Abstract

The authors examine purchase behavior in the context of cashback shopping—a novel form of price promotion online in which consumers initiate transactions at the website of a cashback company and, after a significant delay, receive the savings promised to them. Specifically, they analyze panel data from a large cashback company and show that, independent of the predictable effect of cashback offers on initial demand, cashback payments (1) increase the probability that consumers will make an additional purchase via the website of the cashback company and (2) increase the size of that purchase. These effects pass several robustness checks and are also meaningful: At average values in the data, an additional $1.00 in cashback payment increases the likelihood of a future transaction by .02% and spending by $.32—figures that represent 10.03% of the overall impact of a given promotion. Moreover, the authors find that consumers are more likely to spend the money returned to them at generalist retailers, such as department stores, than at other retailers. They consider three explanations for these findings; the leading hypothesis is that consumers fail to treat money as a fungible resource. They also discuss implications for cashback companies and retailers.

The continued growth of e-commerce is motivating firms to test new means of reaching and enticing consumers with better prices—anything from voucher codes to different models of daily deals and group buying. Within this context, cashback shopping is a relatively young but increasingly popular alternative. For example, Ebates, the leading cashback company in the United States, has processed cashback payments of more than $800 million to over ten million consumers since it began operating in 1998. In the United Kingdom, Quidco processed more than $64 million of cashback payments to its seven million registered users in 2016 alone and facilitated sales of close to $1 billion for 4,300 retailers—a figure that represents 1% of all e-commerce in the country for that year. 1

The feature that distinguishes cashback shopping from its peers is that consumers can view cashback offers and initiate purchases at the website of the cashback companies rather than directly with individual retailers. These offers are negotiated in advance with retailers and posted on the website, typically as a percentage of money spent. The cashback company earns a commission on each transaction that occurs and, on receiving this commission, deposits cashback payments directly into the bank accounts of consumers. Importantly, the delay between a given purchase and the cashback payment is significant: a minimum of 30 days, but often as much as four months.

We study data from a large cashback company to understand the impact of cashback payments on purchase behavior. The data record cashback offers, cashback payments, and individual purchases over a period of more than eight years. We find two notable results. First, cashback payments increase the probability that consumers will make an additional purchase via the website of the cashback company. Second, cashback payments increase the size of that purchase. These effects pass several robustness checks. They are also meaningful: At average values in the data, an additional $1.00 in cashback increases the likelihood of a future transaction by .02% and spending by $.32—figures that represent 10.03% of the overall impact of a given promotion. Notably, the impact of cashback payments is separate from that of cashback offers on initial demand—that is, although consumers likely respond positively to cashback offers, they again respond positively to cashback payments.

Moreover, cashback payments affect purchase behavior differently depending on the type of retailer. Specifically, consumers are more likely to spend the money returned to them at generalist retailers, such as department stores, than at other retailers. This insight has implications for the design of cashback promotions (which are pertinent to cashback companies) and the logic of participating in such initiatives (which is pertinent to retailers). A more fundamental point, however, is that any such practical advice is beneficial insofar as the relevant players are aware of the influence of cashback payments. The following quote from the managing director of the cashback company that facilitated access to the data suggests, however, that this may not always be the case: “We spend a lot of time designing offers that are profitable for retailers and give our users maximum value. Of course, an essential part of our work is to ensure they receive the payments they are promised, but we have never spent time looking at what the repercussions of these payments may be.”

From a theoretical standpoint, our main goal is to bridge the gap between the growing use of cashback shopping and the understanding of the phenomenon. Our research adds empirical evidence to studies that are predominantly analytical in nature (Chen et al. 2008; Ho, Ho, and Tan 2017; Zhou et al. 2017). To our knowledge, the only other empirical study on the subject focuses on the relationship between the size and composition of a user’s network and the extent and pattern of navigation at the cashback company’s website (Ballestar, Grau-Carles, and Sainz 2016). By contrast, we examine how consumers react to cashback offers and payments. The idea that consumers are susceptible not only to the promise of a saving but also to the later payment of that saving is striking because they are free to spend or save this money in any way they choose. We consider the possibility that consumers fail to treat cashback payments as a fungible resource and also that cashback payments act as a scheduling mechanism or prompt a transient state that then affects purchases. The data lend support to the first hypothesis.

In addition to this, our study provides two contributions to the literature. First, we add to research on price promotions online, which to date has focused on instances of group buying (Wu, Shi, and Hu 2014) or daily deals (Aydinli, Bertini, and Lambrecht 2014; Luo et al. 2014). Second, we complement research that questions the logic of delayed discounts. These studies examine the psychology underlying redemption behavior (Gilpatric 2009; Soman 1998) or the economics of tying the payment of a saving to a second purchase (Dhar, Morrison, and Raju 1996; Raju, Dhar, and Morrison 1994). While we describe a setting in which low redemption and forced purchases are irrelevant (cashback payments are automatic and unconditional), we find that delaying a discount is still beneficial.

Empirical Setting

The Data

A nondisclosure agreement prevents us from revealing the name of the cashback company that shared the data, the geographic area in which it operates, or the local currency. For ease of exposition, we convert all monetary values into U.S. dollars. The data span from May 2005 (when the firm started operating) to August 2013. We have information on every purchase by a sample of 76,296 registered users (consumers) of the cashback company in response to every cashback offer and the corresponding cashback payments. 2 We observe 3,433,476 transactions by these consumers at 5,337 retailers. Consumers registered with the cashback company at different points in time and thereafter received emails promoting current cashback offers. The demographic information for a subset of consumers suggests that they are representative of the overall population, albeit somewhat younger and disproportionately male.

Consumers face no restrictions on the number or timing of purchases. We observe the total amount spent by a consumer on a given day, at a given retailer, and for a cashback offer of a given size. We do not observe details such as the type, category, or quantity of the items purchased. Multiple cashback offers from a retailer on a given day and a consumer’s actions on more than one of these offers are recorded as separate purchases in the data.

