Abstract

Longitudinal links between childhood family income and adult outcomes are well documented. However, research on childhood income volatility and young adult outcomes is limited. This study utilizes data from the NLSY (N = 6,410) to examine how childhood family income and income volatility relate to socioeconomic outcomes and mental/behavioral health in emerging adulthood. Results show that lower childhood income was associated with young adult socioeconomic and behavioral health outcomes. Higher income volatility was associated with increased depression and teen parenthood during young adulthood. Additional analyses examining trajectories of income volatility illustrated that children in families with unstable income trajectories (i.e., frequent income losses and gains) showed higher depression scores than those with stable trajectories. These findings suggest that income volatility, not just income level or income loss, is important to consider when studying economic disparities in young adult outcomes. Implications for policies and programs for low-income, high-volatility households are discussed.

Keywords

During the past 50 years, the economic circumstances of families in the U.S. have diverged sharply, with rising levels of income inequality and volatility. Currently, almost half of the U.S. population qualifies as low-income (Institute for Policy Studies, 2018), and approximately one child in every five lives in poverty (Chaudry & Wimer, 2016). At the same time, family income has become increasingly unstable (Hardy & Ziliak, 2014; Ziliak et al., 2011), especially in families with children (Hill, 2018). According to a recent survey, 34% of adults experienced a sizeable change in income (at least 25%) from 1 year to the next (United States, Pew Charitable Trusts, 2017). Higher income volatility, which is particularly problematic among low-wage workers, represents an additional source of household economic risk and hardship (Gottschalk & Moffitt, 2009). COVID-19 and other economic crises are exacerbating these trends, which has implications for children and youth because economic disadvantage and instability undermine important family processes that undergird positive development.

Much research has documented associations between low levels of income and worse outcomes in various aspects of child development, including educational achievement and attainment and behavioral and mental health (Brooks-Gunn & Duncan, 1997; Davis-Kean, 2005; Huston et al., 1994; Magnuson et al., 2009). More recent work has focused on how income volatility may undermine children’s healthy development above and beyond family income level. Income volatility may limit families’ ability to consistently invest in resources that promote children’s long-term development. Income losses also exacerbate family stress, as families struggle to make ends meet in response to income loss (Hill et al., 2013). This gives rise to more chaos and disorganized family processes, which trigger maladaptive stress responses in children and threaten the provision of consistent and nurturing caregiving that promotes academic and behavioral development (Blair & Raver, 2016; Chaudry & Wimer, 2016; Evans & Kim, 2013). Moreover, while families with stable income, even stably low income, may have consistent access to resources such as health insurance, government supports, and childcare, families with unstable income may fluctuate in their eligibility for such programs (Hill et al., 2013). This further hinders income-volatile families from making consistent investments and increases family stress and financial hardship. Indeed, recent studies have linked high income volatility with increased behavioral problems and lower achievement scores even after holding income level constant (Miller et al., 2020; Wolf et al., 2014). Thus, income level and income volatility (together, what we call “income dynamics”) may have distinct associations with youth development.

Importantly, while evidence suggests that economic disadvantage in youth development translates into lower functioning in adulthood, the literature on long-term effects of income dynamic is sparse (Hardy, 2014). In particular, studies have documented longitudinal links between childhood levels of income and adult socioeconomic outcomes and behavioral health (e.g., Chaudry & Wimer, 2016; Duncan et al., 2013), but long-term associations between income volatility and adult outcomes have not been as well studied. Research finding that income volatility during childhood predicts lower educational attainment (Hardy, 2014) and poorer psychiatric outcomes (Cheng et al., 2020) in early adulthood, as well as similar findings for income volatility during adolescence in particular (Hardy & Marcotte, 2020), provide exceptions. This evidence supports a growing consensus that longitudinal relations between childhood income volatility and young adult socioeconomic and behavioral health outcomes warrant more scholarly attention. However, the longitudinal studies on income volatility have been limited in the span of developmental periods studied (e.g., Hardy, 2014; Hardy & Marcotte, 2020). For example, Hardy and Marcotte (2020) studied links between childhood family income volatility only in adolescence (8–18 years) and young adult educational outcomes from 18 to 24 years. Therefore, this study could not shed light on the implications of family income volatility across the entirety of childhood, nor examine whether associations exist beyond age 24.

The present study extends previous work that focused on shorter developmental spans by examining family income dynamics (i.e., annual income and income volatility) across childhood in entirety (prenatal through 18 years) and young adult outcomes at later ages (24–33 years). It also contributes to the budding knowledge of the longitudinal implications of income volatility by examining not only educational outcomes, but also, employment and mental/behavioral health outcomes. Using five birth cohorts followed prenatally through early adulthood drawn from the National Longitudinal Survey of Youth (NLSY), this study examines whether annual family income and income volatility across childhood are linked to rates of depression and risk-taking behavior, teen parenthood, educational attainment, wages, and labor-force participation during young adulthood. The present study includes a wider array of income volatility measures than has been utilized in previous studies, including measures that capture global experiences of economic uncertainty (e.g., magnitude of individual variance), the accumulation of severe income shocks (e.g., frequency of 25% or greater income changes), and trends and directionality in income volatility over time (e.g, stable, upward, downward, and unstable trajectories). As childhood poverty, unemployment, and income instability approach historic highs, research regarding relations between family income dynamics and adult outcomes is important for addressing the intergenerational transmission of poverty and informing prevention and intervention efforts aimed at enhancing child and family well-being.

Theoretical Framework

We use parental investment perspectives and family stress models to conceptualize how family income dynamics jointly shape socioeconomic and behavioral and mental health outcomes in young adulthood. According to investment perspectives, family income dictates how much time, money, and other important resources that parents are able to invest in their children’s enrichment (Attanasio & Weber, 2010; Becker, 1991; Magnuson et al., 2009). Additionally, income volatility, particularly income losses or periods of alternating losses and gains, may cause parents to reduce current and future investments in their children due to the economic uncertainty (Attanasio & Weber, 2010). Thus, higher income and income stability may facilitate consistent investments in materials and experiences that promote healthy child development (Becker, 1991; Hardy, 2014; Votruba-Drzal, 2003) and adaptive behavioral functioning (Yeung et al., 2002). These include cognitively-stimulating materials, extracurricular activities, high quality child care/schooling, healthcare, mental health services, and safe neighborhoods (Becker, 1991; Chaudry & Wimer, 2016; Magnuson et al., 2009). Furthermore, consistent parental investment during childhood and adolescence is important beyond childhood because the growth and development that takes place during these times lay the foundation for wellbeing and skills acquisition in young adulthood (i.e., future returns on investments) (Attanasio, 2015; Hardy, 2014). Cognitive skills and intellectual abilities translate to socioeconomic advantages such as educational attainment and labor-force earnings (Hardy, 2014). Also, childhood behavioral skills (e.g., delayed gratification, emotion regulation, self-regulation, and organization) buttress human capital formation, mental and behavioral health, and educational achievement later on in life (Attanasio, 2015). Moreover, parental investment through adolescence and beyond matters not only for skill acquisition but also opportunities for higher education. Specifically, family income dynamics, along with the capacity for parental investment, have become a larger determinant of both college attendance and quality due to increased college tuition in recent decades (Belley & Lochner, 2007).

