Abstract

Recent developments and the global forecast

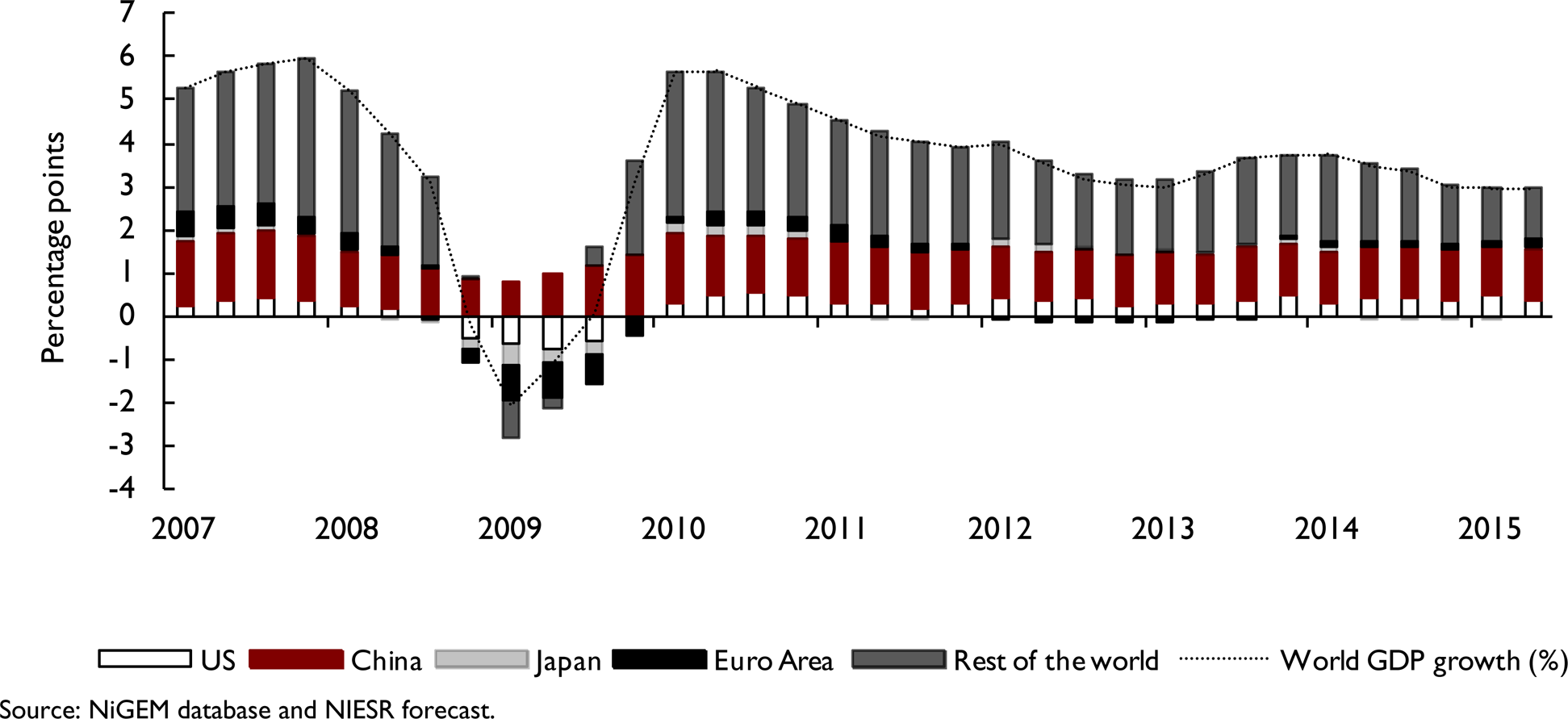

Global economic growth remains moderate and uneven. Our forecast of world GDP growth in 2015 and 2016 has been revised down, by 0.2 and 0.3 percentage points respectively, to 3.0 and 3.5 per cent. Global growth this year is now forecast to be the slowest for any year since the crisis, reflecting a trend of weakening growth in many emerging market economies as well as hesitant recoveries in the advanced economies. Expected drivers of the projected strengthening of the global expansion in the period ahead include continuing highly accommodative monetary policies and waning fiscal consolidation in most advanced economies, together with the boost to demand from the decline in oil prices since mid-2014, which in most cases has not yet been very visible in the data.

