Abstract

Healthcare-acquired infections are due to an exposure to pathogens in the hospital setting and tend to occur within 48 h since the admission or within 3 days from the discharge. Nosocomial infections can often be a source of litigation and compensation claims for patient harm. The aim of our study was to compare two different management policies for medical malpractice claims related to healthcare-acquired infections (MMC) adopted in two different tertiary hospitals of Tuscany and Liguria since the year of the choice to fully retain the medico-legal risk. The two endpoints are as follows: i) to compare the operational risk (considered as the resultant of the frequency of MMC, their cost, and the likelihood of economic losses); ii) to verify how much the hospitals would pay if covered by an insurer. The MMC showed different distributions of frequency in the two hospitals, with mean value and variance higher in Florence (FI) than in Genoa (GE). Overall, FI showed a higher mean cost per claim, although the cumulative annual cost was lower, while GE displayed a higher probability of compensation and a more predictable number of events. These differences reflect the impact of the organizational and medico-legal approaches adopted by the two centers.

Introduction

Healthcare-acquired infections are due to an exposure to pathogens in the hospital setting and tend to occur within 48 h since the admission or within 3 days from the discharge.1–3

The most frequent healthcare-acquired infections are related to invasive medical devices such as urinary catheter-associated infections, central line-associated bloodstream infections, ventilator-associated pneumonia, and surgical site infections. 4 The prevalence of nosocomial infections in high-income countries is estimated at around 7.5%, but available data show considerable heterogeneity, with rates ranging from 4.5% to 7.1% in some European countries and the United States.5–8 In Europe, they cause approximately 16 million days of hospitalization and are responsible for 37,000 deaths. 4 Based on Italian Ministerial data (2018, updated 2024), in Italy approximately 430,000 infections occur each year (overall, a healthcare-associated infection occurs on average in approximately 8% of hospitalizations).4,9 The estimated direct costs related to healthcare-associated infections in Europe are approximately 7 billion euros.4,10 The costs are due to morbidity, mortality, increased healthcare costs, and extended hospital stays.11,12 However, they often cause another kind of economic cost for the hospitals, due to medical malpractice claims. 11 Despite it is virtually impossible to detect a single/specific conduct that could have caused an infection, the cornerstone of these claims is usually the fact that up to the 55% of the hospital infections could be prevented through the compliance with all the prevention and control measures. 13

Nosocomial infections can often be a source of litigation and compensation claims for patient harm.

In Italy, the national healthcare system is designed on a regional basis, and each region is free to opt for insurance coverage with different self-insurance retentions (the portion of the compensations that is directly paid by the hospital) or to fully retain the medico-legal risk (and so to directly compensate medical malpractice). 14 Two Italian regions (Tuscany and Liguria) chose—respectively in 2010 and in 2016—to start fully retaining the medico-legal risk interrupting the respective insurance coverages. Regions are free to adopt specific management policies, as well. The most important challenge to medico-legal claims management from an economic point of view is given by the medical malpractice claims related to healthcare-acquired infections (MMC). 15

The aim of our study was to compare two different management policies for MMC adopted in two different tertiary hospitals of Tuscany and Liguria since the year of the choice to fully retain the medico-legal risk. The two endpoints are as follows: i) to compare the operational risk (considered as the resultant of the frequency of MMC, their cost, and the likelihood of economic losses); ii) to verify how much the hospitals would pay if covered by an insurer.

Materials and methods

General

We collected medical malpractice claims data from two university hospitals in Italy (Careggi University Hospital in Florence, Tuscany—FI—and S. Martino University Hospital in Genoa, Liguria—GE) from the year of the implementation of management policies for MMC (2010 in FI and 2016 in GE) to the end of the first trimester of the 2022 (when the SARS-CoV-2 pandemic was declared ended in Italy). Over these periods, the adopted policies were as follows: in FI MMC were managed by a committee composed of hospital experts in legal medicine, tort law (loss adjusters and/or lawyers), risk management, and prevention and control of infections. Instead, in GE, MMC were evaluated by two separate in-hospital committees: at first, a committee analyzed the infectious aspects (i.e. probability that the infection was actually acquired in healthcare, failures in prevention and control procedures) and then another committee (with experts in legal medicine, in hygiene and preventive medicine and lawyers) was involved and the decision to reject the claim or propose an out-of-court conciliation solution was made.

The MMC variables of interest were as follows: year of the incident, year of the claim (for closed MMC), time required for administrative closure (i.e. judicial/extrajudicial compensation, rejection not followed by further actions, successful defense in civil proceedings), involved medical specialty, and amount of compensation. To allow a proper economic comparison, the cost of the MMC (i.e. paid judicial or extrajudicial compensation) was adjusted for time-sensitive factors like inflation using the coefficients of the main Italian tables used for compensation of medical malpractice claims, as already done in previous Italian studies. 16

Our study cohort encompasses all cases of nosocomial infections for which compensation was sought from the corresponding hospital structures. We included bacterial, viral, and fungal infections without restrictions regarding patient age or the specific type of infection. Cases where compensation was not pursued were excluded from the analysis.

Statistical analysis

The two endpoints of our study have two different statistical methodologies.

