Abstract

Tourism productivity measures are quite diverse, not always compatible and usually based partly on labor productivity for hotels and restaurants. This article develops a holistic approach that integrates the principles of the growth accounting framework and tourism satellite account to measure multifactor productivity, labor productivity and capital productivity for the Australian tourism industry. This study shows that tourism has been identified as a reservoir for other industries through the ebbs and flows of labor demands. Compared with the rest of the economy, the average growth of labor productivity—that is, income per unit of labor—for tourism is stagnant, and has reached an unprecedented low, six times below the market sector average, mainly because of low multifactor productivity. The results are valuable for policy makers and the lobbying groups wanting to identify areas of need for policy changes to ensure the healthy long-term growth of tourism.

Keywords

Introduction

Productivity is a measure of output quantities per unit of input. In limited resource conditions, improvement in productivity is imperative to ensure a healthy long-term contribution of industries to an economy, as it “is an important determinant of long-term economic growth and real per capita income growth, which in turn are crucial (but not the only) determinants of living standards and wellbeing” (Productivity Commission 2013, p. 6). Measured productivity is thus an important indicator for policy makers and peak industry bodies to understand the strengths and weaknesses of the industry in interest. The productivity measures provide a strong basis for strategic policy development.

Most countries, including Australia, have sufficient data on inputs and outputs of industries conventionally recognized in the System of National Accounts (SNA) for productivity to be calculated or estimated. Indeed, the Australian Bureau of Statistics (ABS) publishes annual productivity measures for the market sector industries as well as the aggregate market sector (ABS 2016b). These are industries with well-defined output exchanged in markets at observable prices. In comparison, input and output data for tourism are not compiled explicitly in the SNA. The Tourism Satellite Account (TSA) framework was thus developed by the United Nations World Tourism Organization (UNWTO 1994, 2010) to allow tourism to be recognized as an industry in an economy. Through this TSA, basic tourism statistics are avail-able for comparing tourism with conventional industries; however, tourism productivity measures—in particular, multifactor productivity—are not readily available from all national statistical organizations.

Productivity measurement is a well-established research area in economics, and it is also applied widely in tourism. The approaches to measuring tourism productivity thus vary between researchers. The leading techniques are Data Envelopment Analysis (DEA) and Stochastic Frontier Analysis (SFA), and occasionally the Malmquist Index. They are predominantly adopted to the hotel sector—one of the main constituents of tourism. Findings from these studies are valuable in their own right, specifically for the entities selected in the analysis, as these studies clearly point out the know-how of best practices for others to adopt—which is the main objective of the technique. As tourism consists of more than just hotels, such results for hotels in particular are partial in nature, and it is not ideal to project these productivity measures onto tourism as a whole.

In the Australian context, tourism share of total national GDP has declined steadily from nearly 4% in the early 2000s to approximately 3.2% in recent years (ABS 2016b). And given the fact that tourism is a labor-intensive industry, the declining share could also mean declining wage rates for workers in the industry. This poses an inevitable question about the productivity performance of the entire tourism industry over time, including hotel and all other constituents of the tourism industry such as air transport, ground transport, and café and restaurants that provide goods and services to tourists, as it is this type of productivity that determines the contribution of the overall tourism industry, as shares, to the economy and the living standard or well-being of workers in the tourism industry.

To address this question, this article outlines a new approach that integrates the growth accounting framework with the TSA framework to provide a holistic approach to measuring the productivity of the Australian tourism industry. This approach constitutes one fundamental contribution to the existing tourism productivity literature, in which it develops a framework to calculate all three much-needed but previously uncalculated productivity measures for tourism: capital productivity, labor productivity, and multifactor productivity. The paper provides explicitly a formal relationship among these three measures. It highlights the important role of productivity measures in policy formulation. Findings from this article show a clear deterministic relationship between weak multifactor productivity and subsequent low labor productivity for the Australian tourism industry in recent years—an issue that requires policy changes for rectification. The article also clearly identifies tourism as a reservoir for other industries through the ebbs and flows of labor demands. As changes in these productivity measures are not independent of the overall economic environment, this article diagnoses the determinants of tourism productivity in the context of economic development in the Australian economy—a new perspective of tourism productivity analysis.

Although this empirical study is set for the Australian context, it also has a broader applicability to the tourism industry in many other countries. The paper provides a general approach to measuring all types of tourism productivity that goes beyond relevance only to Australia. It opens up a comprehensive method that analyzes tourism productivity in the context of broad economic environment and policy settings, alongside all other industries in the economy. This article establishes a good basis for policy makers and industry lobbying groups to understand the performance of the tourism industry, a necessary perspective for relevant policy development.

An Overview of Productivity Methodologies

Concepts and Definitions

Increases in the quantity of inputs used can often lead to increases in output; however, changes in input and output growth might not necessarily be the same. In the simplest terms, when output growth exceeds input growth, the unit cost of products is effectively reduced, and this essentially reflects an improvement in the productivity of the production process. In contrast, if output growth is lagging behind input growth, this results in an increase in the unit cost, reflecting a loss of productivity instead.

In a broad classification, a production process typically requires two main types of primary inputs: labor and capital. As a result, productivity measures are also associated with these types of inputs. Labor productivity measures changes of output per unit of labor; similarly, capital productivity measures changes of output per unit of capital used in production. As changes to any inputs will have effects on the outputs, attributing productivity to a single input without any further details about its composition could misrepresent the significance of the other inputs.

Productivity is more about technology or efficiency—the ways in which multiple inputs and knowledge are combined to reduce the unit cost of output. Technological improvement occurs when new machinery and equipment are used by the same employees at the same level of skills to produce more outputs. This aspect of improvement requires new capital. Efficiency improvement occurs when improved labor skills can produce more output from the same machinery and equipment. When both of these occur, output growth will not be the same as growth in the combined primary inputs—labor and capital. This gives rise to a comprehensive measure of productivity with respect to a whole bundle of primary inputs. Measures in this approach are commonly referred to as total factor productivity (TFP) or multifactor productivity (MFP), which are interchangeable terms. The MFP is calculated on the basis of the output growth that is not explained by the composite capital-labor input growth.

Although these concepts seem quite straightforward, their implementation is not always an easy task. The choices of outputs and inputs can lead to different challenges for data requirements and can determine the types of measures for different practical purposes. Putting the concepts into an operational context, the form of output in the productivity calculation can be the total production value (hereafter, gross output) or the gross value added (GVA) component of the interested firm or industry. Gross output is the amount of “the goods or services that are produced within a producer unit and that become available for use outside the unit” (OECD 2001). Alternatively, GVA is the gross output net of all intermediate input values used in production. Essentially, GVA only includes compensation of employees (COE), gross operating surplus (GOS) and net production taxes.

For the labor input, employment numbers and number of hours worked are the two choices. Number of hours worked is a better option, as it accounts for changes in overtime worked, standard weekly hours, leave taken, and proportion of the full-time and part-time combination (Zheng 2005). Capital input is capital services, including produced and nonproduced assets such as land for agriculture.

Among all possible types of productivity measures, the most commonly used are labor productivity (LP) and capital-labor MFP on the GVA basis. Although it is a partial measure, LP is often used as a reference in wage bargaining because it reflects (at least to some degree) living standards of workers among industries or countries, so is relevant to policy makers. In particular, the GVA-based measures are often used because, compared with the gross output–based labor productivity, GVA-based labor productivity is less sensitive to the outsourcing processes involving substitution between intermediate inputs and labor. The GVA-based LP formula effectively removes the distortion effect of outsourcing in productivity measures; when this occurs, values for both GVA and labor input will decrease at the same time, while the value of gross output does not necessarily change in the presence of outsourcing (OECD 2001), thus exaggerating the true values of LP. Furthermore, the GVA-based measures reflect the ability of an industry or an economy to convert primary resources into income—a viable indicator for the producers. It is therefore an analytical tool for comparing the contributions of industries to national income growth, any structural change or changes in living standards in an economy (OECD 2001).

Productivity Measures in Tourism

Although productivity is reflected by a simple principle of an output/input ratio, the actual modeling applications are vastly different from each other. Del Gatto, Di Liberto, and Petraglia (2011) present a comprehensive survey of productivity methodologies, including Data Envelopment Analysis (DEA), Stochastic Frontier Analysis (SFA), growth regression, proxies variables, index number, and growth accoutning framework.

Having inherited such a diverse array of methodologies, productivity analysis of the tourism industry has proliferated over the past two decades. Barros (2005a, 2005b), Barros and Mascarenhas (2005), Assaf, Barros, and Josiassen (2010), and Assaf and Agbola (2011) provide snapshot summaries over several decades of productivity analysis of tourism across all types of modeling approaches. From those studies, it is very clear the concept of output and input is not limited to a single output or a single input. Quite often, they are expanded to multiple outputs and multiple inputs. Outputs are evaluated in the forms of room revenue, revenue per room, sales, gross letting, total revenue or tourism receipts (Anderson et al. 1999; Anderson, Fok, and Scott 2000; Ashrafi et al. 2013; Barros 2005a, 2005b; Barros and Dieke 2008; Barros and Santos 2006; Chen 2009; Hwang and Chang 2003; Morey and Dittman 1995; Peypoch 2007; Reynolds 2003), food and beverage revenue (Ashrafi et al. 2013; Chiang, Tsai, and Wang 2004; Hwang and Chang 2003; Johns, Howcroft, and Drake 1997), occupancy rate (Ashrafi et al. 2013; Chen 2009), operational cost (Barros 2004, 2006), customer satisfaction (Brown and Ragsdale 2002; Reynolds and Biel 2007), visitor numbers, visitor room nights (Johns, Howcroft, and Drake 1997), number of guests (Barros 2005a, 2005b; Chen 2009), and number of trips (Anderson, Lewis, and Parker 1999).

Inputs include labor (full-time equivalent [FTE]), costs of labor, hours worked, average wages, price of capital, price of materials, total costs (Reynolds 2003; Barros 2004, 2005a), ownership forms of hotels (Oliveira, Pedro, and Marques 2013b; Ortega and Chicón 2013; Perrigot, Cliquet, and Piot-Lepetit 2009), surface area in square meters, rooms and median price (Brown and Ragsdale 2002; Tsaur 2001; Wang, Hung, and Shang 2006), customer satisfaction (Assaf and Magnini 2012), hotel star-rating (Oliveira, Pedro, and Marques 2013a), natural resources (Hadad et al. 2012), the role of information communication technologies (Li 2014; Sigala 2003), the number of schooling years of staff (Ortega and Chicón 2013), nights slept (Barros and Santos 2006), and the number of years in business (Assaf and Agbola 2011). Surprisingly, tourist numbers or number of guests were used in relation to both aspects of hospitality: as an input measure (Ashrafi et al. 2013) and an output measure, as seen in many of the studies mentioned previously.

An observation of the inputs used in previous studies shows that some are directly involved in the service provision (production process) of the hospitality industry, such as labor (FTE) and rooms (although they are not homogeneous), but others are just the attributes and conditions under which hospitality services are delivered. The multiple dimensions of inputs and output are well catered for by the flexibility of the frontier approach that allows analyses to cover a wide range of research objectives for different reasons. This is an advantage of the DEA, SFA, and Malmquist Index methods, which can reveal the best practices in various aspects so that others (followers) can adopt them in order to improve efficiency. Results, however, are measured in partial conditions and related to very specific aspects of service provision. Overall, findings across all studies are not strictly comparable, and it is not ideal to project these as productivity measures of the tourism industry.

