Abstract

We study the relation between audit committee accounting expertise, analyst following, and market liquidity. Our main results indicate that analyst following increases subsequent to the appointment of an accounting expert to the audit committee. We also provide evidence that accrual quality, as opposed to audit quality or management earnings forecasts, is the channel through which accounting expertise increases analyst following and improves analyst forecast properties. We also show that audit committee accounting expertise is related to higher trading volume and lower liquidity risk, supporting incentives for greater analyst following. Our study extends prior literature by providing evidence that audit committee accounting expertise enhances firms’ information environment beyond the effects it has on financial reporting quality or analysts’ forecast properties. Our study also complements the literature on determinants of analyst following and market liquidity, both of which are related to cost of capital. Results from our study should be useful to firms seeking to enhance analyst following and market liquidity.

Introduction

In this study, we examine the relation between accounting expertise on the audit committee and analyst following. Boards of directors improve their performance by delegating authority to standing committees, such as the audit committee, that specialize in narrowly defined functions (Klein, 1998). We study accounting expertise as a primary feature of audit committee composition that prior research finds is related to enhanced financial reporting (Carcello, Hollingsworth, Klein, & Neal, 2008; Dhaliwal, Naiker, & Navissi, 2010; Krishnan & Visvanathan, 2008). We extend prior research by providing a more complete understanding of the effect of audit committee accounting expertise on firms’ broader information environment beyond financial reporting, as proxied by analyst following and market liquidity. Understanding the relation between audit committee accounting expertise, analyst following, and market liquidity has important implications for firms seeking greater analyst coverage and lower cost of capital, as well as for regulators concerned with audit committee effectiveness.

Prior research finds that audit committee accounting expertise is associated with greater forecast accuracy and reduced forecast dispersion (Abernathy, Herrmann, Kang, & Krishnan, 2013). 1 However, it does not necessarily follow that accounting expertise will also lead to increased analyst following. While Lang and Lundholm (1996) show that firms with more informative disclosures have greater analyst following and better forecast properties, Lehavy, Li, and Merkley (2011), in contrast, show that firms with more complex disclosures have greater analyst following but worse forecast properties. As Lang, Lins, and Miller (2003) argue, analyst forecast accuracy could operate independently from analyst following because of information gathering by other capital market intermediaries (e.g., buy-side analysts) and/or because firms disclose more information. It is therefore an open empirical question as to whether audit committee accounting expertise affects analyst following.

Theoretically, Bushman, Piotroski, and Smith (2004) argue that governance mechanisms and analysts are “interrelated information mechanisms” (p. 210), suggesting that analysts likely respond to audit committee composition. Consistent with theory, professional practice standards require analysts to incorporate information from governance disclosures in their decision making (CFA Institute, 2005). Prior research demonstrates that analyst following increases with higher Standard & Poor’s rankings of board structure disclosures (M. Yu, 2009). In addition, surveys report that both buy-side and sell-side analysts consider weak corporate governance as one of the two highest indicators of intentional misreporting and more than 75% of sell-side analysts report that corporate governance is a factor in their decision to cover a company (Brown, Call, Clement, & Sharp, 2015, 2016).

We hypothesize that analyst following increases after the appointment of accounting experts to the audit committee. Because analysts monitor management (Jung, Sun, & Yang, 2012), enhanced monitoring by audit committee accounting experts may reduce analysts’ costs to follow a firm, leading to a complementary relation between analysts and audit committee accounting expertise. For example, prior survey research finds analysts report higher confidence in financial reporting quality when an accounting expert is on the audit committee compared with other types of expertise (Dickins, Hillison, & Platau, 2009). In the spirit of Lang and Lundholm (1996), we also expect analysts to be attracted to firms with audit committee accounting expertise because these firms have higher financial reporting quality than firms with other types of audit committee expertise (Carcello et al., 2008). However, we may not find results consistent with our hypothesis if improved financial reporting associated with audit committee accounting expertise reduces analysts’ competitive advantage, leading to decreased analyst coverage (Lehavy et al., 2011). Providing further support for analysts’ incentives to follow the firm, we also expect greater market liquidity for firms with audit committee accounting expertise because of an improved information environment (Healy, Hutton, & Palepu, 1999).

We execute our tests with a random sample of 460 firms over the period 1998-2003. This time period provides a powerful setting for our study because firms were likely to change their audit committee composition to include, for the first time, members with accounting expertise due to the influence of both the Blue Ribbon Committee (BRC) and the Sarbanes–Oxley Act (SOX). For our main test, we construct panel data for the 131 sample firms that appointed an accounting expert to the audit committee during our sample period and use a time-series approach to address potential endogeneity issues (Healy et al., 1999; Hermalin & Weisbach, 2003). Because the dependent variable (i.e., analyst coverage) is a non-negative integer, we use a Poisson model to estimate our main regression.

We find that analyst following increases after the appointment of an accounting expert to the audit committee, even after controlling for other governance strength, institutional investors, the number of analysts employed by the brokerage firm, analyst effort, firm size, growth, profitability, trading volume, security offerings, return volatility, intangibles, year-fixed effects, and firm-fixed effects. Our results are robust to using alternative analysis periods, a pooled cross-sectional model, non-accounting expertise, across the pre- and post–Reg FD periods, an alternative measure of governance strength, and across the pre- and post-SOX periods. Our results are also robust to using a negative binomial model and a Tobit model to control for the count data nature of analyst following (Rock, Sedo, & Willenborg, 2001).

To provide deeper insights into our main result, we test three potential channels through which accounting expertise could affect analyst following: (a) audit quality, (b) management earnings forecasts (MEFs), and (c) accrual quality (AQ). Results indicate that accounting expertise increases analyst following only through the channel of enhanced AQ. That is, we find that the impact of the appointment of an accounting expert on analyst following is significantly greater when AQ is higher, but no effect from audit quality or MEFs. In additional tests, we first replicate results from Abernathy et al. (2013), who find that analyst forecast errors and dispersion are lower following the appointment of accounting experts to the audit committee. Extending Abernathy et al. (2013), we find that accounting expertise on the audit committee has a significant economic impact on forecast properties through the AQ channel, but not through audit quality or MEFs.

Despite our efforts to control for known factors related to analysts’ decisions and our use of firm-fixed effects, results in Brown et al. (2015) suggest that analysts’ incentives to follow firms are not clear. We therefore provide evidence about whether accounting expertise generates positive capital market effects. To do so, we assess the relation between accounting expertise and both trading volume and liquidity risk (Liu, 2006), factors related to cost of capital. The intuition is that audit committee accounting expertise improves firms’ information environment, leading to increased investor interest in firms’ stocks. We report a positive (negative) relation between trading volume (liquidity risk) and accounting expertise, suggesting that accounting expertise provides significant capital market benefits beyond enhanced financial reporting, increased analyst following and enhanced analyst forecast properties. These results also support analyst incentives to follow a firm (Healy et al., 1999).

Our study makes several important contributions to the literature. First, given that analysts are an important aspect of a firm’s information environment (Bushman et al., 2004), our findings are consistent with audit committee accounting expertise having a profound impact on firms’ information environment, beyond that provided by its impact on single dimensions of financial reporting, such as AQ. Furthermore, our results suggest that accounting experts enhance analyst following through their monitoring of accruals. Because analysts proxy for sophisticated investors and influence investors (Mikhail, Walther, & Willis, 2007; Schipper, 1991), our evidence also suggests that audit committee accounting expertise helps to enhance investor confidence in financial reporting. Since firms realize significant benefits from analyst following, 2 evidence of a positive relation between analyst following and audit committee accounting expertise should be useful to firms seeking to enhance analyst coverage.

Second, we extend Abernathy et al. (2013). While Abernathy et al. (2013) attempt to assess whether accruals are the channel through which accounting expertise impacts forecast accuracy and dispersion, they perform an indirect test by including AQ as a control variable and find that it has a weak economic impact on results. In contrast, we perform a direct test by including the interactive effect of accounting expertise and accruals quality on analyst forecast properties and find much stronger economic significance than in Abernathy et al. (2013). Moreover, we test two other channels, audit quality and MEFs, and do not find an interactive impact. We therefore provide comprehensive and compelling evidence about the channels through which accounting expertise affects analyst forecast properties.