Endpoint 1—To perform an operational risk analysis, we evaluated three components: MMC frequency distribution—F, the likelihood of judicial or extrajudicial compensation before the administrative closure—L, and the adjusted cost of the MMC—C. These three components are random variables, and then they were adjusted through normalization for structural and scale-related variables (number of beds, annual admissions, annual surgical case volume), regulatory measures that may have affected risk levels, and risk control strategies adopted by the institutions involved. To model F, the mean and variance of the historical series of observed cases were compared, opting for a Poisson distribution when the variance is less than or equal to the mean, while choosing a negative binomial distribution when the historical variance significantly exceeds the mean. L was calculated as the ratio, ranging between 0 and 1, between compensated MMC and the total number of closed cases. Regarding C, decision trees with the economic impact of the single events as target variables were developed through JMP (V. 18, JMP Statistical Discovery LLC) to evaluate which variables had the highest economic impact. The mean time between the incident occurrence and the MMC and between the MMC and the administrative closure was also noted. The difference in means was tested through student's t-test, conducted under both the equal and unequal variance assumptions.

Endpoint 2—To infer on the distribution of possible annual losses, the first step was a best-fitting analysis through the Anderson-Darling test, comparing the distribution function of the candidate model and the empirical distribution function derived from the sample data. After that, the convolution of the distribution of frequency (defined by the yearly number of MMC) and the economic cost of each event. Convolution analysis was performed via Monte Carlo Simulation (using Python packages—NumPy, SciPy, Pandas, Matplotlib, xlsxwriter) to approximate the full distribution of possible annual losses.

Results

Descriptive data

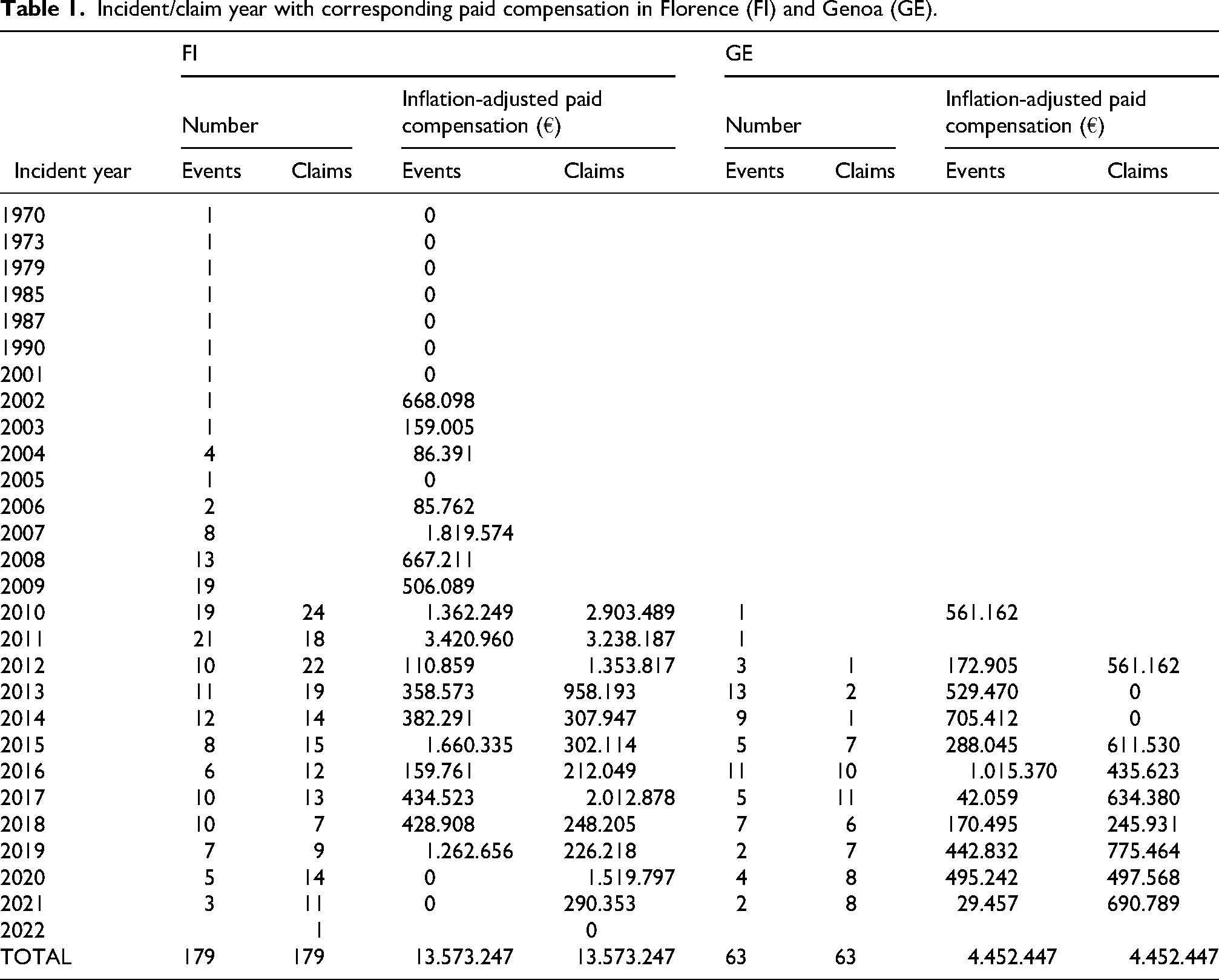

Claims/incidents and relative economic cost are described in Table 1

Incident/claim year with corresponding paid compensation in Florence (FI) and Genoa (GE).

