Abstract

This paper examines how biodiversity risk influences liquidity in global tourism firms and how institutional environments shape this relationship. Using a panel of 1,247 firm-year observations across 27 countries from 2000 to 2022, we find that biodiversity risk is positively associated with firms’ cash holdings, consistent with a precautionary liquidity motive under ecological uncertainty. Dynamic panel data specifications confirm persistence in cash policies. We further observe that business regulations and the freedom to enter markets significantly strengthen this relationship, indicating that institutional quality amplifies firms’ precautionary responses to biodiversity risk. These findings are robust across alternative specifications, subsamples, and liquidity measures. Theoretically, the paper extends the precautionary motive for cash by incorporating biodiversity risk and institutional moderation. Practically, the results highlight the importance of regulatory design and market structure in shaping how tourism firms manage liquidity under environmental pressures.

Keywords

Introduction

Tourism is one of the world’s largest industries and is uniquely dependent on natural environments, biodiversity, and ecosystem services. The attractiveness of many destinations is closely tied to the quality and integrity of their natural assets, including wildlife, forests, beaches, coral reefs, and protected landscapes. These resources underpin cultural, adventure, and nature-based tourism, shaping visitor experiences and sustaining economic activity (Buckley, 2012; Gössling et al., 2015). However, the ongoing loss of biodiversity poses a fundamental risk to the sustainability of tourism. Global assessments warn of accelerating species extinction, ecosystem degradation, and habitat loss (Powers & Jetz, 2019). For tourism firms, such risks translate into increased uncertainty over the continuity of natural resources, potential restrictions on land use, reputational pressures from unsustainable practices, and heightened exposure to environmental regulations (Kumar, 2024).

The ecological and sociocultural implications of biodiversity loss in tourism have been widely discussed (see, e.g., Hall, 2019). However, there is limited understanding of how tourism firms respond financially to such risks. The management of biodiversity risk is not only an environmental concern but also a financial one (Giglio et al., 2026). Firms exposed to high environmental uncertainty often adjust their financial strategies to buffer against potential disruptions (Parker & Ameen, 2018). This study positions biodiversity risk as a key determinant of corporate liquidity behavior in tourism firms.

Cash holdings are a central component of corporate financial strategy. Firms retain cash to mitigate financing frictions, reduce exposure to shocks, and maintain flexibility in investment decisions (Bates et al., 2009). Under uncertainty, precautionary motives dominate, with firms holding greater liquidity to ensure resilience (Opler et al., 1999). Tourism companies are particularly vulnerable to external shocks, such as natural disasters, pandemics, and environmental degradation (Lee et al., 2024). Liquidity is therefore especially critical for their survival and recovery. Prior research has examined the effects of COVID-19 and climate-related shocks on financial resilience in tourism (see, e.g., D’Orazio, 2021; Sheller, 2021); however, the relationship between biodiversity risk and firms’ liquidity strategies remains unexplored.

Institutional settings add further complexity to this relationship. Theories of law, finance, and institutions emphasize that regulatory environments shape corporate behavior (Demirgüç-Kunt & Maksimovic, 1998; Djankov et al., 2002; Klapper et al., 2006). Business regulations influence compliance costs, operational flexibility, and access to finance. In more regulated environments, firms may adopt more conservative financial policies to manage regulatory uncertainty. Similarly, market openness, captured by the ease of entry and competitive intensity, affects firms’ exposure to risk and opportunity (Demirgüç-Kunt & Maksimovic, 1998). In more open and competitive markets, firms may adjust liquidity policies to maintain strategic flexibility (Gamba & Triantis, 2008). For tourism firms operating across diverse institutional contexts, understanding how these factors interact with biodiversity risk is particularly important.

As the tourism sector continues to adapt in the aftermath of COVID-19, attention is shifting toward broader systemic risks that threaten long-term sustainability. Biodiversity loss represents one such structural challenge (Giglio et al., 2026). Understanding how tourism firms incorporate biodiversity-related risks into their financial decision-making is therefore essential for both policy and practice. Against this background, this paper examines the impact of biodiversity risk on cash holdings in the tourism sector. The paper also explores the moderating effects of business regulations and freedom to enter markets. The analysis is based on a panel dataset of 1,247 firm-year observations across 27 countries from 2000 to 2022, enabling a cross-country assessment of environmental and institutional effects.

This paper makes three contributions to the literature. First, it introduces biodiversity risk into the study of tourism firms’ financial behavior, extending prior work that has primarily focused on the ecological, social, and policy dimensions of biodiversity loss (Hall, 2019). By linking environmental risk to liquidity management, the paper bridges tourism research and corporate finance literature. Second, it highlights the role of institutional context in shaping financial responses to environmental risk. While business regulations and freedom to enter markets have been widely studied in law and finance (Demirgüç-Kunt & Maksimovic, 1998; Djankov et al., 2002; Klapper et al., 2006), their moderating role in tourism firms’ responses to biodiversity risk remains underexplored. Third, the study contributes to the broader literature on sustainability and finance by demonstrating how biodiversity risks influence firm-level financial decisions in a highly nature-dependent industry.

The remainder of this paper is organized as follows. Section “Literature Review, Theoretical Background, and Hypothesis Development” reviews the empirical literature and theoretical background on biodiversity risk and corporate cash holdings, and develops the paper’s hypotheses. Section “Data, Model, and Methodology” presents the data, variables, empirical model, and methodology. Section “Empirical Findings” reports the empirical findings and robustness checks. Section “Discussion and Implications” discusses the findings and their implications. Section “Conclusion” concludes the paper.

Literature Review, Theoretical Background, and Hypothesis Development

Biodiversity Risk and Cash Holdings

Biodiversity is increasingly recognized as a fundamental ecological determinant of ecosystem functionality and economic activity (Flammer et al., 2025; Karolyi & Tobin-de la Puente, 2023). This dependence is particularly salient in the tourism industry, where ecosystem health directly underpins destination attractiveness and industry viability (Chen et al., 2025; Cheng et al., 2025). Natural assets such as wildlife, forests, and coastal ecosystems are central to tourism demand and long-term sustainability (Siikamäki et al., 2015). Consequently, biodiversity loss poses not only ecological challenges but also significant financial risks for tourism firms that rely heavily on natural capital (Lenzen et al., 2018; Van der Duim & Caalders, 2002).

While prior research has examined the ecological and operational consequences of biodiversity loss in tourism (Scott & Gössling, 2022), its implications for firm-level financial strategies remain underexplored (Chen et al., 2025; Cheong et al., 2024). This gap is important because biodiversity risk can alter firms’ exposure to uncertainty, regulatory pressures, and demand volatility, thereby influencing financial decision-making.

From a corporate finance perspective, the accumulation of cash reserves is a central response to uncertainty. According to the precautionary and transaction motives of cash holdings (Bates et al., 2009; Opler et al., 1999), biodiversity risk can influence firms’ liquidity strategies through two key channels.

First, as with other forms of uncertainty, such as climate policy uncertainty (Gao & Zhang, 2024) and geopolitical risk (Gozgor et al., 2022), biodiversity risk may induce firms to increase cash holdings as a buffer against potential shocks. Limited access to external financing during environmental disruptions, together with regulatory uncertainty surrounding biodiversity protection, further strengthens this precautionary motive (Berg & Schrader, 2012). This mechanism is particularly relevant in tourism, where revenues are highly sensitive to ecosystem quality and seasonal fluctuations.

Second, biodiversity risk also creates investment opportunities. The transaction motive suggests that firms with greater liquidity are better positioned to capitalize on emerging sustainability-related opportunities, such as eco-certifications, conservation partnerships, and nature-based tourism products (Köberl et al., 2016). Empirical evidence supports this dual role of biodiversity risk. For instance, Ahmad and Karpuz (2024) show that exposure to biodiversity risk increases firms’ cash holdings while enabling investment in adaptive opportunities, particularly for financially constrained firms. Their findings indicate that biodiversity risk can increase liquidity buffers by approximately 3.8 percentage points of total assets.

Beyond risk mitigation, biodiversity can also be viewed as a strategic intangible asset. From the Resource-Based View (Barney, 1991), biodiversity is a valuable, difficult-to-replicate resource that can generate competitive advantage. Cheong et al. (2024) also show that tourism firms investing in biodiversity-related initiatives achieve superior financial performance, suggesting that environmental engagement can enhance both profitability and resilience. This is particularly relevant in tourism markets, where demand for environmentally responsible experiences continues to grow (Casado-Díaz et al., 2014).

The broader literature further highlights the financial materiality of biodiversity. Biodiversity-related activities can enhance firm value by improving stakeholder relations and reducing regulatory risk (Flammer et al., 2025). Tourism destinations with strong biodiversity protection exhibit greater resilience and sustained visitor demand (Scott & Gössling, 2022). At the same time, financial markets increasingly price biodiversity risk, with firms exhibiting higher biodiversity footprints facing higher financing costs (Garel et al., 2024). These findings suggest that biodiversity risk influences both operational and financial outcomes.

