Abstract

The high upfront cost of residential solar photovoltaic (PV) systems and unfavourable financial market conditions hinder their adoption in developing countries. This study evaluated the economic viability of loan-financed urban residential grid-tied solar PV systems with battery electric vehicle (BEV) charging, under Ghana's net billing scheme. The methodology integrates techno-economic simulation of a 10 kWp residential PV system using PV*SOL premium software with socio-economic data from the Ghana Living Standards Survey (GLSS7). Key performance indicators, including levelised cost of energy (LCOE), payback period, annual savings, EV travel cost, debt-to-income ratio, and residual household income, were assessed across Ghana's 16 administrative regions. The results show that LCOE ranges from 0.407 to 0.483 USD/kWh, substantially exceeding the national residential grid tariff. BEV travel costs under PV charging range from 0.082 to 0.091 USD/km, higher than those under grid-based charging. Payback periods range from 12.0 to 14.1 years. High interest rates and short repayment terms result in household debt-to-income ratios ranging from 0.54 to 3.03 and residual household incomes ranging from -USD 9105.32 to USD 5990.94, exceeding acceptable thresholds for most households in low-income regions. Only households in high-income regions demonstrate limited loan repayment capacity. The findings indicate that, under current commercial loan conditions, financing residential PV systems with integrated BEV charging is economically unattractive for most urban households, underscoring the need for concessional financing and improved policy support.

Introduction

The residential sector plays a pivotal role in the energy transition and decarbonisation of global economies.1,2,3,4 Due to the substantial size of this sector and its potential to increase the installed capacity of photovoltaic (PV) technology, residential PV systems have become a key component of governmental energy policies promoting the widespread adoption of renewable energy sources.5,6,7,8 Residential solar PV systems, however, face several economic challenges. Among these challenges, barriers such as high initial costs and unfavourable financial market conditions have impeded the deployment of PV in the sector.9,10,11 Thus, although solar energy is regarded as a renewable and sustainable alternative to fossil fuels, financial challenges do not favour its adoption in the residential sector, especially among low-income households.10,12,13

Although technical advancements in renewable energy technologies have been achieved, these alone are insufficient to meet the low-carbon emission goals of the energy transition. 14 However, financial and systemic change are pivotal to the energy transition.15,14,16 According to Roberts et al., 17 despite the benefits of PV investments, financial constraints can render PV installation unfeasible. Historically, due to the high costs of energy technologies and infrastructures, financial market conditions and access to capital have played essential roles in energy transitions. 18 Financial accessibility not only bridges the gap between availability and investment in the energy sector but also serves as a key enabler of the industry's growth. 19 It is therefore imperative that, given the urgency of climate change mitigation and fossil fuel depletion, financing become more continuous and balanced at both national and international levels to expedite the energy transition.20,21,16 In fact, it is argued that the prospect of the energy transition is no longer mainly about scientific and technological advancement but more about financing. 22 This implies that innovative financing is key to the deployment of solar PV. 11

Nonetheless, in many developing countries, renewable energy financing is a primary concern and a significant challenge. 22 Many vulnerable households struggle to access financing for solar projects, limiting their widespread adoption in developing regions. 10 For instance, Mboumboue and Njomo 13 identified financial barriers, in addition to policy and legal barriers, as the three main barriers to the deployment of renewables in developing countries. In a related study, the lack of access to finance and the unaffordable cost of finance were identified as key challenges to the adoption of renewable energy in developing countries. 23 The study found that factors such as low economic status, a small domestic financial market, and the small size of renewable energy projects made it economically unviable for private investors to invest in these projects. Donastorg et al. 24 investigated trends in the financial area of renewable investment. It was discovered that financial issues remained a major barrier to implementing renewable energy projects. The study highlighted the lack of investment loans, the perceived risk of renewable energy investments, and the lack of a financial guarantor among the financial handicaps to renewable energy deployment.

The work of Roberts et al. 17 identified several challenges related to financing, governance, knowledge, and regulation for solar PV in multi-unit residential buildings. Tamasiga et al. 11 reported that high initial cost is a major impediment to small-scale renewable energy projects. Furthermore, the study revealed that financial challenges, interconnected with social, technological, and environmental factors, influenced the deployment of small-scale renewable energy technologies. Shi et al. 25 documented financial constraints as a major barrier, besides infrastructure, regulation, and participation, to the adoption of renewable energy technologies for sustainable growth. Likewise, Abdelrazik et al. 26 identified financial, human resource, environmental, and technological challenges as major barriers to the widespread adoption of solar PV. Salifou et al. 27 reported high investment costs, perceived risk, and the unavailability of financing as key financing barriers to solar energy projects.

The study by Saraji and Streimikiene 14 explored the challenges with the low-carbon energy transition towards sustainable energy development. Of the 17 challenges identified by the investigation, the most significant was the lack of financial investment, followed by short-termism and reform. According to Fouquet and Pearson, 18 the lack of capital to finance renewable energy has been a major constraint to energy transitions. Other studies likewise identified funding as one of the biggest barriers to the energy transition and social innovation. 28 It has been pointed out that without collaborative, cross-sectoral, and international partnerships, financing for the development of energy projects will remain a major obstacle in low-income regions. 28

In this regard, although Africa has immense potential for solar energy generation and is considered to have the highest solar potential worldwide, accounting for 60% of the world's best solar resources, only 2% of its current capacity is generated from renewable sources. 29 Financing remains a significant barrier to the African PV market due to the high initial investment required and unfavourable economic conditions for renewable energy projects.26,30,29 For instance, studies show that Africa's current financial situation makes solar PV more expensive than other conventional energy sources. 26

Although there are several financing mechanisms for renewable energy projects, such as solar PV, 17 grants are the primary mechanism for these projects on the continent. 26 Specifically, it is estimated that 95% of these projects are funded through grants, 3% through loans, and less than 1% through private equity. 26 Regarding loans, limited availability for financing solar PV projects is primarily due to several factors. Notable among these factors are the perceived high risks and low returns associated with renewable energy investments.31,32 Financial institutions, such as banks, view solar PV financing as an emerging investment sector that deviates from their traditional focus on profit maximisation and risk minimisation. 33 For example, renewable energy projects generally require long-term loans, and many residential customers are seen by financial institutions as high-risk borrowers.34,35

Other factors, such as limited knowledge and experience among banks in financing solar energy projects on the continent, have contributed to their reluctance to support such initiatives.26,36,37 Several studies have highlighted a general bias among commercial banks against funding small-scale solar PV projects.38,33,39 For instance, the study by Saleh and Upham 33 revealed that standard banking procedures have led to a demographically skewed distribution of distributed generation systems, favouring the affluent sections of society. In Africa, the high investment risks associated with renewable energy projects compel investors to demand higher returns to compensate for these uncertainties.40,41 Consequently, financing renewable energy projects remains a primary concern and a significant challenge in Africa and several other developing countries. 22

Therefore, this study examines financing residential solar PV through loans in a typical developing African country, using Ghana as a case study. Ghana has favourable solar radiation for viable solar PV project development with average solar radiation of 4–6 kWh/m2/day and sunshine duration of 1800–3000 h per annum.42,43 In addition, the country has enacted several policies and laws to support the deployment of solar PV. Nevertheless, several barriers, including unfavourable financial market conditions for renewable energy projects, have contributed to the limited solar PV penetration in the country's energy portfolio, accounting for less than 1% of generation capacity.44,45,42

For instance, Boamah and Rothfuß 46 observed that few banks were willing to engage in solar PV financing, and those that did offered loans with high interest rates ranging from 29% to 35%.47,46 Likewise, Salifou et al. 27 reported high loan interest rates as a key barrier to the deployment of small solar PV systems. In a study, Akrofi et al. 48 found that high loan interest rates remain a significant barrier to residential solar PV investments and a key challenge to the wider diffusion of solar PV in Ghana.

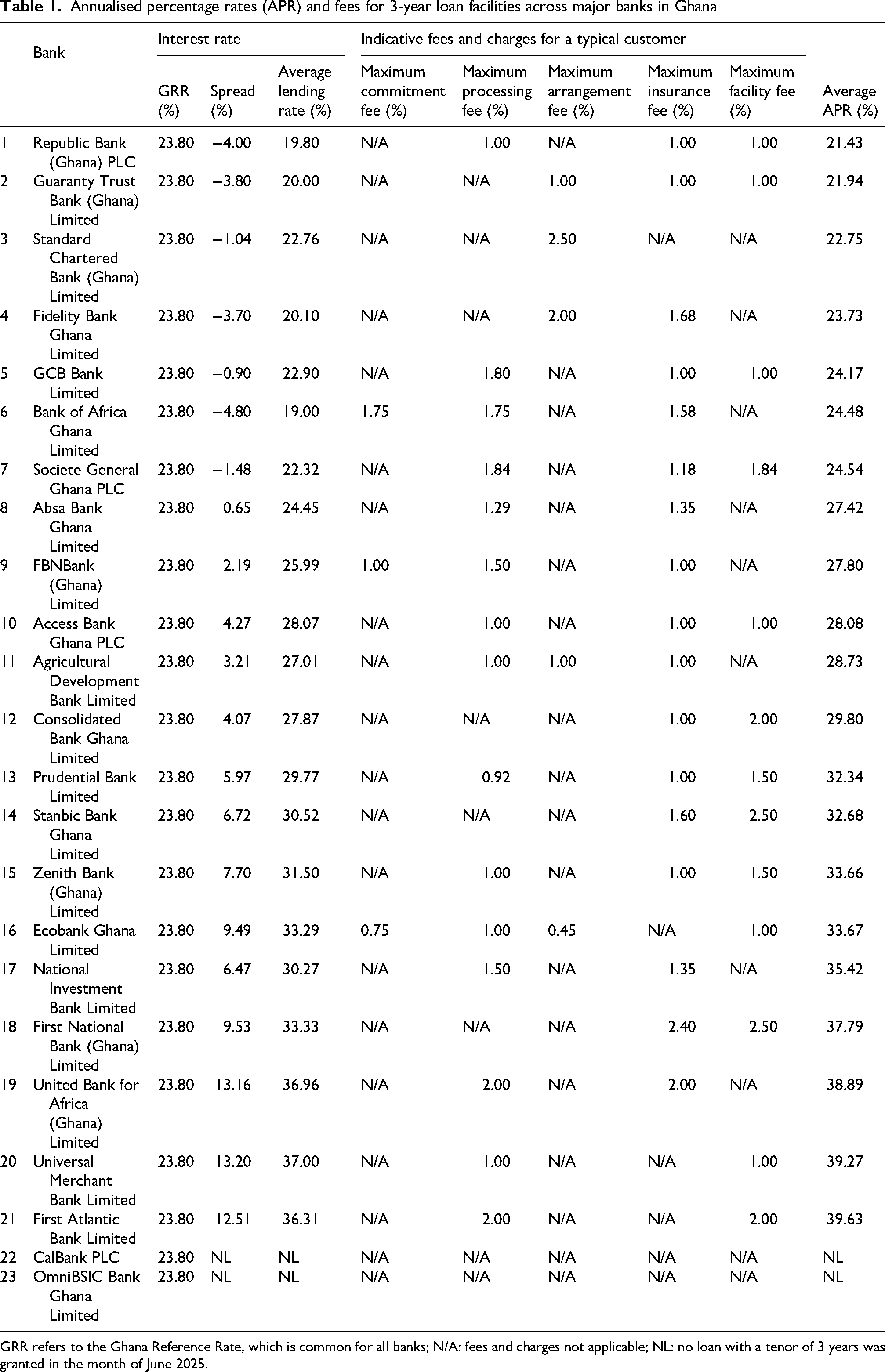

As an illustration of typical loan interest rates, Table 1 summarises the interest rates, fees, and average annualised percentage rates (APRs) for 3-year household loans offered by major banks in Ghana. The APR reflects the cost households face when they go through the approval process to secure a loan facility. It comprises the Ghana reference rate, bank-specific risk premia, and other bank-specific charges. 49

Annualised percentage rates (APR) and fees for 3-year loan facilities across major banks in Ghana

GRR refers to the Ghana Reference Rate, which is common for all banks; N/A: fees and charges not applicable; NL: no loan with a tenor of 3 years was granted in the month of June 2025.

Moreover, studies have revealed that some banks required customers to maintain an account for at least three months before being eligible for loans, while others mandated repayment within very short periods, typically 12 months. The eligibility criteria for these loans were often designed to favour upper-class salaried workers, making it difficult for lower-income individuals to qualify. 46 As a result, these stringent conditions have discouraged many potential borrowers from financing solar PV systems through loans. 46 In a related study, Francis et al. 22 found that the primary stumbling blocks to the energy transition in Ghana include the lack of credit facilities, high and unstable interest rates, profit maximisation, inadequate access to finances and the lack of green banks for renewable energy projects.

Nevertheless, regardless of the financing mechanism for solar PV, studies reveal that an economic justification is usually needed to inform residential sector investment, and that residential sector installation of solar PV is strongly influenced by financial viability.50,17 Moreover, the financial costs and benefits of PV deployment are subject to several uncertainties, including interest rates, inflation rates, and electricity tariffs. These financial conditions create uncertainties that do not favour their investments in solar PV in the residential sector. 17

Kalemis and Upham 10 showed that existing financial market conditions and high PV costs in Africa make it too expensive for low-income households and the vulnerable to install solar PV. Consequently, existing studies indicate that mainstream solar companies in Africa are unlikely to reach low-income households. 51 Also, there is evidence of class- and status-based disparities in accessing financing for solar home systems across several communities in Sub-Saharan Africa. The lower caste communities groups and households with low and unpredictable incomes often do not have access to loans from mainstream financial institutions to finance solar PV installations. 52 These study findings raise concerns about the unfavourable financing conditions regarding residential solar PV, which could adversely impact the pursuit of a just energy transition across the African continent.

Several studies on residential solar PV systems in Ghana have predominantly emphasised the need for government subsidies to accelerate deployment.53,54 However, as the global PV market evolves, subsidies are gradually being phased out due to their high costs and long-term sustainability challenges for central governments.55,56,35 In contrast to the subsidy-dependent approaches proposed in previous studies, this study repositions the ongoing discourse on residential solar PV advancements in Ghana by examining more sustainable and market-oriented financial mechanisms, particularly loan financing. This approach is crucial for developing viable financing models for residential PV systems in Ghana and other developing Sub-Saharan African countries while reducing fiscal burden on central governments.

As socioeconomic factors influence the adoption of solar PV, 11 this study is conducted within the framework of the Ghana Living Standards Survey (GLSS7), which provides a comprehensive reflection of households’ socioeconomic conditions in Ghana. By doing so, this research contextualises households’ ability to repay loans for grid-tied urban residential PV systems within prevailing economic conditions and the residential PV compensation schemes offered by the Ghanaian government: Net billing.

Furthermore, this study incorporates home charging of battery electric vehicles (BEV) into residential electricity load demand. The use of electric vehicles as an alternative to internal combustion engine vehicles provides countries with the opportunity to reduce emissions as well as improve the use of renewable energy sources.57,58,59,60,61,62 Although the adoption of electric vehicles is a key component of Ghana's energy transition framework, 63 there is limited research on e-mobility in developing countries such as Ghana. 64 Integrating electric vehicles into urban residential load demand significantly increases the required PV capacity, thereby increasing the upfront investment cost. As a result, household access to loans from financial institutions could be critical to finance the high investment costs of such a residential solar PV system.

This study, therefore, provides deeper insight into the economic viability of financing residential solar PV systems through loan mechanisms within the context of e-mobility in developing African countries, using Ghana as a case study. Unlike previous studies that proposed government subsidy-dependent approaches to accelerate residential solar PV deployment in Ghana,53,54 this study repositions the ongoing discourse on residential solar PV advancements by exploring more sustainable, market-oriented financial mechanisms, such as loan financing. The novelty of this study lies in its integration of techno-economic PV system modelling with household socio-economic data from the GLSS7 to evaluate the affordability and repayment feasibility of loan-financed residential PV systems with integrated battery electric vehicle charging.