Joppe and Li (2016, p. 144) point out that hotels and restaurants are often used to represent a much broader tourism industry, and they also raise an important concern that most studies seem to perceive a simple ratio of output per employee as sufficient to track productivity. They further highlight that the framework of the TSA could provide a more holistic view on the measurement of tourism productivity. Indeed, what is needed is a measure that embraces changes of productivity of those at the frontier as well as those below the frontier so as to understand the entire group of businesses in tourism, beyond hospitality. For this requirement, the tourism satellite account is undoubtedly the most suitable framework to reflect the entire tourism industry.

An early application of the TSA framework for tourism productivity was developed by Medlik (1988) to calculate the tourism labor productivity only, on the basis of employed persons for the United Kingdom. These estimates are recently updated by the Office for National Statistics of the United Kingdom (2016).

And more recently, based on an econometric approach, Li, Joppe, and Meis (2016) use the Canadian TSA data to calculate elasticities (sensitiveness) of tourism labor productivity with respect to various aspects of the labor force: capital intensity, male/female employees, immigrants/Canadian-born, part-time and full-time employment, age groups, skill levels, and by tourism-related industries (air transport, other transport, accommodation services, entertainment and recreation, food and beverage services, and travel services). While this approach provides important policy instruments, however, it does not assess the actual performance of tourism labor productivity over time—particularly in the context of broader economic development in the country.

This article is set out to measure the performance of tourism productivity explicitly for all three measures: labor productivity, capital productivity, and multifactor productivity on the GVA basis.

The National Account and Tourism Satellite Account

“Tourism is a social, cultural and economic phenomenon related to the movement of people to places outside their usual place of residence” (UNWTO 2010) to seek pleasure and experience from their trips. Thus, tourism consumption is defined by the virtue of consumption purpose rather than the functionality of goods and services. The System of National Accounts (SNA) does not record household consumption in this way: tourism consumption is not apparent in the national account. Therefore, it is not possible to reflect the contribution of tourism activity to the economy in general, or to compare its contribution with other, more conventional, industries.

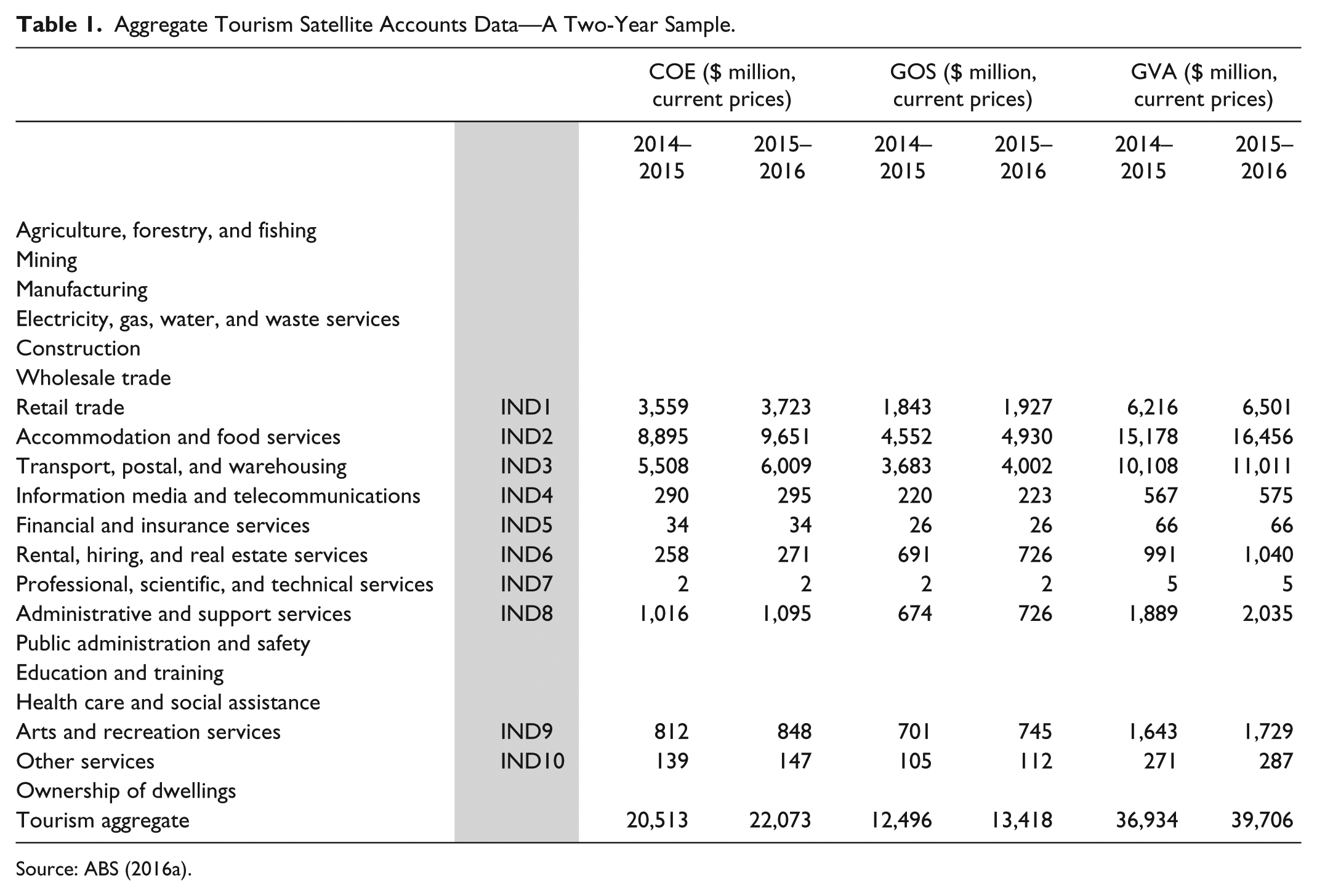

The UNWTO (1994, 2010) creates a well-defined methodology for constructing TSAs, which are based primarily on the demand side through tourism expenditure data collected by surveys. Tourism demand is then translated into the supply-side data of the tourism industry, such as tourism output, tourism GVA, and tourism GDP. TSA data are based on tourism characteristic and connected industries, which are eventually mapped explicitly to the conventional ANZSIC 1 standard in the core SNA, as seen in Table 1. The practical process used to derive TSA data is beyond the scope of this article, but for more information see Pham, Dwyer, and Spurr (2009). In the TSA framework, tourism is now represented explicitly by its constituents in the form of the associated conventional industries. Table 1 shows a two-year sample of the TSA time series data available over the period of 19 years from 1997–1998 to 2015–2016.

Aggregate Tourism Satellite Accounts Data—A Two-Year Sample.

Source: ABS (2016a).

The advantage of using TSA data is that tourism is fully and explicitly captured through its constituent parts. The constituent elements of tourism are more than just hotels and restaurants, among all the other items of tourism expenditure. Changes in tourism productivity could be pinpointed by individual constituents clearly. However, given the nature of the approach that MFP is estimated as a residual in the production function, it could include factors other than technology changes. These could include shifts in the production process, or even short-term measurement errors. Thus, results of average annual growth over each productivity cycle are more reliable.

At the aggregate level, TSA provides GVA series of tourism, but the lack of capital services is an impediment to the calculation of the multifactor productivity measure, which requires three individual input series: labor input, capital input, and GVA series.

This article proposes an approach to deriving the three input series directly, using two sources of information. One of them is the ABS publication catalog number 5260.0 (ABS 2016b), which provides hours worked, capital services, and real GVA indexes for all conventional industries. The three tourism indexes are then calculated as the weighted sum of those series from catalog number 5260.0 using the corresponding shares implied by Table 1 (second source). Hours worked series is aggregated by using the COE shares, capital services by the GOS shares, and GVA by the GVA shares. An important note here is that shares must be calculated on the nominal values to closely reflect the principle of Laspeyres chain volume index.

It should be noted that data in Table 1 represent values of tourism activity as part of those conventional industries. In contrast, the index series from the source of catalogue number 5260.0 represents movements of hours worked, capital services and GVA for the entire industry, including tourism and non-tourism components.

The above approach reflects a few assumptions. First, each conventional industry applies the same technology to produce its goods or services for tourism and non-tourism consumption. Thus, the total cost (output) in each conventional industry is proportionally allocated to non-tourism and tourism activities, depending on the proportion of consumption shares. Second, it also implies that both tourism and non-tourism face the same price for the same goods or services produced within each ANZSIC industry. Consequently, volume changes of both tourism and non-tourism will move in line together with the industry aggregate.

As a counterargument, if it is argued that demand for tourism and non-tourism components can move very differently, then prices faced by the two components can also be very different from each other. This argument warrants a bottom–up approach to estimate the price series explicitly for each good and service consumed by tourists so that chain volume measures (CVM) of GVA, capital services, and hours worked can subsequently be calculated. Although this is ideal, data on prices for individual components for this approach are simply not available for tourism consumption. Our observation of the official data is that the attempted price series for the tourism component at the (conventional) industry level is highly volatile, resulting in improbable CVM values for the GVA series. To some extent, it might be unrealistic to assume that tourists would have to pay a different price from that paid by the household sector for the same product. Although TSA provides GVA for tourism on the CMV basis, for consistency of input data used in the calculation of the multifactor productivity measure, this article estimates the CVM values of tourism GVA together with the hours worked and capital services.

At the core of the SNA, indices for hours worked, capital services, and real GVA (CVM basis) are available for most ANZSIC industries (ABS 2016b), except for education, health services, public administration and safety, and ownership of dwellings, as volume (real) measures for output of these industries are conceptually difficult to evaluate, so the ABS does not calculate them. Only the available series are used in the associated tourism series. From the tourism perspective, these omitted non-market-sector industries represent approximately 18% of the total tourism GVA. Productivity measures in this article therefore capture slightly more than 80% of the entire tourism industry; however, this is still well above the hospitality-only measure (30%) in most previous studies.

The ABS introduced and implemented the concept of productivity cycles to ensure the internal consistency of the measured productivity. Cycles do not have the same length of time, but each is defined in such a way that the level of capacity utilization remains comparable within each cycle throughout the ebb and flow of demands. Average productivity growth estimates in a cycle are likely to be more reliable than year-to-year changes. There have been eight cycles so far since 1973–1974 (ABS 2016b), the most recent three of which are considered in this article.

Methodology and Modeling Approach

Growth Accounting Framework

This section explains how the above three input series are used to derive the tourism productivity measures using the growth accounting framework. Solow (1957) examined productivity measures based on a general production function with time dimension t:

Totally differentiate (1) with respect to time:

where

Divide (3) by Q:

Note that taking partial derivatives on (1) with respect to K and L separately gives

Substitute (6) and (7) into (5):

In a perfect competition condition where factors are paid at their marginal product values, (8) can then be rewritten explicitly with rental prices of capital (r) and labor wage rates (w):

or equivalently with factor cost shares of capital (SHRK) and labor (SHRL):

Note that

where q, a, k, and l are now growth in output, multifactor productivity, capital, and labor, respectively.

Given the available data for output, capital, and labor, changes in variable a can be derived using (11). Essentially, when a is a positive (increasing) number, the output can grow more than the actual increase in inputs, reflecting an improvement in MFP of the economy. In contrast, when a is negative (decreasing), output growth is less than the increase in inputs used, indicating a loss of MFP.

