Abstract

This paper documents the early-source determinants of retirement planning and financial literacy in China. Taking the 1959–1961 China Famine as a natural experiment, it compares the probability of retirement planning and the level of finance literacy in 2014 for the famine-affected cohorts (1953–1961) with those non-affected cohorts (1962–1963) born in provinces with varying famine severity. Taking advantage of a newly added module in 2014 China Family Panel Studies to construct a measure of financial literacy, this paper finds that nutritional deprivation in utero and during early childhood negatively affects financial literacy in older age. As a result of lower financial literacy, these individuals also report lower likelihoods of retirement planning. Further investigations suggest that impairments of cognitive ability are a likely channel through which famine impacts financial literacy and retirement planning, consistent with the notion that the cost of developing a retirement savings plan is higher for cognitively disadvantaged individuals.

Introduction

There is substantial heterogeneity in people's financial literacy level, even among individuals within the same birth cohort sharing similar educational attainment and socioeconomic status (van Rooij et al., 2012). 1 Financial literacy is a strong predictor for a wide range of financial outcomes (e.g., stock market participation) and is considered a critical determinant of household wealth inequality (Lusardi et al., 2017; van Rooij et al., 2011). Recent studies show that financial literacy also matters for financial well-being in older age as it affects wealth accumulation via retirement planning (Banks, 2010; Lusardi & Mitchell, 2008; van Rooij et al., 2012).

Against the backdrop of a vast trend of social security reforms worldwide, individuals are increasingly being asked to manage their own financial well-being in retirement (Lusardi et al., 2017). China is no exception (Fang & Feng, 2018). Yet evidence shows that a majority of Chinese households are not well prepared for their retirement (Niu et al., 2020). A predominant view is that it is because people lack the relevant financial knowledge to come up with a retirement plan, which leads them to be in a low retirement readiness status (Clark et al., 2011; Lusardi & Mitchell, 2008; Niu et al., 2020; Niu & Zhou, 2018; van Rooij et al., 2012). While relatively well-established is the positive link between financial literacy and retirement planning, the question regarding the sources of financial literacy remains largely unanswered. 2

This paper traces an individual's financial literacy and retirement planning back to his (her) circumstances experienced early in life. A large body of literature shows that early-life shocks experienced while in utero and during childhood can generate substantial long-term consequences. 3 However, whether early-life circumstances also play a role in determining financial literacy has not been well explored so far. 4 In this paper, we ask whether children exposed to adverse shocks in utero and during childhood report a lower propensity for retirement planning in older age. If the answer is yes, then relatedly, are these children also less financially literate? By providing answers to these questions, this paper therefore sheds light on the question of to what extent public policies can help to improve people's financial literacy and awareness of retirement planning. If financial literacy begins to arise at a very early age, then public policies that help adversely affected individuals catch up would generate large welfare gains.

To this end, we leverage the 1959–1961 China Famine as a natural experiment and employ a difference-in-differences (DiD) research design to identify the effect of early-life famine exposure on retirement planning and financial literacy in older age. Following the convention of the “fetal origin hypothesis” literature (Almond, 2006; Almond et al., 2009; Almond & Currie, 2011; Cronqvist et al., 2016), causal impacts can be (potentially) identified by comparing outcome trends of cohorts born before and during the famine to cohorts born shortly after the famine, across regions with low versus high famine severity, while controlling for a vector of individual characteristics as well as a set of fixed effects.

The Chinese context provides an ideal setting for testing the “fetal origin” hypothesis. First, the 1959–1961 China Famine was one of the largest natural disasters in human history which killed more than 16.5 million people and is documented to have detrimental consequences on a variety of long-term outcomes (Almond et al., 2010; Chen & Zhou, 2007; Meng & Qian, 2009). It was largely unexpected at that time and was thus exogenous to individuals, which mitigates the concern of selective migration bias (Caruso, 2017). Second, a new module with 13 financial questions was first added to the 2014 China Family Panel Studies (CFPS) data. This small change provides a unique opportunity for Chinese researchers to assess households’ financial literacy by constructing a financial literacy index using the standard factor analysis techniques. 5 With financial literacy data in hand, together with measures on retirement planning and many other control variables, it is therefore feasible to explore whether late-life financial literacy level and retirement planning likelihood are shaped early in life. Additionally, the birth cohorts considered in this paper are all very close to their retirement ages (60 for men and 55 for women). Even the youngest individual of the famine-affected cohort (born in 1961) was already 53 years old when he (she) was surveyed in 2014. These settings make it particularly appealing to investigate the impacts of early-life famine exposure on financial planning for old people in China. 6

Considering that the impact of famine on retirement planning for individuals exposed in utero and during early childhood (slightly older) may operate through divergent channels and therefore exhibit potentially differential patterns in terms of signs and magnitudes, cohort-specific coefficients are reported throughout the paper. Cohorts are defined according to their birth timing relative to the famine. In the baseline case, all famine-affected individuals are divided into three broadly defined cohorts at a three-year window. However, in robustness checks, cohorts are defined yearly in that individuals with identical birth years are grouped into the same cohort. Defining cohorts in this way can capture the potential heterogeneous retirement planning effects of famine for individuals entering retirement versus those slightly younger. For instance, the 1953, 1954, and 1955 cohorts in 2014 were 61, 60, and 59 years old, respectively, and all of them fall into the one-year radius of the full retirement age for males in China.

This paper finds that the probability of retirement planning in older age is significantly lower for famine-affected cohorts, compared with those who were born shortly after the famine. The impacts on all three cohorts are negative and are statistically significant at conventional levels. The impacts are also economically meaningful. A one standard deviation increase in the intensity of famine exposure decreases the likelihood of retirement planning by 0.122 percentage points to 0.190 percentage points for different cohorts. Estimation results of the impact on financial literacy are also similar. Coefficients are negative, consistent with the notion that the cost of developing a retirement plan is higher for less financially literate individuals. 7 Additionally, estimation results of yearly defined cohort-specific regressions show remarkable heterogeneous impacts across cohorts. Although remains negative, coefficients in retirement planning regressions are only significantly observed for individuals in the 1953, 1954, 1956, and 1960 cohorts. Furthermore, it shows that the negative impacts on retirement planning are larger in absolute value for older individuals and for those already retired individuals.

Having established a negative relationship between early-life famine exposure and retirement planning (financial literacy), this paper posits that decreases in cognitive ability are the main driving force behind this empirical pattern. This conjecture is subsequently verified by the finding that famine-affected cohorts score substantially lower in numeracy tests and attain significantly fewer education years. It makes sense that malnutrition in utero and nutritional deprivation in early childhood drive declines in cognitive ability and ultimately result in lower education attainment. These findings are intrinsically consistent with the well-established fact that numeracy is a special aspect of cognitive ability and a critical contributor to financial literacy (Banks et al., 2010; van Rooij et al., 2011, 2012). Hence, it is not surprising that famine-affected cohorts are also less financially sophisticated and exhibit a lower likelihood of retirement planning.

Despite that we interpret the reduced educational attainment as evidence of impaired cognitive ability, we cannot rule out the possibility that the impact of famine on retirement planning and financial literacy also operates through other pathways. This is because reductions in educational attainment are also consistent with famine-affected children being more impatient and less risk-tolerant (Dohmen et al., 2010, 2018; Falk et al., 2018). Using self-assessed measures of impatience and risk aversion and taking advantage of the heterogeneous framework of empirical specifications, this paper also finds suggestive evidence of a risk preference channel. It shows that children who experienced famine during early childhood (around 2–6 years old) are more risk averse than their non-affected counterparts and exhibit less likelihood of retirement planning in older ages. However, the effects are only significant at the 1% level and are only observed for a small part of cohorts.

The rest of this article unfolds as follows. Section 2 conceptually outlines the transmission channels and discusses the related literature. Section 3 presents a brief overview of the background of the China Famine and the Chinese pension system. Section 4 introduces the empirical framework and discusses the identification strategy. Section 5 describes the data and constructs the key variables. Section 6 presents the regression results and Section 7 concludes.

Potential Channels and Related Literature

In-utero and early-childhood exposure to adverse health shocks are causally linked with poor health outcomes such as lower attained height and weight (Chen & Zhou, 2007; Meng & Qian, 2009), early mortality (Black et al., 2007), and even poorer mental health (Adhvaryu et al., 2019). 8 These negative health effects persist into mid-adulthood, late life, and even transfer across generations (Chen & Zhou, 2007; Xie & Zhu, 2022).

Famine typically represents a severe adverse shock to people's health. Despite that the exact mechanisms behind the negative relationship between early-life famine exposure and retirement planning (financial literacy) are not well explored by prior research, at least three channels drive the empirical pattern. First, malnutrition caused by famine can permanently impair an individual's cognition ability. Aguilar and Vicarelli (2022) document that early-life adverse shocks triggered by extreme precipitations in Mexico lead to significantly lower measures of cognitive ability and that the negative impacts are detected as early as 2 years old. Being an important aspect of cognitive ability, numeracy is of pivotal importance in the assessment of basic financial literacy and financial decision-making (Banks et al., 2010; van Rooij et al., 2011, 2012). If famine causes one's cognitive ability to decline permanently and leads to low financial literacy thereof (Muñoz-Murillo et al., 2020), then a negative relationship between famine exposure and retirement planning probably holds.