Finally, our study is the first to provide evidence about the relation between accounting expertise and market liquidity. Evidence about the relation between accounting expertise and both analyst following and liquidity is related to a fundamental issue in accounting research—cost of capital—that has been investigated in other settings. See, for example, Previts, Bricker, Robinson, and Young (1994); Chung and Jo (1996); Lang and Lundholm (1996); Healy et al. (1999); Botosan and Harris (2000); Barth, Kasznik, and McNichols (2001); and Tucker (2010). Our article therefore complements important streams of accounting literature that have assessed determinants of analyst following and market liquidity, both of which are related to cost of capital.

The remainder of the article is organized as follows. “Institutional Background, Related Literature, and Hypotheses” section provides background and develops our hypotheses. “Sample and Univariate Results” section describes our sample and data. “Empirical Design and Multivariate Regression Results” section contains the main empirical results. We investigate channels though which accounting expertise improves analyst following in “Potential Channels Through Which Accounting Expertise Affects Analyst Following” section. We provide supporting analyses of analyst forecast properties in “Information Quality of Analysts’ Forecasts” section. “Capital Market Consequences of Audit Committee Accounting Expertise” section provides capital market evidence on the impact of accounting expertise. We summarize and conclude the study in “Summary and Conclusion” section.

Institutional Background, Related Literature, and Hypotheses

Institutional Background

The primary role of the audit committee is to oversee the financial reporting process and ensure high-quality financial reporting. The Securities and Exchange Commission (SEC) has long recommended that companies utilize audit committees (SEC, 1940). Regulators now focus more on the composition of the audit committee. In 1999, in response to concerns that audit committees were not effective in their monitoring role, the New York Stock Exchange (NYSE) and the National Association of Securities Dealers (NASD) collaborated to form the BRC on improving the effectiveness of corporate audit committees. The BRC recommended that audit committee composition include at least three “financial literates,” at least one of whom is a “financial expert” (BRC on Improving the Effectiveness of Corporate Audit Committees, 1999). The financial analysts’ professional association, Association for Investment Management and Research (AIMR), 3 supported the BRC recommendations for the composition of the audit committee, suggesting that analysts consider audit committee composition important (AIMR, 1999). The U.S. stock exchanges quickly adopted the BRC’s recommendations with SEC approval in late 1999.

Section 407 of SOX underscores the importance of audit committee financial expertise by requiring registrants to disclose the name of at least one member on the audit committee who is a financial expert or disclose the reason for not having such an expert. SOX recommended a narrow definition that required a direct accounting background, but left the final definition to the SEC. The SEC’s initial definition of audit committee financial expertise was also narrow and highly controversial. Among others, AIMR indicated its support for the narrow definition of financial expertise (AIMR, 2002). 4 In its final rule, the SEC allowed firms to use a broad definition of financial expertise that includes direct accounting work experience, but also includes financial reporting supervisory experience (e.g., CEOs) or experience analyzing or evaluating financial statements (e.g., investment bankers).

Related Literature

Researchers have devoted considerable effort to studying the relevance of the broad and narrow definition of financial expertise. Using the broad definition, prior research finds that firms with audit committee financial expertise, compared with those without it, are less likely to restate earnings (Abbott, Parker, & Peters, 2004; Agrawal & Chadha, 2005), less likely to dismiss their auditor following a going concern report (Carcello & Neal, 2003), less likely to engage in earnings management (Bedard, Chtourou, & Courteau, 2004), more likely to update a voluntary earnings forecast (Karamanou & Vafeas, 2005), and more quickly dismiss the audit firm of Arthur Andersen following the Enron scandal (Chen & Zhou, 2007).

Other research examines the consequences of the narrow definition of financial expertise. Using a pre-SOX setting, Krishnan and Visvanathan (2008) find that only audit committee accounting expertise is related to more conservative accruals. Also using a pre-SOX setting, DeFond, Hann, and Hu (2005) find positive 3-day abnormal returns around the appointment of accounting, but not non-accounting, experts to the audit committee. Our study differs from DeFond et al. (2005) in that we assess analyst response to audit committee appointments pre- and post-SOX. Engel (2005) indicates that because of the significant regulatory shift post-SOX, it is not clear that results in DeFond et al. (2005) would hold in a post-SOX setting.

In the post-SOX period, Carcello et al. (2008) find that both accounting and non-accounting expertise are related to lower abnormal accruals. However, using a larger sample, Dhaliwal et al. (2010) report that audit committee accounting expertise is most strongly related to higher AQ when the accounting experts are independent, hold fewer other directorships, have shorter tenure, and when the audit committee also includes a member with a finance background. Dhaliwal et al. (2010) find no evidence of a similar relation between AQ and audit committee members with supervisory expertise.

Two prior studies also examine the association between board characteristics and analyst forecast properties, but not analyst following. In an article somewhat related to ours, Byard, Li, and Weintrop (2006) assess the relation between analyst forecast accuracy and four governance variables: (a) board independence, (b) audit committee independence, (c) CEO duality, and (d) board size. Byard et al. (2006) show that analyst forecast accuracy is positively associated with board independence and board size and negatively associated with CEO duality; they find no association between analyst forecast accuracy and audit committee independence, however. Abernathy et al. (2013) show that accounting expertise on the audit committee is related to higher analyst forecast accuracy and lower analyst forecast dispersion. We extend these studies by examining the relation between accounting expertise on the audit committee and analyst following.

Although analyst following and forecast accuracy are sometimes positively related, this is not always the case. Lehavy et al. (2011) show that firms with more complex disclosures have greater analyst following even though analyst forecast errors and dispersion both increase. As Lang et al. (2003) argue, although analyst forecast accuracy could improve because more analysts follow a firm, analyst forecast accuracy could also operate independently from increased analyst following because of information gathering by other capital market intermediaries (e.g., buy-side analysts), and/or because firms disclose more information. Related to this latter point, Abernathy et al. (2013) report that higher quality accruals associated with accounting expertise help drive the relation between accounting expertise and forecast properties. It is, therefore, an open empirical question as to whether audit committee accounting expertise affects analyst following.

Hypotheses Development

Theoretical and empirical studies, in addition to standards of professional practice, provide support for a plausible link between audit committee accounting expertise and analyst following. Bushman et al. (2004) suggest a theoretical link between corporate governance mechanisms, such as audit committee composition, and analysts. Analysts acquire private information by interacting with management and the board, by touring plant facilities, and by analyzing industry conditions and trends, and so on. Analysts then aggregate public and private information for dissemination to investors (Bushman et al., 2004). Thus, analysts and corporate governance mechanisms are “interrelated information mechanisms” (Bushman et al., 2004, p. 210) that contribute to firms’ transparency.

Empirically, M. Yu (2009) shows that analyst following increases with Standard & Poor’s transparency and disclosure rankings of board structure disclosures, suggesting analysts utilize information from these disclosures. Lang and Lundholm (1996) and Healy et al. (1999) show that analyst following is increasing in the quality of firm disclosures, including those in proxy statements where audit committee expertise is disclosed. Finally, Dickins et al. (2009) report survey evidence that analysts have more confidence in financial reporting from firms with audit committee accounting expertise.

Professional practice also suggests that analysts evaluate the audit committee. The Certified Financial Analyst (CFA) exam covers corporate governance best practices, including expertise of the board and its committees (Robinson & Wiese, 2010). 5 A 1999 survey of financial analysts indicated that analysts believed that boards of directors were doing a poor job (Epstein & Palepu, 1999), suggesting that analysts evaluated board-level corporate governance prior to SOX. As noted above, analysts’ professional association supported the BRC recommendations in 1999, implying that analysts are specifically concerned with the quality of the audit committee.