Consequently, the study contributes to bridging the knowledge gap in the existing literature on the sustainable financing of residential PV systems in Sub-Saharan African countries by providing an in-depth analysis of how financial market conditions, banking practices, and household affordability interact to shape the uptake of loan-based solar PV financing. By empirically linking these factors within the Ghanaian context, the study explains why residential solar PV loan financing remains limited despite supportive policies and strong solar resource potential. The findings advance understanding of household-level financial barriers and provide policy-relevant insights to improve access to affordable credit for residential solar PV deployment.

Materials and methods

This section outlines the study model for evaluating the economic performance of loan-financed grid-tied residential solar PV systems under Ghana's net billing scheme. It details solar resources, household load with electric vehicle integration, tariff and compensation structures, socio-economic data, financing and repayment assumptions, system design, simulation settings, and economic evaluation parameters.

Study area and solar resources

Figure 1(a) displays the location of Ghana within the African continent, whereas Figure 1(b) shows the spatial distribution of long-term average PV power output across Ghana. The figure shows regional variations in solar resource availability, with higher PV potential in the northern zones and comparatively lower, yet still significant, values in the southern coastal regions. Annual PV yield ranges from 1314 to 1607 kWh/kWp, while daily averages range from about 3.6 to 4.6 kWh/kWp.

(a) Geographical context and (b) photovoltaic power potential across the regions of Ghana. 65

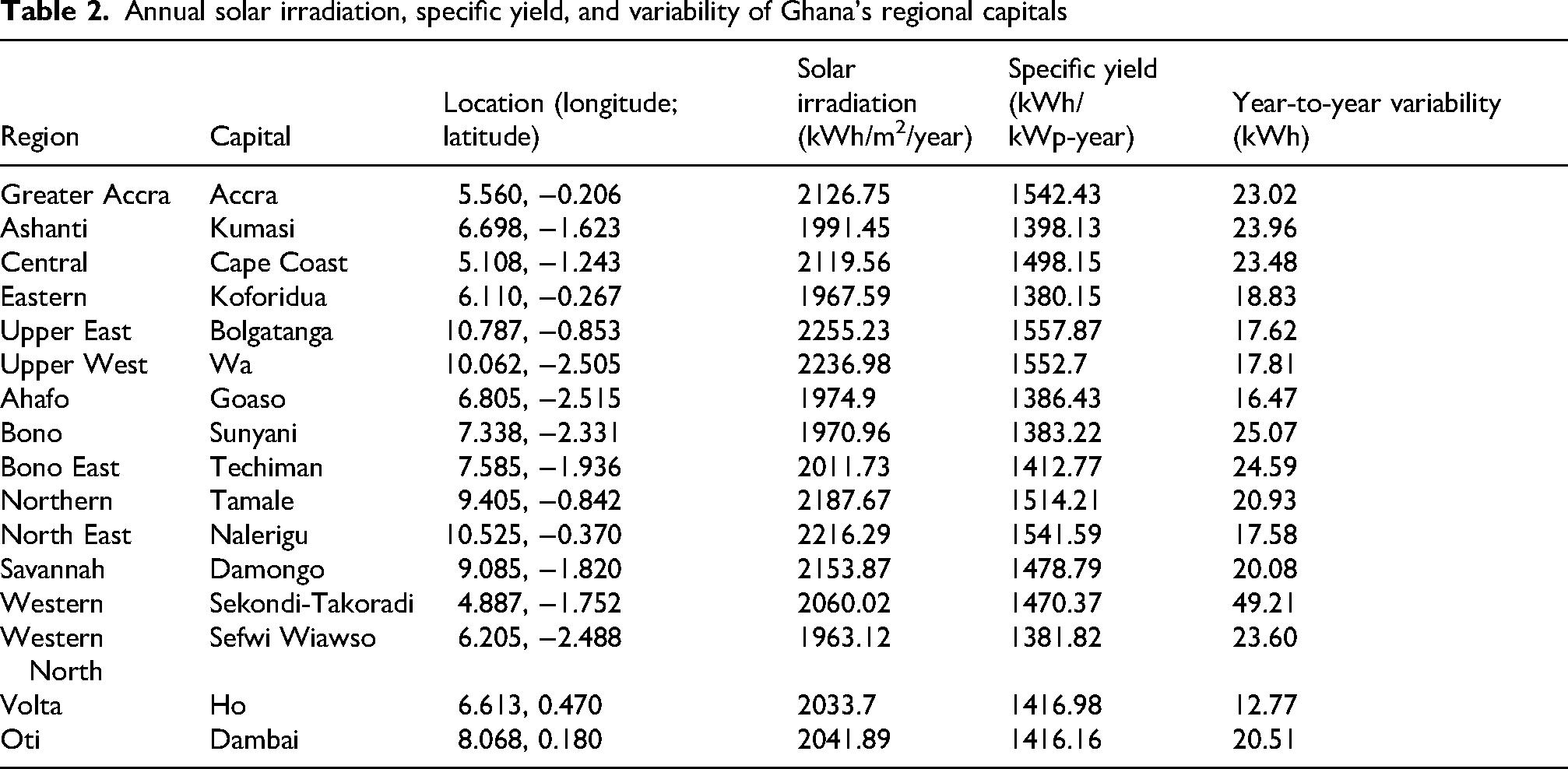

Table 2 provides the annual solar irradiation, specific yield, and year-to-year variability for all 16 regional capitals in Ghana. These values were obtained from the Photovoltaic Geographical Information System (PVGIS ver 5.3), based on the simulation parameters and assumptions given in Table 3. From Table 2, it is observed that the lowest and highest solar irradiation, 1963.12 kWh/m2/year and 2255.23 kWh/m2/year, are recorded in Sefwi Wiawso (Western North) and Bolgatanga (Upper East), respectively. Sekondi-Takoradi (Western Region) exhibited the highest year-to-year variability (49.21 kWh), whereas Ho (Volta Region) recorded the lowest (12.77 kWh). The specific yields of the regional capitals were used to size the residential solar PV systems modelled in this simulation study.

Annual solar irradiation, specific yield, and variability of Ghana's regional capitals

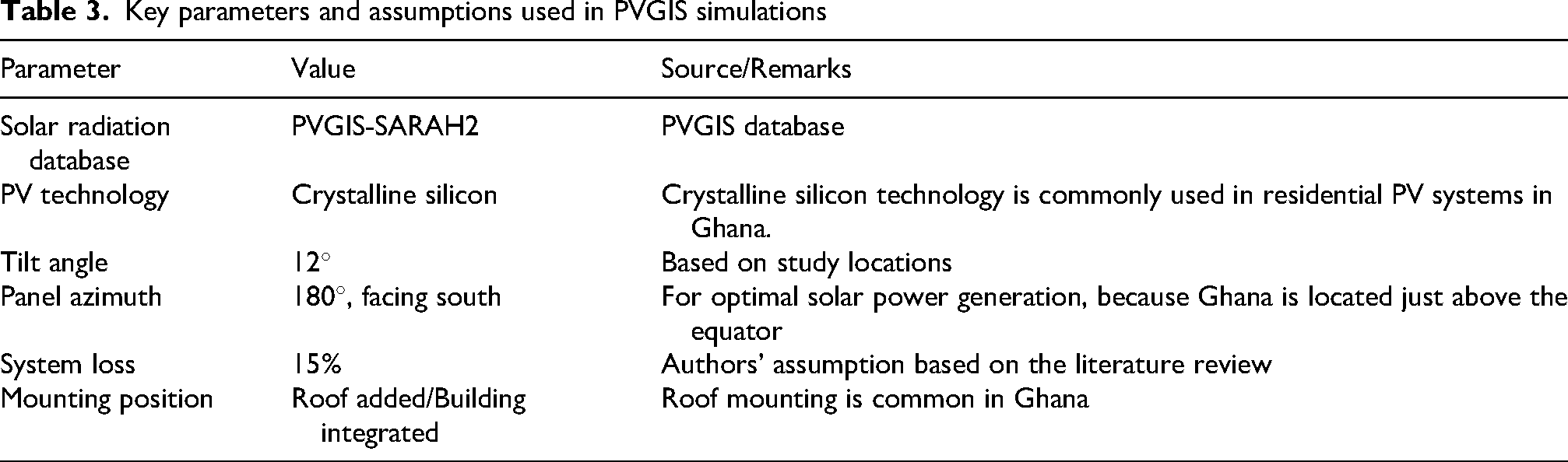

Key parameters and assumptions used in PVGIS simulations

Residential load demand

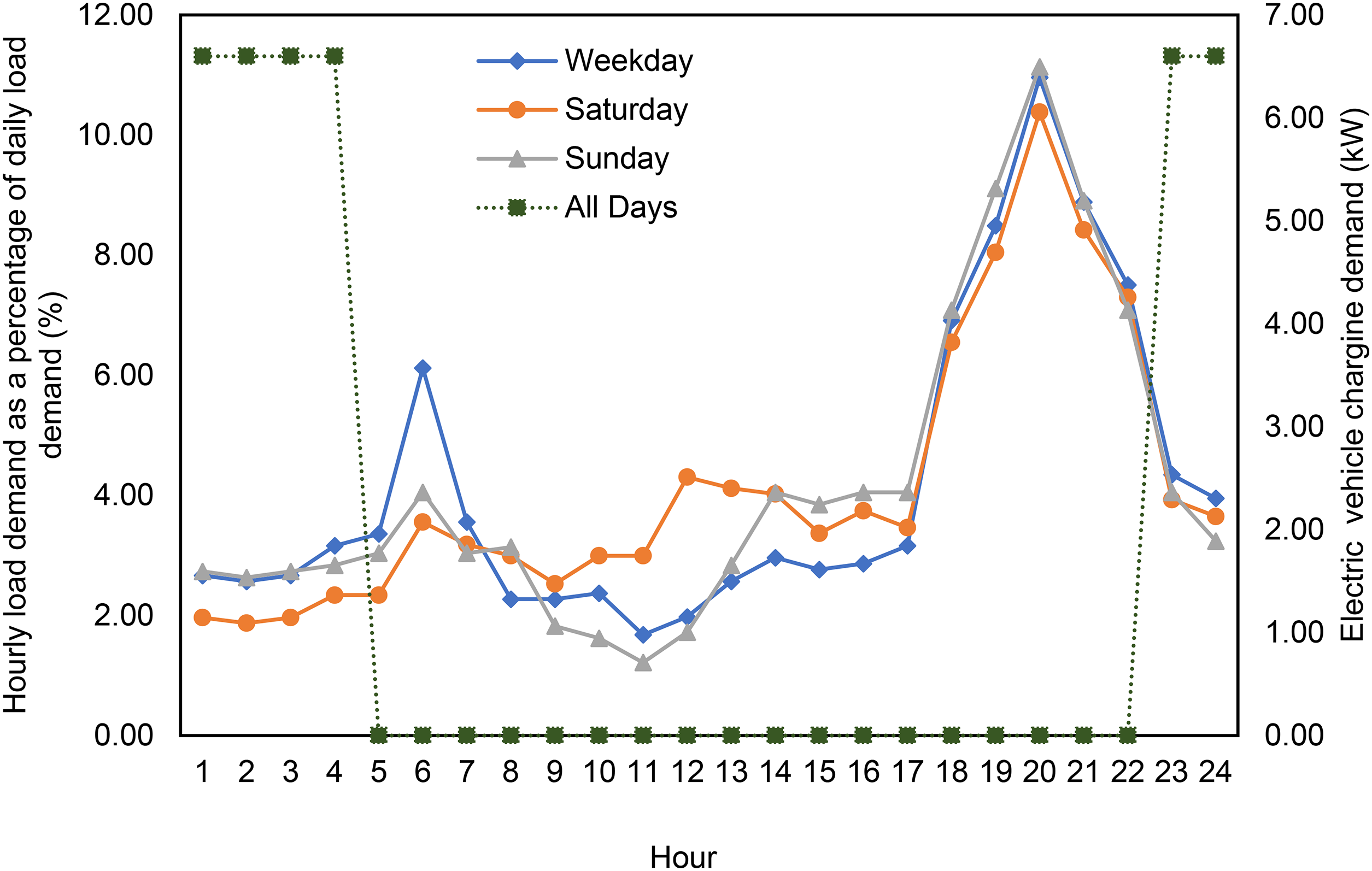

The residential sector constitutes the largest share of electricity consumers in Ghana, accounting for approximately 47% of total power consumption. 66 Therefore, the study focuses on the residential sector, as it can contribute to decarbonising Ghana's power sector through the penetration of residential solar PV systems and electric vehicles (EVs). This study employed a synthetic residential load profile of a Ghanaian estate using PV*SOL premium software. The synthetic profile has been adjusted to match both the weekday and weekend characteristics of a typical urban residential household in Ghana, as reported by Sakah et al. 67 (Figure 2).

Average hourly load profile of a typical urban residential household in Ghana. Adapted and modified from Sakah et al. 67

Therefore, the average electricity consumption per urban residential household is 3234 kWh/year. This consumption profile represents an average household with a household size of 4.2, a floor area of 132 m2, and a monthly income of USD 906. The average weekday and weekend load factors range between 36% and 39%, with morning and evening peaks occurring between 05:00–08:00 h and 18.00–22.00 h, respectively. The characteristics of the hourly urban residential profile reported by Sakah et al. 67 and adopted in this study align with those of related studies that have modelled urban residential profiles for typical West African countries.68,69 This study adopts a generic load demand profile due to the lack of national data on residential electricity consumption in Ghana, a challenge common in several West African countries. 69 In the absence of comprehensive primary data, other studies have also relied on generic load profiles for their analysis. 70 It is worth noting that household load profiles are influenced by weather, appliance ownership and occupancy patterns.68,67 Consequently, substantial variation in demand patterns may exist across Ghana's regions. Therefore, a limitation of this study is the adoption of a single urban residential load profile, which does not capture potential regional variations in household electricity consumption patterns across the country.

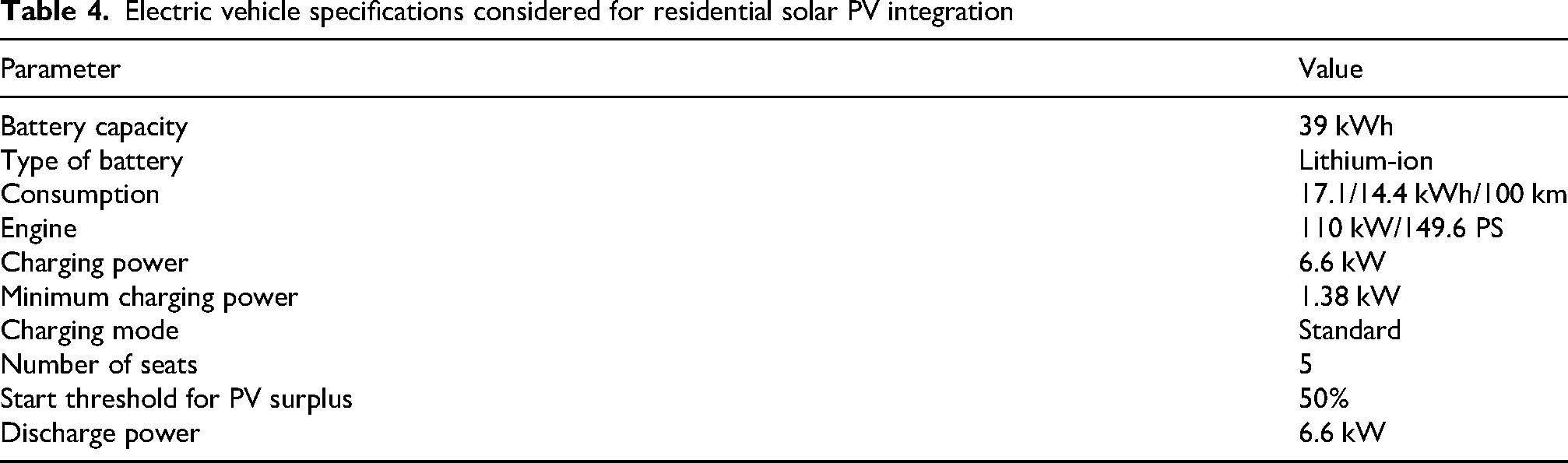

Additionally, this study integrated home charging of BEVs into the urban residential household electricity demand. In this study, a Nissan Leaf BEV with 12,000 annual miles is selected. The BEV's slow charging mode, requiring an average charging duration of 6 h, has been considered for off-peak overnight charging from 23:00 h to 5:00 h, as illustrated in Figure 2. The selection of the Nissan Leaf BEV is due to its being considered an economical and common BEV for the Ghanaian terrain. Also, the night-time charging aligns with the preference of most EV owners in Ghana. 71 Table 4 presents the Nissan Leaf BEV technical specifications, battery capacity, and charging characteristics. With a vehicle consumption specification of 17.1 kWh/100 km, the annual electricity demand for charging is estimated at 3121 kWh. When combined with the baseline household electricity consumption of 3234 kWh/yr, the total aggregated annual urban household electricity demand increases to 6355 kWh.

