Abstract

This article investigates the economic consequences of including more hard-to-measure future activities in a firm’s accounting measurements. Using a simple model of endogenous investment in which payoffs are measured by either a restrictive or expanded recognition rule, we show that, in the process of expanding accounting recognition, firms’ internal investment efficiency and external share-price risk premium may not necessarily be a trade-off. In particular, we show that the consequences of an accounting scope expansion depend on the investment environment (e.g., growth prospects) and the inherent measurement characteristics (e.g., measurement noise). For example, even with a higher measurement noise, an expanded accounting recognition may generate a lower risk premium in the share price. More surprisingly, it may lead to a higher investment efficiency and a lower risk premium at the same time. The underlying driving force is that different accounting regimes can affect the risk premium indirectly through their impacts on the investment level, beyond directly through the different measurement noise levels they bring.

Introduction

Within the accounting measurement structure, a critical scope issue is whether accounting measurements exclude future economic activities that are relevant to firm value but inherently hard to measure. Over the past few decades, the scope of accounting recognition has been expanding to include more and more such hard-to-measure future activities. The Financial Accounting Standards Board’s (FASB’s) newly issued accounting standard for credit losses is a representative example of this scope expansion. 1 Under the previous “incurred loss” model, only expected losses over a specific time horizon that pass a “probable” threshold are recognized. The “current expected credit loss” (CECL) model specified by the new accounting standard, however, removes the “probable” threshold and requires the recognition of the lifetime expected losses of the loan, which are harder to measure. The new CECL model has been referred to by the American Bankers Association as “the biggest change ever to bank accounting.” 2

The expansion is generally justified to be a response to the increasing demand from investors for more value-relevant information about an entity, particularly when much of the firm value emanates from future hard-to-measure events. During the debate of the new accounting standard on credit losses, most investors and analysts expressed their preference for the new CECL model based on their significant concerns with the delayed loss recognition. 3 However, in addition to the relevant implementation and auditing costs, many preparers voiced their concerns over the large measurement uncertainty in the CECL’s long-term forecast of the expected credit losses. In their comment letters to the original exposure draft, preparers claim that it may be very difficult to accurately forecast the amount of losses beyond a certain point of time. For example, Morgan Stanley claims that “an expected credit loss measurement approach based on a life-of-loan estimate would increase substantially the level of estimation uncertainty . . .” In its letter, Ford Motor Company goes even further by saying that “the degree of accuracy or inaccuracy of the forecasts will always be the subject of debate with respect to whether it was an estimate or an error.” This debate on the new CECL model, to some extent, captures the general theme of controversy on most scope expansion issues. By including more hard-to-measure activities, accounting measurements become more useful on one hand. On the other hand, recognizing more hard-to-measure activities inevitably injects more noise into the resulting accounting measures. This apparent conflict between usefulness and noise appears to be a pervasive policy trade-off in designing modern accounting measurements. 4

Our article examines this trade-off. Specifically, we consider two alternative accounting measurements designed to highlight the scope expansion and embed them into a standard investment model. Critical to the scope expansion is the simultaneous increase in both the measurement noise and the alignment between the accounting measure and the long-term investment return. Using this model, we investigate the scope expansion along two economic dimensions: investment efficiency and risk premium in the firm’s stock price. 5 We find that when equilibrium investment levels are taken into account, different accounting regimes can affect the risk premium indirectly through their impacts on the investment level, beyond directly through the different measurement noise levels they bring. Through this indirect mechanism, sometimes there is no trade-off at all: The scope expansion may simultaneously increase investment efficiency and decrease risk premium.

Specifically, we consider a risk-neutral entrepreneur selecting the amount of an initial investment, which determines both the mean and variance of the resulting future cash flows. Along the measurement dimension, some cash flows are easy to measure (or pass an evidential threshold), while other cash flows are hard to measure. Before the realization of the cash flows, the firm must report an accounting signal to risk-averse equity investors who competitively determine the share price of the firm. The accounting signal is noisy, and thus resolves some but not all the uncertainty of the future cash flows. The unresolved uncertainty determines the risk premium required by investors. The firm intends to maximize a weighted average of the short-term share price and the expected future cash flows. We interpret the weight on the share price as the managerial myopia. The larger the weight, the more myopic the firm.

