Abstract

Under what circumstances does terrorism repel foreign investment? The negative effect of terrorism on foreign investment identified in current scholarship masks heterogeneity across host markets and industries. Foreign investment ought to react less to political violence when host markets match firms’ input requirements, when firms lack viable alternative hosts, and when assets are immobile across markets. We model the endogenous codetermination of terror and investment to derive these comparative statics, highlighting empirical challenges in identifying the effects of terror on foreign direct investment. To overcome these obstacles, we use an instrumental variable estimator which exploits differences in the networks along which terror and investment spread. Using industry-level data on the activities of US multinationals, we test our model and conclude that foreign investors that find it hard to leave particular host markets are doubly penalized: their lack of outside options makes them tempting targets for terror. Our findings have implications for other forms of violent and nonviolent political tactics which affect multinationals and for understanding how foreign investment reacts to heightened risk in host markets.

Foreign investment in the developing world is repelled by terrorism and political violence (Abadie and Gardeazabal 2008; Bandyopadhyay, Sandler, and Younas 2018; Braithwaite, Kucik, and Maves 2014; Witte et al. 2016; Powers and Choi 2012). Terrorism raises costs for multinationals for security (Busse and Hefeker 2007), insurance (Jensen 2008), and recruitment (Bader and Berg 2013) and makes it harder to manage supply chains and ensure predictable operations (Gaibulloev and Sandler 2009; Johns and Wellhausen 2016). Multinationals’ defining characteristics—their international profile, mobility, and choices among potential host markets—may enable them to avoid these costs by eschewing host markets suffering from political violence. However, despite the growth in terrorist attacks on foreign firms (Brandt and Sandler 2010; Enders and Sandler 2000), the literature lacks a systematic account of heterogeneity across industries in their responsiveness to terrorism. Are all industries equally averse to operating in markets with terrorism and other political violence? If multinationals’ negative response to terrorism in host markets is driven by their ability to redeploy investments internationally, what happens to firms which cannot easily move investments or have no viable alternative sites for their overseas activities?

In answer to these questions, we argue that there is significant unexplored heterogeneity across industries in their response to terrorism and that this heterogeneity is driven by the quality of alternative investment options available to firms internationally. Where alternative options are good, foreign investment will be highly responsive to terrorism. When the ability to redeploy investment outside a host market is lacking, multinationals must remain and operate under the suboptimal conditions—heightened costs, heightened risk—generated by terrorism (see Frieden [1994] and Steinberg [2018] on site-specific assets).

We consider several explanations for the ability of firms to locate their investments outside of developing markets facing greater risk of terrorism. First, the inputs employed by firms may be a good match for particular host markets, and those firms may lack other markets that are similarly good matches. It is harder to turn away from a market that is a “good fit” if political violence spikes. Second, firms may control country-specific assets—exclusive copyrights or real estate, for example—that can only be exploited in that market. These assets are inherently nontransferable. In a similar vein, we also consider relatively immobile forms of capital investments: fixed capital expenditures among manufacturing firms, and investments in the purchase, exploration, and development of mineral or land rights among mining firms.

To examine these ideas, we develop a formal model of the strategic interaction of multinational firms and terrorists, extended to include a host government undertaking counterterrorism. 1 We prove our main contention on the responsiveness of foreign investment to terror and its interaction with outside options. Where marginal returns on investment in a host market increase relative to returns available in the rest of the world, firms are more willing to stay put in the face of terror. This result holds under a variety of assumptions about terrorists’ motivations.

Our model highlights empirical challenges in estimating the responsiveness of foreign direct investment (FDI) to terror. Terror is both endogenous and mutually codetermined with FDI in a strategic interaction (Bandyopadhyay, Sandler, and Younas 2014; Rasheed and Tahir 2012; Witte et al. 2016). We resolve these issues by developing an instrumental variable estimator of the elasticity of FDI to terror. For our instrument, we use the spread of terrorism through religious and cultural networks across the globe, and the fact that FDI is plausibly lacking in any religious motive. Following Betz, Cook, and Hollenbach (2018), we control for two important threats to the exclusion restriction: temporal effects of terrorism in one market which redistribute investment uniformly and the geographic spread of terrorism.

We test our main contentions using data on the intra-firm trade of US multinational corporations (MNCs) in developing countries, a valuable source of fine-grained industry-level data on the activities of multinationals which has yet to be examined in the literature on FDI and violence. We find that foreign investment is less responsive to terrorism: when an industry’s inputs are a good match to a country’s output profile, when country-specific leased assets are important to the industry’s production, and when capital expenditures on mineral rights and development are high. We examine the robustness of these findings across many models and show the application of our main theoretical mechanism to multinationals’ response to civil conflict. The desirability of host markets’ input mixes is likely to have similar effects in domains beyond political violence including nonviolent civil disorder and organized opposition to foreign investment.

Our model and findings make several contributions to the study of FDI and political violence. First, we show which firms are most responsive to terror and so which countries are most vulnerable—in terms of lost jobs and investment—to terrorism. This heterogeneity across countries has not previously been described and has potentially wide application to other political and nonpolitical forces that increase foreign firms’ costs. Second, our model and results shed new light on terrorist motivations. We argue that terrorists are likely to derive at least some utility from directly or indirectly harming multinational firms, and so have higher marginal benefits from terror when more multinationals are present. Under this assumption, industries that cannot respond to terror by locating in alternative host markets will attract more terror. We therefore describe a double penalty of immobility facing MNCs which lack outside options: the inability to leave when terror grows itself attracts more terror. Finally, our model and findings illustrate a tactical dilemma for states confronting terror. MNCs that have good outside options will be the first to leave when terror strikes, and so logically states should defend these firms to protect jobs and tax revenues. However, multinationals that lack outside options might be tempting targets for terrorists motivated to gain attention by maximizing multinationals’ costs. Negotiating this dilemma depends critically on understanding terrorists’ strategic objectives vis-à-vis MNCs.

The Strategic Interaction of Investors and Terrorists

Political Order, Terrorism, and Multinational Firms

Foreign investment is repelled by political unrest and violence such as protests and strikes (Schneider and Frey 1985) and civil wars (Collier 1999; Lee 2016). A substantial literature investigates terrorism’s effects on foreign investment due to prominent terror attacks on foreign businesses and a wide array of indirect impacts on foreign firms’ operations. Four terrorist tactics that inflict costs on foreign investors have been highlighted. First, terrorists may directly target physical assets or personnel (Brandt and Sandler 2010; Enders, Sachsida, and Sandler 2006). Attacks include the destruction or capture of facilities and the murder, abduction, or extortion of employees. These inflict a profound toll on human lives and well-being and also economic costs in the short term (e.g., damaged facilities and decreased productivity) and long term (increased insurance rates [Jensen 2008], security expenses, and challenges in recruiting workers [Bader and Berg 2013]). Second, the targeting of infrastructure, utilities, suppliers, and markets can hinder day-to-day operations and the transit of goods (Gaibulloev and Sandler 2011; Meierrieks and Gries 2013). Third, attacks against public spaces create a hazardous environment for local employees and domestic market activity (Benmelech, Berrebi, and Klor 2010; Blomberg, Hess, and Orphanides 2004). Finally, terrorist campaigns contribute to government duress, forcing policy makers to neglect economic investments in favor of military spending (Gaibulloev and Sandler 2009). Budget pressures may result in violation of contracts or indirect expropriation.