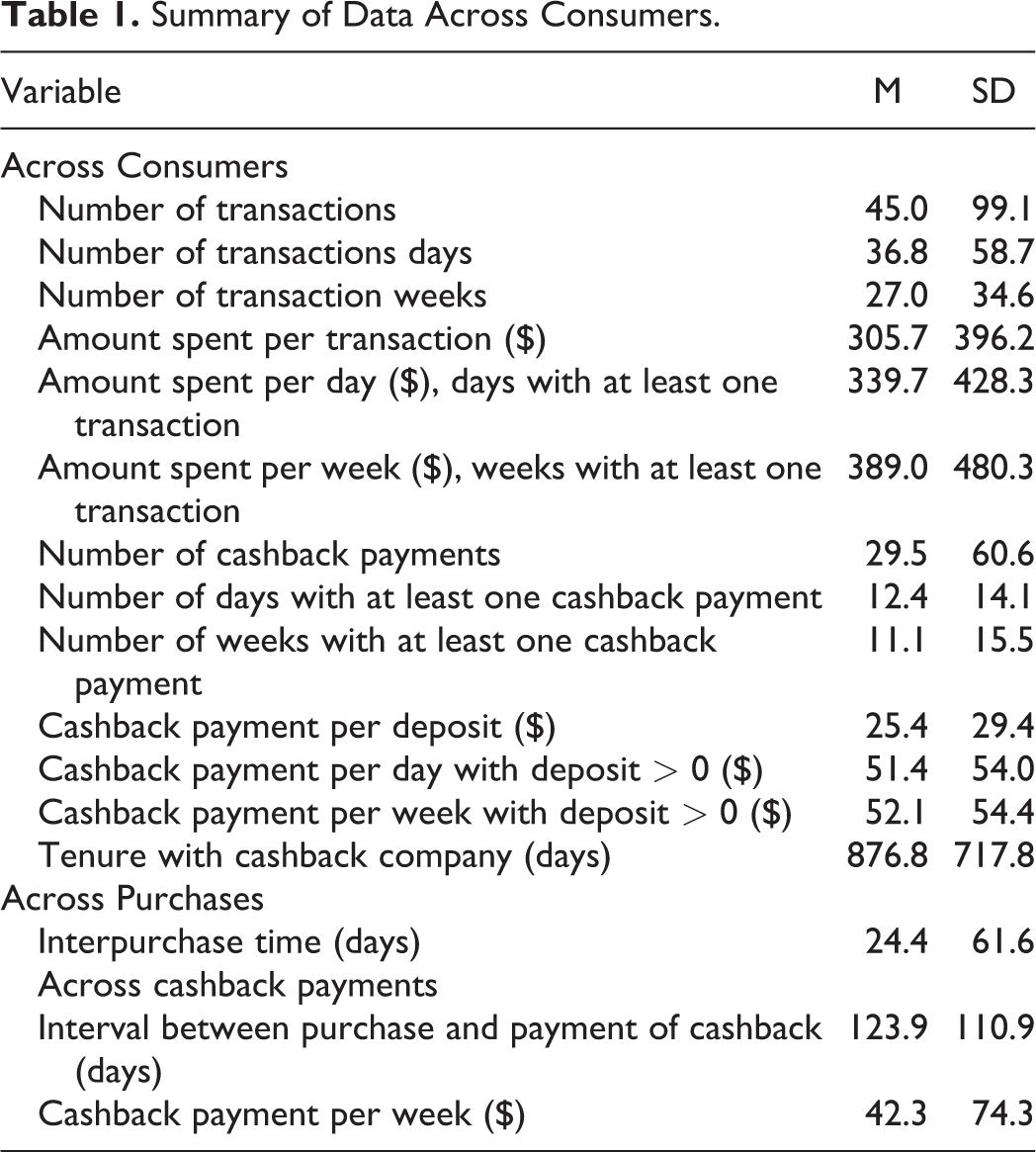

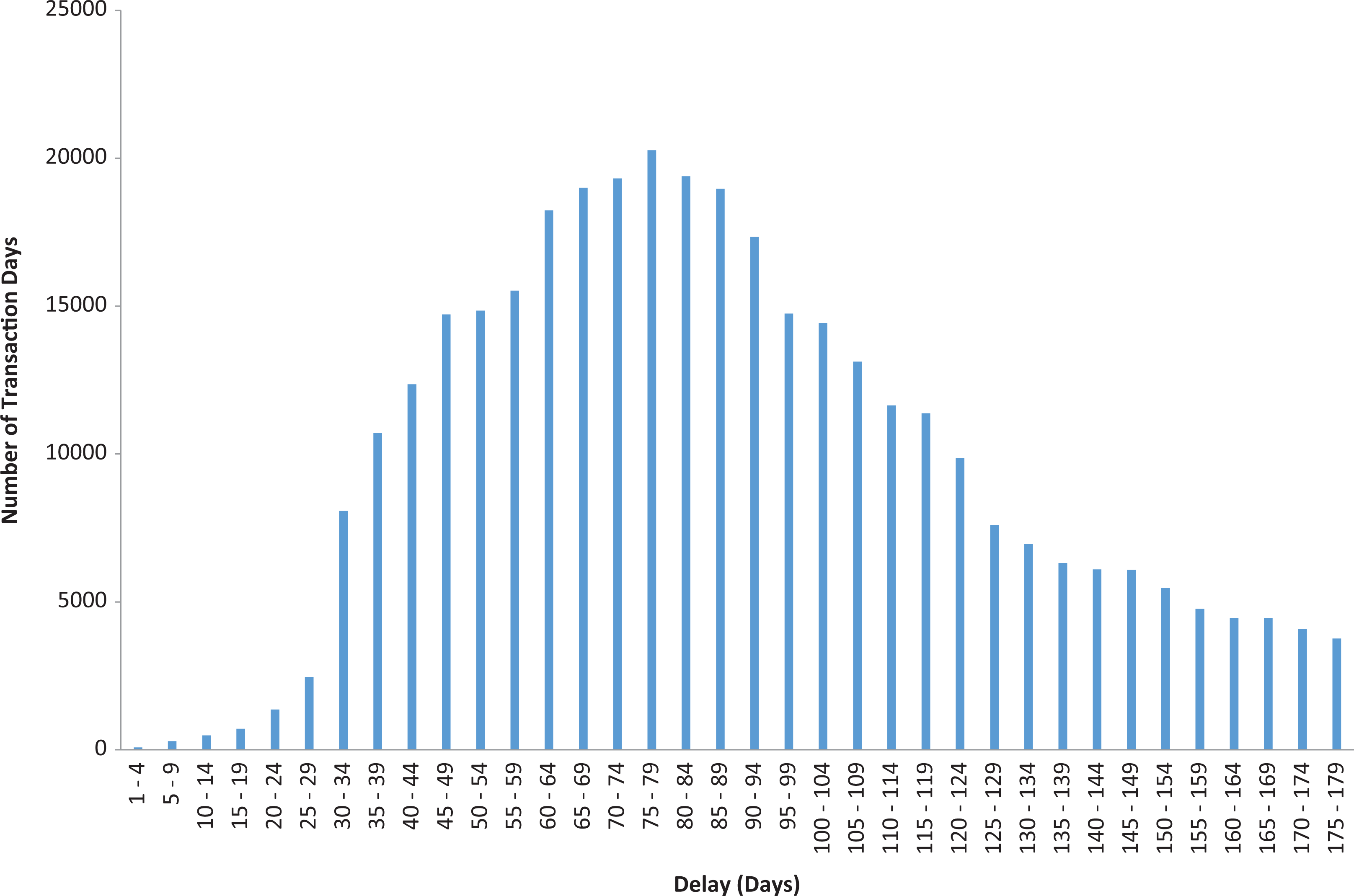

Table 1 provides summary statistics. The average tenure of a consumer, measured as the time between the first and last purchase, is 876.8 days. On average, a consumer made 45 purchases on 36.9 days, each worth $305.66, and received a cashback payment on 12.4 days, each worth $51.44. 3 The mean time between successive purchase days is 24.4 days. The mean time between purchase and cashback payment is 123.9 days, with a standard deviation of 110.9 days (Figure 1).

Summary of Data Across Consumers.

Delay between purchase and cashback payment.

One reason for the size and variability of the delay between purchases and cashback payments is that retailers process commissions to the cashback company only after the return periods for the items in question expire. Return periods vary across retailers depending on regulations, policies, and routines. In turn, the cashback company seldom executes a cashback payment before receiving the corresponding commission, and its own processes are subject to delays. Another reason is that the cashback company enters into different agreements with different retailers, often as a function of the product category.

