Abstract

This article examines the politics of the Mexican power industry between 1949, when the World Bank made its first major loan to a developing country, and 1954, when the loan project came to an end. By analyzing Mexico's largest power company, Mexican Light and Power, it argues that business history is central to understanding development politics and diplomatic relations. On the brink of bankruptcy and incapable of meeting growing power demand, in 1949 Mexlight received a large loan from the World Bank to expand its generation capacity. The article argues that the Bank's involvement with the Mexican power industry should be understood as part of a broader Bretton Woods project to strengthen private enterprise in the developing world. The article advances an understanding of Latin American postwar development premised on willful integration into US economic structures. The article shows how the Bank's project was successful in building infrastructure to expand generation capacity, but it failed at securing private enterprise a space of economic autonomy free from government intervention. Contributing to discussions on developmental states, it argues that Mexico's private power industry expanded by deepening its reliance on government support.

On 1 January 1949, the first World Bank loan project to Mexico got underway. The product of 2 years of negotiations between the US government, US banks, Bretton Woods institutions, Mexican officials, and the Belgian owners of Mexico City's electric utility, the loan made US$50 m available to Mexico's power industry: US$24 m to the state-owned company, and US$26 m to the private-owned Mexican Light and Power. This loan would prove crucial both for Mexico and for the World Bank. The first Bank loan to a large developing country, the project's success at modernizing Mexico's electrical sector would induce the Bank to focus its efforts on power industries as the skeleton key to broader economic development. 1 It also showcased the perils of involvement in a politically hyper-sensitive sector where foreign ownership and nationalist sentiment clashed. For Mexico, the loan made visible the core contradictions of its nascent developmental project. During the Bretton Woods conference, Mexican officials had fought to charge the Bank with a developmental mandate, a campaign in which they were successful but which had not yet materialized in any form of assistance. 2 The Bank's decision to finance the modernization of Mexico's electricity infrastructure suggested, on the one hand, that this effort was bearing fruit. On the other hand, the scheme involved a foreign loan, guaranteed by the Mexican treasury, to a foreign-owned company, indicating to some that the old pattern of US and European control over the country's key economic levers would persist, one generation into the postrevolutionary social compact.

This article examines the first World Bank loans to Mexico from 1948 to 1954 to advance a broad revision of scholarly thinking about Latin American development and US–Latin American relations. As the first in-depth examination of Bretton Woods lending to Mexico, it joins valuable but scarce attempts at writing a ‘deeper’ history of development in Latin America, one detailing the on-the-ground implementation of projects rather than the drafting of international treaties. 3 It seeks to foreground these discussions in a political economy of development and of Latin America's place in the postwar economic world. Firms, both publicly and privately owned, were the main recipients of development funds. The history of development therefore requires examining trilateral relationships between companies, domestic government, and US-based International Financial Institutions (IFIs). To understand the place of firms in the politics of development requires, in turn, an account of businesses, their economic constraints, and their political strategies. This article analyzes the strategies of the three main actors involved in the power industry: the Mexican government, the World Bank, and Mexican Light and Power (Mexlight), the country's largest power utility. It shows that from early on, IFIs were central to the developing world, albeit anything but omnipotent. Here, I join a long-standing discussion about the character of US–Latin American relations after Second World War. Many valuable works have shown how Mexican developmentalism was premised on integration into US economic flows and on US influence, but knowledge of the economic dimension of this integration remains at an unsatisfying level of generality. 4 Another strand of scholarship has argued that Latin American development was stifled by the United States, and insofar as it happened, it entailed a breakaway from the institutions and structures of US power. 5 A subsidiary argument recognizes the role of IFIs in Mexican development but emphasizes Mexico's attempts at reforming them. 6 The case of World Bank lending to Mexico's power industry sheds light on the process of integration into the structures of a US-led economic order, including the forces that rammed it forward and the political challenges it faced. It shows US institutions’ commitment to industrialization in the developing world and argues that making infrastructural buildout central to this project gained the enthusiastic support of Mexico's ruling circles.

This story also contributes to discussions about the nature and power of the Priísta state. 7 Scholars have sought to measure the levels of coercion and consent in the dealings of Mexico's authoritarian state with subaltern groups in order to grasp the extent of its power. 8 However, a focus on subaltern obstacles to hegemonic closure constrains the viewpoints from which to analyze state–society relations. What can we learn about state power if we look at government's relation to capital? What were the mechanisms of collaboration – or sources of friction – between the government and the business community? What was the place of foreign capital in a strenuously nationalist society? In a landmark piece, Miguel Wionczek cast the history of the power industry as a ‘cold war waged between the state and the power companies since the 1930s’. Finding no evidence of war, hot or cold, I follow other scholars who have argued that even at the height of its radicalism in the 1930s, Mexico's revolutionary government had reached a concordat with the capitalist class. 9 I extend this frame to the late 1940s and early 1950s to probe state-capital relations in one of the most important developing countries at the dawn of US hegemony. The Mexican government and the largest power company collaborated on and jointly financed the largest project of infrastructural buildout. But this project faced obstacles and challenges emanating from Mexico's political economy. To show this, I draw on previously unused World Bank records, some of which were declassified at the author's request, allowing reconstruction of backstage negotiations that do not appear in the official government papers most often used for similar research.

In a landmark text from 1963, economist Raymond Vernon diagnosed a political dilemma hampering Mexico's developmental project: an authoritarian but corporatist government found itself immobilized by having to fulfill the demands of both the left and the right, leading to policy incoherence. 10 I follow Vernon in taking seriously the opposing pulls of the need for popular legitimacy and the imperatives of capital reproduction. The making of Mexican developmentalism was the product of a stalemate between competing projects and state factions, but was this was a paralyzing dilemma?

The World Bank's US$50 m loan sought to overcome fundamental economic challenges to Mexico's economic growth. The country's economy expanded rapidly during the Second World War, when it exported record amounts of raw materials to supply the US war effort. Industry leapt forward during these years as an unplanned import-substitution process took hold. 11 But in the wake of the war, major economic imbalances threatened to undo recent successes. As exports cooled down and Mexican industry rushed to purchase capital goods in the United States, the country found itself burning through its foreign exchange reserves, and a major devaluation took place in the summer of 1948. The new industries that sprang up across the country were dependent on electricity to an extent that prior sectors were not, and demand for power multiplied. Consumption restrictions were implemented in 1947 and 1948. At the same time, capital goods for the power industry were among the most expensive imports and could only be paid for in scarce US dollars. By providing much-needed hard currency to expand the power industry, which in turn enabled the growth of new industries, the Bank's loan softened the pressure on the country's foreign exchange reserves. An added benefit was that the loan was shielded from the corruption that had plagued other US–Mexican projects. The money never passed through Mexican hands: the power companies drew up lists of capital goods and the Bank paid US manufacturers directly, debiting the loan project's bank account.

The World Bank was not only interested in infrastructural buildout. The loan should be understood as part of a broader Bretton Woods project to spur development by strengthening private enterprise in the developing world. 12 The US government and US-based IFIs saw a robust power industry as a stepping stone to a healthy capitalist economy open to foreign investment. 13 In an industry subject to government-dictated rates, Mexlight and the World Bank allied in pursuit of a legal firewall that would encase electricity, insulating it from Mexico's authoritarian and nationalist politics and subjecting it to neutral, technocratic control. 14 They hoped that this legally secured economic space would protect the power industry's profit-making capacity from political intervention. But this was not to be. Mexlight and the Bank were unable to shield the power industry's profit-making mechanisms from political interference. The reason for this failure, however, is not to be found in a government coalition seeking to seize control of the sector, as happened in other countries. 15 Mexico had gone through a decade-long revolution only a generation before, and as recently as 1938 had expropriated foreign-owned oil companies. Its leaders had to balance spurring capitalist development with addressing the social demands stemming from the revolution. The challenge to the World Bank program lay in the Mexican government's twin fears of inflation and nationalist reaction to foreign ownership of a key economic sector. These fears led to the government's reluctance to increase power rates to the level that Mexlight needed to be profitable. They were ultimately more powerful than international treaties and contracts. The power industry experienced spectacular growth, but the project failed in its broader aim of strengthening private enterprise. Reliant on government credit and tax breaks to avoid bankruptcy and complete construction, Mexico's power industry came out of its first encounter with Bretton Woods more exposed than ever to the winds of politics.

