Abstract

Euro Area

The modest economic recovery has continued and seems to have gathered some strength in recent months. In the final quarter of 2013, GDP growth picked up to 0.2 per cent from 0.1 per cent in the third quarter, and higher-frequency data suggest a further strengthening in early 2014. Industrial production has shown a moderately accelerating trend and in February was 1.7 per cent higher than twelve months earlier; and recent PMIs suggest GDP growth of about 0.5 per cent in the first quarter. The European Commission's economic sentiment indicator for March was the highest since mid-2011. But the Area's economy remains depressed, with considerable economic slack. Unemployment in February was 11.9 per cent, unchanged since last October and only slightly below its 12.0 per cent peak. Consumer price inflation has fallen further: in March, the 12-month all-items rate declined to 0.5 per cent, while the core rate fell to 0.7 per cent; neither rate has exceeded 1 per cent over the past six months.

The average inflation rate for the Euro Area as a whole of course masks differences among individual member countries. The number of countries experiencing negative inflation has recently risen to five – Cyprus, Greece, Portugal, Slovakia, and Spain – while the highest inflation rates, of about 1.4 per cent on a 12-month basis, have been in Austria, Finland, and Malta. We expect that the deflationary landscape in southern Europe will change somewhat next year, with Greece the only country continuing to experience price declines in 2015 and other economies seeing inflation close to zero, before converging towards the target in the medium term as the recovery becomes more entrenched. This is echoed in our forecast for the Euro Area as a whole where we expect average HICP inflation to be close to zero, at around 0.2 per cent, this year before picking up to around 1.1 per cent in 2015 and 2 per cent in the medium term. There are, however, important downside risks to this forecast, as discussed above in the World Overview.

The ECB has kept its interest rates and operational stance unchanged in recent months, while increasingly emphasising the scope for further easing action if judged necessary. At his press conference following the early-March meeting of the Bank's governing council, President Draghi observed that the moderate economic recovery was proceeding in line with the ECB's previous assessment, and that the expected prolonged period of inflation lower than the objective of ‘below, but close to, 2 per cent’ was less of a concern than it might be because inflation expectations still seemed well anchored, close to the targeted level. At the same time, he “firmly re-iterate(d)” the ECB's forward guidance, that “We continue to expect the key ECB interest rates to remain at present or lower levels for an extended period of time”, given “the subdued outlook for inflation …, the broad-based weakness of the economy, the high degree of unutilised capacity and subdued money and credit creation”. He also again indicated that the ECB remained firmly determined to maintain the high degree of monetary accommodation and to take further decisive action if required.

After the next meeting, in early April, Draghi went further, providing the strongest signal yet that the ECB was prepared to embrace quantitative easing, by stating that “The governing council is unanimous in its commitment to using unconventional instruments within its mandate in order to cope effectively with risks of a too prolonged period of low inflation”. Draghi subsequently confirmed that “unconventional instruments” included bond buying, but at the same time stressed that the Bank had “not exhausted its conventional armoury”, thus indicating that further cuts in official interest rates, possibly into negative territory, might be undertaken first.

As Draghi acknowledged, a factor holding down inflation in the Area has been the strength of the euro, which has appreciated by about 9 per cent against the US dollar and 8 per cent in effective terms since its trough of 2012. Indeed, in mid-April, Draghi acknowledged that the appreciation effectively entailed a tightening of monetary conditions, thus requiring additional stimulus by the ECB. The euro's rise may be attributed partly to the recovery from the Euro Area's financial crisis and partly to the widening of the Area's current account surplus. It has heightened the challenge already faced by the Area's deficit countries of improving their international competitiveness, given the low rates of inflation prevailing throughout the Area, including in the surplus countries. However, the relatively weak economic recovery in the Area and the related prospect that the normalisation of monetary policy in the Area will lag behind other advanced economies seems likely to limit how much further the appreciation will go.

Heightened expectations of additional easing action by the ECB, including purchases of the sovereign bonds of deficit countries, have contributed to a further narrowing of sovereign yield spreads in the Area. By late April, spreads on ten-year government bonds relative to Germany had narrowed to 4.6 per cent for Greece (which returned to international capital markets earlier in the month, with an over-subscribed issuance of five-year instruments), 2.2 per cent for Portugal, and 1.6 per cent for Spain. Nevertheless, credit conditions have remained tight in the peripheral countries, reflecting the continuing weakness of banks' balance sheets, and the volume of credit in the Area has continued to decline, by 2.3 per cent in the year ended February.

The legislative work underpinning the Area's new banking union – an objective since June 2012 – was completed in mid-April. The first leg of the union had been put in place last October with the establishment of the single supervisory mechanism at the ECB. The ECB will be the ultimate supervisor of all banks in the Area from next November; in the meantime, it is carrying out a comprehensive balance sheet assessment of about 130 major banks. On March 20, 2014, agreement was reached between the European Parliament, the European Council, and the European Commission on the single resolution mechanism (SRM), the banking union's second major component. The compromise reached amended the agreement reached by ministers last December in a number of ways: it allows the single resolution fund to be built up from bank levies in eight years rather than ten, a faster pooling of the fund's resources, a larger role for the Commission in resolution decisions, a somewhat simplified procedure for such decisions, and allowance for the establishment of enhanced borrowing capacity for the fund. The agreement was welcomed by the ECB, with President Draghi declaring that the “two pillars (of the Banking Union) are now in place”. However, the mechanism may still be regarded as under-funded, its resolution procedures too complex, and it continues to lack a public backstop. The regulation on the SRM was passed by the European Parliament on April 15, along with a Bank Recovery and Resolution Directive (setting out common rules on bailing-in and state aid for failing banks) and a Directive on Deposit Guarantee Schemes (to facilitate faster pay-outs of insured funds).

Both weak growth and low inflation have been making deleveraging more difficult for public and private sectors across the Euro Area. In several cases, governments have been showing signs that they are finding it tough to meet their deficit and debt reduction targets. In April, France's new administration adopted less ambitious targets for deficit reduction in 2015–17, while reaffirming the commitment not to exceed the upper limit of 3 per cent of GDP agreed with the EU for 2015. Also, Italy's new government has officially asked the EU to extend from 2015 to 2016 the deadline for achievement of a balanced budget.

Germany

Growth has strengthened somewhat further in recent months, while inflation has continued to decline. Following 0.3 per cent growth in the third quarter of 2013, GDP expanded by 0.4 per cent in the final three months of the year, and higher-frequency indicators point to further acceleration in early 2014, although this may have been partly due to favourable weather conditions. The 12-month growth rate of industrial production, which was negative in early 2013, rose to about 5 per cent in the first two months of this year, and business sentiment has recently been at its highest since 2011.

Partly reflecting recent developments, our projections of GDP growth in 2014 and 2015 have been revised up slightly, to 1.7 per cent and 1.9 per cent respectively. Growth will be driven mainly by domestic demand, underpinned by the strong labour market and low interest rates. The contribution of net exports is expected to remain positive throughout the forecast horizon, although their relative role will decrease significantly as domestic demand gains momentum, fuelling imports.

After two years of declining investment amid uncertainty about policies ahead of the federal elections last September and in relation to the financial crisis in the Euro Area, we project a pick-up in investment starting this year. Reduced uncertainty, and steadily increasing capacity utilisation, will be the main drivers of this recovery, while the continuing weak growth and fragile macroeconomic situations in much of the Euro Area, together with slower growth in key emerging market economies, including China, will limit the pace of the upswing.

