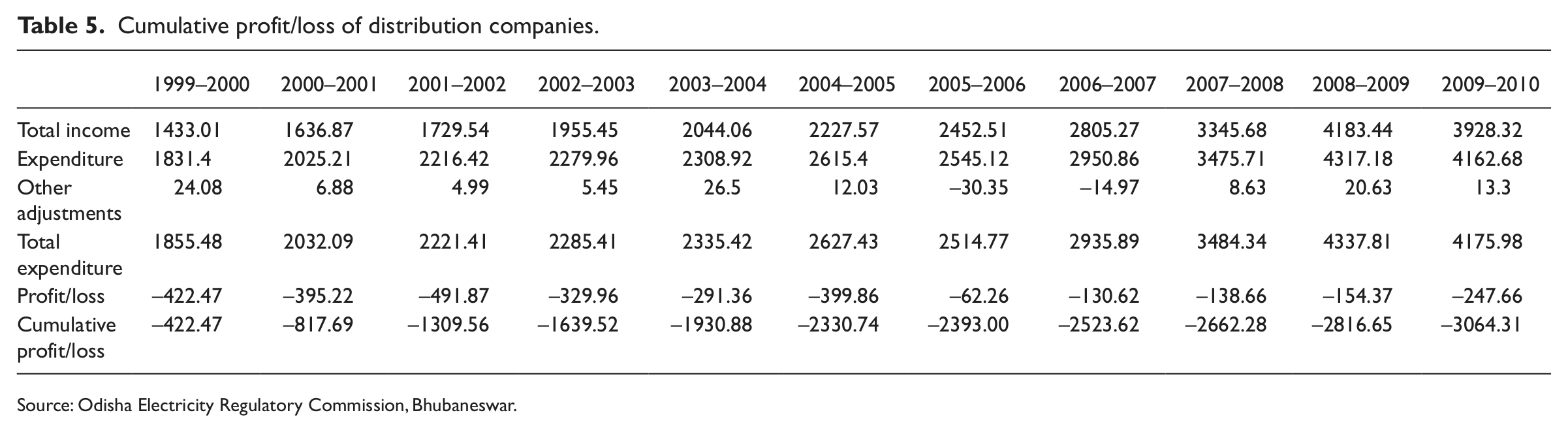

Firstly, it has failed to recover costs even when measured in accounting terms. This is because the average realization has always been lower than the average cost in all the distribution companies, resulting in losses. A comparison of average realization with the average costs incurred by the distribution companies is presented in Table 4. The table shows that the average realization always remained below average costs. Although the cost recovery through tariffs has shown an improvement after reform, the distribution companies have failed to recover costs in an accounting sense. If the cost is assessed by taking the market rate of interest in determining interest payments, and if the depreciation is calculated in terms of replacement cost, losses would be significantly larger. Analysis of the audited profit and loss account of the distribution companies reveals that they have total cumulative loss of Rs 3064 crore up to the year ending 31 March 2010. Although the total income has increased from Rs 1433.01 crore in 1999–2000 to Rs 3928.32 crore in 2009–2010, the expenditure has always been more than the income, growing from Rs 1855.48 crore in 1999–2000 to crore Rs 4175.98 in 2009–2010 (Table 5).

