Abstract

This paper examines the background to calls for further fiscal decentralisation in Scotland in the light of theories of fiscal federalism. In particular, it examines whether spatial differences in preferences, which are central to ‘first generation’ theories of fiscal federalism can be argued to play a central role in the case for granting Scotland further tax and spending powers. ‘Second generation’ theories of fiscal federalism draw attention to the political economy of allocating tax powers to different levels of government. Some of the authors in this strand of theory argue that the case for allocating tax powers to subnational governments can be made in terms of ‘accountability’ – the notion that local politicians can be better held to account for the outcomes of policy actions. Our empirical analysis suggests that there is no clear difference in preferences between Scotland and the rest of the UK along a number of key political dimensions. However, the Scottish parliament enjoys substantially higher levels of trust among the Scottish electorate than does the UK parliament.

1. Introduction

After the May 2015 General Election, with 56 MPs, the Scottish National Party (SNP) was the third largest party in the House of Commons, having only held six seats in the previous parliament. A principal policy aim of the SNP is to have additional fiscal powers – relating to both taxes and spending – devolved from Westminster to the Scottish parliament. It argued in its manifesto that, “Instead of limited and unambitious proposals on tax powers, we should have a greater ability to generate economic growth, deliver more employment opportunities and support family incomes with the devolution of additional taxes” (SNP Manifesto, 2015, p. 35). The fiscal aspects of the party's policy are crucial to its wish to be seen as “standing up for Scotland”. They embody a desire for a different approach to economic and welfare policies, coupled with a belief that enhanced fiscal powers will deliver the economic growth and tax revenues that can support such policies.

The majority of the Scottish electorate appear to support further enhanced fiscal devolution to the Scottish parliament. A survey in April 2015 suggested that 53 per cent of Scottish adults were in favour of the Scottish parliament having ‘full fiscal autonomy’ (control over all taxes in Scotland, and all spending other than on defence and foreign affairs), with 33 per cent opposed and the remainder undecided. (A similar question in December 2014 suggested 51 per cent in favour of FFA, 29 per cent opposed and 20 per cent undecided.) The level of public support for fiscal decentralisation suggests that demand for greater fiscal autonomy is not simply driven by a Niskanen objective on the part of the Scottish parliament to maximise its budget and authority.

The strength of support for further fiscal decentralisation is perhaps surprising. The Scottish government already controls spending on most major public services such as health, education, local government, economic development and transport. Following the establishment of the Scottish parliament, public spending on these services in Scotland has been able to follow a different path from that in the rest of the UK. The major area of spending that is not under the control of the Scottish government is spending on welfare benefits, although, following the recommendations of the Smith Commission, partial responsibility for some sickness and disability benefits will be devolved to the Scottish government.

In contrast to its extensive spending powers, the Scottish government has limited control over tax revenues, creating a large vertical fiscal imbalance (its spending substantially exceeds its ability to raise tax). The incentive to increase tax revenues is therefore relatively weak. However, this position is changing rapidly. The Scotland Act 2012 gives the Scottish government power to set the “Scottish Rate of Income Tax” (effectively giving it control of 40 per cent of income tax revenues raised in Scotland) and control over a number of smaller taxes, notably including the Land and Buildings Transactions Tax. Following the recommendations of the Smith Commission, legislation is currently passing through parliament which envisages the devolution to the Scottish parliament of virtually all income tax revenue raised in Scotland, the assignment of 50 per cent of Scottish VAT revenues, and control over air passenger duty.

The Scottish parliament is thus in the process of becoming one of the most fiscally autonomous devolved governments in the world. If the recommendations of the Smith Commission are implemented in full, the Scottish parliament will control some 55 per cent of all public spending for and on behalf of Scotland, and be responsible for some 38 per cent of revenues raised. 1

Despite this, the Scottish government is arguing for more extensive devolution of welfare benefits, arguing that “further responsibility for the welfare system would allow the Scottish parliament to design a system based on Scottish priorities and preferences” (Scottish Government, 2015). It is also arguing for greater control over taxation, arguing that this will incentivise the Scottish parliament to improve Scottish economic performance, and ensure that the benefits of policy measures are retained in Scotland. Whether it supports full fiscal autonomy (FFA) in the short term has become harder to judge (given the relatively generous grant settlement the Scottish government receives from Westminster, it is difficult to make the case that the Scottish government would be fiscally better off under FFA), but it has recently made the case for devolution of business taxes including corporation tax, National Insurance Contributions (NICs) and capital gains tax (Scottish government, 2015).

This paper explores the case for further fiscal decentralisation to the Scottish government. It does so by exploring the motivations for decentralisation made in the theoretical literature, and examining the extent to which there is empirical support for these arguments in explaining the increased demand for additional tax and welfare powers in Scotland. The paper focuses on the case for fiscal decentralisation, but it should be noted that a case has also been made for further legislative and regulatory decentralisation to the Scottish government.

We concentrate on those aspects of the fiscal decentralisation literature that are particularly relevant to the Scottish case. Much of the fiscal decentralisation literature emphasises differences in preferences for public goods as a justification for the devolution of powers to subnational governments (SNGs). Indeed, it is often assumed that Scottish preferences differ from those in the rest of the UK (rUK). Scotland provides a number of universal (rather than means tested) benefits, such as free university tuition and free prescriptions, that are not available in other parts of the UK. Such policies are sometimes justified on the basis that Scots' prefer universal benefits, while citizens in rUK are more willing to accept means testing. The paper first considers the extent to which preferences for taxation and public services do differ in Scotland from rUK. We do not find evidence for significant differences in preferences.