The family stress model is another key perspective for conceptualizing how family income dynamics during childhood may influence young adult adjustment. Low family income or income volatility increases parental stress, which compromises parental mental health (e.g., increases maternal depression) and family relationships (e.g., reduces parent-child warmth and increases negativity) (Chaudry & Wimer, 2016). This may lead to less responsive parenting and harsher discipline, which undermines parental support of children’s emotional and instrumental needs (Evans & Kim, 2013). In turn, less supportive parenting threatens children’s cognitive, emotional, and behavioral adjustment (Farah et al., 2008; Neppl et al., 2016; Yeung et al., 2002). Moreover, the stress caused by economic uncertainty (i.e., high volatility in both directions) has negative links to children’s self-regulatory and attentional abilities (Blair & Raver, 2016; Evans et al., 2005; Palacios-Barrios & Hanson, 2019), both of which undergird positive academic and behavioral development (Wadsworth et al., 2016). Importantly, family socioeconomic stress has long-term implications for children’s behavioral health that can yield intergenerational consequences for offspring such as early child-bearing, lower maternal education, and increased risk for harsh parenting (Mayer, 1997; Raymo et al., 2015; Scaramella et al., 2008). Taken together, the investment and family stress perspectives tap into key mechanisms underlying the long-term influence of family income dynamics on human capital formation, socioeconomic outcomes, and mental and behavioral health.

Childhood Permanent Income and Young Adult Outcomes

Prior studies have documented associations between average income level across childhood and adolescence and several measures of socioeconomic outcomes in adulthood. For instance, one such study of a birth cohort of more than 1,200 children born in 1977 in a region of New Zealand incorporated a measure of cumulative family income from birth to 14 years to find that increased family income was associated with lower rates of economic inactivity (i.e., time spent unenrolled in school and unemployed) and more post-secondary education (Maloney, 2004). Additionally, in a study using nationally-representative, intergenerational data from the Panel Study of Income Dynamics (PSID) that attempted to address omitted variable bias by controlling for an extensive and powerful set of child and family covariates, Duncan et al. (2010) found that higher average childhood family income (i.e., prenatal-15 years) was associated with increased adult earnings and work hours. Furthermore, a recent economic review also using PSID data found that children who were raised in poverty were twice as likely to drop out of high school than those who were not (Chaudry & Wimer, 2016). These children also had lower annual earnings by age 30. While this study focused on poverty status rather than income level, these findings enrich the discussion of the longitudinal links between childhood family income and adult outcomes. Importantly, studies linking childhood income with adult educational and employment outcomes have been largely correlational and vary to the extent that they address threats to internal validity, however all show small to modest relations between income and attainment/employment. Additionally, effects of family income on achievement, high school graduation, and years of schooling in youth have been established by experimental and quasi-experimental research (Duncan et al., 2017), which may suggest that the associations between family income and adult attainment/employment are, at least in part, causal.

While empirical support for long-term family income effects seems to be strongest for educational and employment outcomes, there are a limited number of rigorous studies that have established causal links between income and behavioral functioning in childhood (e.g., Akee et al., 2010; Dearing et al., 2006). There is also correlational evidence that the effects of family income extend to include behavioral health (e.g., internalizing, externalizing, and early parenthood behaviors) (Duncan et al., 1998; Mayer, 1997). For instance, though it did not follow children through young adulthood, a recent study using nationally representative data on over 7,000 children showed that higher family income experienced in childhood (i.e., prenatal—age 14) was linked with more adaptive internalizing and externalizing behavioral trajectories through adolescence (Miller et al., 2020). Additionally, increased family income has been linked to reductions in the likelihood of nonmarital birth (Duncan et al., 2010) and lower rates of childbirth by age 21 and criminal activity (i.e., arrest or conviction) (Maloney, 2004). Another similar study that focused on poverty status found that those who experienced persistent family poverty during childhood were seven times more likely to become a teen mother (Chaudry & Wimer, 2016). It must be noted that the negative outcomes associated with teen parenthood are not due to chronological age per se, and risks associated with early childbearing vary according to race/ethnicity, availability of pre- and post-natal maternal support, and child-rearing practices and resources (Cross, 2020; Kramer & Lancaster, 2010). However, teen parenthood has been shown to be an indicator of low economic trajectory or the continuation of disadvantage, particularly in the U.S. (Kearney & Levine, 2012). Thus, we include teen parenthood along with internalizing and externalizing behaviors because it provides insight into the intergenerational perpetuation of family income dynamics, rather than as a social risk factor in and of itself.

Income Volatility and Young Adult Outcomes

Research examining longitudinal links between family income volatility experienced in childhood and adult outcomes is extremely limited. Among the earliest to focus on this topic, Hardy (2014) analyzed the PSID and found that family volatility in childhood, as measured using the coefficient of variation and an indicator for whether families experienced 25% or higher percent change in income, was associated with slightly lower educational attainment in adulthood, particularly related to high school dropout rate, especially for children growing up in lower income families. A growing literature, however, has examined associations between family income volatility and childhood/adolescent achievement outcomes both concurrently and longitudinally (Gennetian et al., 2015, 2018; Miller & Votruba-Drzal, 2017). Several ways of operationalizing income volatility have emerged in the literature. These measures focus on magnitude (e.g., coefficient of variation), frequency (e.g., number of periods of income changes), or directionality (e.g., income gains versus losses) of income changes. These measures strengthen the understanding of family experiences of global economic uncertainty, capacity to withstand large income shocks, and trends in income volatility over time, respectively. It is important then to consider whether income volatility, measured in various ways, has enduring effects on educational attainment and employment that extend into young adulthood. For example, Gennetian et al. (2015, 2018) found that higher income instability (using five different measures of monthly income changes), especially repeated income losses, was negatively associated with grade-school attendance and engagement and positively associated with suspension and expulsion, which both have implications for academic achievement.

There have been virtually no studies of the long-term effects of family income volatility and adult behavioral and mental health outcomes. A recent study that found that income volatility during childhood predicted poor psychiatric outcomes in young adulthood provides a lone exception (Cheng et al., 2020). Prior theoretical and empirical research has suggested that income volatility affects children’s behavioral outcomes through parental stress, parenting practices, and parent-child relationships (Conger et al., 2010; Hill et al., 2013). Accordingly, cross-sectional and longitudinal studies that focus on income dynamics and behavioral/mental health outcomes in childhood and early adolescence document links between childhood economic instability and worse behavioral and mental health (Conger et al., 2002, 2010; Hardaway & Cornelius, 2014; McLoyd, 1990; Miller & Votruba-Drzal, 2017; Miller et al., 2020). Given what we know about the cumulative nature of children’s development over time, this evidence further suggests that family income volatility may have long-term implications for mental and behavioral health outcomes, in particular, that endure through young adulthood. To examine this, the present study jointly considers the role that childhood income level and volatility play in socioeconomic and mental and behavioral health outcomes in young adulthood.