Identification Strategy

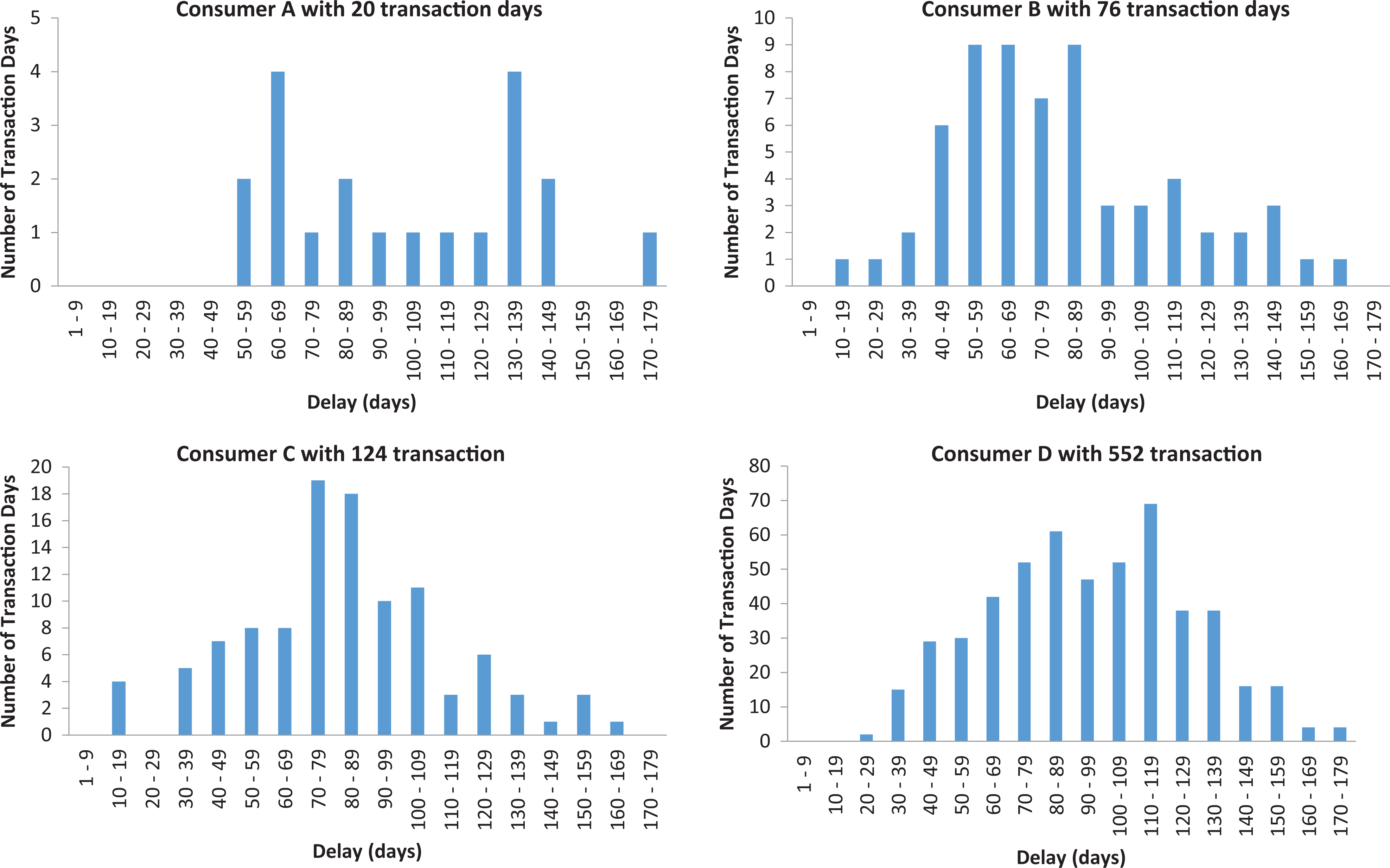

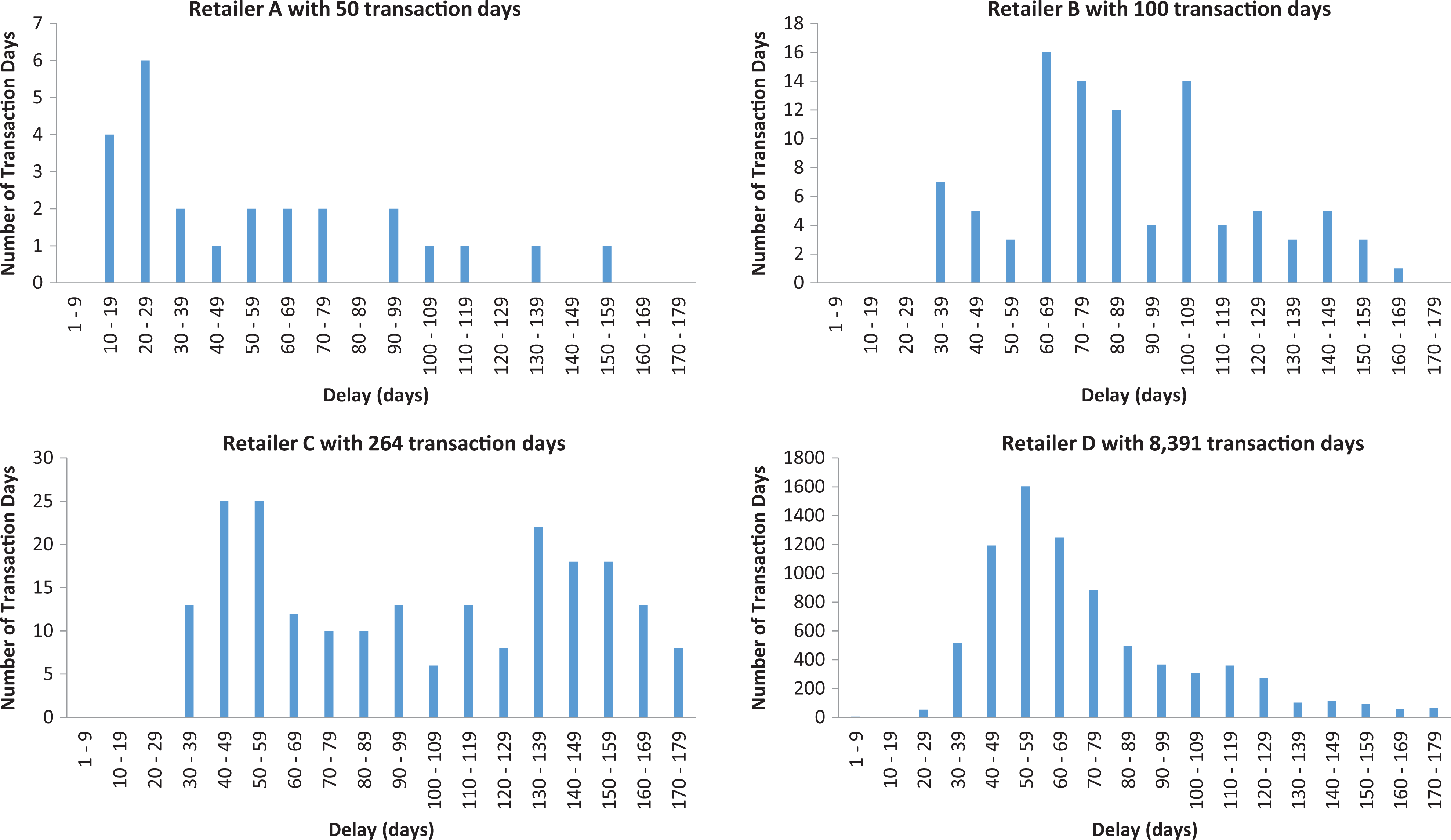

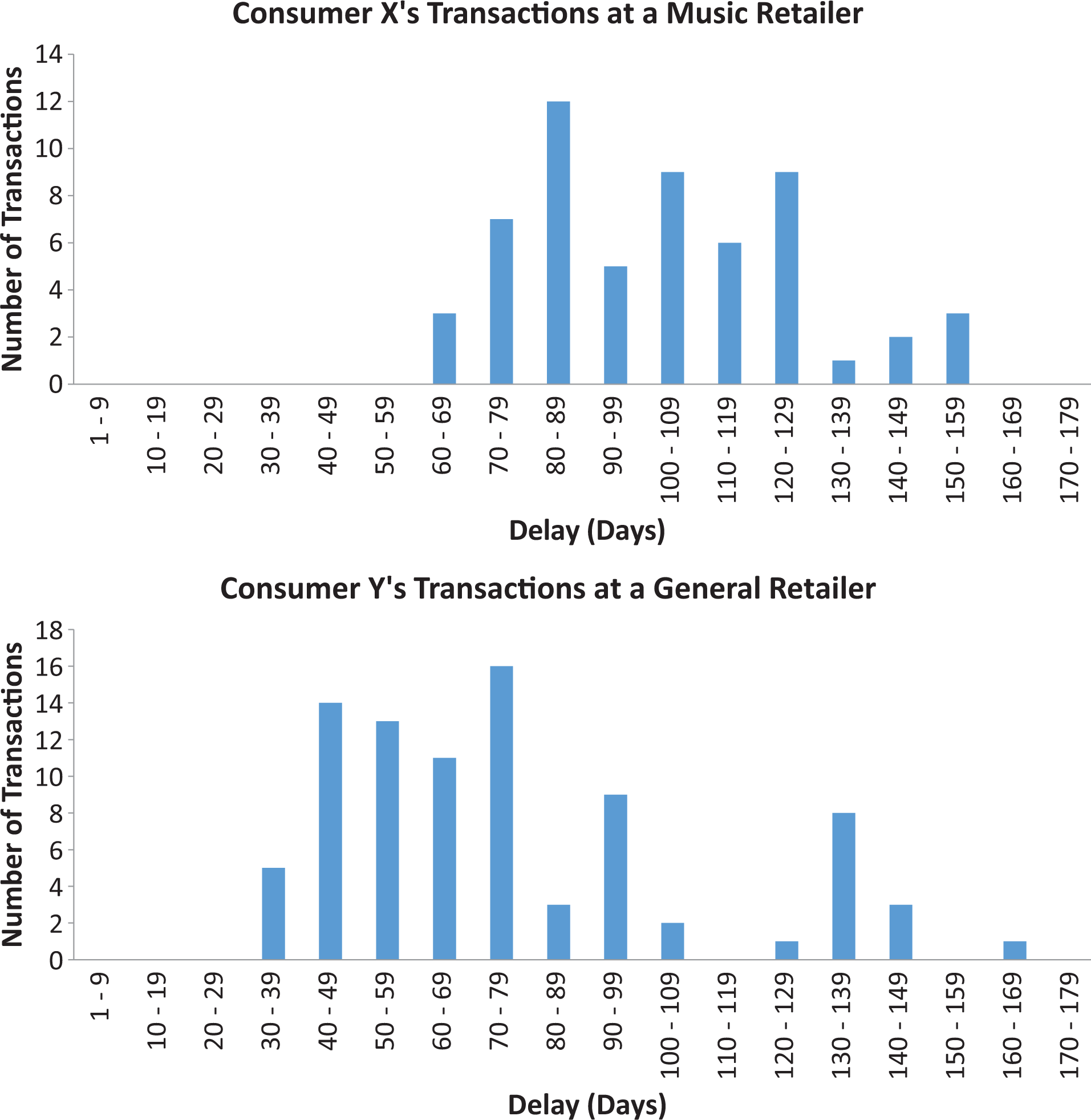

Our ability to identify the causal effects of cashback payments on purchase behavior rests on the assumption that their timing and size are exogenous from the standpoint of consumers. That is, consumers should not be able to predict or influence cashback payments because, otherwise, they could adjust their spending plans. We offer four justifications for this claim. First, the cashback company schedules cashback payments according to the aforementioned internal process, not some strategic consideration. Second, consumers are notified of a deposit only after its execution. Third, there is considerable irregularity in both the time retailers take to pay commissions and the time the cashback company takes to execute cashback payments; the coefficient of variation of delay in the data is .89. There is also significant variation in the interval between purchases and cashback payments at the level of a single consumer (Figure 2), countering the possibility that the pattern in Figure 1 is due to differences between individual consumers. Similarly, the interval varies at the level of a retailer, as Figure 3 demonstrates for four retailers selected at random. Figure 4 shows such variation for the purchases at a single generalist retailer for four consumers selected at random but unmatched on any other variables, and Figure 5 shows this variation among four consumers matched by gender, age, and spending. 4 Fourth, Figure 6 displays the delay for a generalist (offering a broad range of products) and a specialist (offering a narrow range) retailer, suggesting that the delay is not specific to the range of products offered.

Delay for four randomly selected consumers.

Delay at four randomly selected retailers.

Delay for four randomly selected unmatched consumers at a specific retailer.