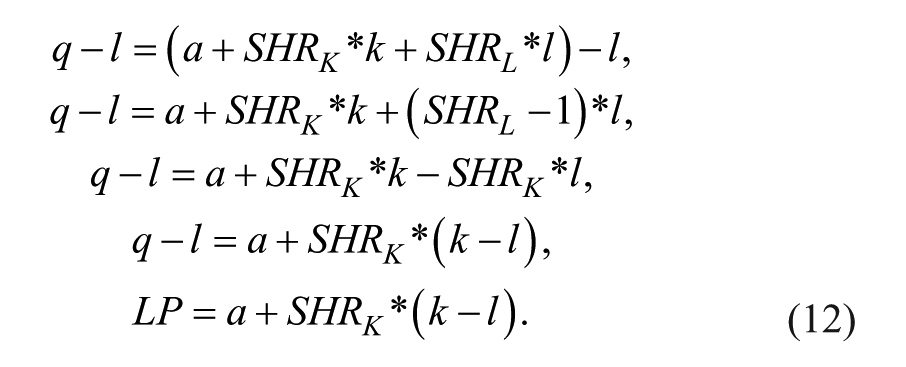

Relationship between MFP and Labor Productivity

Equation (11) can be rewritten as follow to reflect output per unit of labor (hours worked):

Equation (12) shows that LP is positively related to MFP (the a term) and growth rate of capital per hours worked ratio—or capital deepening. Increases in MFP growth will raise labor productivity growth in a ratio of 1:1, creating a powerful policy instrument to enhance income per unit of labor in the economy. This will inevitably entail research and development investment (Doraszelski and Jaumandreu 2013). To that end, government has to play a leading role actively. Labor productivity could also be increased by changing the ratio of physical capital available to workers in the production process; however, increases in capital deepening are only translated into income per unit of labor by a smaller proportion, determined by the capital share in the industry. Thus, increases in capital in labor-intensive industries such as tourism will not result in significant changes in labor productivity—income per unit of labor (hours worked)—because of the constraint of the capital share in the industry cost structure, which is around 40% in the Australian tourism industry (ABS 2016a).

Result Discussions

Input and Output Tourism Indices: An Overall View

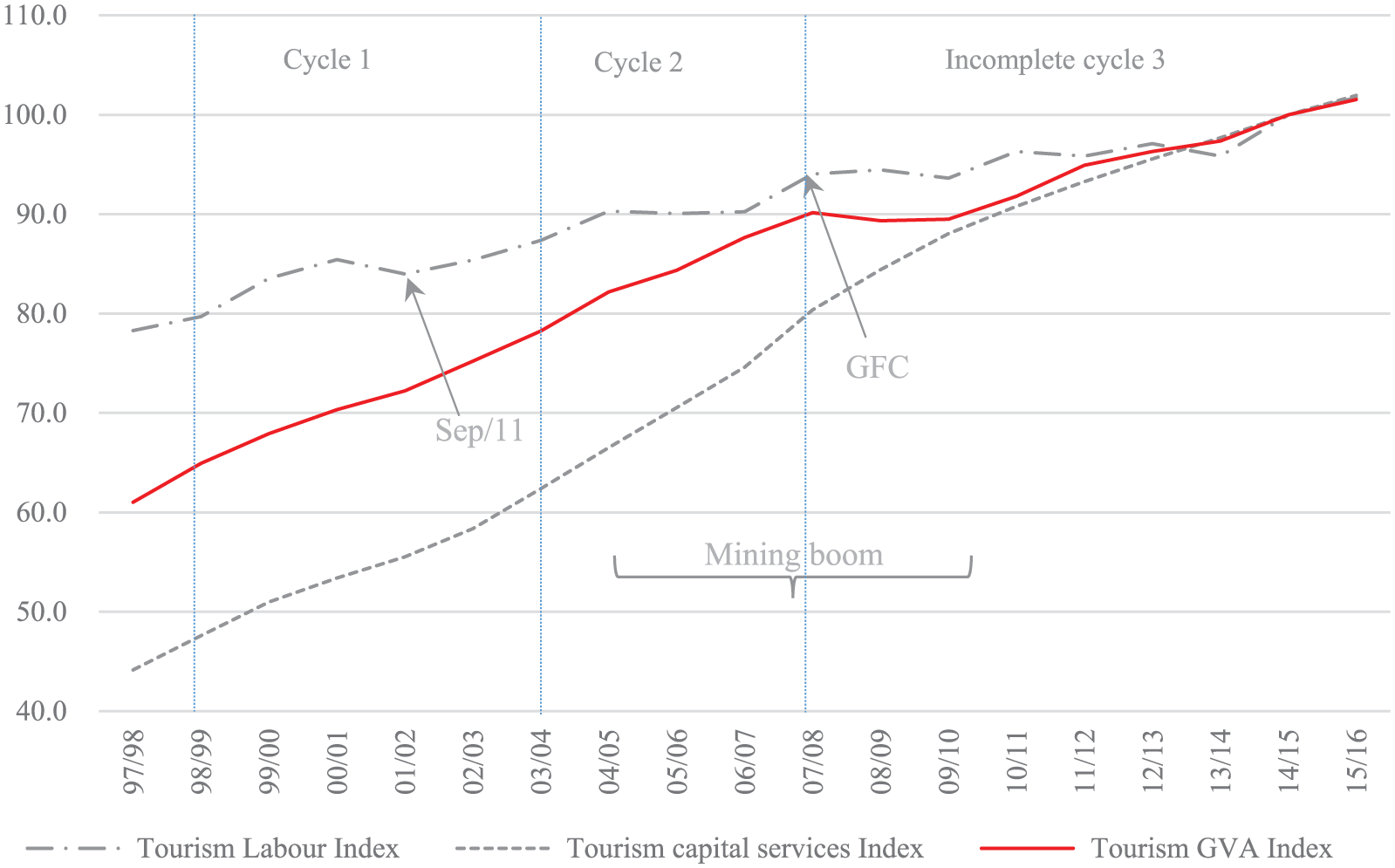

This section identifies determinants of tourism input and output indices, which will ultimately affect productivity of the tourism sector as a whole. The three tourism indices (hours worked, capital services, and GVA) are presented in Figure 1, while the details of calculations for all constituents are included in Appendix A (Tables A1, A2, and A3). Changes in all three indices across cycles are complex, as they were determined by different factors in the economy. Cycle 1 inherited the benefits of economic reforms in the 1980s and experienced a housing boom, of which the increased “equity” significantly stimulated household consumption, including tourism. Cycle 2 had a large mining boom that drew labor away from other industries. The mining boom was the main cause of a record high in the appreciation (31%) of the Australian dollar, creating a three-speed economy: the mining sector with strong growth, one group of sluggish or even declining industries, and another group that benefited from the mining sector (Corden 2011). As will be seen, tourism was actually part of both groups, simultaneously receiving positive and negative impacts from the boom. Cycle 3 suffered severely from the Global Financial Crisis (GFC), so the effects were seemingly uniform across all industries from 2007–2008 onwards.

Derived input and output indices of tourism, 2014–2015 = 100.

Between the two input indices, the hours worked index has fluctuated more than the capital services index (Figure 1). This is because labor is generally more dispensable and mobile than capital in the short run, and the fluctuation has indeed been identified as a major challenge for the tourism industry. Given the fact that tourism businesses are often small in size and labor intensive, vulnerability in the labor market makes it hard for tourism business owners to operate, as the costs of retaining and/or retraining staff are very high. Labor reform remains important for the tourism industry.

Areas of reform need to focus on enhancing flexibility to increase labor supply from external sources such as working holidaymakers, and alleviating labor skill shortages through learning and training. The expensive working holiday visa fee certainly remains as an impediment in this case (Pham et al. 2018). The significant increases in immigration intake in 2016–2017 and part of 2017–2018 were perhaps part of the strategic policy that the Australian government uses in an attempt to address labor shortages (ABS 2018a).

Changes in the capital services index were driven not only by the demand from tourists but also by the prevailing cost of capital formation—which is closely linked to the exchange rate as investment inputs are also sourced from overseas—and the relative cost of using labor and capital. While labor is dispensable and mobile at the industry level, it is constrained at the aggregate level. Tourism demand for hours worked increased steadily between June 1999 and June 2005 but subsequently stalled when mining started drawing resources away from the rest of the economy. The hours worked for tourism began to pick up again in June 2008, but stopped short in June 2009 because of the global financial crisis (GFC). Over the whole period up until June 2009, the higher demand growth in labor pushed up labor costs significantly. On the trend basis, total hourly rates of pay (excluding bonuses) increased approximately 3.7% quarterly on average—nearly double the modest growth rate of 2% per quarter in recent time (ABS 2018b). Furthermore, the appreciation of the exchange rate made imported investment goods cheaper, thereby lowering investment costs from overseas sources. Relatively speaking, the cost of capital was cheaper than the cost of labor. This explains clearly why capital services grew much more strongly over the period 1997/1998 to 2012–2013, particularly in the first two cycles. Over the whole time frame to 2015–2016, the average annual growth of capital services over the entire period is 4.8%, while hours worked only grew at an average of 1.5% per year (Table 2). 2 The tourism industry has become more capital intensive over time, predominantly in the first two cycles. This is in line with the overall changes in the economy. For the tourism GVA index, the effect of the GFC puts a distinguishing mark on the chart, where tourism output growth was completely muted over the period 2007–2008 to 2009–2010.

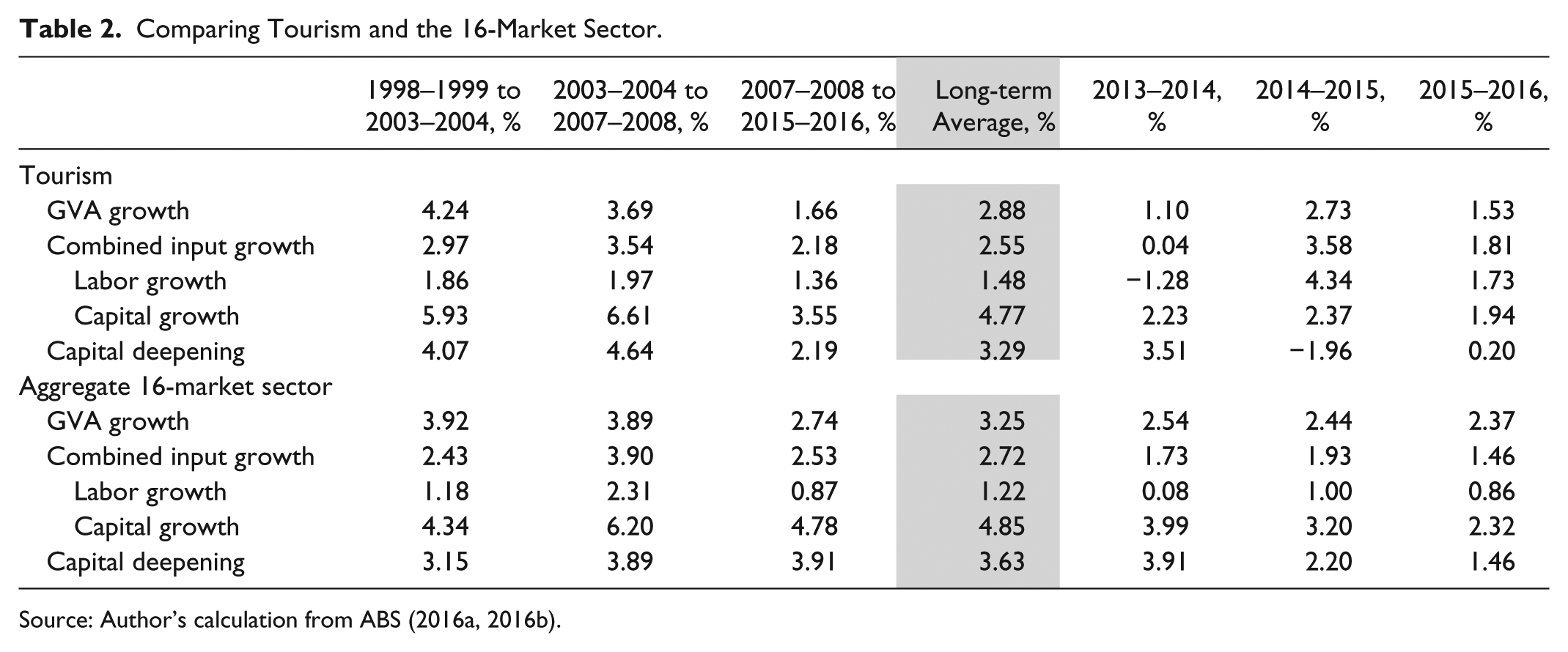

Comparing Tourism and the 16-Market Sector.

