Abstract

Euro Area

The Euro Area remains in recession, with the effects of continuing, though diminishing, fiscal austerity being exacerbated, in the countries of the periphery, by difficult financial conditions. Fiscal drag is expected to be significantly reduced in 2013, with increased attention appropriately being paid by policymakers to progress in reducing structural rather than nominal deficits, and the European Commission accordingly relaxing deficit targets in a number of cases. Output is again projected to fall slightly this year, by 0.4 per cent, before growing in 2014 for the first time in three years, albeit by only 0.9 per cent.

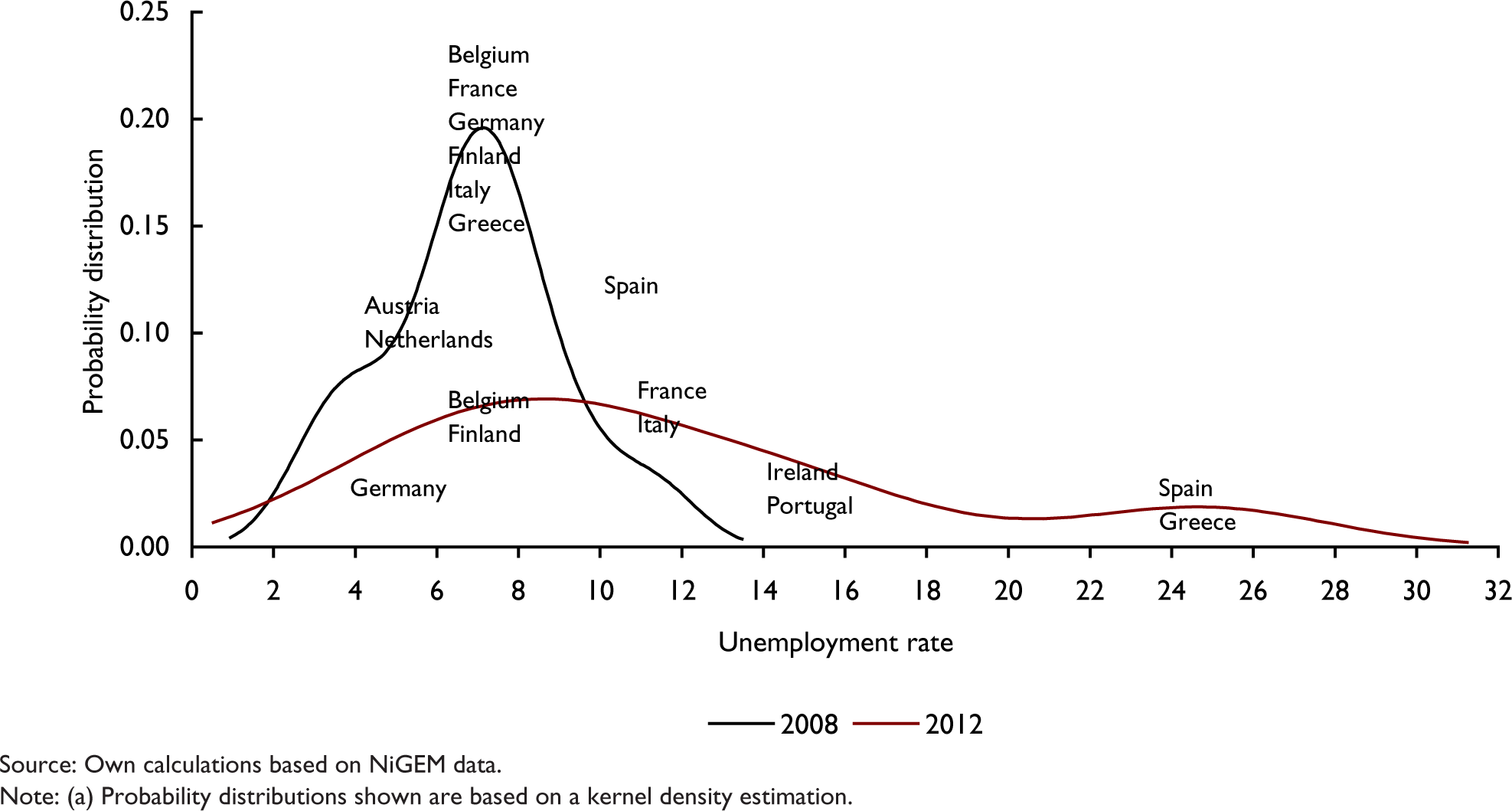

Growth divergences persist among member countries of the Euro Area. Further significant contractions in 2013 are projected for Greece, Italy, Portugal and Spain, while modest positive growth rates are projected for Austria, Belgium, Ireland and Germany. There are also large divergences in unemployment, which have widened significantly since the onset of the crisis. This is illustrated in figure 1; between 2008 and 2012 not only did average unemployment in the Euro Area increase, from 6.9 per cent to 11.7 per cent, but also the difference between the lowest and highest unemployment rates widened considerably, from about 8 percentage points to as much as 20 percentage points.

Distribution of unemployment rates in the Euro Area(a)

Spreads among government bond yields, having narrowed in late 2012 following the ECB's announcement in September of Outright Monetary Transactions, have generally remained compressed. It is particularly notable that yields in Italy have declined further in face of the political uncertainties resulting from the inconclusive elections in late February. The financial crisis in Cyprus, in March, had little immediate impact beyond the country itself. However, the resolution of the crisis involves, for the first time in the crises that have afflicted the Euro Area, the imposition of capital losses on uninsured bank depositors, and it remains to be seen whether this, or even reports of the initial proposal, later abandoned, to impose levies on insured as well as uninsured depositors, will have destabilising effects on the behaviour of bank depositors in the Euro Area.

Despite the narrowing of spreads among government bond yields, financial markets in the Euro Area remain fragmented, with the private sector in the periphery, where there is a considerable overhang of corporate debt, facing inordinately high borrowing costs despite the ECB's accommodative monetary policy. This reflects continuing weaknesses in the financial system and points to the need for further action to clean up banking systems through recapitalisation and restructuring, without weakening the financial positions of the respective sovereigns. Direct recapitalisation of weak banks by the European Stability Mechanism would help the process. Timely progress towards a banking union for the Euro Area, meanwhile, remains essential, to promote the reintegration of financial markets, the delinking of sovereigns from banks, the removal of suspicions of national bias in supervision, and the effective transmission of monetary policy. In March, preliminary agreement was reached among the European Parliament, the Commission, and the Council on the establishment of a single supervisory mechanism (SSM) at the ECB, and draft legislation to this effect is being considered by the Parliament, with the aim of making the SSM operational by mid-2014. Not only may this legislative process be subject to delays, but also the SSM needs to be complemented by a single resolution mechanism for failed institutions, together with a common deposit guarantee scheme, and agreement has yet to be reached on these. Agreement on common rules for bank resolution seems likely to be a particularly difficult challenge, given the role of systemically important banks and the apparent reluctance of economically strong countries to provide the contingent fiscal support that will be needed to underpin the resolution mechanism, even if its primary source of funding will be levies on the banks. In fact, recently reported statements by German officials seem to have rejected a common deposit guarantee scheme ‘for the foreseeable future’, 4 and to envisage only the harmonisation of national deposit guarantee schemes.

