Abstract

The forecasts for the world and the UK economy reported in this Review are produced using the National Institute's model, NiGEM. The NiGEM model has been in use at NIESR for forecasting and policy analysis since 1987, and is also used by a group of about 40 model subscribers, mainly in the policy community. Most countries in the OECD are modelled separately, and there are also separate models of China, India, Russia, Brazil, Hong Kong, Taiwan, Indonesia, Singapore, Vietnam, South Africa, Turkey, Estonia, Latvia, Lithuania, Slovenia, Romania and Bulgaria. The rest of the world is modelled through regional blocks so that the model is global in scope. All models contain the determinants of domestic demand, export and import volumes, prices, current accounts and net assets. Output is tied down in the long run by factor inputs and technical progress interacting through production functions, but is driven by demand in the short to medium term. Economies are linked through trade, competitiveness and financial markets and are fully simultaneous. Further details on the NiGEM model are available on http://nimodel.niesr.ac.uk/.

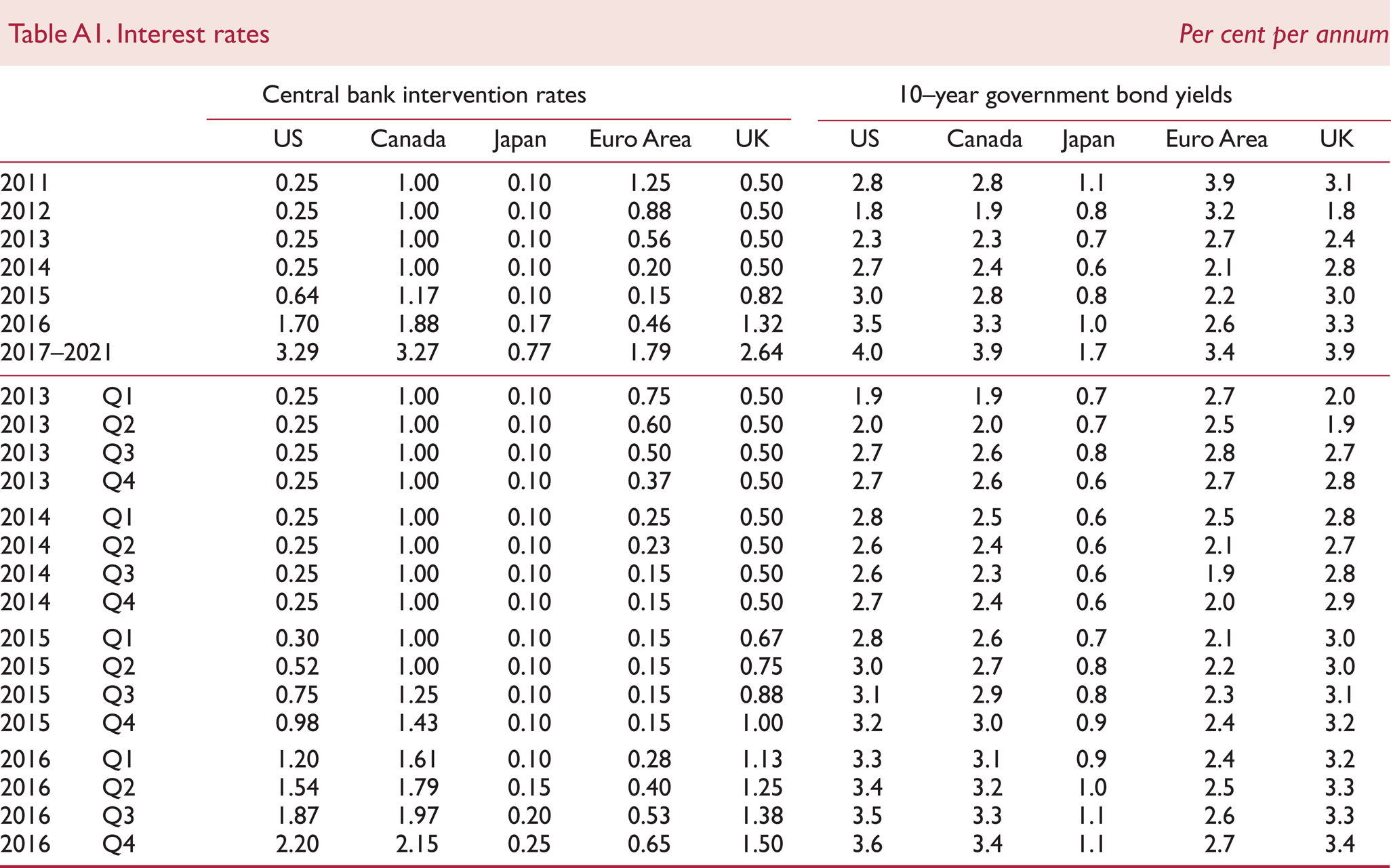

The key interest rate and exchange rate assumptions underlying our current forecast are shown in tables A1–A2. Our short-term interest rate assumptions are generally based on current financial market expectations, as implied by the rates of return on treasury bills and government bonds of different maturities. Long-term interest rate assumptions are consistent with forward estimates of short-term interest rates, allowing for a country-specific term premium in the Euro Area. Policy rates in the major advanced economies are expected to remain at extremely low levels at least until the beginning of 2015. The Reserve Bank of Australia and the Mexican central bank reduced interest rates through 2013 by 50 and 100 basis points respectively and while the Reserve Bank of Australia has kept rates unchanged since, the Mexican central bank cut them by a further 50 basis points in July 2014. After introducing a 25 basis point interest rate cut last year, the Bank of Korea has kept its policy interest rates unchanged. The central bank of Sweden reduced its policy rate by 50 basis points in July, the first reduction since December of last year. The central bank of Turkey has continued lowering its policy rate, bringing it down by 175 basis points in three rounds since April 2014. Since last autumn, both the central banks of Hungary and Romania have lowered their interest rates. The Romanian Central Bank lowered its interest rate by 75 basis points in three steps and has kept rates unchanged since April. The central bank of Hungary brought them down by 110 basis points in eight rounds. In contrast, several emerging market economies have tightened monetary policy in response to inflationary and financial market pressures, most notably in Brazil, Indonesia, India, Russia and South Africa. After raising interest rates in the first quarter of this year, India, and Brazil have kept their interest rates unchanged, while in South Africa and Russia interest rates were increased by a further 25 and 50 basis points respectively. The central bank of New Zealand has increased its policy rate by 75 basis points in four steps since the beginning of the year. 1