Research Aims

In an effort to improve our knowledge of the role of family income dynamics in predicting socioeconomic and mental and behavioral health outcomes in young adulthood, this study draws data from young adults and their families in the National Longitudinal Study of Youth (NLSY79) and its Young Adult Survey supplement (NLSY-YA). The present study examines whether total family income and income volatility, measured various ways, from the year prior to birth through age 18 relate to mental and behavioral health outcomes (i.e., depression, teen parenthood, and risky behavior) in young adulthood and socioeconomic outcomes (i.e., educational attainment, full-time employment, and hourly wage) in young adulthood (24–33 years of age). In addition to cumulative family income, this study includes four measures of income volatility that reflect important dimensions of change in family income (e.g., magnitude, frequency, and directionality). This important effort tests the robustness of volatility findings and contributes to the limited understanding of which indices of volatility most strongly relate to important youth outcomes over time. More specifically, we use measures of individual variation in proportion to mean income level (i.e., coefficient of variation), within-individual variability, frequency of 25% percent changes experienced by families, and specific trajectories of volatility (stable, gains, losses, unstable), which advances the current literature tending to focus only on income losses (e.g., Hill et al., 2013).

We expect that higher levels of family income will yield better educational attainment, employment status, and mental and behavioral outcomes in young adulthood. We further hypothesize that income volatility will be particularly detrimental to mental and behavioral health outcomes, holding income constant, due to its keen relevance to the family stress model. Specifically, we predict that higher magnitudes of income volatility and increased frequency of periods of income volatility will relate to worse mental and behavioral health. With respect to directionality, we do not expect that an upwards trajectory of income gains will relate to adult functioning, but we predict that trajectories of loss will be linked to worse behavioral outcomes due to the increased stress families on these trajectories likely feel. We further predict that trajectories of high income instability (i.e., unstable trajectory of both positive and negative income shocks) will relate to decreased mental and behavioral health since economic uncertainty contributes to increased stress for both parents and children (Chaudry & Wimer, 2016; Palacios-Barrios & Hanson, 2019).

Method

Participants

Data were drawn from the NLSY and NLSY-YA. The Bureau of Labor Statistics initiated the NLSY in 1979 to gather longitudinal data on the labor market activities and other significant life events of young men and women in the U.S. The original sample consisted of a nationally representative group of 12,868 men and women between the ages of 14 to 22, with an oversample of poor and minority individuals. The NLSY gathered income, employment, educational, and other data on the sample annually until 1994 at which point data was collected biennially. In 1986, the NLSY introduced the child and young adult supplement, a separate survey of all children born to NLSY female respondents, to greatly expand the breadth of child-specific information collected. Starting in 1986, children of the NLSY79 mothers have been interviewed and assessed biennially to follow their cognitive, physical, and behavioral development. At age 15, children become part of the NLSY79 Young Adult cohort and were administered the Young Adult Survey—a lengthy self-report interview asking about education, training, employment, health, dating, fertility and parenting, marriage and cohabitation, household composition, and social-psychological factors like risk taking behaviors, substance abuse, delinquency, and depression. As of 2014, a total of 11,521 children have been identified as having been born to the original 6,283 NLSY female respondents. The NLSY-YA includes direct assessments and parent reports of child development, including data on children’s behavioral development.

The current study utilizes five birth cohorts of children captured by the study from early childhood up through at least 24 years of age (in 2014). The first cohort consists of children who born in 1981 to 1982. The remaining cohorts include children born in 1983 to 1984, 1985 to 1986, 1987 to 1988, and 1989 to 1990. Our primary analytic sample contains the 6,410 children within these cohorts, using their data only on a biennial basis to adjust for the aforementioned sampling changes (i.e., we only include data collected every 2 years from each child even for those who may have more annual datapoints). When looking at labor force participation and hourly wage rate, analyses were conducted on the subsample of these participants who were not enrolled in school (N = 3,682) to ensure that our estimates were only for those young adults that were working or available to work. Missing data per variable ranged from a low of 0% for many of the demographic variables, like gender, birth cohort, and race, to a high of about 30% of the data missing for some of the outcome variables. Missing data for income and income volatility variables ranged from 7% to 25%. Missing data were imputed using multiple imputation by chained equations implemented in Stata 16 to create 20 imputed datasets (Royston, 2005).

Measures

Young adult outcomes

Young adult outcomes were assessed via self-report in the Young Adult Survey. All outcomes were taken from the most recent year available, that is when the participant was the oldest (with the exception of teen birth, which we took from the first wave in which participants reported having a child). We controlled for age at the time of the outcome to adjust for the fact that participants in our sample were of varying ages, ranging from 24 to 33 years old.

Mental and behavioral health

Three measures of mental and behavioral health were assessed. First, depression was assessed using a modified version of the Center for Epidemiological Studies Depression Scale (CES-D; Radloff, 1977; Ross & Mirowsky, 1989). A 7-item version of the CES-D was included in the Young Adult Survey every round (α = .72). Respondents were asked to indicate how often they felt particular ways in the past week on a four-point scale (0 = rarely or none of the time/1 day to 3 = most or all of the time/5 to 7 days). Items included how often respondents did not feel like eating, felt depressed, had restless sleeps, had trouble concentrating, etc. Next, the NLSY-YA assessed risk taking behaviors at each wave at using a six item self-report questionnaire (α = .63). Respondents answered these items, which included questions tapping the extent to which the respondent enjoyed taking risks, acted without thinking, believed life without danger was dull, using a four-point scale (1 = strongly disagree to 4 = strongly agree). Higher scores on the risk-taking measure indicate greater propensity to engage in risky behaviors. Lastly, we created an indicator for whether the respondent had a child during his/her teenage years of younger using questions asked by the NLSY-YA about the age at which respondents had their first child. For both male and female respondents, we coded them as being a teen parent (“1” on the indicator) if their reported age of having their first child was 17 or younger. Respondents whose first child was born when they were 18 or older or respondents who had not yet had a child were coded as “0” on this variable.