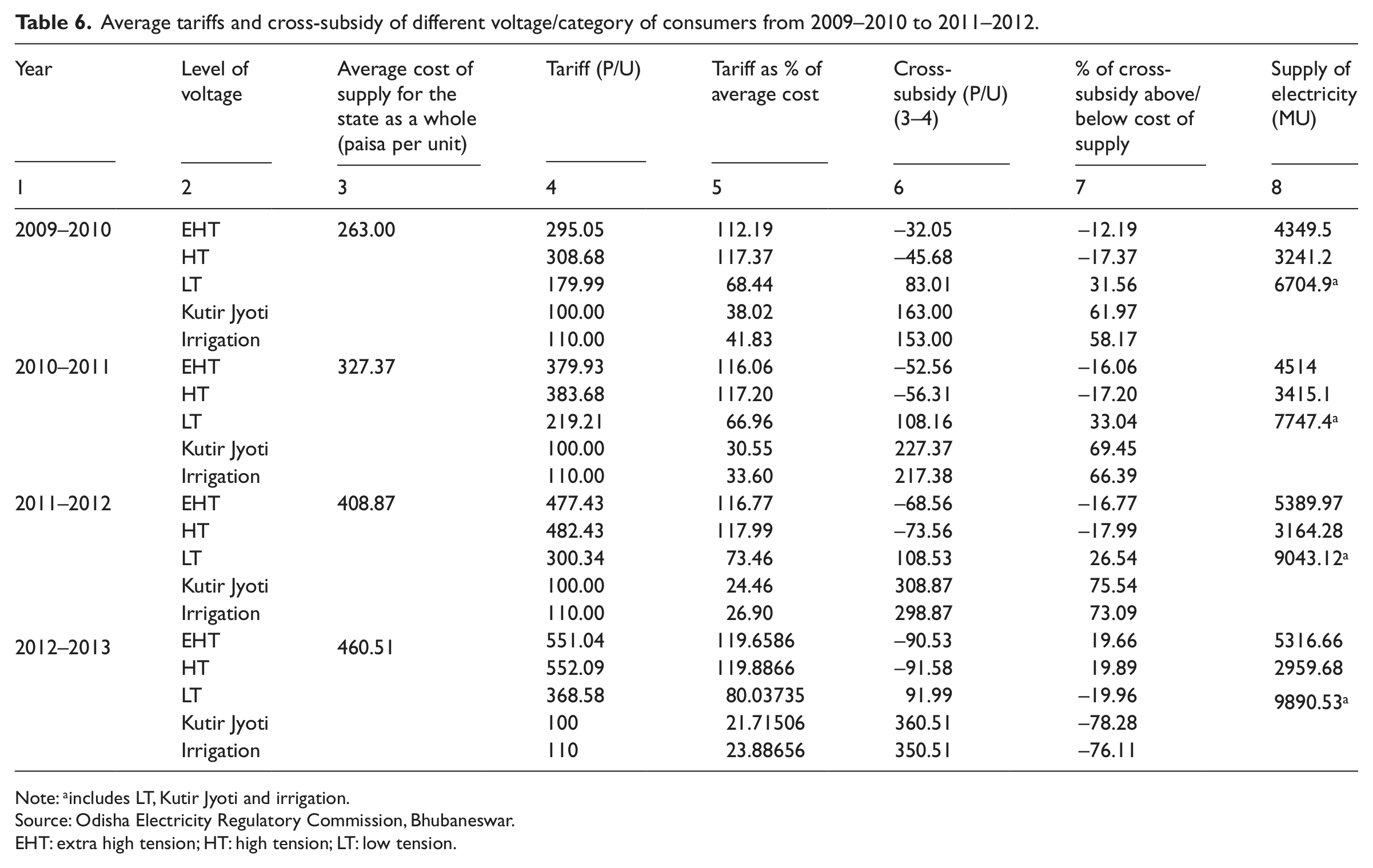

Secondly, economic considerations do not seem to have dictated the determination of tariffs. In this event, the tariffs on different consumer categories bear no relationship to the marginal costs of supplying electricity to them. In fact, in some cases the tariffs are inversely related to the average costs underlying the importance of political factors in their determination, resulting in cross-subsidization (Table 6).

Thirdly, levying very small charges on farmers’ consumption has resulted in uneconomic use of electricity, and also has rendered accurate accounting of consumption by various sectors difficult. The average tariff for irrigation is 110 paisa, whereas the average cost of supply is 408.87 paisa for financial year 2011–2012 and thereby the utilities receive about 73% of the cross-subsidy paid by other categories of consumers. It should be noted that agricultural consumers get their power supply at the LT end, where the unit costs of supply are more than that at the HT end. Despite this, the average revenue realized from agricultural users is far below even the system-wide average cost per unit.

For the domestic category, the average tariff was also below the average unit cost of supply in the state. On the other hand, industrial users are subject to tariffs much higher than the cost of supplying electricity to them, partly to cross-subsidize agricultural and domestic consumers. The average tariffs for the commercial category are above the industrial average tariffs. Industrial consumers, in addition to facing frequent power cuts and outages, have to pay a much higher price than the unit costs. It is therefore not surprising that many of them have found it economical to insulate themselves from an unstable supply of electricity by investing in captive generation capacity.