Second, early-life famine exposure can drive retirement planning (financial literacy) through its impact on time preferences (impatience). The fact that early-life adverse shocks can change an individual's time preference is widely documented in the literature (Cassar et al., 2017; Filipski et al., 2019). For example, Filipski et al. (2019) show that those who lived in the quake areas but did not suffer damages or injuries when an earthquake happened in the Sichuan province of China in 2008 were more impatient after the earthquake. Hence, if early-life famine exposure causes famine-affected individuals to become more impatient, then they might end up accumulating less financial knowledge and are less likely to plan for retirement (Meier & Sprenger, 2013).

Third, early-life famine exposure may negatively influence retirement planning through its impact on risk preferences. Risk preferences are associated with late-life behaviors such as savings, portfolio choices, and wealth accumulation (Falk et al., 2018). Several papers have shown that early-life shocks can permanently alter a person's risk attitude (Bernile et al., 2017; Cameron & Shah, 2015; Cassar et al., 2017; Chriselis et al., 2020; Malmendier & Nagel, 2011). 9 If famine-affected cohorts become more risk-averse potentially because they are more mentally unhealthy and less cognitively able, then they might exhibit less likelihood of retirement planning.

This paper is related to three strands of literature. First, this paper is related to the emerging body of research that explores the determinants of retirement planning, particularly the role played by financial literacy (Bucher-Koenen & Lusardi, 2011; Jappelli & Padula, 2013; Niu & Zhou, 2018; van Rooij et al., 2012). Extant research on the relationship between financial literacy and retirement planning does not clarify how financial literacy is formed, particularly the timing of its formation. This paper extends by linking an individual's financial literacy to the circumstances he (or she) experienced early in life, including in utero and during childhood.

Second, this paper is also related to the “fetal origin” hypothesis literature that highlights the early origins of lifetime outcomes. Since the seminal work of Almond (2006), economists have long been interested in exploring the lifecycle impacts of early-life shocks (Adhvaryu et al., 2020; Almond et al., 2009; Chriselis et al., 2020; Duque & Schmitz, 2025; see Almond & Currie, 2011 for a review), as well as in understanding to what extent can policies mitigate such adverse effects (Aizer et al., 2016; Hoynes et al., 2016; Adhvaryu et al., 2024). In China, several papers have used the 1959–1961 China Famine as a natural experiment to identify the long-term health and socioeconomic outcome impacts of adverse health and nutrition shocks (Almond et al., 2010; Brandt et al., 2016; Chen & Zhou, 2007; Meng & Qian, 2009; Xie & Zhu, 2022). Despite the fruitful findings in terms of outcomes of impact, yet still very little is known about whether a causal relationship also exists between early-life famine exposure and retirement planning (financial literacy).

Third, this paper is also related to the literature that seeks to evaluate the welfare of public policies that help disadvantaged segments of the population improve their financial well-being in older age. A vast body of literature has emphasized the key role of financial literacy in determining retirement planning and post-retirement financial well-being (Bucher-Koenen & Lusardi, 2011; Clark et al., 2011; Lusardi & Mitchell, 2008). Meanwhile, empirical works have repeatedly suggested that financial education programs can be effective in improving households’ financial literacy (Bruhn et al., 2016; Hastings et al., 2013). Grohmann et al. (2015) show that early financial socialization through school and family education is positively associated with financial literacy in adulthood. From a policy perspective of view, this paper's findings suggest that school financial education programs may be effective at fostering retirement savings by increasing financial literacy and retirement planning.

Background

The 1959–1961 China Famine

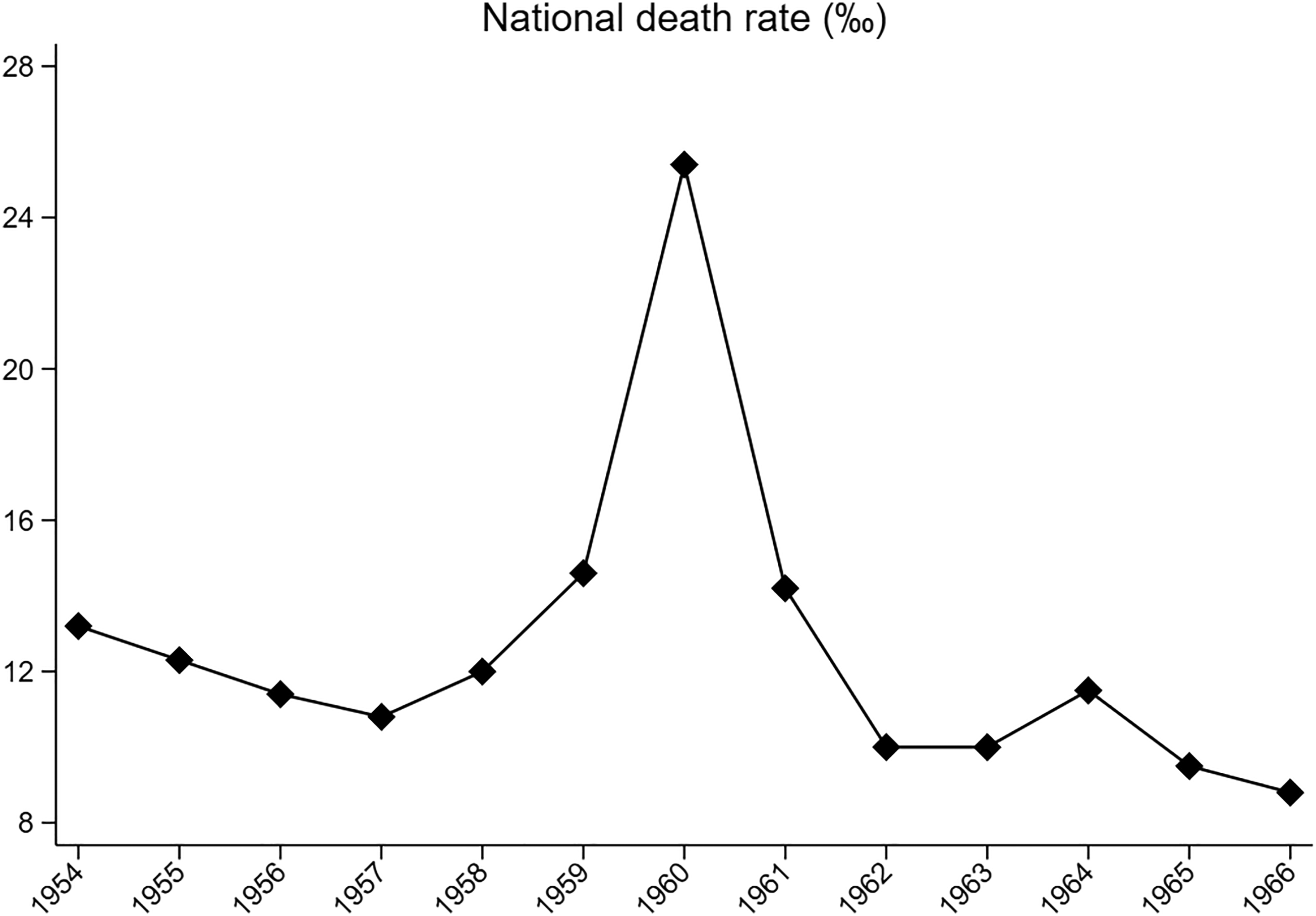

During the twentieth century, approximately 70 million population lost their lives from famine. China is a country where natural disasters are frequently happening, making it among the most heavily hit nations around the globe. The great famine that happened during 1959–1961 was one of the world's largest natural disasters which killed more than 16.5 to 45 million people in just three years, most of whom were rural residents at that time (Meng et al., 2015). The famine led to large surges in the national mortality rate and remarkable decreases in the birth rate, with damages being more severe in rural areas than in urban areas (Brandt et al., 2016). Figure 1 plots the national death rate over time during the 1954–1966 period. It shows that the national death rate was at an all-time high during the 1959–1961 period and peaked in 1960, but quickly dropped to its pre-famine level after the famine's end in 1962.

China's national death rate: 1954–1966.

China's famine that happened during the 1959–1961 period was not totally due to bad weather, even though there was indeed a fall in average agricultural output (Cao et al., 2022). Even after taking into account the fall in agricultural output, aggregate grocery retention in rural areas is still too high to generate famine. Rather, as Brandt et al. (2016) point out, the extent of the famine was largely driven by a set of misguided policies from government procurement of groceries from rural areas. Procurement levels were set in advance according to historical province-specific agricultural outputs and were progressive, meaning that procurement rates were higher in more productive regions. The great leap forward political movement that was carried out in the mid-1950s inefficiently reallocated farmers to less productive industrial sectors, which led to a substantial decrease in the average agricultural output (Cao et al., 2022). However, procurement targets set by the central government were not flexibly adjusted to reflect the drop in agricultural production. As a result, larger shares of expected production were still procured from more productive regions. Over-procurement of grains from rural areas exacerbated the production decline, causing disproportionately severe food shortages in more productive provinces, which ultimately led to famine.

The Chinese Pension System

The multi-layered Chinese pension system consists of three main pillars, referred to as the public pension scheme, corporate pension plans, and personal retirement accounts, respectively.