There are two alternative accounting regimes: Partial accounting measures only the easy-to-measure future cash flows with low noise, whereas Full accounting measures all the anticipated future cash flows (i.e., both the easy-to-measure and hard-to-measure cash flows) with high noise. The key feature of the model is the fundamental difference in the informational properties of the two accounting regimes. This difference is especially large for (a) firms with higher growth prospects, which, in our model, are characterized by higher expected hard-to-measure future cash flows; and (b) firms with higher future profitability risks, which are characterized by higher volatility of the same hard-to-measure cash flows. Investors fully understand this structural difference and make rational inferences based on the accounting signal.

Our model delivers the following results: First, regarding investment efficiency, Full accounting, albeit noisier, better aligns the accounting signal with the investment return. Therefore, it induces more efficient investment than Partial accounting for firms with high growth prospects, because for these firms most of the cash flows from the investment are hard to measure and excluded from the recognition of Partial accounting.

Second, regarding risk premium, we find that it may be lower under Full accounting regardless of its measurement noise. The reason is that while the accounting measurements directly change the risk premium by resolving some cash flow uncertainty (i.e., direct effect), they also change the firm’s investment level, which determines the ex ante cash flow uncertainty to begin with (i.e., indirect effect). This indirect effect opens another channel through which the accounting measurements can affect the risk premium. 6 Under either accounting regime, this indirect effect may dominate the direct effect, causing the risk premium to be, counterintuitively, decreasing in the accounting noise. When the managerial myopia is not low, the indirect effect makes the risk premium generally elevated under Partial accounting, because the hard-to-measure cash flow uncertainty magnified by the investment is left unchecked by the Partial accounting signal. As a result, regardless of the noise level, Full accounting may lead to a lower risk premium in the presence of indirect effect. Furthermore, higher uncertainty in the hard-to-measure cash flows (i.e., higher future profitability risk) could strengthen this distinction by increasing the chance this case happens.

Last, combining the above investment efficiency and risk-premium results, a firm with high growth prospects and high future profitability risks could find Full accounting preferable on both fronts even with a high measurement noise. To these firms, the process of expanding accounting recognition does not necessarily generate a trade-off between investment efficiency and risk premium, as one normally expects.

Two assumptions in our main model require more discussion: First, we do not consider managerial manipulation of the accounting signal in our main model. However, we believe that accounting scope expansion could make accounting measurements more prone to such manipulation. In Section “Accounting Manipulation,” we provide a detailed analysis of a setting that allows managerial manipulation under Full accounting. We find that allowing manipulation does not qualitatively change the main results of the article. Second, similar to Beyer (2009), we assume that a risk-neutral entrepreneur faces a risk-averse pricing of her firm in our main setting. This assumption on the risk preference is consistent with prior empirical findings. 7 In Section “The Risk-Averse Entrepreneur,” we provide additional analysis in a setting where both the entrepreneur and investors are risk averse and how our results could be affected by a higher risk aversion of the entrepreneur.

In our article, the cash flow characteristics (easy to measure vs. hard to measure) present a challenge to measuring an entity’s activities because accounting must deal with the scope issue (i.e., inclusion or exclusion of certain cash flows as a measurement object) in addition to other measurement issues (e.g., measurement noise). As such, our article makes an attempt to explicitly model the expanding recognition scope in accounting measurements. Our article’s central accounting concern follows a broad theme in the modeling work on the accounting measurement structure. In recent strands of this theme that are closely related to our article, Dye (2002) views classification as a foundational accounting measurement function, and its possible manipulation has implications in the equilibrium accounting standards, which he terms “Nash” standards. Dye and Sridhar (2004) focus on accounting aggregation and the resulting trade-off between relevance and reliability. Along a similar line, Liang and Wen (2007) focus on input- vs. output-based accounting measures and their differential effects on equilibrium investment. Among other studies highlighting the importance of accounting structure, Arya, Fellingham, Glover, Schroeder, and Strang (2000) revive the earlier linear algebra work on the double-entry bookkeeping structure into a modern light. Ohlson (1995) and Feltham and Ohlson (1995) bring valuation theory to clean-surplus accounting. Liang and Zhang (2006) study the effects of flexible and rigid accounting regimes when firms face inherent or incentive uncertainties. Bertomeu and Magee (2015) model accounting standard setters in a strategic setting, and study how political pressures may affect the accounting regulation. Some other studies focus on the financial reporting quality choice (e.g., Bertomeu & Magee, 2011; Dye & Sridhar, 2007). Finally, the real-effect literature develops the notion that the disclosure of accounting information has an impact not only upon market prices but also upon corporate production/investment decisions (e.g., Beyer & Guttman, 2012; Kanodia, 1980; Kanodia & Lee, 1998).

