Abstract

This study conducted a systematic literature review of 15 articles on local government reporting on sustainable development goals (SDG), published in Scopus-indexed journals between 2015 and 2025. The findings reveal that research on this topic is relatively limited, with most papers appearing since 2023. Research is predominantly grounded in institutional and legitimacy theory. Empirical studies focusing on Southern European countries dominate the literature. The studies report low levels of SDG reporting and inconsistent findings relating to its drivers. The analysis highlights the need for scholarship into the integration of SDGs in municipal reporting practices, offering guidance to researchers, regulators, and policymakers to enhance SDG reporting.

Keywords

Introduction

The year 2015 marked the biggest global challenge to achieving a sustainable planet. The United Nations defined 17 objectives, known as the Sustainable Development Goals (SDGs), to be achieved by 2030, collectively forming the 2030 Agenda (United Nations General Assembly, 2015). With less than five years to accomplish these goals and bearing in mind that factors such as the crisis caused by the COVID-19 pandemic have hindered progress in their achievement (Martínez-Córdoba et al., 2021), much work remains to be done.

This global commitment affects all institutions, both public and private, which must work towards achieving a more sustainable world (Martínez-Córdoba et al., 2020; Rieiro-García et al., 2023a). National governments are responsible for formulating policies and programmes that adapt the 2030 Agenda to the specific needs and conditions of each country. In this context, public agencies and public administration fulfil a dual role: firstly, as promoters of public policies that foster sustainable practices among citizens, businesses, and other economic actors (Ball et al., 2007; Navarro et al., 2010) and secondly, as role models for these actors by adopting sustainable practices and integrating them into their management models (Škare & Golja, 2014).

The proximity of local governments to all stakeholders makes them one of the most influential agents in the achievement of the SDGs (Martínez-Córdoba et al., 2021). This proximity enables them to engage with companies, the general population, and other entities to implement sustainable initiatives (Cohen et al., 2023; Masuda et al., 2021). In addition, local governments have a responsibility to communicate actions related to the SDGs to demonstrate their commitment to sustainability, a challenge for the public sector (Nicolò et al., 2023).

Much of the literature on SDGs is dominated by the private sector, with little attention given to local governments (Guarini et al., 2022; Guerrero-Gómez et al., 2021; Martínez-Córdoba et al., 2021). Some authors (Cohen et al., 2023; Guerrero-Gómez et al., 2021; Nicolò et al., 2023) claim that the literature on reporting of SDG-related information by the public sector is still in its early stages, although an increasing number of papers on this topic are being published. Nevertheless, given the pivotal role of local governments in achieving the SDGs, it is important to understand the current state of research into how local governments report information related to the 2030 Agenda and the SDGs (Erin & Bamigboye, 2021; Nicolò et al., 2023).

The aim of this study is to analyse the state of the art in research on this topic. To this end, we conducted a systematic literature review examining all publications indexed on the Scopus database related to the disclosure of the SDG-related information by local governments, from 2015 to 2025. We analysed the temporal evolution of publications, the number of publications per journal and year, the number of publications per country, the number of publications per author, the most used theories and methodologies and the most investigated SDGs.

This study identifies publication trends (e.g., key journals, the most cited papers and the most relevant authors) and the knowledge structure (e.g., theoretical frameworks, methodologies or SDGs analysed) in research on SDG reporting by local governments. Through a systematic review of existing research on this topic, it provides an overview of the current literature, highlighting key characteristics, research designs, and gaps; thereby offering valuable insights for future studies

Following this introduction, the next section provides context on the SDGs and outlines the role that local governments can play in achieving them. The following section details the research methodology, before attention turns the key findings. We with an examination of our, main conclusions, highlighting its implications and outlining s the study’s limitations and potential directions for future research.

Background

Sustainable Development Goals

Since the concept of sustainability in the context of economic development was first introduced in the Brundtland Report in 1987, countries and economic actors have taken a series of actions and made significant commitments to achieve full sustainability for the planet (De Iorio et al., 2022). At the beginning of the 21st century, the United Nations General Assembly adopted the Millennium Declaration introducing the Millennium Development Goals (MDGs). These goals comprised a series of commitments that countries were expected to adopt and fulfil by 2015 (Bowen et al., 2017; Cohen et al., 2023; Martínez-Córdoba et al., 2021).

By the end of this period, however, much work remained to be done. Nevertheless, the experience gained throughout this process led to the most significant milestone in sustainability to date: the adoption of the 2030 Agenda for Sustainable Development by the 193 member countries of the United Nations in 2015. Titled “Transforming our World: Agenda 2030 for Sustainable Development,” this document sets out 17 goals and 169 targets to be achieved by the year 2030, with three core commitments: caring for the planet, eradicating poverty, and ensuring population prosperity (United Nations General Assembly, 2015). These goals represent the most significant declaration for achieving global sustainability (United Nations General Assembly, 2015; Verboven & Vanherck, 2016) and bring together the three key dimensions (economic, social and environmental) that encompass the concept of sustainable development (Guerrero-Gómez et al., 2021).

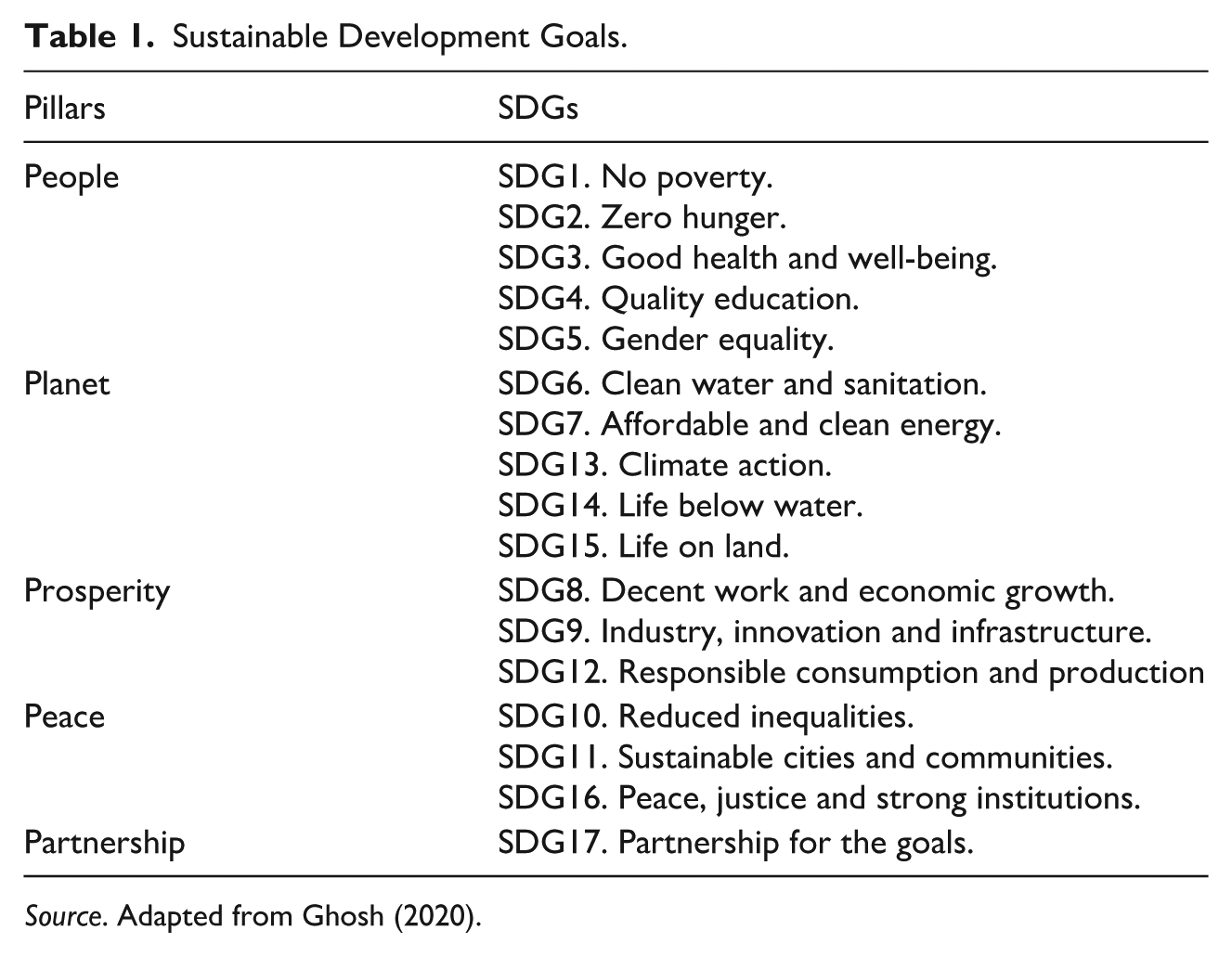

The SDGs can be classified in various ways, with the most common being the division into five pillars, known as the “5Ps,” which expand the Triple Bottom Line classification: people, planet, profit/prosperity, peace, and partnership. This classification covers a wide range of actions and encompasses all economic agents at all levels, leaving no one behind. This classification is closely linked to the ESG dimensions: environment (planet), society (people), and governance (peace and partnership), as well as to the economy (prosperity; García-Peña et al., 2021).

