Abstract

This article examines whether the level of environmental, social, and governance (ESG) disclosure in Andalusian municipal-owned enterprises varies by two attributes: industry and the local government that owns the company. To do this, the authors conduct a content analysis of multiple communication channels of 307 MOEs using a validated instrument. Consistent with our initial expectation, we find that ESG disclosure among Andalusian MOEs tends to be isomorphic across firms operating in the same sector and those owned by the same local government. Our follow-up analysis has allowed us to identify alternative explanations for the higher levels of voluntary rather than mandatory disclosure among Andalusian MOEs. Companies that engage in greater voluntary ESG disclosure evidently are driven more by normative than coercive forces.

Introduction

The prevailing social and institutional context is changing the conversation about the role organizations can play in disclosing environmental, social, and governance (ESG) information (Bebbington & Unerman, 2020). Over the past decade, two significant factors have strengthened large corporations’ commitment to ESG disclosure: the introduction of sustainability reporting regulations and the adoption of the 17 Sustainable Development Goals (SDGs) outlined in Agenda 2030 (Gutiérrez-Ponce et al., 2022; Gutiérrez-Ponce, 2023).

In this scenario, municipal-owned enterprises (MOEs) 1 are increasingly pressured to provide ESG disclosure (Ligorio et al., 2022; Torres et al., 2024). Compared to the private sector, MOEs face higher expectations and obligations regarding accountability (Giacomini et al., 2020; Greiling & Grüb, 2014). As providers of essential public services, such as water supply and public transport, MOEs play crucial roles in the transition toward a more sustainable society (Dicorato et al., 2020; Valenza & Damiano, 2023). With a mission to promote the common good (Greiling & Grüb, 2014), MOEs are responsible for addressing the challenges and needs of their local communities, including working toward the achievement of the SDGs (Giacomini et al., 2020; Gutiérrez-Ponce, 2023). MOEs face significant public scrutiny due to their close ties with the communities they serve (Andrades et al., 2019; Garde et al., 2017). Consequently, ESG disclosure can offer MOEs two main advantages: (1) it serves as a tool for accountability to society, reflecting their impact on the community (Dicorato et al., 2020; Valenza & Damiano, 2023) and (2) it acts as a legitimizing mechanism in response to their public exposure (Greiling & Grüb, 2014; Nicolo et al., 2021).

Meanwhile, as “organizations situated at the boundary between the public and private sector” (Nicolo et al., 2021, p. 139), many regard MOEs as hybrid entities because they possess a mix of ownership from both public and private sectors (Argento et al., 2019). As a result, MOEs must adhere to mandatory disclosure requirements mandated by both public and private laws (Andrades & Larran, 2019; Valenza & Damiano, 2023). The complexity of MOEs, stemming from their mixed ownership structure, is also reflected in how they integrate social and business principles in their management practices (Grossi et al., 2022; Ligorio et al., 2022). According to Yetano and Sorrentino (2023, p. 296), hybrid organizations, including MOEs, “face challenges and risks that are similar to private organizations, while they differ from them due to their crucial societal role.” This supposes that MOEs need to be accountable to a broad range of stakeholders with multiple interests (Grossi et al., 2022; Ligorio et al., 2022). Thus, MOEs could provide ESG disclosures to simultaneously address the expectations of diverse stakeholders with varying interests in the organization (Valenza & Damiano, 2023; Yetano & Sorrentino, 2023). Nonetheless, existing scholarship on sustainability disclosure in this setting is relatively limited (Vinnari & Laine, 2013). Indeed, some scholars have pointed out that the role of sustainability disclosure in MOEs is still not clearly defined (Ligorio et al., 2022).

This article utilizes a neo-institutional theory perspective to analyze the degree of convergence in ESG disclosure practices among Andalusian MOEs. Specifically, we investigate whether the level of ESG disclosure tends to be isomorphic based on influence from two fields: the industry and local government. We content analyzed texts from the communication channels of 307 MOEs, including websites, transparency portals and non-financial and sustainability reports, using a validated tool previously employed in the literature.

Andalusia requires special attention due to its climate, which notably affects the physical environment, particularly in terms of water availability (Cabello et al., 2021). A recent report by the AXA Foundation for the period of 2023 to 2024 reveals that 83.7% of Andalusian citizens believe that climate change is occurring and view it as the main problem facing the region (Axa Foundation, 2023). Consistent with previous research, Andalusia can be considered a high-risk area from an environmental perspective (Young & Marais, 2012). Therefore, organizations in this region may be more sensitive to environmental issues and are likely to disclose ESG information to meet societal demands (Andrades & Larran, 2019).

This study addresses a gap in the literature on ESG disclosure, focusing on a type of under-researched organization known as an MOE. This type of enterprise provides a distinctive context for exploring ESG disclosure issues due to MOEs’ organizational structure, varied agency environment, specific objectives, and connection to the community (Argento et al., 2019; Grossi et al., 2015). The complexity of their structure, combined with the diverse stakeholders they must engage with, makes ESG disclosure particularly challenging for these entities (Yetano & Sorrentino, 2023). Scholars have noted the need for more research that connects ESG disclosure to MOEs to better understand how hybrid organizations operate (Argento et al., 2019; Grossi et al., 2022). Given their hybrid nature, MOEs may have different motivations for providing ESG disclosures compared to private companies or solely public sector organizations.

Theoretical Framework and Hypothesis Development

Institutional theory is a key framework for understanding how organizations react to external pressures regarding ESG disclosure (Adams & Larrinaga, 2019; Higgins & Larrinaga, 2014). This theory posits that organizations often conform to the prevailing norms and values within their social context (Oliver, 1997). Consequently, organizations tend to become isomorphic with their environment by adopting similar practices or structures that align with socially expected norms for survival (DiMaggio & Powell, 1983). Specifically, organizations that occupy similar positions within a field are more likely to adopt comparable practices, norms, or structures (de Villiers et al., 2014; Posadas et al., 2023). Three primary sources of institutional isomorphism—mimetic, coercive, and normative forces—explain whether and how organizations respond to external pressures to gain legitimacy (Collin et al., 2009; DiMaggio & Powell, 1983). The interaction of these mimetic, coercive, and normative forces shapes the extent to which ESG disclosure drives isomorphic behavior in a given context (Higgins & Larrinaga, 2014; Posadas et al., 2023).

Organizations often reflect the practices of similar institutions in uncertain environments due to the mimetic forces of institutional isomorphism (de Villiers et al., 2014). They are influenced by their peers’ actions and strive for legitimacy (Andrades et al., 2023). Additionally, the coercive aspect of institutional isomorphism indicates that organizations may feel external pressure to conform to regulations or directives (de Villiers & Alexander, 2014; Zhao & Patten, 2016). Typically, coercive isomorphism is associated with the resource-dependency perspective, which suggests that companies rely on other focal organizations (Haraldsson & Tagesson, 2014). Moreover, the normative force of institutional isomorphism emphasizes the role of professionals—such as standard-setters, academic networks and consultants—that are instrumental in developing norms (Bebbington et al., 2012; Zhao & Patten, 2016). Their expertise can create an environment where disclosing ESG information is seen as a socially expected practice (Montecalvo et al., 2018; Posadas et al., 2023).

Here, the organizational field is a key concept in neo-institutional theory (Higgins & Larrinaga, 2014; Wooten & Hoffman, 2017). According to Scott (1995, p. 56), an organizational field is defined as “a community of organizations that partake of a common meaning system and whose participants interact more frequently and fatefully with one another than with actors outside the field.” Following the ideas of DiMaggio and Powell (1983, p. 143), an organizational field consists of “those organizations that, in the aggregate, constitute a recognized area of institutional life.” Under these definitions, organizational fields are communities of diverse organizations that interact within a shared environment, collectively shaping norms and expectations (Higgins et al., 2018; Zapp & Powell, 2016). The behavior of organizations in these fields is influenced by three main sources of institutional pressure that produce common reactions, resulting in isomorphism (DiMaggio & Powell, 1983; Scott, 1995).