Socioeconomic outcomes

At every wave, respondents reported on aspects of educational attainment and employment. Highest level of education was assessed using a three-level scale that reflected whether the respondent’s highest degree obtained was less than a high school degree or GED, high school degree or GED, or bachelor’s degree or higher. To measure labor force participation, we created a dichotomous indicator reflecting whether the respondent was employed full time, which we defined as working 30 or more hours a week. Lastly, respondents were also asked to report their hourly wage rate (i.e., the amount of dollars per hour they earned in their current job). For respondents that did not report an hourly rate but reported a yearly salary, we calculated their hourly rate by dividing yearly salary by the number of work hours in a year (2,000 hours assuming they work 40 hours a week and 50 weeks a year). The wages of individuals in the labor market tend to increase from late adolescence to adulthood (Lee et al., 2014; Luong & Hébert, 2009), thus the hourly rate was age-normalized. For this, the participant’s income was divided by the average income at the participant’s age group or birth cohort. Thus, this variable can be understood as an age-adjusted earnings ratio.

Childhood income dynamics

Each year (or every other year after 1994), the NLSY79 asked parents to report on household income received in the prior calendar year from a variety of sources, including wages, salaries, interest, dividends, alimony, business earnings, government transfer programs, and income from other household members. On the basis of these answers, the NLSY creates a total net family income variable. The natural log of the income variable was calculated to account for evidence that income changes matter more for families with low income (Votruba-Drzal, 2003). Additionally, we added a value of $1 to family income (e.g., family income of 0 amounts to $1) and scaled to $10,000 increments (Dynan et al., 2012; Hardy, 2014). Since research has shown that cumulative income is a stronger predictor of children’s outcomes than is income in any period (Blau, 1999), we created income measures that averaged across income measures from the year prior to birth through age 18 for the sample. We created a cumulative income term only for households with at least two-thirds of waves of valid income data from the prenatal wave until age 18. In order to capture family income across childhood, available measures of net income were escalated to year 2013 dollars using formulas provided by the Bureau of Labor Statistics’ Consumer Price Index so that income measured across different years was comparable (Duncan et al., 2010). Escalation adjusts for monetary inflation over time.

Income volatility was measured using four indices that capture different dimensions of volatility. These different dimensions reflect magnitude, frequency, and direction of income change (Gennetian et al., 2015), and it is important to note the changes in metric across these measures of income volatility for accurate interpretation of the results. We used a 2-year panel because income was measured consistently in our sample every 2 years (e.g., Hardy & Ziliak, 2014).

In order to capture the variability and magnitude of income instability, we created two measures of within-person variability. First, within-person variance of annual income (“transitory variance”; Gottschalk et al., 1994) from the prenatal year though age 18 was calculated to reflect overall variability of income from year to year. Second, we created a coefficient of variation (Gennetian et al., 2015). It was calculated as the ratio of the household’s standard deviation of annual income to the household’s mean annual income. Thus, while these two volatility measures reflect family’s income variability, the second measure reflects a variance measure that is relative to the family’s average income.

Our third measure of income instability aimed to capture the frequency of large income shocks. For this, we calculated the total number of 2-year periods in which a participant’s household experienced an income gain or loss of at least 25% (“frequency of 25% volatility”). We chose the 25% cutoff based on prior research that examined income volatility (e.g., Hardy, 2014). This variable was created by subtracting previous income from income earned 2 years later. The change in income was divided by income at the earlier wave to represent the percent of income change. Finally, our fourth volatility measure reflects trends in the direction of income changes that participants experienced across childhood, given that the consequences of a series of income shocks could be substantially different for families if experiencing gains, losses, or changes in both directions. Thus, our fourth measure categorized participants in households experiencing one of four trajectories of income volatility (“volatility trajectories”): stable, gain, loss, and unstable trajectories. Participants were assigned to each category depending on their households’ pattern of 25% or larger income changes between ages 0 to 18. A household was assigned to the stable trajectory if it had one or no income changes, to the gain trajectory if it had two or more gains compared to losses, to the to the loss trajectory if it had two or more losses compared to gains, and to the unstable trajectory if it had roughly equal numbers of gains and losses (equal or plus or minus one).

Child and family covariates

Several child and family characteristics that may be correlated with family income and children’s behavior were included in the models to control for their associations with the outcomes. Child covariates included age at the time outcome was assessed, gender (female reference group), and cohort in which the child was born (cohort 3 reference group). For race/ethnicity, the NLSY measures child race using mothers’ race based on information gathered during the initial household screening. Race/ethnicity was categorized as either Hispanic, Black, or other, and we included dummies reflecting these categories (“other” reference group).

Family covariates included average number of children under the age of 18 living in the house, age of the mother at the birth of the focal child, percentage of waves mother was married, and percentage of waves mother was employed. Highest level of maternal education was coded as the highest grade that mothers had completed, ranging from 0 to 20 years, with 20 years representing 8 years of college or more. We also controlled for an additional trait of mothers that may relate to both family income and children’s behavior. Mothers’ percentile score on the Air Force Qualification Test (AFQT) was included as a covariate. The AFQT measures aptitude on a variety of intellectual tasks like arithmetic reasoning, word knowledge, paragraph comprehension, and numerical operations. Time-varying family characteristics were averaged over all available waves of data.

Data Analysis

To address our research aims, we estimated regression models consistent with the prior studies on childhood family income and adult functioning (Duncan et al., 2010; Ziol-Guest et al., 2009, 2012). We examined links between cumulative income dynamics and adult functioning using equation (1) shown below. In separate models, each adult outcome was predicted by annual family income and a measure of income volatility, as well as all covariates, as shown in equation (1) below.

In this equation, i denotes the participant, β1INC represents the cumulative measure of income for of child i between ages 0 to 18. β2VOL represents the cumulative measure of income volatility for child i between ages 0 to 18. β3TIMEVACOV indicates the cumulative measures of time variant covariances for child i, aggregated between ages 0 to 18. Finally, β4TIMEINVCOV represents the measures of time invariant covariances for child i.

All analyses were conducted in Stata 16 and weighted using custom weights created by the NLSY to adjust for clustering and oversampling (Center for Human Resources, 2001). Logistic regressions were used for outcomes that were dichotomous (teen parenthood and full-time work status), and multinomial logistic regressions were used for modeling educational attainment, which was operationalized as a set of three indicator variables. Since yearly family income can reflect additional sources of income (e.g., business investments, cash transfer payments, or child support) or broader economic factors, we performed sensitivity analysis by substituting annual income for a measure of labor earnings to determine whether links between labor-related outcomes (e.g., hourly rate and working full-time) related specifically to working wages/salary as expected. We also tested models with interaction terms (not shown here) to examine whether our income findings varied by birth cohort. In both cases, our results replicated.