The power industry's modernization was set against the backdrop of a momentous transformation of Mexican politics. Mexico's entry into the Allied camp during the war brought it closer to the United States after the diplomatic crisis occasioned by the oil expropriation. Business–labor relations were normalized as the left's power receded. President Miguel Alemán took office in 1946 with the aim of deepening these tendencies and expanding economic growth. 16 The formation of the Party of the Institutionalized Revolution (PRI) in 1946 was another mechanism for the control of subaltern classes and the centralization of authority. No one better illustrates Mexico's unrevolutionary politics than Alemán himself. 17 The first president who had not earned his legitimacy on the battlefield, Alemán became a shareholder and investor in numerous industrial ventures during his presidential tenure. 18 He and his successors ruled over a significantly more authoritarian and powerful state than the one built in the aftermath of the revolution, but one that nonetheless had to accommodate assertive union and peasant leaders and revolutionary old-timers. The challenge posed by Mexico's subaltern classes had been domesticated, not defeated. Though forcefully committed to strengthening the domestic capitalist class and attracting foreign investors, Alemanistas could not depart too openly from the norms and expectations of the revolutionary social pact. Part of this pact was controlling inflation, which posed a vital threat to the popular classes’ standard of living. As electric power became more tightly woven into the fabric of urban working-class life, keeping power cheap was one way to keep revolutionary promises from seeming too threadbare. 19

Mexico's power industry was concentrated around Mexico City. This area, which housed the largest industrial districts, consumed around half the country's electricity. Since 1903, Mexlight held a monopoly on distribution. In the 1920s the Belgian investment trust Société Financière de Transports et d'Entreprises Industrielles (Sofina) had acquired a controlling interest in Mexlight. Key decisions about the Mexican power industry were thus made in Brussels. In the mid-1920s, Mexlight built major expansions to its generating system, but from the Depression onwards, all new major projects were put on hold. Harried by the Revolution and then the Depression, the company did not pay any dividends on its common stock from 1913 on. Mexlight experienced sluggish growth prior to the war but saw its sales double in the decade after 1940. New demand brought acute strain to the company's unchanged generating capacity. As factories under construction placed orders for electricity, it became clear that Mexlight's system would break down if generation was not expanded. In 1946, a power supply schedule was implemented to prevent large consumers from overburdening the system. Actors across government and industry realized that Mexico's economic takeoff would sputter if electricity supply fell short. 20

Recognizing the problem was one thing; solving it was another. Mexlight, constrained by a regulatory regime that catered to a politics of cheap power, struggled to convert heightened demand into increased supply. Rates were low, credit was scarce, and the supply of capital goods remained subject to wartime restrictions. Sofina had lost some of its most profitable assets in Europe. 21 The Société's leaders were unwilling to commit new equity if they were not sure that it would yield healthy profits. But Mexlight's entanglement with Mexican politics made such investments risky. The tramways, owned by the city government, had stopped paying for electricity and owed over a million dollars. 22 The official newspaper of the PRI refused to pay for its power bills, too. 23 Aware that the company could shut down neither the government's printing presses nor the transport system, Mexlight was compelled to allow large unpaid debts to accumulate. Generation capacity had expanded only thanks to the Federal Power Commission (Comisión Federal de Electricidad, CFE), a state-owned enterprise. In 1944, CFE finished construction on two new generating units that were connected to Mexlight's grid and sold their power wholesale to the latter. These new units were crucial in avoiding a blackout in the immediate aftermath of the war. But they were not enough.

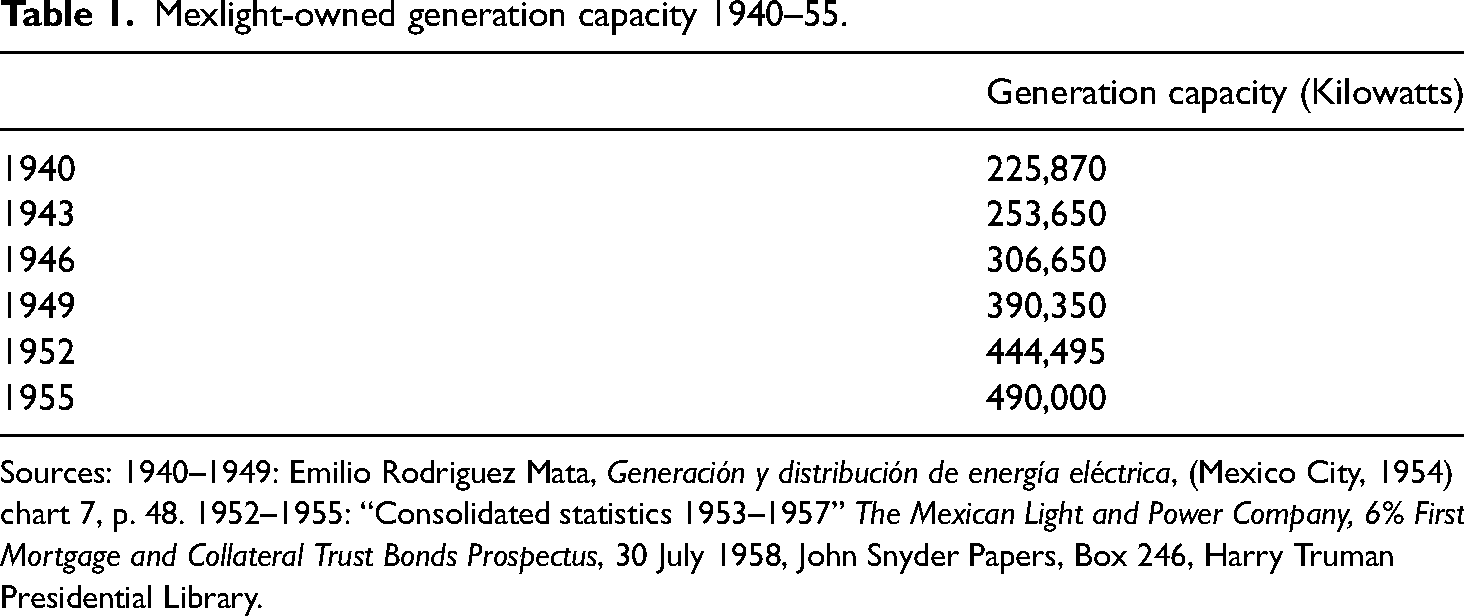

In this context, the Mexican government and the World Bank negotiated a major loan for the power industry – strictly speaking, two loans. Some two-thirds of the total were spent in the Mexico City area. CFE would expand the hydroelectric system west of Mexico City. Mexlight was to expand two hydroelectric dams, build another from scratch, set up a thermal generator, and construct a 200km-long high-tension line connecting the dams in the Puebla highlands with the new industrial districts north of the capital. As shown in Table 1, Mexlight's installed capacity doubled in 12 years. This was the first major loan from the World Bank to a developing country. In focusing narrow-mindedly on the power industry, it tested a pattern that was to prevail over the Bank's relations with the developing world in years to come. George Messersmith, head of Mexlight, captured this sense of experimentation when he wrote that ‘Mexlight has been a sort of guinea pig (…) for the Bank’. 24 While delegates from the developing world – Mexicans foremost among them – had secured a developmentalist mandate at Bretton Woods, the World Bank set the terms on which it was to happen: through private, and whenever possible foreign, initiative. 25

Mexlight-owned generation capacity 1940–55.

Sources: 1940–1949: Emilio Rodriguez Mata, Generación y distribución de energía eléctrica, (Mexico City, 1954) chart 7, p. 48. 1952–1955: “Consolidated statistics 1953–1957” The Mexican Light and Power Company, 6% First Mortgage and Collateral Trust Bonds Prospectus, 30 July 1958, John Snyder Papers, Box 246, Harry Truman Presidential Library.