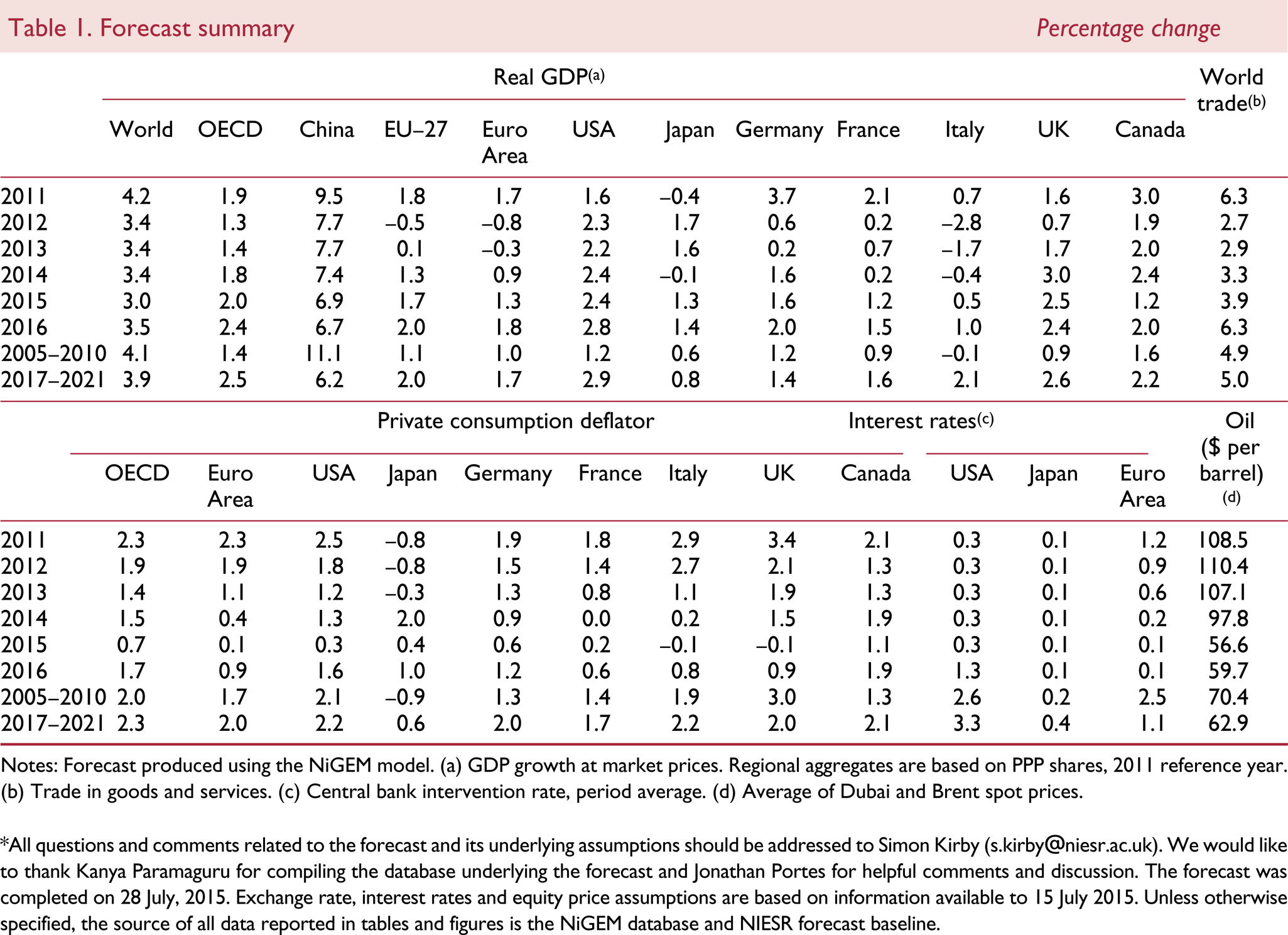

Forecast summary Percentage change

Notes: Forecast produced using the NiGEM model.

GDP growth at market prices. Regional aggregates are based on PPP shares, 2011 reference year.

Trade in goods and services.

Central bank intervention rate, period average.

Average of Dubai and Brent spot prices.