The first pillar aims to cover the universe of the Chinese population by providing basic social security to all residents. By 2022, the number of population who participate in the public pension scheme amounts to 1.05 billion. The public pension scheme consists of three components: known as the urban employee pension, the urban resident pension, and the new rural resident pension. The urban employee pension scheme was oriented toward employed workers in firms and the government, 10 while the urban and rural resident pension schemes were for non-employed individuals in urban and rural areas. At the end of 2022, the urban employee pension had 503.49 million participants and the urban and rural resident pension had 549.52 million participants.

Different schemes of the public pension system differ in terms of participation, rate of contribution, benefit level, and eligibility requirements. Urban employee pension is mandatory and the contribution is shared jointly between employers and employees. On the benefit side, employees with a contribution history of 15 or more years are eligible for claiming pension benefits. The replacement ratio depends on the number of years of contribution and the individual's wage relative to the local average wage. By contrast, the urban and rural resident pension program is non-mandatory, in which the unemployed and self-employed make voluntary participation decisions and is required to pay a certain amount of contribution if they choose to participate. The benefit that each participant receives is paid both from government funds and the individual account. Participants who are entitled to receive pension benefits are also required to make contributions to the system for at least 15 years.

The second pillar, known as the corporate pension plans (employer-sponsored annuity programs) or (civil servant) occupational pension plans, are considered supplementary to the public pension scheme, i.e., the first pillar. Unlike the broad coverage of the first pillar, participation in the second pillar is much more limited. Only about 80 thousand firms, approximately less than 0.5% of all the firms in China, set up corporate pension plans. And employees who were covered by corporate pension plans were only 23.3 million in 2017 (Fang & Feng, 2018). Finally, tax-preferred household savings-based annuity insurance schemes, such as savings in private accounts and annuity insurance provided by insurance companies, constitute the third pillar. However, the third pillar was not introduced until 2022 and is still in its infancy.

Due to its mandatory nature, most households have access to the public pension, which has been shown to generate positive spillover effects on Chinese households (Huang & Zhang, 2021). However, the benefits it provides are too limited to maintain a comfortable living standard after retirement for most Chinese households. 11 Not surprisingly, Chinese retirees to date are heavily dependent on wealth accumulated during working times to support post-retirement consumption. In China, the homeownership rate is high and home equity wealth makes up the lion's share in the households’ balance sheet while the share of values stored in liquid financial assets such as bonds and stocks is relatively low. Despite that Chinese households hold considerable wealth in the form of housing equity, lacking access to equity release vehicles such as reverse mortgage products greatly limits their abilities to annuitize their housing assets into a stream of income at older age. As a result, savings through bank deposit accounts are still preferred by most Chinese households, which partly explain why China has so high a saving rate in the world.

Empirical Strategy

The “fetal origin” hypothesis literature leverages a treatment effect framework to identify the causal impact of early-life circumstances on long-term outcomes (Adhvaryu et al., 2020; Almond, 2006; Almond et al., 2009; Cronqvist et al., 2016). This methodology typically exploits variations in shock exposure triggered by exogenous events (e.g., natural disasters) by linking birth cohorts to their place of birth, which is exactly the idea of the DiD research design.

This paper follows this convention. My basic strategy is to compare trends in outcomes among individuals exposed in early childhood with those born slightly later, across provinces with high versus low famine severity. Since the 1959–1961 China Famine represents a potentially exogenous shock to individuals, causal effects can be obtained by exploiting the province-by-cohort variations in famine exposure.

Upon implementing a DiD research design, we define as in the treatment group those sampled individuals who were born during the 1953–1961 period. These individuals were born before the famine, which ended in 1962. Among the treated individuals, the 1959–1961 cohort was exposed while in utero and the 1953–1958 cohort in early childhood. Meanwhile, the control group is defined as comprising those who were born during the 1962–1963 period. 12 As a result, famine-affected individuals were 0–6 years old when the famine first occurred.

The empirical specification is presented in equation (1):

Conceptually, we consider the outcomes of three cohorts: those born before (1953–1958), during (1959–1961), and after (1962–1963) the famine. In practice, the before-famine-born cohort is further split into two smaller cohorts: 1953–1955 and 1956–1958. As a result, the sample is composed of Cohort 0 (1962–1963), Cohort 1 (1959–1961), Cohort 2 (1956–1958), and Cohort 3 (1953–1955). Cohort 0 is the control group while the other three cohorts belong to the treatment group. This setting explicitly takes into account two dimensions of heterogeneities: old versus young, and in-utero versus early childhood exposure. In particular, note that individuals in Cohort 3 are within the one-year radius of the full retirement age in 2014.

Besides the specification in equation (1) where cohorts are defined broadly on a three-year basis, we also consider more disaggregated definitions of cohorts. As shown in equation (2), cohorts are defined as individuals who were born in the same year.

In equation (2), the other variables are similarly defined. The control group is defined as those born in 1962 and the treatment group comprises those born before 1962. Therefore,

Data and Variable Construction

Data

The main data used in this paper come from the 2014 China Family Panel Studies (CFPS), a nationally represented household survey that covers households in 29 mainland provinces. The survey is conducted biennially by the Institute of Social Science Survey at Peking University, China. The CFPS was first surveyed in 2008. However, we only picked up the 2014 wave because it is the only wave that aimed at investigating and measuring various aspects of financial knowledge among Chinese people. The CFPS data also contains a rich set of other demographic and socioeconomic characteristics, which allows me to include these characteristics as control variables in the regressions.

Famine Exposure

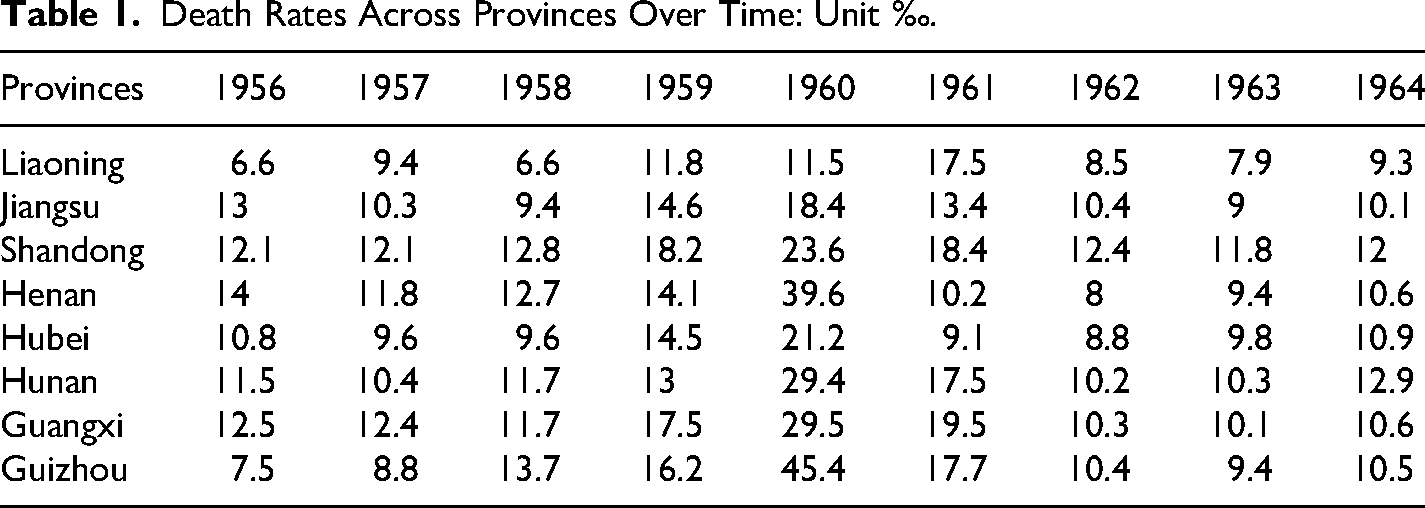

As defined in Section 4, famine exposure is an interaction term of province famine severity and cohort dummies. This subsection focuses on the measurement of province-level famine severity. We define a province's famine severity as the gap between the average death rates three years before the beginning of the famine (1956–1958) and the average death rates of the famine period (1959–1961). Raw data on the death rate is compiled from Chen and Zhou (2007). 13 Even though the 1959–1961 China famine is a nationwide shock that influences all provinces, provinces differ significantly in the extent of famine severity. 14 Table 1 displays the death rate for several selected provinces over the 1956–1964 time period.

Death Rates Across Provinces Over Time: Unit ‰.