The results in our article also have implications for empirical work on the relation between accounting quality and cost of capital. Prior literature has documented mixed evidence on the association between earnings quality and cost of capital (e.g., Beyer, Cohen, Lys, & Walther, 2010; Botosan, 1997; Botosan & Plumlee, 2002; Francis, LaFond, Olsson, & Schipper, 2004). The comparative statics results of our model indicate that factors such as managerial myopia, future profitability risk, intensity of the use of present value estimates (i.e., proxy for Partial accounting vs. Full accounting), and firms’ growth prospects may help explain the mixed empirical findings. For example, our results imply that if managerial myopia is low, the cost of capital decreases in the accounting quality. However, if managerial myopia is at an intermediate level and the accounting quality is not too high, the cost of capital increases in the accounting quality, contrary to our common intuition.

The rest of the article proceeds as follows: Section “Model” describes the model. Section “Main Analysis” presents the main analyses and results of the model, and Section “Extensions” provides discussions on accounting manipulation, model assumption, and the relation to cost of capital studies. Section “Conclusion” concludes the article.

Model

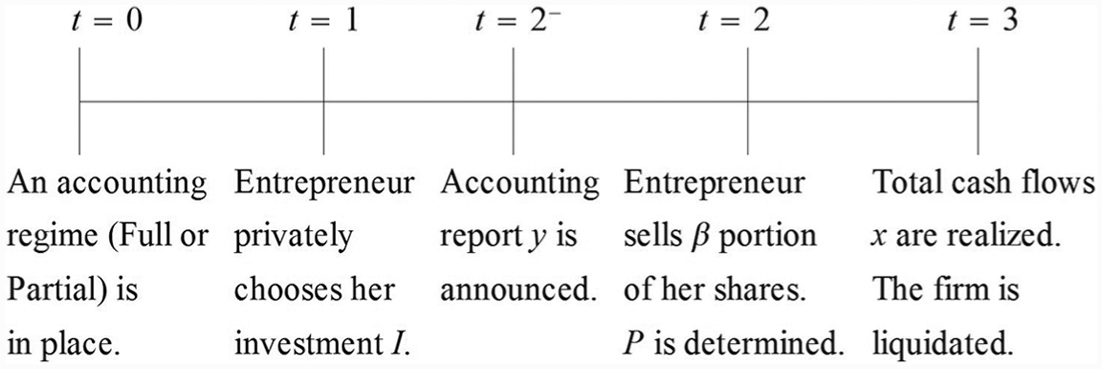

A risk-neutral entrepreneur owns a technology, which requires an initial investment. Before making the investment, on date-

The time line of events.

We next provide more details on the model.

Cash Flows

Following previous literature (e.g., Dye, 2002; Dye & Sridhar, 2004), the date-1 investment

We interpret

Two Accounting Regimes

On date-0, two accounting regimes are possible: Partial accounting and Full accounting. The selection of the accounting regime is a choice problem which, in practice, involves many relevant parties with conflicting incentives such as regulators, reporting firms, auditors, and other capital market users. While we do not explicitly model this complex choice problem and take the accounting regime in place as given, we do provide an analysis of the firm welfare under each regime in Section “Main Analysis.”

Partial accounting

The scope of the Partial accounting system is limited: It excludes, from its measurement, cash flows with hard-to-measure characteristics such as high noise, lack of evidence, and/or being associated with future activities. We capture the measurement dimension distinction as follows: Suppose there are two components of the profitability variable

where

Therefore, the prior distribution of

Growth prospect: We use

Future profitability risk: We use

Independence: We assume that the correlation between the two types of cash flows is 0, which reflects the underlying economic logic. One important reason that certain cash flows are hard to measure is that they are subject to future economy-wide or industry-wide shocks, which should be less correlated with the firm-specific factors underlying the easy-to-measure cash flows. 10

