Abstract

This paper examines the impact of diverse financial sources on the export performance of small and medium-sized enterprises (SMEs) in Togo, with a specific focus on gender-based disparities. Utilizing firm-level data from the 2018 General Business Census (RGE), the study employs probit and ordered probit models, validated by the Lewbel instrumental variable (IV) procedure to address endogeneity. The results reveal that while nearly 94% of SMEs rely on microfinance, this access remains insufficient for internationalization. Conversely, formal banking significantly drives export intensity. Interaction analysis reveals a gendered duality: while male-led firms leverage networks more effectively for market entry, female entrepreneurs demonstrate superior marginal efficiency in scaling export intensity once the initial barriers have been overcome. These findings suggest that gender-sensitive financial reforms and institutional guarantee mechanisms are essential for transforming SME potential into sustainable export growth under the AfCFTA framework.

Keywords

Introduction

In the contemporary global economy, small and medium-sized enterprises (SMEs) serve as the primary engines of growth, accounting for 95% of the entrepreneurial landscape and approximately 50% of global GDP (International Trade Center (ITC), 2020, 2021). In Sub-Saharan Africa, and specifically in Togo, these enterprises constitute the heartbeat of socioeconomic development, representing 99.6% of economic units (INSEED, 2019) and generating between 60% and 80% of total employment. Despite this significance, the integration of African SMEs into global value chains remains marginal. In Togo, fewer than 10% of these firms successfully export their goods and services (CCI, 2021), revealing a persistent gap between entrepreneurial potential and international performance that continues to hinder the national economic growth (Mania and Rieber, 2019; Sun, 2021). This disparity underscores the urgent need to examine why the internationalization of Togolese SMEs remains severely limited, despite various institutional initiatives such as the Business Formalization Center (CFE), the National Agency for Promotion and Financing Guarantee for SMEs (ANPGF), and numerous tax exemption schemes.

Recent academic literature suggests that the answer lies in the complex navigation of firms through institutional voids and fragmented financial architectures. According to Tajeddin et al. (2023), the internationalization of SMEs in emerging markets is not solely a product of internal resources but depends on the strategic capacity to mitigate local market failures. In Africa, this dynamic is exacerbated by constraints in access to credit that impose a rigid “financial hierarchy.” Simba et al. (2024) highlighted that African SMEs are often trapped in short-term financing, which is ill-suited for the high fixed costs and inherent risks of exporting. In Togo, this reality is striking: while the traditional banking system remains highly selective, nearly 94% of SMEs turn to microfinance institutions (MFIs) for survival (INSEED, 2019). However, the ability of these funding sources—often perceived as tools for social inclusion rather than industrial growth—to propel firms into foreign markets remains a significant theoretical and empirical “gray area.”

Furthermore, this performance deficit among SMEs can be understood by analyzing the interaction between firm structure and the environment. According to Industrial Organization theory (Scherer and Ross, 1990), a firm’s export performance stems from the “structure–conduct–performance” (SCP) triad, where barriers to market entry and access to strategic resources, such as financing, dictate the capacity to survive in foreign markets. This perspective is complemented by contingency theory (Lawrence and Lorsch, 1967; Mintzberg, 1979), which postulates that export performance depends on an optimal fit between the firm and its context. For Togolese SMEs, this context is defined by institutional voids (Tajeddin et al., 2023) and a fragmented financial architecture in which the vast majority of firms rely on MFIs.

At the core of this financing and export dilemma lies the issue of gender inequality—a performance lever that is often underestimated in macroeconomic analyses. To understand why female-led SMEs in Togo are less involved in exporting, it is necessary to draw upon fundamental theories of female entrepreneurship. On the one hand, liberal feminist theory (Fischer et al., 1993) posits that women face structural discrimination in accessing critical resources. In Togo, unequal land ownership rights drastically limit women’s ability to provide the collateral required by commercial banks, effectively relegating them to microfinance with limited loan amounts. On the other hand, social feminist theory suggests that divergent socialization trajectories result in differences in social capital and institutional trust (Keefer & Knack, 2005, Black et al., 1991). These biases influence “credit filtering”: female managers may face stricter monitoring requirements or engage in self-censorship, hindering not only their market entry (participation) but also their ability to scale (intensity).

Empirically, various factors explain the low participation or performance of SMEs in exports, including firm and manager characteristics (Beleska-Spasova, 2014; Kasema, 2023), technology and innovation (Ortigueira-Sánchez et al., 2022; Radicic and Djalilov, 2019), and access to credit (Raju and Thillai Rajan, 2019). However, the role of specific financing sources in export performance has received little attention, particularly in developing countries where SMEs are largely excluded from traditional banks (Amornkitvikai and Harvie, 2018). Within this context, this paper addresses the following research question: what is the effect of different financing sources on the export performance of SMEs in Togo?

Consequently, this article analyzes the impact of various funding sources on the export performance of Togolese SMEs, placing gender disparities at the center of the analysis. It examines the determinants of access to different financing sources and evaluates their effect on export intensity, with an emphasis on gender-based analysis. This study makes a threefold contribution to the literature. First, it situates the Togolese case within global debates on institutional constraints in Africa by testing whether the predominance of microfinance constitutes a “glass ceiling” for internationalization. Second, it refines the conceptual framework of gender by demonstrating how guarantee mechanisms and social capital modulate financing effectiveness. Finally, by distinguishing different scales of export intensity, this paper provides policymakers with empirical tools to calibrate support policies that are no longer gender-neutral, but truly inclusive and oriented toward global competitiveness.

The remainder of the paper is structured as follows: The Brief literature review section presents the literature review, while the Materials and methods section details the methodology. The empirical results are presented in the Results and discussion section. Finally, the conclusion and economic policy implications are discussed in the final section.

Brief literature review

Restrictions on access to external finance arise from pervasive structural factors, most notably information asymmetries and agency problems (Fazzari et al., 1987; Stein, 2003). Theoretically, SME export performance is anchored in three primary approaches: industrial organization (IO) theory, the resource-based view (RBV), and contingency theory. The IO theory attributes international performance to the external environment and to the firm’s specific marketing advantages (Morgan et al., 2003; Zou and Stan, 1998). Conversely, the RBV perspective emphasizes strategic resources, technical capabilities, and proprietary know-how as drivers of the competitive advantages necessary for export market positioning (Laghzaoui, 2009). Finally, contingency theory explains performance through the alignment between a firm’s internal structure and its external context (Robertson and Chetty, 2000; Yeoh and Jeong, 1995). Together, these theories provide the conceptual framework for identifying the determinants of SME export performance.

Empirically, while the relationship between financial access and SME performance has been widely studied, the role of specific financing sources has received limited attention, particularly regarding SMEs in developing countries. In Thailand, Amornkitvikai and Harvie (2018) found that both the Export-Import Bank of Thailand and the Department of International Trade Promotion (DITP) played pivotal roles in enhancing export participation and intensity for both SMEs and large manufacturing firms. Furthermore, they noted that firms relying on informal capital from friends and family tended to participate less in foreign markets, while firm-level technological innovation significantly boosted international engagement.