The product of over 2 years of close involvement by the Bank with different economic actors and government officials across Mexico, the loan was contingent on the Mexican partners agreeing to several conditions before receiving the money. First, the Bank asked the Mexican government to commit money to the loan too, while capping Mexlight's maximum debt to the government. Mexico's development bank, Nacional Financiera (Nafin), loaned Mexlight $44 m pesos ($10 m USD), with a ceiling of $50 m pesos. That is, the government could provide very little extra money to Mexlight over what it had provided at the beginning of the loan. Secondly, the Bank demanded from Mexlight a thorough reorganization of its capital structure. The company's balance sheet was a crazy quilt of asset classes and debenture holders, the product of Sofina's decades-long struggle to keep its subsidiary alive. The Bank demanded a simplification: some bondholders would become shareholders, and the remaining ones would accept second mortgage status for the World Bank's credit to achieve first mortgage status. 26

Finally, the Bank demanded changes in the Mexican government's power to regulate the electricity industry. It is essential to understand the legal underpinnings of the power industry, because it was in this terrain that the ensuing battles were fought. The government would calculate the total capital value of the company. Upon this figure, an annual profit rate was set—say 8 percent. A streamlined accounting system would compute the company's cost items to establish the income needed to obtain this rate. Then, if a cost item, such as fuel or labor, increased, the company could demand the application of an adjustment clause to proportionally increase power rates and obtain the agreed-upon profit. 27 This new set of rules, friendly as they were to the power companies, left several elements unstated. It was not entirely clear how and why profit rates were to be set. 28

The Mexican government broadcasted its goodwill toward the Bank and Mexlight. A few months after the loan project kicked in, it provided the latter with the most significant rate hike in years. This was crucial, for the company planned to reinvest all its profits in the loan project. Mexlight's sweat equity was to make up about a fifth of the total cost of the project, which was calculated at $50 m. 29 The company, recall, had not paid dividends since 1913 and was in arrears with many of its loan repayments. In this way the company's liability was to remain under control. Mexlight was prohibited from distributing dividends during the duration of the project, but it was bound to resume dividend payment right after the project finished in 1953.

From the beginning of Alemán's presidency, Mexico's ruling coalition set its eyes on a large US loan. Minister of Finance Beteta had discussed the matter with US Treasury Secretary John Snyder during Alemán's inauguration in December 1946, and the industrialist and Minister of the Economy Antonio Ruiz Galindo had pushed forcefully for a loan to the power industry during 1947 and early 1948. 30 The alemanistas’ economic plans and projects of infrastructural buildout depended entirely on such a loan. As suggested earlier, they saw this as the fulfillment of the promise made at Bretton Woods. Officials in government were thralled at the announcement of major investments in the power industry, and they interpreted them as a sign of ‘trust’ from foreign capital in the government's economic program. 31 But a US loan had different valences for different sectors of Mexican society, and even for the different factions of the ruling coalition. Conflicts came to a head in the weeks prior to the beginning of the loan project, late in 1948, when the Mexican legislature discussed a law to provide sovereign cover to the loans. ‘How are we going to explain to the Mexican people, to the campesino’, argued a congressman of the People's Party, less an opposition party than an appendix to the PRI, ‘that we are compromising the Treasury … a Treasury formed through the effort of many Mexicans who know nothing of the modern miracles of electricity … for the benefit of a foreign company?’ The alemanistas in Congress turned the nationalist critique on its head: was it not patriotic to have abundant electricity to power the textile mills and the mines’ conveyor belts? The opposition was steamrolled, and the law was approved 84 to 2. 32 As the executive strengthened its grip over the multifarious components of its coalition, when a similar law was up for discussion 1 year later, Alemán's group was able to call for a secret session and approve it without public scrutiny. 33 Congressional arithmetic is unlikely to be a good guide of public sentiment. The critique that coded US financial and political engagement as tantamount to domination found echo in broad swaths of a postrevolutionary society, foremost among Mexlight's own workers. When the US-financed investment plan was announced, union leaders said it represented a ‘moral blow’ to the country, as it delayed the nationalization of the power industry. 34 A cartoon from a communist publication for electrical workers, shown as Image 1, depicted the loans as bait with which the wolf of US imperialism lured the sheep – Latin American countries – to their death.

Sofina, for its part, could do little to improve its subsidiary's domestic popularity, but it could try to improve its leverage in the United States. The Belgian group rushed to integrate its companies into the structures of the US government and business communities. At first, Sofina sought to appoint Secretary of War Robert Patterson as Mexlight Chairman, but these attempts came to naught. 35 They chose instead George Messersmith, former US Ambassador to Mexico, Argentina, and Cuba, and a representative of the Good Neighbor Policy at its zenith. A high US official was needed, Sofina leaders explained, because ‘financing needs [are] all about possible assistance and may necessitate as large as possible American interest’. 36 ‘We need Messersmith to intervene officially in the financial negotiations. We are certain that his appointment will produce excellent results for the entire group’, explained Sofina leader Dannie Heineman. 37 Simultaneously, they brought in several US banks and consultancy agencies – First Boston, Chase, Lazard, Madigan Hyland – to put together financing and technical plans, and to open the doors of US capital markets. 38 Messersmith spent his first weeks as Mexlight Chairman in Washington, DC, not in Mexico, in meetings with the Secretary of the Treasury, Commerce, the Export-Import Bank Board, and officials in the State Department. 39 Sofina sought to parlay its decades-old presence in Latin America to turn Mexlight into a hinge of US-Mexican economic relations. They explained to the US business community that ‘[in the] expansion program which is so acutely needed for the welfare of the economy … Mexico looks to American industry to produce the bulk of the heavy equipment. [The program will] alleviate the power shortage … and will thus further the development of the Good Neighbor Policy of the United States government in this hemisphere’. 40

Construction work launched simultaneously across Mexlight's different sites in early 1949. The company placed orders with capital goods providers and laid the groundwork for the arrival of Westinghouse and General Electric generators and turbines by building some of Mexico's largest reservoirs in the Sierra Madre. But facing a dire balance of payments crisis, in the summer of 1948, the government was forced to devalue the currency. In 1949 inflation climbed to 30 percent. 41 Inflation caused construction costs to increase by at least $10 m, a one-fifth increase above original projections. Making matters worse, Mexico experienced one of the worst droughts of the twentieth century from 1947 to 1950. 42 Mexlight had to rely more on thermal generation than hydropower, driving up operating costs and squeezing profits. Restrictions in place in 1949 and 1950 reduced the company's income by about $2 m. 43

Inflation's most salient consequence, however, was to sharpen the conflict with the Mexican Electrical Workers’ Union (Sindicato Mexicano de Electricistas, SME). One of the oldest and most powerful unions in the country, SME was born during the crest of the Revolution in 1914. At the heart of Mexico's most important general strike in 1916, SME then fended off cooptation by government-sponsored union federations in the 1920s and 1930s. 44 Its power and autonomy derived from its place at the very heart of the capital's transport and economic system, and its sixty-five hundred employees formed one of the most powerful contingents of Mexico's working class. But formal autonomy from the corporatist unions did not mean it was exempt from the violence and corruption that prevailed across Mexican politics. Its leader, Juan José Rivera Rojas, was a PRI senator and close associate of President Miguel Alemán. In power for over a decade, Rivera Rojas’ group strong-armed oppositional factions and made opaque use of the millions of pesos in union dues flowing through its treasury. Rivera Rojas' iron grip over the union depended as much on his vocal campaign against the company as on the gunmen that enforced his wishes. 45 He constantly called for Mexlight's nationalization, arguing that the company was siphoning money off the country and contributing to its balance of payments crisis.