However, differences in preferences may not be necessary for fiscal decentralisation to yield welfare improvements. There is a contrasting literature which stresses the importance of the ‘proximity of decision making’ and ‘local accountability’ as rationales for fiscal decentralisation. Decentralisation may also enhance local accountability and facilitate improvements in public services and enhanced economic development through improved information flows.

The paper is structured as follows. In section 2 we highlight the importance in the fiscal federalism literature of heterogeneous preferences in underpinning the case for fiscal decentralisation, and then consider empirically the extent to which there is evidence that Scots' preferences for public services do diverge from those in rUK. We find that, although there is some evidence for preference heterogeneity, these differences are generally small and statistically insignificant, and thus cannot explain the demand for greater fiscal autonomy in Scotland. In Section 3 we review alternative theoretical arguments for decentralisation that are not dependent on preference heterogeneity but on arguments around accountability and trust. We consider empirically what evidence there is to support these theories as motivating the demand for decentralisation in Scotland, again drawing on survey findings. Section 4 concludes.

2. Identity, preferences and fiscal decentralisation

The seminal contributions to the fiscal decentralisation literature assumed that preferences for public goods varied spatially. This preference heterogeneity was at the heart of the rationale for decentralisation. Central government was either unable to know these preferences (due to lack of information) or to act on them (perhaps because of political constraints on the central government which limited the extent to which levels of public goods could be varied). In these circumstances, SNG decision-making over public good provision is welfare enhancing relative to uniform provision of the public good by central government. This is known as the ‘decentralisation theorem’ after the seminal work of Oates (1972). In another seminal work, Tiebout (1956) shows that the gains from decentralisation are even greater where individuals sort (i.e. migrate) across regions to move to the SNG that most closely aligns with their preferences. Bewley (1981) argues that the equilibrium implied by Tiebout requires that the “public goods become essentially private”. Indeed, much of the literature assumes that the debate about decentralisation is essentially about public goods, though in practice the range of pure local public goods is probably very limited. If goods are essentially private, then it is less clear why government should be involved in their provision at all.

One possible objection to decentralisation identified in these ‘first generation’ theories of fiscal federalism involves the spillover effects from public good provision in one SNG affecting other SNGs (for example, SNGs may under-provide some types of infrastructure which benefit residents of neighbouring jurisdictions). Welfare is then optimised if central government ensures that appropriate transfers are made so that SNGs produce local public goods up to the point where marginal social benefit for society as a whole equals marginal cost.

Oates (2005) thus summarises the trade-off between the functions of central and decentralised governments as: “on the one hand, the inefficiencies under centralised provision of public services stemming from more uniform outputs that fail to reflect divergences in local tastes and decisions, versus, on the other hand, inefficiencies in local provision resulting from the failure to internalize inter-jurisdictional externalities”.

The ‘first generation’ models of fiscal decentralisation also argued that decentralised government should only have a minor role in influencing macroeconomic and redistributive policies. The case against involvement in redistribution policy is based on the argument that aggressive redistribution in one region might lead to out-migration of the rich and in-migration of the poor from elsewhere. This point is relevant in the Scottish context as the main spending policies which are not yet devolved tend to be redistributive welfare policy levers.

Similarly, Prud'Homme (1995) argues that redistribution should be excluded from decentralisation policies because “poor people are poor everywhere and should be aided irrespective of their place of residence” (p. 202). Differences in mean incomes between regions will be exacerbated by fiscal decentralisation. Generally critical of decentralisation, Prud'Homme also argues that centralised fiscal policy is more likely to realise both economies of scale, by saving on costly replication of administrative functions and economies of scope – through its ability to attract a wider range of skills and expertise.

The ‘second generation’ theory of fiscal federalism (see Oates, 2005, for a review) focusses on issues of political economy and information asymmetries. These may lead to different conclusions about the desirability of decentralisation. Instead of governments acting benevolently as is the case in the first-generation models, second-generation fiscal federalism allows agents to have objective functions that are not necessarily aligned with the common good. For example, Besley and Coate (2003) argue that there is no reason in principle why central government cannot identify and act upon spatial differences in preferences for public goods – there should not be an assumption that equates central government with ‘uniform provision’. However, if preferences do vary, centralised decision-making in a national legislature implies conflict between citizens in different SNGs seeking to form a winning coalition which best reflects their preferences. The outcome, and therefore the relative merits of centralisation versus decentralisation, will depend on how political coalitions interact in this setting, but tends to involve various forms of misallocations. Nonetheless, although the framework is quite different, the importance of preference heterogeneity in underpinning the case for decentralisation remains in some of the second generation literature. Besley and Coate suggest that “the key insight remains that heterogeneity and spillovers are correctly at the heart of the debate about the gains from centralisation”.

In a Scottish context, it is also worth making the point that Scotland's relatively generous block grant from Westminster has been rationalised on the basis of it having heterogeneous preferences for national (as opposed to local) public goods. Christie and Swales (2010) for example argue that Scotland's generous grant settlement reflects the fact that it is geographically and culturally distanced from the centre. This means that it has different preferences for national public goods, giving it an incentive to secede. At the same time, because provision of these national public goods are associated with economies of scale, secession would impose costs on the UK government. The grant to the Scottish government for local public goods thus offsets the (assumed) lower value the Scottish electorate places on national public goods.

Preference heterogeneity is clearly critical to much of the theoretical literature on the economic case for decentralisation. And as noted in the introduction, the case for further welfare devolution to the Scottish government is often made on the basis that Scottish preferences for welfare are in some way different. What evidence is there that preferences for public good provision are different in Scotland compared to rUK? The remainder of this section considers the empirical evidence for preference differences.