The relationship between biodiversity risk and firm behavior can be understood through multiple theoretical lenses. The Precautionary Motive Theory (Opler et al., 1999) explains the increase in cash holdings under uncertainty. The Resource-Based View (Barney, 1991) highlights biodiversity as a strategic asset. Real Options Theory (Dixit & Pindyck, 1994) emphasizes the importance of maintaining financial flexibility in the face of uncertainty.

Taken together, these theories suggest that biodiversity risk affects firms’ financial behavior through two complementary mechanisms. First, it increases precautionary demand for liquidity to hedge against ecological uncertainty and regulatory risks. Second, it raises financing frictions, as investors may perceive tourism firms as more exposed to environmental risk, thereby increasing the cost of external finance. To mitigate these constraints, firms accumulate internal liquidity to preserve financial flexibility. Based on these arguments, we propose the following hypothesis:

The Role of Business Regulations in Corporate Financial Policies

Business regulations play a central role in shaping corporate financial strategies, particularly in sectors exposed to environmental risks such as tourism, energy, and manufacturing. Regulatory frameworks influence firms’ financial behavior by affecting the cost of capital, altering risk exposure, and imposing compliance requirements (Delmas & Toffel, 2008). In response to environmental regulations, firms often adopt more conservative financial policies, including higher cash holdings and lower leverage, to mitigate potential fines, legal liabilities, and reputational risks (Phan et al., 2019). Firms in high-risk industries also reallocate resources toward sustainability investments and operational adjustments to reduce regulatory uncertainty and enhance resilience (Albuquerque et al., 2019).

Prior research shows that regulatory environments shape firms’ responses to external shocks. For example, Krueger et al. (2020) find that firms operating in countries with stronger environmental policies exhibit greater financial resilience to climate-related risks. Similarly, regulatory requirements related to environmental protection, sustainability, and disclosure can strengthen the precautionary motive for holding cash by increasing exposure to compliance costs and regulatory uncertainty (Phan et al., 2019).

While biodiversity risk is expected to increase cash holdings (H1), the strength of this relationship depends on the institutional environment. Drawing on Institutional Theory (DiMaggio & Powell, 1983), regulatory frameworks impose pressures that compel firms to internalize environmental risks. In environments with higher regulatory quality, characterized by more transparent, predictable, and efficiently implemented rules, firms are more likely to anticipate and incorporate biodiversity-related risks into their financial decisions. Such anticipation may lead to higher precautionary cash holdings to absorb compliance costs, legal contingencies, and operational disruptions associated with environmental regulation (Iraldo et al., 2011).

Empirical evidence also supports this mechanism. Firms operating in environmentally sensitive industries, including tourism, tend to hold more cash in response to regulatory pressures (Fard et al., 2020), suggesting that institutional environments can amplify precautionary financial behavior.

However, an alternative view, grounded in the Efficiency Hypothesis (Porter & Linde, 1995), suggests that well-designed regulatory frameworks may reduce uncertainty and weaken the need for excessive liquidity. Clear and transparent regulations provide firms with predictable operating conditions, reduce informational asymmetries, and encourage efficiency-enhancing innovations (Ambec et al., 2013). In such settings, firms may face lower regulatory uncertainty, potentially reducing the need for large precautionary cash buffers.

These competing perspectives highlight the importance of regulatory quality, not regulatory stringency alone. In the tourism sector, this distinction is particularly relevant. Tourism firms are highly dependent on local ecosystems and cannot easily relocate their operations (Van der Duim & Caalders, 2002), making them especially sensitive to environmental regulation. As a result, well-functioning regulatory environments may increase the salience of biodiversity risk while simultaneously enabling firms to respond more effectively through financial adjustments.

Integrating Precautionary Motive Theory (Opler et al., 1999) with Institutional Theory (DiMaggio & Powell, 1983), we argue that more efficient and less burdensome regulatory environments strengthen firms’ precautionary responses to biodiversity risk. By reducing regulatory ambiguity and improving predictability, such environments enable firms to internalize environmental risks and proactively adjust their liquidity policies. Consequently, firms operating in higher-quality regulatory frameworks are more likely to accumulate precautionary cash reserves when exposed to biodiversity risk. Accordingly, we propose the following hypothesis:

Freedom to Enter Markets as a Moderator in the Biodiversity Risk-Cash Holding Relationship

Freedom to enter markets, that is, the ease with which new firms can enter and compete, represents a key structural dimension shaping corporate financial strategies (Demirgüç-Kunt & Maksimovic, 1998; Djankov et al., 2002; Klapper et al., 2006). In economies with low barriers to entry, increased competition typically reduces profit margins and destabilizes market shares (Nickell, 1996). In response to heightened competitive pressure and greater earnings uncertainty, firms often adopt more conservative financial policies, including higher cash holdings, to maintain flexibility and buffer against revenue volatility (Almeida et al., 2004).

From a theoretical perspective, Industrial Organization Theory (Bain, 1956) emphasizes that market contestability influences firm behavior. In highly contestable markets, the threat of entry compels incumbent firms to adopt flexible financial and operational strategies. Maintaining financial slack, such as higher cash holdings, enables firms to respond to competitive pressures by investing, adjusting pricing strategies, and innovating (Lyandres, 2006). Accordingly, firms operating in more open and competitive markets may accumulate larger liquidity buffers as a hedge against uncertainty arising from market entry and competition.

The precautionary motive for cash holdings (Opler et al., 1999) further reinforces this argument. In markets with greater freedom to enter, firms face increased demand uncertainty as new entrants fragment customer bases and intensify competition (Frésard & Valta, 2016). Moreover, the risk of disruptive innovation increases, requiring incumbent firms to respond rapidly through strategic investments or organizational adjustments (Lyandres, 2006). These conditions strengthen the need for liquidity as a buffer against both operational and strategic uncertainty.

However, an alternative perspective, grounded in Agency Theory (Jensen, 1986), suggests that increased competition may reduce cash holdings by limiting managerial discretion. Intense market competition constrains managers’ ability to accumulate excess cash for inefficient or self-serving purposes (Giroud & Mueller, 2011). Under this view, firms in more competitive markets may prioritize efficiency and reduce precautionary cash buffers.

The relevance of this disciplining effect is likely to vary across industries. In the tourism sector, where demand is highly seasonal and sensitive to external shocks, firms face greater revenue volatility and operational risk. As a result, the precautionary motive for holding cash remains strong, even in competitive environments (Faulkender & Wang, 2006). Firms with high fixed costs, such as hotels, resorts, and airlines, are particularly exposed to demand fluctuations and, therefore, rely on liquidity buffers to maintain financial stability (Opler et al., 1999). In addition, tourism firms often operate in dynamic environments that require strategic adaptability, including responses to sustainability transitions and changing consumer preferences (Prayag et al., 2024).

Taken together, these arguments suggest that, in the tourism sector, the precautionary motive dominates the disciplining effect of competition. Greater market openness increases both competitive pressure and uncertainty, reinforcing firms’ incentives to maintain liquidity buffers when exposed to environmental risks. In particular, biodiversity risk, by affecting demand stability and operational continuity, interacts with competitive dynamics to further increase the value of financial flexibility.

Drawing on IO Theory (Bain, 1956) and Precautionary Motive Theory (Opler et al., 1999), we argue that firms operating in more open and competitive markets respond more strongly to biodiversity risk by increasing their cash holdings. This relationship is further reinforced by ecological uncertainty (Flammer et al., 2025) and the strategic pressure to maintain competitiveness in sustainability-oriented markets (Frésard & Valta, 2016). Accordingly, we propose the following hypothesis:

Data, Model, and Methodology

Sample

This study examines the relationship between cash holdings and biodiversity risk in the global tourism sector. The sample comprises publicly listed firms operating in the tourism sector from 27 countries, encompassing the hotel, restaurant, recreation, casino, and airline industries, over the period from 2000 to 2022. 1 These sectors represent key segments of the tourism ecosystem, including hospitality services, leisure and recreation activities, and transportation services that support global tourism flows. The final sample comprises 1,247 firm-year observations. The firm-level variables are winsorized at the 1st and 99th percentiles to address potential bias from outliers consistent with Ahmad and Karpuz (2024).

To provide further insight into cross-country variation in biodiversity risk and institutional indicators, Supplemental Appendix Table A1 reports country-level averages of the key variable, and it highlights substantial cross-country variation in both biodiversity risk and institutional conditions. Countries such as New Zealand, Singapore, and the United Kingdom exhibit relatively high levels of business regulation efficiency and market openness. In contrast, countries such as Zimbabwe, Vietnam, and Russia display lower institutional scores. Similarly, biodiversity risk varies across countries, reflecting differences in ecological exposure and environmental conditions. The institutional variables also show meaningful dispersion across the sample, suggesting that firms operate under diverse regulatory and competitive environments. This variation provides a suitable empirical setting to examine how institutional conditions shape firms’ financial responses to biodiversity risk.

Variables and Data Sources

Dependent Variable

In this study, cash holdings are the dependent variable, measured as the ratio of cash and cash equivalents to total assets. This measure reflects a firm’s liquidity position and has been widely used in previous research (e.g., Yuan et al., 2025). In the robustness checks, we consider two alternative measures of liquidity: Liquidity2 is defined as cash and short-term investments scaled by total assets (Al Mamun et al., 2024), while Liquidity3 is measured as cash and cash equivalents relative to net assets (i.e., total assets minus cash and cash equivalents) (Tran et al., 2025). The data on the dependent variable (i.e., cash holdings) and firm-level control variables were sourced from the London Stock Exchange Group (LSEG) database.