Delay for four randomly selected matched consumers at a specific retailer.

Delay at a music retailer and at a general retailer.

One concern is that the delay between purchases and cashback payments varies with the size of the former. This would be the case if, for example, more expensive products enjoy longer return periods, and consumers know this. However, our conversations with executives at the cashback company suggest that no such relationship exists, and the data indicate a low correlation between the size of a purchase or cashback payment and the delay in the data (R2 = .015, p < .001; R2 = –.016, p < .001, respectively). Another concern is that the nature of certain purchases improves the ability of consumers to predict cashback payments. An example is travel, for which consumers may infer that a service provider safeguards against cancelations by processing cashback payments only after completion of the event (e.g., a flight, a hotel stay). This scenario affects a small subset of transactions, and even then, consumers cannot pinpoint the date of payments. Regardless, one of our robustness checks excludes observations with long delays. Section 1 of the Web Appendix reports further evidence that consumers are unlikely to predict the timing of cashback payments.

Analysis and Results

Model-Free Evidence

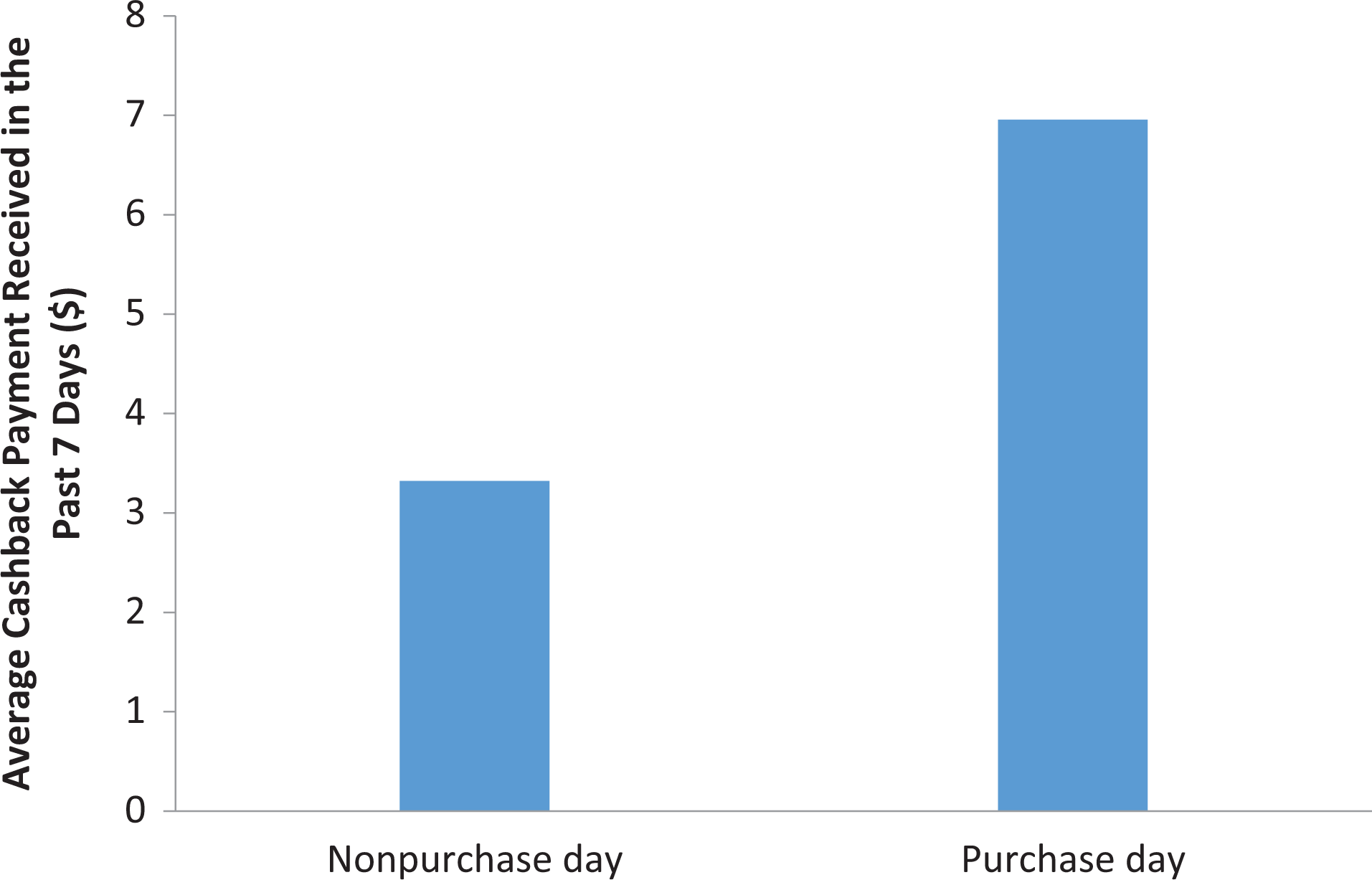

We explore the relationships between cashback payments and purchase likelihood and between cashback payments and spending. Regarding purchase likelihood, we classify every consumer–day observation as a “purchase” or “nonpurchase” event depending on whether the consumer transacted at least once through the cashback company on that day. We then compute the average cashback payment received in the seven days prior. The pattern in Figure 7 suggests that cashback payments affect purchase likelihood: On average, consumers receive $2.50 more in the seven days before a purchase event than before a nonpurchase event (p < .001).