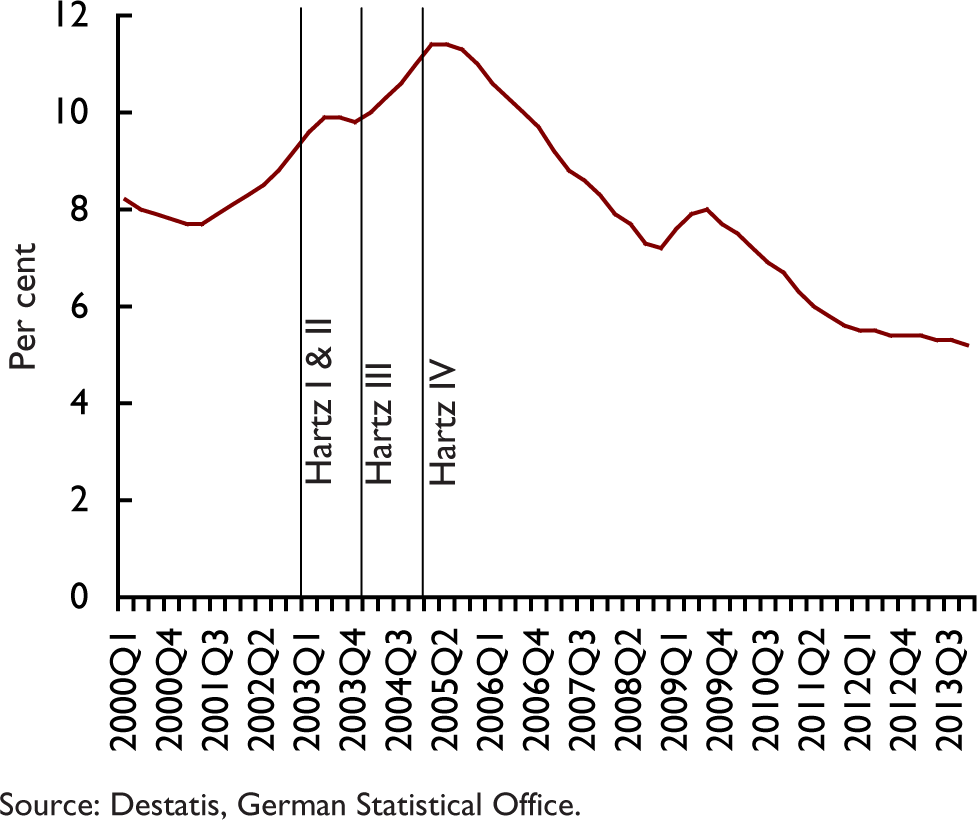

Unemployment has fallen further, to post-unification lows of around 5 per cent. This is, in part, an outcome of the implementation during 2002–05 of the laws known as the Hartz labour market reforms – see figure 3. Strong labour market conditions have contributed to significant recent immigration from both Southern, and Central and Eastern, Europe, as discussed in the January Review.

Unemployment in Germany

Although the economy is operating close to full capacity, and growth is running slightly above its estimated potential rate of about 1.3 per cent, inflation has declined further, to 1.0 per cent in terms of the 12-month change in consumer prices in March. We forecast that consumer prices will increase by 1.4 per cent, on average, in 2014 and 1.6 per cent in 2015. While higher unit labour costs are likely to pass through to inflation, this should be partly offset by the projected easing of oil price pressures.

France

While the French economy has remained weak in recent months, a continued slow improvement in activity is apparent. In the fourth quarter of 2013, GDP growth turned positive, albeit by only 0.3 per cent, and indicators of more recent activity suggest continuing modest expansion. The 12-month growth rate of industrial production, which was negative for most of 2012–13, has been positive in most recent months, and in March 2014 PMIs reached 2–3 year highs, although they indicate only muted growth. Unemployment, down slightly to 10.2 per cent in the fourth quarter of 2013 after a revision of data, has remained close to 16-year highs. Consumer price inflation fell to 0.6 per cent on a 12-month basis in March; it has been at or below 1 per cent since early last year.

There have been several developments with respect to the Government's ‘responsibility pact’ with business announced by President Hollande in January to promote growth, employment, and the associated fiscal policies. In early March, labour and business representatives reached agreement on aims for job creation under the pact. In early April, following local government elections, newly appointed Prime Minister Valls presented a policy programme to parliament which reiterated Hollande's commitment to public spending cuts worth EUR 50 billion over 2015–17 – to be split between central state (ε18 billion), local authorities (ε11 billion), health care (ε10 billion) and social security (ε11 billion) – and also promised EUR 11 billion in tax cuts for businesses and households over the same period, additional to the EUR 30 billion cuts in payroll tax announced by Hollande in January. The Prime Minister also, in mid-April, reaffirmed the government's commitment to observe the fiscal deficit ceiling for 2015 of 3 per cent of GDP agreed last year with the European Commission, even though the deficit in 2013, at 4.2 per cent of GDP, overshot last year's target of 4.1 per cent. Later in the month he set out less ambitious targets for deficit reduction in 2015–17 than those adopted earlier, but with the 3 per cent ceiling for 2015 still honoured: the new targets are 3.0, 2.2, and 1.3 per cent of GDP, respectively, for 2015–17, up from 2.8, 1.7, and 1.2 per cent.

These policies promise continuing fiscal consolidation in 2014–16, though at a more moderate rate than over the past three years. Given this continuing fiscal drag, the strengthening of growth will depend partly on continuing accommodative monetary conditions and the healing of private sector balance sheets, but also, importantly, on needed improvements in France's international competitiveness. Such improvements have recently been difficult to achieve given the strength of the euro in foreign exchange markets and the low rates of inflation throughout the Euro Area. But they should be promoted by the tax cuts included in the responsibility pact, and also by the structural reforms, already implemented or being planned, in the labour market, the energy and transport sectors, and public administration.

In light of recent data, we have revised down slightly our GDP growth forecast for 2014 by 0.2 percentage points, although our forecast for 2015 is unchanged. We also forecast that France will miss its 3 per cent deficit target in 2015, not crossing this threshold until 2017.

Italy

After nine consecutive quarters of economic contraction, Italy emerged from recession in the final quarter of 2013, albeit with minimal, 0.1 per cent, positive growth. The economy shrank by 1.8 per cent in 2013 as a whole and remains deeply depressed: in February, unemployment rose to a 37-year high of 13.0 per cent, with the rate among 15–24 year-olds at 42.3 per cent. Inflation has continued to decline: in March, the 12-month increase in consumer prices fell to 0.4 per cent. Substantial fiscal consolidation over the past three years has contributed to the weakness of activity. With fiscal drag waning in the short run, we forecast weak positive growth to continue through 2014 before picking up pace next year.

As well as high unemployment, Italy's economic problems include chronically weak productivity growth. Prime Minister Renzi, newly appointed at the end of February, has declared these two issues to be his top priorities for economic policy, and in March he announced a programme of fiscal and labour market reforms designed to improve conditions in the labour market and spur productivity growth, while keeping Italy within the fiscal deficit ceiling of 3 per cent of GDP. They include a number of tax cuts to be implemented on May 1, and to be financed partly by spending reductions; the payment by July of arrears owed by the public to the private sector; and proposed measures, currently being considered by parliament, to improve labour market flexibility.

Related to low productivity growth, real disposable incomes have continued to contract, despite muted inflation. This has weighed on consumer spending – now at its lowest level since 1999 – and on demand more broadly.

By the end of 2013, Italy had returned to a marginally positive external current account balance. Unlike Spain, which has achieved surplus partly through strong export performance, Italy's adjustment has occurred predominantly through a contraction of imports, which continued last year. We expect the downward pressure on imports to ease somewhat in 2014 as growth boosts domestic spending power. However, robust exports, driven by a rebound in demand from Italy's main trading partners and any competitiveness gains the reforms may bring, will mean that the current account balance should remain positive through 2014 and 2015.

Spain

The economic recovery that began late last year, with GDP growth of 0.2 per cent in the fourth quarter, strengthened somewhat in the first quarter of 2014. The upturn in activity is being driven by strong export performance alongside pickups in investment and consumption. Recent data have prompted a significant upward revision to our growth forecast, to 1.1 per cent and 1.4 per cent for 2014 and 2015 respectively.

Underpinning export growth has been an improvement in international competitiveness brought about by falling domestic labour costs, with high unemployment and labour market reforms holding wages broadly flat since 2010.

The benefits of lower wage growth for competitiveness, however, must be weighed against its wider implications for inflation and the easing of debt burdens. Falling wage costs, together with the appreciating euro, have exerted downward pressure on prices, and the 12-month change in the HICP turned negative in March at −0.2 per cent. We are now forecasting deflation of 0.2 per cent in 2014 as a whole, followed by 0.8 per cent inflation in 2015. This low or negative inflation will make more difficult the deleveraging process that needs to continue in both the private and public sectors, where debt levels, though reduced from their peaks, remain high. The government narrowly missed its deficit target for 2013, by less than 0.2 per cent of GDP, but with inflation lower than expected earlier subsequent targets may prove harder to achieve, even with upward revisions to growth projections. With government spending already forecast to contract into 2015, further cuts in pursuit of targets for deficits and debt risk derailing growth at the very moment it is gathering pace.