Given these costs, scholarship on terrorism and FDI has generally identified a negative relationship between terrorism and FDI, although this relationship is not uniform across the literature. Abadie and Gardeazabal (2008) finds that even modest fluctuations in terror risk cause firms to shift assets to safer locations. Similar findings emerge in country-specific studies (Enders and Sandler 1996; Kinyanjui 2014). In contrast, Li (2006) finds that neither predictable nor unexpected terror attacks are significantly associated with reduced FDI inflows. Witte et al. (2016) likewise finds no significant relationship between terrorism and FDI.

In the face of these mixed results, the literature has disaggregated political violence according to its magnitude (Barry 2018; Christensen 2019; Braithwaite, Kucik, and Maves 2014; Enders, Sachsida, and Sandler 2006; Li 2006) and target selection (Bandyopadhyay, Sandler, and Younas 2014, 2018; Enders, Sachsida, and Sandler 2006; Powers and Choi 2012). Transnational attacks—involving perpetrators, targets, or victims from multiple countries—have been used to measure the most direct risks to MNCs (Bandyopadhyay, Sandler, and Younas 2014). Powers and Choi (2012) finds only attacks on business targets to be associated with reduced inflow of FDI. Some studies find the impact of terrorist violence to be particularly acute for developing countries (Blomberg, Hess, and Orphanides 2004; Gaibulloev and Sandler 2009) but may be moderated by investors’ ability to anticipate violence (Li 2006) and by robust counterterrorism capabilities (Bandyopadhyay, Sandler, and Younas 2014; Lee 2017).

Only a few studies attempt to resolve the disparate results in the literature by examining heterogeneity across industries or firms in sensitivity to political violence (Blair, Christensen, and Wirtschafter 2019; Lee 2017; Witte et al. 2016). Burger, Ianchovichina, and Rijkers (2015) shows that nonresource tradable sectors are the most sensitive to political shocks. Dai, Eden, and Beamish (2017) highlights the different barriers to exit firms face based on their proximity to fighting, portfolio diversity, and resilience. Political violence may increase investment from firms that are geographically removed from violence but benefit from decreased government oversight or increased commodity prices due to instability (Blair, Christensen, and Wirtschafter 2019; Lee 2017). Some work has identified sectors that are more vulnerable to terrorist violence, for example, tourism (Drakos and Kutan 2003; Sloboda 2003), air travel (Ito and Lee 2005; Merari 1998), and energy (Forest and Sousa 2006; Toft, Duero, and Bieliauskas 2010). Bandyopadhyay, Sandler, and Younas (2018) shows a larger impact of terrorism on trade in manufactured goods compared to primary commodities. Surveying the literature, there is a need for a systematic account of industry features which facilitate or inhibit a rapid response to deteriorating security conditions in host markets. We focus on the strategic interaction of a terror group and foreign investors, but we emphasize that the components of our theory translate naturally to other political actors using other tactics that create costs for multinational firms.

Terrorists’ Motivations

The objectives of terror groups at the broadest level include toppling governments (see Fortna 2015; Hultman 2007; Kalyvas 2004), gaining permanent sovereignty over territory, ejecting foreign powers and their agents (Krueger and Laitin 2008), weakening political opponents (Crenshaw 1981), and securing policy concessions from home governments or other important actors (on the effectiveness of terrorism, see Abrahms [2006, 2012], Fortna [2015], and Jones and Libicki [2008]). The literature identifies several strategic objectives of terrorism: defeat conventional armed opponents with unconventional means; persuading populations by publicizing ideologies, aims, and outbidding rival groups (see Bloom 2005; Chenoweth 2010; Conrad and Greene 2015; Crenshaw 1981; Kydd and Walter 2006; Nemeth 2014); provoking overreactions from governments to grow mass support (Fromkin 1975; Kydd and Walter 2006); and delegitimizing governments by demonstrating their inability to maintain order.

In the context of these objectives and strategies, terrorists make decisions about target selection, perpetrating attacks against targets that help them pursue their strategies at the lowest cost. Target selection allows groups to signal their capacity, ideology, or reliability to potential adherents, rivals, and governments (Bloom 2005; Chenoweth 2010; Kydd and Walter 2006). In particular, most groups depend on some level of support from local civilians (financial, intelligence, recruitment) and they choose targets with this audience in mind (Berman and Matanock 2015; Bloom 2005).

To model the strategic interaction of MNCs and terrorists, we do not need to consider all possible terrorist objectives, strategies, or tactics. We do however need to understand how terrorists’ activities impinge on the business activities of MNCs and to understand what value terrorists place on harming MNCs’ interests. To provide some structure, we develop four ideal cases around three questions: (1) Are MNCs’ profits affected by terrorism, even incidentally? (2) Are terrorists motivated to attack MNCs, directly or indirectly? (3) Is the marginal benefit of terror increasing in the current amount of foreign investment?

Terror does not affect MNCs

If terrorism has no effect on the profits of MNCs, then multinationals will not respond in any way to changes in terrorism. Likewise, terrorists would likely have no incentive to deliberately target MNCs directly or indirectly. 2 Under this assumption, terrorists and MNCs are not strategically responding to one another and there is no causal relationship between terror and investment in either direction.

Terror incidentally harms MNCs

A more realistic alternative is that terrorism incidentally affects the costs or profits of MNCs, 3 but terrorists place no value on reducing the presence of MNCs. In this case, terrorists and MNCs are not truly strategically interacting, and terror groups would be unlikely to target MNCs either indirectly or directly. However, MNCs would still be responsive to terrorism and would reduce their investments if terror increases.

Terrorists aim to minimize MNC presence

A third possibility is that terrorist groups intentionally seek to reduce the operations of MNCs as one goal among many. They might do this by directly attacking MNCs or by attacking other targets which impact the operations of firms, such as infrastructure, suppliers, workforces, the state, or markets. We formulate the goal of reducing multinational presence in two ways which turn out to be formally identical: terrorists seek to maximize activities targeting FDI or terrorists seek to maximize the marginal costs faced by foreign firms. The formal commonality in these cases is that the marginal benefit to the terrorist of additional terror activities does not depend on the current amount of investment. Under this assumption, terrorists would not increase their activities if FDI were to exogenously increase.

