Abstract

This study investigates gender differences in remittance practices among migrants in Japan, focusing on motivations, behaviors, and financial inclusion outcomes. Using Principal Component Analysis (PCA), we identify eight thematic subgroups based on underlying patterns in factors like socioeconomic background, financial service familiarity, and migration stage. Findings both affirm and challenge conventional views, revealing that while women overall prioritize savings, men are more motivated by altruism and family support. By examining these interactions, we offer new insights into how gender roles evolve in different migrant contexts, enhancing our understanding of the complex drivers behind remittance practices and financial inclusion.

Introduction

Financial inclusion, defined as equitable and sustainable access to financial products and services, is widely recognized as a cornerstone of global economic growth and poverty reduction efforts. It is cited as a catalyst for achieving seven of the 17 Sustainable Development Goals, given its role in advancing key development priorities such as poverty alleviation, food security, health and well-being, and reduction of inequalities (World Bank, nd). Despite progress in the expansion of overall financial access in the past decade, significant challenges persist, particularly for marginalized populations such as migrants and women. According to the 2023 World Bank’s Global Findex Report, 1.4 billion people remain unbanked, lacking even a basic account with a financial institution or a mobile money provider. Many more are underbanked, meaning they have inadequate access to mainstream financial services such as insurance and loans. Gender disparities in financial inclusion remain pronounced, with gaps in global account ownership at 4% globally and 6% for developing countries (World Bank, 2023). This persistent inequality underscores the need for gender-responsive strategies to achieve universal financial inclusion.

Concurrently, the surge in international migration, coupled with advancements in technology and a boost in digital services due to COVID-19, has led to a remarkable increase in the amount of international migrant remittances—money sent back to families and friends in their countries of origin. In 2023, remittance flows reached an estimated United States Dollar (USD) 857 billion globally, up from USD 843 billion in 2022 and USD 717 billion in 2020 (International Organization for Migration, 2025). Of this, low- and middle-income countries (LMICs) received a record of USD 656 billion, nearly three times the amount of Official Development Assistance (ODA). Although these figures likely underestimate actual flows, as they do not capture unrecorded transfers through informal channels, they nonetheless highlight the growing importance of remittances as a source of external financing for LMICs and a crucial driver of both financial resilience and social development. Yet, within this evolving landscape, the gendered dimensions of migrant remittance practices remain inadequately understood.

Existing research has examined gender differences in remittance motivations (Carling, 2008), behaviors such as frequency and amount (Petrozziello, 2013), and empowerment outcomes (Lopez-Ekra et al., 2011), often through focused case studies on specific migrant communities or bilateral migration corridors. While this approach can incorporate unique sociocultural factors within particular groups, it provides valuable but fragmented insights that limit the generalizability of findings. Furthermore, many studies treat gender as a discrete category rather than as an intersecting axis shaped by factors such as legal status, financial literacy, household roles, and life cycle stages to shape cross-border remittance behaviors (Del Motto, 2024). Scholarship and policy-making on women migrants have made significant progress, but still tend to neglect the structural and intersectional forces that shape women’s financial practices and opportunities (Bastia and Piper, 2019). Existing research also tends to isolate individual or household remittance behaviors without considering the broader institutional or spatial systems that shape financial flows (Guermond, 2021). There remains the need for analytical frameworks and methodologies that can better account for these intersecting structural factors and uncover emergent patterns within diverse migrant populations.

This study aims to address this gap by employing Principal Component Analysis (PCA) to investigate the gendered dimensions of remittance practices among a diverse pool of income-earning migrants in Japan. PCA allows for the identification of distinct profiles of remittance practices, offering insights into how gender intersects with demographic, financial, and migratory factors to shape remittance dynamics. Focusing on three dimensions: (1) remittance motivations; (2) remittance behaviors and patterns; and (3) financial inclusion outcomes—this study advances a novel quantitative approach that complements existing qualitative and ethnographic work. By uncovering complex and overlapping drivers of migrant remittances, the analysis contributes both methodologically and conceptually to the study of financial inclusion. It also offers practical insights for researchers and policymakers seeking to develop gender-responsive and intersectional financial systems that empower migrants in transnational contexts.

Literature review

Early migration theories, such as Ravenstein’s “laws of migration” (1885), Lewis’ “two-sector model” (1954), and Lee’s “push-pull” framework (1966), sought to explain migration primarily through economic or demographic factors, driving movement from one place to another. These approaches focus on migration as a linear process motivated by wage differentials, labor demand, and population pressures, emphasizing individual decision-making and rational choice. While influential, such frameworks often portray migration as a one-way movement from origin to destination and overlook the enduring connections migrants maintain with their home communities. In contrast, transnational migration theory provides a more dynamic lens, emphasizing the sustained social, economic and cultural ties that migrants develop and maintain across borders (Schiller et al., 1992, 1995). Rather than fully assimilating into their destination societies or severing ties with their countries of origin, migrants function as active agents who participate in and contribute to both, often forming new identities rooted in their transnational experiences. These ties are embedded in transnational social fields—dense networks of kinship, obligation, and exchange that span multiple national contexts. Such fields serve as both constraints and resources, shaping migrant’s daily lives, influencing their financial behaviors, cultural practices, and identities (Levitt and Schiller, 2004; Schiller et al., 1995).

A key component of transnationalism is economic transnationalism, where migrants engage in financial activities such as remittances and entrepreneurship to maintain their cross-border ties. These transactions are not solely economic acts but also moral and affective practices through which migrants negotiate intergenerational reciprocity, care obligations, and social status. Remittances, which serve as a vital source of income for many households and act as a driver of development in origin communities, are influenced by diverse factors such as migrants’ income levels, education, and familial structure, but also by cultural expectations and gendered roles (Ratha, 2005). They function as intertemporal contracts between migrants and their families, enabling households to share risk, invest in futures, and maintain social ties across distance. Beyond individual remittances, transnational entrepreneurship enables migrants to leverage opportunities in both local and international markets by establishing businesses or investments, facilitating personal economic advancement while stimulating development in both home and host countries (Portes et al., 2002).

This perspective reframes remittances as part of a moral economy—a system where social relationships govern economic practices and where financial flows are guided not only by utility or profit, but by notions of duty, reciprocity, and trust. These moral economies are gendered; women and men may be subject to different expectations, norms, and constraints in how they send, receive, or manage money, reflecting broader structures of patriarchy, migration regimes, and labor segmentation.

The concept of social remittances broadens the scope to include the transfer of ideas, norms, and practices that migrants bring back to their countries of origin (Levitt, 1998). These intangible flows can have a profound impact on political, economic, and social change in migrant-sending countries. For instance, Levitt and Lamba-Nieves (2011) highlight how Dominican migrant remittances were used over 20 years to transform community institutions, foster civic engagement, and strengthen social ties. Circular and return migration further illustrate the iterative nature of transnationalism, as migrants move between home and host countries, continuously renegotiating their roles within transnational families and economies (Massey et al., 1998).

Gender is a critical dimension of labor migration and remittance practices, influencing motivations, behaviors, and outcomes. Numerous studies revealed that male and female migrants often have different motivations for sending remittances, often shaped by broader gender roles in their home and host countries. Many find that female migrants tend to be driven by altruistic motives, such as close family ties, concern for family welfare, and a sense of obligation toward the family (Khamkhom and Jampaklay, 2020; Orozco et al., 2006; Vanwey, 2004). Gendered expectations often frame mothers as selfless caregivers, prioritizing familial well-being in their decisions about resource allocation (Abrego, 2009; Osaki, 1999).

However, gendered remittance behaviors are not fixed. Studies show that migration can open up new forms of financial agency for women. Tacoli’s (1999) study of Filipino labor migrants highlights how spatial distance and increased financial independence enable women to pursue self-interested goals, while Khumya (2015) illustrates how infrastructure development in the Mekong Sub-Region has opened economic opportunities for young women, challenging traditional norms. These examples reflect the evolving nature of gender norms, especially as women navigate complex transnational expectations and opportunities.

Gendered remittance patterns also reflect broader structural inequalities in the global labor market. While men typically remit larger absolute amounts, often a function of gendered wage gaps, women remit a higher proportion of their earnings and do so more frequently (Petrozziello, 2013; Posel, 2001; Rahman and Fee, 2009; Vanwey, 2004). Women also tend to allocate a greater portion of their remittances toward basic household needs and daily consumption, while men often direct funds to investments or business ventures (De La Cruz, 1995; Orozco et al., 2006). These patterns are shaped by gendered divisions of labor and occupational segregation. Women account for nearly half of all international migrants, but are often concentrated in largely informal, “feminized” sectors like domestic and care work (International Organization for Migration (IOM), 2025).

Importantly, gender does not operate in isolation. As Kimberlé Crenshaw (1989) first articulated, intersectionality describes how multiple forms of marginalization—such as race, class, and sexuality—interact to shape the experience of women (Cooper, 2016). Collins and Bilge (2016) similarly emphasize that social inequality is not structured along a single axis but emerges through interlocking systems of power. Understanding remittances through this lens allows for a more nuanced analysis of how financial opportunities and behaviors are shaped.