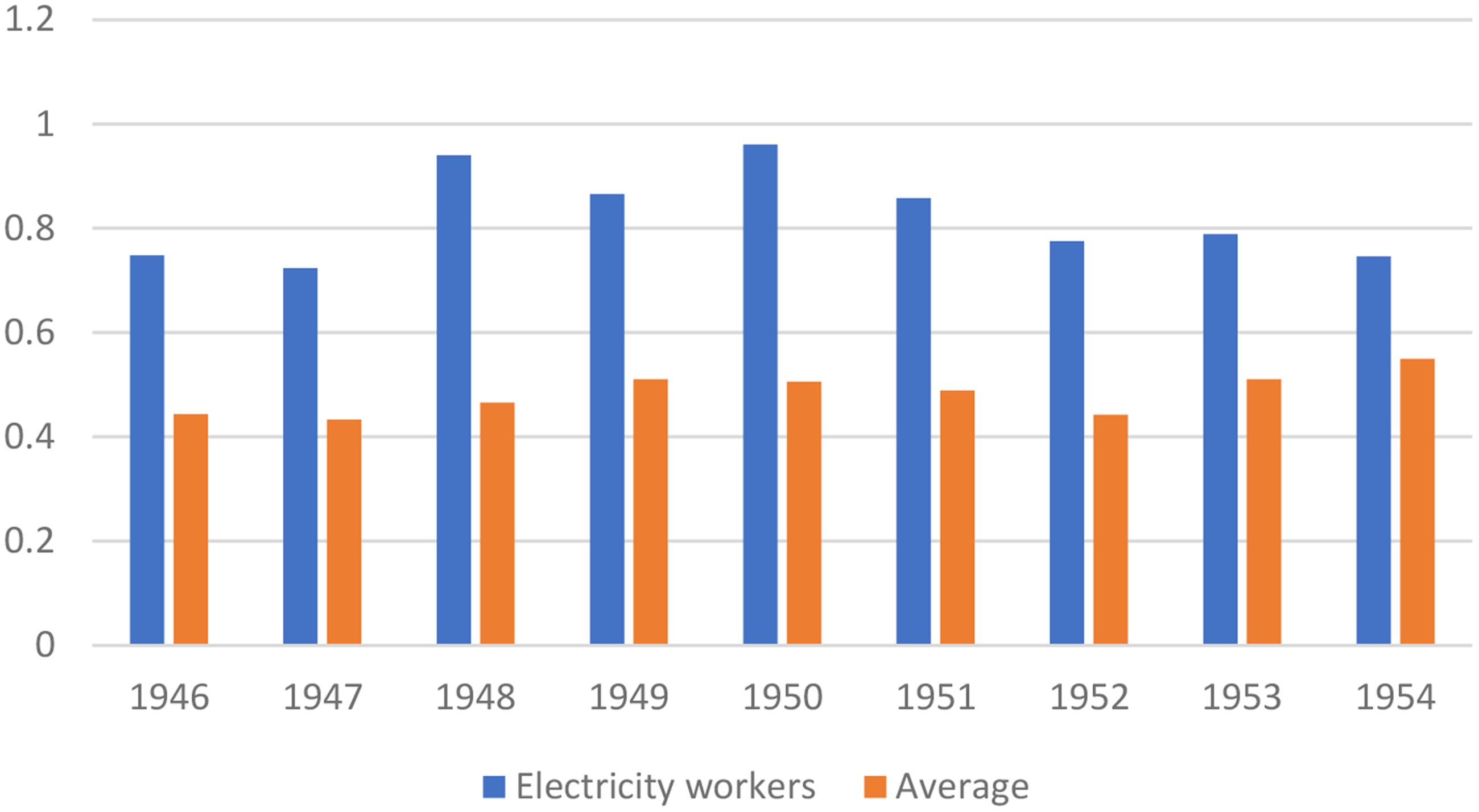

Early in 1950, union leadership asked for a wage increase of 15 percent to make up for inflation. Under the rate adjustment clause, awarding this increase should not have put strain on Mexlight's construction program: rates would increase proportionally to keep profit levels intact. But this mechanism made SME directly responsible for the increase in the price of power. Rivera Rojas demanded that power rates not be raised to make up for the wage increase, arguing that the 1949 rate increase had brought the company windfall profits. 46 After weeks of bitter attacks in the press, in May, negotiations broke down and workers struck. 47 Tramways halted, factories shut, and much of the city's water supply had to be suspended. Alemán's emissaries forced the parties to the negotiating table and concocted a peculiar solution. Because SME argued that Mexlight could in fact make its legally mandated profit rates after providing a wage increase, a 1-year provisional wage increase was awarded. Within a year of the agreement, government accountants would look at Mexlight's books. If its profit levels had taken a hit, the increase would lapse, and workers had to return the 15 percent bump to the company. Mexlight was under no illusion that this would happen, but it had no other option but to accept a presidentially mandated solution to the strike. 48 Union-management struggles should be read in the context of the evolution of electricity workers’ wages, charted in Figure 1. The 1950 increase represented the zenith of SME members’ wage levels both in absolute terms and vis-à-vis average industrial workers in Mexico City; they earned almost double what the latter did. Rivera Rojas' popularity was cemented by his skillfulness at increasing constituents’ wages over and above other sectors. Electricians’ wages had increased 30 percent since 1946, adjusted for inflation, whereas average workers’ wages had increased only 10 percent. Subsequent wage increases were much more modest than the 1950 bump. After this year, SME's wage levels no longer kept up with inflation, and by 1952, a good 25 percent of their earning power had already vanished to inflation. As the gap that separated electricians from Mexico City's deprived working masses narrowed, Rivera Rojas found himself on shaky ground.

When the 12-month period approached, in spring 1951, Mexlight faced the Mexican government's full repertoire of foot-dragging tactics. It had been agreed that the accounting study would be carried out based on 8 months of real accounts and 4 months of projections in order for the solution to be ready exactly a year after the strike. But early in 1951, President Alemán argued that the study would only be legitimate if it was based upon real, not projected, accounts. That pushed the publication date to fall 1951. The company accepted. 49 But by that time, the country was embroiled in the delicate mechanisms of the presidential succession. Midway through 1951, Alemán hand-picked his successor, Adolfo Ruiz Cortines. From then on, the president-in-waiting enjoyed broad authority as the lame duck president saw his powers diminish. Following Priísta politeness codes the decision to increase power rates, which still posed a dual threat of strike and inflation, should be made in by the president-in-waiting. 50 But no incoming president wanted to increase the cost of power as his first policy move. In short, all actors, and particularly the incoming president, had excellent reasons to shy away from raising the cost of electricity. Mexlight's income was fully intertwined with the vagaries of Mexican politics.

There are two main reasons why a rate hike was unpalatable to political authorities. The first is that they were afraid of an inflationary spiral. After the 1949 devaluation, the government went to great lengths to tame inflation. They reasoned that a rate hike affecting transport, industry, and domestic users would undermine these efforts. The second is that in a context of tense, nationalist popular politics, Mexlight was seen as alien to the body politic. Its owners and leadership were all foreign. Minister of Communications Carlos Lazo spoke for a broad swathe of public opinion when he said that Mexlight's very existence was ‘a remnant of imperialism’. 51 In part to temper these spirits, George Messersmith was made company chairman. A New Dealer, Messersmith did much to build goodwill for the company among Mexicans, especially bankers and industrialists. 52 Nonetheless, it remained true that the broader public was bound to see a rate increase as an affront.