Main Variables of Interest

The main explanatory variable of interest is biodiversity risk, proxied by a firm-level text-based measure (Giglio et al., 2026). This variable is derived using the Bidirectional Encoder Representations from Transformers (BERT) model for sentiment analysis. The measure is calculated as the difference between the number of negative and positive biodiversity-related sentences in firms’ 10-K filings. The benchmark measure of biodiversity risk is Biodiversity Negative (Bio_risk_negative), which has potentially significant financial implications for tourism firms. Higher index values correspond to greater biodiversity risk, reflecting the frequency of negative sentiment toward biodiversity in firms’ 10-K disclosures (Giglio et al., 2026). We consider the negative biodiversity-risk variable to be highly concentrated at zero; non-zero values account for approximately 1.12% of the sample size. While this distribution is sparse, it is consistent with prior biodiversity-risk research. For instance, Giglio et al. (2026) report that approximately 2.9% of 10-K filings mentioned biodiversity-related regulation risks between 2015 and 2020.

Moderating Variables

The moderating variables capture key aspects of the institutional environment and are drawn from the Economic Freedom of the World Index (Gwartney et al., 2025). Specifically, we use two indicators: business regulations and freedom to enter markets and compete.

The business regulations index reflects the regulatory burden imposed on firms, including administrative requirements, bureaucratic costs, business-start-up procedures, informal payments, favoritism, licensing restrictions, and tax compliance costs. These subcomponents are aggregated into an index ranging from 0 to 10, where higher values indicate a less burdensome and more efficient regulatory environment, while lower values indicate stricter, more restrictive regulation.

The freedom-to-enter index captures the degree of market openness and competitive intensity. It incorporates factors such as the absence of price controls, limited government favoritism, and low barriers to entry. Similar to the business regulations index, it ranges from 0 to 10, where higher values indicate greater market openness and stronger competition, and lower values reflect higher entry barriers and more restricted markets.

Importantly, the interpretation of these indices is such that higher values of both indices correspond to more favorable institutional conditions. Therefore, in the interaction models, a positive coefficient on the interaction term indicates that the effect of biodiversity risk on cash holdings is stronger in less-restrictive regulatory environments and more open markets.

Control Variables

Following recent studies on biodiversity and cash holdings (e.g., Ahmad & Karpuz, 2024; Cheong et al., 2024; Yuan et al., 2025), we include firm-level variables commonly recognized as significant determinants of cash holdings, namely, firm size, leverage, cash flow, Tobin’s Q, tangibility, dividends, and capital expenditures (CAPEX). Firm size (SIZE) is defined as the natural logarithm of total assets (Ahmad & Karpuz, 2024; Cheong et al., 2024; Yuan et al., 2025). Leverage is the ratio of total debt to total assets. Cash flow is the ratio of cash flow from operating activities to total assets (Ahmad & Karpuz, 2024). Tobin’s Q is computed as the sum of the market value of equity and total assets, less the book value of equity, divided by total assets (Ahmad & Karpuz, 2024). Tangibility is calculated as total net property, plant, and equipment divided by total assets (Cheong et al., 2024). Dividends are the ratio of cash paid for dividends to total assets (Yuan et al., 2025), and CAPEX is the ratio of capital expenditures to total assets (Yuan et al., 2025).

Empirical Models

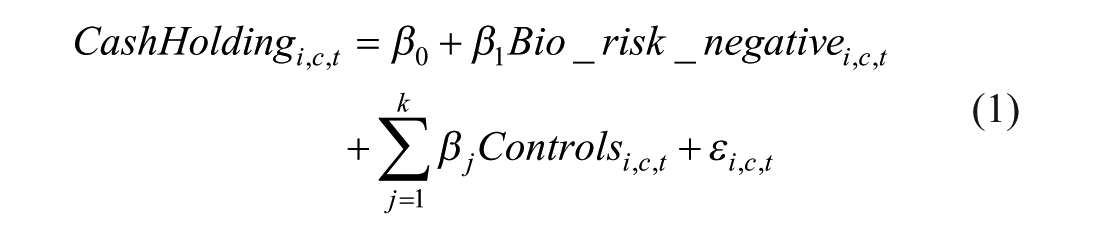

To examine the relationship between biodiversity risk and corporate liquidity, we employ panel data estimation techniques that account for unobserved heterogeneity and potential confounding factors. Specifically, we adopt a firm-level fixed-effects model as our baseline specification. The fixed-effects approach is appropriate in this setting because it controls for time-invariant firm characteristics, such as managerial style, business model, or location-specific advantages, that may simultaneously influence both biodiversity exposure and liquidity policies. This is particularly important in the tourism sector, where firms are often tied to specific natural environments and destinations. Accordingly, the following model is used to test H1:

where

The fixed-effects specification is preferred over pooled ordinary least squares because it mitigates bias arising from unobserved firm-specific factors. Compared to random-effects models, the fixed-effects approach does not rely on the assumption that unobserved heterogeneity is uncorrelated with the regressors, an assumption unlikely to hold in our context. This makes the fixed-effects model a more conservative and appropriate baseline estimator.

To test H2 and H3, we extend the baseline model by incorporating interaction terms that capture the moderating roles of institutional factors, namely, business regulations and freedom to enter markets:

Where

In interpreting the interaction models, the coefficient

Finally, while the fixed-effects framework addresses time-invariant heterogeneity, it does not fully account for potential dynamic adjustment in cash holdings or reverse causality. To address these concerns, we complement our baseline analysis with dynamic panel estimations using the generalized method of moments (GMM), presented in Section “Dynamic Panel GMM Estimations.” This approach allows us to control for persistence in liquidity policies and mitigate endogeneity due to simultaneity and omitted-variable bias.

Descriptive Statistics and Pairwise Correlations

Supplemental Appendix Table A2 reports descriptive statistics for the main variables. Cash holdings average 0.099 (SD = 0.109), indicating variation in liquidity positions, while Bio_risk_negative has a mean of −0.009 (SD = 0.147). Among controls, Tobin’s Q averages 2.50 (SD = 3.58) and firm size 20.67 (SD = 2.16), suggesting heterogeneity in firm characteristics. For institutional factors, business regulations average 6.51 (SD = 1.00) and freedom to enter markets averages 8.60 (SD = 1.66), indicating cross-country variation.

Supplemental Appendix Table A2 reports pairwise correlations among the variables. Cash holdings are highly correlated with alternative liquidity measures (e.g., 0.976 with Liquidity3 and 0.890 with Liquidity2). Bio_risk_negative generally exhibits weak correlations with firm-level variables (e.g., −0.025 with cash holdings). Among institutional variables, business regulations and freedom to enter markets are strongly and positively correlated (r = .722), indicating overlap in regulatory dimensions.