Driving down the total quantity of FDI in the home market is consistent with several objectives. Terrorists may wish to minimize foreign presence for sociocultural reasons. They may wish to reduce FDI to damage the economy, create joblessness, or symbolically attack the government’s economic policies. Terror groups may wish to displace MNCs from key markets or assets, so that they can take over those markets or assets, as with easily exploited natural resources. Finally, terrorists may seek to maximize terror against MNCs to demonstrate their ability to reach ostensibly better-protected foreign targets. Attacks on international businesses garner more media attention (Crenshaw 1981; Weimann and Winn 1994).

Terrorists aim to maximize MNC pain

A final alternative is that terrorists might seek to maximize their aggregate negative impact on foreign investment. This assumption turns out to be formally equivalent to minimizing the profits of the multinational firms operating in the host market or to maximizing the total costs of MNCs (rather than their marginal costs, as above). While these motivations may sound similar to the case of minimizing MNC presence, there is a key formal difference: the terrorist’s marginal benefit from attacks against firms is increasing in the amount of investment in the home market. Put differently, terrorists will increase their activities if FDI exogenously increases.

This strategy is consistent with several strategic objectives for terror groups. Terrorists may try to maximize the “impression” of the terror group to MNCs, pushing these corporations to lobby the host or home government. These firms serve as a conduit to a wider audience for the group to broadcast grievances, attract adherents, and solicit donations (Kelly and Mitchell 1981). Terrorists may wish to minimize the government’s tax revenues from corporate profits. Such a goal might also ensure that MNCs cannot contribute to the state’s security efforts (Murdie and Stapley 2014). Likewise, attacks on corporate profits make it harder for MNCs to profitably contribute to the local economy or to engage in corporate social responsibility which can broaden support for the firm or state, undermining a message of grievance. Finally, terrorists may be intrinsically motivated to inflict pain on foreign corporations or citizens, and the marginal value of that pain might increase in the presence of more of those MNCs.

Model Setup, Assumptions, and Equilibrium

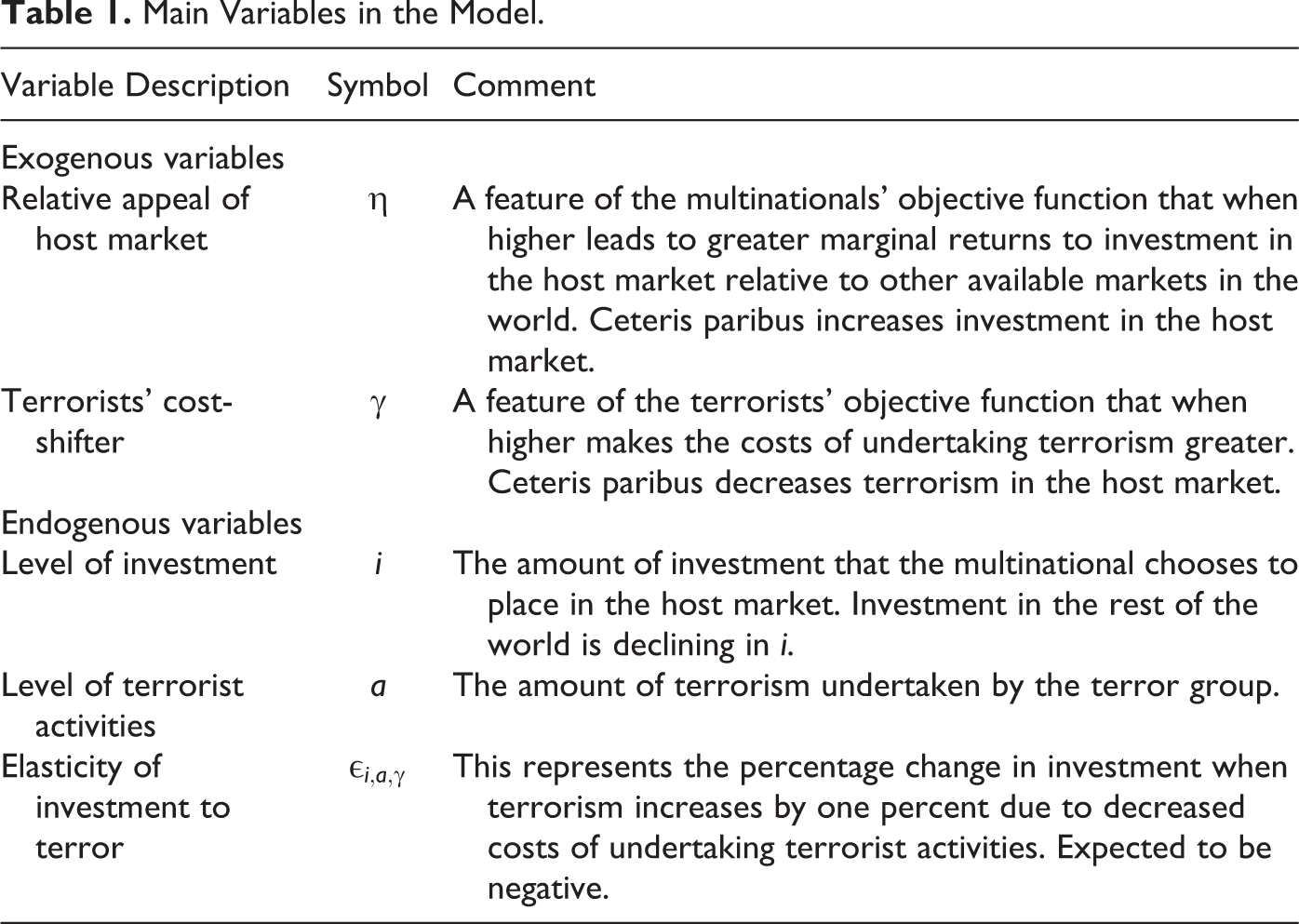

Our model, whose main elements are summarized in Table 1, begins with a multinational firm (or firms) denoted by F considering how much to invest

Main Variables in the Model.

The second issue the firm confronts is that it has an outside option to repurpose underperforming investment in the host market. We refer to this outside option as the “rest of the World,” and denote profits earned there with the function

All of these pieces comprise the objective function for the multinational firm:

The multinational’s objective is to choose a level of investment i to maximize the profits represented in this equation. Of course, this decision will be made in anticipation of the level of terror activities a undertaken by the terrorist group T.