Interest rates Per cent per annum

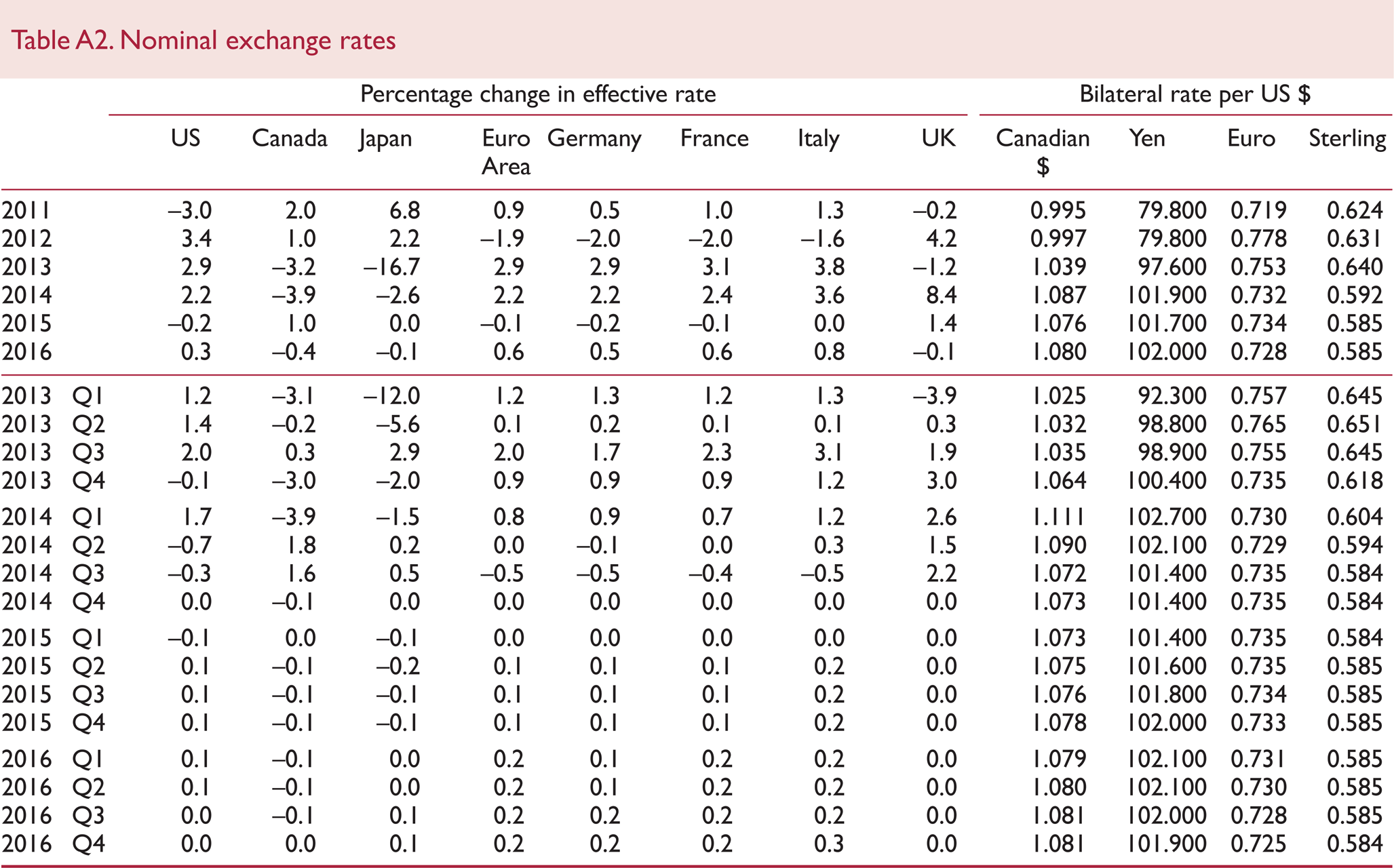

Nominal exchange rates

Policymakers in the US and UK are expected to begin to raise interest rates in the first half of 2015, pre-empting rate rises in the Euro Area by four quarters. This is broadly consistent with the interest rate path for the US signalled by the Federal Open Market Committee (FOMC). In March the FOMC replaced its quantitative threshold with qualitative guidance, emphasising that it did not indicate a change in policy intentions, but rather was adjusting guidance due to the proximity of the unemployment rate to the 6½ per cent threshold of its original forward guidance policy. Instead of a single threshold (the 6½ per cent unemployment rate), the FOMC will take into account a wide range of data (consistent with its objectives of maximum employment and an inflation rate of 2 per cent per annum) while determining the path of the federal funds rate. But despite changes in its guidance the FOMC expects the target range for the federal funds rate to remain unchanged for a “considerable time after the asset purchase program ends”. 2

At the meeting in December 2013, the FOMC announced a modest reduction in the pace of its asset purchases, by $10 billion a month starting in January 2014, on the back of the cumulative progress towards full employment and improvements in the outlook for the labour market. FOMC has consistently implemented this policy decision in each month since January 2014. The Federal Reserve decided in mid-June that from July ‘tapering’ would accelerate to $35 billion per month. The minutes of the June meeting also indicated that the FOMC expects tapering to conclude with a $15 billion reduction in purchases in October 2014. In contrast, the ECB and the Bank of Japan are considering reintroducing further rounds of balance sheet expansion. In early June, the ECB announced measures, expected for several months, to ease monetary conditions further and boost bank lending to the private sector. These included the further lowering of its key interest rates: the rate on its main refinancing operations by 10 basis points (b.p.) to 0.15 per cent; the rate on its marginal lending facility by 35 b.p. to 0.40 per cent; and the rate on its deposit facility (and on excess reserves) by 10 b.p. to −0.10 per cent. The ECB thus became the first major central bank to lower a benchmark interest rate into negative territory. The Bank indicated that although its rates had now, for all practical purposes, reached their lower bound, it was “unanimous in its commitment to using unconventional instruments” (in particular, bond-buying) if necessary.

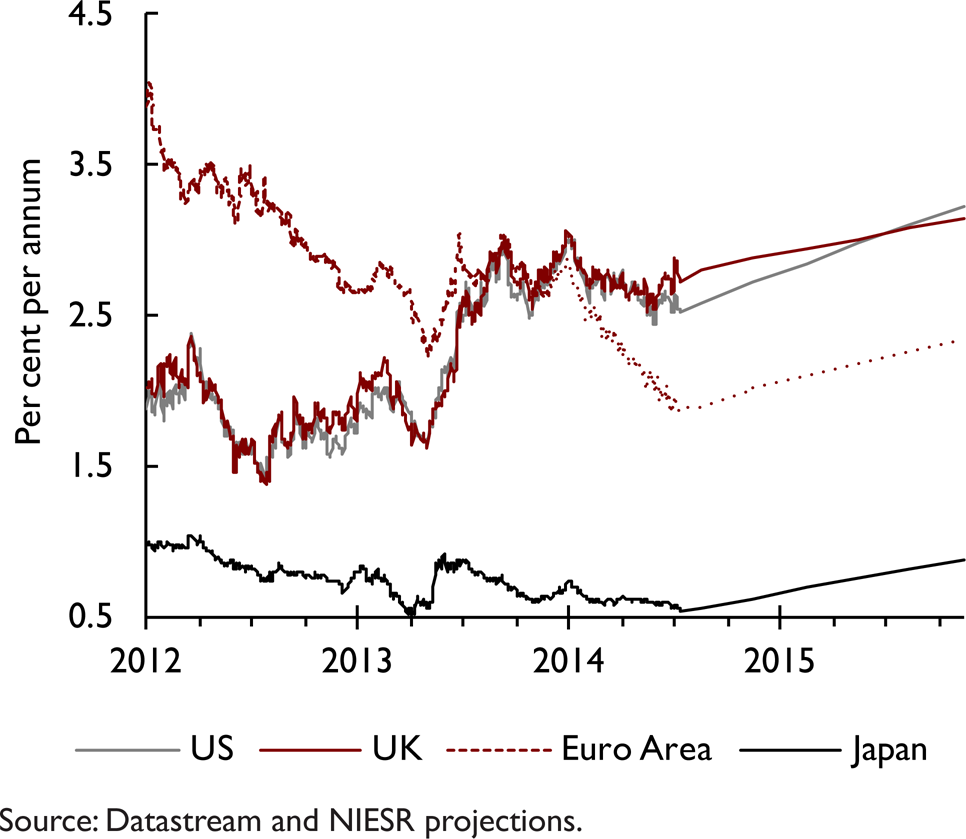

Figure A1 illustrates the recent movement in, and our projections for, 10-year government bond yields in the US, Euro Area, the UK and Japan. Government bond yields in the US, Euro Area and the UK picked up towards the end of December last year, but have drifted down since and have stayed broadly unchanged recently. Convergence in Euro Area bond yields towards those in the US, observed since the start of 2013, reversed at the beginning of this year. Since February 2014, the margin between Euro Area and US bond yields started to increase, reaching more than 80 basis points (in absolute terms) in July. The expectations for bond yields throughout 2014 are lower than expectations just three months ago in the US, Euro Area and Japan and are marginally higher in the UK. However, while the expectations for yields in the US and Japan are marginally lower (ranging from about 10–20 basis points), expectations of yields in the Euro Area have fallen by more; by approximately 40 basis points.

