Abstract

This study addressed how communication about retirement fits in the communicative ecology model of successful aging (CEMSA). U.S. American older adults (N = 294, MAge = 59.27 years) reported on a memorable message they heard about retirement, as well as on their own talk about how they can be financially prepared for retirement. Older adults who wrote a memorable message with a theme of (a) saving money for retirement or (b) relaxing or enjoying life during retirement reported talking about how they can be financially prepared for retirement more than did older adults who did not write a memorable message with one of these themes. Older adults’ talk about how they can be financially prepared for retirement was indirectly associated with successful aging, via the serial mediators of positive affect about aging and aging efficacy. Talking about how one can be financially prepared for retirement may be a worthwhile theoretical addition to the CEMSA.

Keywords

Introduction

Building on the communicative ecology model of successful aging (CEMSA; e.g., Fowler et al., 2015; Gasiorek et al., 2016), the current study examined how the memorable messages that older adults internalize about retirement are associated with older adults’ own talk about how they can be financially prepared for retirement and successful aging. The study also tested how older adults’ own talk about how they can be financially prepared for retirement is associated with their successful aging. By examining these associations, the study makes several theoretical contributions to the CEMSA. First, the CEMSA proposes that people’s own communication is, in part, based on their observations of others’ communication (Gasiorek et al., 2016). Gasiorek et al. called for sustained attention to this linkage in the CEMSA, which would foster understanding of how people’s own communication may be the result of a dynamic learning process between them and their social environments.

Second, Gettings and Kuang (2022) proposed expanding the CEMSA to include adults’ talk about their retirement preparations as a new domain of adults’ own age-related communication, above and beyond the original seven domains proposed by Fowler et al. (2015). The original seven domains are (1) using age-related excuses to account for one’s shortcomings, (2) expressing optimism about one’s aging process, (3) teasing other people about their age, (4) playing along when one’s own age is the subject of teasing, (5) displaying skepticism toward anti-aging messages in the media (e.g., advertisements for anti-aging beauty products), (6) discussing one’s caregiving preferences before a need for care arises, and (7) remaining updated with new communication technologies (e.g., smart phone apps, social media) to stay in touch with family members and friends (Fowler et al., 2015). In Gettings and Kuang’s (2022) study, adults’ talk about their retirement preparations included (a) general talk about what retirement will look like for them, (b) talk about how they have accomplished what they wanted to in their careers, and (c) talk about being financially prepared for retirement. This composite variable was not associated with adults’ positive affect about aging, negative affect about aging, or aging efficacy (Gettings & Kuang, 2022). Their study helped show that overall talk about several retirement issues may not be associated with certain aging experiences. The current study considers if one more specific domain of retirement communication—namely, adults’ talk about how they can be financially prepared for retirement—is associated with positive affect about aging, negative affect about aging, and aging efficacy. Significant associations in this regard may highlight the merit of considering more circumscribed domains of retirement communication.

The decision to focus on older adults’ talk about how they can be financially prepared for retirement—as opposed to older adults’ general talk about what retirement will look like for them or talk about how they have accomplished what they wanted to in their careers—was grounded in narrative reviews of successful aging. Teater and Chonody (2020), for example, conducted a narrative review of 22 studies exploring older adults’ definitions of successful aging. They described 12 themes in older adults’ definitions of successful aging. The fourth-most common theme was financial security, observed in 13 of the 22 studies (59.09%). In this theme, older adults described having enough money to pay for healthcare, routine expenses (e.g., utility bills), and activities that they enjoy doing. Being able to pay for these things allowed older adults to have fewer worries and a greater sense of security when aging. In contrast, none of the 12 themes addressed what retirement will generally look like or career accomplishments.

In another narrative review, Badache et al. (2023) synthesized findings from 15 studies on older adults’ perceptions of what it means to age successfully. They categorized these perceptions into 15 themes. One theme was financial resources, appearing in eight of the 15 studies (53.33%). Financial resources involved older adults budgeting, investing, being debt-free, and engaging in financial planning. These activities helped older adults have fewer worries about their aging. Another theme was reflections on life and past experiences, appearing in seven of the 15 studies (46.67%). Reflections on life and past experiences included older adults thinking about their previous educational and career accomplishments (e.g., serving their country during wartime), as well as anticipating what their future retired lives would bring. This theme overlaps with Gettings and Kuang’s (2022) focus on talk about career accomplishments and general talk about what retirement will look like. Thus, all three types of talk in Gettings and Kuang’s composite variable are arguably relevant to successful aging. With that said, the greater prevalence of themes surrounding finances in these narrative reviews suggests that scholars are justified in first examining talk about how to be financially prepared for retirement. Scholars can then examine the other two types of talk in Gettings and Kuang’s composite variable in follow-up research.

In the following sections, the CEMSA’s main concepts and logic are reviewed, followed by a discussion of the associations tested in the current study.

Connecting Communication About Retirement and Finances to Successful Aging

CEMSA Overview

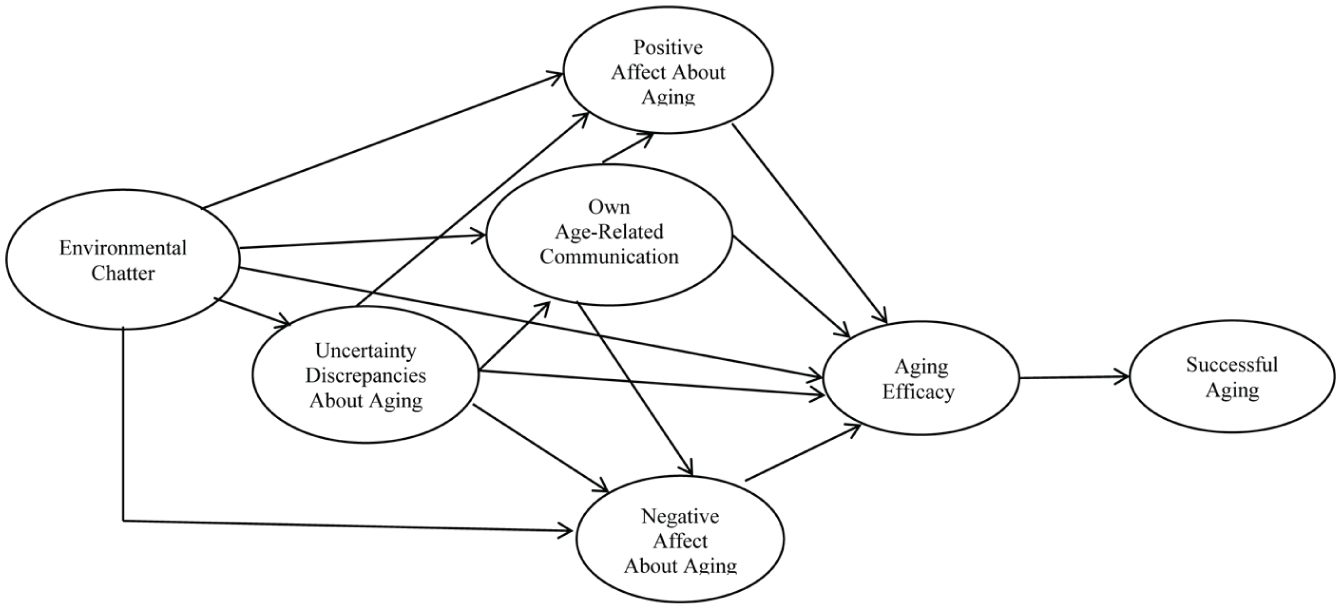

The CEMSA (see Figure 1) addresses how communication might bear implications for successful aging. In the model, environmental chatter is the communication about aging that people internalize from their social environments (Gasiorek et al., 2016). The environmental chatter component of main interest in the current study is memorable messages about retirement. Memorable messages are messages “remembered for extremely long periods of time and which people perceive as a major influence on the course of their lives” (Knapp et al., 1981, p. 27). Environmental chatter is associated with people’s uncertainty discrepancies about aging, own age-related communication, affect about aging, and aging efficacy (Gasiorek et al., 2016). Uncertainty discrepancies are differences between what people know and what people would like to know about the prospects of aging (Gasiorek et al., 2016). When people experience high uncertainty discrepancies, they are less certain than they would like to be about what their life will be like as they get older (Fowler et al., 2015). In the CEMSA, uncertainty discrepancies are associated with people’s own age-related communication, positive affect about aging, negative affect about aging, and aging efficacy (Fowler et al., 2015; Gasiorek et al., 2016).