In the labour market, unemployment has fallen slightly, to 25.6 per cent in February from the peak of about 27 per cent reached early last year. The slow decline is expected to continue for seven years before stabilising at around 13–14 per cent, a level consistent with the historical average. The recent decline has been due in part to shrinkage of the labour force arising from emigration, particularly by non-nationals. Employment actually fell for 22 consecutive quarters up to the end of 2013. However, we estimate that employment grew by 0.3 per cent in the year to the first quarter of 2014, and expect employment growth to continue through 2014 and 2015.

Other EU countries in Central and Eastern Europe

Economic growth in Central and Eastern Europe strengthened further in the fourth quarter of 2013, with GDP rising by 0.9 per cent, after its 0.6 per cent increase in the third quarter. Growth differentials among the countries of the area have meanwhile been narrowing. As in the Euro Area, inflation in the region has declined further, partly reflecting continuing substantial output gaps. In Bulgaria, there is a risk of deflation setting in: consumer prices trended downwards through 2013, driven by declines in import prices, administratively set energy prices, and food prices, and the 12-month inflation rate reached −2.3 per cent in March 2014. Inflation has also recently has been below 0.5 per cent in the Czech Republic, Hungary, and the Baltic countries; only slightly higher, at 0.5–0.7 per cent, in Poland and Slovenia; and about 1 per cent in Romania.

We expect GDP growth in the region to pick up by 2.4 per cent this year and 3.2 per cent in 2015, spurred partly by the recovery in the Euro Area but also by strengthening domestic demand. We project that consumer prices in the region will increase by 1.5 per cent this year, and 2.3 per cent next year.

In Poland, the largest country of the region, growth is expected to strengthen from 1.5 per cent last year to 2.9 per cent in 2014 and 3.9 per cent next year. Rising growth is expected to be driven mainly by domestic demand, with the relative contribution of net exports decreasing as the recovery strengthens. Private investment is expected to be particularly buoyant over the next two years, reflecting favourable demand prospects, high capacity utilisation in manufacturing, high levels of liquidity enjoyed by non-financial corporations, and an improving supply of credit. Inflation is expected to be significantly below the 2.5 per cent target of the National Bank of Poland: we forecast that it will pick up from its recent levels and reach 1.4 per cent on an average basis this year and 2.2 per cent in 2015, up from 0.8 per cent last year.

In Hungary, growth is expected to pick up from 1.2 per cent last year to 2.3 per cent this year, driven primarily by domestic demand, and to remain close to this rate in 2015. Private consumption growth will return to positive territory this year, mirroring rising disposable incomes, shored up by cuts in regulated prices and increasing public-sector wages, as well as more favourable credit conditions, including a new subsidised mortgage scheme. Credit conditions for corporations are also expected to ease, which, together with a high pace of absorption of EU funds, will help boost investment. Twelve-month consumer price inflation fell to zero in January 2014. We project that HICP inflation will increase somewhat this year, to an average rate of 1.2 per cent, before rising to 2.4 per cent in 2015, still below the Central Bank's target of 3 per cent.

After six quarters of contraction, GDP in the Czech Republic turned up last spring, and growth strengthened significantly late last year. Average growth was still negative in 2013, at −0.9 per cent, but it is expected to pick up to 1.1 per cent this year, and 2.1 per cent in 2015. The main engine of growth is expected to be domestic demand, benefiting from improving labour market conditions and rising business and consumer confidence. With its benchmark interest rate already close to zero, the Czech National Bank since last November has used foreign exchange market intervention as an instrument of monetary policy, to depreciate the Czech koruna and then maintain the exchange rate close to CZK 27 to the euro. On the back of a drop in regulated prices of electricity, inflation is expected to remain subdued this year, at 1.2 per cent on average, before rising to 2.1 2015, slightly above the official 2 per cent target.

United States

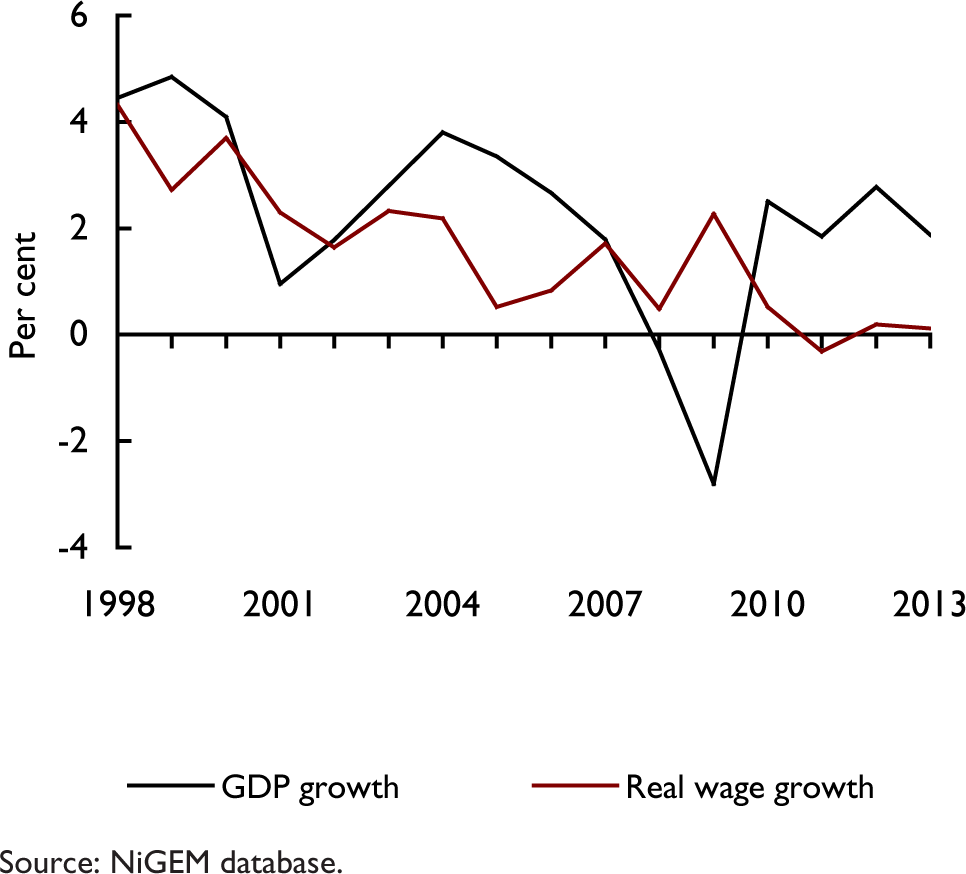

Recent data indicate a continued underlying strengthening of the recovery, despite a period of weakness around the turn of the year related to unusually severe winter weather. GDP growth eased back to 2.6 per cent, annualised, in the fourth quarter of last year from 4.1 per cent in the third, and a further sharp deceleration seems to have occurred in the first quarter. But data for the period since January, including industrial production and retail sales, have been more favourable, and growth seems likely to rebound in the current quarter. In the labour market, non-farm payrolls increased by an average of 195,000 in February and March, compared with the averages of 114,000 in the previous two months and 183,000 in the year to February. Most other indicators also suggest a continuing, slow improvement in the labour market: unemployment in March, at 6.7 per cent, was unchanged from December, but labour force participation has risen slightly in recent months, and broader measures of unemployment have fallen by more. Key indicators of annual wage growth remain subdued at about 2 per cent. Consumer price inflation has remained close to 1 per cent a year: in February, the 12-month change in the price index for personal consumer expenditure was 0.9 per cent, while the increase in the corresponding core index was 1.1 per cent. In March, the 12-month change in the core CPI, a narrower index, was 1.7 per cent. Real wages have recently been stagnant (figure 4).

US GDP and real wage growth

Monetary policy has remained highly accommodative. Judging the economic outlook as broadly unchanged, the Federal Reserve has continued to reduce its monthly ‘QE3’ asset purchases by $10 billion at recent meetings of the FOMC. Thus at the March meeting, it reduced purchases to $55 billion a month from April. It seems likely that such reductions will continue so that the asset purchase programme will expire late this year. Also at its March meeting, the FOMC revised its forward guidance on short-term interest rates. In December 2012 it had introduced an unemployment threshold of 6½ per cent, indicating that it expected that the near-zero federal funds rate would remain appropriate at least as long as unemployment remained above this level and inflation was well behaved. In December 2013, with unemployment having fallen to 7 per cent, it amended this guidance by adding that it expected it to be appropriate to maintain the near-zero federal funds rate “well past the time that the unemployment rate declines below 6½ per cent”, assuming inflation to be well behaved. This March, with unemployment having fallen to 6.7 per cent, the FOMC replaced the quantitative threshold with the qualitative guidance that “In determining how long to maintain the current 0 to ¼ per cent target range for the federal funds rate, the Committee will assess progress – both realized and expected – toward its objectives of maximum employment and 2 per cent inflation”, taking into account a wide range of information. It reiterated that it viewed it as likely that the current target range for the federal funds rate would remain appropriate “for a considerable time after the asset purchase program ends …”.

