Abstract

This research assesses the importance of financial access on value added in three economic sectors in 25 countries in Sub-Saharan Africa using data for the period 1980–2014. The empirical evidence is based on the Generalized Method of Moments. Financial access is measured with private domestic credit, while the three outcome variables are: value added in the agricultural, manufacturing, and service sectors, respectively. Enhancing financial access does not significantly improve value added in the agricultural and manufacturing sectors, while enhancing financial access improves value added in the service sector. An extended analysis shows that, in order for the positive net incidence of enhancing credit access on value added to the service sector to be maintained, complementary policies are required when domestic credit to the private sector is between 77.50 percent and 98.50 percent of GDP. Policy implications are discussed.

The research question of this study is straightforward and simple to follow: how does enhancing financial access influence value added across economic sectors in Sub-Saharan Africa (SSA)? Two premises in the scholarly and policy literature motivate the positioning of this research: the role of financial access in economic development and contemporary gaps in the economic value-added literature. These two motivational underpinnings are taken in turn.

First, as supported by the theoretical framework outlined a little later in this article, contemporary financial development studies are broadly consistent with the importance of financial access in development outcomes, especially in enhancing avenues of investment and the betterment of households and business entities, the amelioration of standards of living, the creation of jobs, and improvements in societal welfare (Boadi et al. 2017; Bocher, Alemu and Kelbore 2017; Chapoto and Aboagye 2017; Chikalipah 2017; Iyke and Odhiambo 2017; Makina 2017; Obeng and Sakyi 2017; Odhiambo 2010, 2013, 2014; Ofori-Sasu, Abor and Osei 2017; Osah and Kyobe 2017; Tchamyou 2019, 2020; Tchamyou, Erreygers and Cassimon 2019; Wale and Makina 2017). This research complements the attendant literature by focusing on the relevance of financial access in value added across economic sectors owing to an apparent gap in the contemporary value-added economic literature.

Second, it is relevant to note that the attendant literature has focused distinctly on each of the three sectors without engaging the financial access channel. The contribution of the present study to the attendant literature is to engage the three sectors simultaneously within the framework of the hitherto neglected financial access channel. The corresponding scholarship on value added across economic sectors has, to the best of our knowledge, focused on the three main sectors of the economy: namely, the agricultural, manufacturing, and service sectors.

In the agricultural sector, the attendant scholarship has been oriented toward smallholder agricultural development (Lutz and Olthaar 2017). Specifically, van Rijsbergen et al. (2016) engage the impact of coffee certification on farmers’ welfare in Kenya. Lutz and Tadesse (2017) are involved with competitiveness versus inclusiveness in global value chains and the African farmers’ market organization. Olthaar and Noseleit (2017) position their research on a comparative analysis of farmers cooperatives to non-members in SSA. Metzlar (2017) assesses the strategic intents and projects of farmers with smallholder features in the cocoa industry of Ghana. Vermeire, Bruton and Cai (2017) examine linkages between global value chains and the economic prosperity of poor landowners. Finally, Uduji and Okolo-Obasi (2018a, 2018b) assess how crop varieties can be improved with the help of gender inclusive policies.

Within the framework of the manufacturing sector, van Lakerveld and Van Tulder (2017) focus on leading Dutch corporations in SSA that are involved with supply chain practices, which are characterized by transition management; Banga, Kumar and Cobbina (2015) are concerned with trade-related value chains in SSA within the premise of the leather sector, while Ruben, Bekele and Lenjiso (2017) focus on the dairy sector of Ethiopia in which they investigate connections between value chains and quality upgrading. Previous studies on the service sector are, however, sparse. In this strand, Beerepoot and Keijser (2015) are concerned with the relevance service sector outsourcing as a driver of economic prosperity in the Ghanaian information and communication technology (ICT) sector.

