Abstract

Mobile applications in the personal development sector increasingly integrate goal-enabling technology features (GETFs), which allow users to define a service-related end goal, set implementation strategies through subgoals, and monitor progress. Little is known, however, about how the difficulty of goals chosen during GETF adoption affects subsequent app behaviors. This study examines whether customers who set more versus less difficult end goals and subgoals show greater engagement and retention, and whether firms can nudge customers toward goal-difficulty levels conducive to sustained engagement. Using behavioral data from an investment app that introduced GETFs, the authors employ hierarchical modeling with staggered synthetic control and instrumental variable regression to address self-selection and endogeneity. Results reveal substantial heterogeneity: Many adopters show no or negative engagement changes, whereas those selecting moderately challenging goals and subgoals significantly increase in-app investment actions, though not sign-ins. Higher engagement postadoption predicts improved retention after one year. A field experiment confirms that subgoal difficulty causally drives in-app actions. These findings suggest that personalized guidance during GETF adoption can enhance sustained engagement. Marketing managers are advised to tailor goal-setting features to individual needs, providing expert-like support. This research provides novel empirical evidence on goal-difficulty levels that most effectively promote app engagement.

Consumers increasingly seek to improve their physical, mental, social, professional, and financial well-being, fueling the explosive growth of self-help books, podcasts, motivational speakers, and coaching services (Berger 2022). To achieve these personal development outcomes, consumers are turning to technological tools, particularly mobile applications (apps), as evidenced by compound annual growth rates of 5% for money-budgeting apps, 15% for education apps, and 18% for fitness apps (Business Research Insights 2023). However, translating intentions into sustained action remains a persistent challenge. Previous research (Norcross and Vangarelli 1988; Uetake and Yang 2020) and industry statistics (Valuates Reports 2022) document the difficulty of following through on resolutions. User engagement, defined as the “continued and repeated usage of an app” (Paschmann et al. 2024, p. 249), is particularly short-lived across personal development categories. After 30 days, retention rates plummet to just 4.6% for finance apps, 2.1% for education apps, and 3.7% for fitness apps (Grand View Research 2023; Statista 2022). Consequently, app-based service providers in the personal development sector face the ongoing challenge of keeping their customers motivated and engaged (Wolf et al. 2021).

One strategy to better motivate and engage customers in their pursuit of personal development is to integrate goal-enabling technology features (GETFs) into mobile apps. GETFs are technological features within mobile apps that enable customers to (1) explicitly specify an end goal they want to achieve by using the app, (2) set implementation strategies through subgoals, and (3) monitor their progress toward the end goal. Prominent examples of such apps include Duolingo, a language-learning app whose GETF allows customers to select specific proficiency levels as end goals (e.g., achieving business-level communication skills), establish daily subgoals (daily “XP goals”), and track their advancement. Similarly, the fitness app Strava incorporates GETFs into its premium version, enabling customers to set and monitor fitness objectives alongside exercise tracking. The goal of this research is to understand how end-goal and subgoal choices made during the GETF adoption process drive app engagement and retention.

Personal finance apps—our research setting—frequently offer GETFs that allow customers to set financial end goals (e.g., saving for a car or house deposit) and corresponding subgoals (e.g., weekly or monthly savings targets) while monitoring progress. Consider in this context a customer who earns $52,000 annually (or $1,000 per week) and who intends to use the GETF. This customer faces two key decisions during GETF adoption: First, the customer must choose an end goal, such as a low-difficulty target of saving $5,200 (10% of their annual income) or a high-difficulty target of $15,600 (30% of their annual income). Second, the customer must choose an implementation strategy by specifying a subgoal amount. Again, the customer can choose a low subgoal difficulty of saving $50 per week (5% of weekly income) or a high subgoal difficulty of $250 per week (25% of weekly income). High end-goal difficulty might increase motivation and engagement by providing a stronger sense of challenge, yet overly ambitious end goals may decrease motivation and engagement if perceived as too demanding. Similarly, high-difficulty subgoals may lead to faster goal progress and thus increase motivation, yet overly ambitious subgoals increase the risk of failing them, in turn increasing the likelihood that the end goal and the service are abandoned altogether. Understanding the impact of end-goal and subgoal difficulty on app engagement and retention, and whether customers can be guided to set moderately challenging levels, is thus crucial for the successful implementation of GETFs.

Companies have shown significant interest in GETFs due to their potential benefits. GETFs empower customers to co-create and customize their app experiences by defining service-related goals, potentially fostering greater satisfaction and loyalty (Ball, Coelho, and Vilares 2006; Cossío-Silva et al. 2016). Extensive research demonstrates strong connections between goal setting, motivation, and performance across diverse contexts, including reading, sports, and negotiation (Van der Sande et al. 2023; Williamson et al. 2022; Zetik and Stuhlmacher 2002). Additionally, achieving service-related goals correlates with higher self-reported commitment and loyalty to service providers (Wolf et al. 2021). Given that customer retention strategies are often ineffective (Ascarza 2018), GETFs present a promising opportunity to enhance app engagement. Indeed, recent findings by Gargano and Rossi (2024) show that adopting a GETF increases saving behavior—reflecting one form of engagement—in a financial services app.

However, research on how the choice of goal difficulty during GETF adoption impacts subsequent app engagement and retention remains limited. Although previous literature documents the importance of app engagement for customer spending (Gu and Kannan 2021), highlights the potential negative consequences of initiatives to drive app engagement (Paschmann et al. 2024), and calls for more research on how marketing-mix strategies can improve app engagement (Narang and Shankar 2019), little is known about the boundary conditions that shape the effectiveness of GETF adoption: GETFs grant customers full autonomy in setting goal difficulty, thereby leaving alignment of goals, strategies, and abilities to the customer. Since GETFs are usually employed in contexts (e.g., finance, mental health, nutrition) that are characterized by low levels of literacy and self-efficacy (Ramsey et al. 2022; Tay, Tay, and Klainin-Yobas 2018) and where customers typically rely on expert advice for guidance, there is reason for concern that customers may make end-goal and subgoal choices that are not well aligned with their individual circumstances. These poor choices may, in turn, undermine app engagement and ultimately harm retention. In fact, prior research on goal setting highlights the risks of unrestricted choices of end-goal difficulty, noting that a myriad of contingency effects can limit or even reverse the effectiveness of goal setting (e.g., Locke and Latham 2002, see also Web Appendix A, Table W.1). Previous research also stresses the importance of aligning goal pursuit strategy, that is, subgoal difficulty, to the individual's circumstances (Scholer and Higgins 2012), as failure to achieve subgoals often reduces commitment to the end goals (e.g., Devezer et al. 2013). Service providers tempted to implement GETFs within a mobile app, therefore, have to consider whether and how customer-determined end-goal and subgoal difficulty choices during GETF adoption translate to better app engagement behaviors and retention.

In summary, we ask: Do customers who set more (vs. less) difficult end goals and subgoals via GETF exhibit greater app engagement behaviors and retention (RQ1)? If so, can firms nudge customers to consider the importance of moderately difficult end goals and subgoals to further enhance app engagement behaviors and retention (RQ2)? To address these questions, we combine an empirical analysis of large-scale observational data with a field experiment conducted with a financial services provider.

The financial services provider is an app-based fintech firm in Australia, Raiz Invest Limited, which offers customers the opportunity to make micro-investments in a range of exchange-traded fund portfolios. The firm introduced a GETF to its app within our data observation window. A unique characteristic of this empirical context is that we observe end-goal and subgoal difficulty, initial goal progress (how much customers have saved toward their end goal at the time of GETF adoption), sociodemographic characteristics, and multiple measures of app engagement behaviors, including in-app actions (i.e., the amount of net contributions invested via the app) and app sign-in, both before and after customers have adopted the GETF. We also observe app retention one year after the end of the estimation window, which enables us to gauge the long-term effects of GETF-induced app engagement.

To identify the impact of the two goal difficulty dimensions on app engagement behaviors and retention (RQ1), we propose a hierarchical model that jointly estimates (1) the main effect of GETF adoption on the individual customer (heterogeneous treatment effects [HTEs]) and (2) the effect of the goal difficulty dimensions on these HTEs. To identify the first item, we exploit the variation in GETF adoption timing between customers and compare the behaviors of customers before and after GETF adoption. We account for the timing of customers’ self-selection to adopt GETF by combining the staggered synthetic control (SC) method (Abadie, Diamond, and Hainmueller 2010; Ben-Michael, Feller, and Rothstein 2022) with a control function approach using time-varying instrumental variables (IVs). We identify the impact of the goal difficulty dimensions in the second item by using IV regression to treat the potentially endogenous nature of these dimensions.

The steps undertaken in items 1 and 2 to deal with self-selection into GETF adoption and the endogeneity in goal difficulty dimensions do not allow us to completely rule out endogeneity concerns. We, therefore, conducted a large-scale field experiment with the service provider to provide evidence of the causal effect of goal difficulty dimensions on customers’ subsequent app engagement behaviors as well as showcase that highlighting these dimensions can nudge customers toward more beneficial GETF adoption (RQ2).

Our results reveal significant heterogeneity of GETF adoption effects on app engagement behaviors. Specifically, a substantial segment of GETF adopters showed zero or negative changes in in-app actions and app sign-ins. Notably, customers who adopted moderately challenging end goals and, more importantly, moderately challenging subgoals demonstrated greater in-app actions (i.e., investments), although this effect did not extend to app sign-ins. We further find that individuals who exhibited higher app engagement behaviors following GETF adoption (i.e., greater GETF-induced HTEs) are more likely to remain active one year later. Our field experiment offers additional evidence that merely setting goals within apps is insufficient to increase app engagement behaviors. In line with our analysis of the observational data, the field experiment emphasizes the causal effect of subgoal difficulty on in-app actions, while confirming that goal difficulty dimensions do not impact app sign-ins.

Our article offers both theoretical and actionable managerial insights for personal development services that deploy GETFs in mobile apps to boost customer engagement and retention. To our knowledge, we provide the first empirical evidence on how goal difficulty levels specified during GETF adoption affect subsequent app engagement and retention. Leveraging a rich data set, we move beyond hypothetical or short-term outcomes common in prior goal-setting research to assess and quantify the behavioral impact of customers’ own goal difficulty choices.

The findings advance the app engagement literature and offer clear guidance for practice. Marketing managers should avoid one-size-fits-all approaches and instead assist customers to align goal-setting during GETF adoption with their individual needs and capabilities, much like expert advisers do in traditional settings. We base our recommendation on the results from our observational data, which reveal that moderate levels of goal difficulty can improve engagement and retention, and our field experiment, which provides causal evidence that guiding customers toward these levels further enhances outcomes.