The FOMC and Chair Yellen emphasised that this was only an “updating” of guidance to take into account the proximity of unemployment to the 6½ per cent threshold, and that it did not indicate any change in policy intentions. Markets, however, initially brought forward somewhat their expectations of the first increase in the federal funds rate, partly because the Federal Reserve's revised projections showed that FOMC participants' assessments of the appropriate federal funds rate at the end of 2015 had risen slightly since December, and partly because in her press conference on March 19 Chair Yellen suggested that the interval between the end of the asset purchase programme and the first increase in the rate would be “something on the order of six months”, though she hedged this with caveats. More recently, however, partly in response to further statements by Yellen, markets have reverted to expecting the first increase in the federal funds rate in the second half of 2015.

Fiscal restraint on economic growth is diminishing after the substantial adjustment of the past three years. In 2013, according to the IMF's estimates, the general government's cyclically adjusted primary balance was reduced by 2.1 per cent of GDP, but its reduction this year is forecast to be only 0.4 per cent of GDP. In mid-April, the CBO revised its baseline forecast of the federal budget deficit to 2.8 per cent of GDP this year and 2.6 per cent of GDP in 2015. Further fiscal gridlock in Congress is unlikely in the near term: in mid-February, Congress approved suspension of the debt ceiling until March 2015.

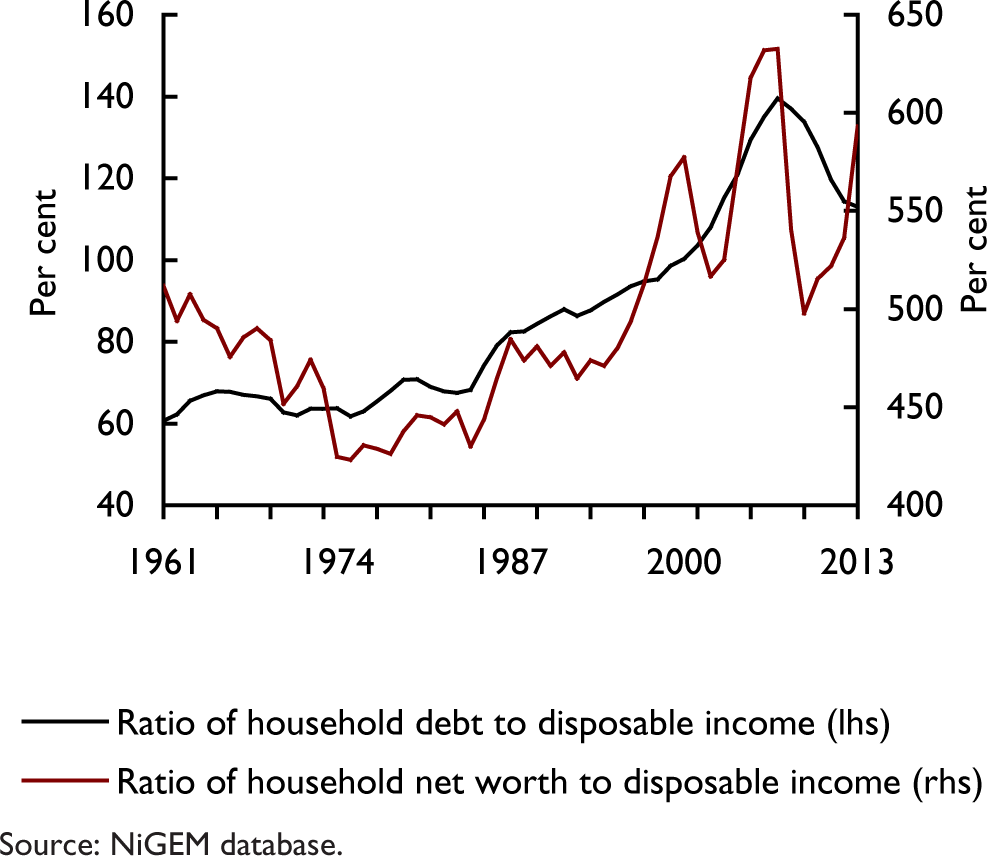

The easing of fiscal drag, together with highly accommodative monetary policy, is expected to help drive a continuing moderate strengthening of growth. Improving labour market conditions should help to boost real wages and consumer spending, which is already being supported by the progress made in reducing household indebtedness and by rising household net worth, partly reflecting rising asset values, notably in the housing and equity markets (figure 5).

US household debt to disposable income and net worth to disposable income ratios

Canada

The improved growth performance observed earlier in 2013, driven largely by household consumption and housing investment, was maintained in the fourth quarter, with GDP growth of 0.7 per cent from the previous three months. For 2013 as a whole, growth was 2.0 per cent, slightly above the forecast in our February Review. Higher-frequency indicators for early 2014, including PMIs, suggest that the expansion has strengthened further.

Consumer price inflation has been below the Bank of Canada's target of 2 per cent since early 2012, partly reflecting the slack in the economy: unemployment has fluctuated around 7 per cent since early last year. But inflation has picked up in recent months from below 1 per cent (on a twelve-month basis) to 1.5 per cent in March, owing partly to a depreciation of about 7 per cent of the Canadian dollar against the US currency between October 2013 and February this year. This depreciation is attributable partly to below-target inflation and accommodative monetary policy, but also to weak export performance in recent years and the authorities' aim of rebalancing growth in favour of exports and investment and away from consumption and residential construction. In mid-April, the Bank of Canada announced that it was maintaining its intervention rate at 1 per cent. Even though the Bank's Governor indicated that the possibility of future rate cuts cannot be dismissed, in our view this is unlikely given the expected rise in inflation towards the target, and the still elevated levels of household leverage and house prices. However, we do not expect official interest rates to be raised until at least 2015. Our inflation projections for 2014 and 2015 are unchanged at 1.7 and 1.8 per cent respectively.

Boosted by the depreciated currency and stronger external demand, especially in the US, exports are expected to be an important contributor to growth this year. Business investment, benefiting from a rebound in producer confidence indicated by recent surveys, and aided by supportive borrowing conditions and stronger corporate balance sheets, is also expected to play a key role in helping to improve growth this year. We have thus raised our growth forecast for 2014 slightly to 2.4 per cent, and this remains our forecast for 2015.

Japan

The government's strategy aimed at reviving economic growth, ending deflation, and attaining a sustainable fiscal position, by means of the ‘three arrows’ of ‘Abenomics’ – expansionary monetary policy, flexible fiscal policy, and structural reforms – has been maintained, but progress towards its objectives has been mixed.

Initially, following the government's election in December 2012 and the introduction of more expansionary fiscal and monetary policies, GDP growth picked up sharply to about 4 per cent at an annual rate in the first half of 2013; but it slowed markedly in the second half, to about 1 per cent. More recent indicators, including industrial production and retail sales, have been more buoyant, and overall growth seems likely to have strengthened in the first quarter of this year, driven partly by consumer spending ahead of the increase in the consumption tax rate from 5 to 8 per cent on April 1.

Progress towards the Bank of Japan's target of 2 per cent annual inflation, fuelled partly by its policy of ‘quantitative and qualitative easing’ begun in April 2013, seems to have stalled in recent months: 12-month core CPI inflation (excluding only seasonal food) was unchanged between December and February, at 1.3 per cent. Progress is expected to resume, however: the Bank's March Tankan survey indicates that enterprises, on average, expected general inflation to be 1.5 per cent in the year ahead and 1.7 per cent annually both over the next three and the next five years. Although somewhat short of the target, this would represent substantial progress from the deflation of the past decade. There have also been signs of a pickup in wages: partly in response to government pressure, a number of major companies announced in mid-March that they would be increasing workers' basic pay, in many cases for the first time since 2008 or earlier. We expect average consumer price inflation to rise slightly above the target to 2.2 per cent this year, boosted by the sales tax increase, but to ease back to about 1.5 per cent in 2015 and 1.3 per cent in the medium term.

