Abstract

This commentary article proposes three ideal types of ‘anchoring of finance capital into the city’, i.e. the way in which capital, as it is valued in financial markets, is transformed into real capital and vice versa. Some contexts will allow market finance s visions of the city to become reality without great alteration, and this produces the ‘financialised city’. In this case, the value of the city corresponds to trading on the financial markets and largely depends on the financial operators’ comparative and mimetic criteria. Second, the ‘entrepreneurial city’ corresponds to a tangible and localised vision of the city, outside the trading rooms. This requires interactions between intermediary and allied actors so that urban value can be translated into real profits and tangible urban objectives while mobilising market finance. Third, some contexts may promote debate, the creation of interdependencies and the genesis of multiple externalities, particularly around major urban development projects. This is what we call the ‘negotiated city’. Here, urban value depends much more directly, and more exclusively, on more or less complementary interactions between local and non-local actors, users, consumers, public actors, tourists, etc.

The articles in this special issue are positioned in relation to the work of David Harvey (2006 [1982]) in particular. The intention is to show both the different actors and various forms of ‘capital landing’ in the city and the way in which ‘land as a financial asset’ is made possible. To give nuance, firstly, to the macrocentric and abstract perspective of financial capitalism but also the vision of the city as a passive receptacle of financialisation, the authors of this special issue mobilise intermediary theories to allow us to ‘link the scales’ and understand the actors and their relationships (agency) as they are located within their institutional context.

Drawing on various streams of socio-economic theory, Crosby and Henneberry (2016) highlight, in particular, the investment assessment tools used by financial actors; Sanfelici and Halbert (2016) and Rouanet and Halbert (2016) address discourse within the context of financial actor visions of the city; Ashton et al. (2016), Gotham (2016), Fields and Uffer (2016) and Guironnet et al. (2016) focus on the contracts and legal formatting required for the construction of financialised urban rent. In other words, while mobilising theories of action and, in particular, the sociology of the financial markets, the authors come out of the ‘trading rooms’ (Corpataux and Crevoisier, 2015). They show how the various intermediary actors – developers, real estate consultants, municipalities, etc. – within the financialised branch of urban production (Theurillat, 2011) are able to perform the various translations (Callon, 1999) required for anchoring financial capital in the city, i.e. the way in which capital, as it is valued in financial markets, is transformed into real capital and vice versa. In this commentary, we extend previous reflections (Theurillat, 2011; Theurillat and Crevoisier, 2012, 2013) on this anchoring process under the general proposition that different forms of value both arise and receive varying degrees of recognition and legitimation within particular local urban contexts based on negotiations between different actors, including financial actors and/or their intermediaries.

Specifically, we distinguish between three ideal types of cities (see Table 1). Some contexts will allow market finance’s visions of the city to become reality without great alteration, and this produces the ‘financialised city’. In this case, the value of the city corresponds to trading on the financial markets and largely depends on the financial operators’ comparative and mimetic criteria. Secondly, the ‘entrepreneurial city’ corresponds to a tangible and localised vision of the city, outside the trading rooms. This requires interactions between intermediary and allied actors so that urban value can be translated into real profits and tangible urban objectives while mobilising market finance. Thirdly, some contexts may promote debate, the creation of interdependencies and the genesis of multiple externalities, particularly around major urban development projects. This is what we call the ‘negotiated city’. Here, urban value depends much more directly, and more exclusively, on more or less complementary interactions between local and non-local actors, users, consumers, public actors, tourists, etc. Based on these ideal types, we advance the thesis that when market finance largely imposes its visions, the value of the parts of the city that it shapes and controls can rapidly progress towards obsolescence while, when local actors anchor this capital more openly, urban value is greater right from the start and can grow over time to the benefit of many actors, including financial actors.

The financialised, the entrepreneurial and the negotiated cities.

Source: Authors’ own research.