Electric vehicle specifications considered for residential solar PV integration

Electricity tariff structure for residential consumers

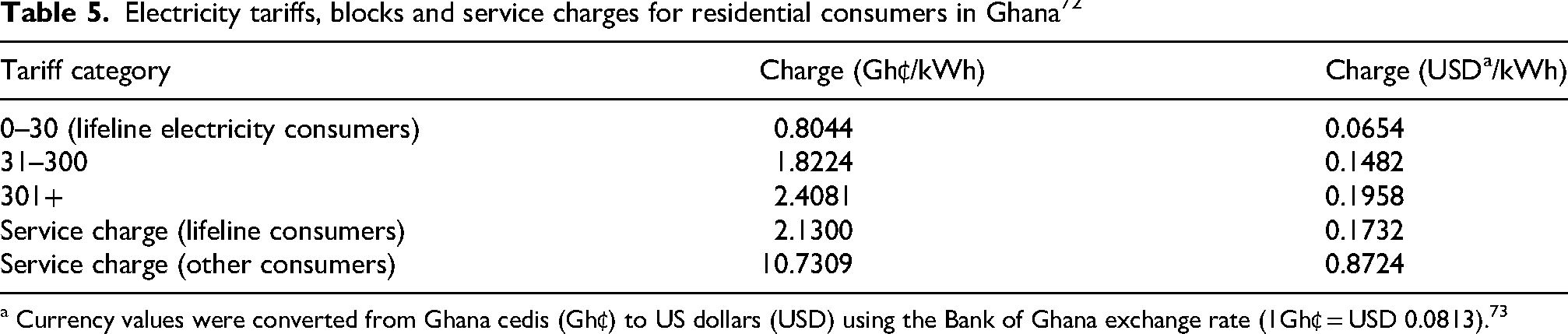

Ghana currently employs a progressive block tariff structure for electricity. The residential sector is divided into three blocks based on monthly electricity consumption: 0–30 kWh, 31–300 kWh, and >300 kWh. In addition to the energy charge per kWh, residential electricity users are required to pay a service charge. Table 5 outlines the electricity tariff blocks and associated service charges applicable to residential consumers in Ghana. Notably, given an estimated average aggregated urban residential household electricity demand of 6355 kWh (equivalent to 529.58 kWh/month), the urban households considered in this study fall within the third residential electricity tariff block, which is over 300 kWh per month.

Electricity tariffs, blocks and service charges for residential consumers in Ghana 72

a Currency values were converted from Ghana cedis (Gh₵) to US dollars (USD) using the Bank of Ghana exchange rate (1Gh₵ = USD 0.0813). 73

Ghana's net billing scheme

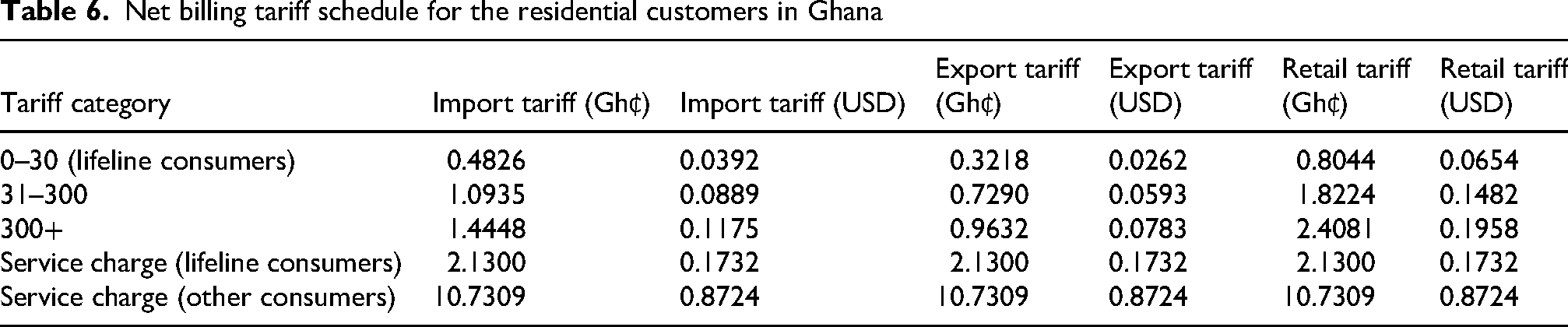

In accordance with the statutory duties outlined in Ghana's Public Utility Regulatory Commission (PURC) Act 538 and the Renewable Energy Act 832, as amended by the Renewable Energy Act 1045, the commission published Ghana's net metering tariff schedule with an effective date of 1 October, 2025, as shown in Table 6.

Net billing tariff schedule for the residential customers in Ghana

Although the commission has labelled it a Net Metering Tariff Schedule, the compensation scheme considered in this study is treated as a net billing mechanism. The core principle of the net metering scheme is that excess energy exported to the grid is valued the same as the energy purchased from the utility grid. 9 However, the key characteristic of the net billing scheme is that excess electricity injected into the grid is compensated at different monetary rates or buy-back rates. 74 The compensation rate under the net billing scheme is typically below the electricity retail rate and may be based on market value, such as avoided costs or wholesale prices. 9 Considering the average aggregated urban residential household electricity consumption of 6355 kWh/yr, the urban households considered in this study fall within the third customer generator PV compensation block, characterised by imports, exports, and retail tariffs of Gh₵ 1.4448, Gh₵ 0.9632, and Gh₵ 2.4081, respectively.

Ghana's net billing scheme stipulates the following conditions for customer-generators: if the amount of electricity imported from the distribution company (DISCo) equals the amount exported to the distribution network, the customer shall pay the DISCo the import tariff for the energy imported, as specified in the schedule. If the electricity imported from the distribution network exceeds the electricity exported, the customer-generator shall pay the DISCo the import tariff for the total energy imported and, in addition, pay the export tariff for the net imported energy, as provided in the schedule. Conversely, if the electricity exported to the distribution network exceeds the electricity imported, the customer-generator shall pay the DISCo the import tariff for the energy imported and receive a credit for the net exported energy at the export tariff. 75

Demographic and socio-economic characteristics of Ghanaian residential households

The ability to acquire residential solar PV is influenced by a household's income level, purchasing power, and socio-economic status.76,3 Higher-income groups have a greater affinity for solar home systems than lower-income groups.46,76 This study assessed the ability of residential households to repay loan-financed solar PV systems using data from the Ghana Living Standards Survey Round 7 (GLSS7), while accounting for household income, expenditures, and socio-economic factors. The GLSS is a nationwide household-based survey that assesses the socio-economic characteristics and well-being of households in Ghana. It focuses on measuring and monitoring living conditions, income, and expenditure patterns. 77

Household income

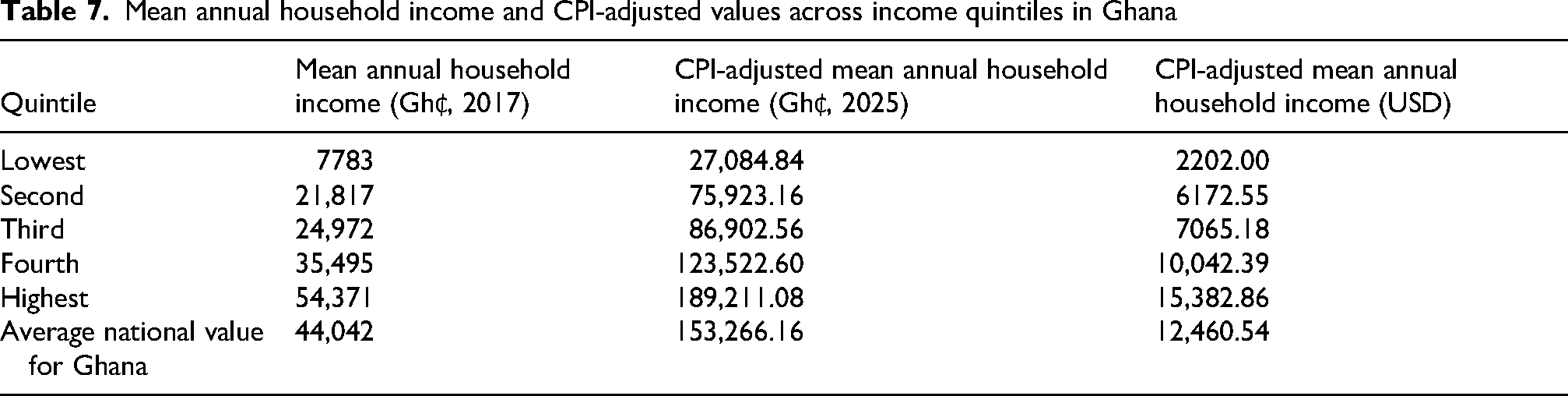

Household income in GLSS7 comprises both monetary and non-monetary earnings received by all household members. This includes wages and salaries, income from agricultural and non-agricultural activities, pensions, disability and relief payments, regular rental and remittance receipts, returns from businesses or ventures, investments, and other irregular gains, such as compensation and lottery winnings. Accordingly, the household incomes reported by the GLSS7 closely relate to gross household income. According to GLSS7, the national mean annual gross household income is GH¢44,032, with an average household size of 3.8 members. The lowest and highest income quintiles have mean annual household incomes of GH¢7783 and GH¢54,371, respectively.

Household incomes in the latest GLSS7 are reported in constant 2017 Ghana cedis and were therefore adjusted to July 2025 prices to ensure comparability with current economic conditions. In this study, this adjustment was carried out using the consumer price index (CPI) with a 2021 = 100 base. Specifically, the December 2017 CPI of 74.39 was used as the baseline, while the July 2025 CPI of 259.1 was used as the target index, yielding an adjustment factor of 3.48.

78

The adjustment was performed using a direct point-to-point ratio, as shown in

Mean annual household income and CPI-adjusted values across income quintiles in Ghana

where

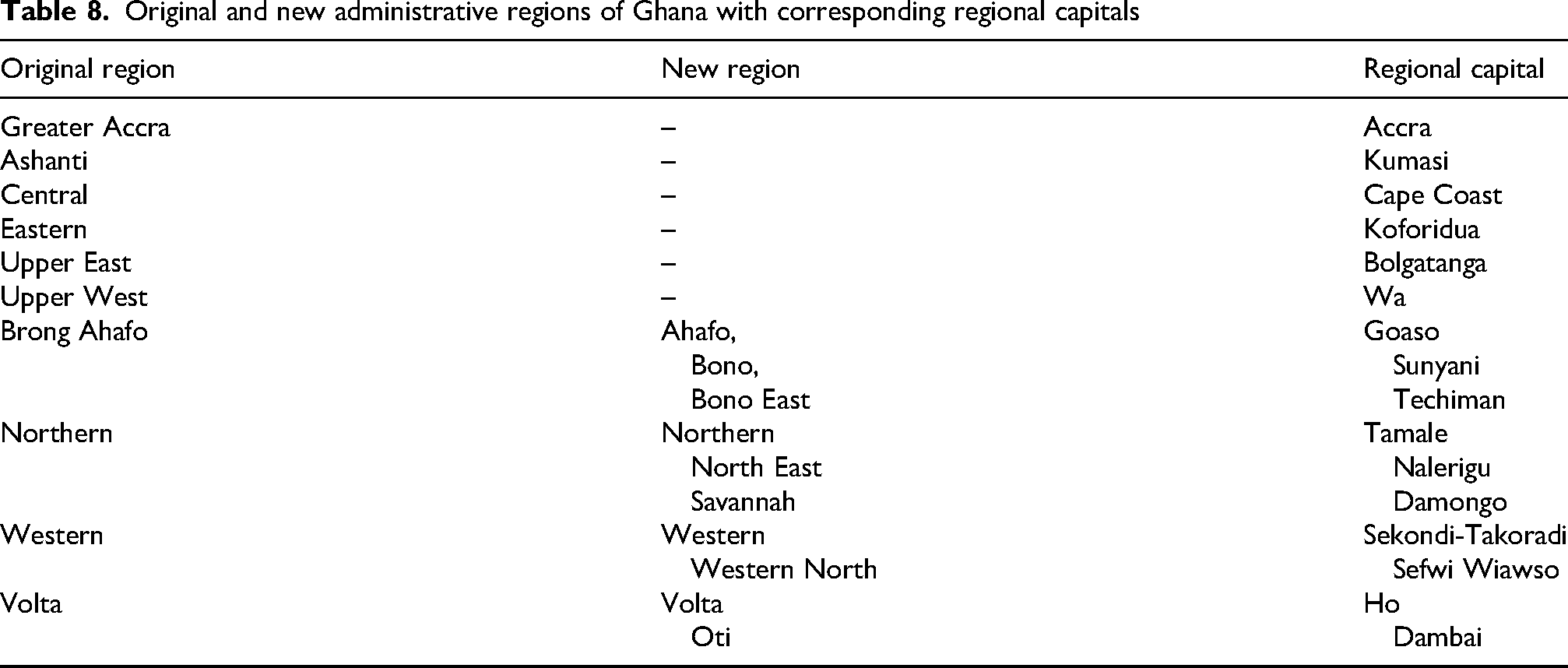

It is worth noting that Ghana expanded its regions from 10 to 16 following a 2018 referendum. However, the six newly created regions are not distinctly captured in the latest survey (GLSS7). In this study, household incomes for the newly created regions are assumed to be similar to those of their original parent regions. Table 8 shows the original and newly created administrative regions of Ghana, including the corresponding regional capitals, following the 2018 regional re-demarcation. Notably, six of the original regions remained unchanged, while four were re-demarcated to form the new regions.