Model-free evidence for purchase likelihood.

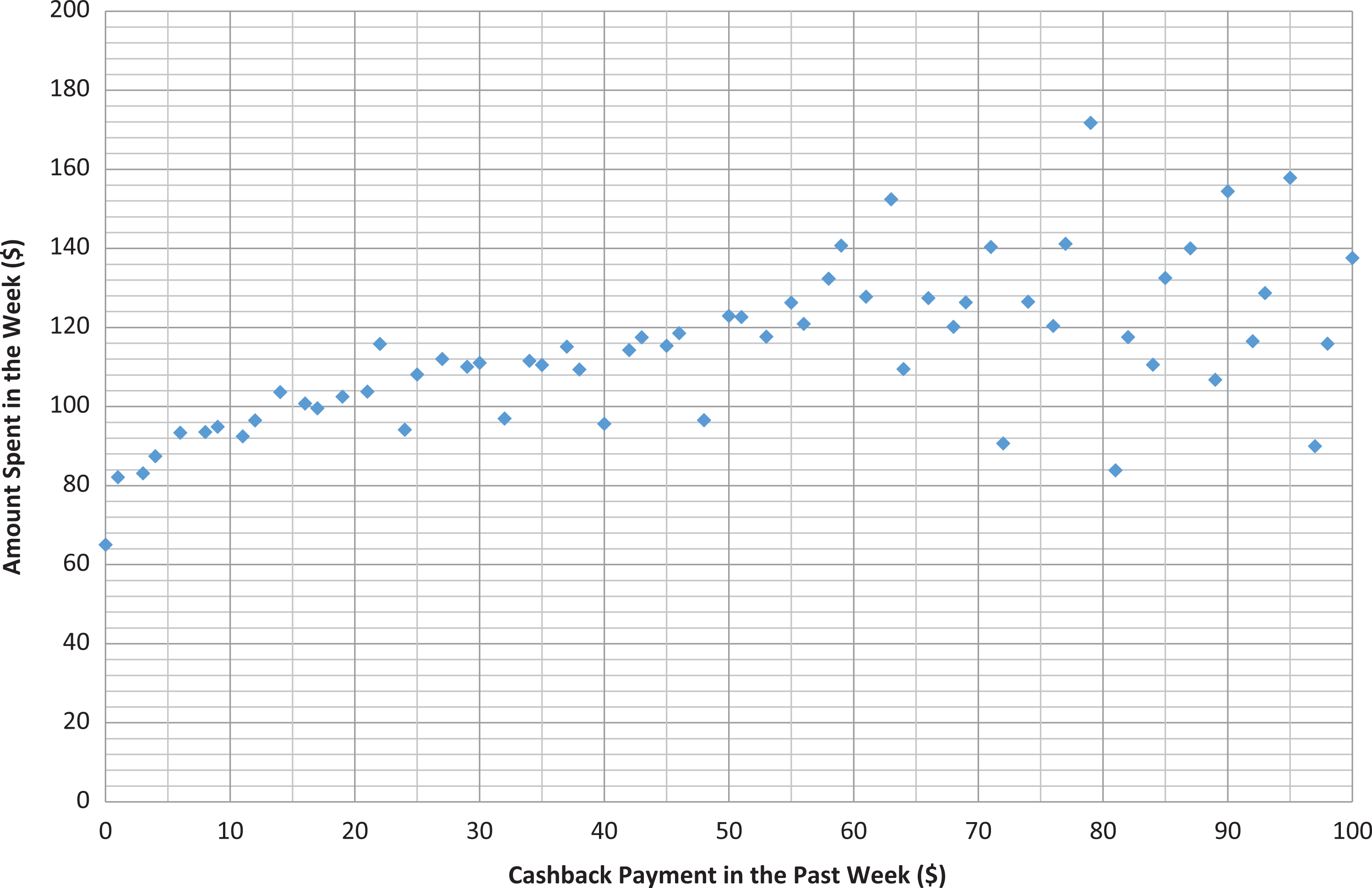

With regard to spending, we associate the cashback payment paid to a consumer over a seven-day interval (from a given Saturday to the next Friday) to the money spent by the same consumer in the following seven days. We use this interval because the cashback company processes 51.5% of deposits on a Thursday or Friday (the results hold for alternative specifications). For each amount of cashback payment, we calculate the average weekly spend across all consumer–week observations. We then correlate the level of cashback payments and the average weekly spend. Figure 8 illustrates a positive relationship: As cashback payment increases, so does spending—the correlation is .332 (p < .001).

Model-free evidence for spending.

These initial analyses clearly do not control for consumer heterogeneity, which matters because consumers who purchase frequently are more likely to receive cashback payments than consumers who purchase infrequently. Similarly, consumers who make large purchases—and are likely to do so in the future—receive larger cashback payments than consumers who do not. We turn to this concern next.

Cashback Payments and Purchase Likelihood

Model setup

We use a semiparametric proportional hazard model to estimate whether, on any given day, the cashback payment a consumer receives in the seven days prior increases the probability of a purchase through the cashback company on that day. 5 We model a consumer’s purchase decision from the first transaction observed in the data to the last.

In a proportional hazard model, the dependent variable T represents the time (in days) between two consecutive purchase days. We model the hazard of a purchase by consumer i on any given day t, hi(t|Xit), as

Here, h0i(t) is the baseline hazard function specific to consumer i. To account for individual differences, we take a stratified baseline approach and let the baseline hazard function vary nonparametrically across consumers (Prentice and Gloeckler 1978). The baseline hazard is shifted proportionally by exp(Xitβ), where Xit is a vector of time-varying covariates. We specify the vector of covariates as