The first pillar (People) focuses on achieving well-being for the entire population by eradicating poverty and reducing inequalities and social exclusion. The second pillar (Planet) aims to protect and care for the environment and marine ecosystems, as well as their biodiversity. This involves addressing issues such as climate change and creating sustainable consumption and production patterns. The third pillar (Prosperity) focuses on promoting inclusive, sustainable, and equitable economic growth and development. This involves promoting sustainable production, supporting entrepreneurship and innovation, and ensuring access to financial services and growth opportunities. The fourth pillar (Peace) aims to achieve peace by reducing conflict, violence, and terrorism, and by ensuring the rule of law. Finally, the fifth pillar (Partnership) fosters collaboration and relations between different economic agents to fulfil commitments (Correa-Mejía et al., 2024; Ghosh, 2020; Rieiro-García, Amor-Esteban, & Aibar-Guzmán, 2023). Table 1 depicts the classification of the 17 Sustainable Development Goals (SDGs) according to the five pillars of the 2030 Agenda.

Sustainable Development Goals.

Source. Adapted from Ghosh (2020).

Local Governments and SDGs

The achievement of sustainable development is the responsibility of all public and private actors within the global economy (Guillamón et al., 2025; Mol et al., 2025). Consequently, achieving the SDGs involves a wide range of entities, with governments playing a fundamental role (Martínez-Córdoba et al., 2020; Rieiro-García et al., 2023b). These entities have two key functions: firstly, they must implement policies that align with the concept of sustainable development (e.g., policies related to the environment and health); and secondly, they must serve as examples and models for other economic agents to follow (Rieiro-García, Amor-Esteban, & Aibar-Guzmán, 2023).

Although all governmental entities must be aligned with the SDGs, particular attention must be given to local governments (Benito, Guillamón, & Ríos, 2025; Benito, Guillamón, Ríos, & Cifuentes-Faura, 2025). The 2030 Agenda recognises the pivotal role of regional and local governments in both the implementation and achievement of the SDGs. A key difference from the MDGs is the broader inclusion of implementation actors, which presents a significant challenge for the organisations involved (García-Peña et al., 2021; Koch & Krellenberg, 2018). The 2030 Agenda emphasises the importance of multi-level government collaboration in integrating the SDGs into public policies and budgeting processes (Guarini et al., 2021).

Local governments are responsible for managing public services that are directly linked to the SDGs, including water and transportation services, among others (Martínez-Córdoba et al., 2020; Masuda et al., 2021). Therefore, the way in which they design and implement policies will directly influence the fulfilment of the 2030 Agenda (Joseph et al., 2019). Their proximity to citizens and other stakeholders also gives local governments a strong understanding of public preferences, making them well-placed to promote the importance of collaborating to fulfil the 2030 Agenda (Cohen et al., 2023; Masuda et al., 2021; Nicolò et al., 2023; Raffer et al., 2022; Rieiro-García et al., 2023b).

It is clear that “local governments are policymakers in the best position to link SDGs with local communities and drive bottom-up global change” (Nicolò et al., 2023, p. 1491). Furthermore, the Organisation for Economic Co-operation and Development (OECD) recognises the substantial contribution of local governments to achieving the SDGs, emphasising that their involvement, alongside regional governments, is crucial for attaining most SDGs. Specifically, 105 of the 169 targets defined in the 2030 Agenda require the participation and involvement of these entities (OECD, 2020). For example, SDG 11, which aims to “make cities and human settlements inclusive, safe, resilient, and sustainable,” is clearly aimed at local governments (Cohen et al., 2023; Martínez-Córdoba et al., 2021).

SDG Reporting

The crucial role of public entities in achieving the SDGs must be explicitly reflected incommunication of all actions taken in support of the 2030 Agenda (Cohen et al., 2023). Governments must inform their various stakeholders of the actions they have taken in relation to the SDGs and the outcomes they have achieved (Rieiro-García, Amor-Esteban, & Aibar-Guzmán, 2023; Tavares & da Cruz, 2020). This will strengthen the connection with stakeholders and demonstrate governmental responsibility for and commitment to sustainable development (Nicolò et al., 2023; Nicolò et al., 2024; Niemann & Hoppe., 2018; Rieiro-García et al., 2023a). In this sense, transparency is also a key objective in achieving sustainability (Guerrero-Gómez et al., 2021).

While the private sector has much more stringent regulations for publication of sustainability information, SDG reporting by public sector actors varies by country, with some countries having mandatory legislation and others having none (Gacutan et al., 2023; Nicolò et al., 2024). Germany, for instance, is one of the most advanced countries in the field of local sustainability management. The Local Sustainability Reporting Framework (BNK 2.0) provides German local authorities with a flexible yet structured standard for reporting on their sustainability initiatives. Meanwhile, Sweden and Norway have strong legal frameworks that promote transparency in resource management and local governmental emissions reporting. However, Spain’s 2030 Agenda, which is a key part of the national government’s management plans (Rieiro-García et al., 2023b), lacks legislation requiring local governments to disclose sustainability information through reports (Curtó-Pagès et al., 2021; Sol, 2013). Furthermore, countries such as the USA and the UK have a Freedom of Information Act (FOIA), which grants citizens the right to access government-held information, including that related to sustainability initiatives.

Disclosing sustainability information is both challenging and important for local governments (Kaufmann & Kraay, 2002; Piotrowski, 2008). In 2021, the Chartered Institute of Public Finance and Accountancy (CIPFA) published a report on public environmental reporting, which assessed the current sustainability reporting landscape in the public sector and highlighted the key challenges, opportunities, and barriers faced by public sector organisations. Building on this momentum, the International Public Sector Accounting Standards Board (IPSASB) launched three sustainability reporting initiatives specifically tailored to the public sector in 2022. These efforts culminated in a consultation document aimed at strengthening sustainability reporting guidance for the public sector. The document positions the IPSASB as the global leader in developing sustainability standards for the public sector and offers an initial framework for disclosing sustainability-related information (Nicolò et al., 2023).

Good governance involves using the 231 existing indicators to assess progress on the SDGs and communicating the results through Voluntary National Reviews (VNRs; Cohen et al., 2023; Donchin et al., 2024; Fraisl et al., 2023; Gacutan et al., 2023), thereby ensuring greater local government accountability than under the MDGs (Cohen et al., 2023).

Given the low level of disclosure of sustainable actions by public sector entities (García-Sánchez et al., 2013) and the absence of clear regulations, it is important to note that existing sustainability-related information is often not included in local governments’ official reports. Instead, these entities tend to use other channels, such as their websites, to disclose this type of information. In turn, an increasing number of international organisations are demanding this information, prompting more governments to take responsibility for sharing data about their sustainable initiatives and the results they achieve (Ciambra et al., 2023; Guerrero-Gómez et al., 2021; León-Silva et al., 2022; Narang Suri et al., 2021).

Method

Data Collection

To ascertain what has been published thus far on local-government disclosure of SDG-related information, we reviewed existing literature. The first step was to identify relevant publications that met specific criteria. Our search strategy included several elements:

Since the SDGs were defined in 2015, the analysis covers publications from 2015 to 2025, the latest complete year available.

Scopus was selected as the database for the review because it covers a wide range of studies on the topic, indexes more journals than the Web of Science, and is widely used for systematic reviews (Mio et al., 2020; Sweileh, 2020).

Only journal articles were considered, and no filters were applied to select subject areas.

The search was conducted beginning with: “Title, keywords, or abstract.”

Following these steps, we conducted the following search in the Scopus database:

(TITLE (“sdg” OR “sustainable development goals” OR “sdg*” OR “2030 agenda” OR “global agenda”) AND KEY (“sdg” OR “sustainable development goals” OR “2030 agenda” OR “transpa*” OR “disclos*” OR “sustainability disclosure” OR “report*”) AND ABS (“public entities” OR “public sector” OR “government” OR “govern*”) AND ABS (“local govern*” OR “muncipalit*” OR “local entities” OR “city council*” OR “cit*”) AND NOT ABS (“companies*” OR “business*” OR “private sector” OR “private”) AND ABS (“disclos*” OR “dissem*” OR “transp*” OR “report*” OR “commitment*” OR “communicat*” OR “sustainability disclosure” OR “diffus*”) AND PUBYEAR > 2015 AND PUBYEAR <2025 AND ( LIMIT-TO (DOCTYPE, “ar”)) AND (LIMIT-TO (LANGUAGE, “English”))

This search yielded 66 publications that met our criteria. The first step was to read the abstracts of the papers to confirm their relevance to the intended topic of investigation. After this initial phase, 34 articles were discarded as not related to the topic. Next, following Mol et al. (2025), each author independently read and analysed the remaining papers, summarising their key characteristics. The results were then compared and harmonised. During this analysis, 19 papers that focused on sustainability in a generic way, rather than specifically on the SDGs were excluded.

It should be noted that, upon reviewing the search results, we identifie two papers that several frequently cited studies cited. These papers were not retrieved in the initial search but were added manually to the sample. Finally, 15 papers were selected. Figure 1 summarises the steps taken to obtain the final sample.

Article selection process.

