Abstract

Drawing on Dynamic Capabilities and Institutional theories, this paper examines how climate change exposure influences capital allocation in tourism, a spatially immobile and climate-sensitive industry. Using a global panel of 420 publicly listed tourism firms from 2001 to 2024, we employ the Least Absolute Shrinkage and Selection Operator and double-selection methods. The findings show that higher climate exposure increases capital expenditure, consistent with place-bound adaptive investment. This relationship strengthened after the Paris Agreement, underscoring the role of credible climate policy coordination. Stronger national legal institutions reinforce the relationship, whereas higher public climate awareness weakens it. Decomposing climate exposure reveals heterogeneity: opportunity and regulatory exposure increase capital expenditure, while physical exposure reduces it. These findings demonstrate how climate-related risks and opportunities reshape capital allocation in spatially immobile industries and highlight the importance of credible policy implications in encouraging long-term adaptive investment by tourism firms.

Keywords

Introduction

Climate change has emerged as one of the most pressing challenges confronting the global economy, with profound implications for political systems, human health, and long-term economic growth. Beyond these macro-level consequences, climate change increasingly shapes firm-level behavior by altering risk profiles, investment incentives, and strategic priorities (Ginglinger & Moreau, 2023; Li et al., 2024). Firms experience these effects through their exposure to climate-related risks and opportunities, commonly conceptualized as climate change exposure, which captures the extent to which climate issues affect a firm’s operations, assets, and market perceptions, as reflected in managerial discourse and investor communications (Sautner et al., 2023). While a growing body of research examines how climate risk influences firm performance and financial policy, important questions remain regarding how firms translate climate exposure into long-term capital investment decisions.

The tourism and hospitality sector provides a uniquely salient context for addressing this question. Tourism activities are inherently place-based and heavily dependent on natural and climatic conditions, rendering tourism firms especially vulnerable to rising temperatures, extreme weather events, sea-level rise, and ecosystem degradation (see, e.g., Becken & Hay, 2012; Peeters et al., 2024; Scott et al., 2019). Unlike many asset-intensive industries, tourism firms are structurally climate-embedded. Their core assets, hotels, resorts, and destination infrastructure, are geographically immobile and closely tied to local environmental quality (Akamavi et al., 2023). This immobility magnifies exposure to local climate shocks and long-term environmental degradation, limiting firms’ ability to diversify geographically or relocate production.

Moreover, tourism is an experience-based industry in which environmental conditions influence not only operational continuity but also consumer perception, destination image, and seasonal demand patterns (Steiger et al., 2024). Therefore, climate exposure in tourism operates simultaneously as a physical threat, a demand-side risk, and a reputational factor. Tourism firms are further embedded in destination ecosystems characterized by interdependence among infrastructure, local governments, and shared environmental commons. As a result, climate adaptation often requires long-term capital investments in resilient facilities, sustainable energy systems, and environmental upgrades. These sectoral characteristics suggest that tourism firms may respond to climate exposure through distinctive investment dynamics that are not fully captured by general corporate finance research.

Within tourism scholarship, climate change has been examined primarily through the lenses of destination vulnerability, demand-side impacts, and policy uncertainty. Early studies focused on how climate variability affects tourist arrivals and destination choice. More recent research has begun to explore supply-side outcomes. For example, Gozgor et al. (2022) show that geopolitical risk reduces tourism investment, consistent with Real Options theory. Gao and Zhang (2024) demonstrate that climate policy uncertainty depresses investment among U.S. tourism and hospitality firms. Together, these studies establish that external risks and uncertainty influence tourism investment behavior.

However, three important gaps remain. First, existing tourism studies focus largely on policy uncertainty or geopolitical shocks rather than on firms’ direct exposure to climate change. Second, much of the evidence relies on aggregate or country-level measures, limiting insight into firm-level strategic adaptation. Third, although tourism research acknowledges the importance of institutional context, there is a limited understanding of how formal and informal institutions condition firms’ capital investment responses to climate exposure.

This study addresses these gaps by examining how firm-level climate change exposure influences capital expenditure among global hotel and tourism firms. Drawing on the Dynamic Capabilities theory, we conceptualize firms as active agents that sense climate-related threats and opportunities, seize strategic investment possibilities, and reconfigure assets to sustain competitive advantage under environmental change (Eisenhardt & Martin, 2000; Teece, 2007). In tourism, capital expenditure represents a primary mechanism of in-situ adaptation, enabling firms to upgrade infrastructure, enhance resilience, and reposition their asset base. Unlike climate policy uncertainty, which may encourage investment delay, direct climate exposure may necessitate proactive capital allocation.

At the same time, firms’ adaptive responses unfold within institutional environments. Institutional theory emphasizes that strategic decisions are embedded in formal and informal contexts, including legal systems, regulatory frameworks, and societal expectations (North, 1990; Oliver, 1997; Peng et al., 2009). Given the long payback periods and asset specificity characteristic of tourism infrastructure, regulatory clarity and legal protection are particularly critical for climate-resilient investment. Conversely, heightened public climate awareness may intensify reputational pressures in this perception-driven industry, potentially shaping the form and magnitude of investment responses.

Importantly, we conceptualize climate change exposure as multidimensional. Rather than treating climate risk as uniformly adverse, we decompose exposure into opportunity-related, regulatory, and physical components. Transition-related pressures, such as emerging green-market opportunities and tightening regulations, may stimulate capital investment as tourism firms build adaptive capabilities. In contrast, physical climate risks may increase uncertainty regarding asset durability and destination viability, discouraging long-term investment. This distinction enables us to identify heterogeneous adaptation pathways within tourism.

Empirically, we analyze a global panel of 420 publicly listed hotel and tourism firms across 39 countries from 2001 to 2024. To address high-dimensional controls and potential endogeneity concerns, we employ the Least Absolute Shrinkage and Selection Operator (LASSO) combined with partialling-out and double-selection approaches. These methods strengthen findings while accommodating complex heterogeneity at the firm- and country-levels.

Beyond combining firm-level climate exposure with capital expenditure data in a tourism context, this study advances tourism theory in three conceptual ways. First, it reframes capital expenditure as a firm-level mechanism of destination resilience, linking corporate strategic behavior to tourism adaptation scholarship. Second, it introduces the notion of place-bound adaptation logic, emphasizing that tourism firms’ spatial immobility fundamentally shapes their responses to climate exposure. Third, by decomposing exposure into opportunity, regulatory, and physical dimensions, the study reveals bifurcated adaptation pathways in tourism, where transition-related exposures stimulate investment while physical risks suppress it. These insights extend tourism research beyond aggregate vulnerability assessments and illuminate the micro-foundations of climate resilience in experience-based industries.

Theoretical Background and Hypotheses Development

Tourism Vulnerability and Firm-Level Climate Adaptation

Tourism scholarship has long emphasized the sector’s vulnerability to environmental change. Research on destination resilience, climate vulnerability, and sustainable tourism development highlights the structural dependence of tourism systems on environmental stability (Scott et al., 2019;Scott & Gössling, 2022). However, much of this literature operates at the macro or destination level, focusing on aggregate impacts rather than on how individual tourism firms strategically respond to climate pressures. Bridging destination resilience research with firm-level strategic management requires examining how tourism firms adjust their capital allocation decisions in response to climate exposure.

Tourism firms are structurally climate-embedded. Their core assets, hotels, resorts, transportation facilities, and recreational infrastructure, are geographically immobile and directly tied to local environmental conditions. Unlike firms in industries where production can be geographically diversified, tourism firms cannot easily relocate in response to climate shocks. Therefore, climate change affects not only operational continuity but also destination attractiveness, seasonality patterns, and visitor perceptions. This combination of asset immobility, demand sensitivity, and destination interdependence renders tourism firms theoretically distinct in both their exposure and their strategic responses to environmental risk stability (Scott et al., 2019;Scott & Gössling, 2022).

Because tourism assets are place-bound and long-lived, climate adaptation often requires in-situ capital-intensive adjustments. Infrastructure retrofitting, energy-efficiency upgrades, structural reinforcement, and environmentally adaptive redesign represent concrete mechanisms through which tourism firms seek to preserve asset viability and maintain destination competitiveness. These characteristics suggest that capital expenditure in tourism can be understood as a firm-level mechanism of climate adaptation rather than merely a routine investment decision.

Climate Change Exposure and Capital Investment Behavior

The broader literature on climate change exposure provides mixed expectations regarding firms’ investment responses. One stream emphasizes adverse financial effects, documenting negative impacts on firm value (Hoang et al., 2025) and shareholder wealth (Sarajoti et al., 2026), suggesting that heightened climate-related risks erode financial performance. Another stream highlights the transformative potential of climate exposure, arguing that it can catalyze organizational change, strengthen corporate culture (Treepongkaruna et al., 2024), and enhance engagement in social responsibility (Mbanyele & Muchenje, 2022).

Related research has examined how climate risk affects firms’ financial policies, particularly capital structure and investment behavior. Ginglinger and Moreau (2023) show that greater physical climate risk is associated with lower leverage ratios, reflecting attempts to reduce financial vulnerability. Agoraki et al. (2024) find that climate exposure increases financing costs and reduces investment activity. In tourism contexts, Arian et al. (2026) report that heightened climate risk induces more conservative financial strategies and lower capital expenditure in emerging markets.

While informative, much of this literature conceptualizes climate risk through a financial economics lens, emphasizing retrenchment and financial constraint. However, this perspective may not fully capture the strategic realities of tourism firms. Given the sector’s asset immobility and environmental dependence, tourism firms cannot easily hedge or geographically diversify away from localized climate shocks. Instead, they may respond by reallocating resources toward adaptive investment.

In addition, the capital expenditure measure used in this paper captures overall firm-level investment rather than climate-specific spending categories. In publicly available financial statements, climate adaptation expenditures are typically embedded within broader capital budgets and are not separately disclosed. Therefore, we conceptualize capital expenditure as an aggregate indicator of the intensity of strategic capital reallocation. If climate exposure is economically meaningful, it should influence firms’ overall capital allocation decisions, even if adaptation-related spending is not itemized. Thus, the empirical test examines whether climate exposure is systematically associated with shifts in aggregate capital intensity rather than narrowly defined climate-designated projects.