We hypothesize a positive relation between audit committee accounting expertise and analyst following. Analysts’ decisions to follow a firm depend on the costs and benefits of doing so (Barth et al., 2001). We argue that audit committee accounting expertise lowers the costs of following a firm because analysts are able to rely more on public information and less on costly private information acquisition activities. This is because audit committee accounting expertise improves the quality of financial reporting (Carcello et al., 2008; Dhaliwal et al., 2010; Krishnan & Visvanathan, 2008) and higher quality corporate reporting is associated with greater analyst following (Arya & Mittendorf, 2007; Bhushan, 1989; Healy et al., 1999; Lang & Lundholm, 1996; M. Yu, 2009). In addition, analysts facilitate monitoring of managers, reducing insiders’ information advantages, and constraining management’s asset-wasting behavior (Ellul & Panayides, 2011; Jung et al., 2012). If so, then accounting expertise may support analysts’ monitoring efforts, again reducing the cost of following the firm.

However, a competing theoretical argument suggests enhanced information from corporate reporting could reduce analysts’ competitive advantage, thus decreasing incentives for private information acquisition (Lang & Lundholm, 1996; Lehavy et al., 2011). If so, the decreased incentives suggest a negative relation between accounting expertise and analyst following. Despite this competing argument, we expect that the arguments supporting a positive relation between accounting expertise and analyst following will outweigh the arguments supporting a negative relation due to the deeper prior literature that finds a positive relation between enhanced corporate reporting and analyst following and due to the positive views of analysts toward accounting expertise expressed in practice (e.g., AIMR, 1999). Thus, our first hypothesis states as follows:

To the extent that audit committee accounting expertise is associated with an improvement in firms’ information environment, we also expect greater market liquidity for these firms. We base our prediction on Healy et al. (1999), who show a positive relation between firm disclosure and market liquidity. The intuition for our second hypothesis is that audit committee accounting expertise improves firms’ information environment, leading to increased investor interest in firms’ stocks. Thus, our second hypothesis states as follows:

Support for H2 would be consistent with analysts’ incentives to increase coverage of firms with audit committee accounting expertise because market liquidity creates additional analyst interest in firms (Healy et al., 1999).

Sample and Univariate Results

Sample

We hand-collect data for audit committee expertise from firms’ annual proxy statements. 6 Because hand-collecting this data is non-trivial, we randomly select 500 firms across the S&P 1500 from the intersection of Institutional Brokers’ Estimate System (I/B/E/S), Compustat, Investor Responsibility Research Center (IRRC), First Call, and the Center for Research in Security Prices (CRSP) data sets over the years 1998-2003. This time period is important because many firms were likely changing their audit committee accounting expertise in response to SOX. For each firm, we obtain the name and business experience of each audit committee member from the background information provided on board members in the firm’s proxy statements.

We follow prior literature and partition our sample based on both accounting and other types of expertise (e.g., DeFond et al., 2005; Krishnan & Visvanathan, 2008). In our primary analyses, we test accounting expertise. In sensitivity tests, we use other measures of financial expertise. Thus, we code categories of expertise as follows:

Accounting expertise: Individuals with current or previous experience as Vice President of finance, CFO, controller, or other principal financial or accounting officer of a publicly traded company, or as a CPA in public practice, consistent with the SEC’s initial proposed definition of a financial expert (SEC, 2003).

Supervisory expertise: Individuals with current or previous experience as a CEO or president of a publicly traded company, consistent with the SEC’s final definition of financial expertise.

Finance expertise: Individuals with current or previous experience in investment banking, working at the SEC, loan/credit rating experience, or financial analyst experience, also consistent with final SEC rules (SEC, 2003).

Other: Individuals with experience that does not fall into any of the above categories.

Some individuals appointed to an audit committee have experience in multiple categories. To ensure that each individual is counted in only one category, we use the following ranking when coding: (1) accounting expertise, (2) finance expertise, (3) supervisory expertise, and (4) other. This ranking process means, for example, that while some members with accounting expertise also have finance expertise, the finance expertise category does not include members with accounting expertise, and so on.

We obtain analyst data from the detail file in I/B/E/S and data for control variables from Compustat, CRSP, and IRRC. After deleting firms with incomplete proxy filings or missing data for certain variables, our final sample consists of 2,342 firm-years and 460 unique firms, of which 267 are firms with accounting expertise (sample firms) and 193 are firms without accounting expertise on the audit committee (control firms). We winsorize all variables at the 1% and 99% levels to mitigate the impact of outliers. This initial sample is used in a number of sensitivity tests. For the main tests, we construct a panel of the 131 firms that appointed an accounting expert from 1998-2003. In Table 1, we present the classification of industries across the 131 firms used in the main analyses, demonstrating that the sample is from a broad spectrum of industries.

Industry Classification of Sample Firms.

Note: SIC=Standard Industrial Classification.

Univariate Results

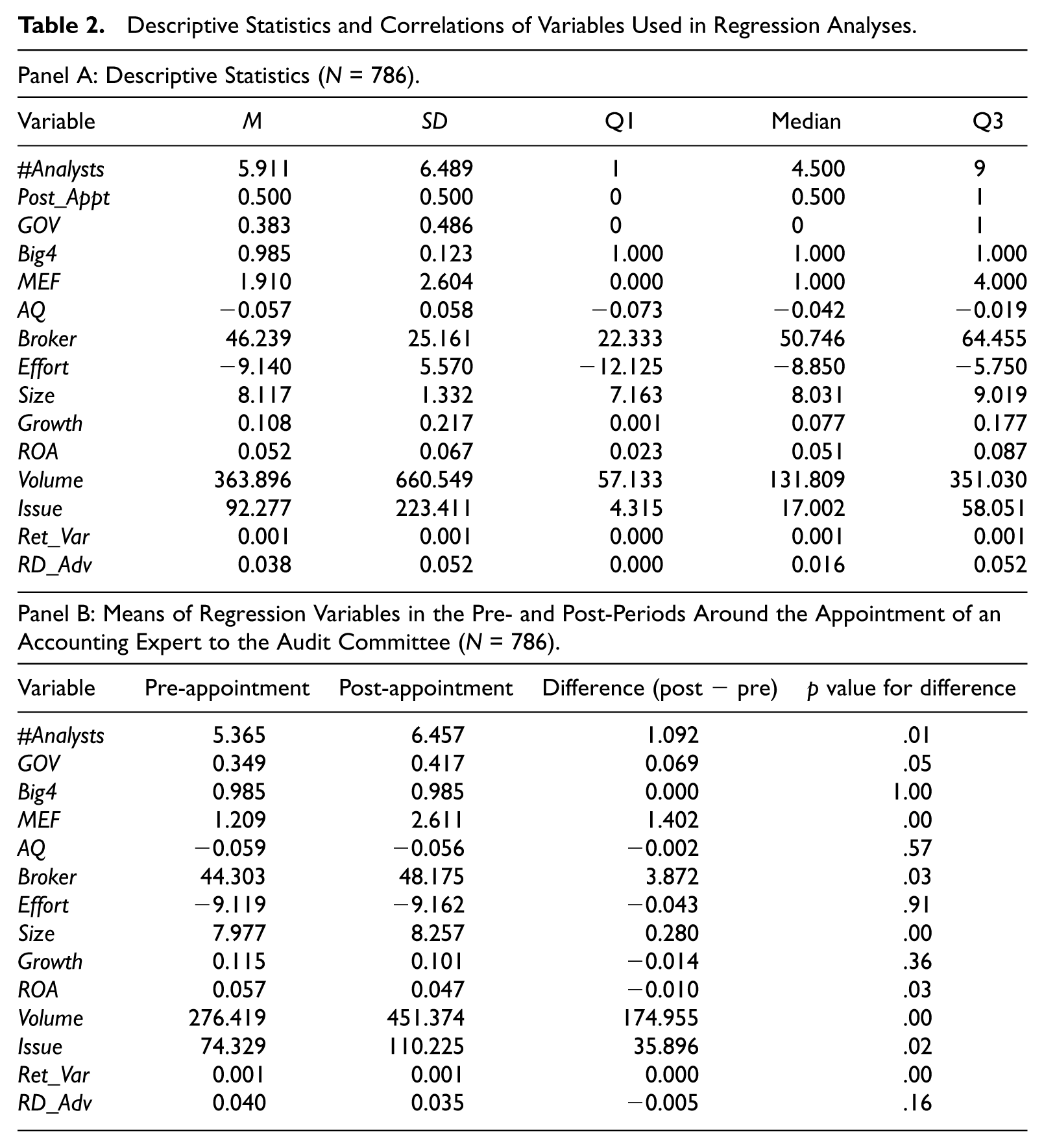

Panel A of Table 2 provides descriptive statistics for the variables used in the regression analyses (for the 786 firm-years included in panel A). The mean analyst following is about six. Panel B of Table 2 provides descriptive statistics for the variables by pre- and post-appointment of an audit committee accounting expert. This panel shows a mean increase of about one analyst between the pre- and post-appointment periods, consistent with H1. This panel also shows a significant increase in trading volume, consistent with H2.