Following our discussion above, we assume that the terror group may not be motivated to attack MNCs but incidentally affects their operations or is motivated to attack MNCs in order to minimize foreign investment or is motivated to attack MNCs to maximize the aggregate costs of these firms. These are nested possibilities, which might all operate at the same time. To incorporate the idea that terror incidentally affects MNCs, we assume that terrorists have an objective of maximizing the function

We also assume that terrorist activities have costs (reprisal or capture, matériel, and manpower) that increase in the amount of terror undertaken. These costs are represented by the function

and the terrorist’s goal is to choose a level of activities which maximizes this objective function. Note the parameter

We examine results across the nested cases of terrorist motivations. For example, if terrorists are assumed to only incidentally impact MNCs, then we assume that their objective function is

We imagine that the multinational firm and the terrorists make their choices about investment and activities simultaneously and with complete information about one another’s means and motives. We assume an interior solution for both i and a and then identify a Nash equilibrium in pure strategies. Our assumptions about the second derivatives described above ensure that the first order conditions for the firm’s and terrorist’s problem implicitly define the optimal i and a chosen in equilibrium.

The Responsiveness of Foreign Investment to Terror

How does foreign investment respond to terror? In our model, both investment and terror are endogenous choices of strategically interacting agents, so to answer this question, we focus on an exogenous shock to the ability of terrorists to undertake terrorism. This occurs through a change in

What factors mitigate or exacerbate the responsiveness of investment to terrorism? We focus on the ability of the firm to move its investment from the host market H and to profit from it in the rest of the world W. The ability to do this is driven by the parameter

We can now present our main result.

The two possible sufficient conditions contained in Assumption 1 are sufficient but not necessary: there are several terms in the formal statement of

Translating the Model into Testable Propositions: Relative Appeal of the Host Market

We test our proposition by developing measures of

A host country is a good fit for a firm if it has a relative abundance of the inputs used intensively in that firm’s production. A good match could represent endowments in a resource or availability to fulfill a diverse set of input requirements. Of course, a host country is compared to all other available host countries. To account for a firm’s ability to invest elsewhere, we consider the match between a firms’ input needs in all other available markets outside of the current host market. If the match between the firm’s input needs and the host is high compared to the rest of the world,

Leased assets—such as real estate, exclusive use rights, and intellectual property—represent largely nontransferable, country-specific contracts. For example, a company might own the exclusive mineral rights for a particular oil field in some country. This represents an ideal case for a high

We also complement our examination of leased assets by examining fixed capital expenditures within particular sectors. In the case of manufacturing, we look at an industry’s total capital expenditures (which might include machinery, nonmaterial assets, and buildings) as well as buildings specifically. For mining, we examine capital expenditures on land and mineral rights as well as investments in minerals exploration and development. We expect that each of these forms of capital investments are relatively nontransferable across borders and so force firms to “stay and fight” when terrorism makes doing business more costly or unsafe.

We conclude by highlighting that the mechanisms that we describe above extend to domains beyond terrorism. First, other groups may have incentives to impair or eliminate foreign investment. These include mass protest movements, insurgent groups, labor and human rights groups, and environmental groups. Our model and discussion of the motivations of FDI opponents can contribute to understanding these other areas. Second, our core theoretical mechanism on the mobility of foreign investment as a function of host market input profiles and asset mobility has potentially wide application. This is true for other instances of civil disorder and violence (as in civil wars, which we investigate below), for strategic interactions with nonviolent groups, and even for understanding the effects of essentially nonpolitical events that raise costs for multinationals like exogenous economic changes or natural disasters.

Data and Empirical Strategy

Data

Our outcome variable is the related party exports (to the United States) of MNCs located in developing countries.

7

These data cover 138 host markets, and are available for 2002 to 2016 only, defining the time frame for our study. We examine 109 such goods-producing industries at the four-digit North American Industry Classification System (NAICS) code level.

8

Related-party exports from a host market to the United States cross a border but stay within a single firm. They include the exports of United States-based multinationals producing in a host market for sale in the United States, the exports of host market multinationals to their affiliates in the United States, or the exports of MNCs from a third country with affiliates in both the host market and the United States. We refer to these related-party exports as Intra-firm exportsnit where

Intra-firm exports are not the same thing as stocks or flows of FDI. First, they are a measure of exported production and not investment. As such, they respond to the scale of vertical foreign investment (producing abroad for sale back home) rather than of horizontal foreign investment (producing abroad to sell abroad). We therefore examine a separate measure of foreign activity which includes horizontal FDI in the Online Appendix, while noting that vertical FDI is of primary importance for North-South FDI. Second, related-party exports to the United States may include the sales of host market firms, which are not the primary subject of this study (although they may still fit our theory since those firms are MNCs). Such exports are likely to be low in any event, because most developing countries have little or no FDI in the United States. The use of related-party exports to proxy for level of foreign investment has several advantages. First, the data are at an extremely fine-grained level—much more than is available for stocks of FDI. Second, production is likely to be more responsive to terror than investment, making it easier to identify the effects of sudden increases in terror. Third, intra-firm exports do not suffer from the issues associated with FDI data identified in the literature, in particular, that the strategic reallocation of mobile assets to offshore tax havens are often included in FDI measures (Kerner 2014).

Our primary explanatory variables are measures of terrorist attacks in market i. The Global Terrorism Database (GTD 2018) provides incident-level data on terrorist attacks and their attributes. The main explanatory variable, Terror countit, is the number of terror attacks in the host country in a given year. We also isolate the most direct tactic for harming multinationals, attacks against domestic and foreign firms. Bus. terror countit is a count of all GTD terrorist attacks against a business target and Foreign bus. terror countit is attacks on foreign firms only.

Our theoretical model suggests that the effects of terror on multinational activity are conditional on host market and industry features. We construct a variable called Input matchnit, which measures the fit between a given industry’s input profile and the ability of a host market to produce those inputs. To measure an industry’s input requirements, we use the vector of input shares for a four-digit US industry created using benchmark input-output tables from the Bureau of Economic Administration. To measure a country’s ability to supply inputs, we use the vector of all exports to the United States at the four-digit NAICS industry (normalized to sum to one). The Input matchnit variable is defined as the cosine similarity between the two vectors and equals 1 if the two vectors exactly align and 0 if the two vectors share no overlap.