The communicative ecology model of successful aging (CEMSA). In the current study, environmental chatter is considered as a memorable message about retirement that older adults have internalized. The study tests how the themes in the memorable message are associated with the other constructs connected to environmental chatter. Own age-related communication is considered as older adults’ own communication about their financial preparations for retirement. All of the paths in Figure 1 were tested in the current study.

Own age-related communication refers to how people talk about their own age and the aging process (Fowler et al., 2015; Gasiorek et al., 2015). The current study considers one new domain of own age-related communication, namely own communication about financial preparations for retirement. Own communication about financial preparations for retirement refers to people’s talk about how they can be financially ready for retirement, such as how they can save enough money for retirement. Own age-related communication is associated with positive affect about aging, negative affect about aging, and aging efficacy in the CEMSA (Fowler et al., 2015; Gasiorek et al., 2016). According to Fowler et al. (2015), the ways in which people communicate about the aging process “create ecologies, or ‘aging spaces’ within which people have greater (or reduced) potential to age well” (p. 433). These communicatively-constructed aging spaces are theorized to be the underlying mechanism driving how people think and feel about their own aging (Fowler et al., 2015). Consistent with this theorizing, several domains of own age-related communication (e.g., expressing optimism about aging, remaining updated with new communication technologies) have been associated with affect about aging and aging efficacy (Fowler et al., 2015). The current study addresses if this theorizing also transfers to people’s own communication about their financial preparations for retirement.

The original seven domains of own age-related communication can be studied individually (e.g., Fowler et al., 2015) or combined into profiles (e.g., Bernhold et al., 2020; Gasiorek et al., 2015). With respect to combining the domains into profiles, researchers have categorized adults into four profiles based on how they communicate across the seven domains (e.g., Bernhold et al., 2020; Gasiorek et al., 2015). First, engaged agers report relatively high levels of expressing optimism about aging, displaying skepticism toward anti-aging messages in the media, discussing caregiving preferences in advance, and remaining updated with new communication technologies. They report relatively low levels of making age-related excuses for their shortcomings, teasing others about their age, and playing along when their own age is the subject of teasing (Gasiorek et al., 2015, 2019). Second, bantering agers score relatively high on all seven domains of own age-related communication, with the exception that their discussions of future caregiving preferences seem to be somewhat less frequent than those of engaged agers (Gasiorek et al., 2015; Gasiorek & Fowler, 2016). Third, disengaged agers report relatively low levels of all seven domains of own age-related communication, with the exception that they remain updated with new communication technologies at roughly the same levels as engaged and bantering agers (Bernhold & Giles, 2019; Gasiorek et al., 2015). Finally, gloomy agers score relatively high on making age-related excuses for their shortcomings, but relatively low on the six other domains (Bernhold, 2022; Bernhold et al., 2020). Relative to engaged agers, bantering, disengaged, and gloomy agers have reported less successful aging, via less aging efficacy (i.e., own age-related communication → aging efficacy → successful aging; Bernhold, 2022; Bernhold et al., 2020).

One advantage of studying an own age-related communication domain individually is that researchers can gain precise insights into how that specific domain is associated with other CEMSA constructs. In the current study, our goal was to examine how one specific domain of own age-related communication (namely, own communication about financial preparations for retirement) is associated with other CEMSA constructs. When pursuing this goal, it is important to control for the other domains not of focal interest to help ensure that the one domain of focal interest explains unique variance in other CEMSA constructs. We control for adults’ probabilities of being in the profiles (rather than adults’ scores on the original seven domains) for two reasons. First, Fowler et al. (2015) reported reliability coefficients below α = .70 for some of the original seven domains (e.g., expressing optimism about the aging process: α = .62). Latent profile analysis (LPA) is the analytic technique used to classify adults into the engaged, bantering, disengaged, and gloomy profiles. LPA can retain survey items at the individual level (e.g., Gasiorek et al., 2015), so these lower reliability coefficients are not necessarily problematic when employing LPA. Second, controlling for adults’ scores on the original seven domains would mean that researchers are adding seven additional covariates to their model. In contrast, controlling for adults’ probabilities of being in the profiles would mean that researchers are adding three covariates to their model. We chose engaged agers as the reference profile and controlled for participants’ probabilities of being bantering, disengaged, and gloomy agers. Thus, the decision to control for the profiles helped keep the overall number of covariates manageable.

Regarding other CEMSA constructs, positive affect about aging refers to the pleasing feelings that arise at the prospect of growing older, such as feeling excited, strong, or enthusiastic (Bernhold et al., 2024; Fowler et al., 2015). In contrast, negative affect about aging refers to the displeasing feelings that arise at the prospect of growing older, such as feeling nervous, scared, or upset (Fowler et al., 2015; Gasiorek & Fowler, 2022). Positive and negative affect about aging are proposed to be associated with aging efficacy in the CEMSA (Fowler et al., 2015; Gasiorek et al., 2016). Aging efficacy is people’s perception that they are capable of handling whatever changes or challenges might arise as they grow older (Fowler et al., 2015). The CEMSA positions aging efficacy as the proximate predictor of successful aging (Fowler et al., 2015; Gasiorek et al., 2016). Successful aging is “an individual, subjective judgment of how well one is experiencing the process of aging at a given point in time” (Gasiorek et al., 2015, p. 578). It captures the extent to which a person experiences high life satisfaction and contentment with the current state of their life (Bernhold et al., 2025).

CEMSA researchers have traditionally asked adults to report on their uncertainty discrepancies about aging, positive affect about aging, negative affect about aging, aging efficacy, and successful aging at the general level (i.e., by reflecting on their overall aging experiences; e.g., Bernhold et al., 2024; Gasiorek et al., 2015). Researchers have correlated adults’ own age-related communication in very specific domains with these general aging constructs (e.g., Gettings & Kuang, 2022). For example, in the inaugural CEMSA study, Fowler et al. (2015) found that middle-aged and older New Zealanders’ discussions of their future caregiving preferences were positively associated with their positive affect about aging. Fowler et al. did not examine how discussions of future caregiving preferences were associated with positive affect about receiving care. The current study follows this precedent by examining how older adults’ own communication about financial preparations for retirement is associated with general aging constructs in the CEMSA.

Anticipated Associations

The study first considers what themes appear in memorable messages about retirement. Although previous research has not directly addressed this topic, research in related domains can help contextualize this inquiry. First, Holladay (2002) asked adults to recall a memorable message about aging. One theme in the messages was advice about the importance of financial planning (e.g., “Make sure you start saving now for retirement because social security may not be around when we retire”, p. 691). Very similarly, Bernhold (2022) asked older adults to recall up to three memorable messages about aging. One theme in the messages was practical advice on how to age, often involving saving funds for retirement (e.g., “Make sure you have enough money to retire on for the next 25–30 years if you’re going to retire early from your job”, p. 142). These studies suggest that saving money for retirement is an important component of memorable messages about aging. A similar theme may appear in memorable messages about retirement.