Theoretical Background

Our study draws primarily on two literature streams: app engagement and goal setting. We briefly review these streams and our contributions before focusing on end-goal and subgoal difficulty as key customer choices during GETF adoption and assessing how they may impact subsequent app engagement behaviors.

Mobile App Engagement Literature

Our article contributes to the growing literature on mobile app usage (Narang and Shankar 2019) and the persistent challenge of sustaining app engagement (Rutz, Aravindakshan, and Rubel 2019). Previous literature has repeatedly demonstrated the potential of apps to increase engagement with the service provider (Gill, Sridhar, and Grewal 2017), yet app engagement and retention are often very short-lived (Van Heerde, Dinner, and Neslin 2019). Factors influencing app engagement include, for example, the app's fee structure (paid vs. free; Lee, Zhang, and Wedel 2021) and technical performance issues such as app crashes (Shi et al. 2025). Stocchi et al.'s (2022) review paper on mobile apps discusses further antecedents of app engagement, such as intensity of individual participation or motivation, yet also highlights the continuing “scope for new research empirically evaluating the impact of innovating apps’ technological features” (p. 208).

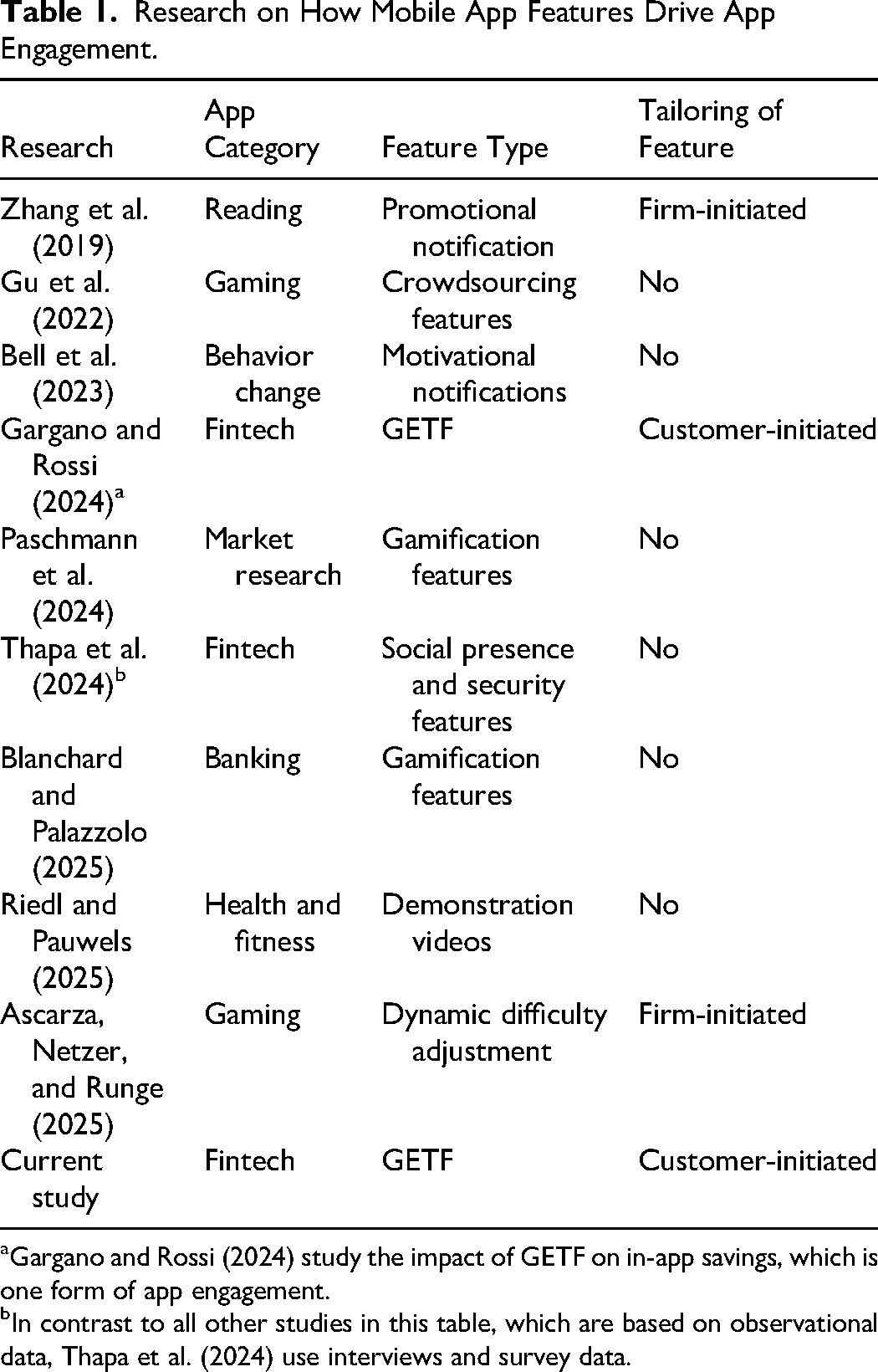

As shown in Table 1, prior research documents a range of app features that can increase engagement, including notifications (e.g., Bell et al. 2023; Zhang et al. 2019), crowdsourcing features (Gu et al. 2022), and gamification features (e.g., Blanchard and Palazzolo 2025; Paschmann et al. 2024). Of particular relevance are studies that examine tailoring app features to customer needs. For instance, Zhang et al. (2019) investigate the impact of firm-initiated promotional notifications tailored to customers’ (unobserved) engagement levels, while Ascarza, Netzer, and Runge (2025) analyze firm-initiated adjustments in game difficulty based on customers’ performance. These studies suggest that personalization of app features can enhance engagement. The closest paper to ours is Gargano and Rossi (2024): Using data from a fintech app, the authors demonstrate the positive impact of GETF adoption on in-app savings. However, their analysis evaluates only the average effect of adoption. It does not consider how the difficulty of chosen end goals and subgoals shapes app engagement, despite evidence that personalized features have heterogeneous effects (Ascarza, Netzer, and Runge 2025) and that customization can enhance satisfaction and loyalty (Ball, Coelho, and Vilares 2006; Cossío-Silva et al. 2016). This omission is significant because the difficulty of goals may determine whether customers continue to use, disengage from, or abandon the app. As a result, understanding the impact of goal difficulty choices is critical for theory, by clarifying how app features impact engagement when customers rather than firms configure features, and practice, by informing how firms can guide customers toward goals that sustain app engagement. To our knowledge, our article is the first to investigate how goal difficulty choices during GETF adoption affect subsequent app engagement and retention, and whether firms can nudge customers toward better decisions in this regard.

Research on How Mobile App Features Drive App Engagement.

Gargano and Rossi (2024) study the impact of GETF on in-app savings, which is one form of app engagement.

In contrast to all other studies in this table, which are based on observational data, Thapa et al. (2024) use interviews and survey data.

Goal Literature

The value proposition of a personal development app is that it enables customers to reach their personal development goals. Customers will, in turn, assess the value of the app based on how well the app enables them to reach their goals. In fact, Wolf, Weiger, and Hammerschmidt (2020) show that achieving a service-related goal leads to higher satisfaction with and loyalty to the service. As such, we expect that the more an app enables customers to achieve their goals, the higher the app engagement will be. To understand the impact of goal difficulty choices during GETF adoption on app engagement, we therefore draw from the literature on goal pursuit, the effect of explicit goal setting, and its link to customer behavior.

Impact of goal-enabling technology feature on app engagement behaviors

GETFs may influence app engagement in three ways: First, by enabling customers to set a clear end goal within the app, GETFs help create a mental representation of the desired outcome. This increased goal salience can enhance focus and motivation (Maes and Karoly 2005; Ülkümen and Cheema 2011), which may lead to more consistent and meaningful interactions with the app.

Second, GETFs help customers break down their main goal into smaller, manageable subgoals—such as specifying how much progress should be made within a certain time frame. This type of goal planning requires customers to think about future outcomes, which strengthens mental representations of their goals (Gollwitzer 1999). As a result, customers may develop more automatic, goal-aligned behaviors, reducing their reliance on conscious effort (Gollwitzer 1999) and increasing habitual app use. In fact, Hershfield et al. (2014) show that framing savings in more granular formats (e.g., “save $ 5 a day” vs. “save $150 a month”) encourages greater saving behavior.

Third, GETFs allow customers to monitor their progress toward their goals. Research suggests that the ability to monitor goal progress can enhance goal-congruent behavior by enabling customers to evaluate their current performance against a set standard and adjust accordingly (Ilies and Judge 2005; Kluger and DeNisi 1996; Standen and Rothman 2023). More specifically, control theory suggests that consumers are motivated to reduce the gap between their current state and desired goal (Carver and Scheier 1982): Progress tracking within the app prompts customers to adjust their behavior to stay aligned with their targets. By linking goal setting and progress tracking, the app provides ongoing feedback loops that can sustain app engagement over time. In summary, features that facilitate goal setting, subgoal planning, and progress monitoring not only support goal achievement but may also drive sustained engagement with the app. As customers interact more frequently and purposefully with these features, overall app engagement is likely to increase.

Impact of goal difficulty dimensions on app engagement behaviors

As we have discussed, the literature on goal setting suggests that GETF adoption may increase app engagement. In support of this, Gargano and Rossi (2024) have recently shown that customers who set an end goal via a GETF increased their in-app saving behavior, one particular form of app engagement. Yet, several authors also point out possible moderators that limit or even reverse the benefits of setting goals (e.g., Harkin et al. 2016; Soman and Cheema 2004; Wallace and Etkin 2018). Contrary to the potential positive effects of goal setting highlighted previously, a meta-analysis (Laranjo et al. 2021) examining the effectiveness of apps in increasing physical activity outcomes found that specifying a goal does not necessarily lead to greater physical activity. This suggests that the mere option of setting goals within apps may fail to help customers achieve service-related objectives and, as a result, not enhance app engagement. The same meta-analysis, however, indicates that a personalized feature in an app significantly improves its effectiveness. These observations raise the question of whether the difficulty of the end goal and subgoals chosen during the GETF adoption results in improved app engagement and retention.

Prior research has shown that end-goal and subgoal difficulty have a medium to large effect on goal-congruent behavior: In their meta-analysis of 125 studies, Wood, Mento, and Locke (1987, p. 421, Table 3) report effect sizes (Cohen's d) between .42–.77 for end-goal difficulty on task performance, and McEwan et al. (2016) find an effect size (Cohen's d) of .59 for strategy (subgoal) on physical activity behaviors in their meta-analysis consisting of 52 studies. However, previous research also provides mixed results regarding the optimal levels of (end-) goal difficulty (Erez and Zidon 1984) for performance. Similarly, the effectiveness of goal strategy (i.e., choice of subgoals) depends not only on the inherent properties of the strategy (size of subgoals) but also on whether the strategy fits the individual (Scholer and Higgins 2012). Understanding the suitable end-goal and subgoal size relative to an individual's skills, capabilities, or resources enables companies to actively guide customers’ planning processes, maximizing the positive impact of GETFs on app engagement. We test for an inverse U-shaped impact of end-goal difficulty and subgoal difficulty on app engagement for the following reasons.