Focusing on the preferred financing modes for exports, Chugan and Singh (2014) concluded that commercial bank funds and reinvested profits significantly impact SME export performance. However, they found the effect of development finance sources (such as EXIM Bank, SIDBI, and IFCI) to be negligible when compared to other medium- and long-term financial instruments. Similarly, Abora et al. (2014) emphasized the specific role of bank financing, revealing that access to bank credit improves the likelihood of exporting. They argued that bank finance is essential for covering the substantial fixed costs—such as international marketing, branding, and meeting stringent foreign quality standards. Their study also indicated that older, larger, and more productive firms are more likely to enter export markets, suggesting that policymakers should focus on reducing bottlenecks in commercial bank lending.

While formal banking is crucial for internationalization, microfinance remains significant for domestic performance. Arinzeh (2022) demonstrated that SME growth in Nigeria over a 2-year period was driven by microfinance access. In addition, Raju and Thillai Rajan (2019) found that, while various financing sources impact profitability, institutional finance plays a far more critical role in export performance. They further concluded that increasing bank credit flows is essential for boosting SME exports.

General studies on the finance–export nexus present mixed results. Fowowe (2017) highlighted that finance is vital for the growth of African firms, justifying initiatives to increase capital availability. In contrast, Sibanda et al. (2018) observed a negative impact of financial access on firm performance in Zimbabwe. Furthermore, Wagner (2019) concluded that, contrary to conventional wisdom, a statistically significant negative relationship between severe financial constraints and export activity is seldom robustly established in the literature.

Finally, research has sought to identify the factors explaining the persistent credit challenges faced by SMEs. Wignaraja and Jinjarak (2015) identified several key patterns: (1) SMEs tend to rely on internal sources rather than external finance or trade credit; (2) they often turn to informal non-bank sources when formal credit is denied; (3) there is a positive correlation between bank borrowing and firm characteristics such as financial audits, firm age, and export participation; and (4) the personal assets of owners are often more critical than corporate collateral for bank loans. The authors suggest that improving credit guarantee systems, strengthening bank monitoring, and broadening the range of acceptable collateral are vital pathways to increasing SME access to bank borrowing.

In summary, while the existing literature provides a robust theoretical framework—anchored in IO theory, resource-based, and contingency theories—to explain SME internationalization, empirical evidence on the role of specific financing sources remains fragmented. Studies, such as those by Abora et al. (2014) and Raju and Thillai Rajan (2019), emphasize the dominance of formal bank credit in overcoming fixed export costs; however, they frequently overlook the unique institutional landscape of sub-Saharan Africa, where microfinance and national development funds represent the primary, and often the only, financial touchpoints for SMEs. This study addresses this gap by specifically examining these diverse financial channels in the Togolese context.

Materials and methods

Variables selection, definition, and measurement

The choice of variables in this study is informed by established theoretical frameworks, empirical literature, and the specific socioeconomic context of Togo. To address the research objectives, this analysis employs three primary dependent variables. First, access to financial institutions is operationalized as a binary indicator of formal financial inclusion. Following Quartey et al. (2017), this variable takes the value of 1 if an SME maintains an established business relationship with a formal provider (including commercial banks or MFIs) and 0 otherwise. This measurement captures the firm’s capacity to mobilize essential financial services—such as payments, savings, and credit guarantees—which serve as fundamental prerequisites for growth and internationalization (Aterido et al., 2013). Second, export intensity assesses the scale of international engagement, calculated as the ratio of export turnover to total annual turnover. Following standard classification in the international business literature (Ganotakis and Love, 2012; Minetti and Zhu, 2011), this ratio is categorized into five distinct levels of intensity: (0) no export; (1) low intensity (less than 25%); (2) moderate intensity (25% to 50%); (3) high intensity (50% to 75%); and (4) very high intensity (exceeding 75%). This nuanced classification allows for a robust analysis of how financial access influences not only the initial decision to export but also the subsequent depth of global integration (Wagner, 2007). Finally, for reasons of robustness, we used the continuous ratio of export intensity.

To examine the determinants of these export outcomes, the analysis incorporates two sets of key explanatory variables. Central to the research objective is the gender of the SME manager, operationalized as a binary variable (1 if male-led, 0 if female-led). This distinction allows for rigorous testing of whether structural disparities and “gendered financial exclusion” significantly impede internationalization (Bardasi et al., 2011; Marlow and Patton, 2005). Furthermore, the study disaggregates various sources of finance, specifically distinguishing between national commercial banks, international banking institutions, MFIs, and national program funds. This granular approach is essential for testing the “financial hierarchy” hypothesis, evaluating whether the specific type of financial provider—beyond mere access—differentially mitigates the fixed entry costs and risk exposure inherent in exporting (Minetti and Zhu, 2011).