We use Input matchnit to construct a measure of firms’ abilities to locate production in a viable alternative market. To construct this, we weight all other inputs matches in other potential host markets by their GDP and geographic distance from the current market. Markets that are larger and nearer are likely to provide more appealing alternatives. The measure is therefore:

Here, we use

We also measure the percentage of inputs that come from leased assets (including not only land and mineral rights but also nonfinancial intangible assets like intellectual property) and the percentage of input costs that arise from the purchase or rental of real estate. 10 The former measure connects our examination to the long-running literature on intangible assets and corporate mobility. These variables are called Leased assetsn and Real estaten, respectively. As noted above, we complement these measures of leased assets with sector-specific measures of capital expenditures available only in manufacturing and mining, respectively. Because these tests are conducted on a different sample, we only describe the results of these tests in the main text and report on details of the variables and the empirical strategy in the Online Appendix.

One final point is that the distributions of some of the four proxies for

Empirical Strategy

Our formal analysis points to a focus on the elasticity of foreign investment to terrorism. Specifically, we would like to know if an exogenous shock to terrorist operations which increases terrorism will tend to push down foreign investment. This relationship is represented symbolically by

Our focus on this elasticity suggests that we regress the logged amount of intra-firm exports on the logged count of terror attacks. This log-log setup generates an estimate of the elasticity given by the coefficient on the terror count variable. However, our model makes clear that a simple regression of this sort will generate a highly misleading estimate of

Thus, we use an instrumental variable estimator for the elasticity of investment to terror, employing two-stage least squares. Our instrument plays the role of the

This instrument for the number of terror attacks in country i at time t (i.e.,

We use the same instrumental variable when

One core assumption behind this instrument is that terror propagates across national boundaries along religious lines or other cultural lines. Terror committed by or against members of a religious group in one country is likely to raise the probability of terror committed by or against the same group in other countries. Of course, this inclusion requirement is testable in the first stage of our two-stage procedure, and we show below that it holds. The exclusion restriction requires that religion-weighted terror of other countries does not have any effect on foreign investment in country i except through its impact on terrorism in country i. We think that is plausible in general because we do not expect foreign investment—particularly the vertical foreign investment on which we concentrate—to have any religious dimension to it whatsoever. For example, it is implausible that greater terrorism in countries with a high percentage of Catholics will lead firms to reinvest in other Catholic countries because they are Catholic.

That being said, there are two plausible challenges to our exclusion restriction. First, greater terrorism in one country is likely to lead to more investment in all other countries, creating a link between our instrument and the outcome via simple diffusion. For this reason, we employ year fixed effects in all specifications. Second, religions are geographically concentrated, and the multinational operations of firms may be too. These correlations would lead to an unwanted correlation between our instrumental variable and our outcome that does not operate via terrorism in country i as our exclusion restriction requires. So we include in all specifications a control for terrorism in all countries weighted by their inverse geographic distance. Defining

Controlling for

Before introducing our estimating equations, we make one final note. Any estimation of the effect of terror on FDI is likely to be plagued by observable and unobservable country-specific effects. Most obviously, larger countries might attract more FDI and terror, but it could also be that more unequal or more developed countries attract both of each, too. For this reason, we include country fixed effects (or higher dimensional fixed effects) in all of our models.

When we investigate how the elasticity of foreign investment to terror is conditioned by structural features of the industry and the host market, the unit of analysis is the four-digit NAICS industry-country-year (

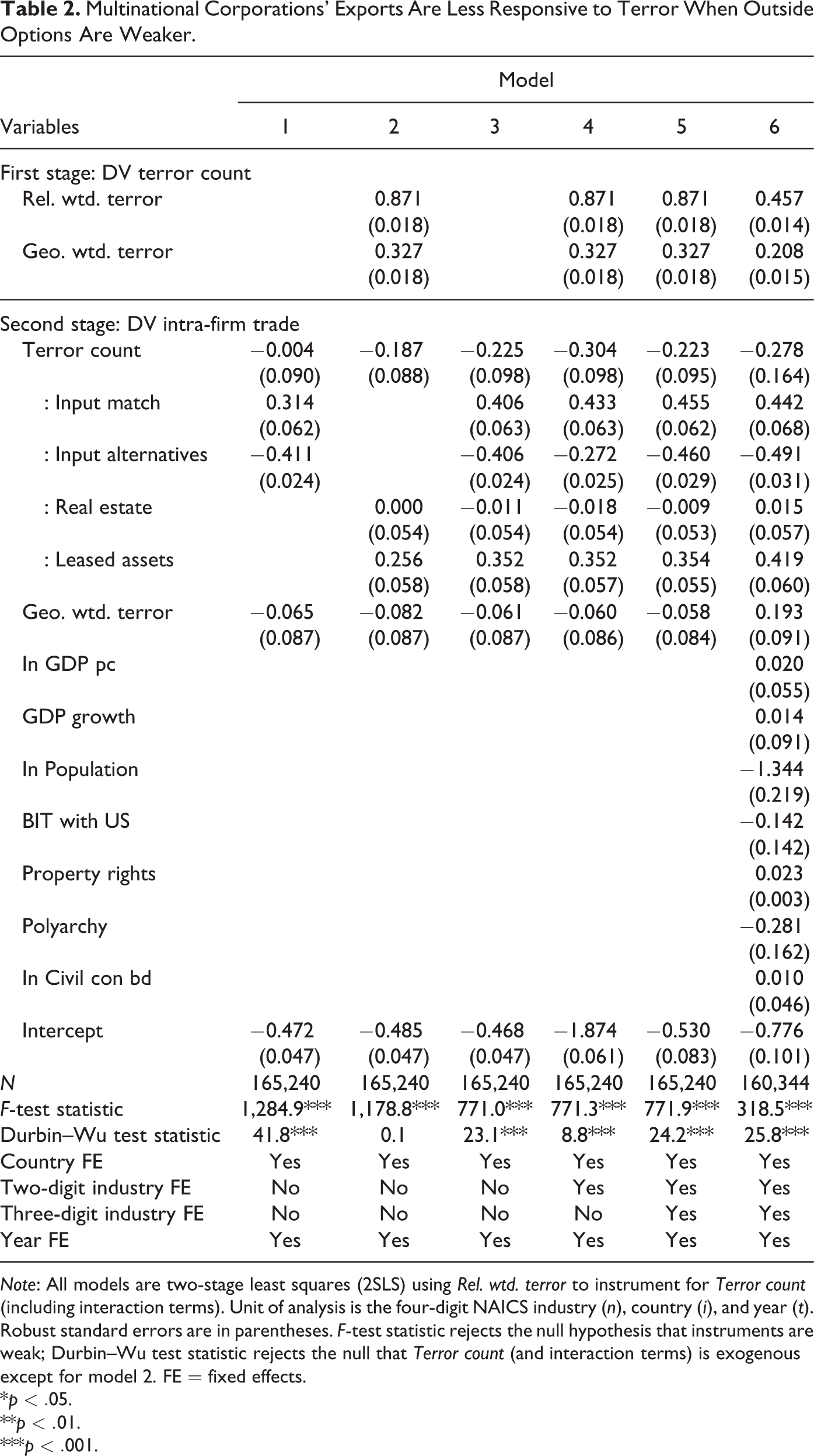

Multinational Corporations’ Exports Are Less Responsive to Terror When Outside Options Are Weaker.