Trends in average cost recovery in Odisha.

Source: Odisha Electricity Regulatory Commission, Bhubaneswar.

Cumulative profit/loss of distribution companies.

Source: Odisha Electricity Regulatory Commission, Bhubaneswar.

Average tariffs and cross-subsidy of different voltage/category of consumers from 2009–2010 to 2011–2012.

Note: aincludes LT, Kutir Jyoti and irrigation.

Source: Odisha Electricity Regulatory Commission, Bhubaneswar.

EHT: extra high tension; HT: high tension; LT: low tension.

It should be noted that for agricultural users, and domestic, commercial and industrial customer categories, marginal prices increase with the quantity of electricity consumed. This is because of an increasing multi-part tariff. This type of tariff is justified on the basis of ability to pay and the need for power conservation, especially by large users. However, due to the cross-subsidy given to the consumers availing electricity at the level of LT, including Kutir Jyoti and irrigation, there is adverse impact on the financial health of the distribution companies. The state government is not giving any subvention for the loss to the electricity sector due to the cross-subsidy to LT, Kutir Jyoti and irrigation sectors and, hence, there is no damage to the state finance. However, the electricity sector is adversely affected due to the cross-subsidy.

Different pricing of electricity to different categories of consumers results in cross-subsidies to some sectors and taxes on others due to the policy of cross-subsidization (Table 6). These estimates are based on the formula

where AC is the average cost of electricity supply for the state as a whole and ATi is the average tariff for consumer category i. The above method of measuring cross-subsidy, even in an accounting sense, is questionable. The correct accounting estimates of cross-subsidies should be based on the following formula:

where ACi is the average cost of supplying electricity to the i th consumer category. Since the unit costs of electricity for agricultural and domestic users are higher than unit costs at the state level, and as the unit costs of industrial users are lower than the average cost for the state as a whole, it can be concluded that the estimates of subsidies for the agricultural and domestic categories given in Table 6 are biased downward and the cross-subsidies are biased upwards.

A cost-reflective tariff structure would normally result in the lowest tariffs being charged to industrial customers, which have the highest consumption and load factor. The highest tariffs would be paid by household customers.

Hence, the pricing policy followed in Odisha is far removed from rational principles. This uneconomic pricing policy has an adverse impact on the financial health of the distribution companies, the incentives and consequences for inter-sectoral resource allocation and the lack of cost consciousness and demand-side management.