The independent variable of interest is

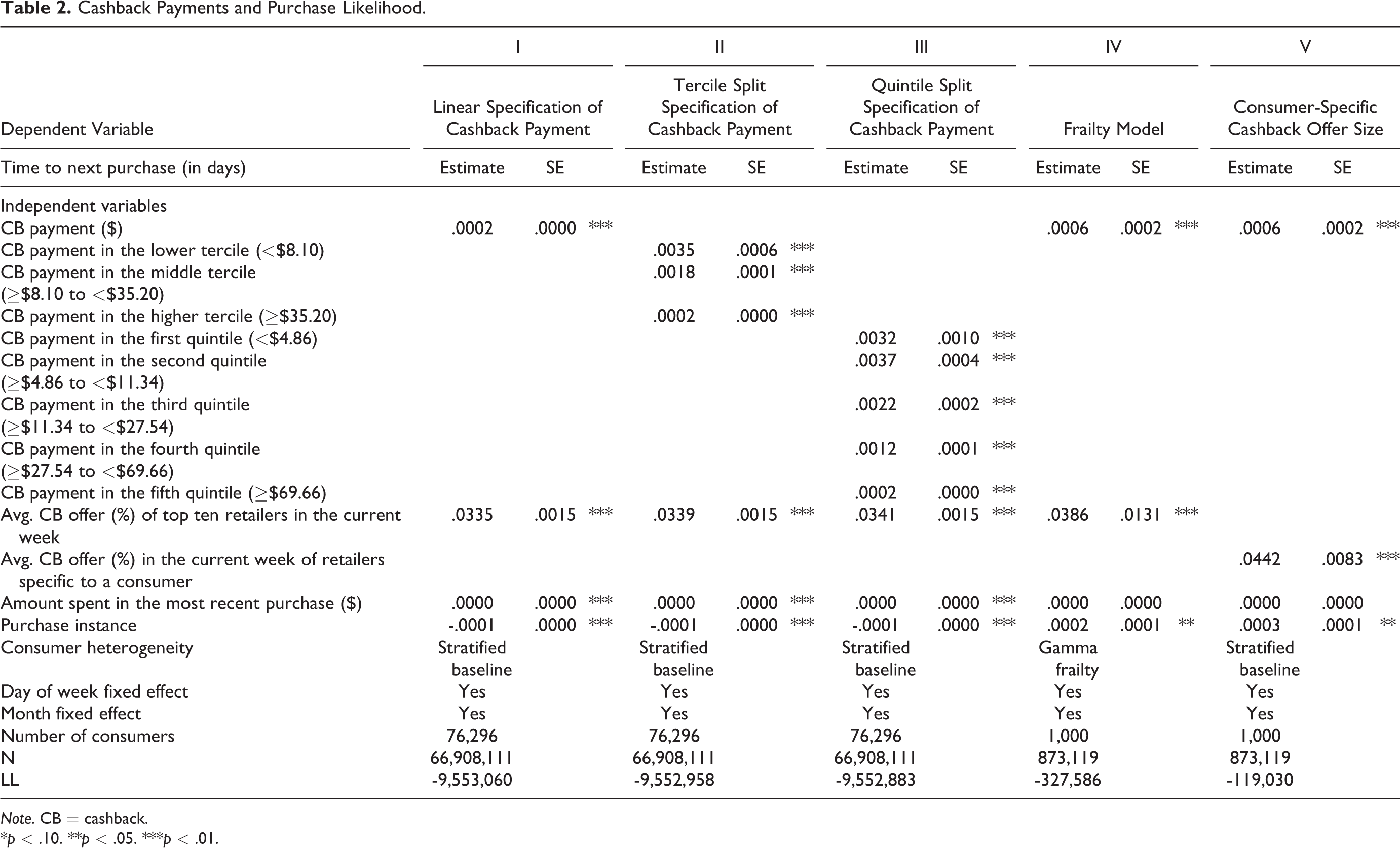

Results

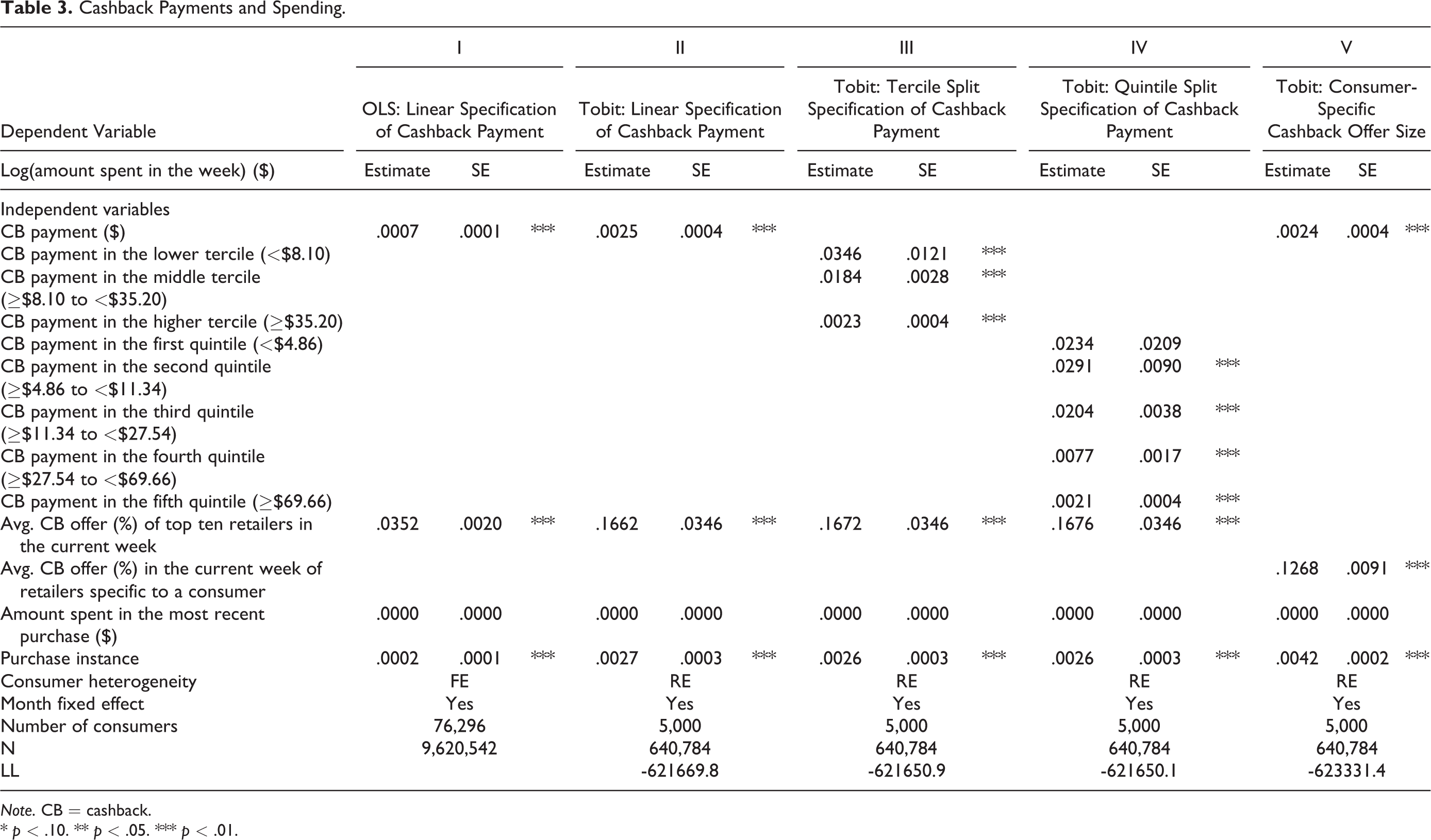

Column I of Table 2 shows that larger cashback payments increase purchase likelihood. The associated hazard rate of 1.0002 implies that on any given day, an additional $1.00 in cashback in the seven days prior raises the probability of purchase by .02%. Columns II and III measure the effect separately by terciles (<$8.10, ≥$8.10 and <$35.20, ≥$35.20) and quintiles (<$4.86, ≥$4.86 and <$11.34, ≥$11.34 and <$27.54, ≥$27.54 and <$69.66, ≥69.66), demonstrating that this $1.00 increment has a stronger impact on purchase likelihood when the cashback payment is small—in other words, the marginal effect of cashback payments decreases as their size increases. 6

Cashback Payments and Purchase Likelihood.

Note. CB = cashback.

*p < .10. **p < .05. ***p < .01.

Column IV shows that the result holds when we specify a frailty model with a gamma-distributed random effect to account for consumer heterogeneity rather than taking the stratified baseline approach (McGilchrist and Aisbett 1991). While in the initial specification the baseline hazard varied nonparametrically across consumers, the frailty model assumes a multiplicative effect of the heterogeneity parameter on the baseline hazard function. Finally, Column V shows that the results are robust to using a post hoc consumer-specific cashback offer variable reflecting only offers by retailers at which a consumer shopped in the past.

For the remaining covariates, we find that purchase likelihood decreases with the number of past purchases, which is consistent with studies on consumer attrition over time (Fader, Hardie, and Shang 2010). Similarly, consumers who recently spent large amounts are more likely to purchase. In line with broader evidence, the size of cashback offers has a positive effect on purchase likelihood.