Original and new administrative regions of Ghana with corresponding regional capitals

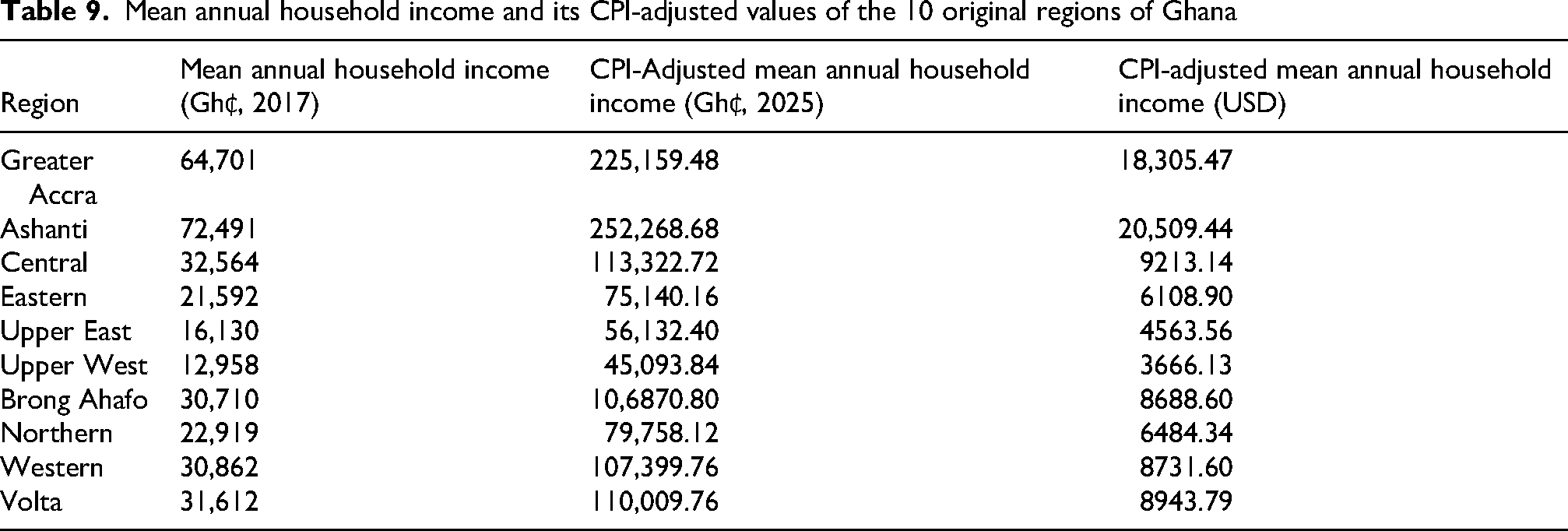

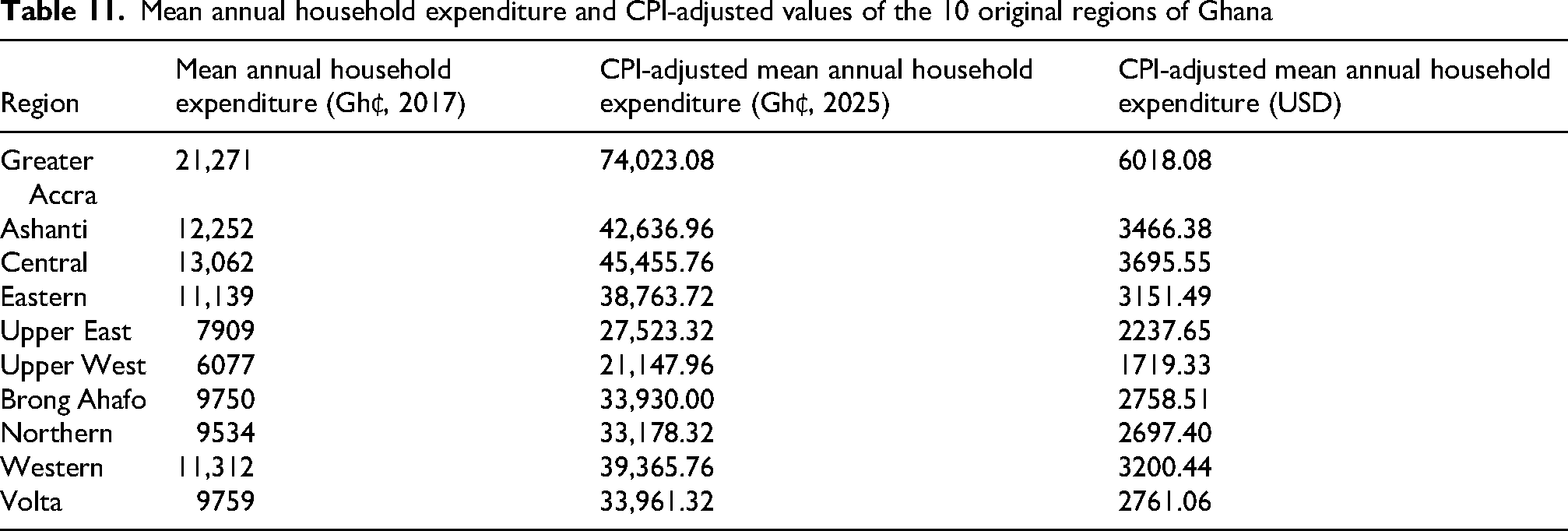

Table 9 presents the mean household incomes from GLSS7 (2017) for Ghana's 10 original regions, along with CPI-adjusted values in Ghana cedis for July 2025 and corresponding USD values. It is assumed that the newly created regions follow the income patterns of the original parent regions out of which they were formed. Specifically, the Ahafo, Bono, and Bono East Regions are considered to have household incomes comparable to Brong-Ahafo; the North East and Savannah Regions are considered comparable to the Northern Region; the Western and Western North Regions are considered comparable to the Western Region; and the Volta and Oti Regions are considered comparable to the Volta Region.

Mean annual household income and its CPI-adjusted values of the 10 original regions of Ghana

Household expenditure

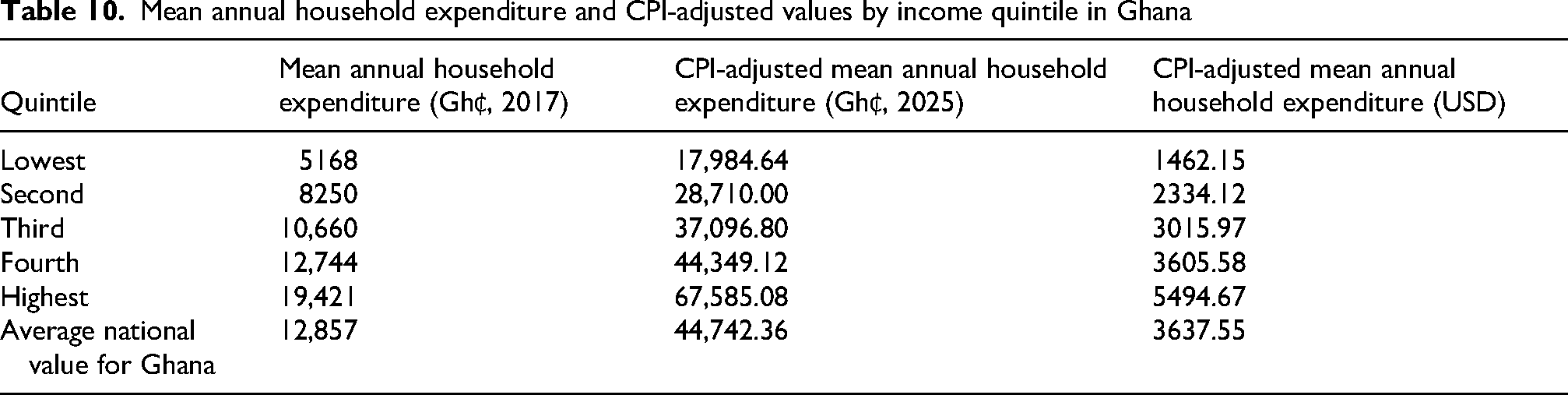

The GLSS7 defines household consumption expenditure as the sum of the value of goods and services purchased by households, consumed from own production, received as gifts and payments in kind. According to GLSS 7, the average annual household expenditure in Ghana was estimated at Gh₵ 12,857. The lowest and highest quintile groups have annual expenditures of Gh₵ 5168 and Gh₵ 19,421, respectively. As these values are expressed in 2017 constant Ghana cedis,

where

Table 10 presents the mean household expenditure from GLSS7 (2017) and their CPI-adjusted equivalents, re-expressed in July 2025 Ghana cedis and corresponding USD values, by quintile group. In addition, Table 11 provides the mean household expenditure for the 10 original regions of Ghana, adjusted to July 2025 values.

Mean annual household expenditure and CPI-adjusted values by income quintile in Ghana

Mean annual household expenditure and CPI-adjusted values of the 10 original regions of Ghana

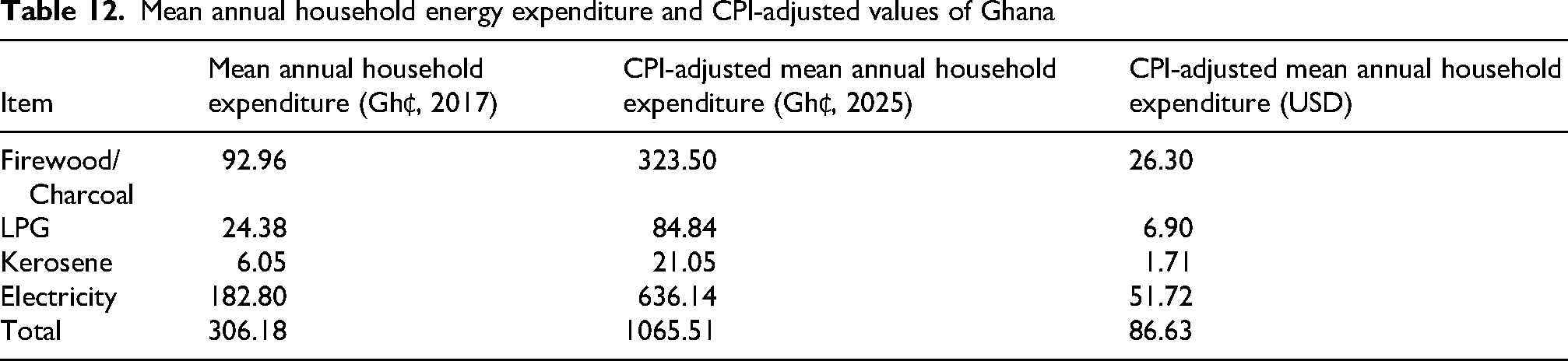

According to GLSS7, on average, households’ total annual expenditure on food accounts for 42.9% of total expenditure, while expenditure on housing accounts for 15.8%, and other expenditure accounts for 41.3%. 77 Tetteh and Kebir 79 demonstrated that household electricity expenditure in Ghana influences the adoption of solar PV. Table 12 provides details on household energy expenditure and its CPI-adjusted values for July 2025, in Ghana cedis and corresponding USD values. Residential energy expenditure includes total household expenditure on lighting and cooking fuels, including firewood, charcoal, and other fuels; kerosene; liquefied petroleum gas (LPG); and electricity. On average, households incurred an energy expenditure of Gh₵306.18, with electricity accounting for approximately 60% of this total. 80

Mean annual household energy expenditure and CPI-adjusted values of Ghana

Loan parameters for residential solar PV systems

The loan assessment parameters are based on the prevailing commercial lending rates provided by the Bank of Ghana, as no national loan policy currently exists for financing residential solar PV systems. Accordingly, households are assumed to obtain loans for such projects at commercial bank lending rates. Table 13 outlines the commercial loan parameters for financing urban residential grid-tied solar PV systems under prevailing Bank of Ghana lending conditions.

Commercial loan parameters for financing residential solar PV systems in Ghana

It is noteworthy that commercial loan interest rates in Ghana are considerably higher than those reported in related studies.82,9 According to the GLSS7, only 7.1% of the population applies for a loan. Among those who did not apply, 78.4% indicated that there was no need for credit, while 13.0% cited the prohibitively high interest rates as a deterrent. This study further extends the economic assessment of loan-financed residential solar PV systems to consider soft loan conditions. Soft loans are concessional credits that typically offer lower interest rates than market rates and longer repayment periods, and may cover all or part of the debt. 83 Although Ghana currently lacks a national policy for soft loans targeting residential renewable energy systems, some private financial institutions have partnered with solar companies to provide such financing. A notable example is the SUNREF Ghana Financing Programme, which, in collaboration with local partner banks, provides businesses, organisations, and households with access to financing for sustainable energy projects, including solar PV systems. The programme offers competitive loan terms, a potential grant of up to 10%, and free technical assistance for project implementation. 84 In this context, residential solar PV systems in Ghana could attract soft loan financing. Therefore, this study examines the feasibility of financing residential PV through soft loans. Table 14 summarises the soft loan parameters assumed, based on examples from related studies and programmes, such as the SUNREF Ghana financing programme.83,85