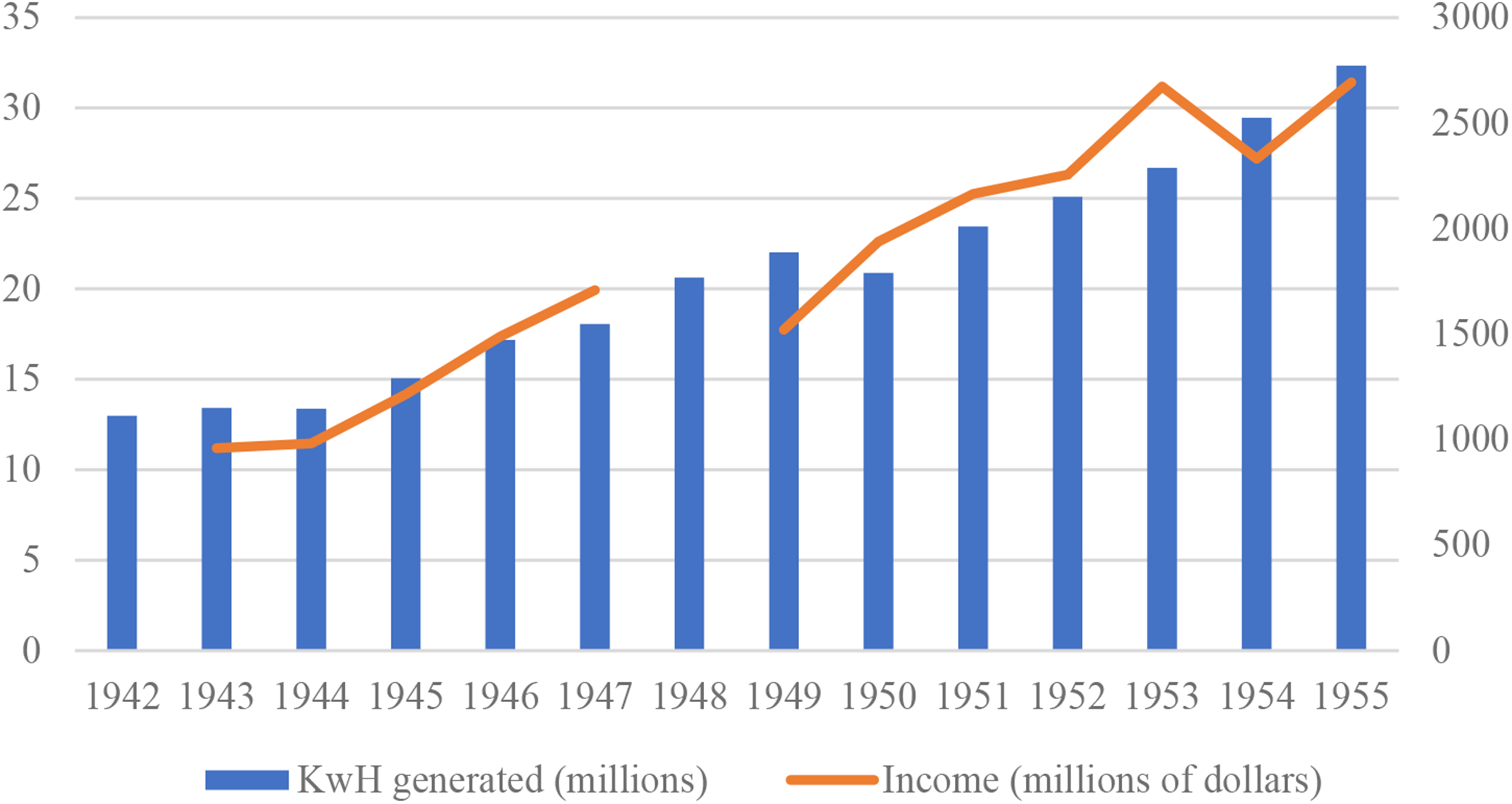

How did these cost increases affect Mexlight's cash situation? As shown in Figure 2, the company's yearly income grew sputteringly during the late 1940s, but when the effects of the devaluation had passed in 1950 it approached $25 m. Midway through 1951, inflation had increased domestic construction costs by $3 m. The wage increase represented an extra cost of just over $1 m a year. 53 Despite growing sales, the company's commitment to reinvest profits into the construction project made for an extremely tight treasury. Before these cost increases, Mexlight had forecasted that it would have less than a $1 m in cash at any time during the next few years: it was all to be reinvested. The upshot of the delay in receiving the adjustment after the strike was that the company would dip into the red by the end of the year. If no quick change was enacted, it would find itself with yearly deficits of 10 to 20 percent of its income during the next years. 54

Electrical workers’ wages vis-à-vis average industrial workers in Mexico City, adjusted for cost-of-living indexa.

Mexlight's generation and incomea.

The wolf of US imperialism luring Latin American countries to their slaughter with the bait of foreign loans (empréstitos).

How could Mexlight extricate itself from this conundrum? The government had signaled that it would not provide a rate increase until the new president took office, in December 1952. The World Bank was unwilling to it expand its credit. 55 In summer 1951, Mexlight knocked on the door of the loan's co-signatory, the Mexican state-owned development bank Nacional Financiera (Nafin). Nafin's director, Antonio Carrillo Flores, responded positively to George Messersmith's request, and opened a credit line of $3 m. This required raising the debt ceiling agreed upon with the Bank, which happily complied. This money would help Mexlight continue construction work during the remainder of 1951, but it would not be enough to see the company through the last year of Miguel Alemán's presidency. 56 Nafin's credit, however, was significant beyond the liquidity it provided. It signaled that important members of government were sympathetic to the company. It was now up to Messersmith to build a coalition to defend Mexlight's interests and force the president to enact a rate increase.

Mexlight's plan was to hold the president to his word. He had promised a rate increase if accounts showed that the company's income targets had not been met after the wage increase. The resolution had been delayed, partially out of government's unwillingness to raise the cost of energy, and partially due to Rivera Rojas' close alliance with Miguel Alemán. But Rivera Rojas was not liked by all members of Alemán's cabinet. Through Nafin director Carrillo Flores’ good offices, in November 1951, Messersmith met with Minister of Labor Manuel Ramírez Vásquez. Ramírez Vásquez wanted Rivera Rojas gone, and he advised Messersmith that Rivera Rojas seemed to be losing ground during the ongoing union elections campaign. If the company launched an offensive against him, the Minister of Labor would support them behind the scenes. The Minister told Mexlight executives that the staunchest opposition to their company came from the Ministry of the Economy, the agency that was supposed assess whether a rate increase was justified. The report had been ready for months, but Minister of the Economy Martínez Báez had refused to share it with the rest of the Cabinet. 57 Mexlight canvased a simple demand to the Cabinet: let the report be known. If it turned out that Mexlight had not made its target profit levels, the president should personally decide whether a rate increase would take place before he left office. Mexlight was able to convince the powerful Minister of Finance to broker a meeting with the president and bring to him the company's views. 58

Early in January 1952, under pressure from Mexlight's allies, the accounts commission made the report public. The result was no surprise: the 15 percent wage increase had sunk Mexlight's profit levels well below its legal targets. The company, at the Minister of Labor's behest, went on the offensive against the union. Since the 15 percent wage increase was conditional on meeting profit targets, Mexlight immediately slashed wages by that same amount. Rivera Rojas did not flinch: SME planned a strike unless a 45 percent wage increase was awarded. 59 But the Minister of Labor had control of the labor courts, which ruled that a strike would be against the law. Messersmith responded to the union's use of the press with a public campaign of its own. Mexico's most important industrialists came together around the power company, decrying in newspapers and on radio how destructive a new strike would be, and, ironically enough, defending the need for a rate increase to assure reliable electrical service. 60 Antonio Carrillo Flores sponsored the settlement with the union. 61 SME accepted a reorganization scheme. Mexlight conceded the 15 percent wage increase granted in 1950 and awarded an extra 10 percent, valid over the next 2 years. 62 Now at least the cards were on the table: the wage increase was no longer conditional, and there was no doubt that the company was not making its legally mandated profit targets. Messersmith and associates could now focus their efforts on securing a rate adjustment.

The Bank had remained in the back seat through these events. By spring 1952, however, the Bank's unhappiness with the Mexlight situation had become palpable. They took the government's delayed implementation of the adjustment clause as a betrayal of the spirit of the loan project. Bank officials were unhappy with the company for letting itself be drawn into the political mud and failing to draw a line before its financial situation became dire. Mexlight might have won a political victory against the union, but their reinvestment plans had so far failed. Moreover, the construction work on the most important dam in the eastern Sierra Madre had suffered delays. 63 The entire project seemed on the verge of collapse.

In early 1952, the Bank sent a team to convince Alemán to raise rates and obtain a picture of where the loan was going. At the behest of this team, Mexlight carried out forecasts to calculate what the long-term consequences of the cost increases would be. These scenarios showed that Mexlight's tight reinvestment scheme had capsized. If no significant rate increase was awarded soon, the company's deficit for the construction program would reach unsustainable levels. In 1953 alone, there was a hole in its books of $12 m, half its yearly income. The way out of this deadlock, the Bank argued, was to insulate rate-setting decisions from cabinet politics. They proposed setting up an interministerial technical committee to study Mexlight's financing needs. The committee ought to issue a binding decision regarding power rates. 64 They argued that while Mexican electricity law mandated company-friendly adjustments, the institution in charge of running the numbers and awarding rate hikes belonged to the Ministry of the Economy, considered a redoubt of leftists and nationalists. If the law could be applied by a ‘neutral’ institution, the problem of creeping politicization could be removed. 65 Here we see the most transparent expression of the Bank's strategy to strengthen private enterprise by securing the terms and the staffing of regulatory agencies.