Contributions to world GDP growth (from four quarters earlier)

GDP growth weakened in the US and turned negative in Canada in the first quarter of 2015, partly because of special temporary factors, but also reflecting a drop in investment in the energy sector in the wake of the oil price decline. In the second quarter, growth picked up in the United States but the contraction seems to have continued in Canada. This recent underperformance of activity in North America, relative to our May projections, accounts for a large part of the downward revision of our global growth forecast for 2015; the other main contributors are downgrades for a number of emerging market economies in Asia and Latin America.

In the Euro Area, the crisis in Greece has been the main preoccupation of policymakers. The Greek economy, weighed down further by new uncertainties about policies, a recent three-week closure of banks, limits on deposit withdrawals, and controls on external payments, has weakened further, and our forecast of growth in 2015 and 2016 has been marked down, by 2.7 and 5.1 percentage points respectively, to −3.0 per cent and −2.3 per cent. With Greece representing less than 2 per cent of the Euro Area economy, contagion from Greece to other countries and financial markets has been limited, and our growth forecast for the Euro Area has been lowered only slightly. The Greek crisis and issues facing the Euro Area are discussed below and in a Note following this chapter.

In Japan, growth performance has remained mixed. Among the major emerging market economies, the moderate slowing of growth in China has continued, while in Brazil and Russia recessions have deepened.

