Abstract

We examine the association of insider ownership with financial analysts’ forecast accuracy and dispersion in a sample of U.S. dual-class firms. Insider ownership exerts two effects: a positive incentive effect and a negative entrenchment effect. The lack of significant findings in prior research regarding the association between insider ownership and forecast accuracy may be attributable to the offsetting forces of these two effects. Using a comprehensive hand-collected sample of U.S. firms that maintain more than one class of common stock, we are able to disentangle incentive and entrenchment effects which are confounded in single-class firms. We find that disproportionate insider control is negatively associated with forecast accuracy and positively associated with forecast dispersion. Moreover, insider cash flow rights (insider voting rights) are positively (negatively) associated with forecast accuracy and negatively (positively) associated with forecast dispersion, consistent with incentive-alignment and entrenchment effects of ownership affecting financial analysts’ forecasting environment in opposite directions.

Introduction

This study examines the association of insider ownership with financial analysts’ forecast accuracy and forecast dispersion. Prior work on the association of firms’ ownership structure and the forecasting environment of financial analysts documents that institutional ownership significantly affects forecast accuracy (Kerl & Ohlert, 2015; Ljungqvist, Marston, Starks, Wei, & Yan, 2007). However, prior studies have not been able to show a significant link between insider ownership and forecast accuracy (Byard, Li, & Weintrop, 2006; García-Meca & Sánchez-Ballesta, 2011). This is puzzling, because insider ownership has been recognized as an important aspect of firms’ overall corporate governance structure (e.g., Harris & Raviv, 1988; La Porta, Lopez-de-Silanes, Shleifer, & Vishny, 2000; Singh & Davidson, 2003). Insider ownership can help align the interests of management and shareholders, but at the same time it provides management with a means of entrenchment (Duellman, Ahmed, & Abdel-Meguid, 2013; Morck, Shleifer, & Vishny, 1988). We posit that the non-significant findings in prior work may be due to these peculiar counteracting effects conveyed by insider ownership.

To disentangle the incentive and entrenchment effects of ownership, we therefore follow prior studies (Francis, Schipper, & Vincent, 2005; Gompers, Ishii, & Metrick, 2010, hereinafter: GIM; Masulis, Wang, & Xie, 2009) that focus on a set of companies with unique characteristics: firms with more than one class of common stock. 1 Unlike in firms with a single class of common stock, cash flow rights and voting rights owned by insiders tend not to be identical in dual-class firms. This unique feature of dual-class firms allows us to separately assess how incentive-alignment effects of insider ownership (from cash flow rights) and entrenchment effects of ownership (from voting rights) affect financial analysts’ forecast accuracy and dispersion. Moreover, we are also able to examine how disproportionate insider control, measured as the excess of insider voting rights over their cash flow rights, commonly referred to as “wedge” (GIM, 2010), affects financial analysts’ forecast properties.

We expect disproportionate insider control to be negatively associated with financial analysts’ information environment for two interconnected reasons. First, managerial entrenchment may be associated with reduced credibility of the accounting information available to market participants (Francis et al., 2005). Less credible accounting information can generate uncertainty in analysts’ information environment (Barniv & Cao, 2009) and therefore trigger less accurate analyst earnings forecasts. Second, concentrated ownership by insiders may stem from insiders’ desire to operate in greater secrecy, which results in tighter control of the information flow from the corporation to external users (Fan & Wong, 2002).

However, we note that a negative effect of disproportionate insider control on the quality of financial information is not unambiguous. For instance, Nguyen and Xu (2010) and Chen (2008) present evidence of a lower instance of earnings management in dual-class firms. Because entrenched insiders are less dependent on the goodwill of shareholders, they may have less reason to conceal or manage financial information. While this rationale suggests possibly higher quality information, for the same reason the quantity of information supplied may be lowered, because entrenched insiders may have lowered incentives to provide timely and/or comprehensive information to their outside shareholders. On the whole, we therefore believe that disproportionate insider control likely is negatively associated with financial analysts’ information environment.

We begin our examination by developing a new hand-collected sample of dual-class firms from 2000 to 2012 largely following the approach of GIM (2010). That is, we first build a comprehensive list of potential dual-class firms identified from several sources, and then check all candidates to determine whether the firm actually has a dual-class structure of shares. Through these procedures, we are confident to present a sample which approaches the population of public dual-class firms in the United States during this time period. 2 Our focus on dual-class firms potentially introduces a sample-selection bias into our analysis, because the sample of firms we study is not randomly selected from the population of U.S. public firms. In addition, like most studies of companies’ ownership structure or governance characteristics, endogeneity may affect the interpretability of our results. To address these concerns, we use two-stage regressions that control for sample-selection bias, following the Heckman (1979) methodology, and endogeneity, in addition to our single-stage regressions.

Across all three approaches, we find a significant negative relationship between disproportionate insider control and analysts’ forecast accuracy. Likewise, insider voting rights are negatively associated with forecast accuracy, whereas insider cash flow rights show a positive association. Consistent with our results for accuracy, we also find that disproportionate insider control is positively associated with the dispersion of earnings forecasts. Increased dispersion indicates greater uncertainty and lower consensus among analysts (Barron, Kim, Lim, & Stevens, 1998; Barron & Stuerke, 1998; Imhoff & Lobo, 1992) and a poorer information environment (Byard, Li, & Yu, 2011). The association of insider voting rights (cash flow rights) with forecast dispersion is correspondingly positive (negative). All of these results are robust across different forecast horizons, model specifications, and a number of additional robustness tests, for instance, controlling for firms’ private benefits’ capacity and reverse causality. In addition, we find results consistent with our levels models also when employing a changes (first differences) model, which demonstrates that contemporaneous and lagged changes in disproportionate control are positively (negatively) associated with changes in analysts’ forecast dispersion (accuracy).

Taken together, our findings add to prior work by establishing that insider ownership does have a bearing on financial analysts’ forecast accuracy and forecast dispersion. However, the association is a product of counteracting elements of ownership. While incentive-alignment effects of ownership have a positive impact, entrenchment effects of ownership exercise a force in the opposite direction. For this reason, perhaps, prior work (Byard et al., 2006; García-Meca & Sánchez-Ballesta, 2011) was unable to discern an effect of insider ownership on financial analysts, on average. Our results suggest that insider ownership influences the information environment of firms and provide further evidence of the importance of considering insider ownership in understanding firm and analyst behavior.

In the “Literature Review and Hypothesis Development” section, we discuss the related literature and develop our research hypotheses. We describe our data and research design in the “Data and Research Methodology” section. The “Empirical Analysis” section presents empirical results. Concluding remarks appear in the “Summary and Conclusion” section.

Literature Review and Hypothesis Development

The question of the impact of insider ownership on the forecasting environment of financial analysts is largely open in the literature. Only a few studies to date examine the association between insider ownership and financial analysts’ forecast accuracy and dispersion. Byard et al. (2006) do not discern a statistically significant effect of CEO or director ownership on the accuracy of financial analysts’ forecasts in a sample of U.S. firms. Similarly, García-Meca and Sánchez-Ballesta (2011) do not find that insider ownership, defined as board of director ownership, significantly affects financial analysts’ forecast errors using a sample of Spanish firms. In a related study, Haw, Ho, Hu, and Wu (2010) on average also do not detect a significant effect of the divergence between the controlling owner’s control and cash flow rights on forecast accuracy and dispersion in a sample of East Asian and Western European firms. 3

Given the influence of insiders on the quality and quantity of firms’ mandatory and voluntary financial reporting, this lack of significant findings is surprising. However, the difficulty in demonstrating the influence of insider ownership on analysts’ forecasting environment may stem from the nature of ownership itself. Insider ownership exerts two distinct forces. On one hand, insider ownership mitigates the classic agency conflict between owners and managers of the firm by aligning interests of outside shareholders and those in charge of managing the firm. This incentive-alignment effect should result in increased informativeness of mandatory financial reporting as managers’ incentives to manipulate earnings for private benefits are reduced (Duellman et al., 2013; Wang, 2006; Warfield, Wild, & Wild, 1995). A positive association of managerial ownership with the extent of voluntary disclosures, documented, for instance, by Nasir and Abdullah (2004) in Malaysia, also supports positive incentive-alignment effects. Because the incentive-alignment effects of ownership provide insiders with incentives for improved quality and quantity of financial information, insider ownership may therefore exert positive effects on the information environment of financial analysts.