Source: Author’s calculation from ABS (2016a, 2016b).

Components of Input and Output Tourism Indices

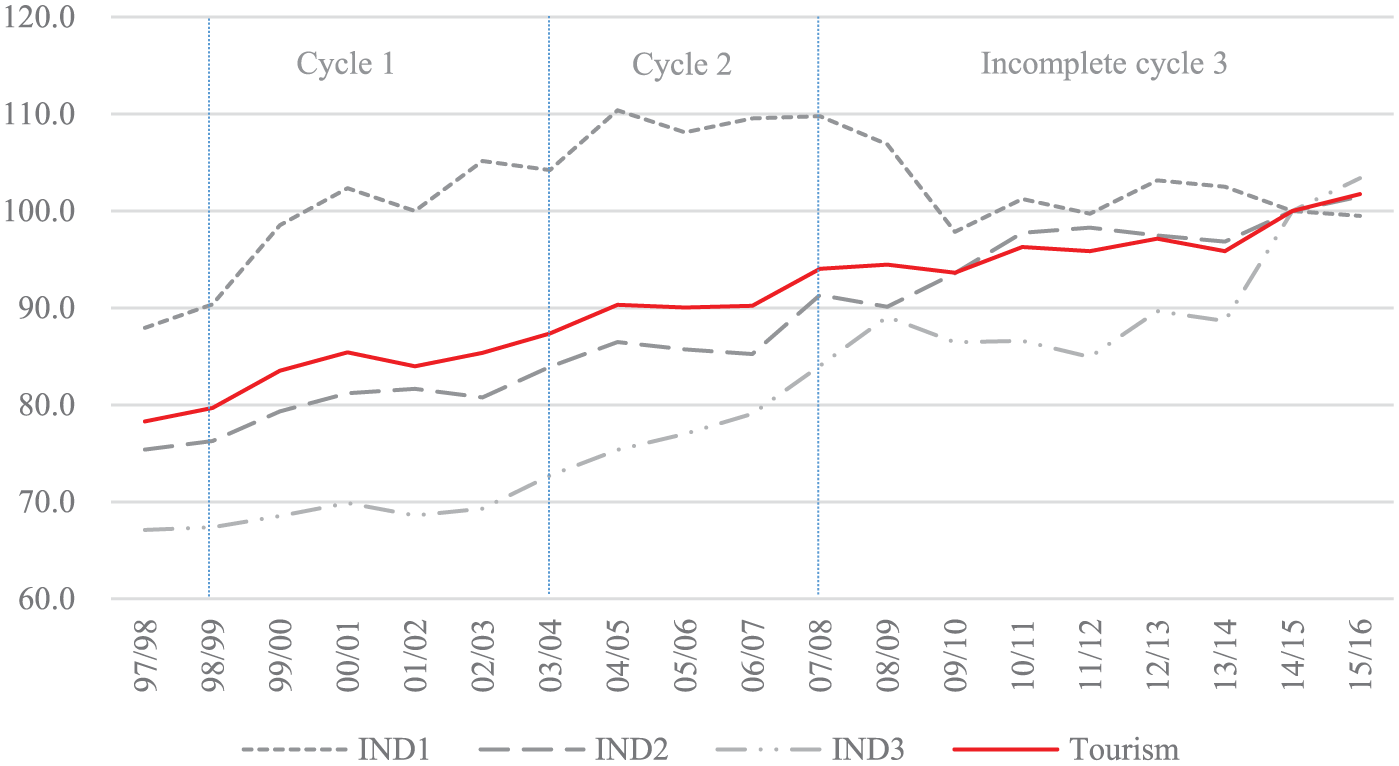

At the constituent level, the fluctuation of labor is even more volatile (Figure 2). Among the top three (for short: IND1, retail; IND2, accommodation; and IND3, transport), hours worked generally increased throughout cycle 1 until mid–cycle 2, before the mining boom started affecting domestic industries.

Hours worked index and its main constituents, 2014–2015 = 100.

The upward trends of hours worked for all sectors in cycle 1 were mainly due to the effect of the housing boom in Australia, which generated a larger “equity” share in household assets and boosted consumer confidence over the period. Changes in tourism demand for labor in the subsequent cycles were not uniform across the constituents of the tourism industry. The mining boom in a period spanning cycles 2 and 3 (2004–2005 to 2009–2010) significantly raised the demand for fly-in fly-out (FIFO) 3 mining employees. This not only increased domestic airfares to deter holidaymakers, but also reduced the seats available to holidaymakers in general. This FIFO demand effectively altered the mix of tourism demand toward more business travelers, who did not spend as much as holidaymakers on retail goods (gifts and souvenirs).

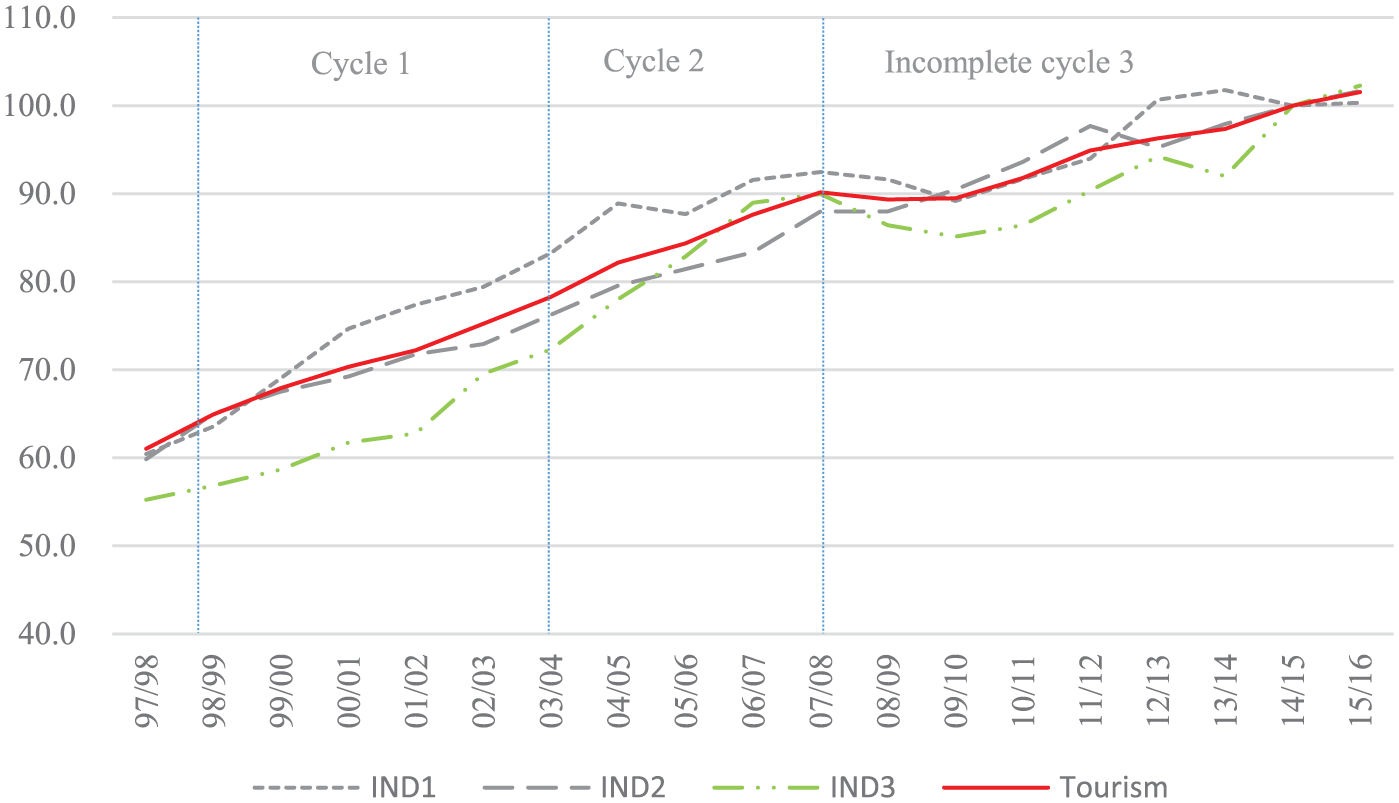

In addition, the nature of the mining boom led to a strong appreciation of the Australian dollar, a record high in the exchange rate (Corden 2011; Corden and Neary 1982; Pham et al. 2015), which stimulated a strong substitution of imports for domestic goods and services generally, and outbound for domestic travel in tourism particularly, which subsequently resulted in a reduced demand for a wide range of local goods and services (Pham et al. 2015). Outbound tourism expenditure increased at a double-digit growth rate of 12.6% a year on average between 2004–2005 and 2007–2008 (ABS 2016a). Lower demand for domestic leisure travel contributed partly to the reduced demand for tourism retail trade between the two years, as seen in Figures 2 and 4. This downturn in demand for hours worked in the retail trade sector was further exacerbated by the compound adverse effect of the GFC in the inbound market, where consumers in general and tourists in particular were losing their appetite for spending. The pattern of stagnation in hours worked and GVA for retail (Figures 2 and 4) are similar up until 2009–2010. However, growth in hours worked in this retail sector for tourism consumption has continued to tumble since then, while tourism GVA of retail actually seems to have recovered from the GFC effect. This is probably due to a general decline in retail sales of department stores since 2003, because of increased online sales activity, as can be seen in Appendix B (ABS 2017). Thus, hours worked in the entire retail sector have generally fallen over time.

Unlike the retail trade sector, demand for both accommodation (IND2) and transport (IND3) sectors was actually boosted by the mining boom, because of a significant demand generated by the FIFO mining workers for both of these sectors—particularly transport—as reflected by changes in hours worked and GVA indices in Figures 2 and 4. Although the GFC effects occurred after 2007–2008, the mining boom effects were still dominating the domestic economy, strongly stimulating business travelers to offset the decline in domestic nights for leisure traveling; hours worked and demand for accommodation were still growing steadily until the tail end of the mining boom in 2010–2011. In contrast, hours worked and GVA for transport dropped significantly after the GFC, well before the tail end of the mining boom in 2009–2010. This is because inbound visitors contributed more than 30% of the total long-distance transport revenue, and these inbound visitor numbers slowed down in both 2007–2008 (–0.6%) and 2008–2009 (–1.9%) and remained weak until 2012–2013 (ABS 2016a). Most importantly, the composition of the inbound markets changed considerably. While visitor and visitor nights from traditional markets such as New Zealand, United Kingdom, United States, and Japan reduced significantly as a result of the GFC, visitors and visitor nights from the Chinese market continued to grow strongly at a double-digit level (Tourism Research Australia 2017). Given the fact that visitors from those traditional markets tend to travel much more widely across Australia compared with Chinese visitors, who tend to stay at the same location and predominantly focus on education, the share of airfares in total expenditure is far higher for visitors from the traditional markets than for Chinese visitors (unpublished regional tourism expenditure from Tourism Research Australia). The loss of demand for air transportation from the traditional markets could not be offset sufficiently by the increased number of Chinese visitors. As a result, demand for air transport reduced noticeably in the immediate post-GFC period, as seen in Figures 2–4, while demand for accommodation remained steady throughout.