The financialised city: Weak anchoring of capital imposed by the ‘trading rooms’

‘Pure’ market finance is characterised by continuing and comparative quoting of asset values (Table 1). Among these, real estate investment funds are an investment class just like any other. For portfolio managers and financial operators, the only question is, at any given moment and in the context of the listed investment vehicles, which securities should be sold in order to purchase which other securities. The city is compartmentalised and grouped into homogeneous and standardised categories (residential, offices, infrastructure, etc.), which are characterised by two numbers; risk and expected yield. Market finance indeed can transform a real, immobile asset such as a building or an infrastructure into a financial asset that is negotiable on the financial markets and that becomes liquid and mobile in space (Corpataux and Crevoisier, 2005). This abstract representation, independent of tangible qualitative conditions, is sufficient to enable financial actors to effect their transactions. They are not interested in seeing what happens behind their screen. They ‘place’ their money; they do not ‘invest’ because they do not have the skills to allow them to build tangible parts of the city. Moreover, based on a logic of portfolio management, investors compare the financial risks and yields of one real estate investment fund (in offices, flats, infrastructure …), with another, but above all with those of other categories of financial assets, by sector (company stocks, derivatives, commodities, for example) and by territory (European countries, emerging countries, etc.) (Theurillat, 2011; Theurillat and Crevoisier, 2013).