The Dynamic Capabilities theory provides a useful theoretical lens. Firms are seen as proactive actors capable of sensing environmental change, seizing emerging opportunities, and reconfiguring resources to sustain competitiveness (Eisenhardt & Martin, 2000; Teece, 2007). In tourism, capital investment decisions represent concrete manifestations of these adaptive capabilities. By upgrading infrastructure and adopting resilient technologies, firms operate their strategic response to climate exposure.

Taken together, tourism’s structural characteristics and the Dynamic Capabilities theory suggest that climate change exposure may stimulate capital-intensive adaptation rather than pure financial retrenchment. However, this expectation is not universal across industries. In sectors where assets can be geographically redeployed, firms may respond to climate risk by relocating, diversifying, or engaging in financial hedging. In contrast, tourism firms operate under spatial immobility and destination dependence, where core assets cannot be easily relocated without undermining value creation.

This structural constraint implies that adaptive reconfiguration in tourism manifests primarily through in-situ capital intensification and asset upgrading rather than geographic repositioning. Therefore, climate exposure activates a place-bound adaptation mechanism specific to climate-embedded industries. In this sense, H1 does not merely test a general climate–investment association but evaluates whether climate exposure translates into structural capital reallocation under spatial immobility constraints:

Heterogeneous Channels of Climate Exposure

Climate change exposure is multidimensional, and it may arise from distinct sources with different strategic implications. Following Sautner et al. (2023), we distinguish between opportunity-related exposure, regulatory exposure, and physical exposure.

Opportunity-related exposure reflects discussions of emerging green markets, renewable energy adoption, and sustainability-oriented innovation. Such exposure may signal strategic growth pathways and encourage firms to invest in asset upgrading to capture transition-related opportunities. From a Dynamic Capabilities theory, opportunity exposure activates sensing and seizing mechanisms that translate into capital intensification.

Regulatory exposure reflects attention to environmental regulation, carbon pricing, and compliance requirements. In asset-intensive industries such as tourism, regulatory tightening may necessitate structural capital upgrading to maintain operational legitimacy and avoid penalties. Therefore, regulatory exposure is also expected to stimulate capital expenditure.

In contrast, physical exposure reflects discussions about extreme weather, sea-level rise, temperature volatility, and environmental degradation. For tourism firms operating under spatial immobility, heightened physical exposure may increase uncertainty regarding asset durability and long-term return horizons. Under such conditions, firms may adopt a more cautious investment posture to preserve liquidity and flexibility.

Thus, while aggregate climate exposure may be positively associated with capital expenditure, the underlying channels may operate in opposite directions. Distinguishing among these dimensions allows us to reconcile mixed findings in the broader climate-investment literature and provides a more nuanced understanding of adaptation dynamics in tourism. Because opportunity and regulatory exposures reflect transition dynamics, whereas physical exposure reflects asset vulnerability, the net association in H1 reflects the combined influence of heterogeneous channels.

Institutional Conditioning of Climate Adaptation in Tourism

While climate exposure may incentivize adaptive investment, its effect is unlikely to be uniform across institutional contexts. Institutional theory emphasizes that strategic decisions are embedded in formal and informal environments that shape both constraints and incentives (North, 1990; Oliver, 1997; Peng et al., 2009). In tourism, where investments are long-term and highly specific, institutional quality may be particularly consequential.

Formal Institutions: Legal Credibility and Investment Certainty

While climate change exposure may incentivize adaptive investment, the credibility and enforceability of the institutional environment shape whether firms translate exposure into long-term capital commitments. Rather than whether developed legal systems are inherently pro-climate, we conceptualize the strength of the legal environment as a source of institutional credibility and investment.

Tourism infrastructure is characterized by high asset specificity, long payback periods, and high sunk costs. Under such conditions, firms face heightened vulnerability to regulatory unpredictability, contract disputes, and policy reversal. A well-developed legal system enhances contract enforcement, protects property rights, constrains arbitrary administrative actions, and provides credible dispute resolution mechanisms (North, 1990; Oliver, 1997; Peng et al., 2009). These features reduce institutional uncertainty surrounding long-term capital allocation decisions.

Importantly, the development of the legal system does not necessarily imply a pro-climate political orientation. However, even in politically volatile environments, strong legal institutions can provide procedural stability and protect investors from abrupt, non-credible policy implementation. For asset-intensive tourism firms, such institutional reliability is particularly important when undertaking climate-related infrastructure investments that are difficult to reverse or relocate. Thus, we argue that the strength of the legal environment moderates the climate exposure–investment relationship not because it signals climate-friendly ideology, but because it enhances the credibility of long-term capital commitments under environmental uncertainty. Accordingly:

Informal Institutions: Public Climate Awareness and Adaptive Trade-offs

Informal institutional pressures shape corporate behavior through legitimacy expectations, social norms, and stakeholder scrutiny (Bansal & Roth, 2000; Dhir et al., 2025; DiMaggio & Powell, 1983). Public climate awareness reflects the extent to which climate change is socially salient and prioritized within a country. Unlike formal institutions, which influence investment through regulatory credibility, informal pressures operate through reputational and normative channels.

In tourism, these pressures may have distinct strategic implications. Tourism firms are highly sensitive to destination image, brand perception, and consumer sentiment. Heightened public climate awareness increases reputational scrutiny and short-term stakeholder expectations. Under such conditions, managers may prioritize actions that are immediately visible and legitimacy-enhancing, such as sustainability certifications, eco-labeling, public commitments, or marketing-oriented environmental initiatives.

Importantly, this argument does not assume a purely mechanical zero-sum allocation of financial resources. Rather, it reflects managerial attention constraints and temporal trade-offs in strategic prioritization. Capital expenditure in tourism involves long planning horizons, irreversible sunk costs, and delayed performance realization. In contrast, symbolic or communication-based initiatives can generate immediate reputational benefits at lower levels of commitment. When informal climate pressure intensifies, firms may allocate managerial attention and short-term resources toward legitimacy-preserving activities, thereby reducing the marginal propensity to commit to large-scale, irreversible capital investments.

Moreover, heightened public awareness may amplify uncertainty regarding stakeholder expectations and future regulatory trajectories. In perception-sensitive industries such as tourism, firms facing intense scrutiny may adopt a cautious posture toward long-term capital commitments, particularly when such investments cannot be rapidly adjusted. Thus, informal institutional pressure may reshape the form and timing of adaptation rather than uniformly increasing structural investment.

Accordingly, we propose that while climate change exposure generally encourages adaptive investment, higher levels of public climate awareness moderate this relationship by weakening the translation of exposure into capital expenditure:

Taken together, the proposed hypotheses form an integrated framework linking climate exposure to capital allocation in a place-bound service industry. H1 examines whether climate exposure activates capital intensification under spatial immobility constraints. H2 and H3 specify how formal and informal institutional environments condition this translation mechanism through distinct channels, legal credibility, and legitimacy pressure. Finally, decomposing exposure into opportunity, regulatory, and physical dimensions refines this framework by distinguishing transition-driven adaptation from asset-vulnerability-induced caution. This structured theoretical architecture ensures alignment between constructs, mechanisms, and empirical tests.

Data and Methodology

Data

We use a sample using firm-level data from the Compustat North America and Compustat Global databases. Following Lyssimachou and Bilinski (2023), hotel and tourism firms are identified based on their North American Industry Classification System codes, yielding an initial sample of 2,251 firms. This sample was then merged with firm-level climate change exposure data from Sautner et al. (2025). The final matched sample comprises 420 firms and 3,840 firm-year observations in 39 countries, covering the period from 2001 to 2024. Online Appendix Table A1 lists the country-level distribution of sample firms and observations.

All firm-level financial variables are obtained from Compustat and are winsorized at the 1% level to mitigate the influence of outliers. Country-level macroeconomic variables are collected from the World Bank (2026). To reduce heteroskedasticity and improve normality, all continuous variables are transformed using natural logarithms where appropriate.

Dependent Variable: Capital Expenditures

Following Gustafson and Kotter (2023), capital expenditure is measured as capital expenditures scaled by total assets. 1 This ratio captures the intensity of firms’ long-term investment decisions. To ensure comparability and consistency across firms, capital expenditure, cash flow from operations, and research and development expenditure are all scaled by total assets. Using total assets as the scaling variable is consistent with prior studies examining corporate investment behavior (Sarajoti et al., 2026).

Main Variable of Interest: Climate Exposure Measures

Our primary independent variable, Climate Change Exposure, is obtained from the climate exposure dataset developed by Sautner et al. (2023) and updated by Sautner et al. (2025). The dataset is constructed using textual analysis of quarterly earnings call transcripts for publicly listed firms. It is designed to capture financially salient climate-related exposure as reflected in analyst–management discussions.

The underlying transcripts are sourced from the London Stock Exchange Group (LSEG) (formerly Refinitiv) earnings call databases. The construction procedure follows a dictionary-based textual analysis approach. Specifically, the methodology identifies climate-related terms using a predefined lexicon that captures three distinct dimensions of climate exposure: (a) Physical climate risk exposure (e.g., extreme weather events, flooding, temperature shifts), (b) Regulatory climate exposure (e.g., carbon taxes, environmental regulation, emissions policy), (c) Opportunity-related exposure (e.g., renewable energy, green innovation, transition opportunities).

Each earnings call transcript is parsed at the sentence level. Sentences containing climate-related keywords are identified and classified into the corresponding exposure category using the structured dictionary provided by Sautner et al. (2023). The exposure measure is constructed as the frequency of climate-related terms relative to total transcript length, thereby normalizing for call size and verbosity.

We use the August 21, 2025, version of the Sautner et al. (2025) climate exposure dataset. To enhance coefficient interpretability, the exposure indices are multiplied by 10. This linear rescaling does not affect statistical inference or model fit but allows estimated coefficients to be interpreted in economically meaningful units.

It is also important to note that the exposure measure captures financially salient climate exposure as reflected in analyst–management discussion, rather than purely objective physical climate risk. This attention-based measure is theoretically appropriate in our setting because corporate capital allocation decisions respond to managerial perceptions, investor scrutiny, and the salience of financially material risk. Nevertheless, we acknowledge that the measure may partially reflect disclosure dynamics, and we address this concern through lag structures, fixed effects, and quasi-experimental designs in our robustness analyses. 2

Control Variables

Following Ginglinger and Moreau (2023), Huang et al. (2018), and Li et al. (2024), we include a comprehensive set of firm-level and country-level control variables. First, we control for firm financial characteristics that influence investment capacity and financing constraints. These include market valuation (Tobin’s Q), cash flow from operations (CFO), firm age (Age), interest coverage ratio (Coverage), Market leverage (Leverage), and firm size (Size). Larger firms typically have greater internal resources and easier access to external financing, which facilitates capital expenditure. Conversely, highly leveraged firms may reduce investment to preserve financial flexibility. Controlling these factors ensures that underlying financing conditions do not confound the estimated effect of climate exposure.