Institutional scholars often compare “fields” compared to “industries,” but fields also can also develop in specific geographic locations (Higgins et al., 2018). Recent studies suggest that ESG disclosure tends to show similarities in certain geographic regions and industry sectors (Dienes et al., 2016; Young & Marais, 2012). From a geographic perspective, previous research has demonstrated that sustainability reporting patterns do not converge on an international level due to various social, political, and legal factors (Bebbington et al., 2009). Similar patterns in sustainability reporting are generally confined to regional areas where organizations share historical, cultural, and socio-political elements that affect their ESG disclosure practices (Bebbington et al., 2012). For our research purposes, it is important to closely examine the role of local municipalities in influencing ESG disclosure by Andalusian MOEs. From an institutional perspective, resource dependency exists between the MOEs and the municipalities that own them (Haraldsson & Tagesson, 2014). The municipality is the most powerful stakeholder of Andalusian MOEs, as it is the main provider of their financial resources (Royo et al., 2019). Consequently, MOEs owned by the same municipality are inserted in a geographically-based local field (Higgins et al., 2018). This positioning compels these companies to adopt ESG disclosure practices to meet the expectations of their owner and maintain legitimacy (Ligorio et al., 2022).

Accordingly, we anticipate that Andalusian MOEs under the same local government will likely demonstrate similar levels of ESG disclosure compared to others:

Focusing on the industry, numerous empirical studies have identified variations in ESG disclosure patterns that correspond to the sensitivity of different industries to environmental issues (Bebbington et al., 2009; Young & Marais, 2012). This suggests that institutional pressures can vary by industry sector, which may explain why ESG disclosure is more common in some areas than in others (Dienes et al., 2016; Higgins et al., 2018). In the context of the MOE setting, companies operating in environmentally sensitive sectors, such as water management, waste collection and transportation, have greater incentives to enhance their levels of ESG disclosure (Testa, 2024).

In addition to managing and providing essential public services, these companies also generate negative externalities that harm the environment due to their inherent characteristics (Imperiale et al., 2023). As a result, they become more visible and face increased scrutiny from local communities (Ligorio et al., 2022). Therefore, we anticipate that organizations in environmentally sensitive sectors are likely to demonstrate comparable levels of ESG disclosure to those in other sectors.

Methodology

Contextualization of the Research

The Spanish context is particularly interesting due to its long-standing tradition of ESG disclosure practices (Reverte, 2015). Furthermore, various historical, cultural and socio-political developments have influenced ESG disclosure activities in Spain over the past two decades (Archel & Husillos, 2009).

In the 1980s and 1990s, the Spanish government implemented a substantial privatization process within the public business sector (Royo et al., 2019). However, this trend began to reverse at the beginning of the 21st century, especially for MOEs (Andrades & Larran, 2019). Consequently, there has been an increase in the number of such enterprises, the majority of which focus on promoting regional and cultural development, developing tourism and sports activities, or enhancing housing initiatives.

The Spanish government has aligned its regulations on the disclosure of ESG information with the European Union through two key laws: Law 2/2011 on Sustainable Economy and Law 11/2018 on Non-Financial Information (Larrinaga et al., 2018). The first law does not require MOEs to produce annual sustainability reports. However, the second law mandates that larger MOEs prepare a non-financial information statement (Andrades et al., 2023). Furthermore, Spanish Law 19/2013 on Transparency and Good Governance requires Public Sector Organizations (PSOs), including MOEs, to disclose information about their economic and corporate governance practices (Royo et al., 2019). In accordance with institutional theory, MOEs, which are either partially or fully government-owned, face pressures to disclose ESG information due to these regulations (Carpenter & Feroz, 2001).

Among all the regions in Spain, Andalusia is particularly noteworthy due to its environmental challenges related to water (Cabello et al., 2021; Larrinaga-Gonzélez & Pérez-Chamorro, 2008). The 2023 report on the socio-economic situation of Andalusia, prepared by the Economic and Social Council of Andalusia, emphasizes the urgent need for effective ecological transition policies (Economic and Social Council of Andalusia, 2023). It recognizes that achieving sustainability is a significant challenge for the region. Additionally, Andalusia is the second most populated region in Spain and has the highest number of MOEs 2 compared to other regions.

Sample

We followed a specific procedure to obtain the sample of Andalusian MOEs. First, we visited the website of the General Intervention Board of the State Administration (IGAE) and selected the menu option, “Inventory of Entities of the Public Sector.” Next, we used the entity finder to compile a list of enterprises owned by local municipalities in Andalusia, excluding those owned by central or regional governments. As of November 2020, 307 public enterprises were under the control of various local governments in Andalusia.

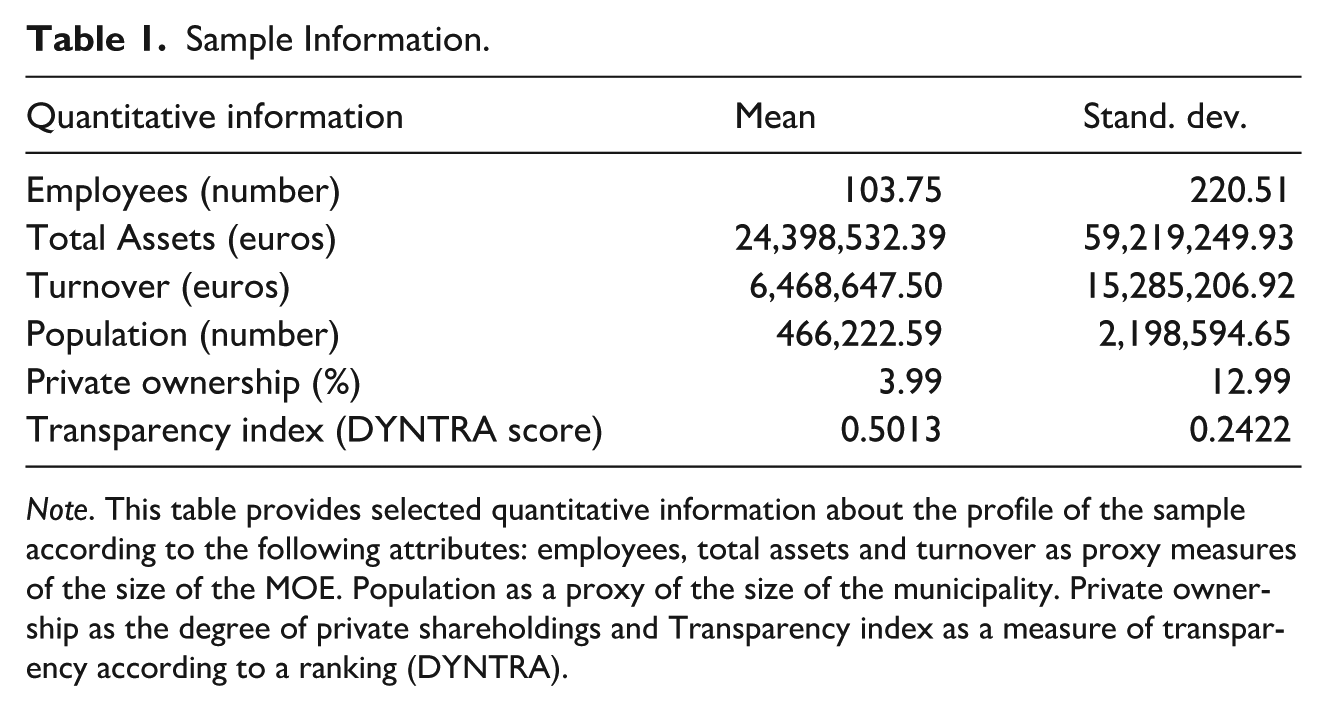

Based on the National Classification of Economic Activities (CNAE), these 307 MOEs was divided into the following industries: Agriculture, forestry and fishing (4); Manufacturing (1); Electricity, gas, steam and air conditioning supply (21); Sewerage, waste management and remediation (56); Construction (67); Wholesale and retail trade, repair of motor vehicles and motorcycles (3); Transport and storage (10); Accommodation and food service (2); Information and communications (26); Real estate (12); Professional, scientific and technical (7); Administrative and support service (21); Public administration and defense, compulsory social security (31); Education (1); Human health and social work (9); Arts, entertainment and recreation (17); Other services (7); Extraterritorial organizations and bodies (1) and others not classified (11). Table 1 shows the main characteristics of the MOEs sampled. The average values of the quantitative attributes indicate that the sample consists of medium-sized companies primarily providing services in the largest municipalities. The relatively high standard deviations indicate considerable variability in the sizes of the Andalusian MOEs and the populations of the municipalities they serve.

Sample Information.

Note. This table provides selected quantitative information about the profile of the sample according to the following attributes: employees, total assets and turnover as proxy measures of the size of the MOE. Population as a proxy of the size of the municipality. Private ownership as the degree of private shareholdings and Transparency index as a measure of transparency according to a ranking (DYNTRA).