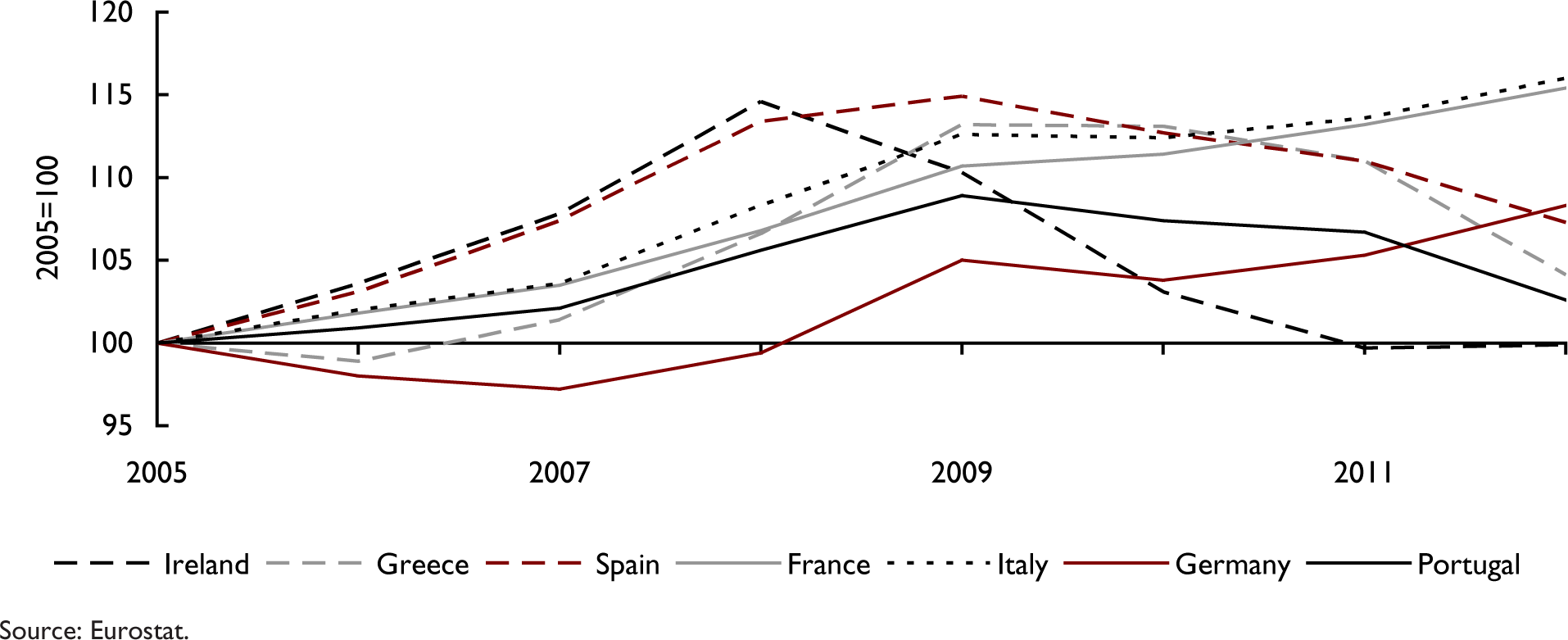

Important among the root causes of the crisis in the Euro Area have been the divergences of international competitiveness and associated payments imbalances that developed in the decade following the establishment of the monetary union. Since the crisis erupted, there has been some slow and painful correction of these divergences, notably through absolute reductions in unit labour costs in the countries that have suffered the most severe recessions (see figure 2). It is unclear, however, to what extent the corrections seen thus far are merely cyclical rather than sustainable, and significant divergences and imbalances remain, notably including Germany's current account surplus, projected to widen further to 7.8 per cent of GDP in 2014. With Euro Area inflation, and inflation expectations, comfortably within or below the ECB's target of ‘below but close to 2 per cent’, there is scope for official interest rates (in particular, the ECB's refinancing rate of 0.75 per cent) to be reduced further; given downward nominal wage rigidities, the moderately higher inflation that this would allow would promote further adjustment of relative costs. Demand and activity in the Euro Area would also be boosted if Germany and other surplus countries with fiscal space would contribute to adjustment through expansionary fiscal measures.

Unit labour costs in selected EU countries

Germany

Our growth projections for Germany in 2013 and 2014 have been revised down slightly, to 0.5 per cent and 1.3 per cent respectively. As in our last forecast, the projection for average growth this year is weighed down by the 0.6 per cent drop in GDP in the last quarter of 2012. We expect activity to pick up moderately in the course of this year, though recent leading indicators have been mixed. The April purchasing managers’ index points to the first decline in private sector business activity since last November, and business confidence has also weakened.

As in 2012, fiscal policy is expected to be broadly neutral this year and next, with the budget close to balance. Given Germany's strong international competitiveness, net trade is expected to continue to make a positive contribution to growth, and this seems likely to increase as the global economy strengthens. A component of domestic demand that is especially buoyant is housing investment. The strong rise in house prices has continued. According to the BulwienGesa AG data for 125 towns and cities house prices rose in 2012 by about 5¼ per cent, and although this index is likely to have exceeded the overall index for Germany (413 towns and municipalities) which will be available at a later date, the picture is consistent with the trend acceleration that can be seen in other price indicators (see Bundesbank, 2013). Housing supply has also been expanding; the construction of apartment blocks has increased significantly. Favourable financing conditions have been stimulating housing demand, which may also have been boosted by capital inflows from the Euro Area's periphery. The increase in borrowing for house purchase, and the pace of increase in prices, have raised questions about the sustainability of the rise in household debt and the possible need for stricter prudential controls, such as loan-to-value ratios.

Unemployment has remained low, at about 5.4 per cent in recent months. In fact, while GDP contracted in the last quarter of 2012, employment rose by 0.1 per cent. The unemployment rate may understate the slack in the economy, however, as the weak growth of labour productivity in recent years, common to much of Europe, may indicate significant potential for greater utilisation of hoarded labour.

France

The French economy has continued to weaken, with unemployment in recent months rising to levels that have not been seen for 16 years (3.2 million, close to 11 per cent of the labour force). After zero growth of GDP in 2012 as a whole and a 0.3 per cent drop in the fourth quarter, INSEE's business climate index points to further deterioration, particularly in the building and services sectors. We forecast a small decline in GDP of 0.2 per cent this year, and only weak growth of 0.5 per cent in 2014.