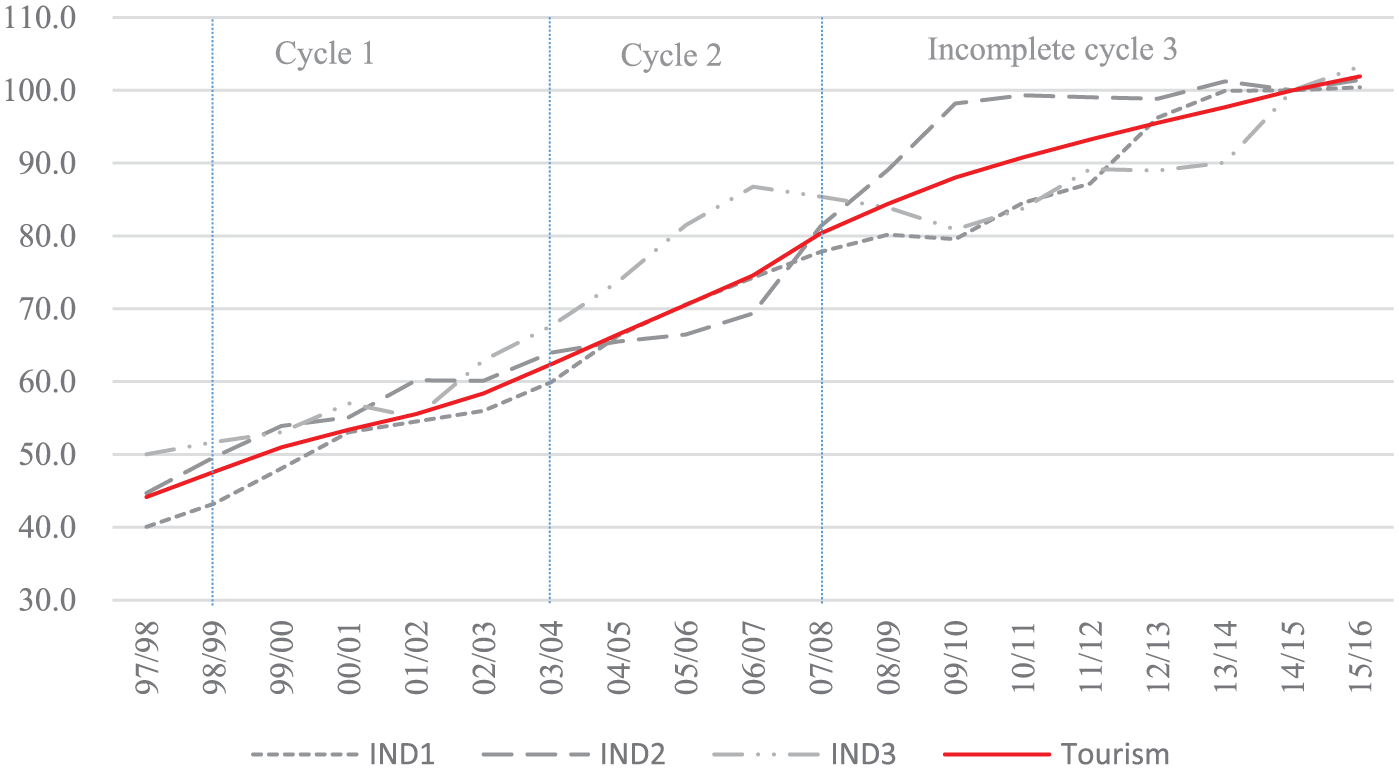

Capital service index and its constituents, 2014–2015 = 100.

Tourism GVA index and its constituents, 2014–2015 = 100.

The movements of capital services indices of the three main constituents (Figure 3) did not fluctuate as much as those of the hours worked. While the hours worked in the retail trade sector were adversely affected at the beginning of the mining boom period, capital services growth in the retail trade sector continued to grow throughout, from cycle 1 to cycle 3. Capital services for transport (IND3) increased noticeably over the period 2003–2004 to the pre-GFC year 2006–2007 (Figure 3). It is interesting to see that the transport sector started to accelerate (Figure 3) much earlier than the accommodation sector (IND2) at the commencement of the boom, as it did take time for investment construction to be realized as rooms and hotels before they could be used. Once they were in operation, its growth was phenomenal, fueled by both the FIFO demand and the compositional change of demand pattern of the inbound sector (more Chinese visitors, thus more accommodation than air transport services). Unfortunately, the tail end of the mining boom has completely neutralized the growth of capital services in the accommodation sector since 2009–2010, while the retail trade and transport sectors seem to have recovered from the effects of the GFC.