Bank officials’ sojourn in Mexico helped the pro-Mexlight coalition in government to coalesce. Carrillo Flores emerged as the Bank's key ally and interlocutor. 66 The plan for a rate-setting committee relied, in fact, on knowing that Nafin and Carrillo Flores would hold the upper hand in it. To bring the Ministry of Finance on board, Bank President Eugene Black sent Finance Minister Ramón Beteta a firm missive expressing its disappointment with the government's behavior. 67 Beteta, worried at Mexico's loss of face, liaised with President Alemán and gave his backing to the independent committee. Alemán greenlighted it. The company awaited its decision as the last few millions of pesos in its coffers were spent on the construction program.

The committee issued its ruling in early June. There was to be no rate increase. Nafin's emissaries were elbowed out, and Beteta's remained silent. The committee's decision had been made at the behest of President Alemán. 68 The adjustment clause to make up for increased labor costs was to be delayed further. Any decision about a rate increase, vital as it was to the country's economy, ought to be made by the coming president in 1953. But the ruling confirmed the government's commitment not to let construction work grind to a halt. The country's international credit could be affected if it did, and Mexico's new loan applications with the Bank would be imperiled. They offered Mexlight a new loan of $4.6 m to bridge the gap until the new government came in. 69

Disappointed, the Bank decided that it ought to step up its involvement. Bank President Eugene Black told Messersmith that they would support Mexlight if the company rejected the offer and used their nuclear option: stopping construction work. 70 In September 1952, the Bank and the International Monetary Fund would hold their annual joint meeting in Mexico City. This provided Mexlight a perfect setting to go nuclear, but it was a risky gambit. For the company to halt construction on the most important infrastructure works carried out in decades, in front of an audience of central bankers, would back the Mexican government into a corner. While Mexlight had the Bank's support in this line of action, its very suggestion elicited frantic opposition from the company's Mexican allies. Carrillo Flores hurried to convince Mexlight to walk back this threat. Even if they obtained a rate increase by cornering the government, he said, this would be read as blackmail, and the company would lose any goodwill it had garnered from officials. Difficult as the situation was for the company, he argued, it was a sensible principle that it was the coming President's prerogative to make a vital economic decision. The head of Nafin told them that he would provide all the financial support necessary to see that construction proceeded apace. 71

Mexlight accepted the committee's ruling. 72 The company was on a cliff's edge. They had drawn down the credit provided by Nafin faster than expected. Out of cash, they had stopped paying workers’ fringe benefits and social security contributions. They delayed all construction not already under contract and stopped paying the CFE for energy purchased from it. If no solution was found quickly, they would not be able to meet their most basic obligations. 73 But the company's unwillingness to confront its adversaries changed the Bank's opinion of its Mexican partners. 74 In an official letter to Finance Minister Beteta, Black argued that it was not just the power industry what was at stake, but ‘the preservation of the balance between the forces of public and private enterprise’. 75 This scolding of Mexico's most important economic policymaker marked a dramatic change in tone in the Bank's relationship with the country. But this scolding was, in the end, an expression of vulnerability. In internal memoranda, Bank officials argued that if Mexlight was now ‘forced to fight in the last ditch a battle that could have been much better fought’ before, then the Bank should not ‘allow itself to be maneuvered into the position of Mexlight's whipping boy. (…) The Bank ought not to take the initiative in trying to avert a crisis. It would indeed be desirable to let the storm break’. 76 Pulling out of Mexico would be much more damaging for the Mexicans than for the Bank. The Mexican government responded to Bank pressure with complete silence. Throughout this period, Beteta afforded himself not to respond to Black's official letters, and the doors of the Presidency and Secretary of the Treasury were likewise closed to Mexlight. This was in part a consequence of a real paralysis gripping Mexico's ruling coalition, fearful of the consequences of a rate increase but lacking a clear strategy to improve the financial health of the power industry. But one can also read Beteta's silence as a statement of power. The loan had already been disbursed. The dams were being built. Was the Bank going to walk out? It was the Mexican government's prerogative – top officials seemed to say – to decide when and how to increase rates.

Aware of the Bank's disappointment, Mexican officials took the opportunity provided by the Bankers’ Meeting to smooth things over. Eugene Black met with incoming President Adolfo Ruiz Cortines, who made an impression of ‘seriousness and modesty’. Antonio Carrillo Flores let it be known that he was to be the next Minister of Finance and that he would see that Mexlight's interests were taken care of. The government offered more cash and a tax exemption to make sure that the company did not run out of money in the remaining months. The Bank found hope in the departure of Miguel Alemán's associates and in the arrival of their closest ally to the most important cabinet position. 77 The alternative, to concede that their involvement with one of the world's most important developing countries had gone awry, was costly. One cannot overstate how important this loan was for the World Bank and how accommodating they were of Mexican idiosyncrasy. Their first in-depth involvement with a large developing country, the Mexico file mattered not just for the country's sake or for the $50 m dollars loaned, but due to its laboratory-like character. This was a guinea pig, as Messersmith had suggested, but it was one handled with kid gloves. The French representative at the Bank, for instance, complained that the Mexicans got away with things that the French could never. 78 True to this spirit, Eugene Black told Carrillo Flores that ‘the Bank was approving this operation only on the understanding that the new Administration would vigorously tackle the problem of finding a longer-term solution to the company's financial problems’. 79 As one Bank official recognized, they were ‘relying entirely on Carrillo's goodwill’. 80

It is worth pausing for a moment to make sense of the agency that emerged as the key lender to the Mexican power industry. Nafin had been founded in the late 1930s as a development bank charged with spurring Mexico's industrialization. Only truly active after 1941, during its first decade of life it primarily supported agricultural enterprises and irrigation schemes. In the aftermath of the Second World War, under Carrillo Flores, Nafin reoriented its energies toward industrial ventures. During the period 1945–1955, its total lending increased fivefold. 81 But its lending remained marginal in relation to the wide array of industrial ventures that needed credit. Numerous scholars have shown how inward-looking Mexican banks remained throughout the twentieth century, their credit focused on a handful of large firms connected by blood or marriage. 82 The capital needs of the power industry were well above the financing capacities of the local banking sector, which Mexlight found ‘confined almost entirely to real estate’. 83 The power industry emerged as Nafin's most important client. During the period considered, Nafin provided Mexlight a grand total of $41 m, well above the $26 m the Bank had provided. 84 Against the backdrop of the credit-scarce Mexican economy, this was an enormous amount: the federal budget amounted to less than $260 m during the late forties. Providing Mexlight with this money was thus not just a significant fiscal effort, but also a risky political statement. The power industry, after all, was one of the few sectors that had already found capital abroad. In leaving an open flank to the accusation of favoritism toward foreign companies, it exposed the government to nationalist attacks. There was also the financial side to Nafin's support: since the World Bank credit had taken first mortgage status, what were the chances that Mexlight could repay its Nafin loans in time?