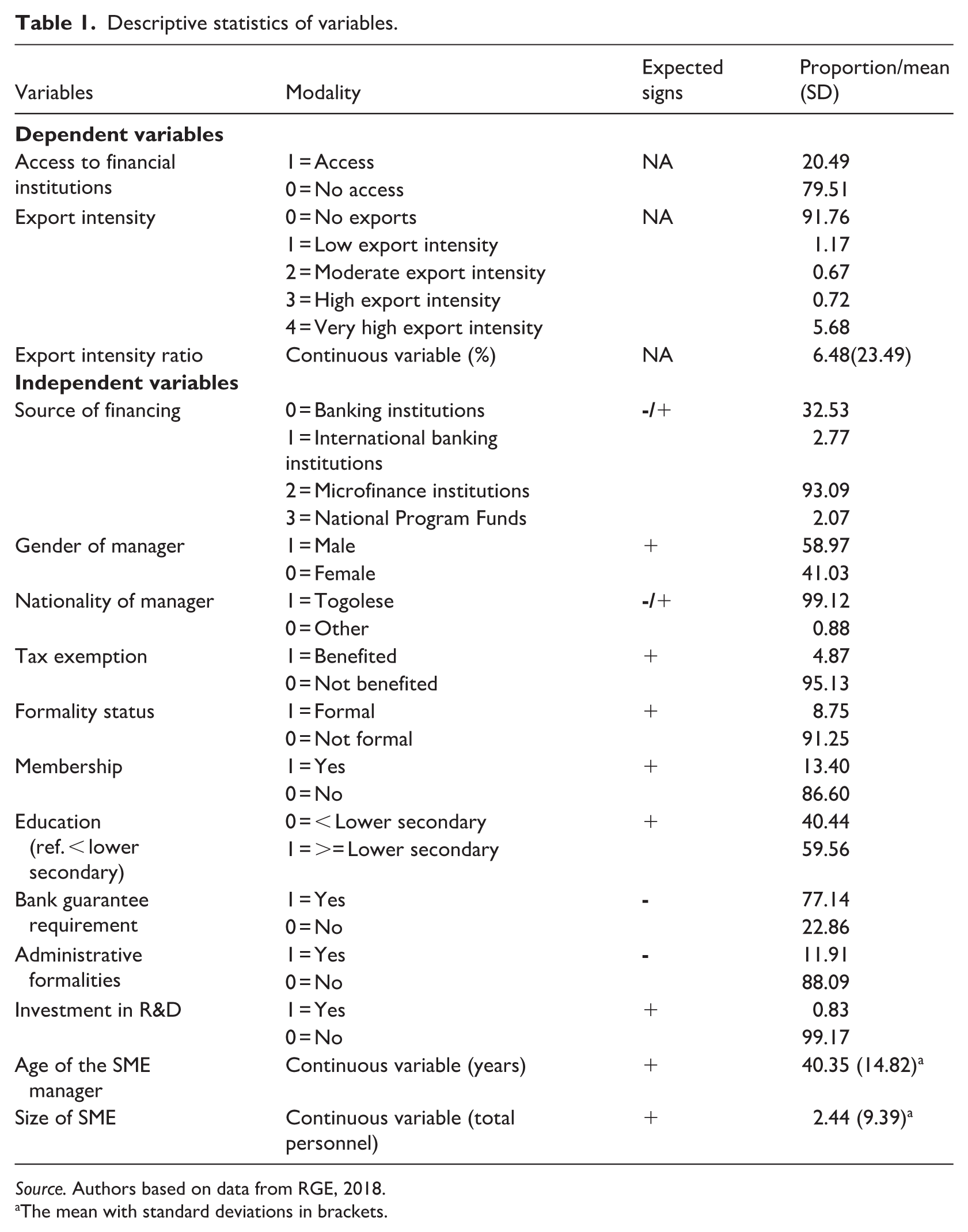

To enhance empirical validity and mitigate potential omitted variable bias, several control variables are included. These encompass the nationality of the manager, tax exemption status, and firm formalization. Organizational membership is included to capture social and network effects (Mertzanis et al., 2024). In addition, the analysis accounts for the manager’s education and age, the firm’s investment in research and development (R&D), and SME size, which are recognized in the IO theory as critical firm-level capabilities (Bernard and Jensen, 1999). Table 1 provides a comprehensive synthesis of all variables included in the analysis, detailing their respective modalities, expected signs, and descriptive statistics.

Descriptive statistics of variables.

Source. Authors based on data from RGE, 2018.

The mean with standard deviations in brackets.

Empirical model

Estimation technique for access to financial institutions

Following the methodology of Amornkitvikai and Harvie (2018), we estimate the determinants of SMEs’ access to financial institutions using a probit model estimated via maximum likelihood (MLE).

The dependent variable is nominal and dichotomous, taking the value of 1 or 0. Estimating such variables using ordinary least squares (OLS) would result in a linear probability model (LPM), which often leads to spurious results, such as predicted probabilities outside the 0–1 range. Furthermore, the use of OLS inherently addresses the issue of heteroscedasticity, a common challenge when analyzing cross-sectional data (Wooldridge, 2013).

Let

This econometric specification is deeply rooted in our multi-theoretical framework, where

This binary outcome indicates whether the firm has successfully established a relationship with a formal financial institution, providing the basis for our subsequent analysis of export performance.

The empirical model for the determinants of access to financial institutions is specified as:

In this equation,

Estimation technique for export intensity

We apply the ordered probit model to analyze the intensity of SME export participation, given that the dependent variable is ordered across five distinct levels: no export, low export intensity, moderate export intensity, high export intensity, and very high export intensity. This hierarchical classification is theoretically critical for distinguishing between the extensive margin (participation) and the intensive margin (scaling) of internationalization.

In line with the performance component of IO theory, export intensity represents the final outcome of a firm’s strategic conduct (Bernard and Jensen, 1999). Moreover, analyzing intensity levels allows us to test the “glass ceiling” hypothesis derived from feminist theories (Marlow and Patton, 2005), exploring whether gendered constraints—such as limited access to large-scale banking credit (Aterido et al., 2013)—prevent female-led SMEs from scaling up, even after they have successfully entered the market (Bardasi et al., 2011).

In general, the ordered probit model is derived from an underlying latent variable model as follows:

This latent variable,

In Equation (5),

The specific form of the econometric model estimated for this purpose is as follows:

In this specification,

To ensure the internal validity of our results, these key variables are supplemented by a vector of controls, including the age of the SME and its manager (ageU and ageD), nationality of manager (nat), and tax exemption status (tax), all of which account for the diverse socioeconomic profile and fiscal environment of Togolese SMEs. The parameters to be estimated are denoted by

Gender-based heterogeneity model

To further explore the specific mechanisms through which gender moderates the impact of financial sources, we extend Equation (6) by incorporating interaction terms. This expanded specification allows us to test whether the marginal effect of each financing channel on export participation differs between male- and female-led SMEs. The model is specified as follows:

Equation (7) specifies the interaction model, where

Instrumental Variable (IV) approach: Sensitivity analysis

To ensure the robustness of our findings and address potential endogeneity bias, we employ an IV approach. A valid instrument must be correlated with financial access but uncorrelated with the error term (Wooldridge, 2013). While the literature often suggests external instruments such as geographic distance to financial institutions (Degryse and Ongena, 2005; Mian, 2006) or local interest rates (Rice and Strahan, 2010), these variables are unavailable in our dataset.

Consequently, we follow the method of Lewbel (2012) to construct internal instruments by leveraging heteroskedasticity in the first-stage regressions (Baum and Schaffer, 2026). This approach is widely recognized in recent economic literature for addressing endogeneity when external instruments are scarce (Abor et al., 2024; Mishra and Smyth, 2015). Finally, to mitigate potential information loss from the categorical export intensity indicator, we perform a sensitivity check using the continuous volume of export intensity. This ensures that our results remain robust across different functional specifications.

Data source

The data used in this study are derived from the most recent General Business Census (Recensement Général des Entreprises, RGE) conducted by the National Institute of Statistics and Economic and Demographic Studies (INSEED) in 2018 in Togo. The dataset provides comprehensive information on financial sources, export activities, and the socioeconomic and demographic characteristics of firm managers, among other variables. While the original census encompasses 119,318 businesses, including large corporations, this study specifically focuses on a subset of data pertaining to SMEs. The survey instrument and the complete database are publicly accessible on the official INSEED-Togo website (https://inseed.tg).

Results and discussion

Descriptive results analysis

Descriptive statistics

Table 1 presents the descriptive statistics for the variables included in the model. The data reveal that the average age of an SME manager in Togo is 40 years, with a standard deviation of 15 years. On average, these SMEs employ 2.44 people, and the average duration of business operations is 5 years.

The data also indicate that 20.49% of SMEs have access to financial institutions, specifically national and international banks, MFIs, and national program funds. Conversely, only 3.15% of SMEs are involved in exporting activities. In terms of the institutional environment, 8.75% of SMEs in Togo are formalized, while 4.87% have benefited from tax exemptions. Furthermore, approximately 41% of SMEs are led by women. Finally, SMEs in Togo are almost exclusively owned by Togolese nationals (99.12%).

Sources of finance and SME export participation: Descriptive analysis

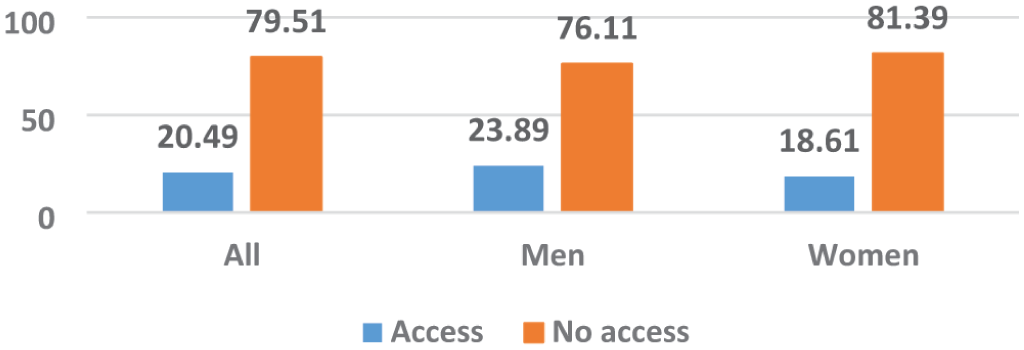

Figure 1 reveals disparities in terms of access to financial institutions according to the gender of the SME manager in Togo. Specifically, 23% of male-owned SMEs have access to financial institutions, compared to only 18.61% of female-led SMEs.