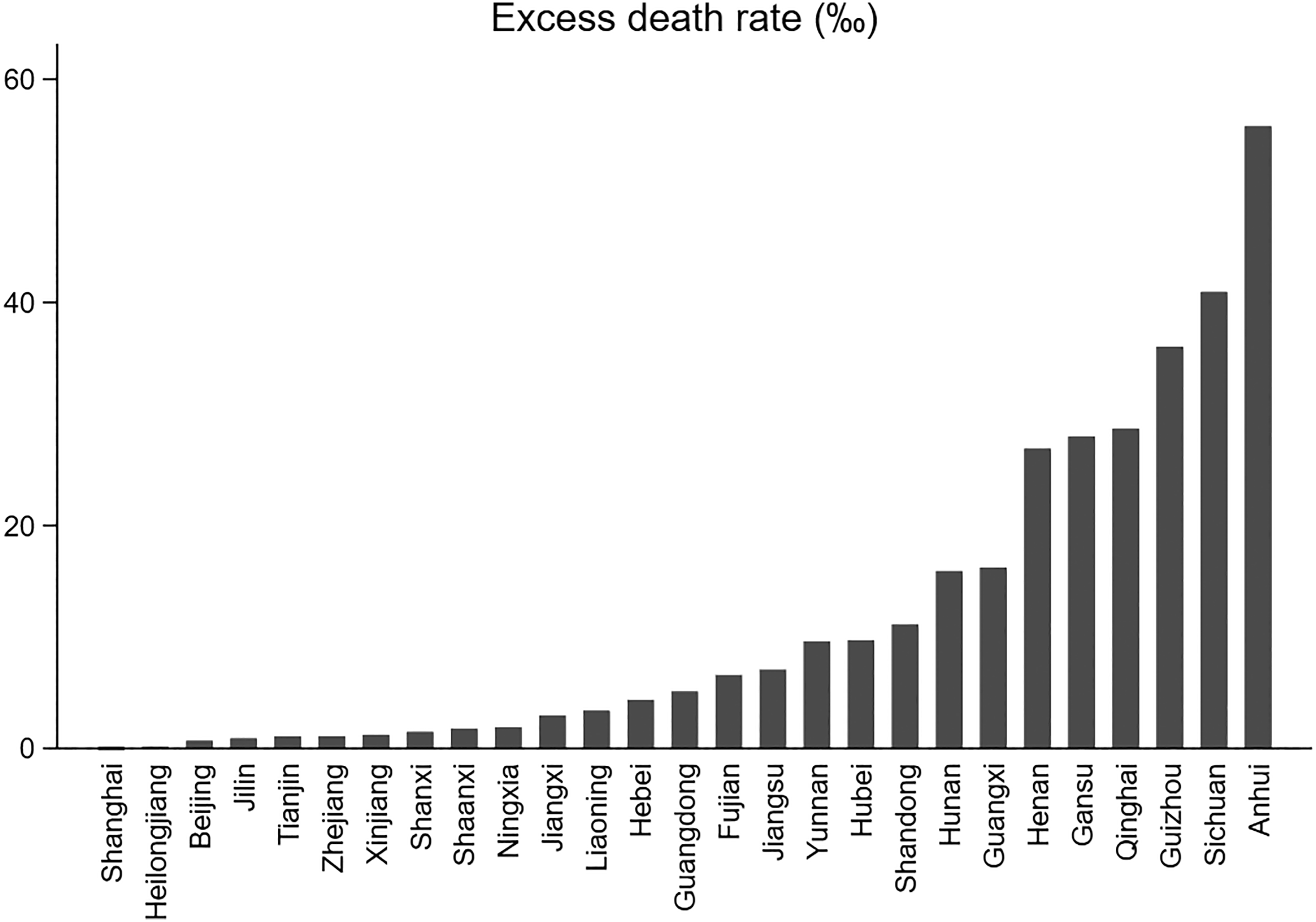

Figure 2 provides additional visual evidence of the variations in famine severity across provinces by plotting the excess death rate of 27 Chinese provinces for which we have data. The average excess death rate is 11.80 and the standard deviation is 14.74. Anhui, Sichuan, Guizhou, and Qinghai are among the top provinces that suffer the most from the famine, while Shanghai, Heilongjiang, Beijing, and Jilin are less affected. For example, the extent of family severity in 1960 in Anhui is over 82-fold as large as in Beijing.

Excess death rate across provinces.

Financial Literacy

The 2014 CFPS survey contains thirteen questions designed to measure financial literacy. Following the literature, these questions are divided into two groups and are utilized to construct basic and advanced financial literacy based on a factor analysis technique (van Rooij et al., 2011, 2012). Following a series of studies in the literature that measure financial literacy in various countries, we distinguish the incorrect answer from the unknown answer in constructing the two kinds of financial literacy indices (Bucher-Koenen & Lusardi, 2011; Hastings et al., 2013; Niu et al., 2020; Niu & Zhou, 2018; van Rooij et al., 2011, 2012). 15

Basic financial literacy is considered a prerequisite for day-to-day transactions and financial decision-making. Questions of this sort are composed of five questions, including contemporaneous interest level in the survey year, numeracy, interest compounding, inflation, and the time value of money, respectively (see Appendix A for details). Similarly, the other eight questions are used to construct the advanced financial literacy index (see Appendix B for details). These are much more complicated questions than their basic counterparts. The advanced questions involve assessments of the awareness of the central bank and knowledge of complex financial instruments such as the functioning of the stock market.

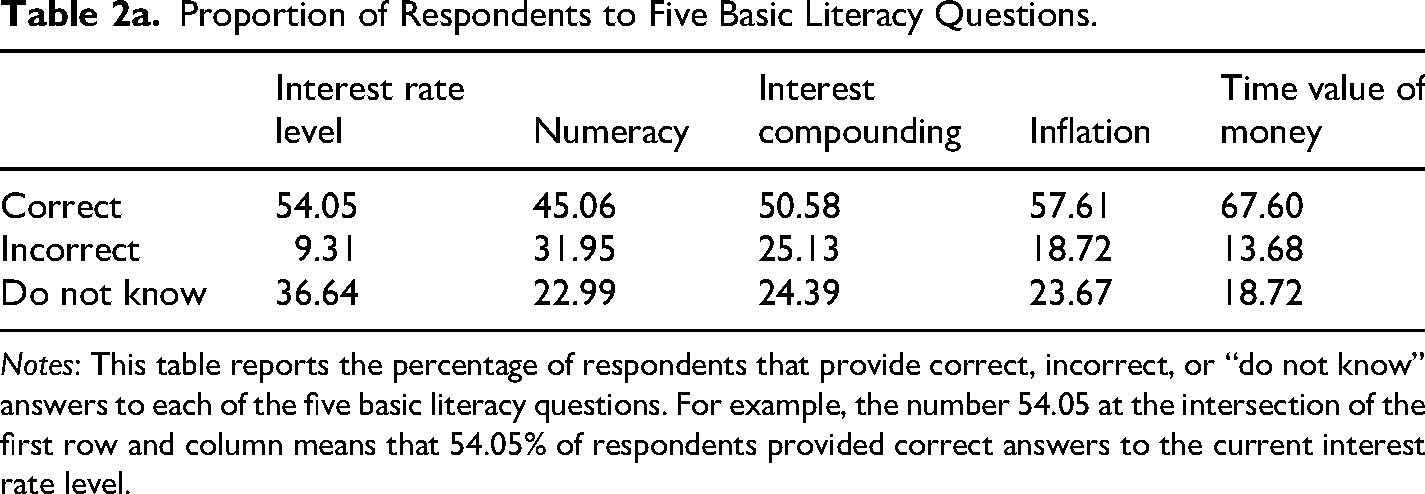

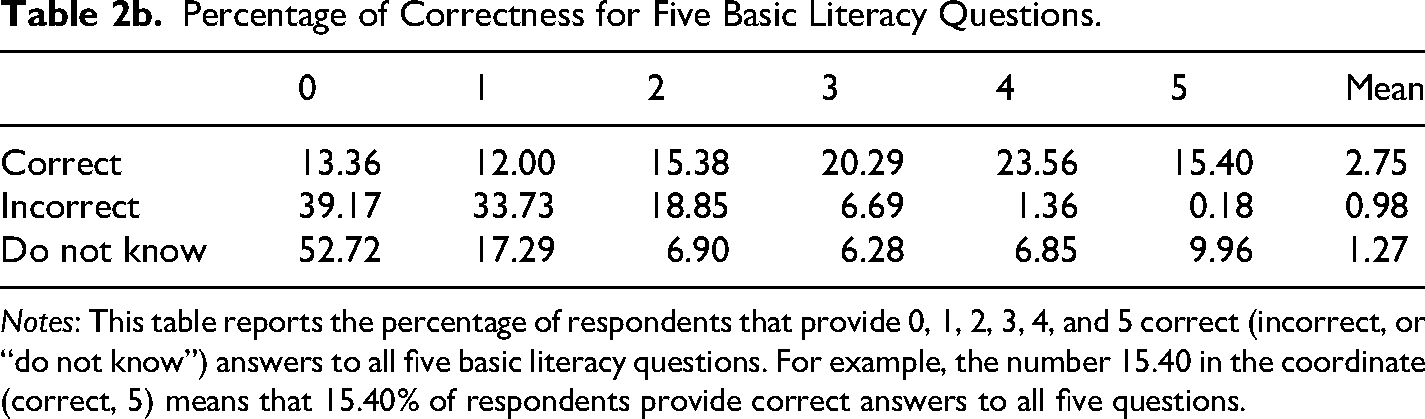

Tables 2 and 3 present answers to five questions for basic financial literacy and eight questions for advanced financial literacy, respectively. Each table consists of two sub-tables. The first sub-tables report the proportion of respondents who provide correct, incorrect, and “do not know” answers to each question, and the second sub-tables report the distribution of correctness for each question.