10-year government bond yields

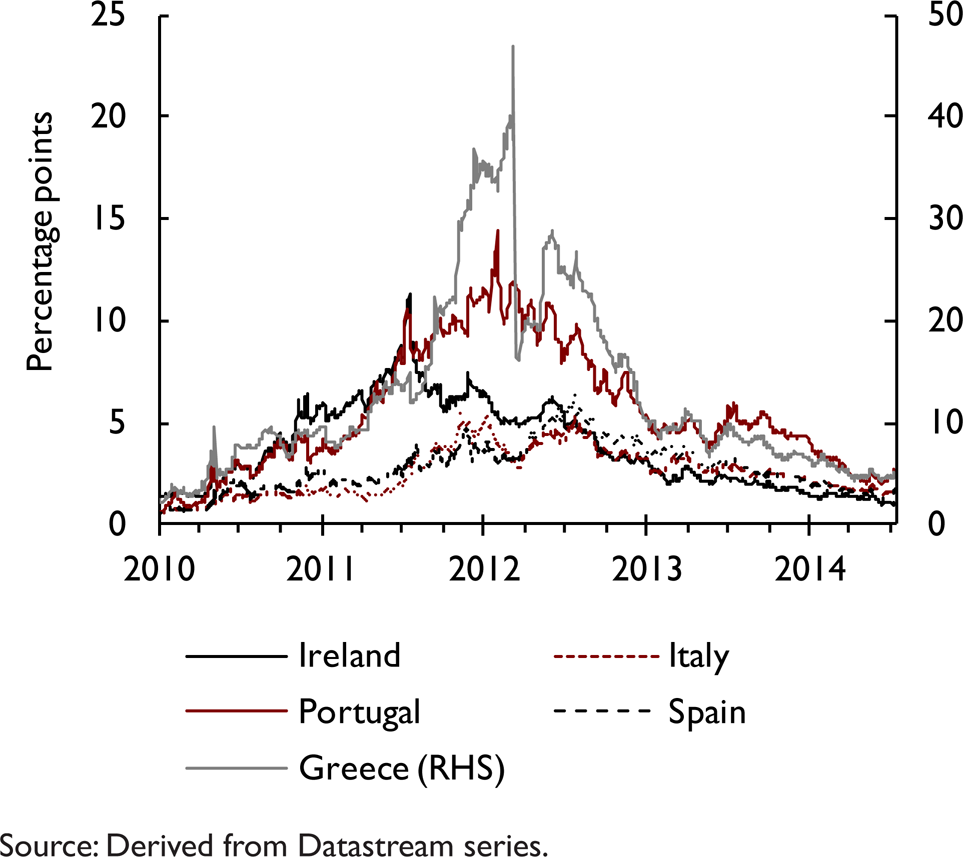

Sovereign risks in the Euro Area have been a major macroeconomic issue for the global economy and financial markets over the past three years. Figure A2 depicts the spread between the 10-year government bond yields of Spain, Italy, Portugal, Ireland and Greece over Germany. The final agreement on Private Sector Involvement in the Greek government debt restructuring in February 2012 and the potential for Outright Money Transactions (OMT) announced by the ECB in August 2012 brought some relief to bond yields in these vulnerable economies. During summer 2013 there was some upward pressure on yields in Portugal, related to uncertainty over its fiscal austerity programme, parts of which were declared unconstitutional by the Portuguese Constitutional Court. However, better than expected GDP figures for the second quarter of 2013 calmed the financial markets somewhat and bond spreads narrowed. In June 2014, as foreshadowed in preceding weeks by its officials, the ECB announced a number of measures aimed at providing additional monetary accommodation and supporting bank lending to the private sector, with the ultimate aim of supporting aggregate demand and raising inflation nearer to the target of “below, but close to, 2 per cent”. Sovereign yield spreads generally narrowed further in most Euro Area countries, but have somewhat widened in Portugal (where questions arose in July about the solvency of a major commercial bank) and Greece (on the back of heightened risks perceptions).

Spreads over 10-year German government bond yields

In our forecast, we have assumed spreads over German bond yields continue to narrow in all Euro Area countries. In the case of Portugal, we have taken into account its exit from its international bail-out programme in May 2014, which caused a modest jump in its funding costs in the near term, as a result of the return to market sources for funding. The implicit assumption underlying this is that the Euro Area continues to hold together in its current form and further progress will be made towards establishing a banking union.