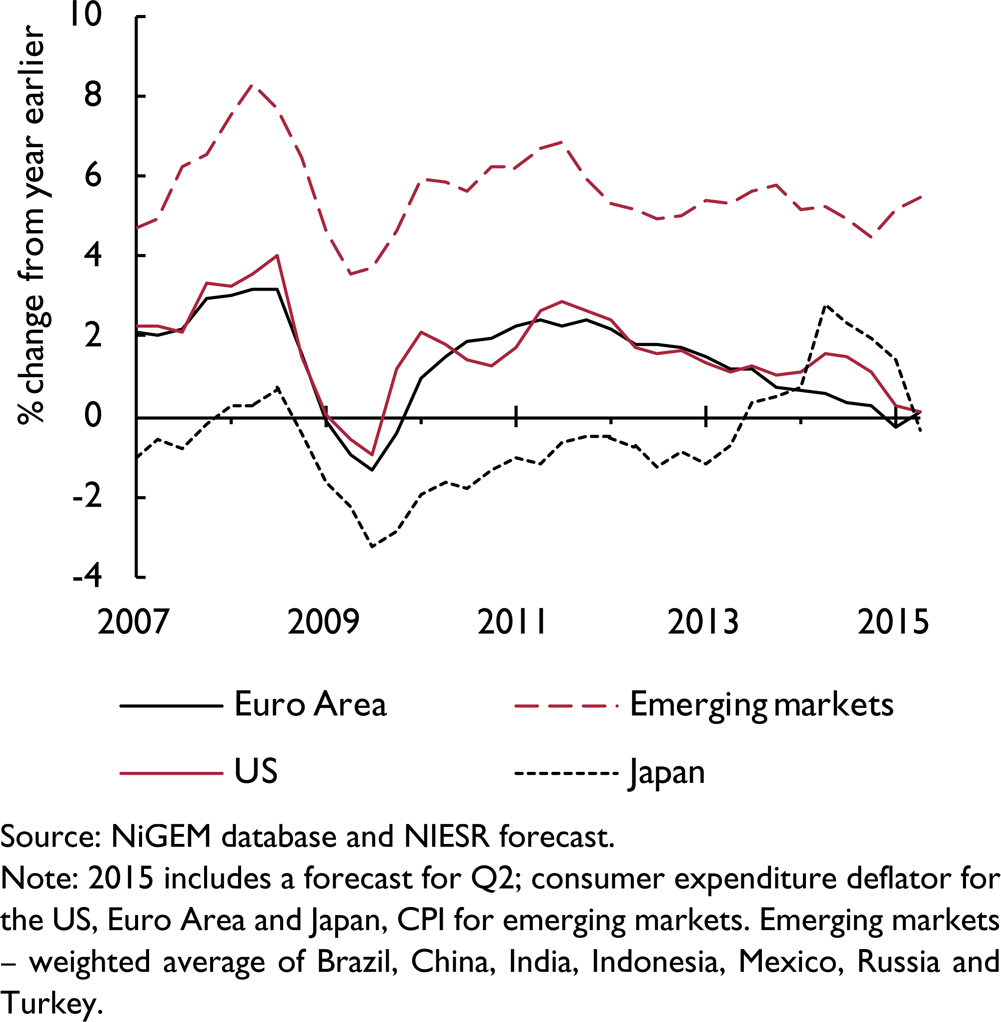

Recent data have confirmed the May Review's finding that the threat of deflation in the advanced economies, which had been a particular concern in the Euro Area, has receded. Although still below central banks' objectives, headline inflation in most major advanced economies has risen to positive levels, and it is expected to rise further in the coming months as the oil price decline begins to drop out of 12-month comparisons. Core inflation rates have remained broadly stable and estimates of expected future inflation (from financial markets and surveys) have risen closer to targets. Inflation has remained negative, however, in several of the smaller economies in the Euro Area. In emerging market economies, inflation developments have been uneven – well above targets in Brazil and Russia, while in China annual consumer price inflation has fallen to about 1.5 per cent (half the official target) while producer prices have been declining for more than three years.

The central banks of the Euro Area and Japan have continued their programmes of large-scale asset purchases, with their benchmark short-term interest rates set at or below zero. In the United States, Federal Reserve officials have indicated that while their decisions will remain data-dependent, the first increase in the target federal funds rate from the near-zero floor where it has sat since December 2008 is likely before the end of 2015. In fact, at the Fed's mid-June policy meeting most participants indicated that they expected that two or three increases of 25 basis points would be appropriate by the end of this year, with only two out of the seventeen expecting none. Chair Yellen has emphasised that the timing of the first increase is less important than the future path of rates, and that the Fed expects this path to be gradual, with monetary policy remaining highly accommodative for some time. Our forecast is based on the assumption of one increase in 2015, in September. Among other advanced economies, central banks have lowered benchmark interest rates further since late April in Australia, Canada, Iceland, New Zealand, Norway, South Korea, and Sweden, in the last case deeper into negative territory, to −0.35 per cent. Official interest rates have also been lowered since late April in China, India, and Russia, but raised in Brazil and South Africa.

World inflation

In financial markets, the most significant development since April has been a general rise in government bond yields across the advanced economies, most markedly in the Euro Area. Since late April, 10-year sovereign yields in the major countries of the Euro Area have risen by 50–70 basis points, compared with about 40–45 basis points in the US and the UK and 10 basis points in Japan. Possible explanations include upward revisions in expectations for growth and inflation – the latter being indicated also by market and survey estimates of inflation expectations, and being related, possibly, to the stabilisation and partial recovery of oil prices between March and June. Another is the possibility that yields had earlier overshot on the downside: in some cases, they had fallen to unprecedented levels, even lower than 0.1 per cent in mid-April at the 10-year maturity in the case of Germany. Contagion from the Greek crisis in financial markets has been limited to a modest and temporary widening of yield spreads in the peripheral economies of the Euro Area.

