Abstract

Global growth prospects for this year and next have weakened slightly further since early May. This is partly due to further signs of a significant slowing in a number of key emerging market economies, particularly China. But activity has also been somewhat weaker than assumed in some advanced economies, including the United States. In addition, although some central banks, including the European Central Bank (ECB), have eased monetary conditions in recent months, the significant rise in global long-term interest rates since early May, in anticipation of steps towards a normalisation of monetary policy by the US Federal Reserve, entails a tightening of financial conditions that will tend to weaken demand and slow the recovery. Thus our forecast of global GDP growth in 2013 is now 3.1 per cent, revised down from 3.3 per cent in May. World growth is projected to pick up to 3.6 per cent in 2014, a downward revision of 0.1 percentage point.

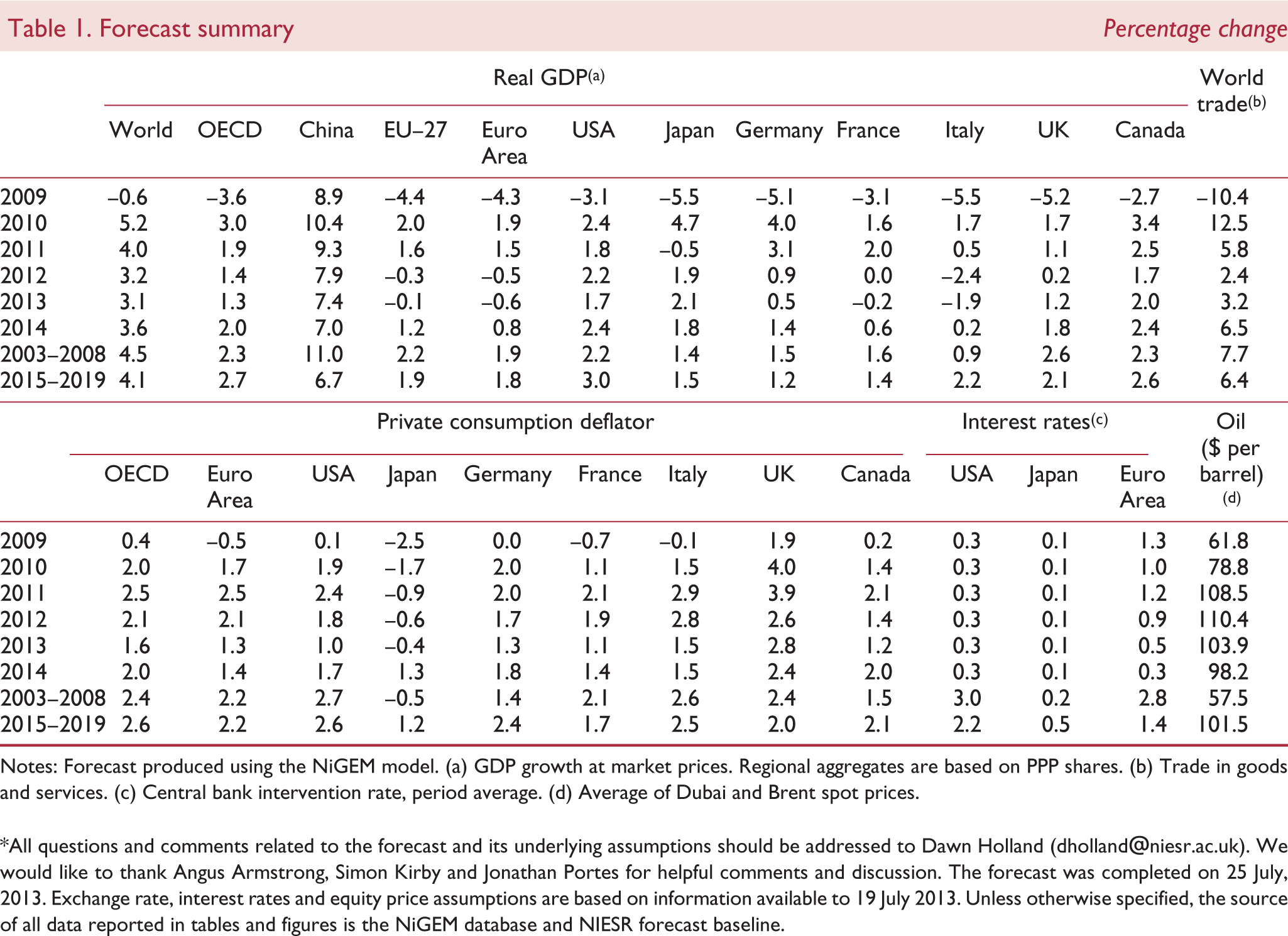

Forecast summary Percentage change

Notes: Forecast produced using the NiGEM model. (a) GDP growth at market prices. Regional aggregates are based on PPP shares. (b) Trade in goods and services. (c) Central bank intervention rate, period average. (d) Average of Dubai and Brent spot prices.