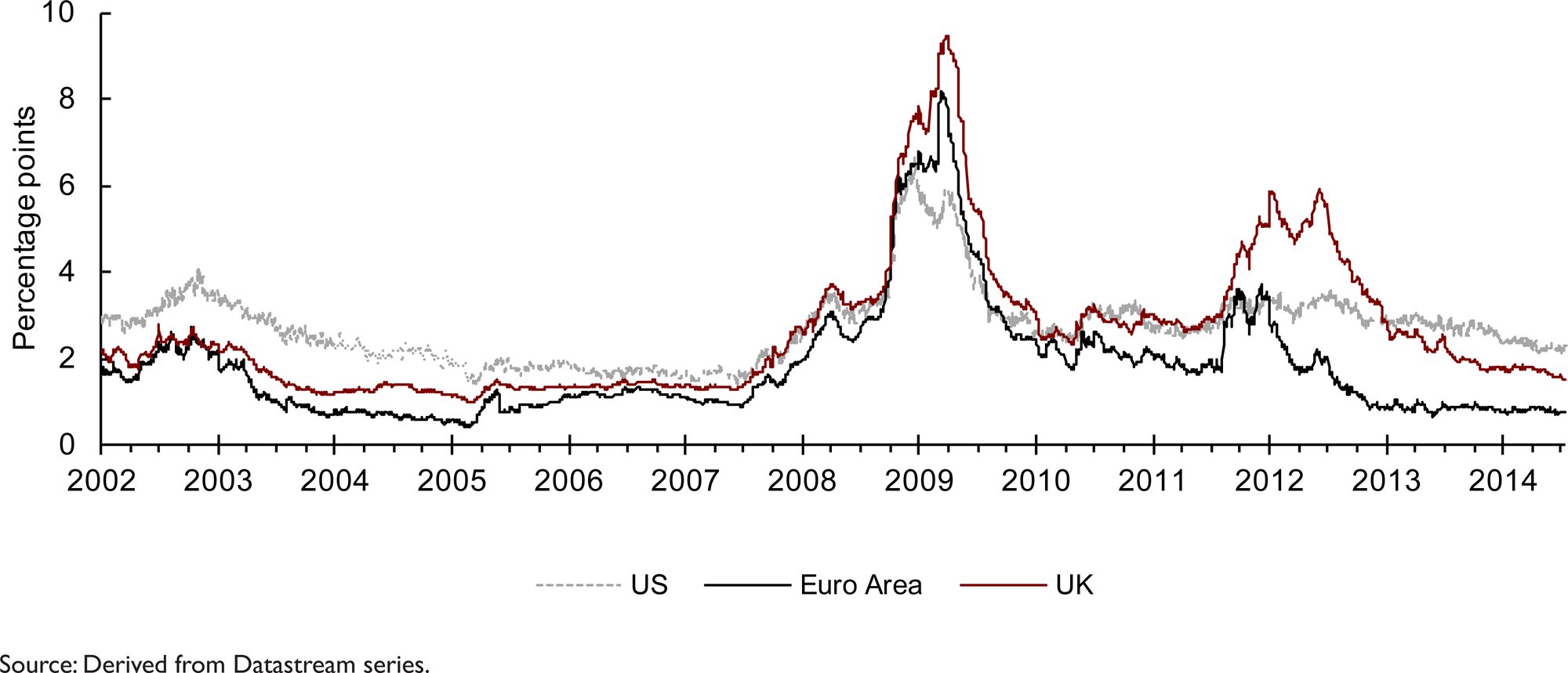

Figure A3 reports the spread of corporate bond yields over government bond yields in the US, UK and Euro Area. This acts as a proxy for the margin between private sector and ‘risk free’ borrowing costs. Private sector borrowing costs have risen more or less in line with the observed rise in government bond yields since the second half of 2013, illustrated by the stability of these spreads in the US, Euro Area and the UK. Our forecast assumption is for corporate spreads to remain at current levels until the end of 2014, and then gradually converge towards their long-term equilibrium level from 2015.

Corporate bond spreads. Spread between BAA corporate and 10-year government bond yields