Based on the above cash flow structure, the Partial accounting signal, denoted by

where the accounting measurement noise

The potential problem of Partial accounting is, of course, that the measurement is less comprehensive and less aligned with the entire economic return of the investment. This problem is more pronounced when the portion of cash flows excluded from the measurement is large (i.e., a large

Full accounting

Under Full accounting, the accounting signal, denoted by

where the accounting measurement noise

Returning to the same loan loss example, the total expected “lifetime” losses under the new CECL model include the expected losses from the added time horizon and below the “probable” threshold in addition to those obtained under the previous incurred loss model. Naturally, the resulting estimated loan losses would contain more noise than those from the previous incurred loss model. While our model abstracts away from the underlying detailed measurement process, the properties of any such summary accounting measures would be fairly represented by the

The Entrepreneur’s Objective Function and Interim Share Price

Following previous literature (e.g., Einhorn & Ziv, 2007; Liang & Wen, 2007; Stein, 1989), we assume that the entrepreneur is interested in both the firm’s current market price and the future cash flows. Accordingly, the entrepreneur’s objective is to maximize a weighted average of the expected date-

Here,

The firm shares are priced in a competitive rational capital market. Investors in the market are risk averse and have a constant absolute risk aversion (CARA) utility function with risk-averse coefficient

where

where

Main Analysis

Equilibrium Characterization

Before proceeding to the detailed analysis, we first define the equilibrium:

given the pricing function

given the market’s conjecture

the market’s conjecture is correct. That is,

As a benchmark, we label

The following proposition characterizes a linear equilibrium for both Partial accounting and Full accounting. We denote the equilibrium investment under Partial accounting and Full accounting by

1. Under Partial accounting, the linear pricing function

with

and

2. under Full accounting, the linear pricing function

with

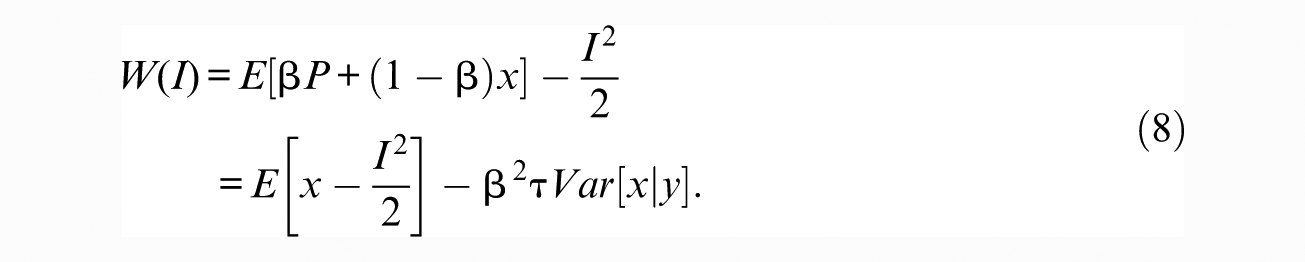

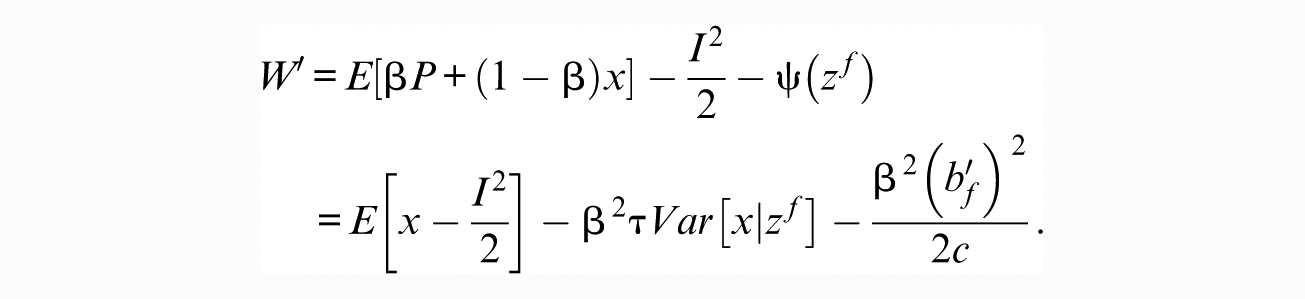

The entrepreneur’s ex ante payoff or welfare on date-

The first term in Equation 8 is the expected total future cash flows net of the investment cost, which depend on the efficiency of the equilibrium investment. The second term in (8) measures the risk premium to compensate outside investors for bearing the risk. The entrepreneur’s welfare depends on both the investment efficiency and the risk premium induced by the existing accounting regime. Proposition 1 shows that the equilibrium investment (