On the other hand, increasing levels of insider ownership may result in an entrenchment effect. High insider ownership reduces the threat of an ouster and may enable corporate insiders to influence financial reporting and firm disclosure practices according to their self-interest (Baik, Kang, & Morton, 2010; Lang, Lins, & Miller, 2004). Insider ownership thus can create a Type II agency conflict between controlling and minority shareholders, where controlling shareholders may use their influence in the firm to extract perquisites at the cost of minority shareholders (Villalonga & Amit, 2009). Accordingly, users may place less credence in the accounting information produced by firms with high levels of insider ownership (Fan & Wong, 2002). The credibility of accounting information, however, has been shown to be positively associated with its informativeness (Teoh & Wong, 1993), and less credible accounting information can generate uncertainty in analysts’ information environment (Barniv & Cao, 2009). Moreover, as insider ownership increases, insiders are able to operate with greater discretion and to exercise tighter control over the flow of information (Fan & Wong, 2002). Specifically, concentrated ownership allows insiders to better manage who possesses information in the organization, and thereby to better guard against information leakage. 4 For these reasons, greater levels of insider ownership could decrease the informativeness of financial reporting, and the quality and quantity of firm voluntary disclosure.

In sum, theory and prior research therefore suggest that insider ownership may improve or diminish the quality of financial analysts’ information environment, depending on whether incentive or entrenchment effects dominate. Yet typically these effects are confounded. The two separate forces—incentives and entrenchment—must be identified using only one variable: insider share ownership. We posit that prior studies potentially did not discern an association of insider ownership with financial analysts’ forecast accuracy due to the countervailing effects of these two forces.

An analysis of dual-class companies offers a way around this problem. In a typical firm with a dual-class equity structure, one class of common stock has more votes per share than the other, while both classes generally have similar cash flow rights. The equity structure of dual-class firms therefore breaks the link between voting rights, which proxy for the entrenchment effect, and cash flow rights, which proxy for the incentive-alignment effect of ownership. By creating a material difference between the proportion of voting rights and cash flow rights held, insiders are able to exert disproportionate control; insiders do not bear the economic consequences of their actions pro rata with their level of control over the firm.

Several studies examine how disproportionate insider control affects aspects of financial reporting quality. Francis et al. (2005) document that the informativeness of earnings, as indicated by the returns–earnings relationship, decreases as disproportionate insider control increases in a sample of U.S. dual-class firms. Fan and Wong (2002) present similar results and show that a separation of voting rights from cash flow rights, accomplished through cross-holdings and pyramid structures common in Asian economies, reduces earnings informativeness. Using samples of East Asian and Western European countries, the divergence of control from cash flow rights of the ultimate owner has also been shown to be positively associated with accruals-based earnings management (Haw, Hu, Hwang, & Wu, 2004), classification shifting (Haw, Ho, & Li, 2011), and lowered earnings conservatism (Lim & Tan, 2009).

These findings in the literature strongly suggest that disproportionate insider control negatively affects the information environment of analysts. However, a few studies also suggest otherwise. For instance, because entrenched insiders are less beholden to shareholders, they have less reason to conceal or manage financial information. Pleasing investors by meeting earnings benchmarks matters less when insiders have enhanced influence over their compensation and job security. Consistent with this conjecture, Nguyen and Xu (2010) find that earnings management activities are associated positively with managerial cash flow rights, but negatively with managerial voting rights. Chen (2008) similarly finds lower earnings management in dual-class compared with single-class firms, but explains the finding with decreased capital-market pressure on entrenched managers who can focus on long-term value creation and hence have lowered incentives for short-term earnings manipulation.

While a lower concern about earnings may help earnings quality by reducing incentives for manipulation, the same lowered concern should in general reduce incentives to provide timely and/or comprehensive information to shareholders. That is, while the quality of some financial information may be higher, by the same logic the quantity of information supplied should be lower. Indeed, Tinaikar (2014) documents that the separation of voting and cash flow rights in dual-class firms is negatively associated with firms’ voluntary compensation disclosures.

Overall, we therefore expect that disproportionate insider control is negatively associated with financial analysts’ information environment. Furthermore, we expect the incentive-alignment effects of ownership, which capture the sharing in the economic success of the firm through insider cash flow rights, to exercise a force toward higher quality information. Conversely, the entrenchment effect, which captures the extent to which insiders are isolated from the control by outside shareholders through insider voting rights, exerts a negative influence on financial analysts’ information environment. When the information supplied to financial analysts is of inferior quality, analysts will tend to make less accurate forecasts (Hope, 2003; Lang & Lundholm, 1996). Accordingly, we hypothesize the following:

We similarly expect forecast dispersion to vary with the quality of the information environment. Forecast dispersion has been found to be associated with greater levels of information asymmetry (Barron & Stuerke, 1998; Irani & Karamanou, 2003; Lang & Lundholm, 1996) as well as a less rich information environment (Byard et al., 2011). Furthermore, Barron, Byard, Kile, and Riedl (2002) demonstrate that when financial information is less useful for predicting firm performance, the information contained in forecasts of individual analysts will tend to consist more of private knowledge than common knowledge. Accordingly, to the extent that the divergence of voting rights from cash flow rights reduces overall information quality, financial analysts will rely more on idiosyncratic information. Because dispersion reflects idiosyncratic error arising from reliance on private information (Barron et al., 1998), we hypothesize with respect to forecast dispersion:

Data and Research Methodology

Sample

We construct a sample of U.S. dual-class firms from 2000 to 2012 following the approach of GIM (2010). That is, we first build a comprehensive list of potential dual-class firms from sources identified in GIM (2010). 5 We eliminate foreign and financial firms. For all remaining candidates, we access proxy statements and/or 10-Ks on the U.S. Securities and Exchange Commission’s (SEC) EDGAR database to verify the corporate structure and to determine insider ownership for each class of stock every year. 6 We follow GIM (2010) in defining insider ownership comprehensively and include shares owned by family members, or trusts for the benefit of family members, as well as shares owned by parent or subsidiary corporations with board representation. 7 We also collect dividend data because classes of shares may differ not only with respect to voting but also with respect to their dividend rights. At this stage, we also collect governance characteristics included as controls: CEO–Chairman identity, board size, and number of independent directors. Through these procedures, we are confident to present a high-quality, comprehensive sample, which likely approaches the population of U.S. non-financial dual-class firms in our sample period. Upon merging our dual-class data with Compustat, Institutional Brokers’ Estimate System (I/B/E/S), and Thomson Reuters, our final sample consists of 2,050 firm-years, representing 356 unique firms.