Box A. The macroeconomic implications of rising government bond yields

Global government bond yields have followed a rising trajectory since early May 2013. This movement has been widely attributed to signals from the Federal Reserve that it will begin to taper (i.e. reduce) QE later this year. Since January 2012, monetary policy statements from the Federal Reserve have been accompanied by a transparent summary of the projections made by members of the Federal Open Market Committee (FOMC) for the appropriate path of the federal funds rate over the next several years. This currently points to interest rate rises commencing in 2015. Given that the further asset purchases related to quantitative easing measures all should terminate before any interest rate rises begin, this gives a fairly clear timetable for the tapering process.

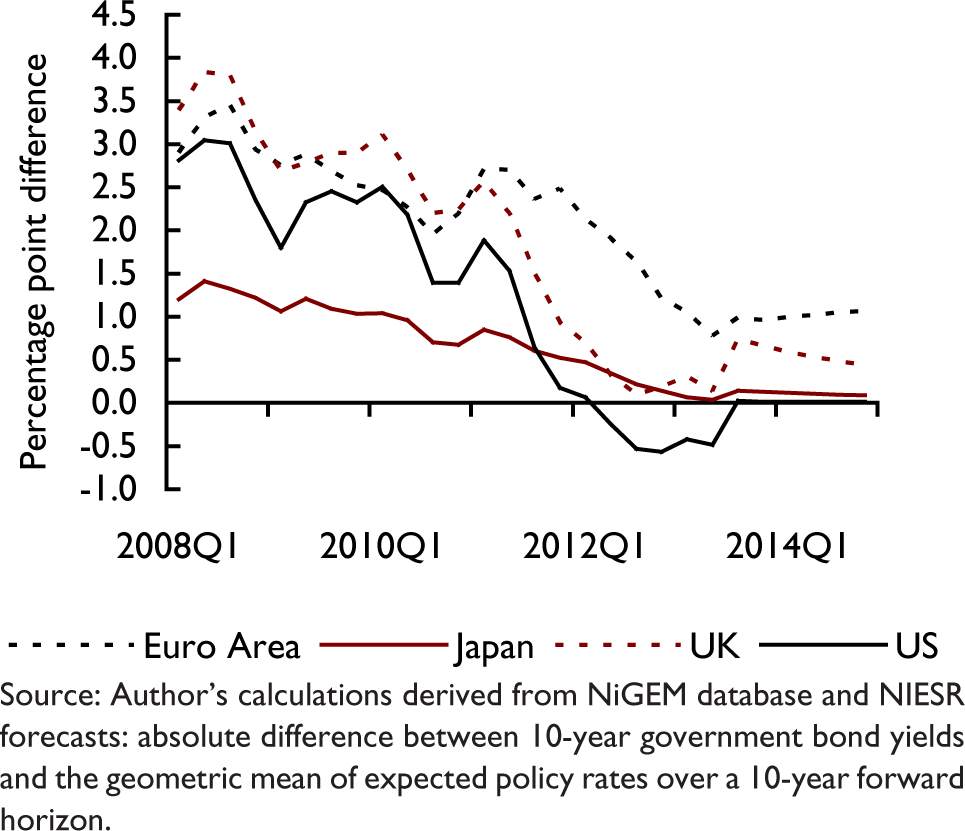

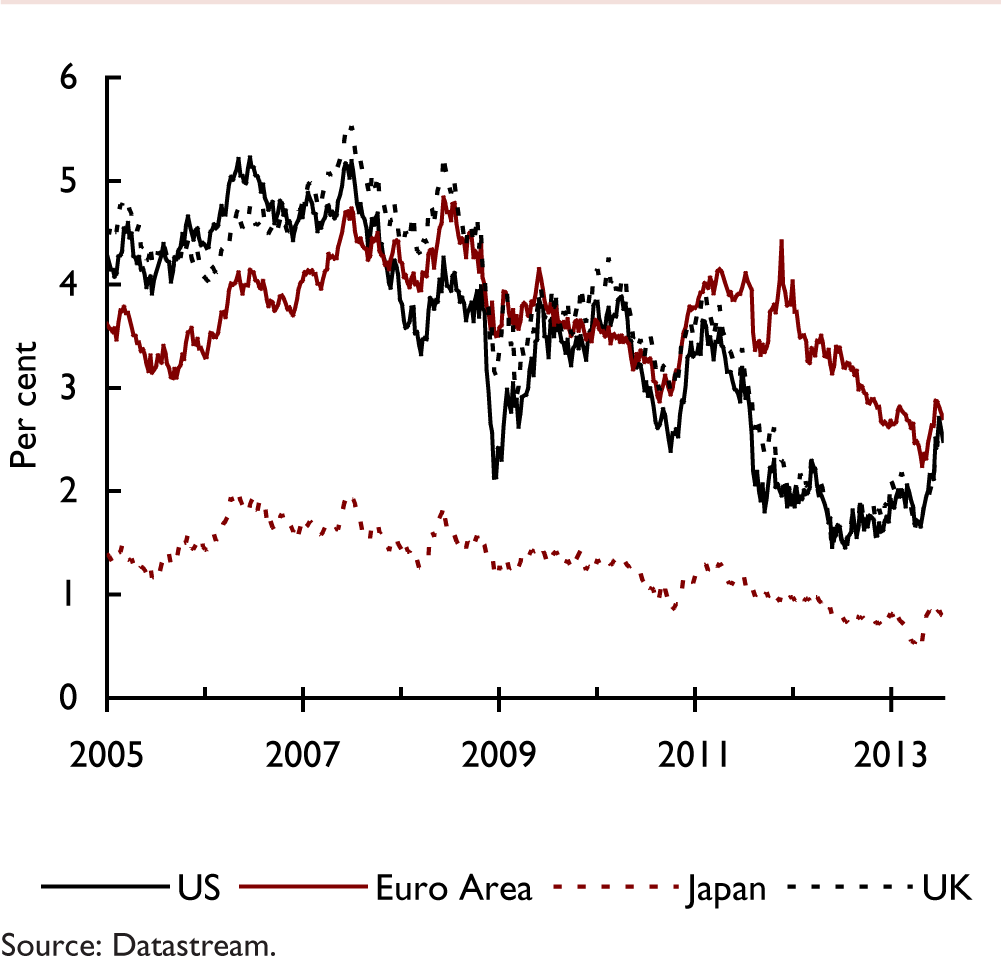

Bond yields in the US have reacted to the Fed's signals – the expected tapering of QE has pushed yields up by 90 basis points since the recent trough reached in early May 2013. This can be seen as a narrowing of the negative term premium on US bond yields that emerged in early 2012. Figure A1 illustrates the difference between 10-year government bond yields in the US, UK, Japan and the Euro Area and the geometric mean of expected policy rates over a 10-year forward horizon in the same country. In theory, if investors have perfect foresight, this difference should reflect a term premium – the extra return demanded to cover the risk of holding longer-term maturities. In practice, the difference is at least as likely to reflect investor forecasting errors. Clearly in 2009–10, the historically low interest rates in the major economies were not expected to persist into 