Table 2a shows that somewhat fewer than seven out of ten respondents provided the correct answer to the understanding of the time value of money. The percentage of correct answers drops to between 50 and 60% when we consider questions on interest level, interest compounding, and inflation. Approximately one-third of respondents provide incorrect answers to the question that relates to numeracy and a similar fraction do not know the current interest rate level in China. A striking observation is that only 15.4% of respondents were able to answer all five questions correctly (Table 2b). Overall, respondents display a very limited understanding of basic financial concepts.

Proportion of Respondents to Five Basic Literacy Questions.

Notes: This table reports the percentage of respondents that provide correct, incorrect, or “do not know” answers to each of the five basic literacy questions. For example, the number 54.05 at the intersection of the first row and column means that 54.05% of respondents provided correct answers to the current interest rate level.

Percentage of Correctness for Five Basic Literacy Questions.

Notes: This table reports the percentage of respondents that provide 0, 1, 2, 3, 4, and 5 correct (incorrect, or “do not know”) answers to all five basic literacy questions. For example, the number 15.40 in the coordinate (correct, 5) means that 15.40% of respondents provide correct answers to all five questions.

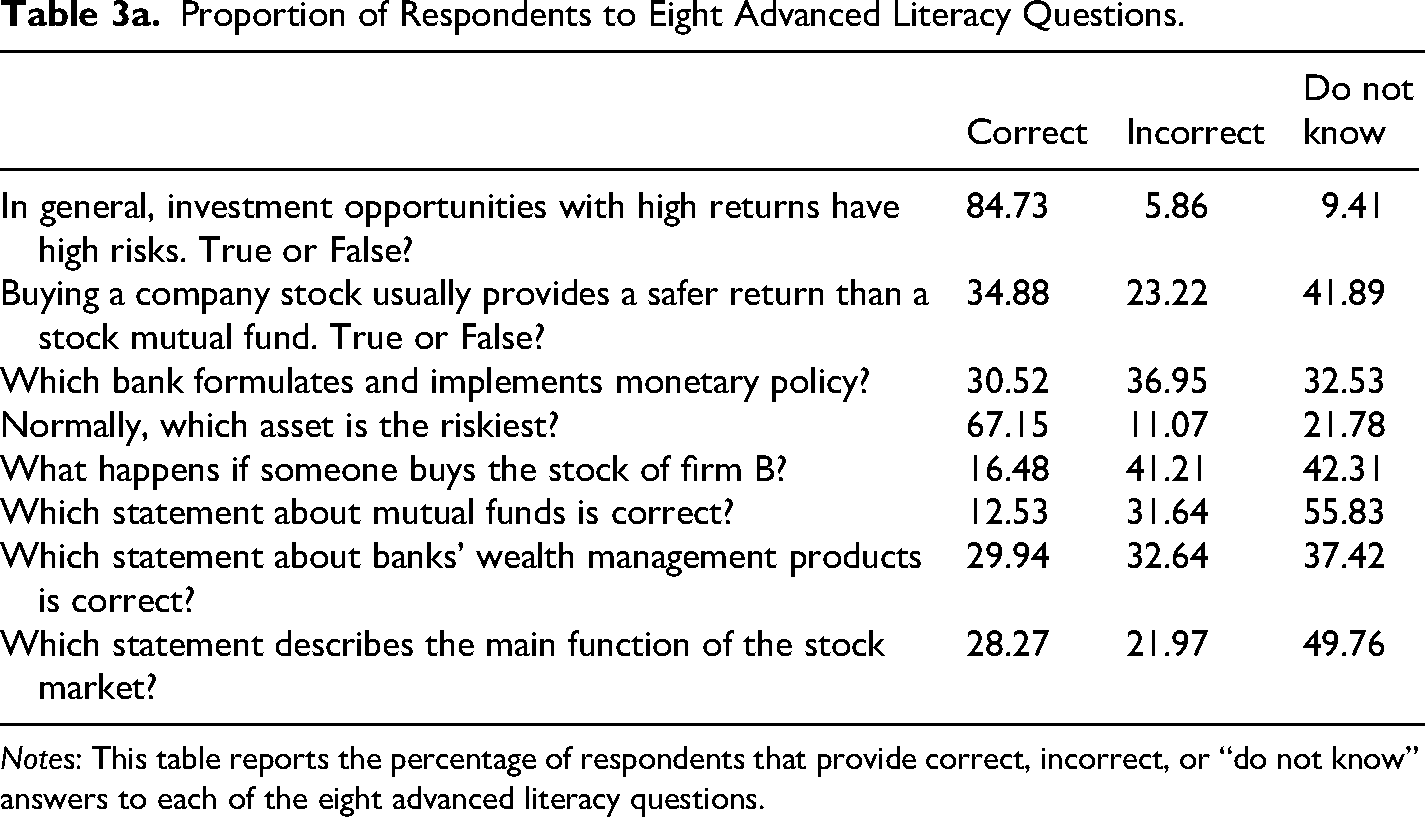

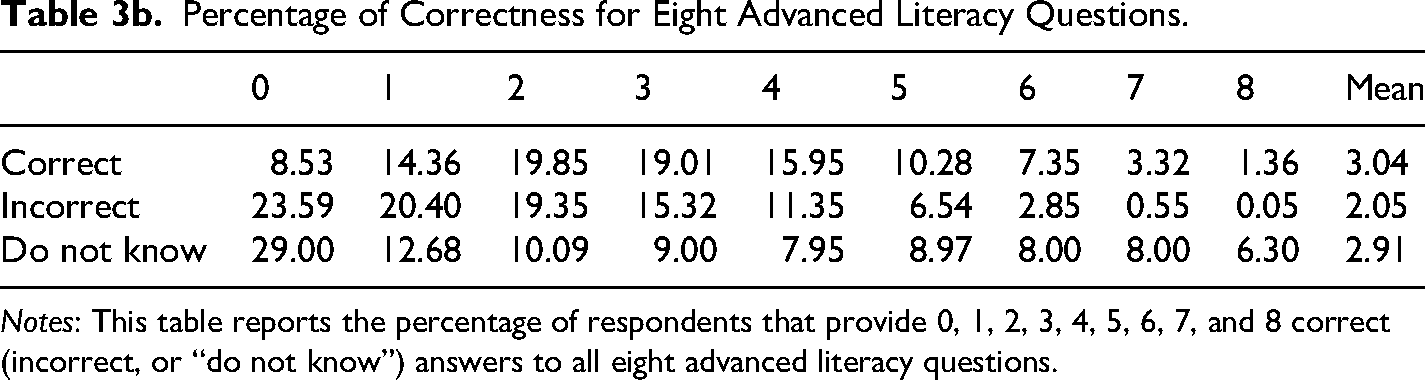

In Table 3a, the fraction of correct answers becomes much lower. For example, only 12.5% of respondents know how mutual funds work, and only 16.5% know how stock works. A notable exception is that 84.7% of respondents are correct about the tradeoff between risk and return. Approximately half of respondents do not know the answer to the question about the main function of the stock market and even more state that they do not know the answer to the question about the workings of mutual funds. Barely more than 1% of respondents provide correct answers to all eight questions (Table 3b). These results reveal the scarcity of advanced financial knowledge among Chinese households.

Proportion of Respondents to Eight Advanced Literacy Questions.

Notes: This table reports the percentage of respondents that provide correct, incorrect, or “do not know” answers to each of the eight advanced literacy questions.

Percentage of Correctness for Eight Advanced Literacy Questions.

Notes: This table reports the percentage of respondents that provide 0, 1, 2, 3, 4, 5, 6, 7, and 8 correct (incorrect, or “do not know”) answers to all eight advanced literacy questions.

Retirement Preparation

Following van Rooij et al. (2012), we use two variables to proxy for retirement planning. The first measure is a dummy variable Retirement Planning, indicating whether a household has ever planned for retirement or not. The second measure is a dummy variable Financial Planning, indicating whether a household has a long-term financial plan or not.

A questionnaire in the 2014 CFPS data set asks “Have you ever tried to figure out how much you need to save for retirement?” We use this question to construct the Retirement Planning dummy variable. It takes 1 if the answer that the respondent provides is yes and takes 0 otherwise. Similarly, it asks “Do you agree with the following statement? I have a long-term financial plan” and provides five answers that respondents can choose from. (1) Completely disagree; (2) Disagree; (3) Neither agree nor disagree; (4) Agree; (5) Completely agree. I use the question to construct a dummy variable Financial planning (1 = agree, or completely agree; 0 = neither agree nor disagree, disagree, or completely disagree).