Note: All models are two-stage least squares (2SLS) using Rel. wtd. terror to instrument for Terror count (including interaction terms). Unit of analysis is the four-digit NAICS industry (n), country (i), and year (t). Robust standard errors are in parentheses. F-test statistic rejects the null hypothesis that instruments are weak; Durbin–Wu test statistic rejects the null that Terror count (and interaction terms) is exogenous except for model 2. FE = fixed effects.

*

**

***

where:

and

where

Results

Country-level Results on FDI and Terror

We begin our empirical analysis by examining a key finding in the literature that terrorism repels FDI. We do so as a validity check of our dependent variable and empirical strategy and to set the stage for our detailed investigation of heterogeneity in terror’s effect on FDI. To conserve space, the results of this analysis are presented in Online Appendix B. Our first-stage equation shows that Rel. wtd. terror has a positive effect on Terror count, as is necessary to be a valid instrument. In our second stage estimate of the elasticity of FDI to terror, we find a negative and statistically significant estimate: a 1 percent increase in the Terror count is predicted to reduce Intra-firm exports by about 1.2 percent. This negative effect of terror on foreign investment is somewhat higher when additional controls are included. Our findings at the country-level therefore correspond with extant findings that terror has an on average negative effect on foreign investment.

Heterogeneity in Response to Terror across Industries

We now consider heterogeneity across industries in their responsiveness to increased terror. We examine separately our two types of explanations for the ability of firms to redeploy investments overseas: input match with current and alternative host markets; and reliance on real estate, leased assets, and fixed forms of capital.

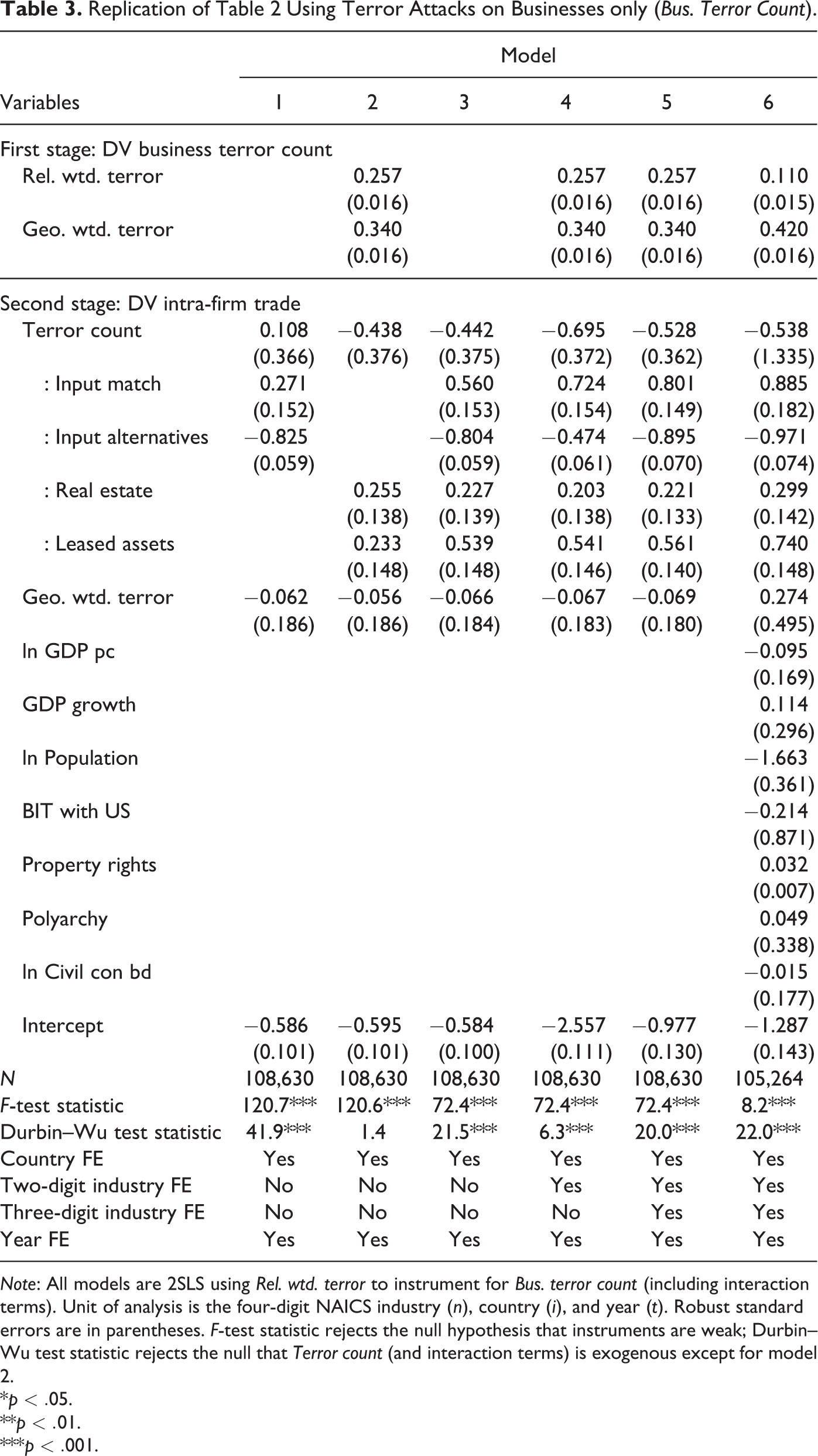

Our primary focus is on the estimates from the models in Table 2. In the table, we use colons to refer to interactions between two variables. For example, the row labeled “Terror count” refers to the coefficient on the lower-order term for the Terror count variable, while the row labeled “: Input match” is the coefficient for the interaction between Terror count and Input match. We suppress coefficient estimates for all other lower order terms to preserve space. We first examine models with a bare minimum of interaction terms (columns 1 and 2). We also check the robustness of our main findings to two types of industry fixed effects and other controls in models 3 to 6 and then subsequently discuss robustness with high dimensional country-industry fixed effects, lagged dependent variables, and reduced form estimates which are presented in the Online Appendix. Most importantly, we provide in the main text (as Table 3) a replication of all of our main results using Bus. terror count instead of Terror count as our main independent variable. 15

Replication of Table 2 Using Terror Attacks on Businesses only (Bus. Terror Count).