Other themes may also appear. For example, Anderson and Gettings (2020) noted that anticipatory socialization messages (i.e., messages that people receive prior to joining an organization or entering a specific phase of their career) may shape young adults’ expectations for retirement. They examined young adults’ expectations for what a successful retirement involves, potentially shaped by such messages. In addition to financial security, young adults mentioned that a successful retirement may (a) be the product of hard work throughout life, (b) involve relaxation and enjoyment of life, and (c) involve various activities (e.g., traveling, golfing, shopping). Gettings and Anderson (2021) also applied an anticipatory socialization framework to understand the meanings young adults ascribe to retirement. Thirteen meanings emerged from the young adults’ responses, some of which were (a) being financially prepared for retirement, (b) spending time in passive ways during retirement (e.g., relaxing), (c) spending time in active ways during retirement (e.g., pursuing hobbies), (d) retiring due to a physical inability to work any longer, (e) retirement appearing to be a long way away, and (f) experiencing various challenges during retirement (e.g., boredom). Some of these findings could also appear as themes in memorable messages about retirement. Nonetheless, given that the exact number and nature of themes that would emerge were unclear, the following research question was proposed:

The themes from RQ1 may be associated with uncertainty discrepancies about aging, affect about aging, aging efficacy, and own age-related communication. Gasiorek et al. (2016) argued that memorable messages “are more likely to influence, rather than be influenced by, individuals’ levels of uncertainty about aging” (p. 40). Some memorable messages that offer concrete information may reduce uncertainty discrepancies about aging. However, some vague memorable messages (e.g., aphorisms) may increase uncertainty discrepancies. With respect to this latter possibility, Gasiorek et al. used the example of a person internalizing a memorable message of “Don’t get old!”. This message may increase the person’s uncertainty discrepancy and prompt them to have additional questions about aging (e.g., “Why shouldn’t I get old?”, p. 41). Thus, the specific directionalities of the associations between the memorable message themes and uncertainty discrepancies are likely to depend on the content of the memorable message themes (Gasiorek et al., 2016). A similar argument can be made about how the memorable message themes are associated with positive affect about aging, negative affect about aging, and aging efficacy. For example, a potential message theme about remaining active during retirement could be associated with high positive affect about aging, low negative affect about aging, and high aging efficacy. In contrast, a potential message theme about experiencing challenges such as boredom during retirement could be associated with low positive affect about aging, high negative affect about aging, and low aging efficacy.

The CEMSA also holds that environmental chatter is associated with people’s own age-related communication (Gasiorek et al., 2016). Supporting this, Gettings and Kuang (2022) found that adults’ observations of (a) negative environmental chatter (e.g., nonaccommodation, negative role models for aging) and (b) positive environmental chatter (e.g., accommodation, positive role models for aging) were both positively associated with adults’ own communication about their retirement preparations. These findings might have emerged “because communication from individuals’ social environments, despite its valence, can prompt them to reflect more on the intersections of work and aging and thus, lead to more communicative engagement about such topics” (Gettings & Kuang, 2022, p. 508). Given that both positive and negative forms of environmental chatter were positively associated with adults’ own communication about their retirement preparations, it seemed likely that some memorable message themes about retirement would make retirement and finances salient issues, thereby prompting older adults to talk about their own financial preparations for retirement.

Perhaps the most obvious example of this involves adults who internalize memorable messages about saving enough money for retirement. These messages could make financial security a salient issue, and this issue salience could prompt these adults to talk about their own financial preparations for retirement. Other less obvious examples may also emerge. For example, Anderson and Gettings (2020) found that some adults associate retirement with activities such as golfing and shopping, which require funds and are tied to financial success. Given this, internalizing memorable messages about these activities might prompt adults to think about whether or not they have the requisite funds for these activities. Adults who think about whether or not they have these funds may then be likely to talk about how they can save enough money for retirement. As another example, adults who internalize memorable messages about retirement being a long way away for another person may consider why that person cannot retire in the foreseeable future. They may conclude that the person does not have enough money saved for retirement. This conclusion could lead them to consider whether or not they have enough money saved for retirement and communicate about how they can be financially prepared for retirement. In these ways, memorable messages both explicitly about finances and not explicitly about finances may be associated with older adults’ own communication about their financial preparations for retirement.

Taken together, this logic suggests that some of the message themes may be associated with uncertainty discrepancies, positive affect about aging, negative affect about aging, aging efficacy, and own age-related communication. However, given that the exact number and nature of the themes were unknown, the following non-directional hypothesis was offered:

Next, the CEMSA stipulates that uncertainty discrepancies are associated with affect about aging, aging efficacy, and own age-related communication (Fowler et al., 2015; Gasiorek et al., 2016), and research has supported these parts of the model. Uncertainty discrepancies have been negatively associated with positive affect about aging and aging efficacy, as well as positively associated with negative affect about aging (Fowler et al., 2015; Gettings & Kuang, 2022). With respect to the associations between uncertainty discrepancies and own age-related communication, high uncertainty discrepancies have been associated with seemingly maladaptive ways of communicating. Conversely, low uncertainty discrepancies have been associated with seemingly adaptive ways of communicating. For example, uncertainty discrepancies have been positively associated with the use of age-related excuses to account for shortcomings and negatively associated with expressed optimism about aging (Fowler et al., 2015). Own communication about financial preparations for retirement is considered to be an adaptive way of talking about the aging process. This is because adults often define successful aging in terms of financial security (e.g., Teater & Chonody, 2020). Talking about how they can be financially prepared for retirement may be empowering for adults in their quests to age more successfully, because this talk may provide them with concrete actions to consider implementing (e.g., investing in stocks, bonds, real estate, or their employer-sponsored retirement accounts). Given that own communication about financial preparations for retirement is considered an adaptive form of communication, it may follow trends from previous research, whereby high uncertainty discrepancies are associated with low levels of adaptive communication.

On a more substantive note, the theory of motivated information management (TMIM; e.g., Afifi & Weiner, 2004) proposes that when people experience an uncertainty discrepancy about a given topic, they generate an outcome expectancy regarding the likely consequences of seeking information on that topic. If the outcome expectancy is negative, people will often refrain from seeking information and instead engage in information avoidance (Afifi & Matsunaga, 2008). Adapted to the current study, this logic suggests that adults with large uncertainty discrepancies about aging or financial preparations for retirement will generate an outcome expectancy about the likely consequences of seeking information on financial preparations for retirement. They may believe that seeking information will bring about largely negative outcomes (e.g., learning that they are behind where they should be in saving for retirement). As a result of these negative outcome expectancies, they may refrain from seeking information on how to be financially prepared for retirement. Thus, adults with large uncertainty discrepancies may not regularly talk about how they can be financially prepared for retirement.

As a whole, this reasoning suggests the second hypothesis:

In turn, own communication about financial preparations for retirement may be positively associated with positive affect about aging and aging efficacy, but negatively associated with negative affect about aging. Gettings and Kuang (2022) offered two reasons why the associations might emerge in these ways. First, increased talk about preparing for retirement may be associated with increased preparatory behaviors for retirement. Given this, people who talk more about saving funds for retirement may be more likely to actually save funds for retirement, compared to people who talk less about this topic. Having more money saved for retirement may then generate more positive affect about aging, less negative affect about aging, and a greater perceived ability to manage the aging process (more aging efficacy; Gettings & Kuang, 2022).

Second, talking about their preparations for retirement allows people to express a positive identity. This projection of a positive identity could be associated with increased positive affect and aging efficacy, as well as decreased negative affect (Gettings & Kuang, 2022). Consistent with this, Gettings (2019) interviewed retirees to understand the meanings associated with their talk about the transition to retirement. One meaning involved retirees identifying as members of a group who prepared the “right” way for retirement (p. 486). For example, one interviewee was a retired insurance agency owner who described people who saved for retirement as being “smart enough to be able to put it away and do what you’re supposed to do” (p. 487). She called herself and her husband “big savers”, whereas she described people who experience disrupted retirements and reenter the workforce as making incorrect financial calculations or failing to “save properly” (p. 487). Thus, when people talk about how they are saving for retirement, they may be asserting a positive component of their identity (e.g., their identity as a saver or planner). Asserting this valued identity may facilitate positive affect about aging and aging efficacy, while reducing negative affect about aging (see also social identity theory; e.g., Tajfel & Turner, 1986).