Insider Voting and Cash Flow Rights

In companies with multiple classes of common stock, separate classes of shares may entitle their holders to a different number of votes per share and/or different dividend rights. Differences in the number of votes per share are the primary mechanism of creating a divergence between voting rights and cash flow rights in dual-class firms. A second control-enhancing mechanism is disproportionate board representation (Villalonga & Amit, 2009). We define insider voting rights (VR) as board election rights, that is, the proportion of board seats insiders are able to command, regardless if this voting power stems from differences in the number of votes per share, from disproportionate board representation rights, or from both sources. 8 We compute insider cash flow rights as the ratio of shares owned by insiders to shares outstanding of all classes, weighted by dividend rights per class (Francis et al., 2005; GIM, 2010). Our primary measure of disproportionate insider control is the ratio of insider voting rights to insider cash flow rights (WEDGE). 9

Research Design

We measure our two dependent variables, analysts’ forecast accuracy (ACC) and forecast dispersion (DISP), similar to Duru and Reeb (2002) and Byard et al. (2006). Specifically, we compute ACC as the absolute value of the difference between the mean I/B/E/S consensus forecast of annual earnings and the actual annual earnings reported by I/B/E/S, scaled by stock price on the day prior to the measurement of the I/B/E/S consensus forecast. 10 For ease of interpretation, we multiply this scaled forecast error by −1, so that higher values of ACC indicate higher accuracy. DISP is the standard deviation of analysts’ forecasts scaled by stock price on the day prior to the measurement of the I/B/E/S consensus forecast. Following Byard et al. (2011), we require that a minimum of two analysts are included in the computation of the consensus forecast to ensure that dispersion is meaningful. 11

In addition to our variable(s) of interest, we include controls for firm, forecast, and corporate governance characteristics in our primary model:

A negative (positive) coefficient on the independent variable of interest, WEDGE, the extent of divergence of voting rights owned by insiders from cash flow rights owned by insiders, will provide evidence in favor of H1a (H2a). We further investigate H1b and H2b by replacing WEDGE with the proportion of voting rights (VR) and cash flow rights (CFR) owned by insiders in Equation (1). We expect a negative (positive) coefficient on VR (CFR) when ACC is the dependent variable and the opposite signs when DISP is the dependent variable.

Our first set of controls reflects firm characteristics. lnSIZE is the natural log of market capitalization, LOSS represents an indicator variable equaling one if net income for the firm is negative, and zero otherwise, and EPS_VOL is the standard deviation of earning per share over the prior 5-year period (or as many years as available). Second, we control for forecast characteristics. HORIZON is the number of calendar days between the I/B/E/S consensus forecast date and fiscal year end, and FOLLOW is the number of analysts following a firm, measured by the number of individual financial analyst forecasts included in the computation of the consensus forecast. As a third set of controls, we include the set of corporate governance characteristics used by Byard et al. (2006): CEO_CHAIR is an indicator variable equal to one if the CEO is also the chair of the board, and zero otherwise; BOARD_SIZE is the number of directors on the board; IND_DIR is the percentage of independent directors; and INST_OWN is the proportion of stock held by institutional investors. 12 Data for CEO_CHAIR, BOARD_SIZE, and IND_DIR have been collected from firms’ annual proxy statements; institutional ownership data (INST_OWN) is sourced from Thomson Reuters. Finally, we control for year and industry fixed effects by including year and industry (Fama & French, 1997) indicator variables in all models.

In addition to examining single-stage results from Equation (1), we conduct two additional analyses which control for potential sample-selection bias and endogeneity. It is possible that dual-class firms are different from single-class firms with respect to characteristics other than dual-class status, and that such differences affect the association between insiders’ disproportionate control rights and the forecasting environment of financial analysts. Accordingly, analyses of a sample of dual-class firms could be affected by self-selection bias and, as a consequence, our findings may not extend to single-class firms. We therefore control for possible sample-selection effects by using the Heckman (1979) methodology.

To this end, we estimate the following probit model, based on GIM (2010), which models the decision to establish a dual-class structure at initial public offering (IPO):

The dependent variable DUAL is equal to one for firms electing a dual-class structure and zero otherwise. The independent variables are an indicator if at IPO the firm name contains a person’s name; an indicator if the firm operated in the media industry at the time of its IPO 13 ; the percentile rank of the firm’s sales and profits in the year of its IPO relative to firms with the same IPO year; the percentage of all firms and all sales in the same Core Based Statistical Area (CBSA) in the year prior to the firm’s IPO; the percentage of the firm’s sales relative to the sales of all firms in the same CBSA in the year of its IPO; and indicator variables for the firm’s listing year and the 48 Fama and French (1997) industries. 14 Results indicate that NAME, MEDIA, and SALESRANK (SALES/REGIONSALES) are significantly positively (negatively) associated with the probability of choosing a dual-class structure. 15 Following Amoako-Adu, Baulkaran, and Smith (2014) and McGuire, Wang, and Wilson (2014), we use the coefficient estimates from Equation (2) to construct an inverse Mills ratio (INV_MILL; Heckman, 1979), which we include as a control for sample-selection bias in Equation (1).

Endogeneity is a concern in any study of firms’ corporate governance or ownership characteristics. We therefore perform a two-stage least squares (2SLS) analysis and regress WEDGE, VR, and CFR, on a set of firm-level instrumental variables identified in Khalil, Magnan, and Cohen (2008) and Haw et al. (2010):

FAMILY indicates a family firm defined as a firm where the founder and/or his or her descendants own 25% or more of the firm’s voting rights (Andres, 2008). We research firms’ founders from SEC filings and publicly available sources. FIN_NEED is a firm’s need for financing, proxied by Return on Equity (ROE / [1-ROE]) as in Khalil et al. (2008); ΔSALES is percentage sales growth; lnAT is the natural log of total assets; ROA is income before extraordinary items divided by total assets; INTANG is the percentage of intangible assets, computed as 1 − (net property, plant, and equipment + inventories) / total assets; MEDIA is an indicator variable that takes a value of one if the firm operates in the media industry, and zero otherwise; and FIRMAGE is the age of the firm, based on its founding year, which we collected from publicly available information. In our third set of regressions, we replace WEDGE, VR, and CFR with their predicted values from the First-Stage Regression Equation (3) as an explicit control for endogeneity.