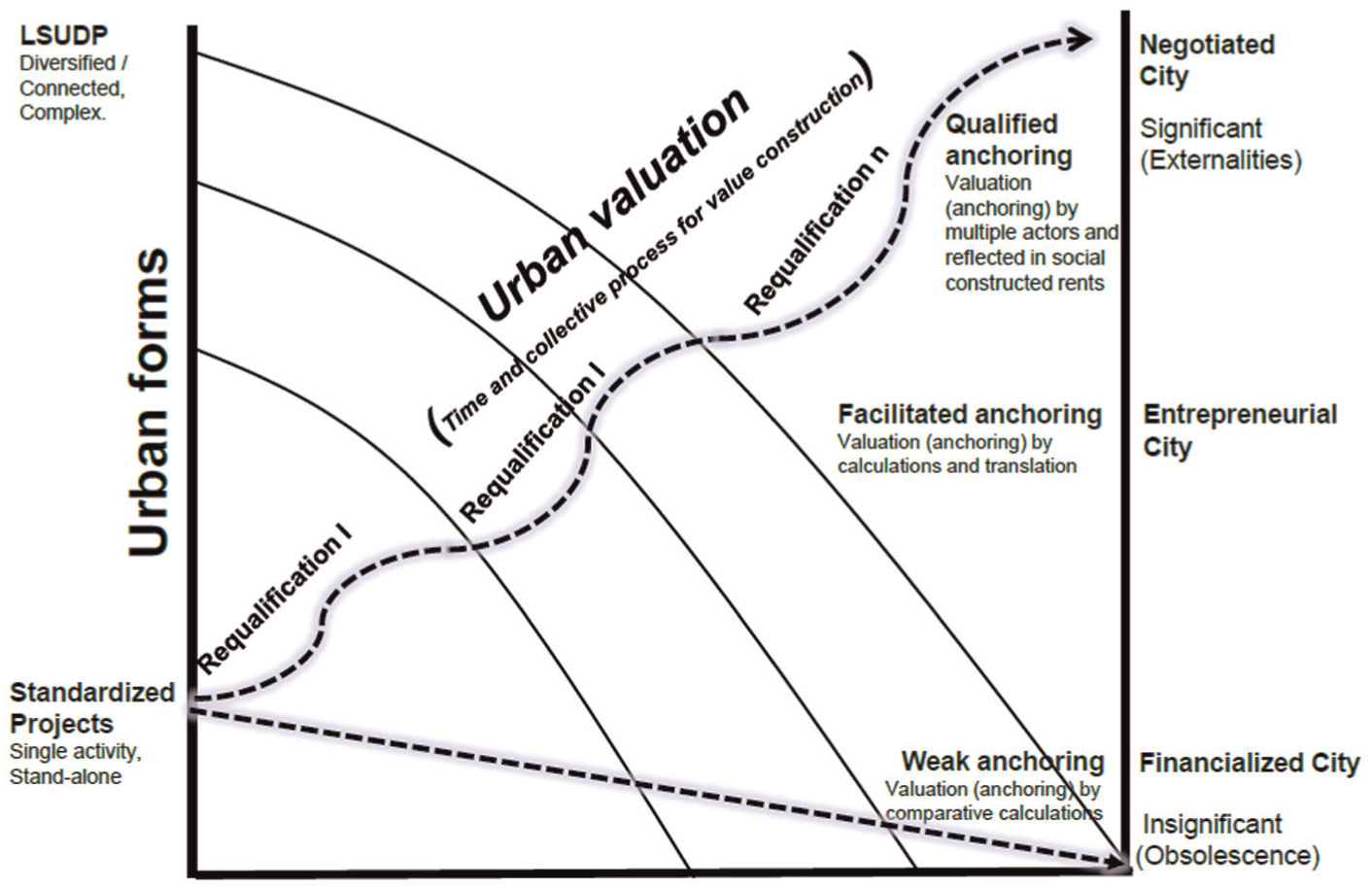

The contributions to this special issue largely look beyond this stereotypical trader behind a screen whose work is limited to buying and selling on the basis of a rational comparative calculation. Players in the market finance ‘real estate/urban infrastructure’ asset class (which includes all the various and less liquid investment funds: Ashton et al., 2016; Fields and Uffer, 2016; Guironnet et al., 2016; Rouanet and Halbert, 2016) do have strategies and investment horizons that can range from years to decades, and which are also directly linked to the buildings they hold on behalf of their shareholders. As a corollary, they need intermediary actors, such as developers, municipalities or various real estate investment advisors and professionals to anchor the capital involved more or less effectively in the urban context. These indispensable intermediaries ‘translate’; they anchor the financial criteria of risk, yield and liquidity in urban objects. This translation will vary depending, on the one hand, on the power of the financial players and, on the other, on the ability to play the interdependencies extant within local communities. In Actor-Network-Theory (ANT) terms (Callon, 1998; Latour, 2005), finance ‘calculates’ and ‘performs’, i.e. it is able to make reality, but via a more or less developed translation of its own way of understanding the world. The anchoring of financial capital in the city can be more or less ‘rich’, ranging from weak, decontextualised and financialised to qualified and negotiated (see Figure 1 and Table 1).

Three types of capital anchoring and urban valuation.

A ‘weak’ and decontextualised anchoring is characteristic of the financialised city. It culminates when the city is completely subordinated to market finance, allowing it to extract monetary value almost instantaneously in order to reinvest it elsewhere. This means the financial calculation focuses exclusively on risk/yield in the short term (liquidity), which inevitably leads to the obsolescence of certain fragments of the city (Lamunière, 2004). Weak anchoring of financial capital is the preferred method of operation of private equity funds (Fields and Uffer, 2016). In such cases, the city is overrun by finance; it becomes dysfunctional and quickly loses monetary value. Obsolescence can be rapid. An extreme example is that of the Spanish ghost towns (Gentier, 2012; Coq-Vuelta, 2013), where the reconstitution of financialised capital was so fast that usage value was never even realised; fast successive sales within financial markets ensured that developers and early investors recouped their investment without the question of value for other urban actors ever arising. These homes will probably never be occupied, revealing an immediate obsolescence. In short, in this case, it was hardly necessary for the capital involved to take an actual form in order to be reproduced and accumulated; ‘real’ capital and value proved nothing but pretexts for the reproduction of financial capital.

The entrepreneurial city: Facilitated anchoring of financial capital and a look beyond the ‘trading rooms’

The second type of anchoring of financial capital in the city is represented in the notion of the entrepreneurial city (Brenner and Theodore, 2002; Harvey, 1989; Theurillat, 2011). Here the anchoring is facilitated or even organised. Financial actors succeed with the help of intermediaries and a coalition of actors, such as municipalities and developers, to format and extract urban rent. The capital of financial investors, which provides a boost to the real estate industry (Guironnet et al., 2016; Rouanet and Halbert, 2016; Sanfelici and Halbert, 2016), is accompanied by framing and calculations (risk, yield and liquidity) that perform the city (Callon, 1999; MacKenzie, 2003). Urban models are standardised and the extraction of rent can be secured in the long term, e.g. for office real estate (Crosby and Henneberry, 2016), operation of urban infrastructures or industries (Ashton et al., 2016; Gotham, 2016) or through the construction of large-scale urban development projects (LSUDP) (Guironnet et al., 2016).