SME access to financial institutions by manager’s gender.

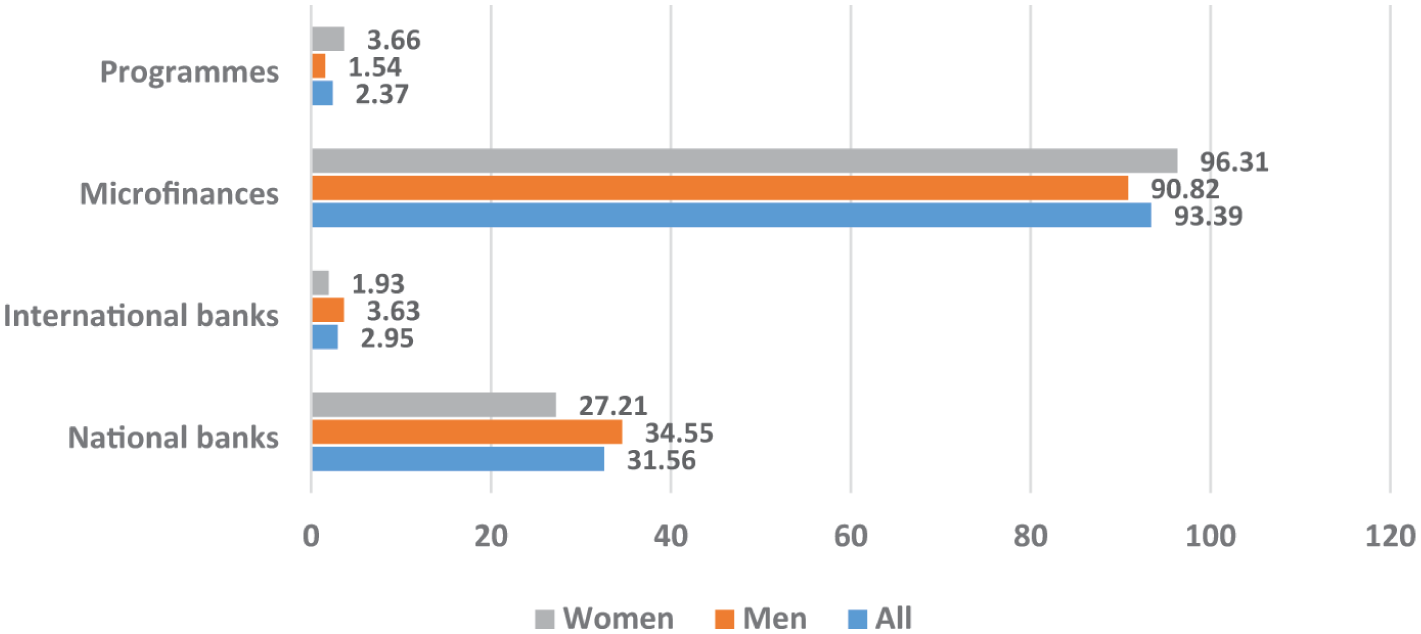

Figure 2 shows that the vast majority of SMEs in Togo rely solely on MFIs to finance their activities (over 93%), regardless of the gender of the manager. This finding is particularly striking, given that MFIs often offer loans at double-digit interest rates in Togo. This predominance could be explained by the fact that SMEs are generally excluded from traditional banking systems due to stringent collateral requirements and complex administrative formalities. Conversely, national program funds and international banks represent the least utilized financial channels by SMEs.

Sources of finance utilized by SMEs, by manager’s gender.

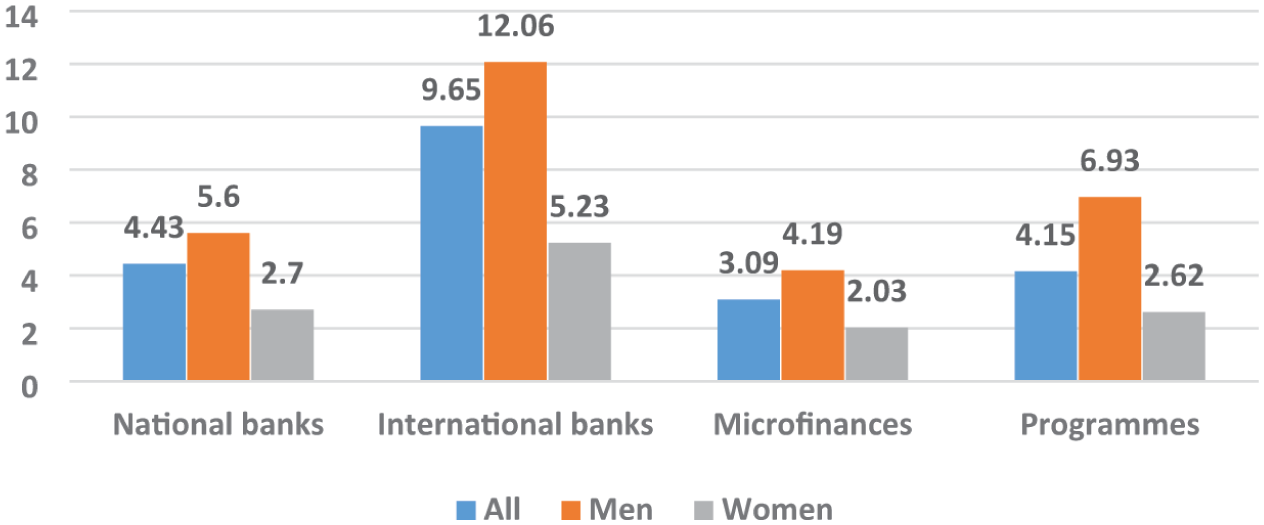

Figure 3 illustrates that access to various sources of finance significantly impacts the export participation of SMEs in Togo. Although the vast majority (93%) of SMEs rely on microfinance as their primary source of funding, the data reveal that firms with access to international banks exhibit the highest levels of export participation (9.65%), regardless of the manager’s gender. These are followed by SMEs funded by national banks (4.43%) and national program funds (4.15%). In contrast, SMEs primarily accessing MFIs are the least involved in the export of goods and services, with a participation rate of merely 3.09%. Furthermore, gender-based disparities persist across all financial sources, with male-managed SMEs consistently outperforming female-led SMEs in export involvement. The widespread reliance on microfinance among Togolese SMEs occurs within a context of scarce formal credit, forcing these enterprises to depend on alternative financing mechanisms (Nuhu et al., 2026).

SME export participation by type of financial institution.