Results

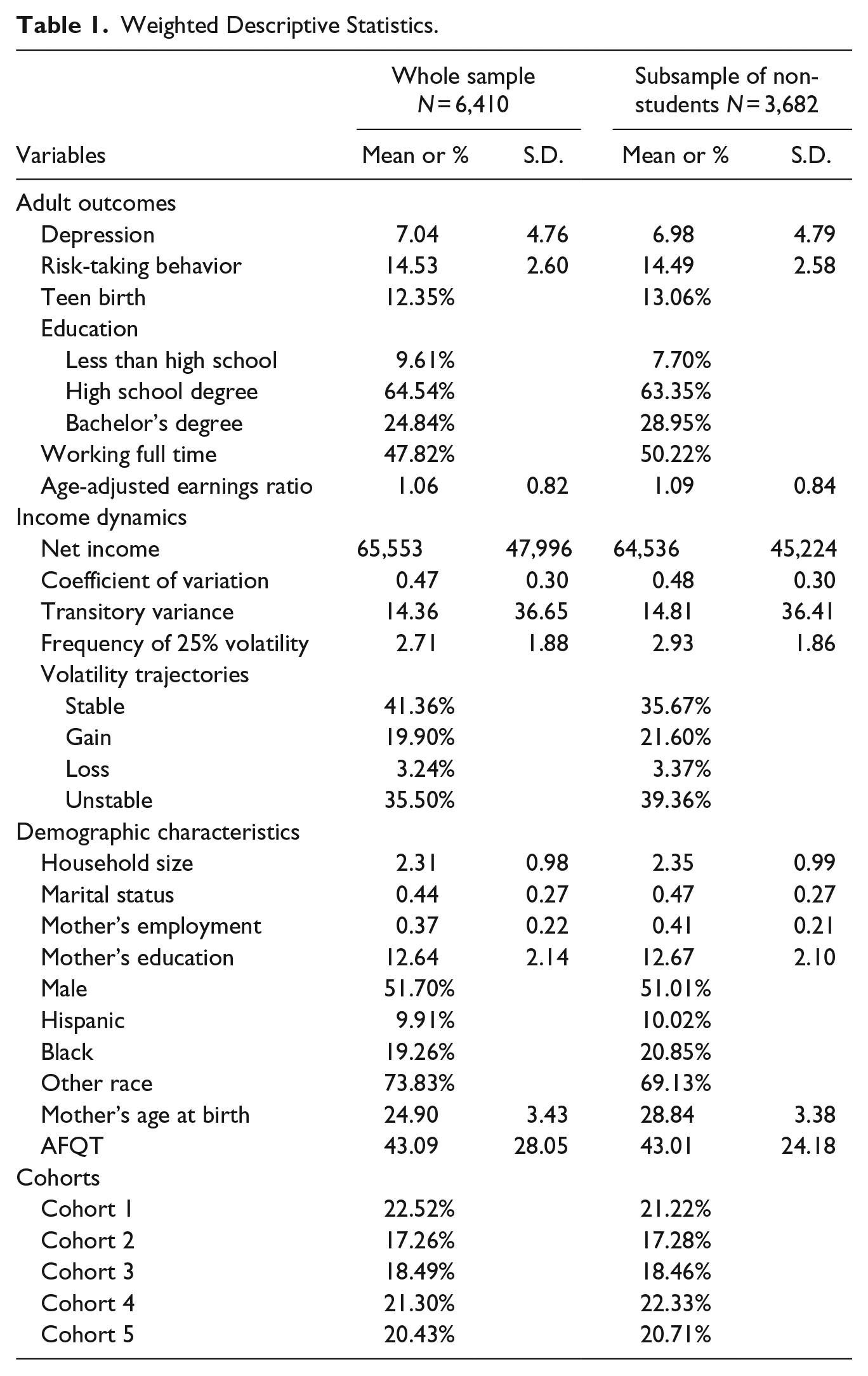

Table 1 presents weighted descriptive statistics for the full sample and the sub-sample analyzed in models predicting employment outcomes. Descriptive statistics show that participants were diverse in terms of race/ethnicity, parental marital status and employment, and family income dynamics. Regarding income, the families in the sample reported an annual average of around $65,000 net income and large variability (SD = $48,000), with income that ranged between $0 and over 500,000 dollars. Descriptive statistics of the sample also indicated that on average, participants experienced 2.71 (SD = 1.88) income shocks of at least 25% during childhood. In addition, when considering the trajectories of volatility, results indicated that while ~40% of participants experienced a stable income across childhood, the remainder ~60% experienced some volatility during those same years. Specifically, 20% of the sample experienced an upward income trajectory, 3% suffered a downward trajectory, and 36% of families were in a volatile trajectory in which they experienced both gains and losses.

Weighted Descriptive Statistics.