This research complements the engaged literature by focusing on the importance of financial access in value added across the three economic sectors. The corresponding research question is: how does enhancing financial access affect value added in the agricultural, manufacturing, and service sectors in SSA? The remainder of the study is structured as follows. The theoretical underpinnings are covered next, before we focus on the data and methodology. The empirical findings and attendant discussion are then provided. The research concludes with policy implications and future research directions.

Theoretical Underpinnings

Two principal theoretical considerations can be employed to motivate the connection between financial access and values added in the agricultural, manufacturing, and service sectors. Beyond these considerations, from intuition, corporations need funding to improve agricultural goods in the primary sector, manufacturing goods in the secondary sector, and services in the tertiary sector. Hence, it is natural to associate enhanced financial access with improvements in the quality of activities or value added in the three attendant sectors.

The main theories are the intensive and extensive margin theories (Asongu, Nnanna and Acha-Anyi 2020a; Asongu, Nnanna and Acha-Anyi 2020b). The intensive margin theory reflects the perspective that more financial access is offered to enterprises that are already using financial services in the formal financial sector so that such enterprises can enhance the value for their products and services. This, by extension, improves the value of the corresponding sectors. The extensive margin theory is not contradictory but complementary to the intensive margin theory. The reason is because it implies that enterprises previously not benefiting from formal financial sector credit can be offered credit for the purpose of improving their goods and services and, by extension, the value of the sector in which such enterprises (which were previously excluded from the formal banking sector) operate. However, the three contending strands are discussed before the extensive and intensive margin theories to clarify various perspectives of the theoretical literature in order to balance the narrative and prepare the reader for an outcome of the empirical analysis that may be contrary to expectations.

According to Tchamyou et al. (2019), one contending theory on the importance of financial access in economic prosperity maintains that enhanced access to finance is essential in fostering economic development and associated components, including the three main sectors of the economy. This strand is in line with a bulk of literature on the nexus between financial access and development outcomes which posit that financial access by means of financial intermediary allocation efficiency enables the tailoring of projects to profitable and promising projects of investment (Aghion and Bolton 2005; Galor and Moav 2004; Galor and Zeira 1993). This research contends that such investment projects should be apparent in one of the three sectors of the economy: namely, the agricultural, manufacturing, and/or service sectors.

Conversely, another strand maintains that owing to stringent conditions for financial access, inter alia, information asymmetry, transaction costs, and collateral requirements, financial access could be limited and hence financial institutions are characterized with concerns of surplus liquidity (Asongu and Odhiambo 2018a, 2018b). In this strand of scholarship, the benefits of financial access are fundamentally skewed in favor of wealthier and well-connected fractions of households and corporations (Asongu, Nwachukwu and Tchamyou 2016). The result of restricted financial access is that households and businesses recourse to remittances and the informal financial sector for financing purposes (Beck, Demirgüç-Kunt and Levine 2007). The engaged two strands are reconciled by a third strand which maintains that the relationship between financial access and economic development can be non-linear such that the nexus can be either positive or negative depending on the amount of finance or stage in the industrialization process (Asongu and Tchamyou 2014; Greenwood and Jovanovic 1990). This non-monotonic element is considered in this research because interactive regressions are involved in the empirical approach used to assess the relevance of enhancing financial access on value added in the three economic sectors.

The stances for and against, and the contingent relevance of financial access in improving economic and corporate development, can be further expatiated by the intensive and extensive margin theories in the light of contemporary financial access and economic development literature (Tchamyou et al. 2019). On the one hand, the intensive margin theory suggests that financial development influences economic development via both indirect and direct channels to benefit clients and corporations that are already in possession of formal bank accounts (Chipote, Mgxekwa and Godza 2014). On the other hand, the extensive margin theory posits that financial access can also be beneficial to corporations and households in the margins of business and society (Bae, Han and Sohn 2012; Batabyal and Chowdhury 2015; Black and Lynch 1996; Evans and Jovanovic 1989; Holtz-Eakin, David and Rosen 1994; Odhiambo 2014; Orji, Aguegboh and Anthony-Orji 2015; Chiwira et al. 2016). In other words, from the perspective of the extensive margin theory, financial access could also benefit the fraction of corporations and households previously excluded from formal financial services.