Empirical Findings

Biodiversity Risk and Cash Holdings: Baseline Estimations

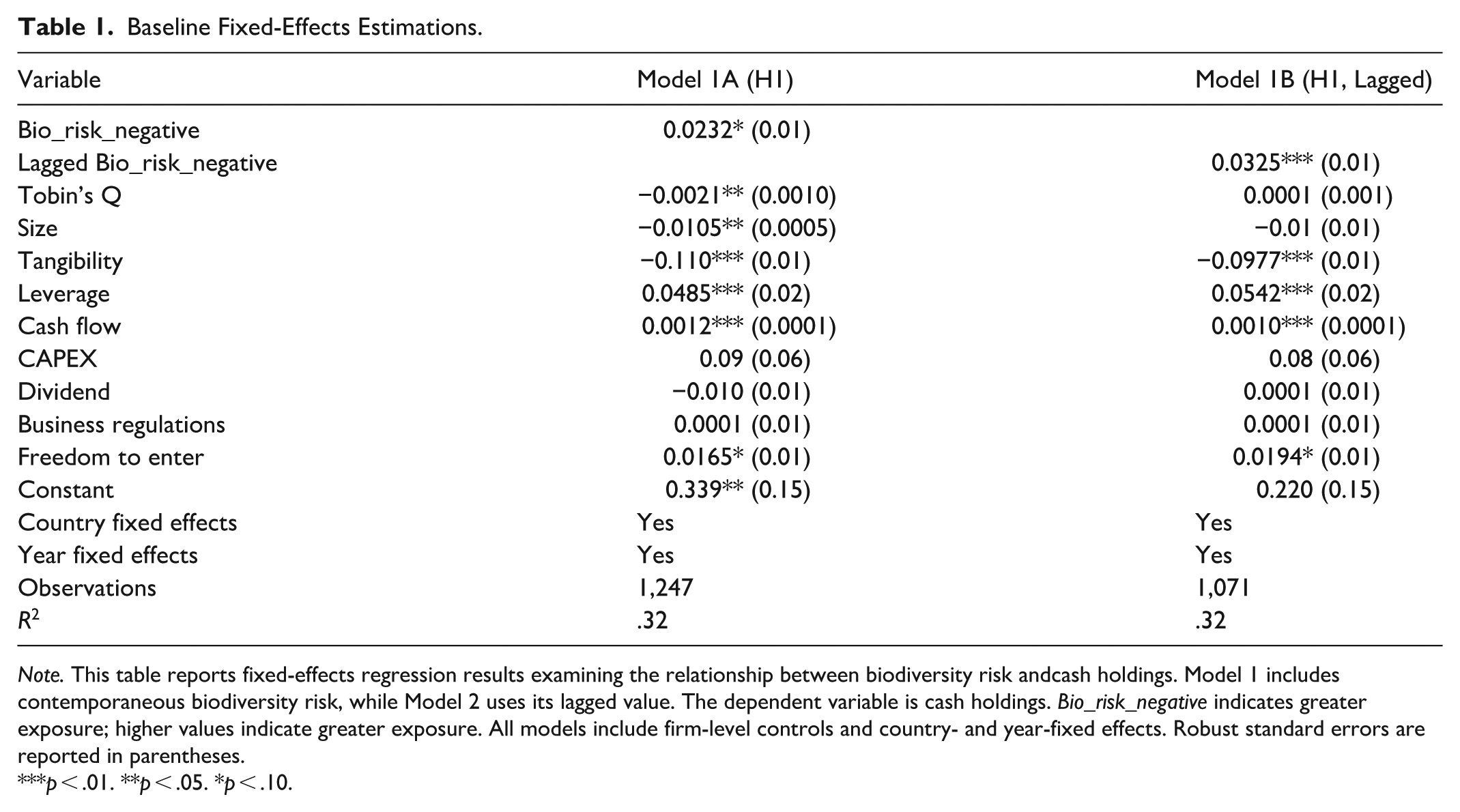

Table 1 reports the baseline fixed-effects estimates of the relationship between biodiversity risk and firms’ cash holdings. In Model 1, Bio_risk_negative is positively associated with cash holdings (β = .0232, p < .10), providing initial support for the precautionary motive. Model 2 incorporates a lagged measure of biodiversity risk and shows a stronger, more statistically significant effect (β = .0325, p < .01), indicating that firms adjust their liquidity buffers not only contemporaneously but also in response to prior exposure to biodiversity-related risks. This persistence suggests that biodiversity risk has a sustained impact on firms’ liquidity management.

Baseline Fixed-Effects Estimations.

Note. This table reports fixed-effects regression results examining the relationship between biodiversity risk andcash holdings. Model 1 includes contemporaneous biodiversity risk, while Model 2 uses its lagged value. The dependent variable is cash holdings. Bio_risk_negative indicates greater exposure; higher values indicate greater exposure. All models include firm-level controls and country- and year-fixed effects. Robust standard errors are reported in parentheses.

p < .01. **p < .05. *p < .10.

Among the control variables, firm size and asset tangibility are negatively associated with cash holdings, whereas leverage and cash flow are positively associated with cash holdings. CAPEX and dividend payouts are not statistically significant, whereas market openness, proxied by the freedom to enter markets, is positively associated with cash holdings. These patterns are broadly consistent with established findings in the corporate finance literature.

Overall, the results indicate that biodiversity risk is an important determinant of firms’ liquidity policies. The positive and robust association, particularly in the lagged specification, supports the view that tourism firms adopt precautionary cash-holding strategies in response to ecological uncertainty.

Moderating Role of Business Regulations and Freedom to Enter Markets

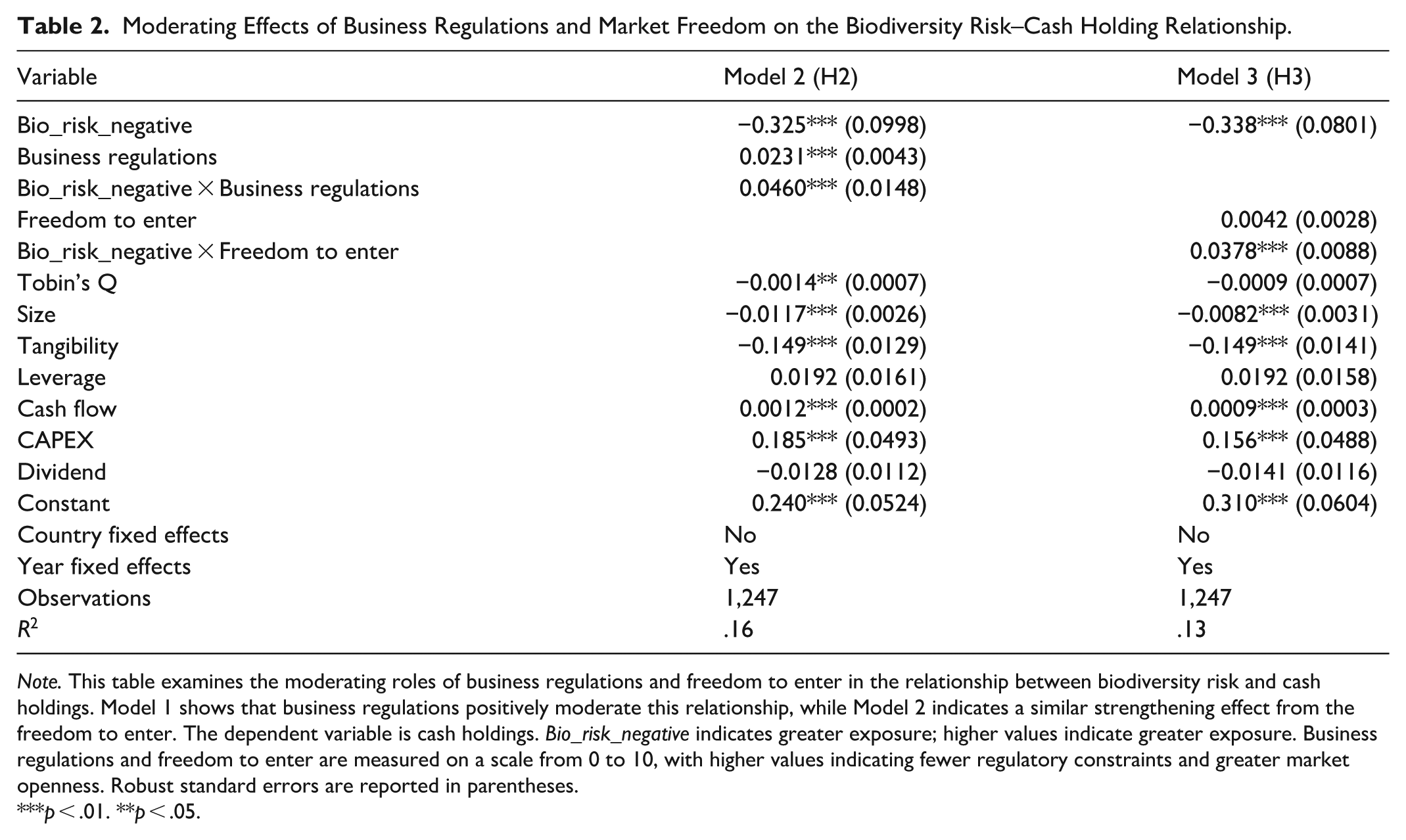

Table 2 reports the moderating effects of business regulations and market entry freedom on the relationship between biodiversity risk and firms’ cash holdings. In the interaction specifications, the coefficient on Bio_risk_negative reflects the marginal effect when the moderating variable equals zero. Accordingly, the economically relevant effect is the conditional marginal effect, defined as

Moderating Effects of Business Regulations and Market Freedom on the Biodiversity Risk–Cash Holding Relationship.

Note. This table examines the moderating roles of business regulations and freedom to enter in the relationship between biodiversity risk and cash holdings. Model 1 shows that business regulations positively moderate this relationship, while Model 2 indicates a similar strengthening effect from the freedom to enter. The dependent variable is cash holdings. Bio_risk_negative indicates greater exposure; higher values indicate greater exposure. Business regulations and freedom to enter are measured on a scale from 0 to 10, with higher values indicating fewer regulatory constraints and greater market openness. Robust standard errors are reported in parentheses.

p < .01. **p < .05.

In both models, the coefficient on biodiversity risk is negative when evaluated at zero values of the moderator (β = −.325, p < .01; β = −.338, p < .01). However, this baseline effect is not economically meaningful in isolation because it does not align with the observed institutional environments in the sample. The interaction terms provide critical insight into how this relationship evolves across institutional settings.

First, business regulations positively moderate the relationship (β = .0460, p < .01). Given that higher values of the business regulations index indicate less burdensome and more efficient regulatory environments, this result implies that the effect of biodiversity risk becomes less negative and eventually positive as regulatory environments become more efficient. Solving for the turning point at which the marginal effect equals zero yields a threshold value of 6.061. Based on the sample distribution (N = 1,247 firm-year observations), approximately 75.7% of observations lie above this threshold. This indicates that, for most firms, biodiversity risk increases cash holdings, consistent with a precautionary response.

Second, the interaction between biodiversity risk and freedom to enter markets is also positive and significant (β = .0378, p < .01). Since higher values of this index reflect greater market openness and lower barriers to entry, the results indicate that firms in more open and competitive markets respond to biodiversity risk by increasing liquidity buffers. The corresponding turning point is 7.863, with approximately 68.8% of observations exceeding this level, again suggesting that the dominant effect in the sample is positive.