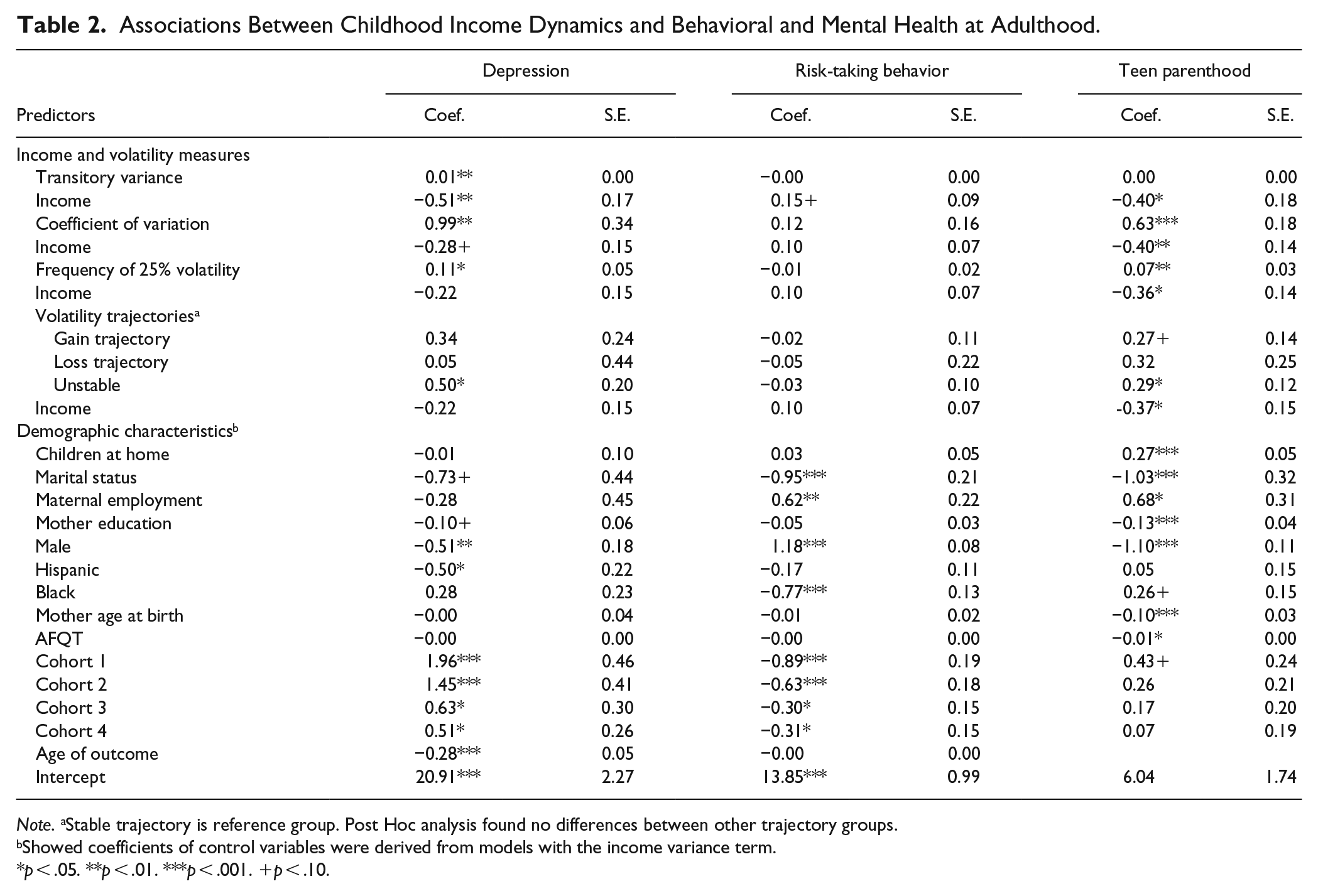

Regression results of associations between childhood income dynamics and adult outcomes are presented in Tables 2 (behavioral/mental health outcomes) and 3 (education and employment outcomes). Family income was measured in natural log units. An increase in a natural log unit corresponds to an approximately 2.71 factor increase. Thus, in a hypothetical family with earnings of $10,000, a log unit increase in yearly income would represent a change from $10,000 to approximately $27,100. The estimates of income-adult outcomes associations for dichotomous outcomes (i.e., teen parenthood, educational attainment, and full-time work) are presented in terms of relative risk ratios (RRR). RRR’s indicate whether the predictors put participants at higher or lower risk of becoming a teen parent or working full time. A significant RRR < 1 represents a decrease in the likelihood of endorsing the outcome, and a significant RRR > 1 represents an increased likelihood of endorsing the outcome.

Associations Between Childhood Income Dynamics and Behavioral and Mental Health at Adulthood.

Note. aStable trajectory is reference group. Post Hoc analysis found no differences between other trajectory groups.

Showed coefficients of control variables were derived from models with the income variance term.

p < .05. **p < .01. ***p < .001. +p < .10.

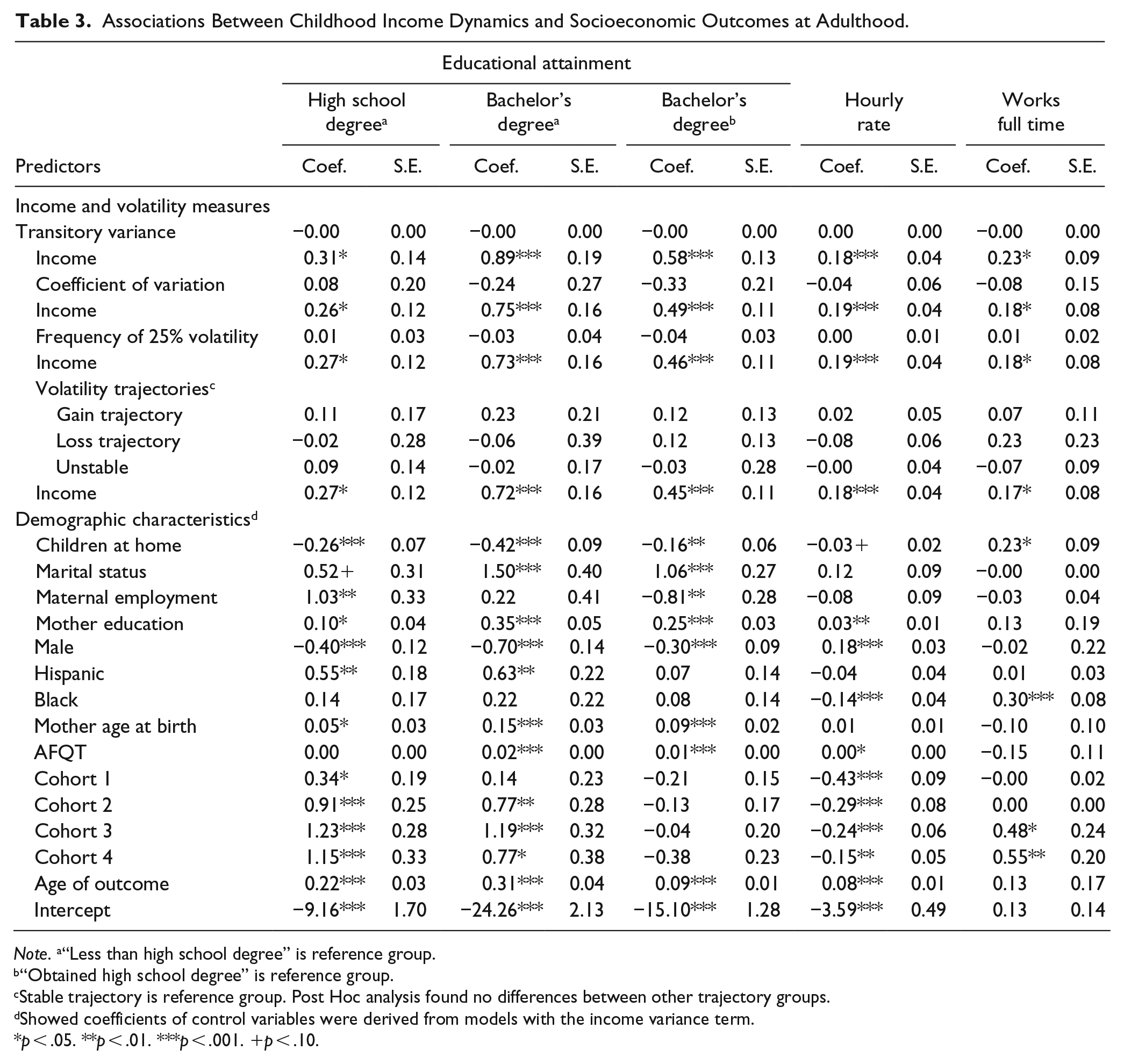

Associations Between Childhood Income Dynamics and Socioeconomic Outcomes at Adulthood.

Note. a“Less than high school degree” is reference group.

“Obtained high school degree” is reference group.

Stable trajectory is reference group. Post Hoc analysis found no differences between other trajectory groups.

Showed coefficients of control variables were derived from models with the income variance term.

p < .05. **p < .01. ***p < .001. +p < .10.