Descriptive Statistics and Correlations of Variables Used in Regression Analyses.

Note. Variable definitions: #Analysts is the number of analysts with annual earnings forecasts in the month closest to, but preceding, the annual earnings announcement adjusted by subtracting the industry median. Post_Appt is a dummy variable equal to one for the 3 years following the appointment of an accounting expert and zero for the 3 years prior to the appointment of an audit committee accounting expert. GOV is an aggregate governance measure that is comprised of the following components: board size, board independence, audit committee size, audit committee independence, G-index (Gompers, Ishii, & Metrick, 2003), and institutional ownership. Please refer to DeFond, Hann, and Hu (2005), for details of each of these components. Each component equals one if it exceeds the sample median and zero otherwise. We sum the components and create a dichotomous variable equal to one if the sum exceeds the median of the summed values of all observations. Big4 is a dummy variable equal to one for firms with a Big4 auditor. MEF is the number of annual management earnings forecasts in fiscal year t. AQ is total abnormal accruals multiplied by −1; we follow Kothari, Leone, and Wasley (2005) and compute unsigned abnormal accruals using a modified version of the Jones (1991) model with performance matching based on return on assets. Broker is the average number of analysts employed by the brokerage houses of the firm’s analysts. Effort is the negative of the average number of firms covered by the firm’s analysts. Size is the natural log of market capitalization (in US$ million). Growth is the firm’s prior 5-year sales growth. ROA is the mean of prior 5 years’ return on assets (net income divided by total assets). Volume is trading volume (in millions of shares). Issue is the dollar amount of the issuance of public debt or equity in the current or prior year. Ret_Var is daily stock return variance estimated over the 200 days prior to the end of the fiscal year. RD_Adv is the sum of research and development and advertising expenses scaled by sales.

Panel C of Table 2 reports the Pearson correlations between the variables used in the regression analyses. There is a positive and significant correlation between analyst following and the appointment of an audit committee accounting expert, providing univariate evidence consistent with H1. There is also a positive and significant correlation between trading volume and the appointment of an audit committee accounting expert, consistent with H2. Although most of the variables are correlated at fairly low levels, we nevertheless perform formal tests for collinearity in our regression analyses. 7

Empirical Design and Multivariate Regression Results

Empirical Design

Our first dependent variable of interest is analyst following. We use panel data for the sample of firms that appoint accounting experts to the audit committee to examine the impact of these appointments on changes in analyst following. An important issue with this approach is the time over which to expect the change in analyst behavior. In other words, is there an immediate effect, or does it take time for the new audit committee member to have an impact? It is reasonable to assume that a new audit committee member requires time to understand the intricacies of his or her firm’s business and thus be in a position to influence a firm’s disclosures. In the spirit of Lang et al. (2003), we therefore examine whether analyst following changes from 3 years prior to the appointment of an accounting expert on the audit committee to 3 years afterward. We use a time-series specification to avoid self-selection bias. To execute our test, we use the following model:

where #Analysts is the number of analysts (adjusted for the median of analyst following in the firm’s industry) 8 with annual earnings forecasts in the month closest to, but within a preceding 3-month window of, the annual earnings announcement (Barth et al., 2001). 9 Our variable of interest, Post_Appt, is equal to one for the 3 years following the accounting expert appointment and zero for the 3 years prior to the appointment.

To control for the effect of other governance mechanisms, we use the composite variable, GOV. Following DeFond et al. (2005), we aggregate board size, board independence, audit committee size, audit committee independence, G-index (Gompers, Ishii, & Metrick, 2003), and institutional ownership. 10 Each component equals one if it exceeds the sample median and zero otherwise. We sum the components and create a dichotomous variable, GOV, equal to one if the sum exceeds the median of the summed values of all observations.

Because of the mechanical relation between the size of the brokerage firm that covers a firm and the number of analysts that cover a firm, we include the variable, Broker, the average number of analysts in the brokerage houses that cover a firm (Barth et al., 2001). Barth et al. (2001) also report that firms requiring more analyst effort have lower analyst following, so we include the negative of the average number of firms covered by the firm’s analysts (Effort).

We include controls for firm size (Size), measured as the log of market capitalization at the end of the fiscal year, and growth (Growth), measured as the average sales growth over the 5 prior years (Bhushan, 1989; Lang & Lundholm, 1996; O’Brien & Bhushan, 1990). Following Ali, Chen, and Radhakrishnan (2007), we include a control for firm profitability, ROA, measured as net income divided by total assets.

Following Barth et al. (2001), we control for analysts’ incentives to follow a firm and include the variables volume and issue. Volume is a firm’s trading volume and reflects potential trading commissions to brokerage houses. Because analysts are compensated for trade in stocks that they cover (Irvine, 2000), analyst following is likely to increase with trading volume. Also, firms that issue public securities generate investment banking fees that brokerage houses value. We measure issue as the dollar magnitude of issuances of either public debt or equity in the current or prior year. We include a control for return variance, Ret_Var, because firms with higher return variance are likely to have higher expected trading profits, leading to increased analyst following (Bhushan, 1989). We measure Ret_Var using daily stock return variance estimated over the 200 days prior to the end of the fiscal year.

Firms with more intangible assets are likely to have less informative financial statements, thus providing incentives to analysts with superior skills to generate trading profits for their clients (Barth et al., 2001). We use the variable RD_Adv, the sum of research and development expenses and advertising expenses divided by sales, to control for this effect. Finally, we control for year- (YearDum) and firm-fixed (FirmDum) effects.