Taken together, these findings reveal a clear threshold effect. In weaker institutional environments, characterized by more restrictive regulation and limited market openness, biodiversity risk is associated with reduced cash holdings, potentially reflecting financial constraints or limited capacity to build precautionary reserves. In contrast, in more efficient regulatory environments and more competitive markets, biodiversity risk induces firms to accumulate cash, consistent with precautionary and strategic liquidity management.

Among the control variables, firm size and tangibility are negatively associated with cash holdings, while cash flow and CAPEX are positively related, consistent with prior literature (Bates et al., 2009; Opler et al., 1999).

Overall, the results highlight that institutional quality and market conditions play a decisive role in shaping how biodiversity risk translates into corporate liquidity policies. The results provide strong support for H2 and H3. Both business regulations and freedom to enter markets strengthen the precautionary response to biodiversity risk, demonstrating that more efficient regulatory environments and greater market openness amplify firms’ financial adaptation to ecological uncertainty.

Dynamic Panel GMM Estimations

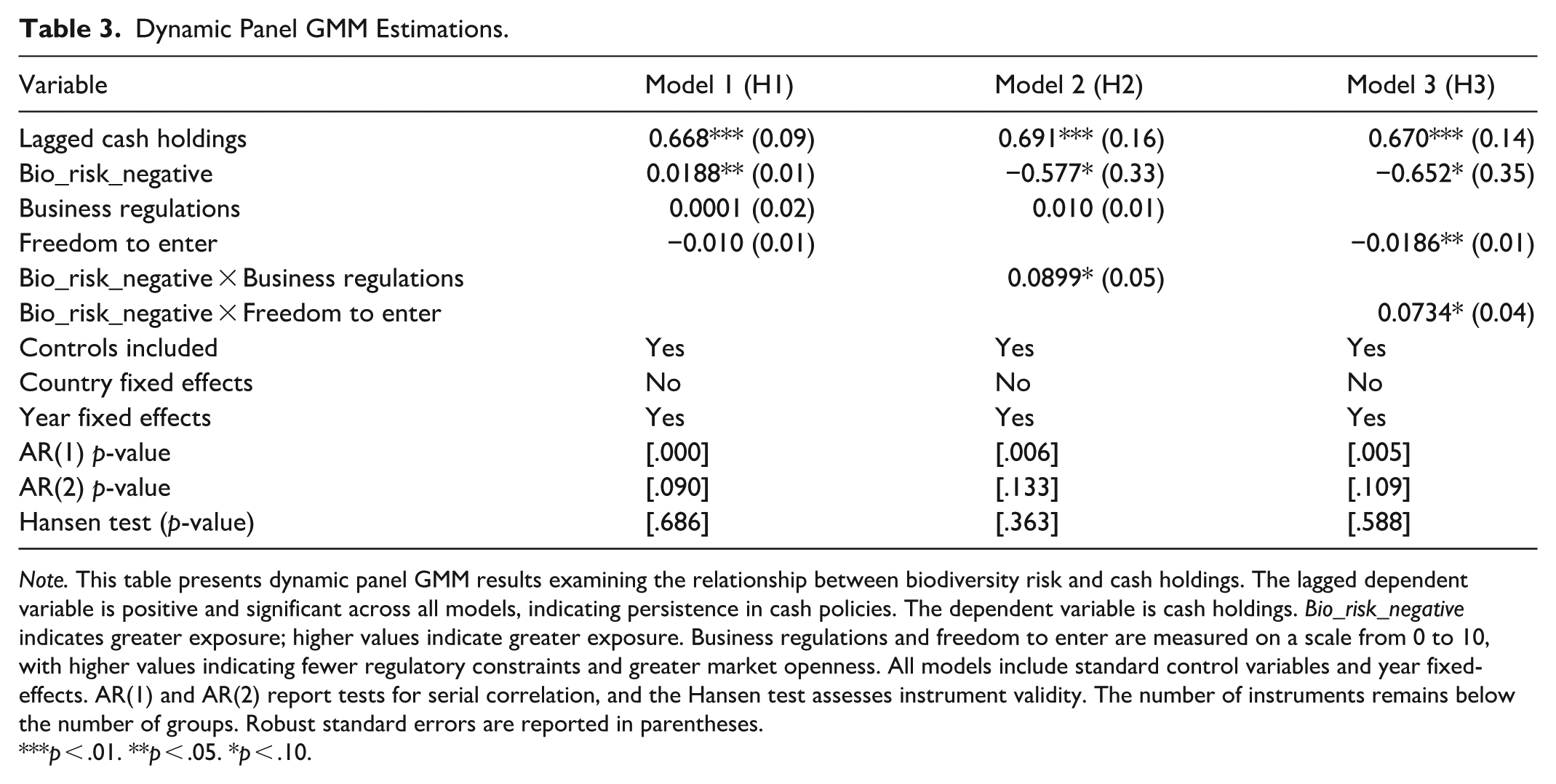

To address potential endogeneity concerns and account for the persistence of firms’ cash-holding policies, we re-estimate our models using a dynamic panel GMM estimator, following Arellano and Bond (1991). This approach allows us to control for unobserved firm-specific heterogeneity, reverse causality, and the dynamic adjustment of liquidity decisions.

The dynamic panel GMM results reported in Table 3 confirm the persistence of firms’ liquidity behavior, as the coefficient on lagged cash holdings remains positive and highly significant across all specifications (0.668–0.691, p < .01). 2 In the model testing H1, Bio_risk_negative exhibits a positive, statistically significant effect on cash holdings (β = .0188, p < .05), reinforcing the baseline finding that firms respond to biodiversity-related uncertainty by increasing precautionary liquidity buffers.

Dynamic Panel GMM Estimations.

Note. This table presents dynamic panel GMM results examining the relationship between biodiversity risk and cash holdings. The lagged dependent variable is positive and significant across all models, indicating persistence in cash policies. The dependent variable is cash holdings. Bio_risk_negative indicates greater exposure; higher values indicate greater exposure. Business regulations and freedom to enter are measured on a scale from 0 to 10, with higher values indicating fewer regulatory constraints and greater market openness. All models include standard control variables and year fixed-effects. AR(1) and AR(2) report tests for serial correlation, and the Hansen test assesses instrument validity. The number of instruments remains below the number of groups. Robust standard errors are reported in parentheses.

p < .01. **p < .05. *p < .10.

In the models testing H2 and H3, the coefficient on biodiversity risk is negative (β = −.577 and −.652, p < .10). However, as in the fixed-effects specifications, this coefficient represents the marginal effect when the moderating institutional variables are set to zero, which does not correspond to the typical institutional conditions observed in the sample. Therefore, the economically relevant effect is the conditional marginal effect.

Consistent with H2, the interaction between biodiversity risk and business regulations is positive and statistically significant (β = .0899, p < .10). Given that higher values of the business regulations index indicate less burdensome and more efficient regulatory environments, this result implies that stronger institutional quality amplifies firms’ precautionary liquidity response to biodiversity risk. Similarly, the interaction between biodiversity risk and freedom to enter markets is positive and significant (β = .0734, p < .10), indicating that firms operating in more open and competitive markets are more likely to accumulate cash when exposed to ecological uncertainty. These findings are consistent with the baseline results and confirm that the effect of biodiversity risk on liquidity is conditional on institutional and market environments.