An emerging body of research explores the transformative potential of women’s remittances. By remitting, women may experience increased self-esteem and influence within their families and communities, challenging traditional gender roles and norms (Bhadra, 2007; Lopez-Ekra et al., 2011). Momsen (2010) frames empowerment as part of a participatory development process, emphasizing how remittances can contribute to increased financial autonomy and decision-making power for women. Thus, gender should not be understood as a fixed category, but as a fluid social relation that is actively produced and reshaped through migrants’ transnational economic practices.

Building on this relational perspective, understanding the motivations driving migrant remittances has long been central to migration and development studies. Traditionally, researchers have identified and categorized two primary motivations: Altruism and self-interest, with many frameworks now emphasizing their complex and overlapping nature. Lucas and Stark (1985) introduced an altruism-to-self-interest continuum, where migrants are categorized as altruistic if their remittances are driven by a sense of duty, responsibility, and care for their families and communities. These migrants prioritize the financial well-being of their families, desiring to improve education, healthcare, and the quality of life of their family or community members. In contrast, self-interest-driven remittances are viewed as a means to further the migrant’s own aspirations, such as acquiring assets, inheritance, building capital, or enhancing social prestige.

Increasingly, scholars have recognized that remittance motivations often blend. However, these elements, in a form category, are rarely mutually exclusive. Lucas and Stark (1985) introduced the concept of “tempered altruism” or “enlightened self-interest” (Czaika and Spray, 2013; Lucas and Stark, 1985) and most contemporary frameworks acknowledge such a spectrum or continuum between the two. In this intermediate form view, remittances can be interpreted as “part of intertemporal, mutually beneficial, contractual arrangements between migrants and the family of origin” (Carling, 2008). Migrants may thus view remittances as neither entirely selfless nor purely strategic, but as embedded in a moral economy of reciprocity, obligation, and long-term expectations. Portes et al. (2002) and Orozco (2017) extend this interpretation by framing remittances as an action going social contract, expressions of economic reciprocity—fulfilling that not only meet familial needs while strengthening but also reinforce migrants’ emotional ties and enhance their own social recognition (Orozco, 2017; Portes et al., 2002). This dual role reflects not only financial support but also an ongoing social contract within transnational networks.

More recent research has emphasized that motivations are dynamic and contingent, shaped by evolving household needs, migration trajectories, and sociopolitical contexts. Withanalage and Kulendran (2020), for example, explore how motivations can shift from self-interest to altruism over time, while Osili (2007) highlights how factors such as family welfare, investment opportunities, and return migration considerations influence these motivations, further complicating the continuum. These decisions are thus rarely made in isolation, but are negotiated within familial structures and shaped by expectations around gender, age, and kinship roles.

While the altruism to self-interest continuum remains a useful heuristic, this study approaches remittance motivations as socially embedded, gendered, and context-dependent. By analyzing remitting patterns among migrants in Japan, this research explores how migrants navigate familial expectations, structural constraints, and personal aspirations through financial transfers. The findings complicate binary models of motivation and instead reveal the layered and negotiated nature of remittance practices within transnational households.

Japan’s unique migration regime presents a valuable site for analyzing such gendered remittance practices. Historically restrictive in its immigration policies, a rapidly aging population and shrinking workforce have necessitated gradual policy shifts. These include expanded labor entry pathways such as the Technical Intern Training Program and the Specified Skilled Worker scheme, which channel migrants into sectors like industrial labor, food processing and elder care (Nakamura and Suzuki, 2024). These roles are also heavily gendered—since the 1980s, Southeast Asian women have migrated to Japan in significant numbers, initially occupying roles in the nighttime entertainment sector and more recently in caregiving and domestic labor—industries vital to addressing Japan’s demographic challenges (Koido, 2021).

Despite these deficits, Japan continues to favor short-term migration over long-term settlement, with migrants primarily coming under temporary visa schemes and facing limited access to long-term integration, social protection, or upward mobility (Nakamura and Suzuki, 2024; Oishi, 2012). At the same time, public and political discourse surrounding immigration has grown increasingly polarized. Recent electoral gains by nationalist parties and the adoption of more restrictive rhetoric by mainstream political actors reflect rising anti-foreigner sentiment amid economic insecurity and demographic decline (Associated Press, 2025). This discursive shift has been accompanied by stricter immigration and security policies, including proposed increase in visa and immigration fees (Mainichi Japan, 2025), tougher enforcement targeting non-compliance with public health insurance and pension contributions (NHK World Japan, 2025), and accelerated deportation initiatives such as the “Zero Illegal Foreign Residents Plan for the Safety and Security of People in Japan” (Immigration Services Agency, 2025).

Notwithstanding this shift in political climate, structural indicators point to a deepening reliance on migrant labor. In 2024, the number of foreign workers in Japan hit a record of 2.3 million, an increase of 12.4% year-on-year, while the number of companies employing foreign workers reached its own record high, rising 7.3% to over 300,000 workers (Ministry of Health, Labour and Welfare, 2025). Projections suggest that Japan will require between 4.2 million foreign workers by 2030 and up to 6.7 million by 2040 to sustain medium-growth scenarios, implying annual inflows well above recent historical levels (JICA, 2022). The divergence between increasingly tense political narratives and persistent labor market dependence further reinforces the precarious positioning of migrants within Japan’s political economy.

Taken together, these patterns highlight the dual role of migration in meeting Japan’s labor needs while offering economic opportunities for foreigners, including for women from countries with significant financial inclusion gender disparities (Marquardt and Ikeda, 2022). Japan’s efforts to reconcile its labor demands with policies that enhance migrants’ economic agency and skill acquisition—however partial or uneven—present a valuable framework for examining remittances as instruments of developmental and social transformation.

Research design

Data for this study were collected via an original survey conducted between October 2022 and February 2023, yielding 75 responses from income-earning foreign residents representing 37 nationalities. Respondents were recruited using a non-probability sampling strategy that combined purposive outreach through community-based migrant-serving organizations with recruitment via a professional survey company. Principal Component Analysis (PCA) was then performed to uncover underlying structures in the data and identify latent factors to explain the variance in remittance behaviors among different migrant groups.

An original survey was conducted to collect data on the remittance behavior of migrants through a gender lens. The primary aim was to assess gender-based distinctions in motivations, patterns, and financial inclusion-related outcomes of remittances sent by migrants in Japan. A structured questionnaire was designed and reviewed by the Kyoto University Graduate School of Advanced Integrated Studies in Human Survivability Ethics Committee. 1 The survey was prefaced with information on the purpose of the study and participants were required to provide informed consent before continuing with the questionnaire. The questionnaire is made up of three sections.

The first section focuses on the demographic profile of the migrants, including gender, age, nationality, education, and visa type. Additionally, we delve into family structure, investigating the presence of a spouse, children, or parents and whether these family members reside in Japan or the migrant’s home country. As the presence of family members in the home country often acts as a strong incentive to remit funds, this section provides essential context to understand the motivations driving remittance behaviors.

The second section pertains to the economic dimensions of migrant’s lives, exploring income, and spending patterns. This includes average monthly earnings, monthly savings, and changes in the use of financial services since migrating to Japan, such as internet shopping, online payments, savings, insurance, and investment. To gauge altruism levels, we draw inspiration from Dahlberg’s (2005) investigation into the spending patterns of garment workers in Cambodia and ask how respondents would allocate a one-time bonus if it were left up to their discretion. To explore gender differences in financial resilience, we ask about the ability to come up with significant funds of Japanese Yen (JPY) 300,000 (approximately United States Dollar (USD) 1,900) in case of an emergency. This question and amount were inspired by the World Bank’s Global Findex survey, which asked about the ability to come up with emergency money roughly equivalent to 5% of gross national income (Ansar et al., 2022). Respondents were asked to choose either the source of their emergency funds or select “not possible to raise money.”

The third section centers on remittance-related aspects, covering average remittance amount and frequency, sending channels, recipient accounts, and the purpose of remitted funds. We ask whether the remitted funds are spent toward family consumption, investment, debt repayment and/or savings and which household member makes the decisions regarding money usage. To further explore the social dynamics that may influence remittance practices, respondents are asked about their family’s dependence on remittances and the family’s income level relative to their home country’s average. These inquiries allow us to account for the migrant’s socio-economic context at the national, household, and individual levels. The final questions relate to the difficulties faced in sending remittances and plans for money earned while in Japan.

The questionnaire was pre-tested for clarity on respondents of varying levels of Japanese, and the wording was adjusted under the guidance of Japanese language teachers with experience teaching migrants. Several dual-language surveys were created, with native speakers in English, Vietnamese, Chinese, Korean, and Indonesian consulted for translations to appear under the original beginner-level Japanese wording. These languages were selected based on their prevalence among migrants in Japan and cover the national language of 68.9% of foreign residents, according to FY2023 reports (Ministry of Justice Immigration Services Agency, 2023). Additionally, these languages align with our regions of interest as outlined in the introduction.