For these reasons, the following hypothesis was offered:

With respect to affect, the CEMSA posits that affect about aging is associated with aging efficacy (Fowler et al., 2015; Gasiorek et al., 2016). Experiencing positive affect about aging (e.g., excitement, enthusiasm) should make people feel more confident in their ability to handle the aging process, whereas experiencing negative affect about aging (e.g., nervousness, distress) should make people feel less confident in their ability to handle the aging process. In line with this part of the model, positive affect about aging has been positively associated with aging efficacy, whereas negative affect about aging has been negatively associated with aging efficacy (e.g., Fowler et al., 2015; Gasiorek et al., 2019). These associations were expected to replicate:

Aging efficacy is the direct antecedent to successful aging in the CEMSA (Fowler et al., 2015; Gasiorek et al., 2016). When people think that they are capable of handling age-related changes or challenges, such a perception should foster high satisfaction and contentment with life. Consistent with this, research has repeatedly documented positive associations between aging efficacy and successful aging (e.g., Bernhold & Gasiorek, 2020; Gettings & Kuang, 2022). This association was also expected to emerge in the current study:

Finally, the CEMSA proposes that aspects of environmental chatter are indirectly associated with successful aging, via the serial mediators of uncertainty discrepancies about aging, own age-related communication, affect about aging, and aging efficacy (Gasiorek et al., 2016). The CEMSA also proposes that own age-related communication is indirectly associated with successful aging, via the serial mediators of affect about aging and aging efficacy (Fowler et al., 2015). The last two hypotheses were offered given these points:

Method

Participants

The final sample consisted of 294 older adults (MAge = 59.27 years, SDAge = 7.23 years, RangeAge = 50–80 years). Participants were male (36.1%), female (63.6%), and unreported (0.3%). They listed their ethnicity as African American (14.3%), Asian American (2.7%), European American (78.2%), Latina/o American (2.0%), Multi-Ethnic (0.7%), Native American (1.4%), another ethnicity not listed in the closed-ended options (0.3%), and unreported (0.3%). Their annual household incomes were less than $9999 (2.0%), between $10,000 and $19,999 (6.1%), between $20,000 and $29,999 (7.5%), between $30,000 and $39,999 (8.2%), between $40,000 and $49,999 (9.2%), between $50,000 and $59,999 (10.2%), between $60,000 and $69,999 (7.1%), between $70,000 and $79,999 (7.5%), between $80,000 and $89,999 (5.8%), between $90,000 and $99,999 (6.8%), $100,000 or above (29.3%), and unreported (0.3%). Their highest levels of education were less than a high school diploma (0.7%), high school diploma or GED (11.9%), some college but no college degree (21.1%), associate’s degree (12.2%), bachelor’s degree (32.7%), master’s degree (16.7%), doctorate degree (4.4%), and unreported (0.3%). Participants reported their current employment statuses as employed full-time (50.0%), employed part-time (15.3%), retired (19.7%), unemployed and actively seeking work (5.4%), unemployed and not actively seeking work (5.8%), stayed at home during their adult life (e.g., a stay-at-home parent; 1.4%), another employment status not listed in the closed-ended options (2.0%), and unreported (0.3%).

Procedures for Participants

Adults were recruited from Prolific to take a 15-minute survey entitled “Research on Retirement and Aging”. Two filters were applied on Prolific, specifying that all participants had to (a) be at least 50 years old and (b) be living in the United States. The survey first asked participants to write the most important memorable message they heard about retiring from the workforce that has shaped their life as they have grown older. The online-only supplemental materials include the full instructions participants read when asked to write the memorable message. The survey then asked participants to complete the closed-ended measures of all the other constructs (e.g., successful aging), and the survey ended with demographic questions. Each participant received $3.00 for taking the survey.

Verifying the Authenticity of Participants

Mee (2025) described Prolific’s quality controls for ensuring the integrity of responses provided by its workers. One quality control involves setting a waitlist for people who want to become Prolific workers. Over 1,000,000 people are on this waitlist, whereas only 200,000 people are verified and active Prolific workers. Only 13% of people are invited off this waitlist and given the chance to become Prolific workers. Once given this chance, a person must pass over 50 verification checks before they can complete studies, including bank-grade identity checks. Only 55% of the people who are invited off the waitlist pass the verification process. A second quality control involves ongoing fraud detection once a person has been accepted as a Prolific worker. This ongoing fraud detection includes periodic identity re-confirmation checks (Mee, 2025). These quality controls help ensure that the Prolific workers who participated in the current study were who they said they were and that their responses were high-quality.

As an additional step to ensure data integrity, we included an open-ended question in the demographic section near the end of the survey asking each participant to type their age in years. A total of 299 Prolific workers initially provided data on the survey. Five of those 299 workers (1.67%) wrote an age less than 50 in the open-ended text box. The five responses from these workers were removed from the data set before data analysis, resulting in a final sample of 294 participants.