The positioning of this study is consistent with both the intensive and extensive margin theories in the perspective that enhancing financial access can benefit both existing users of financial services and previously excluded users from the underlying financial services. Accordingly, the estimation approach in this study is tailored such that financial access is enhanced in the regression exercise within the framework of interactive regressions. The consistency between this study's positioning and attendant theories is put in more perspective in the following passages.

First, the research aligns with the intensive margin theory in which financial development influences economic development both directly and indirectly. Financial access affects value added across economic sectors because corporations in these sectors depend on formal financial establishments for credit for their business operations. Within an indirect perspective, financial access also affects the underlying economic sectors because interactive regressions are involved and, by extension, there are inflection points that distinguish the positive and negative effects of financial access on value added in the various economic sectors.

Second, the extensive margin theory accords with the positioning of the study in the view that enhancing financial access is a policy measure that is often designed to increase both the depth and width of financial access such that both existing and previously excluded users are susceptible to benefit from the enhancement of financial access. In essence, as argued by Tchamyou et al. (2019), the extensive margin theory is relevant when interactive regressions are taken on board.

Data and Methodology

Data

The research focuses on 25 nations in SSA using data for the period 1980–2014. Constraints in the availability of data at the time of the study motivate the adopted geographical and temporal scopes. The dataset is restructured to be consistent with the empirical strategy to be adopted for the research: the Generalized Method of Moments (GMM). Accordingly, the underlying estimation technique requires that the number of agents (i.e., cross-sections) be more than the number of periods each agent is characterized by (i.e., the number of years in each cross-section). Hence, in order to meet the N > T criterion for the employment of the empirical strategy (Tchamyou, Asongu and Nwachukwu 2018), the restructuring produces two sub-datasets: (i) seven five-year and (ii) five seven-year averages. From an exploratory exercise, it is apparent that only the seven five-year datasets can produce estimated models that are void of concerns pertaining to instrument proliferation even when the option of collapsing instruments is taken on board in the regression exercise. It follows that the retained data averages in terms of non-overlapping intervals are: 1980–1986; 1987–1993; 1994–2000; 2001–2007 and 2008–2014.

Consistent with the motivation of the research, three outcome indicators are used: value added in the agricultural sector, value added in the manufacturing sector, and value added in the service sector. The selection of these indicators, which are sourced from the World Development Indicators of the World Bank and the United Nations Conference on Trade and Development databases are in accordance with contemporary literature on value added across economic sectors (Meniago and Asongu 2019). The credit channel is used for financial access in accordance with contemporary financial development literature (Tchamyou 2019, 2020). This indicator is from the Financial Development and Structure Database of the World Bank. The average value of financial access in the sampled countries is about 21 percent (i.e., domestic credit to private sector as a percentage of GDP).