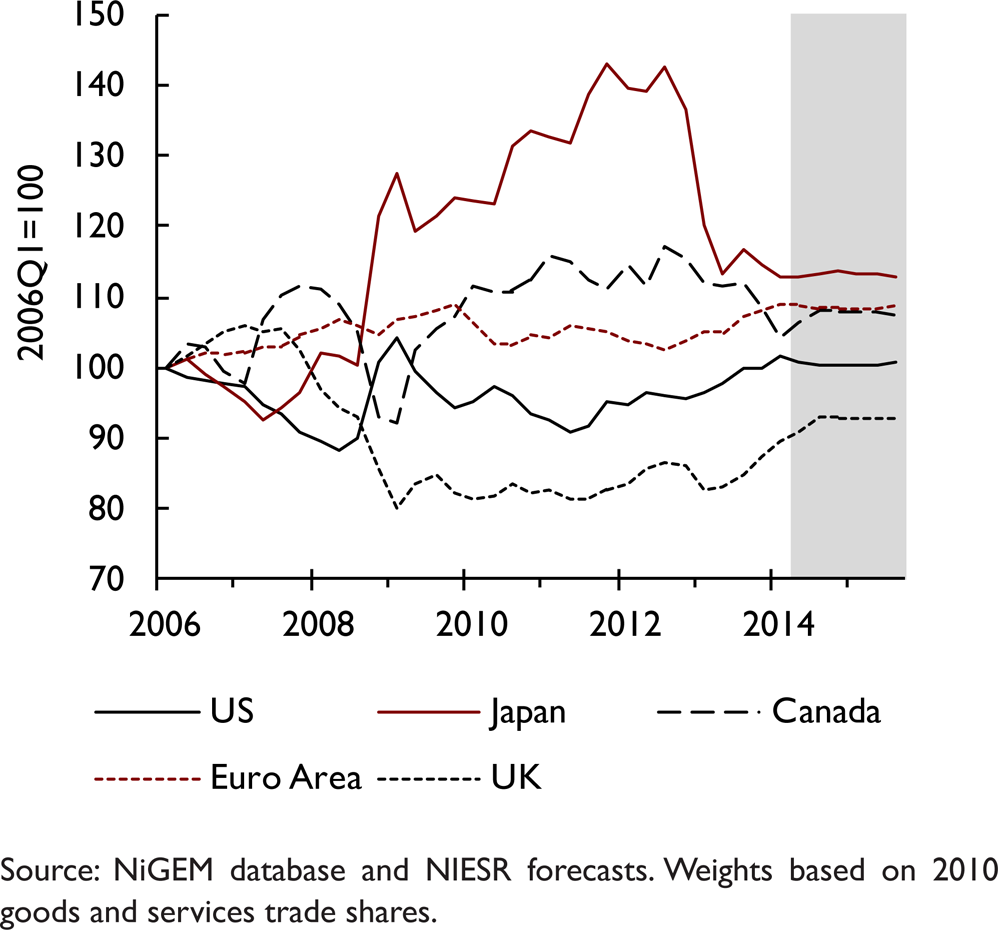

Nominal exchange rates against the US dollar are generally assumed to remain constant at the rate prevailing on 14 July 2014 until the end of March 2015. After that, they follow a backward-looking uncovered-interest parity condition, based on interest rate differentials relative to the US. We have modified this assumption for China, assuming that the exchange rate target continues to follow a gradual appreciation against the US$, of about 2½ per cent annually from end 2014 to 2016.

Our oil price assumptions for the short term are based on those of the US Energy Information Administration, who use information from forward markets as well as an evaluation of supply conditions, and are reported in table 1 at the beginning of this chapter. Recent increases in oil prices due to crises in Iraq as well as Ukraine were short lived. We assume oil prices remain broadly unchanged during the course of the year and decline modestly towards the end of 2014 by about $3 per barrel. Over the medium term, oil price growth will be restrained in part by the rise in new extraction methods for oil and gas, especially in the US (see the discussion in February 2013 National Institute Economic Review and Chojna et al., 2013). However, ongoing crises in Iraq and Ukraine (and the associated international dispute), continue to pose an upside risk to the price of oil in the short term.