Sources of finance and export intensity of SMEs: An econometric analysis

Determinants of SME access to financial institutions in Togo

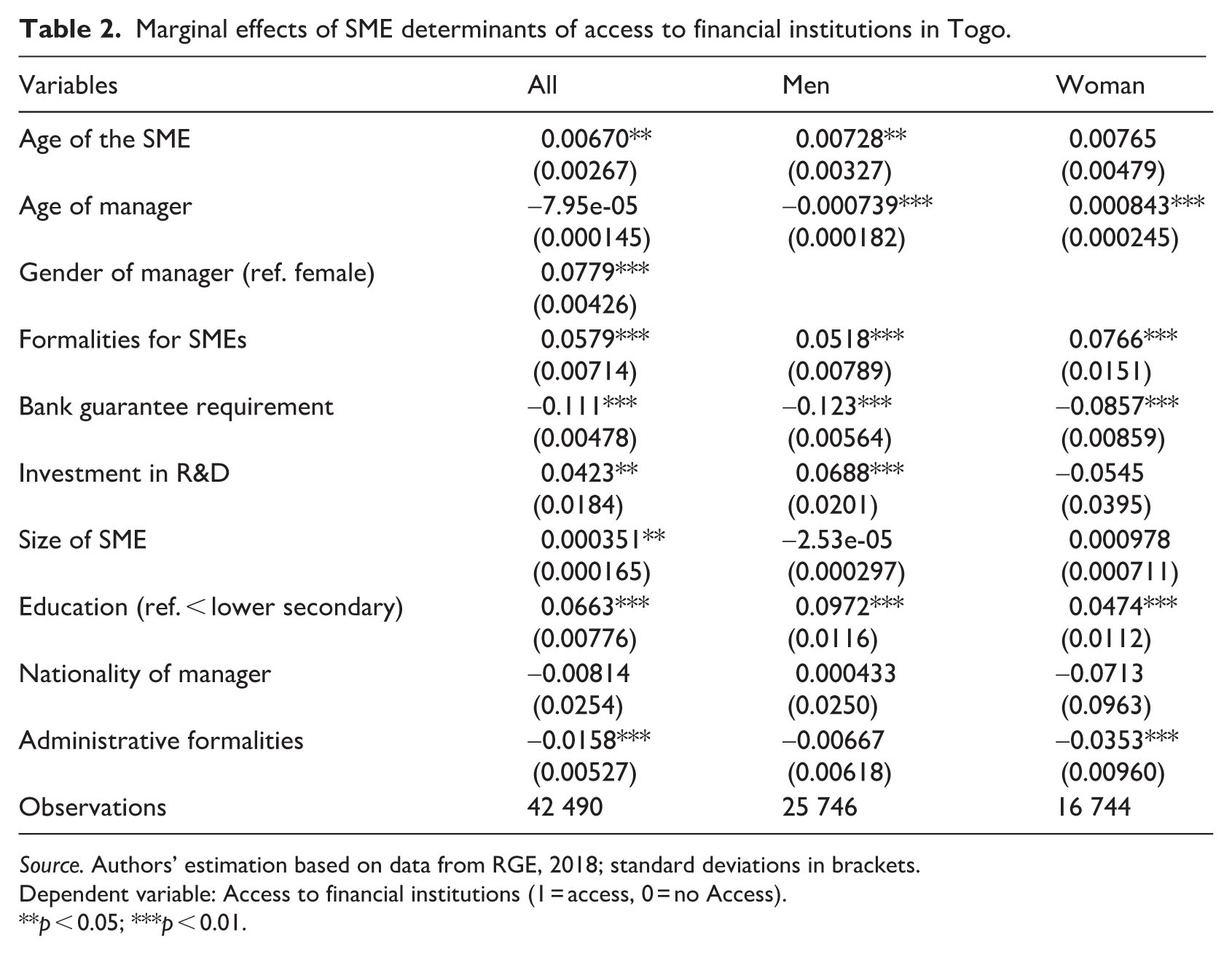

Since the coefficients of probit or logit models are not directly interpretable and only indicate the direction of the relationship (Yovo and Gnedeka, 2023), Table 2 reports only the average marginal effects.

Marginal effects of SME determinants of access to financial institutions in Togo.

Source. Authors’ estimation based on data from RGE, 2018; standard deviations in brackets.

Dependent variable: Access to financial institutions (1 = access, 0 = no Access).

**p < 0.05; ***p < 0.01.

The results demonstrate that the managerial human capital plays a pivotal role in gaining access to financial institutions for SMEs in Togo. A higher level of education significantly increases the probability of an SME securing institutional access; specifically, this probability is 6.66 percentage points for managers with more than lower secondary. However, this effect remains notably stronger for male-led SMEs (9.72%) compared to those managed by women (4.74%).

In light of Human Capital Theory (Becker, 1964) and Capabilities Approach (Sen, 1999), the educational attainment serves as a strategic intangible asset that facilitates access to external financing. The positive relationship operates primarily through cognitive competence and information-processing channels. Highly educated managers possess a superior ability to navigate complex financial systems, interpret technical regulatory requirements, and utilize reliable market information. From a capability perspective, education is not merely a credential but a functional power that enables the manager to convert available financial opportunities into effective inclusion for the firm. This enhanced capacity explains the observed increase in the probability of financial inclusion. Our findings align with the work of Woldie et al. (2008), who emphasized that the education level of directors is a critical determinant of access to finance, while differing from Amornkitvikai and Harvie (2018), who found no significant effect of education in their study.

The age of the SME exerts a positive and significant effect on the probability of accessing financial institutions. Each additional year of operation increases this probability by 0.67% overall and by 0.72% for businesses managed by men. This result suggests that younger firms are more sensitive to cash flow constraints yet often lack the experience or reputation necessary to secure institutional credit (Devereux and Schiantarelli, 1990; Oliner and Rudebusch, 1992). Furthermore, these findings support Penrose’s (1952) growth theory, which posits that startups face greater difficulties in accessing finance due to information asymmetry and a lack of history.

Strikingly, the results in Table 2 indicate that male-led businesses have a 7.79-percentage-point higher probability of accessing financial institutions compared to their female counterparts. This finding is consistent with the descriptive analyses in the previous section and with existing literature highlighting gender inequality in credit access (Martinez, 2007). In the Togolese context, this may suggest that men who successfully formalize their businesses are more likely to seek institutional support. Indeed, stringent collateral requirements imposed by formal financial institutions create a significant gender gap in terms of access. Gender differences in access to collateral, credit screening processes, social capital, and institutional trust explain these disparities within the framework of this study. Finally, business formalization has a positive and significant effect on the probability of accessing financial institutions, whereas banking guarantee requirements act as a deterrent to SME financial inclusion in Togo.