Regarding end-goal difficulty, if customers specify an end goal that is too easy or too difficult to achieve, their engagement with the app while pursuing their personal development goal may not increase. Although goals must be difficult enough to be motivating (Locke and Latham 2006), overly ambitious goals can be demotivating (Soman and Cheema 2004). If the end goal is too easy, it will not be motivating; if it is too difficult and reaches the limits of an individual's ability, goal performance decreases (Locke and Latham 2002).

While setting a goal is the first step toward goal realization, planning how to reach that goal is an equally important subsequent task (Gollwitzer and Sheeran 2006). This planning/organization of goal pursuit is usually done by organizing the end goal into smaller and more manageable subgoals (Heath, Larrick, and Wu 1999). Previous research has shown that subgoals motivate consumers to pursue their end goal by allowing them to infer progress toward the end goal based on progress made toward individual subgoals (Kettle et al. 2016). The size of the subgoal relative to one's capabilities or resources (i.e., subgoal difficulty) needs to be carefully chosen: If the subgoal difficulty is too high, consumers are less likely to achieve it, which, in turn, can negatively impact the commitment to the overall end goal (Devezer et al. 2013). In contrast, if these subgoals are seen as too easy, the consumer may experience a sense of accomplishment that justifies temporary disengagement from the goal (Fishbach, Dhar, and Zhang 2006).

While companies cannot force customers to set end goals and subgoals of specific difficulty levels, understanding how these dimensions influence app engagement behaviors is crucial for delivering personalized nudges that effectively drive greater app engagement. The two goal difficulty dimensions are integral to the in-app GETF adoption process, requiring customers to make decisions about the difficulty of their end goals and subgoals. Our research contributes to the literature on consumer goal setting by providing, to our knowledge, the first investigation that empirically examines how consumer choices regarding the two goal difficulty dimensions impact subsequent app engagement behavior.

Context and Data

Institutional Setting

Our evidence draws on observational data from a financial investment app. Raiz Invest (previously Acorns) is an online-only fintech company that started in Australia in early 2016. Customers predominantly access Raiz Invest's services via the associated app located on iOS and Android mobile devices and use it to make micro-investments into a preselected portfolio of funds. When signing up to Raiz, customers provide information about themselves, including gender, age, income, and employment. Once customers have signed up to the service, Raiz enables them to link their third-party banking accounts directly to the Raiz account, with any positive Raiz account balance automatically invested into a selected investment portfolio. This allows customers to easily invest in a portfolio of funds or withdraw from their investments. The main source of revenue for Raiz is monthly fees, which are a function of customers’ account balances.

Customers can make three types of deposits to increase net contributions to their investment portfolio directly via the app: round-ups, lump sums, and recurring investments. 1 Customer balances can also increase in ways not directly initiated by customers. These include rewards that customers receive when making purchases at partnering brands through the Raiz app, dividends earned and reinvested, and returns that represent increases (or decreases) in the balance due to the portfolio growing (or declining). Customers select a specific investment portfolio based on the desired risk profile.

We operationalize app engagement in line with prior literature by recognizing that “engagement behavior is highly specific to the context in which it is being observed, … [which] implies that appropriate measures of user engagement ought to be constructed based on the use scenarios involved” (Gu et al. 2022, p. 1301). More specifically, while including app sign-ins as a traditional measure of app engagement (Bell et al. 2023), we also focus on in-app actions that reflect value-added engagement, that is, “value-added activity that contributes to the business model” (Paschmann et al. 2024, p. 250). Such value-added engagement may comprise different actions by the user, such as in-app shopping for shopping apps, watching in-app ads for social networking apps, or time spent answering surveys for market research apps (see Paschmann et al. 2024). In the context of Raiz Invest, the main value-added activity that contributes to the business model is net contributions (deposits minus withdrawals), as they represent the platform's most consequential form of active app usage: They directly change customers’ account balances and therefore the fees paid to Raiz. Our dual operationalization of engagement thus both respects established definitions and captures the behaviors most meaningful for understanding app engagement and firm outcomes in our setting.

Notably, our data also allows us to gauge the long-term impact of GETF adoption. Specifically, we know whether customers remained with Raiz one year after the observation period, providing a direct measure of retention. A customer is classified as retained if they maintain a positive investment balance and have not explicitly closed their Raiz investment account.

Description of the GETF

Raiz Invest launched a GETF on April 4, 2018, to help customers better achieve their financial goals. The GETF enables customers to set a savings goal (end goal) in the app and subsequently observe their progress toward this end goal. Customers who adopt a GETF are required to specify the target amount of the end goal and provide a brief description of the purpose of the goal (e.g., car, holiday, rent, house). Customers must also specify how they want to break this end goal into smaller subgoals: They have to define a (nonbinding) automatic deposit—both in terms of amount ($) and frequency. These automatic (recurring) deposit amounts, which we label subgoals, help the customers achieve their end goal. Nonautomated contributions, such as ad hoc lump-sum deposits and round-up deposits, accumulate alongside the automatically recurring deposits and contribute toward the end goal.

As such, customers had the same savings options (lump-sum investments, round-ups, and automated deposits) before and after the GETF launch. If a customer adopted the GETF, these savings were simply illustrated as contributions to their newly and explicitly specified end goal. Customers who did not adopt the GETF still had the three types of deposits available to them, namely recurring investments, lump-sum deposits, and round-ups. Figure W.1 in Web Appendix B illustrates the GETF adoption process for Raiz customers.

Only one end goal can be set at a time; multiple concurrent end goals are not permitted. Customers can, however, set different end goals over time, each one replacing the previous goal. Similarly, customers can specify only one automated investment frequency and amount (i.e., subgoal size) at a time.

Customers can only view their progress toward the end goal when they sign in, check their balance, and select the tab relevant to their goal. Customers do not receive any email notifications about their progress or any extrinsic motivation—such as badges—as a reward for app engagement behaviors. Any communication that customers receive from the company is not related to their GETF usage, except for the confirmation email they receive when adopting the GETF or making a deposit.

The GETF we observed is typical for GETFs in contexts where behavior can be automated: It allows customers to set subgoals by directly predetermining resources toward the end goal and thus automating future behavior at the time of GETF adoption (e.g., automated savings, automated energy saving, screen time restrictions, meal plan subscriptions) (see Shortt et al. 2021). Yet, such automated future behavior can always be changed at no cost (except for the time needed to change the app setting), and nothing prevents customers from deviating from these preset strategies. GETFs, however, also exist in contexts where behavior cannot be automated (e.g., exercise, nutrition), but where customers still set subgoals. Further, in contrast to our GETF, other GETFs may only require the specification of a rather vague end goal (e.g., “get fit”) or include gamification elements (e.g., Duolingo awards badges for achieving daily learning goals), which could boost engagement. Similarly, some apps are designed exclusively for goal achievement and progress tracking (e.g., HabitTracker, Strikes) and position GETFs as their primary value proposition.

Adoption of GETF over Time

We observed customers’ behaviors from 21 weeks before GETF launch until 50 weeks after. We split this timeline into three parts: The time before the GETF launch (T0 − 21 < t < T0), the estimation period (T0 ≤ t ≤ T = T0 + 40), and the holdout period (T < t < T + 10). For any customer j, Tj denotes the time (week) the customer adopted the GETF. By construction, Tj ≥ T0, and we define Tj = ∞ if the customer never adopted the GETF in our observation period. In total, we observed the behavior of 36,300 customers, with 2,447 adopting the GETF during the estimation period and 37 during the holdout period. We provide a bar graph (Figure W.2 in Web Appendix C) of the number of GETF adopters per time period since launch.

Goal Difficulty Dimensions

We operationalize goal difficulty choices in the following way. The difficulty of the end goal depends on an individual's savings capability (Senko and Harackiewicz 2005), for which we use income as a proxy measure. We, therefore, define end-goal difficulty as the ratio of goal size to annual income, that is, (end-goal amount)/(annual income). An end-goal difficulty of 10% implies that 10% of annual income is needed to reach this goal.

We use the ratio between subgoal amount (weekly recurring investment) that customers specify when adopting the GETF and their weekly income, that is, (subgoal amount)/(weekly income), as a measure of subgoal difficulty. A subgoal difficulty of .02 implies that a customer aims to save 2% of their weekly income each week.

Given the strong skewness of the goal difficulty dimensions, we winsorize them at the 95th percentile to reduce the impact of outliers (see Goswami and Urminsky 2020). The median end-goal amount is $5,000 (range = $20 to $999,999, mean = $16,075, SD = $50,143) 2 ; the median weekly subgoal is $25 (range = $1.15 to $10,500; mean = $77; SD = $277)—with the standard deviations of both difficulty dimensions highlighting the substantial heterogeneity in these choices. Given these median values as well as the median starting balance (how much GETF adopters have already saved when adopting the GETF) of $472, it would take an average customer approximately three years (160 weeks) to reach their end goal solely based on the automated deposits. The actual length of time for customers to reach their goals is, however, a function of both automated (recurring investment) and ad hoc contributions. Only 58 (2%) out of the 2,484 adopters reached their goal within the observation period.