Soft loan parameters for financing residential solar PV systems in Ghana

Solar PV system sizing and simulation

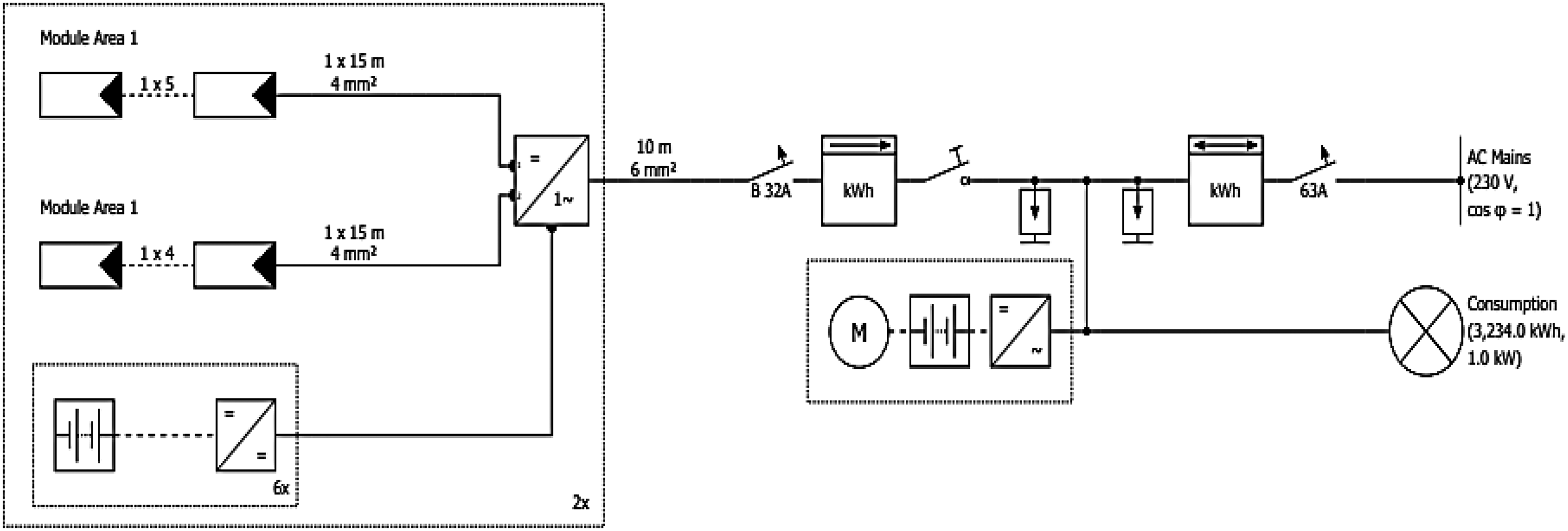

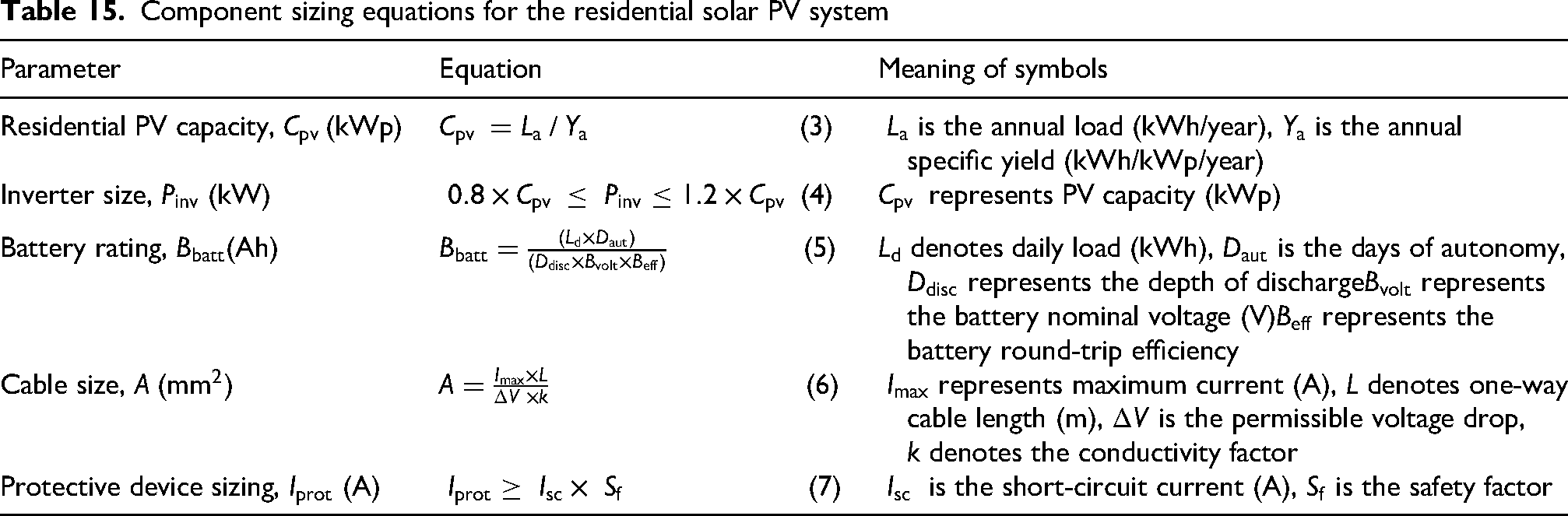

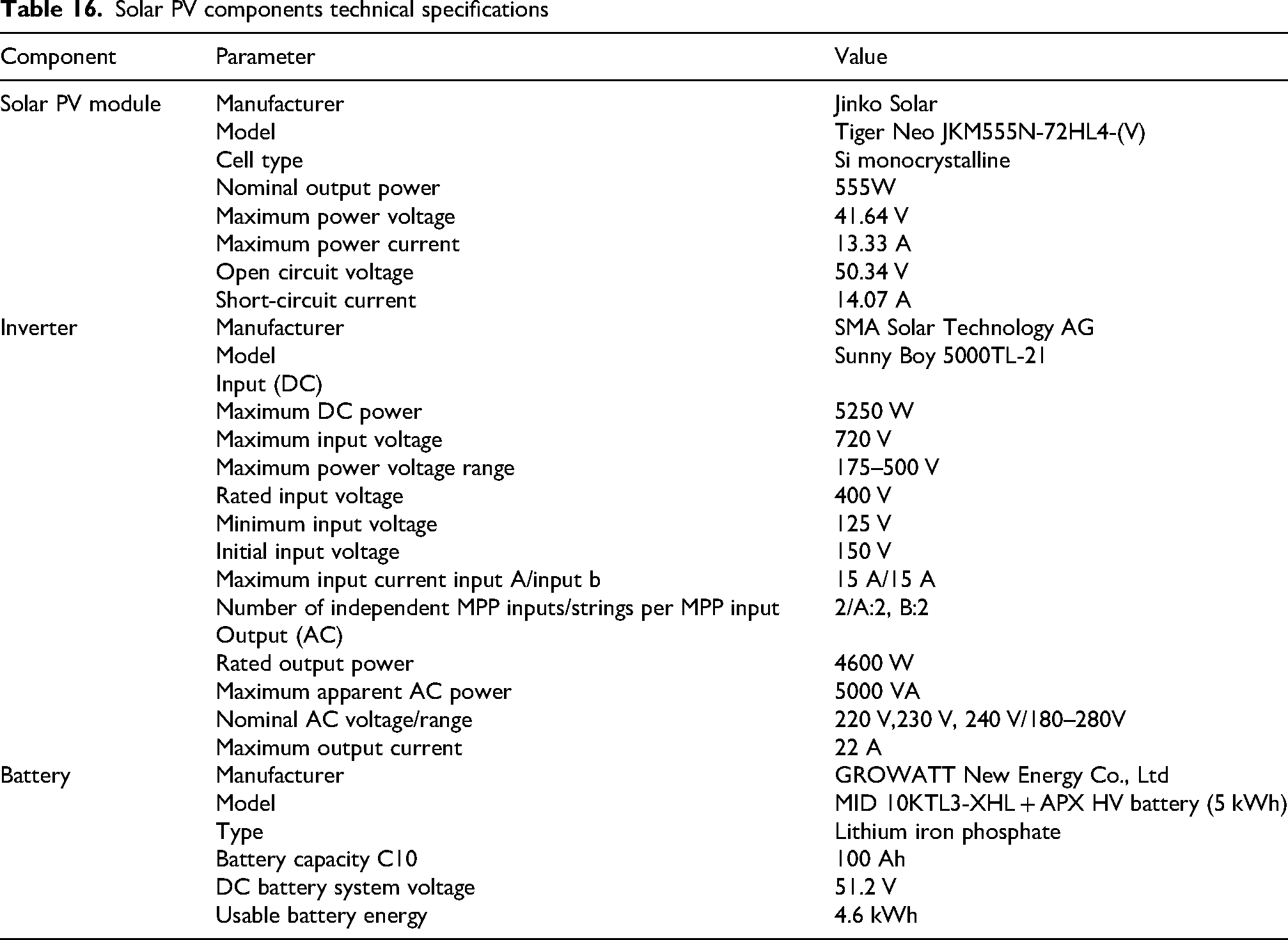

In this study, the residential grid-tied solar PV system was designed using the PV*SOL Premium simulation software. PV*SOL Premium software was selected for this study because it provides a detailed simulation of the residential solar PV performance, battery storage operation, electric vehicle charging behaviour, and utility grid integration under net billing schemes. Table 15 presents the fundamental equations employed to size key components of the PV system. The sizing of these components is based on the specifications and assumptions outlined in Table 16.86,87 The proposed system configuration consists of a 10 kWp PV array, a 10 kW inverter, and a 30 kWh battery storage system. Figure 3 presents the single-line schematic diagram of the proposed residential solar PV system for this study. The system design comprises two parallel 5 kW single-phase solar PV units. This configuration was adopted to comply with Ghana's technical requirements for residential grid-tied solar PV installations under the net billing scheme. 88

Single-line schematic diagram of the proposed residential 10 kW grid-tied solar PV system.

Component sizing equations for the residential solar PV system

Solar PV components technical specifications

Solar PV systems economic metrics

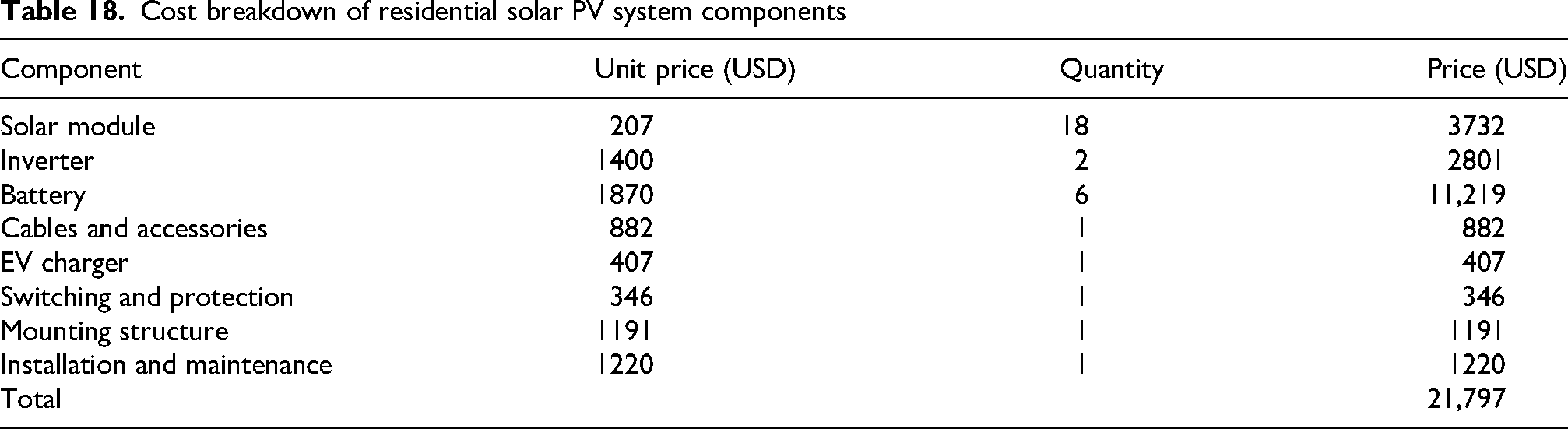

This study evaluates the economic performance of a loan-financed urban residential grid-tied solar PV system under Ghana's net billing scheme using several key indicators: levelised cost of energy (LCOE), BEV travel cost, payback period, annual savings, and accrued cash flow. These metrics provide a comprehensive basis for assessing both the cost-effectiveness and long-term financial viability of the proposed system. Table 17 presents the key system parameter assumptions adopted for the economic analysis. In addition, Table 18 provides a detailed breakdown of the residential PV system components and their associated costs. Cost data for the solar PV system components were obtained from Zotch Engineering Services, a leading solar PV installation company in Ghana. This firm was selected because of its active participation in the national solar market and its willingness to provide reliable cost and design information relevant to this study. The following subsections highlight the economic metrics in detail.

Assumptions and parameters used in the economic analysis

Cost breakdown of residential solar PV system components

Table 18 shows that battery storage is a major cost component of the designed urban residential solar PV system with integrated home charging for BEVs. High initial capital requirements remain a major barrier to the adoption of small-scale and residential PV.9,10,11 Consequently, without adequate supportive policy interventions, the high cost of residential PV could hinder their adoption by households in Ghana. Nevertheless, the residential PV cost estimates in this study are based on retail prices from Zotch Engineering Services, and significant cost variations may occur depending on market conditions. Thus, under other market conditions, the estimated solar system cost may vary considerably based on factors such as product brand, warranty terms, system capacity, installation costs and maintenance charges.91,92

Levelised cost of energy

The LCOE is defined as the sum of the initial cost of the system and the net present value (NPV) of all costs over the lifetime of the investment, divided by the energy generated by the system over its operational lifetime, as given in

Battery electric vehicle travel costs

The BEV travel cost represents the average cost of energy required to drive the EV over the specified distance. Therefore, it quantifies the operational cost of mobility based on the cost of electricity consumed for EV propulsion and is expressed as follows

94

:

Payback period

The payback period is the time required for a project to recover its initial investment from the revenue it generates.

Annual cash savings

The annual cash savings (

Accrued cash flow

Accrued cash flow is the cumulative sum of cash flow of a project from the beginning of a project up to a given year, and is computed as the running total of all annual cash inflows and outflows associated with projects95,96:

Household's loan repayment burden assessment

This study assesses the financial implications of financing residential solar PV systems for households by examining the loan repayment burden using two indicators: the debt-to-income ratio and residual income. These metrics are calculated based on annual scheduled loan repayments and household income and expenditure data derived from the GLSS7. Because GLSS7 household income and expenditure data are reported in constant 2017 Ghana cedis, they were adjusted to July 2025 price levels to ensure comparability with current economic conditions. The scheduled payments for a fully amortised loan were computed using the standard annuity-based method as follows97,96:

Debt-to-income ratio

The debt-to-income ratio

Residual income

The residual income (

Results and discussion

Solar PV economic performance

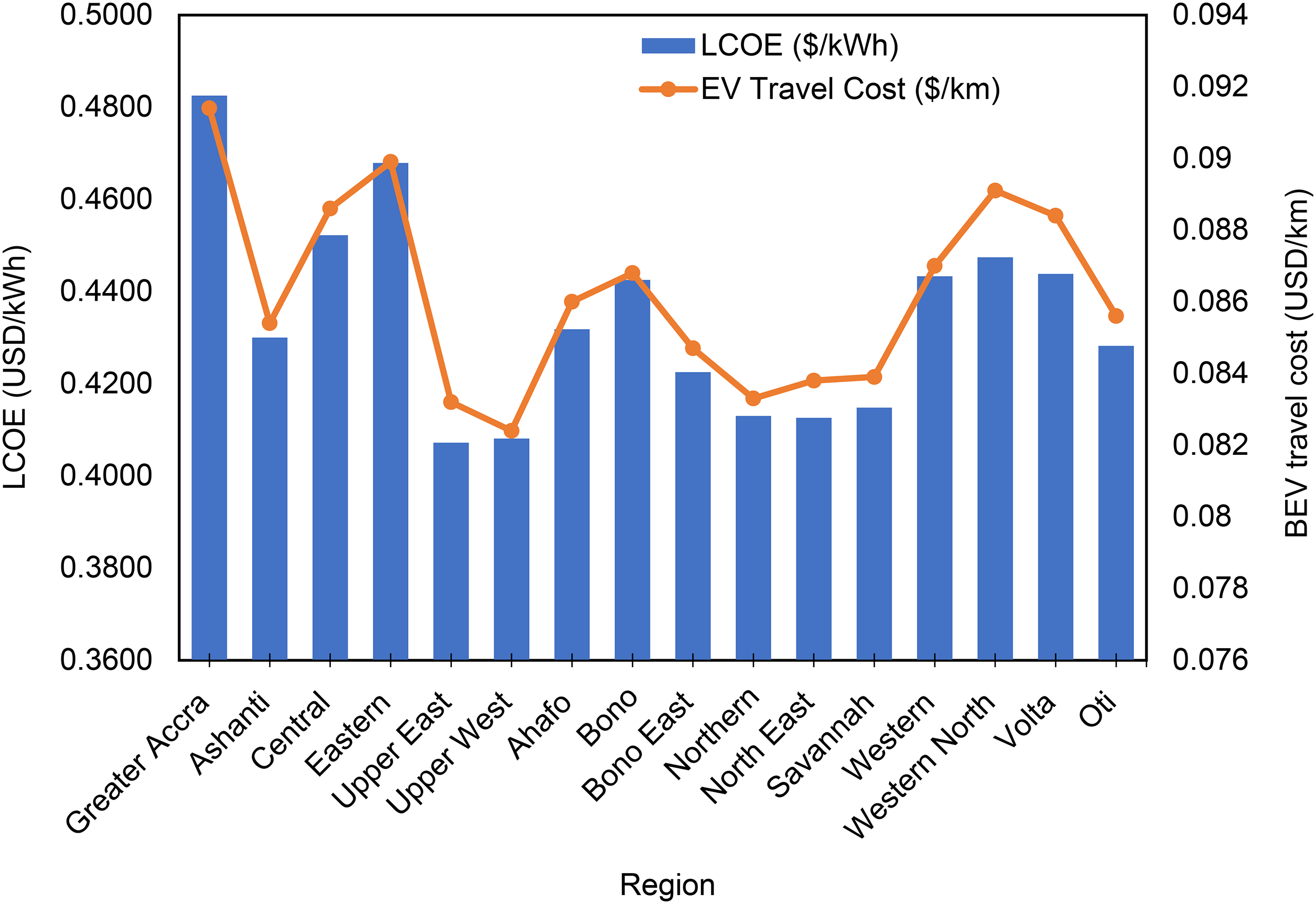

Figure 4 shows the LCOE and BEV travel costs for the residential grid-tied solar PV system in all administrative regions.

LCOE and BEV travel cost for residential grid-tied solar PV systems across Ghana's regions.

It is observed that regions in Northern Ghana, such as the Upper East, Upper West, Northern, and North East, recorded lower LCOE and BEV travel costs. For instance, the Upper East Region recorded the lowest LCOE of 0.4072 USD/kWh, followed closely by the Upper West Region at 0.4081 USD/kWh. Similarly, the lowest BEV travel costs among the 16 regions, 0.0824 USD/km, were observed in the Upper West Region. In contrast, the Southern regions of Ghana, including Greater Accra, Central, Western North, and Eastern regions, displayed higher LCOE and BEV travel costs. For example, the Greater Accra region recorded both the highest LCOE and BEV travel cost at 0.4825 USD/kWh and 0.0914 USD/km, respectively.

The observed regional performance differences in LCOE and travel cost closely align with the regional solar irradiation and system yield in Table 2. The northern regions recorded higher economic performance due to higher solar irradiation, enabling greater solar power generation and reduced reliance on the grid. Conversely, lower solar insolation in the southern regions accounted for the higher LCOE and travel costs. These findings are consistent with those of previous studies, indicating that Northern Ghana is favourable for solar PV system performance. 100

Notably, the poor LCOE and BEV travel costs performance of the Greater Accra Region cannot be explained solely by lower levels of solar irradiation and specific yield. This is because several regions, including Western North, Eastern, and Ahafo, have lower solar irradiation and yields than the Greater Accra, but they have yielded better performance. A possible reason for this outcome is the alignment between solar power generation and household load demand. In some regions, solar generation may not align optimally with residential consumption patterns, leading to greater reliance on grid electricity and, consequently, higher LCOE and travel costs. However, this study does not account for heterogeneity in residential load demand profiles across Ghana's regions.68,67,101

Compared to Ghana's national grid electricity tariff rate of USD 0.1958/kWh for residential consumers who consume more than 300 kWh per month, the LCOE results, ranging from USD 0.4072 to USD 0.4825, are markedly higher. A comparison of the LCOE obtained in the current study with values reported in the literature shows that the present estimates for Ghana (0.4072–0.4825 USD/kWh) are substantially higher than those reported for similar residential PV systems in Morocco, Iran, China, and earlier studies in Ghana (Table 19). Previous studies report LCOE ranges of 0.090–0.1252 USD/kWh in Morocco, 102 0.174–0.195 USD/kWh in Ghana, 103 0.063 USD/kWh in Iran, 104 and 0.164–0.220 USD/kWh in China. 105 Even when compared with the earlier Ghanaian study, the current LCOE values are more than double.