Data Collection

This research differs from previous studies (Patten et al., 2015; Ruiz-Lozano et al., 2019) by using multiple sources to collect ESG disclosures from Andalusian MOEs. Some researchers, such as Andrades et al. (2019), have noted that relying on a single data source can be problematic when searching for disclosed ESG information, as each reporting medium serves distinct purposes and targets different audiences. To overcome this limitation, we advocate using various communication channels by combining reports and websites (de Villiers & Alexander, 2014). This strategy enables a more comprehensive capture of information available from different sources (De Klerk et al., 2015).

We utilized various reporting mediums as communication channels, such as stand-alone sustainability reports, financial statements, non-financial statements, collective agreements, statutes and codes of conduct and ethics. To gather information from these sources, we relied on three primary data sources. First, we accessed the websites of all 307 MOEs. Second, we consulted the websites of the local governments that own each MOE. Lastly, we accessed the website https://rendiciondecuentas.es, an online database where local entities provide their economic, financial and budgeting information in accordance with the Spanish Law 19/2013 on transparency and good governance. Data collection occurred from December 2020 to February 2021.

In line with previous studies, we performed a content analysis to find out the extent of ESG information disclosed by Andalusian MOEs (Argento et al., 2019; Ruiz-Lozano et al., 2019). Based on Krippendorf (1980, p. 21) content analysis “is a research technique for making replicable and valid inferences from data according to their context.” This method allows for measuring the presence or absence of specific informational disclosures (Al-Mohareb et al., 2025). Content analysis has been widely employed in social and environmental accounting research and is recognized as a valid data collection method (Gutiérrez-Ponce et al., 2021).

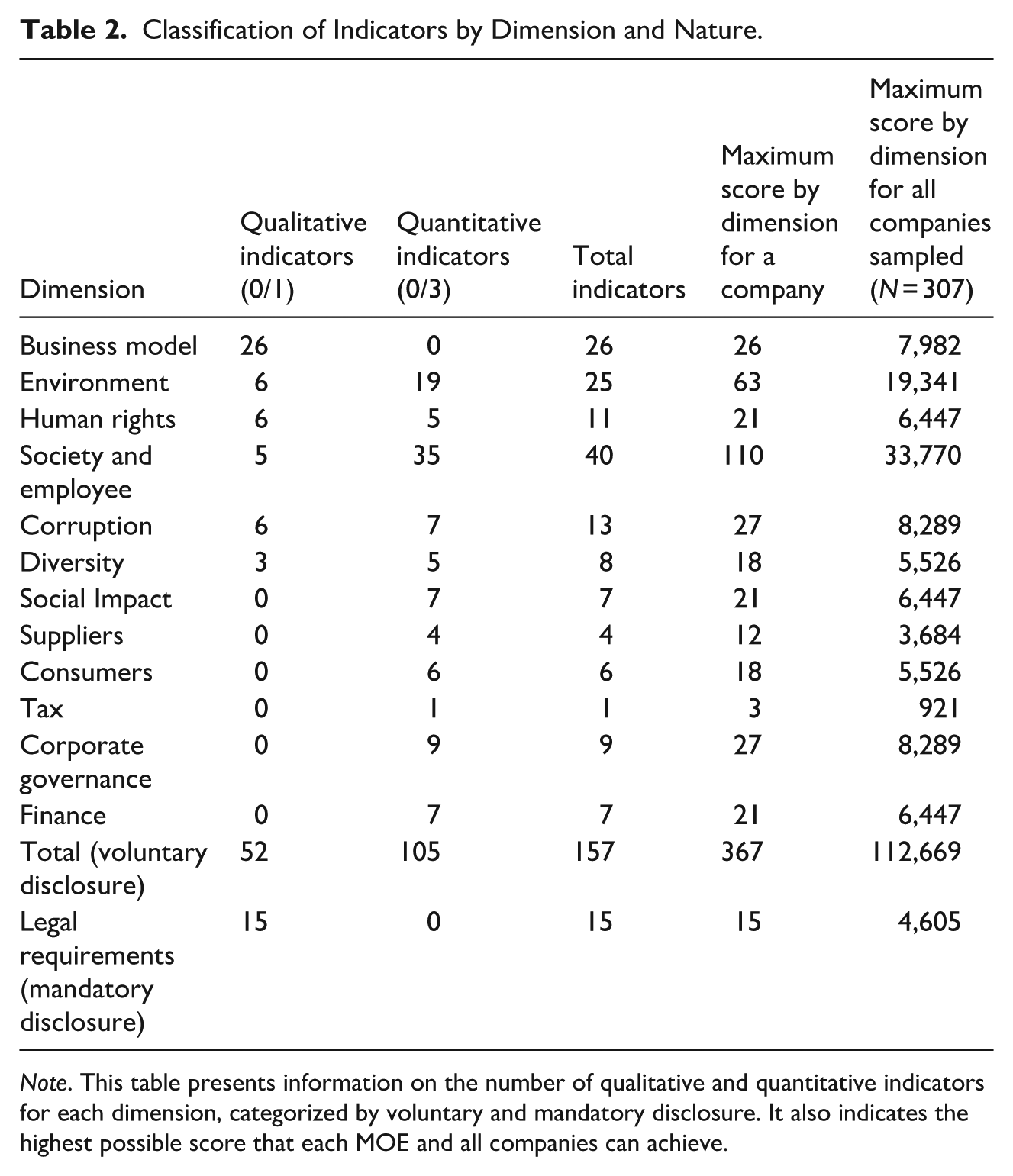

The Global Reporting Initiative (GRI) standards are generally considered the main tool for tapping the level of ESG disclosure in different types of organizations (Larrinaga & Bebbington, 2021). In our study, however, we employed a specific instrument that we created to measure the extent of ESG disclosure in MOEs. This instrument tool was developed after a thorough review of existing literature and previous guidelines. Subsequently, the items identified in this review were validated by a panel of managers working in MOEs. They evaluated the relevance and feasibility of each item. After this refinement process, we achieved a final measurement index with 172 indicators. 3 On the one hand, 157 indicators were classified as voluntary of which (52 qualitative and 105 quantitative). Qualitative indicators were used to score the presence (1) or absence (0) of narrative information, without quantifiable results. Meanwhile, quantitative indicators were employed to assess different levels of disclosure, with scores ranging from 0 to 3. A score of zero indicated that no information was disclosed about a particular item. A score of one meant that the information was only disclosed in a narrative or qualitative manner. A score of two was assigned when the disclosure of an item was quantitative. Finally, a score of three was given when, in addition to quantitative data, annual comparative data were disclosed. Conversely, the other 15 indicators were considered mandatory information elements. They were scored using a dichotomous scoring system (1 for presence and 0 for absence) to measure the degree of compliance with mandatory disclosure requirements. Table 2 categorizes the 172 indicators by dimension and highlights several key characteristics. It presents detailed information on the following aspects: the number of qualitative indicators (coded as 0–1), the number of quantitative indicators (coded as 0–3) and the total number of indicators. For each dimension, it indicates the maximum score that an MOE can achieve. Additionally, it displays the maximum score by dimension for all companies included in the sample.

Classification of Indicators by Dimension and Nature.

Note. This table presents information on the number of qualitative and quantitative indicators for each dimension, categorized by voluntary and mandatory disclosure. It also indicates the highest possible score that each MOE and all companies can achieve.

To help ensure consistency and reduce subjectivity, two researchers, working independently, collected and analyzed the data as a strategy to improve reliability in the coding process (Luque-Vílchez & Larrinaga, 2016). Each researcher coded a sample of MOEs selected adopting the same criteria. A third researcher intervened to enhance the accuracy of the coding process resulting from different interpretations of the coding information (Larrinaga et al., 2018). Once no significant differences were detected between the researchers’ assessments, content analysis was conducted on the rest of the sample. This process of data collection has been frequently employed in previous research (Ruiz-Lozano et al., 2019). Data analysis was performed from March 2021 to June 2021.