Results

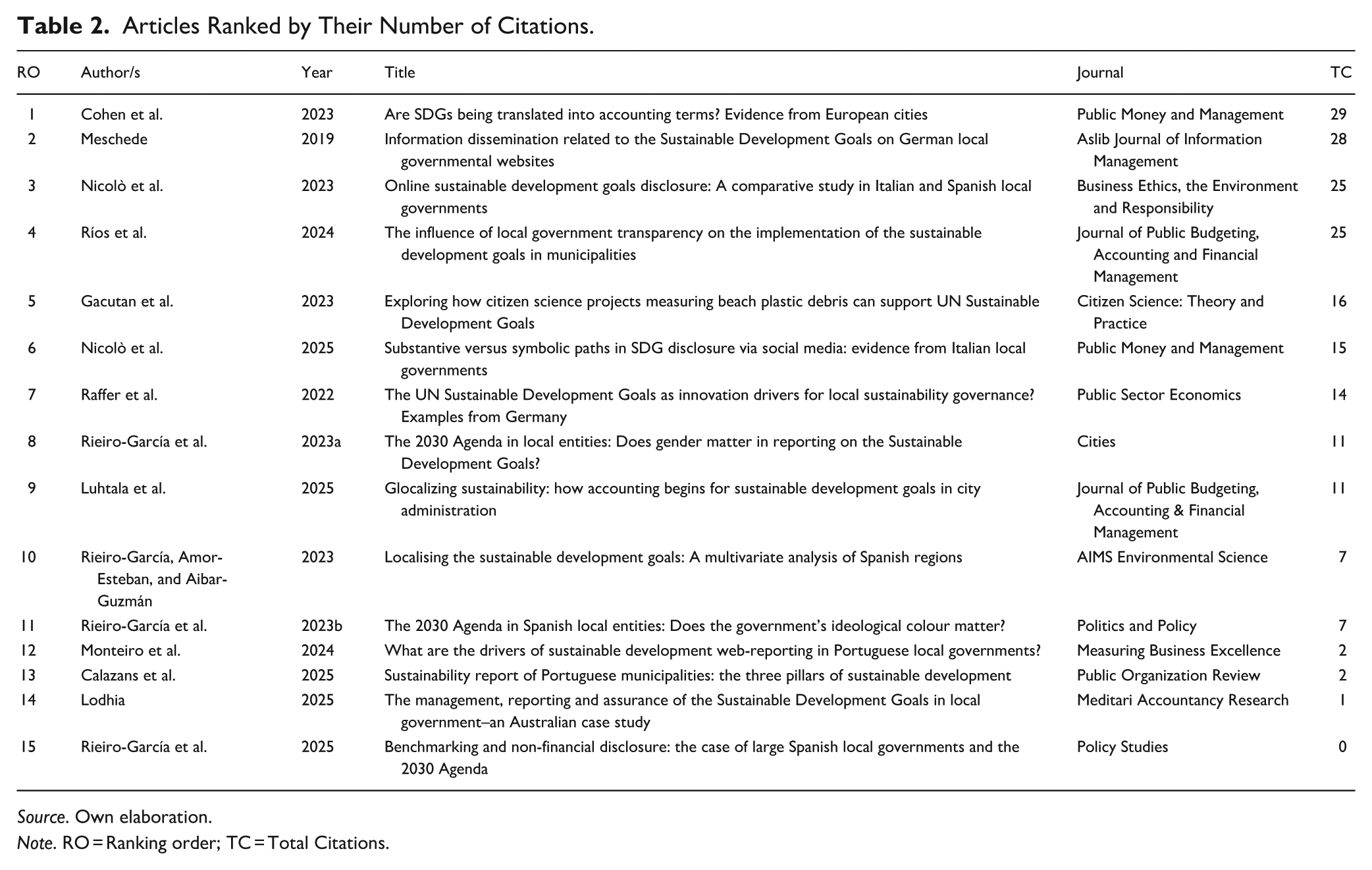

Table 2 presents the articles in the sample, ranked from the highest to the lowest number of citations. Four articles stand out with more than 25 citations: Cohen et al. (2023) with 29 citations; Meschede (2019) with 28; and Nicolò et al. (2023) and Ríos et al. (2024) with 25 each. Interestingly, this group includes both the oldest paper in the sample and some more recent papers. This finding contrasts with Dumay’s (2014) observation that the number of citations an article receives depends on how long ago it was published. Yet it is consistent with the findings of Mol et al. (2025), who reported that older articles were gradually replaced by more recent ones as the most frequently cited, a pattern indicating an increasing academic interest in sustainability reporting by public entities. Five articles received between 10 and 20 citations, while another 6 received fewer than 10. The latter group comprises some of the most recent papers.

Articles Ranked by Their Number of Citations.

Source. Own elaboration.

Note. RO = Ranking order; TC = Total Citations.

Publication Trends

Time Evolution

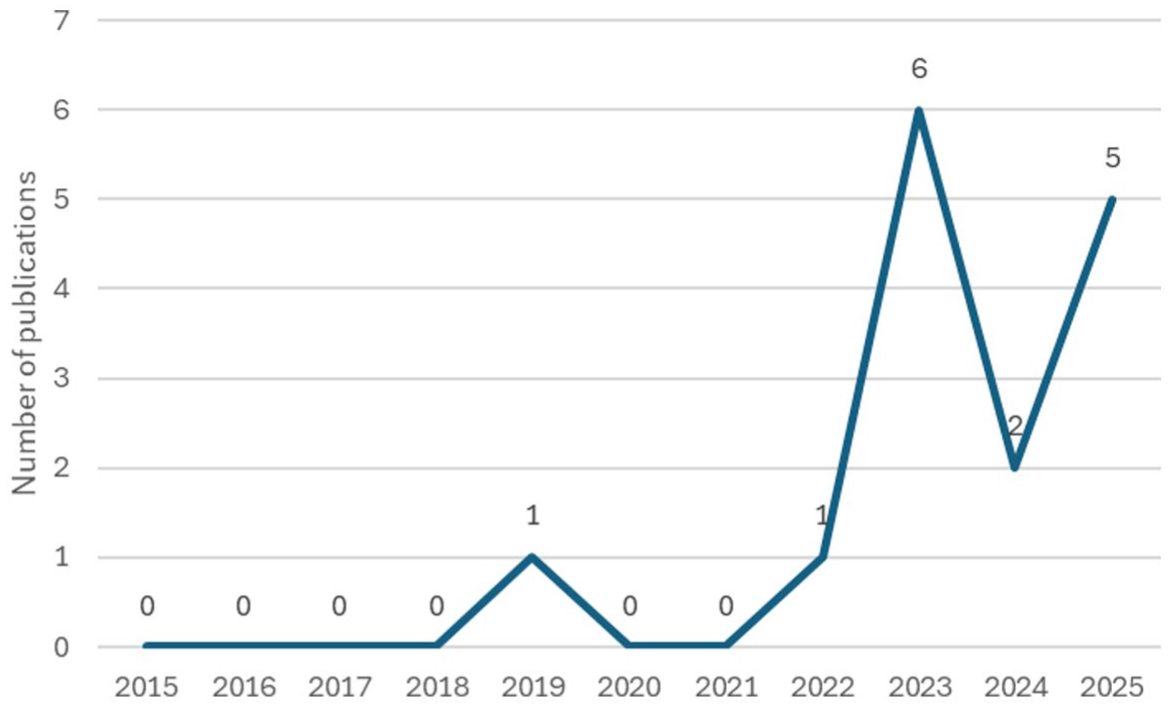

Figure 2 shows how publications on local government disclosure of information about SDGs has evolved. Although the SDGs were adopted in 2015, publications on this topic did not emerge until 2019. Interest in this topic declined in subsequent years, with no publications in 2020 and 2021. This may be because the focus of researchers during that period shifted towards the ongoing global health crisis caused by the COVID-19 pandemic. In 2022, only one paper was published. From then on, the number of studies increased significantly, peaking in 2023 with six papers published that year. In 2024, two papers addressing the topic were published, and by 2025, this figure had more than doubled with the publication of five articles. As can be seen, 13 of the 15 papers that make up the sample (86.67%) were published in the last 3 years (2023, 2024, and 2025). Nonetheless, the publications show an erratic pattern during this period, with a fluctuating number of articles being published. This may be partly explained by the lack of standardised databases at the local level for measuring the extent to which local governments disclose SDG-related information. The fluctuating growth in the number of publications on SDG reporting by local governments is similar to that observed by Fusco and Ricci (2019) in their literature review on sustainability reporting by public sector entities. Yet it contrasts with the constant increase identified by Mol et al. (2025).

Publications time trend.

The first published work on this topic was by Meschede (2019), who examined the disclosure of SDG-related information on the websites of German local governments. The study found that awareness of the SDGs was increasing and discussed the main topics of SDG reporting. Meschede’s work can be considered one of the first to explicitly explore the intersection between SDGs and their implementation in public sector organisations, thus contributing to a research area still underexplored.

Following a 2-year pause, Raffer et al. (2022) revisited the topic in a theoretical paper, examining whether the SDGs drive innovation in local sustainability governance with a focus on German municipalities. Throughout the article, the authors analyse various examples of public sector innovation related to the SDGs. They also mention a German institution called “SDG Indicators for Municipalities,” which supports governments in integrating and communicating the SDGs.

Articles published in 2023 address the disclosure of the SDGs by local governments from different perspectives. Gacutan et al. (2023), for example, focus on citizen science, examining its importance in collecting and reporting SDG data. Cohen et al. (2023) analyse whether the indicators used to report on the achievement of the SDGs rely on accounting information. The study examines whether the transition of the SDGs from a macro (UN) to a micro level (local government) level is supported by accounting data.