Fields considered in the database were as follows: incident date, claim date, closure date, claim status, paid amount, and involved specialty.

In FI, in the study period, we found 179 closed MMC: in 64 of them, the hospital accepted the claim, in 25, the patient desisted, and in 90, the claim was rejected. When the claim was rejected, in 25 cases, the following civil proceeding ended with compensation.

In GE, in the study period, we found 63 MMC. In three cases, the two committees’ decisions were discordant (the main committee admitted the claim in two cases and rejected it in one case). There were 38 admissions, 24 rejections, and a desistance. When the claim was rejected, in 15 cases, the following civil proceeding ended with compensation.

Statistical results

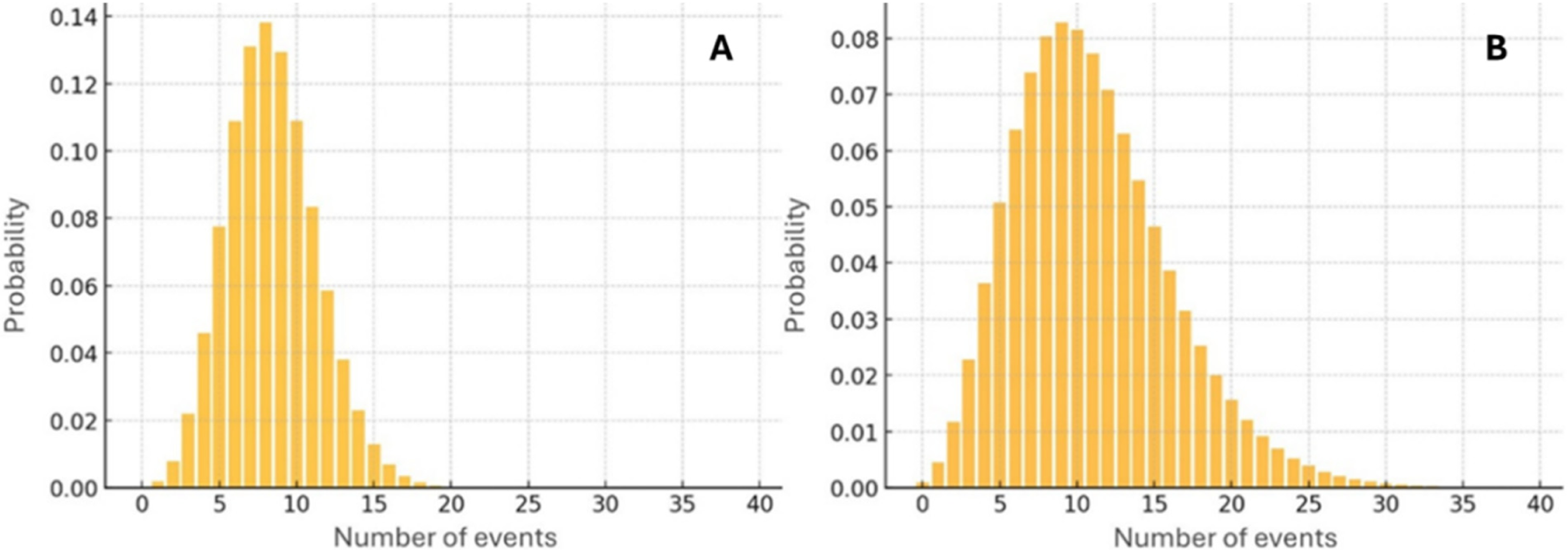

Endpoint 1—in FI, F was described by a negative binomial distribution with a mean of 11,0 events and a variance of 26,0, while in GE it was described by a Poisson distribution with a mean/variance of 8,4 events (Figure 1)

Frequency distributions in GE (A) and in FI (B). Figures relate the number of events to the probability that in a year the number of events actually falls into the ranges of events represented by the orange rectangles.

L was of 0,51 in FI and 0,69 in GE. The mean adjusted cost of MMC was 149.157 € in FI and 123.679 € in GE with most of the MMC belonging to 10.000-300.000 € cost area. Involved medical specialty and the time required to administratively close the claim were found to be the most impactful variables on C. In detail, medical specialty as an aggregated variable was found to be significant, while the relatively small samples did not allow relevant analysis for specific specialties. The mean time between the incident occurrence and the MMC was of 3,56 years in FI and of 2,18 in GE, while the mean time between the MMC and the administrative closure was of 2,09 years in FI and of 3,33 in GE. The differences in both couples of mean values were found to be statistically significant with Student's t-test.

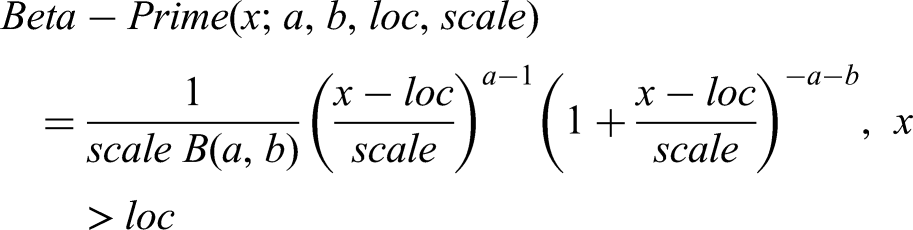

Endpoint 2—following the Anderson-Darling test, the best-fitting distribution for FI was as follows:

Where:

s = 1.6970 (shape)

loc=1874.0 (position parameter)

scale=37022 (scale parameter).