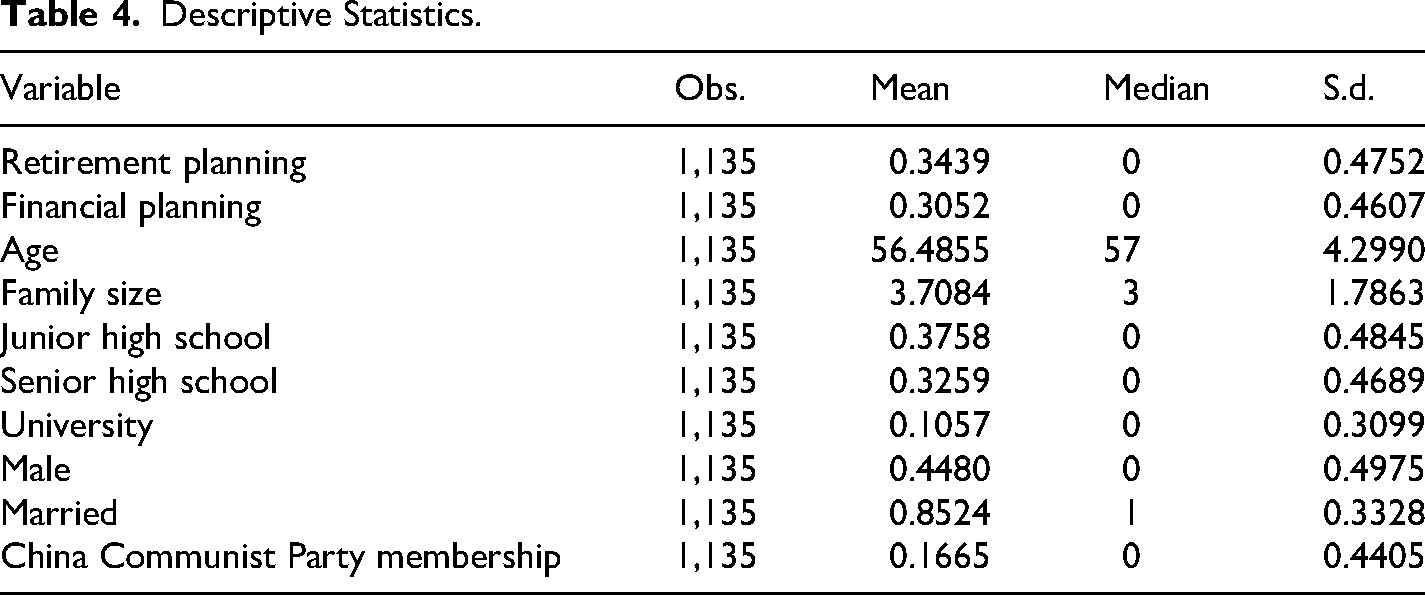

Table 4 presents descriptive statistics of the survey. Both the share of people with retirement planning and the share with financial planning are around one-third. This result indicates that the majority of respondents do not adequately prepare for retirement. The average age of the sample is approximately 56. There is a great deal of heterogeneity in educational attainment: 11% of respondents have a university degree, while 57% do not obtain even a senior high school diploma. Men are slightly underrepresented (45%), and the majority of respondents (85%) are married.

Descriptive Statistics.

Results

Baseline Results

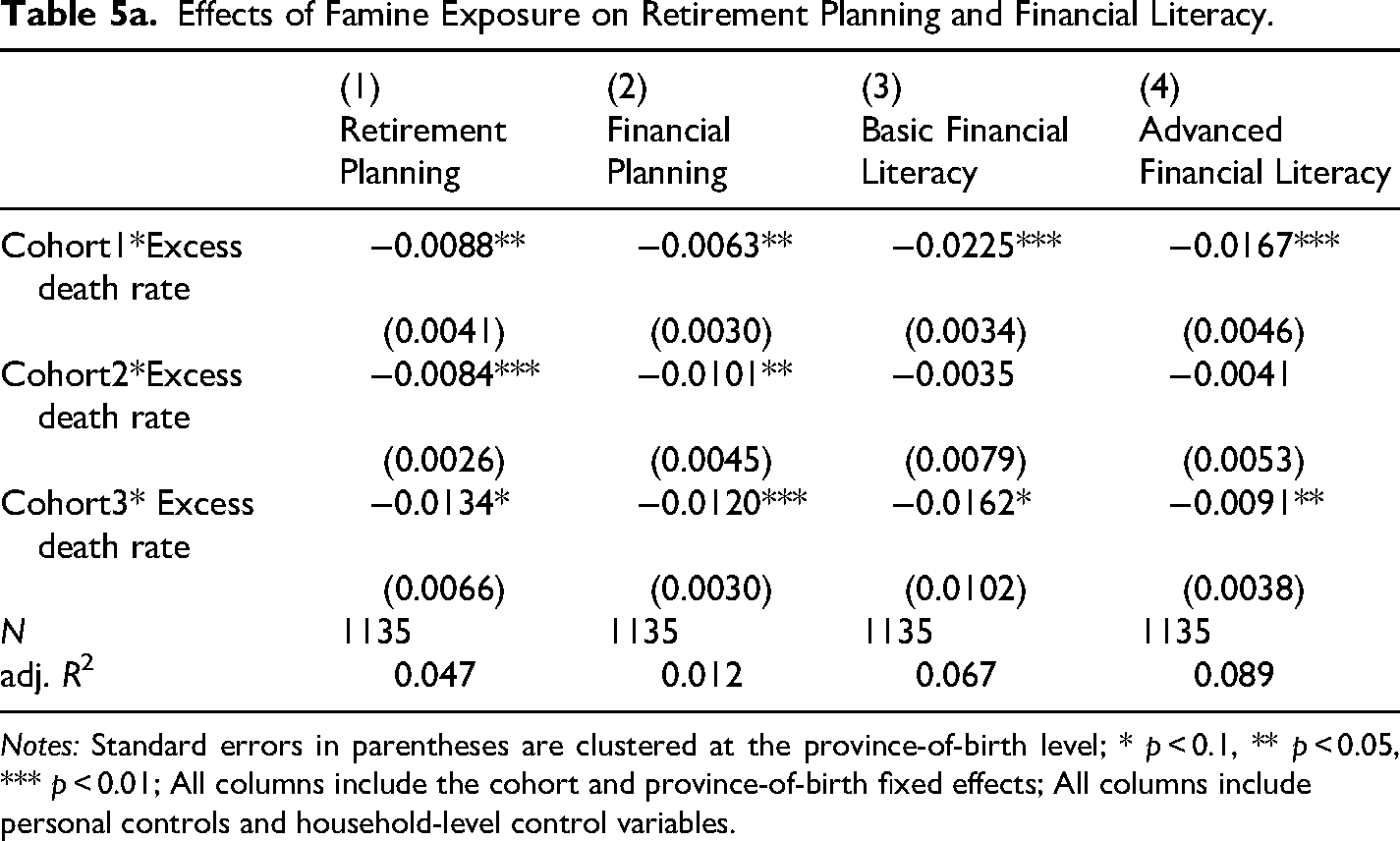

Table 5a presents estimates of

Effects of Famine Exposure on Retirement Planning and Financial Literacy.

Notes: Standard errors in parentheses are clustered at the province-of-birth level; * p < 0.1, ** p < 0.05, *** p < 0.01; All columns include the cohort and province-of-birth fixed effects; All columns include personal controls and household-level control variables.

Effects of Famine Exposure on Retirement Planning and Financial Literacy.