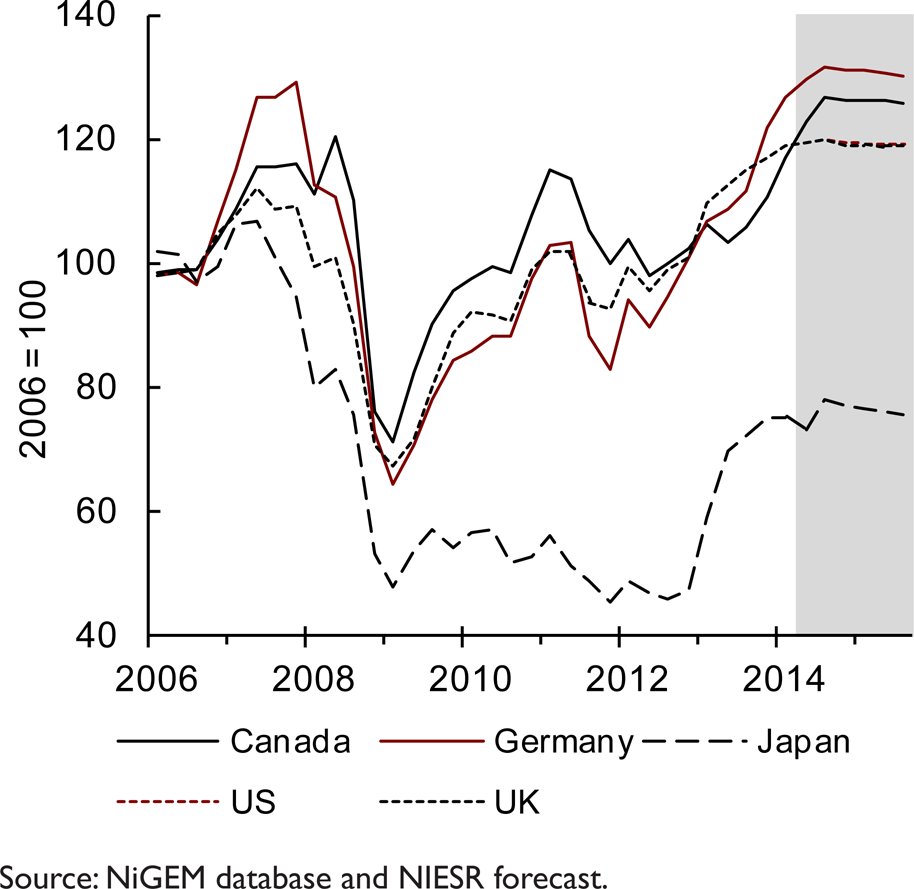

Our equity price assumptions for the US reflect the expected return on capital. Other equity markets are assumed to move in line with the US market, but are adjusted for different exchange rate movements and shifts in country-specific equity risk premia. Figure A5 illustrates the key equity price assumptions underlying our current forecast. Global share prices have performed well since the beginning of 2013, irrespective of a short lived drop – a reaction to the QE tapering signals emanating from the Federal Reserve last summer. Share prices in some of the more vulnerable economies of the Euro Area, however, remain depressed relative to their position in the first quarter of 2013 (e.g. Hungary and the Czech Republic). After gaining in excess of 50 per cent during 2013, share prices in Japan stalled at the turn of this year, and have even lost about 2 per cent since the first quarter of 2014.