Empirical Analysis

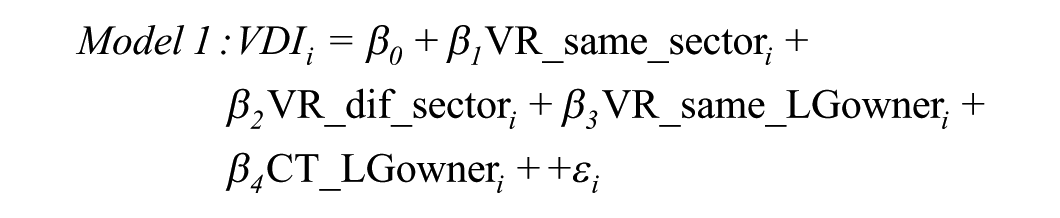

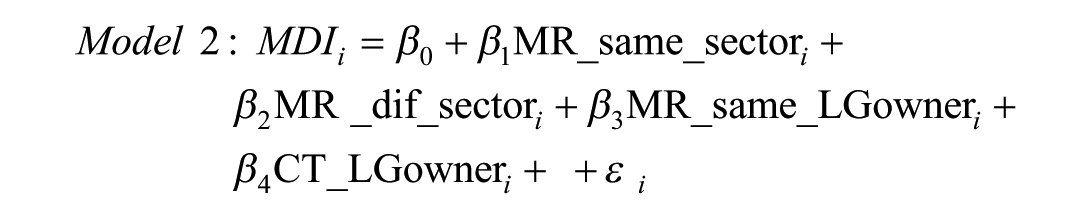

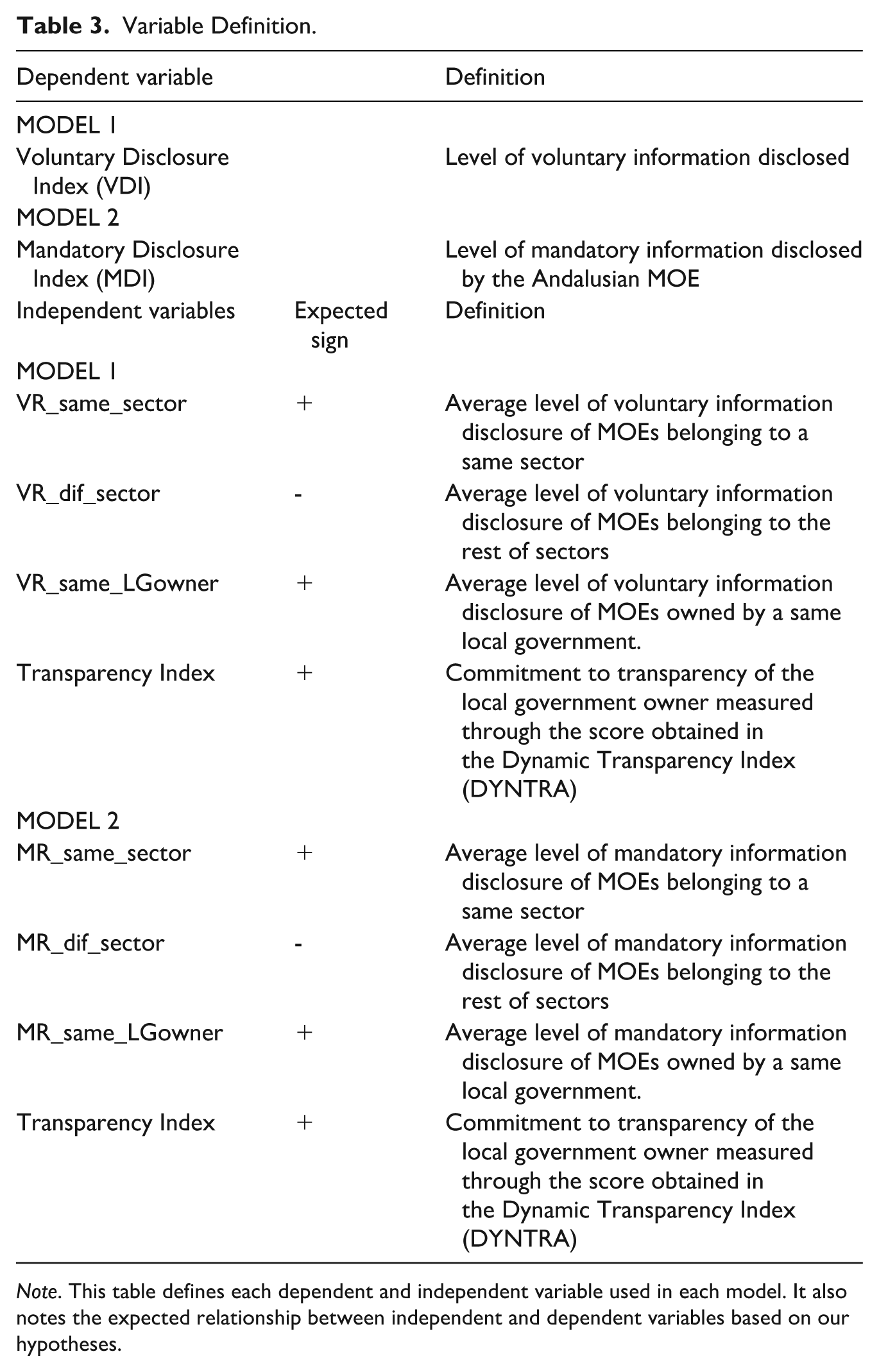

We conducted two multiple linear regressions to examine our hypotheses. The first aims to explore whether Andalusian MOEs owned by the same local government have similar ESG disclosure patterns. The second hypothesis examines whether Andalusian MOEs in the same sector have similar levels of ESG disclosure. This type of regression has been widely employed in previous research exploring the relationship between different variables (Argento et al., 2019; Ruiz-Lozano et al., 2019). Consistent with our instrument tool, we developed two models: one for voluntary ESG disclosure (Model 1) and another for mandatory ESG disclosure (Model 2).

Dependent Variables

The Voluntary Disclosure Index (VDI) used in model 1 measures the extent of voluntary disclosure of ESG information provided by each of the 307 Andalusian MOEs. To calculate the VDI, we followed the following steps: For each company, the index was created by adding the individual scores that each one received and dividing them by the maximum score that the company could achieve.

Additionally, for each dimension, the index was calculated as the company’s mean score divided by the maximum score for that dimension. The Mandatory Disclosure Index (MDI)utilized in Model 2 indicates the level and quality of mandatory ESG information disclosed by the Andalusian MOEs. This index was calculated by dividing each company’s total score by the maximum possible score (15).

Independent Variables

In Model 1, we used the following independent variables:

- VR_same_sector: The mean level of voluntary disclosure provided by companies in the same sector.

- VR_dif_sector: The mean level of voluntary disclosure of information by companies in different sectors.

- VR_same_LGowner: The mean level of voluntary disclosure provided by companies owned by the same local government.

For Model 2, we used the same independent variables but focused on the level of mandatory information disclosed.

Additionally, both models included the Transparency Index, reflecting the score each local government achieved in the Dynamic Transparency Index. Table 3 includes the description of the dependent and independent variables.

Variable Definition.

Note. This table defines each dependent and independent variable used in each model. It also notes the expected relationship between independent and dependent variables based on our hypotheses.