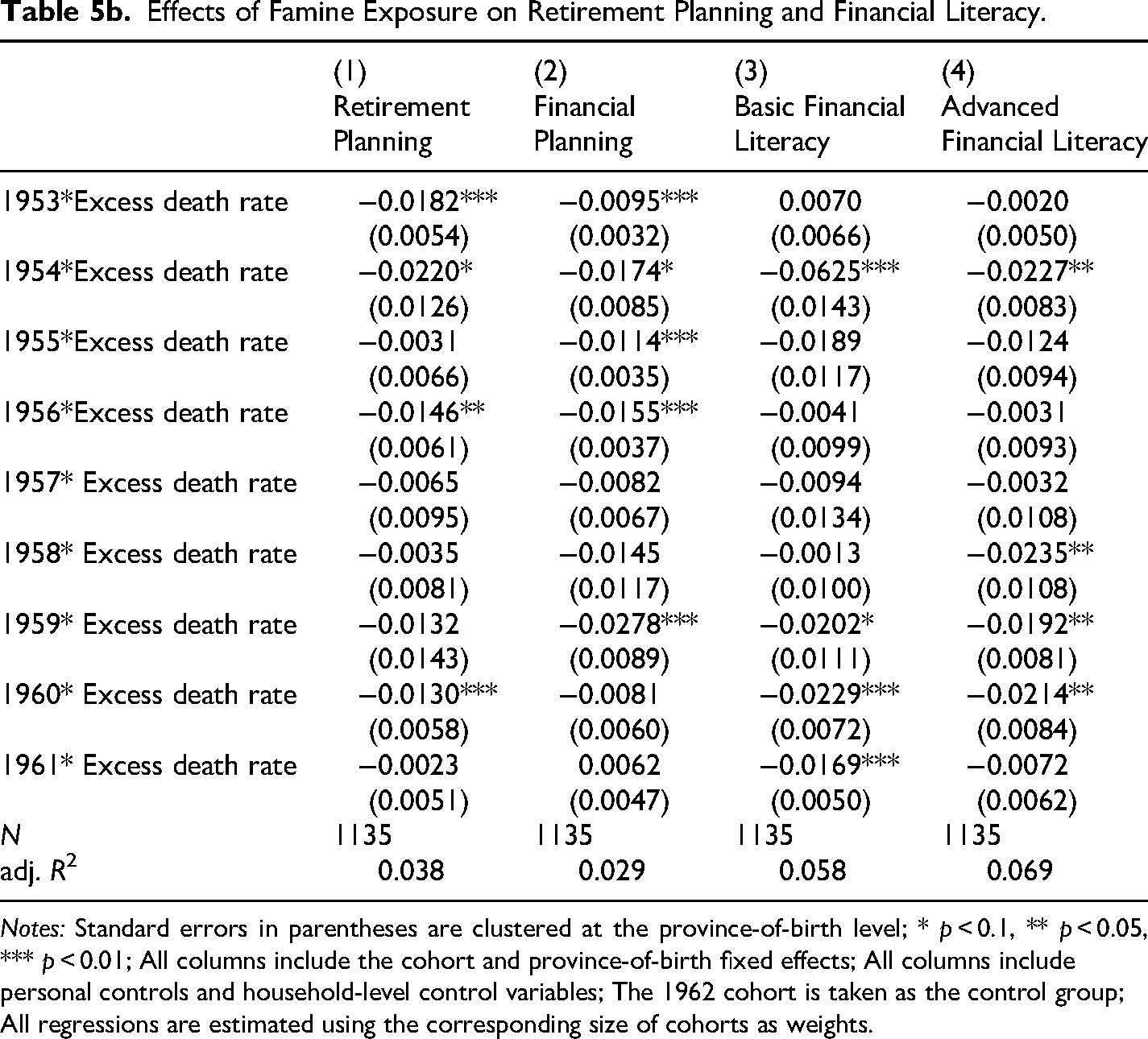

Notes: Standard errors in parentheses are clustered at the province-of-birth level; * p < 0.1, ** p < 0.05, *** p < 0.01; All columns include the cohort and province-of-birth fixed effects; All columns include personal controls and household-level control variables; The 1962 cohort is taken as the control group; All regressions are estimated using the corresponding size of cohorts as weights.

Column (1) shows that all three famine-affected cohorts have lower probabilities of retirement planning than the counterfactual case in which the famine had not occurred. The coefficients of the interaction terms are all negative, with the coefficient on Cohort 3 somewhat larger than other cohorts. Results in column (2) show similar patterns using the probability of financial planning as the dependent variable. These results imply that early-life adverse health shocks indeed generate lasting negative impacts on retirement planning for survivors. In particular, the finding of negative impacts of in-utero famine exposure (Cohort 1) on retirement planning lends strong support for the “fetal origin” hypothesis. In terms of the magnitude of impact, column (1) shows that one standard deviation increase in the intensity of famine exposure decreases the likelihood of retirement planning by 0.122 percentage points to 0.190 percentage points for different cohorts.

In stark contrast with the statistically significant and economically meaningful negative impacts of early-life famine exposure on retirement planning for all cohorts, the impact on financial literacy varies across cohorts. For the in-utero exposed cohorts (Cohort 1), both the impacts on basic and advanced financial literacy are significant at the 1% level, consistent with the notion that financially literate individuals are more likely to plan for retirement (Lusardi & Mitchell, 2008; van Rooij et al., 2011, 2012). Meanwhile, the impacts on both financial literacy measures are statistically significant for Cohort 3 at conventional levels. In contrast, though still economically meaningful, the effects on both financial literacy measures are statistically insignificant for Cohort 2.

Put together, these results verify the hypothesis that financial literacy begins to form at a very early age and that adverse early-life health shocks can discourage the likelihood of retirement planning in older age through its impact on financial literacy.

Yearly-Defined Cohort-Specific Effects

Table 5b presents (yearly defined) cohort-specific effects of the impact of early-life famine exposure on retirement planning and financial literacy using equation (2). At least five basic conclusions can be derived from column (1).

First, the impacts on retirement planning are negative for all famine-affected cohorts, despite that impacts on certain cohorts are statistically indifferent from zero. Second, among the cohorts that were born exactly during the famine period (the 1959–1961 cohorts), the impact is only significantly observed for the 1960 cohort. Third, among cohorts who are one year around retirement (1953–1955), both the 1953 and 1954 cohorts (already retired) are negatively affected, with impacts on the 1954 cohort being slightly larger. By contrast, the impact on the 1955 cohort (not retired) is statistically indifferent from zero. Fourth, the negative impact on the 1956–1958 cohorts as a whole is mainly driven by the 1956 cohort. Fifth, among the cohorts with significant coefficients, the magnitudes of impacts are stronger for the older cohorts. For example, the absolute magnitude of the negative impact on the 1954 cohort is 1.7 times as large as that of the 1960 cohort.

Impacts on financial literacy are estimated in the same way. As columns (3) and (4) of Table 5b show, all the impacts are negative, though impacts on several cohorts are not significant. Even though the coefficients on (basic and advanced) financial literacy do not match one-by-one to those of retirement planning in terms of statistical significance, we can still conclude with substantial confidence that early-life famine exposure negatively impacts retirement planning through financial literacy.

Discussion

While estimation results presented in Tables 5a and 5b provide strong support for the (potential) causal relationship between early-life (in-utero and early childhood) famine exposure and late-life retirement planning (financial literacy), we still know very little about the specific forces driving this relationship.

As discussed in Section 2, the negative impacts potentially work through three channels. Early-life famine experience can cause the level of financial literacy and the probability of retirement planning to decline through impairments in cognitive ability, alterations of time preferences, and changes in risk preferences. This subsection explicitly tests the plausibility of these three channels.

We use two measures to proxy for cognitive ability: Education years and Numeracy. Education years are measured as year equivalents of education levels. Specifically, a 3-year university education level is equivalent to 15 education years, a 4-year university education equals 16 education years, a senior high school 12 years, a junior high school 9 years, and an elementary school 6 years, while those illiterate are assigned 0 education years. Numeracy is a dummy variable indicating whether a respondent provides the correct answer to the second basic literacy question, 16 it takes 1 if he (she) is correct and 0 if he (she) is incorrect or provides the “Do not know” answer.

Impatience and Risk Aversion are two variables that measure an individual's time preference and risk preference, respectively. First, the survey asks “Do you agree with the following statement? I prefer instant gratification over delayed gratification. (1) Completely disagree; (2) Disagree; (3) Neither agree nor disagree; (4) Agree; (5) Completely agree.” Based on the answers that respondents provide, we construct a dummy variable Impatience. It takes one if the answer is “agree” or “completely agree”, and it takes 0 if the answer is “neither agree nor disagree”, “disagree”, or “completely disagree”.

Second, the CFPS survey also asks “If you are going to make an investment, which projects would you like to choose? (1) High risk, high return projects; (2) Average risk, average return projects; (3) Low risk, low return projects; (4) Not willing to take on any risk.” We use this question to construct a categorical variable Risk Aversion (1 = high risk, high return projects; 2 = average risk, average return projects; 3 = low risk, low return projects; 4 = not willing to take on any risk). The larger the value of Risk Aversion one scores, the more risk averse he (she) is.

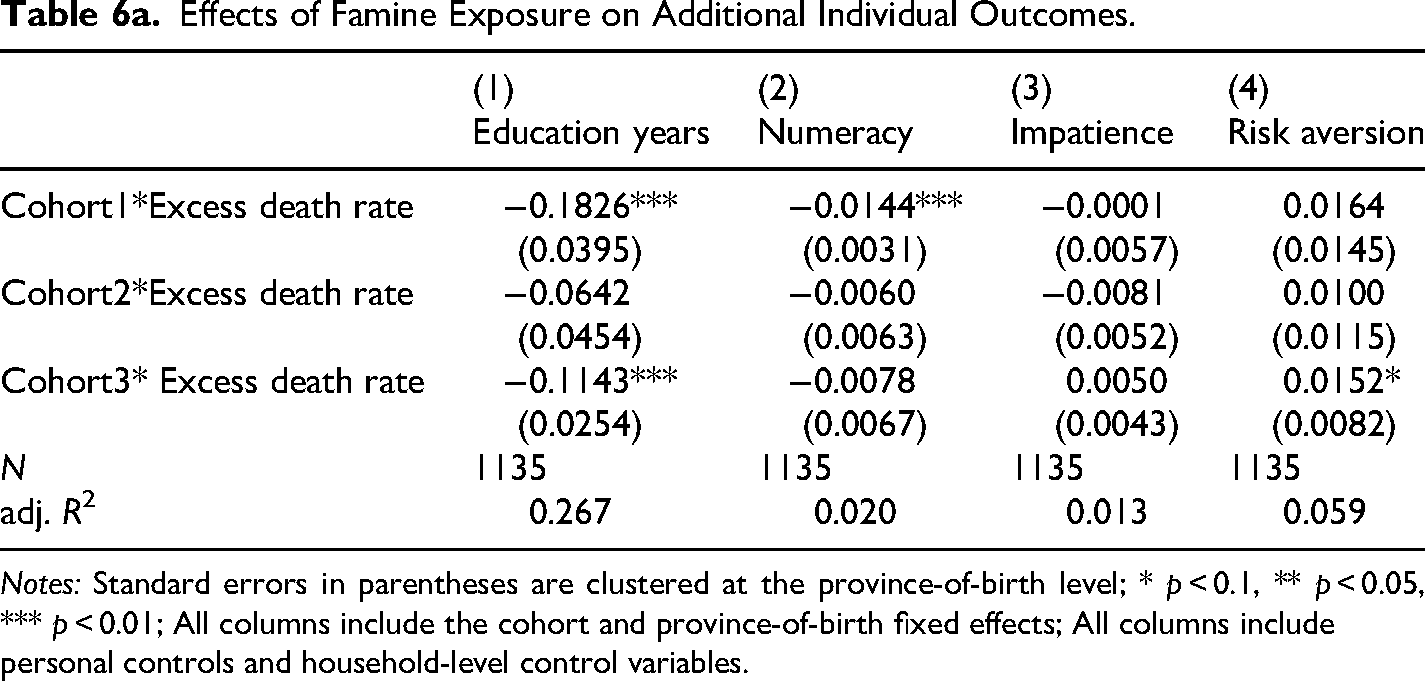

Table 6a provides the estimation results. To begin with, focusing on Cohort 1 which experienced famine while in utero shows that the impacts on education years and numeracy levels are both negative and significant at conventional levels. In contrast, both impacts on time preference (impatience) and risk aversion are statistically indifferent from zero. These results indicate that impairments of cognitive ability while in utero might be the deep roots of early-source determinants of financial literacy and retirement planning.