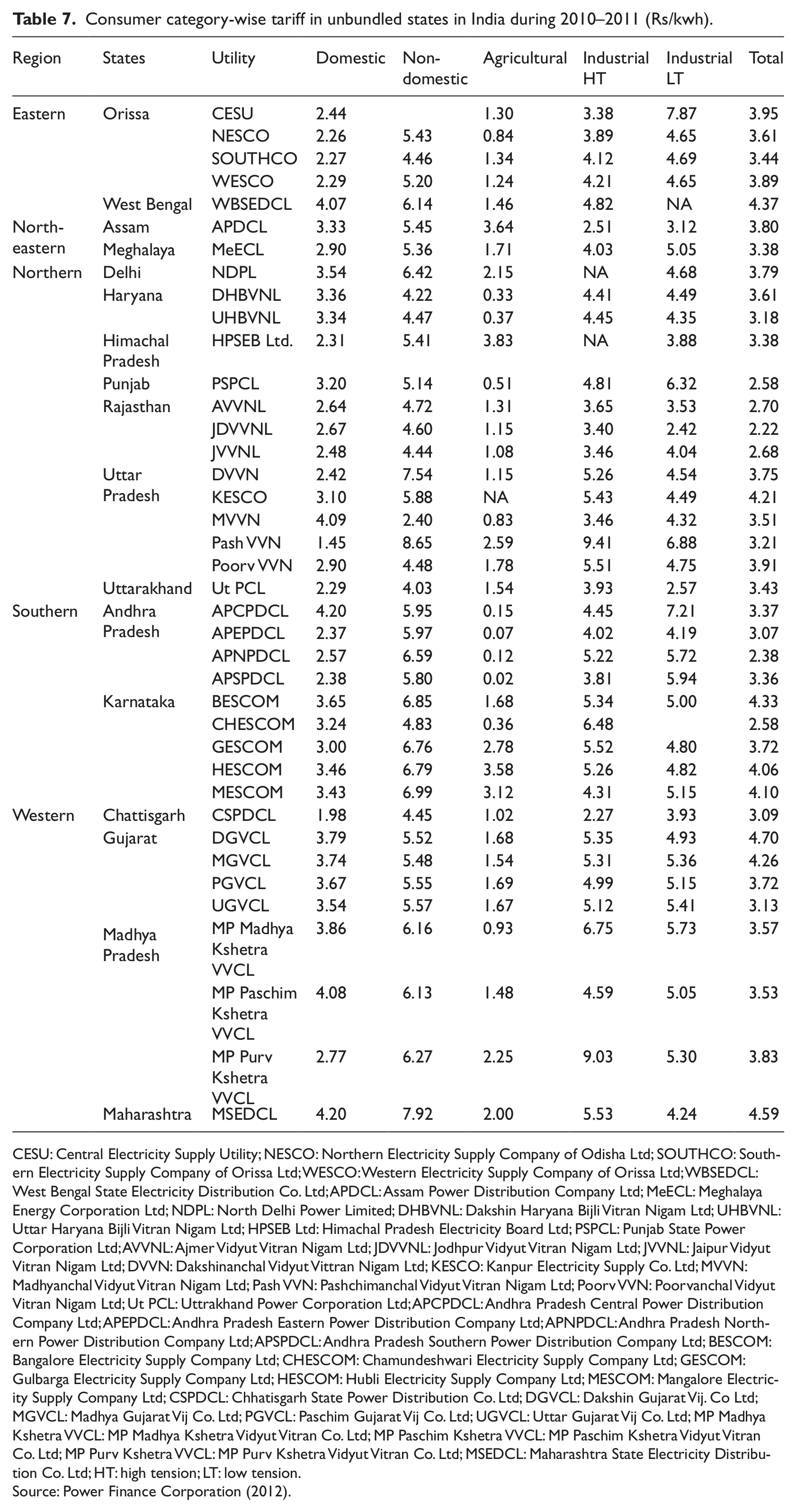

The tariff in the state can be compared with other states in India. It can be seen from Table 7 that the tariff per unit from the domestic category is one of the lowest in the country for domestic consumers (Table 7). Since the price is unable to recover the cost, it has an adverse impact on the power sector industry.

Consumer category-wise tariff in unbundled states in India during 2010–2011 (Rs/kwh).

CESU: Central Electricity Supply Utility; NESCO: Northern Electricity Supply Company of Odisha Ltd; SOUTHCO: Southern Electricity Supply Company of Orissa Ltd; WESCO: Western Electricity Supply Company of Orissa Ltd; WBSEDCL: West Bengal State Electricity Distribution Co. Ltd; APDCL: Assam Power Distribution Company Ltd; MeECL: Meghalaya Energy Corporation Ltd; NDPL: North Delhi Power Limited; DHBVNL: Dakshin Haryana Bijli Vitran Nigam Ltd; UHBVNL: Uttar Haryana Bijli Vitran Nigam Ltd; HPSEB Ltd: Himachal Pradesh Electricity Board Ltd; PSPCL: Punjab State Power Corporation Ltd; AVVNL: Ajmer Vidyut Vitran Nigam Ltd; JDVVNL: Jodhpur Vidyut Vitran Nigam Ltd; JVVNL: Jaipur Vidyut Vitran Nigam Ltd; DVVN: Dakshinanchal Vidyut Vittran Nigam Ltd; KESCO: Kanpur Electricity Supply Co. Ltd; MVVN: Madhyanchal Vidyut Vitran Nigam Ltd; Pash VVN: Pashchimanchal Vidyut Vitran Nigam Ltd; Poorv VVN: Poorvanchal Vidyut Vitran Nigam Ltd; Ut PCL: Uttrakhand Power Corporation Ltd; APCPDCL: Andhra Pradesh Central Power Distribution Company Ltd; APEPDCL: Andhra Pradesh Eastern Power Distribution Company Ltd; APNPDCL: Andhra Pradesh Northern Power Distribution Company Ltd; APSPDCL: Andhra Pradesh Southern Power Distribution Company Ltd; BESCOM: Bangalore Electricity Supply Company Ltd; CHESCOM: Chamundeshwari Electricity Supply Company Ltd; GESCOM: Gulbarga Electricity Supply Company Ltd; HESCOM: Hubli Electricity Supply Company Ltd; MESCOM: Mangalore Electricity Supply Company Ltd; CSPDCL: Chhatisgarh State Power Distribution Co. Ltd; DGVCL: Dakshin Gujarat Vij. Co Ltd; MGVCL: Madhya Gujarat Vij Co. Ltd; PGVCL: Paschim Gujarat Vij Co. Ltd; UGVCL: Uttar Gujarat Vij Co. Ltd; MP Madhya Kshetra VVCL: MP Madhya Kshetra Vidyut Vitran Co. Ltd; MP Paschim Kshetra VVCL: MP Paschim Kshetra Vidyut Vitran Co. Ltd; MP Purv Kshetra VVCL: MP Purv Kshetra Vidyut Vitran Co. Ltd; MSEDCL: Maharashtra State Electricity Distribution Co. Ltd; HT: high tension; LT: low tension.