Nafin's financial commitments provide a window onto the relationship between Mexican capitalists and the developmental state. The funds provided by Nacional Financiera did not originate in the federal budget, meaning they did not come from taxation. Officials in the Ministry of Finance and the Central Bank had implemented two sets of heterodox policies to finance infrastructural buildout. On the one hand, the booming insurance and private banking sector was forced to invest 20 percent of its assets in state bonds. A variety of bonds were offered, from ‘National Savings Bonds’ to road construction and power industry bonds. With different repayment periods (ranging from 5 to 25 years) and different interest rates, they were all guaranteed by the federal government. While the government hoped to find broad demand for them, this bond-purchasing public never materialized, and in the spring of 1947 bankers were forced to step up their contribution to 30 percent of their assets. 85 Some bankers complained bitterly about this practice, which in their view encumbered their freedom to allocate capital as they saw fit, thereby threatening the functioning of the credit market. 86 At the same time, private bankers were represented in the corporatist structures of the Central Bank, and the committee in charge of bond operations was staffed by the best-known names from the country's private banks. 87 The largest or second-largest of these bond issuances were power industry bonds. With nonexistent public demand and having reached the limit of semiforced contributions from domestic capitalists, the government nonetheless needed to sell more bonds to finance its infrastructure projects. From 1945 onwards, a clear pattern emerged in which the Mexican government forced the Central Bank to purchase its own bonds by printing paper money to pay for them, money that was transferred to Nafin, which in turn loaned it to Mexlight. By the end of 1948, the Central Bank had in its coffers MXN$103 m (US$15.8 m) in power industry bonds and had recently purchased the entirety of an MXN$60 m bond offering. 88 The US Treasury and Bretton Woods institutions were critical of this practice and sought to obtain commitments from the Ministry of Finance that it would be reined in. 89 Central Bank bond purchases and inflationary spending were curtailed after the 1948 devaluation. But these avenues remained open to the Mexican government. When the head of the Central Bank asked Minister of Finance Ramón Beteta for assurances that the budget would be balanced, Beteta disavowed him: ‘he needed 200,000,000 pesos additional for the balance of 1948 and would need an additional 500,000,000 pesos annually thereafter’. 90 Despite the pressure, foreign or macroeconomic, to curtail inflationary paper printing, when Mexlight faced bankruptcy, economic officials hurried to its aid.

On 1 December 1952, Antonio Carrillo Flores took office as Minister of Finance under President Ruiz Cortines. Mexlight and the Bank rejoiced. 91 He was the man of the hour -celebrated by the leading newspaper's editorial as a man of ‘ancestral and congenital probity’. 92 The union was shaken up by the Presidential permutation too. When the President departed, Juan José Rivera Rojas’ days at the head of the union were counted. Challenged by internal opposition, his final gambit was to present himself as the victim of the dark forces of imperialism: he accused Messersmith of hiring gunmen to have him killed. 93 The public did not buy the story and Rivera Rojas was routed in the elections. The new union leadership, moreover, exposed in the press the corruption of his administration, which went well beyond graft to include orgies in the union's offices with sex workers paid by union fees. 94

In mid-January 1953, George Messersmith and Carrillo Flores met to discuss the company's situation. The finance minister was candid: He wanted to help Mexlight, and the best way of doing so was to award a new rate of return. This would increase its earnings over and above what an adjustment clause, which could only maintain profit levels, would. But the new president was crusading against inflation as a means of distancing himself from the corruption and overspending of his predecessor. A generalized increase in the price of power did not sit well with this. President Ruiz Cortines, Carrillo told Messersmith, was sympathetic to Mexlight. He just asked for a few months. The government was ready to provide all the necessary cash and a tax exemption to finish construction, and a proper rate increase in the last quarter of 1953. 95 In spite of a friendlier government, Mexlight remained encircled by the politics of anti-inflation. But anti-inflation worked both ways. When the new union leadership demanded a raise, the company responded that they were committed to the government's policy of inflation control. Increasing wages would mean increasing the cost of power. Did the union wish to bear the burden of breaking the social pact? A secret agent hypothesized that if enough government pressure was put on them, SME's leaders would fall in line. 96

The loan contract's reorganization scheme added to the problem. Shareholders had accepted the reinvestment of their company's profits during the 5 years of the loan project. But in 1953 the company was obligated to start paying dividends on its shares. Otherwise, it would fall into receivership. That is, control of its operations would pass to a creditors’ committee. Under Carrillo's proposal, the Mexican government would provide the company cash to pay its foreign owners, a politically unpalatable arrangement. Carrillo brushed the issue aside and said that everything must be done to prevent Mexlight from falling into receivership. 97 Mexlight accepted the terms of this offer and proceeded to carry out the surveys and forecasts upon which a new rate of return was to be demanded. In consultation with Chase National Bank and First Boston Corporation, the power utility computed its best-case scenario: a gross return of 13 percent on its capital could see them finish construction with their own resources and start paying dividends. This meant an income of 9.5 percent, net of taxes and financing costs. 98 In 1949 the government had awarded Mexlight an 8.6 percent gross income for a 6 percent net. This rate would represent a significant hike.

Carrillo Flores’ advocacy came to naught. In early spring 1953, the new rate was communicated. It was to be 7.5 percent net, well below what Mexlight expected, and it would kick in in October at the earliest. While higher than the current rate, 7.5 percent would not let Mexlight finish construction work, let alone repay the extra loans they had contracted, or start paying dividends. 99 What was more ‘outrageous’ to the Bank was that the government offered them a rolling subsidy arrangement, whereby if the rate award was delayed or if costs increased, the government would make up for the gap between the money it was making and its profit targets. It was an acknowledgement that the award might in fact take much longer, and that the adjustment clause mechanism was dead in the water. On top of this, the government was ready to provide a loan to finish construction work, scheduled for early 1954. Accepting a subsidy arrangement would ‘destroy the company's capacity to obtain financing’ in capital markets, for it left its income-generating capacity entirely at the whim of government decisions, Mexlight's leadership believed. 100 It was, in short, the exact opposite of the Bank's program of a legally secured dimension for profit-making.

The Bank wasted no time in preparing a response. They wanted a course of action to be decided by all the stakeholders in the loan project. They scheduled a joint meeting between their Loan Committee and Mexlight's board, composed by board members based in Mexico, Sofina's representatives, and John Snyder, who had just left office as US Secretary of the Treasury. Preparations were made to bring in the State Department, for ‘only negotiations at the highest level are likely to produce this result’. 101 During the meeting, held in the New York offices of First Boston Corporation, Mexlight's executives explained that the company could do nothing but accept the government's award. Halting construction, they argued, brought political peril, opening the door to nationalization. The Bank would have none of it. If Mexlight did not draw a bright line, the Bank would walk away, and the company would be on its own. Mexlight's leadership was divided, and Messersmith changed track. The company should not deplete its reserves to pay for construction work, he said, and wondered at what point in the ongoing depletion of their reserves they should stop construction. The joint meeting agreed that a subsidy would be disastrous, but during the discussion a preference for a tax rebate over a direct cash transfer emerged. The final issue was whether the Bank was to veto – as was its right – the new loans Nafin had promised Mexlight. Softening its hardline position, Bank executives stated they would not, but they demanded a repayment proviso. New credits could only be repaid from the increased earnings obtained from the new rate. In this way the government had an incentive to award the company a higher rate of return. 102

Why had Carrillo Flores, Mexico's supreme economic policymaker, failed to award a friendly rate to the power company? One last plot twist was in store. In May 1953, the government awarded Mexlight the 7.5 percent net profit rate the company and the bank had been informed of a few weeks before. But reviewing the complex calculations behind the award, Mexlight's officials realized that there was a key change in the way the company's expenses had been computed. Net profits had always meant profits net of taxes, and only taxes. But the documents they had been handed understood net profits to mean net of taxes and debt service. For a company as highly leveraged as Mexlight, this was a major difference, increasing its profit mass by millions of dollars. In fact, under this definition, Mexlight's gross profit rate was the same its US bankers had arrived at as a best-case scenario, over 13percent. Was this a mistake? Messersmith now recalled that Carrillo Flores had asked to see the financial analysis carried out by Chase and First Boston. The Bank and the company raced to figure out whether the new government had made a mistake, or whether this was the way Carrillo had found to award the company the rate it demanded while avoiding cabinet insurgency. The Bank told them that they had to assume that the Mexican government was cognizant of what it was doing ‘without giving the impression that they thought it too good to be true’. 103

A game began where Mexlight and the Bank, when talking to Mexican officials, made passing reference to the rate of return while winking the eye, and anxiously examined their interlocutors’ faces to find out whether they were winking back. They could not get confirmation from Nafin's director nor from the ambassador to the United States, who did not seem to understand what was happening. 104 Not even Eugene Black, when talking on the phone to Carrillo Flores, could fully corroborate what the new award meant. Messersmith talked with the Minister of Finance, but the most confirmation he could get was that the Minister ‘did not blink when it was pointed out to him that the rate of return, as calculated by the Mexican government, was after deduction of interest as well as of taxes’. This was enough, and Messersmith became convinced that the awarded rate was no mistake. 105