Significant fiscal consolidation will again weigh on the economy in 2013, for a third successive year. The public sector deficit stood at 4.8 per cent of GDP in 2012, down from 5.2 per cent in 2011 but 0.3 percentage points above the official target. The government revised this year's deficit target from 3.0 to 3.7 per cent of GDP, but reiterated its commitment to structural balance by 2017.

Fiscal adjustment is compressing domestic demand, which is expected to fall by 0.8 per cent this year. Rising taxes, as well as rising unemployment and declining real wages, all point to a continuing decline in households’ real disposable income in 2013, depressing both private consumption and housing investment. Business investment is also set to continue to decline in the short term in the light of poor demand prospects and low margins.

After this year, the pace of fiscal consolidation is set to ease. Public debt is expected to peak in 2014 at about 94 per cent of GDP. The government's target of fiscal balance by 2017 is expected to be revised to a planned deficit of 0.7 per cent of GDP.

Exports have remained sluggish and industrial production has been in decline reflecting France's weak international competitiveness as well as the economic stagnation of its Euro Area trading partners. A revival of growth in France will depend not only on further progress towards sustainable public finances and economic recovery in the Euro Area but also on reforms to tackle the country's competitiveness challenge, including reforms in the labour market.

Italy

After six consecutive quarters of GDP decline, and a 2.4 per cent drop in 2012 as a whole, Italy's economic outlook for 2013–14 remains weak and uncertain. The inconclusive outcome of the February general election and the ensuing two-month political deadlock added to policy uncertainties, although government bond yields have fallen further, to about 4 per cent at the 10-year maturity, along with those of other sovereigns.

Short-term indicators point to a further decline in economic activity this year, though milder than in 2012. Our forecast suggests a fall in output of 1.3 per cent in 2013 – larger than the 0.9 per cent drop we projected last time – with a slow recovery from 2014, assuming that the new government makes further progress in tackling the country's fiscal and structural challenges. Markets welcomed the news in late April of the formation of a new government, driving government borrowing rates down to historical lows, and also boosting the stock market.

Yet, continuing fiscal consolidation this year, rising unemployment (11.6 per cent in the first quarter this year) and falling real disposable income are weighing heavily on consumer spending, while both business and housing investment continue to weaken, partly as a result of high borrowing costs. As a result, domestic demand is expected to fall by a further 2.4 per cent this year and inflation (as measured by the private consumption deflator) to soften to 2.1 per cent. Net exports will continue to be the only component of aggregate demand to make a possible contribution to growth.

The Italian government's Economy and Finance Document for 2013, issued in April 2013, called for pro-growth policies, starting with a one-off package of measures aimed at injecting liquidity (¢40 billion over 2013–14) into the economy by speeding up payments in arrears owed by general government bodies to the private sector. The planned net borrowing target for this year is set at 2.4 per cent of GDP, down from 2.9 per cent last year. A reduced pace of fiscal adjustment next year should assist a slow recovery, and the new Prime Minister has urged for a further easing of austerity.

Spain

Spain's recession is expected to continue this year as a result of further fiscal adjustment, downward pressure on wages in the very weak labour market, and further deleveraging by what remains one of the most indebted private sectors in the EU. We are projecting a larger GDP fall in 2013 (1.8 per cent) than in 2012 (1.4 per cent) but the pace of contraction is expected to moderate over the course of this year. Output is expected to stabilise in 2014, which should see modest average growth of about 0.2 per cent.

In the first quarter of 2013, unemployment rose above 6 million (27 per cent) for the first time. Moreover, it seems unlikely to have reached its upper limit. About half of those who have become unemployed since the start of the crisis worked in the construction sector, where employment declined from over 2.7 million at the end of 2007 to about 1.0 million at the end of 2012. The continuing decline in housing investment and house prices is expected to erode employment in the sector further.

Despite the economic recession, the government broadly implemented its sizeable fiscal consolidation plan in 2012, although it missed the deficit target by a narrow margin. The fiscal deficit, including support for the financial sector (equivalent to 3½ per cent of GDP), widened to 10¼ per cent of GDP from 8½ per cent in 2011, but the cyclically adjusted deficit was reduced by close to 3 per cent of GDP. Furthermore, as in other countries of the Euro Area, financial market stress indicators in Spain have improved since late 2012, and Spain's 10-year government bond yield has declined to below 5 per cent recently. This helped the Spanish government raise nearly 35 per cent of its medium- and long-term funding needs for 2013 in the first three months, January to March.

Since the start of the crisis unit labour costs in Spain have declined by more than in any other Euro Area country except Ireland. Reflecting the resulting improvement in competitiveness, Spain's exports to destinations outside the Euro Area have been growing, and increasing net exports are expected to contribute positively to growth this year and next. The external current account, which was in deficit to the tune of 5 per cent of GDP in 2009, is expected to be roughly in balance in 2014.

Central and Eastern Europe (EU8+2)