LCOE results reported in related studies

The higher LCOE values in this current study could be attributed to several factors. First, the present analysis incorporates loan-based financing for a 10 kW residential PV system, which introduces interest payments and financing charges that increase lifecycle costs. Most studies comparing upfront cash payments and concessional financing assume lower discount rates, leading to lower LCOE estimates. Second, the current study demonstrates prevailing market conditions in Ghana, including higher capital costs for PV components, exchange rate volatility, and elevated borrowing rates, all of which raise the effective cost of electricity generation. Third, differences in system assumptions such as degradation rates, operation and maintenance costs, and capacity factors also contribute to the observed disparity. In contrast, countries such as Iran and Morocco benefit from lower system costs and, in some cases, more favourable solar resource conditions and supportive financial structures, resulting in lower LCOE.

Several factors can account for the relatively high LCOE obtained for the loan-financed, grid-tied residential solar PV system proposed in this study. Firstly, the high LCOE relative to the residential grid electricity tariff in Ghana is attributable to the high upfront capital investment required for a PV system capable of meeting both household demand and BEV charging needs. Although solar PV systems generally benefit from economies of scale, 106 the integration of BEV charging considerably increases the required battery storage capacity, particularly for night-time charging. Battery storage technologies are among the most expensive components of PV systems; thus, increased storage requirements raised the overall cost per installed kilowatt. Other related studies in Ghana found that battery costs constitute the major component cost of PV systems. 107

In addition, residential electricity consumption patterns in Ghana are characterised by low daytime consumption and a low load factor. 67 Consequently, the additional demand for battery storage capacity for BEV night charging, along with its associated costs, substantially increased the upfront cost and the system's overall LCOE. It can therefore be observed in the PV system cost breakdown that battery storage accounts for the largest share of the total system cost (Table 18). Similar observations have been reported across Africa, where high initial capital requirements remain a major barrier to the adoption of small-scale and residential PV.26,30,27,29 The challenge becomes even more evident when EV charging is incorporated into residential load profiles, given the preference for night charging in Ghana's residential sector.

Nevertheless, as earlier stated, the system cost estimates in this study were based on retail prices from Zotch Engineering Services. Consequently, under other market conditions, the estimated solar system cost may vary depending on factors such as product brand and warranty terms, system capacity, and installation and maintenance charges.91,92 Secondly, the prevailing financial market conditions in Ghana, characterised by high loan interest rates and returns on capital, may have increased the financing costs of the proposed PV system, thereby raising the LCOE reported in this study. Compared with other related studies,82,9 the loan interest rates and discount rates used in this study are higher. However, they reflect current financial conditions and are consistent with rates reported in other analyses of loan-financed residential PV systems in Ghana.47,46

For a loan-financed solar PV system, households are required to repay both the system's capital cost and the financing costs, including interest. High interest rates, therefore, increase the overall cost of adopting residential solar PV and directly contribute to the higher LCOE observed. Regarding this observation, limited access to affordable financing is a major barrier to renewable energy adoption in developing countries. 23 The elevated financing costs are often attributed to the high investment risks associated with renewable energy markets in Africa.40,41

According to Khatib, 95 a high discount rate favours projects with low capital costs and high operational costs, whereas a low discount rate favours those with high capital costs and low operational costs. Since residential solar PV systems typically show high capital expenditure and low operating and maintenance costs, high discount rates work unfavourably against them. A related study by Chanyisa 19 found that infrastructure costs accounted for about 90% of lifetime costs in a typical African country (Kenya). In this regard, Ghana's high discount rate environment does not support the cost competitiveness of residential grid-tied PV systems. Similar findings suggest that financial conditions in many African countries make solar PV systems relatively more expensive compared to conventional energy sources. 26

Furthermore, electricity tariff rates in Ghana are influenced by political considerations, price distortion and government subsidies.108,109 As a result, the residential tariff of 0.1958 USD/kWh may not reflect the true cost of electricity supply by the state-owned utility companies. The underpricing of grid electricity could partially explain the wide gap between the grid tariff and the higher LCOE estimated for the residential PV system in this study. Many studies noted that the adoption of residential PV systems is strongly driven by economic justification.50,17 Therefore, the substantially higher LCOE relative to grid tariffs may act as a disincentive for households to invest in residential PV systems despite Ghana's abundant solar resource.

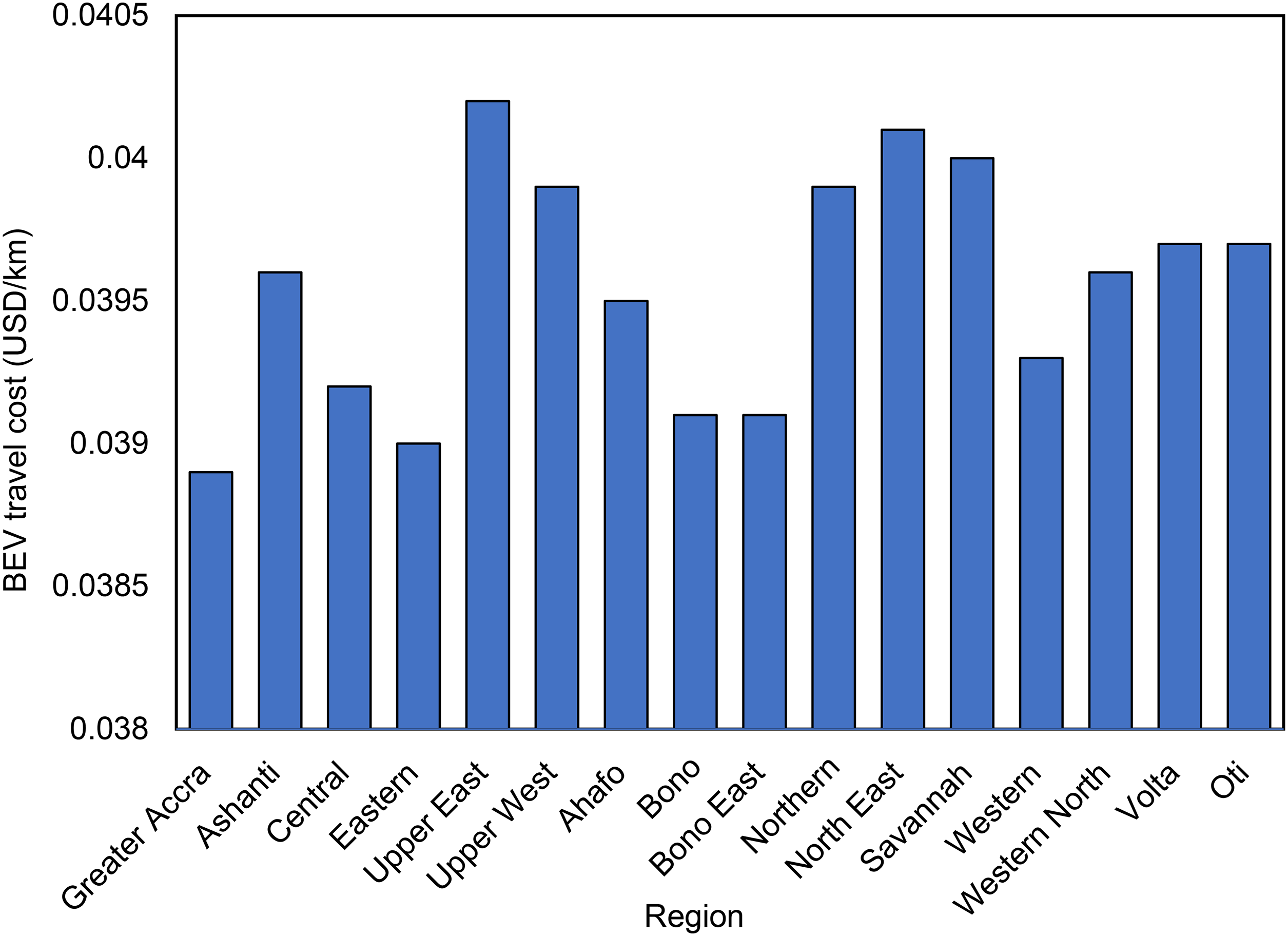

Regarding BEV travel costs, the study results in Figure 4 indicate values ranging from 0.0832 USD/km to 0.0914 USD/km across Ghana's 16 regions. These values are substantially higher than the travel costs associated with BEVs charged exclusively from the national grid, which range from 0.0389 USD/km in the Greater Accra to 0.0402 USD/km in the Upper East Region (Figure 5). The same factors that may have contributed to the elevated LCOE observed in this study could also explain the higher BEV travel costs. Consequently, the generally high BEV travel cost results reflect the compounded effect of high investment and financing costs associated with residential PV systems, the adverse financial impacts of large storage requirements for night-time BEV charging, and potentially underpriced grid electricity tariffs.

Travel cost of BEV charged exclusively from the utility grid across Ghana's regions.

From Figure 5, it can be observed that the BEV travel costs for vehicles charged directly from the utility grid in the southern regions generally outperformed those in the northern regions. This observation contrasts with the results for BEV travel costs charged using residential solar PV systems, which showed higher performance in northern regions. Notably, the lowest grid-charged travel cost of 0.0389 USD/km was recorded in the Greater Accra Region, whereas the highest was 0.0402 USD/km in the Upper East Region. This study's outcome is attributable to differences in climatic and geographical conditions between the southern and northern parts of Ghana. Ghana has three major climatic zones: Savannah, Forest, and Coastal. The northern regions, located within the Savannah zone, experience significantly higher ambient temperatures than the southern regions, which fall within the Forest and Coastal zones. 110 Lower temperatures in southern regions can enhance BEV performance by reducing battery thermal stress and lowering energy consumption. This effect could contribute to the relatively lower travel cost observed in Greater Accra compared to the Upper East, despite the latter's marginally higher solar irradiation. Ambient temperature differences may also explain the slightly higher BEV travel cost in the Upper East compared to the Upper West, 111 as shown in Figure 5.

The comparatively higher BEV travel costs associated with residential solar PV relative to utility grid-charged BEVs may discourage households from adopting residential PV systems for BEV charging, particularly under loan-financed scenarios. However, despite its lower financial cost, the utility grid in Ghana is dominated by thermal power generation. 44 Therefore, although grid charging is economically cheaper, charging BEVs with residential solar PV yields greater environmental benefits by reducing CO2 emissions, thus supporting Ghana's long-term decarbonisation targets. 63

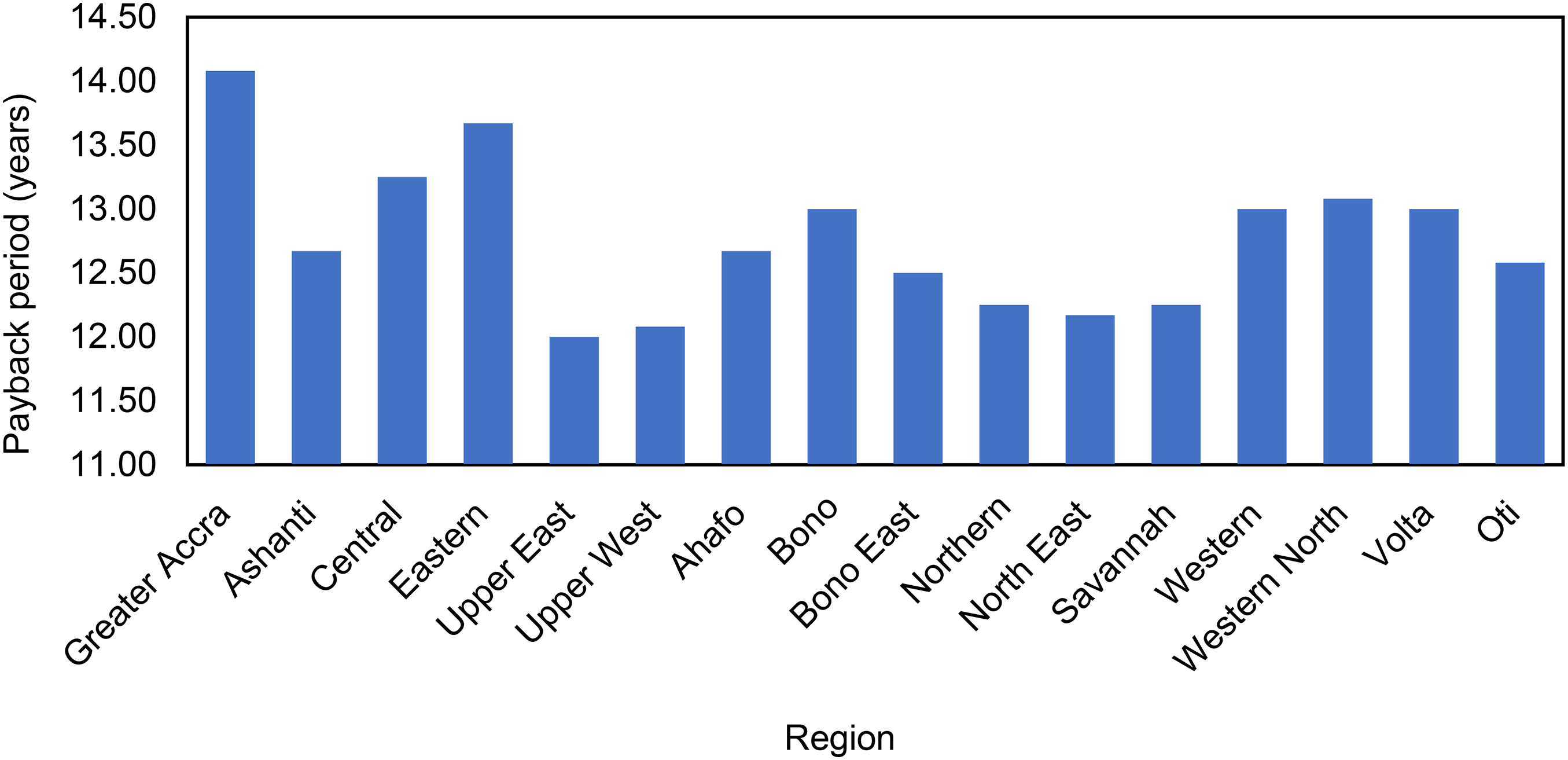

Figure 6 displays the payback periods for the grid-tied solar PV system across Ghana's 16 administrative regions. The payback period ranges from 12.0 to 14.1 years. As expected, the northern regions, which receive higher solar resources, recorded shorter payback periods than the southern regions with relatively lower solar resources. For instance, the Upper East and Upper West Regions recorded payback periods of less than 13 years. In contrast, the southern regions, including Greater Accra, Eastern, Central, Western, and Western North, recorded longer payback periods ranging from 13 to 14 years.

Regional comparison of payback periods for loan-financed residential solar PV systems.

These findings suggest that regional variations in solar resource availability influence the economic performance of residential solar PV systems. In practical terms, longer payback periods imply that consumers require more time to recoup their initial investment costs. Consequently, studies have shown that investors in solar projects generally prefer shorter payback periods. For example, Roberts et al. 17 found that green technologies with payback periods of 2–3 years were more attractive to households than those with payback periods of 8–10 years. Similarly, Rock et al. 112 reported that both landlords and tenants show greater interest in green investments that generate quicker financial returns.

Given consumers’ preference for shorter payback periods, the estimated payback period of 12–14 years obtained in this study suggests that loan-financed residential solar PV systems with BEV charging capability may not be financially attractive to many residential households in Ghana, even in regions with high solar resource potential. This finding is consistent with broader evidence indicating that short-termism remains a major barrier to investments in low-carbon technologies and the global transition towards sustainable energy development. 14

To further contextualise these findings, the estimated payback period obtained in the present study is compared with those reported in similar studies in the literature. The payback period of 12.0–14.1 years is longer than those reported in most comparable studies. For instance, Ahmad et al. 113 reported payback periods ranging from 7.8 to 9.7 years for grid-connected solar PV systems serving small-scale industries in Pakistan, while Shamim et al. 114 reported a shorter payback period of 6.4 years for a 420 kW grid-connected PV system operating under a net-metering scheme in Bangladesh. Similarly, Singh et al. 115 found payback periods of 9.4–11.3 years for large-scale solar PV plants in India. In contrast, Ayora et al. 116 reported a payback period of 9.1 years for a 600 kWp rooftop PV system in Kenya. Luqman et al. 117 reported a payback period of 11.4 years for a 1 MW grid-connected PV plant in Nigeria. It should be noted that the comparatively longer payback period obtained in the present study can be attributed to several factors. For instance, the analysis considers a relatively small-scale 10 kW residential PV system integrated with EVs, whereas most previous studies focused on larger commercial, industrial, institutional, or utility-scale installations that benefit from economies of scale and lower unit installation costs. Also, the inclusion of EV charging capability increases the initial capital investment, thereby extending the cost recovery period. In addition, differences in policy frameworks also influence project economics. In particular, Ghana's net billing scheme may generate lower revenues from exported electricity compared with the more financially attractive net-metering arrangements adopted in some of the reviewed studies. Furthermore, variations in solar resource availability, electricity tariffs, inflation rates, discount rates, and system costs across countries contribute to differences in payback periods. Therefore, the longer payback period observed in the present study demonstrates the combined influence of system scale, EV integration costs, economic assumptions, and the prevailing regulatory environment in Ghana.