In the following, we first analyze how the accounting measures affect the equilibrium investment or investment efficiency. We then analyze how they affect the conditional variance or risk premium. In particular, we show that they affect the conditional variance both directly through uncertainty resolution and indirectly through the endogenous investment. Counterintuitive results arise when the indirect effect dominates the direct effect.

Investment Analysis

In this section, we focus on the investment decision and analyze the induced investment efficiency under the two accounting regimes. Given the equilibrium in Proposition 1, the following corollary presents some comparative statics results regarding the equilibrium investment:

The equilibrium investment under both accounting regimes approaches The equilibrium investment Under both accounting regimes, the equilibrium investment is higher when the accounting signal is less noisy and when the entrepreneur is less myopic.

Under both accounting regimes, the equilibrium investment is lower than the first best. The underinvestment equilibrium is a standard result in the literature.

14

Due to the noise in the accounting signal, investors discount the accounting signal in pricing the firm, leading to the underinvestment result. The underinvestment problem is alleviated as the accounting signal becomes less noisy. Similarly, a lower

The structural differences between the two accounting regimes lead to the different equilibrium investments. Under Partial accounting, the accounting signal is only a noisy measure of the easy-to-measure cash flows and does not measure the hard-to-measure cash flows. The price does not respond to the incremental hard-to-measure cash flows caused by a marginal change in the investment. As a result, the hard-to-measure cash flows do not provide any investment incentives through the price. Accordingly, even with no measurement noise, the investment under Partial accounting is still lower than the first best. When the growth prospect

In contrast, under Full accounting, the accounting signal measures both the easy-to-measure and hard-to-measure cash flows, which makes the signal more “congruent” with the entire investment return. Therefore, Full accounting provides more incentives for the investment all else equal. When there is no measurement noise, the investment under Full accounting achieves the first best. Furthermore, when the growth prospect

Given the above discussion on the structural differences between the two accounting regimes, when the growth prospect

Note that the parameter

Risk Premium and the Entrepreneur’s Welfare Analysis

In this section, we first focus on the risk-premium concern. According to Proposition 1, the conditional variance consists of two components as shown in (4) under Partial accounting. The first component is the unconditional variance of the hard-to-measure cash flows, and the second component is the conditional variance of the easy-to-measure cash flows. Notice that only the second component is lowered by the accounting signal

If the investment is exogenously given, our model delivers a common intuition: under either accounting regime, the noisier the accounting signal, the less cash flow uncertainty is resolved, and the higher the conditional variance. However, with endogenous investment, our model casts a challenge to this common intuition. The relationship between the accounting noise and the conditional variance becomes more subtle. In particular, the accounting noise has two effects:

Direct effect: Higher noise increases the conditional variance due to less uncertainty resolution, and

Indirect effect: Higher noise leads to lower equilibrium investment, which reduces the conditional variance because it reduces the total (ex ante) cash flow uncertainty.

As a result, this indirect effect through the endogenous investment works against the direct effect. Given such countervailing direct and indirect effects, the net impact of the accounting noise on the conditional variance is not unambiguous, and depends on the dominant effect.