We start by noting that ‘preference heterogeneity’ may be linked to differences in the groups that individuals identify with, which in turn reflect the social categories that individuals consider themselves to be part of. Akerlof and Kranton (2000) suggest that individual utility is affected, not only by preferences for consumption goods, but also by how individuals feel that their identity is perceived by others. Significant differences in perceptions of identity may be indicative of variations in preferences across groups. Our first empirical test addresses this issue using differences in ‘British’ identity between Scotland and rUK to measure contrasts in how individuals perceive the ‘group’ to which they belong.

Since 2001, the UK Labour Force Survey (LFS) has asked the following question: “How would you describe your national identity? Please choose all that apply”. Possible responses include “English”, “Scottish”, “Welsh”, “Northern Irish” and “British”. The role of Scottish identity in the debate on constitutional change has been subject to extensive analysis by political scientists (see e.g Bechhofer and McCrone, 2009; Bond and Rosie, 2002). However, their analysis of trends in identity has tended to rest on relatively small datasets which do not provide compatibility with the rest of the UK, whereas the LFS interviews around 40,000 households in the UK each quarter. We focus on ‘Britishness’ as being an expression of a common identity shared across Great Britain. Figure 1 below shows the percentage of LFS respondents who described themselves as British between 2001 and 2014. It is clear that residents of Scotland are less likely than those living in rUK to describe themselves as British. One explanation is that those living in England are less likely to see any distinction between ‘Englishness’ and ‘Britishness’. Nevertheless, what is clear from the data is that the proportion of residents in Scotland describing themselves as British has increased quite markedly, from 23.0 per cent in 2001 to 32.5 per cent in 2014. Over the same period, the share of those resident in rUK describing themselves as British increased from 37.7 per cent to 47.0 per cent. The increasing acceptance of the adjective ‘British’ has been marginally greater in Scotland than in rUK over this period. Though some of the increase may have been the response to an increasing share of respondents that are immigrants who are more comfortable with the ‘British’ identity than with its constituent parts, these data do not suggest that a diverging sense of identity can have played a role in the rise of support for fiscal decentralisation for Scotland. Indeed, the data suggest the reverse.

Per cent of respondents living in Scotland and rUK describing themselves as British