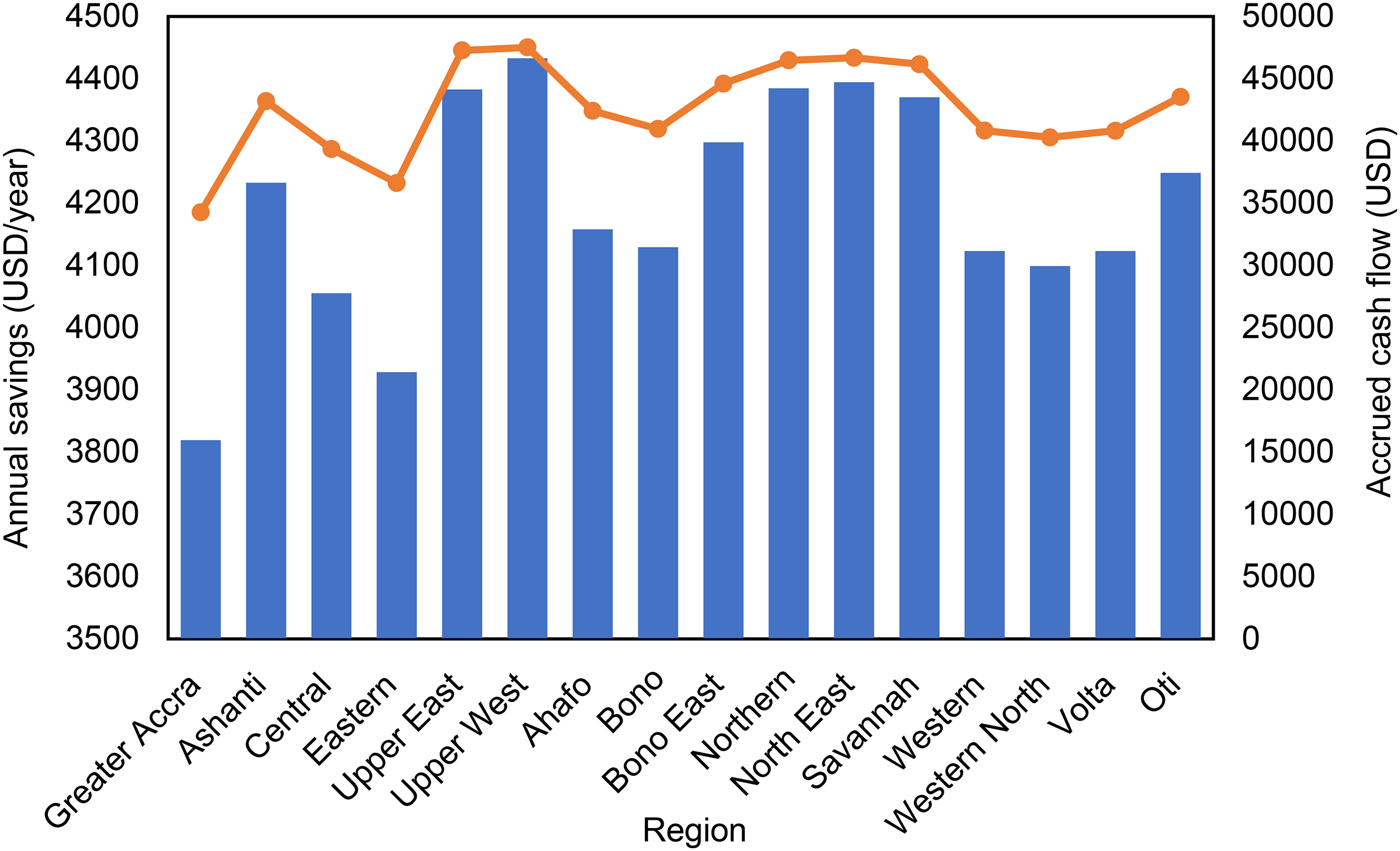

Figure 7 presents the annual savings and accrued cash flow. It can be observed that households across all regions can achieve substantial financial benefits. In northern Ghana, where solar is abundant, households can save up to USD 4370.1, USD 4382.6, and USD 4432.6 annually in the Savannah, Upper East, and Upper West Regions, respectively. These annual savings accumulate to USD 46,153.95, USD 47,255.98 and USD 47,509.45 over the system's operational life. In southern Ghana, solar resources are relatively lower; households could realise yearly savings of up to USD 3819.2, USD 4055.3, and USD 4122.9 in the Greater Accra, Central, and Western Regions, accumulating to USD 34,261.7, USD 39,343.52, and USD 40,812.14, respectively.

Annual savings and accrued cash flow.

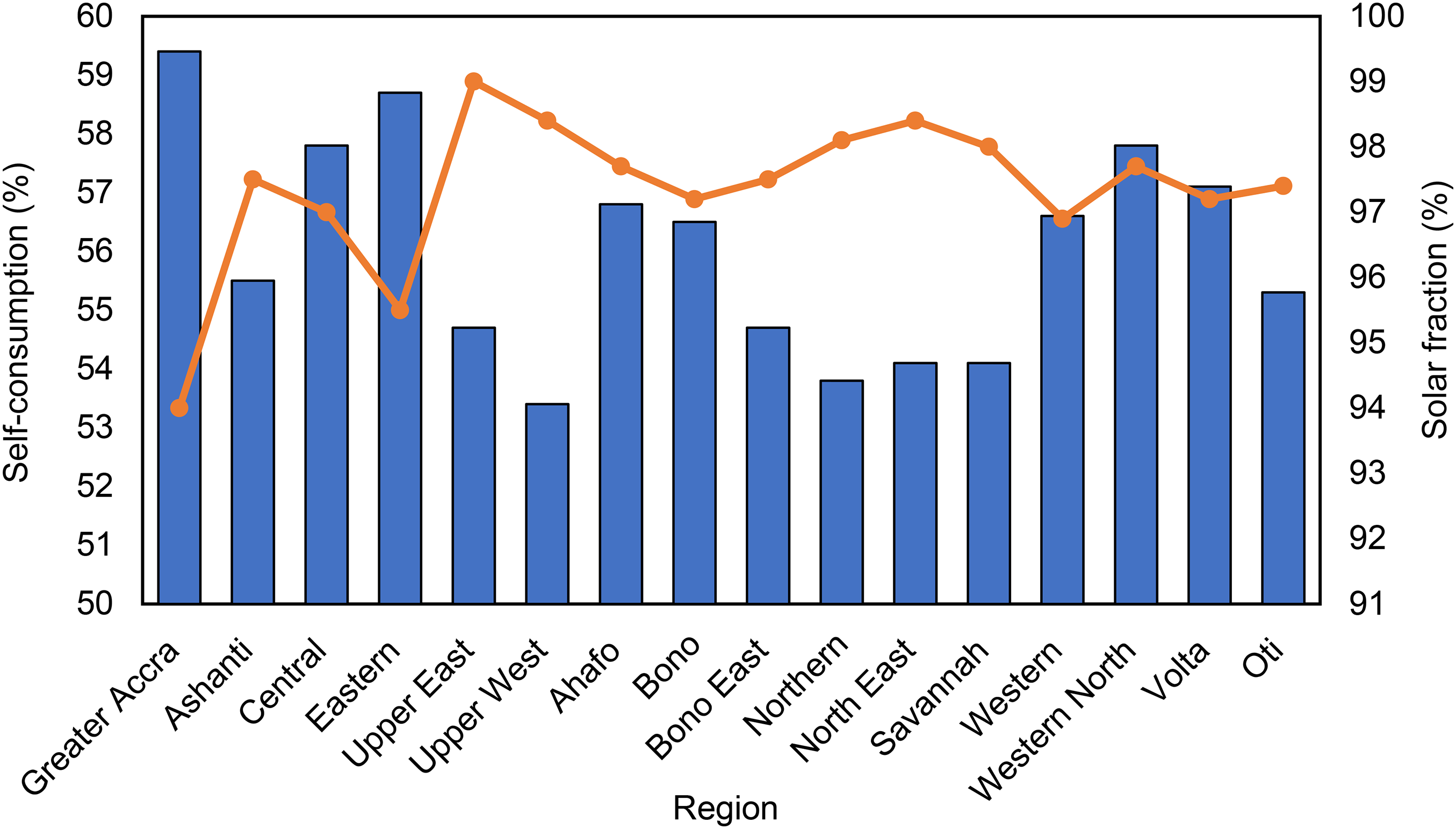

The household self-consumption and solar fraction are displayed in Figure 8. The self-consumption ratio is the proportion of PV-generated electricity consumed directly by the household. The results indicate that households consume 53.4% to 59.4% of the electricity produced from solar PV. In other words, almost half of the energy generated by the residential PV system was exported to the utility grid. The high proportion of electricity exported to the grid is due to the low daytime demand in the residential profile. Residential households in Ghana with monthly consumption over 300 kWh are compensated at 0.0783 USD/kWh for electricity exported to the utility grid, compared to import and retail rates of 0.1175 USD/kWh and 0.1958 USD/kWh, respectively (Table 6). The export rate corresponds to only about 40% of the retail rate, which is considerably lower than the bulk generation cost component, which constitutes about 62.2% of the electricity tariff. Under the current export rate offered to residential prosumers, it is economically advantageous for households to consume PV-generated on-site rather than export to the grid. 17 Consequently, the exportation of nearly half of the generated electricity, coupled with the importation of higher-cost grid electricity to meet night loads, negatively impacts the economic performance of the residential PV system in terms of BEV travel cost, payback period, annual savings, and accrued cash savings. Therefore, shifting demand to daytime, especially BEV charging, can improve self-consumption and enhance the overall economic performance of residential solar PV systems.

Household self-consumption and solar fraction.

Also, as shown in Figure 8, solar PV contributed substantially to household electricity consumption across all regions. The minimum solar fraction of 94% was recorded in the Greater Accra Region, whereas the Upper East Region recorded a solar fraction of 99%. The relatively lower solar fraction observed in Accra among Ghana's 16 regions is a contributing factor to the loan-financed residential PV system's generally poorer economic performance in the region.

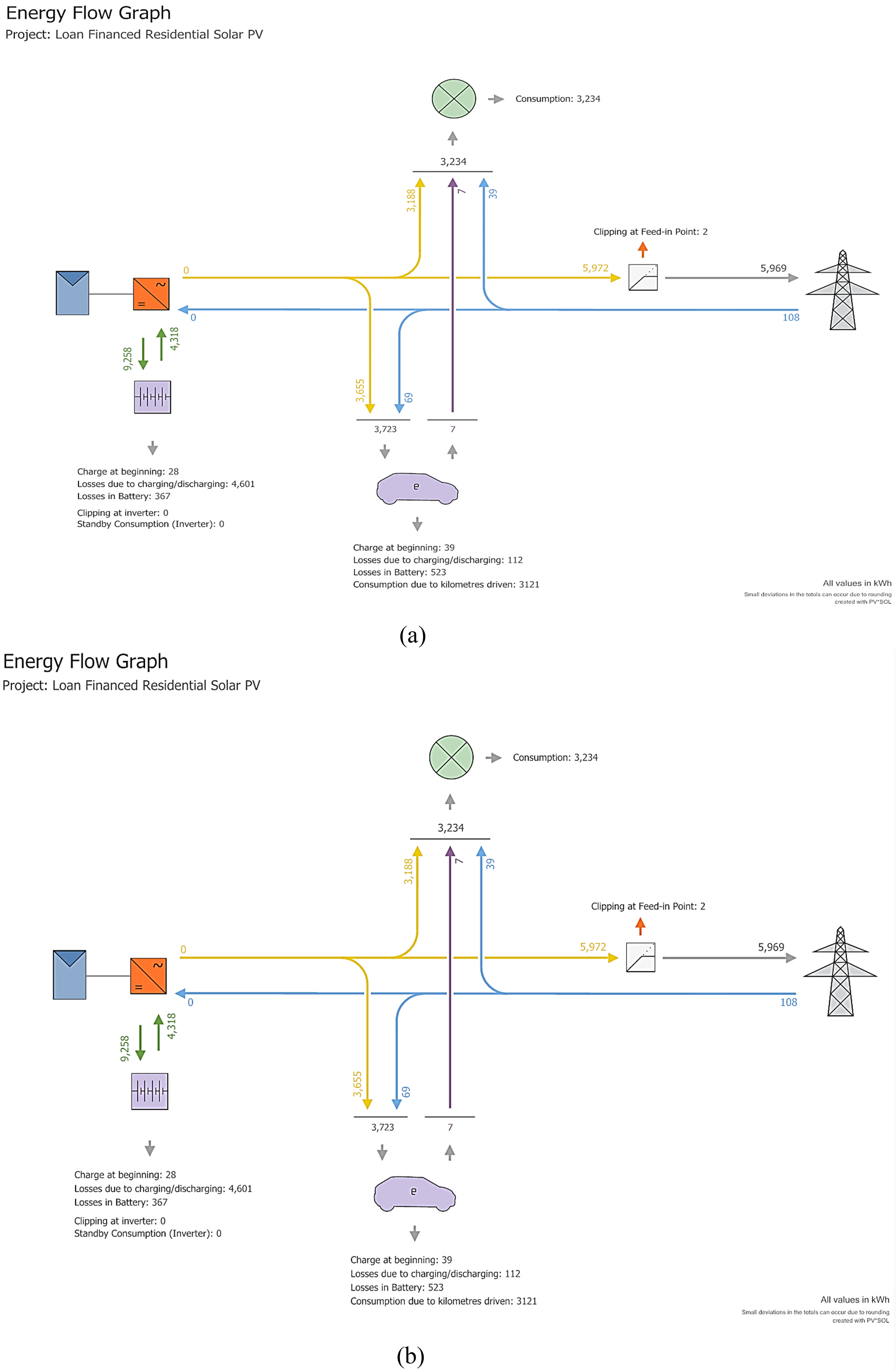

Figure 9 shows the energy flow diagram for the PV*SOL Premium simulated residential PV system in the Greater Accra and Upper West Regions. The figure provides details on annual PV generation and its distribution among self-consumption, battery storage, grid export, and grid import under Ghana's net billing conditions.

Energy flow distribution from residential solar PV systems in (a) Greater Accra and (b) Upper West Regions.

To evaluate the impact of loan repayment burden on residential households, Figure 10 presents the annual debt-to-income ratio for residential solar PV financing through loans across Ghana's 16 regions. The study reveals annual debt-to-income ratios ranging from 0.54 to 3.03 across the regions. The Ashanti region recorded the lowest debt-to-income ratio, while the Upper West recorded the highest. From the figure, it is observed that, except for the Greater Accra and Ashanti regions, the debt associated with financing residential solar PV with capacity to meet both household electricity and BEV charging demand substantially exceeds household incomes reported in GLSS7, adjusted to the July 2025 CPI, in Ghana cedis. For example, the debt-to-income ratio was 3 times higher in the Upper West Region and 2.4 times higher in the Upper East Region. Notably, the Upper East and Upper West regions, which yielded the best solar PV system performance, have the lowest financial capacity to fund the PV system through household incomes. Conversely, the Greater Accra Region, despite recording the poorest LCOE and BEV travel cost, demonstrated the second-highest financial capacity after the Ashanti Region. These results suggest that households would face significant challenges in financing residential solar PV through loans at a high interest rate (30%) and a short repayment period (3 years), reflecting prevailing financial market conditions in Ghana.