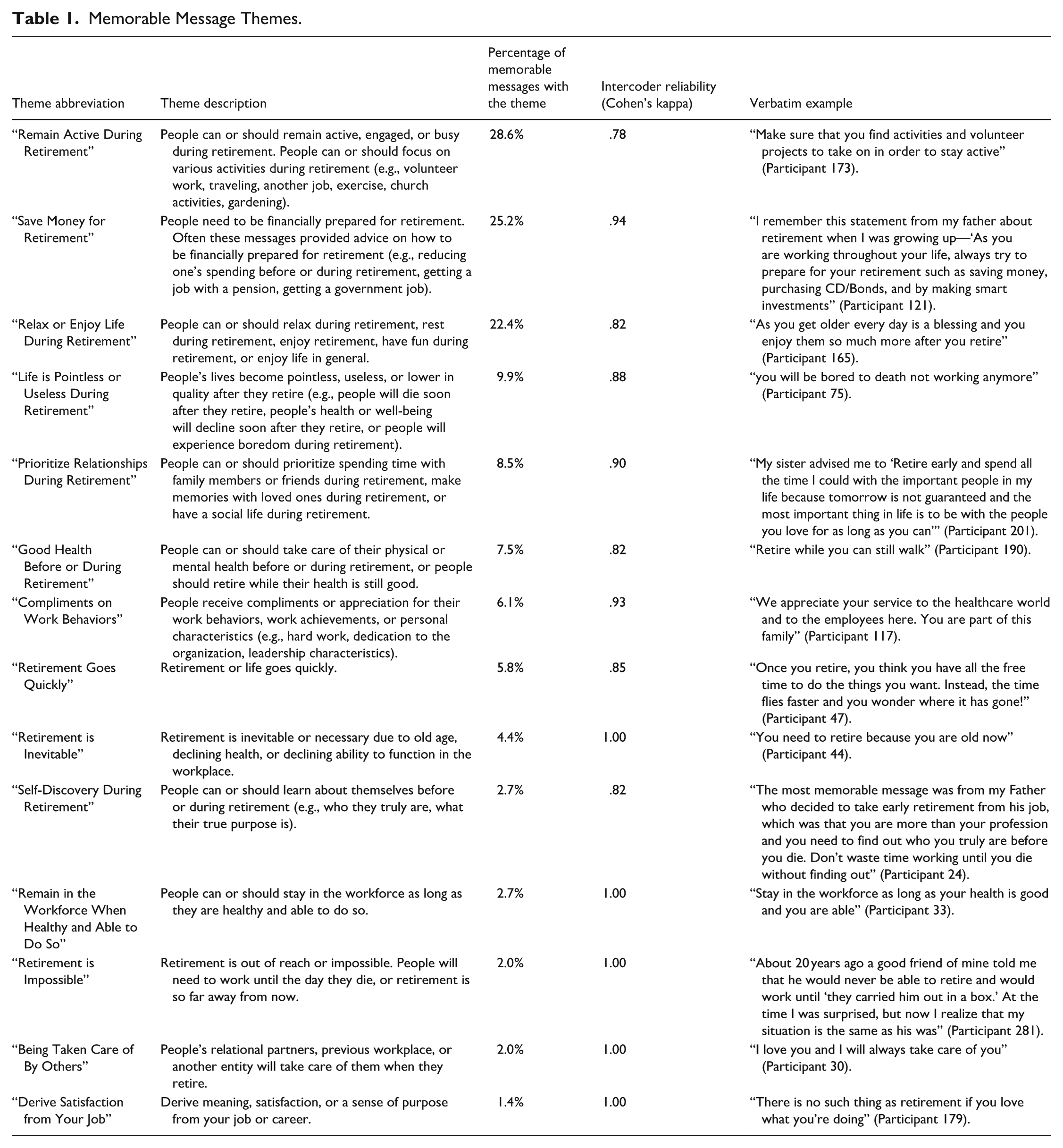

Coding Procedures to Answer RQ1

To code the memorable messages into themes, the first author initially read the messages multiple times to familiarize himself with the data. He then wrote a label capturing the key content of each message. Using the constant comparative technique (Strauss & Corbin, 1990), he looked for similarities and differences across the labels and collapsed conceptually similar labels into a category representing a theme. This process resulted in 20 themes created by the first author. The first author then recruited five graduate research assistants (GRAs) to provide feedback on whether or not the 20 themes appropriately captured the content of the messages. The GRAs pointed to several themes that conceptually overlapped with one another and offered feedback on how to consolidate the 20 themes into a shorter, more manageable set of themes. The first author implemented their feedback, resulting in 14 final themes.

The first author assigned all five GRAs to independently code the first 80 memorable messages for each theme. He then calculated intercoder reliability for each pair of two GRAs for each theme. All the themes demonstrated sufficient intercoder reliability after this first round of independent coding. Next, the first author assigned the two GRAs who coded a given theme most reliably with one another to code the remaining messages for that theme. Each GRA in this pair coded half of the remaining messages for the theme. Each GRA in this pair also reviewed half of the messages from the first round of independent coding and looked for any points of disagreement between them and the other GRA regarding whether or not a given message contained the theme. When they found a point of disagreement, the GRA acted as a tie-breaker and decided if the message contained the theme. The themes were not mutually exclusive, so a message could be coded as containing multiple themes. The GRAs coded a message as containing multiple themes if separate parts of the message addressed different topics. For example, Participant 277 wrote the following memorable message: “

Memorable Message Themes.

Theme Trustworthiness

The first author took several steps to ensure the themes’ trustworthiness. First, data saturation occurs in qualitative coding when researchers are gaining no new insights from the data (Morse, 1995). Reaching data saturation helps ensure that qualitative findings are sufficient in scope and depth (Naeem et al., 2024). The first author reached data saturation around the 200th memorable message when he was initially creating the themes. Second, the first author consulted with the five GRAs about their impressions of the 20 themes he initially created. The first author agreed with the GRAs’ feedback about how certain themes should be combined given their conceptual overlap. Franklin et al. (2010) labeled this practice investigator triangulation, whereby a researcher cross-checks their interpretations of the data with other researchers’ interpretations to arrive at favored interpretations. After the first author combined certain themes based on the feedback from the GRAs, the GRAs agreed that the 14 final themes appropriately captured the messages’ content. Third, methods triangulation, which involves combining qualitative and quantitative analyses in the same study, is another procedure to establish the trustworthiness of qualitative findings (Franklin et al., 2010). The incorporation of the three most common memorable message themes into the quantitative path model (described below) and the significant associations between these themes and other CEMSA constructs suggest that the themes were meaningfully capturing key content in the messages.

Closed-Ended Measures of the Substantive Variables

Bivariate correlations appear in Table S1 in the online-only supplemental materials. The online-only supplemental materials also describe confirmatory factor analyses that were run to verify that the measures were operationalizing distinct constructs.

Uncertainty Discrepancies

Three items from Fowler et al. (2015) operationalized uncertainty discrepancies (e.g., “I know less than I would like to about what my life will be like as I get older”; 1 = strongly disagree, 7 = strongly agree; M = 4.26, SD = 1.63, α = .91).

Own Communication About Financial Preparations for Retirement

One item adapted from Gettings and Kuang (2022) and two new items measured own communication about financial preparations for retirement (i.e., “I talk with family or friends about how I will financially support myself during retirement”, “I discuss with others how I can be financially prepared for retirement”, “I talk about how I can save enough money for retirement”; 1 = strongly disagree, 7 = strongly agree; M = 4.48, SD = 1.72, α = .91).

Positive Affect

Consistent with other CEMSA research (e.g., Fowler et al., 2015), five items from the Positive and Negative Affect Schedule (PANAS; Watson & Clark, 1994) operationalized positive affect about aging. Participants reflected on their feelings when they think about growing older and rated the items (e.g., “excited”, “enthusiastic”) on a five-point scale (1 = very slightly/not at all, 5 = very much; M = 3.03, SD = 1.17, α = .94).

Negative Affect

Consistent with other CEMSA research (e.g., Fowler et al., 2015), four items from the PANAS (Watson & Clark, 1994) operationalized negative affect about aging. Participants reflected on their feelings when they think about growing older and rated the items (e.g., “scared”, “upset”) on a five-point scale (1 = very slightly/not at all, 5 = very much; M = 2.18, SD = 1.13, α = .92).

Aging Efficacy

Four items from Fowler et al. (2015) assessed aging efficacy (e.g., “I feel able to cope with things that might happen to me as I age”; 1 = strongly disagree, 7 = strongly agree; M = 5.13, SD = 1.33, α = .93).

Successful Aging

Three items from Fowler et al. (2015) measured successful aging (e.g., “How do you rate your life these days?”; 1 = very poor, 7 = very great; M = 5.30, SD = 1.27, α = .90).

Covariates

The path model used to test H1–H8 is described in the next sub-section below. Eleven covariates were originally included in this path model: the participant’s sex (0 = male; 1 = female), age, ethnicity (0 = all ethnicities other than European American; 1 = European American), annual household income, highest level of education, employment status (0 = retired, unemployed and actively seeking work, unemployed and not actively seeking work, stayed at home during their adult life [e.g., a stay-at-home parent], or another employment status other than employed full-time or part-time; 1 = employed full-time or part-time), perception of their physical health, perception of their mental health, probability of being a gloomy ager, probability of being a disengaged ager, and probability of being a bantering ager. One item measured perceived physical health (i.e., “Overall, I am physically healthy”; 1 = strongly disagree, 7 = strongly agree; M = 5.37, SD = 1.50), and one item measured perceived mental health (i.e., “Overall, I am mentally healthy”; 1 = strongly disagree, 7 = strongly agree; M = 5.75, SD = 1.37).

Twenty-one items from Fowler et al. (2015) measured the original seven domains of own age-related communication (e.g., “When I forget something, or have trouble with a task, I often say it is because of my age”; 1 = strongly disagree, 7 = strongly agree). LPAs were run on these 21 items in Mplus 8.10, with one- to five-profile models being explored. The four-profile model was selected as the best model given that the four profiles in this model closely resembled the four profiles from previous research (e.g., Bernhold et al., 2020). In the four-profile model, participants were classified as engaged agers (24.1% of the sample), gloomy agers (33.3%), disengaged agers (19.7%), and bantering agers (22.4%). In addition to classifying each participant into their most likely profile, Mplus provides continuous probabilities of each participant belonging to each profile. Each participant’s four probabilities always sum to 1.00. One profile needs to be selected as the reference profile and omitted from the model to avoid redundant information in the model (see Bernhold, 2022; Bernhold et al., 2020). We selected engaged agers as the reference profile.