This study focused on income-earning migrants residing in Japan. Anonymized data collection was conducted in two waves over 4-month periods from October 2022 to February 2023, employing a purposive sampling strategy combining community-based outreach and professional online survey recruitment. In the initial wave, conducted from October to December 2022, we collaborated with a network of 23 Japanese language schools in the Kyoto region and engaged cultural organizations, community centers, migration-related non-profit organizations, and foreign business associations in the Kansai region. These organizations were first approached with detailed information about our survey. Those organizations consenting to participate were provided with flyers, explanatory materials, and a link to an online questionnaire to disseminate through their networks. These institutions supported survey dissemination both online and through in-person events, resulting in completion from 38 respondents. Participation was voluntary and based on self-selection. The second wave, conducted from 14 February to 17 February 2023, was facilitated by a professional survey company using an online panel and targeted potential respondents who met our inclusion criteria of being income-earning foreign residents in Japan. The company fielded 240 survey responses, of which we could verify the foreign nationality of 85 respondents.

To ensure the quality and integrity of the dataset, several data-cleaning steps were implemented. First, any responses containing random characters, nonsensical entries, or blanks were excluded to maintain data quality. Second, a minimum monthly income threshold of JP¥10,000 (approximately US$65) was applied to filter out individuals whose reported income was too low for meaningful analysis of remittance and expenditure patterns. Third, one outlier representing a disproportionately high-income earner was removed to prevent skewed trends in the analysis. Finally, we removed the single non-binary respondent, while the initial survey design included an option for respondents to identify as “male,” “female” or “other,” only one respondent identified as non-binary. As PCA requires multiple observations to meaningfully detect patterns across subgroups, the inclusion of the single non-binary case would not have supported an interpretable analysis.

Descriptive statistics.

To account for the diverse origins of the respondents, their countries of origin were classified into advanced and emerging economies following the International Monetary Fund (IMF)’s country classification (IMF, 2023). Likewise, visa types were categorized into low, medium, and high skill levels, based on the Ministry of Foreign Affairs of Japan (MoFA)’s classifications of “General Visa,” “Working Visa” and “High Skilled Professional Visa” (MoFA, 2023).

This study integrates Principal Component Analysis (PCA), a multivariate statistical technique commonly used to identify underlying patterns within a dataset. PCA allows us to reduce the dimensionality of data by transforming a wide range of possibly correlated variables into a smaller set of linearly uncorrelated variables called “Principal Components” (PCs). Each PC represents a unique combination of the original variables and is ordered based on its ability to explain data variance, with the first PC explaining the most variance in the data and successive PCs explaining less. Studies commonly retain only the first few PCs, as these typically capture the majority of the variance in the data. PCA helps identify patterns by grouping similar samples and highlighting variables that distinguish different sample groups.

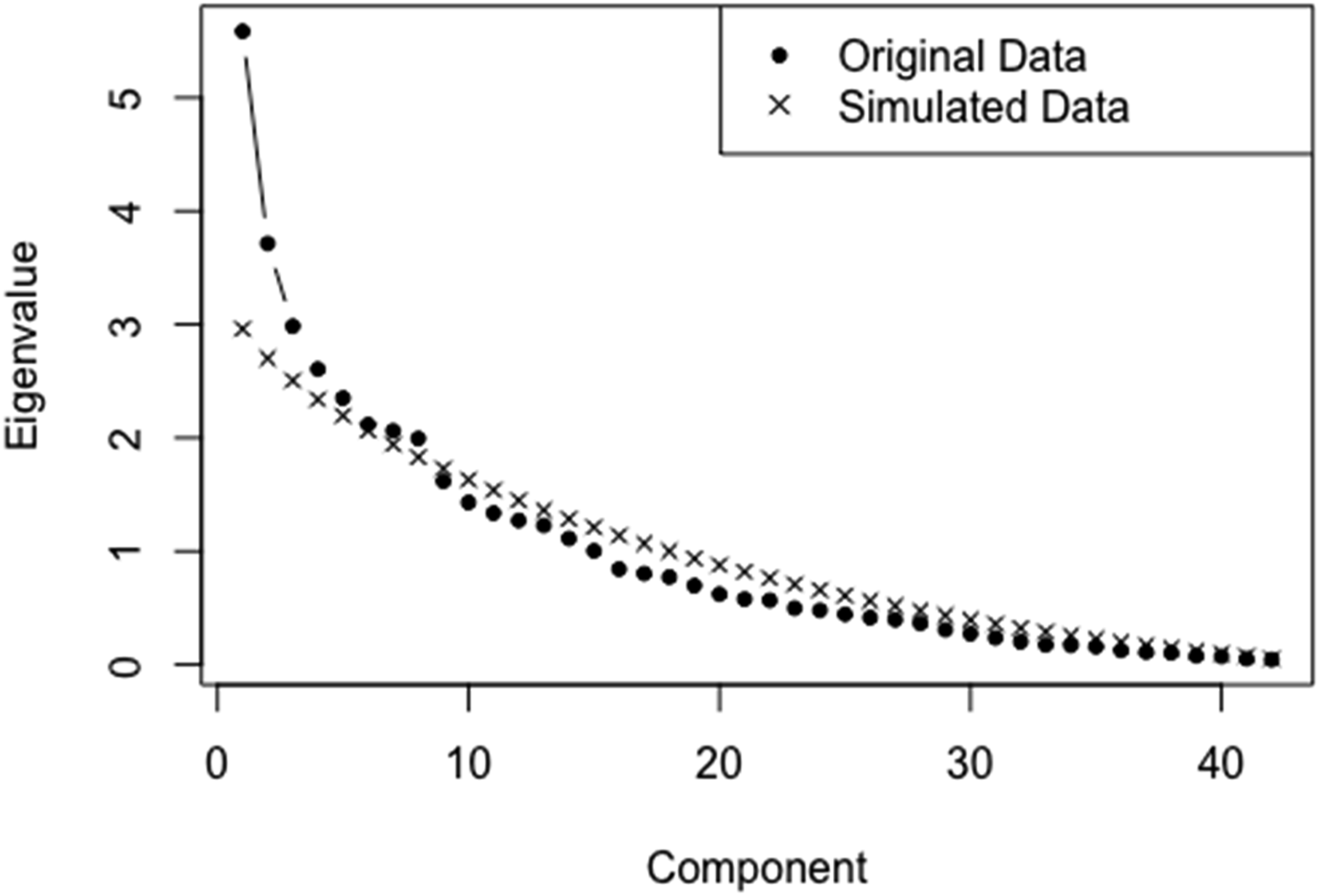

We employed parallel analysis, a widely accepted technique for determining the optimal number of components to retain (Franklin et al., 1995). This technique compares the eigenvalues derived from the original data with those obtained from a set of randomly generated datasets. The random datasets were generated through permutation to preserve the structure of the original data. The process was iterated 1000 times to ensure statistical rigor, and the eigenvalues derived from the average of the simulated data were then compared to the eigenvalues obtained from the original data. Components were retained when the observed eigenvalues exceeded the corresponding simulated eigenvalues. In total, eight components were retained for further analysis.