Cashback Payments and Spending

Model setup

We use a Type I Tobit specification to estimate the effect of cashback payments in a given week (from a Saturday to the next Friday) on spending at any time in the following seven days. The analysis is at the weekly rather than daily level because the latter yields a large number of null (zero-spend) observations per consumer. For consumer i in week w, Spendiw is the observed weekly expenditure,

and

The vector of covariates is

The independent variable of interest is CBPaymenti, w-1 (the amount of cashback consumer i received in the week before week w). We control for the size of cashback offers advertised in week w by taking the average percentage of cashback offered by the ten largest retailers, AvgCBOfferw. The variable LastPurchaseSpendiw captures the amount consumer i spent in the most recent week with a purchase. The variable PurchaseInstanceiw is the number of transactions consumer i made up to but not including week w, and Monthw controls for month fixed effects.

Consumer-specific random effects, αi, are distributed αi∼N[0, σ2 v ] and account for heterogeneity in the average weekly spending level. The likelihood function for the Tobit model must be integrated over the distribution of αi, which is computationally intensive because integrating over the normal distribution does not yield closed-form expressions and the likelihood is estimated numerically. As such, for all Tobit analyses we randomly select 5,000 consumers. To demonstrate that the findings generalize to the full sample, we also estimate an ordinary least squares (OLS) specification using the full sample. Finally, ∊iw is an i.i.d. normal error term.

Results

Column I in Table 3 reports the OLS specification using the full sample, where the dependent variable is the weekly amount spent. The effect of cashback payments is significant and positive. Column II displays the results of the Tobit specification. Again, the money consumers spent in any given week increases with cashback payments received in the seven days prior. 7 For the other covariates, we find the expected positive effect of cashback offers on spending. Similarly, we find that purchase instance has a positive effect on amount spent, consistent with the pattern Fader, Hardie, and Lee (2005) observe.

Cashback Payments and Spending.

Note. CB = cashback.

* p < .10. ** p < .05. *** p < .01.

Next, we examine whether the effect of cashback payments on spending is sensitive to the size of cashback payments. Columns III and IV in Table 3 show that this is the case when we take cashback payments by tercile or quintile: An increase in cashback payment by $1.00 has a greater effect on spending when that payment is small rather than large. Column V shows that the results hold when we use a consumer-specific cashback offer variable.

We also evaluate the size of the effect of cashback payments on spending using estimates from Column III in Table 3. We consider the marginal effect of increasing the cashback payment by $1.00 on the weekly spend as

Figure 9 plots this effect at the median level of cashback payments in each tercile ($3.24, $17.82, and $81.00). The x-axis shows the amount spent (Spendiw). For each amount, the y-axis indicates the change in spending that would result from an additional $1.00 of cashback payment. At the mean level of amount spent of $69.34 and the median cashback payment of $17.82, the marginal effect of such an increase is $.32. Again, this result is in addition to the impact of cashback offers on initial demand, and the magnitude of the marginal effect declines with the tercile level of payment: At the same weekly spend of $69.34, increasing a cashback payment of $3.24 by $1.00 contributes $.58 in further spending. Section 2 of the Web Appendix provides more details on the effect of cashback payments on spending.

Marginal effect of cashback payment on observed spend, by tercile of cashback payment.

Finally, we compare the effect of cashback payments on spending with the effect of cashback offers on initial demand. Note that the marginal effects from the Tobit model refer to increases in cashback offers by one percentage point and in cashback payments by $1.00. We conclude that at the average values in the data, the effect of cashback payments accounts for approximately 10.03% of the overall effect of the promotion (see Web Appendix, Section 3).

Robustness Checks

We complete several checks to ensure the robustness of our findings. 8 First, note that the independent variable to this point is the amount of cashback payment a consumer received in the prior week. We test whether the results in Column II of Table 3 replicate for an interval of 14 or 28 days. Columns I and II in Table 4 show that this is the case. Second, recall that our argument of causality hinges on the assumption that cashback payments are exogenous to consumers. The initial analysis supports this idea, but we also noted a subset of purchases (e.g., travel expenses) for which consumers may have a better sense of the timing of cashback payments. To check this possibility, we estimate the model excluding consumer–week observations with delays exceeding the mean plus one standard deviation. Column III in Table 4 replicates the main findings. Third, we want to know whether the effects of cashback payments are due to the sum paid rather than the mere act of receiving money. For example, the emails the cashback company sends to notify consumers of a deposit may drive traffic to the website of the cashback company, which in turn may affect spending. Column IV shows that the results hold when we use only the consumer–week observations in which cashback payments are greater than zero.

Robustness Checks and Extension: Delay.

Note. CB = cashback.

* p < .10. ** p < .05. *** p < .01.

Extensions

We consider three extensions. First, we question whether the delay between purchases and cashback payments moderates the effect of the latter on spending. Column V of Table 4 reports separate coefficients for cashback payments depending on whether the corresponding delay is in the lower, middle, or upper tercile. Cashback payments have a stronger effect on spending when delays are short and a weaker effect when delays are long. That is, although some lag is necessary to induce future spending through the cashback company, it appears that a greater lag is associated with a lower effect, perhaps because excessive delays cause frustration. In Section 5 of the Web Appendix, we test whether consumers respond to perceived rather than absolute delays and find similar results.

Second, we check for patterns that suggest that consumers learn to predict the delay between purchases and the corresponding cashback payments. The results, again reported in Section 5 of the Web Appendix, indicate that such learning is unlikely.

Third, we question whether our results replicate for different categories of retailers. These categories are defined by the cashback company. Table 5 covers the four largest categories in the data. The outcome variable is spending in a particular retailer category. We estimate the effect of cashback payments separately when these originate from retailers in the same or different categories. Column I shows that cashback payments from generalist retailers (mostly department stores) affect spending with generalists more than they do with other (more specialized) retailers. The results in Column II, which pertain to travel, are similar but significant only at the 90% confidence level. This may be because, in this category, consumers purchase infrequently or because travel products tend to be expensive and time consuming. Columns III and IV pertain to subscription services—mostly utilities and insurance in the first case and mostly magazines in the second. Here, a purchase typically implies a contractual obligation for at least one year. The negative relationship between cashback payments and spending may be because consumers who recently subscribed to a service are unlikely to do so again in the near future. Finally, although the number of transactions by individual consumers with individual retailers is low, we estimate a model for the largest generalist (by number of transactions). Column V shows that the effect of cashback payments on spending is significantly higher for the same retailer than other retailers, suggesting that the results in Column I hold even at the level of a single retailer.

Extension: Retailer Category Analysis.

Note. CB = cashback.

* p < .10. ** p < .05. *** p < .01.

Behavioral Explanations: Initial Evidence

Money Is Not Fungible

First, a basic premise in research on mental accounting is that people decompose wealth into categories, including “current assets,” for which the temptation to spend is low, and “current income,” for which the temptation to spend is high (Shefrin and Thaler 1988). In addition, people code small windfalls as current income and tend to match the source of this income with its use. For example, Kooreman (2000) finds that government payments labeled as child benefits increased spending on children’s clothing, and Milkman and Beshears (2009) show that patrons of a grocery store spent more at that store when redeeming an unexpected coupon than when they did not. Closer to our interest, Reinholtz, Bartels, and Parker (2015) show that consumers perceive funds that are specific to a retailer as an account governed by the goal to purchase from that same retailer.

These arguments are relevant to our context under the assumption that consumers (1) segregate cashback payments from purchases and (2) perceive the former as windfalls, a possibility Soman (1998) also raises in the context of mail-in rebates but does not test empirically. If true, the implication is that consumers spend cashback payments through the cashback company. Moreover, Shefrin and Thaler (1988) stress that people spend windfalls to the extent that these appear as small, meaningless changes in their wealth. As windfalls grow, consumers are more likely to treat them as assets and, as such, are more likely to save them.