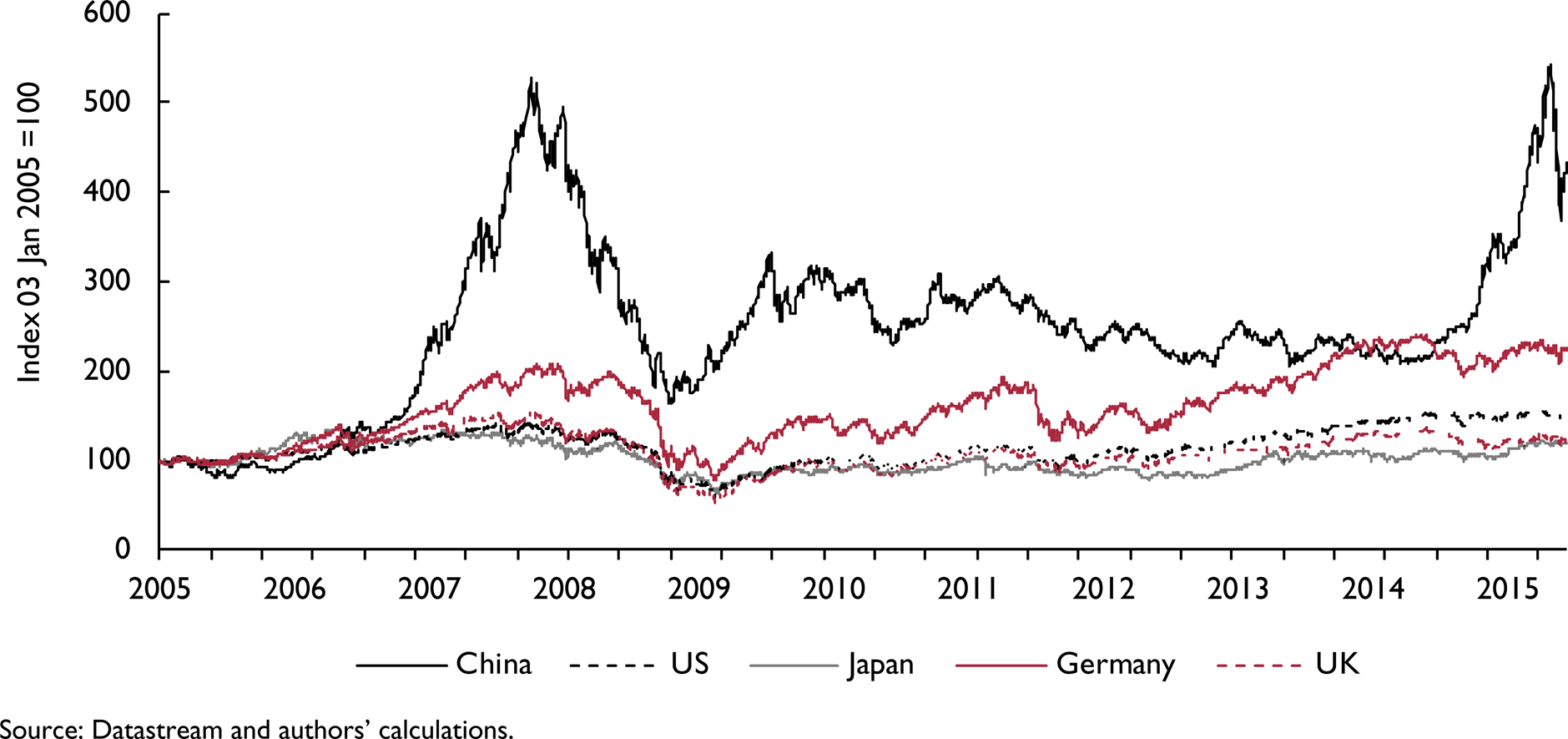

Another striking development in financial markets has been the swings in Chinese equity markets. After a period of relative stability since the 2007–8 price drop, these markets began rising in July 2014, and by mid-June this year prices were 140 per cent higher than a year earlier. This surge, hardly attributable to fundamentals, seemed to be encouraged, implicitly or explicitly, by the authorities, including by several cuts in interest rates. Prices peaked and turned around in mid-June, and by early July had fallen by about one third from their peaks, to levels last seen in March. The authorities then took a number of extraordinary actions to reverse the decline, including the suspension of trading in shares of about half the companies quoted on the main markets, and restrictions on selling by brokerages to apply as long as the market remained below a certain level. These measures halted the fall in prices and led to a partial but erratic recovery in late July. Movements in other equity markets in recent months have been unremarkable.

In foreign exchange markets, the US dollar's value in late July was little changed from three months earlier in terms of the euro, the Chinese yuan, and the Indian rupee, but moderately higher against the Canadian dollar and the yen and slightly lower against the pound. The weakest major currencies in this period were the Brazilian real and the Russian rouble, both of which depreciated by 12 per cent. The recent depreciations of the Canadian dollar and the rouble seem to be related to the renewed weakness in oil prices since early June. By late July, oil prices had fallen by about 20 per cent in US dollar terms since early June, although they still stood about 5 per cent higher than the lows reached in January. A report from the International Energy Agency in early June projected robust growth in oil supplies this year, despite a slowdown in supply from non-OPEC sources. The prospective removal next year of sanctions on Iranian exports, following the international agreement reached in July with Iran on the curtailment of its nuclear programme, is a new factor weighing on prices.

Risks to the forecast and implications for policy

The risks discussed in recent issues of this Review remain relevant. The risk of deflation has waned in most advanced economies, but it is still apparent in some of the smaller European economies and also in China, and it may reappear more broadly if the renewed weakening of oil prices since June deepens. On the other hand, especially given the apparently limited demand response so far to the fall in oil prices over the past year, an upside risk to our growth forecast is a larger, lagged boost to demand than we are assuming for the period ahead. An important downside risk remains the possibility of disruptive financial market reactions to the start of the normalisation of monetary policy in the United States, even though the forewarnings have been many and loud. Further appreciation of the US dollar is one possible response to an upward move in US short-term interest rates, and this would damage the balance sheets of dollar debtors, especially corporate borrowers in emerging market economies, with likely negative consequences for demand and growth. A further strengthening of the dollar may also threaten a re-widening of global payments imbalances. The continuing weakness of economic recoveries in most cases, the fragility of balance sheets associated with continuing high levels of debt, and the toxic effects on debt burdens of weak economic growth and below-target inflation point to the need for continuing highly accommodative monetary policies, as acknowledged, for example, by the Fed.