However, the various contributions show that this second type of anchoring is caught in a vice. On the one hand, the capital anchoring emerges well here, based on the tangible nature of buildings, a ‘real’ yield and management that must reflect usage value or other urban values, such as aesthetics, for example (office buildings, LSUDP). Financial management of urban objects in the more or less long term is made possible thanks to the intermediary actors who analyse, reflect and embody the aspirations of both the financial actors and the other actors within the urban fabric. On the other hand, despite these important socio-technical tools – the expertise and knowledge of local markets and the alliances with local actors – the city also remains subject to the visions of the ‘trading rooms’. Indeed, financial investors, those located upstream of the investment chain, such as portfolio managers, traders and the shareholders of various investment funds, keep the properties in Excel spreadsheets and ‘arbitrate’ according to market finance categories (risk, yield, liquidity). The city is seen as a collection of buildings, each fulfilling a standardised function on the international scale (for example, a Class A office building), independently of each other, for which amortisation is determined in advance over a certain time period, ranging from a few years for an ‘opportunistic or value-added’ real estate fund to 30 years for a ‘core’ real estate fund or pension fund, and which are located in an abstract space generating no externalities. The question of interdependencies between the different parts of the city and the relationship between spaces is removed from the financial calculation, which partitions functions and spaces to allow the financial operator to create her or his own portfolio.

Production of the negotiated city: A co-construction of urban value

In contrast to the ‘financialised city’, and as a continuation of the key role played by the various intermediaries and local actors in the entrepreneurial city, we advance the idea that a third type of anchoring is possible. The negotiated city postulates spatial, social and economic interdependencies within the city, between the city and its hinterland and between cities. It is these interdependencies that are the characteristic of urbanity itself, which generates both positive and negative externalities and demands more comprehensive understandings of the notion of urban value (Table 1). Here it is not so much about considering the performativity of financial theories but rather the social construction of urban value, and the process of urban valuation – how the values of the various participating actors are collectively translated into the more specific forms of economic and monetary value for investors (Aspers and Beckert, 2011; Stark, 2011), usage value for users and experiential value for those who spend time in the city (Guex and Crevoisier, 2015; Jeannerat, 2013; Schulze, 2005). Furthermore, valuation includes the way in which socio-cultural values, such as aesthetics, sustainability, innovation, etc., are implemented within the social processes of evaluation and value-creation. These various socio-cultural values add quality to a project, and must be somehow also translated into quantitative metrics and monetary terms. This translation becomes here the core analytical issue (Aspers and Beckert, 2011).

In other words, urban value when properly understood results from local context and is the outcome of multi-participant negotiation and, while reflected in rents, is not normally identical to the value ascribed to financialised urban assets, the evaluation of which depends largely on abstracted comparative factors and general movements within financial markets.

Negotiations on space: Interdependencies and externalities

For neoclassical economics, external effects do not matter if relevant costs/benefits are compensated through the market. Thus, a well-located apartment near a train station does not enjoy an externality where the market demands a higher price. However, this example says nothing about how potential externalities first arise (in the example just mentioned, how the station was built say, including the appropriation of added value by the owner at the time of construction of the station, by the public authorities that set a tax, by the company that built the station, etc.). We must bear in mind that it is the construction of externalities, and therefore the starting point of the process of construction of value, which is the object under examination here, not a situation at a given time. In addition, the construction of rent in this instance must not to be confused with ‘traditional’ rent (Alonso, 1964), which corresponds to an increase in urban value induced by an increase in external (productive) competitiveness within a region. Here, externalities are seen as the result of social interactions that can be self-sustaining, at least partly, due to significant multiplier effects for local urban investments.

For ‘functional’ projects, as in the examples of buildings in the heavily populated neighbourhoods of New York and Berlin (Fields and Uffer, 2016), infrastructure such as a car park or bridge in Chicago (Ashton et al., 2016) and industrial projects of all types in Louisiana (Gotham, 2016), value is often created mainly by the producer. In these instances, it is more difficult to mobilise the usage or experiential values or the opinions of consumers. In contrast, negotiations may be intense during the creation of LSUDPs, which often shape the city by virtue of their size and which are often symbolic urban centralities. Because of their importance within and to the city, they generate a lot of externalities and their value increases when one takes fully into account the environmental, social and cultural elements that give ‘meaning’ to their existence, and which contribute to their monetary value: ultimately, where solutions are found, the price will be higher. LSUDPs will be ‘evaluated/calculated’ not only by the financial owners but also by the municipality, tenants/operators, as well as citizens and consumers. However, there are considerable differences in the way in which these actors will perform their valuation of the city as well as formidable challenges in the search for common metrics.