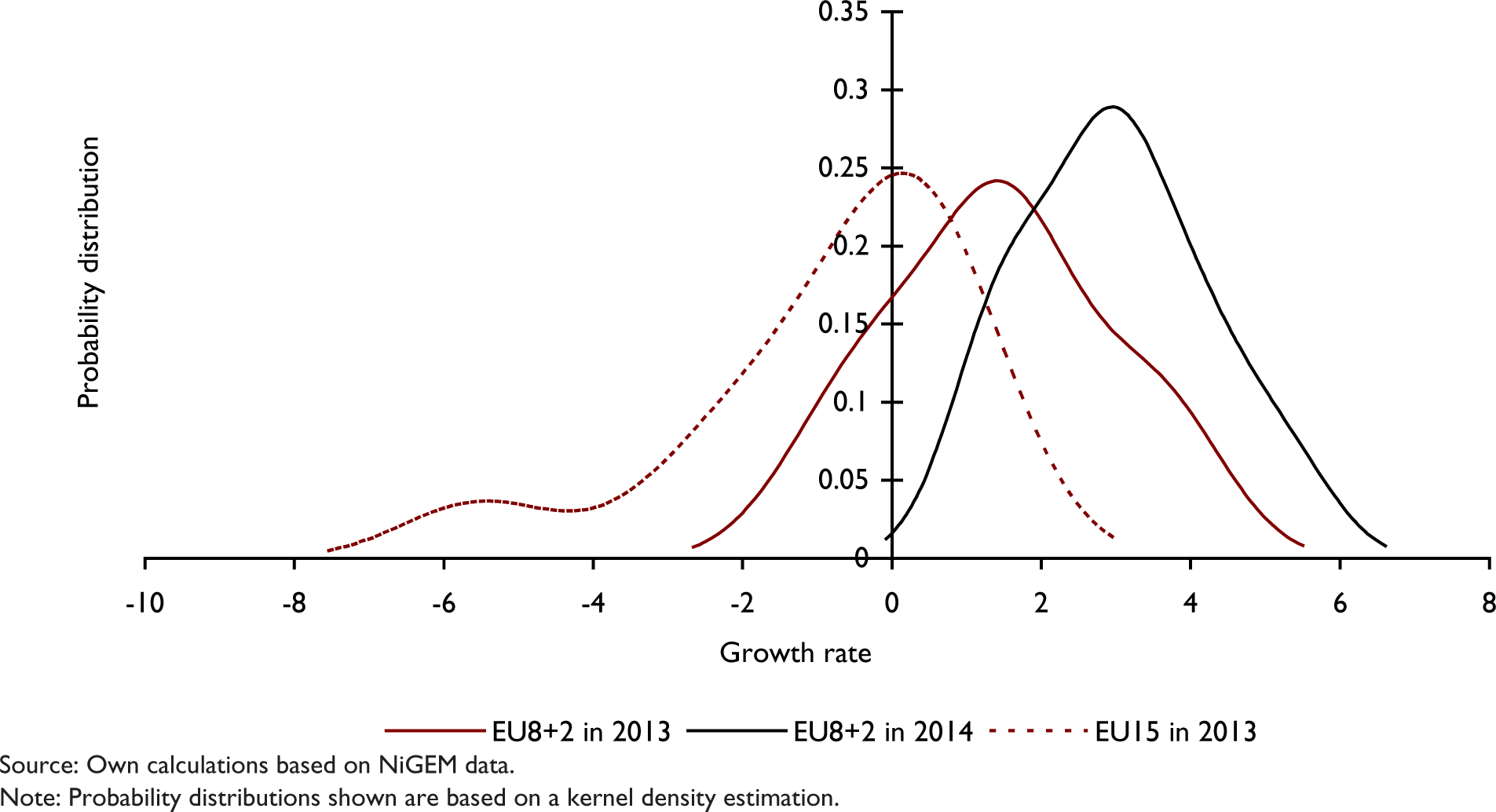

The countries of Central and Eastern Europe have continued to be affected by spillovers from the financial crises and recession in the Euro Area, not only through trade but also through tighter external financing conditions and reduced funding by western European banks for their subsidiaries in the region. Domestic policy tightening has also weighed on demand and activity in several cases. As a result we maintain the view that growth in the EU8+2 block will decelerate this year. A moderate recovery may materialise throughout the region next year. figure 3 shows the expected distribution of growth rates across the region in 2013 against the background of the EU15 countries’ expected growth rates in 2013, and forecasts for the EU8+2 region for 2014.

The distribution of GDP growth rates in the EU8+2

The Czech Republic, Hungary, and Slovenia fell back into recession in 2012, and a further decline in output is projected this year for Slovenia, which has been experiencing financial pressures (discussed below). The economic situation in Hungary reflects high levels of debt in both the public and private sectors, and also the damaging effects on confidence of political developments. These countries seem unlikely to see significant positive growth until 2014. Among the other countries in the group, Latvia is the only country that did not experience an economic slowdown last year, although the other Baltic countries managed to maintain growth in the 3–3½ per cent range. Growth in the Baltics is projected to continue at a relatively high rate, although output is projected to remain significantly below potential. In Bulgaria, Poland, Romania, and Slovakia, growth seems likely to remain below par this year before recovering in 2014. In Poland, the largest country in the region, growth is being held back this year by low external demand and further declines in EU-funded public investment.

One of the factors behind diverging growth in the region remains the situation of the banking sectors. Recently Slovenia has faced particular difficulties, which have been compared to those of Cyprus. However, there are important differences. In particular, Slovenia is not a tax haven, and financial services represent a much smaller part of its economy; banking sector assets amount to less than 1.5 times Slovenia's annual GDP, compared with 8 times in Cyprus before its crisis. The Slovenian authorities have acknowledged that reforms are needed, in the banking sector and in the economy more broadly, but intend to address these issues without external assistance.

United States

In the United States, the economic recovery, though still tepid overall, has become noticeably stronger than in most other advanced economies, thanks partly to substantial progress in repairing the financial system and in improving households’ balance sheets. Thus, for example, the ratio of households’ debt service payments to personal disposable income, in the fourth quarter of 2012, was about 40 per cent below its pre-crisis peak, and lower than at any time since the early 1980s.

This progress, spurred by the Federal Reserve's expansionary monetary policies, including its purchases of mortgage backed securities, has been reflected in a pick-up in credit growth, a significant strengthening of the housing market, and a recovery in construction activity, with housing starts rising sharply to levels, in March, that were the highest since mid-2008. There has also been some broader strengthening in private sector demand, and in output and employment, but these developments have been considerably more hesitant and less clear, and, as in our last forecast, GDP growth is projected to be about 2¼ per cent per annum in both 2013 and 2014.

This tepid pace of economic recovery is accounted for in large part by contractionary fiscal policy. The structural fiscal deficit was reduced by 1¼ per cent of GDP in 2012, and a larger adjustment, of 1¾ per cent of GDP, is projected for this year. The fiscal cliff was avoided at the beginning of the year, but the measures taken to resolve that dispute – especially the expiration of a reduction in payroll taxes – are restraining demand. In addition, the sequester, which began in March in the absence of a budget agreement, and which imposes significant spending cuts on a wide range of programmes, is expected alone to reduce GDP growth in 2013 by about ½ a percentage point if maintained until the end of the fiscal year. 5

The current pace of fiscal tightening is clearly excessive given the weakness of the recovery, but major budget uncertainties remain. In the short term, agreement on the debt ceiling will need to be reached by mid-year. And to establish control over the debt path in the medium term, agreement will need to be reached on entitlement reforms and other much-needed measures, including reform of the tax system. Our projections assume further fiscal tightening measures, amounting to about 1 per cent of GDP, in 2014, in line with current policy plans, with more moderate consolidation of about ½ per cent of GDP per annum over the medium-term horizon.

Current and prospective fiscal headwinds point to a continuing need for easy monetary policy for some time. The projections suggest that although strengthening growth may provide some scope for reducing the pace of quantitative easing later this year, unemployment is unlikely to fall below the Federal Reserve's 6.5 per cent intermediate threshold for an increase in official interest rates to take place early in 2015.