Instead, the best-fitting distribution for GE was as follows:

Where:

a = 0.855980 (first shape parameter)

b = 1.83950 (second shape parameter)

loc=−485.020 (position parameter)

scale = 149994 (scale parameter).

GE distribution showed a higher probability for intermediate impact, whereas FI had a fatter tail for very high impacts.

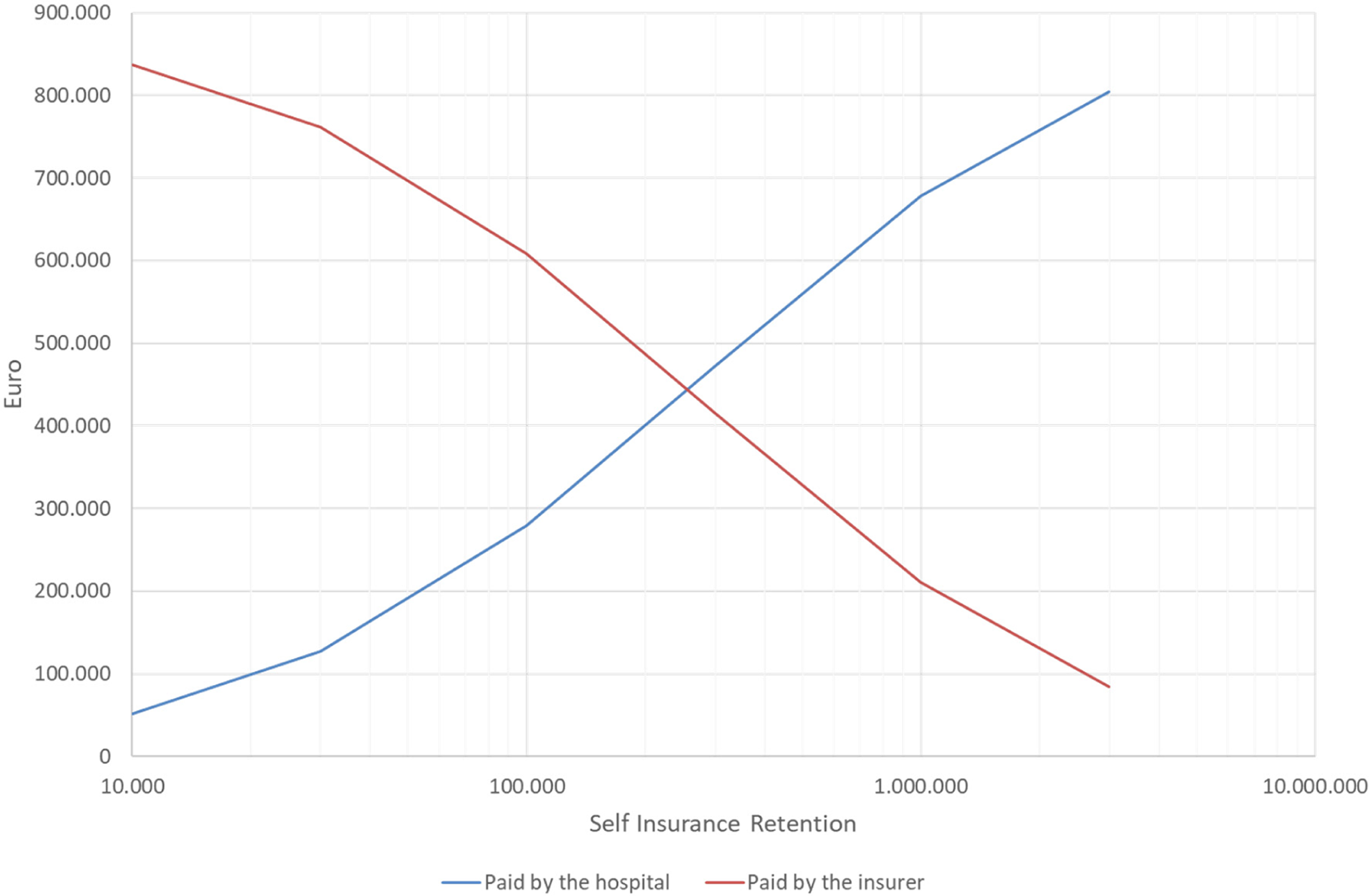

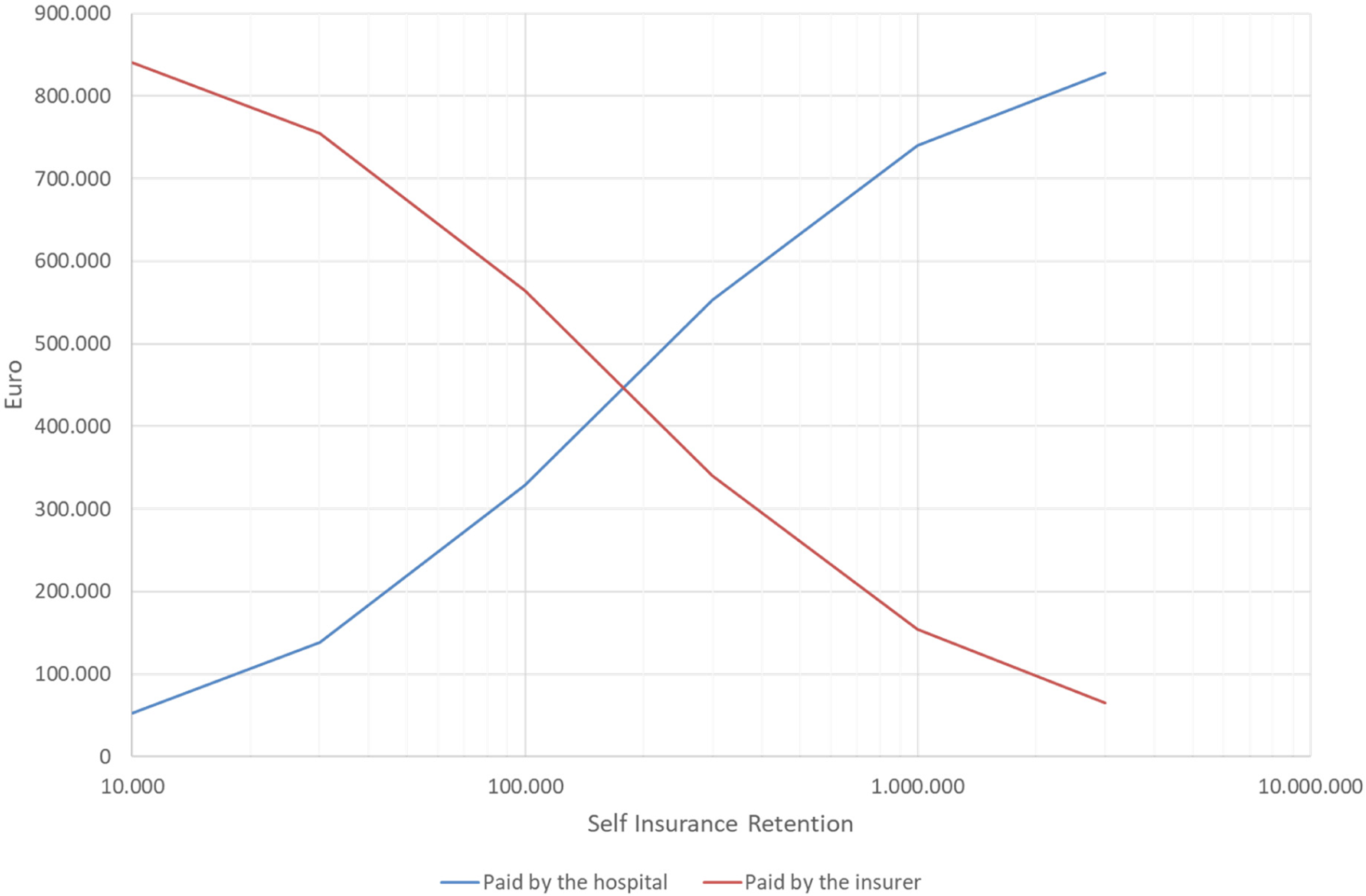

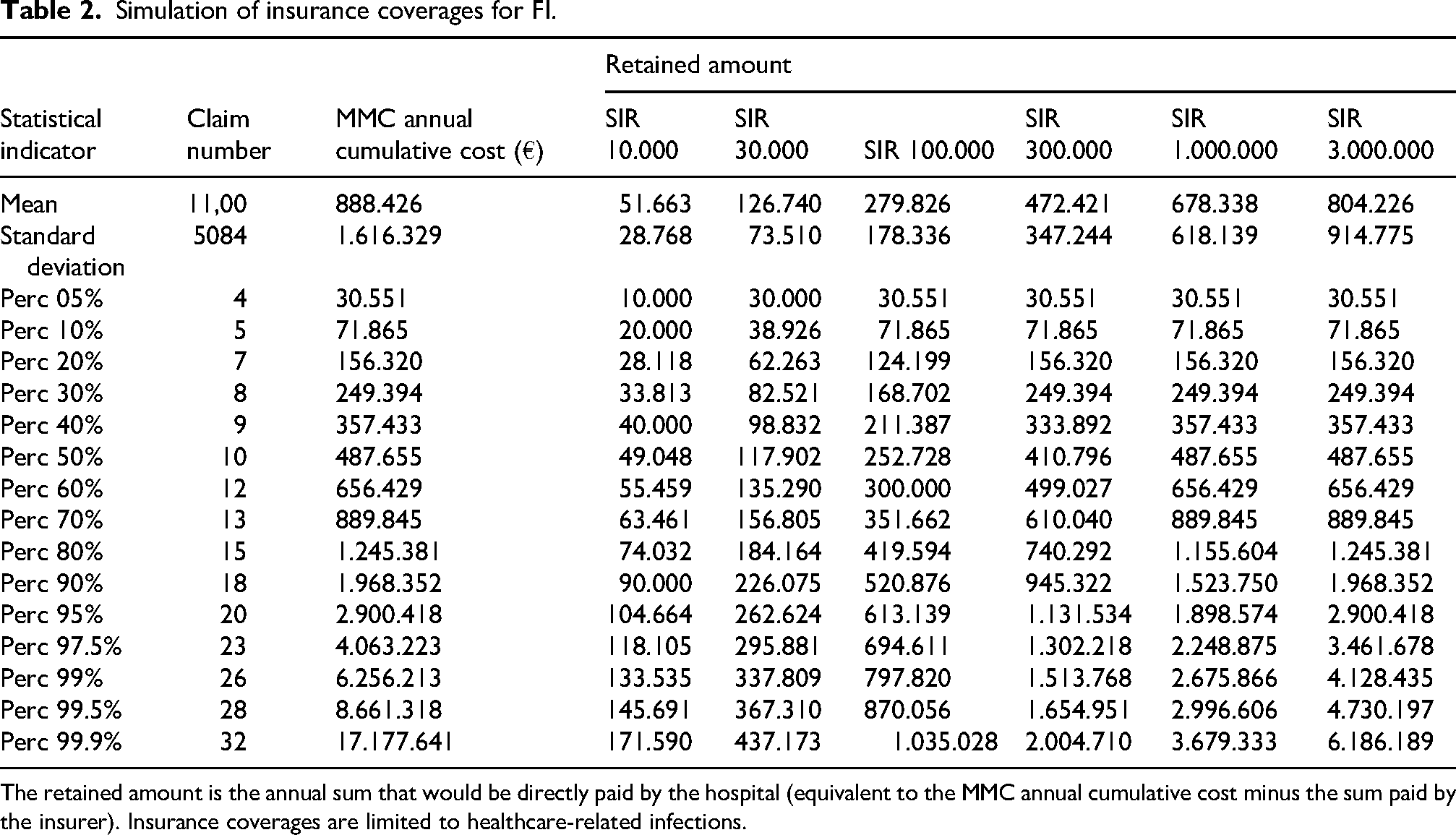

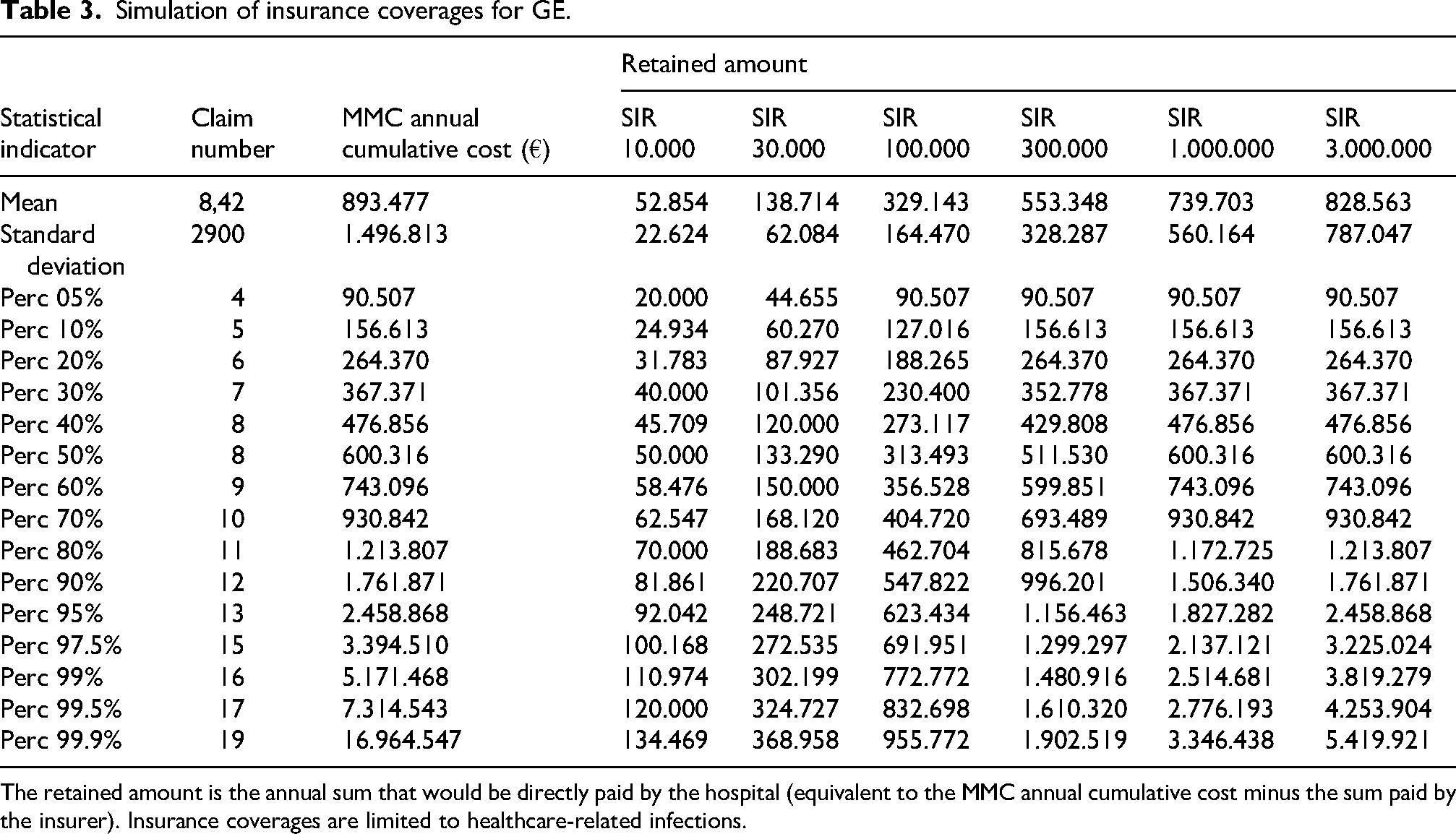

The simulation of how much money the hospitals should pay to yearly compensate the annual amount of claims is shown in Tables 2 and 3 and in Figures 2 and 3, varying with the SIR adopted for insurance coverage. Instead, the cost sustained directly by the insurer is given by the annual cumulative cost of the MMC minus the cost retained by the hospital.