Japanese gross government debt, relative to GDP, remains the highest in the world: it was about 220 per cent at end-2013; net government debt was about 135 per cent of GDP. The government's objectives with regard to economic growth and inflation are directed partly towards reducing the real burden of this debt over time. But in addition, the government is appropriately committed to sizeable fiscal consolidation – to halving the primary deficit by 2015 and returning it to surplus by 2020, thereafter slowly reducing the absolute level of debt. The sales tax increase on April 1 this year is part of this consolidation effort; a further increase in the rate, to 10 per cent, is planned for October 2015. Also contributing to fiscal tightening will be the unwinding both of reconstruction spending related to the 2011 tsunami and nuclear accident, and of the 2013 fiscal stimulus. Current budget plans, however, taking into account stimulus spending this year intended to offset the effect of the April tax hike, imply that fiscal consolidation will not begin until 2015, and this is what our forecast assumes. A concrete plan is yet to be announced for the further substantial fiscal consolidation that will be needed over the medium term. This adjustment will need to be managed in a way that does not jeopardise the other aims of Abenomics.

Partly because of the recent sales tax increase, consumption growth is likely to weaken in the second quarter, before rebounding in the second half of the year. We expect consumption to grow by around 1 per cent in 2014 as a whole and 0.5 per cent in 2015.

One of the effects of the monetary easing undertaken by the Bank of Japan has been a large depreciation of the yen – by about 24 per cent in terms of the US dollar since October 2012. However, export growth has remained weak. This may be due to J-curve effects, but it may also suggest some underlying structural problems with the export sector. We expect export volume growth to remain flat in 2014 at around 2.8 per cent, before picking up in 2015 to above 5.6 per cent. Import growth has been robust, partly due to Japan's increased reliance on imported fuels, and we expect this to remain so over our forecast horizon.

Taking into account the slowing of growth in the latter part of 2013, we expect average GDP growth to weaken somewhat in 2014, to 1.3 per cent, and this rate to be maintained in 2015. If growth weakens unduly, it will be important for the Bank of Japan to undertake further easing action.

The longer-term prospects for the growth and debt reduction strategy will depend partly on the ‘third arrow’ of Abenomics – structural reform – where progress has remained slow. The effectiveness of the special strategic economic zones intended to increase investment remains to be seen. Negotiations on the Trans-Pacific Partnership are reported to have encountered difficulties, including on the liberalisation of Japan's agricultural imports. Other mooted reforms, such as reducing the corporate tax rate and encouraging an increased participation rate of woman in the labour force, remain to be specified. Liberalisation of immigration policies, which could also help Japan address the constraint on growth formed by its declining labour force, remains to be addressed.

China

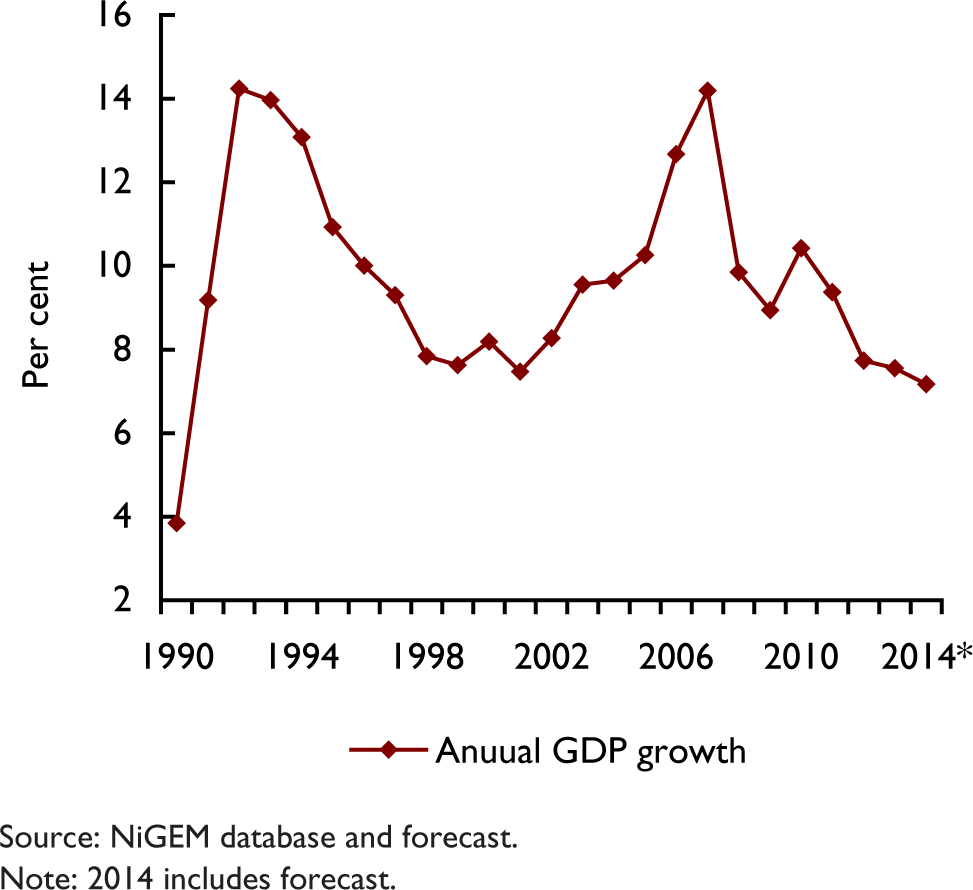

Economic growth in China has continued its moderate slowdown. In the year to the first quarter of 2014, GDP rose by 7.4 per cent, the lowest four-quarter growth rate since 2012, and the expansion we forecast for this year as a whole, at 7.2 per cent, would be the slowest annual growth since 1990 (figure 6). GDP data for the first quarter surprised some observers on the upside, given indications in some other data of a marked slowing in recent months. In March, the Prime Minister announced that the official target for GDP growth in 2014 was 7.5 per cent, unchanged from 2013. A month later, in response to signs of slower growth, the government introduced a ‘minipackage’ of measures to support the expansion, including tax breaks for SMEs and targeted infrastructure spending. It has also indicated, however, that its GDP growth target has some flexibility – that it is less concerned with this precise target than with ensuring adequate employment growth and promoting the transition to a growth model less dependent on investment, exports, and credit, and that it does not envisage a larger stimulus package unless these priorities are jeopardised. A continuing moderate slowdown still seems the most likely prospect, and we expect GDP to expand by about 7.2 and per cent this year and 7.0 per cent in 2015.

China: annual GDP growth

Significant downside risks to this forecast remain, however, from the ongoing shift in the growth model and the associated moderation of credit expansion already in progress, especially given unusually high corporate leverage, local government debt, and real estate investment. To illustrate the possible effects of a more severe drop in Chinese domestic demand on world GDP, oil prices and output in selected Asian economies we ran a simulation using NIESR's global econometric model: see Box A (page 19) of this Review.

Box A. Effects of a drop in Chinese domestic demand on world GDP, oil prices and output in selected Asian economies

China is the second largest economy in the world (based on GDP at PPP exchange rates) and its contribution to world output growth has increased from less than one tenth in the early 1980s to more than a third since 2011. China's annual GDP growth, after exceeding 9 per cent in eight out of ten years since 2002, has recently slowed and in 2013 was 7.7 per cent.