The remaining 2023 papers present more empirical studies. Rieiro-García et al. (2023b), explored how the political ideology of the governing party influences a city council’s commitment to the SDGs and SDG reporting. They found that hat municipalities governed by left-wing parties tend to disclose more SDG-related information. In addition, Rieiro-García et al. (2023a), analysed the impact of the elected officials’ gender on the level of SDG-related information disclosed by local governments. Their results show that having a female mayor was positively related to disclosure. Rieiro-García, Amor-Esteban, and Aibar-Guzmán (2023) analysed the SDG-related information disclosed on the websites of various Spanish municipalities, evaluating their commitment to the SDGs and how it has evolved. Lastly, Nicolò et al. (2023) performed a comparative analysis to determine the extent to which local governments in Spain and Italy use their websites to disseminate information on the SDGs.

In 2024, two papers addressed this topic. Ríos et al. (2024) analysed 103 Spanish municipalities to evaluate the effect of local government transparency on the achievement of the 2030 Agenda’s goals. Monteiro et al. (2024) examined the situation of Portuguese municipalities to determine whether they disclosed SDG-related information on their websites, and which municipality characteristics influenced such reporting.

In 2025, Nicolò et al. (2025) analysed how Italian local governments use social media (specifically X) to disclose information related to the SDGs, which a focus on SDG 13. Rieiro-García et al. (2025) evaluated the level of SDG disclosure of Spanish local governments based on information published on their websites. The authors identified trends and drivers, and categorised municipalities according to their commitment to the 2030 Agenda. Luhtala et al. (2025) analysed the extent to which the SDGs were integrated into the municipal strategies, budget plans and financial reports of Finland’s six largest cities. Regarding reporting, they observed that the SDGs were generally not considered a performance metric to be disclosed to stakeholders in financial reports, although sustainability-related issues were addressed in these reports. Calazans et al. (2025) analysed the extent to which Portuguese local governments ‘ sustainability reports provide information related to the SDGs and found that more than half of the entities in their sample did not disclose such information. The researchers also identified the SDGs that were most disclosed by Portuguese local governments. Finally, Lodhia et al. (2025) conducted a case study of an Australian local council, analysing changes to management and reporting systems aimed at addressing the SDGs, as well as the evolution of SDG reporting. They found that SDG reporting was still in its early stages and was predominantly focused internally.

The temporal pattern of publications suggests that SDG reporting by local governments is an emerging focus of academic research that still needs to be consolidated, despite a significant increase in recent years. Although research on this subject has been somewhat erratic, the increase observed after 2022 can be interpreted as indicative of the 2030 Agenda’s consolidation in local governments’ public policies and reporting practices as well as the need to assess implementation at the local level.

Journals

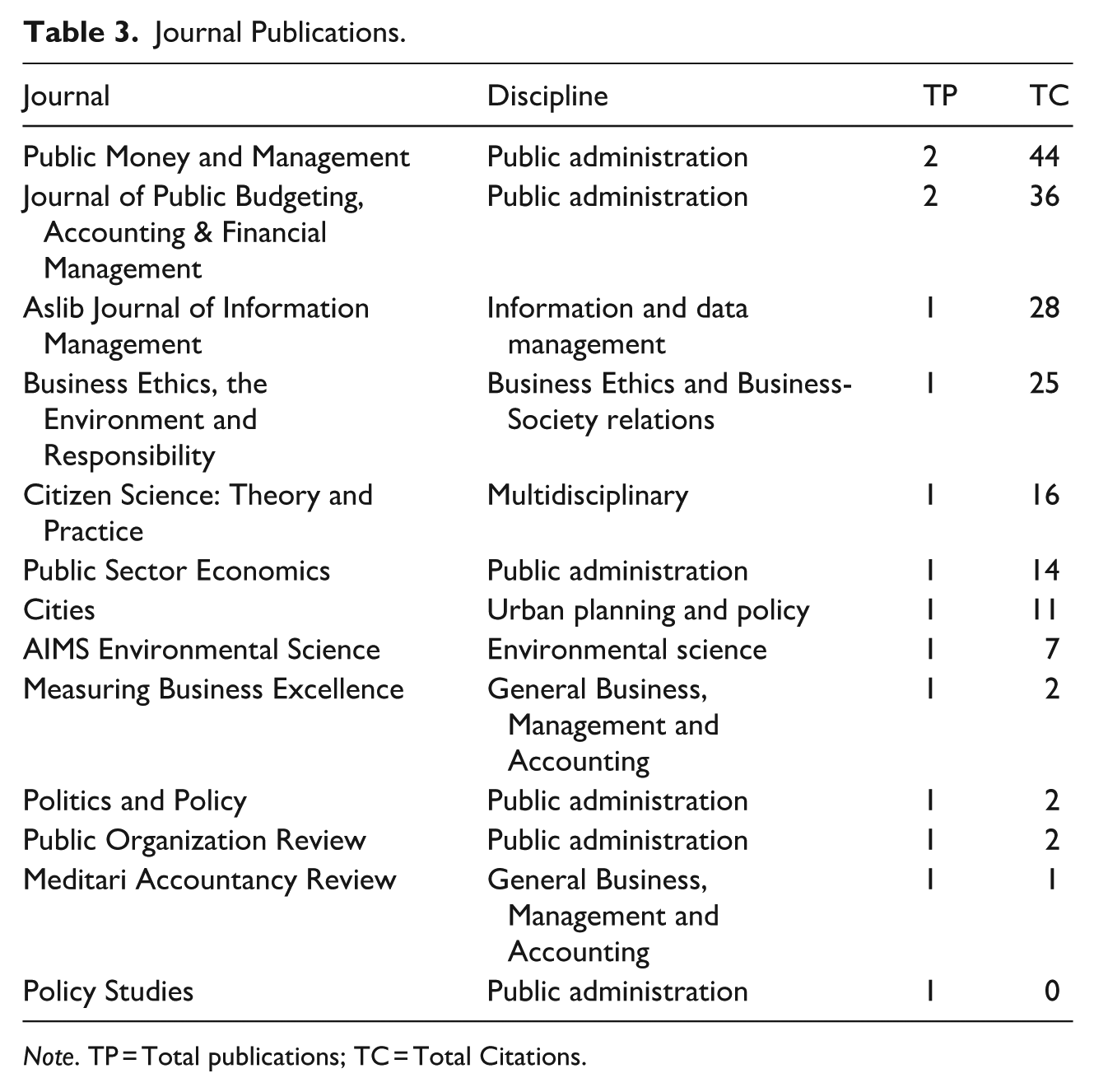

The sample consists of 15 articles published in 13 different journals. The main aim of most of these journals is to improve understanding of the management of public entities, including public policies, financial matters, regulations and public service management. Several journals, however, focus specifically on matters related to ethical and environmental issues (e.g., AIMS Environmental Science and Business Ethics, the Environment and Responsibility), accounting (e.g., Meditari Accountancy Research), or information management (e.g., Aslib Journal of Information Management). Table 3 shows the papers ranked by total citations and the journals in which they were published.

Journal Publications.

Note. TP = Total publications; TC = Total Citations.

Notably, two journals—Public Money and Management and the Journal of Public Budgeting, Accounting & Financial Management—published more than one article on the topic, with two papers each. Furthermore, these journals contain three of the most frequently cited papers. Public Money & Management stands out, with two of the five most-cited articles. The remaining most-cited articles have been published in the Aslib Journal of Information Management and Business Ethics, the Environment & Responsibility.

Authors’ Productivity, Impact, and Affiliation

In total, 44 authors have contributed to the literature on this subject. Most of the papers have been written by more than one author, with the most common number of authors being three. Only one author, Christine Meschede (2019), has published a paper individually. Furthermore, it is notable that only four authors have published more than one paper on this subject. Cristina Aibar-Guzmán and Manuel Rieiro-García have each authored four papers, followed by Beatriz Aibar-Guzmán, who co-authored in three of them, and Giuseppe Nicolò, who has published two other works in this field. Consequently, these authors can be considered as the most experienced in this area. Giuseppe Nicolò is the most frequently cited author, with 40 citations in two papers.

As for the authors’ affiliations, Table 4 shows the institutions (universities or organisations) to which the authors belong. The University of Santiago de Compostela (Spain) tops the list with four publications, followed by the University of Salerno (Italy) with two publications. Those at the remaining institutions published one paper each.

Authors’ Affiliation.

Source. Own elaboration.

Note. TP = Total publications.

The countries with the largest number of institutions researching local government reports on SDGs are Spain, Germany, Portugal, and Australia. These countries are developed, and the first three are major European economies.