Source: Power Finance Corporation (2012).

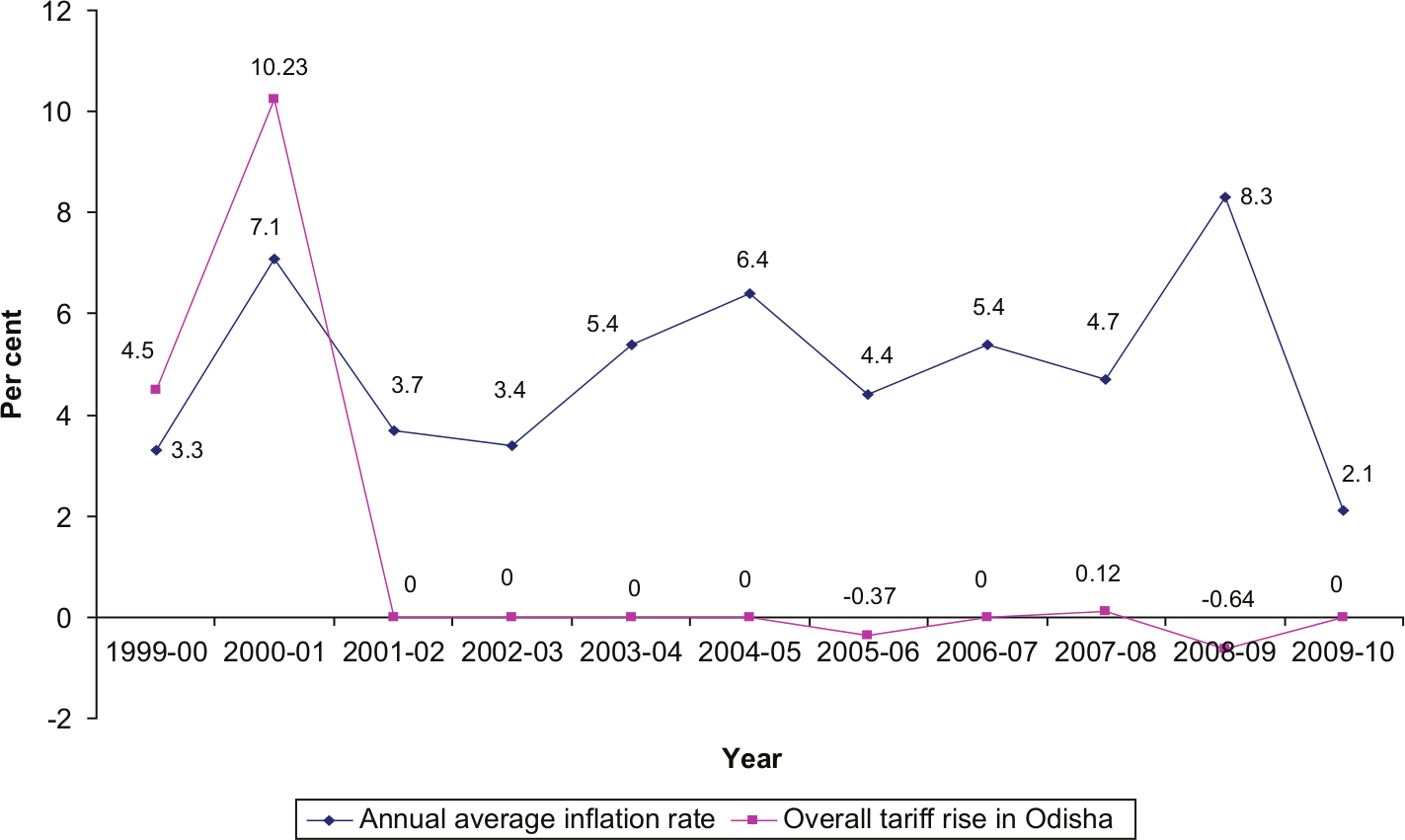

Another aspect of the tariff after reform is that there had been no tariff rise from 2001–2002 to 2009–2010, except for some minor changes. In fact, the annual increase in retail tariff had been much smaller and sometimes negligible as compared to the prevailing average rate of inflation (Panigrahi, 2009). Normally, the tariff should at least keep pace with inflation, otherwise the investors are likely to get a negative return. However, it is observed that after 2009–2010 that there is a significant increase in the tariff (Figure 2). It has increased at the rate of 30.6% during 2010–2011, which is much higher than the inflation rate. Hence, the pricing of electricity in Odisha, based on cost-plus regulation, is far removed from rational pricing principles. It is suggested that the state should try for incentive-based regulation in the form of price cap regulation for better pricing and sustainability of the power sector in the state.

Percentage rise in electricity traffic and inflation.

Summary and conclusions

Odisha embarked upon the process of power sector reforms in 1995 with the enactment of the Orissa Electricity Reform Act and a radical programme of reform to address the fundamental issues underlying the poor performance of the OSEB and to revive its moribund electricity industry. The key features of the reform programme were restructuring and unbundling of the OSEB; private sector participation in generation, transmission, distribution and supply; establishment of an independent regulatory body; competitive bidding for procurement of power in new generation; a licensing system in respect of the T&D activities; and tariff setting to attract investment from private investors.

Odisha adopted the average cost pricing principle for determination of electricity price during the reform period. The regulation adopted by the OERC is the RoR regulation, which is also known as cost-plus regulation. This is a traditional form of regulation wherein a company’s historic costs are reviewed and prices are set to allow profits that deliver the required RoR. In this regulation, there are the problems of determining allowable costs, there being very little incentive for a firm to hold down operating costs and there being no clear guideline on how the capital stock should be measured. Since the retail tariff in Odisha applicable to the consumers of electricity is a combination of cost of generation and T&D, all these costs are intended to be recovered from the consumers, which actually distribution companies fail to collect, thereby adding to the cumulative losses. These cumulative losses are to be amortized over the years, thereby jacking up the current prices. The cost of regulation, wherein all the costs of the distribution companies are passed through, affects pricing as inefficiencies are built up in the price.

This process of tariff determination not only takes a long time but also involves huge cost. Further, actual tariffs levied by the OERC are at variance with the broad principles of rational pricing policy, which is incentive compatible and is required to generate resources for reinvestment. This uneconomic pricing policy has adverse impact on the financial health of the distribution companies. For better pricing and sustainability of the power sector in Odisha it is therefore suggested that the state should try for incentive-based regulation in the form of a price cap, which offers a better alternative than the more traditional form of RoR regulation, and has the potential to yield better outcomes in terms of economic efficiency while requiring relatively minimal regulatory effort.

Footnotes

Acknowledgements

The unrevised version of this article was presented at the internal seminar at the Nabakrushna Choudhury Centre for Development Studies, Bhubaneswar, in January 2012. The authors wish to thank Prof. RK Panda and other participants of the seminar for their useful comments and suggestions. The authors also wish to thank the anonymous referee of Journal of Asian and African Studies for the useful comments and recommendation for publication of the article.

Funding

This research received no specific grant from any funding agency in the public, commercial or not-for-profit sectors.