Effects of financial sources on export intensity of SMEs in Togo

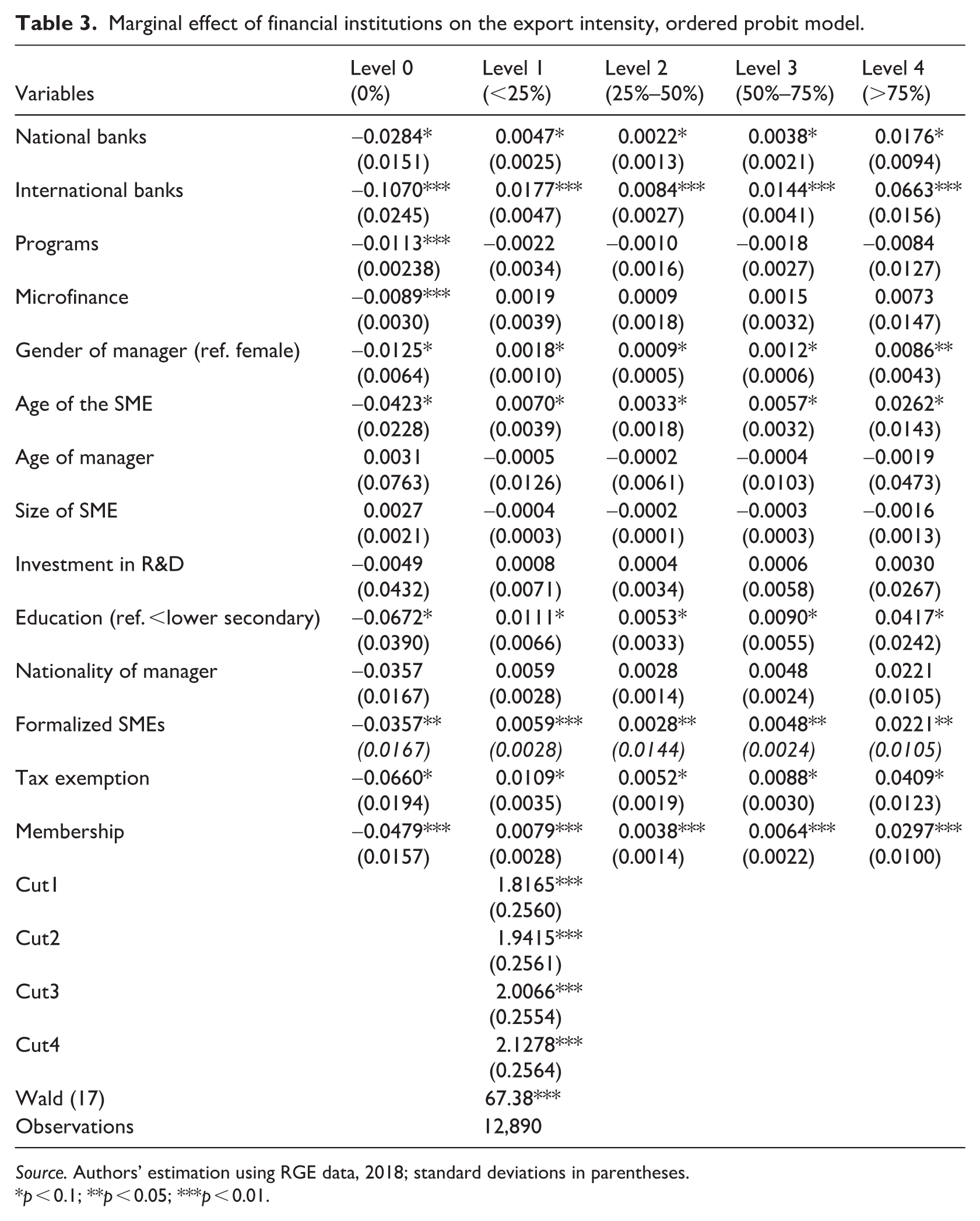

The model in Table 3 is statistically robust (Wald

Marginal effect of financial institutions on the export intensity, ordered probit model.

Source. Authors’ estimation using RGE data, 2018; standard deviations in parentheses.

p < 0.1; **p < 0.05; ***p < 0.01.

Indeed, our empirical estimates reveal that access to international banking institutions by SMEs in Togo reduces the probability of non-export by 10.7 percentage points (p < 0.01) and boosts intensive exports by 6.6 percentage points. This means that international banks act as gatekeepers offering sophisticated services (international collateral, currencies, cross-border networks) that are essential for navigating institutional voids in emerging or global markets (Simba et al., 2024; Tajeddin et al., 2023). As far as domestic banks are concerned, although their impact is significant (+1.7% at level 4), it is almost four times less than that of international banks. This indicates that Togo’s domestic banking sector is still too focused on the domestic market, limiting the shift to high export intensity (Amornkitvikai and Harvie, 2018). This result is in line with IO theory, which highlights the ability of a firm to access scarce strategic resources to overcome structural market barriers.

Our results reveal a nuanced but significant role of non-banking financing mechanisms in initiating the internationalization process. Access to government programs and microfinance reduces the probability of non-participation in export (level 0) by 1.13 (p < 0.01) and 0.89 percentage points (p < 0.01), respectively. Although these effects confirm a positive contribution to market entry, their low magnitude compared to banking institutions underscores a structural paradox. This observation implies that MFIs in Togo, while facilitating the crossing of the initial barrier, remain structurally calibrated toward subsistence micro-commerce rather than industrial-scale transformation (Sonhaye and Kounetsron, 2022). From the perspective of contingency theory, this phenomenon reflects a lack of optimal “strategic fit”: there is a mismatch between the scope of the financial tool (MFI) and the complex environment of exporting SMEs (Lawrence and Lorsch, 1967). These findings suggest that policymakers need to make greater efforts to strengthen funding mechanisms (national program funds) for SMEs in Togo.

While these financial institutions help cover certain variable startup costs, they prove insufficient to mitigate the massive fixed entry costs and exchange rate risks inherent in cross-border trade. Indeed, the relative ineffectiveness of microfinance on export intensity reveals a financial “glass ceiling.” While it facilitates initial market access (extensive margin), the mismatch between short-term micro-loans and long-term export cycles hampers volume growth (intensive margin). This result corroborates the works of Sodokin (2022): SMEs excluded from the traditional banking system turn to microfinance by default. However, due to a lack of greater financial capacity, this support tends to keep firms within and “inward-looking” vision, limiting their progression toward higher intensity levels. Thus, MFIs act as a safety net for initial participation but have yet to serve as a driver for high-level export performance.

Institutional levers also show significant effectiveness. The tax exemptions have a major positive effect (+4.09%) on the export intensity at level 4 of SMEs. This result can be explained by the fact that the tax exemption would provide immediate liquidity by allowing SMEs to absorb financial volatility and thus invest in the domestic capacity needed to export. In addition, compliance with standards or the formalization of companies (+2.21%) and membership of networks (+2.97) appear to be prerequisites in Togo for the intensive participation of SMEs in exports. Compliance with standards reduces transactional uncertainty, facilitating access to global markets (Caruana et al., 1998).

Finally, our estimates indicate that being male reduces the probability of non-export by 1.25% and significantly increases the probability of intensive export (level 4) by 0.86%. This result validates the liberal feminist theory according to which men have better access to productive resources and networks of influence in Togo. This higher endowment of financial and social capital makes it easier for them to overcome barriers to entry into international markets. Conversely, women suffer from a “resource bias” that limits their progress toward high export levels (Fischer et al., 1993; Nuhu et al., 2026). From the perspective of feminist social theory, our results suggest that male outperformance is explained by deeper integration into formal business networks and lower exposure to time poverty constraints. Male leaders have greater flexibility to engage in the administrative procedures and business trips required for intensive export (Safari and Saleh, 2020; Wonyra et al., 2021).