Analysis of Results

General Picture of the Status of ESG Disclosure in Andalusian MOEs

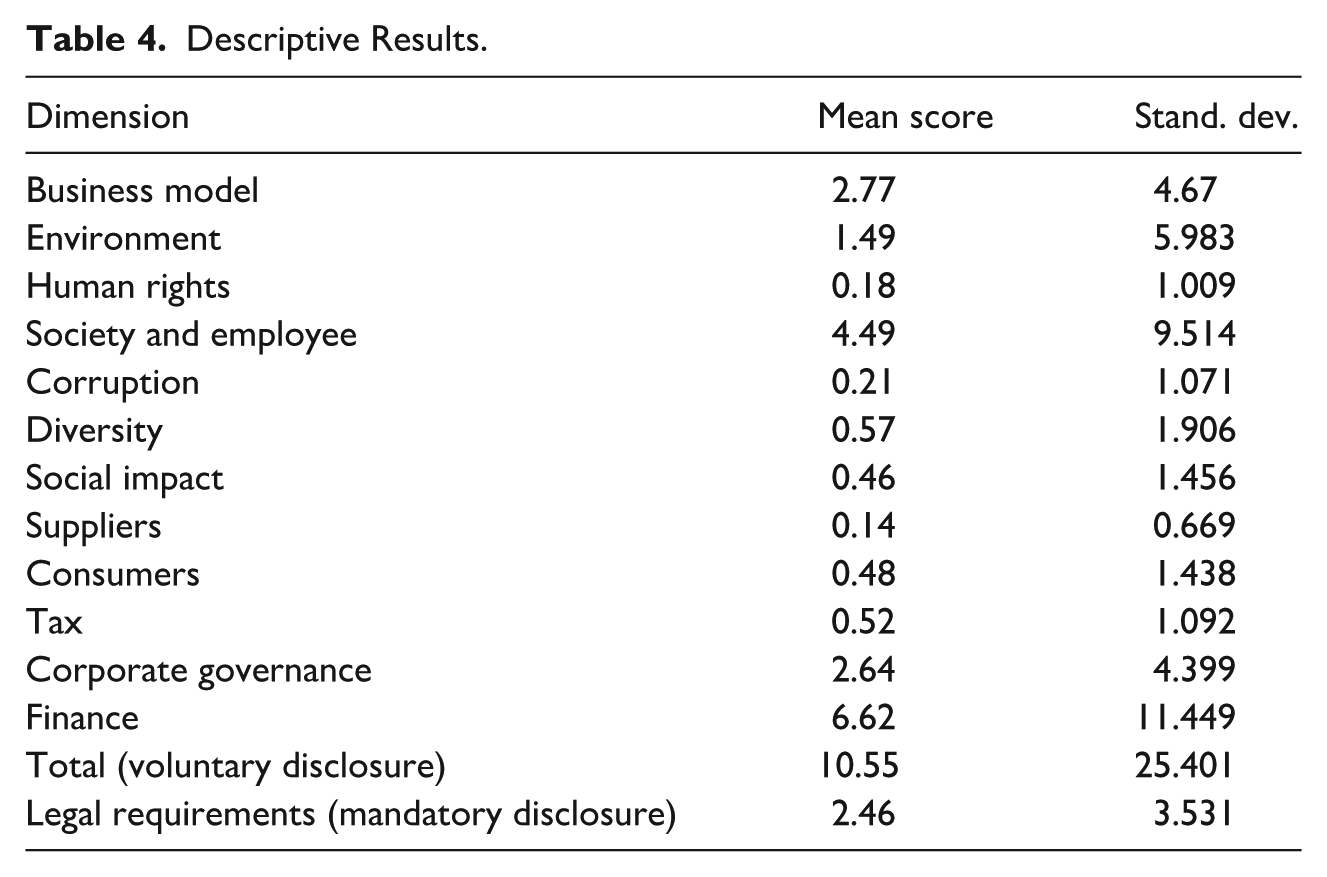

Table 4 presents the descriptive results for all Andalusian MOEs, highlighting the mean value and standard deviation for each dimension.

Descriptive Results.

The analysis of the average scores highlights a clear need for improvement in both the quality and quantity of disclosed ESG information. Comparatively, Andalusian MOEs have shown higher levels of mandatory ESG disclosure, scoring 2.46 out of 15 (16.4%), while voluntary disclosure is 10.55 out of 367 (2.87%). Overall, the standard deviation values are notably high for several dimensions, indicating considerable variability in the level of ESG disclosure among the Andalusian MOEs. This variation may stem from the diverse composition of the sample companies based on their size, as Table 1 reported.

When we break down the data by dimension, two main findings emerge. First, the sampled Andalusian MOEs have demonstrated a stronger emphasis on disclosing information related to finance, business models, taxes, and corporate governance. This type of information typically pertains to aspects such as strategic goals, stakeholders and economic issues. Most of these elements are implicitly included in Spanish Law 19/2013 on Transparency and Good Governance as aspects that must be disclosed. Second, the disclosure of voluntary ESG information among sampled Andalusian MOEs is almost non-existent, regardless of the specific dimension being examined. In particular, little information is disclosed about social impact (0.46 of 21), corruption (0.21 of 27) and society/employee (4.49 of 110). The low level of voluntary ESG disclosure for these elements is surprising, considering that MOEs as providers of public services are responsible for promoting the common good. Furthermore, as publicly funded entities, they arguably should be exemplary in their commitment to disclosing information related to corruption.

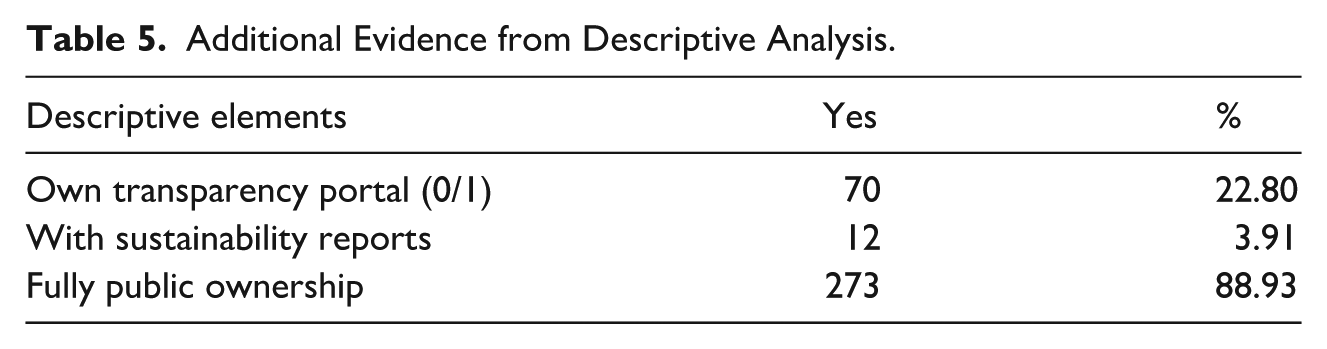

Table 5 highlights the lack of commitment among Andalusian MOEs to disclose ESG information: only a limited number of companies have a transparency portal and publish sustainability reports in accordance with the GRI guidelines. Specifically, fewers than 23% of the 307 Andalusian MOEs have established their own transparency portals, which are required to disclose information mandated by Spanish Law 19/2013 on Transparency and Good Governance. Furthermore, only 12 of the 307 Andalusian MOEs (3.91%) have published sustainability reports.

Additional Evidence from Descriptive Analysis.

Statistical Analysis: Influence of Sources of Institutional Isomorphism Concerning ESG Disclosure