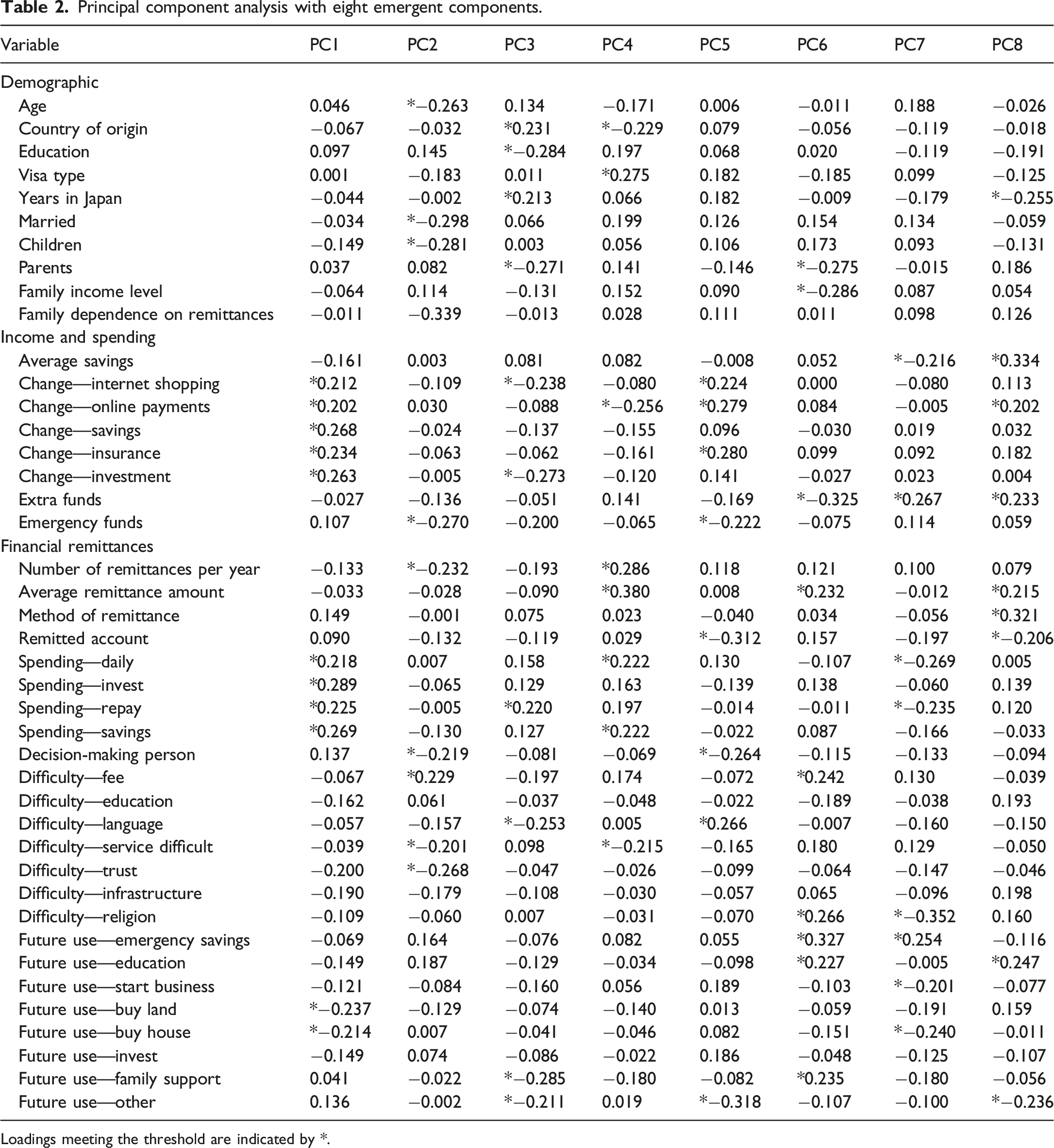

To interpret these eight components, the variable weights (or loadings) were calculated. Loadings provide information on the contribution of an observed variable to the retained component. Each loading is calculated by taking the square root of the associated eigenvalue and multiplying it by the corresponding element of the eigenvector for the variable. Higher loadings indicate a stronger relationship, while lower loadings suggest a weaker relationship. The loadings were standardized, and a loading threshold of |0.2| was set to identify the most influential contributing variables in each PC. By identifying these influential variables, we can interpret the thematic profile represented by each PC.

To examine gender-based disparities within the PCs, we computed the loadings for each respondent and compared the mean contributions of male and female respondents to each variable. The percent change of male and female contributions was calculated and standardized using z-scores. A threshold of |0.1| was applied to identify significant gender differences. This method allows us to discern which PCs exhibit the most pronounced gender disparities, and more critically, to pinpoint the variables within the PCs that contribute most to these differences. By evaluating how the contributions of male and female respondents differ across variables, we gain insight into the gendered dynamics of remittance practices in our sample.

Results

A covariance matrix for the first observed variables was formed and the eigenvalues were computed, yielding an initial set of 43 Principal Components. Parallel analysis determined that the first eight PCs had eigenvalues higher than those obtained from the random data. We therefore retained these eight PCs, accounting for 55.75% of the total data variance (see Figure 1). Eigenvalue comparison.

Principal component analysis with eight emergent components.

Loadings meeting the threshold are indicated by *.

PC1: Financially included and active

The first component represents individuals whose migration to Japan has resulted in changes to their financial habits. These individuals remit funds actively for current and future needs. A particular focus on savings and investments in the short term is apparent, with an intention to accrue assets such as land and housing in the future.

PC2: Not financially included, struggling to support family

This component highlights individuals who face challenges in both supporting their families and accessing remittance services. It is driven by family factors, such as the presence of a spouse and children and the family’s heavy reliance on remittances. Difficulties include a lack of trust in remittance services, high fees, and challenges in navigating these services.

PC3: Future planning for family, integration in Japan

This component has a focus on considerations of future family support, as well as the role of parents and education level. Variables about the level of integration in Japan are also significant, such as the presence of a language barrier and the number of years spent in Japan.

PC4: Consistent but basic remittance usage

This component suggests a subgroup characterized by specific sending patterns, with remittance amount, number of remittances, changes to online payment habits and usage toward basic financial habits (daily necessities and savings) featuring prominently. Demographic background, such as the development level of their country of origin and the skill level of the visa type, is also significant.

PC5: Decision-making and financial autonomy

A driving theme in this component is the autonomy over remittance funds. While these migrants exhibit greater financial inclusion through sophisticated services like insurance, online payments, and internet shopping, they seem to have limited agency over how their remitted funds are used. Variables related to whose account receives the funds and decision-making on their use are significant here.

PC6: Building security for the family

This component exhibits an inclination to save for emergencies, navigate family income dynamics and reconcile cultural or religious restrictions. Variables relating to future stability (emergency savings, family support, and education) and emphasis on family (family income group, presence of parents, and the intention to support family in the future) indicate a distinct priority to build security for the family unit.

PC7: Future-oriented with loans

This component reflects migrants who are comfortable with financial obligations and loans and prioritize asset-building. Current spending is focused on daily necessities and loan repayments, but there are long-term plans to buy a house and start a business—activities that may involve further reliance on loans.

PC8: Saving for future education

In addition to average monthly savings being a key variable, this component has a marked emphasis on technical aspects of remittance, including method of remittance, amount, and intended account. The focus on saving and making remittances could be explained by the intention to allocate the funds towards educational pursuits in the future.

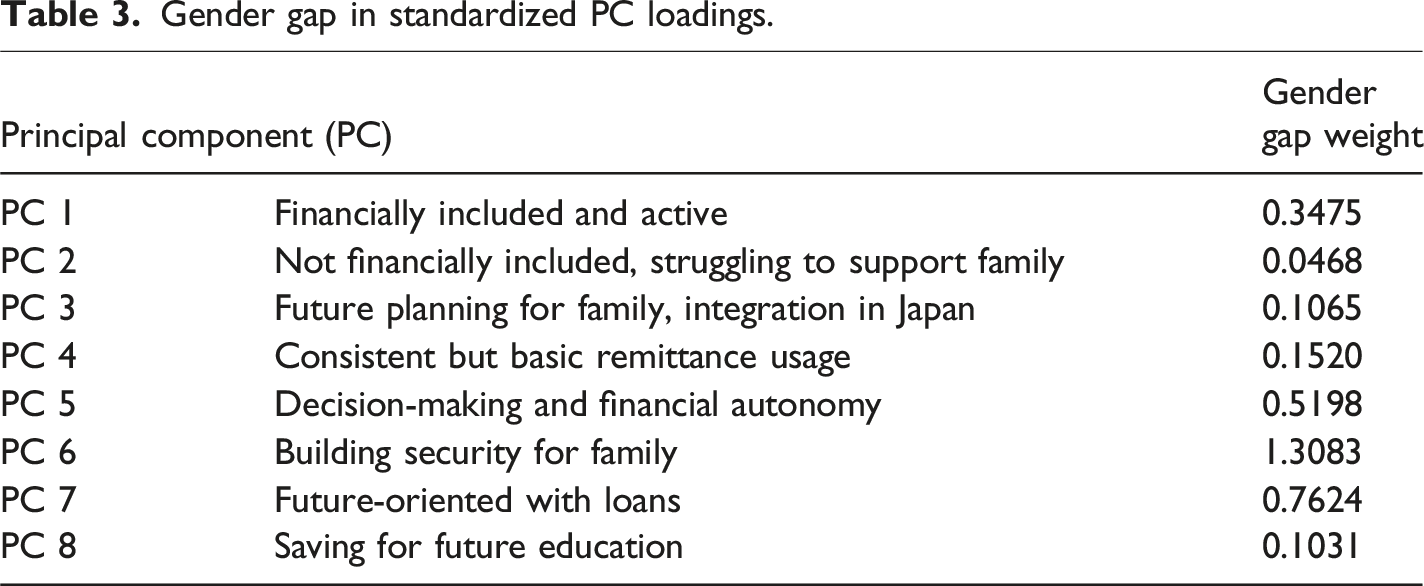

Gender gap in standardized PC loadings.