Household debt-to-income ratio for loan-financed residential solar PV systems across Ghana's regions.

Johnson and Li 98 reported that households with a high debt-to-income ratio are more likely to be denied credit by institutions such as banks. Furthermore, studies indicate that banks generally perceive financing small-scale renewable energy projects as risky and financially unattractive.24,31,32,33,27 Consequently, the high debt-to-income ratio observed in this study suggests that, under prevailing financial market conditions and based on Ghana's household income levels in GLSS7 adjusted to the July 2025 CPI Ghana cedis, households in the majority of Ghanaian regions are unlikely to secure loans for residential PV projects. Even in the Ashanti and Greater Accra regions, which recorded better debt-to-income ratios, values exceeding 0.5 indicate potential repayment difficulty, and households may still be denied loans.99,98 Additionally, households may carry other financial obligations, such as mortgages or vehicle loans, which would further increase the debt-to-income ratio and reduce the likelihood of obtaining credit. 98

Figure 11 shows the residual household income results after accounting for solar PV loan payments and essential expenses, ranging from -USD 9105.32 to -USD 5990.94. The negative residual income observed in most regions, except Greater Accra and Ashanti, further reinforces the assertion that households in the majority of regions may face significant challenges financing solar PV through loans with high interest rates and short repayment terms, based on income and expenditure levels reported in GLSS7, adjusted to 2025 CPI Ghana cedis. Kalemis and Upham 10 likewise observed that the high initial costs of solar PV systems and the limitations of existing financial models can create loan repayment challenges and financial burdens for vulnerable households in typical West African countries. Additionally, historical evidence suggests that solar companies in Africa tend to focus on market hotspots in more affluent regions, neglecting financially vulnerable areas. 50 Based on the results of the debt-to-income and residual income analysis, it is likely that solar companies and financial institutions providing loan facilities for residential solar PV in Ghana would prioritise regions such as the Greater Accra and Ashanti regions, where households demonstrate sufficient financial capacity to meet loan repayment obligations.

Residential household income after loan repayments.

Furthermore, Figures 12(a) and 12(b) display the annual debt-to-income ratio and residual income for the five household income quintiles in Ghana, ranging from the poorest (Q1) to the wealthiest (Q5) segments in GLSS7.

(a) Household debt-to-income ratios across income quintiles, (b) residual household income after loan repayments across income quintiles in Ghana.

It can be observed that the residual income was negative for all quintile groups. Only households in the highest quintile recorded debt-to-income ratios below 1. Generally, household annual debt-to-income ratios in the fourth to the lowest quintiles ranged from 1.11 to 5.04, indicating substantial financial strain in servicing solar PV loans. The results suggest that, based on incomes and expenditures in GLSS7, adjusted to the 2025 CPI, Ghana cedis, only households with very high incomes, representing the wealthier segment of society, may be able to obtain loans to finance residential PV with EV-charging capability. The observed high debt-to-income ratios align with findings from previous studies, which reported that while solar energy is a sustainable and renewable alternative to fossil fuels, financial constraints significantly limit its adoption among low-income households.10,12,13 Our results are consistent with those of Ojong, 52 which showed that lower-income households have limited access to loans from mainstream financial institutions for solar PV installations. Similarly, Kalemis and Upham 10 demonstrated that prevailing financial market conditions and high PV costs in Africa make solar unaffordable for low-income and vulnerable households.

Nevertheless, the negative residual income results observed even among the highest-income quintile (Figure 12(b)) suggest that, under high interest rates and short repayment periods, even affluent households may face challenges repaying loans for residential PV systems with EV-charging capability for BEVs. It is noteworthy that the use of indicators such as the debt-to-income ratio and residual income to assess the impact of loans on households can be subjective and has been widely criticised in the literature.99,98

Our results indicate that without adequate interventions and supportive governmental policies, households across most regions are likely to face significant financial challenges in financing residential solar PV systems with EV-charging capability through loans. Factors contributing to these challenges, as shown in this study, include the high upfront costs of PV systems, high interest rates, short loan repayment terms, and generally low household incomes. Such financial barriers hinder the equitable adoption of residential solar PV, particularly among low-income households, and consequently pose challenges to a just energy transition in Ghana.

Sensitivity analysis

The findings of this study show that the high loan interest rates and short repayment terms that typically characterise loans from financial institutions severely impact the economic performance of loan-financed residential solar PV systems. The loan repayment burden indicators also show that these loan conditions place a significant financial strain on households. Sensitivity analysis is therefore conducted to investigate alternative loan conditions, particularly changes in interest rates and repayment terms, that could enhance the feasibility of loan-financed residential solar PV systems. This study focuses on the loan interest rates and repayment periods because previous studies identify these factors as critical determinants of household access to solar financing from financial institutions such as banks.47,46 Although the sensitivity analysis covers interest rates from 30% to 0%, it is acknowledged that a 0% interest rate loan represents an idealised scenario unlikely to be feasible in Ghana's current economic context. Accordingly, the discussion emphasises a low-interest scenario around 5%, which aligns with soft-loan structures advocated in the related literature to promote residential PV adoption.83,85

Figure 13 displays the reduction in interest rates from 30% to 0% in 5% decrements, along with the economic performance of a 3-year loan facility used to finance a residential solar PV system across Ghana's 16 regions.

Impact of reducing loan interest rates on (a) LCOE, (b) BEV travel cost, (c) payback period, (d) accrued cash flow, (e) debt to income ratio, and (f) residual income.

Generally, the results show that all economic performance indicators improved substantially as loan interest rates decreased. For example, the LCOE across all regions, initially ranging from 0.4825 USD/kWh to 0.4072 USD/kWh, declined to 0.3853 USD/kWh to 0.3311 USD/kWh, representing a reduction of about 18.69% to 20.14%. Similarly, travel costs fell by 19.47% to 20.02%, decreasing from 0.0824 USD/km to 0.0914 USD/km, and then to between 0.0659 USD/km and 0.0736 USD/km. The average LCOE across the 16 regions reduced from 0.4342 USD/kWh to 0.3476 USD/kWh, while the average travel cost reduced from 0.0862 USD/km to 0.0693 USD/km. Notably, the reduction in interest rate had a greater impact on the LCOE than the travel costs.

However, despite the improvements, both LCOE and BEV travel costs remained considerably higher than utility electricity tariffs and grid-charged BEV travel costs. The average LCOE at baseline conditions is approximately 84.2% higher than the retail tariff for households in equivalent consumption blocks on the national grid. Even at an interest rate of 5%, the LCOE remained about 70% higher than the applicable utility tariff. Likewise, although average travel cost decreased from 0.0862 USD/km to 0.0693 USD/km as interest rates fell from 30% to 0%, it remains substantially above the average travel cost of 0.03955 USD/km for BEVs charged directly from the national grid.

Nevertheless, reductions in LCOE and travel costs associated with lower interest rates led to meaningful improvements in payback periods across all regions. For instance, the payback period in the Upper West Region decreased by almost 3 years, from 12.08 to 9.58 years, as interest rates fell from 30% to 0%. On average, the payback period decreased from 12.77 years to 10.16 years across Ghana's 16 regions.

Also, the reduction in loan interest rates resulted in a substantial improvement in annual savings and accrued cash flow. For instance, in the Eastern region, which has the lowest solar irradiation in Ghana, the accrued cash flow increased from USD 36,612.61 to USD 46,157.50, representing a 26.07% increase. In the Upper East region, which has the highest solar irradiation in Ghana, accrued cash flow increased from USD 47,255.98 to USD 55,956.64 (18.41%). Similarly, the accrued cash flow in the Greater Accra region rose by 27.89% from USD 34,261.7 at a 30% interest rate to USD 43,806.59 at a 5% interest rate.

Regarding household loan repayment burden, Figure 13 shows that as interest rates declined to 5%, most households’ incomes exceeded their annual debt obligations, with debt-to-income ratios ranging from 0.38 to 0.9. As interest rates fell to 0%, the debt-to-income ratio improved slightly, ranging from 0.35 to 0.84. However, in several regions, including Upper East, Upper West, Northern, North East, Savannah, and Eastern, households continued to record debt-to-income ratios above 1.0. Specifically, these regions recorded debt-to-income ratios ranging from 1.12 to 1.98 even at a 0% interest rate. Regarding residual income, all regions except Greater Accra and Ashanti continued to record negative residual income values even at a 0% interest rate, indicating persistent repayment difficulty. Previous research by Boamah and Rothfuß 46 highlighted that the typical 12-month repayment period required by banks in Ghana for solar PV loans is too short and discourages many potential borrowers. In agreement, this study's results on the debt-to-income ratio and residual income suggest that, based on household incomes reported in GLSS7, adjusted to 2025 CPI Ghana cedis, households in most regions would experience financial stress in repaying residential solar PV loans over short payment periods, even under very low-interest-rate scenarios. Such financial stress may deter households from adopting loan-financed residential solar PV. 46

To further assess the effect of concessional financing conditions, the study examined how declining interest rates influence both economic performance and loan repayment burden over a longer repayment period. Specifically, the study evaluated system performance as interest rates decreased from 30% to 0% under a 10-year repayment period, as illustrated in Figure 14.

Impact of reducing loan interest rates on (a) LCOE, (b) BEV travel cost, (c) payback period, (d) accrued cash, (e) debt-to-income ratio, and (f) residual income of residential solar PV systems with a 10-year loan across Ghana's regions.

From the Figure, at a 30% interest rate, extending the repayment period to 10 years significantly increases the LCOE compared to the 3-year repayment scenario. For example, the LCOE, which initially ranged from 0.4072 USD/kWh to 0.4825 USD/kWh for a 3-year repayment period, increased substantially to 0.5245 USD/kWh to 0.6327 USD/kWh for a 10-year repayment period at the 30% rate. Similarly, the travel cost increased from 0.0824 USD/km to 0.1010 USD/km and from 0.0914 USD/km to 0.1189 USD/km at 30% interest, as the repayment period increased from 3 years to 10 years. The average payback period also increased considerably, from 12.77 years to 16.89 years, as the repayment period was extended from 3 to 10 years at a 30% interest rate. These results are attributable to an increase in the financing cost of the residential PV system, which negatively impacted the system's LCOE, travel cost, payback period, and accrued cash flow.

Although extending the loan repayment duration adversely affected the economic performance indicators, it considerably reduced the household loan repayment burden. Debt-to-income ratios fell across all regions, from the initial range of 0.54–3.03 to 0.34–1.88. Residual incomes also improved across all 16 regions. For instance, residual income in the Upper West Region improved from −USD 9105.32 to −USD 4896.80 when the repayment period was extended from 3 to 10 years at the 30% loan interest rate. Thus, longer repayment terms at high interest rates reduce the economic performance of residential solar PV systems. However, they also alleviate household financial constraints by increasing residual incomes and decreasing debt-to-income ratios.

As loan interest rates declined from 30% to 0%, the economic performance of residential solar PV systems with a 10-year repayment period improved substantially, eventually surpassing that of the 3-year repayment scenario. For instance, the Upper West and Greater Accra regions had the lowest and highest LCOE values for the 10-year repayment period at an interest rate of 5%, respectively, at 0.3171 USD/kWh and 0.3749 USD/kWh. The corresponding LCOE values, which ranged from 0.3382 USD/kWh to 0.3999 USD/kWh for the same regions, were higher under the same 5% interest rate but with a 3-year repayment period. A similar pattern was observed for travel cost. Specifically, values declined to 0.0642–0.0717 USD/km for the 10-year repayment period, compared with 0.0684 USD/km and 0.0763 USD/km for the 3-year repayment period in the Upper West and Greater Accra regions, respectively. Payback periods and accrued cash flows also significantly improved under the extended repayment period as interest rates fell across all 16 regions. Despite these improvements, even under low interest rates, the LCOE of residential solar PV financed over 10 years remained nearly twice the prevailing electricity tariff for consumers on the national utility grid. Likewise, BEV travel costs remained roughly double those of households charging from the grid.

The loan repayment burden eased considerably as interest rates fell under the extended repayment period. Debt-to-income ratios decreased from the initial range of 0.54–3.03 for a 3-year loan at 30% interest to 0.14–0.76 at 5%. While some other regions, including Central, Ahafo, Bono, Bono East, Volta, and Oti, recorded moderate ratios around 0.3, Ashanti and Greater Accra showed the lowest ratios at 0.14 and 0.15, respectively. Low debt-to-income ratios are associated with a higher likelihood of loan approval by financial institutions. 99 Regarding residual income, Figure 14 shows that only the Upper East and Upper West regions recorded negative residual income at a 5% interest rate. As the interest rates declined further to 0%, debt-to-income ratios improved to 0.11–0.59, and all regions except Upper West recorded positive residual incomes. The substantial improvement in both economic performance and loan repayment burden as interest rates declined, particularly under extended repayment periods, demonstrates that soft-loan structures could make residential solar PV financing more attractive while reducing financial stress on households. Financial institutions traditionally regard long-term, low-interest loans for residential solar PV as high-risk ventures.34,35 However, several studies highlight the urgent need for financial and structural reforms to accelerate global transitions towards renewable energy technologies such as solar PV.15,14,16 In light of the high interest rates and short repayment periods that currently characterise loan offerings in Ghana, and the adverse impacts these conditions impose on the financial viability of residential solar PV systems,47,48,46 there is a clear need for substantial reductions in lending rates and extensions of repayment periods. Achieving this will require coordinated government intervention and targeted policy reforms to make residential solar PV adoption financially feasible for households.

Figure 15 displays the results for economic performance and loan repayment burden for a loan repayment period extended to 20 years, with interest rates declining by 30%–0%.

Impact of reducing loan interest rates on (a) LCOE, (b) BEV travel cost, (c) payback period, (d) accrued cash, (e) debt to income ratio, and (f) residual income, of residential solar PV systems with a 20-year loan across Ghana's regions.

Similar to the results observed under the 10-year loan repayment duration period, at high interest rates, the economic performance of residential solar PV systems financed over 20 years was poorer than that of systems financed over shorter repayment periods. At an interest rate of 30%, the LCOE ranged from 0.5715 USD/kWh to 0.7696 USD/kWh, while BEV travel costs ranged from 0.1167 to 0.1440 USD/km. Payback periods were prolonged, ranging from 17.08 to 23.00 years, and accrued cash flows were relatively low (USD 6055.20–28,467.10). These outcomes were inferior to those observed for the 3-year repayment period at the same interest rate.

In contrast, the extended repayment period substantially eased the household loan-repayment burden. At 30% interest, debt-to-income ratios ranged from 0.32 to 1.79, while residual income varied widely from -USD 4558.04 to USD 10,538.22. As interest rates declined, the economic performance indicators for the 20-year loan improved substantially and ultimately surpassed those of both the 3-year and 10-year repayment structures. Thus, at an interest rate of 5%, the LCOE decreased to a range of 0.2969 USD/kWh–0.3510 USD/kWh, and BEV travel costs dropped to a range of 0.0601 USD/km–0.0673 USD/km. Payback periods and accrued cash flows also improved substantially, ranging from 8.75 to 10.17 years and from USD 47,179.03 to USD 60,426.78, respectively. As interest rates fell to 0%, all performance indicators improved the most across all regions. LCOE values ranged from 0.2502 USD/kWh to 0.2959 USD/kWh, and BEV travel costs ranged from 0.0508 USD/km to 0.0572 USD/km. Despite these improvements, the resulting LCOE and travel cost values remain higher than the prevailing retail electricity tariffs and the cost of charging BEVs from the national grid.

In the context of GLSS7 household incomes adjusted to the July 2025 CPI, Ghana cedis, the results of debt-to-income ratios at 5% interest varied from 0.08 to 0.47 over the 20-year repayment period, indicating a range of household loan repayment burdens. Notably, all regions except Upper East and Upper West had debt-to-income ratios below 0.3, suggesting a favourable outlook for loan access for residential solar PV financing. Besides, residual incomes ranged from USD 272.32 to USD 15,368.58, indicating that all regions achieved positive household residual income at a 5% interest rate. Extending loan repayment periods to 20 years has been proposed as an effective way to reduce borrower payment burdens and improve affordability. 118 The findings of this study suggest that long-term, low-interest loans could make residential solar PV systems with BEV charging capability financially viable while minimising repayment stress on households in Ghana.