Model-Free Evidence

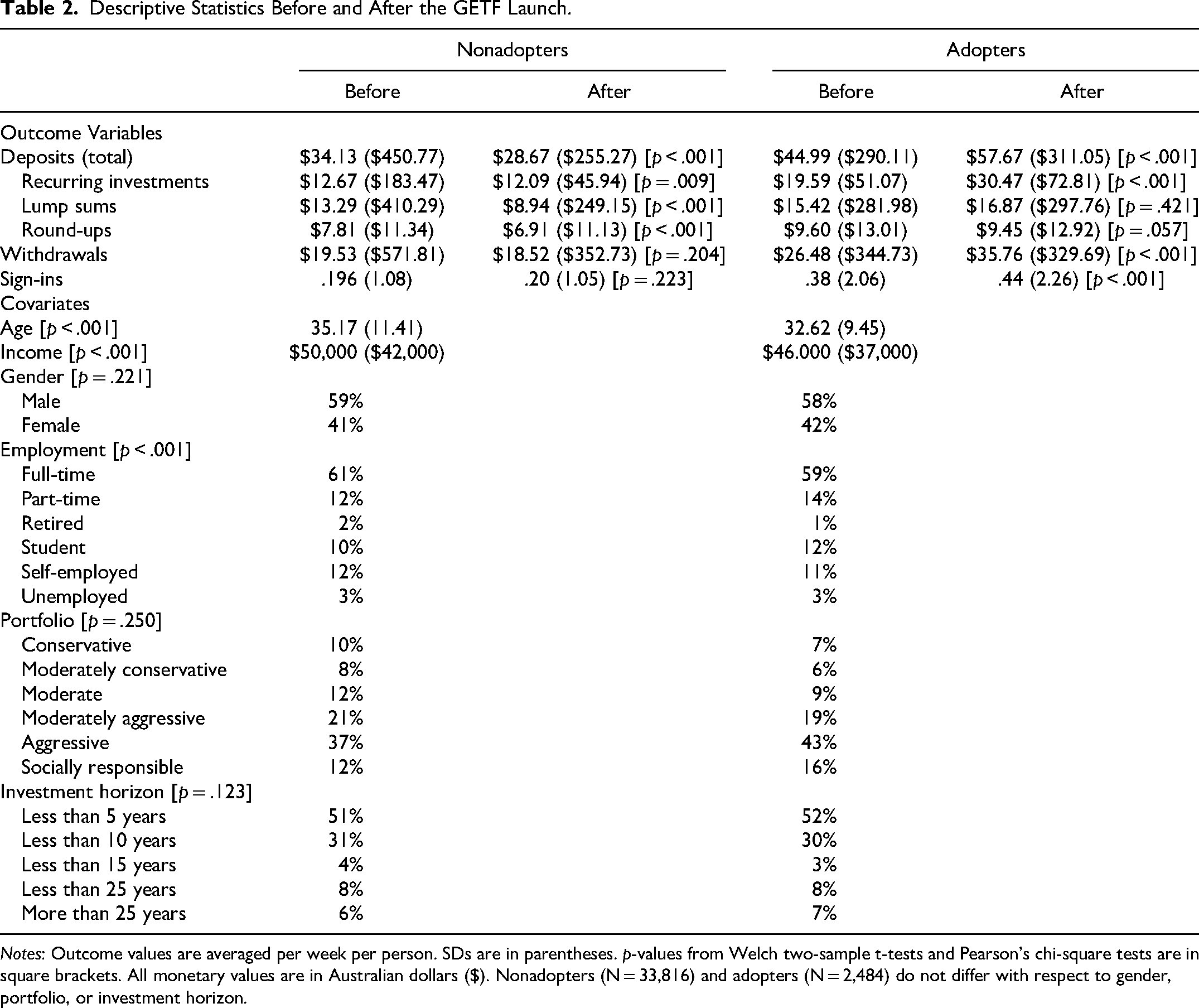

A first approximation of the effects of GETF adoption on customer behavior can be found in Table 2. This table reports the statistics of customers who adopted the GETF in the observation period versus customers who did not adopt the GETF during this period. The table reports the demographics of these two groups as well as summary statistics of their interactions with Raiz before and after the GETF launch. Table 2 shows that adopters are younger than nonadopters and have a lower income. The distribution of gender, portfolio, and investment horizon (i.e., the time horizon for investing stated at app sign-up) is similar between the adopters and nonadopters.

Descriptive Statistics Before and After the GETF Launch.

Notes: Outcome values are averaged per week per person. SDs are in parentheses. p-values from Welch two-sample t-tests and Pearson's chi-square tests are in square brackets. All monetary values are in Australian dollars ($). Nonadopters (N = 33,816) and adopters (N = 2,484) do not differ with respect to gender, portfolio, or investment horizon.

Table 2 indicates several differences between the two customer groups before versus after GETF launch (see also Web Appendix D, Figures W.3 and W.4, for a visual representation of changes in outcome variables over time). For in-app actions, we find that total deposits increased for adopters after GETF launch but decreased for nonadopters. In-app withdrawals also increased for adopters after the GETF was made available, partly offsetting the deposits. Thus, we focus on net contributions for subsequent analysis, accounting for deposits and withdrawals. We find that app sign-ins increase more for GETF adopters than for nonadopters.

In summary, the model-free statistics in this section provide some evidence that GETFs may have a positive impact on app engagement outcomes, yet the differences between GETF adopters and nonadopters before launch also reveal the challenge of observational data in that customers who adopt the GETF may be inherently different from those who do not adopt the GETF.

Modeling Approach

Overview

Our first research goal is to estimate the effects of goal difficulty dimensions on app engagement behaviors for those who adopt GETFs (RQ1). As such, we first estimate the impact of GETF adoption on engagement behavior k for customer j in time t (Tj ≤ t ≤ T), which is the difference between the observed engagement behavior yjkt and the counterfactual engagement behavior that would have arisen if the customer had not adopted the GETF,

In Step 1, we use the SC method (Abadie 2021) to construct

In Step 2, we propose and estimate a hierarchical model in which the first layer (Layer 1) identifies the HTE on a set of outcome behaviors for customer j, attributed to GETF adoption, and based on the counterfactual outcome

In Layer 2, we have to consider that a customer's choice of goal difficulty may be impacted by unobserved variables that also impact how much this customer benefits from adopting the GETF, such as motivation to pursue the goal or self-efficacy. These unobserved and consequently omitted variables raise endogeneity concerns. We therefore adopt the IV method with a different set of variables than used for the control function approach in Layer 1.

In the following sections, we discuss our approach in greater detail. To facilitate presentation, we drop the subscript k from the outcome variable in the equations.

Step 1: Staggered SC

Assume there are a total of J customers with Tj < ∞, and these customers are ordered so that customers who adopted the GETF in the estimation window (T0 ≤ Tj ≤ T) are labeled j ∈ 1, … J0, whereas those who adopted the GETF in the holdout window (T < Tj < T + 10) are labeled j ∈ J0 + 1 …, J. The corresponding timing of adoption is indicated by Tj, with timing T1 ≤ T2 ≤ … ≤ TJ. Customers who adopt the GETF do so once only, and once they have adopted the GETF, they stay in this state (i.e., it is an absorbing state).

Focusing on a specific GETF adopter j ∈ 1, … J0, the aim is to find weights

We use the staggered SC method (Ben-Michael, Feller, and Rothstein 2022) to obtain these weights. This approach accounts for observed time-varying differences between customer j and customers who adopt the GETF in the holdout window by matching observed behaviors based on L = 21 periods before customer j adopted the GETF. According to Abadie, Diamond, and Hainmueller (2010), matching preintervention (i.e., preadoption) outcomes for a sufficiently long period also helps control for unobserved differences between the treated and untreated customers. The approach uses partially pooled SC-method weights, which minimize a weighted combination of the imbalance for each GETF adopter j ∈ 1, …, J0 and the imbalance for these GETF adopters’ average.

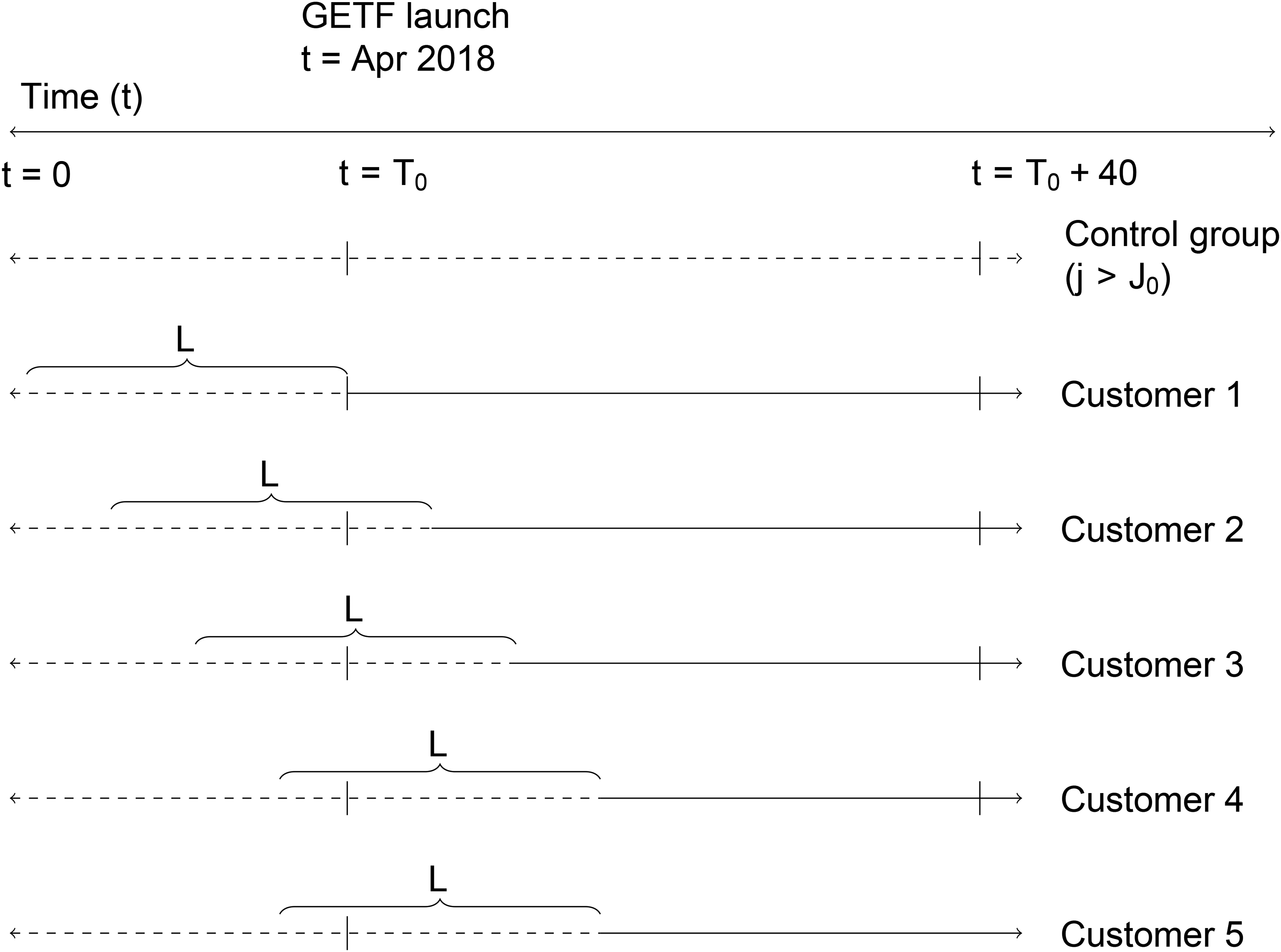

The procedure of constructing the staggered SC group for each customer is visualized in Figure 1. This figure illustrates that we observe app engagement behaviors as a longitudinal panel before and after the GETF launch, including before and after each individual customer adopted the GETF. The variation in GETF adoption time is used in the staggered SC method to calculate the weights needed to construct the counterfactual

A Graphical Illustration of the Launch and Adoption of the GETF.