Knowledge Structure

Main Theories

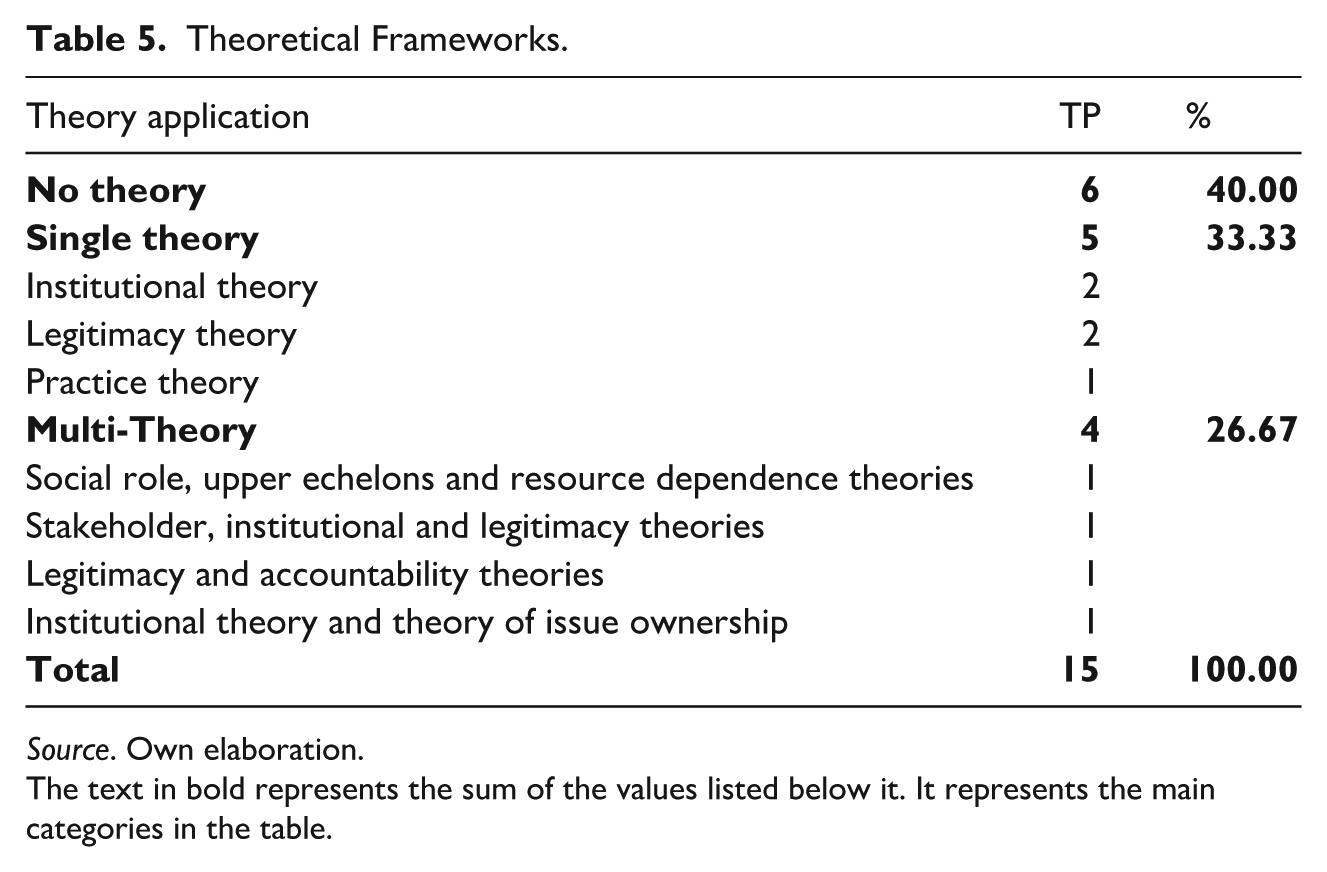

Table 5 shows the different theories that the papers in the sample employ. A significant proportion of the sample (40%) consists of papers that primarily discuss the importance of the SDGs and their disclosure for local governments or present descriptive analyses. Such papers lack specific theoretical frameworks. Conversely, 60% of the papers use one or more theories to support their research.

Theoretical Frameworks.

Source. Own elaboration.

The text in bold represents the sum of the values listed below it. It represents the main categories in the table.

Notably, 33.33% of the papers in the sample use a single theory to inform their study, while 26.67% adopt a multi-theoretical approach, drawing on several theories to support their research. This finding differs somewhat with the conclusion reached by Mol et al. (2025), who found that multiple theories were necessary to explain the sustainability reporting choices and practices adopted by local governments.

Institutional theory and legitimacy theory stand out as the most used theories. According to institutional theory (DiMaggio & Powell, 1983), organisations (both public and private) face pressure to align their behaviours and values with those deemed desirable or appropriate within their institutional environment, thereby enforcing formal coherence in human activity (Joseph et al., 2019; Nicolò et al., 2023; Rieiro-García et al., 2023a). Legitimacy theory (Suchman, 1995) is also used to explain organisational behaviours related to sustainability reporting. It is based on the premise that reporting serves as a tool for gaining legitimacy in the eyes of stakeholders (Monteiro et al., 2024; Ríos et al., 2024).

Other theoretical frameworks employed in research on SDG reporting by local governments include social role, upper echelons, and resource dependence theories (Rieiro-García, Amor-Esteban, & Aibar-Guzmán, 2023) as well as stakeholder(Rieiro-García et al., 2023b), accountability (Ríos et al., 2024), and practice theories (Lodhia et al., 2025).

Focusing on the most used theories (institutional theory and legitimacy theory), we find that they are were applied in seven papers, all of which share several characteristics. Firstly, they all are empirical studies published within the last years. Secondly, all were developed at European institutions, in Mediterranean countries with similar characteristics, such as Portugal, Spain, and Italy.

The studies that rely on institutional theory are those by Luhtala et al. (2025), Nicolò et al. (2023), Rieiro-García et al. (2023a), and Rieiro-García (2023b), the latter two of which also justify their work with legitimacy theory. Luhtala et al. (2025) applied institutional theory to analyse the process by which the SDGs were institutionalised and integrated into the management of six Finnish local governments, as well as the subsequent disclosure of information about them.

Nicolò et al. (2023) examined the extent to which local governments use their websites to disseminate information related to the SDGs, comparing Spanish and Italian municipalities. The authors justify the use of institutional theory on the basis that the survival of an organisation depends on its adherence to socially accepted norms and its ability to adapt to its environment. The results confirm that few local governments present non-financial reports on their websites, with Spanish results being better than Italian ones.

Rieiro-García et al. (2023a) analyse how the gender of elected officials is related to the level of SDG-related information disclosed by local governments. Their results show that having a female mayor is positively associated with the level of SDG disclosure. Rieiro-García et al. (2023b) analyse the evolution of commitment to the SDGs (measured through outreach) in Spanish local and regional governments between 2016 and 2021. The results reveal a low level of commitment to the SDGs among Spanish municipalities, although this has increased over time.

In addition to Rieiro-García et al. (2023b), studies by Monteiro et al. (2024), Ríos et al. (2024), and Nicolò et al. (2025) also adopt legitimacy theory as their theoretical framework. The first of these studies (Monteiro et al., 2024) investigates how Portuguese local governments disclose information about the SDGs on their websites, identifying the factors that influence this reporting. Their analysis is based on legitimacy theory, describing it as the dominant theoretical framework for explaining organisational behaviour related to sustainability reporting, as reporting is viewed as a means of gaining legitimacy among stakeholders. The findings suggest that the disclosure of SDG-related information is influenced by municipal size, with larger municipalities being more likely to disclose SDG information. Similar patterns are observed in municipalities located in coastal areas, those with stronger financial positions, and those participating in sustainable programmes and networks. In contrast, political ideology, and gender of elected officials are not significant predictors, although gender becomes significant when considered alongside with participation in sustainable network programmes.

Ríos et al. (2024) analyse the impact of local government transparency on achieving SDGs. The authors justify their use of legitimacy theory, arguing that organisations’ survival is linked to their stakeholders’ perceptions of them, so it is essential to maintain legitimacy and meet social expectations. The study reveals a positive association between transparency and SDG implementation, which is consistent with legitimacy theory, suggesting that municipalities may leverage transparency to enhance their legitimacy.

Nicolò et al. (2025) also used legitimacy theory to explain the motivations that may drive local governments to disclose information about the SDGs. They posit two opposing views: on the one hand, SDG reporting may be intended to project a responsible image to stakeholders and gain legitimacy; on the other hand, it may reflect the genuine communication of actions being implemented, in which case legitimacy is derived implicitly from effective performance.