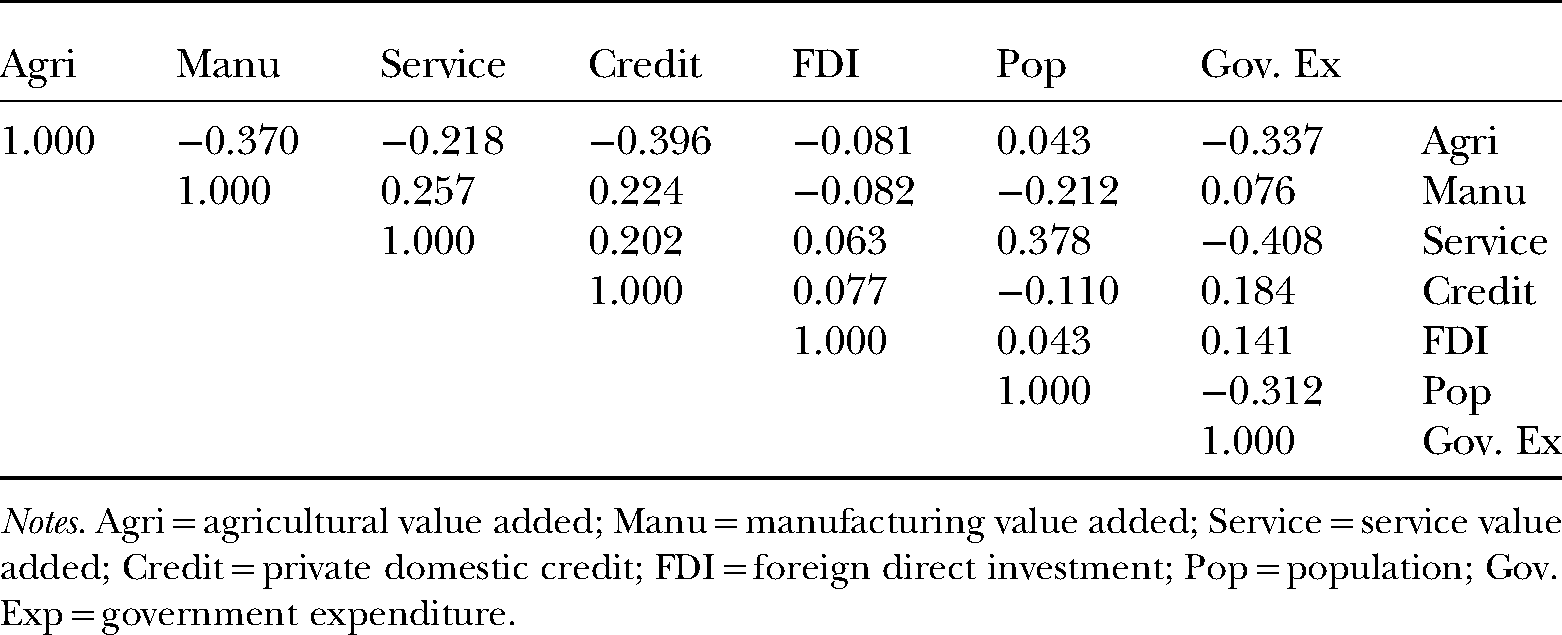

To control for the omission-of-variable bias, three variables are adopted in the conditioning information set, namely: foreign direct investment (FDI), population, and government expenditure. The choice of these variables from the World Development Indicators of the World Bank is in accordance with contemporary productivity and economic development studies; notably, Becker, Laeser and Murphy (1999), Barro (2003), Heady and Hodge (2009), Sahoo, Ranjan and Nataraj (2010), Ssozi and Asongu (2016a, 2016b), Elu and Price (2010, 2017), Dunne and Masiyandima (2017), Tchamyou (2017), and Efobi, Tanankem and Asongu (2018). All the three adopted variables are expected to positively affect the outcome variables. However, if the government expenditure is not tailored to promote economic activity in the various economic sectors, an opposite incidence may be apparent, especially when such expenditure is more skewed for consumption than production processes on the one hand, and on the other, characterized by activities of corrupt officials. Moreover, while population has been documented to promote investment and productivity, the expected impact may be significant if the majority of the population is employed (Asongu 2013). It follows that the anticipated effect of population may also be insignificant because most of the population is unemployed and, by extension, fewer people are productively involved in the corresponding economic sectors. Appendices A, B, and C disclose the definitions and sources of variables, the summary statistics, and the correlation matrix, respectively.