Sums yearly paid the hospital vs paid by the insurer (varying with the SIR) in the insurance coverage simulation for FI. Insurance coverages are limited to healthcare-related infections.

Sums yearly paid the hospital vs paid by the insurer (varying with the SIR) in the insurance coverage simulation for GE. Insurance coverages are limited to healthcare-related infections.

Simulation of insurance coverages for FI.

The retained amount is the annual sum that would be directly paid by the hospital (equivalent to the MMC annual cumulative cost minus the sum paid by the insurer). Insurance coverages are limited to healthcare-related infections.

Simulation of insurance coverages for GE.

The retained amount is the annual sum that would be directly paid by the hospital (equivalent to the MMC annual cumulative cost minus the sum paid by the insurer). Insurance coverages are limited to healthcare-related infections.

Discussion

In our paper, we analyzed how different management policies for MMC can impact on the operational risk. Composition of the committees addressing these claims is relevant because the study of these incidents is particularly complex, due to the fact that hospitals must verify their compliance with every policy that may concern the prevention and control of infectious diseases and, at the same time, verify the correctness of the diagnostic and therapeutic process. 4 Hence, a multidisciplinary approach is usually advocated. 11

In Italy, civil defense in these cases is extremely complex because it should be proven that all the policies concerning the prevention and control of the infections have been actually applied. MMC compensations represent a sort of “double cost” for healthcare institutions that invest significant resources in policies of disinfection, and antibiotical stewardship and control of antibiotical resistance that are public health issues.16,17

The MMC showed different distributions of frequency in the two hospitals, with mean value and variance higher in FI than in GE. These findings have not a direct explanation, merely describing the trends in MMC in two different regions, with a downward trend in FI between 2010 and 2015 before stabilization in 2016 and a substantially stable trend in GE. In general terms, in all Western countries, medical malpractice claims incidence tends to gradually decrease over time, while the costs tend to increase.18,19

Our data shown in Figure 1 suggest that the higher variance in FI makes it harder to predict the probability of having a set number of events in a year and then a proper preparedness from both a management and economic point of view. The probability of compensating a claim in the judicial or extrajudicial setting was higher in GE than in FI (0,69 vs 0,51), with about a half of MMC ending without economic loss in FI. Indeed, the probability of paying these claims is reported as high in scientific literature, mainly because of the difficulty of the hospital to prove full and actual compliance with all the measures of infections’ prevention and control.15,16

Similar findings have been reported in other healthcare systems. In the United Kingdom, Goldenberg et al. 20 analyzed litigation data from the National Health Service and demonstrated that healthcare-associated infections represent a substantial proportion of clinical negligence claims, often resulting in compensation when hospitals cannot fully demonstrate adherence to evidence-based infection-control measures. Their conclusions mirror the challenges observed in our study, confirming that HAI-related litigation consistently exposes institutions to a high medico-legal risk across different countries.

In our cases, the mean adjusted cost of MMC was higher in FI as well (149.157 € in FI and 123.679 € in GE). In both hospitals, C mainly fell inside the 10.000-300.000 € cost area, with the involved medical specialty and the time required to administratively close the claim as the most impactful variables on C. Instead, regarding the time required for administrative closure, the FI management policy (MMC addressed by a single multidisciplinary committee) was associated—in a statistically significant fashion—with a shorter time (- 40%) required to close the case. The shorter time required and the lower probability of compensating a claim in FI may explain why the annual cumulative cost is lower even if the mean adjusted cost of MMC is higher.

Regarding the strongest determinants of the claims cost, it is clear that a time-effective management of a MMC is crucial to contain the costs, for instance avoiding—when possible—(long) judicial proceedings. 21 However, despite in our study the single-committee policy has performed better in this sense, the time required for closure was higher in both institutions than that reported by institutions in other countries. Comparable medico-legal patterns have been described in other European jurisdictions. An analysis of court decisions in Poland by Zieliński et al. 22 showed that healthcare-associated infections constitute a recurrent basis for liability, with courts increasingly requiring hospitals to provide detailed evidence of infection-prevention systems and compliance with infection-prevention and control protocols. When such documentation is incomplete or inconsistent, compensation is frequently awarded. These findings reinforce the relevance of robust organizational structures and traceable decision-making processes in mitigating the legal and economic impact of HAI-related claims.

On the other side, in our cases, the role of the medical specialty may be explained by the fact that the risk of infection is higher when the patient are immunosuppressed and/or require long stays, mechanical ventilation support, indwelling devices, and intravenous antibiotics (that are relatively common—for instance—in intensive care units).23,24 At the same time, surgical site infections are often indicated as the most frequent healthcare-related infections, and they tend to mostly concern orthopedic, cardiac, and intra-abdominal surgery. 25 From a practical perspective, being the medical specialty is an independent predictor of higher economic loss, the hospitals should consider convenient to implement data-driven policies like targeted audits or specific training programs for high-risk departments.

The association between high-risk specialties and litigation related to healthcare-associated infections has also been documented internationally. In a nationwide analysis of malpractice judgments in South Korea, Park et al. 26 found that surgical site infections represented a leading cause of litigation in surgical disciplines, with compensation frequently awarded when perioperative infection-prevention measures were judged insufficient. These findings align with our results, suggesting that specific clinical areas inherently carry higher medico-legal vulnerability in the context of HAIs.