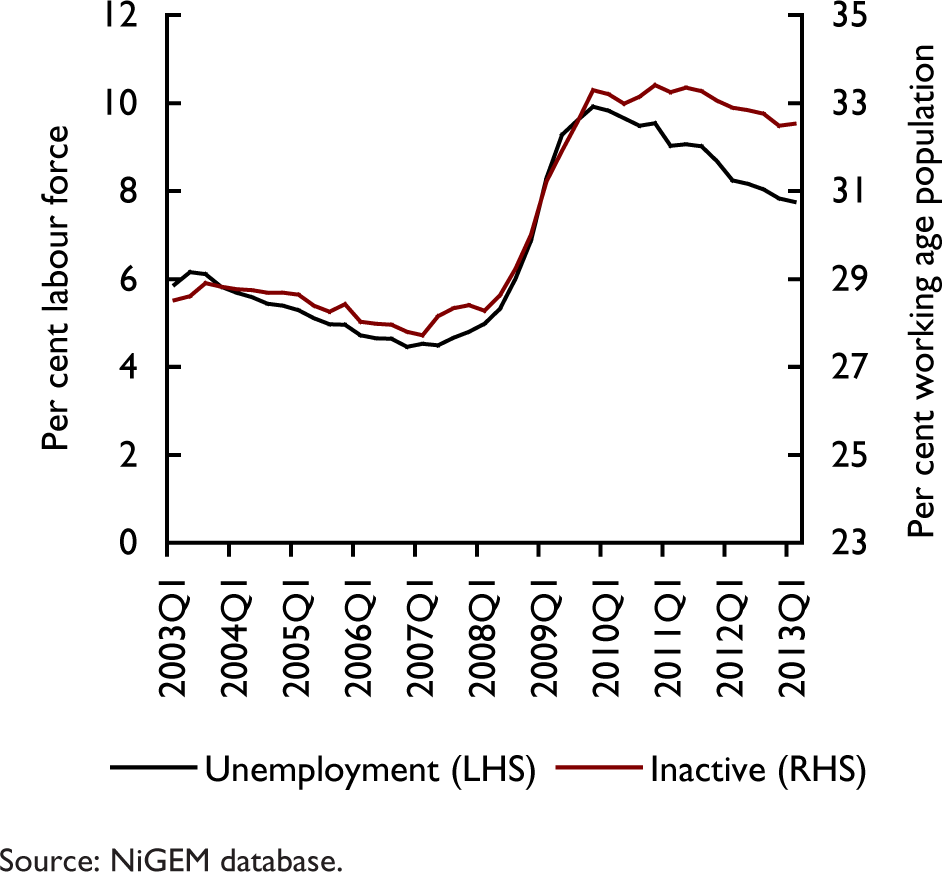

There are downside risks to the forecast of the unemployment rate, given the large pool of inactive working-age individuals. Since 2007, the labour force participation rate has declined by more than 2 percentage points, equivalent to a withdrawal of 4½ million workers from the labour force. While the observed unemployment rate has declined by 2.4 percentage points since its peak in 2009, the inactivity rate has declined by just 0.8 percentage points (see figure 4).

United States: unemployment and inactivity rates

If the rebound in the housing market encourages some inactive participants to re-engage with the labour force, the unemployment rate may recede more gradually than currently forecast. However, this would be a welcome development in the US labour market, as the recovery in labour force participation would have a long-run positive impact on the productive capacity of the US economy.

Canada

Growth in the Canadian economy, which weakened in 2012 to 1.8 per cent even as the US economy gathered some steam, is projected to slow further this year to 1.6 per cent. Fiscal consolidation, high household debt, and a cooling housing sector are restraining domestic demand. Consumer price inflation, 1.2 per cent in the year ended February, is well below the Bank of Canada's 2 per cent target.

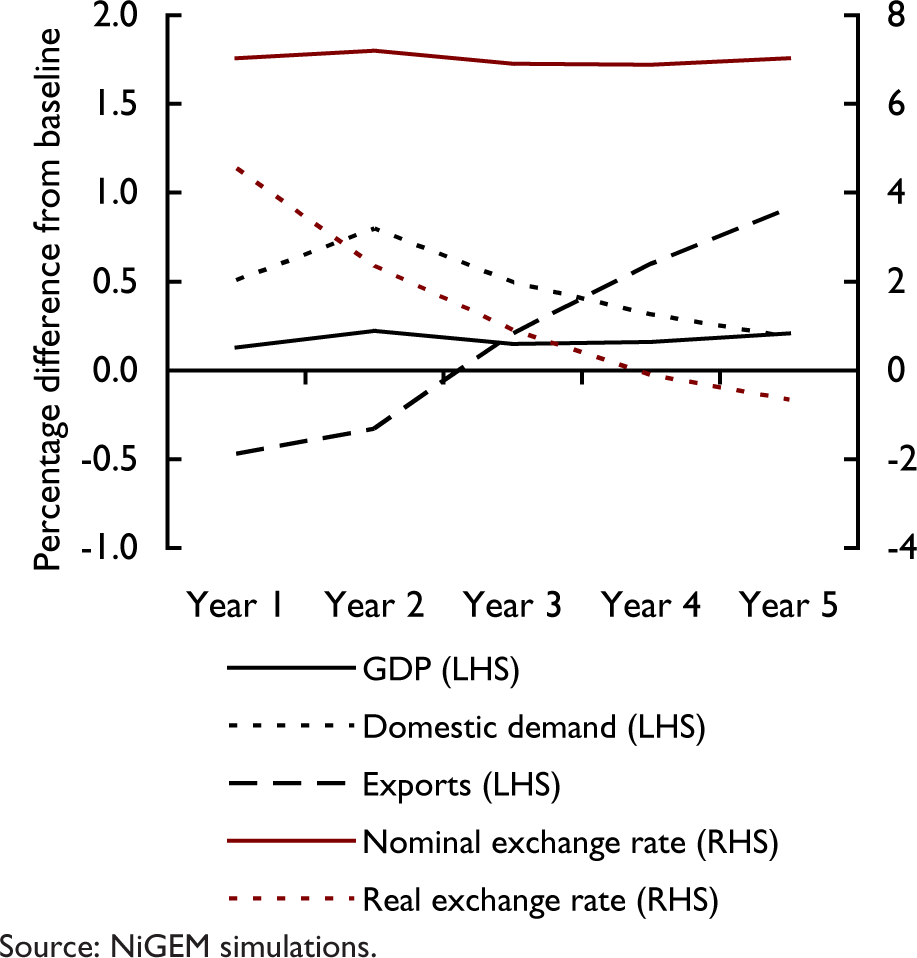

As mentioned in the Overview, a debate has recently emerged about the potential effects of protracted QE by the US Federal Reserve on competitiveness in the rest of the world, including Canada. figure 5 illustrates the expected effects of a monetary loosening by the Federal Reserve on the main Canadian macroeconomic indicators, according to a simulation study using NIESR's model, NiGEM. The analysis suggests that a monetary easing associated with a 5½ per cent effective depreciation of the US dollar would lead to an effective appreciation of the Canadian dollar in nominal terms by about 7 per cent. The effects on competiveness would be short-lived, however, and the real effective exchange rates in both the US and Canada would be expected to return to base within four years.