Second, we include growth and operational controls, such as R&D expenditure (R&D) and tangible asset ratio (PPR), which capture investment opportunities and operational dynamics. Firms experiencing strong R&D expenditure and PPR may increase capital expenditure independently of climate exposure. Including these variables allows us to distinguish climate-driven adaptation from general expansionary investment behavior.

Third, we account for macro- and country-level factors that may influence capital allocation decisions, including gross domestic product growth (GDPG), per capita GDP (PGDP), and country size (measured by population density-POPD). These controls capture broader economic conditions and country size that shape investment incentives across tourism markets. 3

Moderating Variables

To test the moderating hypotheses (H2 and H3), we proxy formal and informal institutional environments using a country’s legal environment and public climate awareness, respectively.

Following Huang et al. (2018), the legal environment (LEGAL) is constructed using principal component analysis based on three indicators: the legal origin of the system, law enforcement effectiveness, and creditor rights. Legal origin (COMMON) refers to whether a country follows a common-law system, which is generally associated with stronger investor protection and a more developed legal environment than civil-law systems (Beck et al., 2003). Law enforcement effectiveness (ENFORCE) is measured using the Fraser Institute’s (2025) dataset, with higher values indicating stronger judicial capacity and enforcement quality. Creditor rights (CR) are obtained from Djankov et al. (2007) and reflect the degree of legal protection afforded to creditors in bankruptcy and reorganization proceedings, with higher values indicating stronger protection. A higher composite legal environment score, therefore, reflects a more developed and effective formal institutional framework (Porta et al., 2008).

Public climate awareness (PCA) is also proxied using the Google Search Volume Index (Choi et al., 2020). Data are obtained from Google Trends and measure the relative frequency of searches for the keyword “global warming” at the country level. Monthly search volume data are collected for each country and aggregated to annual averages to construct a country-year panel. The index ranges from 0 to 100, with higher values indicating greater public attention to and awareness of climate change.

Definitions of all variables are reported in Supplemental Appendix Table A2. In addition, Supplemental Appendix Table A3 presents summary statistics for the full sample. Capital expenditure ranges from 0 to 0.242. The mean value of climate change exposure exceeds the median, indicating a right-skewed distribution.

Estimation Strategy

Empirical Model

To test H1, we estimate the following baseline econometric model:

where

Specifications of LASSO Models

Given that traditional econometric models often suffer from overfitting and estimation bias, a common approach is to reduce the number of explanatory variables to mitigate these issues. However, this may lead to omitted variable bias. Therefore, we employ LASSO-based selection models, including Standard LASSO, Adaptive LASSO, and Elasticnet, for feature selection and regularization. The variables selected through these procedures are then incorporated into the baseline regression, Partialling-out Linear Regression (POLR), and Double-selection Linear Regression (DSLR) methods.

Subtracting Equation 2 from Equation 1 yields:

This transformation removes the influence of control variables on both the dependent and independent variables, allowing the coefficient α1 to be consistently estimated through regression on the residuals. Since the conditional expectations

Finally, the residual regression is performed as:

In this specification, α1 denotes the net effect of climate change exposure (CCE) on capital investments, controlling for all control variables.

To address this issue, the DSLR adopts the idea of “two selections and one estimation.” Specifically, the first LASSO regression identifies control variables that are strongly predictive of

It is important to note that although LASSO-based selection, fixed effects, Propensity Score Matching (PSM), and quasi-natural experiments strengthen inference, the analysis cannot fully eliminate all sources of endogeneity, such as time-varying unobservables or strategic disclosure behavior.

Empirical Results

Baseline Results

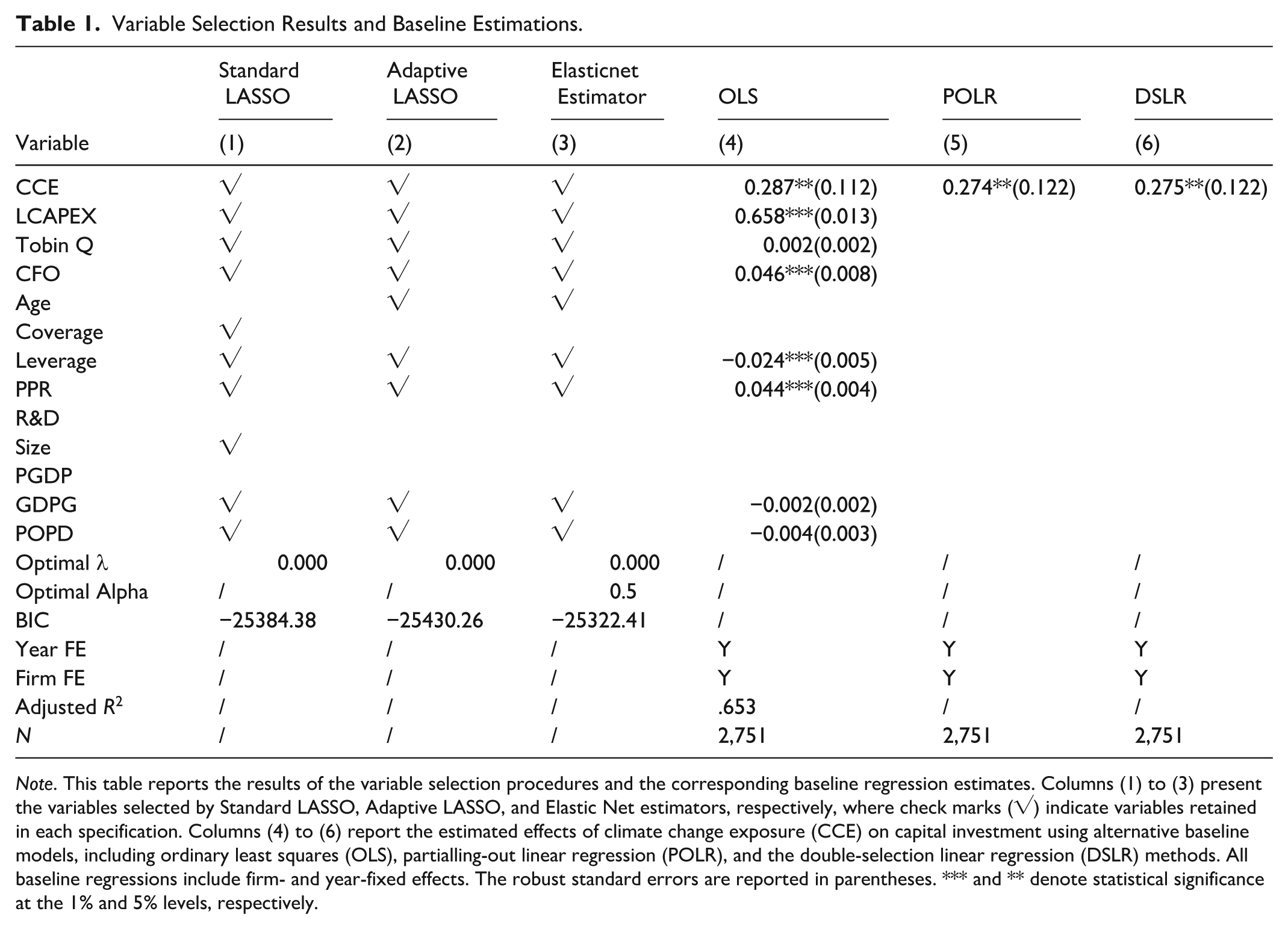

Before estimating the baseline models, we conduct variable selection, with the results reported in Columns (1) to (3) of Table 1. Following the selection criterion, only control variables consistently selected by the Standard LASSO, Adaptive LASSO, and ElasticNet estimators are retained. Consequently, the final set of controls includes all firm-level variables and country-level variables.

Variable Selection Results and Baseline Estimations.

Note. This table reports the results of the variable selection procedures and the corresponding baseline regression estimates. Columns (1) to (3) present the variables selected by Standard LASSO, Adaptive LASSO, and Elastic Net estimators, respectively, where check marks (√) indicate variables retained in each specification. Columns (4) to (6) report the estimated effects of climate change exposure (CCE) on capital investment using alternative baseline models, including ordinary least squares (OLS), partialling-out linear regression (POLR), and the double-selection linear regression (DSLR) methods. All baseline regressions include firm- and year-fixed effects. The robust standard errors are reported in parentheses. *** and ** denote statistical significance at the 1% and 5% levels, respectively.

Lower Bayesian Information Criteria (BIC) values suggest improved model fit relative to alternative specifications. Accordingly, the variable selection results are considered credible.

The OLS estimates are reported in Column (4) of Table 1, while Columns (5) and (6) present the results from the POLR and the DSLR models, respectively. Across all specifications, the coefficient on climate change exposure is positive and statistically significant. Specifically, a one-unit increase in climate change exposure is associated with a 0.27 percentage-point increase in firm-level capital investment, significant at the 5% level, thus supporting H1. Among the three specifications, we adopt the POLR model as the primary baseline for subsequent analyses, as it allows for greater control over potential confounding factors and is less susceptible to model misspecification than the DSLR model.