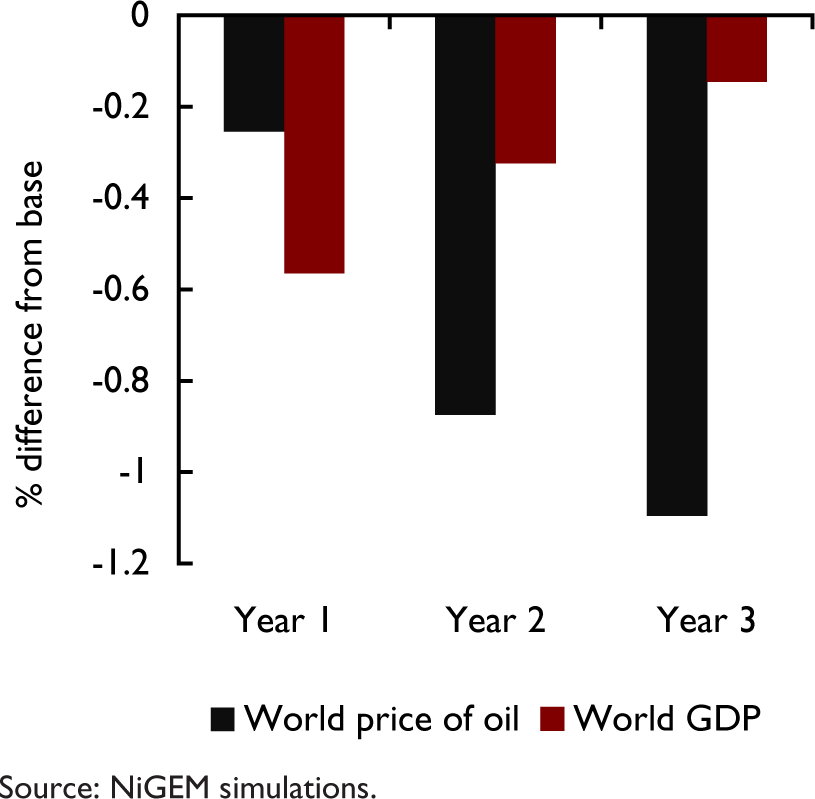

Our baseline forecast shows a continuing moderate slowing in China's growth. But what if growth slows more abruptly? In this box we use the National Institute's model, NiGEM, to estimate the likely effects of a reduction in China's output, via weaker domestic demand, on world GDP, oil prices and the output of China's trading partner countries in Asia. In the simulation, output in China is reduced via an endogenous temporary decrease in domestic demand (the dynamics of demand response are taken into account). The Renminbi is assumed to be pegged to the US dollar and oil prices are determined endogenously, allowing them to react, in particular, to changes in the energy intensity of world output. Chinese domestic demand is assumed to fall by about 5 per cent from the baseline value over the first two years, which reduces GDP by about 2.3 per cent as compared to the baseline projection.

The reduction in Chinese demand reduces world oil prices and world output (figure A1). The effect on world GDP is felt straight away, but oil prices react more slowly and are reduced by about 1 per cent after three years. World output is reduced by just under 0.5 per cent for two years, but the impact is transitory as other components of global demand adjust.

Effects of a reduction in Chinese domestic demand on world GDP and oil prices

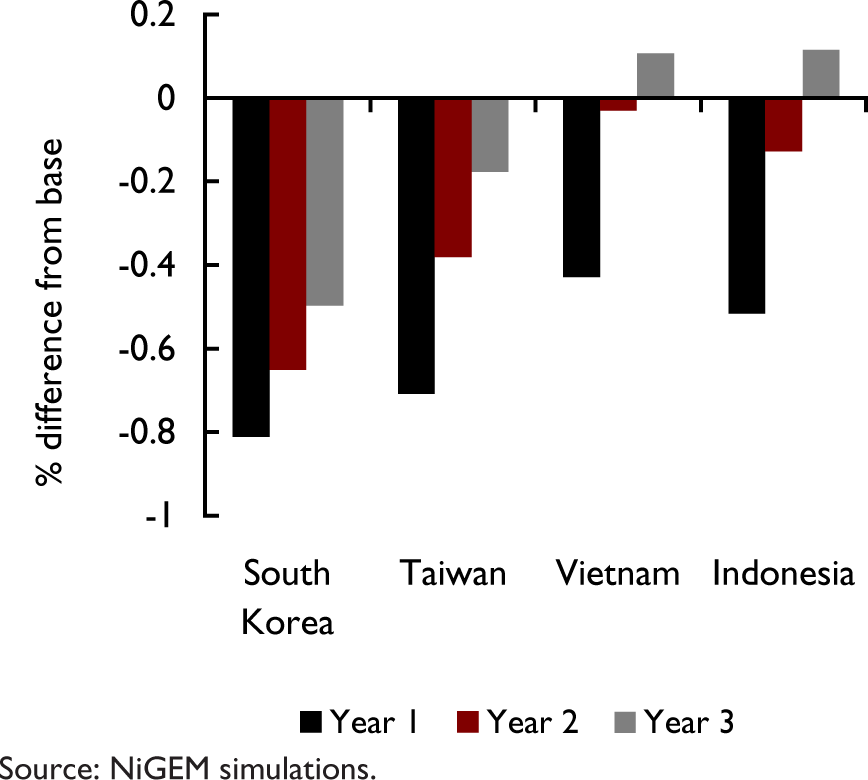

The drop in China's domestic demand has a heterogeneous effect on its trading partner countries, with a combination of factors having a role to play: the immediate direct effect of a reduction in demand from China will vary among countries depending on the share in each country's GDP of exports to China; there will also be an indirect effect via the reduction in world demand, changes in the terms of trade, and changes in the oil intensity of output. Figure A2 illustrates the effect on GDP relative to baseline values for selected Asian countries from the assumed drop in Chinese domestic demand. Countries that are major suppliers of intermediate products to China, like South Korea and Taiwan, are affected the most, while minor suppliers of intermediate products, like Indonesia and Vietnam, are affected significantly less in terms of both the depth and the duration of the shock.

Effect of a reduction in Chinese domestic demand on GDP in selected Asian countries

Corporate debt has risen from 85 per cent of GDP in 2008 to about 120 per cent recently, and a large proportion of this debt is due for repayment or renewal this year. Concerns about the productivity of the investment financed by this credit expansion, together with fears of slowing economic growth, have given rise to increased concerns about corporate default. In early March, China's first corporate bond default occurred, and a week later the Prime Minister warned that “isolated cases of default will be unavoidable”. These developments suggest a shift in policy after many years of corporate bailouts. One of its consequences may be to heighten awareness of risk in the financial sector – a pre-condition for liberalisation of the sector.

Indeed, further steps have been taken towards financial and exchange market liberalisation. In early March, there was the first official indication of the timing of further interest rate liberalisation, including of deposit rates: the Governor of the People's Bank said that he expects to see full interest rate liberalisation in 1–2 years. Beginning in mid-February, after a prolonged period of appreciation against the US dollar, the renminbi's exchange rate turned around and the currency began to depreciate slowly. Officials indicated that this was a deliberate result of intervention, intended both to show that the exchange rate did not offer a one-way bet (partly to discourage speculative capital inflows) and to prepare the currency for wider trading. A month later, the PBoC announced that, beginning on March 17, the width of the daily trading band for the renminbi/dollar exchange rate would be doubled to 2 per cent either side of the parity rate, which continues to be fixed daily by the PBoC. (The half-width of the band had last been widened in April 2012 from 0.5 per cent, and before that in May 2007 from 0.3 per cent.) The slow and limited depreciation has continued, and by late April the yuan was 2.6 per cent lower in terms of the US dollar than in mid-February, at a level last seen in April 2013. China's effective exchange rate, however, both in real and nominal terms, has continued to appreciate.

India

Economic growth has recently remained broadly stable, in the 4½–5 per cent range prevailing since early 2012 – roughly half the rates experienced in much of the previous decade. Thus GDP increased by 4.6 per cent in the year to the final quarter of 2013, and by 4.4 per cent in 2013 as a whole, the lowest average annual growth rate since 2001. Growth in 2013 was driven predominantly by services; manufacturing contracted and construction was virtually stagnant. Data for early 2014 indicate that private sector activity has continued to stagnate, especially in manufacturing. Slow growth in recent years has been attributed to delays in infrastructure project approvals and uncertainty over government policies. Current general elections (results due on May 16) should help resolve some of these issues and lead to an investment recovery. On this assumption, growth is likely to strengthen moderately, with GDP expanding by 5.4 and 5.8 per cent, respectively, this year and next.

Inflation has eased recently, the 12-month change in consumer prices falling to 8.3 per cent in March, compared with its peak last November of 11.2 per cent. In light of high and rising inflation, the Reserve Bank raised its benchmark interest rate by 25 basis points three times between September 2013 and January 2014, to 8 per cent. This moderate tightening of monetary policy has helped lower inflation, partly by helping to strengthen the rupee. After losing about a fifth of its value, in US$ terms, between May and August 2013, the currency has since recovered more than half of this fall. We expect inflation to continue declining, towards 7.0 per cent on average in 2015. Sharper tightening of monetary policy may be needed to reduce inflation further, for example to meet the 4 per cent target that the Reserve Bank is considering.

Other factors contributing to the rupee's recovery since last summer, apart from the rise in interest rates, include increased capital inflows drawn by expectations of more business-friendly policies after the election, and improvements in macroeconomic imbalances. Last year's actions by the government and the Reserve Bank to curb gold imports, plus an improvement in export performance, have helped reduce the current account deficit since early last year. On the fiscal front, the government announced in February tax cuts aimed at boosting consumption and lifting the weak economy ahead of the elections, while stressing its commitment to its deficit target. The budget deficit was estimated by the government to have been 4.6 per cent of GDP in the fiscal year ended March 2014, less than the 4.8 per cent target for 2013/14 and the 4.9 per cent outturn for the previous fiscal year.