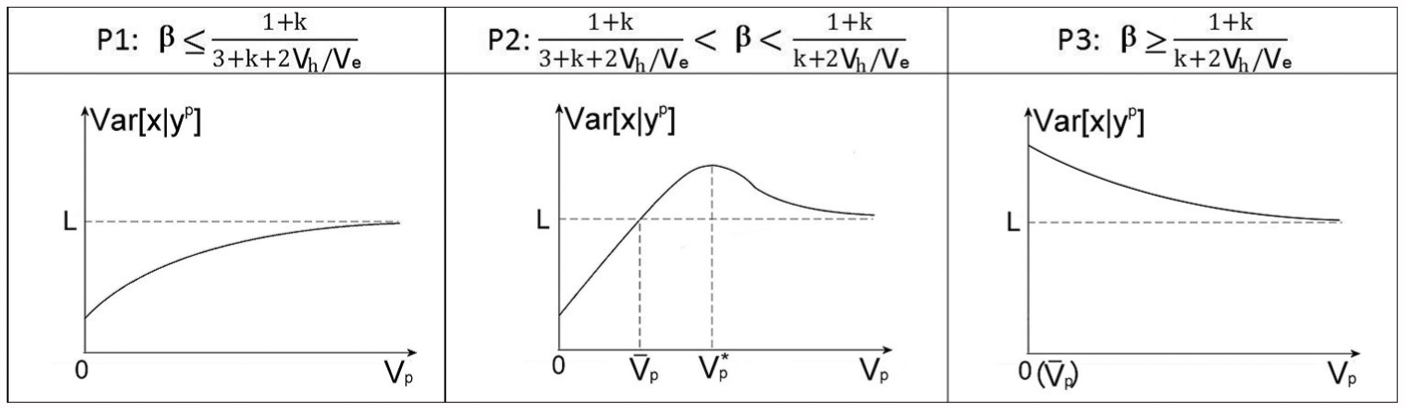

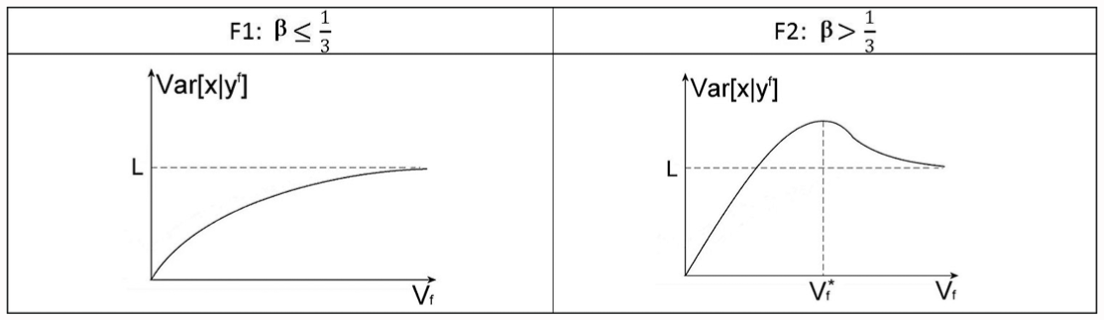

Under the Partial accounting regime, if the managerial myopia is small ( if the managerial myopia is at an intermediate level ( if the managerial myopia is large ( Under the Full accounting regime, if the managerial myopia is small ( if the managerial myopia is large (

Figures 2 and 3 visualize the results in Corollary 2 for Partial accounting and Full accounting, respectively.

The impact of the accounting noise on the conditional variance under Partial accounting.

The impact of the accounting noise on the conditional variance under Full accounting.

Under Partial accounting, Figure 2 shows that the conditional variance may increase or decrease in the accounting noise depending on the managerial myopia

From Figure 2, one can also see that the cutoff points for the different cases depend on

Risk premium may be smaller under Full accounting even with a high noise

Using the results in Corollary 2, we now compare the conditional variances under the two accounting regimes. To focus our analysis on interesting parameter regions to highlight the key economic results, we assume, for the following analysis, that the profitability of the hard-to-measure cash flows is relatively volatile:

The result in Proposition 3 comes directly from the comparison of the related graphs in Figures 2 and 3. By comparing Figure 2, P3 with Figure 3, F1, one can see that for any noise levels under the two accounting regimes, the conditional variance is always higher than the unconditional variance

A couple of other observations also emerge from the proposition. First, Proposition 3 is a robust result in the sense that it does not rely on any specific (functional) relationship between the accounting noises under the two accounting regimes (i.e., the proposition is valid for any pair of

Full accounting may benefit both investment efficiency and risk premium

The results in Propositions 2 and 3 only focus on the sole impact of the investment efficiency and risk premium on the entrepreneur’s welfare, respectively. The following proposition combines the impacts from both on the entrepreneur’s welfare:

Proposition 4 presents a strong result that Full accounting could perform better on both welfare components even if it contains a large noise, as long as the given conditions are satisfied. The intuition is as follows: First, as Proposition 2 shows, for any given other parameters, when the growth prospect is relatively large (i.e.,

Extensions

Accounting Manipulation

Another major concern associated with the expansion of accounting recognition is that the measurement of hard-to-measure cash flows is less reliable and easier to manipulate. To explore the potential impact of this concern on the main results of the article, we allow for managerial manipulation in this section.