Main Regression Results

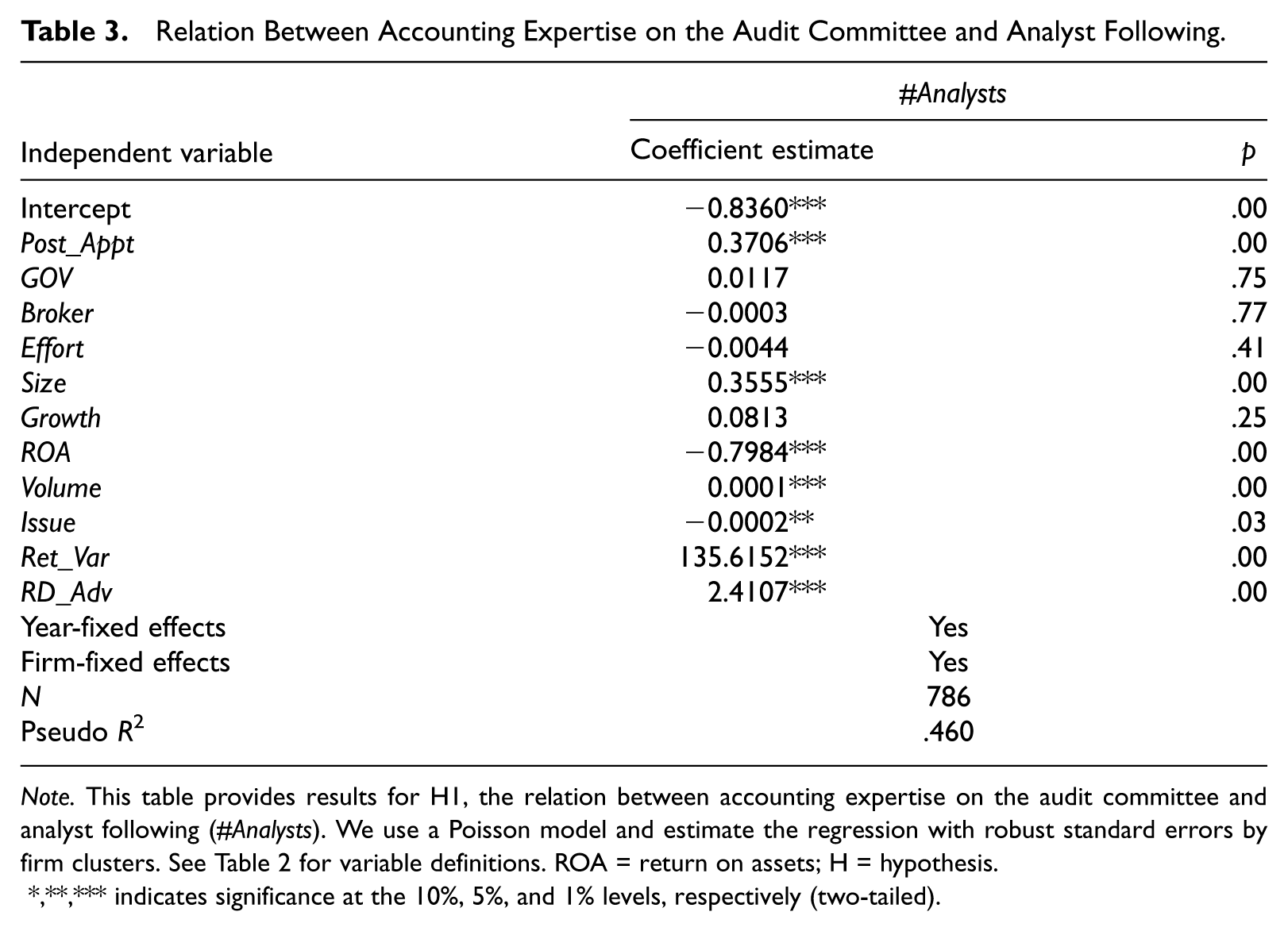

We use a Poisson model to estimate Equation 1 and report results after adjusting for firm clusters. 11 Consistent with H1, results in Table 3 show a positive and significant coefficient of 0.3706 (p < .01) on Post_Appt, implying that analyst following increases following the appointment of an accounting expert to the audit committee. 12 This result is consistent with the univariate results in panel B of Table 2. We next assess the economic significance of this result. Because a Poisson regression coefficient represents the change in response (natural logged response) corresponding to a one unit change in the corresponding predictor, we need to exponentiate results to obtain the percentage change in analyst following. Doing so yields a value of 1.45 (i.e., exp(0. 3706) = 1.45). This result implies that firms appointing an accounting expert to their audit committees experience a 45% increase in analyst coverage. Given that median analyst coverage is 4.5, the addition of an audit committee accounting expert results in about two additional analysts for a typical firm. Thus, our results are economically significant. Results for the coefficients on the control variables are generally consistent with prior research.

Relation Between Accounting Expertise on the Audit Committee and Analyst Following.

Note. This table provides results for H1, the relation between accounting expertise on the audit committee and analyst following (#Analysts). We use a Poisson model and estimate the regression with robust standard errors by firm clusters. See Table 2 for variable definitions. ROA = return on assets; H = hypothesis.

*,**,*** indicates significance at the 10%, 5%, and 1% levels, respectively (two-tailed).

Robustness Tests

We next perform a battery of untabulated robustness tests, the results of which do not affect inferences from our main results reported in Table 3.

As we argue above, it likely takes some time for a new audit committee member to become knowledgeable enough about a firm’s operations to influence the firm’s financial reporting. We nevertheless estimate our main regression model over the alternative periods of 1 year before and after and 2 years before and after the appointment of an accounting expert. As we conjectured, the magnitude of the coefficient on our variable of interest increases in size as the analysis period lengthens. The coefficient on our variable of interest is 0.0905 (p = .07) for years −1 to +1 and 0.1808 (p = .00) for years −2 to +2. Recall that the coefficient on our variable of interest in Table 3 is 0.3706 (p = .00).

Although our changes analysis reported in Table 3 incorporates controls for other variables expected to affect analyst following, a limitation of this approach is that other events potentially confound our results. As another check on the robustness of the results, we use the full sample of 460 (2,342) firms (firm-years) and estimate the results using a pooled cross-sectional regression. We find results consistent with those reported.

Given that the SOX definition of audit committee financial expertise encompasses more than accounting expertise, we also assess the effects of non-accounting financial expertise (i.e., supervisory and finance) on analyst following. We include in Model 1 firms that appoint non-accounting financial experts during our sample period and find that non-accounting expertise is not significant, while the coefficient on the accounting expertise variable remains significant and consistent with the main results in Table 3.

Dhaliwal et al. (2010) find that the combination of accounting expertise and finance expertise on the audit committee is associated with improved AQ. In an additional test, we find that accounting expertise, alone or in combination with finance and/or supervisory expertise, is positively related to analyst following, while neither finance nor supervisory expertise alone is significant.

Reg FD was passed on October 23, 2000, and could affect analyst following because of restrictions on private communications between firms and analysts. We re-estimate Model 1 and include an interaction of Post_Appt and a dummy variable equal to one for the post–Reg FD period (i.e., 2000-2003). Results indicate that the coefficient on the interaction is not significant, implying that Reg FD does not affect results.

We re-estimate Model 1 using an alternative measure of governance strength. We follow Carcello et al. (2008) and estimate the alternative measure using the following variables: board size = 1 if the firm’s board size is between six and nine members, else 0; board expertise = 1 if the percentage of independent directors who hold seats on other firms’ boards is greater than the sample median, else 0; relative audit committee power = 1 if the proportion of the firm’s audit committee size to its board size is greater than the sample median, else 0; audit committee independence = 1 if the audit committee is 100% independent, else 0; audit committee meetings = 1 if the number of audit committee meetings is greater than or equal to five, else 0; and institutional ownership = 1 if the firm’s percentage of institutional ownership is greater than the sample median, else 0. As we did earlier, we sum the governance variables and create a dichotomous variable for governance strength equal to one if the sum exceeds the median of the summed values of all observations. Using this alternative governance measure, we obtain results similar to those reported.

It is reasonable to assume that SOX increased pressure to add accounting expertise, which could also change analysts’ view of the audit committee. Thus, it is possible that the relation between audit committee accounting expertise and analyst following differs between the pre- and post-SOX regimes. To test our conjecture, we re-estimate Equation 1 after adding an interaction between Post_Appt and a dummy variable equal to one for the years after SOX (i.e., 2002-2003). We find that neither the coefficient on SOX nor the interaction term with SOX is significant.

Potential Channels Through Which Accounting Expertise Affects Analyst Following

We next provide an exploratory analysis of channels through which accounting expertise might affect analyst following. Guided by prior research, we conjecture that accounting experts could influence analyst following through their influence on audit quality proxied by Big 4 auditors (Big4), MEFs, and/or AQ. The positive relation between accounting expertise and analyst following that we find could be attributed to the effect of the audit committee on these three channels.

We investigate audit quality because Behn, Choi, and Kang (2008) show that Big4 auditors improve the properties of analysts’ forecasts. Accounting experts could affect analyst following either by influencing the appointment of Big4 auditors or by facilitating the effectiveness of existing Big4 auditors. We measure Big4 as an indicator variable equal to one for firms that use a Big4 auditor. We investigate MEFs because prior studies find that MEFs are an important channel through which managers can provide firm-specific information to investors (e.g., Coller & Yohn, 1997; Lennox & Park, 2006). Again, accounting experts could affect analyst following by influencing management disclosure of forward-looking information. We obtain MEFs from the First Call Historical Database’s company issued guidance file and use the number of annual MEFs issued during the fiscal year.

Finally, we investigate AQ because prior research finds a positive relation between accounting expertise on the audit committee and earnings quality. In addition, F. Yu (2008) finds that analyst following and abnormal accruals are negatively related. We argue that accounting experts can use their skill to improve AQ and thus positively influence analyst following. We test the AQ channel using the absolute value of abnormal accruals (AQ) multiplied by −1. Thus, higher values of AQ imply higher AQ. We follow Kothari, Leone, and Wasley (2005) and compute unsigned abnormal accruals using a modified version of the Jones (1991) model with performance-matching based on return on assets.