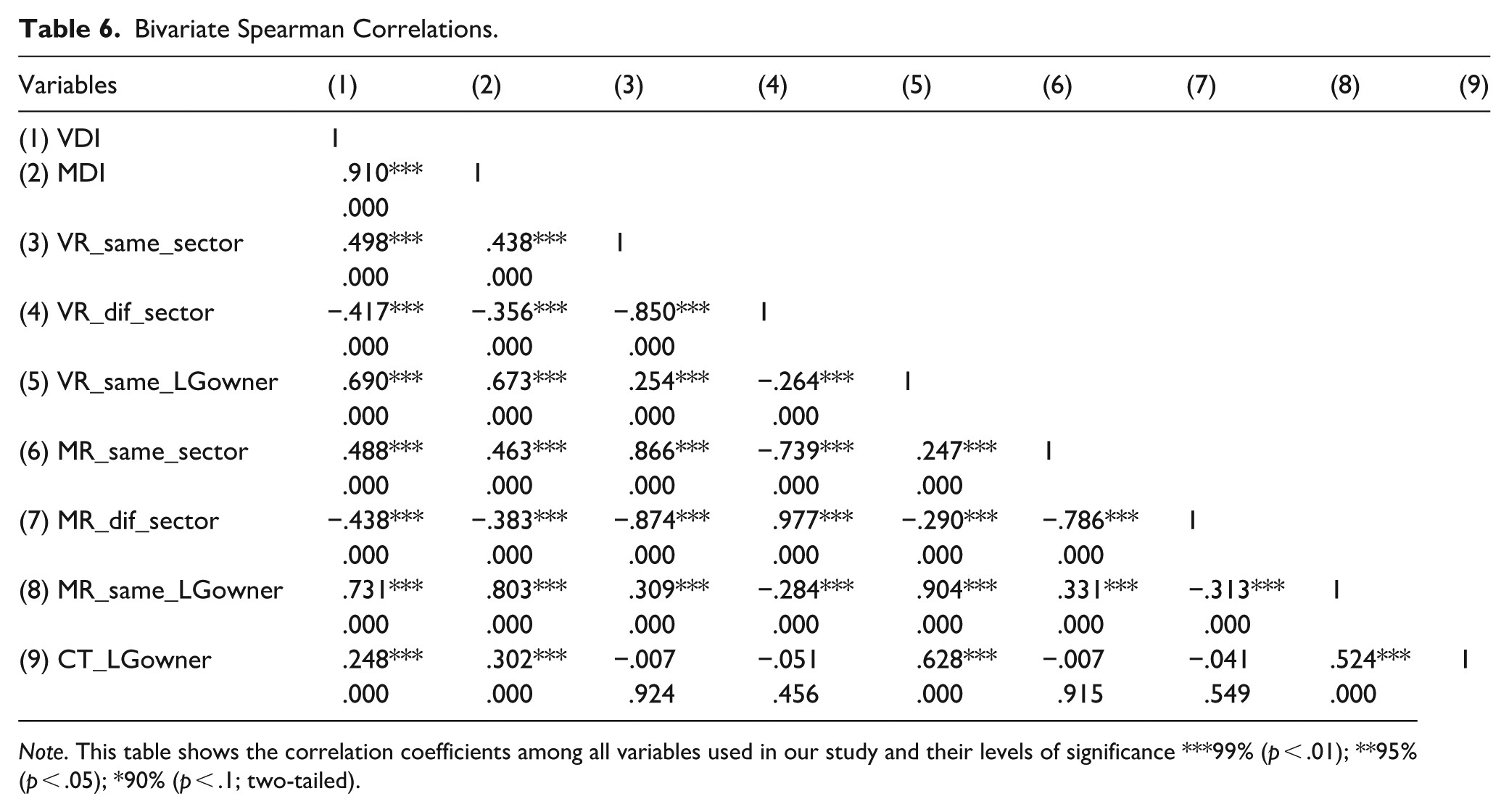

We performed a data normality test to verify that the sample was not based on a normal distribution. Then we employed the Spearman’s analysis of associations to evaluate the relationship between the dependent variables in the models. Table 6 shows that there is a positive and statistically significant association between voluntary and mandatory disclosure indexes (VDI and MDI): the higher the mandatory ESG disclosure is, the higher voluntary ESG disclosure. This analysis also revealed that, except for the ESG information MOEs in different sectors disclosed, all of the variables are significantly and positively associated with the ESG information disclosed, both on a voluntary and mandatory way basis. That is, regardless of the information provided, the level of ESG information an MOE disclosed aligns with the average levels of information disclosed by other MOEs in the same sector and by MOEs owned by the same parent institution.

Bivariate Spearman Correlations.

Note. This table shows the correlation coefficients among all variables used in our study and their levels of significance ***99% (p < .01); **95% (p < .05); *90% (p < .1; two-tailed).

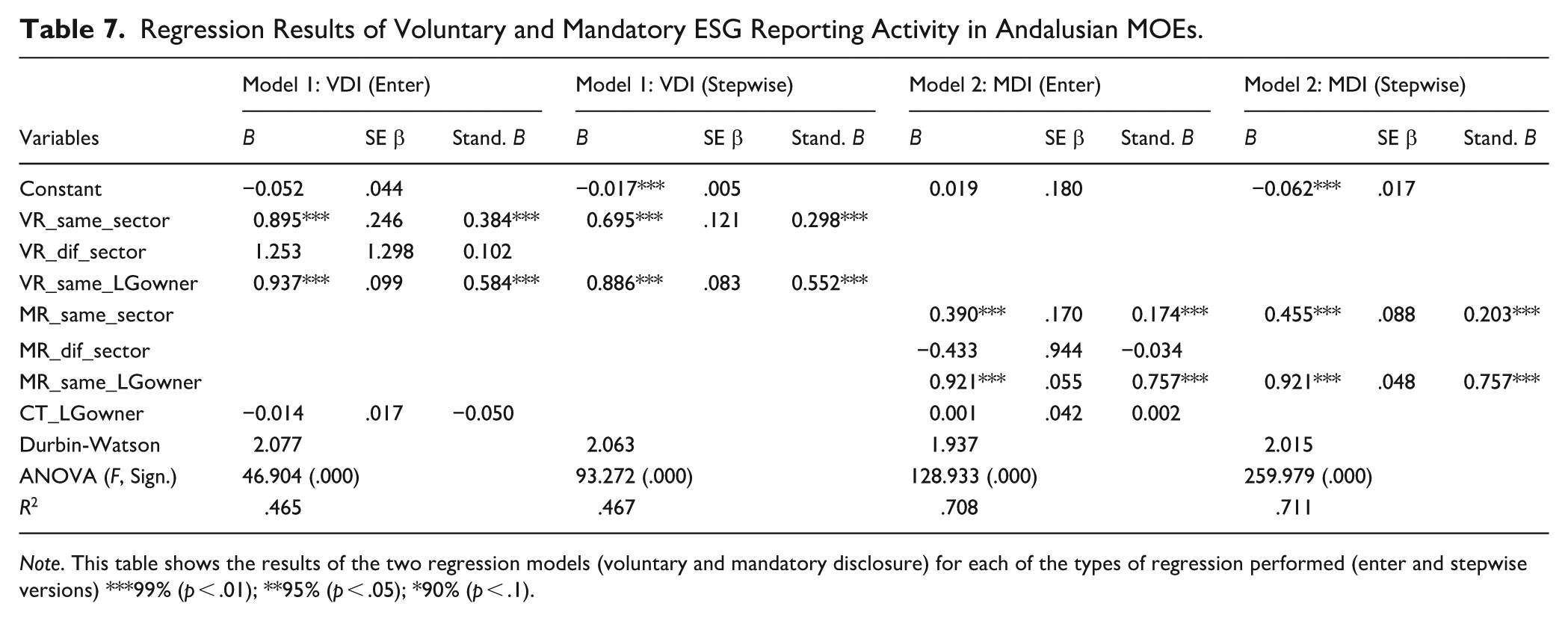

Table 7 shows the results of the multiple linear regression models. According to the F test, the two models that were initially run using the enter approach were statistically significant. However, the analysis of variance inflation factors obtained for each of the explanatory variables detected a multicollinearity problem between VR_same_sector and VR_dif_sector on the one hand, and between MR_same_sector and MR_dif_sector on the other. Accordingly, we performed stepwise linear regression for each index. This kind of regression model guarantees that each step adds new explanatory variables to the model.

Regression Results of Voluntary and Mandatory ESG Reporting Activity in Andalusian MOEs.

Note. This table shows the results of the two regression models (voluntary and mandatory disclosure) for each of the types of regression performed (enter and stepwise versions) ***99% (p < .01); **95% (p < .05); *90% (p < .1).

According to the R2 analysis, the set of independent variables more fully explains the variation in the mandatory disclosure index than than in the voluntary disclosure index (71.1% versus 46.7%). Only two of the four independent variables initially considered as potential explanatory factors in each model have statistically significant relationships with the levels of voluntary and mandatory ESG information disclosed by MOEs: VR_same_sector and VR_same_LGowner in Model 1 and MR_same_sector and MR_same_LGowner in Model 2. In particular, in the two models, the variable that better explains the level of MOE disclosure is the information disclosed by other MOEs owned by the same parent institution and by the same local government. These findings are consistent with our initial expectations. Thus, Hypotheses 1 and 2 cannot be rejected.

Follow-Up Analysis: Alternative Explanations for Higher Voluntary and Mandatory Disclosure

To gain a better understanding, we conducted a detailed analysis to identify common behaviour patterns among the Andalusian MOEs that show higher levels of voluntary and mandatory ESG disclosure.

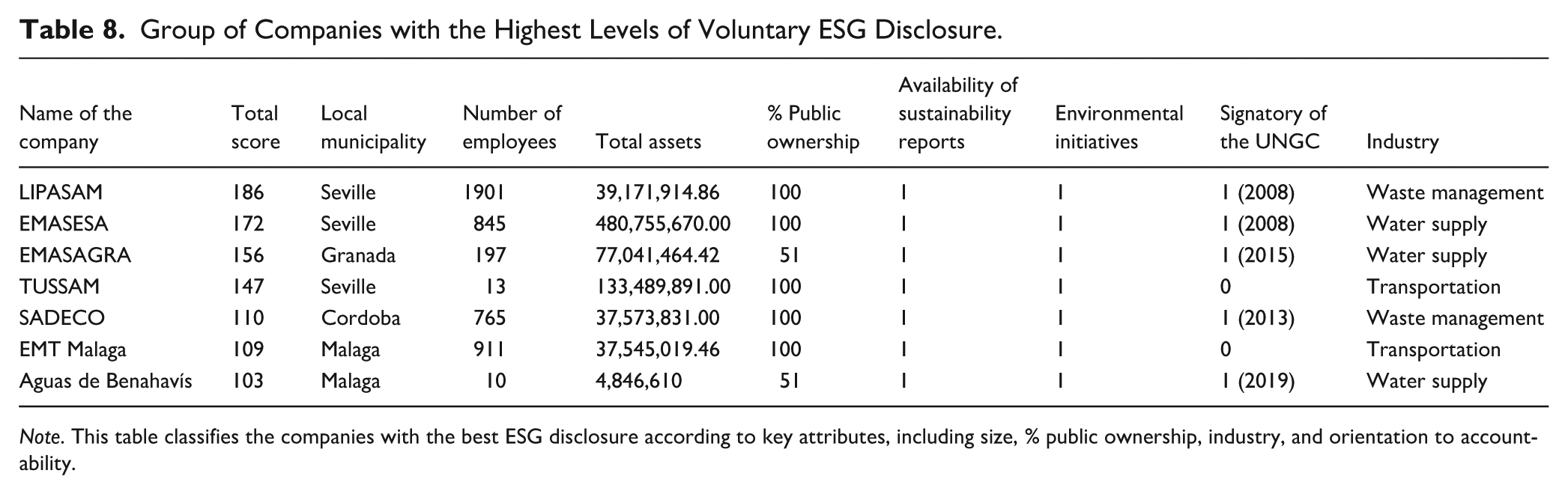

Companies were selected based on having average total scores exceeding 100. This threshold indicates a voluntary disclosure level higher than 27%. Of the 307 companies analyzed, only seven met this criterion. Table 8 presents the profiles of these seven best-performing MOEs in terms of their ESG disclosure levels. It also includes information about several attributes of each MOE: the number of employees, total assets, extent of public ownership, availability of sustainability reports, signatory status of the United Nations Global Compact (UNGC) and implementation of environmental initiatives.