Urban value as the outcome of different valuations

The concepts of calculation, performativity, framing and overrunning, developed by Callon (1999, 2007) as part of a broader sociology of translation, clearly help us to interpret the negotiations that take place between actors in urban development contexts. Callon is specifically concerned with addressing what actually makes calculation possible. He also gives the notion of calculation a very broad meaning, since, for him, it is the activity of identifying and ordering ‘possible world states’, as well as identifying the actions needed for the production of each of these world states.

Applied to the urban fabric, the different contributions in this issue highlight the importance of typical intermediary actors and ‘translators’ that support financiers and large construction and development companies. The latter cannot ignore qualitative and contextual elements, especially in the case of a LSUDP, and this is true in the three main valuation stages (design, implementation and operation) (Theurillat and Crevoisier, 2013). Negotiation is prominent in the design phase. The development company, in conjunction with local authorities and other actors, will organise a more or less open negotiation process, which is largely dependent on local institutions and political practices. However, LSUDPs may require regulatory changes, significant public investment and typically have a significant impact on the urban landscape. Consequently, public debates that are essential for the construction of urban value should always take place, notably in countries where voice (Hirschman, 1986) is made possible.

All the uncertainties associated with LSUDPs make calculation in advance difficult for most actors. On the one hand, some actors, such as development companies, investors, tenants, retailers etc., need a strong framing and will, therefore, privilege a number of possible limited and controllable elements on which to base their calculation. On the other hand, for public authorities, civil society, users, etc., uncertainties, externalities and overruns, concerning not only quality but also the distribution of value and over-costs retain priority.

From a territorial perspective, and contrary to Harvey’s vision, urban production is not a zero-sum game, where the question can be summarised as the division of a rent created by the accumulation of capital. In the negotiated city, financiers are only one kind of actor among all the others, and are also often absent from direct negotiations (Theurillat and Crevoisier, 2013). This is where the financial actors are both upstream and downstream or, rather, overlooking the urban value construction process. The negotiation and valuation process involves several evaluation frameworks and multiple measuring grids to estimate value (calculation algorithms) (Antal et al., 2015). This process is not exclusive to financiers but results from a collective effort that is not free from conflict (Callon et al., 2009). These ‘conflicts of values’ can block an urban project or, on the contrary, give rise to compromises which take the form of transactions (mainly monetary but also non-monetary in nature) between the actors involved and which are necessary for the consideration of multiple interests.

The negotiated city against ‘simple’ capital landing into the city

In conclusion, we posit, as an exploratory and normative thesis, that the negotiated city, due to the greater consideration shown to local context, increases urban value provided that it integrates qualities, externalities and obsolescence into the negotiations and power balances within the urban fabric (Figure 1). As is well understood by planners, real estate objects can acquire a high economic, socio-cultural and environmental value if they are both diverse and complementary and form a system due to a broader negotiation process.

Ultimately, urban value cannot depend solely on financial actions, even in alliance with privileged local actors. It should be borne in mind that collective value construction processes (urban valuation) result in validations, invalidations and periodic requalification. Our thesis is that when these processes take place within the context of a negotiated city, urban value can increase and the risk of obsolescence can be mitigated. It is therefore necessary to take into account the diversity of the local capacity to anchor projects and thus generate more usage value from the same amount of investment. Some local contexts follow ‘virtuous’ valuation trajectories; others, which may not have the institutions – not forgetting places where public debates are simply not possible – or the tradition of negotiation, or where the local environment proves to be confrontational and blocking, will not allow the (re)qualification of objects.

Footnotes

Funding

We would like to express our sincere thanks to the Swiss National Science Foundation (SNSF) for its support to our research (Project Number P300P1-147823/1and CompleXdesign PDFMP1_ 141728).