It only took a week for Mexlight's dreams to be crushed. On June 12, Minister of the Economy Gilberto Loyo, who formally issued the decision, responded with a strongly worded and bitingly ironical letter. Including debt service in the calculation of net income, he said, was neither common practice nor the law. 106 ‘Messersmith called me this morning to say that his worst fears had been realized’, wrote a Bank official. 107 The company was back to square one, facing a low profit rate, and out of political cards to demand a higher one. Carrillo Flores' stealth award was a fragile tactic. Loyo had gone along with the ruse at first, but when officials in his Ministry and the head of the Federal Power Commission became aware of the plan, they cornered him into opposing it. Stoking nationalist feelings aroused by the foreign power company, Loyo won over the president, who was happy to hear a good reason not to raise power rates. 108

Mexlight's income was far from enough to finish construction work, let alone make profits. 109 The company issued a formal notification that the project was imperiled. Bank President Eugene Black called on Carrillo Flores to signal his displeasure. 110 Clearly worried, the Mexican government issued an amended resolution in September. The rate would be half a percentage point higher, though well below what the company wanted. 111 Most importantly, Nafin offered a $20 m, 22-year-long loan. 112 In Mexican pesos this was over four times what Nacional Financiera had provided at the beginning of the loan project. The loan would let Mexlight finish construction work and fulfill dividend payment obligations. The company's tax exemption arrangement was extended, too.

The last construction items, the Patla dam in the Eastern Sierra Madre and the high-tension line that connected it to Mexico City, were completed in the first half of 1954. With the lush mountains as their background, Mexican officials, foreign bankers, and power executives came together for President Ruiz Cortines dedication of this massive hydroelectric plant. 113 Throughout these years, Mexlight's customer base widened, and with increased sales at a higher price it was able to make modest profits. Rate wars had verged on catastrophe, but when the most dramatic moment of construction and labor insurgency had subsided, the company found itself making more money than ever and in command of a state-of-the-art fleet of generators. From the government's point of view, the most significant upshot of the loan project was the dramatic expansion of generation capacity in a vital region. Mexico City never again faced blackouts like it did before 1952. The Bank and the company congratulated themselves, but they had failed to achieve their most important goal. The Bank's strategy for an insulated, healthy power industry was crushed. The law existed, but it was a dead letter. The industry's profit-making mechanisms were subject to the vagaries of cabinet politics, presidential cycles, union insurgency, and nationalist sentiment. Not even the friendliest of policymakers had been able to turn the tide. The Bank's project to ‘retain the balance between the forces of public and private industry’ teetered, even as this industry expanded. It was challenged not so much by political antagonists as by the government's innate fear of inflation and loss of legitimacy. As this process unfolded, debt emerged as the path of least resistance. It let all opposed actors avoid a reckoning: it let government keep rates low; it let the company achieve modest profits; it showcased Mexico's commitment to infrastructural development; and it let the union increase wages, too. But in buying time, it brought about a host of new problems. The country's most important private company remained dependent on government credit and tax concessions for its very survival, let alone its expansion. Mexlight came out of the construction project burdened by debt. Nafin, conceived to provide credit and spur broad industrial growth, used a growing share of its resources in the power industry, the one sector that had access to foreign funds. 114 The unintended consequence of the World Bank's program was to place the industry's regulation, generation, and financing in the hands of government.

IFIs like the World Bank wielded an uneven power in a developing country like Mexico. The Bank could set the technical and financial tune of infrastructural buildout, but it had a harder time untying the political knots that stood in the way of its project of institution building. The Bank was not ready to dissociate itself from the project's management and had little power to block further loans, although at critical moments it considered these options. The credits that Mexico applied for were endorsed by the US government and had been negotiated with Truman's Treasury. The political and economic stabilization of Mexico was one of the centerpieces of US foreign policy for the developing world, and a squabble over a few percentage points of profitability for the power industry was not going to overturn this policy. For Mexico, its guinea pig status and its importance to the world's new hegemon allowed it to reap substantial benefits in its negotiations with the World Bank. When, in late 1954, Mexico faced its last major devaluation until 1976, the Bank awarded it its single largest loan to date. A decade later, Carrillo Flores still thanked Black for his steadfast support in sending markets a sign of confidence despite the recent tensions. 115 But if one can find ample evidence of Mexican stubbornness in the face of development institutions’ blueprints for economic and social engineering, this obduracy cannot be read as resistance, and Mexico's development policy can be meaningfully conceptualized neither as an attempt to break away from the US-based financial order, nor as an effort to reform it. The central dialectic of this period is best understood as one of the deliberate integration into US-centered capital flows and development institutions. The actors who carried forward this integration – officials, businessmen, and experts – and the mechanisms through which it took place remain in need of further study.

What new light does this study of the power industry shed on the Mexican state? Mexico's ruling coalition pursued a bold project of development through infrastructural buildout, had a sober understanding of the need for US support to realize it, and was skilled at positioning itself as a laboratory of development at a time when no blueprint for similar projects existed. As Raymond Vernon would argue a decade later, policy options were constrained by the political imperatives inherent in the Priísta coalition. The Mexican government could not forcefully adopt a pro-company policy that would have incited nationalist wrath and inflationary pressure. But neither could it forgo collaboration with the companies, much less consider taking them over. However, the space between these two policy choices was broader and more open to creative arrangement than what Vernon believed. Mexico did face a developmental dilemma, but it was not a paralyzing one. The Mexican government could afford a decade-long stalemate in the power industry because during this stalemate, the industry grew, modernized, and met consumers’ needs. The Mexican state did not have the ability to break the deadlock brought about by the industry's structural problems, either in a statist or a pro-capital direction. Decisions about whether profit rates were set at 8 or 13 percent, or whether the adjustment would kick in after a month or a year, were made in the headwinds of enormous political pressure. But when officials decided to address Mexlight's problems by providing inexhaustible credit, they handed the reins of a politically sensitive sector to the President and his top officials. The discretionary use of government finance shielded government policy towards the power industry from public view and political challenge. Officials would tug on these reins less with foresight than with brinkmanship, seeking to soften the short-term pressures coming from labor, consumers, and foreign banks. The result was suboptimal for everyone involved: lenders and borrowers, generators and consumers. Underwritten not by healthy profits but by World Bank credit and Presidential grace, Mexlight limped forward, more vulnerable than mighty.

Footnotes

Acknowledgments

For their patience and gracious feedback on earlier drafts, the author would like to thank Elizabeth Chatterjee, Aurora Gómez-Galvarriato, Emilio Kourí, William Sewell, Jon Levy, Paul Cheney, and the participants of the History of Capitalism Workshop at the University of Chicago, particularly Eduardo Terra, Nico Santistevan, Atman Mehta, and Juan Wilson. My thanks also to the three reviewers for their comments, which greatly improved this article. This piece owes the most to Kate Reed, and I thank her warmly for her careful revision and comments. Archival research was made possible by the University of Chicago History Department and by a François Furet fellowship from the France Chicago Center.

Biographical Note

Archival Sources

World Bank Group Archives, Mexico, Power Project 7499

Folders: 1695885, 1695888, 1695889, 1695890, 1695891, 1695892, 1695893, 1695894, 1695895, 1695896, 1696897

George Messersmith Papers, University of Delaware Special Collections, Messersmith-Daniel Heineman Correspondence.

Ministère des Affaires Etrangères (France) – Archives Diplomatiques, Site de La Courneuve, B Amérique, Mexique.

National Archives and Records Administration, Harry Truman Presidential Library, John Snyder Papers, Box 243.

Archive General du Royaume du Belgique, Sofina-2

Archivo Histórico del Banco de México, Sede Legaria

Archivo Histórico del Banco de México, Sede Centro Histórico

Archivo General de la Nación (Mexico), Ramo Presidentes, Miguel Alemán Valdés

Archivo General de la Nación (Mexico), Dirección Federal de Seguridad

Centro de Estudios de Historia de México CARSO, Fondo Antonio Carrillo Flores, CCCLXII