Robustness Checks of the Baseline Results

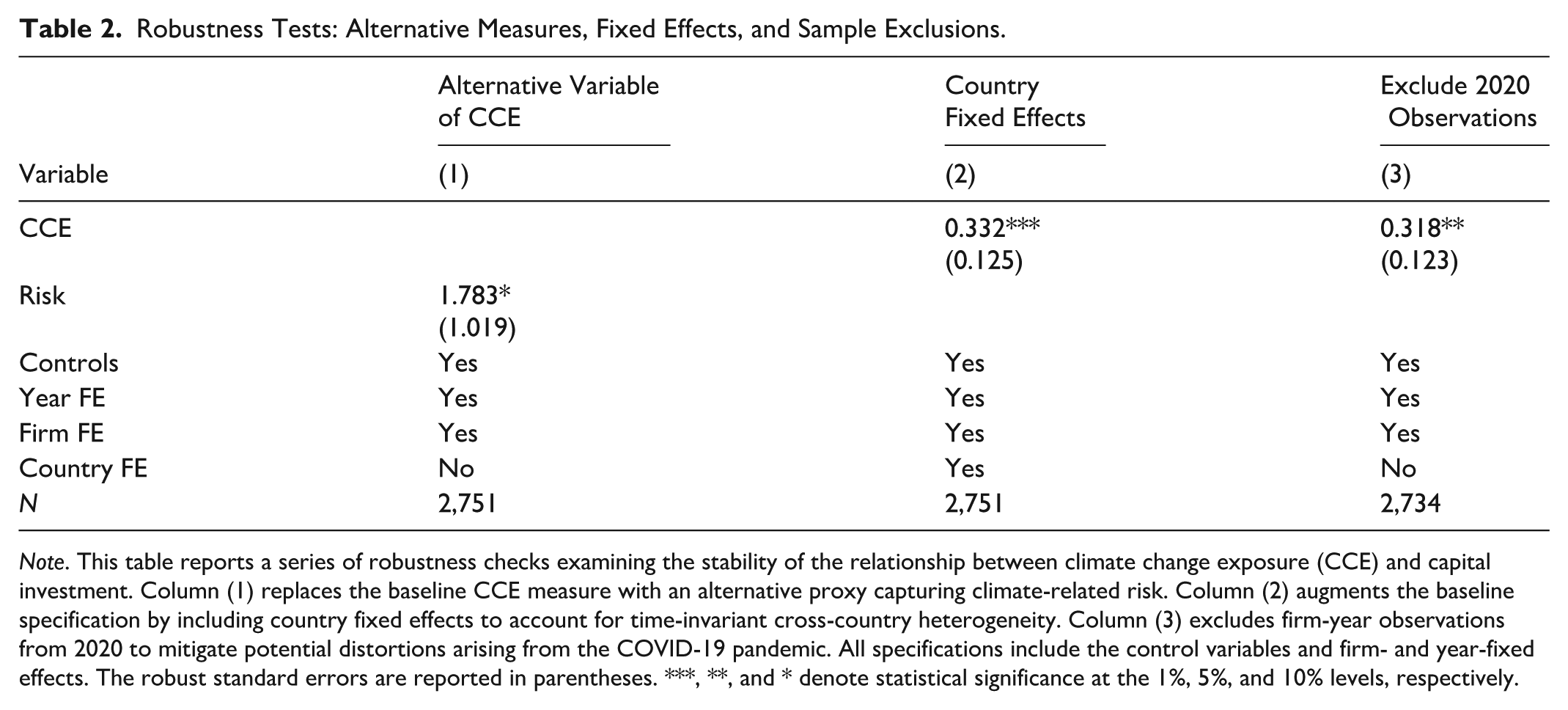

We perform a series of robustness checks, with the results reported in Table 2. First, we replace the climate change exposure measure with the climate change risk (Risk) index developed by Sautner et al. (2023); the corresponding results are presented in Column (1). Second, we incorporate country fixed effects to control for time-invariant cross-country heterogeneity and report the results in Column (2). Third, to account for the potential impact of the COVID-19 pandemic, we exclude observations in 2020, and the results are shown in Column (3).

Robustness Tests: Alternative Measures, Fixed Effects, and Sample Exclusions.

Note. This table reports a series of robustness checks examining the stability of the relationship between climate change exposure (CCE) and capital investment. Column (1) replaces the baseline CCE measure with an alternative proxy capturing climate-related risk. Column (2) augments the baseline specification by including country fixed effects to account for time-invariant cross-country heterogeneity. Column (3) excludes firm-year observations from 2020 to mitigate potential distortions arising from the COVID-19 pandemic. All specifications include the control variables and firm- and year-fixed effects. The robust standard errors are reported in parentheses. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively.

Across all specifications in robustness checks, the coefficient on climate change exposure (and climate risk) remains positive and statistically significant, thereby confirming the robustness of the baseline findings.

PSM Results

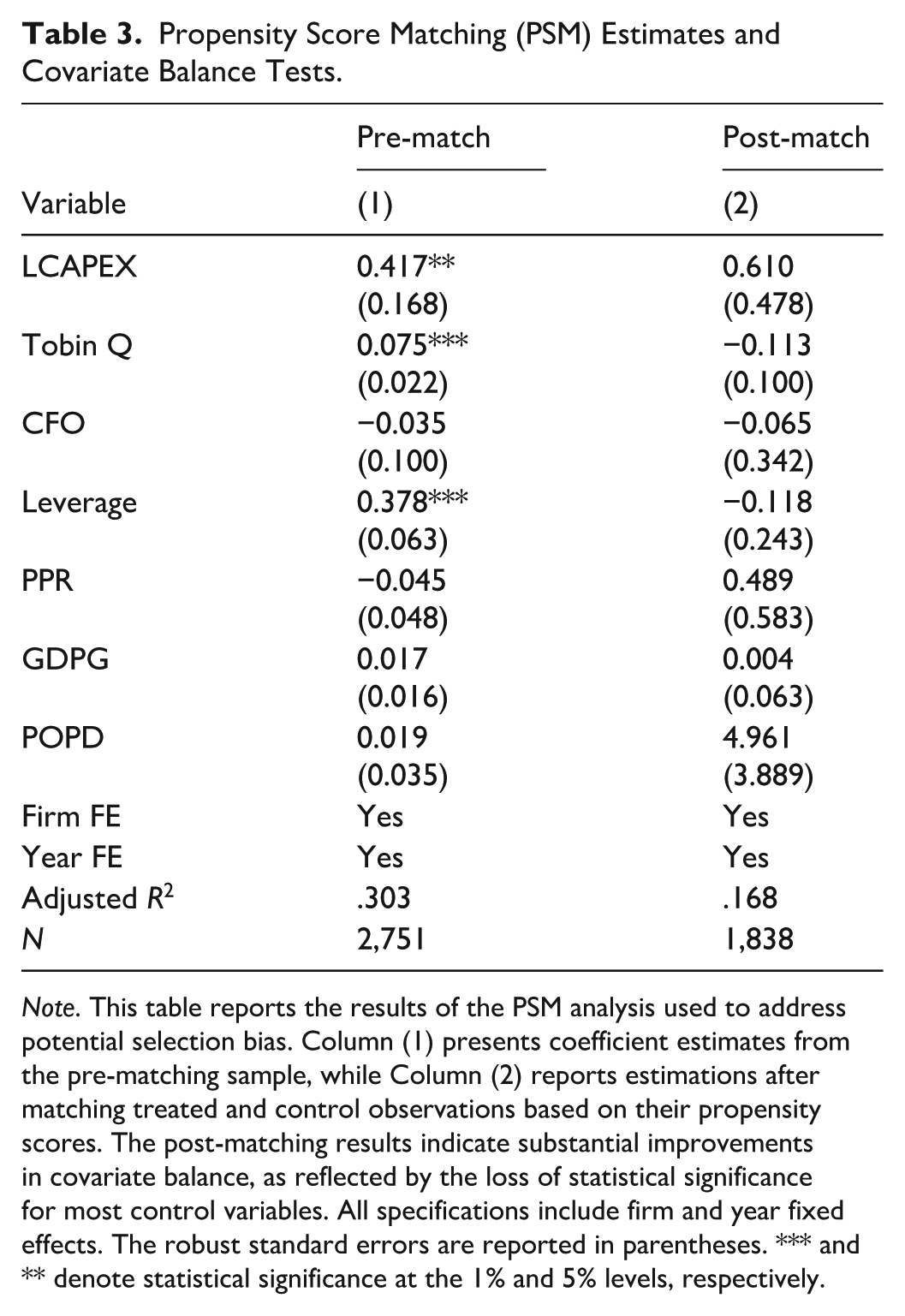

We also employ a PSM approach to mitigate potential sample selection bias arising from the non-random distribution of firms’ climate change exposure. Firms may face heterogeneous climate change exposure due to differences in geographic location and host-country regulatory environments. Accordingly, this section applies a matching framework to evaluate the impact of climate change exposure on firms’ capital investments. Specifically, firms with available climate change exposure values are classified as the treatment group. Firms without recorded climate change exposure values are assigned to the control group, indicating that they are not identified as exposed to or involved in climate-related risks. We implement a one-to-one nearest-neighbor matching procedure with replacement to enhance comparability between the two groups. Matching is based on a comprehensive set of firm- and country-level characteristics, including Tobin’s Q, cash flow, market leverage, GDP growth rate, and the legal environment.

Table 3 reports the PSM results along with the associated balance tests. Column (1) shows that several firm characteristics, such as lagged CAPEX, Tobin’s Q, and Leverage, differ significantly between the treatment and control groups prior to matching, suggesting that firms exposed to higher climate risk systematically differ in size, financial structure, and operating characteristics.

Propensity Score Matching (PSM) Estimates and Covariate Balance Tests.

Note. This table reports the results of the PSM analysis used to address potential selection bias. Column (1) presents coefficient estimates from the pre-matching sample, while Column (2) reports estimations after matching treated and control observations based on their propensity scores. The post-matching results indicate substantial improvements in covariate balance, as reflected by the loss of statistical significance for most control variables. All specifications include firm and year fixed effects. The robust standard errors are reported in parentheses. *** and ** denote statistical significance at the 1% and 5% levels, respectively.

After matching, as shown in Column (2) in Table 3, these covariates are no longer statistically different between the two groups, indicating that observable differences have been effectively eliminated. This result confirms that the PSM procedure substantially improves covariate balance and enhances comparability between treated and control firms.