We execute our channel analysis by using the same basic regression model from Table 3. We separately add to the baseline regression proxies for each of the three channels and also combine all three channels in one regression. We utilize interaction terms between each channel and our indicator variable for the appointment of an accounting expert. These interaction terms allow us to directly assess the impact of each channel on analyst following. We tabulate results of our channel analysis in Table 4 using five models. Model 1 is the baseline regression and provides key results reported in Table 3. Model 2 shows results for Big4, Model 3 shows results for MEFs, Model 4 shows results for AQ, and Model 5 shows results including all three channels.

Analysis of Potential Channels Through Which Audit Committee Accounting Expertise Affects Analyst Following.

Note. This table provides an assessment of three potential channels through which accounting expertise impacts analyst following (#Analysts). Model 1 is our baseline model that was reported in Table 3. Model 2 tests the audit quality (Big4 indicator variable = 1 for Big 4 firm) channel. Model 3 tests the frequency of MEF channel, Model 4 tests the AQ channel, and Model 5 is the full model that controls for all three potential channels. Results for control variables are omitted for brevity. We use a Poisson model and estimate regressions with robust standard errors by firm clusters. See Table 2 for detailed definitions of the variables. MEF = management earnings forecasts; AQ = accrual quality.

*,**,*** indicates significance at the 10%, 5%, and 1% levels, respectively (two-tailed).

Results in Table 4 show no impact of a Big4 auditor (Model 2) or MEFs (Model 3) on analyst following either before or after the appointment of an accounting expert. In contrast to results for Big4 and MEFs, we report in Models 4 and 5 that AQ has a positive and significant impact on analyst following after the appointment of an accounting expert. 13 These results are consistent with analysts recognizing that accounting experts enhanced their firms’ financial reporting through higher AQ.

Information Quality of Analysts’ Forecasts

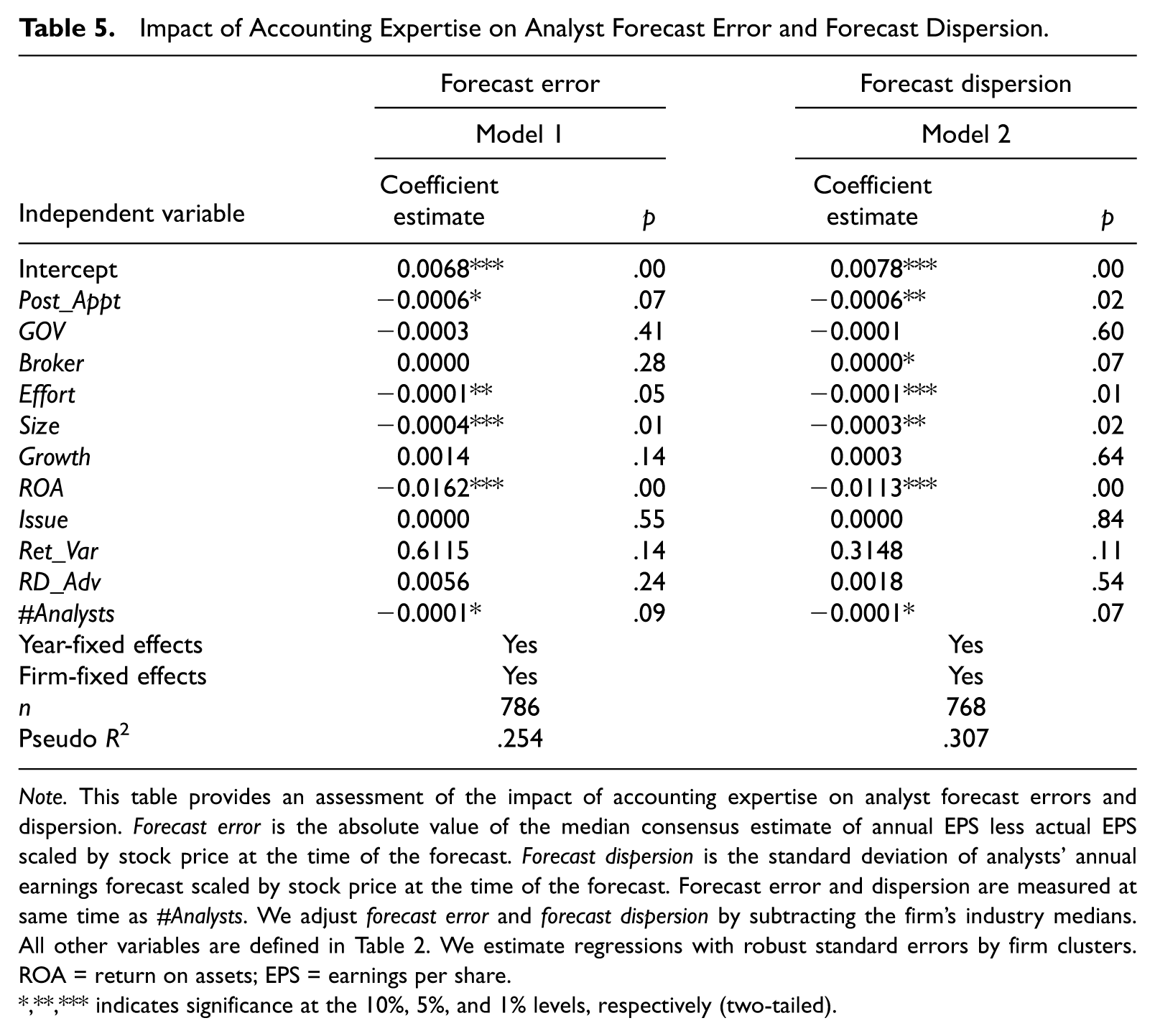

Similar to Abernathy et al. (2013), we also examine the relation between the appointment of an accounting expert and analyst forecast properties. A finding that analysts’ information quality is higher in the presence of audit committee accounting expertise would support the beneficial effects of audit committee accounting expertise on the information environment. Following prior research, we assess the relation between audit committee accounting expertise and (a) forecast error and (b) forecast dispersion as proxies of analysts’ information quality.

We execute our tests of analyst forecast properties using Model 1, except that we substitute analyst forecast error and analyst forecast dispersion for analyst following and include analyst following as a control variable. We measure analyst forecast error as the absolute value of the median 14 forecast of annual earnings per share (EPS) less actual EPS scaled by stock price. We measure forecast error at the same time as analyst following. We measure forecast dispersion as the standard deviation of analysts’ annual earnings forecasts scaled by stock price (again, measured at the same time as analyst following). Because we require at least three analysts to calculate dispersion, fewer observations are available for dispersion than for analyst following and forecast accuracy.

In Table 5, we report results for tests of analyst forecast properties. We report a negative and significant coefficient of −0.0006 (−0.0006) on Post_Appt for forecast error (forecast dispersion). 15 These findings are consistent with those in Abernathy et al. (2013) and the argument that audit committee accounting expertise improves information quality and reduces the need for analysts to obtain costly private information. 16 The coefficients on effort, size, ROA, and volume are significant and generally consistent with prior research.

Impact of Accounting Expertise on Analyst Forecast Error and Forecast Dispersion.

Note. This table provides an assessment of the impact of accounting expertise on analyst forecast errors and dispersion. Forecast error is the absolute value of the median consensus estimate of annual EPS less actual EPS scaled by stock price at the time of the forecast. Forecast dispersion is the standard deviation of analysts’ annual earnings forecast scaled by stock price at the time of the forecast. Forecast error and dispersion are measured at same time as #Analysts. We adjust forecast error and forecast dispersion by subtracting the firm’s industry medians. All other variables are defined in Table 2. We estimate regressions with robust standard errors by firm clusters. ROA = return on assets; EPS = earnings per share.

*,**,*** indicates significance at the 10%, 5%, and 1% levels, respectively (two-tailed).