Step 2: A Hierarchical HTE Model

Basic setup of the hierarchical model

The staggered SC method discussed in the previous section provides for each customer j who adopted the GETF in the estimation period a weight

Layer 1 of our hierarchical model is therefore: Ωj is a weight matrix constructed based on the weights α0j and α1j are coefficients to be estimated; and

Layer 2 of our hierarchical model links the hierarchical treatment effects α1j to a vector of covariates Zj, which include the goal difficulty dimensions and their quadratics

To account for possible self-selection into GETF adoption, which may bias estimates in Equation L1, and possible omitted variable bias in L2, we make adjustments to each layer, as discussed in the following. We estimate the resulting hierarchical model consisting of several sublayers (Equations L1a, L1b, L2a, and L2b) within a Bayesian estimation framework (see Web Appendix E.2 for a detailed description). By formulating a Bayesian approach to the IV methods used in both layers, we follow Zhang, Wedel, and Pieters (2009), who incorporated the latent IV (Ebbes et al. 2005) approach into a Bayesian framework.

Layer 1: Accounting for Selection Effects in GETF Adoption

The staggered SC approach used to construct the weights

In Equation L1b,

These instruments are constructed to retain variation that is useful for identification while deliberately excluding immediate geographic neighbors who may exert social influence or word-of-mouth effects on the focal customer. By removing customers from the same postcode, we mitigate the possibility that the instruments reflect direct behavioral spillovers among socially connected individuals, such as neighbors, friends, or family members. Instead, these state-level aggregates are designed to reflect shared regional characteristics, such as social status, income, lifestyles, exposure to statewide trends, economic conditions, or macro-level patterns of digital engagement that may shape the general environment in which a customer makes app-related decisions. For example, a high rate of GETF adoption across the state may indicate increasing popularity of the feature, possibly driven by regional financial trends, or economic uncertainty, either of which could indirectly affect the focal customer's propensity to adopt the feature.

Similarly, a spike in app logins among state-level customers (outside the postcode) could indicate heightened engagement with the platform across the region, which might correspond with broader campaigns, app updates, or seasonal trends in financial behavior. In contrast, increased regional app engagement may signal that general platform use is already high, thereby reducing the salience or perceived necessity of adopting an additional feature such as GETF. The widespread app activity may be an indication that core functionalities are sufficient, leading to a substitution effect where engagement with existing features replaces the motivation to adopt new ones.

Importantly, these two instruments are not visible to the focal customer and are, therefore, highly unlikely to have a direct effect on their individual app engagement or decision-making processes. The focal customer cannot observe how many people in the broader state, especially those outside their postcode, have adopted the GETF feature or are logging in during a given week. As such, we argue that these instruments satisfy the exclusion restriction by influencing the focal customer's GETF adoption decision only through their impact on broader informational or behavioral cues at the regional level.

Details on the choice of variables included in the probit selection equation, the results and trace plots can be found in Web Appendix F.1, Table W.2 and Figure W.5. Importantly, we find a significant negative effect of

Layer 2: Controlling for Endogeneity in Goal Difficulty Dimensions

As we seek to estimate the impact of goal difficulty dimensions on the HTEs α1j via Equation L2, we face the concern that the goal difficulty choices themselves are potentially endogenous: Unobserved customer motivation to engage with the app and customers’ self-efficacy beliefs are likely to influence both goal difficulty dimensions as well as engagement with the app, thus leading to endogeneity concerns. To address these concerns, we again adopt an IV approach. To obtain unbiased estimates of α1j in Layer 2, we thus use the following sublayers:

In finding the IVs

Results

The staggered SC method (Step 1 in Section 4) generates a set of weights

Next, we focus our discussion on the estimates of the hierarchical model (our Step 2 discussed previously).

Effects of GETF Adoption and Goal Difficulty Dimensions on App Engagement Behaviors

Effects of GETF Adoption

For each draw from the Gibbs sampler, we compute the average treatment effect (ATE) by taking the mean of the individual-level treatment effects (i.e., HTEs) across all GETF adopters. Repeating this process over 25,000 iterations yields a posterior distribution of the ATE. This distribution captures the overall effect of GETF adoption on app engagement behaviors at the population level. Our analyses show that GETF adopters exhibit significant increases in their two app engagement behaviors. Weekly net contributions increased on average by µα = $12.22 (95% CI = [.23, 24.18]), and weekly sign-ins increased on average by µα = .13 (95% CI = [.13, .14]) after GETF adoption (see Figure W.6 in Web Appendix G.1).

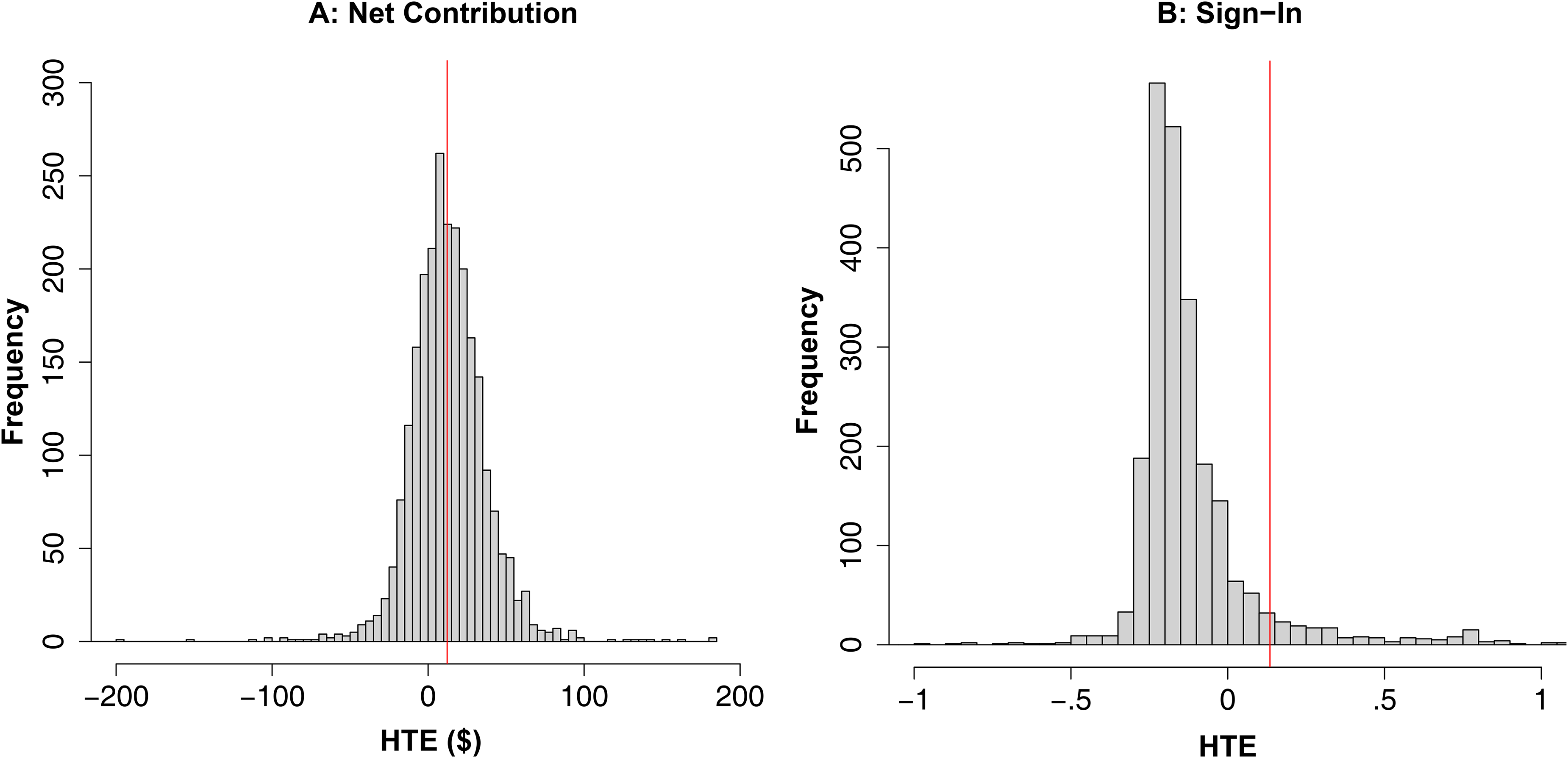

In addition, we examine HTEs at the individual level to explore how the impact of GETF adoption varies across customers. For each of the 2,447 GETF adopters, we estimate their individual HTE by averaging their treatment effect draws over the 25,000 Gibbs sampler iterations. This results in a distribution of individual-level effects, rather than a single population average. Figure 2 presents the distribution of the HTEs and reveals their substantial heterogeneity. This suggests that a segment of customers experienced some unintended consequences from adopting the GETF and indicates that there seem to be some moderating conditions to this effect.

Layer 1a Results: HTE Distributions.

To explore the moderating conditions of goal difficulty dimensions on app engagement behaviors after GETF adoption (see the discussion in our “Theoretical Background” section), we include linear as well as quadratic terms for these variables in Equation L2a. We also control for the linear and quadratic influence of initial goal progress and include age, gender, income, employment, and investment horizon as possible control variables that may further impact how much GETF adoption changes app engagement. We include the total portfolio return rate during the weeks in which customers adopted a GETF to account for the return on investment, the portfolio they are in at the end of the observational period as a measure of their investment risk preference, the type of device they have most frequently used to sign in to the app during the observational period, and the average number of emails and push notifications sent during the weeks in which they adopted a GETF.