Effective exchange rates

Share prices

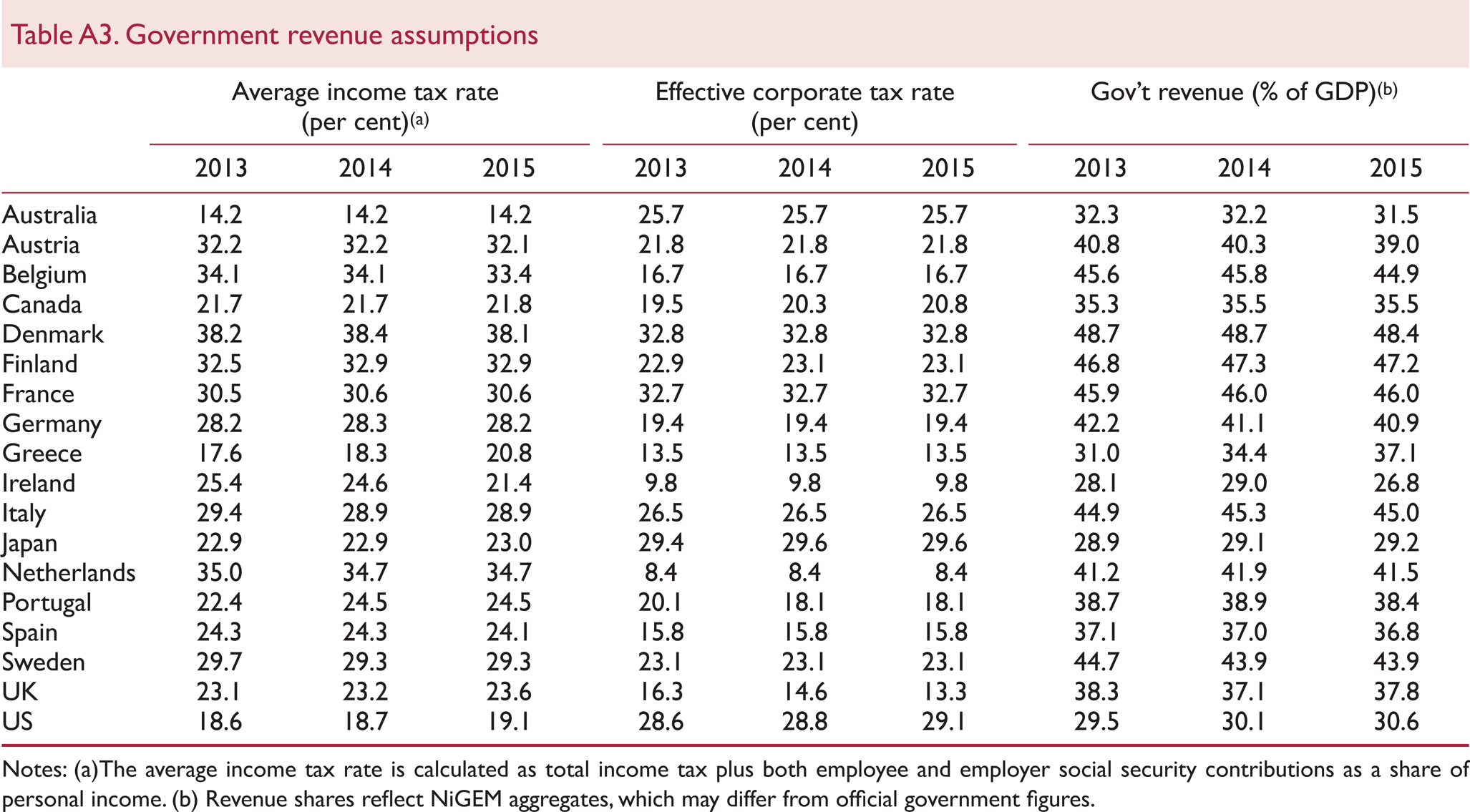

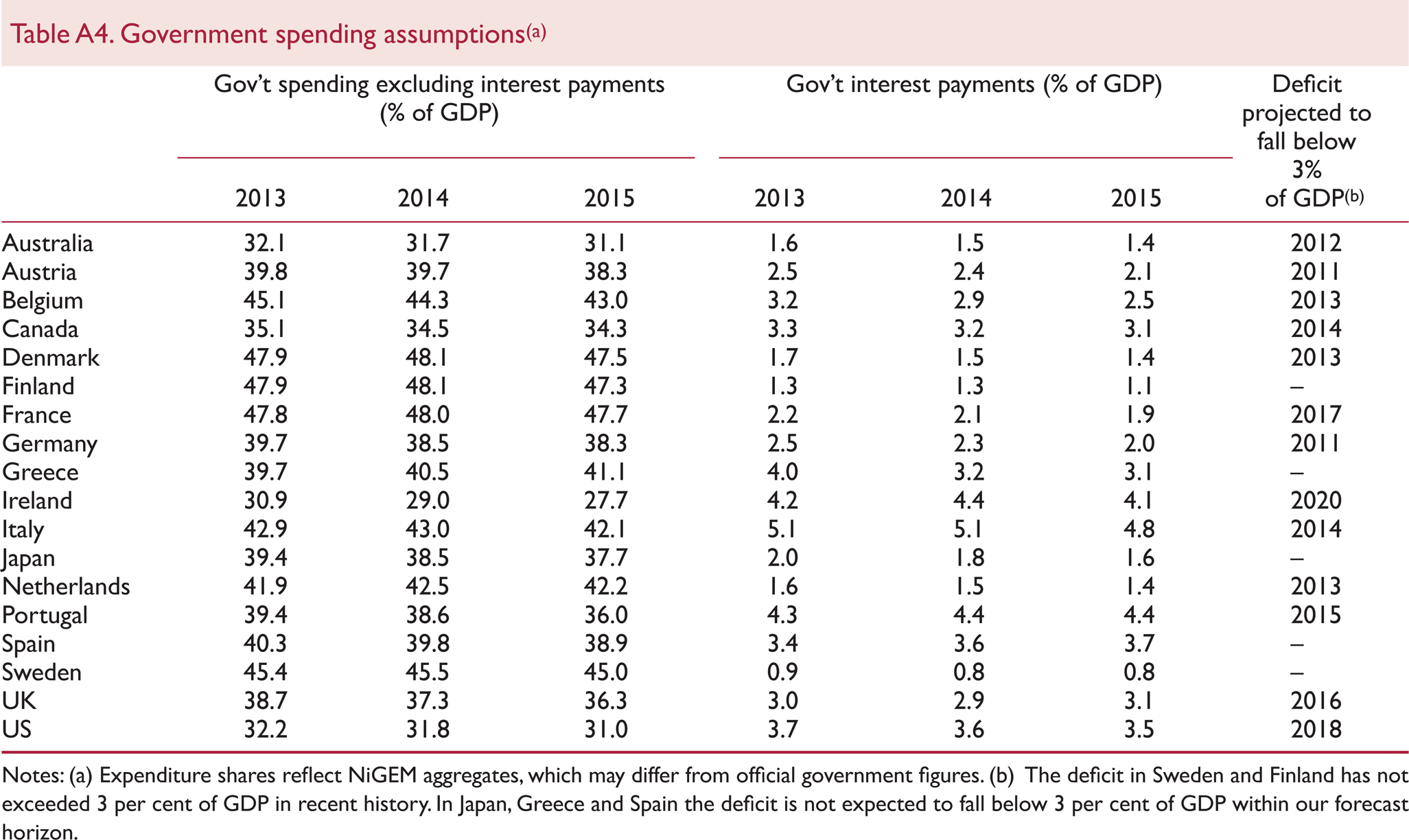

Fiscal policy assumptions for 2014–15 follow announced policies as of 1 July 2014. Average personal sector tax rates and effective corporate tax rate assumptions underlying the projections are reported in table A3. Our forecast also incorporates planned/enacted changes in VAT rates in 2013–14 for Canada, Finland, France, Italy and Japan. Government spending is expected to decline as a share of GDP between 2014 and 2015 in most Euro Area countries reported in the table. We expect the burden of government interest payments to rise this year as compared to the past year in Ireland, Spain and Portugal and remain unchanged in Italy. Recent policy announcements in Portugal, Spain, Italy and elsewhere suggest that the commitment to fiscal austerity in Europe may be waning. A policy loosening relative to our current assumptions poses an upside risk to the short-term outlook in Europe. For a discussion of fiscal multipliers and the impact of fiscal policy on the macroeconomy based on NiGEM simulations, see Barrell, Holland and Hurst (2013).

Government revenue assumptions

The average income tax rate is calculated as total income tax plus both employee and employer social security contributions as a share of personal income.

Revenue shares reflect NiGEM aggregates, which may differ from official government figures.

Government spending assumptions(a)

Expenditure shares reflect NiGEM aggregates, which may differ from official government figures.

The deficit in Sweden and Finland has not exceeded 3 per cent of GDP in recent history. In Japan, Greece and Spain the deficit is not expected to fall below 3 per cent of GDP within our forecast horizon.

Footnotes

1

Interest rate assumptions are based on information available to 14 July 2014 and do not include a 50 basis point reduction by the Central Bank of Turkey on 17 July 2014, 25 basis point increase by the Central Bank of New Zealand on 24 July 2014, and 50 basis point increase by the Central Bank of Russia on 25 July 2014.

2

Federal Open Market Committee statement, the Federal Reserve, 19 March 2014.