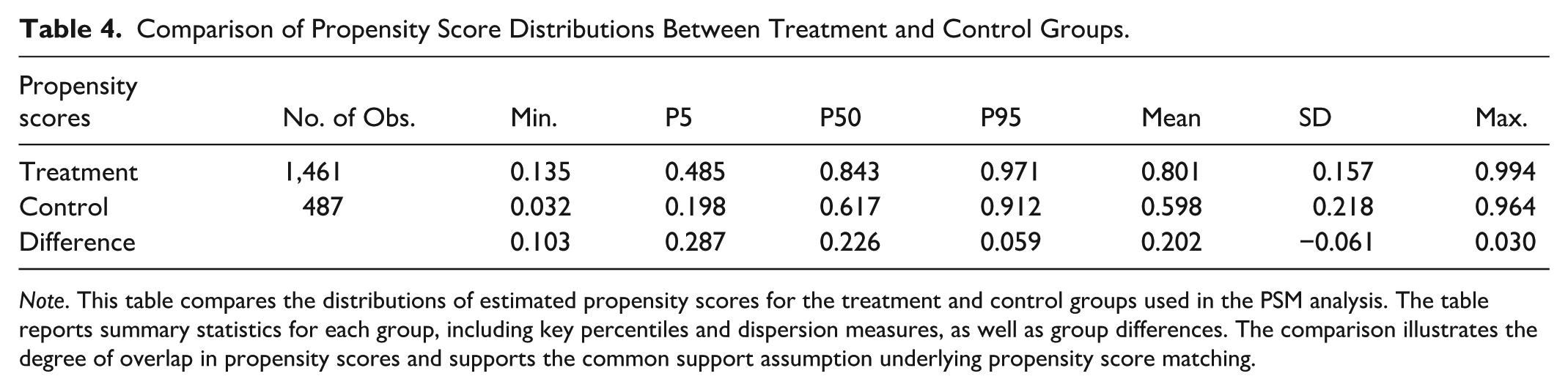

Table 4 also presents the distributional characteristics of the propensity scores for the treatment and control groups. The minimum and the maximum propensity score differences are very small, indicating that the matched propensity score distributions across the two groups are highly similar.

Comparison of Propensity Score Distributions Between Treatment and Control Groups.

Note. This table compares the distributions of estimated propensity scores for the treatment and control groups used in the PSM analysis. The table reports summary statistics for each group, including key percentiles and dispersion measures, as well as group differences. The comparison illustrates the degree of overlap in propensity scores and supports the common support assumption underlying propensity score matching.

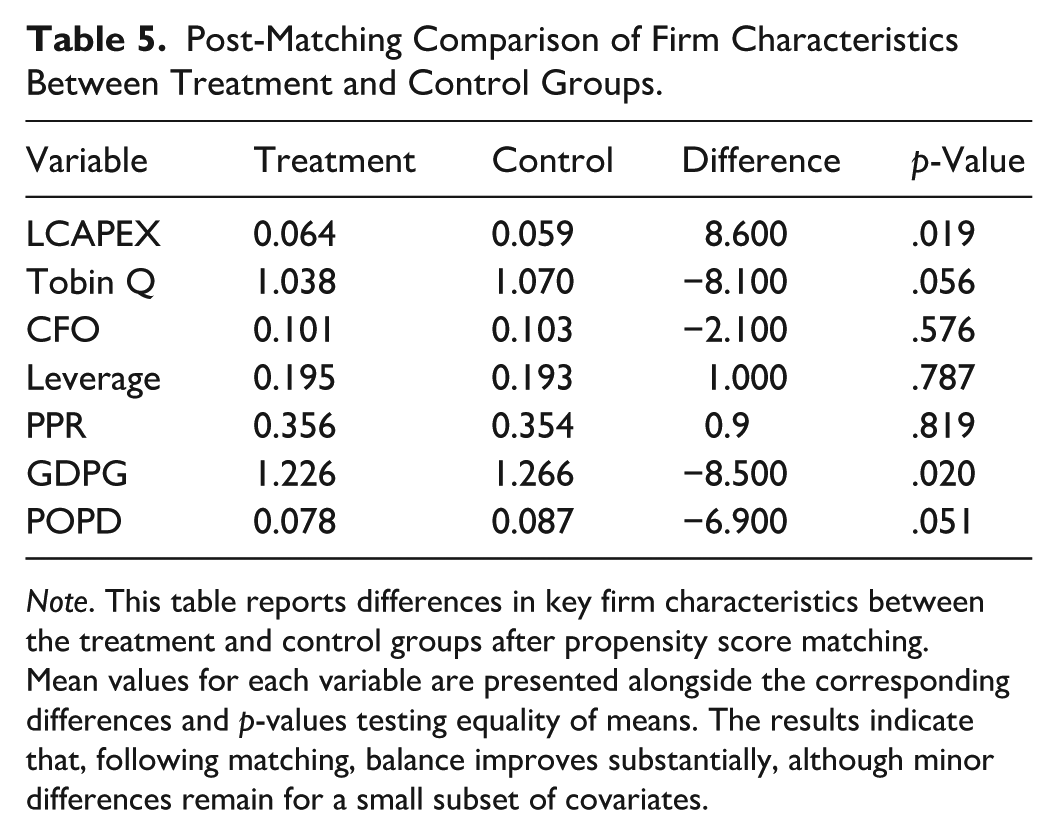

Table 5 reports the mean differences in firm characteristics between the treatment and control groups after matching. Most covariates exhibit small differences, with standardized biases below 10%, and none of the associated p-values are statistically significant. These results suggest that observable differences in key covariates have been effectively minimized, resulting in a well-balanced matched sample.

Post-Matching Comparison of Firm Characteristics Between Treatment and Control Groups.

Note. This table reports differences in key firm characteristics between the treatment and control groups after propensity score matching. Mean values for each variable are presented alongside the corresponding differences and p-values testing equality of means. The results indicate that, following matching, balance improves substantially, although minor differences remain for a small subset of covariates.

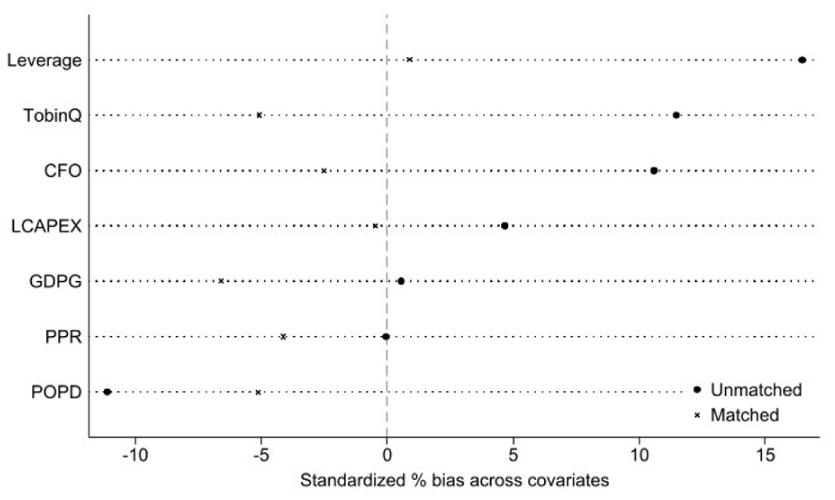

In addition, Figure 1 illustrates the standardized biases for all covariates before and after matching. The post-matching biases are substantially closer to zero across all variables, further confirming the effectiveness of the matching procedure.

Standardized mean differences before and after propensity score matching (PSM).

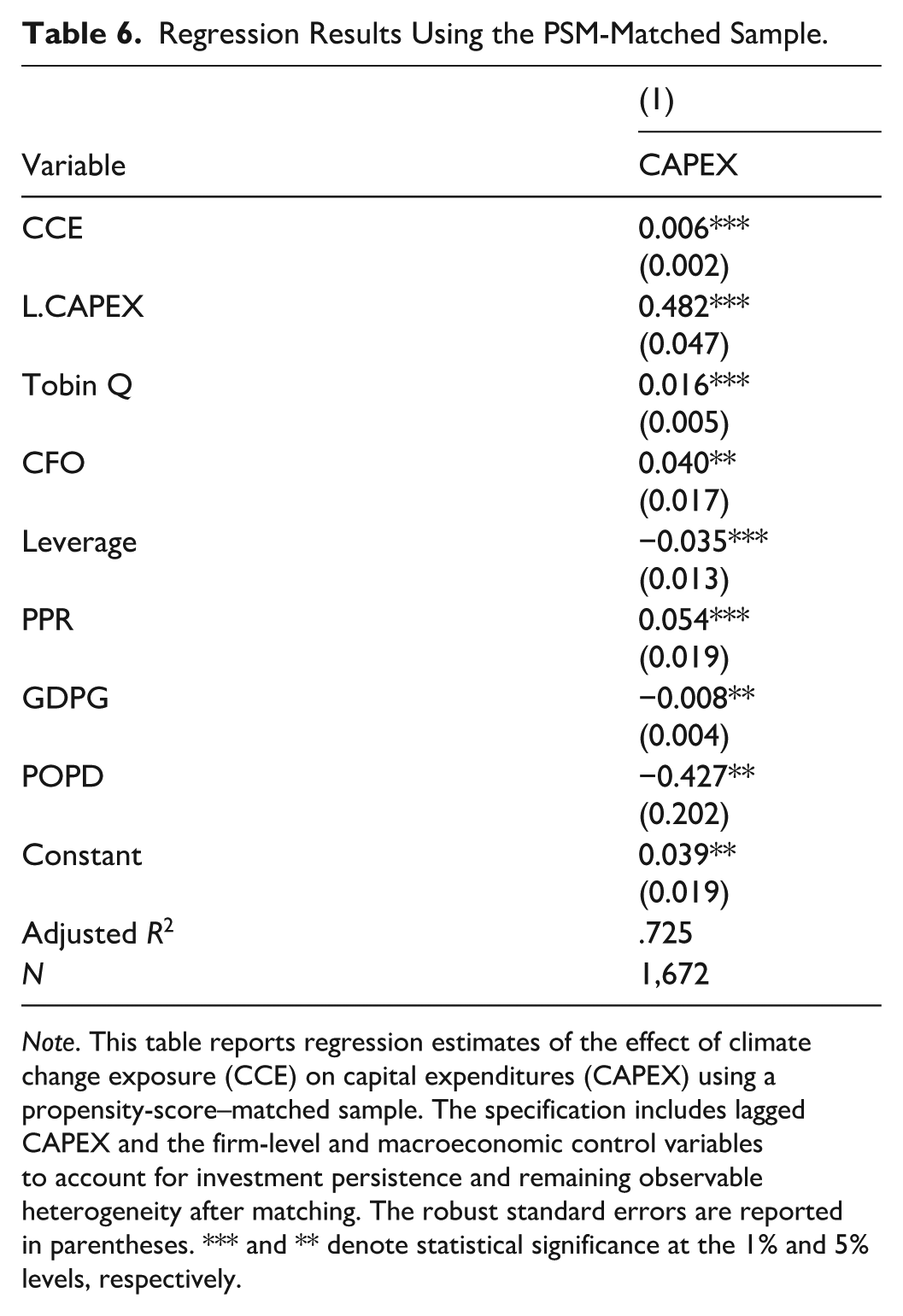

Finally, Table 6 presents the regression results for the PSM-matched sample. The coefficient on climate change exposure remains positive and statistically significant at the 1% level, indicating that firms with higher climate change exposure continue to increase their capital expenditure even after accounting for potential sample selection bias. This evidence further corroborates the robustness of the main findings.