2014. The margins declined significantly in 2011, as the sovereign debt crisis in the Euro Area erupted and the US pursued its second round of quantitative easing. From early 2012, figure A1 suggests that a negative term premium had opened on long-term US government bonds, indicating that investors were willing to accept a lower expected rate of return on these safe assets than on shorter term bonds. Since May 2013, the negative premium in the US has effectively dissipated, suggesting that current market rates are essentially neutral, and in line with market expectations for the federal funds rate. It is not at all clear that this neutrality holds for other countries, and the term premium in the UK appears to have widened significantly. This suggests that investors in the UK are less willing to take on longer-term investments, and may adversely affect, for example, investment in major infrastructure projects and other projects that entail a long time lag before seeing a financial return.

Implied term premium on 10-year government bonds

Global bond markets are highly correlated and, as the US dollar accounts for more than 60 per cent of global foreign currency reserves, US markets are a key influence on global interest rates. Bond markets in the US and the UK move together particularly closely, with about 60 per cent of the weekly shift in US long rates tending to pass through to UK yields. Many countries, including the UK and Germany, have benefited from the low global interest rates, which can, at least in part, be attributed to the loose US monetary stance in recent years. The tightening in the US since May has effectively tightened financial conditions in the other major economies as well, and this may prove challenging for many of the struggling European economies.

