Abstract

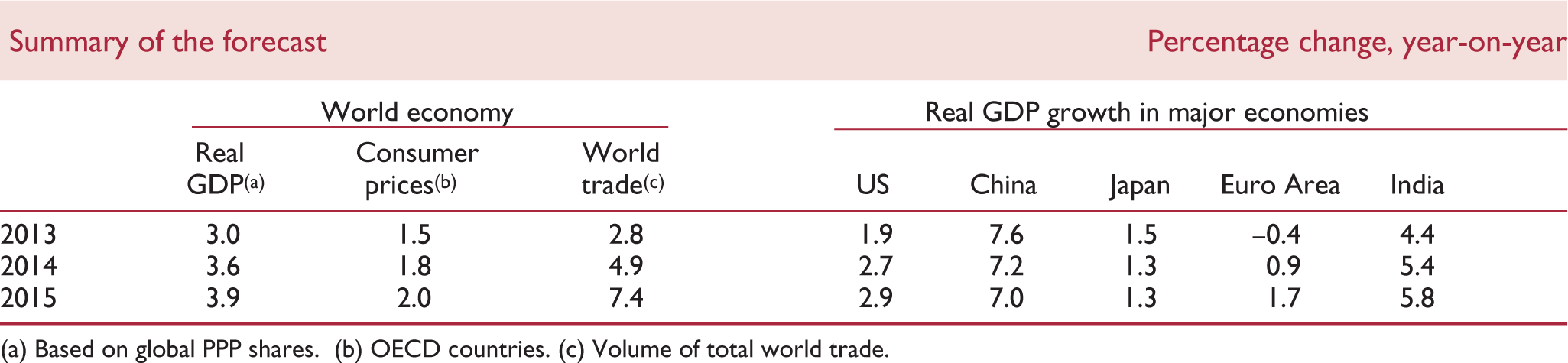

Following growth of 3.1 per cent in 2013, the world economy is projected to expand by 3.6 per cent in 2014 and 3.9 per cent in 2015. Growth prospects have improved in most advanced economies, with the exception of Japan, although much of the Euro Area remains very depressed. Key risks include deflationary pressures in advanced economies, especially the Euro Area. Provided that it is contained, the impact of the Ukraine crisis on the global economy is likely to be small.

Cyclical recoveries continue in the major advanced economies, supported this year by continuing highly accommodative monetary policies and, in both the United States and the Euro Area, by less restrictive fiscal policies than in the past three years. In Japan, however, growth slowed sharply in late 2013, and the prospect of significant fiscal consolidation raises questions about the need for additional monetary action to boost demand.

Among the major emerging market economies, growth is continuing to slow in China. Growth prospects for Russia, which were already weak, have been marked down significantly further as a result of the Ukraine crisis. Growth in India, recently half the rates seen a few years ago, is expected to strengthen assuming that the current general election reduces political uncertainties. Growth in Brazil has also remained sluggish, reflecting macroeconomic imbalances and capacity constraints. Brazil, India, and Russia all suffer from excessive inflation, a factor constraining monetary policy.

Deflation remains a key risk, especially in the Euro Area. A common misperception is that while deflation may be damaging, low inflation is benign – even that the lower inflation is, the better, with absolute price stability the best outcome of all. In fact, excessively low, positive inflation could impede economic growth and recovery in a number of ways. In the Euro Area, the problems of low inflation are particularly salient because of the dual needs of the weak ‘peripheral’ economies both to reduce debt and to improve their international competitiveness. The weakness of bank balance sheets, and hence of credit growth, aggravate this problem. Other risks relate to the eventual unwinding of extraordinary monetary policy measures, especially in the United States, and the potential impact on asset prices and capital flows.

The crisis in Ukraine will have a significant negative impact on the Ukrainian and Russian economies, and a smaller impact on some European countries. However, barring a major escalation, the impact on the global economy is likely to be limited, unless there are serious disruptions to fuel supplies.

Summary of the forecast Percentage change, year-on-year

Based on global PPP shares.

OECD countries.

Volume of total world trade.