Consistent with this logic, both Columns II and III of Table 2 and Columns III and IV of Table 3 report an inverse relationship between the marginal effect of cashback payments on purchase likelihood and spending. However, the data do not indicate whether consumers spend the money received elsewhere or save it. To address this limitation, we surveyed 441 workers on the Amazon Mechanical Turk platform. Respondents first read general information about cashback shopping and then were asked to split seven cashback payments ($3, $7, $18, $54, $113, $162, and $287) shown in random order into saving and spending. 9 We examined whether the money allocated to saving varied with the size of the cashback payment. The OLS specification in Column I of Table 6 shows that the percentage of cashback payment saved increases with the size of the cashback payment after we control for income, age, gender, and respondent fixed effects. Given the nature of the dependent variable, Column II reports a fractional logit specification as a robustness check (Papke and Wooldridge 1996). Section 6 of the Web Appendix provides more details on the stimulus, and Section 7 adds to the analysis. Overall, the results of this survey lend support to the idea that the effects of cashback payments are due to mental accounting.

Cashback Payments: Spending Versus Saving.

* p < .10. ** p < .05. *** p < .01.

Cashback Payments Are a Scheduling Device

A second explanation is that consumers use cashback payments to schedule future purchases. One motivation for this could be financial: Consumers with liquidity problems postpone spending until they receive cashback payments and have more money on hand. However, the evidence presented so far suggests that consumers cannot predict with reasonable accuracy the timing of cashback payments. Nevertheless, assume that consumers engage in scheduling and receive a salary at the end of each calendar month. If so, the effect of cashback payments on spending should be more (less) pronounced at the end (beginning) of a given month. Column I of Table 7 displays the results for cashback payments executed during the first week of a given month or at any other time. We find no significant differences across the two estimations. Similarly, in Column II we find no significant differences between the last week and any other time in a month.

Evidence for Behavioral Mechanism.

Note. CB = cashback.

* p < .10. ** p < .05. *** p < .01.

Another motivation could be self-control. Suppose that people tend toward immediate gratification but know that deferring a purchase can improve the quality of the decision or make the purchase more pleasurable (Caplin and Leahy 2001; Hoch and Loewenstein 1991). One way to exercise patience is to tie future purchases to cashback payments, but again the data show no such evidence. While the average interval between successive purchases is 24.4 days, it is 56.1 days in the case of successive cashback payments. The average delay between purchases and cashback payments is 123.9 days. Therefore, consumers make 5.08 purchases between a given purchase and the associated cashback payment and make 2.21 purchases between successive cashback payments.

Moreover, note that the incidence of cashback payments varies across consumers. Consumers who purchase more frequently experience a shorter delay between successive cashback payments, which makes self-control less relevant. As such, the effect of cashback payments on spending should be weaker for this group. Column III of Table 7 compares consumers across three groups who differ in purchase frequency: <19.08 days between purchases, ≥42.68 days, or anytime in between. Column IV does the same using quintiles. Contrary to the idea of self-control, the effect of cashback payments is stronger for consumers who purchase more frequently. The results are not significant for the first group (i.e., those who purchase infrequently), probably because the estimation contains many cashback payments and spending levels with a value of zero.

Cashback Payments Prompt a Transient State

A third explanation is that cashback payments trigger a transient state. For example, it is possible that cashback payments elevate consumers’ mood or that they perceive these payments as acts of kindness and reciprocate by spending through the cashback company (Heilman, Nakamoto, and Rao 2002; Rabin 1993). It is also possible that the emails notifying consumers of cashback payments make shopping through the cashback company more salient (Obermiller 1985). Regardless, our hypothesis is that cashback payments prompt a temporary effect that, in turn, increases the propensity to purchase and spend.

While the data do not allow us to conclusively confirm or rule out these explanations, the last two predict a positive or, at best, a null relationship between the size of a cashback payment and its marginal effect on spending. The inverse relationship in Columns II and III of Table 2 and in Columns III and IV of Table 3 suggests that other mechanisms, such as mental accounting, are at play.

Conclusion and Implications

In this study, we examined how cashback payments affect consumer purchase behavior. We found two main results. First, cashback payments shorten the time consumers take to make additional purchases via the website of the cashback company. Second, cashback payments increase the size of these purchases. Specifically, at the average values in the data, increasing cashback payment by $1.00 increases the probability of a new transaction by .02% and spending by $.32. These figures represent 10.03% of the overall impact of a given promotion.

The finding that consumers are susceptible not only to the promise of a saving but also to the later payment of that saving is surprising, as they are free to spend the money in any manner they choose or to set it aside. It is also surprising when we consider that cashback payments are trivial within the context of lifetime income—these payments should not influence purchase behavior in any product category, with any retailer, or through any intermediary in a meaningful way. Regardless, one possible explanation is that consumers ultimately fail to treat money as a fungible resource. The data lend support to this argument, as we observe an inverse relationship between the size of cashback payments and their marginal effect on spending. Two other possible explanations are that cashback payments act as a scheduling mechanism or prompt some transient state, but we find little support for either in the data.

With this in mind, our research is relevant given Hastings and Shapiro’s (2013) call for more evidence of mental accounting in the real world. Our work is perhaps closest to that of Milkman and Beshears (2009), though in reality the comparison ends at the fact that we both construe discounts as windfalls. First, we examine the effect of discounts that are delayed and conditional on a past purchase, not standard “dollars-off” coupons. Second, cashback payments have no usage or time restrictions; this is important because consumers spend (again) through the cashback company money that, at least in principle, is fully fungible. Third, consumers respond to multiple offers of varying amounts, not a single offer of a fixed amount, which enables us to test whether the size of the windfall matters to the extent predicted by mental accounting. Finally, the data span many product categories and retailers, a large number of consumers, and eight years of purchases and cashback payments.

Because the interval between purchases and cashback payments rarely falls below 30 days in the data (and in cashback shopping in general), we cannot make recommendations regarding optimal delays. Further research could address this constraint by implementing experiments that vary the delay, either in the field or in the laboratory. Moreover, while the data provide insights into possible behavioral mechanisms, we do not have direct process evidence. Again, future studies could take up this challenge by testing specific mediating variables and their logical moderators.

Our finding that cashback shopping stimulates demand at different points in time has practical implications for both cashback companies and retailers. First, the fact that cashback shopping stimulates demand at two different points matters to cashback companies, which seem largely unaware of the effects of cashback payments. The analysis suggests that cashback companies can increase revenue by designing promotions not only to attract an initial purchase but also to stimulate future purchases. In addition, we find that consumers are more likely to spend the money received at generalist retailers, such as department stores, and less likely to do so in categories such as travel and subscription-based services, which implies that the selection of participating retailers is important. Finally, if as our results suggest, mental accounting influences consumers’ purchase decisions in the context of cashback shopping, cashback companies need to emphasize the link between cashback payments and their company. For example, the emails notifying consumers of recent cashback payments should emphasize that the cashback company is responsible for the deposit and also indicate which retailer funded the payment, with the intent of increasing the probability of a future purchase at that retailer.

Second, the effect of cashback payments on demand matters to retailers. Understanding the dual effects of cashback offers and payments is useful to assess the full benefits and costs of collaborating with a cashback company—focusing only on the ability of cashback offers to generate demand underestimates these offers’ full potential. Such an understanding can also help retailers make smarter decisions about the timing of cashback payments; it may be beneficial to execute commissions quickly and, in turn, insist that the cashback company does the same with cashback payments. Finally, although it is not straightforward to compare the effectiveness of different forms of price promotions across studies (as these may focus on different customer segments, product categories, geographies, and so on), we find that the effectiveness of cashback shopping is broadly similar to that of other established online and offline methods of price promotion (Web Appendix, Section 8). This suggests that an individual retailer planning to use price promotions can benefit from considering—and potentially testing—a wide range of options, including cashback shopping, daily deals, and email coupons.

Supplemental Material

Supplemental Material, jmr.15.0125-web-appendix - Cashback Is Cash Forward: Delaying a Discount to Entice Future Spending

Supplemental Material, jmr.15.0125-web-appendix for Cashback Is Cash Forward: Delaying a Discount to Entice Future Spending by Prasad Vana, Anja Lambrecht, and Marco Bertini in Journal of Marketing Research

Footnotes

Acknowledgments

The authors thank Bruce Hardie and Puneet Manchanda for their suggestions.

Declaration of Conflicting Interests

The authors declare no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Associate Editor

P.K. Kannan served as associate editor for this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.