Regression Results Using the PSM-Matched Sample.

Note. This table reports regression estimates of the effect of climate change exposure (CCE) on capital expenditures (CAPEX) using a propensity-score–matched sample. The specification includes lagged CAPEX and the firm-level and macroeconomic control variables to account for investment persistence and remaining observable heterogeneity after matching. The robust standard errors are reported in parentheses. *** and ** denote statistical significance at the 1% and 5% levels, respectively.

A Quasi-Natural Experiment: The Paris Agreement and the Stern Review

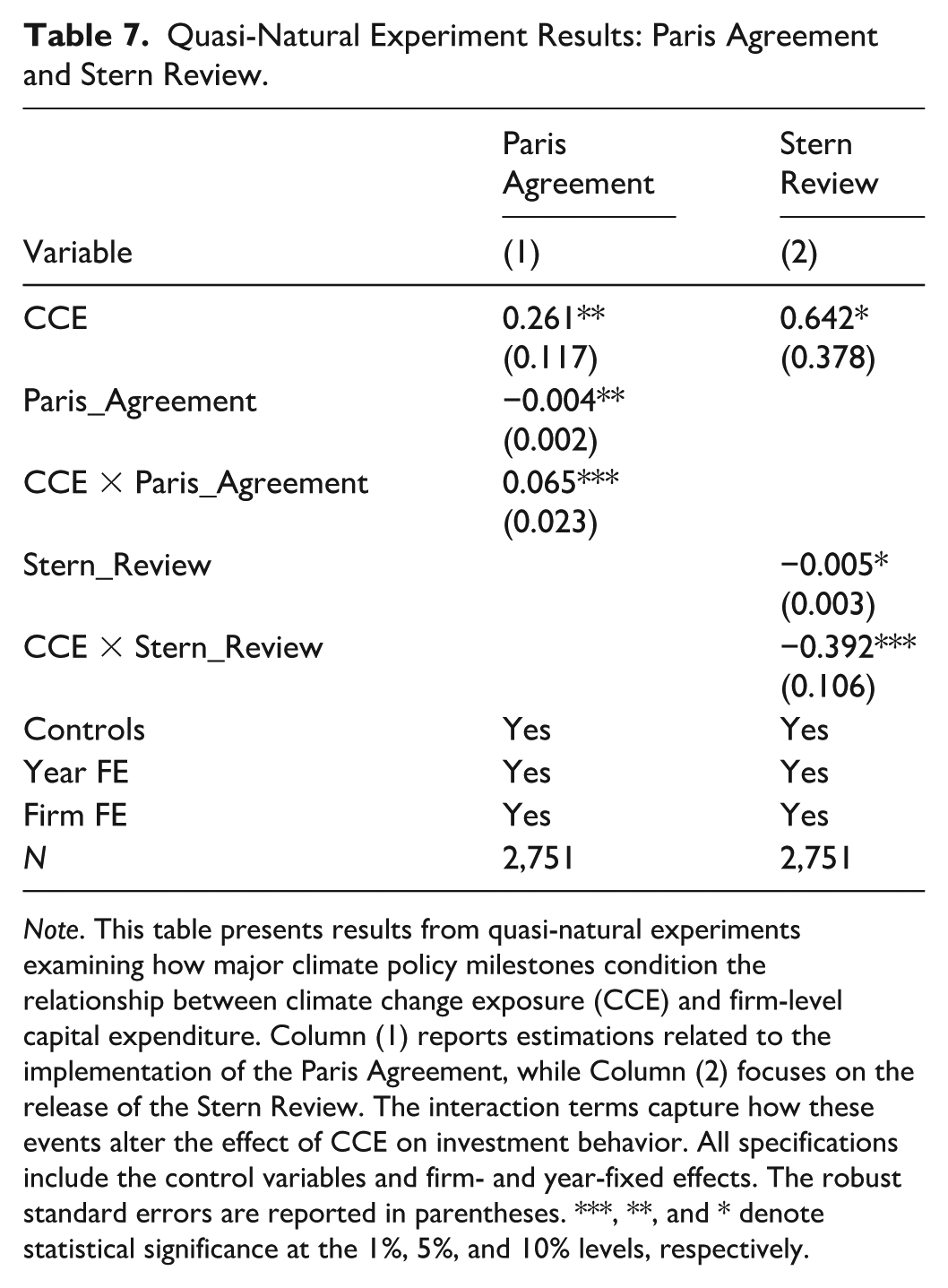

To strengthen identification, we exploit two major climate-related events as quasi-natural experiments: the Paris Agreement and the Stern Review. These events represent exogenous shifts in the global climate policy and discourse environment that are unlikely to be directly driven by individual firms’ capital expenditure decisions (Dyck et al., 2019; Gustafson & Kotter, 2023; Painter, 2020). The results are presented in Table 7.

Quasi-Natural Experiment Results: Paris Agreement and Stern Review.

Note. This table presents results from quasi-natural experiments examining how major climate policy milestones condition the relationship between climate change exposure (CCE) and firm-level capital expenditure. Column (1) reports estimations related to the implementation of the Paris Agreement, while Column (2) focuses on the release of the Stern Review. The interaction terms capture how these events alter the effect of CCE on investment behavior. All specifications include the control variables and firm- and year-fixed effects. The robust standard errors are reported in parentheses. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively.

The Paris Agreement, adopted on December 12, 2015, established internationally coordinated commitments to reduce greenhouse gas emissions and formalized long-term temperature targets. We construct a dummy variable, Paris_Agreement, equal to 1 for the post-agreement period (2016–2024) and 0 for the pre-agreement period (2001–2015). To assess whether credible policy coordination alters firms’ investment responses, we interact climate change exposure with Paris_Agreement. As shown in Column (1), the interaction term (CCE × Paris_Agreement) is positive and statistically significant, indicating that the association between climate change exposure and capital expenditure becomes stronger following the Agreement. This pattern is consistent with the view that credible and coordinated climate policy enhances the translation of exposure into long-term capital allocation.

Next, we consider the publication of the Stern Review in 2006, which provided a prominent assessment of the economic costs of climate inaction and substantially increased global climate awareness (Painter, 2020). Unlike the Paris Agreement, however, the Stern Review did not introduce binding international commitments. We define a dummy variable, Stern_Review, equal to 1 for the post-publication period (2007–2024) and 0 for the pre-publication period (2001–2006), and interact it with climate change exposure. As reported in Column (2), the interaction term (CCE × Stern_Review) is negative and statistically significant. This suggests that heightened awareness without binding institutional commitment may weaken the positive association between climate change exposure and capital expenditure, potentially reflecting increased uncertainty regarding future policy direction.

Taken together, the contrasting effects of these two events reinforce the importance of institutional credibility. While coordinated policy commitment strengthens climate-related capital allocation responses, awareness shocks alone do not appear sufficient to generate similar investment intensification.

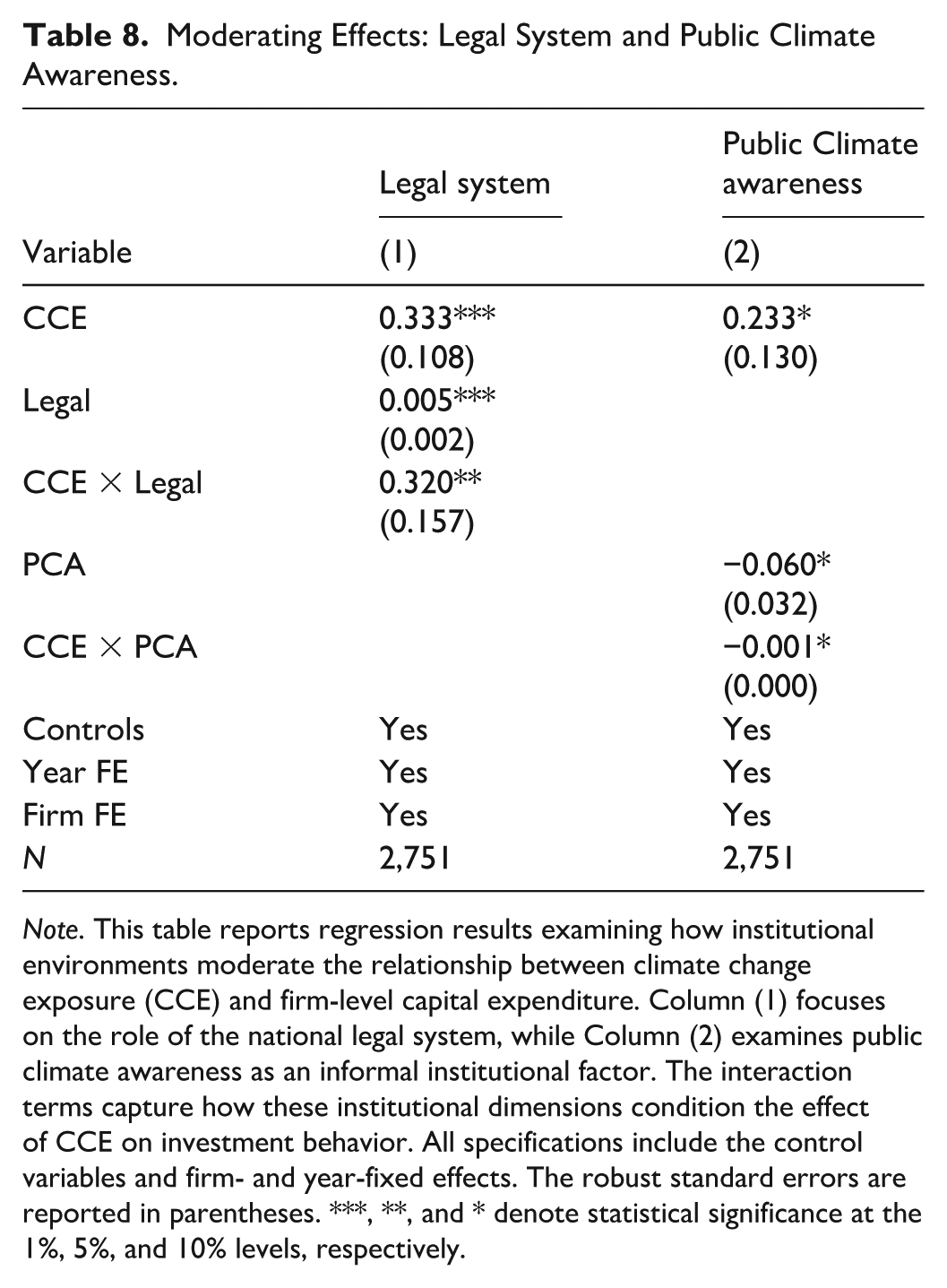

Moderating Effects

To test H2 and H3, we construct interaction terms between climate change exposure and the proposed moderating variables, Legal × CCE and PCA × CCE, capturing the moderating roles of formal and informal institutions, respectively. The related results are presented in Table 8.