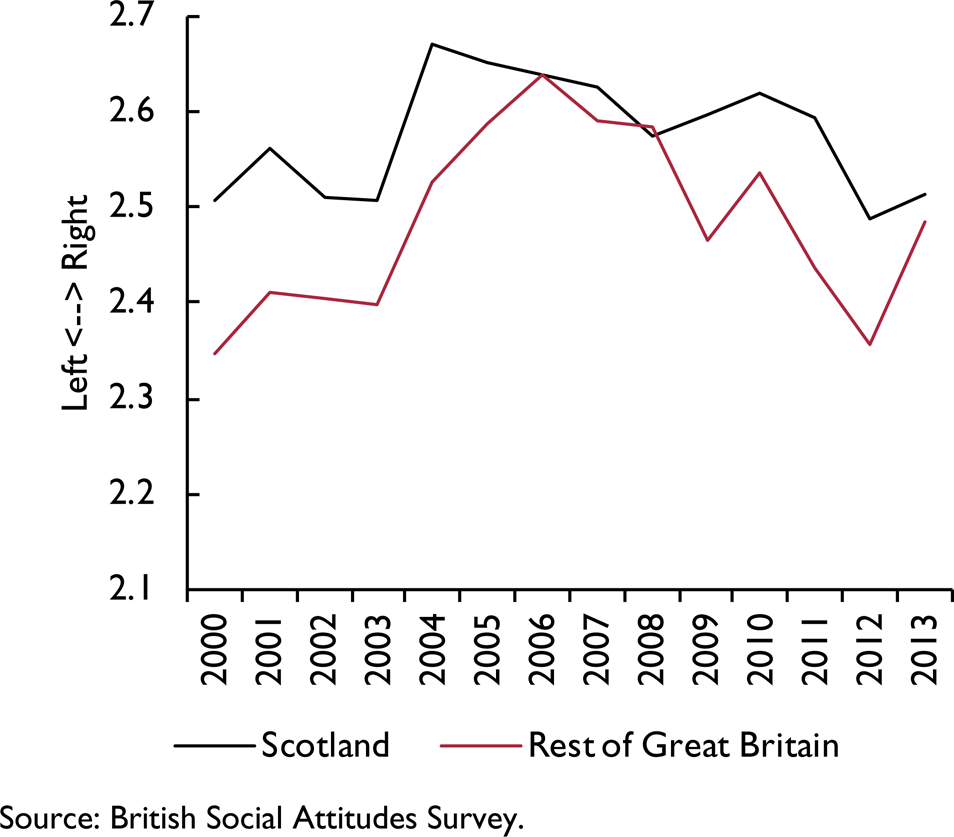

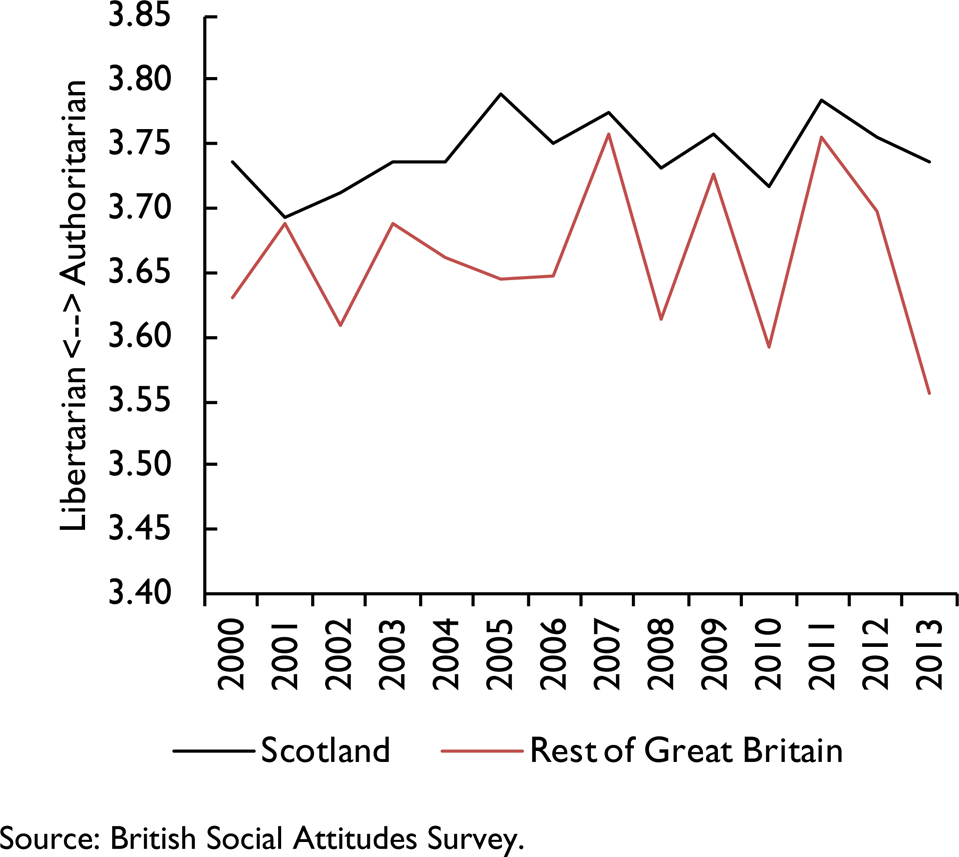

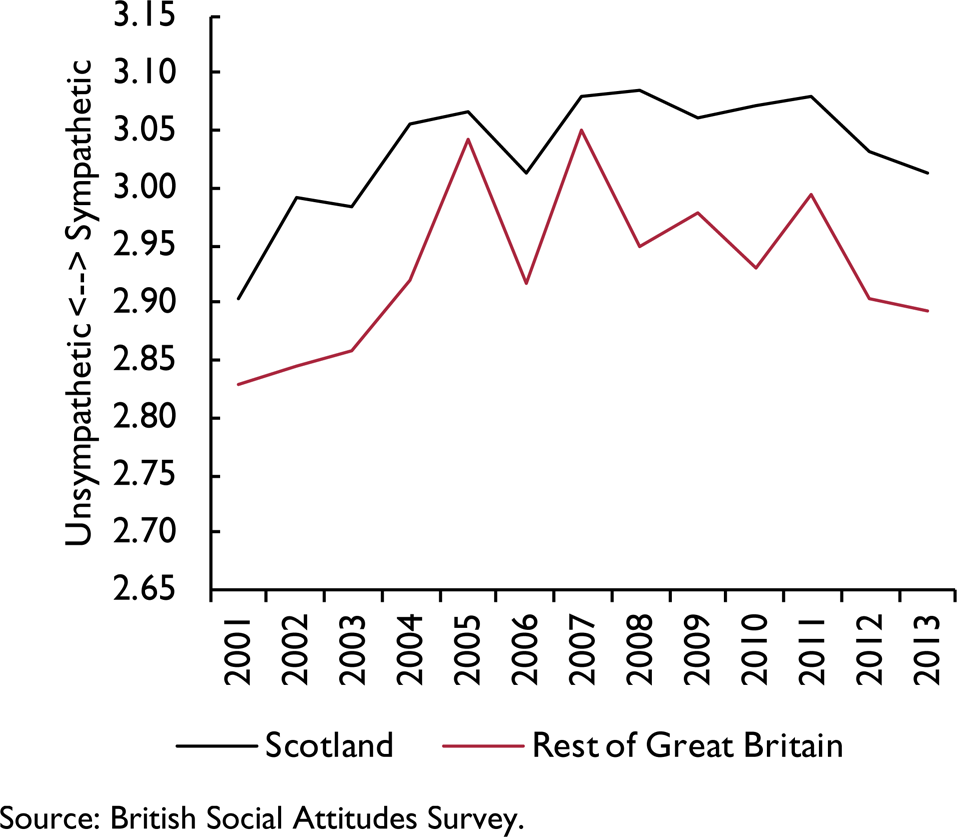

If the dynamics of identity do not provide an explanation of the increasing pressure for fiscal decentralisation to Scotland, then perhaps more direct measures of preferences may provide a different conclusion. For this we turn to evidence of differences in political attitudes between Scotland and rUK. The British Social Attitudes (BSA) survey has consistently collected three multiple-item scales: ‘left-right’, ‘libertarian-authoritarian’ and ‘welfarism’. The left-right scale asks respondents how far they agree with statements such as “ordinary people do not get their fair share of the nation's wealth”. The libertarian-authoritarian scale is based on responses to statements such as “people who break the law should be given stiffer sentences”. The welfarism scale is based on responses to statements such as “The government should spend more money on welfare benefits for the poor, even if it leads to higher taxes”.