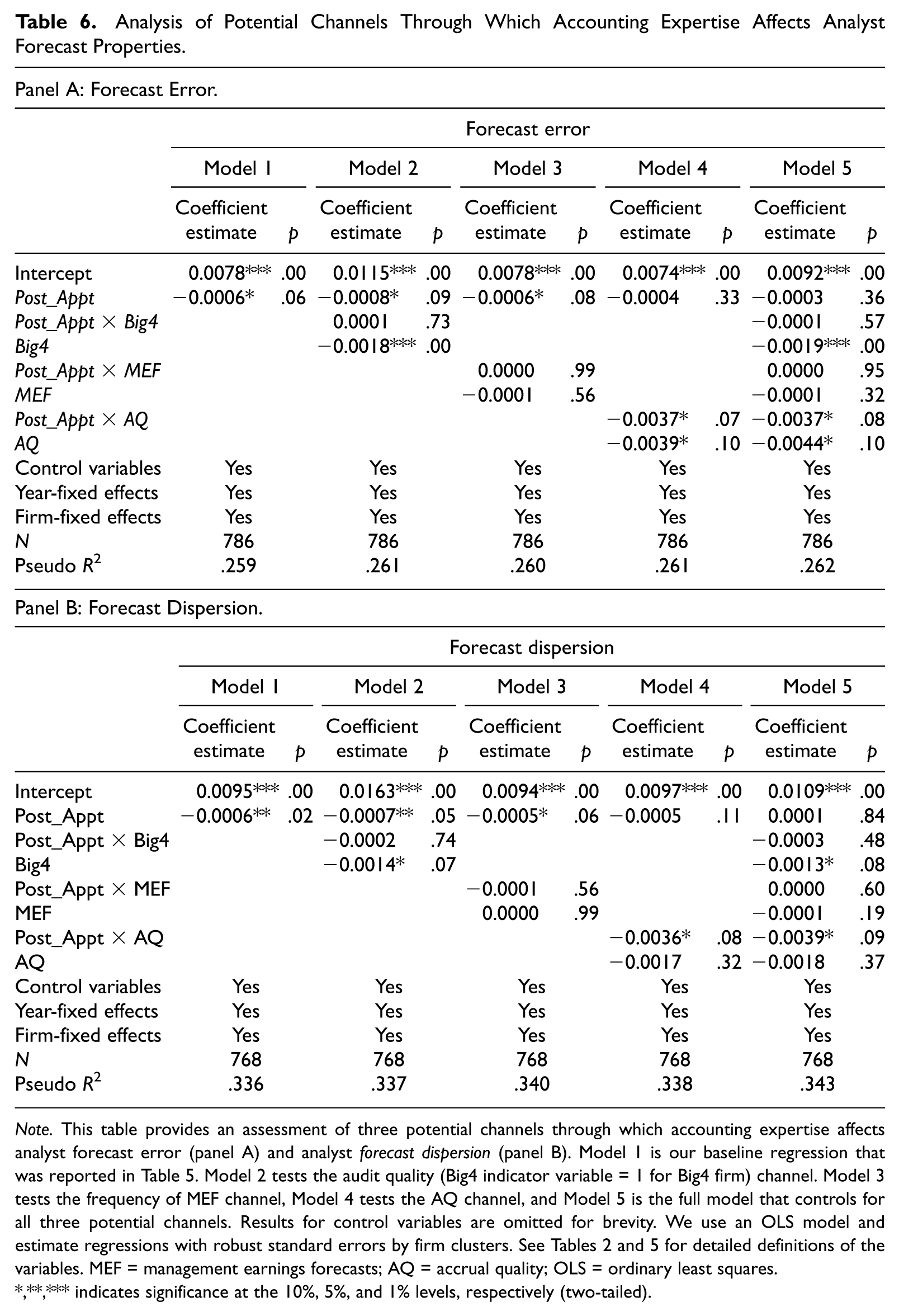

Analysis of Channels Through Which Accounting Expertise Affects Forecast Properties

Although results in Table 5 largely confirm those in Abernathy et al. (2013), missing from Abernathy et al. (2013) is a direct test of the channel through which accounting expertise enhances analyst forecast properties. Abernathy et al. (2013) perform an indirect test by adding to their cross-sectional regression a variable intended to capture AQ. We extend Abernathy et al. (2013) by performing a more direct test of the channels through which accounting experts can potentially influence analyst forecast properties. In addition, our tests are more comprehensive in that we use three potential channels, while Abernathy et al. (2013) only use one channel.

We follow the method used in Table 4 to assess the channels through which accounting expertise affects analyst forecast properties. We present the related results in Table 6. Results for forecast error are reported in panel A. Model 1 presents baseline results from Table 5. Model 2 indicates that while Big4 firms reduce forecast errors, there is no difference in the effect of a Big4 firm on forecast error before or after the appointment of an accounting expert. Model 3 shows no impact of MEFs on forecast errors in either the pre- or post-appointment periods. Models 4 and 5 show that AQ significantly reduces forecast error following the appointment of an accounting expert, consistent with results reported in Table 4. In panel B, we report results for forecast dispersion that are similar to those for forecast error, except that AQ has no impact on forecast dispersion in the period prior to the appointment of an accounting expert to the audit committee.

Analysis of Potential Channels Through Which Accounting Expertise Affects Analyst Forecast Properties.

Note. This table provides an assessment of three potential channels through which accounting expertise affects analyst forecast error (panel A) and analyst forecast dispersion (panel B). Model 1 is our baseline regression that was reported in Table 5. Model 2 tests the audit quality (Big4 indicator variable = 1 for Big4 firm) channel. Model 3 tests the frequency of MEF channel, Model 4 tests the AQ channel, and Model 5 is the full model that controls for all three potential channels. Results for control variables are omitted for brevity. We use an OLS model and estimate regressions with robust standard errors by firm clusters. See Tables 2 and 5 for detailed definitions of the variables. MEF = management earnings forecasts; AQ = accrual quality; OLS = ordinary least squares.

*,**,*** indicates significance at the 10%, 5%, and 1% levels, respectively (two-tailed).

Note that Abernathy et al. (2013) report very small changes in the magnitude of the coefficient on their variable for accounting expertise when they add AQ to their regression. By contrast, the coefficients on our interaction term of accounting expertise and AQ show large and significant improvements in analyst forecast properties due to accounting expertise. Overall, results in Table 6 are consistent with those in Table 4 and demonstrate a direct link between accounting expertise and analyst forecast properties through enhanced AQ. 17

Simultaneous Equation Analyses of Analyst Following and Analyst Forecast Properties

We recognize that analyst following and analyst forecast characteristics are interrelated, though not in a mutually exclusive or redundant way (Lang et al., 2003). Alford and Berger (1999) indicate that analyst following and forecast accuracy are simultaneously determined. We consequently estimate a system of equations similar to that in Alford and Berger (1999). In the first model, we regress analyst following on forecast accuracy, the accounting expertise indicator variable, and the same set of control variables from Model 1, except that we drop volume. In the second model, we regress forecast accuracy on analyst following, accounting expertise, and the same set of controls from Model 1, except that we drop RD_Adv. For completeness, we also estimate a similar system of equations to control for the simultaneity of analyst following and forecast dispersion. Untabulated results indicate that inferences for accounting expertise are consistent with those reported in Table 3. These results suggest that simultaneity is not an issue in our setting.