The covariates were specified as predicting the memorable message themes, uncertainty discrepancies, own communication about financial preparations for retirement, positive affect, negative affect, aging efficacy, and successful aging in the path model. However, the participant’s sex and annual household income were not associated with any of the substantive variables. As such, these two covariates were removed from the path model for parsimony.

Path Model to Test H1–H8

To test the hypotheses, a path model was run in Mplus 8.10 (Muthén & Muthén, 2017). The path model utilized the observed versions of the variables. In the model, the three most common memorable message themes were specified as predicting uncertainty discrepancies, own communication about financial preparations for retirement, positive affect, negative affect, and aging efficacy. These three themes were included given that there was a sizable gap in frequency between the third-most common theme and the fourth-most common theme (see Table 1). It therefore seemed most logical to include the three most common themes. Each theme was coded as 0 = memorable message does not contain the theme; 1 = memorable message contains the theme. Uncertainty discrepancies were specified as predicting own communication about financial preparations for retirement, positive affect, negative affect, and aging efficacy. Own communication about financial preparations for retirement was specified as predicting positive affect, negative affect, and aging efficacy. Positive and negative affect were specified as predicting aging efficacy, and aging efficacy was specified as predicting successful aging. The “Model indirect:” command tested for indirect associations (Muthén, 2016).

Results

RQ1 asked what themes appear in memorable messages about retirement. Fourteen themes emerged from the data, and Table 1 describes all 14 themes.

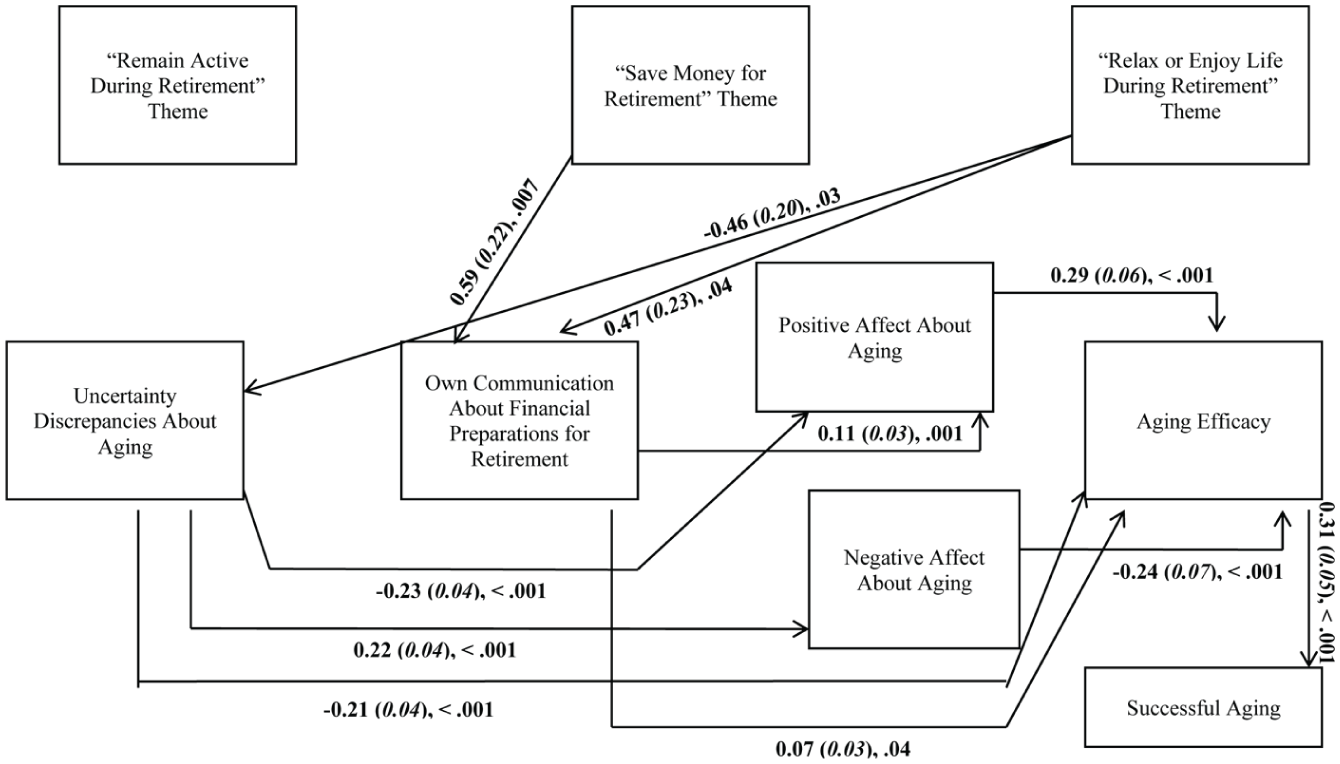

Figure 2 is the path model displaying the significant associations between the substantive variables. Only the significant associations appear in Figure 2 for the sake of readability. A path model depicting both the significant associations and the nonsignificant associations appears as Figure S1 in the online-only supplemental materials. Table S2 in the online-only supplemental materials provides path coefficients for the associations between the covariates and substantive variables.

Path model results. Each series of numbers is the unstandardized path coefficient, followed by the (standard error) and p-value. With the exception of an elevated RMSEA, the path model demonstrated acceptable fit: χ2 (7) = 47.24, p < .001, CFI = 0.96, RMSEA = 0.14 (90% CI = 0.10 – 0.18), SRMR = 0.02. Other interpersonal communication research has also reported models with one fit index outside the range of acceptable fit (e.g., Pusateri et al., 2016). The model (with covariates included) explained 24.7% of the variance in uncertainty discrepancies, 17.3% of the variance in own communication about financial preparations for retirement, 40.9% of the variance in positive affect about aging, 41.2% of the variance in negative affect about aging, 56.0% of the variance in aging efficacy, and 54.1% of the variance in successful aging.

H1 predicted that the memorable message themes would be associated with uncertainty discrepancies about aging (H1a), positive affect about aging (H1b), negative affect about aging (H1c), aging efficacy (H1d), and own communication about financial preparations for retirement (H1e). H1a was partially supported, because participants who wrote a message with the “relax or enjoy life during retirement” theme reported lower uncertainty discrepancies, compared to participants who did not write a message with this theme. H1b, H1c, and H1d were not supported. H1e was partially supported, because participants who wrote a message with the (a) “save money for retirement” theme or (b) “relax or enjoy life during retirement” theme reported higher own communication about financial preparations for retirement, compared to participants who did not write a message with one of these themes.

H2 proposed that uncertainty discrepancies about aging would be positively associated with negative affect about aging (H2a) and negatively associated with positive affect about aging (H2b), aging efficacy (H2c), and own communication about financial preparations for retirement (H2d). H2a, H2b, and H2c were supported, but H2d was not supported.

H3 stipulated that own communication about financial preparations for retirement would be positively associated with positive affect about aging (H3a) and aging efficacy (H3b) and negatively associated with negative affect about aging (H3c). H3a and H3b were supported, but H3c was not supported.

The next hypotheses predicted that positive affect about aging would be positively associated with aging efficacy (H4), negative affect about aging would be negatively associated with aging efficacy (H5), and aging efficacy would be positively associated with successful aging (H6). H4, H5, and H6 were all supported.