Note: All models are 2SLS using Rel. wtd. terror to instrument for Bus. terror count (including interaction terms). Unit of analysis is the four-digit NAICS industry (n), country (i), and year (t). Robust standard errors are in parentheses. F-test statistic rejects the null hypothesis that instruments are weak; Durbin–Wu test statistic rejects the null that Terror count (and interaction terms) is exogenous except for model 2.

*

**

***

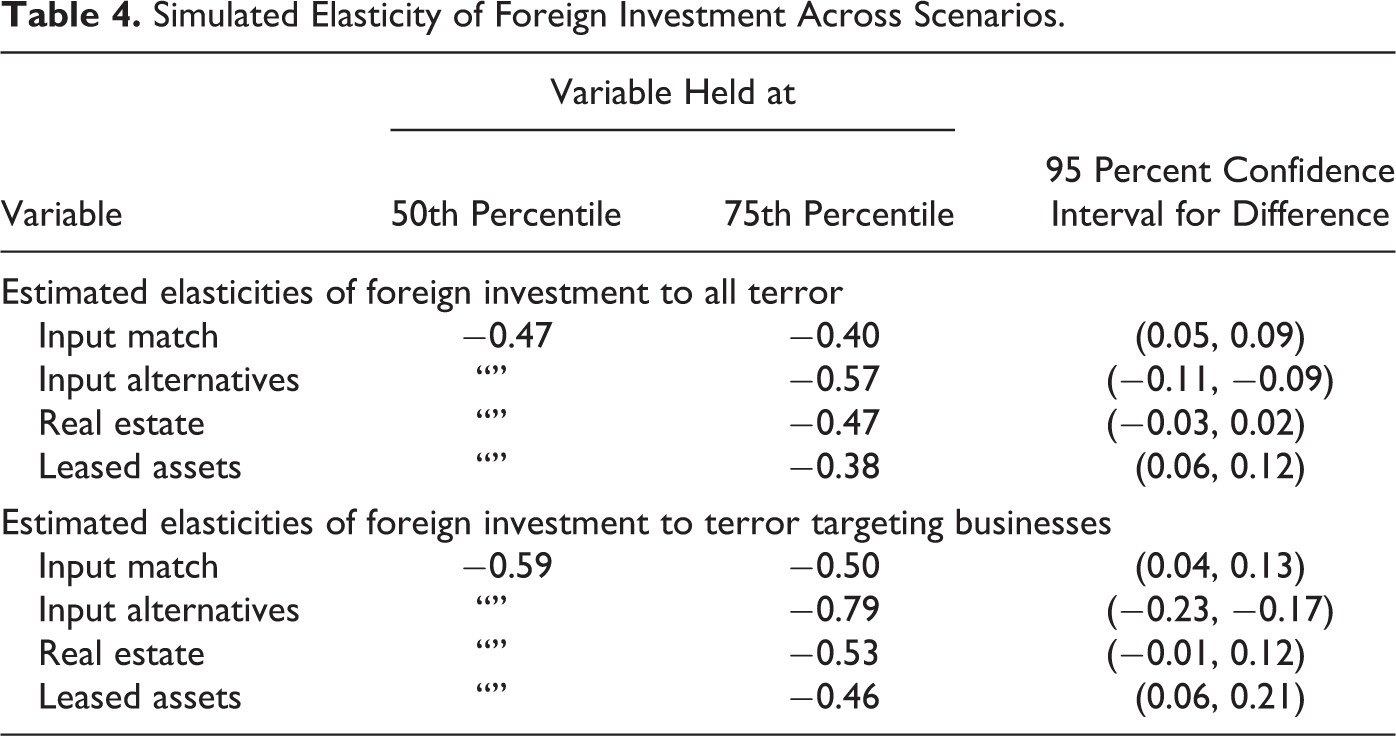

In order to translate our results into interpretable quantities of interest, we provide estimated changes in the elasticity of foreign investment to terror in Table 4. For these first differences, all explanatory variables are held at their median in the data and one variable is changed at a time.

16

For example, the first row shows the change in the estimated elasticity of investment to terror when Input match is moved from its 50th to its 75th percentile, while holding all other variables constant. A confidence interval for each first difference is provided in the final column. Note that with all variables held at their median, the estimated elasticity of investment to terror (of any kind) is

Simulated Elasticity of Foreign Investment Across Scenarios.

Input match in the host market and alternative markets

Model 1 shows that firms whose input demands are a better match to the host markets in which they are invested are more resistant to leaving those markets. This is shown by the positive coefficient on the Input match interaction term. The estimated effect of Input match on responsiveness to terror is quite large as seen in Table 4. Increasing Input match from its median value to the 75th percentile in the data reduces the elasticity of investment to terrorism from

Models 1 and 3 also show the predicted negative coefficient on the interaction term between Terror count and Input alternatives. This negative coefficient means that industries which have more alternative markets that provide a good match to their needed inputs are more responsive to terror attacks. Looking at the first differences in Table 4, the predicted effect of an increase in Input alternatives from its 50th to its 75th percentile on the elasticity of investment is about

Use of immobile assets

In our theoretical discussion, we predicted that the heavy use of relatively immobile assets would lead to reduced responsiveness of foreign investment to terror. For this reason, we expected that industries that rely heavily on real estate and the leasing of intangible assets—whether intellectual property, franchise agreements, or leasing rights—ought to be more willing to stick around when increasing terrorism raises the costs of doing business. Our main results in Table 2 do not support the claim that the use of real estate leads to less responsiveness to terror (or more, for that matter). On the other hand, our results in Table 3, where we examine terror attacks on businesses specifically, do align with our expectations. Some of the subsequent models with higher-dimensional industry-country fixed effects are supportive of the hypothesis, too, so overall, we see a somewhat mixed picture with some support for our claim that the extensive use of real estate may create unwillingness to leave host markets where terrorism has increased.

In contrast to the findings on real estate, we see a consistent and highly robust pattern that the use of leased assets is associated with a significantly reduced willingness to retreat in the face of terror. An increase in the use of Leased assets from its median value to its 75th percentile is predicted to reduce the elasticity of investment to terrorism from

We examine, in Online Appendix B (models B7 and B8), the responsiveness of investment to terror as a function of expenditures on fixed capital assets. These analyses require examining mining and manufacturing industries separately. Consistent with our findings on Leased assets, we find that mining industries which spend more on “minerals exploration and development” and “mineral land and rights” (as recorded by the Economic Census of the United States) are much less responsive to terrorism. Note that this result describes heterogeneity among the industries within the mining sector. We find a positive relationship between capital expenditures on “buildings and other structures” and responsiveness to terror among manufacturers. A post hoc explanation for this is that firms which must invest in buildings fixed in specific locations are reticent to end up “trapped” should political violence flare or are more vulnerable to menacing by terror groups.