18

By measuring the hard-to-measure cash flows, the Full accounting signal is more susceptible to managerial manipulation than the Partial accounting signal. For simplicity, we assume that only the Full accounting signal is subject to manipulation.

19

In particular, under Full accounting, the entrepreneur could report an accounting signal

where

We first characterize the equilibrium under Full accounting with manipulation.

with

and the equilibrium reporting strategy

According to (11), the equilibrium accounting report

By comparing Propositions 1 and 5, one can see how the introduction of manipulation affects our main results on investment efficiency and risk premium. From (7) and (10) as well as the expressions for

Similarly, from (6) and (9), the difference between the conditional variances with and without manipulation also comes from the different variances of the signal noise. The introduction of manipulation is equivalent to increasing the variance of the signal noise from

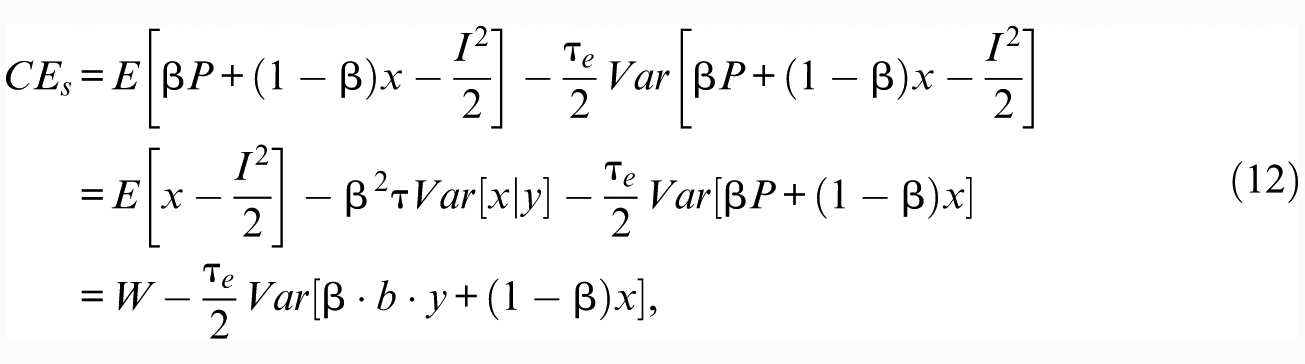

Anticipating the ex post manipulation, the entrepreneur’s ex ante welfare under Full accounting, denoted by

Compared with the welfare

Note that if there is a strong legal and auditing system in place, the manipulation cost

In summary, allowing manipulation does not qualitatively change the positive impacts on the entrepreneur’s welfare from the scope expansion as shown in the main setting. Admittedly, the manipulation generates a dead-weight loss that does not exist in the main setting. However, if the positive impacts are dominant, for example, when a strong legal and auditing system is in place, the expansion is still preferable.

The Risk-Averse Entrepreneur

In our main setting, as the entrepreneur is risk neutral, her welfare only depends on the investment efficiency and investors’ risk premium. However, if the entrepreneur is risk averse, she has to further consider her own risk premium. Suppose the entrepreneur has a CARA utility function with risk-averse coefficient