Empirical Analysis

Descriptive Statistics

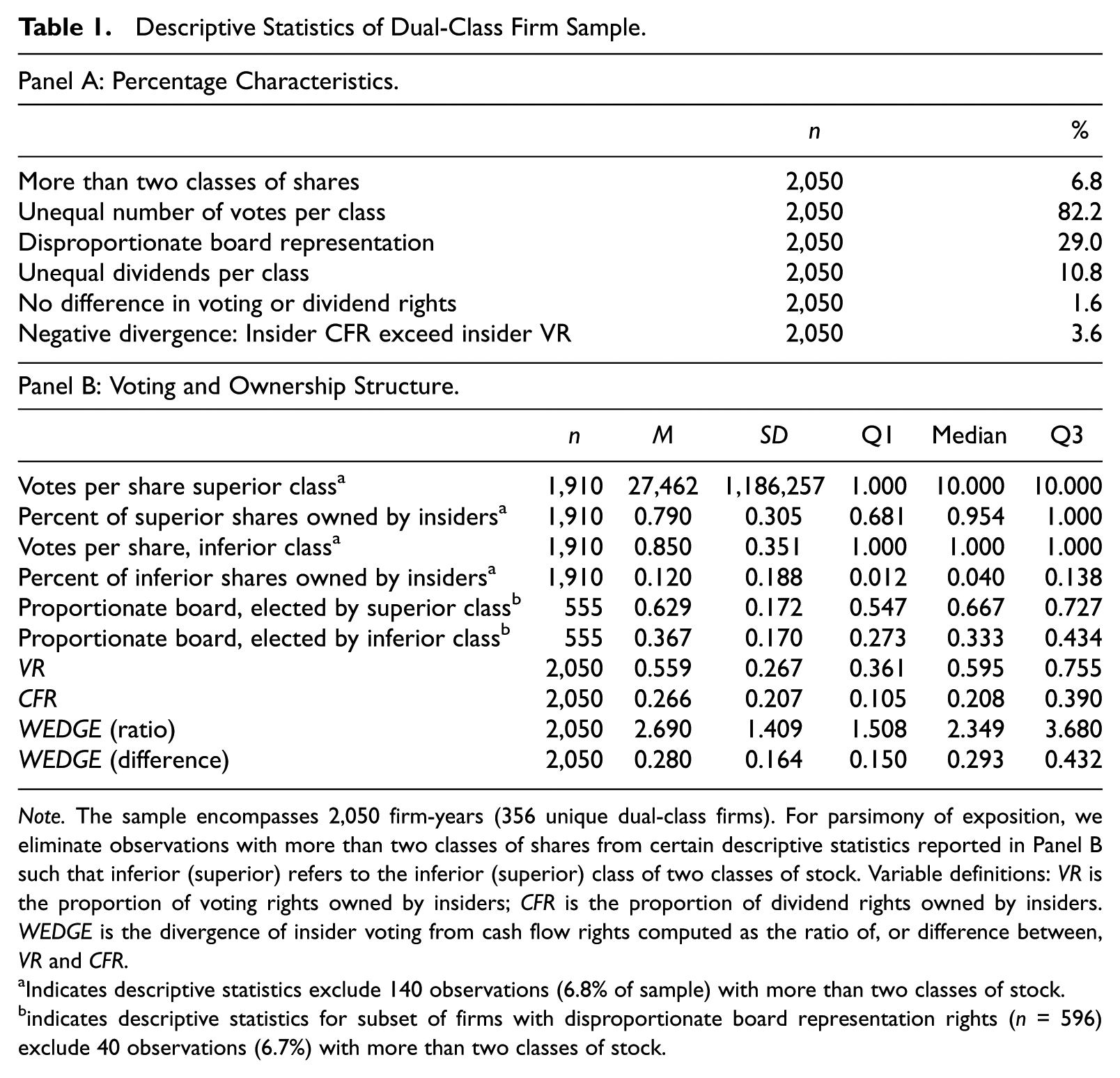

Table 1 reports descriptive statistics concerning our sample of dual-class firms, which encompasses 356 unique firms contributing a total of 2,050 firm-years. As reported in Panel A, a strong majority of observations (n = 1,910) have two classes of shares. In the remaining 140 cases, more than two classes of common stock exist (6.8% of the sample). In 82.2% of cases, differences exist in the number of votes per share in the election of the board of directors. In addition, voting schemes whereby each class of stock elects a certain number of directors are common, as 595 observations (29.0% of the sample) maintain such an arrangement. The proportion of firms with unequal votes across classes of shares and disproportionate board election rights exceeds 100% due to a number of firms which have adopted both of these elements.

Descriptive Statistics of Dual-Class Firm Sample.

Note. The sample encompasses 2,050 firm-years (356 unique dual-class firms). For parsimony of exposition, we eliminate observations with more than two classes of shares from certain descriptive statistics reported in Panel B such that inferior (superior) refers to the inferior (superior) class of two classes of stock. Variable definitions: VR is the proportion of voting rights owned by insiders; CFR is the proportion of dividend rights owned by insiders. WEDGE is the divergence of insider voting from cash flow rights computed as the ratio of, or difference between, VR and CFR.

Indicates descriptive statistics exclude 140 observations (6.8% of sample) with more than two classes of stock.

indicates descriptive statistics for subset of firms with disproportionate board representation rights (n = 596) exclude 40 observations (6.7%) with more than two classes of stock.

While voting rights differ substantially, all shares are generally entitled to receive equal dividends. In only 10.8% of observations, do dividend rights differ across classes of stock. Also, in only 32 observations (1.6% of sample), do we find that shares are identical with respect to voting and cash flow rights, but differ in other characteristics only; for instance, differences may pertain to redemption rights or voting rights other than in the election of the board. These observations indicate that dual-class structures are overwhelmingly created to achieve a significant discrepancy between voting and cash flow rights across classes of shares. “Benign” dual-class structures, where insiders predominantly hold the inferior class of shares, are rare. In only 74 observations (3.6% of sample), do we find that insiders own fewer voting than cash flow rights.

With respect to the voting and ownership structure of firms in our sample, as reported in Panel B of Table 1, insiders on average own 79.0% of the superior, but only 12% of the inferior, shares outstanding. 16 The median superior class of stock has 10 votes per share, whereas the median inferior share only commands one vote. 17 Among firms that maintain disproportionate board representation schemes, the median (mean) proportion of directors elected by the superior class is 66.7% (62.9%), the remaining number of directors being elected by the inferior class.

Finally, with respect to our variables of interest, insiders of the firm control median (mean) voting rights in the election of the board of directors of 59.5% (55.9%) compared to cash flow rights of 20.8% (26.6%). The ratio of voting rights to cash flow, our primary measure of the degree of separation between the two, shows that insiders command a median (mean) of 2.35 (2.69) times the number of voting rights as they do cash flow rights. The median (mean) difference between the proportion of voting and cash flow rights owned by insiders, our alternate measure of the wedge between the two, is 29.3% (28.0%).