H7 proposed that the memorable message themes would be indirectly associated with successful aging, via the serial mediators of uncertainty discrepancies about aging, own communication about financial preparations for retirement, positive affect about aging, negative affect about aging, and aging efficacy. Thirty-six indirect associations were tested for H7, and one emerged as significant: “relax or enjoy life during retirement” theme → uncertainty discrepancies → aging efficacy → successful aging (indirect association = 0.03, SE = 0.015, p = .049). This indirect association should be interpreted with caution given the possibility of Type I error and how close its p value is to the conventional cutoff of p < .05.

H8 stipulated that own communication about financial preparations for retirement would be indirectly associated with successful aging, via the serial mediators of positive affect about aging, negative affect about aging, and aging efficacy. Three indirect associations were tested for H8, and one emerged as significant: own communication about financial preparations for retirement → positive affect about aging → aging efficacy → successful aging (indirect association = 0.01, SE = 0.004, p = .01).

Discussion

Theoretical Contributions

The study offers four theoretical contributions. First, the CEMSA holds that environmental chatter may bear implications for own age-related communication (Gasiorek et al., 2016). Several counterintuitive findings have emerged in research testing this part of the model. For example, Gasiorek and Fowler (2020) found that middle-aged and older adults’ perceptions of receiving both accommodation and nonaccommodation from younger adults were positively associated with middle-aged and older adults’ collusions with age stereotypes in their own communication (e.g., using simpler language and sentences when talking with older adults). Gasiorek and Fowler noted that both intergenerational accommodation and nonaccommodation may be forms of environmental chatter that render age salient. It may be the “salience of age in intergenerational interaction—rather than the valence or quality of the interaction—that prompts middle-aged and older adults to communicate with others in ways consistent with age stereotypes” (Gasiorek & Fowler, 2020, p. 113; see also Gettings & Kuang, 2022).

Associations between environmental chatter and own age-related communication also emerged in the current study. To understand these associations, it is first helpful to consider how the three most prevalent memorable message themes are conceptually distinct from one another. The “remain active during retirement” theme differed from the other two themes in its focus on keeping busy with activities. Messages with this theme often referenced activities such as exercising, gardening, getting another job, participating in church events, traveling, or volunteering. As such, this theme had an instrumental focus on engaging in tasks. The “save money for retirement” theme also had an instrumental focus, but this focus was limited to how people could save enough money for retirement and the necessity of saving enough money for retirement. In contrast, the “relax or enjoy life during retirement” theme had an affective focus rather than an instrumental focus. This theme emphasized the importance of relaxing during retirement, enjoying retirement, having fun during retirement, or enjoying life in general. Thus, this third theme highlighted the importance of people’s affective well-being.

All three themes might make saving enough money for retirement a salient issue. For the first theme, certain activities (e.g., gardening, traveling) often require financial resources. If people hear memorable messages about these activities, they may think about whether or not they have enough money for these activities. For the second theme, hearing memorable messages about the importance of saving enough money for retirement may make saving enough money for retirement a salient issue. In terms of the third theme, older adults may not be able to fully relax or enjoy life if they do not have enough money to meet their basic living expenses. Consistent with this reasoning, Teater and Chonody’s (2020) narrative review of successful aging research reported that older adults often worry when they do not have enough money to meet their basic living expenses. Hearing memorable messages about relaxing or enjoying life during retirement may prompt adults to consider if they have enough money to meet their basic living expenses during retirement. If so, they may think that they will be able to relax and enjoy life during retirement. If not, they may think that they will not be fully able to relax and enjoy life.

There may be some credence to the notion that these memorable message themes make having enough money saved for retirement a salient issue. Participants who wrote a memorable message with the “save money for retirement” theme or the “relax or enjoy life during retirement” theme reported engaging in more communication about their own financial preparations for retirement compared to participants who did not write a memorable message with one of these two themes. Although the association between the “remain active during retirement” theme and own communication about financial preparations for retirement was null, it was positive in direction. Future researchers should continue probing this association by dividing the “remain active during retirement” theme into three more specific sub-themes: (1) messages that reference keeping busy without naming specific activities, (2) messages that reference keeping busy by naming specific activities that often cost money (e.g., gardening, traveling), and (3) messages that reference keeping busy by naming specific activities that are often free (e.g., volunteering). Of these three sub-themes, the second sub-theme may be most likely to make saving enough money for retirement a salient issue and may therefore be most likely to be associated with own communication about financial preparations for retirement.

A second theoretical contribution pertains to the significant associations involving own communication about financial preparations for retirement, after controlling for adults’ probabilities of being in the ager profiles. Scholars could, conceivably, offer numerous additional domains of own communication above and beyond the original seven domains proposed by Fowler et al. (2015). For example, Bernhold et al. (2025) proposed adding older adults’ (a) offering of religious support to others and (b) seeking religious support from others as two new domains of own communication in the CEMSA. Bernhold et al. found that both of these communication domains were indirectly associated with successful aging, via aging efficacy. However, Bernhold et al. did not control for adults’ probabilities of being in the ager profiles when testing these indirect associations. Further, the two new domains offered by Bernhold et al. seem to stray away from the CEMSA’s original spirit of focusing on age-related communication.

It may therefore be worthwhile to reexamine all of the new domains of own communication offered after Fowler et al.’s (2015) original delineation of the CEMSA to determine whether they merit inclusion in the CEMSA. In this spirit, the current study tested how own communication about financial preparations for retirement was associated with other CEMSA constructs, while controlling for the probabilities of being in the ager profiles. Two of the three most common memorable message themes were associated with own communication about financial preparations for retirement. Additionally, own communication about financial preparations for retirement was (a) directly associated with positive affect about aging and aging efficacy and (b) indirectly associated with successful aging, via the serial mediators of positive affect about aging and aging efficacy. This range of associations suggests that own communication about financial preparations for retirement may warrant a place in the CEMSA alongside the original seven domains. If future researchers continue proposing new domains of own age-related communication, they should account for the original seven domains in their statistical analyses. Doing so helps determine if the new domains explain unique variance in CEMSA constructs, above and beyond what can be explained by the original domains.

A third theoretical contribution concerns uncertainty discrepancies about aging. Older adults who wrote a memorable message about relaxing or enjoying life during retirement reported lower uncertainty discrepancies about aging, compared to older adults who did not write a message with this theme. Gasiorek et al. (2016) reasoned that memorable messages may reduce uncertainty discrepancies if memorable messages offer information about what older age is likely to entail, and the current study’s findings offer some support for this reasoning. Equally important, uncertainty discrepancies were not associated with people’s own communication about their financial preparations for retirement. Uncertainty discrepancies may prompt people to anticipate what a search for information is likely to bring about (Afifi & Weiner, 2004). When they experience uncertainty discrepancies about aging or retirement, some people may anticipate that talking about their own financial preparations for retirement will bring about negative outcomes, such as revealing that they are behind where they should be in saving for retirement. When outcome expectancies are negative, people often refrain from seeking information (Afifi & Matsunaga, 2008). For this reason, uncertainty discrepancies were hypothesized to be negatively associated with own communication about financial preparations for retirement.

Although the association in the current study was null, it was negative in direction. Future researchers should test outcome expectancies as moderating this association. The association might be negative for older adults who hold negative expectancies about what seeking information about financial preparations for retirement is likely to bring about. In contrast, the association might be positive for older adults who hold positive expectancies about what seeking information about financial preparations for retirement is likely to bring about. If researchers test outcome expectancies as a moderator, they would contribute to the CEMSA by delineating a contingency condition in the model (see DeAndrea & Holbert, 2017).