Mental and Behavioral Health

Results examining associations between childhood income dynamics and adult mental and behavioral health outcomes are presented in Table 2. Across all model specifications, childhood income dynamics were not associated with adult risky behaviors. Significant associations between income dynamics and both depression and teen parenthood emerged. Income volatility predicted higher depression in adulthood across all measures of volatility. The model including transitory variance showed that a 10,000 dollar increase within the individual variance of participants predicted an increase of depressive symptoms of 0.002 SD. The estimates including the coefficient of variation indicated that an income change equivalent to the participant’s income mean was associated with an increase of 0.21 SD of depression scores. Results of the model using the measure of frequency of 25% periods of volatility showed that every income change of at least 25% was associated with an increase of depressive symptoms of 0.02 SD. When the categorical trajectories of volatility were considered, results showed that participants in the unstable trajectory group exhibited 0.11 SD more depressive symptoms than participants in the stable trajectory group. When it came to income level, yearly income was only associated with depression in models using transitory income variance as the volatility measure. An increase of a log unit of income was associated with a 0.11 SD decrease in the depression scale.

Models predicting teen parenthood indicated that a log increase in the income during childhood was associated with 30 to 33% reduction in the likelihood of becoming a teen parent (RRR = 0.67 to 0.70). Turning to income volatility, results using the coefficient of variation showed that that an income change equivalent to the participant’s mean was associated with an 88% (RRR = 1.88) increase in the likelihood of becoming a parent during the teen years. Findings also suggested that experiencing an income change of at least 25% was associated with an increase of 7% in the likelihood of teen parenthood. Results using volatility trajectories indicators showed that members of the unstable income group were 34% (RRR = 1.34) more likely to become a teen parent in comparison to participants in the stable income group.

Socioeconomic Outcomes

Next, this study asked whether yearly income and income volatility predicted education and employment outcomes in early adulthood. Results, presented in Table 3, indicated that higher income during childhood predicted better socioeconomic outcomes. Income volatility, however, was never significantly related to young adult socioeconomic attainments. With respect to income level, a log increase in yearly income was associated with a 30 to 36% (RRR = 1.30 to 1.36) higher likelihood of obtaining a high school degree and a 105 to 143% (RRR = 2.05 to 2.43) greater likelihood of obtaining a bachelor’s degree in comparison to not attaining a high school degree. In addition, when compared to a group with high school degree, a log increase in yearly income was associated with 57 to 79% (RRR = 1.57 to 1.79) greater likelihood of obtaining a bachelor’s degree. With respect to wages, for each log unit increase in yearly income during childhood, there was an increase of 0.18 to 0.19 (SD = 0.21) in the participants’ earnings in young adulthood, expressed as a proportion of the mean for their age group. Finally, income level was related to the likelihood of working full-time during adulthood. Specifically, a log increase in childhood income level predicted an 18 to 26% (RRR = 1.18 to 1.26) higher likelihood of working full time as a young adult.

Discussion

The present study provides a better understanding of the longitudinal links between childhood family income dynamics (i.e., cumulative family income and income volatility) and socioeconomic and mental and behavioral health outcomes in young adulthood. Results suggest that childhood income dynamics are related to important outcomes in young adulthood.

Findings demonstrated that family income dynamics during childhood matter for young adult mental and behavioral functioning, supporting similar findings of other birth cohort studies (Chaudry & Wimer, 2016; Maloney, 2004; Najman et al., 2010). Specifically, increased yearly income was associated with a reduction in depression and a reduction in the likelihood of teen parenthood, while increased income volatility predicted higher levels of depression and rates of teen parenthood. These findings were robust across each of the alternative measures of volatility, and importantly, the findings related to specific trajectories (e.g., stable, losses, gains, and unstable) suggested that income volatility was disadvantageous regardless of directionality. More specifically, evidence showed that the unstable trajectory (i.e., experiencing upward and downward changes in income over time) was detrimental for young adult mental/behavioral health outcomes compared to income-stable families. Interestingly, and contrary to our hypothesis, consistent income losses over time did not relate to worse mental and behavioral health outcomes. Perhaps the unstable trajectory represents those families whose frequent income and employment changes cause families to move in and out of eligibility for public assistance (Hill et al., 2013). These families face the stressful situation of frequently losing eligibility for benefits and having to reapply/requalify for assistance, which may have negative impacts on family functioning, parenting, and, in turn, children’s mental health and behavior—a stressful situation which may not be present in households that have consistent downward income trajectories. Our volatility findings align with another recent study finding links between early income volatility and young adult mental health outcomes (Cheng et al., 2020). While studies have typically shown stronger links between income dynamics and externalizing behavior rather than internalizing (Magnuson & Votruba-Drzal, 2008), neither income level nor volatility was significantly associated with risky behavior in young adulthood.

Findings also provided evidence that family income level, but not income volatility, during childhood matter for young adult socioeconomic outcomes (e.g., educational attainment, full-time employment, and hourly wage). Higher family income during childhood was positively associated with more years of education, full-time employment, and hourly wage rate. This corroborates prior studies that also found that increased childhood family income related to improved educational attainment (Maloney, 2004) and increased adult earnings and work hours (Duncan et al., 2013). Contrary to a prior study that found links between increased income volatility and lower educational attainment (Hardy, 2014) we did not find links between volatility, measured in various ways, and educational attainment. A reason for the disparate results could be the differences in the educational measures used. While Hardy (2014) specifically examined high school drop-out and whether children attained post-secondary education by 24 to 26 years, we examined educational attainment from “less than high school” through “college or more” from 24 to 33 years. Perhaps the effects of income volatility on education fade over time. A more nuanced explanation could be that children from families with higher income volatility take longer to achieve similar levels of education due to constraints on parental investment or, perhaps, potential omission from need-based financial aid typically reserved for low-income families rather than those with unstable income.

Overall, these findings, consistent with hypotheses, align with prior theory and evidence regarding investment and family stress mechanisms. Resource and investment processes have been touted as the primary driver of income gaps in achievement and academic outcomes, while stress processes are considered paramount in shaping mental health and behavior (e.g., Yeung et al., 2002). The present study found that income level, which has empirically linked to both parental investments and stress (Magnuson & Votruba-Drzal, 2008), was related to all socioeconomic and mental and behavioral health outcomes. Income volatility, on the other hand, was linked to mental and behavioral health outcomes only. This emphasizes the role that income instability plays in the family stress model in particular, as demonstrated in much of the foundational literature (Conger et al., 1992; McLoyd, 1990). It may also indicate that annual income level, more so than volatility, drives investments in children and adolescents. The failure to observe links between childhood income volatility and adult socioeconomic attainments may also be a result of the continuity of achievement. Academic skills stay relatively stable over time, as the skills gained early in life form the basis of future skills acquisition and attainment (Heckman, 2000). Thus, adult socioeconomic outcomes may be less responsive to episodic volatility in family income because these trajectories are set earlier in life and resistant to change. Taken together, the present study provides sound support for the claim that income level and income volatility have long-term consequences for healthy developmental outcomes not only in the cognitive or achievement domain, but also for behavioral health outcomes (Duncan et al., 1998; Hardy, 2014; Hill et al., 2013; Mayer, 1997; Miller & Votruba-Drzal, 2017; Yeung et al., 2002).