Impact of QE in the US on the Canadian economy

The expected boost from dampened inflationary pressures and interest rate cuts is projected to outweigh a negative effect from the drop in exports and have a positive impact on GDP in the first year.

Japan

Shifts in recent months by the government elected last December towards more expansionary fiscal and monetary policies have raised short-term prospects for growth and the end of deflation. A supplementary budget worth about 2 per cent of GDP is expected to stimulate the economy over 2013–14 together with the recently announced ‘new phase of monetary easing’ by the Bank of Japan (BoJ), which aims to raise inflation from negative levels to 2 per cent per annum in two years. The BoJ intends to double the monetary base over the next two years by purchasing long-term bonds, thereby both expanding its asset holdings (‘quantitative easing’) and lengthening their average maturity (‘qualitative easing’). These measures have in recent months contributed to a depreciation of the yen of about 17 per cent in effective terms and to a rise in the Japanese stock market to levels not seen since 2008.

Our current forecast takes these policy measures into account and as a result we have revised up our projections for GDP growth in 2013 and 2014 to about 2 per cent per annum, from projections of 0.6 and 1.4 per cent, respectively, three months ago. We allow for fiscal stimulus of around 1 per cent of GDP in both 2013 and 2014. Japan's fiscal multipliers are relatively high (see Barrell et al., 2013), and this raises growth by about 1 percentage point this year and about ½ percentage point in 2014. The remaining improvement in the growth outlook for this year (about ½ percentage point) is related to the aggressive monetary easing, which has driven a depreciation of the exchange rate, a fall in long-term interest rates and a rise in equity prices.

Longer-term prospects for growth and financial stability in Japan will depend both on the formulation of a concrete plan for medium-term fiscal consolidation and on the implementation of structural reforms to raise trend growth. Without a credible medium-term consolidation plan, the government's stimulus measures may put upward pressure on long-term interest rates, which would threaten debt sustainability. The government's plans for structural reforms are due to be announced in the coming months. An important element of these reforms is expected to be measures designed to encourage greater female participation in the labour force.

China

In China, fears of a ‘hard landing’ have waned. After slowing in 2012, growth seems to have stabilised at an annual pace somewhat above the official target of 7½ per cent, with inflation moderating. But concerns remain about excessive credit growth and financial sector fragilities.

The 7.7 per cent growth of GDP in the year to the first quarter of 2013 was lower than generally expected on the basis of such leading indicators as strong PMI readings and liquidity expansion. The slight slowdown from 7.9 per cent growth in the year to the fourth quarter is accounted for by weaker growth of domestic demand, mainly government-related consumption; external demand contributed positively to growth. We still project GDP growth in 2013 as a whole, at 7.8 per cent, to exceed the official target of 7.5 per cent, on the basis of accommodative monetary policy and strong infrastructure investment.

In the medium term much will depend on success with a range of reforms aimed at restructuring the economy and weaning it off its recent dependence on investment and exports. The growth model that has served the country well over the past decade, resulting in an annual average growth rate above 9 per cent, needs to be changed as it has produced domestic as well as external imbalances and risks to financial stability.

A recent downgrade to China's long-term sovereign credit rating to A-plus from AA-minus by Fitch Ratings was based on concerns about the risks that excessive local government borrowing poses to the economy. Local governments have significantly increased their borrowing since 2008, as part of the stimulus package. In order to avoid balanced budget constraints, they financed investment through creation of financing vehicles, which were mostly land-collaterised bank loans. The worry is over the quality of the majority of these types of loans, as well as the weak state of local government finances. If the central government takes on all the liabilities, including those of local governments, then it is estimated that the government debt to GDP ratio could reach 73 per cent, 6 three times larger than in 2011.

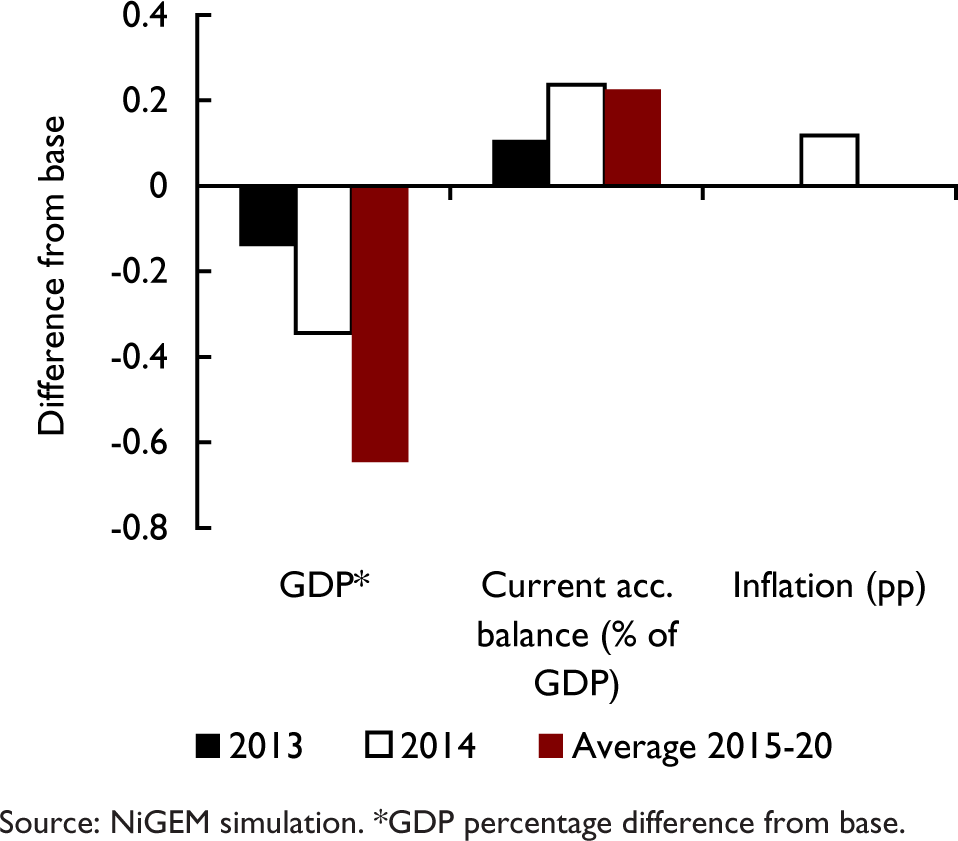

We simulated the effect of tightening bank lending conditions on the Chinese economy using the National Institute's model, NiGEM, by raising the effective cost of private sector borrowing by 1 percentage point permanently. The results of the simulation show that a 1 percentage point increase in borrowing costs (or an equivalent tightening in lending conditions – a qualification that is important given that China's financial system is still heavily regulated) would result in a reduction of potential output in China by about 0.6 per cent in the medium term. For comparison, the magnitude of the impact on GDP in the medium term is about three times as large as that of a similar shock in the US, which is largely explained by China's much higher investment to GDP ratio as compared to the US. There is a limited effect from the shock on inflation, which is not surprising given the regulated financial and monetary system.