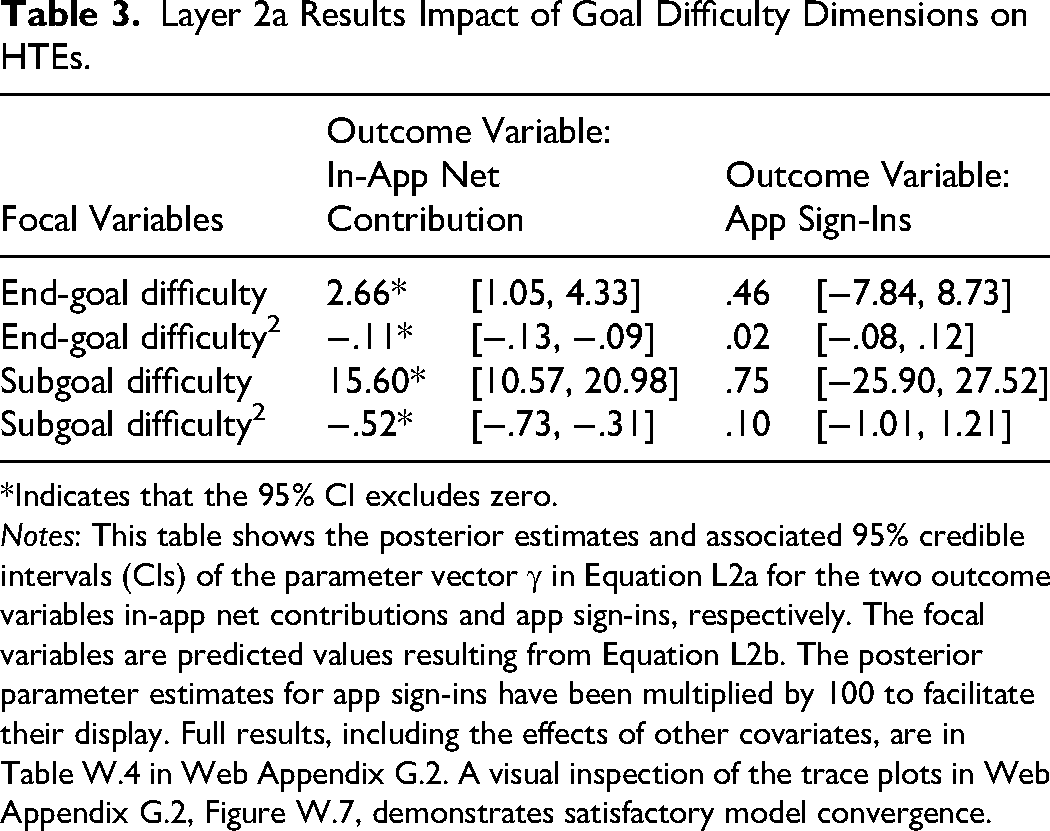

Table 3 provides the estimates for γ in Equation L2a for changes in in-app net contributions and app sign-ins, respectively, and their associated 95% CIs for the focal variables end-goal difficulty, subgoal difficulty, and their quadratics. It reveals that customers’ choices of end-goal and subgoal difficulty at the time of GETF adoption have concave relationships with net contribution, such that moderate levels lead to the highest amount of in-app net contributions. Thus, in line with the literature, we find that goals must be challenging to be motivating but not too challenging, lest their difficulty becomes a deterrent. Detailed estimation results are in Table W.4 in Web Appendix G.2.

Layer 2a Results Impact of Goal Difficulty Dimensions on HTEs.

*Indicates that the 95% CI excludes zero.

Notes: This table shows the posterior estimates and associated 95% credible intervals (CIs) of the parameter vector γ in Equation L2a for the two outcome variables in-app net contributions and app sign-ins, respectively. The focal variables are predicted values resulting from Equation L2b. The posterior parameter estimates for app sign-ins have been multiplied by 100 to facilitate their display. Full results, including the effects of other covariates, are in Table W.4 in Web Appendix G.2. A visual inspection of the trace plots in Web Appendix G.2, Figure W.7, demonstrates satisfactory model convergence.

In contrast to net contributions, none of the independent variables, except for the type of device used most frequently to sign-in to the app, demonstrates significant associations with the HTEs for app sign-ins.

Implications for Goal Difficulty Dimensions

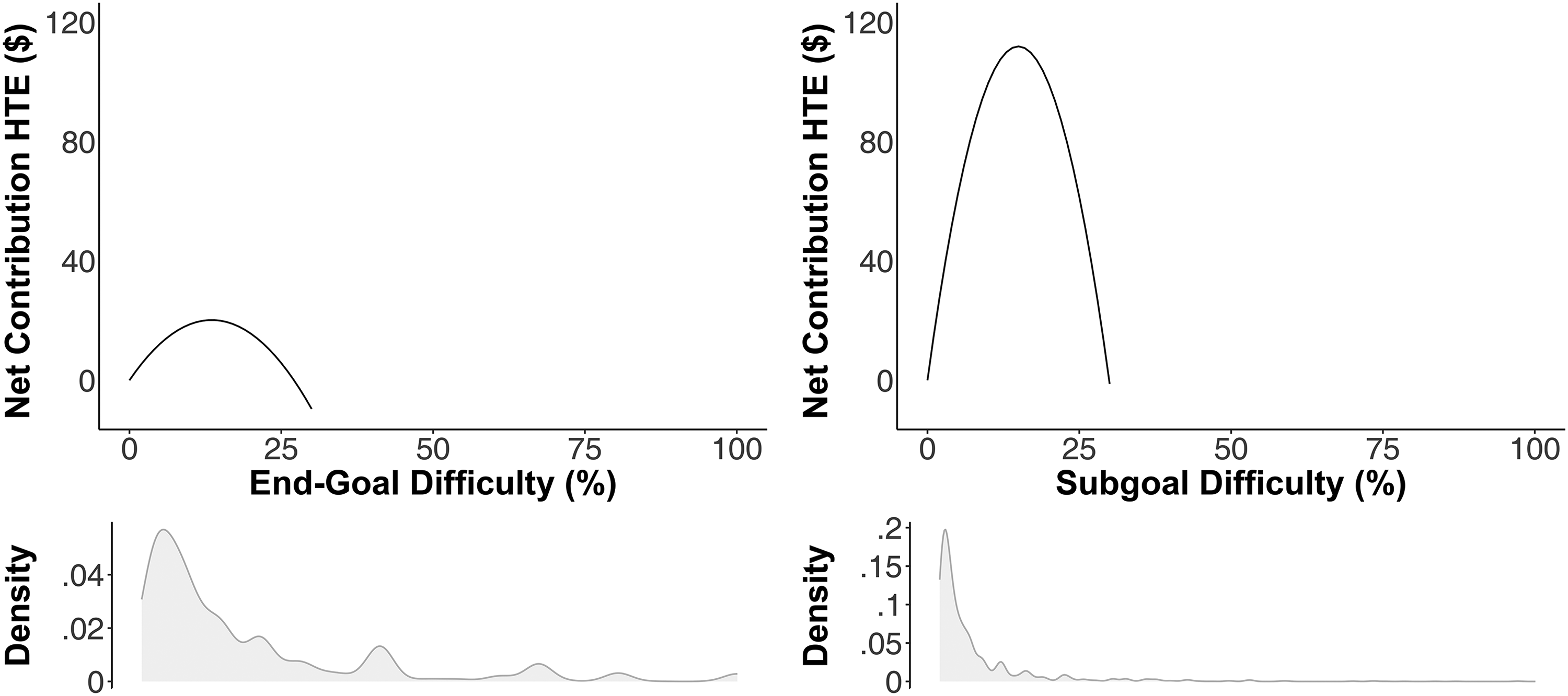

We have demonstrated that GETF adoption does not benefit all customers and that its impact is moderated by end-goal and subgoal difficulty. It is thus useful for customers and managers to know the levels of goal difficulty that are most effective in increasing in-app actions. The results in Table 3 allow us to determine these most effective levels.

Evidenced by the notably flatter curve for end-goal difficulty, Figure 3—which displays the impact of goal difficulty dimensions on net contributions in addition to the actual density of goal difficulty choices—demonstrates that subgoal difficulty holds much greater potential to improve heterogeneous treatment outcomes. It also shows that the HTEs for net contribution are maximized if customers choose an end-goal difficulty of 12.28% (i.e., customers engage in greater in-app net contributions if their savings goal equals 12.28% of their annual income). For the median customer who earns $75,000 per year, this equates to a goal size of approximately $9,200. Customers make the highest in-app net contributions if they set their subgoal difficulty at 15.02% (i.e., customers perform best if they save 15.02% of their weekly income). For the median customer, this equates to $216.63 a week. While these values are higher than the median values currently set by Raiz customers who adopted the GETF, they are within the observed range of values in the sample. We also note that these difficulty levels are not too far from the recommended savings goal of 20% of income often propagated by money-planning tools following Elizabeth Warren's suggestion in All Your Worth: The Ultimate Lifetime Money Plan (Warren and Tyagi 2005).

Layer 2a Results: The Impact of Goal Difficulty Dimensions on Net Contributions.

Effects of GETF-Induced Engagement and Subgoal Failures on Long-Term Retention

Higher engagement with a service provider usually leads to higher retention (Torkzadeh et al. 2022). In this section, we focus on whether GETF-induced higher engagement (i.e., HTEs) translates to higher app retention. We hereby acknowledge that retention is also a function of subgoal and end-goal achievement: Subgoal failures have been shown to reduce commitment to the end goal (Devezer et al. 2013) and thus may also negatively impact customers’ commitment to the app itself. End-goal achievement, in contrast, may reduce customers’ need for the app.