Recent developments have highlighted two particular sets of risks, one relating to Greece and the Euro Area, and the other relating to China.

First, Greece. Our forecast assumes that the new policy programme being negotiated with Greece, supported by the associated financing arrangements, will return the Greek economy to a path of moderate recovery, and that the Euro Area will remain intact. But risks are evident both to the Greek economy and to the functioning of Europe's Economic and Monetary Union and the integrity of the Euro Area.

Risks to the implementation of Greece's policy programme arise partly from the lack of ownership of it by the government and the population. A referendum in early July rejected proposals along the lines of those now being negotiated, and during the parliamentary debate on measures that needed to be approved as a pre-condition for the current talks, the Prime Minister referred to the programme's “irrational proposals” and told the Greek Parliament, “I don't believe the measures will benefit the economy, but we are forced to adopt them”. History has taught the importance of country ownership to the success of externally financed policy programmes, so the clear absence of this in Greece is not auspicious.

Another, related, problem is that agreement is still lacking on the provision of the debt relief that is needed to make Greece's debt burden sustainable. President Draghi of the ECB said on 16 July that “It's uncontroversial that debt relief is necessary, and I think that nobody has ever disputed that”. Yet Germany's Finance Minister has recently said that “a debt cut is incompatible with membership of the currency union”, pointing to apparent difficulties in agreeing on a form of debt relief that is compatible with the rules of the Euro Area, which dictate no bail-outs or fiscal transfers among members. Meanwhile the IMF has indicated that it will not participate in new financial assistance for Greece without substantial debt relief.

Further risks are attached to the economic results of the programme being negotiated. Assumptions about economic growth adopted in earlier Greek programmes have been disappointed by wide margins – to some extent, perhaps, because structural reforms were not implemented as assumed, or because the growth benefits of the reforms that were implemented were over-estimated, but in significant part, clearly, because assumed fiscal multipliers proved to be too small. Similar risks arise again now: in order to avoid policies that cause Greece to sink into even deeper depression – with a debt burden that becomes even more severe as the economy shrinks – the programme currently being negotiated with Euro Area institutions and the IMF will need to involve not only substantial debt relief but also a significant relaxation of targets for the primary fiscal deficit. Otherwise, Greece's exit from the Euro Area may become the only way of resolving its difficulties.

Risks to the broader Euro Area system have been highlighted by recent developments surrounding Greece, including the acrimonious negotiations between Greece and its Euro Area partners on the programme's prior actions. A particularly significant recent development has been the open discussion, for the first time among ministers and officials, of the possibility of a country's exiting the Area. Indeed, the German Finance Minister proposed that an agreed, temporary exit, for “at least the next five years” could be “a better way for Greece”, and the German Chancellor has referred to a voluntary, organized “Grexit” as a “viable option”. It has thus been officially acknowledged for the first time that membership of the Euro Area is not irreversible. There is clearly a risk that this will additionally destabilise the system by reducing its cohesion and confidence in its permanence.

More fundamentally, the Greek crisis has highlighted shortcomings of the Euro Area's institutional and policy arrangements, and revived doubts about whether Europe's economic and monetary union can succeed without deeper economic, fiscal, and political integration than is currently envisaged.

As President Draghi said on 16 July, “this [economic and monetary] union is imperfect. And being imperfect, [it] is fragile, [it] is vulnerable, and doesn't deliver all the benefits that it could if it were to be completed”. Draghi was a co-author of the recent “Five Presidents' Report” on Completing Economic and Monetary Union (EMU) by 2025 (see Box A). This proposes a two-stage programme of action that would, most importantly, complete the banking union (by establishing a unified deposit insurance scheme and a credible common backstop for the Single Resolution Fund), establish a capital markets union, and also establish a fiscal “stabilisation function” to “better deal with shocks that cannot be dealt with at the national level alone”, but which would be available only to economies that have achieved substantial progress in convergence towards “similarly resilient national economic structures”. In Draghi's words, the Report provides a “rather broad roadmap”, and in effect “urges member countries to reflect” on the design of the arrangements to be adopted. Therefore much remains to be done before the Report's proposals are translated into specific reforms and then implemented. And even then, as the Report acknowledges, the completed EMU it envisages would be one with no large-scale or permanent fiscal transfers among members and only limited labour mobility, so that there would still be significantly less economic integration than in other monetary unions.