Sensitivity Analyses

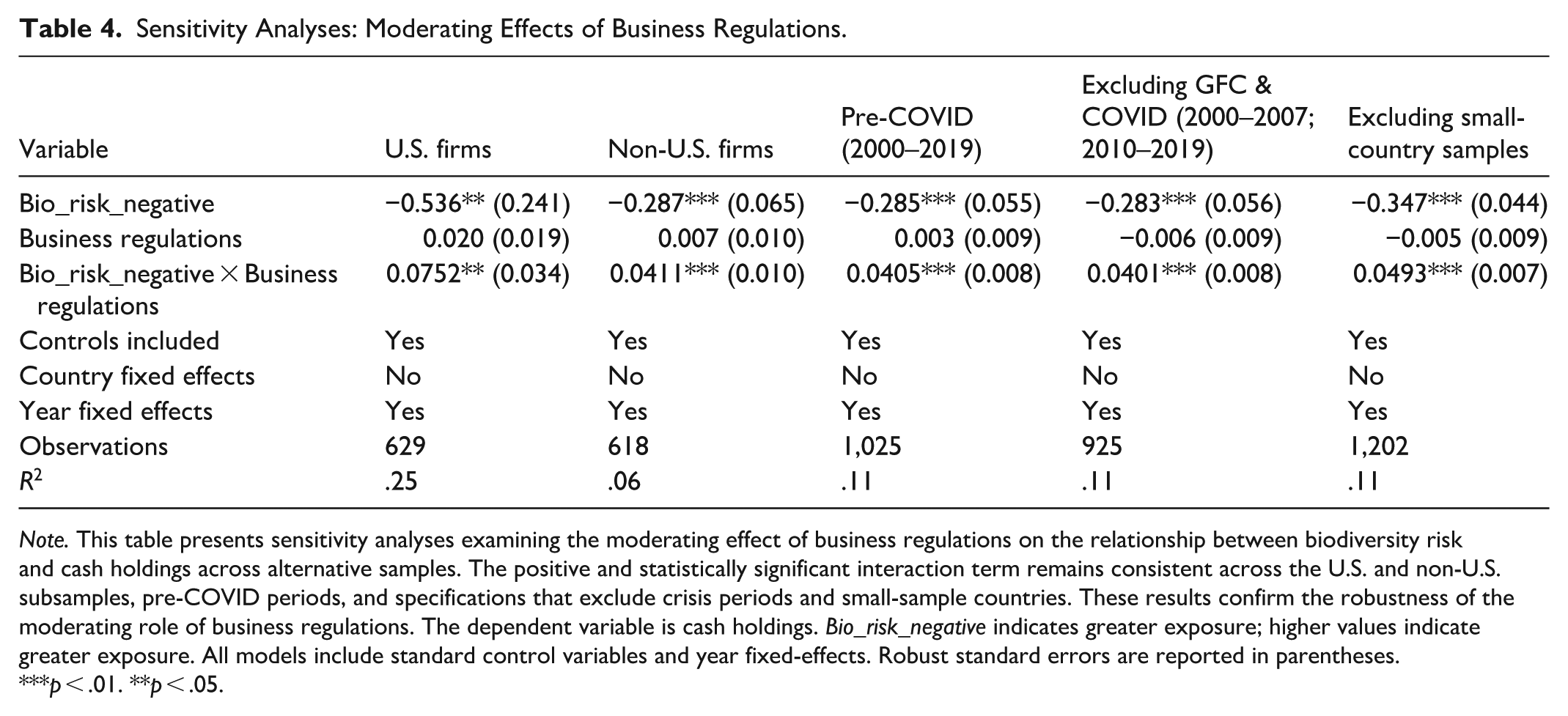

Table 4 provides additional evidence on the moderating role of business regulations across alternative samples and specifications. Across subsamples, the coefficient on biodiversity risk is consistently negative when evaluated at low levels of the institutional moderator, particularly among U.S. firms (−0.536, p < .05) and non-U.S. firms (−0.287, p < .01). This pattern is also observed in robustness checks, including the pre-COVID period (−0.285, p < .01), the exclusion of financial crisis years (−0.283, p < .01), and the removal of countries with limited observations (−0.347, p < .01).

Sensitivity Analyses: Moderating Effects of Business Regulations.

Note. This table presents sensitivity analyses examining the moderating effect of business regulations on the relationship between biodiversity risk and cash holdings across alternative samples. The positive and statistically significant interaction term remains consistent across the U.S. and non-U.S. subsamples, pre-COVID periods, and specifications that exclude crisis periods and small-sample countries. These results confirm the robustness of the moderating role of business regulations. The dependent variable is cash holdings. Bio_risk_negative indicates greater exposure; higher values indicate greater exposure. All models include standard control variables and year fixed-effects. Robust standard errors are reported in parentheses.

p < .01. **p < .05.

Importantly, these coefficients represent the marginal effect of biodiversity risk when business regulations are set to low values and should not be interpreted as the overall effect. The interaction terms provide the relevant economic insight. Across all specifications, the interaction between biodiversity risk and business regulations is positive and statistically significant, with coefficients ranging from 0.0401 to 0.0752; the effect is particularly pronounced for U.S. firms (0.0752, p < .05). This evidence indicates that more efficient and less burdensome regulatory environments strengthen firms’ precautionary liquidity response to biodiversity risk.

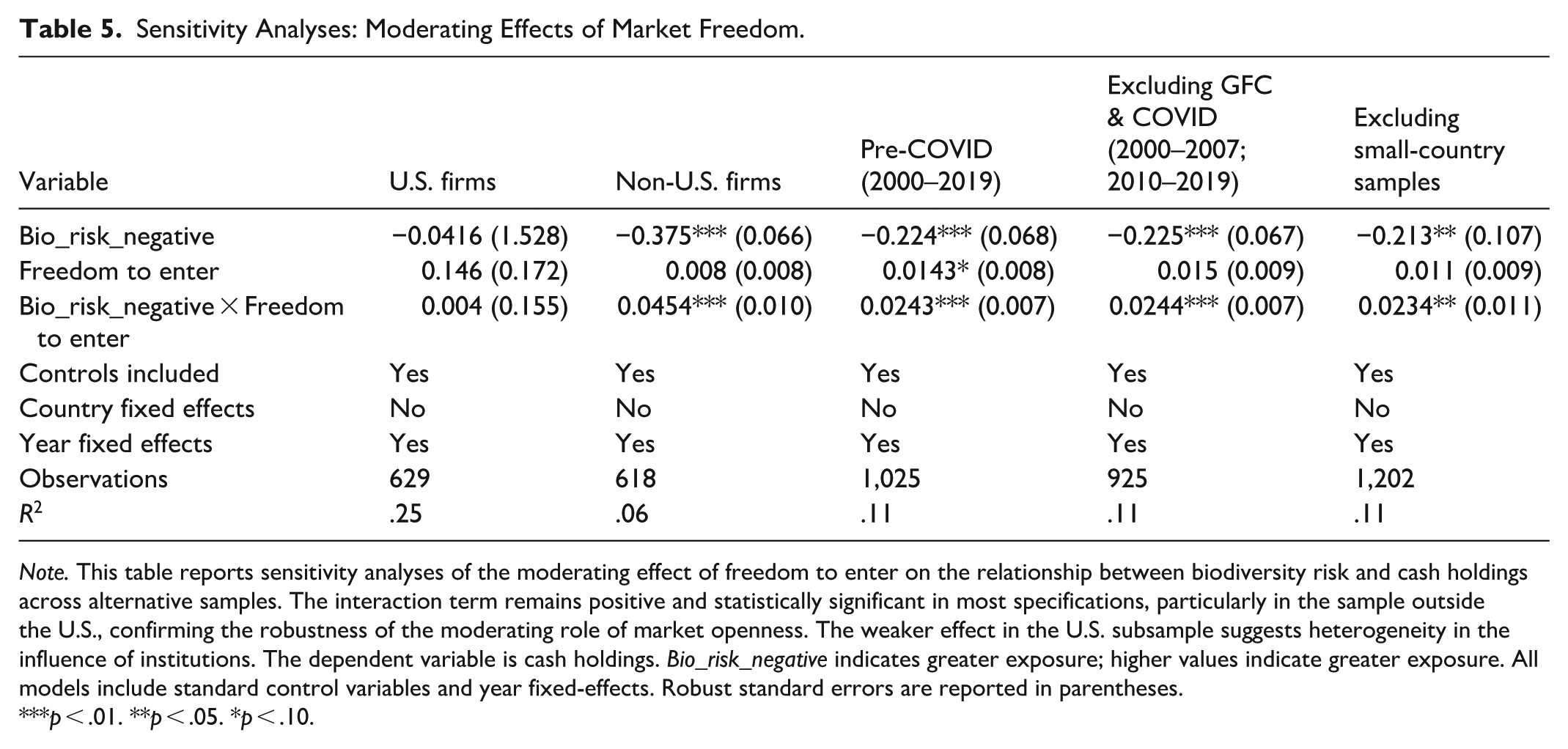

Table 5 extends the analysis to freedom to enter markets. As in previous specifications, the coefficient on biodiversity risk is negative when evaluated at low levels of market openness, particularly for non-U.S. firms (−0.375, p < .01) and across robustness checks: the pre-COVID period (−0.224, p < 0.01), the sample excluding crisis years (−0.225, p < .01), and the sample excluding countries with few observations (−0.213, p < .05). For U.S. firms, the coefficient is statistically insignificant, suggesting heterogeneity across institutional contexts.

Sensitivity Analyses: Moderating Effects of Market Freedom.

Note. This table reports sensitivity analyses of the moderating effect of freedom to enter on the relationship between biodiversity risk and cash holdings across alternative samples. The interaction term remains positive and statistically significant in most specifications, particularly in the sample outside the U.S., confirming the robustness of the moderating role of market openness. The weaker effect in the U.S. subsample suggests heterogeneity in the influence of institutions. The dependent variable is cash holdings. Bio_risk_negative indicates greater exposure; higher values indicate greater exposure. All models include standard control variables and year fixed-effects. Robust standard errors are reported in parentheses.

p < .01. **p < .05. *p < .10.

The interaction terms again provide consistent evidence. The coefficient on Bio_risk_negative × Freedom to enter markets is positive and statistically significant across all specifications, with values ranging from 0.023 to 0.045. The effect is strongest among non-U.S. firms (0.0454, p < .01), indicating that more open and competitive markets amplify firms’ precautionary response to biodiversity risk. These results support H3 and confirm that market openness enhances firms’ ability to adjust liquidity in response to environmental uncertainty.

Taken together, the results from Tables 4 and 5 reinforce earlier findings, showing that the effect of biodiversity risk on cash holdings is conditional on institutional quality. In weaker institutional environments, characterized by more restrictive regulation or limited market openness, firms appear less able to accumulate precautionary liquidity. In contrast, in more efficient regulatory frameworks and more competitive markets, biodiversity risk leads to increased cash holdings, consistent with precautionary and strategic liquidity management.