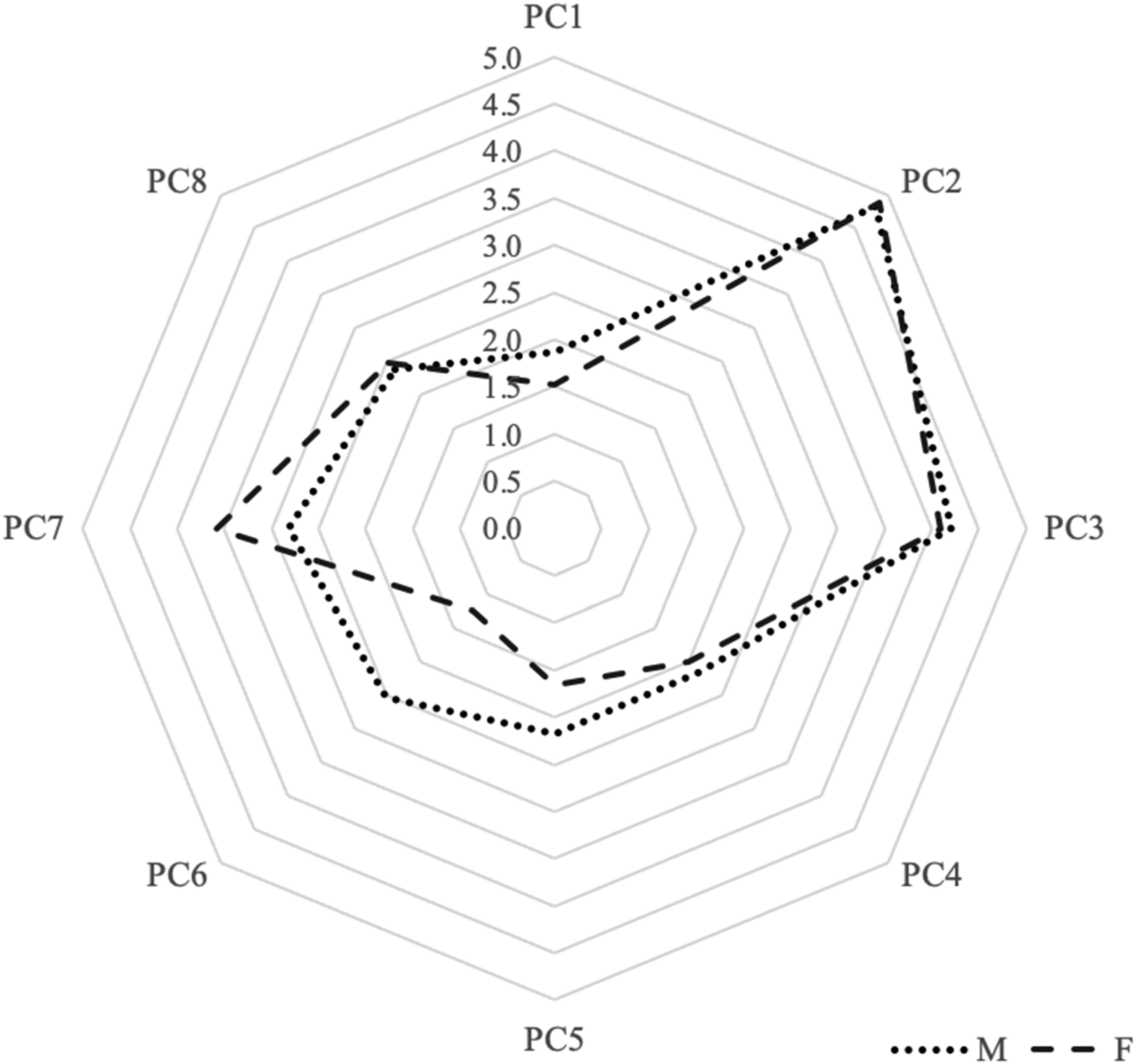

Contribution to each PC.

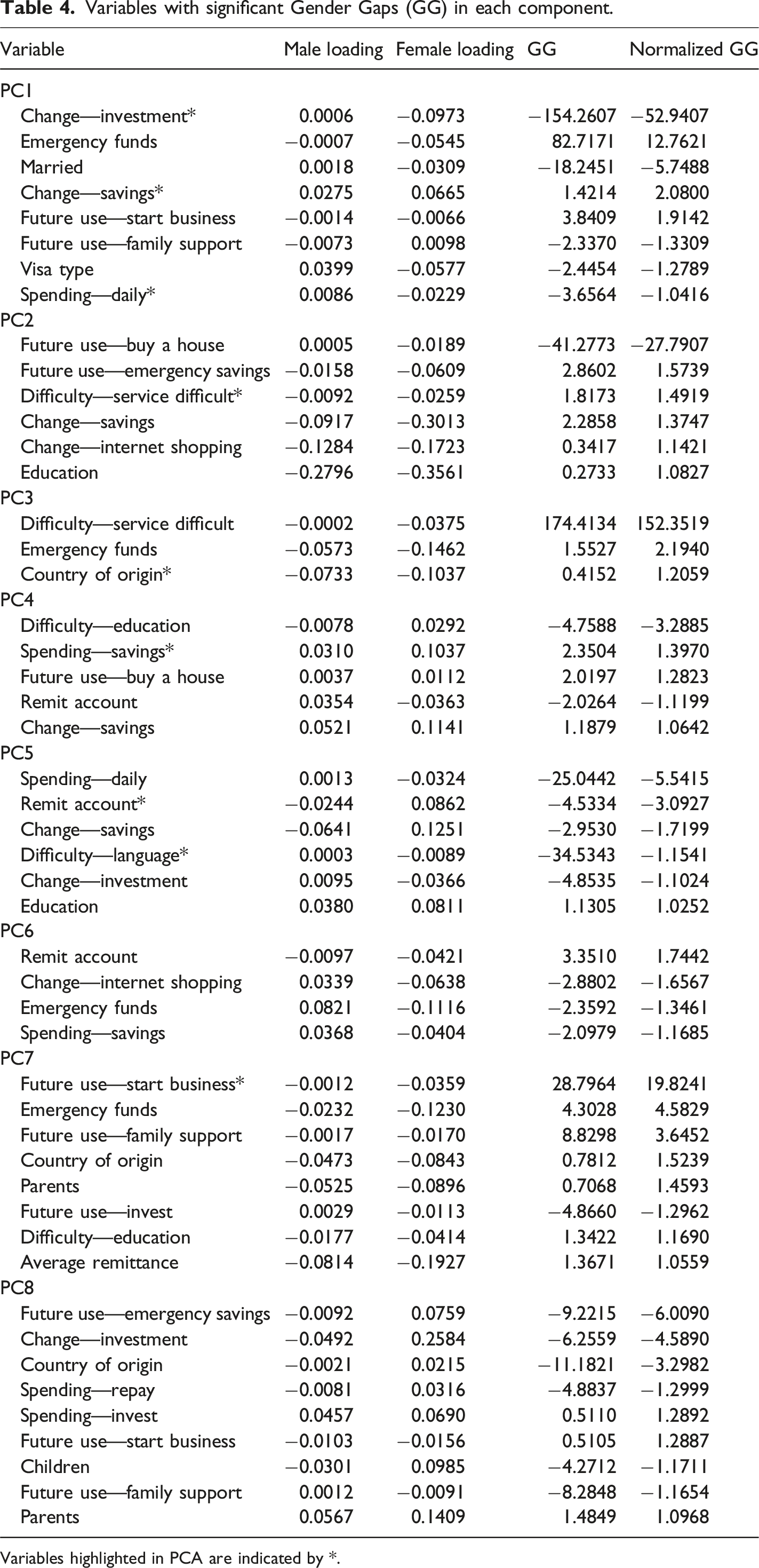

Variables with significant Gender Gaps (GG) in each component.

Variables highlighted in PCA are indicated by *.

In PC1 (Financially Included and Active), the gender gap primarily stemmed from changes in investment and savings behaviors, with female migrants displaying a more pronounced shift. Additionally, female migrants had a higher propensity to allocate remittances toward the support of daily necessities for their families back home. In PC2 (Not Financially Included, Struggling to Support Family, both male and female migrants encountered difficulties navigating remittance services, but women faced more significant challenges, creating a gender disparity. PC3 (Future Planning for Family, Integration in Japan) indicated a gap associated with the development classification of the country of origin, with this difference being more significant for female migrants. In PC4 (Consistent but Basic Remittance Usage), female migrants exhibited a higher inclination to use remittances toward savings. PC5 (Decision-making and Financial Autonomy) highlighted differences in remittance account preferences between male and female migrants, as well as the heightened language barriers faced by female migrants. In PC7 (Future-Oriented with Loans), a gender gap emerged in the intention to use remittance funds for starting a business in the future, with female migrants demonstrating a greater inclination. In contrast, PC6 (Building Security for the Family) and PC8 (Saving for Future Education) did not exhibit any discernible gender gap.

Discussion

Drawing on intersectional and transnational frameworks, we seek to move beyond binary assumptions about altruism and gender by applying PCA to explore how remittance practices emerge from complex and overlapping social positions. While our study is limited in scale and does not incorporate qualitative data, our use of PCA offers a novel contribution by revealing latent patterns that traditional analyses may overlook, particularly in relation to intersecting axes of gender, financial inclusion, and family dependency.