One problematic feature of current arrangements that will apparently remain is the contractionary bias associated with asymmetric adjustment requirements. Countries with financing and competiveness difficulties, like Greece, are required to implement contractionary fiscal measures and structural reforms to compress domestic demand and to reduce production costs and thus achieve “internal devaluation”. But countries with current account surpluses and over-competitiveness are required to do nothing. Germany is currently close to full employment with a large external current account surplus, which we project at 9 per cent of GDP this year – the largest surplus in the world in absolute terms. Full employment and a large current account surplus, together, are classically symptomatic of an undervalued currency, and if Germany had its own currency there would naturally be pressures for revaluation. Given Germany's membership in the Euro Area, this corrective mechanism does not operate. There have recently been signs that a different corrective mechanism – an increase in wage inflation in Germany relative to Euro Area partners – has begun to operate, as shown in the section on Germany below. But such progress has been slow, and there is a strong case for measures in Germany to boost domestic demand and achieve “internal revaluation” by raising domestic prices and costs, especially given that domestic inflation remains close to zero. One example of such a measure would be a boost to public sector investment spending; another would be an increase in public sector wages. But Euro Area arrangements put no effective pressure on Germany to adopt such measures. With the pressure for adjustment therefore only on deficit countries for “internal devaluation”, two damaging consequences follow: there is a contractionary bias to policies in the Area as a whole, and the countries adjusting may find it difficult to achieve their objectives because reducing domestic inflation below the already low levels of Euro Area partners will exacerbate the challenge of reducing their debt burdens.

Second, China. Our forecast assumes a continuing, gradual slowing of growth as the economy makes a transition from a high-growth path dependent mainly on investment and exports, which has led to the accumulation of significant excess capacity and, since 2008, large-scale debt, to a path of more moderate growth driven more by household consumption. This transition is meant to be accompanied by further market-oriented reforms, including in financial markets, for example with the elimination of ceilings on bank deposit rates. Thus in November 2013, the third plenum of the Communist Party's Central Committee pledged a “decisive” role for the market in allocating resources in the period ahead, rather than the “basic” role previously assigned.

Stock market price indexes (in US$)

Some recent developments have increased risks to this strategy. While official GDP data have shown growth in line with the official target for 2015 of “around 7 per cent”, other indicators suggest that growth may have slowed somewhat more sharply. Meanwhile, annual consumer price inflation has slowed over the past year to 1.4 per cent, well below the official 3 per cent target; producer prices have been falling for more than three years; and the GDP deflator also fell in the year to the first quarter. Concerns about deflationary pressure seem to have been one factor leading the central bank to reduce its benchmark interest rates four times between last November and late June, by 1 percentage point in total, to unprecedented lows. But another consideration seems to have been the stock market: the authorities appear to have deliberately encouraged a rise in equity prices, partly through lower interest rates but also through the promotion of equity investment in the media, partly in order to facilitate the replacement of debt with equity finance in state-owned enterprises. The central bank's most recent interest rate cut was implemented in late June, even though equity prices were continuing to rise, far beyond levels that could be reasonably explained by fundamentals. Shortly thereafter, the market peaked and turned around, but the authorities soon took extraordinary measures to halt the decline, showing that they would not trust the market to find its own level.

Three risks are suggested by these developments. One, that the recent stock market decline may significantly reduce the growth of domestic demand, can probably be largely discounted, given the relatively short-lived surge in prices and the relatively narrow ownership of equities (involving only 6 per cent of households in early 2015). A second risk is that the recent easing of monetary conditions may slow the reduction of indebtedness and the associated dangers of financial instability. A third risk, and possibly the most serious, is that the authorities' recent interventions in the equity market, contravening the declared “decisive role” of market forces, may not only discourage participation in the equity market by increasing uncertainty about government intervention (including restrictions on the selling of stock), and thereby impede the needed substitution of equity for debt finance, but also also reduce confidence, more broadly, in the government's market-oriented reform strategy.