Gender-based heterogeneity and institutional channels

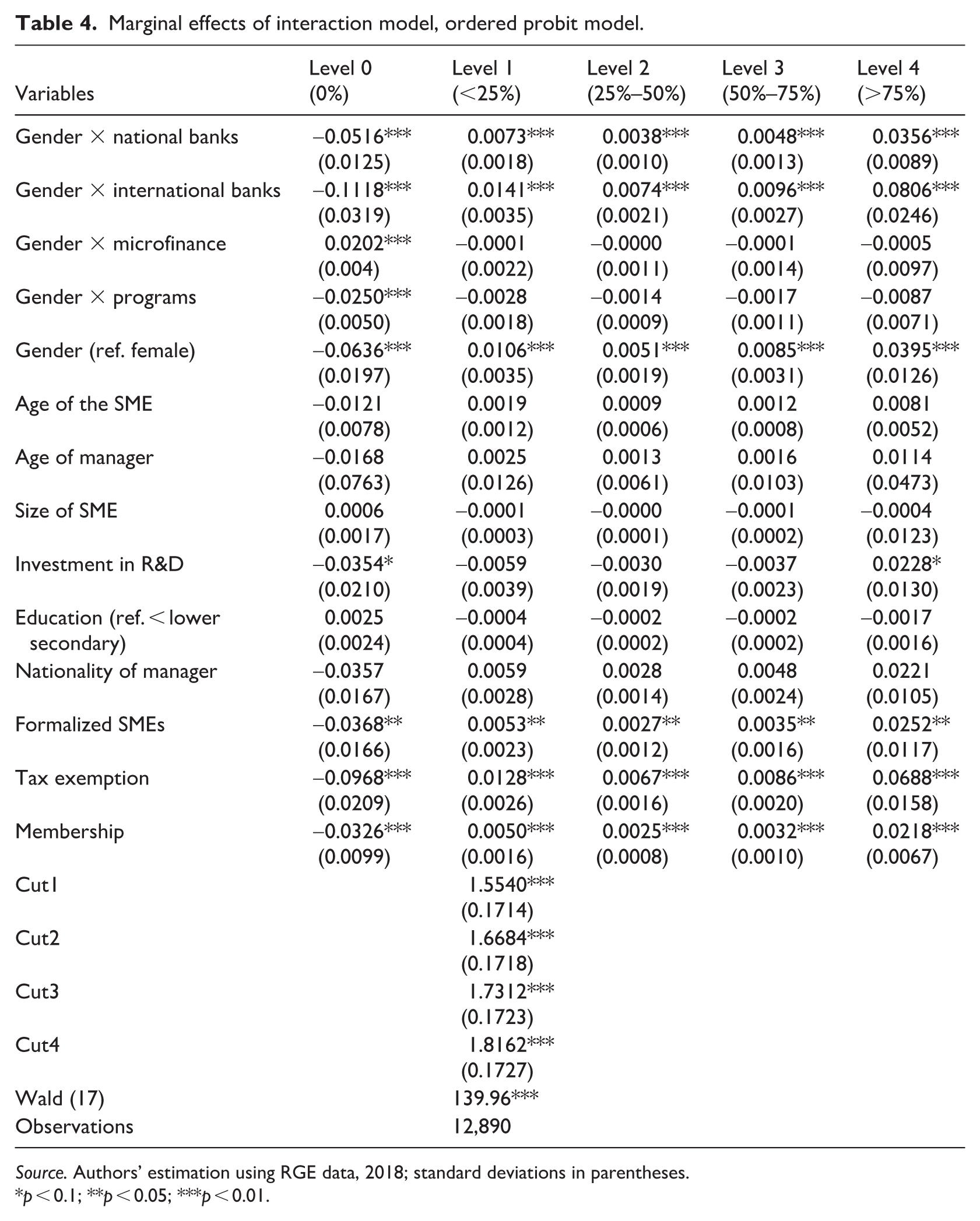

The model in Table 4 is statistically robust (Wald

Marginal effects of interaction model, ordered probit model.

Source. Authors’ estimation using RGE data, 2018; standard deviations in parentheses.

p < 0.1; **p < 0.05; ***p < 0.01.

The interaction between gender and access to international banks has a notable impact on export intensity at level 4 (+8.06 percentage points). This result suggests that men benefit disproportionately from international bank credit in overcoming barriers to market entry. In Togo, this gap can be explained by the “collateral gap”: informal institutional constraints on land ownership limit women’s ability to provide the collateral required by international banks to finance large export volumes. This result is consistent with liberal feminist theory, which suggests that disparities in performance arise from unequal access to productive resources (Fischer et al., 1993).

Our results also reveal that the interaction between gender and access to national banks is also significant and positive at level 4 (+3.56%). Male leaders often benefit from greater mobility and denser information networks. Conversely, the direct effect of gender (ref. female) shows that female entrepreneurs demonstrate strong intrinsic resilience. However, this performance is constrained by “time poverty” linked to the double burden (domestic and professional), restricting their ability to navigate complex administrative procedures (Expósito et al., 2022; Safari and Saleh, 2020). Furthermore, when considering the interaction between gender and access to MFIs and public programs, only slight improvement is observed. The probability of non-participation (level 0) decreases by 2.02% and 2.50% for male-led SMEs with access to microfinance and public programs, respectively. The results indicate that such programs fail to fully compensate for the structural constraints mentioned above (Tajeddin et al., 2023).

Finally, as in the basic model, empirical estimates underline that tax exemption remains the most powerful catalyst of the model (+6.88% at level 4). From the perspective of the IO theory, it acts as a subsidy to price competitiveness, allowing firms to reinvest in their compliance and R&D (+2.28%), thus partially compensating for the weaknesses in the financial system for the most vulnerable segments.