Box B. Economic implications of recent developments in Ukraine

Recent developments in Ukraine, including the overthrow of the government in late February, the Russian annexation of Crimea in March, the conflict and political instability in eastern Ukraine, and the sanctions imposed on Russia by many countries, are already having economic consequences. In the current context of considerable uncertainty about how this geopolitical crisis may evolve, this box attempts to evaluate what the potential economic implications may be.

Thus far, the Ukraine crisis has had clear economic repercussions on Ukraine itself and on Russia – two economies that were already weak in different degrees. But, as yet, broader effects, in global markets and other national economies, have been more difficult to discern.

As discussed in the main text, the crisis had immediate effects on Russian financial markets, raising official and market interest rates, lowering equity prices, and increasing capital outflows. In March, Fitch lowered Russia's debt rating from stable to negative, implying additional difficulties for funding through international capital markets. The increased cost and reduced availability of finance, the application of international sanctions, and the fiscal burden of the Crimean annexation will all damage the Russian economy. It has been estimated that the fiscal costs of the annexation of Crimea, together with budgetary support for the region in the short term alone, could be about 2 per cent of GDP. This adds further pressure to a budget that is already under strain, and which relies heavily on revenue from oil sales. This dependence means that any significant disruption of fuel exports could end prospects for the achievement of the budget targets for 2014–15. In fact, 2013 saw the first deficit in Russia's consolidated budget since the financial crisis, which indicates the vulnerability inherited from last year.

With regard to Russia's external sector, a moderate pick-up in exports this year and lower import demand, both helped by a depreciation of the rouble by about 11 per cent between last October and February, are expected to partly offset a marked deterioration in the capital account. On net, however, the significant downward pressure on the rouble seen in recent weeks is likely to continue, and this will have to be absorbed by a continuing depletion of foreign exchange reserves unless interest rates are raised further or the currency is allowed to depreciate. Russia's official reserves are among the largest in the world, but downward pressure on the rouble has led to substantial declines in recent weeks. As of 1st April, international reserves amounted to $486 billion, down from $528 billion a year earlier.

On Ukraine, its finance minister has recently predicted that the economy will contract by 3 per cent in 2014. Persistence of the crisis would likely cause the economy to continue contracting in 2015. Ukraine's economic vulnerability stems from a number of factors. First, already before the crisis, Ukraine suffered from severe macroeconomic imbalances and governance problems. Second, Russia buys about 20–25 per cent of its exports; if Russia continues to restrict the flow of imports coming from Ukraine, it will particularly damage Ukrainian manufacturers. Third, Ukraine relies on Russia for about 63 per cent of its supply of natural gas. Since April, Russia has raised the price that Ukraine has to pay for Russian gas, to levels higher than those paid by any EU country. This adds to Ukraine's sizeable debt to Russia, which, if defaulted upon, could put part of Europe's energy supply at risk next winter. Financing in prospect through Ukraine's expected programme with the IMF should prevent this, however. Finally, the crisis has called for increased defence spending, which adds to Ukraine's fiscal problems.

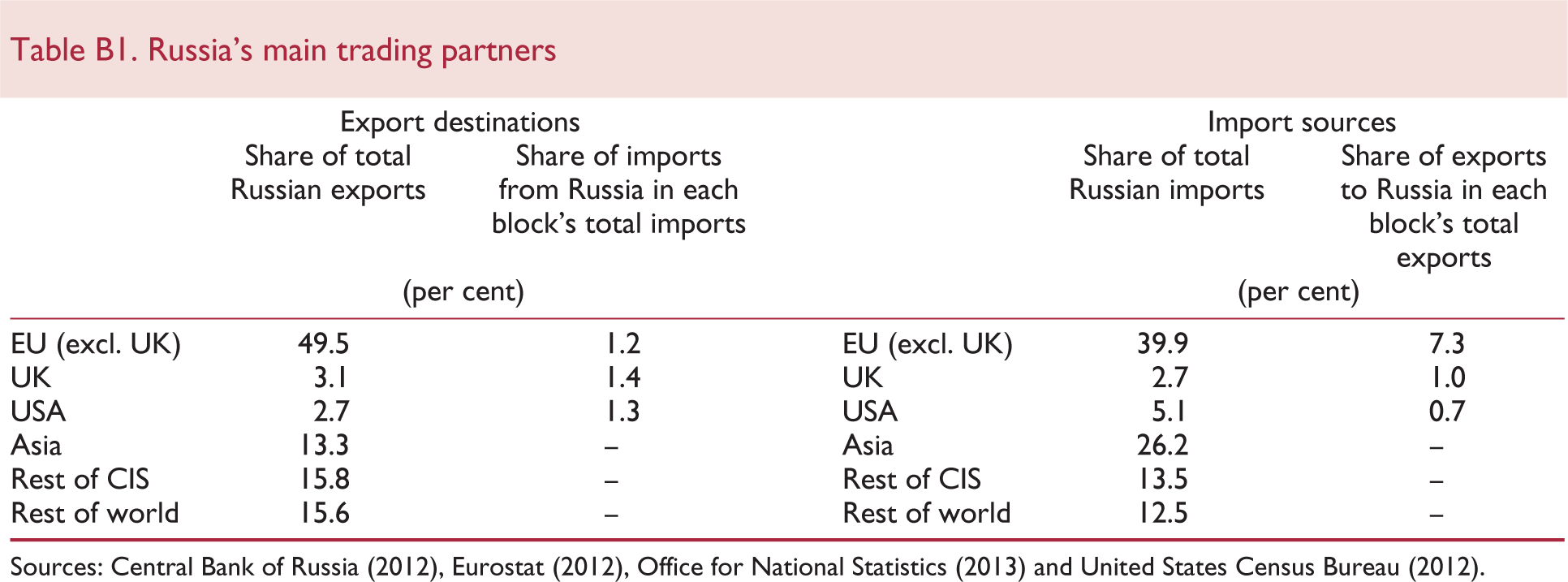

What about the impacts on other countries? Table B1 shows Russia's main trading partners. In light of these numbers, a sharp contraction in Russian imports from the EU would hurt the EU economy. As an illustration, a temporary downward shock to Russian domestic demand resulting in a 20 per cent decrease in Russian import demand this year, simulated using the National Institute's model NiGEM, would lead to an estimated 0.25 per cent drop in Germany's GDP, while having a greater proportionate impact on neighbouring CEE and Baltic economies, where GDP would fall by about 0.3–0.8 and 0.9–2.5 per cent, respectively. Given the added dependence of certain countries (chiefly, the countries geographically closest to Russia) on Russian energy imports, any disruption of trade would be harmful for both regions. However, while the EU is a major buyer of Russian exports, only a small share of the EU's exports are shipped to Russia. (According to data from the German Federal Statistical Office, Destatis, only about 10 per cent of all exporting enterprises in Germany export goods to Russia and, for about 73 per cent of them, exports to Russia account for no more than a quarter of their total exports.) Hence, any worsening of relations leading to a lower volume of trade between the EU and Russia would hurt the latter more than the former. With regard to the US, its exports to Russia are smaller, relative to its total exports, than they are for the EU.

Russia's main trading partners

Sources: Central Bank of Russia (2012), Eurostat (2012), Office for National Statistics (2013) and United States Census Bureau (2012).