All of the scales range between 1 and 5. On the left-right scale, 1 corresponds to ‘left’ and 5 corresponds to ‘right’. On the libertarian-authoritarian scale, 1 corresponds to ‘libertarian’ and 5 corresponds to ‘authoritarian’. On the welfarism scale, 1 corresponds to ‘unsympathetic’ and 5 to ‘sympathetic’ to welfare provision. Evans, Heath and Lalljee (1996) argue that these scales provide consistent indicators of political attitudes, values and ideology across the UK electorate. Therefore, they provide one possible mechanism for calibrating differences in preferences across the UK.

We combined data from the BSA survey from 2000 to 2013. Figures 2, 3 and 4 show mean values over this period for the left-right, libertarian-authoritarian and welfarism scales in Scotland and the rest of Great Britain respectively.

Left-right scale for Scotland and the rest of Great Britain 2000–2013

Libertarian-authoritarian scale for Scotland and the rest of Great Britain 2000–2013

Welfarism scale for Scotland and the rest of Great Britain 2001–2013

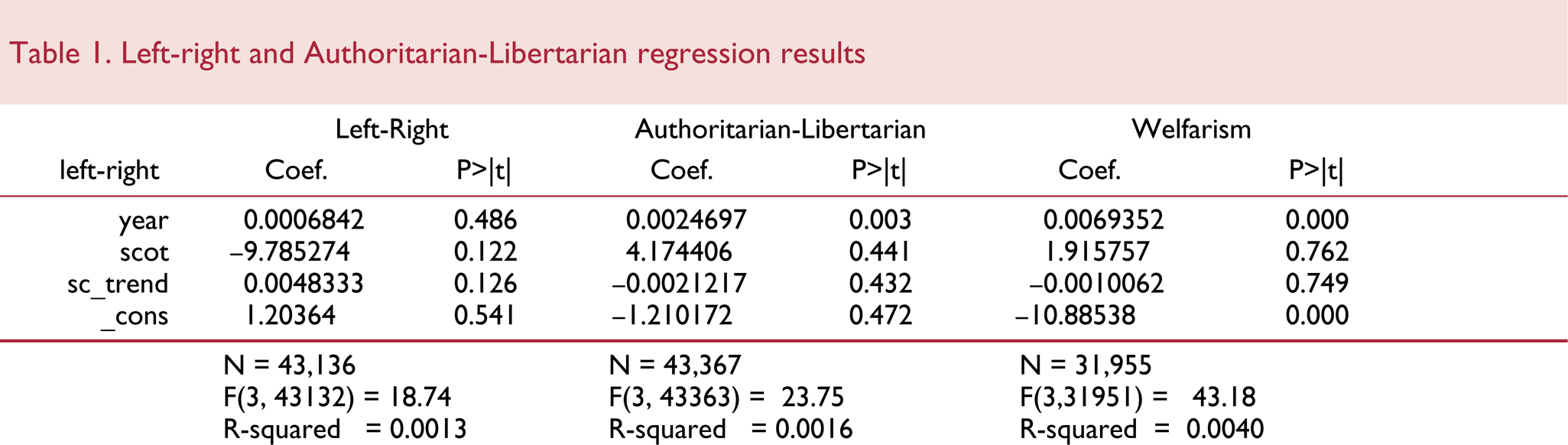

Perhaps surprisingly, Scotland generally scores more towards the ‘right’ and ‘authoritarian’ ends of the left-right and authoritarian-libertarian scales than does the rest of Great Britain. However, the differences between the respective scores on both scales is relatively small. To determine whether there were significant differences in levels and trends between Scotland and the rest of Great Britain, we ran the following regressions on the BSA data from 2001 to 2013,

where j=1 for the left-right scale, j=2 for the authoritarian-libertarian scale and j=3 for the welfarism scale. The variable year is the time trend intended to capture gradual changes in attitudes to these scales, scot is a dummy indicating whether the individual is resident in Scotland or not, while year*scot is an interactive term that allows for Scottish-specific changes in trend. The Scottish parliament was established in 1998. Therefore the estimation period covers almost all of its existence, during which attitudes relevant to these scales may have changed. We did not include additional control variables since changes in the composition of the population may be the cause of changing preferences. Results are shown in table 1 below.

Left-right and Authoritarian-Libertarian regression results

None of the Scottish dummies, nor the time trend interacted with these dummies, is significant in the regressions for the three scales. This suggests that as far as these scales map onto preferences over public goods, there is no evidence of significant difference, or of significant change in the difference between those living in Scotland and those living elsewhere in Great Britain. Our results are in accord with those of Henderson (2014) who also argues that there are no significant differences in preferences between Scotland and rUK across these scales. However, she does note that many Scots believe that other Scots hold more left-wing views than is actually the case, or that they are more supportive of the expansion of welfare than is actually the case. This introduces the intriguing, but untestable proposition that the principals' (citizens) communications with agents (politicians) may be influenced by ‘herd’ effects (Crockett, 2000). Then, irrespective of any flaws in the contracts between principals and agents, the resulting outcome is likely to be sub-optimal – for example, policy may lead to a higher provision of welfare than would emerge from the level determined by individual ballot.

Our findings with respect to various dimensions of preference are consistent with our findings on Scottish identity. Though these indicators do not perhaps fully capture the views that influence differences in preferences for local public goods, they do support the view that the electoral success of the SNP cannot simply be explained by the argument that Scots have different preferences over public goods from citizens in rUK. The next section considers alternative explanations for the increasing demand for fiscal decentralisation to Scotland.