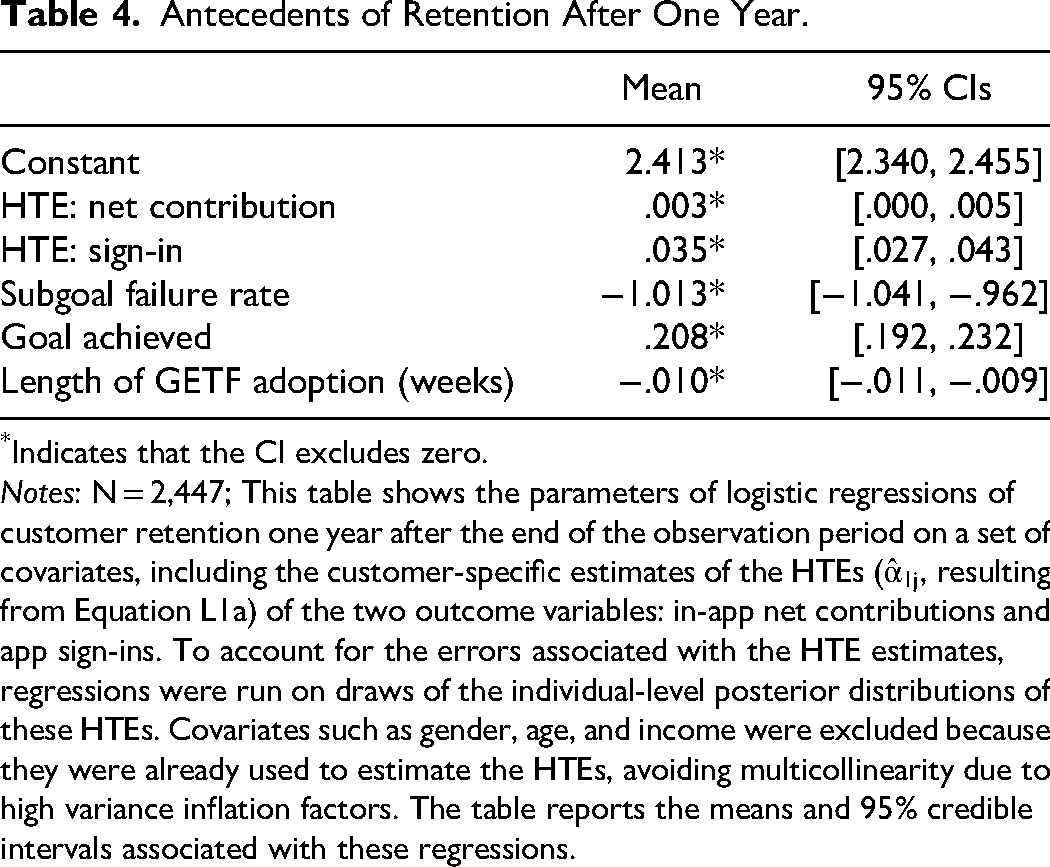

We estimate a logistic regression with retention one year after T (i.e., after the end of the observation period) as a dependent variable. A customer is retained (retention = 1) if they have a positive investment balance and have not yet closed the account (i.e., explicitly churned). Retention equals zero if the customer has closed the account or has an investment balance of $0. Our independent variables are the change in engagement behavior due to GETF adoption (i.e., the estimated HTEs for net contribution and app sign-in), as well as subgoal failure rate (i.e., the number of times the customer failed to meet the subgoal divided by the number of weeks in which the customer used GETF during the observation period), and end-goal achievement (i.e., an indicator variable which equals one if the customer achieved the end goal during the observation period, and zero otherwise). Subgoal failures occur when customers fail to make deposits that meet or exceed the specified subgoal amount. We also include as control the number of weeks that the customer used the GETF in the same period. Our sample includes 2,447 GETF adopters, who adopted the GETF between GETF launch T0 and the end of the estimation period T0 + 40, and for whom we used the estimated HTEs for net contributions and app sign-ins from the previous section.

The results in Table 4 show that long-term retention is positively associated with customers’ GETF-induced app engagement behaviors (HTEs for net contributions and app sign-in), thus supporting previously documented links between engagement and retention. Given that the previous section documented the link between goal difficulty choices and in-app engagement, this finding further stresses the need for managers to provide customers with guardrails in the GETF adoption process.

Antecedents of Retention After One Year.

Indicates that the CI excludes zero.

Notes: N = 2,447; This table shows the parameters of logistic regressions of customer retention one year after the end of the observation period on a set of covariates, including the customer-specific estimates of the HTEs (

Similarly, consistent with prior findings on subgoal failure, we find that higher rates of subgoal failure lead to lower retention in the long term: This finding highlights the possible unintended, negative consequences of GETF adoption and again stresses the need to carefully manage customers’ choices of goal difficulty during GETF adoption. Customers achieving their end goal during the observation period had a positive effect on subsequent retention. This is an encouraging finding for service providers, as it indicates that customers do not stop using the service after they have achieved their end goal; instead, it seems to suggest that the personal development goal (here, financial security) continues to exist. Finally, we find that the length of GETF adoption has a negative impact on long-term retention. This may suggest that the saliency of the savings goal—and, thus, the utility of the app—may decrease with increased distance to GETF adoption.

Field Experiment

In the previous section, we reported that customers who set themselves moderately difficult end goals and subgoals show greater app engagement in terms of net contributions after GETF adoption. These findings are based on observational data, and although we addressed endogeneity concerns in several ways, we cannot completely rule these out. Therefore, while our results suggest a strong association between goal difficulty dimensions and subsequent app engagement behaviors, we do not claim causality.

To further ascertain the importance of end-goal and subgoal choices and provide more evidence for possible causality in the relationship discussed previously, Raiz Invest conducted a field experiment. The objective of this experiment was to demonstrate that stressing the importance of goal difficulty dimensions in communication with customers can change subsequent app engagement behaviors.

The field experiment randomly assigned customers who had not adopted the GETF at that point to one of five between-subject conditions. Two of these conditions were control conditions, where the first encouraged customers to set up a recurring investment without adopting GETF (Control Condition 1: Recurring Investment), and the second encouraged customers to adopt GETF without mentioning recommended goal difficulty choices (Control Condition 2: GETF Only). The other three conditions were the treatment conditions, where goal difficulty choices were suggested and encouraged. Two of the three treatment conditions were Treatment Condition 1: End-Goal Difficulty and Treatment Condition 2: Subgoal Difficulty, suggesting recommended difficulty choices for end goals and subgoals, respectively. The third treatment condition was Treatment Condition 3: End-Goal and Subgoal Difficulty, suggesting recommended end-goal and subgoal difficulty choices at the same time. While customers cannot be forced to make specific difficulty choices, the three treatment conditions likely encouraged customers to think about the merits of setting end-goal and/or subgoal amounts that are neither too easy nor too difficult to achieve.

The exact wording of the five experimental conditions was as follows:

How to save and invest more money effectively—set up a recurring investment [Control Condition 1: Recurring Investment] How to save and invest more money effectively—set up a savings goal [Control Condition 2: GETF Only] How to save and invest more money effectively—set up a savings goal of [end-goal difficulty (%) × annual income ($)] [Treatment Condition 1: End-Goal Difficulty] How to save and invest more money effectively—set up a savings goal with a recurring investment equivalent to [subgoal difficulty (%) × weekly income ($)] per week [Treatment Condition 2: Subgoal Difficulty] How to save and invest more money effectively—set up a savings goal of [end-goal difficulty (%) × annual income ($)] with a recurring weekly investment equivalent to [subgoal difficulty (%) × weekly income ($)] [Treatment Condition 3: End-Goal and Subgoal Difficulty]

The “Set up on Raiz” button in all five conditions led customers to the same page in the app, where they could set either a recurring investment or a savings goal and thus adopt the GETF. Details about the experimental conditions can be found in the Web Appendix H, Figures W.8 and W.9.

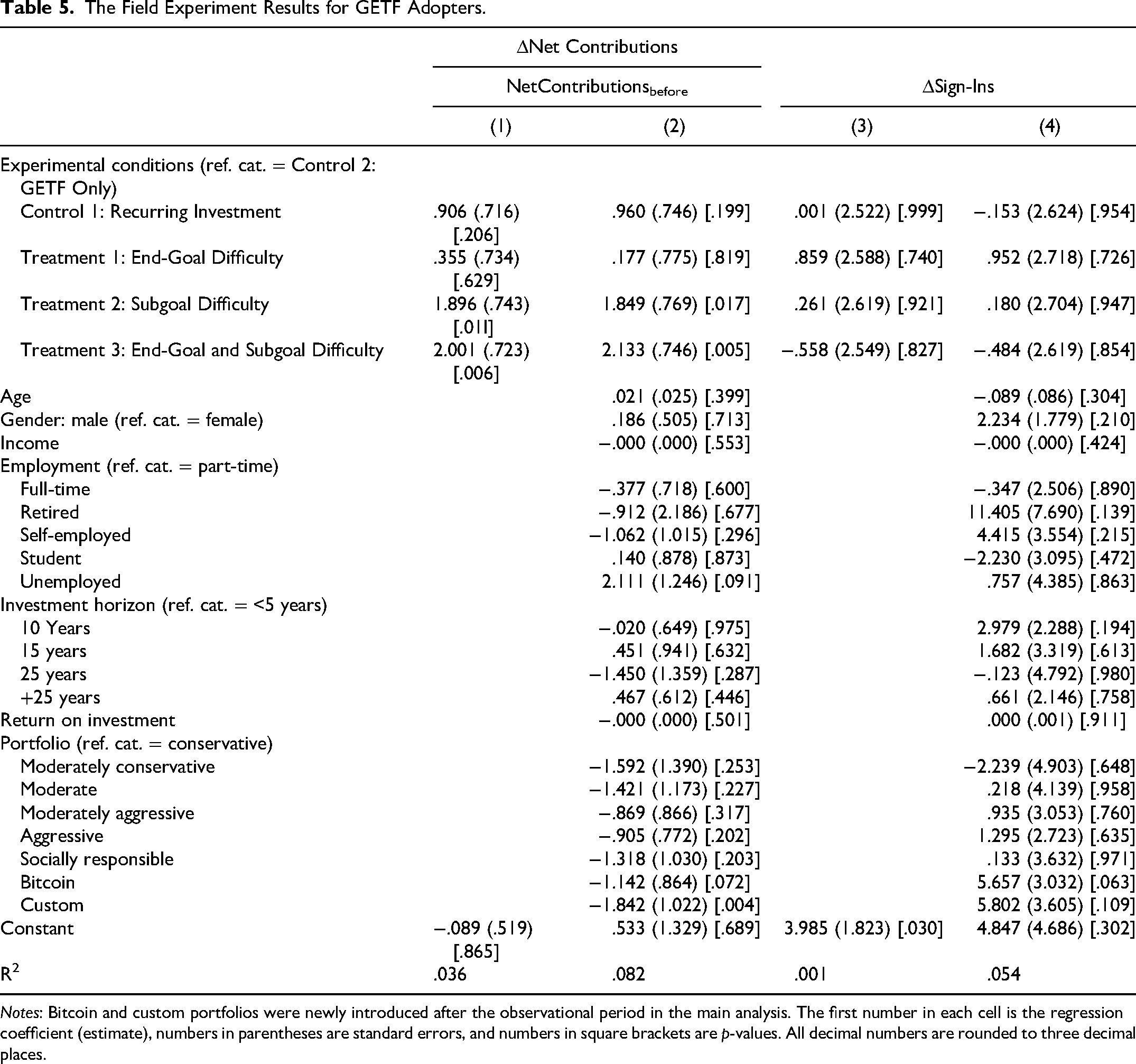

Raiz sent the respective emails on April 16, 2023, targeting, in each condition, 10,000 customers who had a positive balance but had not yet adopted the GETF. Although the assignment of customers into one of the five conditions was randomized, customers still self-selected to adopt GETF. To compare people with similar levels of motivation, we therefore only focused on those customers who adopted the GETF within 14 days after the email was sent to them (i.e., between April 16 and 30, 2023), noting that even customers in Control Group 1 may have chosen to adopt the GETF. This resulted in a total of 329 customers (45.9% female, 54.1% male) across Control Condition 1: Recurring Investment (71 customers), Control Condition 2: GETF Only (65), Treatment Condition 1: End-Goal Difficulty (64), Treatment Condition 2: Subgoal Difficulty (61), and Treatment Condition 3: End-Goal and Subgoal Difficulty (68).

To investigate the impact of the different conditions on app engagement behaviors, we regressed two outcome variables on these conditions while simultaneously controlling for gender, age, income, and portfolio choice of customers: (1) percentage change in cumulative in-app net contributions (ΔNetContributions/NetContributionsbefore), and (2) change in sign-ins (ΔSign-Ins), all observed between March 30 (two weeks before the emails were sent) and May 16, 2023 (one month after the emails were sent). We set Control Condition 2: GETF Only as the reference group in the analyses. The two control groups showed no statistical difference with respect to all outcome variables. The results remained consistent when combining both Control Condition 1 and Control Condition 2 into a single condition.