Research methods

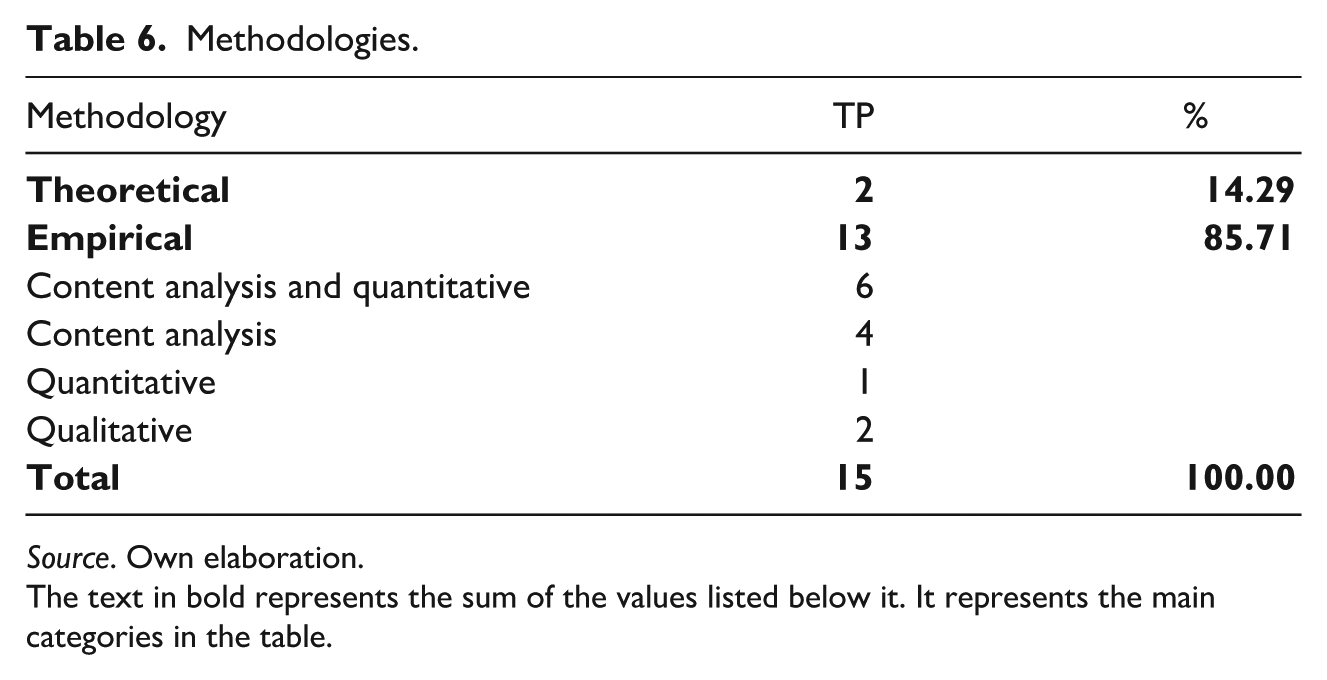

As Table 6 shows, the methodologies the employed in the studies included in the sample are diverse. Following the categorisation of Mol et al. (2025), the papers are divided into theoretical and empirical studies. In our sample, two papers (13.33%) are purely theoretical/conceptual: Raffer et al. (2022) and Gacutan et al. (2023); the remaining 13 papers (86.67%) are classified as empirical. These percentages are slightly comparable with those obtained in previous literature reviews on sustainability reporting by public sector entities (Fusco & Ricci, 2019; Manes-Rossi et al., 2020; Mol et al., 2025; Stefanescu, 2022).

Methodologies.

Source. Own elaboration.

The text in bold represents the sum of the values listed below it. It represents the main categories in the table.

Of the 13 empirical studies, two are qualitative. The first is a multiple case study (Luhtala et al., 2025) employing semi-structured interviews and secondary data sources, and the second is a single case study (Lodhia et al., 2025) employing the same methods. These findings contrast with those of previous literature reviews on sustainability reporting by public sector entities, which documented a predominance of case studies based on interviews.

Content analysis is the most widely used method, typically involving a review of information disclosed on websites regarding the SDGs. Ten of the 12 empirical studies employ content analysis as their primary data analysis method. However, four of these studies (Meschede (2019), Cohen et al. (2023), Calazans et al. (2025) and Rieiro-García et al. (2025)) rely exclusively on this technique, while the others (Monteiro et al., 2024; Nicolò et al., 2023; Nicolò et al., 2025; Rieiro-García et al., 2023a, 2023b; Rieiro-García, Amor-Esteban, & Aibar-Guzmán, 2023) complement content analysis with the application of statistical techniques to the obtained data. In contrast, Ríos et al. (2024) employed a purely statistical approach.

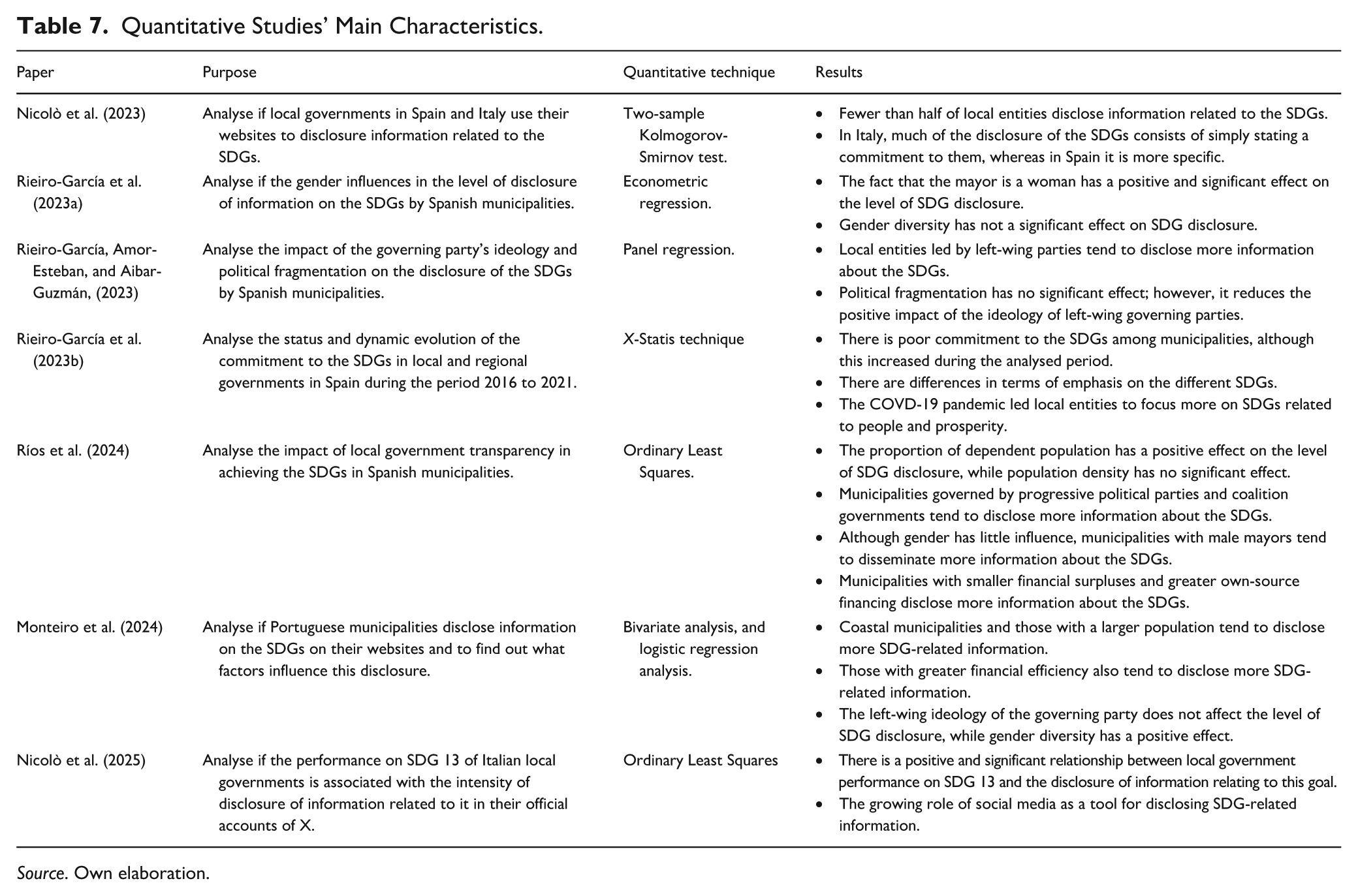

Table 7 summarises the methodologies employed in the seven articles conducting quantitative analysis as well as their main findings. These studies can be grouped into two categories. The first comprises studies that assess the level of SDG reporting by local governments (Monteiro et al., 2024; Nicolò et al., 2023; Nicolò et al., 2025; Rieiro-García et al., 2023b; Rieiro-García et al., 2025). The second includes studies that examine factors that may influence the level of disclosure, such as gender diversity, political ideology, sociodemographic characteristics, and the size of municipalities (Monteiro et al., 2024; Nicolò et al., 2025; Rieiro-García et al., 2023a, Rieiro-García, Amor-Esteban, & Aibar-Guzmán, 2023; Ríos et al., 2024).

Quantitative Studies’ Main Characteristics.

Source. Own elaboration.

Most of the studies report low levels of SDG disclosure in general and inconsistent findings relating to the drivers of SDG reporting. In our opinion, the inconsistent results about the drivers of SDG reporting may reflect differences in how variables are measured, which stems from the lack of unified databases. As previously mentioned, no standardised local-level databases are available that are dedicated to monitoring the disclosure of SDG-related information by local governments. To obtain information on local governments’ practices in SDG reporting, researchers must analyse their websites. This data gap poses a significant challenge to measuring and comparing local progress towards the 2030 Agenda or local government transparency. It could also explain why there are so few studies in this field of research.

Following Mol et al. (2025), these drivers have been categorised as socio-economic factors; political factors; local entity characteristics; and characteristics of the external environment. The first group includes variables such as the locality’s geographic location, its total population, population density, and dependent population. Rieiro-García et al. (2023a), Rieiro-García, Amor-Esteban, and Aibar-Guzmán (2023) found that the total population, dependent population, and population density of a municipality fostered SDG reporting. However, Ríos et al. (2024) observed no statistically significant effect of the last variable. Monteiro et al. (2024) found that municipalities in coastal areas and those with arger populations tend to disclose more information on the SDGs.

Political factors include variables such as the political ideology of the governing party or the level of political fragmentation. Rieiro-García, Amor-Esteban, and Aibar-Guzmán (2023) and Ríos et al. (2024) found that the left-wing ideology of the governing party had a statistically significant relationship, whereas Monteiro et al. (2024) observed no such effect.

Factors related to the characteristics of the local entity include gender diversity, debt level, budget, and SDG performance. Here. Rieiro-García et al. (2023a), Rieiro-García, Amor-Esteban, and Aibar-Guzmán (2023) demonstrate that the presence of a female mayor encourages SDG reporting. Yet, Ríos et al. (2024) came to the opposite conclusion, finding that male mayors foster SDG reporting, while Monteiro et al. (2024) documented no significant association. Neither Rieiro-García et al. (2023a) nor Monteiro et al. (2024) found a significant impact of gender diversity on the city council. They also reported that municipalities with larger budgets (Rieiro-García et al., 2023a; Rieiro-García, Amor-Esteban, & Aibar-Guzmán, 2023) and more financial efficiency (Monteiro et al., 2024) tend to disclose more SDG-related information. Furthermore, Nicolò et al. (2025) found that SDG performance is positively associated with SDG reporting.