Methodology

Specification

In light of the narrative in the data section and following the motivations in contemporary GMM-centric literature (Akinyemi et al. 2019; Tchamyou 2020), a two-step GMM estimation strategy based on forward orthogonal deviations is adopted for the purpose of this study. The motivations for choosing this empirical approach is also consistent with the data structure because: (i) the number of cross-sections is higher than the corresponding number of periods in each cross-section; (ii) the outcome variables are persistent because their levels and first lags correlate to a height of above 0.800 which is the established metric for assessing persistence in a variable (Tchamyou 2019); (iii) there is an account for the simultaneity dimension of endogeneity with the use of internal instruments and some control for the unobserved heterogeneity when time-invariant omitted variables are taken on board; and (iv) the choice of the GMM approach, as opposed to a Two-Stage Least Squares instrumental variable approach, is because of the absence of appropriate external instruments for the study.

The levels and first difference equations below in (1) and (2), respectively, show the standard GMM equations used to assess the relevance of enhancing ICT for value added in economic sectors.

The version of the GMM empirical approach adopted in this research is the forward orthogonal deviations version that is informed by contemporary literature which has documented this version to produce more efficient estimates, relative to more traditional system and difference GMM versions (Asongu and Odhiambo 2019a, 2019b; Boateng et al. 2018; Tchamyou et al. 2019). The version pertaining to forward orthogonal variations is an improvement of the Arellano and Bover (1995) by Roodman (2009).

Identification, Simultaneity, and Exclusion Restrictions

Articulating the robustness of the GMM empirical strategy requires that some elements in the estimation approach are emphasized: identification, simultaneity, and exclusion restrictions. Regarding the first on this list, the approach to identification consists of clarifying three sets of variables: the outcomes, endogenous explaining, and strictly exogenous variables. The outcome variables in this study are value added across sectors in the light of the motivation of the study and narratives in the data section. The endogenous explaining variables are ICT and control variables, while the strictly exogenous variables are identified as years because, as documented by Roodman (2009), years are appropriate strictly exogenous variables because they cannot be endogenous after a first difference. This process of identification is in line with contemporary GMM-oriented literature (Meniago and Asongu 2018; Tchamyou and Asongu 2017). Drawing on this identification strategy, the assumption of exclusion restrictions is assessed by establishing that the identified variables that are strictly exogenous influence the adopted outcome variables exclusively through the identified predetermined variables.

Second, in relation to the issue of simultaneity or reverse causality, forward differenced instrumental indicators are used, and the process entails the use of Helmet transformations to purge fixed impacts which are likely to bias the models estimated given the fact that the correlation between these fixed effects and lagged dependent variables is a source of endogeneity. Arellano and Bover (1995), Love and Zicchino (2006), and Roodman (2009) support this procedure for eliminating fixed impacts because these transformations enable parallel or orthogonal conditions between observations that are forward-differenced and lagged.

Third, the discussed assumption on exclusion restrictions outlined in the first strand can be assessed with the Difference in Hansen Test (DHT) for the exogeneity of instruments. Accordingly, the null hypothesis related to this test is the stance that the value-added dependent variables are affected by the strictly exogenous variables exclusively via the identified predetermined variables (i.e., ICT and control variables). Therefore, the findings provided in the following section should be understood in light of the fact that the assumption of exclusion restrictions disclosed in the first strand is valid when the null hypothesis related to the DHT is not rejected. The criterion for validating exclusion restrictions is consistent with less contemporary instrumental variable approaches in which a rejection of the Sargan/Hansen test is indicative of the fact that the identified strictly exogenous variables influence the outcome variables beyond the proposed mechanisms (Amavilah, Asongu and Andrés 2017; Beck, Demirgüç-Kunt and Levine 2003).