3. Fiscal decentralisation and accountability

In seeking to understand the growing demand for fiscal decentralisation to Scotland, the previous section found limited evidence for differences in preferences between Scotland and rUK. While this finding clearly sits uneasily with the early fiscal federalism literature, more recent contributions do identify arguments for fiscal decentralisation other than those that stem from heterogeneous preferences. For example, Strumpf (2002) argues that decentralisation may encourage policy experimentation, with the potential to create beneficial spillovers; this is similar to the notion of ‘laboratory federalism’ proposed by Oates (1999). Decentralisation may also be used to promote ‘yardstick competition’ as described by Shleifer (1985), where competition between SNGs can help maximise efficiency in public good provision. However, it seems unlikely that either the notion of laboratory federalism or yardstick competition can explain the increased demand for fiscal decentralisation in Scotland – both notions suggest advantages of decentralisation from the perspective of the central government, and there is little evidence that Scottish voters are arguing for decentralisation on the grounds that they can be part of an experiment that will lead to better outcomes for the UK as a whole.

But there is a field of studies within the ‘second-generation’ fiscal federalism literature that makes a case for decentralisation even when preferences are homogeneous across jurisdictions. This literature tends to stress the advantages of decentralisation from the perspective of accountability. Here, we take accountability to mean the extent to which agents can be associated with outcomes. Thus, in large legislatures or where politicians represent large numbers of voters, accountability is relatively diffuse since it is difficult to construct a direct linkage from principal to agent to outcome that is not influenced by the preferences of other voters and/or the design of the decision-making body.

For example, Tommasi and Weinschelbaum (2007), construct a principal-agent model of local public good provision in which the principals (citizens) contract with agents (politicians) to provide these goods. Agents' benefits comprise the payment they receive less the cost of their effort. Citizens in different SNGs need not cooperate when setting contracts with their agents. Where principals and agents can contract for an agreed level of effort, centralisation is preferred to decentralisation because it can account for spillover effects. Where principals can only imperfectly observe effort, the outcome is less clear. If they act together, centralisation is preferable, but when they act separately, the problem of intrinsic common agency may arise, leading to a trade-off between spillover effects and the extent to which the goods constitute private as opposed to public goods. The case for centralisation is increasing in the size of spillover effects, but decreasing in the size of the private element in the goods provided. The case for decentralisation then depends on the value that citizens place on localised control and/or ‘accountability’. This model provides a further addition to the arguments favouring decentralisation without requiring preference heterogeneity.

Along similar lines, Seabright (1996) argues that decentralised decision-making may be favoured on the grounds of accountability, because contracts between citizens and politicians may be incomplete. The allocation of power to central government or SNGs should reflect the probability that agents will act in the way desired by their electorates. Specifically defining accountability as the probability that the welfare of a given jurisdiction determines the election of a government, he argues that politicians based in SNGs are more likely to be ‘accountable’ to their electorates since they will not be constrained to trade-off one set of interests against another as would be the case with a centralised government.

The general message from the Tommasi and Weinschelbaum (2007) and Seabright (1996) studies is thus similar in spirit to the story from the first generation fiscal federalism literature, in that the case for centralisation is increasing in the size of inter-jurisdictional spillovers. However, what distinguishes the latter studies is that decentralisation may be preferable over centralisation even where preferences are homogeneous, given that decentralisation enhances local accountability and control. Local voters are more likely to trust political agents if they are clear that their loyalties are not divided between serving some external interests in addition to the local interest. However, Oates (2005) argues that grants from central government to internalise such spillover effects might allow the gains from coordination and the gains from accountability to be jointly realised.

A somewhat different approach to the accountability argument is evident in that part of the political science literature which is concerned with trust in government. Thus, Miller (1974) argues that, rather than responding directly to stable preferences held by citizens, politicians ‘produce’ policies that are either accepted or rejected by the electorate. Individuals judge politicians not only on how far they share the same preferences, but also on their effectiveness in translating these preferences into policy. Citizens that regularly reject the policies offered by politicians may lose faith not only in these politicians but also in the political system that they represent. Translating to the world of fiscal federalism, different policies are being offered by different levels of government and citizens may rate the trustworthiness of each level of government based on differences in the proportion of policies that they accept or reject from that level.

Thus, another way to describe political accountability is as a principal-agent problem where there are many principals (citizens) with varied preferences and few agents (politicians). Therefore, there are no contracts that simultaneously satisfy all preferences. Principals realise this and focus on other signals (performance) to evaluate agents' reputations. Consistently negative evaluations may weaken trust in the structure of the game (the political system).

Ligthart and van Oudheusden (2011) test the argument that trust in government is likely to be greater in more decentralised fiscal systems. They confirm this finding empirically, based on panel data from the World Values Survey covering 42 countries over the period 1994–2007 and after controlling for a wide variety of other possible influences, heterogeneity and direction of causality. However, they do not provide any strong theoretical basis for this empirical finding. We propose three arguments in line with our discussion of accountability that might explain their finding:

Decentralised government is more trusted because citizens have a local bias in evaluating political performance: irrespective of their preferences, they are more likely to take a positive view of political performances by individuals whom they feel that they can trust due to shared background, heritage, language etc. Decentralised government has limited responsibilities in policy areas such as foreign affairs, defence and microeconomic policy that are subject to significant external shocks. Politicians may have to offer policies in these areas based on relatively limited information about citizen preferences. SNGs may have a smaller set of policy responsibilities than national government. If citizens are subject to loss aversion and there is a 50:50 chance of agreeing or disagreeing with any new policy initiative, then they are more likely to lose trust in national government before SNGs.

Whether these arguments explain Ligthart and van Oudheusden's findings is not feasible to explore within this paper. However, it is clear that there is scope to investigate the rationale for fiscal decentralisation based on accountability and trust. And we can examine how levels of trust vary across different levels of government in Scotland. To what extent is there empirical evidence to support the idea that this is what is underpinning the demand for greater fiscal decentralisation in Scotland?