Finally, concerning the impact of external environmental factors, Rieiro-García, Amor-Esteban, and Aibar-Guzmán (2023) report a positive effect of the pandemic on SDG reporting by local governments. This finding is consistent with Qian et al.’s (2018) observation that, in times of uncertainty, decision-makers demand more information to mitigate risk.

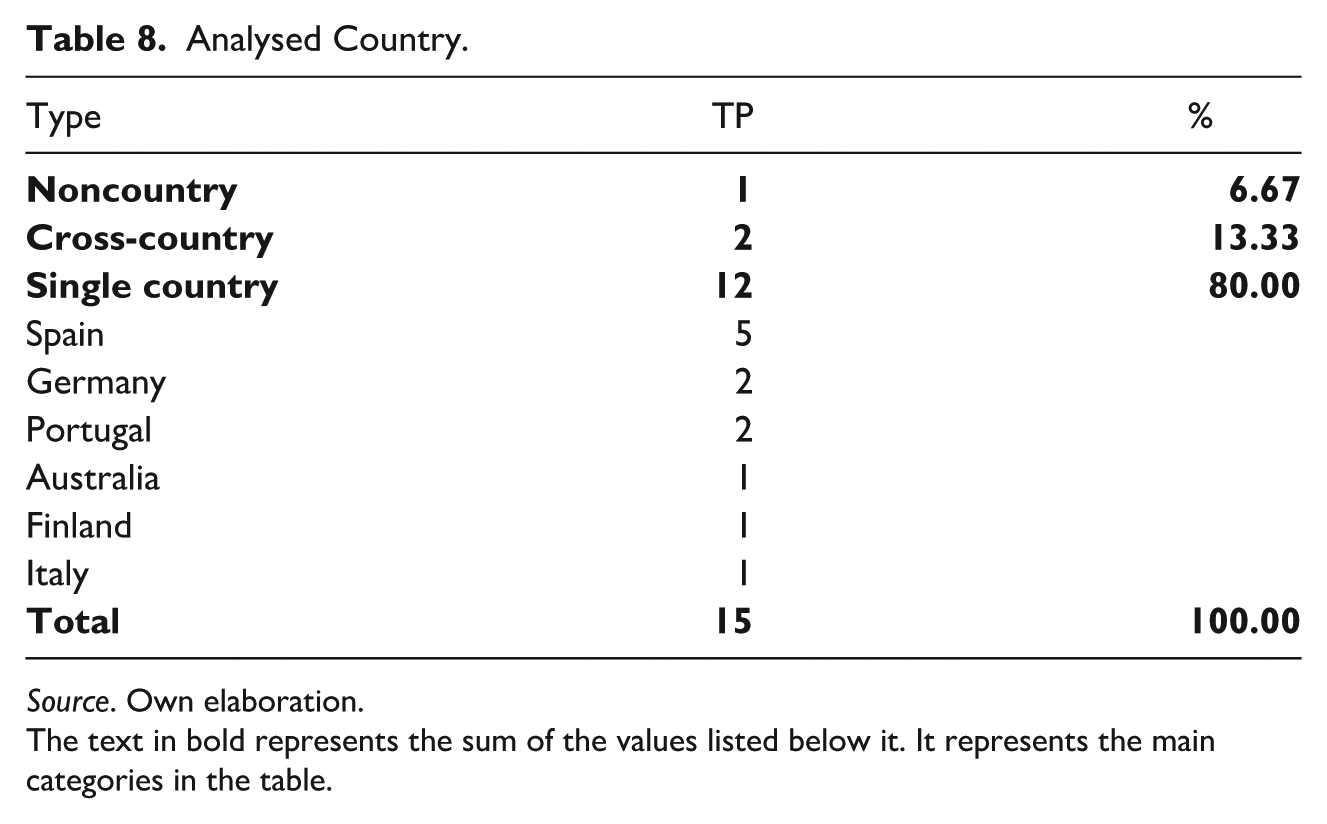

Countries/Regions Studied

Most empirical studies focus on European countries, with only one examining a non-European country. Lodhia et al. (2025) conducted a case study of an Australian local entity. These findings are consistent with those reported by Manes-Rossi et al. (2020) and Mol et al. (2025). In their respective literature reviews on sustainability reporting by public sector entities, they also noted a clear predominance of studies focused on European countries.

Two papers take a cross-country approach, examining multiple countries or making comparisons between them: Cohen et al. (2023) conduct a comparative analysis of SDG indicators disclosed by European cities, and Nicolò et al. (2023) examine the extent to which local governments in Spain and Italy use their websites to disclose information about SDGs.

Most papers (80%) focus on a single country. Spain is the country that has been analysed most frequently, with five papers investigating the situation there. Germany and Portugal follow, having each been the focus of two papers. Other analysed countries include Finland and Australia. Spain’s leading position may be explained by its strong commitment to the 2030 Agenda, which forms a central part of the national government’s management plans (Rieiro-García et al., 2023b). These findings are similar to those documented by Mol et al. (2025) in their literature review of sustainability reporting by public sector entities, which also revealed a predominant focus on Spain, Italy, and Portugal.

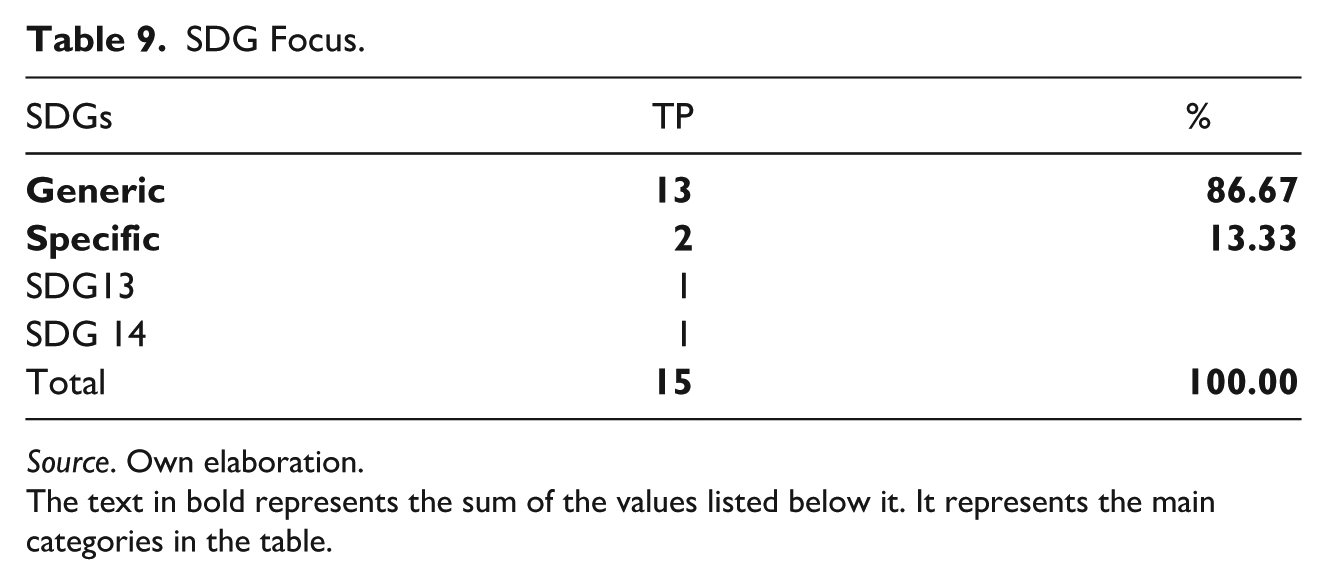

Table 8 shows all the countries analysed in the sample, and Table 9 displays the SDGs analysed.

Analysed Country.

Source. Own elaboration.

The text in bold represents the sum of the values listed below it. It represents the main categories in the table.

SDG Focus.

Source. Own elaboration.

The text in bold represents the sum of the values listed below it. It represents the main categories in the table.

These results highlight the strong geographic concentration of studies in European countries. This focus may be due to their decentralised governance structures, which grant structures, which grant considerable powers to regional and local governments. This institutional configuration enables the SDGs to be implemented and monitored at the subnational level, making these countries highly relevant for research in this area (OECD, 2018; Reddy, 2016). Furthermore, European municipalities are under regulatory and social pressure to make their cities more sustainable and inclusive, highlighting the importance of researching and disseminating data on this progress.

The European Union also funds numerous research projects through programmes such as Horizon Europe, facilitating the creation of scientific networks focused on urban governance and sustainability. Consequently, European researchers are expected to play a pivotal role in enhancing and monitoring sustainability objectives, particularly in evaluating the transparency of local governments. Together, these factors foster an environment conducive to the active involvement of researchers, establishing European researchers as the most active in this field.

The dearth of studies in other regions, however, highlights a notable literature gap, limiting the generalisability of findings and emphasising the necessity for more geographically diverse research.

SDGs

As shown in Table 8, most papers (86.67%, 13 papers) adopt a general approach, discussing the SDGs in broad terms rather than focusing on a specific goal. Only two papers (i.e., Gacutan et al., 2023; Nicolò et al., 2025) examine particular SDGs: SDG 14 (Life Below Water) and SDG 13 (Climate Action), respectively.