Empirical Results

Presentation of Results

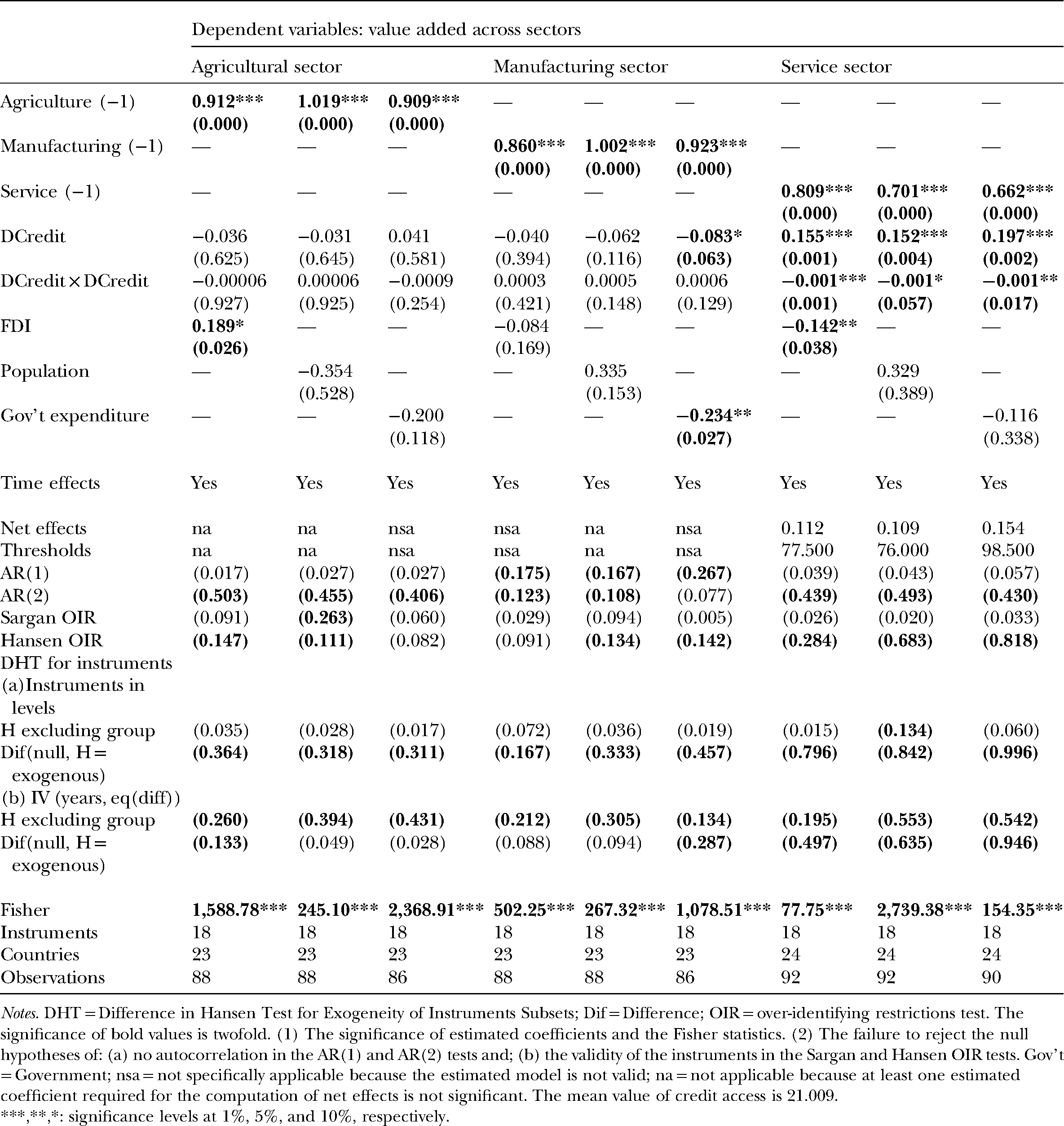

This section discloses the empirical findings that are provided in Table 1. The table is divided into three main sections pertaining to the agricultural sector, the manufacturing sector, and the service sector. The specifications in each section are three in number, with each using an element of the conditioning information set. All three control variables are not used in one specification owing to concerns about instrument proliferation that arise from the inclusion of more control variables or more time-series properties. Note should be taken of the fact that such restrictions of elements in the conditioning information set in order to limit concerns related to instrument proliferation are consistent with mainstream GMM-oriented literature. Examples of GMM studies in which control variables are absent in order to provide robust estimations are: Osabuohien and Efobi (2013) and Asongu and Nwachukwu (2017).