Capital Market Consequences of Audit Committee Accounting Expertise

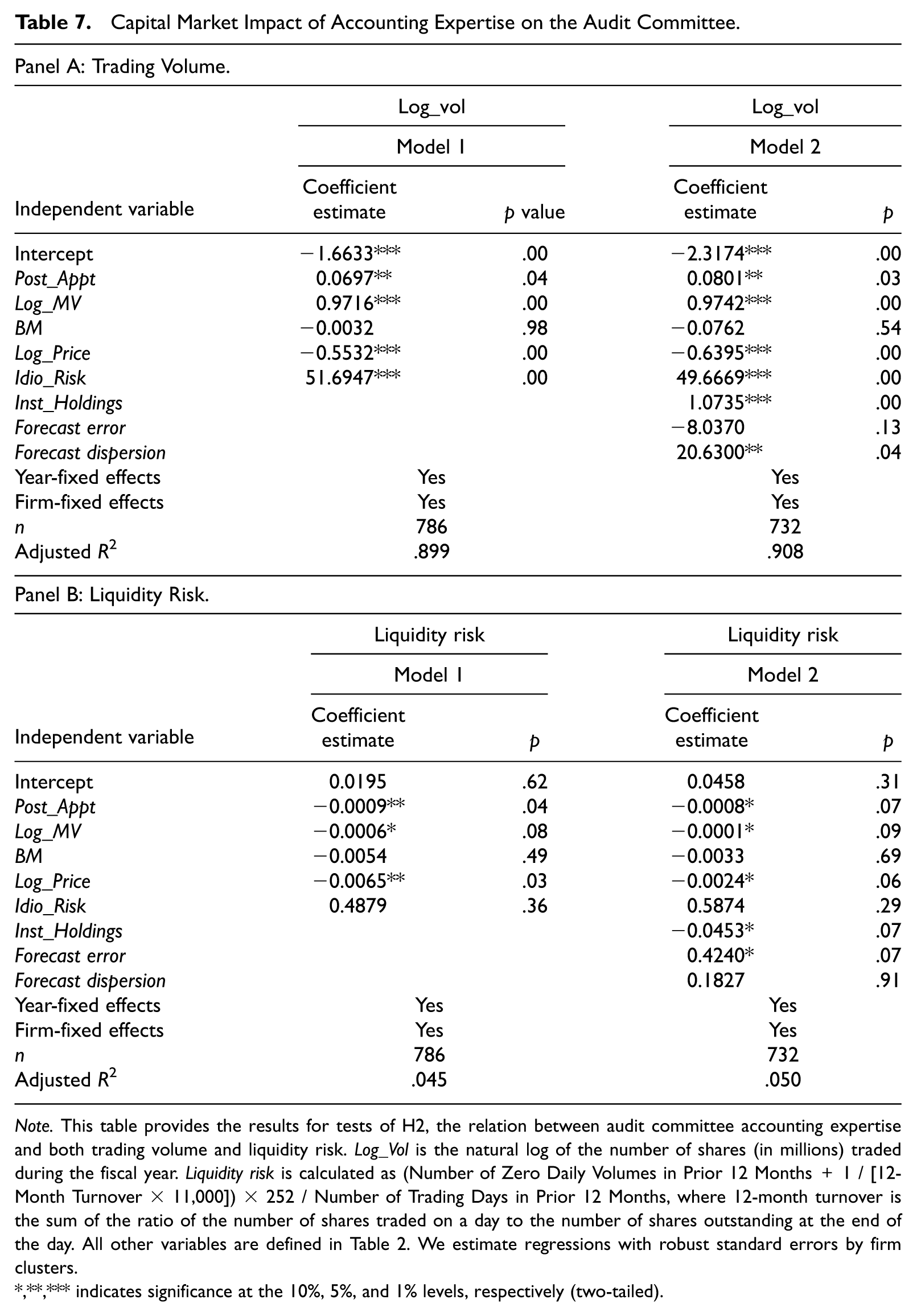

While our prior analyses attempt to control for known factors related to analysts’ decisions and also control for firm-fixed effects, results in Brown et al. (2015) suggest that analysts’ incentives to follow firms are not clear. In H2, we seek to provide more direct evidence of a capital market effect from audit committee accounting expertise by assessing the relation between audit committee accounting expertise and both trading volume and Liu’s (2006) measure of liquidity risk.

Trading volume is a widely used measure related to analysts’ incentives to cover a firm (Beyer & Guttman, 2011). We measure trading volume as the log of the number of shares (in millions) traded during the fiscal year. In panel A of Table 7, we show a positive and significant coefficient on audit committee accounting expertise. Our finding that firms with audit committee accounting expertise generate more investor interest is consistent with theory that suggests trading volume increases in the precision of public information (Kim & Verrecchia, 1994). This result is also consistent with the increase in analyst following, in that higher trading volume generates greater potential trading commissions to brokerage houses. However, theory also suggests trading volume increases in investor disagreement, as proxied by forecast dispersion (Ajinkya, Atiase, & Gift, 1991). Thus, we also control for forecast dispersion in our trading volume model and find that forecast dispersion also increases trading volume. Because audit committee accounting expertise reduces forecast dispersion, our results suggest that both theoretical effects are evident and that the net effect of audit committee accounting expertise on trading volume is positive, consistent with H2.

Capital Market Impact of Accounting Expertise on the Audit Committee.

Note. This table provides the results for tests of H2, the relation between audit committee accounting expertise and both trading volume and liquidity risk. Log_Vol is the natural log of the number of shares (in millions) traded during the fiscal year. Liquidity risk is calculated as (Number of Zero Daily Volumes in Prior 12 Months + 1 / [12-Month Turnover × 11,000]) × 252 / Number of Trading Days in Prior 12 Months, where 12-month turnover is the sum of the ratio of the number of shares traded on a day to the number of shares outstanding at the end of the day. All other variables are defined in Table 2. We estimate regressions with robust standard errors by firm clusters.

*,**,*** indicates significance at the 10%, 5%, and 1% levels, respectively (two-tailed).

As an additional test of the market impact of accounting expertise, we use the measure of liquidity risk from Liu (2006) and include in panel B of Table 7 analyses of the relation between liquidity risk and audit committee accounting expertise. Liu (2006) develops a comprehensive measure of liquidity risk that captures the multi-dimensional nature of liquidity, including trading volume turnover. Liu (2006) finds that his measure of liquidity risk is positively related to asset returns. In our setting, we expect that if accounting expertise reduces information asymmetry and thus lowers liquidity risk, then the coefficient on accounting expertise should be negative and significant.

Following Liu (2006), we measure liquidity risk as the standardized turnover-adjusted number of zero daily trading volumes over the prior 12 months. Consistent with our expectation, results in panel B of Table 7 show negative and significant coefficients on audit committee accounting expertise, implying that the addition of audit committee accounting expertise is related to lower liquidity risk, which has been shown to be related to a lower cost of capital (Liu, 2006). This result is consistent with the trading volume results in panel A of Table 7. Taken together, results for trading volume and liquidity risk imply that investors positively value the addition of accounting expertise to the audit committee, which provides analysts with greater incentives to follow these firms. Showing that accounting expertise provides economic benefits beyond increased analyst following, and analyst forecast properties also extends the broader literature on the economic benefits associated with audit committee accounting expertise.

Summary and Conclusion

We examine the relation between audit committee accounting expertise and analyst following. We find that analyst following is higher after firms increase audit committee accounting expertise. This result is consistent with the notion that audit committee accounting expertise reduces analysts’ costs to follow a firm. Our main results are robust to a host of controls known to be related to analyst following. In robustness tests, we find that our main inferences are unaffected by alternative analysis periods, pooled cross-sectional regressions, other types of audit committee financial expertise, the pre- and post–Reg FD periods, an alternative measure of governance strength, the pre- and post-SOX periods, and simultaneity. Importantly, we demonstrate that accounting experts improve analyst following through the channel of AQ. We similarly show that accounting experts are associated with lower forecast error and forecast dispersion, also through the channel of AQ. Finally, we provide evidence that audit committee accounting expertise is related to higher trading volume and lower liquidity risk, suggesting that accounting expertise provides capital market benefits, thereby supporting incentives for increased analyst following.

We make several important contributions to the literature. Our study is the first to document an empirical link between audit committee expertise and analyst following. This is important because analysts affect firms’ information environment, which is a key determinant of resource allocation and economic growth (Bushman et al., 2004). Our finding that the impact of audit committee accounting expertise on analyst following flows from the channel of AQ deepens our understanding of the interrelations between audit committee accounting expertise and financial reporting in enhancing the information environment. Our study also provides evidence that firms with audit committee accounting expertise enjoy higher trading volume and lower liquidity risk, supporting analyst incentives to follow firms and implying that these firms enjoy additional capital market benefits beyond increased analyst following and enhanced forecast properties. Our findings should therefore be useful to firms seeking to enhance market liquidity and analyst following.

Our findings also contribute to the ongoing debate regarding the efficacy of regulatory and legislative efforts that seek to improve the financial expertise of audit committees. Because analysts are a proxy for sophisticated investors and influence investors (Schipper, 1991), our evidence is consistent with audit committee accounting expertise helping to enhance investor confidence in financial reporting,

Footnotes

Acknowledgements

The authors thank Jong-Hag Choi, Carl Hollingsworth, Boochun Jung, workshop participants at University of Missouri, University of Nebraska, Seoul National University, and University of South Florida and participants at the 2008 AAA Annual Meeting for their helpful comments and suggestions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.