Gacutan et al. (2023) highlight the importance of citizen science and public participation at all stages of scientific research, presenting it as a key tool for expanding collective knowledge. Furthermore, it is characterized as an effective approach to data collection and contributing to SDG monitoring reports. In this case, given the emphasis on plastic waste, local-level citizen participation is particularly important. The study focuses specifically on Goal 14, Target 14.1, and Indicator 14.1.b (plastic debris density).

Moreover, Nicolò et al. (2025) focus on SDG 13 due to its importance for local governments. They state that “cities contribute to 75% of global carbon emissions and are responsible for around two-thirds of global energy consumption” (Nicolò et al., 2025, p. 745). For this reason, they conduct a specific analysis of the disclosure of this SDG on local government X accounts.

Although studies such as those by Rieiro-García et al. (2023b), Rieiro-García et al. (2025), and Calazans et al. (2025) analyse the SDGs more broadly, their findings reveal specific patterns. For instance, the authors identify variations in how municipalities prioritise different SDGs. Notably, SDGs 8 and 11 emerge as top priorities in the papers authored by Rieiro-García and colleagues, showing the greatest growth in commitment, likely due to their close connection with economic development and urban sustainability. In contrast, SDGs 5, 6, and 17 have experienced a decline in emphasis. The authors attribute this shift to the impact of the COVD-19 pandemic, which has led Spanish municipalities to focus more heavily on goals related to people and prosperity. Conversely, Calazans et al. (2025) identified SDGs 3, 6, and 7 as the most frequently disclosed goals, while SDGs 1 and 2 were disclosed less frequently.

These results underscore the need for more studies focusing on each SDG, since little information exists on the specific disclosure of each goal by local governments.

Adjacent Research on Governance and Transparency

This section presents several studies that were identified in the initial search, which, despite providing valuable insights, were not included in the final sample due to the specific inclusion criteria.

The first published work on this topic was by Koch and Krellenberg (2018), who examined three initiatives (one led by the German government, one by a scientific organisation and one by a non-governmental organisation) that aimed to adapt SDG 11 from a global to a national context. Their findings revealed that Germany utilises only some of the original targets and indicators for SDG 11, emphasising the vital role of indicators in communicating and measuring the impact of actions taken to achieve the SDGs. This study is one of the first to explicitly explore the intersection between the SDGs and their implementation within public sector organisations, thus contributing to an under-explored area of research.

One year later, Joseph et al. (2019) examined the integrity of disclosures on local government websites in Malaysia and Indonesia, interpreting these practices in terms of institutional theory (specifically, coercive isomorphism). While the study provides valuable insights into transparency in the public sector and efforts to combat corruption (which is closely linked to SDG 16), it was excluded from the main analysis as it focuses on integrity and governance structures rather than the disclosure of SDG-related information. Nevertheless, we regard it as a relevant contribution to the subject, as it emphasises how SDG reporting integrity can facilitate the achievement of the governance objectives set out in the 2030 Agenda.

Through a case study of a Swedish city and its comparison with other cities, Hansson et al. (2019) analyse the use of indicators in the implementation of the SDGs. Similar to Koch and Krellenberg (2018), they focus on the central role of indicators as tools for measuring and communicating progress towards the 2030 Agenda and the SDGs.

Guerrero-Gómez et al. (2021), meanwhile, identify the factors that promote sustainability transparency on the websites of local governments in Latin America. This study was not included in our sample because it focuses on sustainability transparency in general, without making an explicit reference to the SDGs.

Fraisl et al. (2023) explore the role of citizen science in collecting data related to the SDGs, as well as its potential integration into official monitoring systems. However, their national-level approach, focused on Ghana, justifies the exclusion of our sample, as this literature review emphasizes local governments.

Finally, Göçoğlu and Göçoğlu (2025) investigate the potential of local governments in Turkey to contribute to achieving the SDGs. Although their study provides valuable insights into the extent to which local strategic plans comply with the SDGs, it does not directly address the disclosure of information, resulting in its exclusion from the sample.

Conclusions

As Manes Rossi et al. (2025, p. 637) noted, “the need for credible, transparent, and actionable sustainability reporting in the public sector has never been greater.” This study reviews the academic literature on the disclosure of SDG-related information by local governments, focusing on publications indexed in the Scopus database between 2015 and 2025. In doing so, it acknowledges that, despite their proximity to citizens and their pivotal role in implementing the 2030 Agenda, SDG reporting by local governments has received less attention than the private sector in existing literature (Mol et al., 2025). The final sample included 15 papers exploring the topic from various perspectives. These papers included theoretical and conceptual works, as well as empirical studies involving quantitative analyses and case studies. This literature review reveals that, while the body of research is still in its infancy, it is gradually expanding, with 86.67% of articles published in the last 3 years. Following an initial period of 4 years (2015–2018) during which no papers were published on the topic, the first related publication appeared in 2019. The somewhat erratic temporal pattern of publications suggests that SDG reporting by local governments is an emerging research topic, highlighting the need for further research into the implementation of the 2030 Agenda within the public policies and reporting practices of local governments.

Notably, the sample covers a wide range of journals, most of which are dedicated to public management. Among the top five most-cited papers, however, are those published in journals with a scope that includes environmental, accounting, and information management issues. Additionally, most studies were co-authored, with Meschede (2019) being the only single-author paper in the sample.

Of the articles in the sample, 60% use one or more theories to ground their research, while the remaining 40% lack a specific theoretical framework. Of the articles with a theoretical framework, most (five out of nine) use a single theory, while the rest combine multiple theories. Theoretical approaches are dominated by institutional theory and legitimacy theory, which suggest that researchers tend to conceptualise SDG reporting as a mechanism through which local governments seek external validation and align themselves with institutional pressures.

Most of the articles (86.67%) are empirical analyses, of which only two are qualitative case studies. Content analysis is the most frequently used method for data collection and analysis. The majority of studies focus on European countries, particularly Southern Europe, with Spain, Italy, and Portugal being the most frequently studied countries. Spain emerges as the most active country in this area, with the highest number of publications and leading scholars contributing to the topic. Most studies examine SDG reporting broadly, with only two looking at specific goals. In general, studies report low levels of SDG reporting and inconsistent findings relating to its drivers. The most frequently analysed SDG reporting drivers are sociodemographic, political and organisational characteristics.

These results demonstrate similar trends to those documented in other literature reviews on sustainability reporting by public sector entities (e.g. Fusco & Ricci, 2019; Manes-Rossi et al., 2020; Mol et al., 2025). However, there are some differences, which are likely since these studies focus on the public sector in the broadest sense (including all types of public entities) and on the disclosure of sustainability information in general rather than in relation to the SDGs specifically.

This study makes a valuable contribution to the existing literature by providing a useful reference point to guide future research in this area. Our analysis highlights the urgent need for more qualitative, empirical research on SDG reporting by local governments to shed light on the subtle dynamics that are often neglected in quantitative studies. Developing global databases and standardising variables would improve the consistency and comparability of findings by enhancing methodological rigour. Our analysis reveals a clear predominance of studies focused on European countries, primarily in Southern Europe, and a lack of studies on other geographical contexts (the Americas, Africa and Asia). This implies a lack of knowledge regarding the state of SDG reporting by local governments in these regions. There is also a notable bias towards the analysis of SDG reporting in general, which stresses the need for more studies focusing on specific SDGs to provide a more comprehensive view of SDG reporting practices by local governments.

From a practical standpoint, the findings of this study offer guidance to researchers, regulators, and public administrators by mapping out key themes, methodological trends, and areas that have not been explored enough, such as the analysis of specific goals and non-European countries. The existing focus on European countries highlights the need to systematically expand the research agenda to include sub-Saharan Africa, Latin America, and Southeast Asia, where deficits in SDG implementation remain most significant (Erin & Bamigboye, 2021; Guerrero-Gómez et al., 2021). The findings provide interesting insights by offering a snapshot of the status of SDG reporting by local governments and the factors that previous research has identified as its potential drivers. Understanding these issues could enable local entity managers to better align their reporting practices with the 2030 Agenda. Regulators can also use the insights to refine guidelines and enhance SDG reporting by local governments. Overall, we found that the disclosure of SDG-related information remains consistently low in various jurisdictions, including Spain (Nicolò et al., 2023; Rieiro-García et al., 2023a, 2023b; Rieiro-García, Amor-Esteban, & Aibar-Guzmán, 2023), Italy (Nicolò et al., 2025), and Portugal (Monteiro et al., 2024). This suggests that voluntary frameworks may be ineffective in ensuring systematic accountability. In this respect, national governments and supranational bodies should consider establishing mandatory, standardised municipal SDG reporting frameworks.

Despite the interest and usefulness of the findings, this study has several limitations. Firstly, in accordance with established systematic literature review methodologies (e.g. Mio et al., 2020; Mol et al., 2025), it is confined to English-language papers published in Scopus-indexed journals. This approach ensures a focused scope and enhances the reliability of the research findings. Consequently, other sources, such as books, book chapters, and grey literature, were excluded from the study. Although this approach helps to ensure quality and comparability across studies, it limits the review’s comprehensiveness. Incorporating papers in other languages and data sources, such as Web of Science or Google Scholar, could broaden the scope of the review. Secondly, the selection of papers can be influenced by the keywords used; using alternative keyword combinations could provide a different initial sample of studies.

Drawing on this review, two potential avenues for future research can be identified. Firstly, the findings emphasise the need for more studies focusing on non-European countries. Secondly, the findings highlight the need for further quantitative and qualitative research into the potential drivers of and barriers to sustainability reporting by local governments.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analysed during the current study.