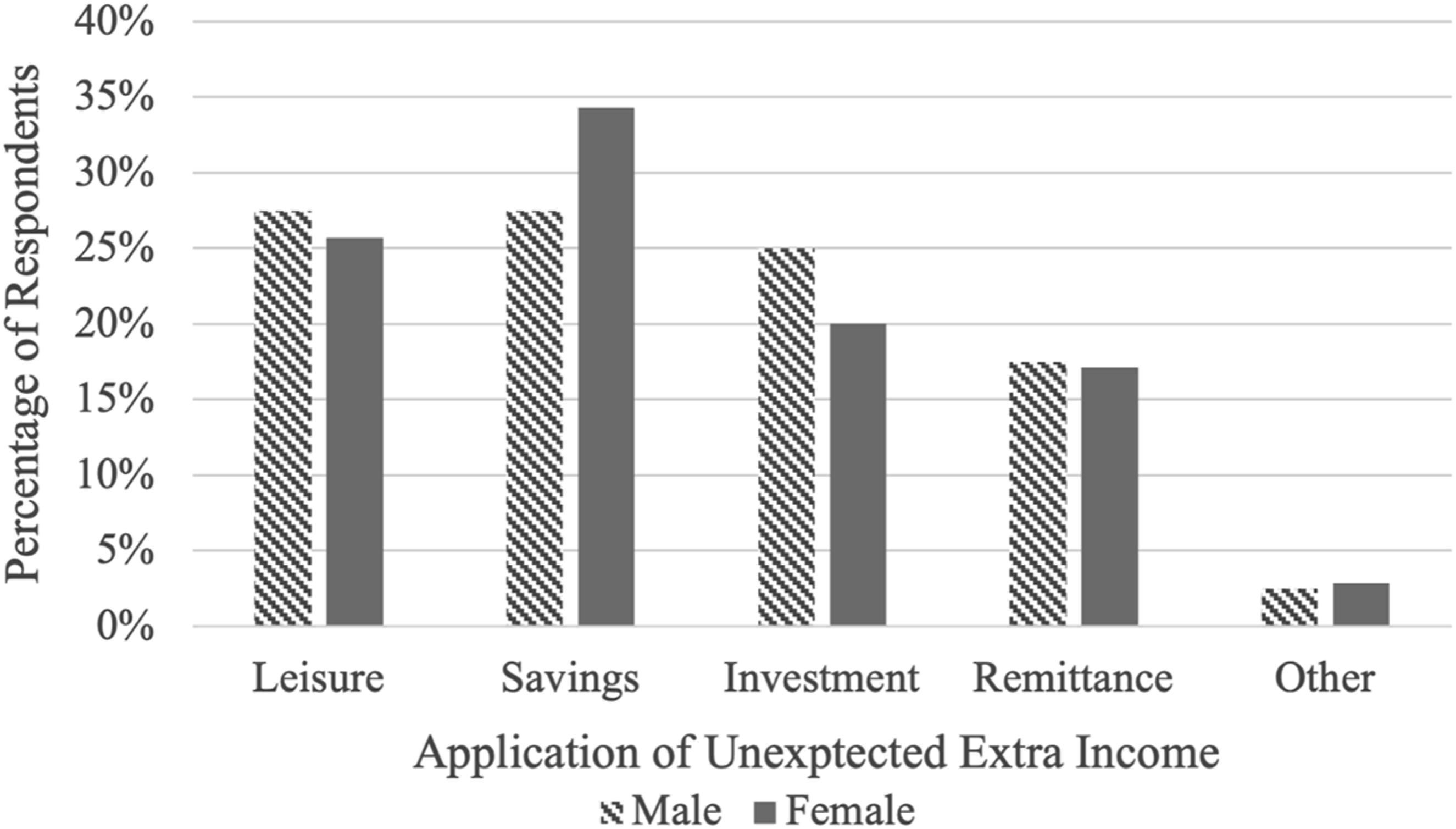

Our analysis of remittance motivations challenges conventional assumptions about gendered altruism. Previous scholarship often suggests that female migrants are more altruistic remitters, prioritizing caregiving, and household welfare. However, when asked how they would allocate an unexpected increase in income of JP¥ 30,000 or about US$ 190 (see Figure 3), male and female respondents were equally likely to remit the amount (17.5% and 17.1%, respectively). Inspired by Dahlberg’s (2005) method for assessing altruistic intent, we used this question as a proxy for discretionary remitting. The results suggest that remittance motivation, at least in discretionary cases, may not be strongly gendered. Application of extra funds.

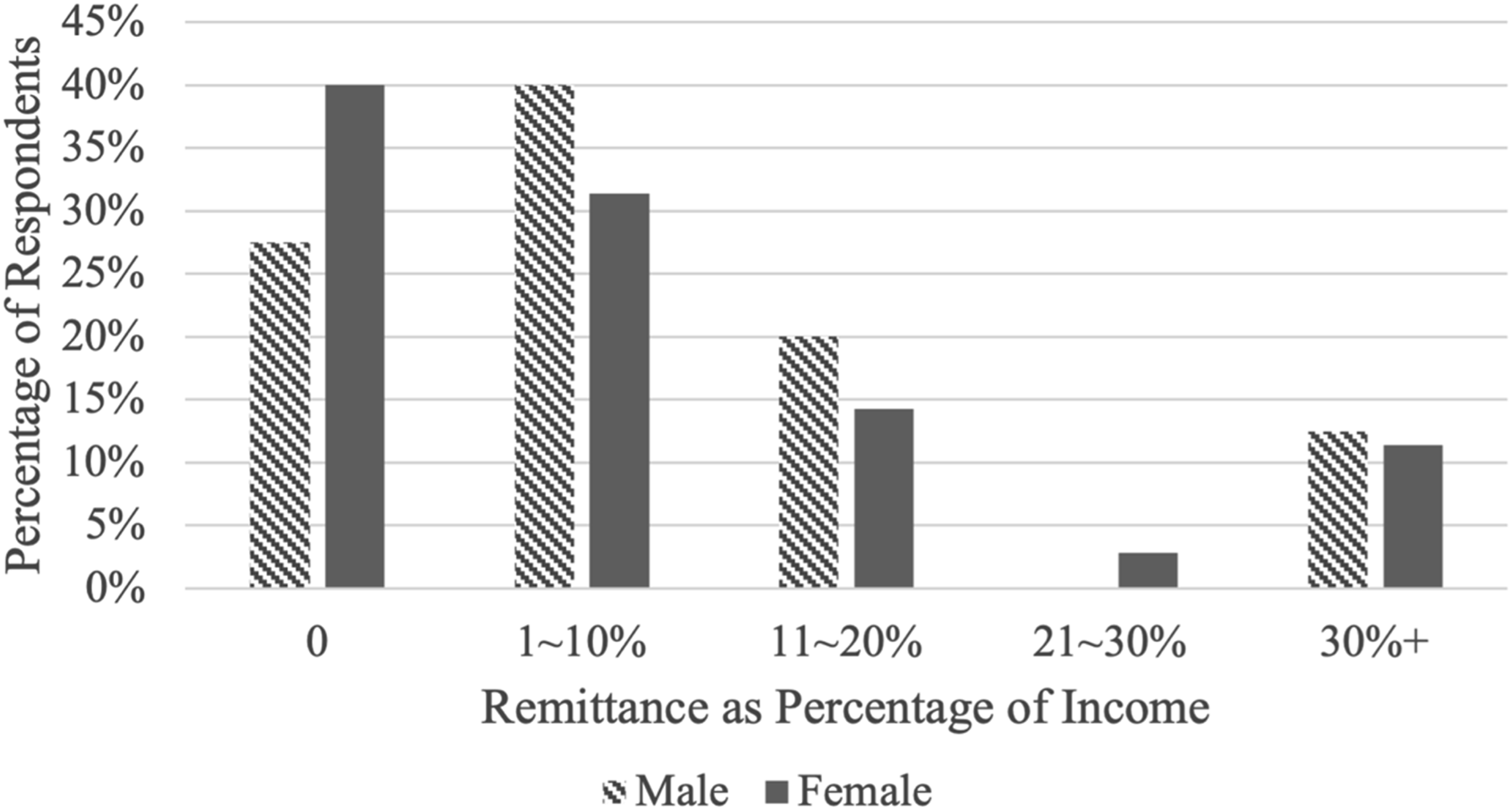

However, deeper gendered dynamics emerged in other aspects of remittance motivations. As Figure 4 illustrates, men remitted a higher proportion of their income, contradicting past findings that while women remit less, they remit a greater portion of their earnings (Petrozziello, 2013; Posel, 2001; Rahman and Fee, 2009; Vanwey, 2004). Furthermore, our study challenges concerns in prior scholarship that women remit smaller amounts more frequently, thereby incurring higher transaction-related fees (Orozco, 2017; Rodgers et al., 2020). Instead, our research consistently shows that male migrants remit more frequently and allocate a greater portion of their income to these transfers. While notable, this does not necessitate that women are less generous. These behaviors must be interpreted within transnational social fields (Schiller et al., 1992), which mediate financial decisions through familial expectations, income background and social positioning. In our sample, female migrants were more likely to come from middle-income families and to report lower familial dependence on remittances. This suggests that gendered remittance patterns are co-produced through socioeconomic differences and family roles—not gender alone. Average monthly remittance as a percentage of monthly income.