Practical Implications

These results may have implications for policies and programs aimed at stemming the intergenerational transmission of disadvantage. Systematic links between income volatility and maladaptive mental and behavioral health outcomes indicate that we should consider children living in families with high levels of income volatility as high-risk regardless of annual income. Given that income volatility is being experienced across the income-distribution much more frequently, children that are not low-income but live in highly volatile economic circumstances may be at risk for educational, economic, and social difficulties in adulthood. Accordingly, these children could benefit from programs and policies aimed at stabilizing family economic resources, such as a universal child allowance or those that incentivize family savings accounts for children, so that families have financial reserves to draw from for investing in their children during years when earnings are lower than anticipated.

For instance, a monthly child allowance for all households with children would provide families with a regular, dependable, monthly cash benefit that would help stabilize family economic resources by providing an “income floor” to families (Shaefer et al., 2018). A child allowance would benefit low-income children with unemployed (or not stably employed) parents as well as children whose parents are working but for low or unpredictable wages. It would also provide assistance to children in working- and middle-class families, most of whose annual incomes fall above the limits for means-tested program but have barely budged in the last 20 years and are more volatile now than ever (Duncan et al., 2011; Hacker & Jacobs, 2008; Morduch & Schneider, 2017; Sandstrom & Huerta, 2013).

Additionally, results support policy recommendations that transfer or in-kind programs should aim to provide financial stability, not just the provision of basic needs, by making amends to the current eligibility and administration practices that greatly limit the stabilizing potentials of these programs (Hardy et al., 2019; Hill et al., 2017). Low-income families often experience income or employment status changes that then cause their eligibility for means-tested programs to fluctuate (Hardy et al., 2019). For instance, the Earned Income Tax Credit program, which requires parents to be steadily employed to receive the supplement, may not help stabilize families who experience unstable income and/or employment and fluctuate in their eligibility, undermining efforts to provide financial security. Thus, it is crucial for means-tested programs for low-income families to consider the implications of program eligibility criteria and other aspects of program administration for income stability over time. Research shows that too many American families lack accessible, predictable cash income (Edin & Shaefer, 2015, 2016) and the stabilizing effects of income support programs have decreased (Hardy, 2014). Our work suggests that income stability, over and above income level, matters greatly for supporting long-term mental and behavioral health.

Limitations and Future Directions

The results of this study are correlational and must therefore be interpreted with caution. Family income and income volatility are not randomly assigned—just as parents make choices that affect their level of investment, they also make choices that affect their earnings and the proximal contexts in which their children develop. Their children also go on to make their own choices that affect educational attainment and employment as they emerge into young adulthood. Thus, it is possible that the associations between income dynamics and young adult outcomes could be due to unmeasured characteristics of the parents and children in our sample, despite our inclusion of a several family demographic covariates in each of our models. The current study’s reliance on self-reported measures may limit the accuracy of the estimated correlations due to this method being shared between input and outcome variables.

However, given what we know of the literature, we may be able to infer causality from these results at least in part. More specifically, the rise in income volatility has been shown to be largely driven by declining economic security (e.g., increased involuntary job displacements, earnings volatility, and variability in cash transfers and social supports against income shocks) (Hardy et al., 2019; Hacker & Jacobs, 2008). Furthermore, the “polarization” of job opportunities concentrated at the high-skill, high wage and the low-skill, low-wage ends at the expense of “middling” high-quality jobs that do not require college degrees (Autor, 2011) represents structural changes in the economy that drive job loss and other labor market experiences that are directly tied to family income volatility (Hardy et al., 2019). Moreover, research has long-established family financial circumstance as a determinant of child developmental and socioeconomic outcomes (Hardy et al., 2019) and increasingly suggests that child outcomes may be worsened by sharp income fluctuations caused by economic insecurity (Hacker & Jacobs, 2008). In fact, one study found compelling causal evidence for the effect of job loss on child achievement using analytic strategies like fixed effects and placebo tests (Stevens & Schaller, 2011). Thus, our findings for income volatility are well situated within the larger body of evidence for direct links between economic circumstance and child wellbeing and may represent the consequences of exposure to economic and employment insecurity, lending themselves to more causal interpretation. Still, it is imperative that future research utilize quasi-experimental methods or natural experiments to strengthen our ability to draw causal conclusions about the impact of income dynamics on wellbeing in order to inform programs and policies.

Additionally, the present study created measures of income volatility based on a net family income variable collected yearly by the NLSY. The impact of income dynamics on families’ stress and investment decisions, and, in turn, on children’s outcomes, may be driven more by variability in income earned week-to-week or month-to-month than yearly income (Hill et al., 2013). Unfortunately, the NLSY does not contain data that captures families’ earnings at shorter intervals, and these findings must be interpreted with respect to the yearly timeframe. We also acknowledge that due to changes in data collection, we were further limited in our ability to use annual datapoints. Thus, there is a good chance that our estimates may be downwardly biased because we are only able to measure volatility on a 2-year interval. Nevertheless, we still uncover significant results. Lastly, the NLSY data oversampled low-income families, which limits the generalizability of the results. However, importantly, this oversampling allows us to examine the effects of income dynamics more precisely for low-income families, compared to their middle-income and upper-income counterparts. Still, more stringent data collection and studies that focus on income dynamics regularly measured on a weekly or monthly basis in more nationally-representative samples are needed to enhance our understanding of how income volatility relates to development.

Conclusion

The present study contributes greatly to the extant literature evidencing joint effects of cumulative family income and income volatility over the life span. Additionally, it contributes to the dearth of information on the impact of income instability by specifically examining absolute volatility, measured in various ways, and expanding the set of outcomes across multiple domains. Remarkably, the present findings underscore the importance of previous claims that family income level predominantly affects parental investment and child achievement outcomes, whereas income volatility affects parental stress and parenting, yielding a greater impact on children’s behavior outcomes (Conger et al., 2010; Hill et al., 2013). This deeper theoretical and empirical understanding of income dynamics points toward the far-reaching, intergenerational contributions to be made by policies that mitigate family poverty and income instability, which, in turn, promote educational attainment, meaningful employment, and healthy family formation as children emerge into adulthood.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Research reported in this publication was supported by the Eunice Kennedy Shriver National Institute of Child Health & Human Development of the National Institutes of Health under Award Number R03HD091610. The content is solely the responsibility of the authors and does not necessarily represent the official views of the National Institutes of Health.