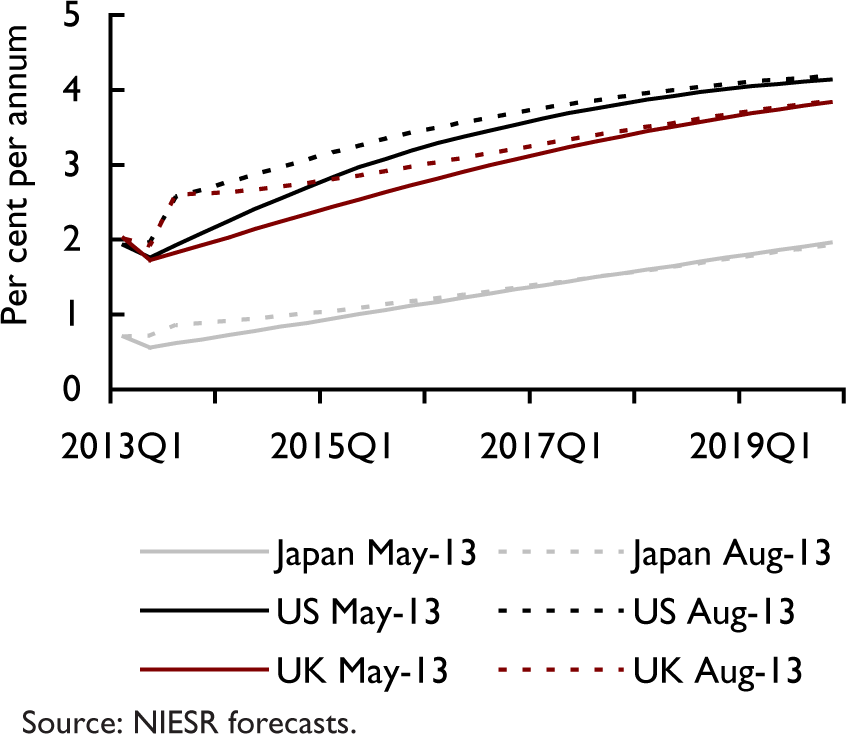

Figure A2 illustrates the projections for 10-year government bond yields for the US, UK and Japan underlying our May 2013 forecast and our current forecast. We have excluded the Euro Area from the analysis, as average bond yields for the Area as a whole are broadly unchanged. The recent rise in yields in Germany is largely offset by a narrowing of spreads over Germany in Greece, Portugal, Spain, Ireland and Italy (see Appendix A). Bond yields in the UK and the US are expected to be about 50 basis points higher in 2014 than anticipated three months ago, while in Japan the expected level of bond yields next year has risen by about 15 basis points. Yields are expected to converge gradually back towards the long-run path anticipated in May by about 2016, so the shock to the expected level of bond yields is a temporary, but protracted, one.

Bond yield projections, May 2013 and August 2013

In order to assess the macroeconomic impact of the observed rise in bond yields since May 2013, we run a scenario using the National Institute's model, NiGEM, 1 that shifts the term premium on government bonds. A similar scenario is described in OECD (2013). 2 Within the modeling framework we adopt, bond yields feed into the macroeconomy through four channels.

Public sector interest rates are assumed to act as a floor for private sector rates, so a rise in government bond yields pushes up private sector borrowing costs, and restrains GDP growth through the investment channel. The housing market is also linked to interest rates. Rising bond yields push up mortgage rates in many countries, putting downward pressure on house prices and thereby restraining GDP growth through the consumption channel. Rising public sector borrowing costs push up government interest payments on newly issued debt, worsening the fiscal deficit. In order to maintain a targeted fiscal position, a tightening of the fiscal stance would be required, slowing demand. Bond yields are inversely related to the market value of bond holdings, so a rise in bond yields implies a loss of financial wealth and a deterioration in the balance sheet position of banks and other private sector bond holders. These effects have direct negative consequences for consumption, which is modelled as partly determined by the financial wealth holdings of the personal sector, and may also lead to a tightening of bank lending conditions, further restraining both investment and consumer spending.