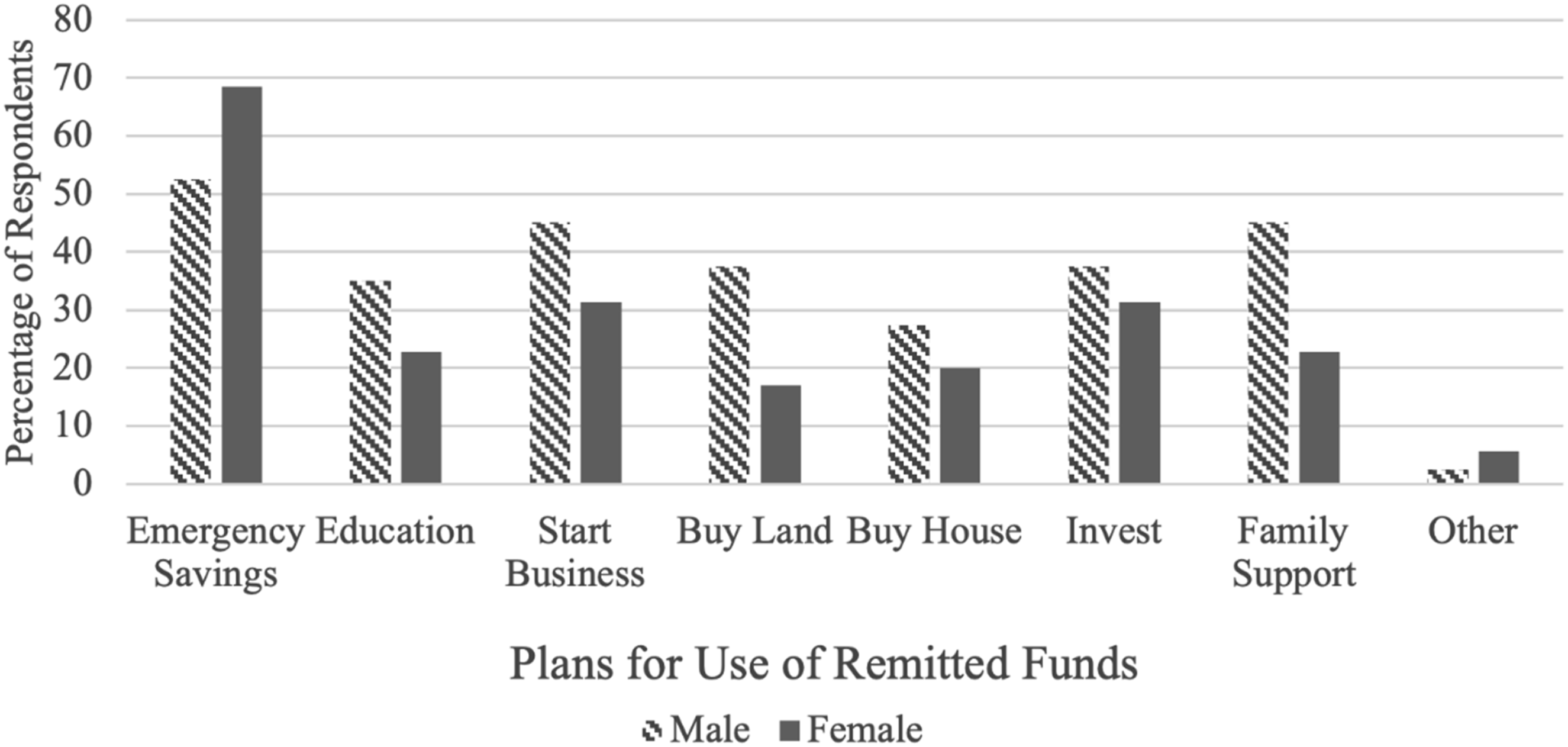

Financial priorities are also reflected in these intersecting structures. Women were more likely to save additional income (Male 27.5% to Female 34.2%) and prioritize remittances for emergencies (Male 52.5% to Female 68.5%), while men were more inclined to invest in education, land, or business (Male 35.0% to Female 22.8%; Male 45.0% to Female 31.4%; Male 37.5% to Female 17.1%) (Figure 5). These trends align with existing research showing that women emphasize financial security and household resilience (Dahlberg, 2005; De La Cruz, 1995). PCA components reinforce this distinction: PC4 (Consistent and Simple Remittance Usage) and PC1 “Financially Included and Active” suggest that women tend to prioritize building savings, while men favor investments that yield long-term economic benefits. Future use of remitted funds.

PCA further reveals nuances that challenge essentialist readings of gender. PC7 “Future-Oriented with Loans” identifies a subgroup of female migrants with loan experience who show a greater inclination to use funds for business development than their male counterparts. This finding not only complicates the assumption that self-interested remitting is a masculine trait, but also suggests a form of transnational entrepreneurship—the harnessing of economic opportunities across borders to benefit both themselves and their families or communities in their countries of origin (Portes et al., 2002). These entrepreneurial activities reinforce the transformative role of migrants as proactive agents driving socioeconomic development. It also demonstrates the financial agency of migrant women who, while operating within gendered labor structures, carve out strategic opportunities for long-term investment and personal autonomy.

These findings offer empirical support for the concept of “tempered altruism” (Lucas and Stark, 1985), whereby remittances are negotiated exchanges that balance familial obligation with individual goals. Yet they also highlight the limits of a simple altruism or self-interest continuum. For instance, male migrants appear to remit more often out of duty to meet daily needs, while female migrants—particularly those from more stable households—remit with a dual focus on security and future planning. These differences are not reducible to gender roles, but are shaped by how migrants are positioned within overlapping networks of family dependence, income status, and social expectation. PCA illustrates how migrants’ financial decisions are rarely driven by a single factor, and instead reflect how migrants negotiate obligations, aspirations, and constraints across multiple economic and relational dimensions. By revealing these latent patterns, our analysis contributes a novel methodological approach to the study of remittances and opens space for future research to link quantitative data with ethnographic insight in the analysis of financial agency.

Migration facilitates exposure to new financial landscapes, enabling migrants to adopt formal remittance channels and utilize diverse financial services such as savings, insurance, and investment. In this study, we find that migrants—both male and female—report increased usage of these services post-migration, reflecting an expansion of financial practices consistent with economic transnationalism. However, financial inclusion is not merely a matter of access. Drawing on intersectional frameworks, we argue that financial behaviors must be understood in terms of how migrants’ social positions, obligations and past experiences shape both the uptake and use of formal and informal financial systems.

Despite gains in usage, gendered disparities persist. Women in our sample reported greater difficulty navigating financial services than men (Male 12.5% to Female 24.2%). This is especially visible in PC2 “Not Financially Included, Struggling to Support Family,” a subgroup characterized by strong remittance obligations but limited financial integration. While barriers exist across genders, women appear more acutely affected, reflecting both systemic inequities and gendered norms around finance, digital literacy, and trust in institutions. Prior studies often attribute this gap to women’s lower financial literacy, but an intersectional approach reveals that gender interacts with other axes of marginality—such as legal precarity, employment in informal sectors, and caregiving burdens—to constrain women’s financial agency in compounding ways (Collins and Bilge, 2016; Crenshaw, 1989).

Interestingly, women’s pre-migration financial inclusion appears to mitigate some challenges. Female migrants were more likely than men to maintain consistent financial services usage post-migration, potentially reflecting a higher baseline of financial inclusion in their home countries. This supports a view of financial behaviors as situated within transnational social fields, where pre-migration experiences and host-country environments jointly shape migrant strategies (Schiller et al., 1992). Rather than adopting host-country practices wholesale, migrants adapt selectively and maintain elements of familiar systems while navigating new ones. These layered practices reflect relational inclusion based not simply on whether migrants have access, but on how they navigate systems based on trust, control, and obligation.

Our findings on emergency funding further support this relational view. Previous research has emphasized the ability (or lack thereof) to raise funds in the case of an emergency as a critical factor contributing to the global financial inclusion gender gap (Marquardt and Ikeda, 2022). Here, we find that women were more likely to rely on personal savings or support from kin in their country of origin—strategies that draw on moral economies of reciprocity and trust. These informal systems are not fallback options but integral tools for navigating risk, especially when formal systems are perceived as slow, costly, or exclusionary. At the same time, the near-universal use of formal remittance channels for international transfers indicates that migrants adopt a dual financial strategy, relying on formal systems for efficiency and informal networks for flexibility. This fluidity aligns with Massey’s (1998) notion of iterative transnationalism and highlights how migrants blend systems in ways that maximize both reliability and relational security.

PCA allows us to move beyond binary distinctions of “included” versus “excluded.” It surfaces patterns where financial hardship, usage difficulty, remittance pressure, and pre-migration experience coalesce in different ways. For example, some components show low inclusion but high remittance activity, suggesting that migrants may remain financially excluded in formal terms while still playing a central economic role within transnational households. These findings challenge narrow definitions of financial inclusion that equate usage with empowerment. They point instead to a need for intersectional and relational understandings of financial life, where inclusion is contingent on social networks, institutional constraints, and evolving obligations.

Remittance practices are not only economic transactions but also social actions with implications for empowerment and agency across transnational households. Our findings indicate that female migrants are more likely to remit to their mothers (Male 15.0% to Female 22.8%), whereas male migrants predominantly remit to their fathers (Male 25.0% to Female 2.8%). These gendered patterns extend to household decision-making: Female migrants more often report that their mothers manage the remitted funds (22.8%), while male migrants report their fathers holding this role (20.0%). These dynamics affirm previous studies showing that women tend to direct remittances to female kin (Rodgers et al., 2020), potentially reinforcing female roles as economic actors within the household.

PC5 “Decision Making and Financial Autonomy” captures this pattern, showing how women’s remittances are tied to financial decision-making by female relatives. This reflects not only material flows, but also the transmission of ideas, practices, and norms, or what Levitt (1998) terms social remittances. The concept of social remittances (Levitt, 1998) provides a valuable framework for exploring this dynamic. Beyond monetary transfers, migrants bring back ideas, practices and norms that can reinforce or challenge existing family and societal structures. Female migrants’ focus on savings and financial security, for example, may encourage changes in how financial resources are managed at the household level, fostering greater stability and resilience. The positioning of women in home countries as decision-makers may enable them to exercise greater economic agency. These changes suggest that migration and remittance practices contribute to relational empowerment, expanding not just individual autonomy but the collective agency of women within families and communities.