where

If the entrepreneur’s risk-averse coefficient

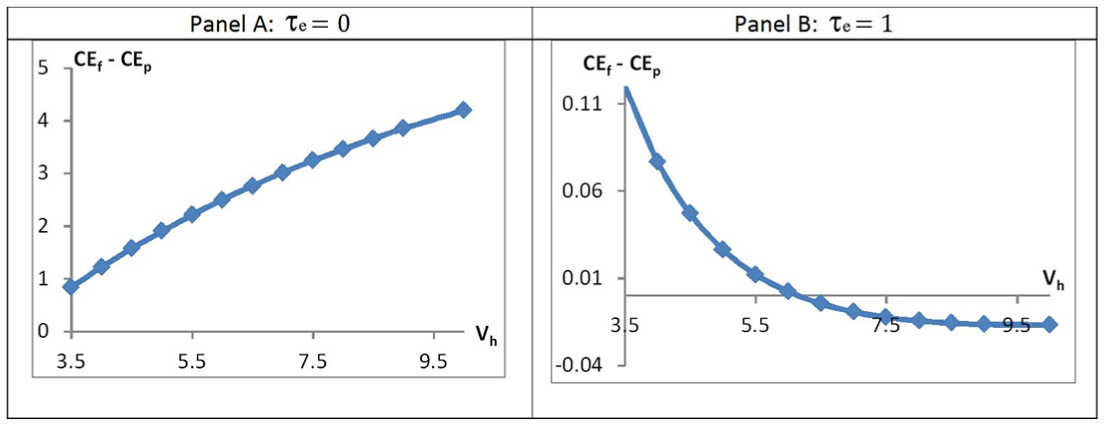

Let

The comparison of the certainty equivalents under Full accounting and Partial accounting.

In Panel A where

Link to the Empirical Cost-of-Capital Studies

Our results on the relation between accounting noise and conditional variance have empirical implications on studies regarding the relation between accounting information quality and (firm-equity) cost of capital. We define the cost of capital of the firm as follows 22 :

The simplification in definition (13) results from Equation 3. The numerator,

Under the Partial accounting regime,

if if if Under the Full accounting regime,

if if

The results in this corollary are similar to those of Corollary 2, which presents the relation between the conditional variance and accounting noise. Therefore, Figures 2 and 3 also graph the relation between the cost of capital and accounting noise. The results indicate that the nature and direction of the relation between the cost of capital and accounting information quality depend on factors such as the managerial myopia in investment decisions (

Empirical work has documented mixed evidence on the association between earnings quality and cost of capital, which Beyer et al. (2010) attribute to some empirical challenges, such as the self-selection problem, the existence of a possible mechanical relationship, and the measurement errors in the proxies of cost of capital and disclosure quality. Given the nonmonotonic relation shown in Figures 2 and 3, our study provides potential factors that may help explain the mixed evidence. For example, based on both Figures 2 and 3, we can see that, if the entrepreneur’s myopia is at an intermediate level and the accounting information quality is not too high (see Figures 2, P2 and 3, F2), the cost of capital increases in the accounting quality, contrary to our common intuition. Also, if the firm extensively relies on Partial accounting measures and the manager is very myopic (i.e., Figures 2, P3), the cost of capital increases in the accounting quality regardless of the accounting quality. In other cases, the relation between the cost of capital and accounting quality could be negative, as normally expected.

Conclusion

In this article, we provide an economic model in which the conceptual scope issue with every accounting measurement has an economic meaning. In particular, we build an accounting model to highlight one important scope dimension: inclusion or exclusion of hard-to-measure future events. We embed the accounting model into a standard economic model in which the accounting measurement affects both distributional and allocational efficiency. We conclude that the scope expansion in accounting measurements may affect both real variables such as investment efficiency and financial variables such as risk premium in share prices. Specifically, we show that in the process of expanding accounting recognition, firms’ internal investment efficiency and external share-price risk premium may not necessarily be a trade-off in that an expanded recognition may lead to both a higher investment efficiency and a lower risk premium at the same time.

While we believe that our study opens the question on a key scope issue in accounting measurement, we view the article as limited on a few fronts. We have limited our attention to the formal accounting measurement and abstracted away from other forms of disclosure such as corporate voluntary disclosure and information disclosed by other market participants. These other forms of disclosure also have an impact on investment efficiency and risk premium. Similarly, outside investors are also silent in collecting their own information in our model. These topics are all fruitful avenues to explore in future studies.

Footnotes

Appendix

Acknowledgements

The authors gratefully acknowledge suggestions from an anonymous reviewer and the editors. In addition, they thank Jeremy Bertomeu, Michael Ewens, Jonathan Glover, Bjorn Jorgensen, Jing Li, Lin Nan, John O’Brien, and seminar participants at Carnegie Mellon University, the 2011 American Accounting Association (AAA) Annual Meetings in Denver, and the 2013 Financial Accounting and Reporting Section (FARS) Meeting in San Diego. Pierre Liang gratefully acknowledges the Dean’s Summer Research funding of the Tepper School. Xiaoyan Wen also gratefully acknowledges the Neeley School of Business Research Excellence Award.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.