Financial sector and social reforms will be necessary to ensure healthy output growth in the medium to long term. In considering medium-term prospects for growth in China, the rate of GDP growth may be decomposed into the growth rates of the working-age population and GDP per head of the working-age population, a close proxy for labour productivity. In recent decades rapid GDP growth in China has reflected rapid growth of productivity – the most rapid among the BRIC economies. This is not surprising given the distance from the global technology frontier of the Chinese economy in the early 1990s. However, if productivity continued to increase at this rate China would be expected to become the new global technology frontier by 2021. This would seem unlikely, and therefore we have assumed a moderation of productivity growth, from an average of 8.3 per cent a year during 1995–2010 to just below 7 per cent a year during 2015–20. By taking into account also a projected decline in the working-age population from 2017, we forecast about 6½ per cent annual trend growth in the medium term.

Effect of 1 percentage point tightening of bank lending conditions in China

Brazil

Brazil has recently been suffering from both weakened growth and increased inflation. Growth fell sharply to 0.9 per cent in 2012 from 7.5 per cent two years earlier, but is projected to pick up to 3.2 per cent this year and 3.4 per cent in 2014, partly in response to the Central Bank's lowering of official interest rates by more than 5 percentage points between late 2011 and late 2012. Private investment is also being boosted by targeted policy measures.

Monetary easing, however, has contributed to a renewed increase in inflation, which in March rose to 6.6 per cent on a twelve-month basis, marginally above the target range of 4.5–6.5 per cent. This, in turn, led the Central Bank to raise its key (SELIC) interest rate in April to 7.5 from 7.25 per cent. Especially given supply constraints – unemployment, at about 5.7 per cent recently, is historically low – it seems likely that further increases in the official rate will be needed to restrain inflation. Fiscal policy is also being tightened in 2013, with the primary budget surplus expected to increase from about 2 per cent to above 3 per cent of GDP. Thus the projections show only a moderate strengthening of growth.

Brazil's external current account balance has moved from modest surplus to modest deficit in recent years as commodity markets have become less favourable. Some further increase in the deficit seems likely in 2013–14 as domestic demand rises relative to export markets.

India

The economic slowdown in India has been more pronounced than forecast, with GDP growth in 2012, at 4.1 per cent, the lowest level in eleven years. Growth is projected to strengthen moderately to 5.3 per cent in 2013 and 6.5 per cent next year, as a result of improving export demand and recent pro-growth policy measures. Significant structural challenges remain to be addressed, however, if the objective of strengthening growth over the medium term is to be achieved.

The recently announced budget for 2013–14 underlined the government's aim of reducing the budget deficit from its recent level of around 8¼ per cent of GDP. 7 However, the planned improvements in the budget rely heavily on a boost to revenues, which is subject to downside risks.

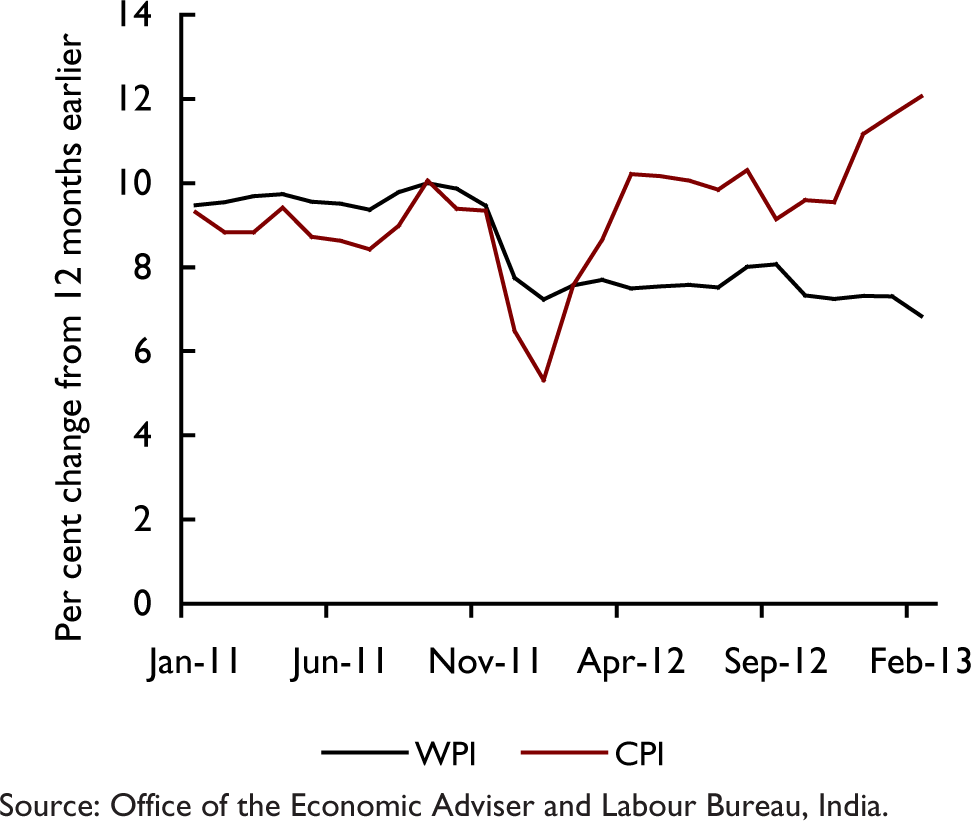

There has recently been an interesting divergence between two of the main inflation indicators, with inflation as measured by the Wholesale Price Index (WPI) easing, while inflation in terms of the Consumer Price Index (CPI) has continued to rise (figure 8). While the explanation for the divergence is not entirely clear, it seems likely that prices in the WPI tend to be flexible prices that are relatively sensitive to market forces, while the retail prices in the CPI tend to be administered and more sticky. The WPI may in some respects provide a better guide to inflationary pressures in the economy, suggesting that the Reserve Bank of India may have more room for monetary easing than CPI inflation suggests.