To investigate this issue we looked at differences in levels of trust for the Scottish and UK parliaments amongst a representative sample of 2037 Scottish respondents to an ESRC funded questionnaire conducted by YouGov in December 2013. Individuals were asked to rate their level of trust in the Scottish and the UK parliaments on a scale from 0 (complete mistrust) to 10 (complete trust). The mean score for the Scottish parliament was 5.6 while that for the UK parliament was 4.3. A similar question was asked in the Scottish Social Attitudes survey (2012). The survey conducted by NatCen questioned a representative sample of 1229 Scots. When asked whether the UK government could be trusted to work in Scotland's best long-term interest, 67 per cent of Scots answered either “only some of the time” or “almost never”. When asked the same question about the Scottish government, only 37 per cent believed that it could be trusted to work in Scotland's best interests only some of the time or almost never. In 2013, the Scottish social attitudes survey asked whether the Scottish and UK governments could be trusted to make fair decisions. While 19 per cent of respondents thought that the Scottish government could not be trusted very much or at all, 39 per cent of respondents felt the same way about the UK parliament. This combined evidence suggests that the Scottish parliament and government command significantly higher levels of trust among Scottish voters than does the UK parliament and government.

Is the greater level of trust in the Scottish parliament to do with its ability to produce policies that are more closely aligned with those of the Scottish electorate? Our survey evidence suggests that the answer to this question is a clear no. A further survey of 1300 Scottish adults was commissioned by the ESRC Centre on Constitutional Change and conducted in November and December 2014 (after the independence referendum). It examined both where voters wished fiscal policy decisions to be made and whether it is desirable that these decisions result in outcomes significantly different from those in rUK.

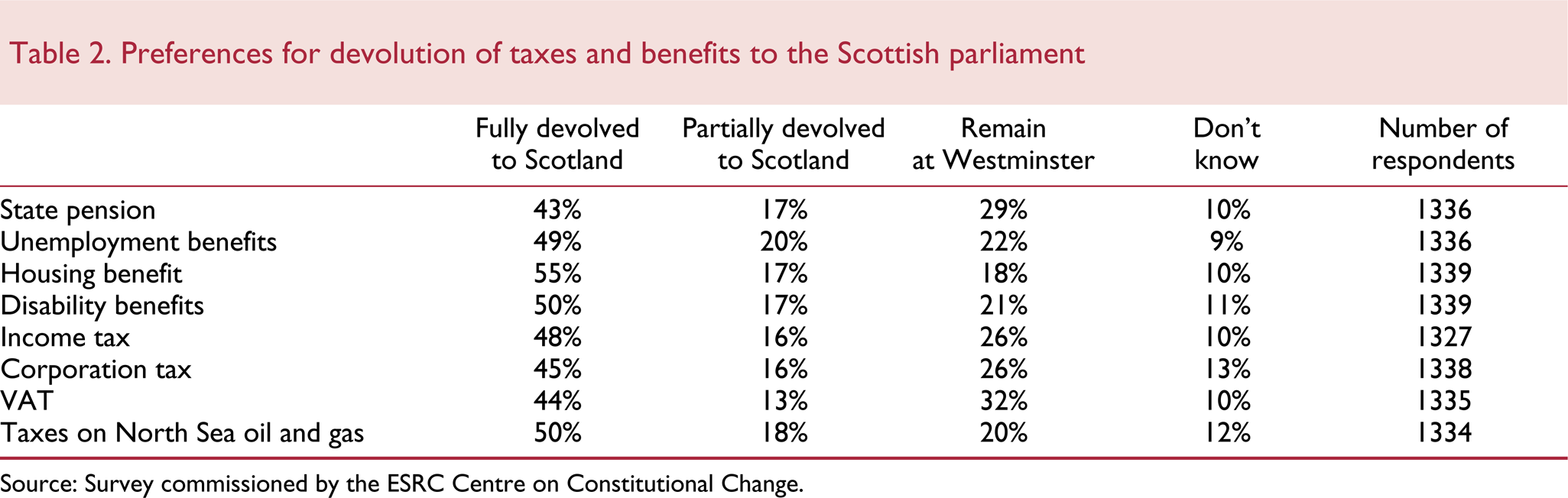

Thus, respondents were first asked whether they thought that various taxes and benefits should be fully devolved to the Scottish parliament, partially devolved, or remain reserved at Westminster. The results are shown in table 2. There is a clear demand for further fiscal devolution to Holyrood. Full devolution of each tax and benefit lever was supported by at least 43 per cent of respondents in each case, with a further 13–20 per cent supporting partial devolution, and less than a third thinking that each tax and benefit should remain reserved at Westminster.

Preferences for devolution of taxes and benefits to the Scottish parliament

Source: Survey commissioned by the ESRC Centre on Constitutional Change.