Comparing Indices between Tourism and the 16-Market Sector

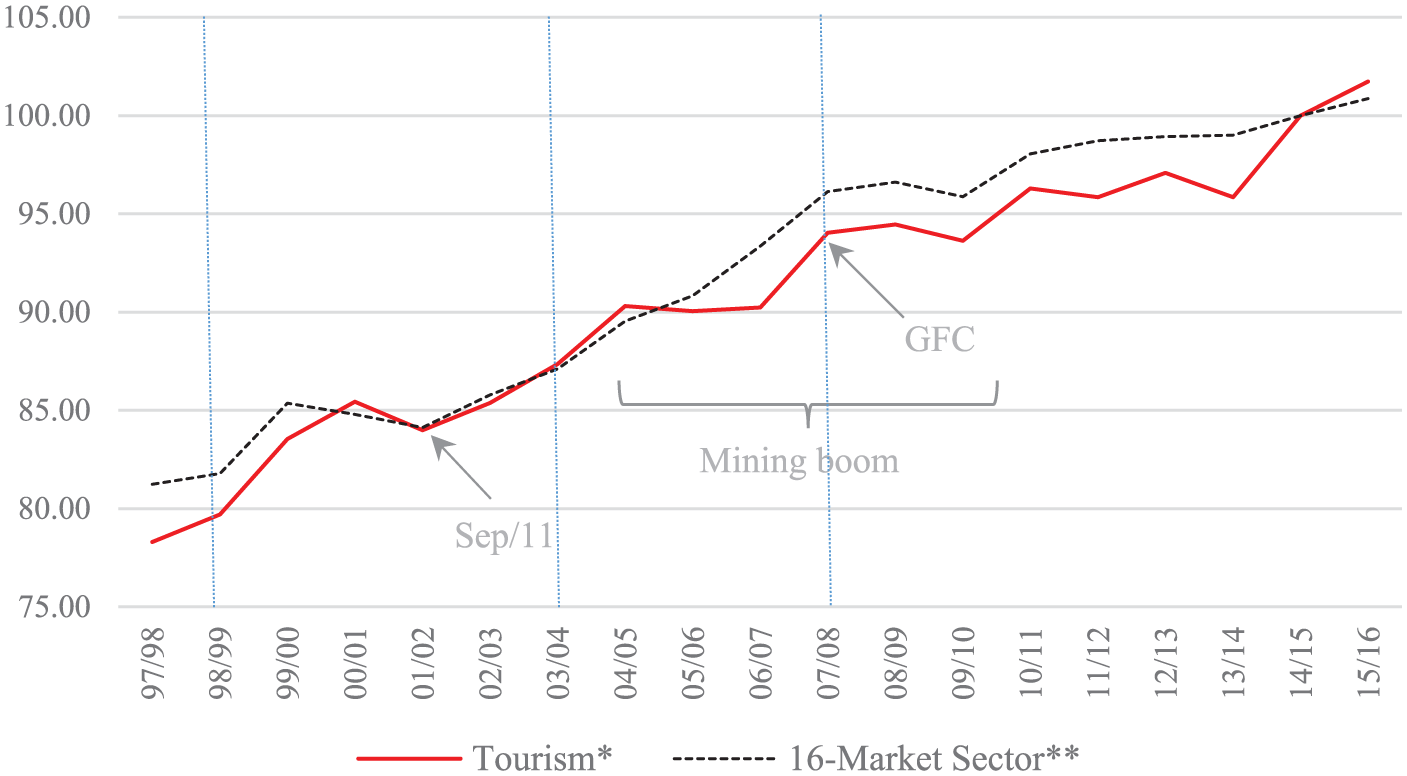

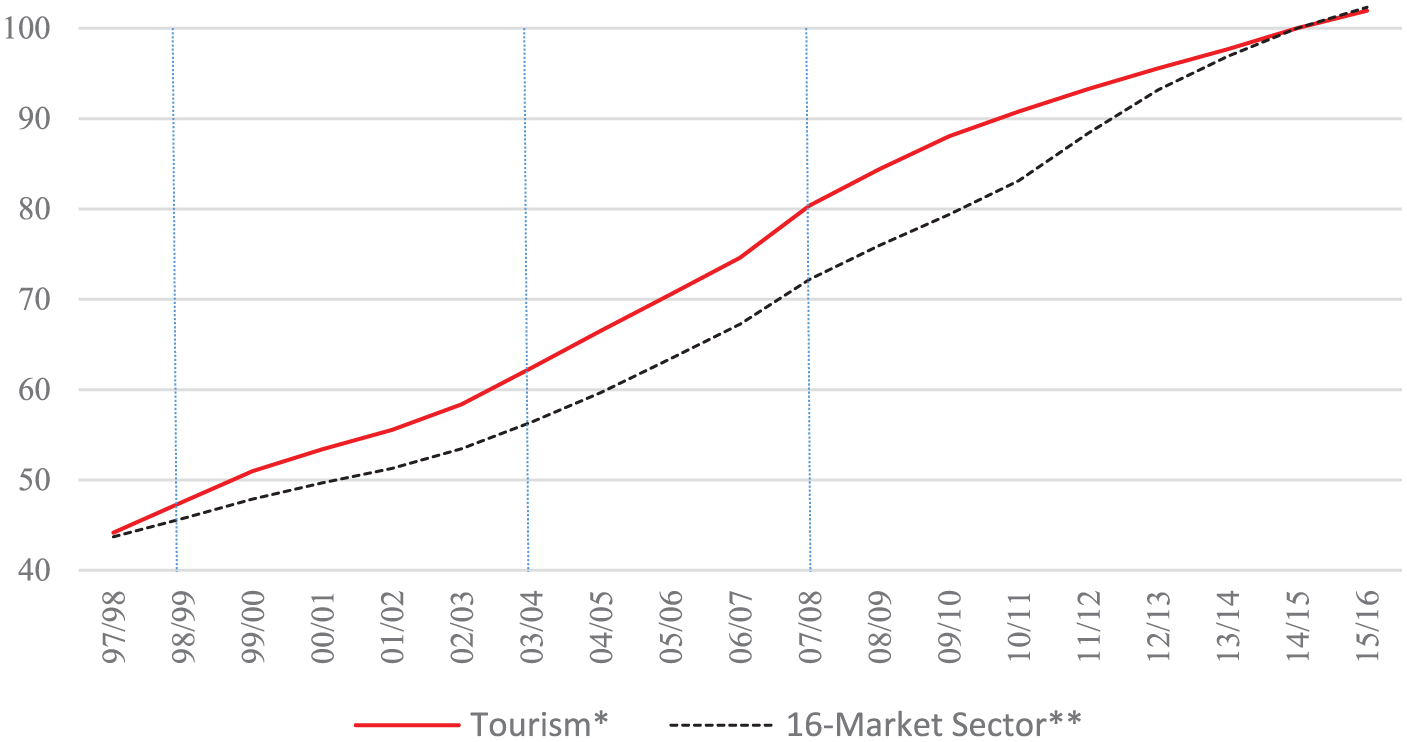

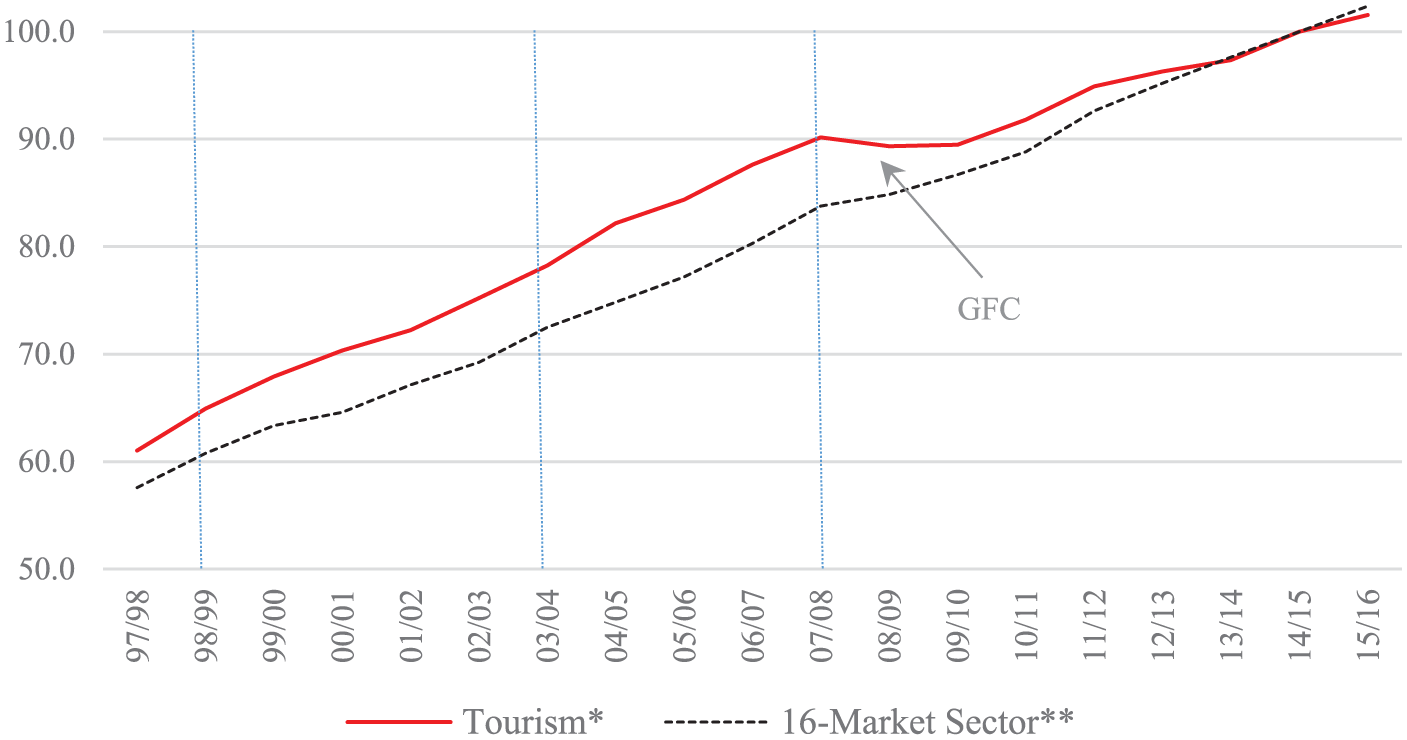

Figures 5–7 compare tourism indices derived in this article with those of the 16-market sector published by the ABS (2016b). As expected, these figures show that overall tourism tracks the 16-market sector over time, although there are differences.

Hours worked indices, 2014–2015 = 100.

Capital services indices, 2014–2015 = 100.

GVA indices, 2014–2015 = 100.

For the labor market, fluctuations in tourism occur more often, exhibiting a staircase stop–start pattern at each adverse event in the short term. Although not shown in this article, the inbound tourism sector was just recovering from the Asian Financial Crisis in the late 1990s, followed up with a boost from the domestic tourism market because of the housing boom of the early 2000s. Hours worked growth was actually accelerating slightly faster in tourism than in the 16-market sector in cycle 1 (Figure 5): 1.86% compared with 1.18% per annum on average, respectively (Table 2). In cycle 2, the mining boom started to draw labor away from tourism and many other sectors in the economy toward the mining sector. Annual average hours worked in the 16-market sector were dominated by demand for labor in the mining sector, thus moving faster (2.31%) than for tourism (1.97%). Demand for labor in tourism actually stalled for a number of years in this second cycle (Figure 5) before a short recovery at the end of the mining boom. Unfortunately, the subsequent GFC further weakened labor demand across all sectors, including tourism, at the beginning of cycle 3. Only at the end of cycle 3 has tourism labor demand picked up to experience a strong recovery compared with the rest of the economy. On average, hours worked in tourism increased by 1.36% annually in the last cycle, noticeably above that of the 16-market sector (0.87%). The data here indicate that tourism is indeed an industry that absorbs ebbs and flows in the economy. At the time of high demand for labor, workers move away from tourism to fill up jobs in other industries where shocks occur. At times of low labor demand, workers return to tourism for jobs. Clearly, tourism provides an employment buffer for the rest of the economy. The movements are driven by the differences in the wage rates between industries.

In contrast to hours worked, the capital services index is smooth over time, illustrating the intrinsic long-term nature of capital—a stark difference between labor and capital. Tourism sustained stronger growth of capital services compared with the 16-market sector in both cycles 1 and 2. However, the drivers and interaction of both tourism and the 16-market sectors were all different. Strong capital growth in tourism in the first cycle arose from the final demand induced by the housing boom, where income elasticity played a major role. As a rule of thumb, changes in demand for luxury goods is magnified from the changes in income (income elasticity is greater than unity), as such tourism would take off faster than most of other commodities during peak time. In this first cycle, annual tourism GVA increased by 4.24% on average—clearly above that of the 16-market sector, 3.9%. Thus, it is not surprising to see faster capital services in tourism (5.9%) than in the 16-market sector (4.3%) in this case.

In the second cycle, however, a major structural change occurred in the economy, where mining was the growth-leading sector while many other industries were crowded out. Capital expenditure growth of mining alone increased 80% in 2005–2006 and remained higher than 20% until 2008–2009 (ABS 2018c). The aggregate growth of capital services of the 16-market sector (6.2%) was slightly below that of tourism (6.6%) on the annual average basis, as the aggregate of the 16-market sector also included industries that were affected adversely by the mining boom. Even though holidaymakers were adversely affected by the mining boom, capital services growth of tourism in this second cycle was induced by the mining boom directly to serve business travelers. Together with the FIFO demand, growth in the Chinese market also started building very strong momentum in this second cycle, leading to the highest growth of capital services compared with the previous cycle.

In the last cycle, with the effects of lost consumer confidence due to the GFC, tourism GVA suffered severely compared with the 16-market sector—slightly more than one percentage point of growth below the 16-market sector per year (1.66% as opposed to 2.74%; see Table 2). Tourism capital services growth (3.55%) was subsequently lower than that of the 16-market sector (4.78%, Table 2).

Tourism Productivity Measures

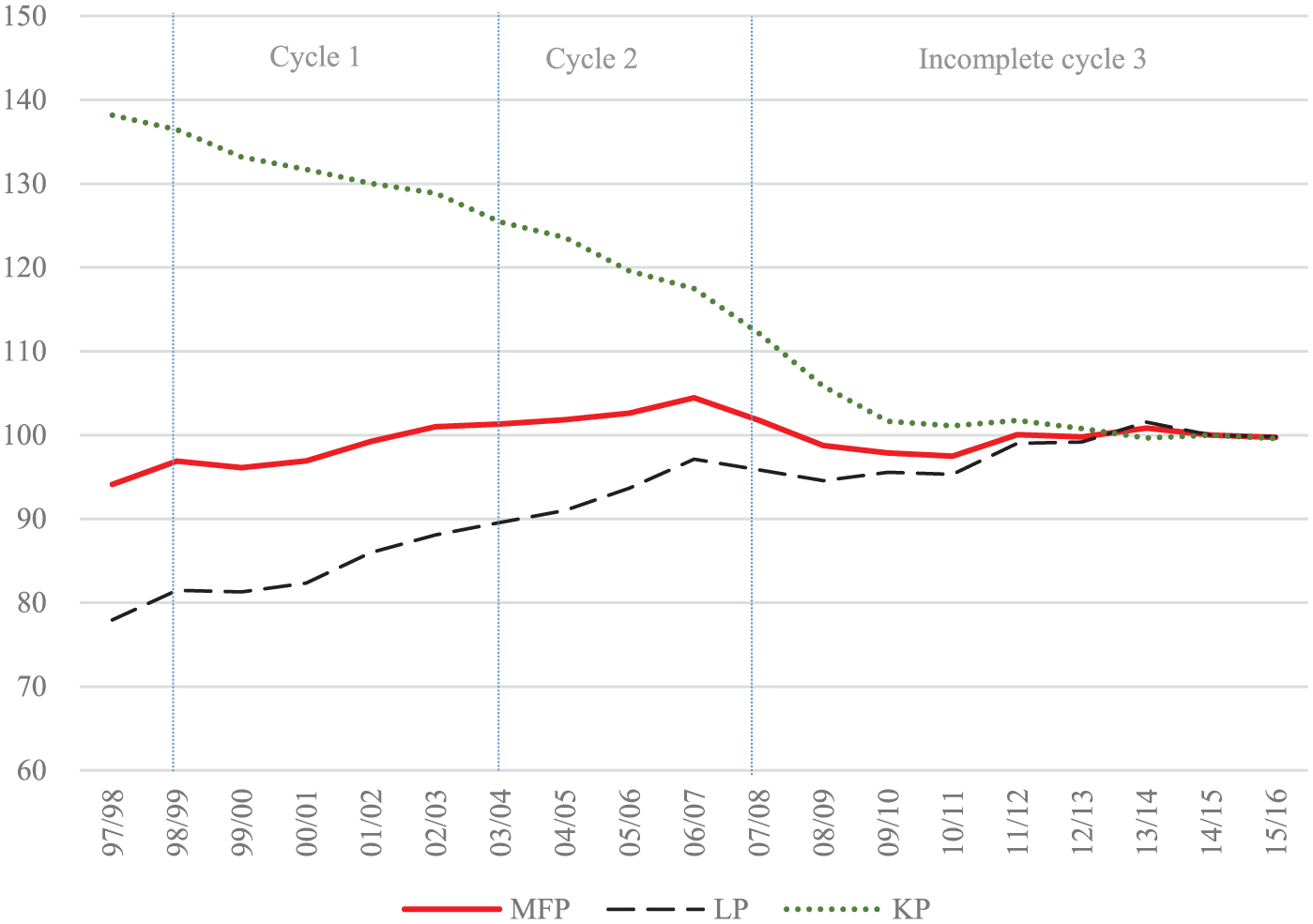

Following the literature, the choice of the GVA-based productivity measures here is to reflect the ability of the tourism industry to convert primary input usages such as capital and labor to income. Figure 8 clearly illustrates the implication of the strong capital inputs growth on the capital productivity measure for tourism. Throughout all three cycles, tourism experienced a long-term decline of −1.89% per year (Table 3) in capital productivity. Of the three cycles, capital productivity in the last (third) cycle has converged to the long-term average trend (−1.89% per year), a step up from the lowest decline of −2.92% per year on average in cycle 2 (Table 3), even though tourism output in the last cycle has been weakened significantly in recent times—at 1.66% per annum (Table 2). The improvement in capital productivity was mainly because of a slowdown in capital inputs. Indeed, although the output growth of tourism in cycle 2 was more than double the growth in cycle 3, it could not match the phenomenal increase in capital services (6.61% per year), leading to the lowest-level capital productivity of the cycle.