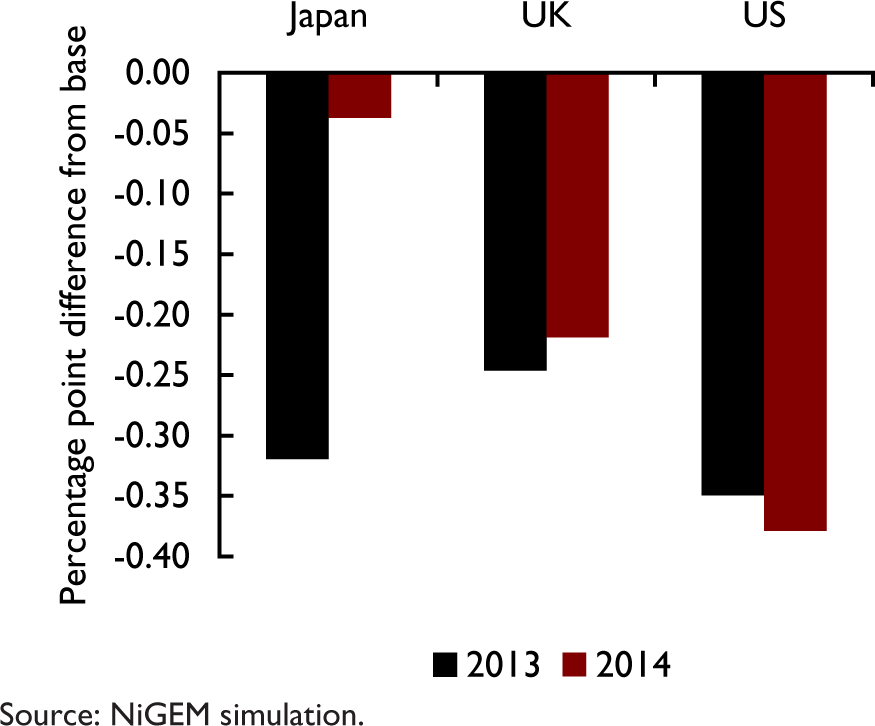

Figure A3 illustrates the expected impact on GDP growth of the recent rise in global bond yields, based on the NiGEM model simulation described above. The simulation suggests that recent movements in bond yields may reduce GDP growth by about 0.3 percentage points this year in the US, UK and Japan. The effects feed through more rapidly in Japan, so while the shock is somewhat smaller, the impact on GDP in the first year is in line with what is expected in the other economies. In 2014, the model simulation suggests that GDP growth in Japan would be unaffected, whereas we continue to see negative effects in both the UK and the US. The decline in GDP growth is driven by a steep drop in investment, which is more sensitive than consumer spending to borrowing costs. Private sector investment growth is reduced by 2–3 percentage points in 2013 as a result of the shock. Consumer spending growth, on the other hand, is only expected to fall by about 0.1 percentage point this year in response to the rise in government bond yields. The fiscal impacts of the shock feed through gradually, as new debt is issued at the higher rate of return. The simulation suggests that government interest payments in the UK would rise by 0.8 per cent this year, while in Japan they would rise by 2.2 per cent and in the US by 2.6 per cent. By 2016, the level of government interest payments in the UK would be 2½ per cent above baseline, with a rise of 5 per cent in Japan and 7¼ per cent in the US.

Impact of rise in yields on GDP growth

NOTES

Further details on the NiGEM model are available at http://nimodel.niesr.ac.uk/.

The main differences between the OECD and NIESR scenarios are that the OECD scenario applies a larger (2 percentage point) and shorter-term (1 year) shock to bond yields, whereas in this box we raise bond yields by 50 basis points in the US and UK and 15 basis points in Japan, with a gradual tapering, so that interest rates more closely resemble the paths illustrated in figure A2.

REFERENCES

Inflation remains generally subdued worldwide, with commodity prices weak. Monetary policy has become more supportive of recovery, through cuts in official interest rates since early May, not only in the Euro Area but also in Australia, Hungary, Israel, Korea, Poland, and Thailand. Key official rates have been raised, however, in Brazil, Indonesia, and Turkey in response to inflationary and currency pressures.

The broad slowing of growth among major emerging market economies stems partly from various idiosyncratic national factors, but a common feature in some important cases is central bank actions to restrain credit growth or tighten monetary conditions. In China the central bank has recently taken action to restrain excessive credit growth and in Brazil the central bank has raised its benchmark rate by a further 1 percentage point in recent months to reduce inflation. In Russia also, the central bank is seeking to lower inflation with the economy operating close to full capacity. And in India, after more than a year of waning inflation and declining interest rates, the Reserve Bank tightened liquidity in mid-July to stem the depreciation of the rupee at a time when inflation seemed to be rising again. In each case, it seems that the slowing of growth has been in response to financial and inflationary pressures, or capacity constraints, which suggests that it may persist for some time.