Instrumental variable results and robustness analysis

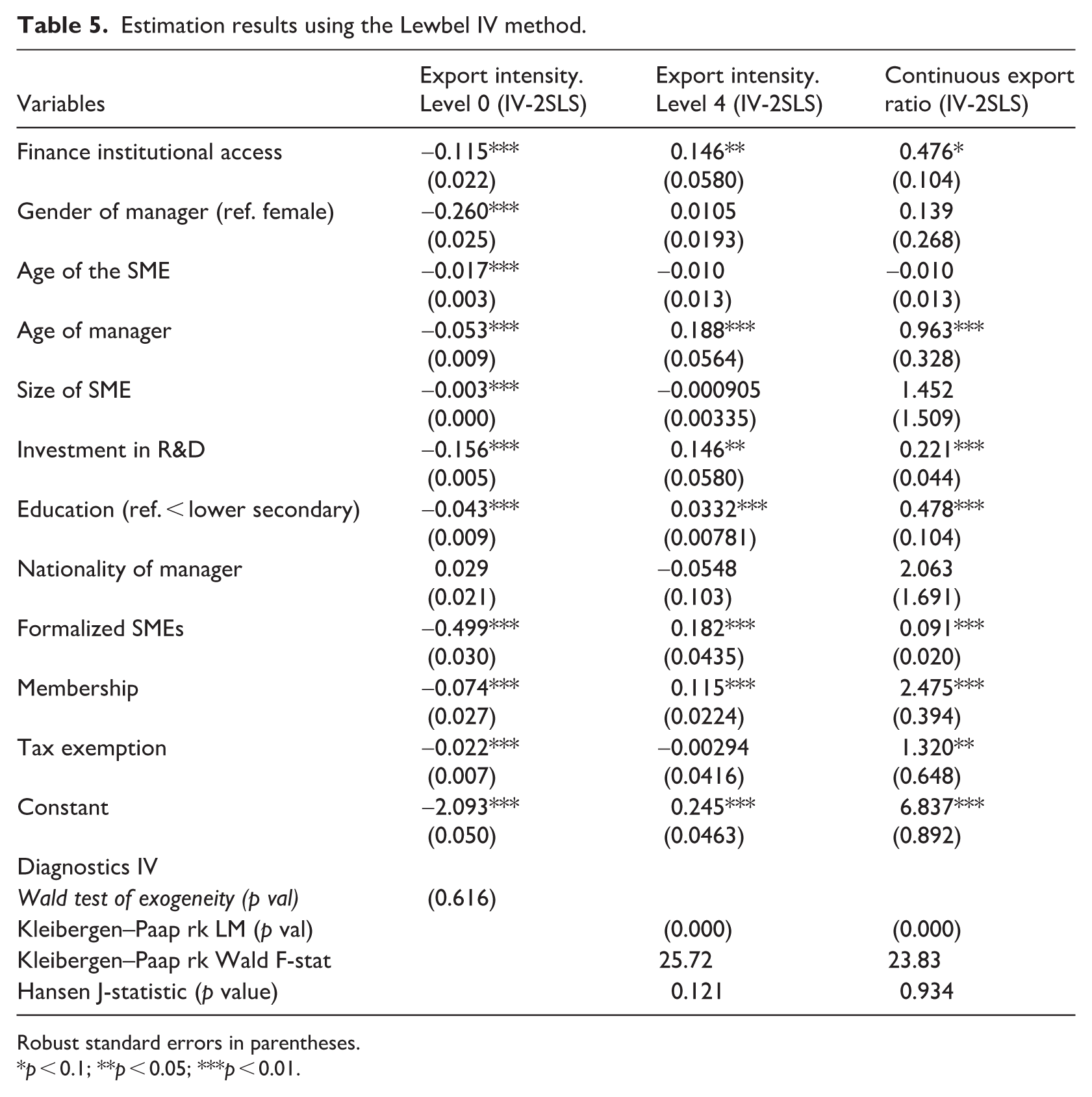

Table 5 reports the estimates obtained using the Lewbel (2012) IV procedure. The empirical results in column 2 confirm a positive and statistically significant relationship between financial access and the export intensity (level 4) in Togo, at the 5% level. These findings are of paramount importance: as they persist after controlling for endogeneity bias, they provide robust evidence that access to financial sources is a causal determinant of export performance, rather than a mere reflection of a firm’s prior international success. This evidence strongly supports the theoretical framework of Manova (2013), who argues that credit-constrained firms are not only less likely to export (the extensive margin) but also export in smaller volumes (the intensive margin). In the Togolese context, this implies that financial frictions act as a major bottleneck, preventing potentially productive firms from scaling their operations globally. The results in column 1 are also consistent with the initial models, although the control variables exhibit higher levels of significance. The reliability of this identification strategy is confirmed by standard diagnostics tests. The Kleibergen–Paap LM test (p = 0.000) rejects under-identification, while the Hansen J-statistic (p = 0.121) validates instrumental exogeneity. Furthermore, the Kleibergen–Paap Wald F-statistic (25.72) confirms instrumental strength, thereby eliminating weak instrument bias.

Estimation results using the Lewbel IV method.

Robust standard errors in parentheses.

p < 0.1; **p < 0.05; ***p < 0.01.

In Column 3, we present the results of the two-stage least squares (2SLS) estimation using a continuous export intensity ratio as the dependent variable. These results remain highly significant (β = 0.475, p < 0.01). This continuous specification demonstrates that our results are robust and not contingent upon the specific thresholds utilized in the baseline ordered probit model. From an analytical perspective, this finding aligns with the seminal work of Berman and Héricourt (2010), who argued that financial access acts as a critical filter for entry into international markets. By mitigating the high fixed costs associated with exporting, financing not only facilitates the initial decision to export but also sustains the scale of international operations. Our results confirm that, for Togolese firms, overcoming these liquidity constraints is a prerequisite for enhancing their competitive position and deepening their participation in global value chains.

Conclusion and policy implications

Small and medium-sized enterprises (SMEs) are the backbone of Togo’s economy, yet they remain constrained by a “missing middle” in trade finance and limited internationalization. This study analyzed the nexus between financial sources and export performance using data from the 2018 RGE conducted by the INSEED-Togo. By integrating probit and ordered probit models with the Lewbel (2012) IV approach, we addressed endogeneity concerns and provided robust causal evidence on how financial access impacts export intensity, while accounting for gender-based heterogeneity.

The empirical findings show that formal financial institutions act as primary “strategic gatekeepers” for export intensity in Togo. While microfinance remains the most utilized funding source (94%), it proves structurally inadequate for overcoming the high sunk costs and exchange rate risks inherent in global trade. Crucially, our results reveal a “gendered duality” in Togo’s export landscape: while male managers more effectively leverage international banks and programs for market entry (participation), female managers demonstrate superior marginal efficiency in utilizing bank credit to scale their operations (intensity), once the initial entry barriers are overcome. Furthermore, R&D investment and tax exemptions emerge as vital mechanisms for providing the liquidity necessary to sustain competitive export operations.

Based on these findings, we propose the following strategic interventions to align with the Togo 2025 Government Roadmap and the African Continental Free Trade Area (AfCFTA) framework: First, there is a critical need for gender-sensitive scaling of finance. The National Agency for Promotion and Guarantee of Financing for SMEs (ANPGF) should pivot from basic financial inclusion toward the creation of specialized “export scaling funds.” These funds must prioritize medium-to-long-term banking credit over subsistence micro-credit, specifically designed to bridge the intensity gap for female-led SMEs that have already successfully entered the market but lack the capital to scale.

Furthermore, the government should focus on reforming institutional filters by establishing a more robust national guarantee scheme. This mechanism should be specifically designed to neutralize the structural biases inherent in traditional banking, such as stringent collateral requirements tied to land ownership. By mitigating these constraints—which currently disproportionately favor male entrepreneurs—the scheme can facilitate more equitable access to the high-level credit required for intensive global engagement.

In addition to financial reforms, national programs must undergo a paradigm shift toward performance-linked incentives. Togo should restructure its institutional aid to move away from survival support and instead link incentives to formalization milestones, compliance with international standards, and R&D benchmarks. This approach would ensure that financial support acts as a ladder for competitiveness rather than a temporary safety net, facilitating a transition toward high-intensity, structured exports. Finally, these efforts must be bolstered by targeted human capital development and digital integration: Enhancing the trade-specific and digital competencies of female managers is essential to capitalize on the opportunities presented by the AfCFTA. By providing specialized training in international contract management and digital trade platforms, Togo can effectively transform informal cross-border activities into formal, sustainable, and competitive export growth, ensuring a more inclusive and resilient national economy.

Although the 2018 RGE remains the most contemporary and comprehensive inventory of Togolese SMEs, we concede that the economic environment has undergone significant shifts, notably in the wake of the COVID-19 pandemic. Nonetheless, the structural impediments to financing highlighted in this research—specifically those related to gender-based disparities and collateral constraints—represent enduring systemic features of the Togolese financial landscape. This analysis thus establishes a rigorous empirical baseline, essential for informing post-pandemic recovery strategies.

Footnotes

Acknowledgements

The authors express their sincere gratitude to the editor and the anonymous reviewers for their instructive comments and insightful suggestions, which have been instrumental in refining our manuscript and strengthening its methodological rigor. We also extend our special recognition to the INSEED-Togo for providing access to the 2018 RGE data, which was essential for conducting this research on the internationalization of SMEs in Togo.

Ethical Considerations

Not required. This study is a secondary analysis of a fully anonymized and de-identified dataset from the General Census of Enterprises (RGE, 2018) provided by INSEED Togo.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data citation

[Dataset] INSEED, 2018 RGE (2018)