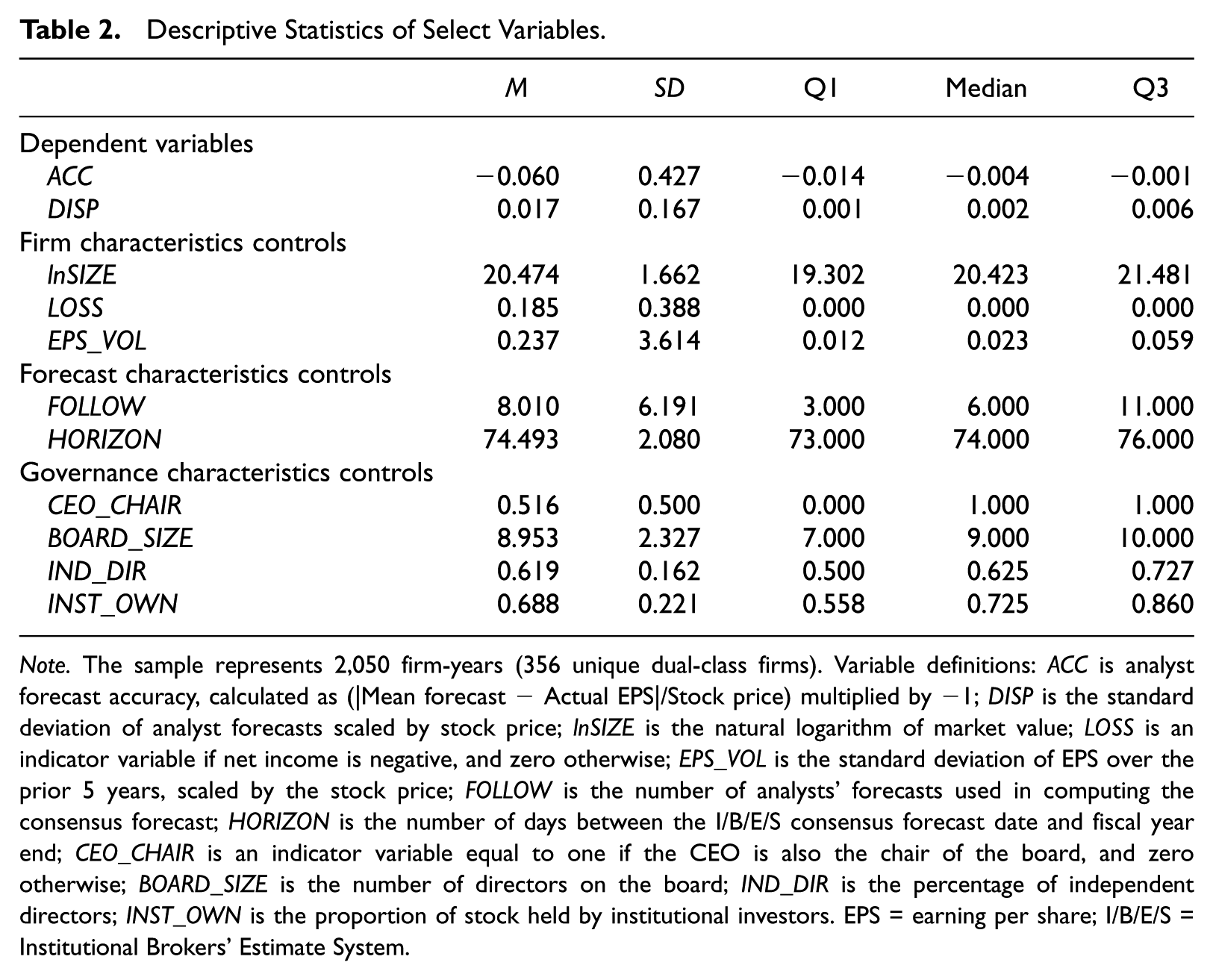

Descriptive statistics of our control variables are summarized in Table 2. Median (mean) lnSIZE of our sample firms is 20.42 (20.47), which corresponds to a median (mean) market capitalization of 740 (3,877) million dollars. Loss years represent 18.5% of our sample, which spans two economic downturns. Descriptive statistics of the board characteristics variables reveal that the CEO serves as chairman of the board in 51.6% of our sample. BOARD_SIZE is fairly uniform across our sample with a mean and median of nine directors and a standard deviation of 2.33. On average, 62% of the board is comprised of independent directors, very similar to the 64.3% mean independent directors reported by Byard et al. (2006). Finally, median (mean) institutional ownership amounts to 72.5% (68.8%).

Descriptive Statistics of Select Variables.

Note. The sample represents 2,050 firm-years (356 unique dual-class firms). Variable definitions: ACC is analyst forecast accuracy, calculated as (|Mean forecast − Actual EPS|/Stock price) multiplied by −1; DISP is the standard deviation of analyst forecasts scaled by stock price; lnSIZE is the natural logarithm of market value; LOSS is an indicator variable if net income is negative, and zero otherwise; EPS_VOL is the standard deviation of EPS over the prior 5 years, scaled by the stock price; FOLLOW is the number of analysts’ forecasts used in computing the consensus forecast; HORIZON is the number of days between the I/B/E/S consensus forecast date and fiscal year end; CEO_CHAIR is an indicator variable equal to one if the CEO is also the chair of the board, and zero otherwise; BOARD_SIZE is the number of directors on the board; IND_DIR is the percentage of independent directors; INST_OWN is the proportion of stock held by institutional investors. EPS = earning per share; I/B/E/S = Institutional Brokers’ Estimate System.

Regression Results

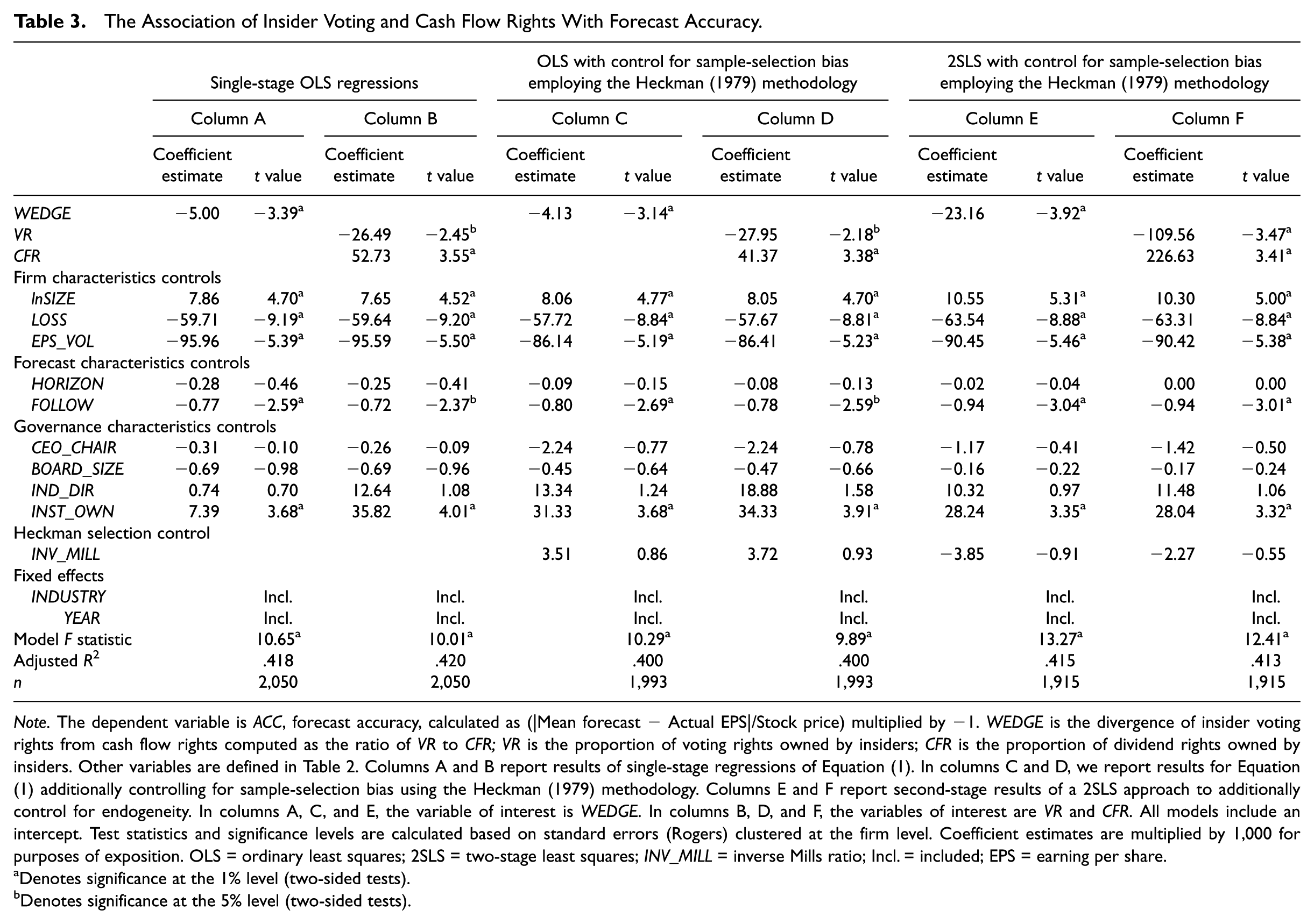

Column A of Table 3 displays the results of our single-stage regression of forecast accuracy on disproportionate insider control and controls, Equation (1). The coefficient on WEDGE is negative and significant (t = −3.39, p < .01, two-tailed). This finding supports our H1a, indicating that the accuracy of financial analysts’ earnings forecasts decrease as the extent of separation of voting rights from cash flow rights increases. With respect to our controls, firm size is positively and significantly associated with forecast accuracy, whereas LOSS, EPS_VOL, FOLLOW, and DISP all show a significant negative association, consistent with prior research. Although most of the firm and forecast characteristics controls are significant, we find little support for our governance characteristics controls except for INST_OWN, which displays a significant positive association with accuracy. 18

The Association of Insider Voting and Cash Flow Rights With Forecast Accuracy.

Note. The dependent variable is ACC, forecast accuracy, calculated as (|Mean forecast − Actual EPS|/Stock price) multiplied by −1. WEDGE is the divergence of insider voting rights from cash flow rights computed as the ratio of VR to CFR; VR is the proportion of voting rights owned by insiders; CFR is the proportion of dividend rights owned by insiders. Other variables are defined in Table 2. Columns A and B report results of single-stage regressions of Equation (1). In columns C and D, we report results for Equation (1) additionally controlling for sample-selection bias using the Heckman (1979) methodology. Columns E and F report second-stage results of a 2SLS approach to additionally control for endogeneity. In columns A, C, and E, the variable of interest is WEDGE. In columns B, D, and F, the variables of interest are VR and CFR. All models include an intercept. Test statistics and significance levels are calculated based on standard errors (Rogers) clustered at the firm level. Coefficient estimates are multiplied by 1,000 for purposes of exposition. OLS = ordinary least squares; 2SLS = two-stage least squares; INV_MILL = inverse Mills ratio; Incl. = included; EPS = earning per share.