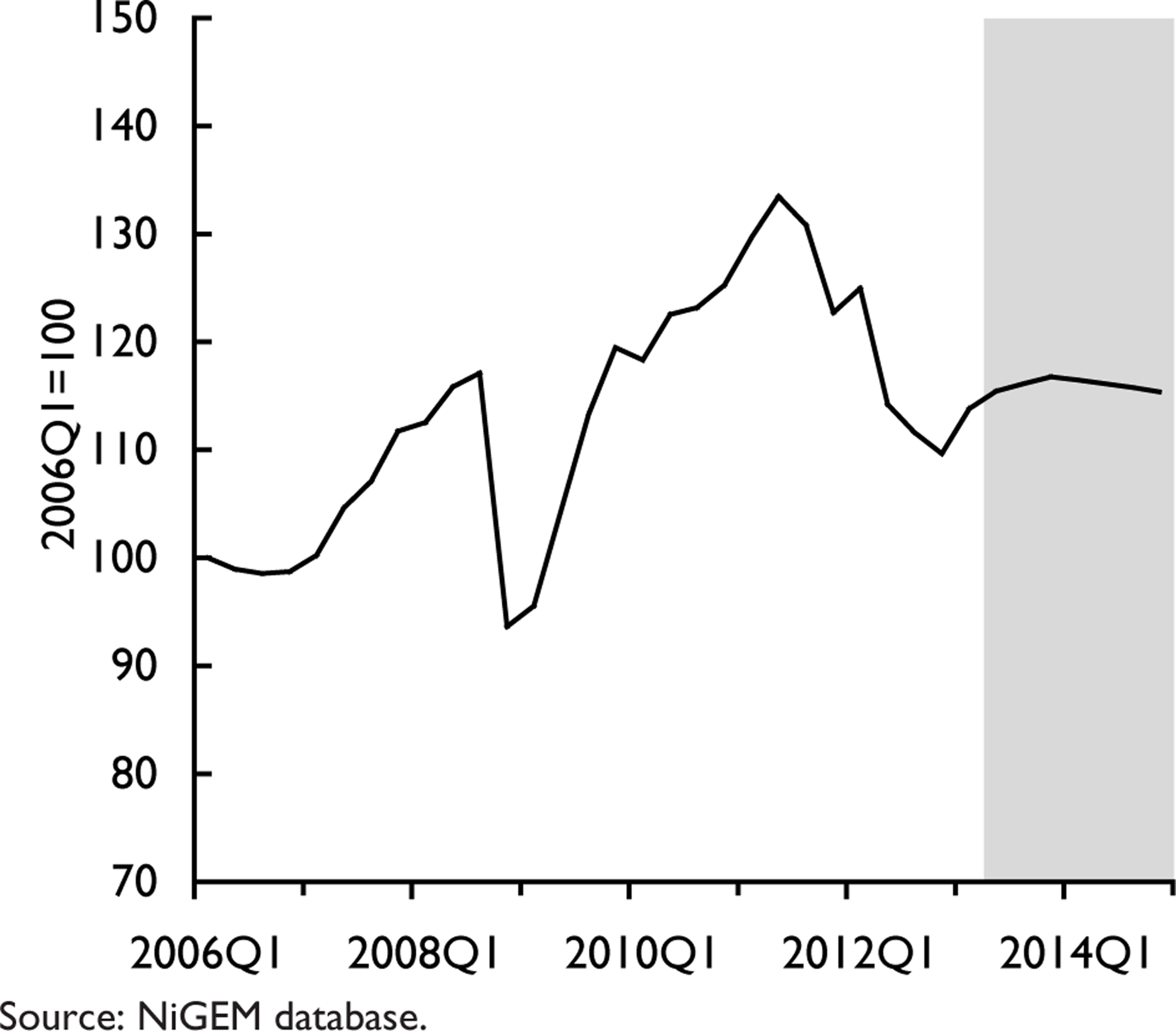

Brazil: real effective exchange rate

India's WPI and CPI inflation

Russia

Russia's short-term economic outlook has worsened significantly. GDP growth slowed to 3.6 per cent in 2012 from 4.3 per cent in 2011, and in the first quarter of 2013 GDP was only 1.1 per cent higher than a year earlier – the weakest four-quarter growth since 2009. The slowdown is attributable partly to subdued demand in Russia's export markets, especially in Europe, although the slowdown in China has also had an impact, especially on exports of primary commodities. In addition, the weakening of oil prices not only reduces export revenues but also dampens domestic demand and narrows the scope for fiscal stimulus as over half of all government revenue is directly related to oil. We project a further slowing of annual average growth, to 2.4 per cent this year and 1.6 per cent in 2014.

To support growth, Russia may resort to monetary stimulus, but the room for interest rate cuts is limited, given inflationary pressure. Our forecast puts inflation at about 5 per cent for both the current year and 2014. With regard to the effects on the Russian economy of the financial crisis in Cyprus and its resolution, it is impossible to estimate the exact loss to Russian depositors but we expect the macroeconomic effect to be negligible.

According to Moody's’ estimates, Russian deposits in Cypriot banks amount to ¢30–40 billion of an estimated total of about ¢70 billion. The Russian official gross foreign asset position stood at ¢1,100 billion in the second quarter of 2012 so an assumed write-off of ¢10–20 billion would be equivalent to a modest 1–2 per cent reduction of official foreign assets. While Cyprus continues to maintain capital controls, only limited amounts can be legally withdrawn from Cypriot bank accounts. Once the capital controls are removed, Russian capital is expected to leave the island. It may be repatriated, in which case it could boost investment in Russia, or depositors might prefer to relocate funds to a different off-shore location, which might be considered more likely.

Footnotes

1

International Labour Organization, Global Employment Trends, 2013. The ILO estimates that in the five years to the end of 2012, unemployment globally rose by 28 million (shared equally between advanced and developing economies) and that a further 39 million people dropped out of the labour market.

2

International Monetary Fund, Global Financial Stability Report, April 2013.

3

Ben S. Bernanke, ‘Monetary Policy and the Global Economy’, Speech delivered at the London School of Economics, March 25, 2013, Board of Governors of the Federal Reserve System.

4

The Dow-Jones news service reported on April 25, 2013 as follows: ‘There will be no common European deposit insurance scheme for the “foreseeable future,” Chancellor Angela Merkel said today at German banking conference. Her remarks are the most explicit yet from a German government official that one of the desired pillars for the EU's proposed banking union won't be in place any time soon. “The German government rejects a unified European deposit insurance – at least for the foreseeable future,” said Ms. Merkel. “We prioritise, however, very clearly and vehemently,” a harmonisation of the European deposit system, she added. Her comments come one day after the head of Germany's central bank told the same conference that at the current time a common insurance scheme was inappropriate. Such a plan is “not sensible” because Europe's financial system isn't sufficiently integrated, said Jens Weidmann, head of the Bundesbank, yesterday.’

5

See the discussion in the National Institute Economic Review, February 2013, p. F17.

6

Ettore Dorrucci, Gabor Pula and Daniel Santabarbara (2013), ‘Chinas’ economic growth and rebalancing’, Occasional paper series, No 142, European Central Bank.

7

World Economic Outlook Database, April 2013, IMF.

ACKNOWLEDGEMENTS

All questions and comments related to the forecast and its underlying assumptions should be addressed to Dawn Holland (

This forecast was completed on 25 April, 2013.

Exchange rate, interest rates and equity price assumptions are based on information available to 19 April 2013. Unless otherwise specified, the source of all data reported in tables and figures is the NiGEM database and NIESR forecast baseline.