Tourism productivity indices, 2014–2015 =100.

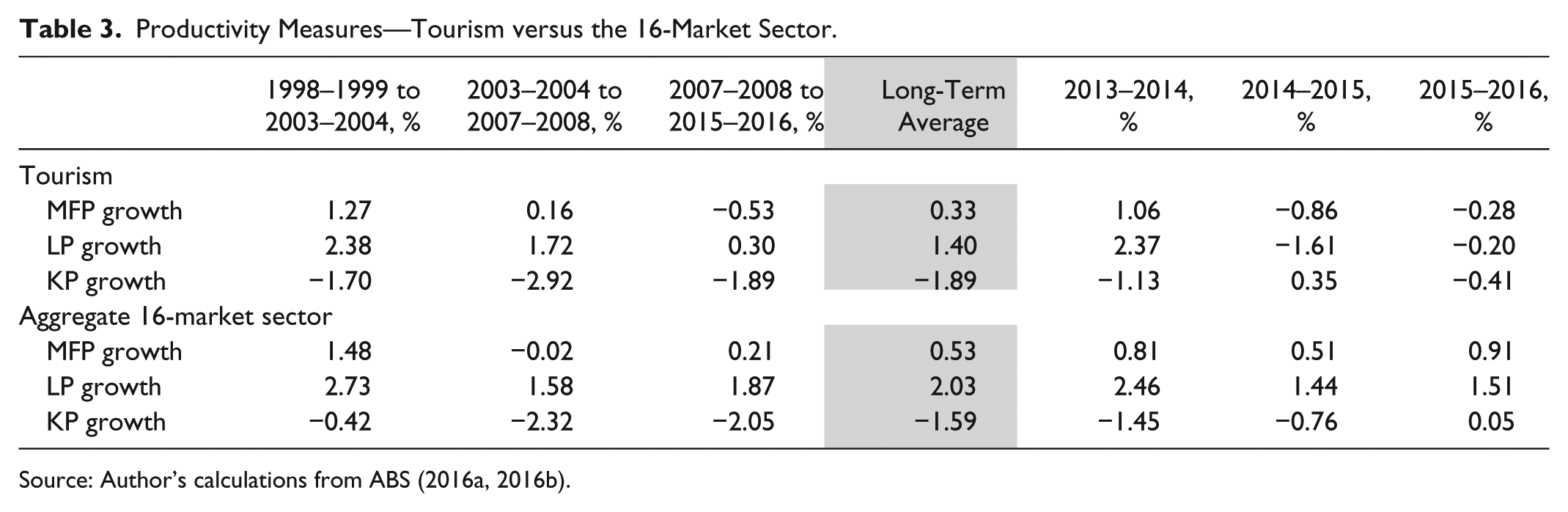

Productivity Measures—Tourism versus the 16-Market Sector.

Source: Author’s calculations from ABS (2016a, 2016b).

In contrast, slow growth in hours worked relative to the output growth of tourism resulted in continuous increases in labor productivity over time, but at a decreasing rate. LP growth in the first cycle was much higher than the long-term average, and was softened in the subsequent two cycles mainly because of the gradual slowdown in tourism GVA, to the extent where it was muted (0.3%) and submerged well below the long-term average of 1.4% per annum in recent times (Table 3).

The differences between capital input growth and hours worked growth indicate a very strong level of capital deepening over time. Tourism employees have had more capital, and perhaps rather better quality capital, with which to work (Table 2). This partly explains the strong LP growth (average income per unit of labor) in the first two cycles (using the framework in Equation 12).

Compared with the composite input of labor and capital, tourism output growth in cycle 1 was much stronger, leading to MFP growth in the cycle; however, growth in MFP started to become more muted from cycle 2, and has exhibited a downward trend since then. Undoubtedly the GFC was part of the reasons for such a decline in the MFP of the tourism industry, as illustrated in Figure 7. Overall, the long-term average of tourism MFP growth has been very modest, at 0.33% per year, which was mainly contributed by cycle 1 (1.27%).

The extent to which the GFC is exactly responsible for the changing landscape of tourism demand is beyond the scope of this article, and remains a topic of further research in this area. Nevertheless, the decline in the MFP by 0.5% per annum in the last cycle is an alarming sign for the Australian tourism industry, as it is not a sustainable condition under which the industry can operate. The strong growth in labor productivity (tourism income per unit of labor) has been neutralized significantly, with workers moving back to the tourism industry for jobs, and output not increasing strongly. While it is important for tourism to provide a job buffer for the rest of the economy, it is imperative for policy makers to be aware that the ability to generate labor income from the tourism sector—which is responsible for nearly 5% of the total employed persons in the economy (ABS 2016a)—seems to have stalled. The introduction of policies such as visitor visa fee reforms, particularly the passenger movement charges (Pham et al. 2018), which can facilitate larger numbers of visitors to Australia, is warranted.

Examining the average income per unit of labor (labor productivity) for tourism, and more generally the whole economy, in the full context with MFP and capital deepening, it is clear that high LP in cycle 1 was mainly contributed by the MFP. This first cycle inherited a series of economic reforms during the 1980s. Compared with cycle 1, the second cycle sustained only a slightly stronger capital deepening effect, but LP was weakened significantly because of a subdued level of MFP. This raises the strategic question of whether investment in physical capital stock alone is the right solution for the long-term sustainable growth of the industry and the economy. It has been shown here that the critical aspect of increasing income growth is strong positive growth in MFP, which is strongly related to better knowledge rooted in research and development, leading to higher levels of technology and efficiency, and ultimately to higher utilization of capital and equipment to generate income. It remains to be seen whether the Australian Government has demonstrated the right focus and strategy to shift gears for the tourism industry and the economy.

Comparing tourism and the 16-market sector, both have similar pattern of changes. Capital deepening was strong in both, but more evenly over time for the 16-market sector, while it seemed to concentrate more in the first two cycles and to reduce significantly in recent times for tourism (Table 2). MFP played an important role in determining the LP in the first cycle—both tourism and the 16-market sector had high LP growth. The main reason why the 16-market sector experienced a decline in MFP subsequently was that the high profitability of the mining boom did not require a commensurate increase in productivity to accompany the increase in export demand of the sector. Larger demands prompt the development of new mines that are deeper and more costly to construct because of the gradual depletion of natural resources. Furthermore, the investment in mining did not translate immediately into output growth, as it did take time for construction to complete before production could take place. The delayed effect significantly lowered the productivity of the sector (Productivity Commission 2013).

The most concerning issue now is the current gap in the growth of labor productivity in the last cycle between tourism (0.3% per annum) and the 16-market sector (1.87% per annum), which is nearly six times larger. The tourism industry and the government need to work closely together to improve equality in income earnings for workers in the tourism sector.

Conclusions

There are many potential techniques used to measure productivity, depending on individual purposes. They all have strengths and weaknesses, and none is superior to the others—it just depends on what answer one is after. However, some techniques are more widely adopted compared with others. In tourism, DEA and SFA are the most well known modeling techniques that have been applied to hotels or hospitality to estimate productivity representative for the tourism sector.

Tourism in fact includes a much wider range of goods and services than just hotels. To reflect the productivity of tourism as a whole, it is better to include all components that make up the industry. Among all constituents of tourism, retail trade, accommodation, and transport are the largest. Although the calculation of productivity incorporates a full set of all constituent industries, the analysis in this article focuses more on the largest three components.

The article has integrated the growth accounting framework with the TSA framework to provide a holistic approach to measuring tourism productivity. This approach is very useful for policy makers and the tourism industry body in the sense that it analyzes tourism productivity in the context of broad economic environment and policy settings, along with all other industries in the economy. Thus, the approach is suitable for policy makers as well as the tourism industry lobbying groups, to identify areas in need of policy change.

The findings are that tourism plays an important role in the Australian economy as a job buffer for all other industries, from boom to burst. Tourism is a reservoir to accommodate fluctuations in demand for labor in the economy. Hence, tourism business owners or operators often have to face situations where they cannot retain employees. Policies on labor flexibility are needed so that labor supply can be supplemented during high-demand seasons. Potential shifts include changes to attract more working holidaymakers; reforms to visitor visa schemes to enhance the competitiveness of the tourism industry; the alleviation of skill shortages through learning, training, and skilled migration; and specifically targeting tourism businesses.

Labor productivity growth in tourism increased significantly up until 2006–2007, but has mostly declined since then, and has dwindled considerably below the 16-market sector. This has been due to losses in tourism demand following the GFC and the subsequent declining trend in its MFP recently. There are concerns about how much government policy on research and development has affected the domestic industries, as the MFP for tourism—which is broadly similar to the 16-market sector—has reached a new low in the last cycle. Promoting and providing incentives for research and development is an area in which government can play an influential role—one it needs to play well. A further concern is how much the Australian tourism industry has innovated its products to entice tourists after a period of losing confidence in spending due to financial uncertainty. It is possible that tourists might have changed their travel propensity after the immense economic shock of the GFC. Perhaps this is an area for further research, to discover how long it would take tourists to resume their travel propensity after such a shock. However, it might also be possible that there are not enough new products to compete with other destinations for more tourists. Productivity improvement originates not only in the production process but also in the business strategy required to create desirable experiences for tourists to incentivize them to travel.

Footnotes

Appendix A: Calculation of Tourism Indices

Tourism Capital Service Index and Its Constituents.