Denotes significance at the 1% level (two-sided tests).

Denotes significance at the 5% level (two-sided tests).

We repeat our analysis replacing WEDGE with its two individual components, VR and CFR. Results of a regression of forecast accuracy on insider voting and cash flow rights and controls are reported in Table 3, column B. The coefficient on VR is negative and significant (t = −2.45, p = .015, two-tailed), whereas the coefficient on CFR is positive and significant (t = 3.55, p < .01, two-tailed). These results confirm that forecast accuracy increases in insider cash flow rights, and decreases in insider voting rights, supporting our H1b. Results for our control variables remain qualitatively unchanged from those previously reported.

In columns C and D of Table 3, we report results specifically controlling for sample-selection bias by employing the Heckman (1979) methodology, and adding INV_MILL, the inverse Mills ratio derived from an estimation of Equation (2), to Equation (1). Results are not affected by using this alternate approach; WEDGE, VR, and CFR all remain statistically significant at similar levels.

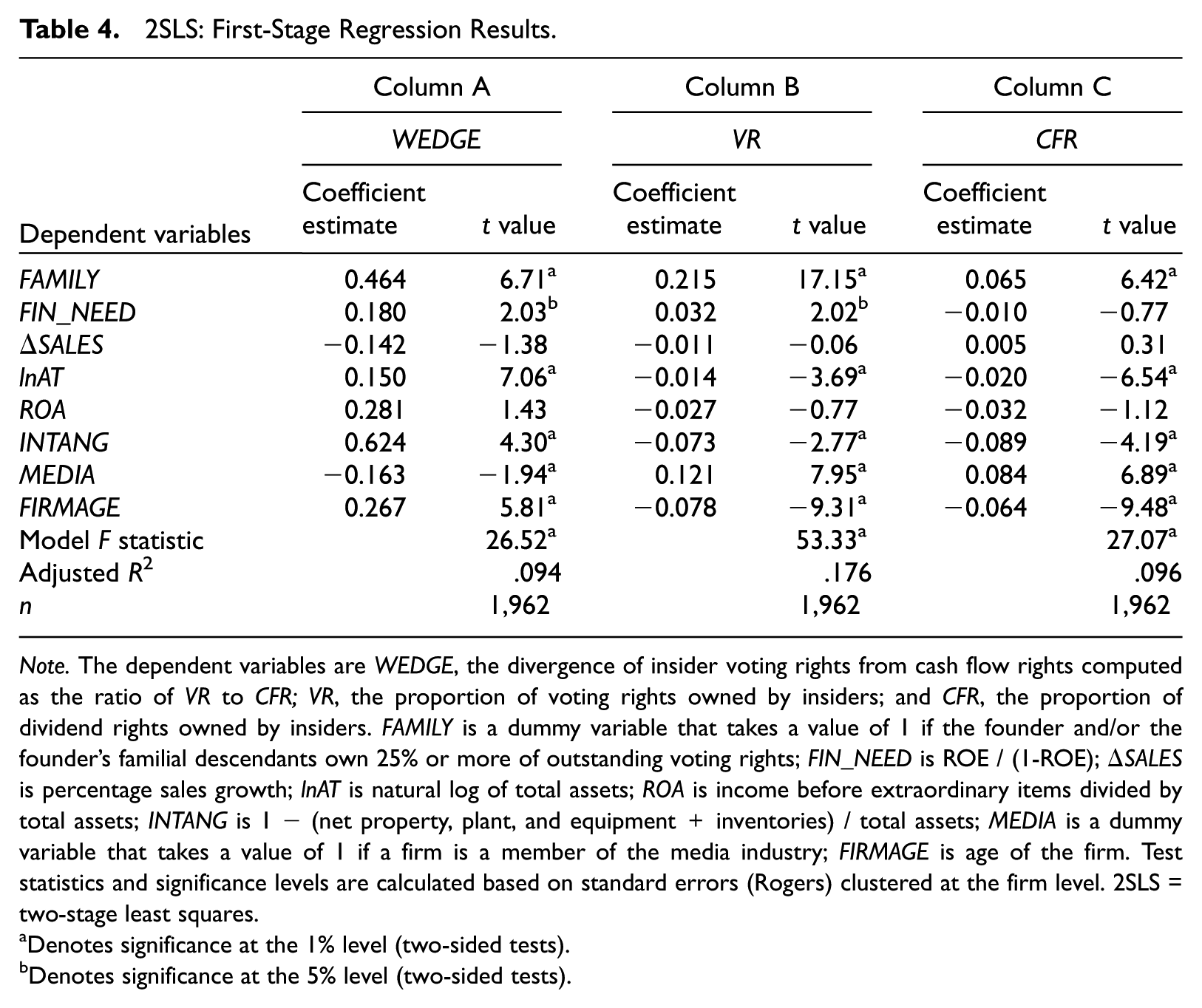

To control for endogeneity, we also replicate our analyses using a 2SLS approach. In the first-stage regression, we regress the potentially endogenous variables WEDGE, VR, and CFR on the set of instrumental variables identified in Khalil et al. (2008) and Haw et al. (2010), Equation (3). The explanatory power of the first-stage regression is reasonable, with an R2 ranging from 9.4% to 17.6%, and comparable with the R2 of approximately 14.3% achieved by Khalil et al. With the exception of ROA and ΔSALES, all variables are significant. The first-stage regression results are summarized in Table 4.

2SLS: First-Stage Regression Results.

Note. The dependent variables are WEDGE, the divergence of insider voting rights from cash flow rights computed as the ratio of VR to CFR; VR, the proportion of voting rights owned by insiders; and CFR, the proportion of dividend rights owned by insiders. FAMILY is a dummy variable that takes a value of 1 if the founder and/or the founder’s familial descendants own 25% or more of outstanding voting rights; FIN_NEED is ROE / (1-ROE); ΔSALES is percentage sales growth; lnAT is natural log of total assets; ROA is income before extraordinary items divided by total assets; INTANG is 1 − (net property, plant, and equipment + inventories) / total assets; MEDIA is a dummy variable that takes a value of 1 if a firm is a member of the media industry; FIRMAGE is age of the firm. Test statistics and significance levels are calculated based on standard errors (Rogers) clustered at the firm level. 2SLS = two-stage least squares.

Denotes significance at the 1% level (two-sided tests).

Denotes significance at the 5% level (two-sided tests).

Next, we re-estimate Equation (1) replacing WEDGE, VR, and CFR with their predicted values from Equation (3). Results, presented in columns E and F of Table 3, indicate that all variables remain significant at comparably (strong) levels. The coefficients of WEDGE, VR, and CFR are greater in the second stage of the 2SLS regression compared with the results from our single-stage approach. We interpret these increases as evidence for a reduction in single-equation bias from using a 2SLS approach. (Beaver, McAnally, & Stinson, 1997).