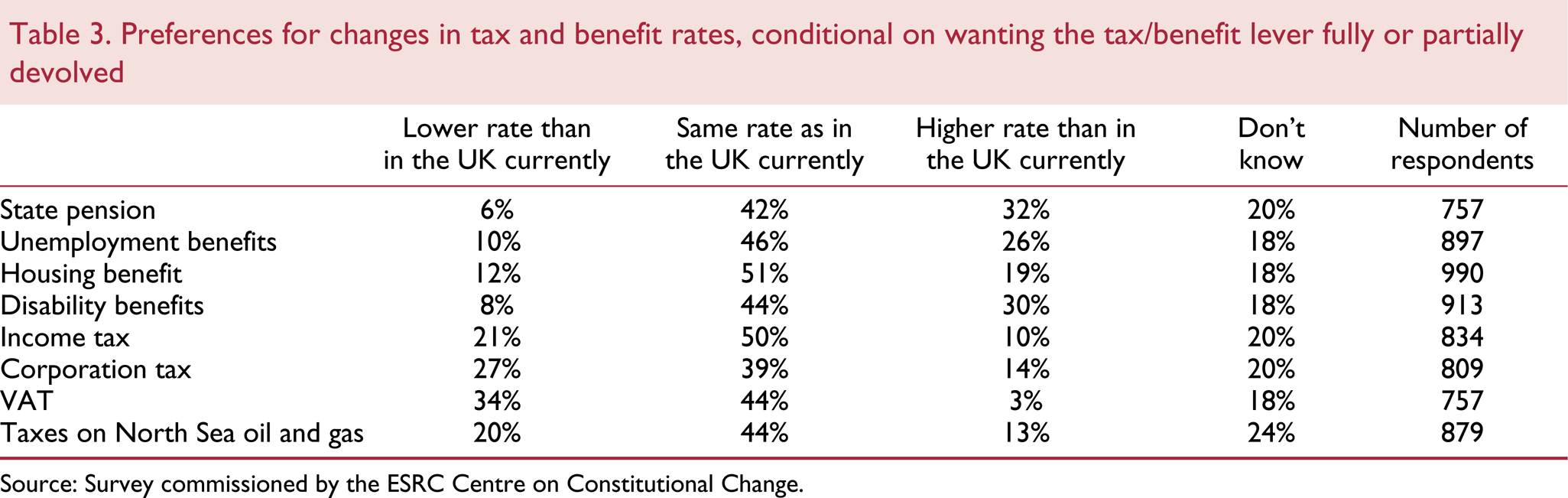

Respondents were then asked to imagine that each of the taxes and benefits listed had been devolved to the Scottish parliament. They were asked to say whether they thought that the tax or benefit rate should remain the same as the current UK rate, be increased, or be reduced. Table 3 reports the results only for those respondents who had supported either the full or partial devolution of each tax or benefit to Scotland. Only a minority (between 30–37 per cent) think that the tax or benefit rate should be changed relative to the UK rate (unsurprisingly, those who did not support devolution of a tax/benefit lever were even less likely to want to see a change in the rate).

Preferences for changes in tax and benefit rates, conditional on wanting the tax/benefit lever fully or partially devolved

Source: Survey commissioned by the ESRC Centre on Constitutional Change.

Table 3 also indicates that, on balance, Scots would prefer reduced taxes and increased benefits. This is somewhat at odds with the prevailing orthodoxy that Scotland differs from the rest of the UK in being willing to support higher welfare payments paid for by increased tax rates. Scots would like to have higher benefits, but also lower taxes.

Thus, while 32 per cent of survey respondents would prefer the state pension to be larger in Scotland than in rUK and only 6 per cent would prefer it to be smaller, 21 per cent of respondents would prefer lower income tax, while only 10 per cent thought that income tax rates should be higher in Scotland than rUK. While holding these views is completely rational for an individual, they are clearly not consistent when aggregated across the population.

The implication of these findings is that there is a considerable taste for fiscal decentralisation in Scotland, but little appetite for significant deviation from UK policy norms. In addition, Scots want both higher welfare benefits and lower taxes: a perspective that is understandable but may not be feasible. Thus, our examination of the survey evidence suggests that it is not differences in preferences that drive the demand for fiscal decentralisation in Scotland. Instead, it has much more to do with local accountability and a belief that decisions made locally are better decisions.

4. Conclusions

This paper has examined some of the theoretical arguments for fiscal decentralisation, and examined the extent to which these various theoretical arguments can support or explain the increased demand for further fiscal decentralisation to Scotland.

Much of the literature on fiscal federalism emphasises differences in preferences as a motivation for fiscal decentralisation. Indeed, the Scottish government has often made its case for further fiscal powers (particularly with regard to welfare spending) on the basis that preferences for public goods are in some way different in Scotland. However, we have not found evidence that there are significant differences across some important dimensions of social preference between Scotland and the rest of the UK. The argument for further fiscal decentralisation in Scotland based on heterogeneous preferences thus seems difficult to make.

Some of the more recent literature on fiscal federalism emphasises accountability and the agency benefits of local decision-making as alternative rationales for fiscal decentralisation. Survey evidence provides more support that these arguments around accountability and trust may be a better explanation of the current pressure for further fiscal decentralisation in Scotland. The Scottish electorate places a higher level of trust in the Scottish relative to the Westminster parliament, and is generally supportive of the notion that more fiscal powers should be decentralised. However, there is relatively limited evidence that the Scottish electorate wants to see radical change to the system of taxation or benefits, supporting the notion that the demand for decentralisation is driven by the desire for local accountability rather than preference heterogeneity.

Thus there is a case for further fiscal decentralisation to Scotland, but this case can be made only weakly by reference to preferences. From a UK perspective of course, any case for decentralisation has to be balanced against the risks of greater macroeconomic stability (as a result of either fiscal competition or loss of macroeconomic control).

Fiscal federalism theory does not provide much insight as to how this balance should be struck. But it is perhaps a mistake to frame the discussion as if there is an unambiguous end-point to the negotiations, as is often assumed. Systems of fiscal decentralisation are delicate, and must evolve in response to political and economic pressures. The risk is that the system evolves too quickly, without due consideration to the principles that decentralisation is trying to achieve.

Footnotes

1

This figure includes the half of VAT revenues that are being assigned to Scotland. If these are excluded (on the grounds that the Scottish parliament will have no ability to vary VAT), then the Scottish parliament will be responsible for 29 per cent of revenues raised in Scotland.