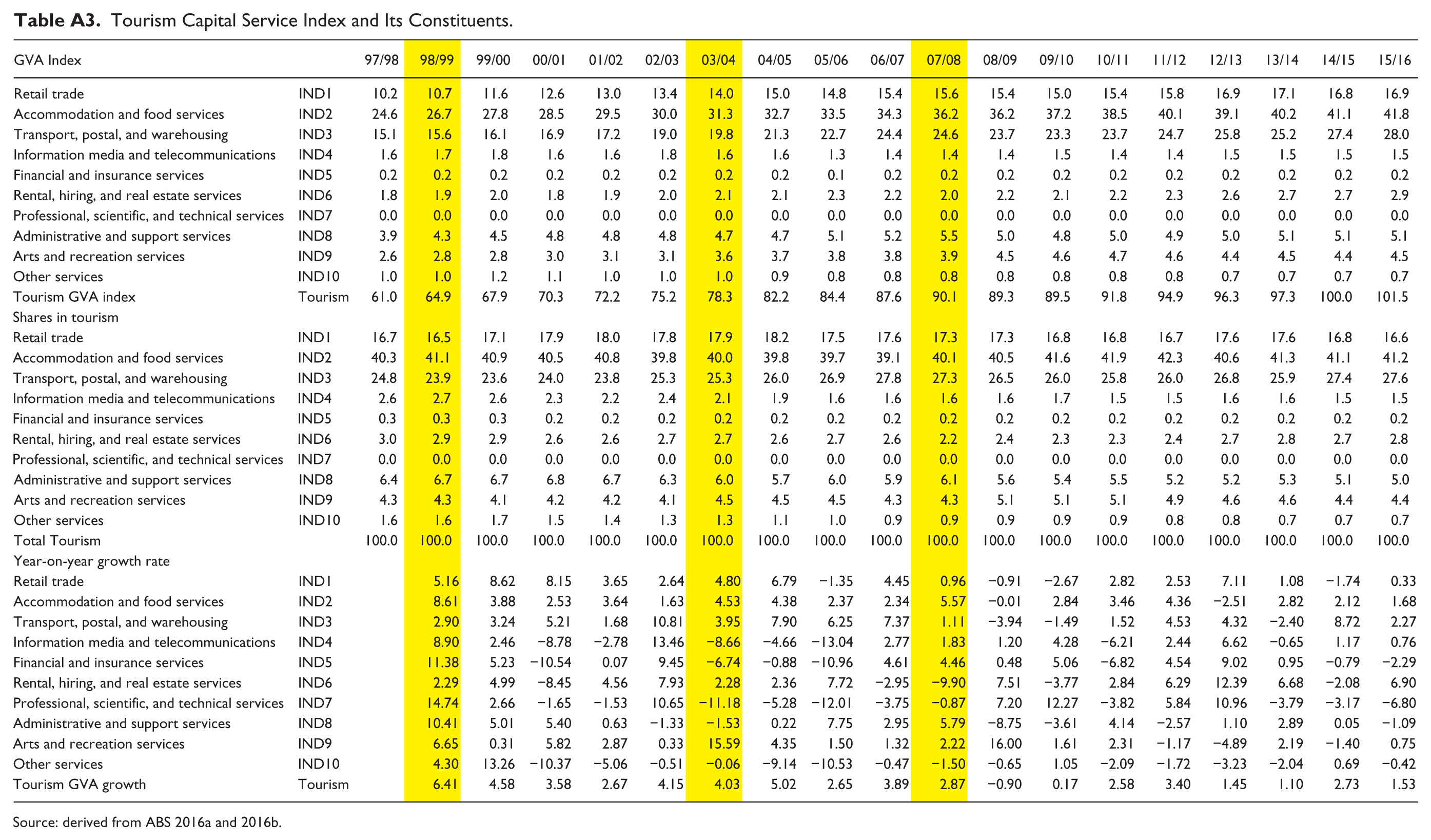

| GVA Index | 97/98 | 98/99 | 99/00 | 00/01 | 01/02 | 02/03 | 03/04 | 04/05 | 05/06 | 06/07 | 07/08 | 08/09 | 09/10 | 10/11 | 11/12 | 12/13 | 13/14 | 14/15 | 15/16 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Retail trade | IND1 | 10.2 | 10.7 | 11.6 | 12.6 | 13.0 | 13.4 | 14.0 | 15.0 | 14.8 | 15.4 | 15.6 | 15.4 | 15.0 | 15.4 | 15.8 | 16.9 | 17.1 | 16.8 | 16.9 |

| Accommodation and food services | IND2 | 24.6 | 26.7 | 27.8 | 28.5 | 29.5 | 30.0 | 31.3 | 32.7 | 33.5 | 34.3 | 36.2 | 36.2 | 37.2 | 38.5 | 40.1 | 39.1 | 40.2 | 41.1 | 41.8 |

| Transport, postal, and warehousing | IND3 | 15.1 | 15.6 | 16.1 | 16.9 | 17.2 | 19.0 | 19.8 | 21.3 | 22.7 | 24.4 | 24.6 | 23.7 | 23.3 | 23.7 | 24.7 | 25.8 | 25.2 | 27.4 | 28.0 |

| Information media and telecommunications | IND4 | 1.6 | 1.7 | 1.8 | 1.6 | 1.6 | 1.8 | 1.6 | 1.6 | 1.3 | 1.4 | 1.4 | 1.4 | 1.5 | 1.4 | 1.4 | 1.5 | 1.5 | 1.5 | 1.5 |

| Financial and insurance services | IND5 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.1 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 |

| Rental, hiring, and real estate services | IND6 | 1.8 | 1.9 | 2.0 | 1.8 | 1.9 | 2.0 | 2.1 | 2.1 | 2.3 | 2.2 | 2.0 | 2.2 | 2.1 | 2.2 | 2.3 | 2.6 | 2.7 | 2.7 | 2.9 |

| Professional, scientific, and technical services | IND7 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Administrative and support services | IND8 | 3.9 | 4.3 | 4.5 | 4.8 | 4.8 | 4.8 | 4.7 | 4.7 | 5.1 | 5.2 | 5.5 | 5.0 | 4.8 | 5.0 | 4.9 | 5.0 | 5.1 | 5.1 | 5.1 |

| Arts and recreation services | IND9 | 2.6 | 2.8 | 2.8 | 3.0 | 3.1 | 3.1 | 3.6 | 3.7 | 3.8 | 3.8 | 3.9 | 4.5 | 4.6 | 4.7 | 4.6 | 4.4 | 4.5 | 4.4 | 4.5 |

| Other services | IND10 | 1.0 | 1.0 | 1.2 | 1.1 | 1.0 | 1.0 | 1.0 | 0.9 | 0.8 | 0.8 | 0.8 | 0.8 | 0.8 | 0.8 | 0.8 | 0.7 | 0.7 | 0.7 | 0.7 |

| Tourism GVA index | Tourism | 61.0 | 64.9 | 67.9 | 70.3 | 72.2 | 75.2 | 78.3 | 82.2 | 84.4 | 87.6 | 90.1 | 89.3 | 89.5 | 91.8 | 94.9 | 96.3 | 97.3 | 100.0 | 101.5 |

| Shares in tourism | ||||||||||||||||||||

| Retail trade | IND1 | 16.7 | 16.5 | 17.1 | 17.9 | 18.0 | 17.8 | 17.9 | 18.2 | 17.5 | 17.6 | 17.3 | 17.3 | 16.8 | 16.8 | 16.7 | 17.6 | 17.6 | 16.8 | 16.6 |

| Accommodation and food services | IND2 | 40.3 | 41.1 | 40.9 | 40.5 | 40.8 | 39.8 | 40.0 | 39.8 | 39.7 | 39.1 | 40.1 | 40.5 | 41.6 | 41.9 | 42.3 | 40.6 | 41.3 | 41.1 | 41.2 |

| Transport, postal, and warehousing | IND3 | 24.8 | 23.9 | 23.6 | 24.0 | 23.8 | 25.3 | 25.3 | 26.0 | 26.9 | 27.8 | 27.3 | 26.5 | 26.0 | 25.8 | 26.0 | 26.8 | 25.9 | 27.4 | 27.6 |

| Information media and telecommunications | IND4 | 2.6 | 2.7 | 2.6 | 2.3 | 2.2 | 2.4 | 2.1 | 1.9 | 1.6 | 1.6 | 1.6 | 1.6 | 1.7 | 1.5 | 1.5 | 1.6 | 1.6 | 1.5 | 1.5 |

| Financial and insurance services | IND5 | 0.3 | 0.3 | 0.3 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 |

| Rental, hiring, and real estate services | IND6 | 3.0 | 2.9 | 2.9 | 2.6 | 2.6 | 2.7 | 2.7 | 2.6 | 2.7 | 2.6 | 2.2 | 2.4 | 2.3 | 2.3 | 2.4 | 2.7 | 2.8 | 2.7 | 2.8 |

| Professional, scientific, and technical services | IND7 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Administrative and support services | IND8 | 6.4 | 6.7 | 6.7 | 6.8 | 6.7 | 6.3 | 6.0 | 5.7 | 6.0 | 5.9 | 6.1 | 5.6 | 5.4 | 5.5 | 5.2 | 5.2 | 5.3 | 5.1 | 5.0 |

| Arts and recreation services | IND9 | 4.3 | 4.3 | 4.1 | 4.2 | 4.2 | 4.1 | 4.5 | 4.5 | 4.5 | 4.3 | 4.3 | 5.1 | 5.1 | 5.1 | 4.9 | 4.6 | 4.6 | 4.4 | 4.4 |

| Other services | IND10 | 1.6 | 1.6 | 1.7 | 1.5 | 1.4 | 1.3 | 1.3 | 1.1 | 1.0 | 0.9 | 0.9 | 0.9 | 0.9 | 0.9 | 0.8 | 0.8 | 0.7 | 0.7 | 0.7 |

| Total Tourism | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | |

| Year-on-year growth rate | ||||||||||||||||||||

| Retail trade | IND1 | 5.16 | 8.62 | 8.15 | 3.65 | 2.64 | 4.80 | 6.79 | −1.35 | 4.45 | 0.96 | −0.91 | −2.67 | 2.82 | 2.53 | 7.11 | 1.08 | −1.74 | 0.33 | |

| Accommodation and food services | IND2 | 8.61 | 3.88 | 2.53 | 3.64 | 1.63 | 4.53 | 4.38 | 2.37 | 2.34 | 5.57 | −0.01 | 2.84 | 3.46 | 4.36 | −2.51 | 2.82 | 2.12 | 1.68 | |

| Transport, postal, and warehousing | IND3 | 2.90 | 3.24 | 5.21 | 1.68 | 10.81 | 3.95 | 7.90 | 6.25 | 7.37 | 1.11 | −3.94 | −1.49 | 1.52 | 4.53 | 4.32 | −2.40 | 8.72 | 2.27 | |

| Information media and telecommunications | IND4 | 8.90 | 2.46 | −8.78 | −2.78 | 13.46 | −8.66 | −4.66 | −13.04 | 2.77 | 1.83 | 1.20 | 4.28 | −6.21 | 2.44 | 6.62 | −0.65 | 1.17 | 0.76 | |

| Financial and insurance services | IND5 | 11.38 | 5.23 | −10.54 | 0.07 | 9.45 | −6.74 | −0.88 | −10.96 | 4.61 | 4.46 | 0.48 | 5.06 | −6.82 | 4.54 | 9.02 | 0.95 | −0.79 | −2.29 | |

| Rental, hiring, and real estate services | IND6 | 2.29 | 4.99 | −8.45 | 4.56 | 7.93 | 2.28 | 2.36 | 7.72 | −2.95 | −9.90 | 7.51 | −3.77 | 2.84 | 6.29 | 12.39 | 6.68 | −2.08 | 6.90 | |

| Professional, scientific, and technical services | IND7 | 14.74 | 2.66 | −1.65 | −1.53 | 10.65 | −11.18 | −5.28 | −12.01 | −3.75 | −0.87 | 7.20 | 12.27 | −3.82 | 5.84 | 10.96 | −3.79 | −3.17 | −6.80 | |

| Administrative and support services | IND8 | 10.41 | 5.01 | 5.40 | 0.63 | −1.33 | −1.53 | 0.22 | 7.75 | 2.95 | 5.79 | −8.75 | −3.61 | 4.14 | −2.57 | 1.10 | 2.89 | 0.05 | −1.09 | |

| Arts and recreation services | IND9 | 6.65 | 0.31 | 5.82 | 2.87 | 0.33 | 15.59 | 4.35 | 1.50 | 1.32 | 2.22 | 16.00 | 1.61 | 2.31 | −1.17 | −4.89 | 2.19 | −1.40 | 0.75 | |

| Other services | IND10 | 4.30 | 13.26 | −10.37 | −5.06 | −0.51 | −0.06 | −9.14 | −10.53 | −0.47 | −1.50 | −0.65 | 1.05 | −2.09 | −1.72 | −3.23 | −2.04 | 0.69 | −0.42 | |

| Tourism GVA growth | Tourism | 6.41 | 4.58 | 3.58 | 2.67 | 4.15 | 4.03 | 5.02 | 2.65 | 3.89 | 2.87 | −0.90 | 0.17 | 2.58 | 3.40 | 1.45 | 1.10 | 2.73 | 1.53 |

Acknowledgements

The author would like to thank Professor Susanne Becken at Griffith Institute for Tourism for a strong support. Comments and feedback from three anonymous referees are greatly appreciated. Thanks are also due to Tourism Research Australia at AusTrade and the Australian Bureau of Statistics for their support of data provision. As usual, the responsibility for any errors remain with the author.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.