Since early May there has been a significant increase in volatility in global financial markets arising mainly from speculation about the timing of the normalisation of monetary policy in the United States, from uncertainties about how the new Japanese government's policies will work and from the action by the Chinese authorities to restrict credit growth. Over the period as a whole, 10-year government bond yields have risen by about 90 basis points in the United States, 20 basis points in Japan, and 40 basis points in the major Euro Area countries (figure 1). Long-term interest rates have also risen in many emerging markets – by about 50 basis points in China and Russia and 100 basis points in Brazil. Statements by the US Federal Reserve about its plans for the future normalisation of monetary policy seem to have been the main factor behind the general rise in yields. The rise in long rates entails a tightening of financial conditions which may be particularly inconvenient for countries still suffering from weak activity. The synchronicity of world financial markets despite very different national economic conditions may prove even more challenging as the major central banks act to normalise conditions.

Ten-year government bond yields

In foreign exchange markets, the US dollar has appreciated in the past three months against commodity-based currencies and emerging market currencies; exchange rates among the currencies of the major advanced economies are broadly unchanged (Appendix A). With pressures on emerging market currencies having reversed, talk of competitive ‘currency wars’ has receded, and some emerging market economies, especially those with significant current account deficits and financing needs, have become concerned instead about how to contain capital outflows and currency depreciation without damaging growth.

The upturn in bond yields was accompanied between mid-May and late June by broad, moderate declines in equity markets. More recently, markets have turned up again, reaching new record highs in the United States. In the period since early May most major markets have risen moderately. The most notable declines, of about 15 per cent and 7 per cent, respectively, in local currency terms, have occurred in Brazil and China.

The modest strengthening of global growth that is projected for the period ahead is expected to be supported by the maintenance of highly accommodative monetary policies in key advanced economies, by the fiscal stimulus being implemented in Japan, and by the waning of fiscal drag in the United States and the Euro Area. The decision by the ECOFIN Council to allow more time for some European countries to reduce their fiscal deficits shows some welcome pragmatism.

There are a number of important downside risks to this outlook. First, it seems likely that financial markets will remain volatile in the period ahead as they respond to the economic data that will provide the input to the Fed's decision on the reduction or ‘tapering’ of its quantitative easing (QE) programme and the subsequent raising of short-term interest rates. Recent market reactions, which have sometimes seemed erratic and difficult to relate to successive, similar official policy statements indicate the possibility of further yield increases and continued volatility. This may damage the recovery in advanced economies and lead to capital flow reversals and lower growth in emerging markets.

Second, the recent slowdown in some key emerging market economies and the indications of supply-side constraints suggest that there are risks of a more prolonged growth slowdown in these economies than we are projecting. While many of these economies are in strong financial positions with significant degrees of policy freedom (including exchange rate flexibility), slower growth after a period of rapid credit expansion may uncover financial vulnerabilities. In addition, if potential output is lower than assumed this would imply less fiscal room for manoeuvre than expected.

Third, in the United States, there is the political risk of further failure in budget negotiations, notably over a timely increase in the debt ceiling when needed later this year.

Fourth, progress towards banking reform remains piecemeal at best, leaving significant financial sector risks in place. In the US, the Federal Reserve restated in early July that banks will be expected to meet the (fairly weak) Basel III capital requirements. Also, together with other regulators, the Fed proposed a rule to strengthen leverage ratio standards for the largest, most systemically significant US banking organisations. In the UK and Europe some large banks have warned that, rather than increase capital to satisfy the new requirements they will significantly shrink their balance sheets which, all else equal, implies less credit availability. This is clearly not the intention of the regulators and is an indication of the deeper challenges still to be addressed in the industry.

Finally, the Euro Area continues to face substantial risks associated with: first, the concentration of the burden of adjustment on the Area's deficit countries and, second, the incompleteness of the institutional framework for the monetary union. Actions to mitigate and reverse financial fragmentation, to strengthen banks’ balance sheets, and to establish a banking union are high on the policy agenda. Some progress has been made with the agreement that the ECB will be responsible for supervision of the larger banks in the Euro Area. But as we have previously warned, the politics of the authority to resolve banks and share the losses is proving difficult to resolve. The German government has warned that such proposals would be beyond the powers permitted under EU treaties. Since the fiscal back-stop is the core element of a banking union, the Euro Area remains vulnerable to further set-backs.