Overall, these findings provide robust support for H1, H2, and H3 and highlight that firms’ financial responses to biodiversity risk are heterogeneous and shaped by institutional conditions. The results demonstrate that institutional quality not only influences baseline financial behavior but also determines how firms adapt to environmental uncertainty.

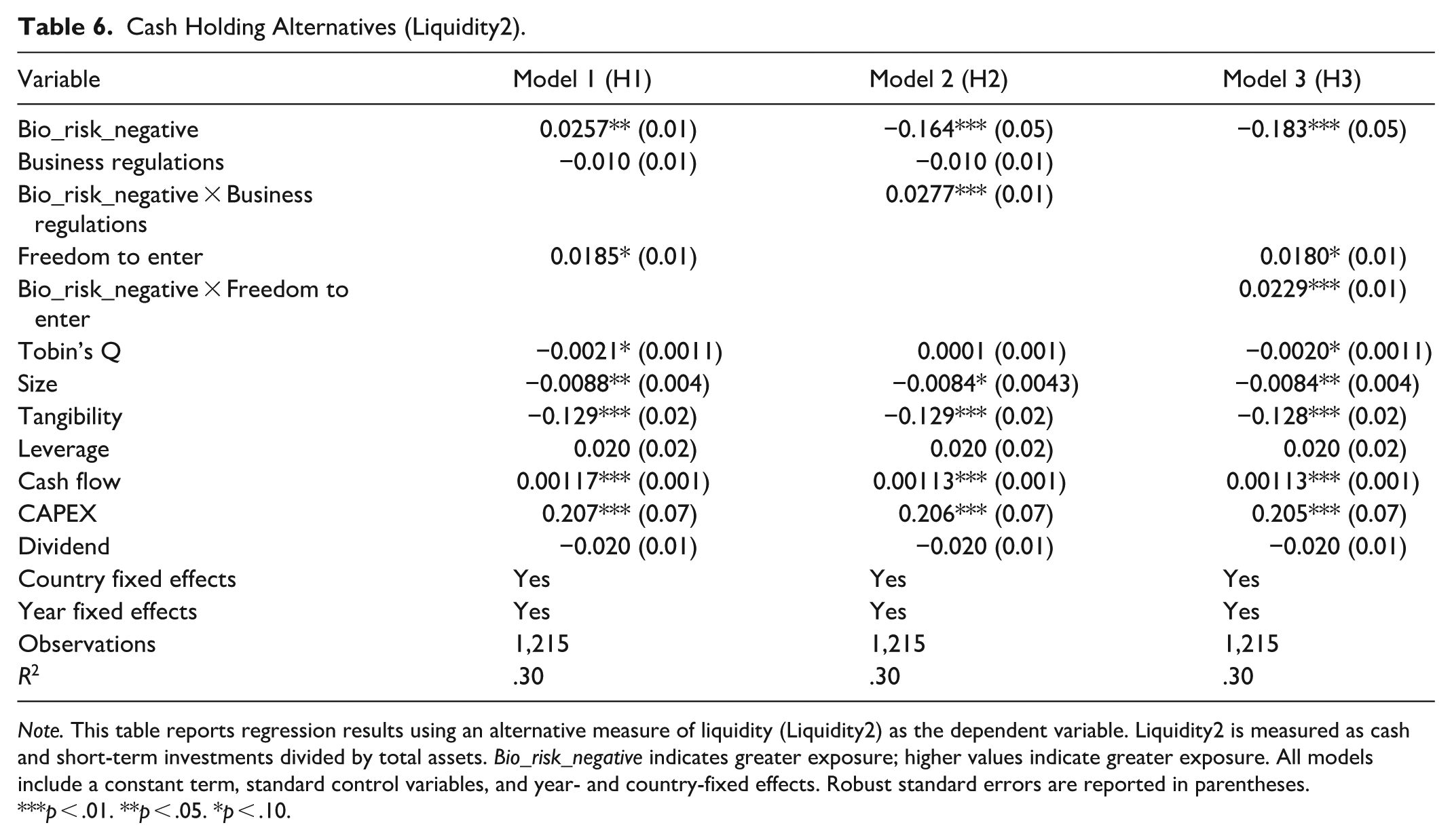

Alternative Measures of Liquidity

To assess the robustness of our findings to alternative definitions of liquidity, we re-estimate the models using two commonly employed proxies. Specifically, Liquidity2 is defined as cash and short-term investments divided by total assets (Al Mamun et al., 2024), while Liquidity3 is defined as cash and cash equivalents divided by net assets (total assets minus cash and cash equivalents) (Tran et al., 2025).

Table 6 reports the results using Liquidity2. Consistent with the baseline findings, Bio_risk_negative is positively and significantly associated with liquidity in Model 1 (β = .0257, p < .05), supporting H1. When interaction terms are introduced, the coefficient on biodiversity risk becomes negative, reflecting the marginal effect evaluated at low levels of the institutional moderators. The interaction terms again provide the economically relevant interpretation. The interaction between Bio_risk_negative and business regulations is positive and statistically significant (β = .0277, p < .01), indicating that more efficient and less burdensome regulatory environments strengthen firms’ precautionary liquidity response to biodiversity risk. Similarly, the interaction between Bio_risk_negative and freedom to enter markets is positive and significant (β = .0180, p < .10), suggesting that greater market openness amplifies firms’ liquidity adjustments under ecological uncertainty.

Cash Holding Alternatives (Liquidity2).

Note. This table reports regression results using an alternative measure of liquidity (Liquidity2) as the dependent variable. Liquidity2 is measured as cash and short-term investments divided by total assets. Bio_risk_negative indicates greater exposure; higher values indicate greater exposure. All models include a constant term, standard control variables, and year- and country-fixed effects. Robust standard errors are reported in parentheses.

p < .01. **p < .05. *p < .10.

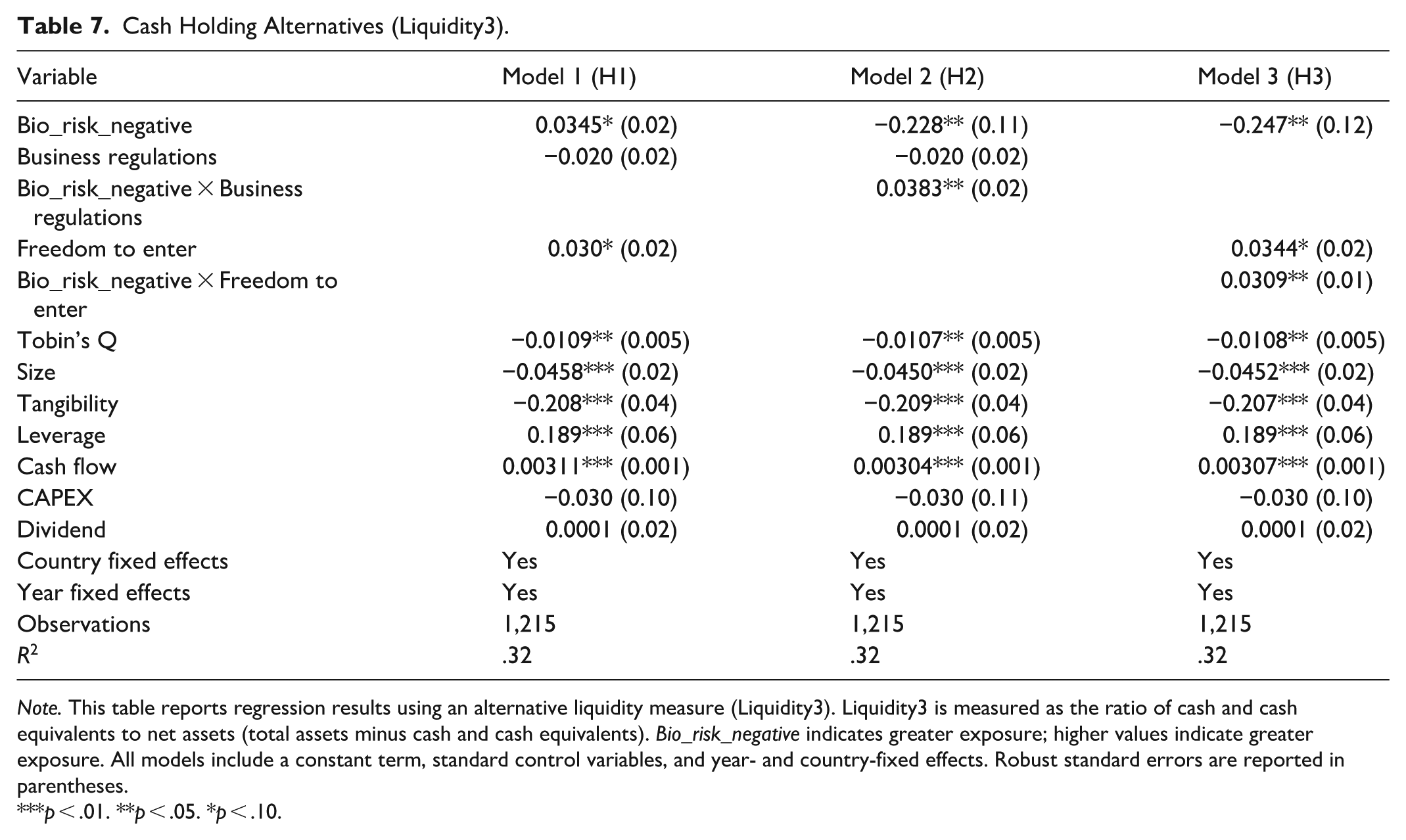

Table 7 presents the results using Liquidity3. The findings remain qualitatively consistent with both the baseline results and those reported in Table 6. Bio_risk_negative continues to exhibit a positive and significant association with liquidity in the baseline specification, while the interaction terms with business regulations and freedom to enter markets remain positive and statistically significant.