Group of Companies with the Highest Levels of Voluntary ESG Disclosure.

Note. This table classifies the companies with the best ESG disclosure according to key attributes, including size, % public ownership, industry, and orientation to accountability.

The seven companies show similar patterns across these different attributes. Six of the seven companies (excluding Aguas de Benahavis) have more employees and total assets than the average for the 307 companies included in the analysis. These companies operate in environmentally sensitive industries such as waste management (LIPASAM and SADECO), water supply (EMASESA, EMASAGRA and Aguas de Benahavis), and transportation (TUSSAM and EMT Málaga). From a reporting perspective, these seven Andalusian MOEs publish annual sustainability reports in accordance with GRI standards to measure and disclose their social and environmental impacts. Notably, EMASAGRA and EMASESA have been publishing such reports for over 10 years. Additionally, all of the companies have implemented and certified an environmental management system based on the ISO 14001 standard. This certification may have served as a framework for these companies in coding and monitoring ESG indicators. Furthermore, five of the seven companies have demonstrated their commitment to sustainability by signing the UNGC and adhering to its ten principles related to sustainability. For instance, LIPASAM and EMASESA became signatories to the UNGC principles in 2008; since then, they have published an annual communication on progress outlining their efforts to address social and environmental issues.

The seven companies are owned by four different local municipalities: three by the Seville City Council, two by the Malaga City Council, one by the Cordoba City Council, and one by the Granada City Council. These cities are the largest municipalities in Andalusia. Out of the seven companies, five are fully owned by their respective local governments, while two have a mix of public and private shareholders.

It appears, then, that the reason for these seven Andalusian MOEs to have the highest level of voluntary ESG disclosure is rooted in their shared cultural and socio-political context. This context evidently shapes how they address social and environmental issues. Their similar behavioral patterns reflect factors such as their size, cultural tradition of sustainability accountability, operations in environmentally sensitive industries, and ownership primarily by large local municipalities.

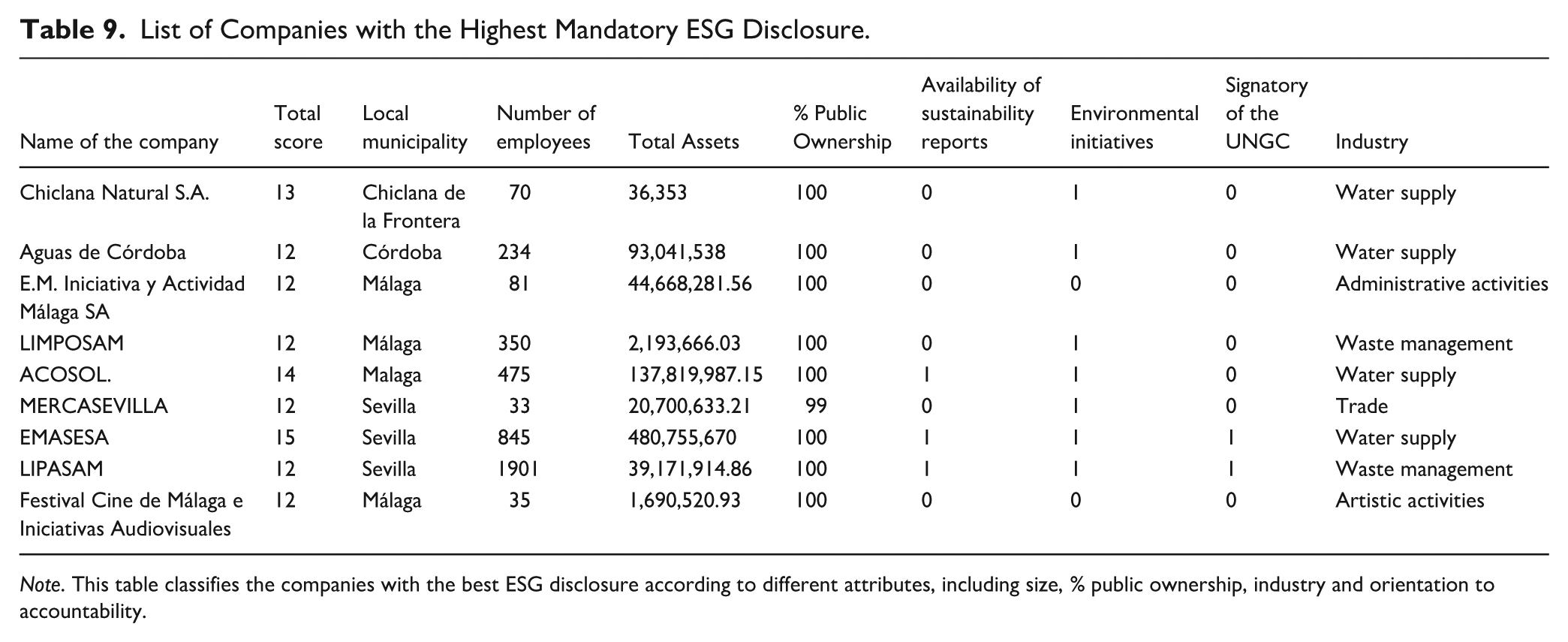

Table 9 lists the nine Andalusian MOEs that have disclosed more than 80% of the 15 mandatory disclosure indicators. We chose this criterion because these indicators tap essential information that companies are required to provide. Among the nine companies, five have more employees and total assets exceeding the average of the 307 companies studied. This suggests that there is not a consistent pattern of mandatory disclosure behavior among the companies based on their size. Out of the nine, only three publish sustainability reports, and two are signatories of the UNGC. Unlike the best performers in voluntary ESG disclosure, the nine companies with the highest levels of mandatory disclosure do not appear to share a common industry or cultural background regarding sustainability accountability. It seems that this group of companies is united by their complete ownership by a local municipality.

List of Companies with the Highest Mandatory ESG Disclosure.

Note. This table classifies the companies with the best ESG disclosure according to different attributes, including size, % public ownership, industry and orientation to accountability.

In sum, this additional analysis suggests that ESG disclosure patterns among Andalusian MOEs depends in part on the voluntary or mandatory nature of the information.

Discussion and Conclusion

Among this article’s contributions is its focus on a particular type of organization, the MOE. This organization faces distinctive governance challenges and accountability pressures than do private enterprises or purely public sector organizations (Grossi et al., 2015; Yetano & Sorrentino, 2023). This highlights the necessity of studying MOEs and their behavior in ESG disclosure.

Descriptively, we have observed a limited level of ESG disclosure among the Andalusian MOEs. These findings are striking, given that these enterprises are expected to have higher accountability than those in the private sector (Giacomini et al., 2020; Greiling & Grüb, 2014). They should play a vital role in advancing a sustainable agenda, as they provide essential public services to local communities (Dicorato et al., 2020; Valenza & Damiano, 2023). Their patterns of behavior regarding ESG disclosure, however, do not reflect this implicit commitment to meeting societal demands and needs.

The low level of ESG disclosure among Andalusian MOEs might be attributed to the absence of a standardized and widely accepted measure for reporting on ESG issues (Andrades & Larran, 2019), insufficient pressure from external stakeholders (Manes-Rossi et al., 2021), and the lack of enforcement mechanisms in existing regulations (Marquis & Qian, 2014). Furthermore, as other scholars suggest, the hybrid nature of MOEs may help explain why these organizations tend to have lower levels of ESG disclosure (Argento et al., 2019). Their structural complexity requires them to balance the demands and needs of various stakeholders (Grossi et al., 2015). This situation creates “tensions between the institutional logics represented, each of them with a different performance expectation, creating a space for multiple accountability channels” (Yetano & Sorrentino, 2023, p. 300). Consequently, disclosing ESG information for these companies can be challenging, as it is often unclear who is accountable to whom and for what (Andrades & Larran, 2019).