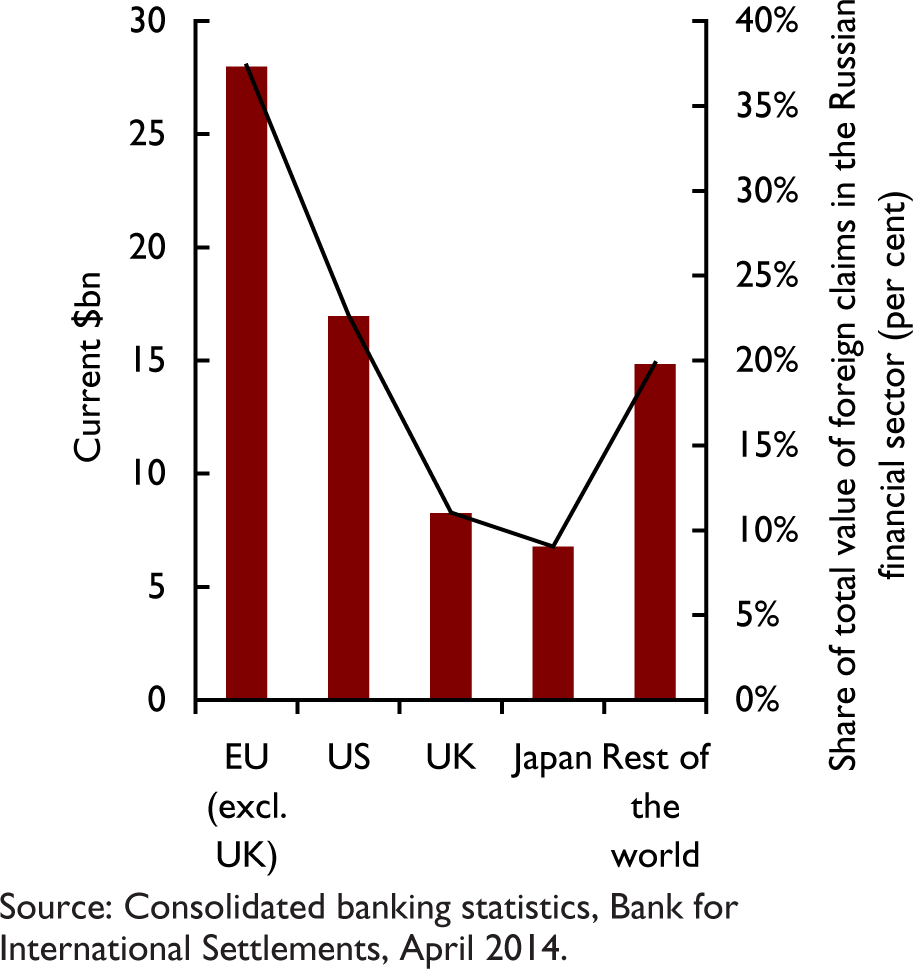

With respect to the degree of financial exposure of foreign investors in Russia, Figure B1 displays the value of assets in the hands of nationals of the countries and country groups with the highest presence in the Russian financial (private and public) sector. The chart shows that the imposition by Russia of sanctions in the form of, for instance, asset freezes, would harm foreign investors. Also, although this seems very unlikely at present, Russia could default on its sovereign debt, a significant part of which is held as assets by foreign banks. The risks that these possibilities pose for foreign owners of Russian assets notwithstanding, the escalation of sanctions and/or threats would, as in the case of trade, arguably hurt Russia to a greater extent. If measures such as economy-wide asset freezes materialise, the very negative precedent created would be likely to severely reduce foreign direct investment inflows to the Russian economy, which could, in the worst case scenario, suffer long periods of financial autarky. Any threat of retaliatory measures would most likely be followed by a sharper outflow of capital, which would notably impair the Russian balance of payments, financing possibilities and productive capacity.

Selected countries' exposure to the Russian private and public financial sectors, 2013Q4

Finally, concerning energy security, even though Russian gas represents roughly one third of the EU's total gas imports, a disruption in the flow would arguably be more damaging to Russia than to the EU, for several reasons. First, partly because of the increase in European domestic production and the shift in energy sources, the ratio of the volume of Russian gas imports to total EU energy consumption has recently declined: at 12 per cent in 2012, it reached its lowest level since 2003, after having reached a ten-year peak in 2008, at 14 per cent. Second, Russia's economy is still heavily reliant on its endowment of natural resources, both for its balance of payments and to finance its budget. Third, European leaders are already looking to reduce their dependence on Russian energy by developing alternative sources such as shale gas, which improves the degree of substitutability of Russian gas. This has been underscored as one of the reasons why the economic impact of a halt in incoming Russian gas and oil on Western economies would be significantly less than that of the 1970s oil crisis. Hence, it seems in Russia's interest to find a compromise solution to the gas dispute over the Ukrainian gas bill, for example, in order not to jeopardise gas revenue from Europe, which may prove crucial in a context characterised by very weak economic resilience.

To conclude, while political uncertainty remains very high, the Ukraine crisis seems likely, short of a major escalation, to have a significant, but small, negative impact on growth in the EU overall, including Germany, and a negligible impact on the rest of the global economy. However the significant negative consequences of the crisis for the Russian economy are already apparent, and as argued in the main text and in this box, are likely to worsen if the situation deteriorates further.

Brazil

S&P's downgrade of its sovereign credit rating for Brazil in March, from BBB+ to BBB–, reflects a plethora of issues plaguing the economy, including deteriorating public finances, sluggish growth, and a widening current account deficit, which in 2013 was the largest since 2001. A contraction of GDP in the third quarter of last year was followed by an upturn in the last quarter, based largely on a rise in exports attributable partly to the depreciation of the Real since mid-2011. The average growth rate of GDP in 2013 was 2.3 per cent, up from 1.0 per cent in 2012. This improvement in performance occurred despite a widening of the external deficit, which stemmed partly from a pick-up in domestic investment that generated a substantial increase in imports.

The central bank has taken further action to reduce inflation to its target of 4.5 per cent a year. It has raised its benchmark (Selic) interest in nine steps over the past twelve months, most recently by 25 basis points each in late February and early April. The Selic now stands at 11.0 per cent, and the central bank has signalled that the peak may not have been reached. Recently, 12-month consumer price inflation has turned up again, reaching an eight-month high of 6.2 per cent in March. Given capacity constraints, including the tight labour market – unemployment in February stood at 5.1 per cent – it seems unlikely that inflation will soon converge on the target. Thus, we have revised up our projections for average inflation in 2014 and 2015, to 6.0 and 5.6 per cent respectively.

The boost to exports this year from strengthening demand in advanced economies and the Real's depreciation since 2011 is likely to be partly offset by the effects of weaker growth in Argentina and China, two of Brazil's key trading partners. And an improvement in the external sector is unlikely to compensate for an expected weakening of investment growth, reflecting business confidence that has recently been at its lowest since 2009. We have thus reduced our growth forecast for 2014 marginally to 1.8 per cent. The persistence of supply constraints, especially in infrastructure, coupled with the likely implementation of more restrictive policies after the October elections, have also led us to lower our growth forecast for 2015 to 2.3 per cent.

The combination of twin deficits, persistently high inflation, capacity constraints, and slow growth makes Brazil vulnerable to possible adverse shocks. To improve the economy's performance and resiliency, decisive efforts are needed to strengthen the public finances, promote investment, and enhance competitiveness.

Russia

Growth in Russia was already weak before its intervention in Ukraine in late February and its absorption of Crimea: in mid-February, the Central Bank lowered its forecast of GDP growth this year to 1.5–1.8 per cent, compared with the government's earlier forecast of 2.5 per cent. Subsequently, short-term growth prospects have deteriorated markedly, as acknowledged by Russian officials: in mid-April the finance minister was reported to have said that growth this year would perhaps be around zero. In fact, GDP estimates for the first quarter of 2014 already show a drop of 0.5 per cent from the final quarter of last year. Reduced growth prospects are due to less favourable financial conditions, arising partly from increased private capital outflows, and to the effects of international sanctions.

Immediately after the start of Russia's intervention in Crimea, on 3 March, the Central Bank raised its benchmark interest rate to 7.0 per cent from 5.5 per cent (the first change in 17 months), referring to the need to address risks to inflation and financial stability arising from increased financial market volatility. It raised the rate again in late April, to 7.5 per cent. Also, since late February, 10-year government bond yields have risen by about 90 basis points. These increases in interest rates, together with reported official intervention in the foreign exchange market, have helped maintain broad stability in the rouble's exchange rate in US$ terms. Despite the rise in domestic yields, there has been a surge in capital outflows: net outflows in the first quarter of the year, at more than $50 billion, roughly matched outflows in the whole of 2013. Moreover, the stock market has declined by about 7 per cent since late February.

The increased costs of domestic finance, and the increased cost and reduced availability of foreign finance linked partly to international sanctions, now weigh on Russian growth. We expect GDP growth in 2014 to be slightly negative, at −0.1 per cent. On the assumption that the geopolitical situation does not deteriorate, we project an upturn in 2015, with 1.4 per cent growth. Monetary policy is unlikely to be available to boost demand, because of both exchange rate pressures and persistent inflation: 12-month consumer price inflation picked up to 6.9 per cent in March, significantly higher than the Central Bank's informal target of 5.0 per cent for 2014. With expectations not well anchored, our inflation forecasts for 2014 and 2015 are revised upwards to 6.0 per cent and 5.6 per cent, respectively. Meanwhile, hopes have diminished for the improvement in business confidence and the investment climate that Russia badly needs to strengthen longer-term growth.