Enhancing Credit and Value Added Across Economic Sectors.

Notes. DHT = Difference in Hansen Test for Exogeneity of Instruments Subsets; Dif = Difference; OIR = over-identifying restrictions test. The significance of bold values is twofold. (1) The significance of estimated coefficients and the Fisher statistics. (2) The failure to reject the null hypotheses of: (a) no autocorrelation in the AR(1) and AR(2) tests and; (b) the validity of the instruments in the Sargan and Hansen OIR tests. Gov't = Government; nsa = not specifically applicable because the estimated model is not valid; na = not applicable because at least one estimated coefficient required for the computation of net effects is not significant. The mean value of credit access is 21.009.

***,**,*: significance levels at 1%, 5%, and 10%, respectively.

To assess the validity of estimated models, four information criteria are taken on board in the light of the attendant GMM-centric literature. Given these criteria, some estimated models in Columns 4, 5, and 7 are not valid because the null hypotheses of the Hansen test and second-order Arellano and Bond autocorrelation test in difference are rejected.

To examine the importance of enhancing financial access on value added across economic sectors, net effects are computed in accordance with contemporary interactive regressions literature (Asongu and Odhiambo 2020b, 2020c; Agoba et al. 2019). The computation of the net effects entails the unconditional effects of financial access and the conditional or marginal effects associated with the interactive regressions. To put this computational insight into more perspective, in the penultimate paragraph of Table 1, the net effect of enhancing private domestic credit on value added in the service sector is 0.109 (2 × [−0.001 × 21.009] + [0.152]). In the corresponding computation, the mean value of private domestic credit is 21.009, the marginal impact of private domestic credit is −0.001, the corresponding unconditional impact of private domestic credit is 0.152, whereas the leading 2 is obtained from the quadratic derivation. In some specifications, net effects are not computed for two main reasons: (i) nsa or “not specifically applicable” denotes scenarios where the estimated model is not valid in the light of the disclosed information criteria for the validity of models while (ii) na or “not applicable” reflects a modelling in which at least one estimated coefficient required for the computation of net effects is not significant.

The following findings can be established from Table 1. Enhancing financial access does not significantly improve value added in the agricultural and manufacturing sectors, while enhancing financial access improves value added in the service sector.

Extended Analysis with Thresholds for Complementary Policies

In spite of the positive net effects, the fact that the marginal effects are negative should also be taken on board in the interpretation of results. In essence, the negative marginal effects imply that, at certain thresholds of the independent variable of interest, the net effect changes from positive to negative. It follows that beyond the attendant thresholds, complementary policies are required to maintain the positive effect of access to credit on value added to the service sector.

To put the above point into perspective, let us consider the last column of Table 1, in which the net effect on enhancing credit access is 0.154 (2 × [−0.001 × 21.009] + [0.197]). The corresponding threshold at which the net effect becomes zero (i.e., 0) is 98.500[0.197/(2 × −0.001)]. It follows that when domestic credit is 98.500 percent of GDP, complementary policies should be taken on board in order to maintain the positive unconditional effect of credit access on value added to service sector. Accordingly, when credit access is 98.500 percent of GDP, the net effect of enhancing credit access becomes 0.000 (2 × [−0.001 × 98.500] + [0.197]). Hence, enhancing credit access beyond the established threshold engenders a net negative effect on value added to the service sector.

For the established thresholds to be policy-relevant and make economic sense, the thresholds should be within the statistical limits disclosed in the summary statistics. Accordingly, the three computed thresholds pertaining to the value added to the service sector are policy—worthwhile because they are situated between 2.238 and 144.397, which correspond, respectively, to the minimum and maximum limits of the credit access disclosed in the summary statistics.

A possible reason for complementary policies when credit access exceeds 98.500 percent of GDP is that negative externalities associated with excess credit, such as inflation and moral hazard, can undermine the economic outlook and, by extension, the value added to the service sector. Hence, complementary policies at the established thresholds may include measures designed to fight inflation and moral hazard associated with credit lending.