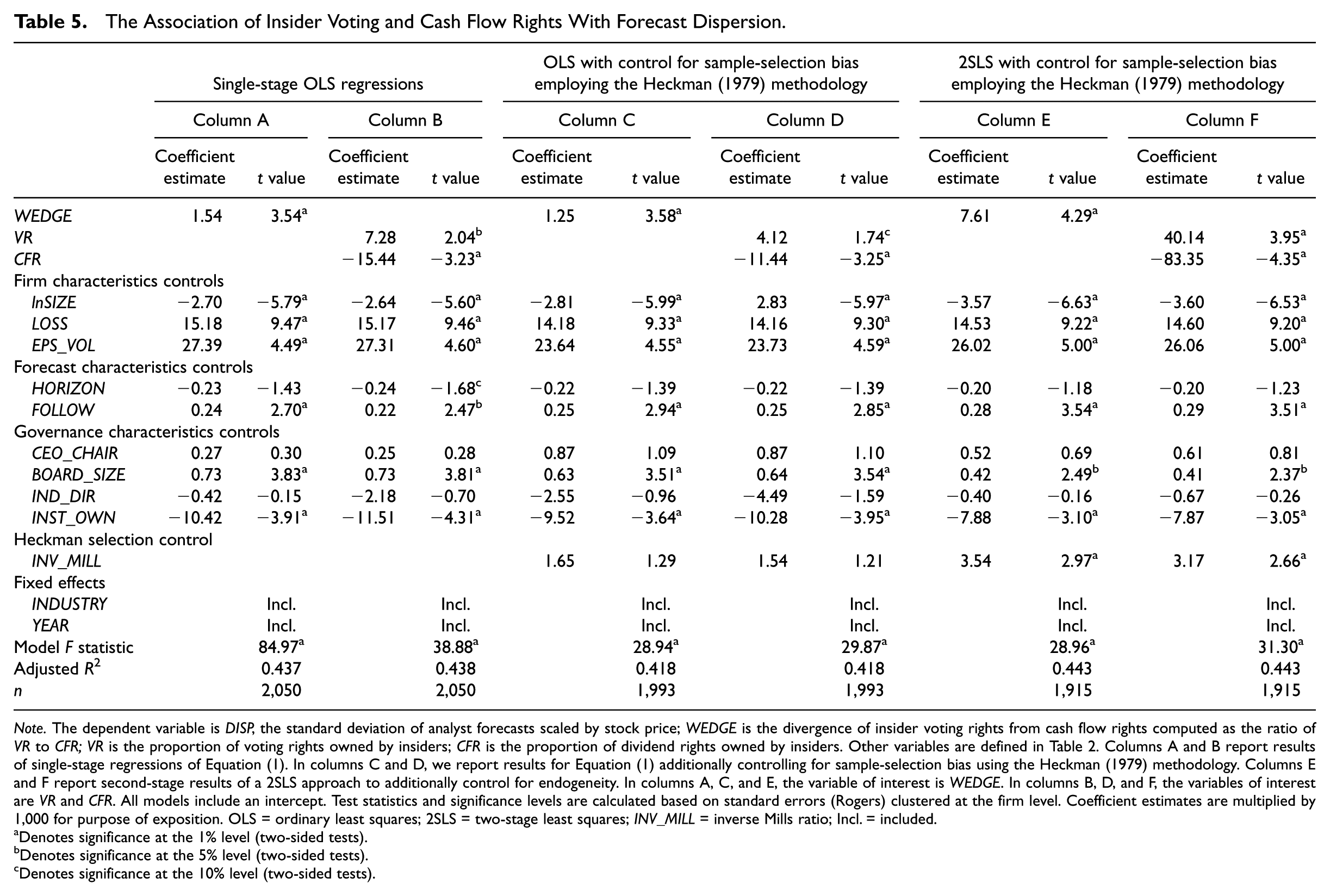

Regression results of Equation (1) using financial analysts’ forecast dispersion, DISP, as the dependent variable are reported in Table 5. Column A shows that the coefficient on WEDGE is positive and significant (t = 3.54, p < .01, two-tailed) indicating that the dispersion of financial analysts’ earnings forecasts increases in disproportionate insider ownership. This finding supports our H2a. In general, results for the control variables in the dispersion regression complement those for accuracy, such that characteristics which increase accuracy reduce dispersion.

The Association of Insider Voting and Cash Flow Rights With Forecast Dispersion.

Note. The dependent variable is DISP, the standard deviation of analyst forecasts scaled by stock price; WEDGE is the divergence of insider voting rights from cash flow rights computed as the ratio of VR to CFR; VR is the proportion of voting rights owned by insiders; CFR is the proportion of dividend rights owned by insiders. Other variables are defined in Table 2. Columns A and B report results of single-stage regressions of Equation (1). In columns C and D, we report results for Equation (1) additionally controlling for sample-selection bias using the Heckman (1979) methodology. Columns E and F report second-stage results of a 2SLS approach to additionally control for endogeneity. In columns A, C, and E, the variable of interest is WEDGE. In columns B, D, and F, the variables of interest are VR and CFR. All models include an intercept. Test statistics and significance levels are calculated based on standard errors (Rogers) clustered at the firm level. Coefficient estimates are multiplied by 1,000 for purpose of exposition. OLS = ordinary least squares; 2SLS = two-stage least squares; INV_MILL = inverse Mills ratio; Incl. = included.

Denotes significance at the 1% level (two-sided tests).

Denotes significance at the 5% level (two-sided tests).

Denotes significance at the 10% level (two-sided tests).

In column B of Table 5, we report results including VR and CFR in place of WEDGE. VR is positively related to DISP (t = 2.04, p = .042, two-tailed), whereas the association of CFR with DISP is negative (t = −3.23, p < .01, two-tailed). We thus find support also for H2b as insider voting rights (cash flow rights) are significantly positively (negatively) related to forecast dispersion. Results for the control variables are not materially different from the results reported in column A.

In columns C and D of Table 5, we show results for our regressions of analysts’ forecast dispersion on WEDGE, VR, and CFR when controlling for sample-selection bias. Similarly, columns E and F of Table 5 show results of our 2SLS approach to adjust for endogeneity. In either case, results are consistent with our single-stage regression results and display comparable levels of statistical significance.

Taken together, results in Tables 3 and 5 confirm that insider voting and cash flow rights exert divergent effects on the accuracy and dispersion of financial analysts’ earnings forecasts. Specifically, we find a negative (positive) association of the degree of separation of insider voting from cash flow rights with forecast accuracy (dispersion). This finding is in line with Francis et al. (2005) and Fan and Wong (2002), who report that the informativeness of mandatory financial reporting decreases as the separation of voting rights from cash flow rights increases.

Also supporting an entrenchment explanation, we find that insider voting rights decrease forecast accuracy, and increase forecast dispersion, while, confirming an incentive story, insider cash flow rights increase accuracy, and decrease dispersion. These results are consistent with insiders reducing the amount and/or reliability of information provided as their entrenchment from voting rights increases. A reduced amount or reliability of public information decreases financial analysts’ ability to issue accurate forecasts, and increases the need to substitute private for common information (Barron et al., 2002) with a resulting increase in forecast dispersion. Conversely, a richer information environment associated with insider cash flow rights enhances forecast accuracy and decreases dispersion.

Taken as a whole, our results appear to conflict with Haw et al. (2010), who pose similar hypotheses concerning the association of control-cash flow divergence and analysts’ forecast properties, but do not find a significant effect on average. Our strong divergent results using a contemporary sample of U.S. dual-class firms may be due to the fact that Haw et al. (2010) document that the association between control-cash flow divergence and forecast properties is contingent on the effectiveness of a country’s legal regime. 19 More importantly, we focus on insider ownership, whereas Haw et al. (2010) examine control-cash flow divergence of the controlling owner regardless of whether this owner is an insider or outsider, a family, the state, a financial institution, or other corporation. It is likely that our narrower focus on insider ownership enables us to find stronger results, because motives and incentives to influence the information environment are likely not constant across different types of ultimate owners.

Additional Analyses and Robustness Tests

Alternate forecast horizons

We follow Horton, Serafeim, and Serafeim (2013) and Byard et al. (2006) and examine the robustness of our results to different forecast horizons. We choose one shorter horizon, the most recent forecast issued before the end of the reporting period, as well as two longer forecasting periods: Forecasts issued on average 6 and 9 months before the end of the reporting period. The results for WEDGE, VR, and CFR are similar to those reported in Tables 3 and 5, and remain statistically significant at comparable levels across all alternate horizons. 20

Changes model

Our theoretical framework assumes a particular direction of causality, where an increasing divergence of insider voting rights from their cash flow rights leads to lower forecast accuracy and increased forecast dispersion. We acknowledge that our empirical analyses presented thus far mainly demonstrate association. To shed additional light on the relationship between disproportionate insider control and financial analysts’ forecasting environment, we therefore also estimate the following changes specification of Equation (1):

In Equation (4), we regress changes in financial analysts’ forecast accuracy (and dispersion) on contemporaneous changes in insiders’ disproportionate control (ΔWEDGE) and controls. We also examine the association of the prior year change in disproportionate control, ΔWEDGEt−1, with the contemporaneous change in ACC and DISP. Results are presented in Table 6.