Moderating Effects: Legal System and Public Climate Awareness.

Note. This table reports regression results examining how institutional environments moderate the relationship between climate change exposure (CCE) and firm-level capital expenditure. Column (1) focuses on the role of the national legal system, while Column (2) examines public climate awareness as an informal institutional factor. The interaction terms capture how these institutional dimensions condition the effect of CCE on investment behavior. All specifications include the control variables and firm- and year-fixed effects. The robust standard errors are reported in parentheses. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively.

Column (1) examines whether a country’s legal environment moderates the effect of climate change exposure on firms’ capital investments. The coefficient on the interaction term CCE × Legal is positive and statistically significant, indicating that a stronger legal environment amplifies the positive impact of climate change exposure on capital investment. This finding supports H2.

Column (2) assesses the moderating role of public climate awareness. The coefficient on CCE × PCA is negative and statistically significant, suggesting that higher public climate awareness weakens the positive effect of climate change exposure on firms’ capital investment, thereby supporting H3.

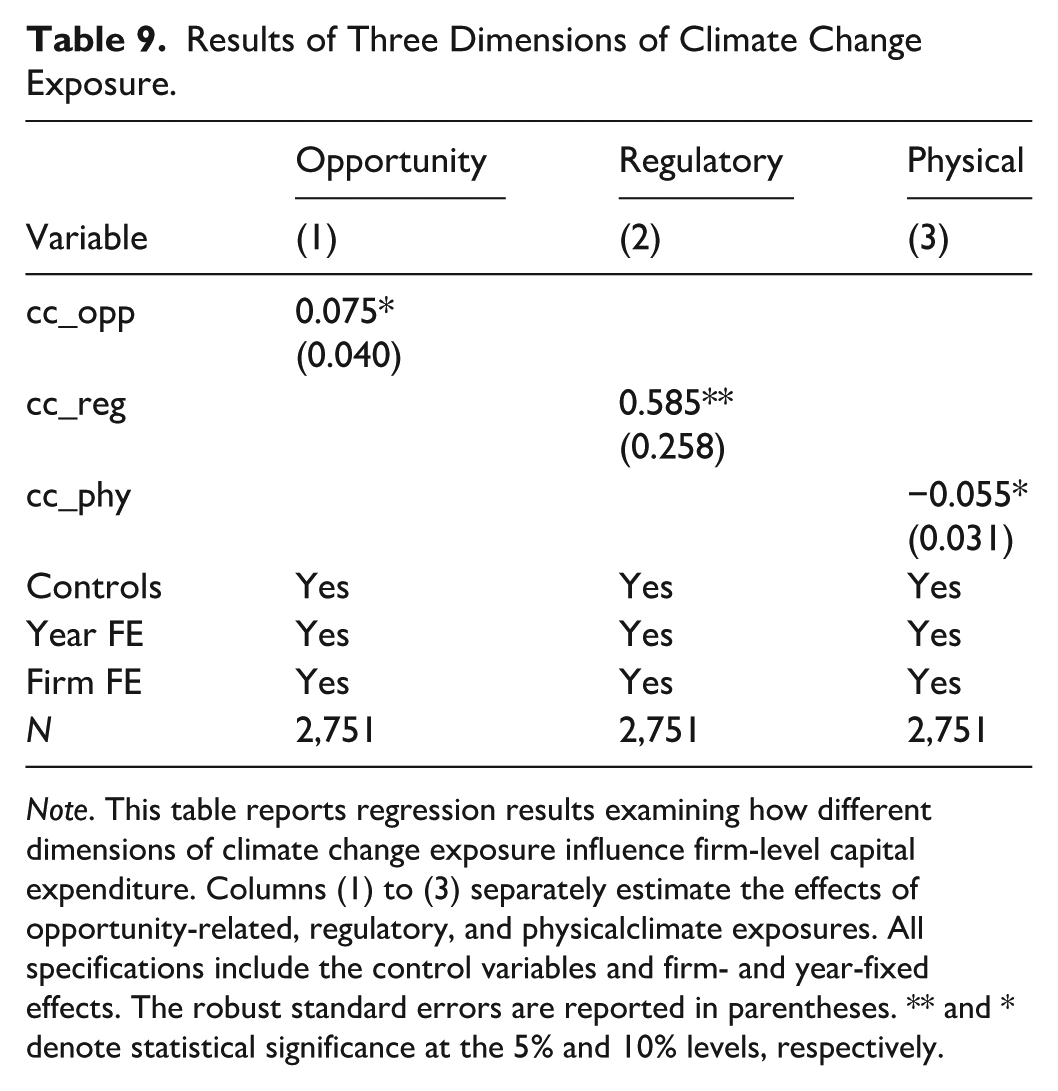

Decomposition of Climate Change Exposure

We further investigate how the multidimensional components of climate change exposure influence firms’ capital expenditure decisions. Following Sautner et al. (2023), we decompose climate change exposure into three sub-dimensions: opportunity, regulatory, and physical exposures. The opportunity dimension (cc_opp) is measured by the frequency with which analysts identify opportunity-related climate terms during earnings conference calls. The regulatory dimension (cc_reg) captures the frequency of terms associated with regulatory climate shocks. In contrast, the physical dimension (cc_phy) reflects the frequency of terms related to physical climate shocks and extreme weather events. Therefore, we examine how firms’ exposure to these three dimensions affects their capital investments. The related results are reported in Table 9.

Results of Three Dimensions of Climate Change Exposure.

Note. This table reports regression results examining how different dimensions of climate change exposure influence firm-level capital expenditure. Columns (1) to (3) separately estimate the effects of opportunity-related, regulatory, and physicalclimate exposures. All specifications include the control variables and firm- and year-fixed effects. The robust standard errors are reported in parentheses. ** and * denote statistical significance at the 5% and 10% levels, respectively.

The findings in Table 9 show that the coefficients on cc_opp and cc_reg are positive and statistically significant, indicating that firms facing greater climate-related opportunities or regulatory pressures tend to increase their capital investments. By contrast, the coefficient on cc_phy is negative and statistically significant, suggesting that firms exposed to higher levels of physical climate risk are more likely to reduce capital expenditure.

Finally, it is important to note that while our empirical strategy incorporates firm and year fixed effects, high-dimensional selection, matching procedures, lag structures, and quasi-experimental variation surrounding the Paris Agreement, we interpret the findings with appropriate caution. These approaches substantially strengthen inference by mitigating observable and some unobservable confounding factors. However, as with most observational research, residual endogeneity, such as time-varying unobservables or strategic disclosure dynamics, cannot be fully eliminated. Accordingly, our results should be interpreted as robust, economically meaningful associations consistent with adaptive investment behavior in tourism firms, rather than definitive causal proof.

Discussion of the Findings and Theoretical Contributions

Discussion of Findings

The central finding, that climate change exposure is positively associated with capital expenditure among hospitality and tourism firms, contributes to and refines existing strands of research in both tourism and climate-investment literatures. In the broader corporate finance literature, climate risk has been shown to either suppress investment through financial constraint (Agoraki et al., 2024; Ginglinger & Moreau, 2023) or stimulate adaptive innovation and restructuring (Yang & Song, 2025). Our findings align more closely with the latter perspective, suggesting that climate exposure can operate as a catalyst for strategic adaptation rather than solely as a source of retrenchment.

However, the tourism context introduces important nuance. Prior tourism research has largely emphasized the investment-dampening effects of uncertainty. For instance, Gozgor et al. (2022) show that geopolitical risk reduces tourism investment, consistent with Real Options theory, and Gao and Zhang (2024) demonstrate that climate policy uncertainty discourages capital expenditure in hospitality firms. By contrast, our results indicate that direct climate exposure, distinct from policy uncertainty, may stimulate investment in adaptive capital. This distinction helps reconcile seemingly conflicting findings in the tourism literature: while uncertainty about policy or geopolitical stability encourages delay, direct exposure to climate-related pressures may necessitate in-situ asset upgrading in a place-bound industry.

The findings also refine the application of the Dynamic Capabilities theory in tourism. Whereas the Dynamic Capabilities theory emphasizes firms’ ability to reconfigure and redeploy resources under environmental change, tourism firms operate within geographically fixed destination systems. Our evidence suggests that, under spatial immobility constraints, adaptive reconfiguration manifests primarily through capital intensification, infrastructure retrofitting, facility upgrades, and investment in resilience-enhancing technologies. This evidence extends Strategic Management theory by demonstrating how dynamic capabilities operate differently in place-dependent service industries compared to more mobile manufacturing sectors.

Institutionally, the results further contribute to ongoing debates in tourism and sustainability research regarding the role of governance and legitimacy pressures. The strengthening effect of legal environments is consistent with institutional scholarship emphasizing regulatory clarity and enforcement as drivers of long-term sustainability investment (Font et al., 2017). At the same time, the dampening role of public climate awareness introduces a more complex picture. While informal institutional pressure is often assumed to promote sustainability engagement, our findings suggest that in perception-sensitive industries such as tourism, reputational scrutiny may redirect adaptation toward visible signaling rather than capital-intensive structural change. This divergence refines Institutional theory by highlighting how industry characteristics condition the substantive versus symbolic nature of adaptive responses.