Conclusion, Policy Implications, and Future Research Directions

This research assesses the importance of financial access on value added in three economic sectors in 25 countries in SSA using data for the period 1980–2014. The empirical evidence is based on the GMM. Financial access is measured with private domestic credit, while the three outcome variables are: value added in the agricultural, manufacturing, and service sectors. Enhancing financial access does not significantly improve value added in the agricultural and manufacturing sectors, while enhancing financial access improves value added in the service sector. Policy implications are discussed in what follows with particular emphasis on the two fundamental concerns pertaining to the findings: notably, (i) why enhancing financial access does not improve added values in the agricultural and manufacturing sectors and what can be done, and (ii) how the role of financial access in the service sector can be improved. These are expanded in chronological order.

First, information asymmetry can explain why the agricultural and manufacturing sectors are not benefiting from enhanced financial access. The substantially documented concerns of surplus liquidity in African financial institutions partly elucidate this concern (Saxegaard 2006). Information asymmetry may be more pronounced in the manufacturing and agricultural sectors because of concerns such as adverse selection on the part of banks and moral hazard from borrowers in the agricultural and manufacturing sectors. Hence, policy makers should improve tools that can contribute toward limiting information asymmetry between financial institutions and operators in the agricultural and manufacturing sectors of the economy. The consolidation of public credit registries and private credit bureaus is a step toward reducing the attendant information asymmetry in order to boost access to finance by operators in the concerned economic sectors. The explanation should be balanced with the perspective that financial access may not interact in isolation to influence value added across the agricultural and manufacturing sectors. Hence, within a framework where the relationship between financial access and value addition is straightforward, other channels may be relevant in explaining value addition in the underlying sectors. For instance, human capital, infrastructure, and information technology can be relevant moderating factors. These are obviously areas for future research. Second, the effect of financial access may be more relevant in promoting the service sector of the economy because most service corporations are more apparent in urban areas where financial institutions largely operate in SSA. Moreover, in the light of the explanation in the previous paragraph, it is reasonable to infer that corporations in the service sector are, on average, ceteris paribus, less characterized by concerns pertaining to information asymmetry between banking institutions and economic operators in the attendant tertiary sector. An extended analysis has shown that, for the positive net incidence of enhancing credit access on value added to the service sector to be maintained, complementary policies are required when domestic credit to the private sector is between 77.50 percent and 98.50 percent of GDP. Such complementary policies can focus on, among others, fighting inflation and moral hazard associated with credit lending. Future studies can extend the established findings by assessing how instruments that reduce information asymmetry can be used to complement financial access to influence value added in the agricultural and industrial sectors. Such instruments that have been documented to complement financial access to reduce information asymmetry include, inter alia: ICT and information sharing offices (Kusi et al. 2017; Asongu et al. 2018; Kusi and Opoku-Mensah 2018).

Footnotes

Correlation Matrix (Uniform Sample Size: 124).

| Agri | Manu | Service | Credit | FDI | Pop | Gov. Ex | |

|---|---|---|---|---|---|---|---|

| 1.000 | −0.370 | −0.218 | −0.396 | −0.081 | 0.043 | −0.337 | Agri |

| 1.000 | 0.257 | 0.224 | −0.082 | −0.212 | 0.076 | Manu | |

| 1.000 | 0.202 | 0.063 | 0.378 | −0.408 | Service | ||

| 1.000 | 0.077 | −0.110 | 0.184 | Credit | |||

| 1.000 | 0.043 | 0.141 | FDI | ||||

| 1.000 | −0.312 | Pop | |||||

| 1.000 | Gov. Ex |

Notes. Agri = agricultural value added; Manu = manufacturing value added; Service = service value added; Credit = private domestic credit; FDI = foreign direct investment; Pop = population; Gov. Exp = government expenditure.