Financial empowerment must be understood as contextual and intersectional, shaped by migrants’ legal status, occupational roles, class background, and family configuration. For instance, female migrants with greater pre-migration financial inclusion or more stable visa categories may be better positioned to exercise agency through remittance choices. Likewise, empowerment does not always correlate with formal financial inclusion; in some cases, migrants with limited access to formal systems still influence economic decisions at home. PCA helps surface these complexities by revealing clusters where empowerment and constraint coexist.

These findings point to the importance of empowerment not as a fixed outcome of migration, but as an ongoing, negotiated process unfolding across transnational social fields (Schiller et al., 1992). Migrants navigate multiple systems of obligation and opportunity and their financial decisions reflect not only personal agency but also structural constraints and gendered expectations. Empowerment, in this sense, is not merely the ability to make choices, but the capacity to act within systems that enable or limit those choices.

At the same time, it is important to recognize that migrants’ financial strategies are shaped not only by individual goals or capabilities, but also by the structural features of the host environment. Japan’s migration regime, for example, is marked by temporary labor schemes and limited pathways to long-term settlement, which can constrain the extent to which migrants can engage in future-oriented financial planning. As Ullah et al. (2024) argue, practices of boundary-making and Othering reinforce migrants’ marginality by symbolically and materially excluding them from national belonging. These dynamics may interact with financial behaviors to shape trust, perceived permanence, and willingness to engage with formal systems.

These patterns point to several policy implications. First, remittances must be formally integrated into broader financial inclusion strategies at both national and international levels. This includes addressing structural barriers such as regulatory hurdles, limited identification options, and digital exclusion. Host countries should facilitate migrants’ access to banking through migrant-focused products like low-cost remittance services, mobile banking, microinsurance, and tailored savings tools. As our findings show, remittance motivations and financial behaviors can differ significantly by gender, financial literacy, and other key factors such as visa status or language ability. For example, temporary workers on short-term visas may prioritize simple low-cost transfers, while long-term residents might seek tools for local savings, credit-building, or investment. Financial services should reflect this diversity through flexible offerings tied to migrants’ goals and constraints. While some tailored services have been developed, such as expedited health insurance plans to cover Technical Trainees from the date they depart their home country (Japan International Trainee & Skilled Worker Cooperation Organization (JITCO), 2025), these remain limited in scope and are often contingent on the initiative of implementing organizations.

Migrant support services such as community centers, language schools, and job placement agencies can be leveraged as accessible spaces for promoting financial literacy, digital skills, and long-term financial planning. These institutions can help to bridge knowledge gaps and provide low-pressure environments to introduce formal services in ways that resonate with migrants’ lived realities.

Second, more attention should be paid to the informal financial practices that remain central to many migrants’ financial lives. Despite increased access to formal institutions, many still prefer to borrow from friends and family or participate in informal savings circles. While these informal strategies are often beyond the direct scope of institutional regulation, support organizations can play a valuable role in strengthening them. This includes providing financial education or digital literacy support in informal or community-based settings, which can help migrants use these tools more safely and strategically while building pathways toward formal inclusion.

Third, a gender-sensitive lens must be embedded across financial inclusion policies, but with greater attention to the diversity of women’s financial behaviors and goals. While our study confirms that many women migrants prioritize savings, it also highlights a range of financial orientations, including entrepreneurial motivations and future-oriented remittance strategies. These findings caution against overly simplistic assumptions that equate gender with altruistic behavior or risk aversion. Women’s financial needs and preferences are shaped by intersecting factors like visa status, employment conditions, household roles, and financial literacy. Future research that disaggregates women into meaningful subgroups—by migration status, occupation, or life cycle stage—can offer more precise insights into what gender-responsive financial products might look like in practice.

In the meantime, policymakers and service providers should ensure that women have access to the full spectrum of financial tools, including credit, insurance, and investment products. Designing for inclusion means not only expanding access, but also being attentive to how services are communicated, delivered, and supported. This includes offering flexible, secure tools that reflect women lived realities and building trust through culturally competent outreach. Moreover, given the observed pattern of women remitting to other women, who often become household decision-makers, gender-responsive strategies can generate empowerment spillovers across transnational networks, expanding the reach of financial inclusion beyond the individual remitter.

Adopting a financial health and wellness perspective strengthens this approach (Joo, 2008; Consumer Financial Protection Bureau (CFPB), 2015; Fan and Henager, 2022). Rather than solely on access or usage, financial inclusion should be evaluated by how effectively it supports migrants’ long-term security, adaptability, and upward mobility. The participants in our study had goals that were varied, from familial support to entrepreneurial plans, or educational investment. Financial products that reflect these diverse aspirations—such as goal-based savings accounts, portable credit histories, or flexible investment tools—can help build not just resilience, but economic autonomy.

In sum, this study calls for a shift in how remittances and financial empowerment are conceptualized in both research and policy. Financial decisions made by migrants are deeply embedded in transnational relationships and shaped by intersecting structures of opportunity and constraint. Effective financial inclusion must be relational, intersectional, and development-oriented, supporting migrants not only as remitters, but as agents of social and economic change.

Conclusion

This study investigates gendered remittance practices among migrants in Japan, focusing on remittance motivations, behavioral patterns, and financial inclusion outcomes. Unlike conventional surveys that target narrowly defined demographic groups, this research incorporates data from a diverse pool of migrants, capturing a diverse cross-section of migrant experiences within Japan’s evolving labor landscape. By employing Principal Component Analysis (PCA), we move beyond binary comparisons to reveal latent patterns in financial behaviors, identifying subgroups that both align with and challenge established assumptions about these practices.

Our findings challenge prevailing notions that portray women as primarily altruistic remitters. Male migrants in our sample remitted more frequently, allocated a greater share of their income to remittances, and were more motivated by familial support. Female migrants—particularly those characterized as financially included and future-oriented—displayed markedly self-interested and entrepreneurial motivations, traits traditionally associated with male remitters. Consistent with prior research, however, female migrants demonstrated a heightened emphasis on savings. These distinctions complicate conventional gendered narratives and highlight how motivations are shaped by intersecting influences of gender, socioeconomic status, financial literacy, and transnational obligations.

Financial inclusion, too, emerged as an uneven outcome of migration. While female migrants reported greater difficulty using financial services, they also displayed consistent engagement with formal financial tools. This paradox suggests that existing financial systems may not be fully designed with all users in mind and that many continue to engage despite barriers, rather than because their needs are being effectively met. This calls for financial services to identify and respond to the specific challenges women face, including through tailored products and support mechanisms. Gendered remittance channels, such as the strong tendency for women to send money to other women, particularly mothers, also reveal potential pathways for transnational empowerment. Female recipients were shown to often take on decision-making roles in managing remitted funds, which may shift household dynamics and redistribute financial agency. These relational patterns illustrate how remittances are embedded in gendered social networks and can initiate ripple effects that extend beyond the migrant themselves, influencing power structures and economic participation within families and communities back home.

Our study affirms that remittance behaviors cannot be reduced to singular explanations like altruism or gender norms. Migrants inhabit multiple, intersecting identities and navigate diverse financial realities. To uncover these complexities, we use PCA not only as a statistical reduction tool but as an intersectional analytic method—one that reveals how combinations of factors such as visa status, employment stability, household obligations, and remittance patterns interact in meaningful ways. By identifying latent subgroups that would otherwise be obscured in aggregate analysis, PCA provides a way to visualize structural inequalities and behavioral clustering at the margins.

While PCA allowed us to detect these underlying patterns, it also opens up new possibilities for mixed-methods research. The clusters and themes identified here could be deepened through qualitative work, particularly interviews or participatory methods that better capture migrants’ lived experiences and evolving financial strategies. In this way, PCA may serve as a methodological bridge between large-scale quantitative data and the context-rich insights of ethnographic or narrative approaches. However, the modest sample size of this study limits the generalizability of findings and constrains our ability to analyze differences by region or country of origin. While the survey included a question on gender identity, only one respondent identified as non-binary. Although we were unable to include their response in our PCA data, we acknowledge that this limits the study’s capacity to engage with the full spectrum of gender diversity. Future research would benefit from a larger and more representative dataset to support intersectional, comparative analysis across contexts.

Ultimately, this study adds to growing calls for more critical and intersectional approaches to remittance and financial inclusion research. Remittances are not just financial transactions, but are shaped by social norms, institutional barriers, and cross-border relationships. Understanding these dynamics is key to building financial systems that are not only accessible but also responsive to the diverse realities migrants face. By using PCA to surface hidden patterns in remittance behaviors, this study shows how quantitative methods can help identify structural inequalities and support more targeted, gender-sensitive financial inclusion strategies.

Footnotes

Acknowledgment

Many thanks to Wildan Ahmad Adani, Haiyi Liu, Fedor Myasoedov, Keiji Sakakibara, and Nguyễn Bích Trâm for their translations and insightful comments. The authors would like to express their gratitude to all of the respondents for their contribution to this research.

Ethical considerations

This study was approved by the Kyoto University Graduate School of Advanced Integrated Studies in Human Survivability Ethics Committee.

Consent to participate

Participants were presented with a survey disclaimer informing them of the study’s purpose, the anonymous nature of their responses, and data usage. By proceeding with the survey, participants indicated their understanding and consent to these terms. Responses were anonymized, and no personally identifiable information was collected.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.