The Association of Changes in Disproportionate Insider Control With Changes in Forecast Accuracy and Dispersion.

Note. The dependent variables are ΔACC, the change in forecast accuracy, calculated as (|Mean forecast − Actual EPS| / Stock price) multiplied by −1 and ΔDISP, the change in the standard deviation of analyst forecasts scaled by stock price; ΔWEDGE is the change in the divergence of voting rights from cash flow rights computed as the change in the ratio of VR to CFR; ΔWEDGEt−1 is the prior year’s change in WEDGE. All other variables are the changes in variables defined in Table 2. All models include an intercept. Test statistics and significance levels are calculated based on standard errors (Rogers) clustered at the firm level. Coefficient estimates are multiplied by 1,000 for purpose of exposition. EPS = earning per share; Incl. = included.

Denotes significance at the 1% level (two-sided tests).

Denotes significance at the 5% level (two-sided tests).

Denotes significance at the 10% level (two-sided tests).

Denotes significance at the 10% level (one-sided test).

The analysis reveals that, consistent with the results for our levels model, changes in disproportionate insider control, modeled either as the contemporaneous or lagged change, are significantly associated with corresponding changes in financial analysts’ forecast accuracy and dispersion. Our finding that the lagged change in disproportionate control is more strongly associated with accuracy and dispersion than the contemporaneous change suggests that changes in disproportionate control may affect changes in firms’ information practices with delay.

Inclusion of firm and year fixed effects

The regression models of all of our main tests include industry and year fixed effects. To further reduce the possibility that unobservable time-invariant attributes affect our results, we repeat all primary tests including firm and year fixed effects in the models. The untabulated results are qualitatively comparable and tend to be statistically significant at similar levels when the models include firm and year fixed effects. 21

Additional endogeneity tests

Endogeneity is a concern in any study of firms’ corporate governance or ownership characteristics. One concern with regard to endogeneity is the possibility of omitted variables that may jointly impact financial analysts’ forecasting environments and WEDGE, VR, and CFR. Our primary approach to address the endogeneity problem is by means of the two-stage least squares analysis presented above. All results prove robust to this approach. However, to further address the possibility that unobserved attributes affect both, insiders’ incentives to select a particular ownership structure and the forecasting environment of financial analysts, we conduct two additional tests.

As suggested by Masulis et al. (2009), one important factor likely affecting insiders’ incentives to choose a specific ownership structure is the availability of private benefits of control. Insiders of firms with a higher capacity for private benefits may be more likely to establish a dual-class structure, which enables the extraction of perquisites. At the same time, insiders interested in extracting private benefits of control potentially have increased incentives to reduce publicly available information when more opportunities to extract private benefits exist. Following Masulis et al., we control for existent opportunities for private benefits of control by including the variables predicting dual-class status based on a firm’s private benefits’ capacity from Equation (2) directly in Equation (1). Moreover, related to the idea that a firm’s private benefits’ capacity may be affecting the selection of its ownership structure as well as analysts’ forecasting environment, we also add an explicit control for firms’ compensation structure, CEO total compensation (ExecuComp variable TDC1), to Equation (1). Our inferences are unchanged when including these two additional controls for firms’ private benefits’ capacity to our model.

Finally, to address concerns of reverse causality, we follow Masulis et al. (2009) and replace the annual values of WEDGE in our levels regressions with its value in the year of a firm’s first appearance in our sample, as well as with its prior year (lagged) value. Results are not materially affected by these alternate specifications.

Other tests

We also test a number of alternative definitions of our variables. We use the difference between VR and CFR, instead of the ratio of the two, as an alternate specification of WEDGE (GIM, 2010). We also replicate all regressions requiring a minimum of three or five observations for the computation of dispersion. Instead of the mean, we also use the median consensus earnings forecasts in our forecast accuracy models. With respect to our control variables, we alternatively use the natural logarithm of the book value of assets as a control for firm size; define HORIZON relative to the earnings announcement date, instead of relative to the fiscal period end date; use the log of FOLLOW and BOARD_SIZE, instead of their count values; and use North American Industry Classification System (NAICS) industry controls instead of the Fama and French (1997) industries. To ensure that results are not driven by, or sensitive to, the inclusion of a small number of observations with uncommon dual-class structures where difference in between classes of shares does not pertain to voting or cash flow rights (32 observations), or where insiders primarily hold the inferior class of shares (73 observations), we rerun all analyses excluding these subsets of firms. Results are not affected by these choices.

Summary and Conclusion

Using a comprehensive hand-collected sample of U.S. dual-class firms, we assess the distinct effects of insider voting and cash flow rights on analyst forecast accuracy and dispersion. Some studies establish that the quality (Francis et al., 2005) and credibility (Fan & Wong, 2002) of financial reporting decrease as the wedge between insider voting and cash flow right widens. However, other studies provide evidence of improved financial reporting quality in the presence of disproportionate insider control (Chen, 2008; Nguyen & Xu, 2010). We find that disproportionate insider control is negatively (positively) associated with the accuracy (dispersion) financial analysts’ forecasts. Moreover, insider cash flow rights (insider voting rights) are positively (negatively) associated with financial analyst forecast accuracy, and negatively (positively) associated with forecast dispersion. These results are robust to controls for sample-selection bias and endogeneity, and not affected by choosing alternative forecast horizons or estimation techniques.

In contrast to prior studies, our results demonstrate that insider ownership does affect the information environment of financial analysts, and that the opposing incentive-alignment and entrenchment effects cause it to do so in a non-monotonic fashion. Forecast accuracy (dispersion) increases (decreases) in insider cash flow rights likely due to an incentive-alignment effect, which positively affects the quality of financial reporting. At the same time, forecast accuracy (dispersion) decreases (increases) in insider voting rights due to an entrenchment effect, which has been shown to negatively impact financial reporting. By delineating these two distinct effects of insider ownership on forecast accuracy and dispersion, we augment, and offer an explanation for, prior research that did not discern a significant association of insider ownership with financial analysts’ earnings forecast accuracy (Byard et al., 2006; García-Meca & Sánchez-Ballesta, 2011; Haw et al., 2010).

We use a sample of U.S. dual-class firms primarily as a laboratory that enables us to separately assess the incentive and entrenchment effects of insider ownership, which are confounded in single-class firms. However, our examination of forecast accuracy and dispersion in dual-class firms is also of interest as a study of this particular subset of firms in its own right. A spate of high-profile IPOs of technology firms with a dual-class structure of common stock has recently thrust this equity structure to the fore. 22 Dual-class firms, which comprised about 6% of U.S. public firms in the 1995 to 2002 period (GIM, 2010), now account for 8.7% of companies included in the Russell 3000 Index (Equilar, 2015). In 2013, 13.6% of all U.S. firms conducting an IPO adopted a dual-class structure of stock (Equilar, 2015). This increasing prominence of dual-class firms calls for a better understanding of their characteristics, especially with respect to these firms’ information behavior and their financial reporting quality. In the light of our findings, particular care appears to be justified in the generation of earnings forecasts for dual-class firms. Likewise, the decreased reliability of earnings forecasts as disproportionate insider control increases suggests particular caution from the investing public relying on financial analysts’ earnings forecasts for these firms.

Footnotes

Acknowledgements

We thank the Associate Editor Siva Nathan, an anonymous reviewer, Indrarini Laksmana, Andrea Scheetz, Phil Shane, and participants at the American Accounting Association (AAA) 2014 Annual as well as the AAA Ohio and Mid-Atlantic region meetings for their helpful comments.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.