Summary of results

Surveying our results, we find that several of our hypothesized factors are strongly associated with a diminished responsiveness of US multinationals to terrorism in host countries. These are the match of the multinational’s input requirements to the host country’s production profile, the availability of alternative markets with similar inputs, and the use of intangible leased assets like intellectual property and mining rights. We also find in separate models specific to mining that capital expenditures on mineral rights and exploration are associated with a smaller elasticity to terrorism. Contrary to our expectations, we find inconsistent results on the use of real estate as an input and on capital expenditures on buildings within manufacturing.

We examine in the Online Appendix several additional models which add confidence to our main findings. First, we check the robustness of our main results to models incorporating high-dimensional fixed effects and in reduced form. We see quite similar results with the above-noted exception of input alternatives. Second, we extend our findings outside the domain of terrorism to another form of political violence by using civil conflict battle deaths as the primary explanatory variable in place of terror attacks. We find that FDI’s response to this alternative form of political violence is remarkably similar.

Conclusion: Firm Mobility and Terror Group Strategy

Our findings contribute to a nascent literature that investigates divergent investor responses to a range of political risks. For example, recent work has shown that the negative impact of armed conflict on investment may be conditional on commodity prices (Lee 2017; Witte et al. 2016), investment lifecycle (Barry 2018) and the geographic location of firms (Blair, Christensen, and Wirtschafter 2019; Dai, Eden, and Beamish 2017; Witte et al. 2016). We contribute to this literature an explanation for why some firms continue to operate amid the heightened risk of terrorism while others choose to exit, focused on the interaction of host market and industry characteristics. Our formal model shows that firms are less responsive to terror when host markets hold site-specific assets which are a good match for firms’ needs. Our results largely support our theory. Firms are less responsive to terrorism when their inputs are a good match to the host country, when other good matches are unavailable, when production relies on exclusive licenses over assets, and when they heavily employ fixed capital expenditures on mineral leases and exploration.

We conclude by considering the implications of our findings for the strategies of terror groups and of host governments in turn. We begin with terror groups and ask how does the immobility of MNC assets affect the incentives of terror groups to produce terrorism? We show in the Online Appendix that the answer to this question is conditional. If the terror group’s marginal utility from terrorism does not depend on the quantity of foreign investment, then equilibrium terror activities are unchanged by increased MNC immobility. If, as seems more plausible, the marginal benefits of terrorism are increasing in the amount of foreign investment, then terrorism will be increasing in the immobility of foreign investment. In the terms of our model

This latter finding sheds light on the economic fundamentals likely to attract terrorism. In some countries, terrorists motivated to drive down corporate profits will be thwarted by resource endowments that are easily found in alternative markets and an industrial mix that does not rely on market-specific leased assets or capital expenditures. In markets with highly specific and hard to replicate assets, however, terror groups find tempting targets in the form of multinationals that have to bear the burdens of terrorist violence. These MNCs are a conduit for terrorists’ demands to be heard by the local host government, home country governments, and the international community. Our model therefore describes a “double penalty of immobility”: firms that lack good outside options must stand and face terrorism and will in fact attract more terror precisely because they lack outside options. Terrorists see immobile firms as sitting ducks providing reusable channels to broadcast their grievances to key audiences, host and home governments, and the world at large. Future work ought to consider the application of this idea to nonviolent activists who have also opposed foreign investment, for example, human rights and environmental groups.

Our results also highlight policy options for host countries facing terrorist violence. Governments have a finite set of resources to allocate toward counterterrorism. Policy makers seeking to minimize firm exit might wish to focus their efforts on firms with more opportunities to profit in the world economy. Firms that are relatively stuck in the market are therefore vulnerable for a third reason that we have not emphasized: governments may prioritize security for firms with a higher flight risk. Future work ought to consider the allocation of counterterror resources across industries and also extending our approach to government efforts to suppress nonviolent political activities that may raise multinationals’ costs.

Supplemental Material

Supplemental Material, sj-csv-1-jcr-10.1177_0022002720908314 - Nowhere to Go: FDI, Terror, and Market-specific Assets

Supplemental Material, sj-csv-1-jcr-10.1177_0022002720908314 for Nowhere to Go: FDI, Terror, and Market-specific Assets by Iain Osgood and Corina Simonelli in Journal of Conflict Resolution

Supplemental Material

Supplemental Material, sj-csv-2-jcr-10.1177_0022002720908314 - Nowhere to Go: FDI, Terror, and Market-specific Assets

Supplemental Material, sj-csv-2-jcr-10.1177_0022002720908314 for Nowhere to Go: FDI, Terror, and Market-specific Assets by Iain Osgood and Corina Simonelli in Journal of Conflict Resolution

Supplemental Material

Supplemental Material, sj-csv-3-jcr-10.1177_0022002720908314 - Nowhere to Go: FDI, Terror, and Market-specific Assets

Supplemental Material, sj-csv-3-jcr-10.1177_0022002720908314 for Nowhere to Go: FDI, Terror, and Market-specific Assets by Iain Osgood and Corina Simonelli in Journal of Conflict Resolution

Supplemental Material

Supplemental Material, sj-pdf-1-jcr-10.1177_0022002720908314 - Nowhere to Go: FDI, Terror, and Market-specific Assets

Supplemental Material, sj-pdf-1-jcr-10.1177_0022002720908314 for Nowhere to Go: FDI, Terror, and Market-specific Assets by Iain Osgood and Corina Simonelli in Journal of Conflict Resolution

Supplemental Material

Supplemental Material, sj-pdf-2-jcr-10.1177_0022002720908314 - Nowhere to Go: FDI, Terror, and Market-specific Assets

Supplemental Material, sj-pdf-2-jcr-10.1177_0022002720908314 for Nowhere to Go: FDI, Terror, and Market-specific Assets by Iain Osgood and Corina Simonelli in Journal of Conflict Resolution

Supplemental Material

Supplemental Material, sj-R-1-jcr-10.1177_0022002720908314 - Nowhere to Go: FDI, Terror, and Market-specific Assets

Supplemental Material, sj-R-1-jcr-10.1177_0022002720908314 for Nowhere to Go: FDI, Terror, and Market-specific Assets by Iain Osgood and Corina Simonelli in Journal of Conflict Resolution

Footnotes

Acknowledgments

The authors wish to thank Christian Davenport, Patrick Egan, Jeffry Frieden, James Morrow, Ragnhild Nordas, Irfan Nooruddin, Thomas Oatley, Tom O’Mealia, Stephanie Rickard, Ronald Rogowski, Nita Rudra, Alexander Slaski, Jessica Sun, and the participants of the Peace and Conflict Workshop at the University of Michigan.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.