The quasi-natural experiment results further situate our findings within the climate governance literature. The Paris Agreement, which introduced coordinated international commitments and clearer transition signals, amplified the positive association between climate exposure and capital expenditure. In contrast, the Stern Review heightened awareness of climate risks but did not introduce binding institutional commitments, and its effect appears to have weakened investment incentives. This comparison suggests that credible policy coordination, rather than awareness alone, is critical for stimulating capital-intensive adaptation in tourism firms characterized by long asset lifecycles and high sunk costs.

Finally, decomposing climate exposure into opportunity, regulatory, and physical dimensions reveals important heterogeneity, which helps reconcile mixed evidence from prior studies. Opportunity and regulatory exposures stimulate capital expenditure, consistent with narratives of transition-driven adaptation. In contrast, physical exposure suppresses investment, reflecting heightened uncertainty regarding asset durability and return horizons. This bifurcation clarifies why aggregate climate risk measures may yield ambiguous results and underscores the importance of distinguishing between transition-related and physical risk channels in tourism research. These heterogeneous effects also confirm the theorized bifurcation between transition-driven intensification and physical-risk-induced contraction.

Although the climate exposure measure reflects financially salient attention rather than purely objective physical risk, this characteristic aligns with capital budgeting processes, which are shaped by managerial perception and investor scrutiny. The consistency of results across fixed effects models, lag structures, matching procedures, and policy shocks strengthens confidence that the observed associations reflect meaningful strategic responses rather than purely disclosure dynamics.

Theoretical Contributions

Our paper also advances theory at the intersection of tourism, strategic management, and institutional analysis by moving beyond empirical application to theoretical refinement. First, this paper contributes to tourism scholarship by introducing a firm-level conceptualization of climate adaptation. While prior tourism research has predominantly examined climate vulnerability and resilience at the destination or national level, this paper theorizes capital expenditure as a micro-foundation of destination resilience. By positioning capital investment as a structural mechanism through which tourism firms adapt to environmental change, the study extends tourism adaptation research from aggregate vulnerability assessments to corporate strategic behavior. This shift reframes tourism firms not merely as passive recipients of climate shocks but as active agents shaping destination-level resilience through long-term asset reconfiguration.

Second, the study refines the Dynamic Capabilities theory by identifying spatial immobility as a boundary condition for adaptive reconfiguration. The Dynamic Capabilities theory emphasizes firms’ abilities to reconfigure and redeploy resources across markets and contexts (Eisenhardt & Martin, 2000; Teece, 2007). However, tourism firms operate within geographically fixed destination systems, where core assets cannot be easily relocated. In such place-bound industries, adaptive capabilities manifest primarily through in-situ capital intensification, retrofitting, upgrading, and the structural reinforcement of existing assets, rather than through geographic repositioning or diversification. By demonstrating that climate exposure activates this place-bound adaptation logic, the study extends the Dynamic Capabilities theory to spatially constrained service industries. It clarifies how adaptation unfolds under constraints on immobility.

Third, the study advances Institutional theory by distinguishing the divergent roles of formal and informal institutions in shaping substantive versus symbolic adaptation. Institutional scholarship often assumes that stronger institutional pressures uniformly promote sustainability-oriented investment. However, the findings reveal asymmetry: while robust legal environments amplify capital-intensive adaptation, heightened public climate awareness in tourism contexts may dampen long-term investment responses. This evidence suggests that informal legitimacy pressures in perception-driven industries can redirect strategic responses toward visible signaling rather than toward reallocation of structural capital. By identifying this divergence, our paper refines Institutional theory in the context of climate adaptation and highlights how industry characteristics mediate the effects of institutions.

Fourth, by decomposing climate exposure into opportunity, regulatory, and physical dimensions, our paper advances theoretical understanding of climate risk heterogeneity. Rather than treating climate exposure as uniformly adverse, the findings reveal bifurcated adaptation pathways: transition-related exposures stimulate capital investment, whereas physical exposures suppress it. This distinction introduces a more nuanced theoretical model of climate adaptation in tourism, demonstrating that the direction of strategic investment depends on the type of exposure faced. In doing so, we clarify why prior climate–investment research has produced mixed findings and show that industry structure and exposure composition jointly shape adaptive outcomes.

In summary, these contributions move beyond applying established theories to a tourism setting. Instead, the study refines Dynamic Capabilities and Institutional theories by introducing spatial immobility, industry-specific legitimacy dynamics, and exposure heterogeneity as key contingencies in climate adaptation processes. In doing so, our paper strengthens the theoretical foundations of tourism adaptation research and situates firm-level capital investment as a central mechanism in the evolving climate–tourism nexus.

Practical Implications for Tourism Managers and Policymakers

The findings of our paper offer several concrete implications for tourism firm managers and policymakers responsible for designing climate adaptation frameworks.

Implications for Tourism Firm Managers

First, the positive association between climate exposure and capital expenditure suggests that climate-related pressures should be incorporated directly into long-term asset planning rather than treated as short-term operational risks. For hotel and tourism firms, climate adaptation is not merely a matter of compliance or reputation management but a structural investment decision. Therefore, managers should integrate climate exposure assessments into capital budgeting models, particularly when evaluating infrastructure upgrades, property redevelopment, and location-specific investments.

Second, the distinction between opportunity-related and physical climate exposure has strategic relevance. Transition-related pressures, such as regulatory tightening and emerging green market demand, appear to stimulate investment. This issue indicates that proactive investments in energy efficiency, resilient design, and low-carbon infrastructure may strengthen competitive positioning. In contrast, heightened physical exposure may suppress capital expenditure, reflecting uncertainty about asset durability and destination viability. Therefore, managers operating in high-physical-risk regions should incorporate scenario analysis and asset stress testing into investment evaluation processes to avoid underinvestment driven by uncertainty.

Third, the moderating role of public climate awareness highlights the risk of substituting visible signaling for substantive adaptation. In highly perception-sensitive tourism markets, firms may feel pressure to prioritize short-term legitimacy-enhancing actions (e.g., sustainability certifications or disclosures). While such initiatives are important, our findings suggest that long-term resilience requires capital-intensive structural upgrading. Therefore, managers should balance reputational strategies with tangible investment in climate-resilient infrastructure to avoid misalignment between signaling and structural preparedness.

Implications for Destination Managers and Policymakers

The results also guide policymakers seeking to support climate adaptation in tourism-dependent economies. First, the strengthening effect of legal environments indicates that institutional quality is critical to enabling private-sector climate investment. Clear regulatory frameworks, predictable enforcement, and strong property rights reduce uncertainty surrounding long-term capital commitments. Therefore, policymakers can stimulate adaptive investment by enhancing regulatory clarity regarding environmental standards, building codes, and climate-transition policies.

Second, the divergence between formal and informal institutional effects suggests that raising public climate awareness alone may not be sufficient to induce substantive capital adaptation. While awareness campaigns are valuable, they should be complemented by institutional mechanisms that align reputational pressure with structural investment incentives, such as tax credits for climate-resilient infrastructure, green financing programs, or co-investment schemes for destination-level resilience projects.

Third, because tourism firms are embedded within destination ecosystems, adaptation often requires coordinated infrastructure planning. Therefore, policymakers should promote collaborative adaptation strategies that integrate firm-level investments with public infrastructure upgrades, including coastal protection, water management systems, and climate-resilient transport networks. Without coordinated institutional support, individual firm investments may be insufficient to ensure destination-wide resilience.

In short, the evidence in this paper underscores that climate adaptation in tourism is not solely a matter of environmental compliance but also a strategic capital-allocation challenge shaped by institutional context. Effective adaptation requires alignment between managerial investment decisions, regulatory frameworks, and destination-level coordination.

Conclusion

This paper investigates how climate change exposure is associated with capital allocation decisions in a spatially immobile and climate-dependent industry. Drawing on the Dynamic Capabilities and Institutional theories, we conceptualize capital expenditure as an observable manifestation of structural asset reconfiguration under environmental uncertainty. Using a global panel of 420 hospitality and tourism firms from 2001 to 2024, the results indicate that climate change exposure is positively associated with aggregate capital expenditure, consistent with a place-bound adaptation mechanism in which firms intensify capital investment rather than redeploy assets geographically.

The findings further demonstrate that this association is institutionally conditioned. In countries with stronger legal environments, climate exposure more readily translates into capital reallocation, reflecting the role of institutional credibility in supporting long-term, irreversible investment. In contrast, higher public climate awareness weakens the exposure–investment relationship, consistent with legitimacy-driven trade-offs in perception-sensitive industries. These results suggest that formal and informal institutions shape not only the intensity but also the form and timing of adaptive responses.

Importantly, decomposing climate exposure into opportunity-related, regulatory, and physical dimensions reveals heterogeneous mechanisms. Transition-related exposures, reflecting regulatory change and strategic opportunity, are associated with increased capital expenditure. In contrast, physical exposure is associated with reduced investment, likely due to heightened uncertainty regarding asset durability and return horizons. This separation clarifies why prior research has reported mixed investment responses to climate risk and underscores the importance of distinguishing exposure channels in tourism contexts.

In short, the findings refine the Dynamic Capabilities theory by identifying spatial immobility as a boundary condition for adaptive reconfiguration and extend the Institutional theory by demonstrating how legal credibility and legitimacy pressure differentially condition structural investment responses. More broadly, the paper highlights capital allocation as a central mechanism through which tourism firms respond to climate-related pressures within destination-based systems.

Despite these contributions, the study is subject to two limitations. First, climate exposure is measured using textual analysis of earnings call transcripts and captures financially salient exposure rather than purely objective physical climate risk. Although such salience is directly relevant for capital allocation decisions, measurement error and disclosure dynamics cannot be fully excluded. Therefore, future papers can integrate additional risk indicators or project-level investment data to refine construct precision further. Second, while our empirical strategy incorporates high-dimensional controls, fixed effects, matching procedures, and quasi-experimental variation, residual endogeneity concerns may remain. Accordingly, our findings should be interpreted as robust associations consistent with adaptive investment behavior rather than definitive causal estimates. Therefore, future papers can exploit localized climate shocks or regulatory reforms that may further strengthen causal identification in tourism settings.

Supplemental Material

sj-docx-1-jtr-10.1177_00472875261456333 – Supplemental material for Climate Change Exposure and Capital Allocation in Tourism Firms

Supplemental material, sj-docx-1-jtr-10.1177_00472875261456333 for Climate Change Exposure and Capital Allocation in Tourism Firms by Riazullah Shinwari, Giray Gozgor, Junyi Feng and Daud Rehman in Journal of Travel Research

Footnotes

Author Contributions

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.