Cash Holding Alternatives (Liquidity3).

Note. This table reports regression results using an alternative liquidity measure (Liquidity3). Liquidity3 is measured as the ratio of cash and cash equivalents to net assets (total assets minus cash and cash equivalents). Bio_risk_negative indicates greater exposure; higher values indicate greater exposure. All models include a constant term, standard control variables, and year- and country-fixed effects. Robust standard errors are reported in parentheses.

p < .01. **p < .05. *p < .10.

Overall, these results confirm that the main findings are robust to alternative measures of liquidity. In particular, the conditional effect of biodiversity risk and the moderating roles of institutional quality and market openness remain stable across alternative liquidity measures.

Discussion and Implications

This paper examines how biodiversity risk shapes liquidity decisions in global tourism firms and how institutional environments condition this relationship. The findings provide consistent evidence that biodiversity risk is associated with higher cash holdings, supporting the precautionary motive under ecological uncertainty. Moreover, the results show that business regulations and freedom to enter markets amplify this relationship, highlighting the importance of institutional and competitive contexts in shaping firms’ financial responses to environmental risk.

These findings extend prior research in both tourism and finance. While earlier studies have primarily focused on the ecological and operational consequences of biodiversity loss (Hall, 2019; Scott & Gössling, 2022), our findings demonstrate that biodiversity risk is also financially material, influencing core corporate policies such as liquidity management. In doing so, our paper responds to recent calls to integrate environmental risks more explicitly into firm-level financial decision-making (Flammer et al., 2025; Giglio et al., 2026).

Theoretical Implications and Contributions

This paper contributes to the literature in three important ways. First, it advances the emerging literature on biodiversity and finance by identifying liquidity management as a key channel through which firms respond to biodiversity risk. Although prior studies have documented the valuation and financing implications of biodiversity exposure (Flammer et al., 2025; Garel et al., 2024), evidence on internal financial policies remains limited. By showing that biodiversity risk increases cash holdings, this paper extends the Precautionary Motive Theory (Opler et al., 1999) to a new and underexplored domain of environmental risk. Importantly, biodiversity risk differs from other forms of uncertainty, such as climate risk (Gao & Zhang, 2024) or geopolitical risk (Gozgor et al., 2022), in that it is location-specific, less reversible, and directly tied to tourism demand, making liquidity adjustments particularly salient in this context.

Second, the paper contributes to tourism research by integrating financial decision-making into the analysis of environmental dependency. The existing tourism literature has emphasized the ecological and reputational consequences of biodiversity loss (Scott & Gössling, 2022) but has paid limited attention to firm-level financial strategies. By linking biodiversity risk to liquidity behavior, this study bridges tourism research and corporate finance, offering a more comprehensive understanding of how tourism firms manage environmental exposure. This integration is particularly relevant given the sector’s reliance on natural capital and its vulnerability to ecosystem degradation (Lenzen et al., 2018).

Third, the paper highlights the important moderating role of institutional environments. Consistent with Institutional Theory (DiMaggio & Powell, 1983), we find that business regulations strengthen the relationship between biodiversity risk and cash holdings, suggesting that regulatory frameworks increase the salience and enforceability of environmental risks. At the same time, the results support insights from Industrial Organization Theory (Bain, 1956), showing that freedom to enter markets amplifies precautionary liquidity behavior by intensifying competitive pressures. These findings refine prior work on regulation and finance (Demirgüç-Kunt & Maksimovic, 1998; Djankov et al., 2002; Klapper et al., 2006) by demonstrating that institutional effects are heterogeneous and interact with environmental risk exposure in shaping corporate policies.

In summary, the paper offers a more integrated theoretical framework that combines precautionary motives, institutional pressures, and market competition to explain how firms respond to biodiversity risk.

Managerial Implications

Our findings also have several implications for managers in tourism firms. First, biodiversity risk should be explicitly incorporated into financial planning and liquidity management. As the results indicate, firms exposed to ecological uncertainty benefit from maintaining higher liquidity buffers to manage potential disruptions, including regulatory changes, demand shocks, and operational constraints. Therefore, managers should treat biodiversity risk not only as an environmental issue but also as a core financial risk that requires proactive liquidity strategies.

Second, liquidity can serve as a strategic tool rather than merely a defensive buffer. Consistent with the transaction motive (Opler et al., 1999), firms with sufficient cash reserves are better positioned to invest in sustainability initiatives, such as eco-certifications, conservation partnerships, and nature-based tourism offerings. These investments can enhance competitive positioning and align with growing consumer demand for environmentally responsible tourism (Casado-Díaz et al., 2014).

Third, managers should consider the institutional context in which they operate. In more regulated environments, firms should anticipate higher compliance costs and stricter environmental standards, reinforcing the need for precautionary liquidity. Similarly, in markets with greater openness to entry, firms should maintain financial flexibility to respond to competitive pressures and innovation dynamics. This finding highlights the importance of aligning financial policies with both environmental exposure and market structure.

Policy and Regulatory Implications

The results also have important implications for policymakers and regulators. First, the findings suggest that biodiversity-related regulations have indirect financial consequences for firms. Although such regulations are essential for environmental protection, they may increase firms’ precautionary demand for liquidity by raising compliance costs and uncertainty. Therefore, policymakers should consider tourism firms’ financial capacity when designing biodiversity-related policies, particularly in regions where firms face limited access to external financing.

Second, the positive moderating role of efficient business regulations indicates that well-designed regulatory frameworks can enhance firms’ responsiveness to environmental risks. Clear, transparent, and predictable regulations reduce ambiguity and encourage firms to internalize biodiversity risks more effectively. This finding supports the view that regulatory quality, rather than regulatory stringency alone, is critical for achieving both environmental and economic objectives (Ambec et al., 2013).

Third, market structure plays a key role in shaping firms’ financial behavior. Greater freedom to enter markets intensifies competition, which in turn affects firms’ precautionary responses to biodiversity risk. Therefore, policymakers should recognize that competitive markets can strengthen firms’ incentives to adopt financially resilient and environmentally responsive strategies. However, greater competition may also increase financial pressures on smaller firms, suggesting a need for supportive policies, such as access to green financing or targeted subsidies for sustainability investments.

In short, the findings highlight the importance of coordinated policy frameworks that align environmental regulation, market structure, and financial support mechanisms to enhance the tourism sector’s resilience to biodiversity loss.

Conclusion

This paper examines how biodiversity risk influences liquidity decisions in tourism firms and how institutional and market conditions shape this relationship. Using a panel of 1,247 firm-year observations from publicly listed tourism firms across 27 countries from 2000 to 2022, the findings show that biodiversity risk is positively associated with cash holdings, consistent with a precautionary response to ecological uncertainty. This relationship is stronger in environments characterized by more efficient business regulations and greater market openness, highlighting the importance of institutional and competitive contexts in shaping firms’ financial behavior. Dynamic panel data estimations further confirm the persistence of liquidity policies and support the robustness of the results.

These findings demonstrate that biodiversity risk is not only an environmental concern but also a determinant of firms’ financial strategies. The results suggest that tourism firms adjust their liquidity policies in response to ecological exposure, and that these responses vary with the institutional and market environments in which they operate.

However, this study is subject to limitations. First, the analysis focuses on publicly listed tourism firms, which may limit the generalizability of the findings to privately held firms and small and medium-sized enterprises (SMEs). These firms often face tighter financing constraints and may adopt different liquidity strategies when exposed to biodiversity risk. Second, biodiversity risk is measured using aggregated indicators that may not fully capture firms’ exposure to local ecosystem conditions or operational dependencies on natural assets.

At this stage, future papers can address these limitations in several ways. First, extending the analysis to SMEs and privately held tourism firms would provide a more comprehensive understanding of how biodiversity risk affects financial behavior across the sector. Qualitative and mixed-method approaches, such as case studies and interviews, can offer deeper insights into how managers perceive and respond to biodiversity-related risks in practice. Second, future papers can explore how biodiversity risk interacts with other environmental and macroeconomic uncertainties to jointly influence corporate financial strategies.

Supplemental Material

sj-pdf-1-jtr-10.1177_00472875261460094 – Supplemental material for Biodiversity Risk and Liquidity in Global Tourism Firms

Supplemental material, sj-pdf-1-jtr-10.1177_00472875261460094 for Biodiversity Risk and Liquidity in Global Tourism Firms by Giray Gozgor, Jing Li, Mahdi Mousavi and Ayotola Owolabi in Journal of Travel Research

Footnotes

Author Contributions

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.