The fourth theoretical contribution involves the associations for affect. Own communication about financial preparations for retirement was positively associated with positive affect about aging. However, the memorable message themes and own communication about financial preparations for retirement were not associated with negative affect about aging. Positive and negative affect about aging may operate independently from one another in the CEMSA (Bernhold et al., 2026). Supporting this, Bernhold et al. (2024) found that older adults’ perceptions of having a positive role model for aging were positively associated with their positive affect about aging, but not associated with their negative affect about aging. As another example, Fowler et al. (2015) found that adults’ (a) planning for their future caregiving needs and (b) use of new communication technologies to stay in touch with loved ones were both positively associated with positive affect about aging, but not associated with negative affect about aging. Thus, just because a component of environmental chatter or own age-related communication is associated with heightened positive affect does not necessarily mean that it is also associated with decreased negative affect. For these reasons, negative affect about aging may be relatively entrenched and difficult to change through seemingly positive forms of communication.

Cultural Contextualization of the Findings and Future Culture-Centered Research

All of the participants in the current study were living in the United States. The United States has been described in general as an individualistic nation (Croucher et al., 2024). Individualism involves people prioritizing their own goals over the goals of groups, meeting their own personal needs, and pursuing their own personal desires (Triandis, 1995). In contrast, collectivism involves people viewing themselves as connected to larger groups (e.g., families, work groups), prioritizing group goals over their own personal goals, and fulfilling responsibilities to groups (Triandis, 1995). There may be differences in how individualistic people of different ethnic groups are in the United States. In particular, vertical individualism refers to “the autonomous self that garners gratification through competition and personal achievement” (Vargas & Kemmelmeier, 2013, p. 196). Meta-analysis of research in the United States has shown that European Americans report higher vertical individualism than do African Americans and Latina/o Americans (Vargas & Kemmelmeier, 2013).

The measurement of own communication about financial preparations for retirement focused on the participant talking about how they as an individual can be financially prepared for retirement (e.g., “I talk about how I can save enough money for retirement”). This measurement appears consistent with individualism (the individual is responsible for meeting their own needs) and vertical individualism (the individual achieves financial success). Own communication about financial preparations for retirement was positively associated with positive affect about aging and aging efficacy. Future researchers should test whether own communication about financial preparations for retirement (as measured in the current study) is more strongly associated with positive affect about aging and aging efficacy for older adults who more strongly endorse individualism or vertical individualism when compared to older adults who less strongly endorse individualism or vertical individualism.

Limitations

The study contributions should be contextualized alongside the study limitations. First, the study measured uncertainty discrepancies about aging, affect about aging, and aging efficacy at the general level. The precedent in CEMSA research is to examine these constructs at the general level (e.g., Fowler et al., 2015; Gettings & Kuang, 2022). The current study followed this precedent. The significant associations that did emerge suggest the merit of considering these constructs at the general level. With that said, future researchers could also find value in examining more circumscribed versions of uncertainty discrepancies, affect, and efficacy. For example, uncertainty discrepancies about aging were not associated with own communication about financial preparations for retirement. Future researchers should test how uncertainty discrepancies about the state of one’s finances during retirement are associated with one’s own communication about financial preparations for retirement. A significant association may be observed if this more circumscribed version of uncertainty discrepancies were measured.

A second limitation is that the study relied on data from a cross-sectional survey, and causality cannot be established. Future researchers should collect longitudinal data to probe which variables temporally precede which other variables. Researchers should also design experiments that test how communication interventions related to financial aspects of aging may prompt changes in other CEMSA variables (e.g., uncertainty discrepancies about aging or about the state of one’s finances during retirement). The CEMSA proposes that uncertainty discrepancies predict one’s own communication (Fowler et al., 2015). Future experiments may show that changes in one’s own communication lead to changes in uncertainty discrepancies. If so, future iterations of the CEMSA could account for these causal relationships.

As a third limitation, the survey did not ask participants how financially prepared they felt for retirement, how much money they have saved for retirement, or what their outcome expectancies are for conversations about their financial preparations for retirement. Future researchers can measure and account for these considerations. Relatedly, participants’ annual household incomes were not associated with any of the substantive variables. One potential explanation for these null associations is that the amount of money participants have saved for retirement is a better predictor of CEMSA variables (e.g., aging efficacy, successful aging) than is participants’ annual household incomes. An older adult with a modest annual household income might still experience high aging efficacy and high successful aging if they have steadily saved for retirement over many decades. In contrast, an older adult with a high annual household income might experience low aging efficacy and low successful aging if they spend all or almost all of their income every year and have little or no money saved for retirement. For this reason, future researchers should measure and account for not only participants’ annual household incomes, but also how much money participants have saved for retirement.

Fourth, the sample was mainly comprised of females and European Americans. Future researchers should obtain samples more balanced in terms of sex and ethnicity. The participant’s sex was not associated with any of the substantive variables, suggesting that the sample’s sex composition may not have unduly influenced the results. The participant’s ethnicity was associated with uncertainty discrepancies about aging, such that European American participants reported larger uncertainty discrepancies than participants who were not European American. Several European countries—including Greece, Spain, Portugal, Belgium, and France—score high on uncertainty avoidance (Yi, 2021). Uncertainty avoidance is “the extent to which societies tolerate ambiguity” (Wennekers et al., 2007, p. 139). In high uncertainty avoidance countries, many people are threatened by ambiguity and therefore try to make their lives predictable (Hofstede, 2001; Wennekers et al., 2007). In low uncertainty avoidance countries, many people are not threatened by ambiguity and therefore accept risks (Hofstede, 2001; Wennekers et al., 2007). In the current study, some European American participants may have experienced high uncertainty avoidance with respect to their lives and futures. This high uncertainty avoidance may have led them to think that there are gaps between how much they know and how much they would like to know about their aging. Future researchers should test associations between uncertainty avoidance and uncertainty discrepancies about aging. Given that European American participants reported larger uncertainty discrepancies about aging, interventions to reduce uncertainty discrepancies may be especially relevant for European American older adults.

Conclusion

In sum, the current study contributed to the CEMSA by examining how retirement communication is associated with aging experiences. One of the study’s main goals was to determine the merit of including own communication about financial preparations for retirement alongside the original seven domains of own communication proposed by Fowler et al. (2015). Gettings and Kuang (2022) found that own communication about retirement preparations (not exclusively about financial preparations) was not associated with affect about aging or aging efficacy. In contrast, own communication about financial preparations for retirement was associated with two of the three most common memorable message themes, positive affect about aging, and aging efficacy in the current study. Thus, the current study revisited the domain of own age-related communication proposed by Gettings and Kuang and found more robust associations when examining a more circumscribed version of this variable.

Another goal was to examine associations between the memorable message themes and own communication about financial preparations for retirement. The fact that two of the three most common themes were associated with own communication about financial preparations for retirement lends additional credence to the notion that various aspects of environmental chatter may make age salient and prompt own age-related communication (Gasiorek & Fowler, 2020; Gettings & Kuang, 2022). The study’s mixed-methods design made these theoretical contributions in a methodologically rigorous way by correlating the memorable message themes with older adults’ closed-ended responses on measures assessing other CEMSA constructs.

Supplemental Material

sj-docx-1-crx-10.1177_00936502261463578 – Supplemental material for Memorable Messages About Retirement, Own Communication About Financial Preparations for Retirement, and Successful Aging: Testing Theoretical Mechanisms in the Communicative Ecology Model of Successful Aging

Supplemental material, sj-docx-1-crx-10.1177_00936502261463578 for Memorable Messages About Retirement, Own Communication About Financial Preparations for Retirement, and Successful Aging: Testing Theoretical Mechanisms in the Communicative Ecology Model of Successful Aging by Quinten S. Bernhold, Cole Jagger Lazerus Burns, Kylie Julius, Peyton Mills, Sarah Devereux and Traci Lively in Communication Research

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by the Faculty Research Innovation Fund in the College of Communication and Information at the University of Tennessee, Knoxville. The first author applied for and received this internal funding.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.