The results in Table 5 show that compared with Control Condition 2: GETF Only, the participants in the Treatment Condition 2: Subgoal Difficulty Condition (β = 1.90, p = .011) and the Treatment Condition 3: End-Goal and Subgoal Difficulty Condition (β = 2.00, p = .006) had a significantly higher proportional change in net contribution. Neither Treatment Condition 1: End-Goal Difficulty (p = .629) nor Control Condition 1: Recurring Investment (p = .206) differed from Control Condition 2: GETF Only. These results remained robust even after controlling for age, gender, income, employment, investment horizon, amount of return on investment, and portfolio as of March 30, 2024. Combined, these findings offer additional evidence of the causal effect of subgoal difficulty on app engagement behaviors, as documented in the “Implications for Goal Difficulty Dimensions” section, and underscore its greater significance compared to end-goal difficulty.

The Field Experiment Results for GETF Adopters.

Notes: Bitcoin and custom portfolios were newly introduced after the observational period in the main analysis. The first number in each cell is the regression coefficient (estimate), numbers in parentheses are standard errors, and numbers in square brackets are p-values. All decimal numbers are rounded to three decimal places.

Lastly, we also examined the effects of the treatment conditions on the number of app sign-ins. However, consistent with the findings from the previous section—specifically, the lack of impact of goal difficulty dimensions on app sign-ins (see Table 3)—we observed no differences between conditions in app sign-ins.

In summary, the results from the field experiment show that highlighting moderate goal difficulty dimensions has a significant positive effect on in-app engagement behaviors. This corroborates the findings of the observational study in the section “Effects of GETF Adoption and Goal Difficulty Dimensions on App Engagement Behaviors,” allowing for greater confidence in the causal effects of goal difficulty dimensions on app engagement behaviors.

Discussion and Conclusion

Consumers are increasingly turning to mobile apps to achieve physical, mental, social, professional, or financial well-being goals. Maintaining customer app engagement is challenging, prompting service providers in these industries to adopt goal-enabling technology features (GETFs) within mobile apps. Whereas in typical personal development services, customers decide on their goals and how to reach them in consultation with a specialist (e.g., financial adviser, medical practitioner, personal trainer), GETFs usually offer customers free choice in determining the goal difficulty dimensions. Building on previous research in app engagement and goal setting, we ask two important questions: Do customers who set more or less difficult goals via GETFs exhibit greater app engagement behaviors and retention? Furthermore, can firms nudge customers to recognize the significance of moderate goal difficulty dimensions to further enhance their app engagement behaviors?

To address these questions, we offer an empirical evaluation of the effects of goal difficulty dimensions within a GETF on customer app engagement behaviors and retention for a fintech company. Using a hierarchical model, we show that goal difficulty dimensions are significantly associated with individual, specific treatment effects on net contribution, even after accounting for endogeneity arising from customers’ self-selection to adopt GETF and from choices of goal difficulty dimensions. Notably, we use a combination of (1) staggered SC weights and (2) a control function with instruments to treat selection effects in the GETF adoption decision, and (3) an IV regression to account for the endogenous goal difficulty choices. As even the most careful treatment of endogeneity cannot completely rule out all endogeneity concerns, we provide further evidence from a field experiment. This field experiment shows that encouraging customers to think about the merits of setting suitable end-goal and subgoal amounts can increase GETF adopters’ in-app engagement behaviors.

Our findings suggest that GETF adoption has an overall beneficial impact, increasing customers’ in-app actions and app sign-ins, as evidenced by the positive and significant means of the HTEs. Yet, the HTEs themselves provide a more nuanced picture of the impact of GETF adoption. While the majority of customers engage in more in-app net contributions when using the GETF, a substantial segment of customers shows a negative change or no improvement in in-app actions and app sign-ins after GETF adoption. We demonstrate how the choices of end-goal and subgoal difficulty during GETF adoption can explain variations in subsequent app engagement. We find evidence of an inverted U-shape effect for both goal choices on in-app engagement behaviors, allowing us to identify difficulty levels associated with the highest engagement. We further show that engagement changes due to GETF adoption as well as failure to achieve subgoals can explain customer retention after one year. Combining these insights with the results from the field experiment, we note that among the two goal-difficulty dimensions, subgoal difficulty consistently and significantly affects app engagement behaviors.

In summary, we extend previous research on app engagement and the impact of goal setting by demonstrating the benefits and boundary conditions of GETF adoption for app engagement and retention.

Managerial Implications

Our results carry powerful and broadly applicable implications for other firms and industries where GETFs proliferate or could be utilized. First, and closely related, a growing number of banking services are adding GETFs to their core apps. In Australia, these include the Commonwealth Bank of Australia and the National Australia Bank. Wells Fargo, in the United States, has added “My Savings Plan,” which enables customers to specify a specific goal as part of their online banking services. In other fields, customers can adopt GETFs to achieve certain health outcomes, such as losing weight (e.g., Weight Watchers, Carb Manager), reducing alcohol or tobacco consumption (e.g., Reframe), or managing blood glucose levels (e.g., DiabetesConnect, Health2Sync). Our results imply that apps that support customers in achieving their goals can benefit from implementing features that facilitate customer goal setting and, as a consequence, motivate greater app engagement behaviors and retention. GETFs may thus address the challenge of balancing customer goals with the firm's objectives, adding to the currently limited set of tools available to firms to enhance both the service's value to the customer and the customer's value to the service. Our results show that even without extrinsic motivation such as badges or other gamification elements, GETFs can have a positive impact on app engagement.

However, our findings also point to considerable heterogeneity in GETF effectiveness across customers. Our findings on the moderating factors influencing GETF effectiveness suggest that more effective levels of goal difficulty exist for end goals and subgoals during GETF adoption. Firms may seek to design their GETFs to guide customers toward these individual well-aligned levels, for instance, by setting default goal sizes based on factors such as income, education level, current health, or fitness status. Our finding that adopting GETFs creates opportunities for customers to fail their subgoals, subsequently reducing retention, should serve as a caution against the naive implementation of GETFs. In this regard, GETFs can be viewed as a double-edged sword: While they generally increase app engagement behaviors, they also have the potential to reduce customer engagement and retention. Our field experiment, however, supports the conclusion that careful GETF design can nudge customers into mutually beneficial outcomes, including customer well-being (e.g., achieving financial goals) and business performance outcomes (via higher customer in-app actions, app sign-ins, and retention).

Limitations and Future Research

Our work provides important contributions to extant research, and its limitations can serve as opportunities for future work. Our research focused on how goal difficulty dimensions at the time of GETF adoption affect customers’ app engagement behavior and retention. GETFs, however, also enable customers to monitor their progress and take remedial action on the path toward their goals. We believe that company interventions to help customers better deal with subgoal failures can be similarly fruitful avenues for further research.

We were unable to directly measure customers’ motivation and self-efficacy. Motivation—that is, the internal cognitive and affective processes that instigate and sustain goal-directed actions and outcomes—may differ between customers and impact not only their choice to adopt the GETF but also their choice of goal difficulty and app engagement behaviors directly. Self-efficacy—that is, one's perceived capabilities to perform actions at designated levels—has been shown to affect goal setting and goal-congruent behavior. Previous research has shown that individuals with high self-efficacy usually choose more challenging goals, adopt better strategies (i.e., set more suitable subgoals), and deal better with negative feedback (Locke and Latham 2002). Self-efficacy influences motivation and is itself a function of performance accomplishments (Schunk and DiBenedetto 2021). As such, self-efficacy varies not only between subjects but also within subjects. In the context of GETFs, self-efficacy may impact whether, how, and when customers adopt the GETF or how much they engage with the mobile app. However, GETF usage itself may also influence self-efficacy, as customers can easily monitor their past performance. In particular, failure to reach subgoals may reduce self-efficacy and, in turn, lower motivation and app engagement. Companies usually do not monitor customer motivation or self-efficacy; they are thus also not available in our dataset. Given the importance of motivation and self-efficacy for customers’ GETF adoption and app engagement behaviors, future research that aims to identify the causal effect of goal difficulty choices on app engagement behaviors should either collect additional information on these variables from customers (e.g., via surveys) or, similarly to our work, carefully account for the endogeneity induced by omitting these variables.

We were also unable to directly measure customers’ disposable income and used actual income instead. Our operationalization of end-goal and subgoal difficulty—which is based on actual income—may therefore suffer from reduced comparability between customers. While in our case one can argue that consumption (and thus disposable income) is frequently modeled as a function of income (Arellano, Blundell, and Bonhomme 2017), and we thus used a reasonable approximation, this concern points to a bigger issue: Companies may not have enough information about customers to aid in the personalization of goal difficulty dimensions. Future research may therefore investigate the possibility of using latent variables to overcome this limitation (see, e.g., Deng, Lee, and Tan [2025], who measure app engagement via latent states).

Finally, it is worth noting that in our data, very few customers reached their goals within the observation period. We also document that reaching the goal does not lead customers to abandon the service, even though it has fulfilled its purpose. In the context of personal development goals, we argue that such abandonment is generally unlikely, as there is always a new savings goal that needs to be met, a new language to be learned, or a new fitness level to be mastered. As such, GETFs for personal development goals promise to enhance both consumer well-being and business performance outcomes. Research in other contexts may, however, find that reaching an end goal has different effects on engagement and retention.

Supplemental Material

sj-pdf-1-mrj-10.1177_00222437261433457 - Supplemental material for Increasing App Engagement Behaviors via Goal-Enabling Technology Features: The Role of Goal Difficulty Dimensions

Supplemental material, sj-pdf-1-mrj-10.1177_00222437261433457 for Increasing App Engagement Behaviors via Goal-Enabling Technology Features: The Role of Goal Difficulty Dimensions by Jake An, André Bonfrer and Christine Eckert in Journal of Marketing Research

Footnotes

Acknowledgments

The authors thank the JMR review team, including Rebecca Hamilton, the editor, and Vikas Mittal, who served as editor during the first revision round of the manuscript. They also thank their colleagues John Roberts, Rahul Govind, Maik Hammerschmidt, Welf Weiger, Tobias Wolf, Chris Dubelaar, Bernd Skiera, Harald van Heerde, Thomas Otter, and Jan Landwehr for their valuable feedback and suggestions. They are further grateful for helpful comments from seminar participants at the University of New South Wales, Yonsei University, Sungkyunkwan University, Tilburg University, the Indian School of Business, EBS University of Business and Law, Deakin University, Goethe University, and University of Technology Sydney Behavioral Insights Group and the Sydney Analytics Group.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.