Effects of Famine Exposure on Additional Individual Outcomes.

Notes: Standard errors in parentheses are clustered at the province-of-birth level; * p < 0.1, ** p < 0.05, *** p < 0.01; All columns include the cohort and province-of-birth fixed effects; All columns include personal controls and household-level control variables.

Effects of Famine Exposure on Additional Individual Outcomes.

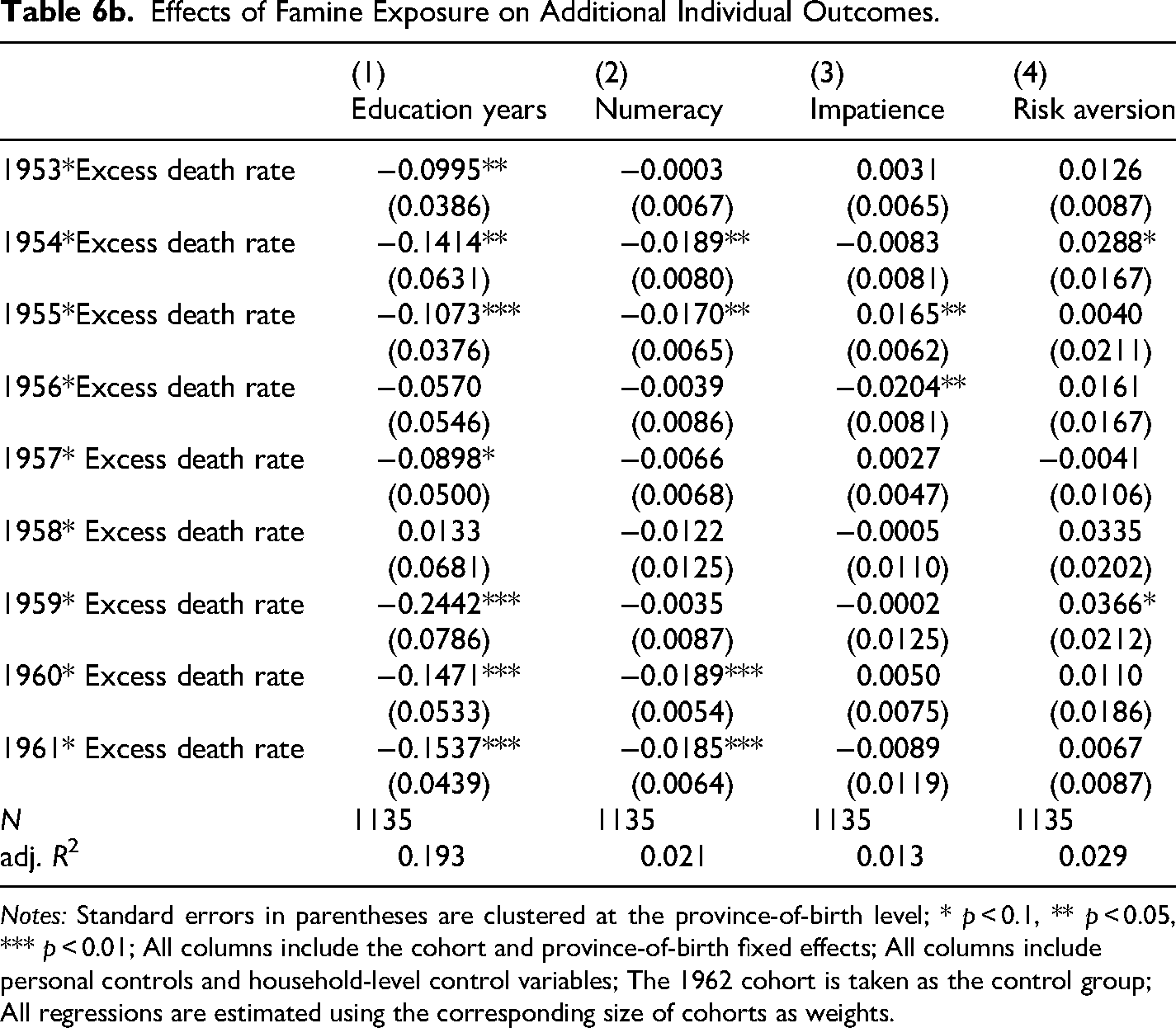

Notes: Standard errors in parentheses are clustered at the province-of-birth level; * p < 0.1, ** p < 0.05, *** p < 0.01; All columns include the cohort and province-of-birth fixed effects; All columns include personal controls and household-level control variables; The 1962 cohort is taken as the control group; All regressions are estimated using the corresponding size of cohorts as weights.

Second, the impacts on education years (but not numeracy) for Cohort 3 are negative and are statistically significant at the 1% level. Also, it shows that Cohort 3 became more risk-averse after experiencing famine in early childhood (column 4). Third, the negative impact on education years for Cohort 3 is much smaller in absolute size than for Cohort 1. This may be because cognitive ability is more severely impaired for Cohort 1 than Cohort 3 due to prenatal maternal nutritional deprivation and cognitive ability matters more for educational attainment. Fourth, the impacts on the four outcome variables for Cohort 2 are all statistically insignificant.

These results suggest that both declines in cognitive ability and changes in risk preferences are likely transmission channels through which early-life famine exposure impacts retirement planning. Meanwhile, it suggests that impairments in cognitive ability are a more important transmission channel for those who experienced famine while in utero, and changes in risk preferences are more plausible among children affected in early childhood.

Table 6b presents additional evidence of the heterogeneous impacts of famine exposure on four outcome variables, with cohorts defined yearly. Estimation results of education years are similar to those obtained in Table 6a. The negative impacts on education years are heterogeneous among the narrowly defined cohorts.

Individuals of the 1953, 1954, 1955, 1957, 1959, 1960, and 1961 cohorts are significantly negatively affected. The size of the impacts is also economically meaningful. In contrast, the impacts on education years for the 1956 and 1958 cohorts are statistically insignificant and negligible in absolute size. Again, it shows that the absolute size of the impact on education years is larger for the in-utero exposed cohorts.

Regression results on time preference (impatience) and risk aversions are also broadly similar to those presented in Table 6a. There are substantial heterogeneities among cohorts. Effects on risk aversions are only observed for the 1954 and 1959 cohorts. In comparison, the impacts on time preference (impatience) are mixed and are only observed for the 1955 and 1956 cohorts.

Conclusions

This paper examines the impact of early-life exposure to the 1959–1961 China Famine on retirement planning and financial literacy later in life. Taking advantage of a special module in the 2014 China Finance Panel Studies (CFPS) data set and exploiting the potentially exogenous province-by-cohort variations in famine exposure, we find that people who were exposed to famine when 0–6 years old are less financially illiterate at ages 53–61. Due to the lower level of attained financial literacy, they tended to report a lower likelihood of retirement planning.

Mechanism analysis verifies the hypothesis of a cognitive ability channel and provides suggestive evidence for a risk preference channel. This paper's findings carry strong implications for remediation policies that help disadvantaged children catch up. This paper suggests that early health intervention programs may have unintendedly improved these cohorts’ financial well-being in older age.

Albeit obtaining interesting findings, this paper is also subject to several weaknesses. First, the risk preference channel is only indirectly identified. Second, lacking direct measures of cognitive ability and risk preference constrains the evaluation of the relative importance between the two channels. Future studies that explore the long-term effects of adverse early-life circumstances may advance by providing more direct evidence of its impacts on unobserved personal attributes such as attitudes toward risk and time preferences.

Supplemental Material

sj-docx-1-ahd-10.1177_00914150251401492 - Supplemental material for Early-Life Famine Exposure, Financial Literacy, and Retirement Planning: Evidence from China

Supplemental material, sj-docx-1-ahd-10.1177_00914150251401492 for Early-Life Famine Exposure, Financial Literacy, and Retirement Planning: Evidence from China by Haopeng Sun and Yuanhua Xu in The International Journal of Aging and Human Development

Footnotes

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Publicly available from the Institute of Social Science Survey at Peking University, China.

Supplemental Material

Supplemental material for this article is available online.

Notes

Correction (February 2026):

This article has been updated with grammatical corrections since its original publication.

Appendix

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.