Our statistical findings suggest that our initial expectation has been confirmed. We have found that ESG disclosure among Andalusian MOEs tends to follow similar patterns within two groups of organizations that share common characteristics. These groups of MOEs are categorized into two fields according to their local government ownership and the industry in which they operate.

Relying on institutional theory, isomorphism is manifested in MOEs owned by the same local government by the interconnected influence exerted by the three sources of institutional pressure.

From a coercive perspective, there is a connection to resource dependence (Carpenter & Feroz, 2001). As stated by Collin et al. (2009, p. 151), “organizations can put pressure on the focal organization to behave and to structure itself in a certain way; otherwise the focal organization will not gain the needed resources or will suffer from sanctions.” Following this logic, Andalusian MOEs that are owned by the same local entity are compelled to conform to these pressures. They have a resource-based incentive to show that their actions meet the expectations of their owner to maintain legitimacy (Andrades et al., 2023). Indeed, the negative consequences of non-conformity can be significant from a resource dependency perspective (Haraldsson & Tagesson, 2014). Therefore, the relationship with the local government may explain why MOEs owned by the same municipality tend to disclose similar levels of ESG information.

Based on normative sources of institutional pressure, accountants within local governments can influence professionals working in an MOE to adopt their practices (Collin et al., 2009). They achieve this by establishing non-imposed norms that encourage the adoption of desired behaviors (Haraldsson & Tagesson, 2014). As a result, professionals in MOEs may feel compelled to conform to these pressures by adhering to the established norms of the accounting profession, thereby demonstrating their professional status (Donatella, 2020). The presence of accounting networks and professional associations within a given region may explain why ESG disclosures tend to be similar among Andalusian MOEs located in the same geographical area.

The combination of coercive and normative forces drives MOEs owned by the same local government to exhibit similar levels of disclosure. According to mimetic sources of institutional theory, this tendency arises because organizations within the same environment are attuned to the actions of their peers and often strive to appear legitimate (Collin et al., 2009; Donatella, 2020).

Meanwhile, consistent with our theoretical framework, we find the following explanations for the institutional isomorphism among MOEs from the same sector.

Companies operating in environmentally sensitive industries face stricter regulatory requirements and heightened demands for transparency from stakeholders, such as consumers and environmental activists (Ligorio et al., 2022; Nicolo et al., 2021). This situation may explain why Andalusian MOEs in industries with significant environmental impacts have demonstrated higher levels of ESG disclosure. The pressure from coercive forces can enhance their social legitimacy, making compliance particularly important for these organizations (Collin et al., 2009).

Companies in high-risk industries are subject to experience obligations from their peers, as professional and industrial associations establish specific rules and standards related to social and environmental issues (Young & Marais, 2012). As a result, ESG disclosure may arise from a greater awareness of social and environmental responsibility (Bebbington et al., 2009). As a result, these companies face increased societal pressure to provide ESG disclosures to maintain their legitimacy (Dienes et al., 2016). In the particular case of MOEs, these enterprises hold an implicit moral obligation to society given that they contribute to the public good by offering services of general interest that benefit the local community (Dicorato et al., 2020; Giacomini et al., 2020). Accordingly, MOEs operating in environmentally sensitive industries can showcase their societal contributions by engaging in ESG disclosure, as it aligns with their social purpose (Greiling & Grüb, 2014; Valenza & Damiano, 2023).

The combined effect of coercive and normative forces evidently leads firms in the same industry, such as Andalusian MOEs, to adopt similar levels of ESG disclosure (Young & Marais, 2012). According to the mimetic source of institutional isomorphism, companies that belong to the same industry “are likely to constitute an organizational field from which emanate strong conformity pressures” (Aerts et al., 2006, p. 299). Thus, their ESG disclosures are likely to be similar (Ligorio et al., 2022). Therefore, our research indicates that Andalusian MOEs within the same sector and governed by the same local government tend to exhibit similar disclosure patterns.

Our follow-up analysis has helped us identify alternative explanations for the behavior of the top performers in terms of the type of disclosure: voluntary and mandatory ESG disclosure. Two common factors among companies with the highest levels of both voluntary and mandatory ESG disclosure are that they are owned by the same local government and operate within environmentally sensitive industries. Yet, though we recognize that Andalusian MOEs that demonstrate better levels of voluntary ESG disclosure possess a cultural commitment to accountability for sustainability, this pattern is not observed among the best performers in mandatory ESG disclosure.

From a theoretical perspective, the behavior of companies with higher levels of voluntary ESG disclosure appears to be influenced more by normative rather than coercive forces. Indeed, Andalusian MOEs with the highest levels of ESG disclosure have a tradition of publishing sustainability reports that follow the GRI framework, and they also have also adhered to the principles of the UNGC. According to institutional theory, adopting internationally accepted reporting frameworks, such as the GRI, can be interpreted as a sign of normative isomorphism (de Villiers et al., 2014; Montecalvo et al., 2018). The GRI reporting framework has established itself as the accepted standard in the voluntary adoption of sustainability reporting (Larrinaga & Bebbington, 2021). Similarly, another indication of normative isomorphism arises from becoming a signatory of the UNGC, which is often a result of normative pressures that “spread through professionalization, formal education, and professional networks” (Higgins & Larrinaga, 2014, pp. 277–278).

The primary behaviour exhibited by MOEs with the highest levels of mandatory disclosure is that they are fully owned by local municipalities. From a coercive perspective, these companies are compelled to comply with the mandatory disclosure requirements outlined in Spanish Law 19/2013 on Transparency and Good Governance. Since they are completely funded by public resources provided by the local government, the behaviour of these MOEs is driven by meeting the demands of their main provider of resources (Andrades et al., 2023; Yetano & Sorrentino, 2023).

Based on our theoretical framework, these findings suggest that ESG disclosure is confined to certain fields rather than spreading as a taken-for-granted activity across the business community, as noted by Higgins et al. (2018).

Our findings have practical implications for managers in MOE settings. Unlike private sector businesses, MOEs have a social responsibility that is deeply rooted in the public value of the services they offer to communities (Argento et al., 2019). This implies that they have a moral obligation to society, which can influence the adoption of practices that are widely accepted and valued within the community (Giacomini et al., 2020; Valenza & Damiano, 2023). Accordingly, MOEs might use ESG disclosure to demonstrate how they contribute to a more sustainable society (Dicorato et al., 2020; Garde et al., 2017). To achieve this, we recommend that managers of MOEs receive training in the skills necessary to measure and disclose their social and environmental impacts. At this stage, experts from professional organizations, along with consultants and academics, can provide valuable expertise and knowledge to help these managers address this issue effectively.

Our study has important theoretical implications for future research on ESG disclosure from the perspective of institutional theory. We apply a traditional view of institutional theory, focusing on the concept of isomorphism to explore how practices like ESG disclosure become institutionalized within specific organizational fields. Previous empirical research has primarily employed institutional theory to investigate how coercive, normative, and mimetic forces contribute to convergence and uniformity in ESG disclosure patterns (Bebbington et al., 2009; de Villiers et al., 2014). Yet, some institutionalist researchers, such as Scott (2014), have suggested incorporating other perspectives within institutional theory. This body of research underscores the need for additional perspectives on institutional change and the intricate socio-political dynamics underlying these processes (Eitrem et al., 2024). Building on the theory of structuration, Scott (2014) proposes shifting attention from the study of institutional structures to the exploration of processes. This perspective, rooted in a structuralist approach to institutional theory, has led some scholars to investigate the dynamic processes that explain how and why ESG disclosure evolves (Larrinaga & Bebbington, 2021; Luque-Vilchez et al., 2024). Thus, future research could employ a structuralist approach to institutional theory by incorporating institutional logics or the concept of normativity to investigate the processes and dynamics involved in ESG disclosure practices.

Like other studies, ours has limitations. The sample focuses on the Andalusian MOEs. Future research could be expanded to include all of Spain to compare MOEs across diverse regions based on socioeconomic factors such as population size, GDP contribution, and regional government ideology. The article is exploratory, and it could benefit from qualitative methods such as by interviewing MOE managers to better understand the motivations and barriers associated with the disclosure of ESG information. Furthermore, a future version of the study might include longitudinal analysis to explore how ESG disclosure has evolved and the influence of differing institutional pressures. This aspect is especially relevant in the current socio-political context, where new regulatory changes are shaping the ESG disclosure practices of Spanish companies, including MOEs.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This article is a part of a research project funded by the FEDER Operational Program Andalusia 2014-2020 (Research Project FEDER-UCA18-107740).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzedduring the current study.