As a secondary endpoint, we investigated the economic profiles of different insurance coverages (corresponding to different SIRs) for the two institutions. In literature, the economic sustainability of insurance coverages with high SIRs has already been investigated, but for general medical malpractice claims. 16 A high-SIR insurance coverage tends to protect the institution from excessive economic exposure but still allows the hospital to monitor and directly manage claims and incidents and to evaluate the impact of its policies 16 As said, in FI the number of events in a specific year is harder to predict than in GE, but the MMC annual cumulative cost in FI is lower than in GE. This finding suggests that the single-committee approach relates to a lower operational risk and then, in case of insurance coverage, it should bring to lower prices. Indeed, premium pricing is set primarily considering the MMC annual cumulative cost and the opted SIR, although a significant variability is also due to the fact that the price is usually negotiated. 27

Conclusions

Regarding healthcare-related infections, in tertiary university hospitals completely retaining the medico-legal risk, a management model based on a single, multidisciplinary decisional committee proved to impact on costs scoring both a higher proportion of claims closed without economic losses and a shorter time for the administrative closure, even when the actual medico-legal risk is particularly difficult to predict. As shown by our actuarial simulation, this model is also related to a lower MMC annual cumulative cost and thus to lower premiums. Medical specialty was confirmed to be an independent economic risk factor, that can be addressed by tailored risk management programs in high-risk departments (like intensive care units). In our opinion, this study creates different perspectives for future research: to enhance the generalizability of the findings, a multicentric study could be promoted, and in future studies, even a prospective design could be adopted to verify if targeting the found relevant factors may improve the hospital policies. Moreover, the same methodology could be used for other types of medical malpractice claims to fully test the effectiveness of different management models.

Limitations of the study

The main limitations of the study are the retrospective design and the reliance on administrative data, which may not capture all the clinical nuances of individual cases. Another limitation, as mentioned in the text, is given by the different observation periods for the two centers, even if the potential impact of this limitation has been contained by the specific adopted methods. However, the comparison between FI (2010–2015) and GE (2016–2022) should be interpreted not only in light of differences in institutional setting, but also in relation to different stages in the maturation of the underlying claims-management framework. The FI window may be viewed as a relative “settling” phase, during which reserving criteria, medico-legal assessment, and settlement practices were still consolidating, whereas the GE window appears to reflect a more mature phase, with more standardized operational and valuation procedures.

Future perspectives

In the future, wider windows from more hospitals could be considered to test the hypothesis. Moreover, operating on bigger datasets, the granularity of the analysis could be enhanced, for instance exploring the specific impact of every single medical specialty. Although the current portfolio-level analysis already provides a robust and methodologically sound representation of the loss process, future work will examine the specialty dimension in order to further improve conditional risk homogeneity. From an actuarial perspective, stratifying the portfolio into clinically more homogeneous specialty groups is expected to bring the data into closer alignment with the key assumptions of the frequency–severity approach. In particular, the homogeneity assumption would be strengthened, since each segment would reflect a more comparable combination of clinical practice, procedural risk, patient complexity, and litigation propensity. Likewise, the assumption that claim severities within each segment are approximately identically distributed would become even more plausible, as the variability attributable to structurally different specialties would no longer be absorbed within a single aggregate distribution. Greater segmentation may also improve the apparent stability of both frequency and severity parameters over time, by reducing the effect of shifts in specialty mix on the overall portfolio. Finally, conditioning the analysis on specialty is expected to attenuate any residual association between claim frequency and claim size that is generated by pooling intrinsically different clinical areas, thereby making the usual working assumption of conditional independence more tenable. In this sense, specialty-based segmentation would preserve the robustness of the current specification while sharpening its actuarial interpretation, improving calibration, and enhancing predictive precision. At the same time, greater granularity inevitably raises a statistical trade-off, since several specialties may generate too few observations to support robust standalone estimation. To improve statistical significance and parameter stability, future analyses will therefore need to assess whether individual specialties should be aggregated into broader groups that remain internally homogeneous from both a clinical and an actuarial standpoint. Such aggregation cannot be specified a priori. It should instead be derived through explicit optimality criteria designed to balance granularity against inferential reliability. These criteria may include maximizing within-group homogeneity and between-group separation in terms of frequency and severity profiles, ensuring adequate exposure and event counts in each class, and identifying the partition that provides the best compromise among goodness-of-fit, predictive performance, and model parsimony.

Footnotes

Author contributions

SG contributed to conceptualization, investigation, writing—original draft, and methodology. MF contributed to investigation. RB contributed to conceptualization, investigation, writing – original draft, and methodology. AC contributed to conceptualization, investigation, writing – original draft, and methodology. IC contributed to investigation and writing—original draft; IB contributed to investigation and writing—original draft; RG contributed to investigation, writing—original draft, and methodology; FV contributed to conceptualization, investigation, writing—original draft, and methodology; VP contributed to conceptualization, investigation, writing—original draft, and methodology.

Funding

The author(s) declare that financial support was received for the research, authorship, and/or publication of this article: The study was funded by the European Union—NextGenerationEU—National Recovery and Resilience Plan, Mission 4 Component 2—Investment 1.5—THE—Tuscany Health Ecosystem—ECS00000017—CUP B83C22003920001.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.